1 Introduction

Market impact games analyze situations in which several agents compete for liquidity in a market impact model or try to exploit the price impact generated by competitors. In this paper, we follow Carlin et al. [6], Schöneborn and Schied [23], Carmona and Yang [7], Schied and Zhang [19], Casgrain and Jaimungal [8], and others by analyzing a market impact game in the context of the Almgren–Chriss market impact model. In [6, 23], all agents are risk-neutral and market parameters are constant, which leads to deterministic Nash equilibria. Deterministic open-loop equilibrium strategies are also obtained in [19], where agents maximize mean variance functionals or CARA utility. In [7] closed-loop equilibria are studied numerically in a similar setup, and it is found by means of simulations that then equilibrium strategies may no longer be deterministic. The approach in [8] is the closest to ours. There, the authors analyze the infinite-agent, mean-field limit of a market impact game for heterogeneous, risk-averse agents in a model with constant coefficients and partial information, and they characterize the mean-field game through a forward-backward stochastic differential equation (FBSDE). In addition, there are several papers that study market impact games in other price impact models, including models with linear transient price impact; see, e.g., [14, 20, 18, 13].

Our contribution to this literature is twofold.

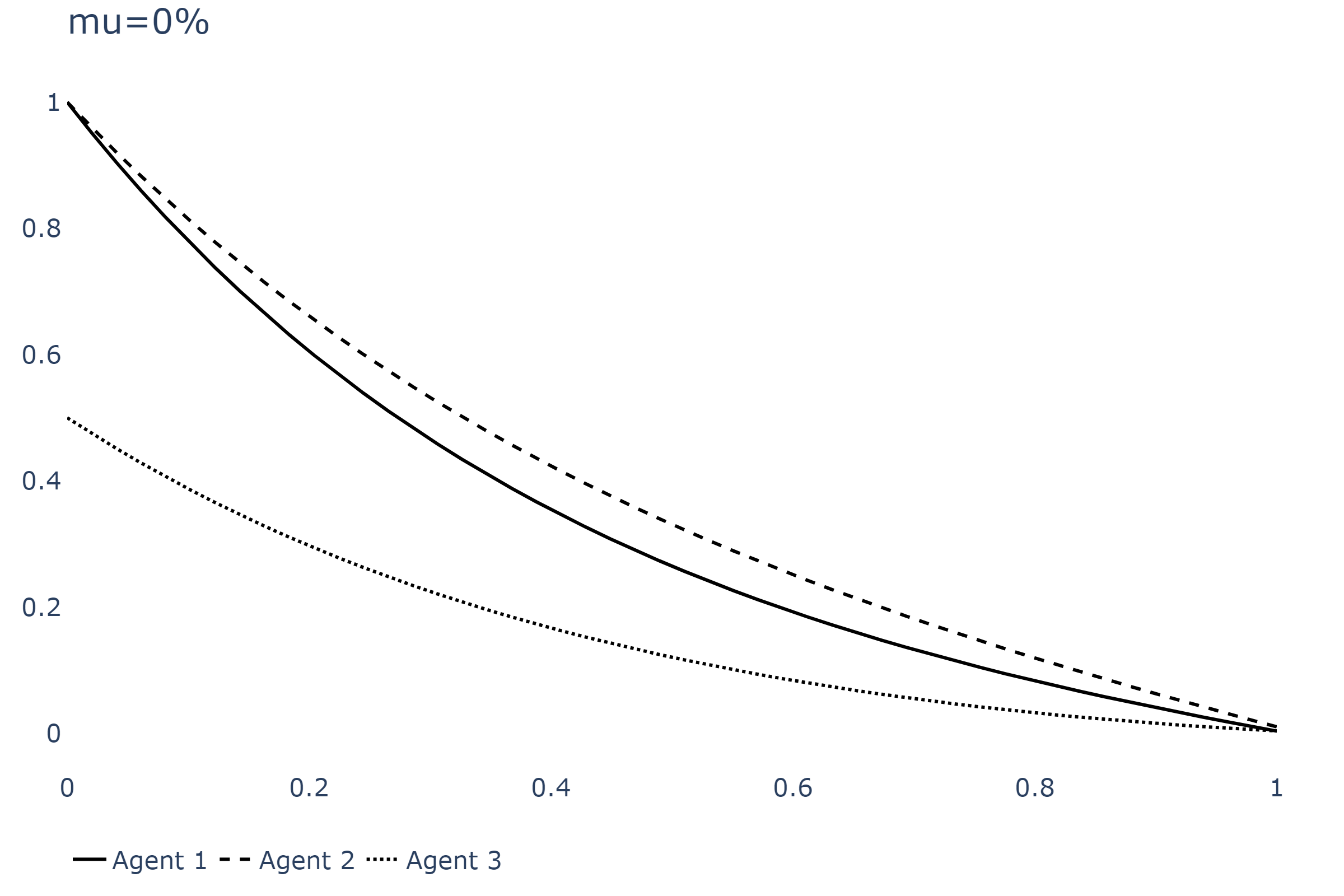

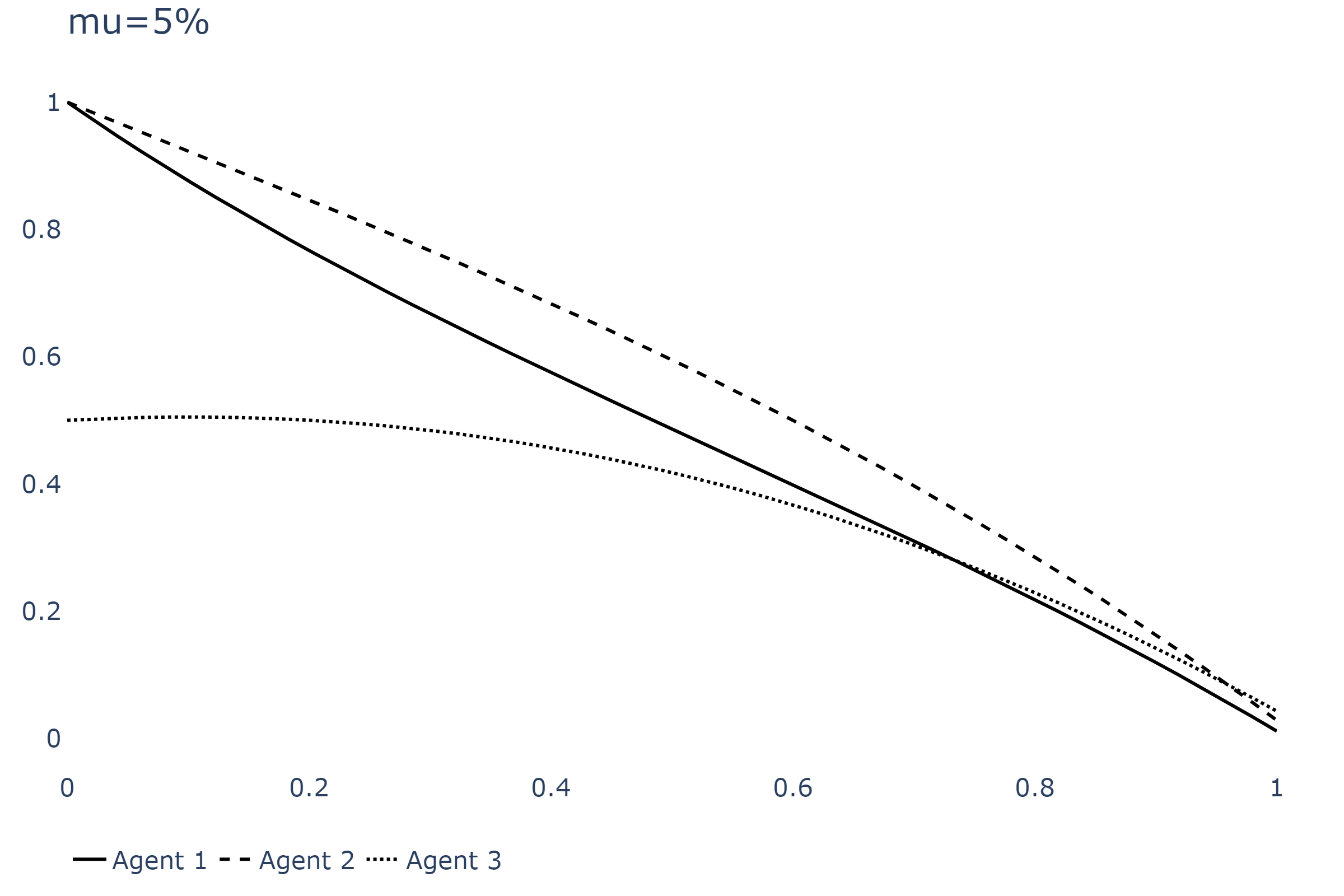

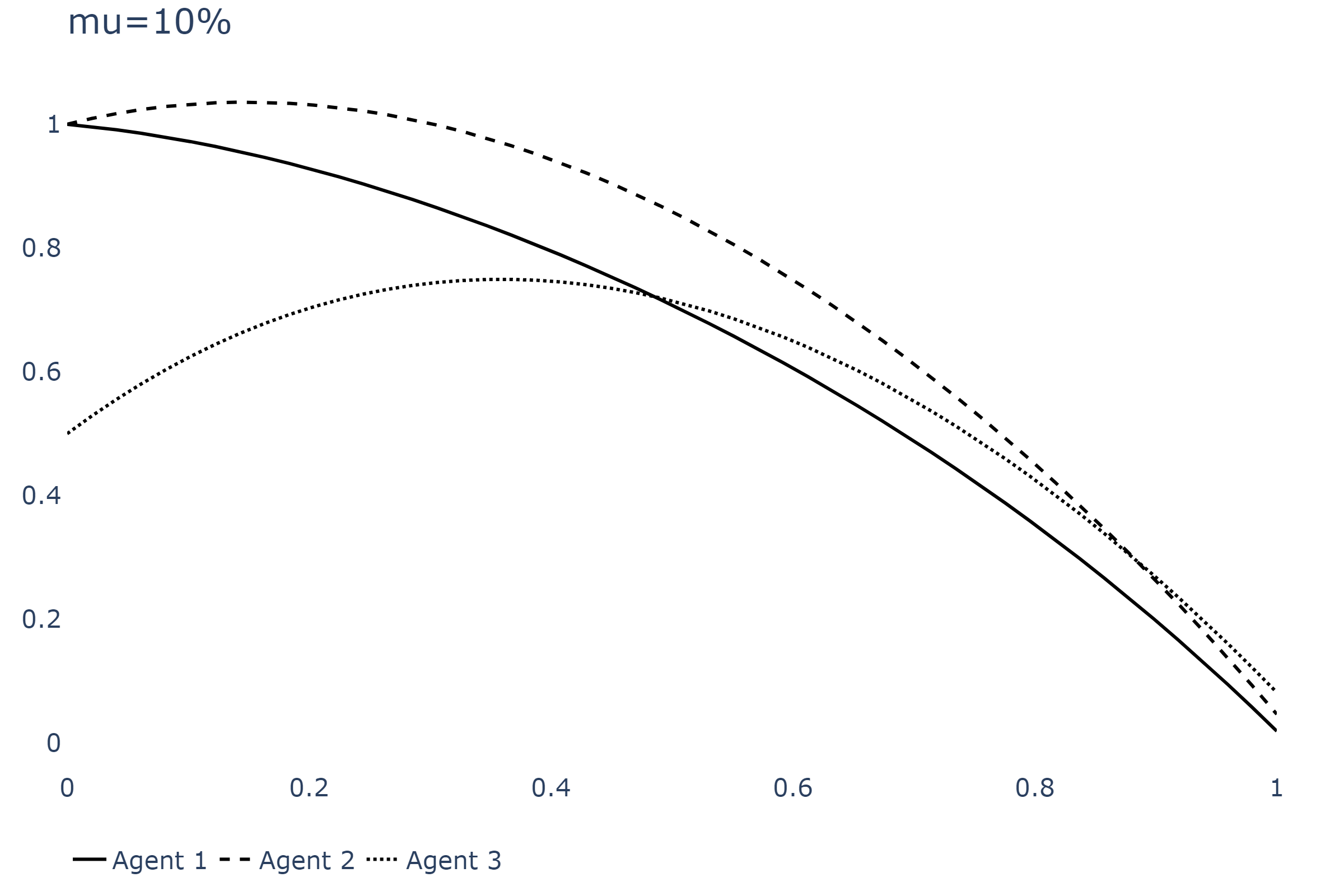

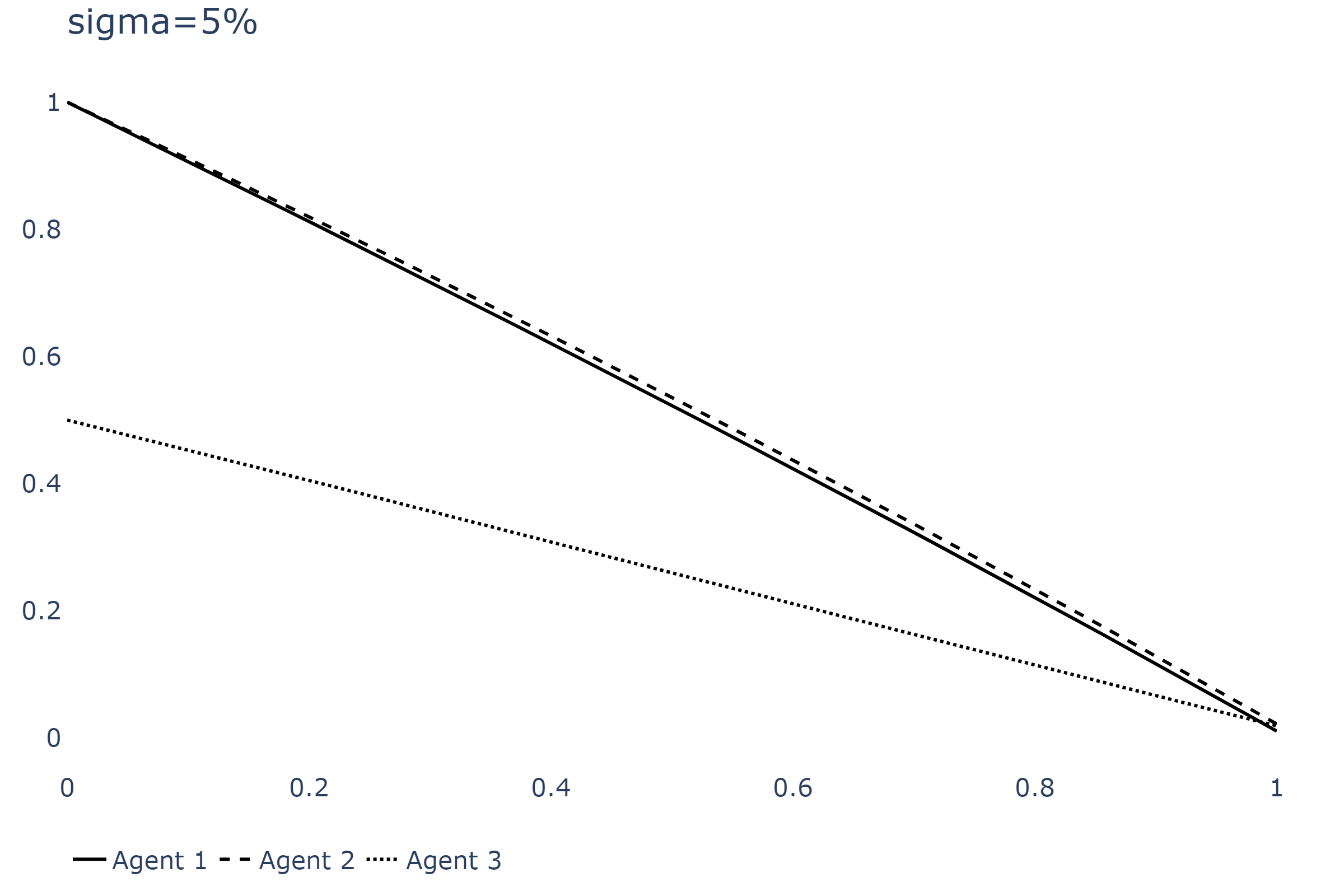

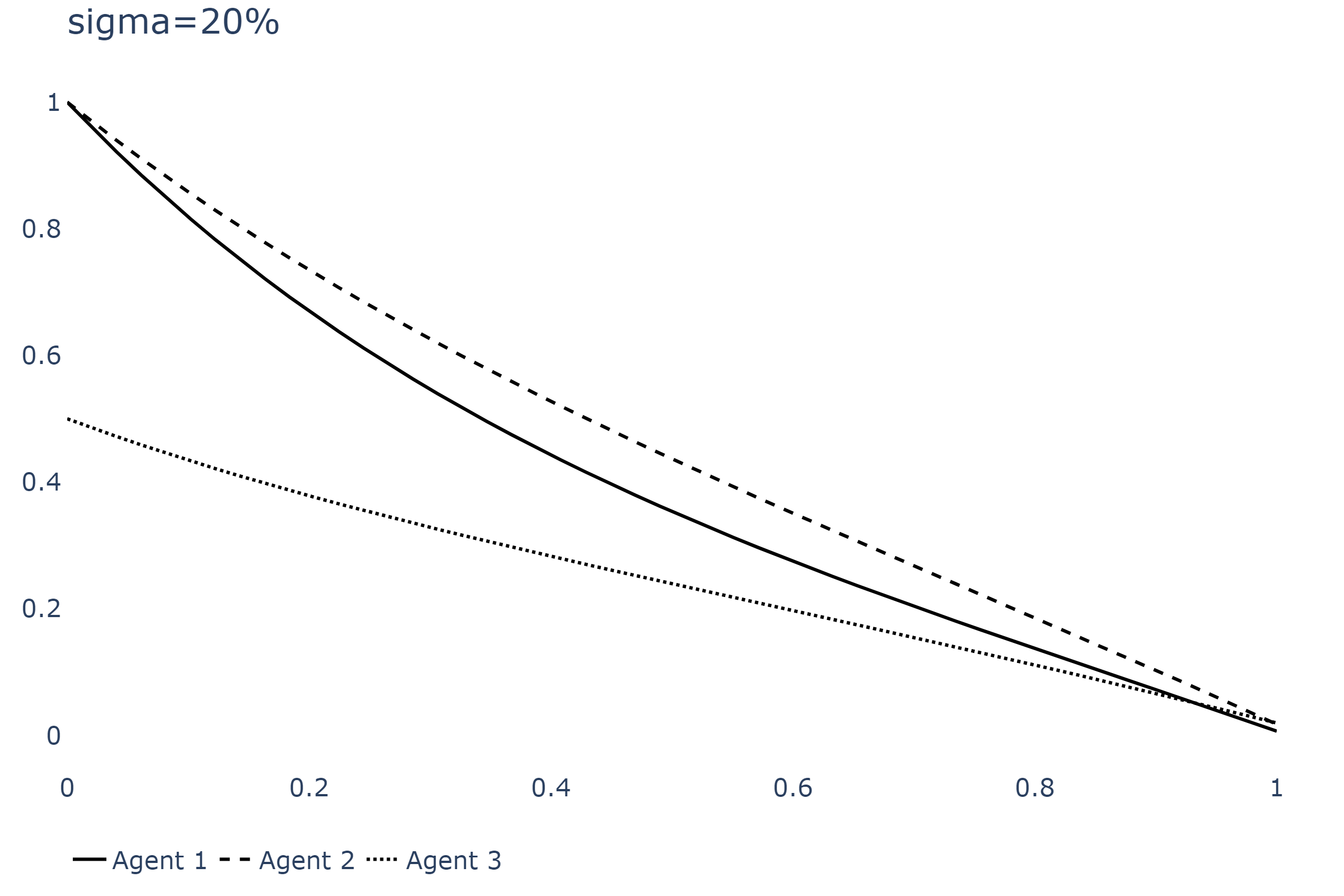

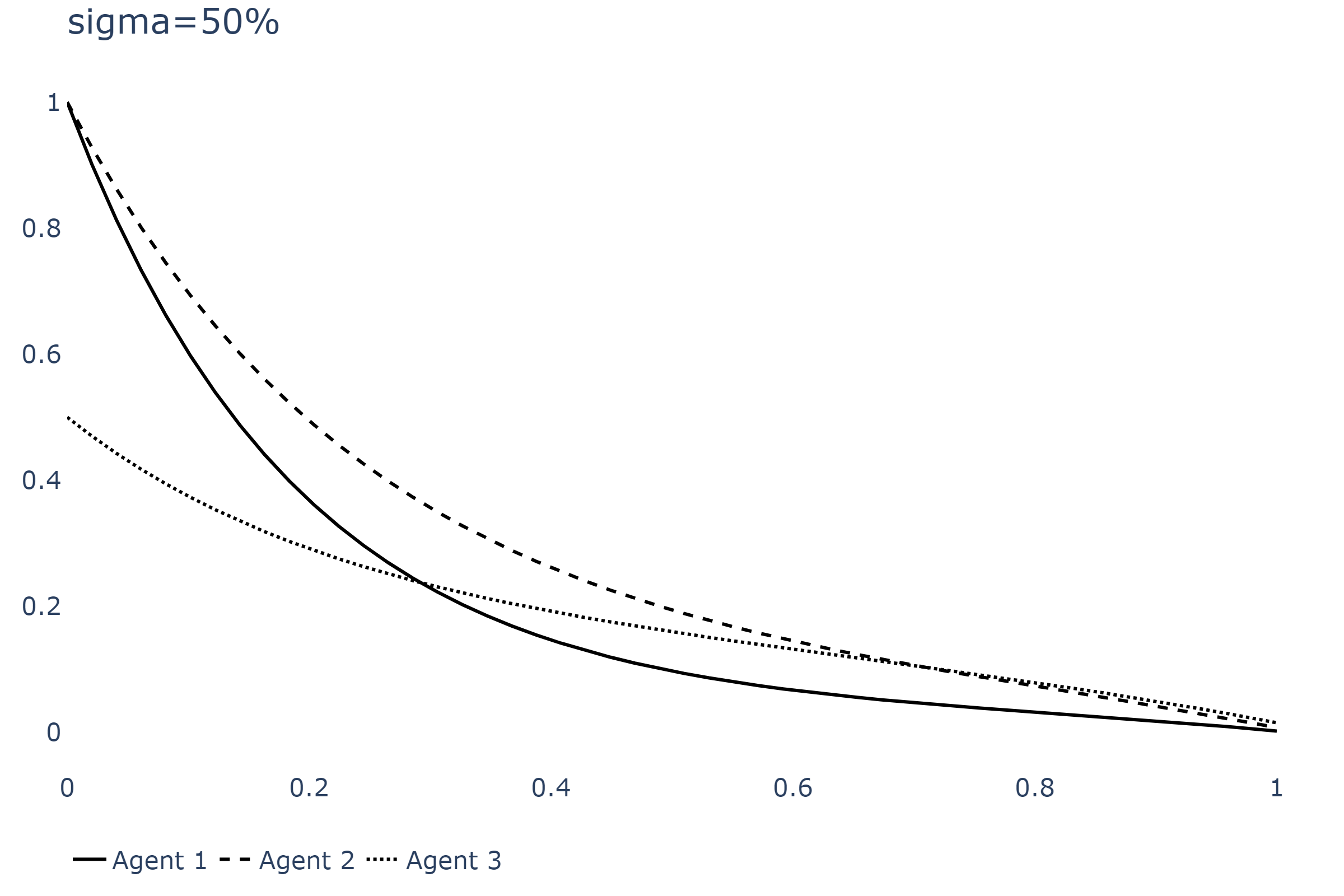

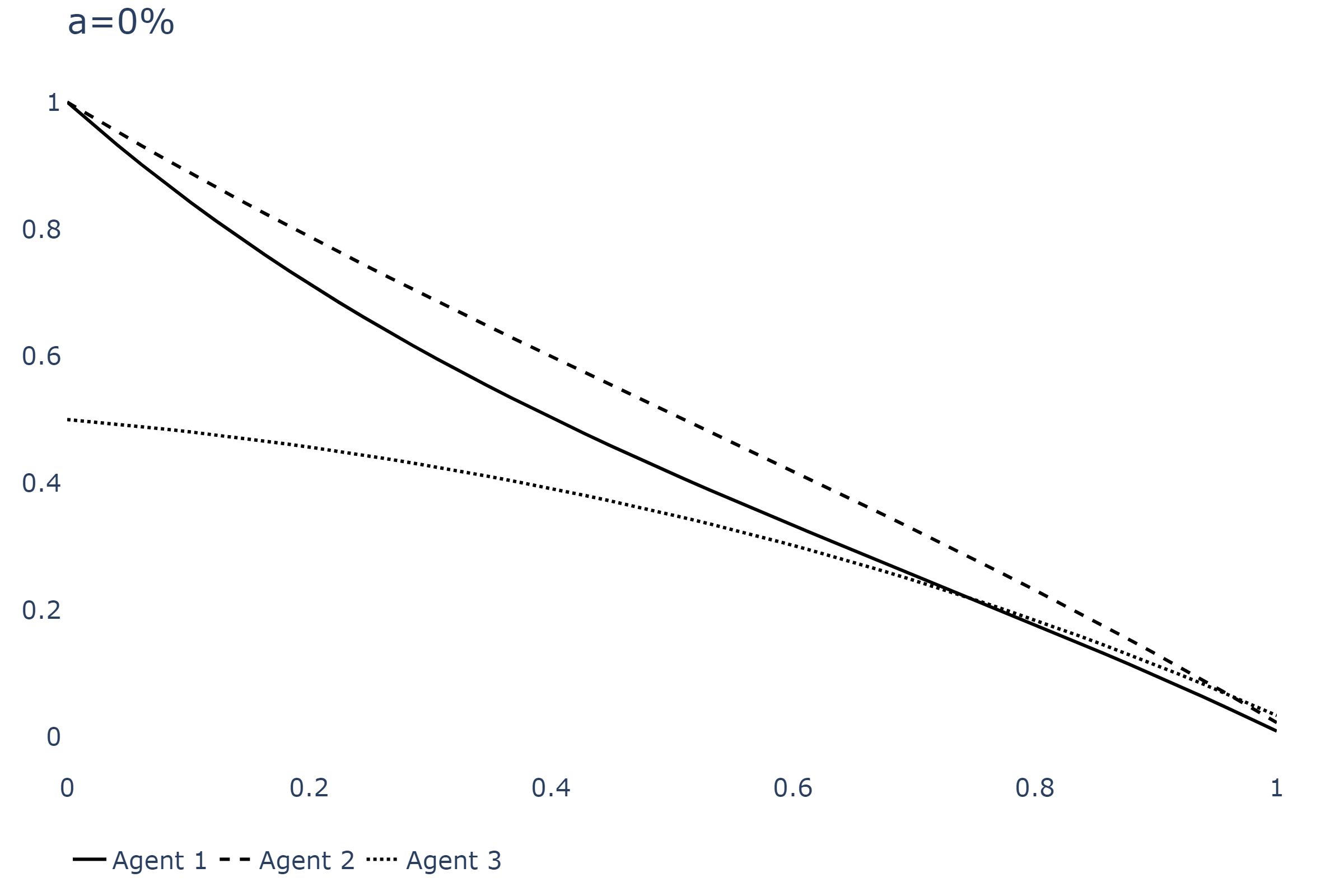

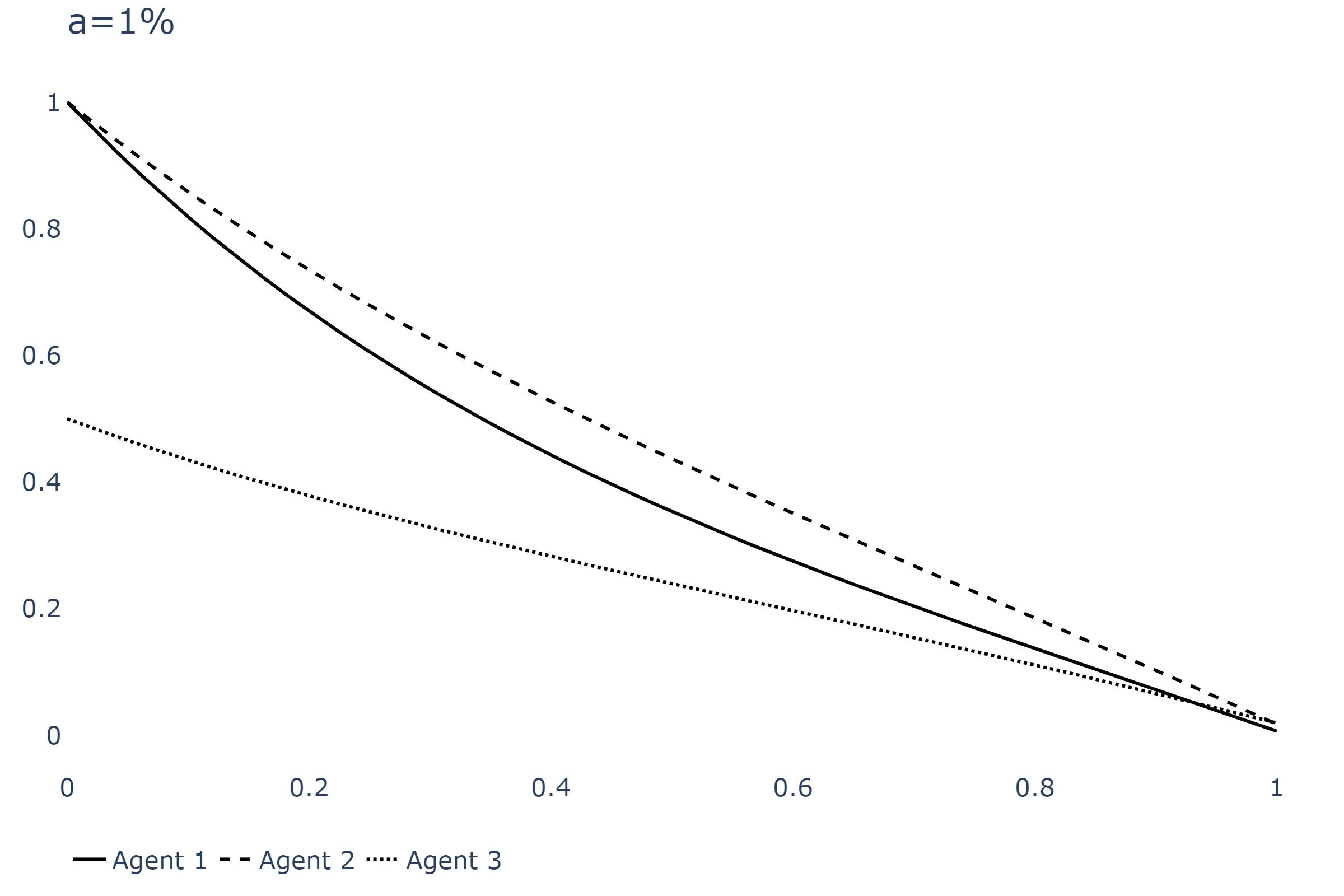

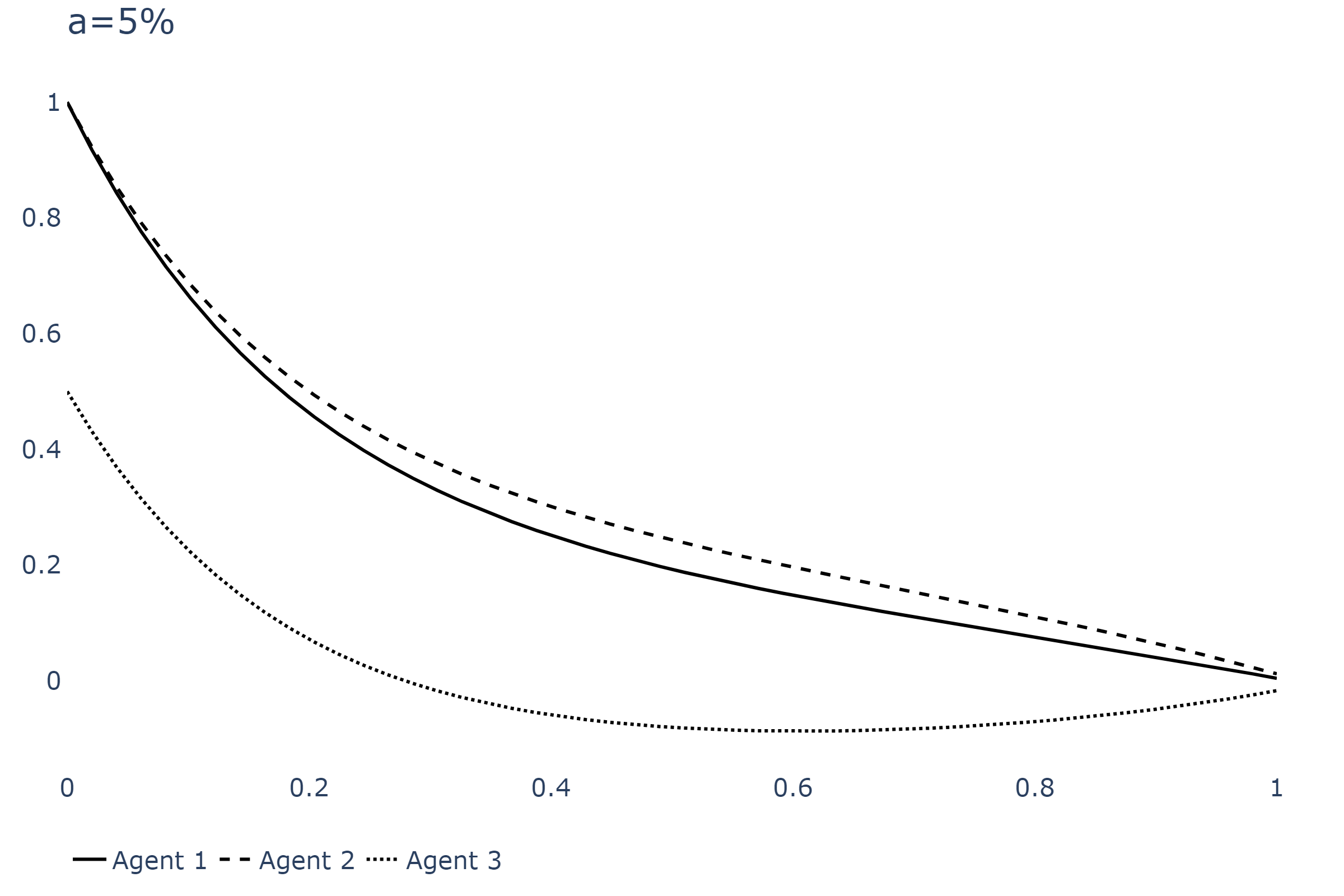

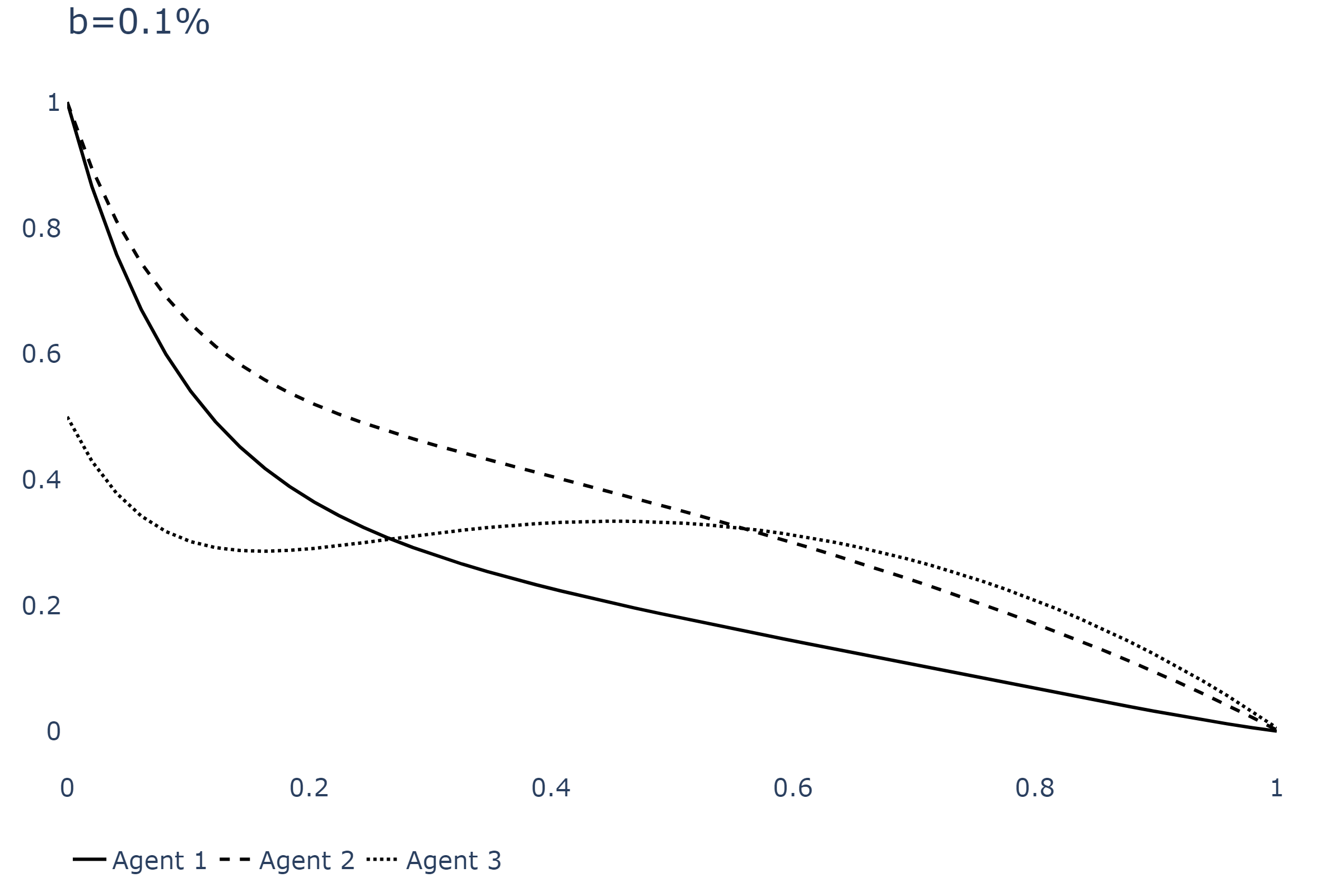

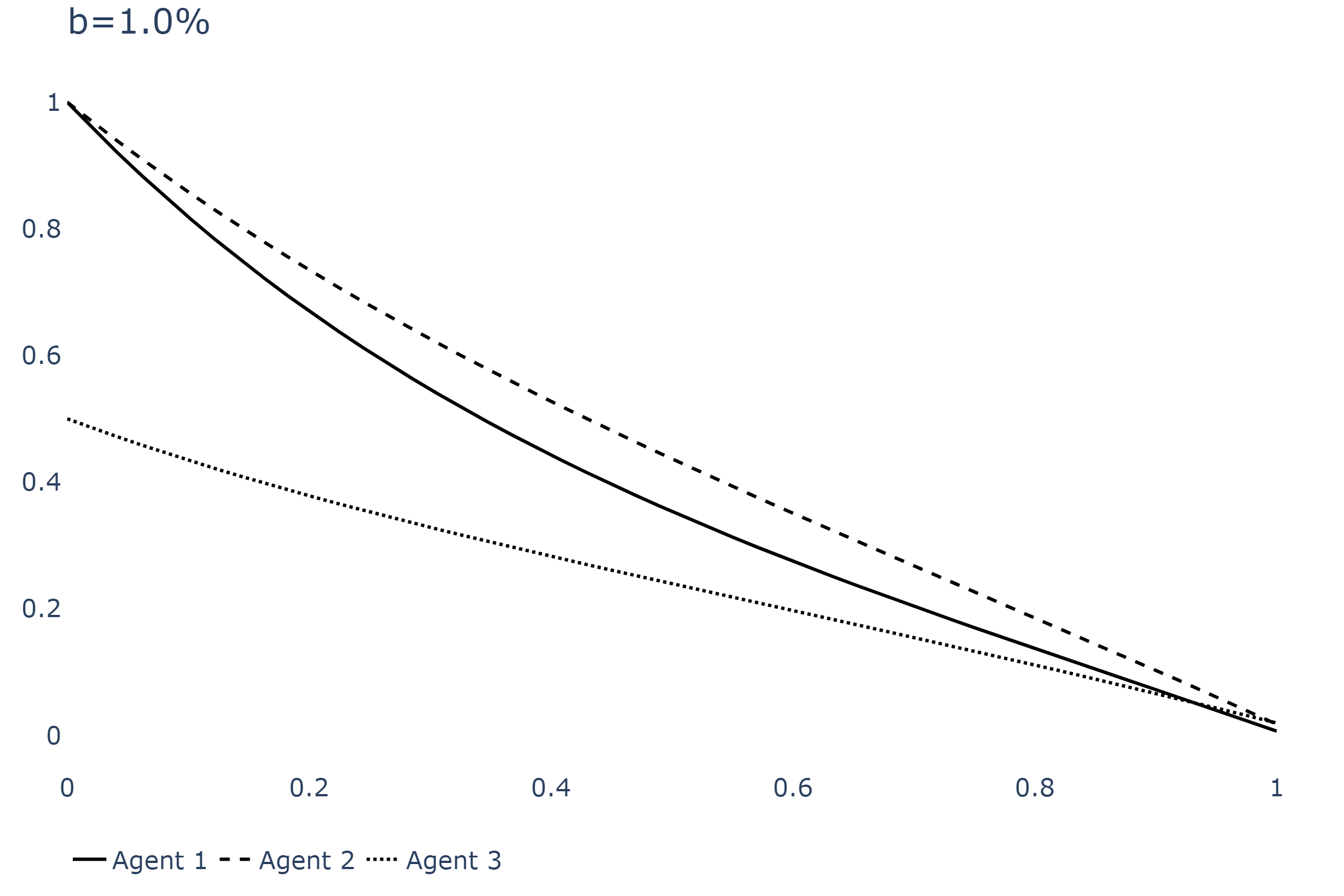

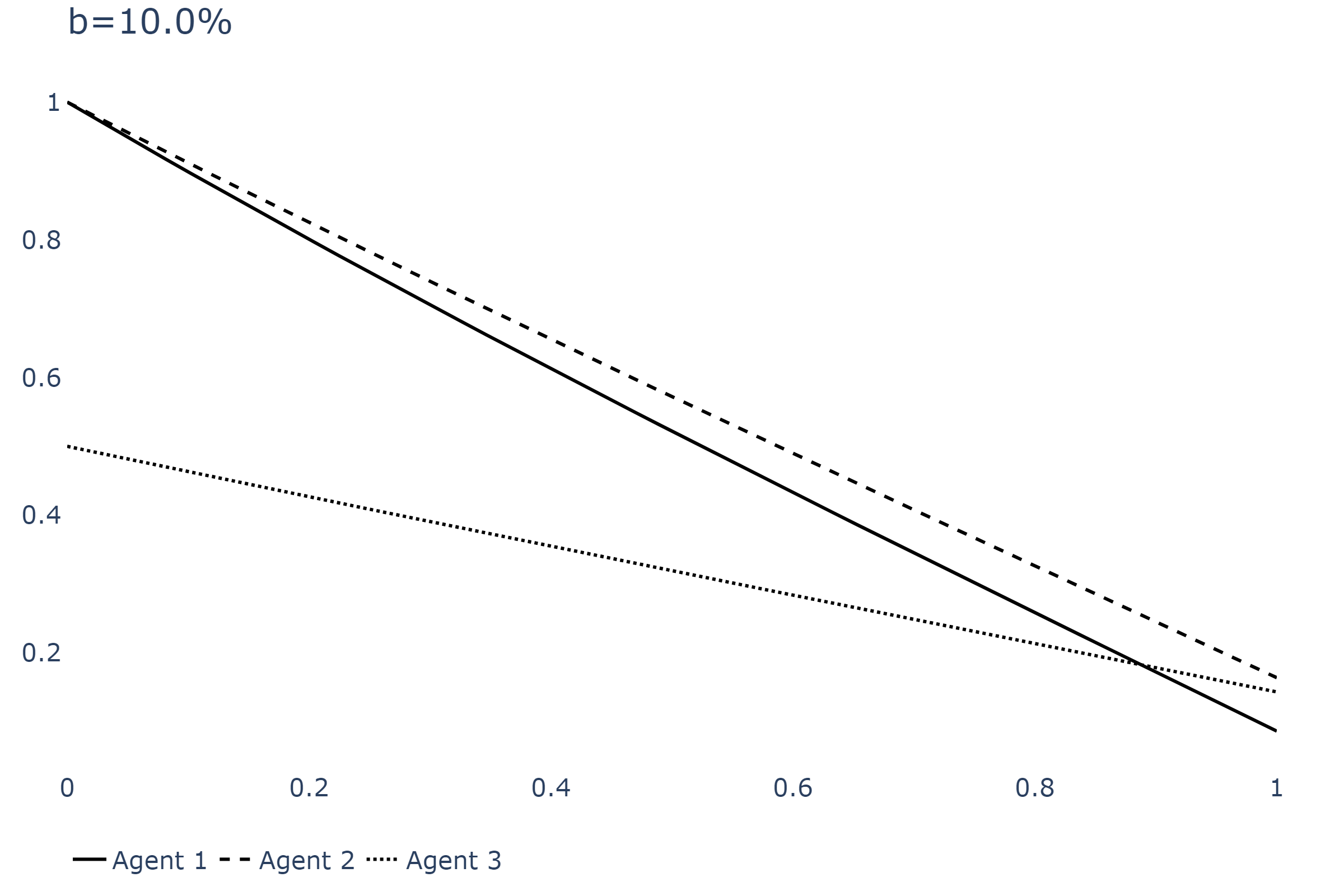

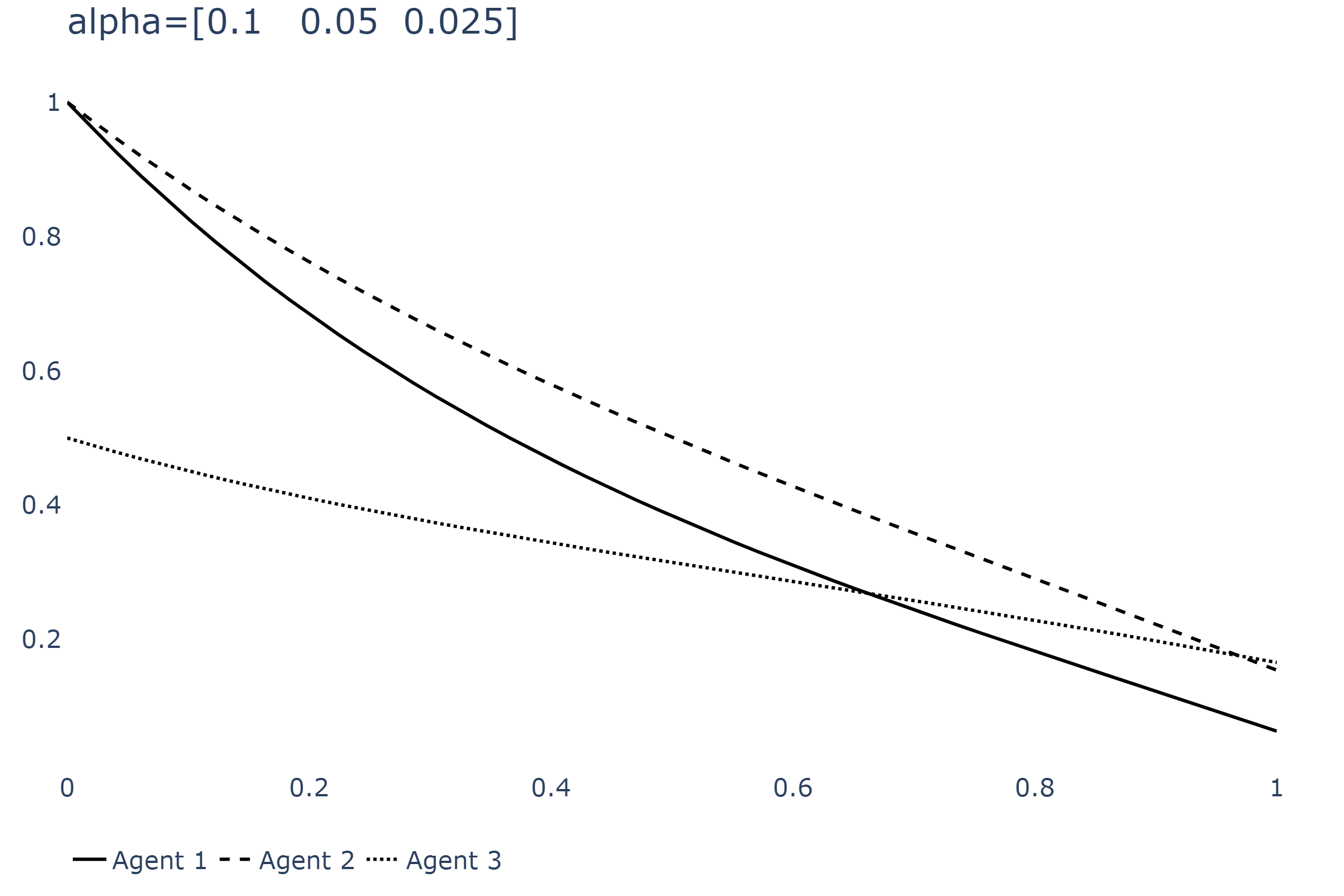

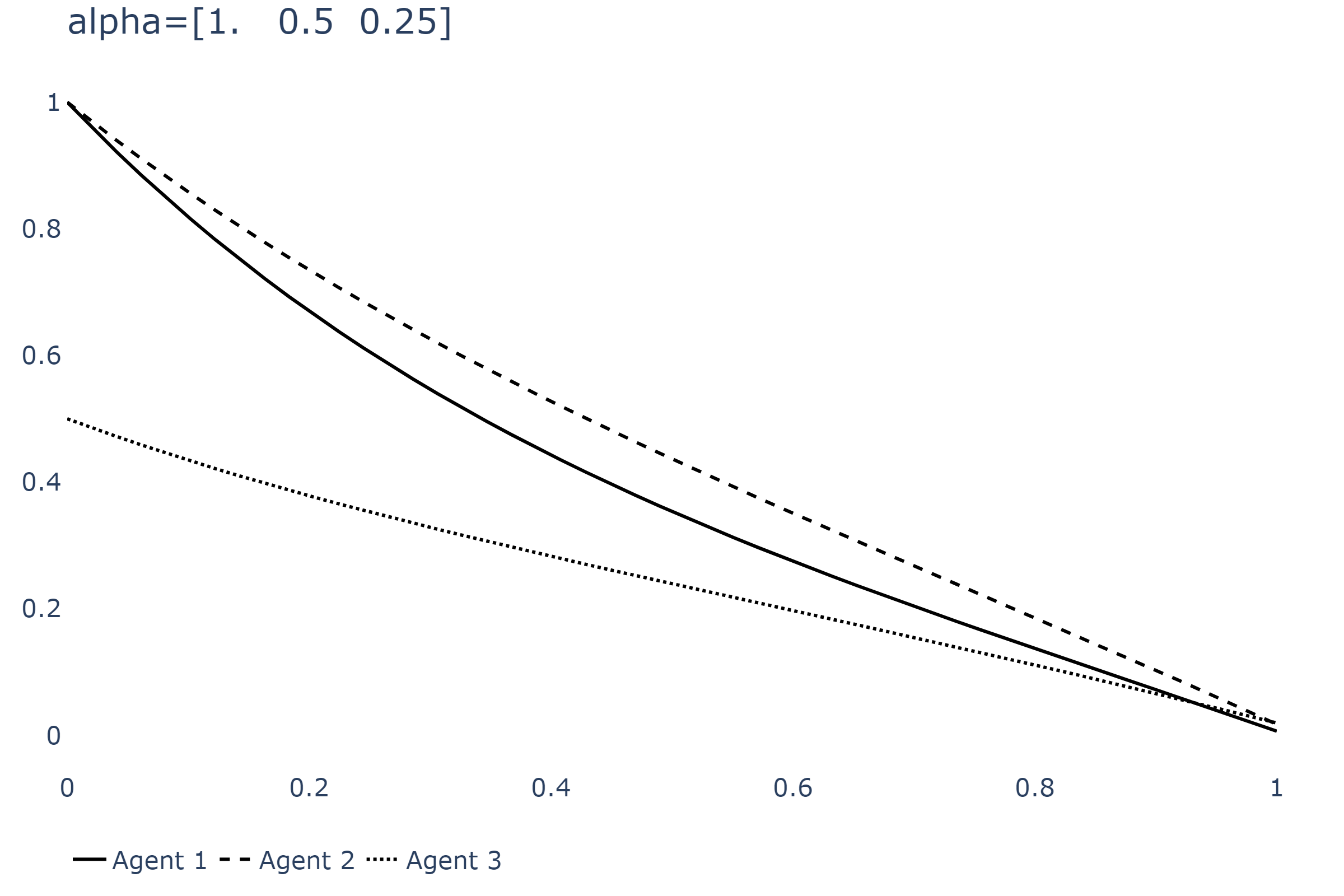

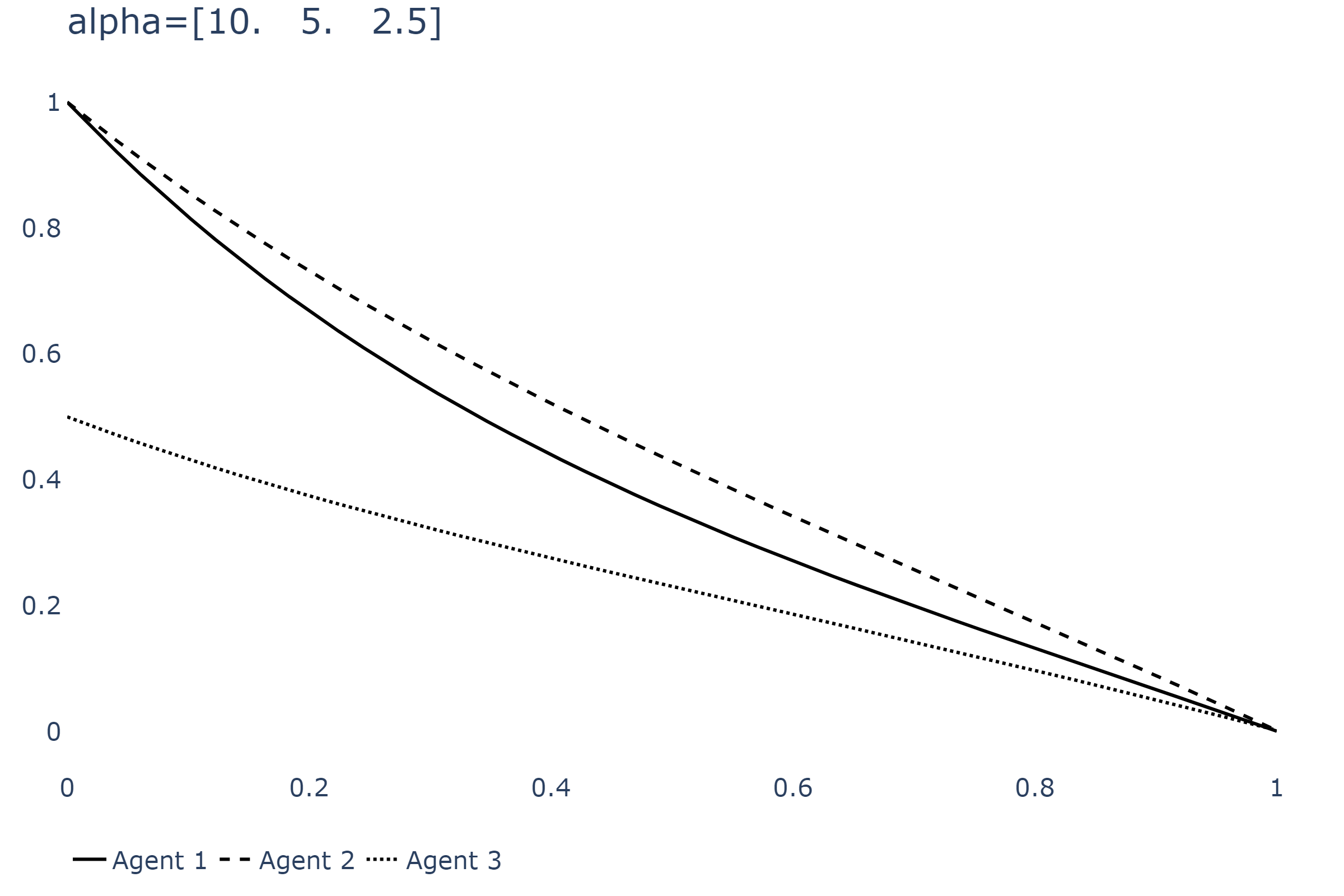

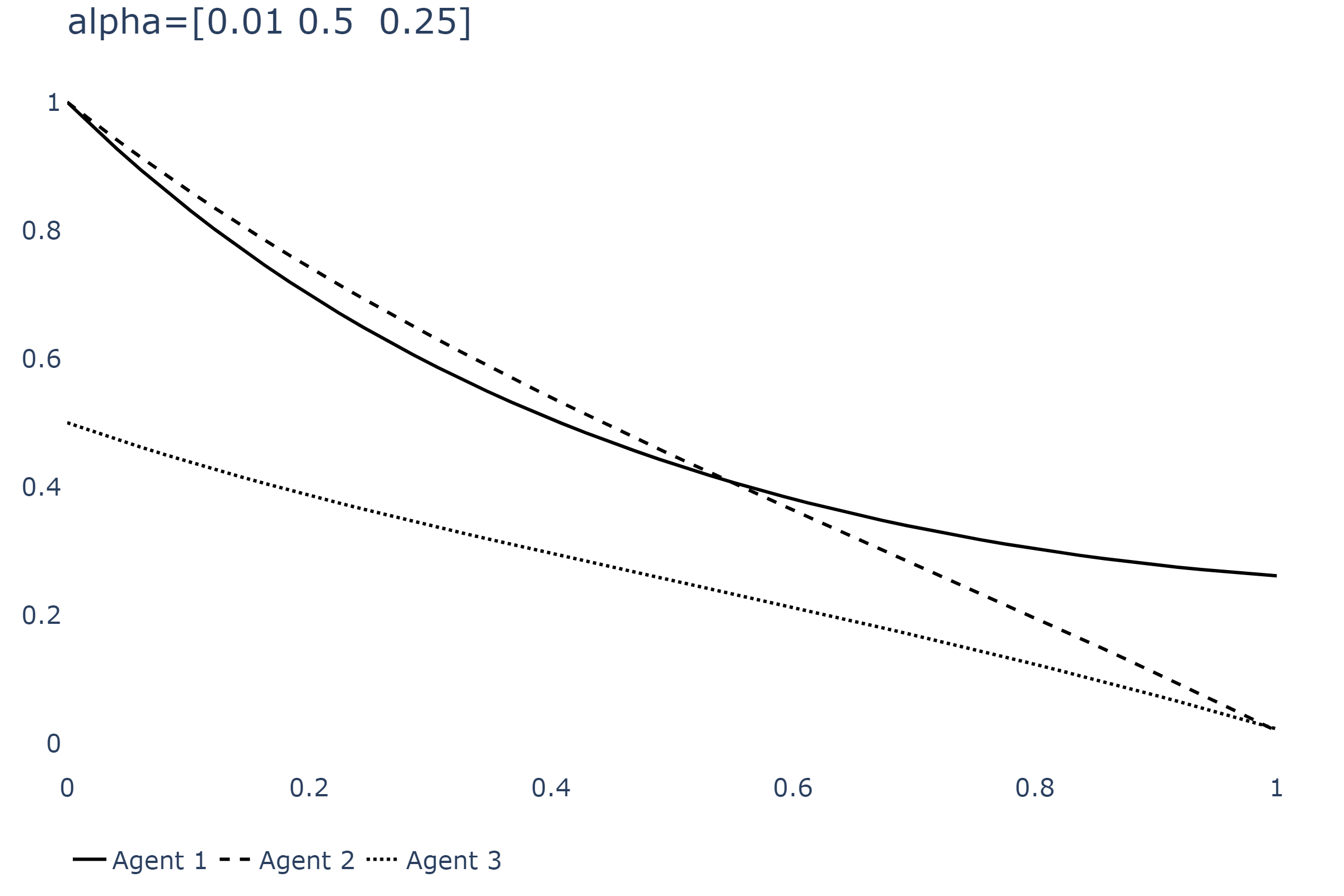

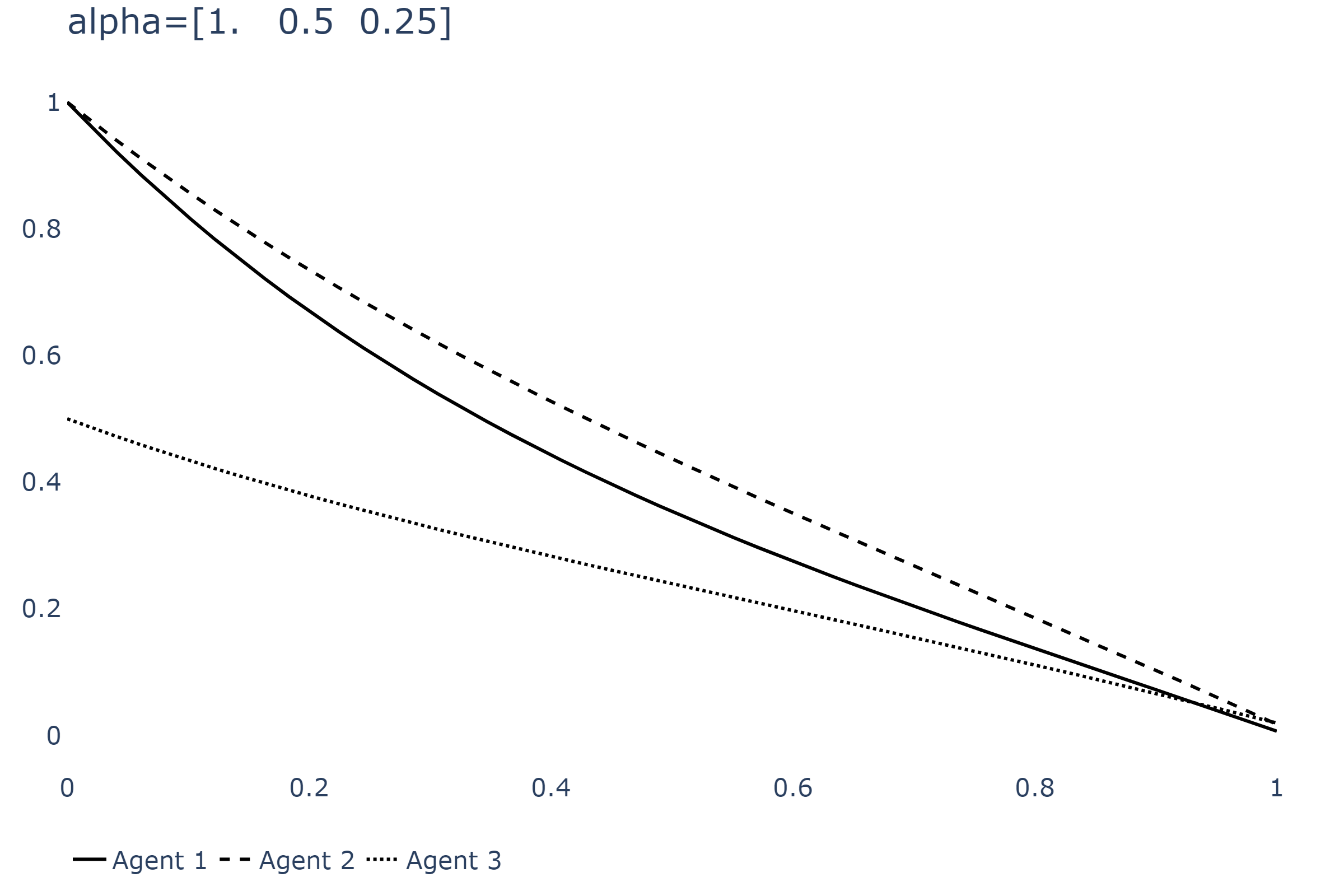

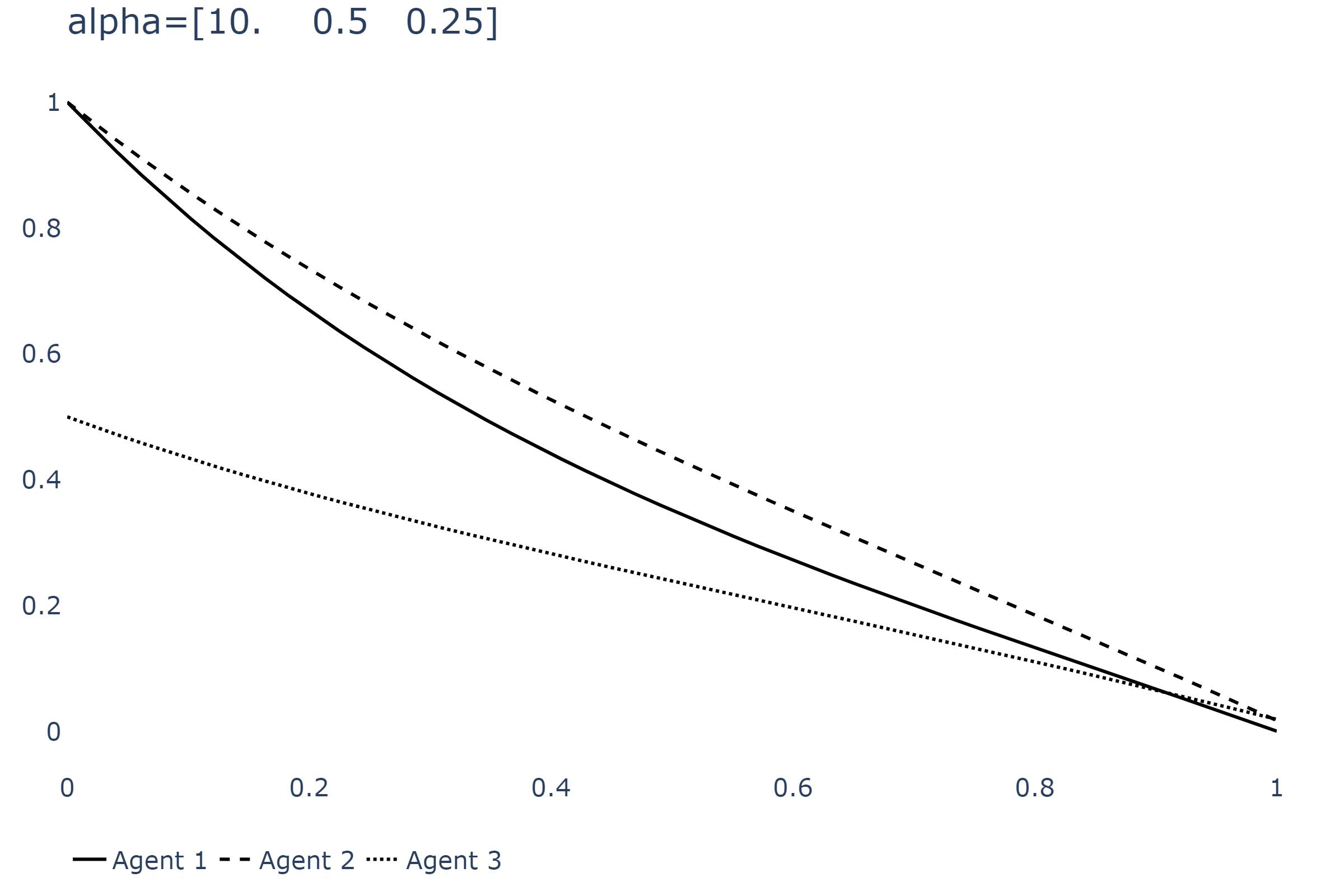

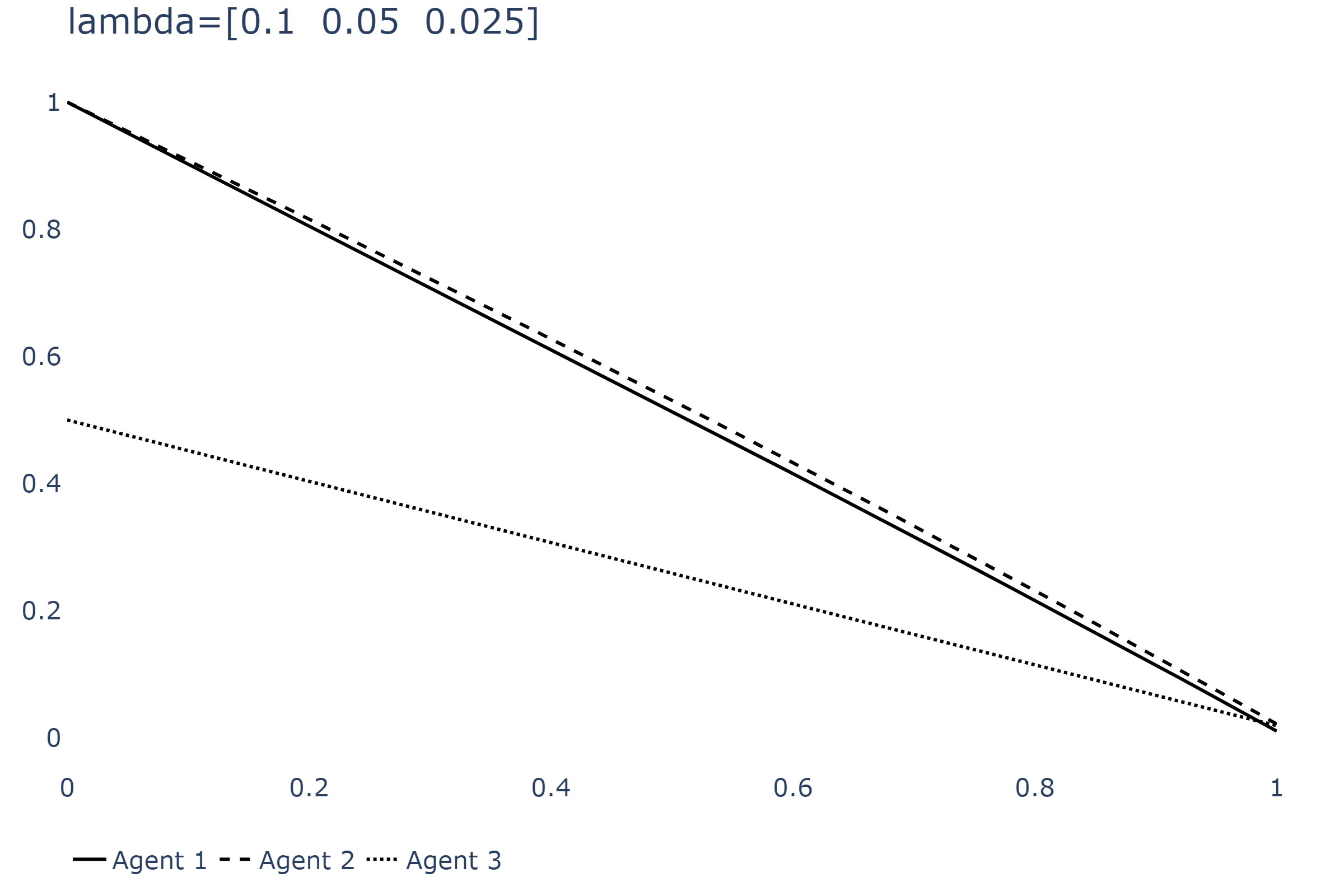

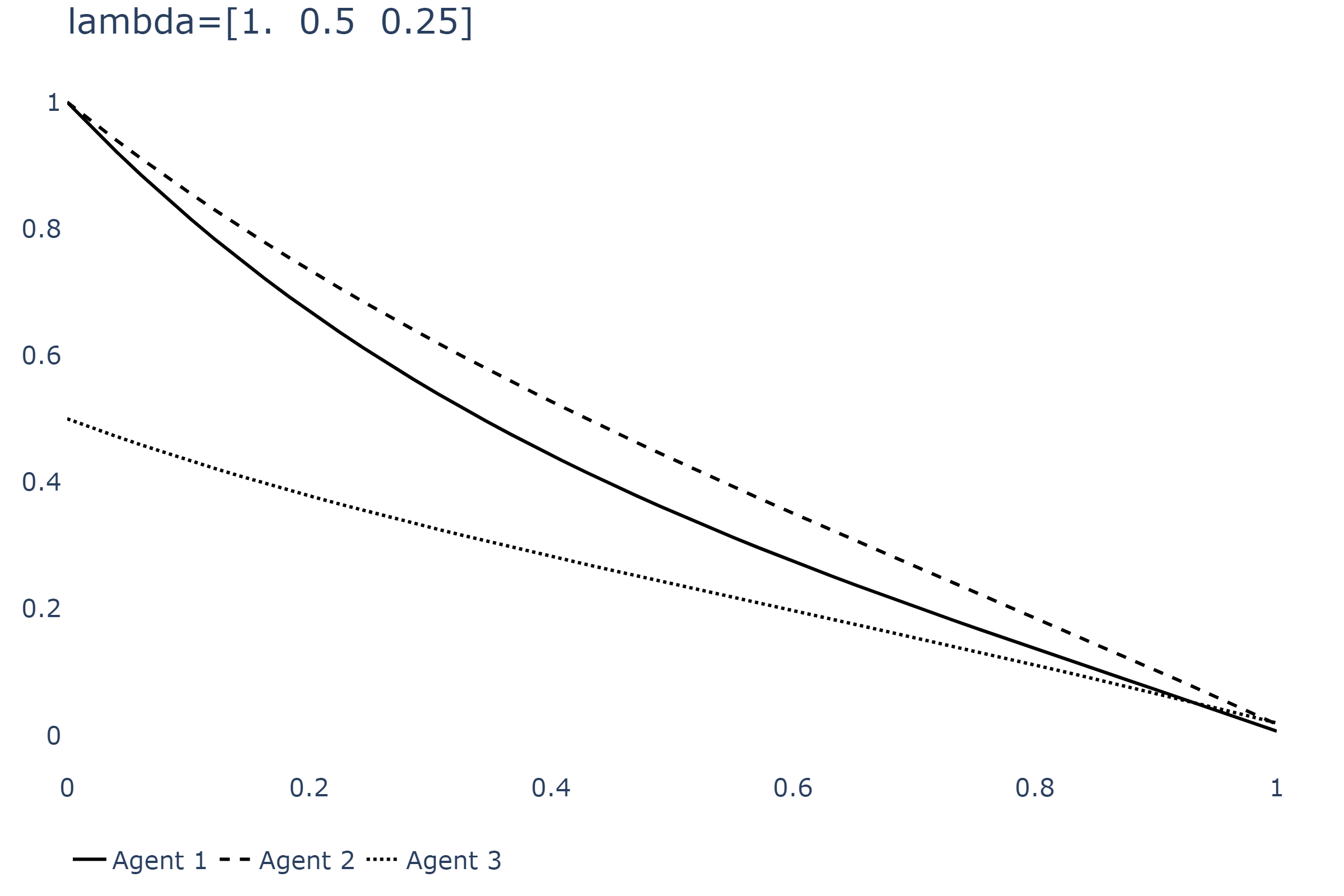

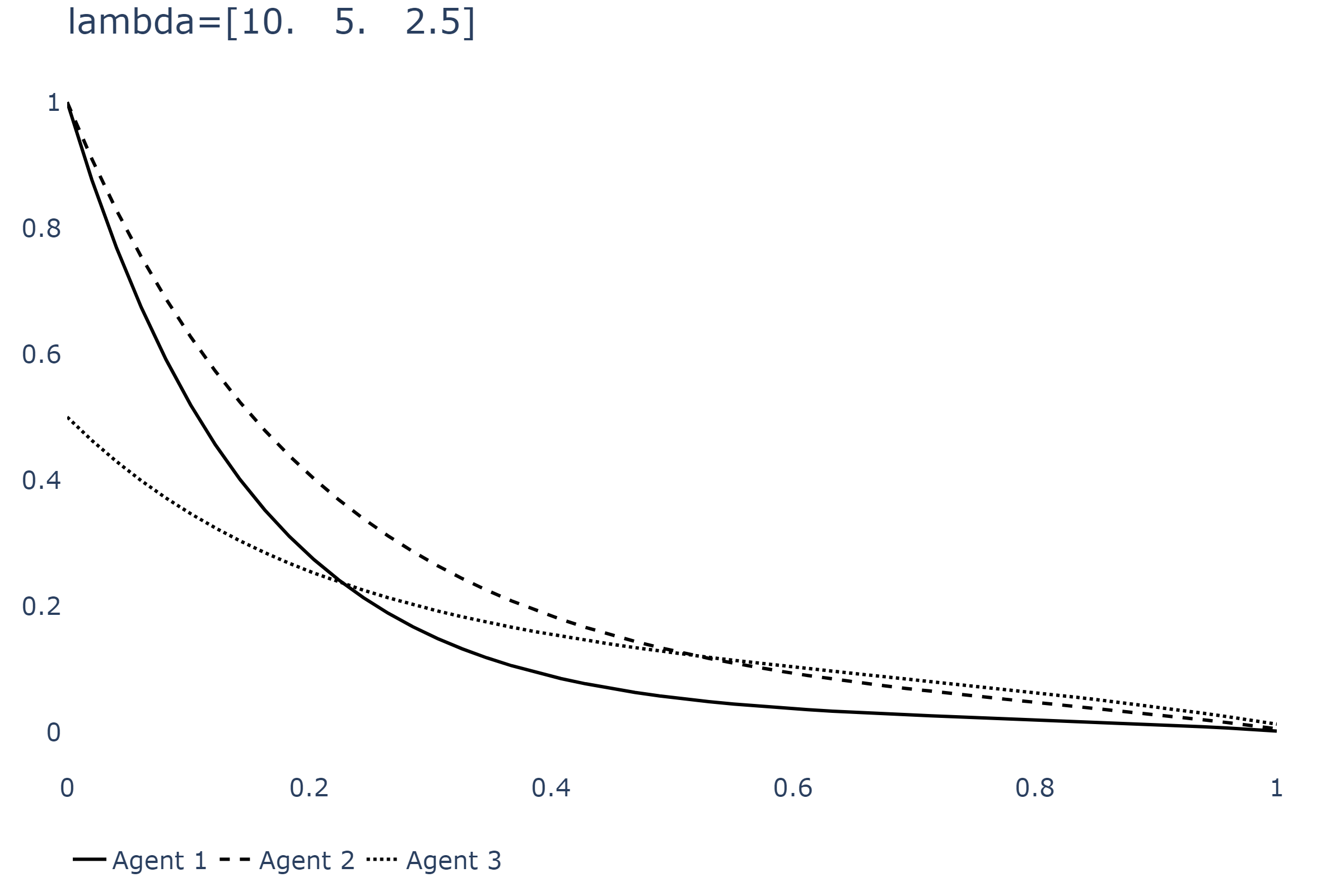

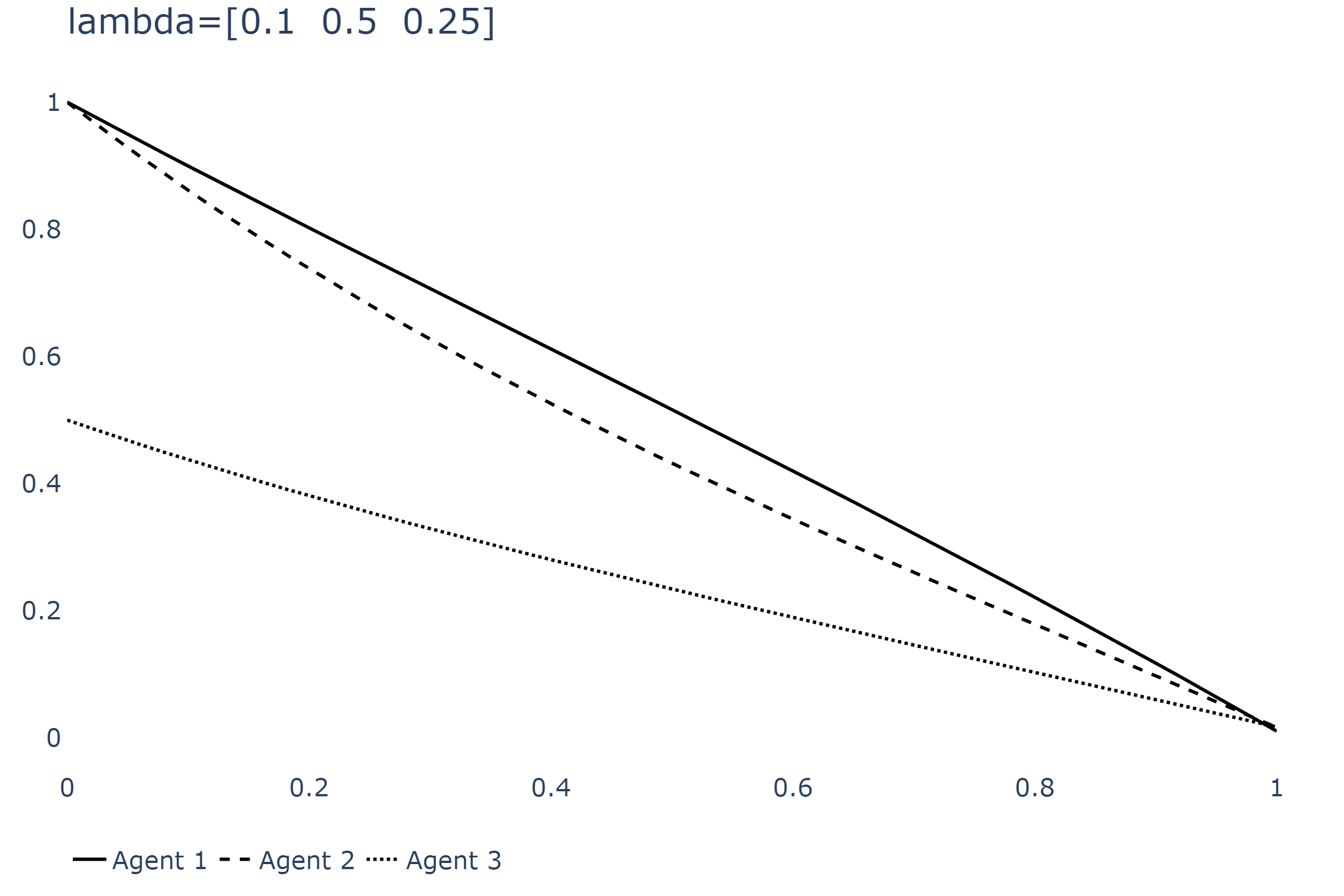

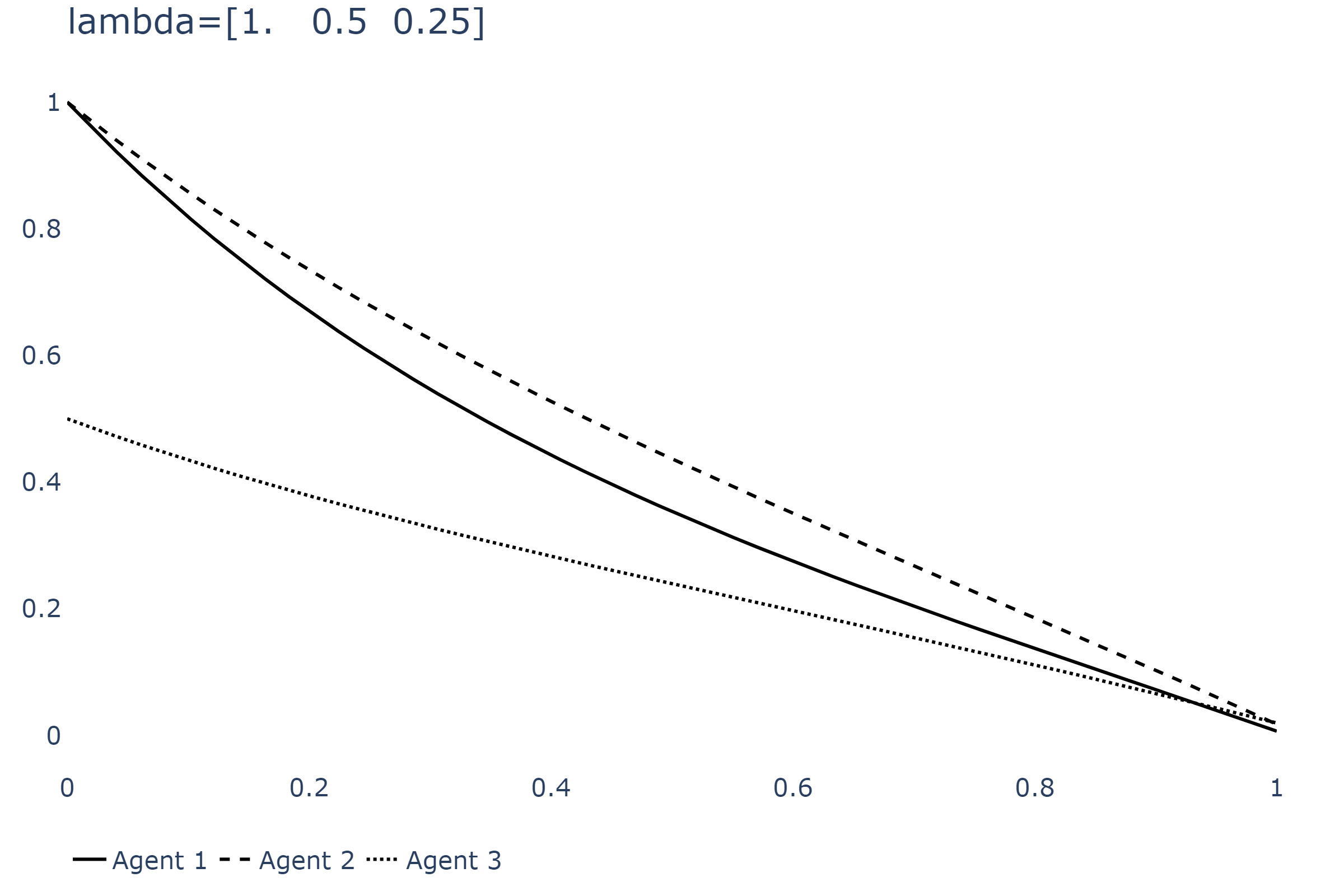

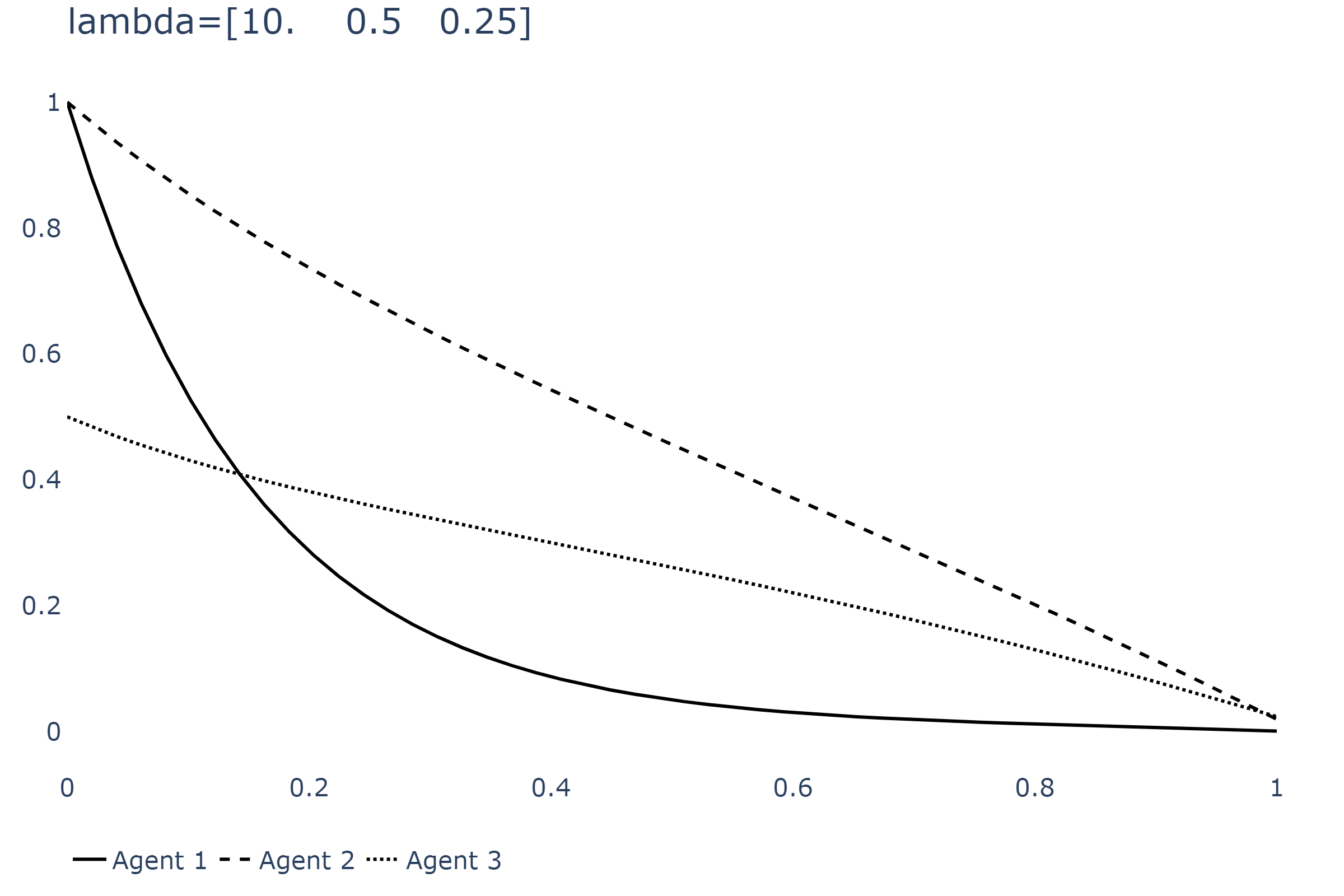

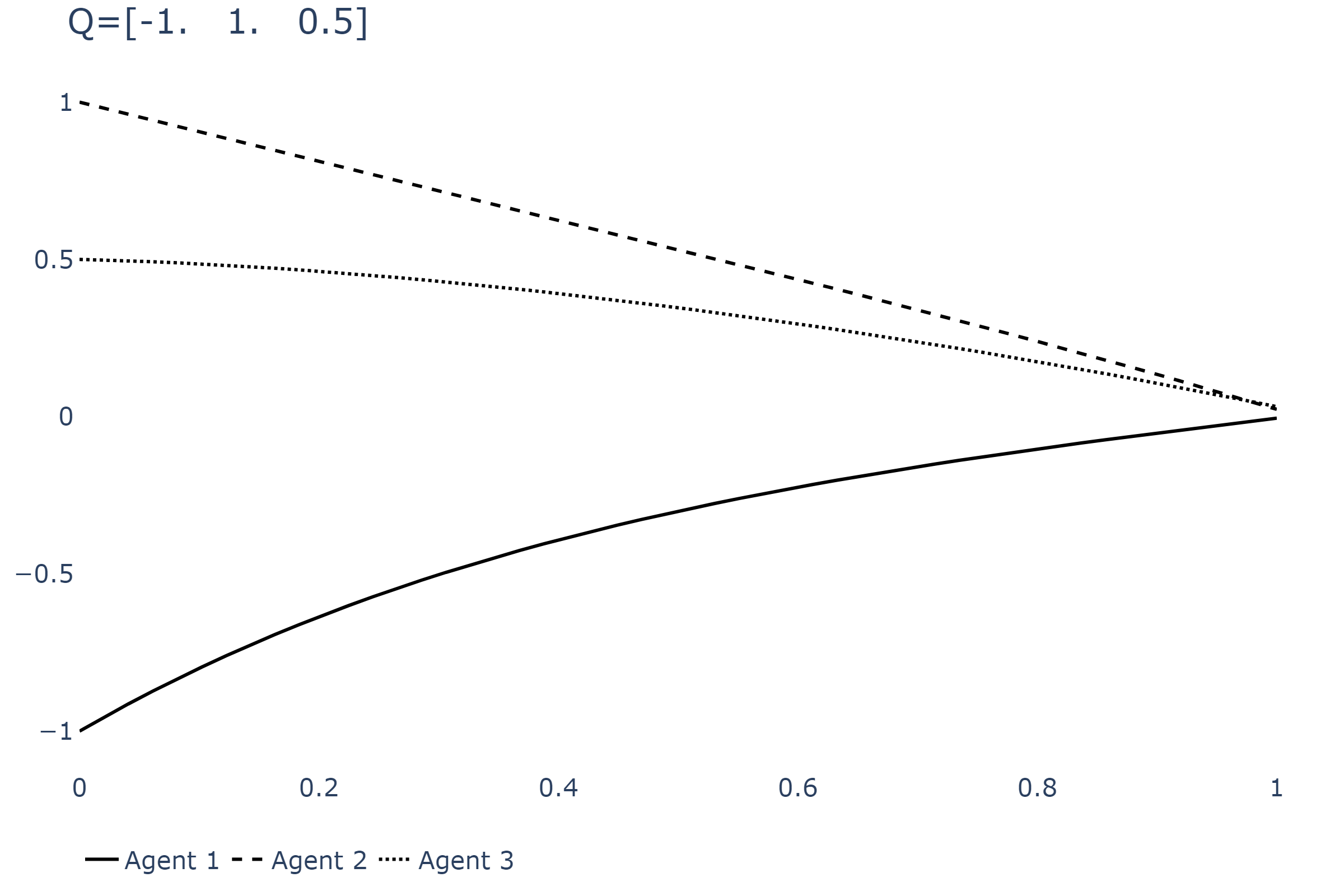

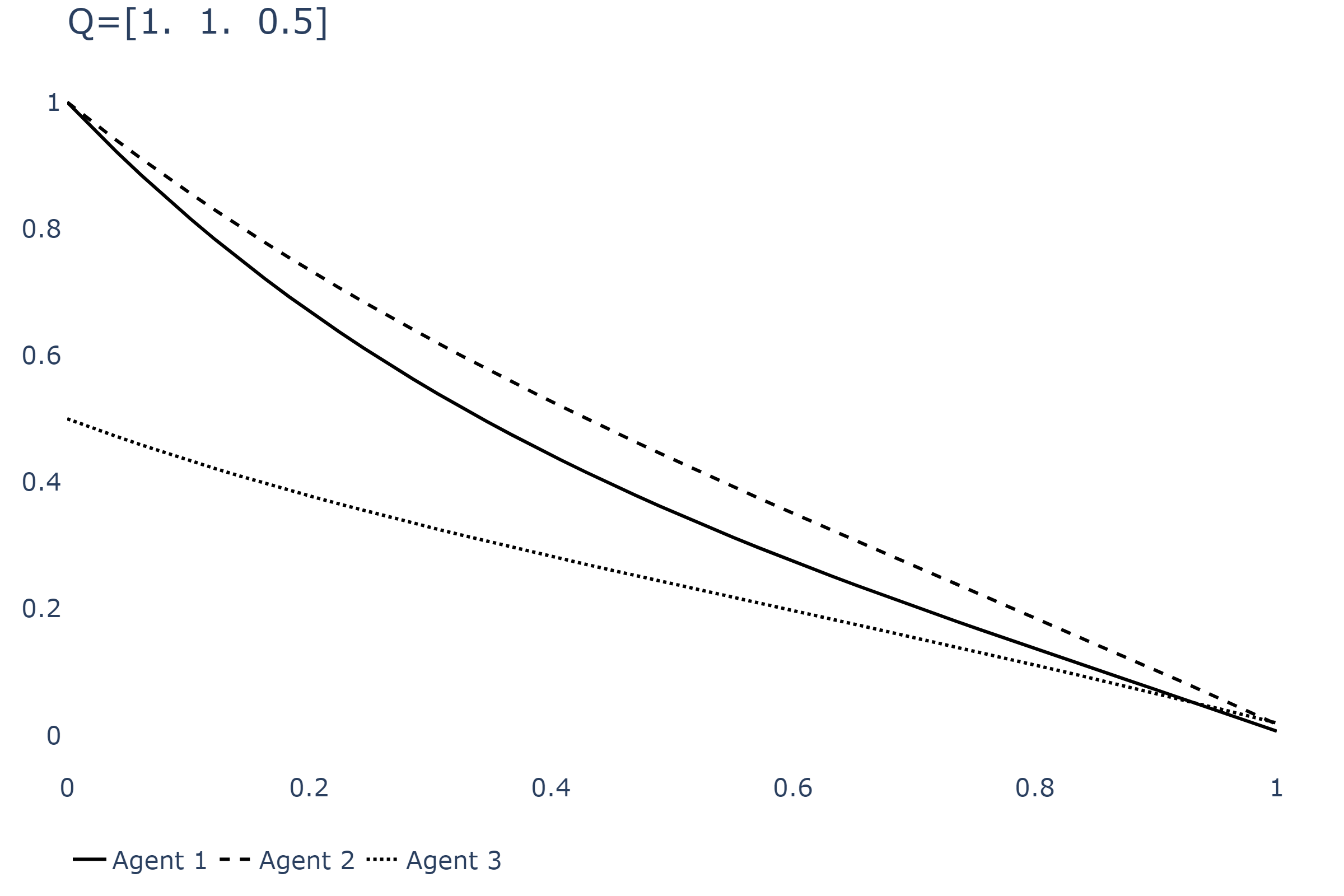

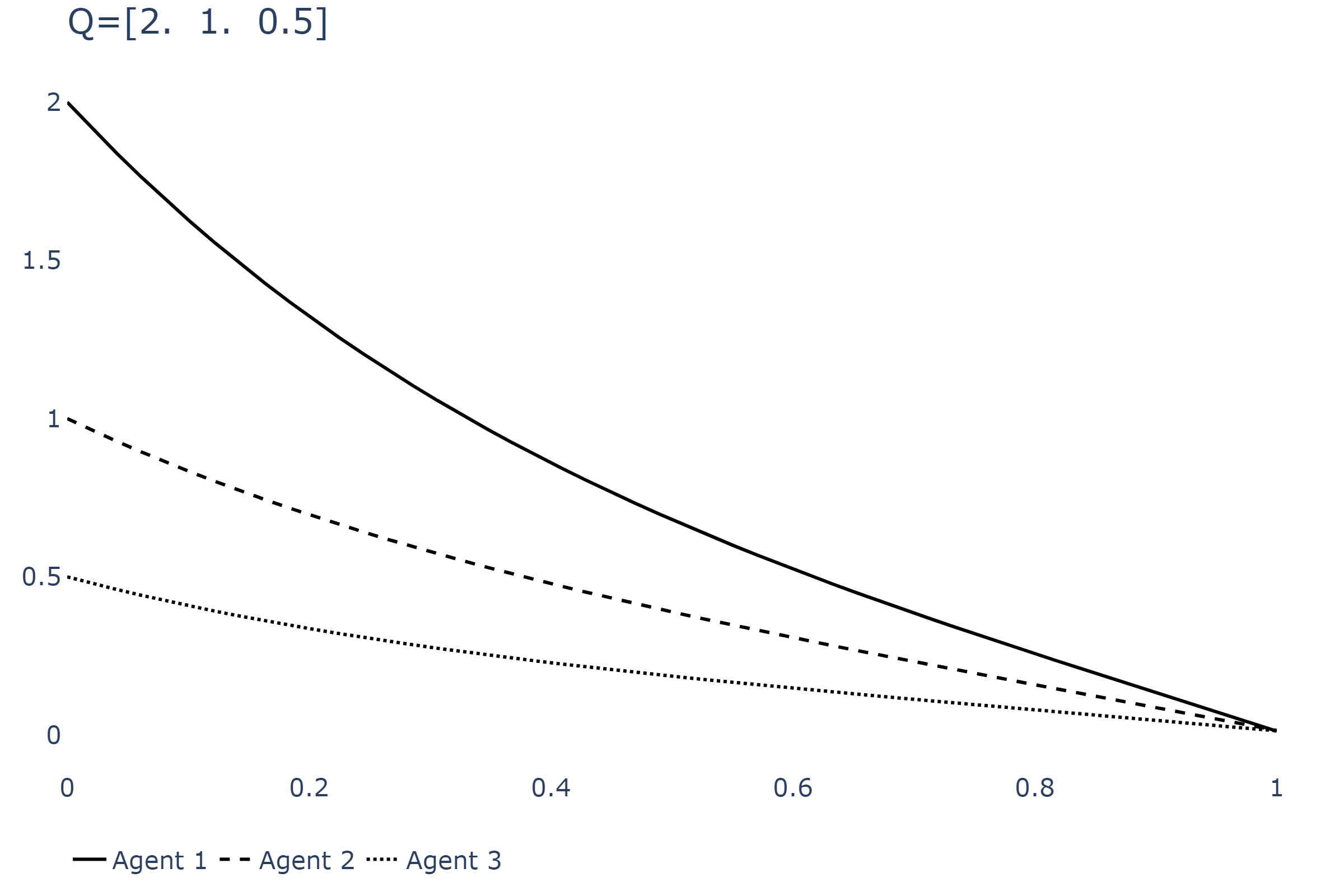

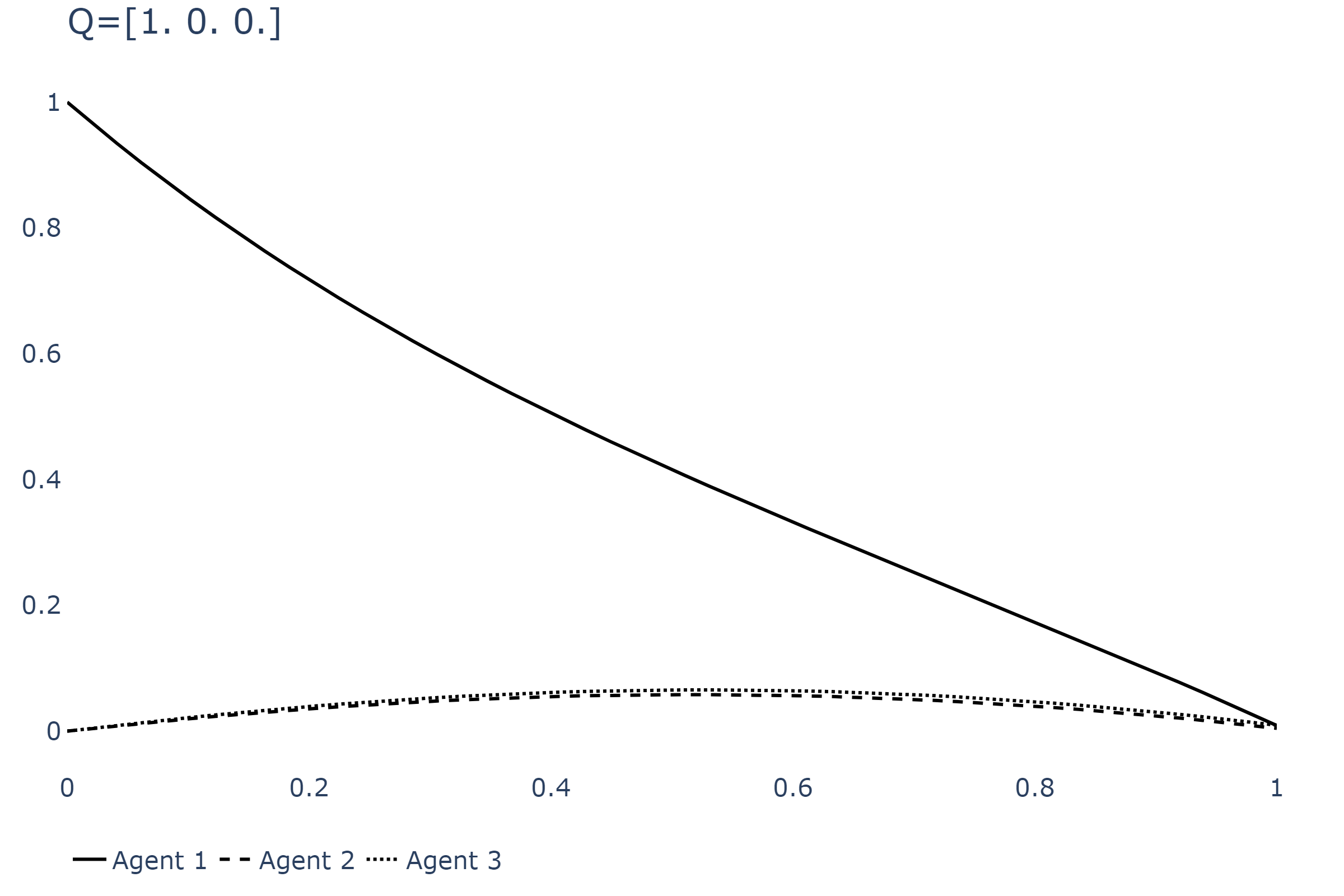

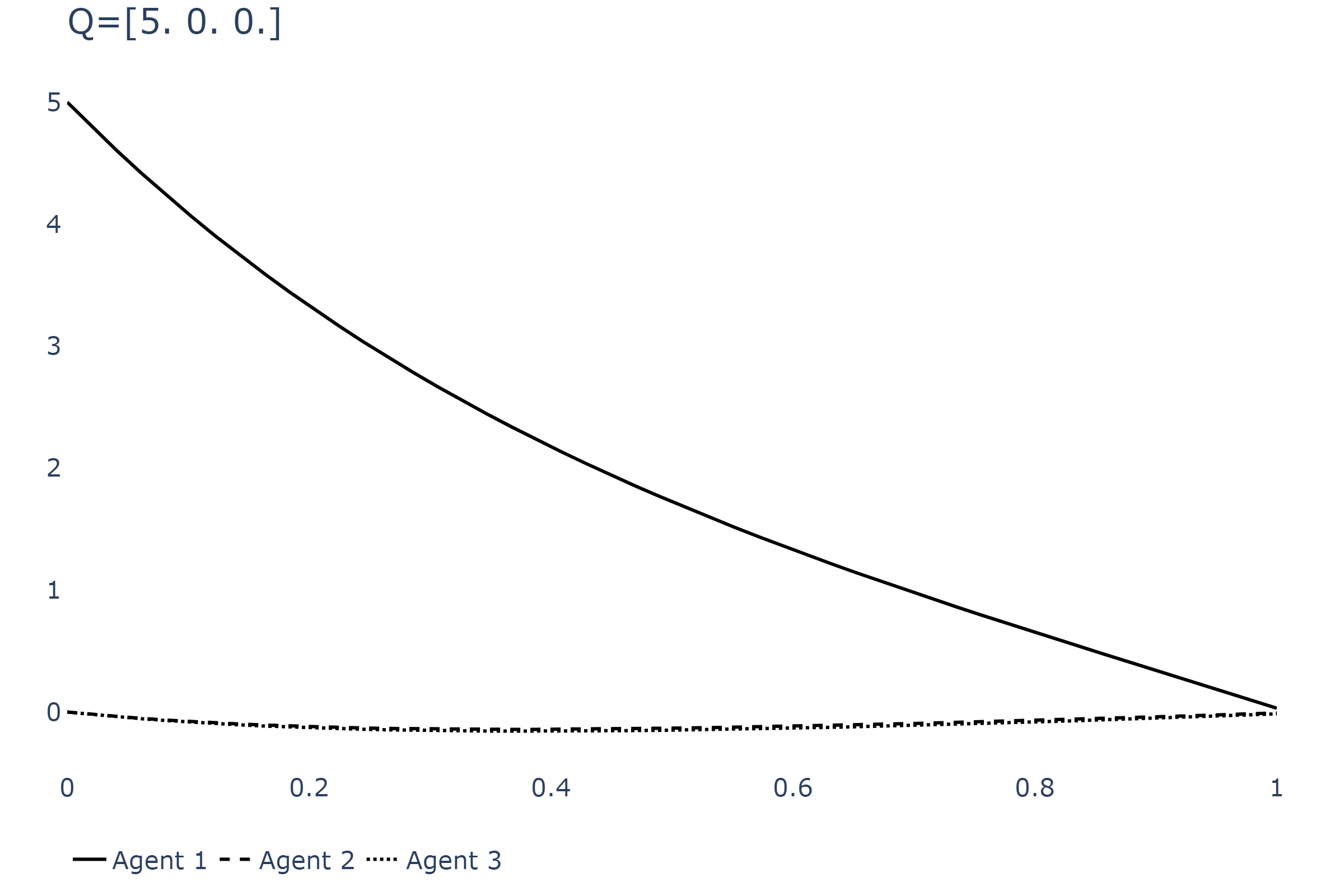

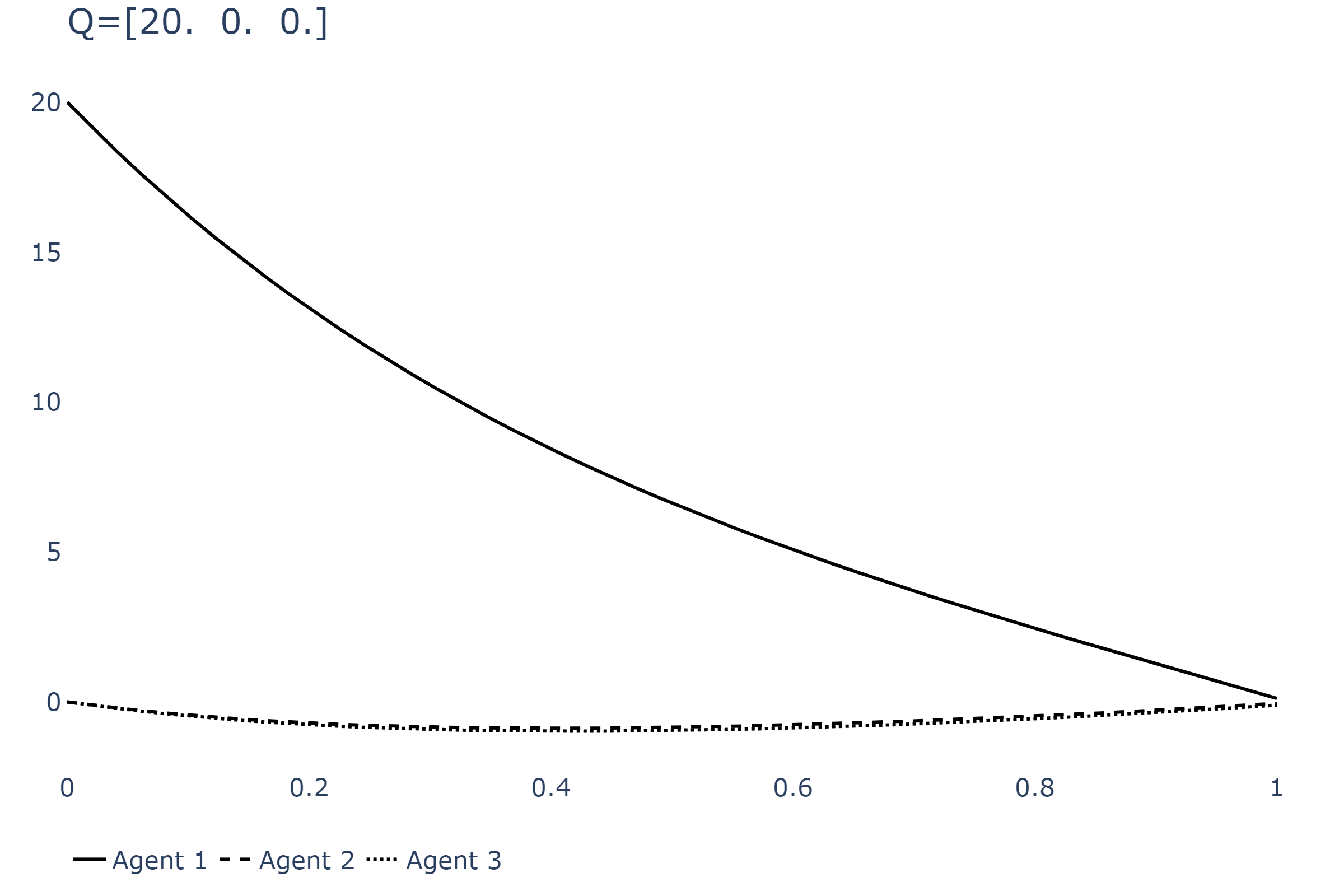

First, on the mathematical side, we completely solve the problem of determining an open-loop Nash equilibrium with stochastic model parameters and risk aversion for arbitrary numbers of agents. Our solution relies on a characterization of the equilibrium strategies in terms of a fully coupled systems of forward-backward stochastic differential equations (FBSDEs). This characterization is given in Theorem 4.1. In the subsequent Theorem 4.2, we give sufficient conditions that guarantee the existence of a unique solution. The main restriction is a lower bound on the volatility. Then we analyze the case of constant coefficients and the case in which all agents share the same parameters but have different initial inventories. Numerical simulations are provided for the case of constant coefficients which work for many agents.

Our second contribution consists in a modification of the traditional setup of the interaction term in a market impact game with Almgren–Chriss-style price impact. The Almgren–Chriss model has two price impact components, one permanent and one temporary. It is clear that permanent price impact must affect the execution prices of all agents equally, and in [6, 23, 7, 19, 8] the same is assumed of the transient price impact. This assumption can sometimes lead to counterintuitive results. For instance, if the temporary price impact is large in comparison with the permanent price impact, then, in the presence of a large seller, it can be beneficial to build up a long position in the stock, because a cessation of the trading activities of the large seller will lead to an immediate upwards jump of the expected price [23]. In the price impact literature, it is however not consensus that “temporary price impact” is of the same nature as permanent price impact. For instance, Almgren et al. [3] write about temporary impact:

This expression is a continuous-time approximation to a discrete process. A more accurate description would be to imagine that time is broken into intervals such as, say, one hour or one half-hour. Within each interval, the average price we realise on our trades during that interval will be slightly less favorable than the average price that an unbiased observer would measure during that time interval. The unbiased price is affected on previous trades that we have executed before this interval (as well as volatility), but not on their timing. The additional concession during this time interval is strongly dependent on the number of shares that we execute in this interval.

Likewise, Gatheral [10, p. 751] writes:

The second component of the cost of trading corresponds to market frictions such as effective bid-ask spread that affect only our execution price: We refer to this component of trading cost as slippage (temporary impact in the terminology of Huberman and Stanzl).

Based on these interpretations of “temporary price impact” as slippage, it appears to be more natural that only the trades of the executing agent and not the trades of the other market participants are affected by the resulting cost. In our paper, we therefore keep a term for “temporary price impact”, but it only affects the execution costs of the corresponding agent and not of the other agents.

The paper is organized as follows. In Section 2, we set up our model on portfolio liquidation in the Almgren-Chriss framework. Single agent optimization is studied in Section 3, where the corresponding existence, uniqueness and characterization results for the optimal liquidation strategy are stated. Section 4 is dedicated to present the characterization result for Nash equilibrium and investigates the solvability of the characterizing FBSDE. Some explicit solutions for Nash equilibria are analyzed in Section 5.

3 Single-agent optimization

In preparation for the discussion of Nash equilibria defined at the end of Section 2.2, we analyze first the optimization problem for a fixed agent when the strategies of all other agents are fixed. A variety of methods has been used to solve similar and related problems; see, e.g., [2, 9, 24, 17, 12, 4]. Here, our goal is to represent solutions in terms of a BSDE in Theorem 3.1.

First, plugging formula (2.1)

for into our expression (2.3)

of the cost-risk functional and integrating by parts, we obtain the alternative expression

|

|

|

|

|

|

|

|

Since, by assumption, and , the stochastic integral is a true martingale, and so taking expectations yields

|

|

|

|

|

|

|

|

In the following, we will denote . Fixing , let

|

|

|

and be the total cost on if, at time , agent starts using the strategy with the inventory , i.e.,

|

|

|

|

|

|

|

|

Let

|

|

|

|

|

|

|

|

Our next goal is to obtain a representation of

|

|

|

in terms of component of a solution of a three-dimensional BSDE, which will be discussed in the following proposition.

Proposition 3.1

Suppose that and , then the following BSDE

|

|

|

admits a unique solution . Moreover, the solution of the BSDE

|

|

|

is well defined and given by

|

|

|

Proof. Denoting , it follows from Pardoux and Peng [15] that BSDE

|

|

|

admits a unique solution . Moreover, we have the following estimate for ,

|

|

|

|

Meanwhile by denoting , it holds that

|

|

|

|

|

|

|

|

Therefore, we have

|

|

|

|

Hence, and satisfies

|

|

|

It is easy to check that . On the other hand, if

|

|

|

admits a solution , we have

|

|

|

|

and

|

|

|

|

|

|

|

|

Therefore, we have

|

|

|

|

Hence, satisfies

|

|

|

Again, it follows from Pardoux and Peng [15] that

|

|

|

admits a unique solution . The rest is clear.

Theorem 3.1

Suppose that and , then is given by

|

|

|

where are given as in Proposition 3.1. The unique optimal strategy for the agent is given in feedback form by

|

|

|

Proof. By denoting

|

|

|

and applying Itô’s formula, we have

|

|

|

|

|

|

|

|

|

|

|

|

Therefore it holds

|

|

|

|

|

|

|

|

|

and rearranging the drift terms, one can see

|

|

|

|

|

|

|

|

|

|

|

|

Hence, it holds that

|

|

|

|

|

|

|

|

Therefore, for any and , by taking for all , we have

|

|

|

|

|

|

|

|

which implies that

|

|

|

Hence, it holds that

|

|

|

|

|

|

|

|

On the other hand, for any and , the following random ODE

|

|

|

admits a unique solution on . Therefore, by taking with

|

|

|

we have

|

|

|

|

|

|

|

|

which implies that

|

|

|

|

|

|

|

|

Therefore, it holds that

|

|

|

It is easy to verify that the unique optimal strategy feedback form for the agent is given by

|

|

|

3.1 Characterization of the optimal strategy in terms of an FBSDE

In this section, we show that the optimal strategy for agent can be given by the unique solution of an FBSDE.

Theorem 3.2

Suppose that and , then is the unique solution of the following FBSDE

|

|

|

(3.1) |

in .

Proof. By denoting

|

|

|

it is easy to deduce that:

|

|

|

|

|

|

|

|

|

|

|

|

Therefore, it holds that

|

|

|

|

Noting that

|

|

|

one has

|

|

|

|

|

|

|

|

Therefore, it holds that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

It is easy to check that is in . We now prove the uniqueness. Suppose that FBSDE (3.1) admits another solution . Then, we have

|

|

|

Therefore, it holds that

|

|

|

|

|

|

|

|

Thus, it holds that

|

|

|

which implies uniqueness.