citecolor=blue, urlcolor = black,

Globally Optimal And Adaptive Short-Term Forecast of Locally Stationary Time Series And A Test for Its Stability

Abstract

Forecasting the evolution of complex systems is one of the grand challenges of modern data science. The fundamental difficulty lies in understanding the structure of the observed stochastic process. In this paper, we show that every uniformly-positive-definite-in-covariance and sufficiently short-range dependent non-stationary and nonlinear time series can be well approximated globally by an auto-regressive process of slowly diverging order. When linear prediction with loss is concerned, the latter result facilitates a unified globally-optimal short-term forecasting theory for a wide class of locally stationary time series asymptotically. A nonparametric sieve method is proposed to globally and adaptively estimate the optimal forecasting coefficient functions and the associated mean squared error of forecast. An adaptive stability test is proposed to check whether the optimal forecasting coefficients are time-varying, a frequently-encountered question for practitioners and researchers of time series. Furthermore, partial auto-correlation functions (PACF) of general non-stationary time series are studied and used as a visual tool to explore the linear dependence structure of such series. We use extensive numerical simulations and two real data examples to illustrate the usefulness of our results.

Keywords: Optimal prediction, auto-regressive approximation, non-stationary time series, correlation stationarity test.

1 Introduction

It is of critical importance to understand the structure of time series in order to accurately forecast the future. For a stationary process , Baxter established an important result on its structure in Baxter (1962, 1963). Together with the deep representation theorems of stationary processes formed in, for instance, Wiener and Masani (1958) and Pourahmadi (2001), Baxter’s inequality implies that can be well approximated by an auto-regressive (AR) process of slowly diverging order provided that is of short memory and uniformly positive spectral density. Consequently, as long as linear prediction with minimum mean squared error (MSE) is concerned, Baxter’s inequality serves as a theoretical foundation that guarantees the asymptotic optimality of forecasting a wide class of stationary processes by AR models with slowly diverging order. Nowadays, as increasingly longer time series are being collected in the modern information age, it has become more appropriate to model many of those series as non-stationary processes whose data generating mechanisms evolve over time. As a result there has been an increasing demand for a systematic optimal forecasting theory for non-stationary processes. Nevertheless, it has been a difficult and open problem to establish general structural representations such as those of Baxter in the non-stationary domain. The main difficulty lies in the loss of Toeplitz structure for covariance matrices of general non-stationary time series. As a consequence deep connections between Toeplitz matrices and their spectral density functions (cf. e.g., Toeplitz (1911), Kac (1954), Grenander and Szegö (2001)) which are crucial in the proof of structural representations of stationary processes cannot be used directly in the non-stationary case.

The purpose of the paper is fourfold. Firstly, we establish a unified structural representation result that every short memory and uniformly-positive-definite-in-covariance (UPDC) non-stationary time series can be well approximated globally by a non-stationary white-noise-driven AR process of slowly diverging order. Here the speed of the divergence is determined by the strength of the temporal dependence. In the best scenario where the temporal dependence is of exponential decay, the order is . Instead of resorting to Toeplitz matrix and spectral density techniques, our proof of the result heavily depends on random matrix theory which controls the proximity of non-stationary covariance matrices and their banded truncations as well as modern spectral theory Demko et al. (1984) that controls the decay rates of inverse of banded matrices. In the special case of locally stationary time series, that is, non-stationary time series whose data generating mechanisms evolve smoothly over time, the UPDC condition is shown to be equivalent to uniform time-frequency positiveness of the spectral density of and the approximating AR process is shown to have smoothly time-varying coefficients. In particular, when linear prediction with loss is concerned, our structural representation result implies that a wide class of locally stationary time series can be asymptotically optimally predicted by an AR model with slowly diverging order and smoothly changing coefficients in the short term.

Secondly, we propose a nonparametric sieve-based regression method to adaptively estimate the time-varying optimal linear forecast coefficients and the associated MSE of forecast. Specifically, we approximate every smooth coefficient function by a finite but diverging term orthonormal basis expansion and perform one high-dimensional simple linear regression to estimate all the coefficient functions which is computationally easy and stable to implement. Contrary to most non-stationary time series forecasting methods in the literature where only data near the end of the sequence are used to estimate the parameters of the forecast, our nonparametric sieve regression is global in the sense that it utilizes all available time series observations to determine the optimal forecast coefficients and hence is expected to be more efficient. Indeed, by controlling the number of basis functions used in the regression, we demonstrate that the sieve method is adaptive in the sense that the estimation accuracy achieves global minimax rate for nonparametric function estimation in the sense of Stone (1982). Additionally, since the sieve regression uses all time series observations, the estimated coefficient functions do not have inferior performances at the boundary of the estimating interval when certain sieves such as the Fourier and wavelet expansions are used. The latter property is an important advantage of the nonparametric sieve method as the short term forecast is determined by the estimated regression coefficient at the right boundary. On the contrary, local nonparametric methods such as the kernel regression face relatively sparse data near the boundary and hence produce more volatile estimates in those regions.

Our third purpose is to develop an adaptive stability test for the optimal forecast coefficients. Many practitioners tend to use classic ARMA models with constant coefficients for time series prediction. Hence it is of great importance to check whether the optimal forecast coefficient functions are time-varying in order to either justify or invalidate such practice. To our knowledge, there exist no results on testing stability of the optimal forecast coefficients for general classes of non-stationary time series in the literature. In this paper, we develop an nonparametric test for the constancy of the optimal forecast coefficients based on their sieve estimators. The test is shown to be adaptive to the strength of the time series dependence as well as the smoothness of the underlying data generating mechanism. The theoretical investigation of the test critically depends on a result on Gaussian approximations to quadratic forms of high-dimensional non-stationary time series developed in the current paper. In particular, uniform Gaussian approximations over high-dimensional convex sets (Chen and Fang (2011) and Fang (2016)) as well as -dependent approximations to quadratic forms of non-stationary time series are important techniques used in the proofs. On the other hand, we demonstrate that stability of the forecast coefficients is asymptotically equivalent to correlation stationarity of locally stationary time series. Here correlation stationarity means that the correlation structure of the time series does not change over time. As a result, our stability test can also be viewed as an adaptive test for correlation stationarity. In the statistics literature, there is a recent surge of interest in testing covariance stationarity of a time series using techniques from the spectral domain. See, for instance, Paparoditis (2010), Dwivedi and Rao (2011), Dette et al. (2011) and Nason (2013). Observe that the time-varying marginal variance has to be estimated and removed from the time series in order to apply those tests to checking correlation stationarity. However, it is unknown whether the errors introduced in such estimation would influence the finite sample and asymptotic behaviour of the tests. Furthermore, estimating the marginal variance involves the difficult choice of a smoothing parameter. One major advantage of our test when used as a test of correlation stationarity is that it is totally free from the marginal variance as the latter quantity is absorbed into the errors of the high-dimensional linear regression and hence is independent of the optimal forecast coefficients. Additionally, our test is expected to be more powerful than the aforementioned tests of covariance stationarity as the latter tests are generally not adaptive to the strength of time series dependence or the smoothness of the data generating mechanism. We refer the readers to Section 6 for a related simulation study. Finally, we mention that Dette et al. (2019) studied change point tests for correlations of non-stationary time series. However, their test can only be applied to a fixed number of lags and cannot be used as a test for overall correlation stationarity of time series.

Finally, we study the partial auto-correlation function (PACF) for general non-stationary time series and use it as a visual tool to study non-stationary time series dependence structure and preliminarily determine an appropriate order of the AR approximation for the optimal forecast. The PACF is a commonly used tool to study the pattern of temporal dependence and determine the order of an AR model in stationary time series analysis (cf. e.g. Brockwell and Davis (2002)). However, to our knowledge there exists no work in the literature conducting statistical inference of PACF under non-stationarity. For a general non-stationary time series, we investigate the PACF as a two-dimensional function of time and lag and develop its uniform decay rate which is determined by the magnitude of the time series dependence measure. In the special case of locally stationary time series, a sieve method is proposed to estimate the smoothly time-varying PACF which is shown to be adaptive and uniformly consistent. For a groups of lags, an test is developed to check whether the PACF at those lags are uniformly zero across time. Consequently, one can visually investigate the pattern of time series dependence not only across lag but also over time from the estimated PACF plot. Together with the -values of the tests, one is able to identity when the time series dependence disappears from the PACF plot and hence preliminarily determine an appropriate order of the AR model for the optimal forecast.

In the statistics literature, there have been some scattered works discussing non-stationary time series prediction. Among others, Fryzlewicz et al. (2003) considered forecasting locally stationary time series by their wavelet process representations and established a wavelet-based prediction equation which is derived from the corresponding Yule-Walker equation; Roueff and Sanchez-Perez (2018) used time-varying AR models of a fixed order to forecast a locally stationary time series; Kley et al. (2016) investigated finite-sample forecasting performances of locally stationary time series using Yule-Walker estimators of both fixed and time-varying parameters. In all the above mentioned works, the optimality of the truncated or clipped AR approximation was not discussed and the non-stationary auto-covariance functions was estimated by simple kernel methods which were not adaptive to the smoothness of the latter functions. On the other hand, Das and Politis (2017) considered optimal model-based and model-free predictions of two special classes of locally stationary time series; that is, locally stationary time series which are correlation stationary and locally stationary processes that can be marginally transformed into stationary Gaussian processes.

At last, we would like to mention that Baxter’s inequality has been extended in many different ways and the application of it goes way beyond optimal forecasting. See, for instance, Cheng and Pourahmadi (1993) for an extension to multivariate processes, Meyer et al. (2015) for an extension to triangular arrays, and Inoue et al. (2018) for an extension to long memory processes. On the application side, among others, Baxter’s inequality is a key component for the theoretical investigation of the sieve bootstrap (Kreiss (1988) and Kreiss et al. (2011)).

This paper is organized as follows. In Section 2, we introduce AR approximation results for general non-stationary time series. The time-varying PACF is also properly defined in this section. In Section 3, we study AR approximation of locally stationary time series. In Section 4, asymptotically globally optimal forecast of locally stationary time series using the AR approximation is studied and the nonparametric sieve method is proposed to estimate the best forecast coefficient functions and the associated MSE of forecast. In Section 5, we test the stability of the best linear forecast using statistics of the estimated forecast coefficient functions. A robust bootstrapping procedure is proposed for practical implementation. In Section 6, we use extensive Monte Carlo simulations to verify the accuracy of our prediction and test. In Section 7, we conduct analysis on two real datasets using our proposed methods. Technical proofs are deferred to an online supplementary material.

2 AR approximations and PACF for general non-stationary time series

In this section, we establish a general AR approximation theory for non-stationary time series. A study of the PACF of such series will also be conducted. We start with introducing some notation. For a matrix or vector we use and to stand for their transposes. For a sequence of random variables and real values we use the notation to state that is stochastically bounded. Similarly, we use the notation to say that converges to 0 in probability. In this paper, unless otherwise specified, for a sequence of random variables we use the notation to state that is stochastically bounded uniformly in the index For general non-stationary time series , we assume that it has the following form

| (2.1) |

where and are i.i.d. random variables and the sequence of functions are measurable functions such that for all is a properly defined random variable. The above representation is very general since any non-stationary time series can be represented in the form of (2.1) via the Rosenblatt transform (Rosenblatt, 1952). Till the end of the paper, we omit the subscript and simply write without causing any confusion.

Next we introduce the physical dependence measure defined in Wu (2005); Zhou (2013b); Zhou and Wu (2010) to quantify the temporal dependence of defined in (2.1).

Definition 2.1.

Let be an i.i.d. copy of Assuming that for some

| (2.2) |

Then for we define the physical dependence measure of by

| (2.3) |

where

In this paper, we focus on time series with short-range temporal dependence. Specifically, we impose the following assumption on the physical dependence measure .

Assumption 2.2.

There exists a constant , where is some fixed small constant, such that for some constant we have

| (2.4) |

The above assumption guarantees that the temporal dependence of decays polynomially fast. Additionally, in order to avoid erratic behaviour of the best linear forecast operators, the smallest eigenvalue of the time series covaraince matrix should be bounded away from zero. For stationary time series, this is equivalent to the uniform positiveness of the spectral density function widely used in Baxter (1962, 1963) et al. Further note that the latter assumption is mild and frequently used in the statistics literature of covariance and precision matrix estimation; see, for instance, Cai et al. (2016); Chen et al. (2013); Yuan (2010) and the references therein. In this paper we shall call this uniformly-positive-definite-in-covariance (UPDC) condition and we formally summarize it as follows.

Assumption 2.3 (UPDC).

For all there exists a universal constant such that

| (2.5) |

where is the smallest eigenvalue of the given matrix and is the covariance matrix of the given vector.

We then provide a simple sufficient condition for UPDC. Denote the covariance matrix of as For and we denote the banded truncation of by such that

Lemma 2.4.

Suppose that for all there exists an such that for some universal constant we have

| (2.6) |

Moreover, assume that for some positive constant such that

| (2.7) |

Then the UPDC condition holds.

2.1 AR approximation for general non-stationary time series

Throughout the paper, unless otherwise specified, we always assume that

| (2.8) |

where is an arbitrarily small and fixed constant. Here is defined in Assumption 2.2. In this section, we show that under Assumptions 2.2 and 2.3, can be well approximated by an process.

For denote as the best linear prediction based on its predecessors i.e.,

Denote Then

| (2.9) |

The theorem below provides a control for . It extends Baxter’s inequality to the non-stationary domain and is an important consequence of Assumptions 2.2 and 2.3 . It states that the magnitude of is negligible when uniformly for and the best linear forecast coefficients of based on and predecessors are close uniformly in .

Theorem 2.5.

For defined in (2.1), suppose Assumptions 2.2 and 2.3 hold true. For any fixed small constant defined in (2.8) and defined in (2.5), there exists some constant such that for satisfying and ,we have for

| (2.10) |

Moreover, denote by the best linear forecast coefficients of based on satisfying

Then we have that

| (2.11) |

An important consequence of Theorem 2.5 is that, under the short-range dependence and UPDC assumptions, any non-stationary time series can be efficiently approximated by an AR process of slowly diverging order. And the order of such approximation is adaptive to the temporal decay rate of the time series dependence. Formally, we summarize the above statements in the following proposition and theorem.

Observe that is a time-varying white noise process, i.e.,

Furthermore, denote the process by

| (2.13) |

By definition, is an AR() process.

Remark 2.8.

In this paper, our discussions are carried out under Assumption 2.2. Our results can be easily extended to the case when the temporal dependence is of exponential decay; i.e.

| (2.15) |

In this case, we can choose and Theorem 2.5 can be updated to

and the bounds in equations (2.11), (2.12) and (2.14) can be changed to .

2.2 PACF for general non-stationary time series

The PACF is a commonly used tool for dependence monitoring and model identification in time series analysis. In particular, it is well known that the PACF is useful in identifying the order of an AR model for stationary processes. The techniques developed for AR approximation in the last subsection can be easily employed to study the behaviour of PACF for general non-stationary time series. In the following, we shall explore this aspect in detail.

Consider the non-stationary time series (2.1), denote the -th order best linear forecast of as

Let and write

| (2.16) |

We next introduce the definition of -th order PACF for non-stationary time series, which is a natural extension for the corresponding definition of stationary process.

Definition 2.9.

For the non-stationary time series (2.1), the -th order PACF at time is defined as

Under Assumptions 2.2 and 2.3, similar to Theorem 2.5, we are able to establish the uniform speed of decay for the PACF. This is formally summarized as the following lemma.

We remark that when the physical dependence measure is of exponential decay, we can derive similar results as in Remark 2.8.

3 AR approximation for locally stationary time series

We now focus our study on an important subclass of (2.1), the locally stationary time series. This class of non-stationary time series is characterized by the fact that the underlying data generating mechanism evolves smoothly over time.

3.1 Locally stationary time series

Following Zhou and Wu (2009, 2010), we say that is a locally stationary time series if

| (3.1) |

where is a measurable function such that is a properly defined random variable for all In (3.1), by allowing the data generating mechanism depending on the time index in such a way that changes smoothly with respect to , one has local stationarity in the sense that the subsequence is approximately stationary if its length is sufficiently small compared to . For locally stationary time series , define the physical dependence measures

| (3.2) |

The following assumption guarantees that the data generating mechanism changes smoothly over time and thus the time series can be locally approximated by a stationary one.

Assumption 3.1.

defined in (3.1) satisfies the property of stochastic Lipschitz continuity, i.e., for some and

| (3.3) |

where Furthermore,

| (3.4) |

The following assumptions 3.2 and 3.3 states that the mean and covariance functions of are -times continuous differentiable for some positive integer .

Assumption 3.2.

For some given integer , we assume that there exists a smooth function where is the function space on of continuous functions that have continuous first derivatives, such that

For each fixed we denote the covariance function of the locally stationary time series as

| (3.5) |

The assumptions (3.3) and (3.4) ensure that is Lipschiz continuous in . Next, we impose the following mild assumption on the smoothness of

Assumption 3.3.

There exists some integer such that for any .

Armed with Assumptions 2.2, 2.3, 3.1 and 3.3, we can conclude that the covariance function decays polynomially fast uniformly in (c.f. Lemma S.2.7). Before concluding this section, we provide an insight on how to check UPDC condition for locally stationary time series. For stationary time series, Herglotz’s theorem asserts that UPDC holds if the spectral density function is bounded from below by a constant (see (Brockwell and Davis, 1987, Section 4.3) for more details). Our next proposition extends such results to locally stationary time series with short-range dependence.

Proposition 3.4.

We shall call the instantaneous spectral density function. Proposition 3.4 implies that the verification of UPDC reduces to showing that the instantaneous spectral density function is uniformly bounded from below by a constant, which can be easily checked for many non-stationary processes. Finally, we list the following example satisfying Assumptions 2.2, 3.1 and 3.3 and the UPDC condition using Proposition 3.4.

Example 3.5 (Non-stationary linear process).

Let be zero-mean i.i.d. random variables with variance . We also assume be functions such that

| (3.7) |

It is easy to see that Assumptions 2.2, 3.1 and 3.3 will be satisfied if

and

Further, we note that the instantaneous spectral density function of can be written as where is defined such that with being the backshift operator. By Proposition 3.4, the UPDC is satisfied if for all and where is some universal constant.

3.2 Smooth AR approximation for locally stationary time series

In this subsection, we focus our discussion on locally stationary time series (3.1) satisfying Assumptions 2.2, 2.3, 3.1, 3.2 and 3.3. We will show that there exists a smooth function which approximates when Specifically, denote via where and are defined as

with and is the -th entry of Moreover, we denote the time-varying function by

The statistical properties of the coefficients are summarized in the following theorem.

Theorem 3.6.

Armed with Theorem 3.6, we find that

| (3.8) |

Moreover, results similar to Theorem 2.7 can be proved, which is summarized in the following corollary. Denote

Corollary 3.7.

Suppose that the assumptions of Theorem 3.6 hold. Then we have

Next, when we show that there exists a smooth function of time such that for each lag the PACF can be well approximated by Denote

| (3.9) |

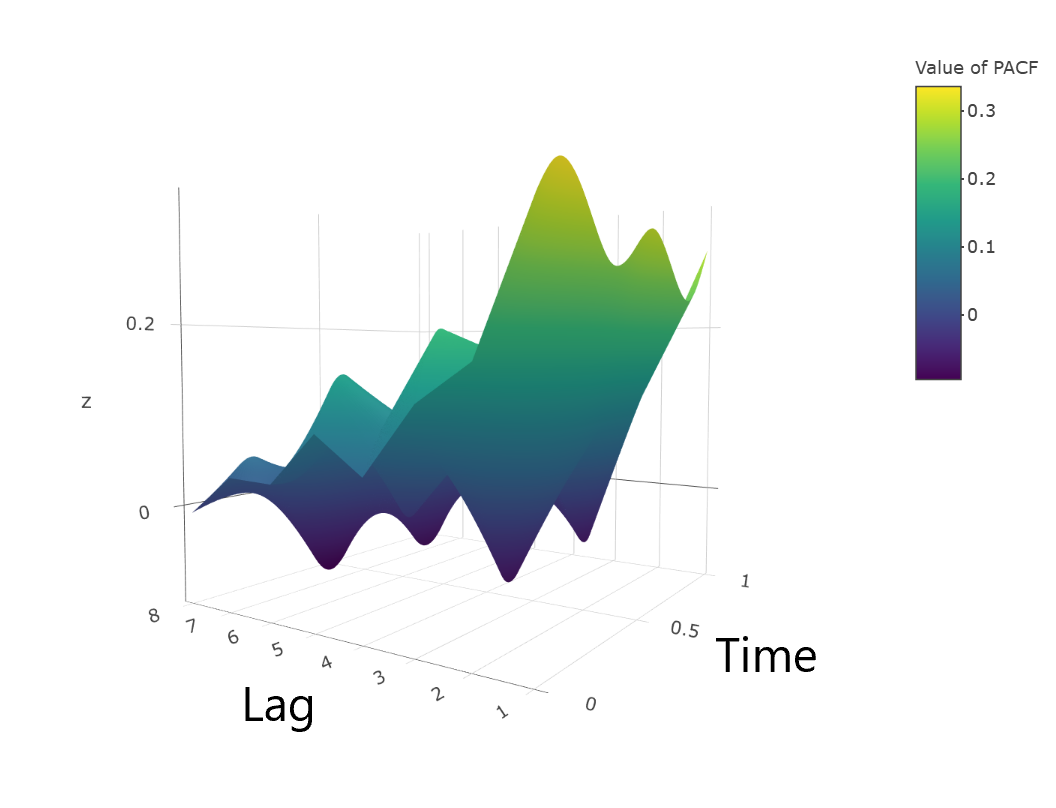

where and where with Denote We summarize the properties of in the lemma below. An example of PACF plot can be found in Figure 1.

Lemma 3.8.

Finally, we can get similar results as in Remark 2.8 when the physical dependence measure is of exponential decay.

4 Globally optimal and adaptive forecasting for locally stationary time series

In this section, we consider short-term forecasting of locally stationary time series by estimating the smooth forecasting coefficients using sieve expansion. We first introduce the notation of asymptotically optimal predictor.

Definition 4.1.

A linear predictor of a random variable based on is called asymptotically optimal if

| (4.1) |

where is the mean squared error (MSE) of the best linear predictor of based on .

The rationale for such definition is that, in practice, the MSE of forecast can only be estimated with a smallest possible error of when time series length is . It is well-known that the parametric rate for estimating the coefficients of a time series model is . When one uses the estimated coefficients to forecast the future, the corresponding influence on the MSE of forecast is (at best). Therefore, if a linear predictor achieves an MSE of forecast within range of the optimal one, it is practically indistinguishable from the optimal predictor asymptotically.

4.1 Asymptotically optimal short-term forecast for locally stationary time series

In this subsection, we shall focus on the discussion of one-step ahead prediction. The general case will be discussed briefly due to similarity. In order to make the forecasting feasible, we assume that the smooth data generating mechanism extends to time . That is, we assume . Naturally, we propose the following estimate for , the best linear predictor of based on all its predecessors ,

| (4.2) |

The next theorem shows that is an asymptotic optimal predictor satisfying (4.1) in Definition 4.1.

Theorem 4.2.

Theorem 4.2 states that the estimator (4.2) is an asymptotic optimal one-step ahead forecast since and .

Remark 4.3.

In the present paper, we focus on one-step ahead prediction. However, our results can be easily extended to -step ahead prediction for where is a fixed constant. We briefly discuss such extension. For general non-stationary time series, we denote by the -step ahead best linear prediction of i.e.

| (4.4) |

4.2 Sieve estimation of AR coefficients and MSE of forecast

In this section, we propose a global and adaptive nonparametric sieve method to estimate the coefficient functions and the associated MSE of forecast. Specifically, since we employ the sieve method to approximate it via a finite and diverging term basis expansion. By (Chen, 2007, Section 2.3), we have that

| (4.6) |

where are some pre-chosen basis functions on and is the number of basis functions which is of the order

| (4.7) |

In light of (4.6), we need to estimate For by (3.8), write

| (4.8) |

where for and By (4.8), we estimate all the using one ordinary least squares (OLS) regression with diverging number of predictors. In particular, we write all as a vector then the OLS estimator for can be written as , where and is the design matrix. After estimating is estimated using (4.6). Specifically,

| (4.9) |

where has blocks and the -th block is and zeros otherwise. Next, we provide an example to list some commonly used basis functions. We also refer to (Chen, 2007, Section 2.3) for a more detailed discussion.

Example 4.4.

(1). Normalized Fourier basis. For consider the following trigonometric polynomials

We note that the classical trigonometric basis function is well suited for approximating periodic functions on .

(2). Normalized Legendre polynomials Bell (2004). The Legendre polynomial of degree can be obtained using Rodrigue’s formula

In this paper, we use the normalized Legendre polynomial

The coefficients of the Legendre polynomials can be obtained using the R package mpoly and hence they are easy to implement in R.

(3). Daubechies orthogonal wavelet Daubechies (1988, 1992). For a Daubechies (mother) wavelet of class is a function defined by

where are the constant (high pass) filter coefficients satisfying the conditions as well as, for

And is the scaling (father) wavelet function is supported on and satisfies the recursion equation as well as the normalization and Note that the filter coefficients can be efficiently computed as listed in Daubechies (1992). The order , on the one hand, decides the support of our wavelet; on the other hand, provides the regularity condition in the sense that

We will employ Daubechies wavelet with a sufficiently high order when forecasting in our simulations and data analysis. The basis functions can be either generated using the library PyWavelets in Python 111For visualization for the families of Daubechies wavelet functions, we refer to \urlhttp://wavelets.pybytes.com, where the library PyWavelets is also introduced there. or the wavefun in the Wavelet Toolbox of Matlab. In the present paper, to construct a sequence of orthogonal wavelet, we will follow the dyadic construction of Daubechies (1988). For a given and we will consider the following periodized wavelets on

| (4.10) |

or, equivalently Meyer (1990)

| (4.11) |

In light of (4.9), with the estimates we forecast using

Next, we shall discuss the estimation of the MSE of forecast, i.e., the variance of . Denote the series of estimated forecast error by Let the variance of be Similar to (Ding and Zhou, 2019, Lemma 3.11), we find that there exists a smooth function such that for some constant

| (4.12) |

Therefore, we shall use sieve expansion to estimate the smooth function Similar to (4.6), we have

Furthermore, by equation (3.14) of Ding and Zhou (2019), write

where is a centred sequence of locally stationary time series satisfying Assumptions 2.2, 2.3, 3.1, 3.2 and 3.3. Consequently, we can use an OLS with being the response and , being the explanatory variables to estimate which are denoted as Finally, we estimate

We are now ready to state the asymptotic behaviour of the estimated coefficients and MSE of (4.2). Denote Recall (4.7). Note that for the commonly used sieve basis functions, we have where for the Fourier basis and orthogonal wavelet, and for Legendre polynomial.

Theorem 4.5.

4.3 Sieve estimation of the PACF of locally stationary time series

In this section, we discuss the estimation of the PACF for locally stationary time series using the method of sieves. By a discussion similar to (4.6), we have that

| (4.14) |

Therefore, similar to (4.8), we can write

where is defined in (2.16), for and Let be the rectangular matrix whose -th row is where . We put all the into a vector The OLS estimator for can be written as where

Denote the sieve estimator of PACF as

We have the following results.

5 Test of stability for locally stationary time series prediction

As we mentioned in the introduction, it is of great practical importance to check whether the optimal forecasting coefficients are indeed time-varying. In this section, we propose a test of stability for the best linear prediction based on the estimated AR coefficients from Section 4.2.

As is related to the trend of the time series and in some real applications the trend is removed before performing forecasting, we shall first test the stability of , Furthermore, as we observe from Theorem 5.1 below, test of stability for , is asymptotically equivalent to testing correlation stationarity of which may be of separate interest. Formally, the null hypothesis we would like to test is

| (5.1) |

Before providing the test statistic for , we shall first investigate the interesting insight that is asymptotically equivalent to testing whether is correlation stationary, i.e., there exists some function such that

| (5.2) |

where stands for the correlation between and We formalize the above statements in Theorem 5.1.

Theorem 5.1.

In some cases, practitioners and researchers may be interested in testing whether all optimal forecast coefficient functions , do not change over time. That is equivalent to testing whether both the trend and the correlation structure of the time series stay constant over time. In this case, one will test

| (5.3) |

5.1 Test statistics and asymptotic normality

In this subsection, we propose test statistics for in (5.1) and in (5.3). Recall (4.9). We focus our discussion on and briefly discuss in the end. To test we use the following statistic

| (5.4) |

Next, we show that the study of the statistic reduces to the investigation of a weighted quadratic form of high dimensional non-stationary time series. Denote and Let be a dimensional diagonal block matrix with diagonal block and be a dimensional diagonal matrix whose non-zero entries are ones and in the lower major part. Recall Let We denote the sequence of -dimensional vectors by

| (5.5) |

Lemma 5.2.

From Lemma 5.2, we find that it suffices to establish the distribution of To this end, we shall establish a Gaussian approximation result for this quadratic form of high-dimensional non-stationary time series . Note that when is a locally stationary time series

| (5.8) |

Choose a sequence of centred Gaussian random vectors which preserves the covariance structure of and define Denote

We will control the Kolmogorov distance

| (5.9) |

Denote

It is notable that can be well controlled for commonly used basis functions. For instance, for the Fourier basis and the normalized orthogonal polynomials; for orthogonal wavelet. The following theorem provides a bound for

Theorem 5.3.

As indicated by Theorem 5.3, since is large, when and is large enough, we can allow where is a sufficiently small constant. Asymptotic normality of can be readily derived by the above Gaussian approximation. Denote the long-run covariance matrix for as

| (5.10) |

and the aggregated covariance matrix as can be regarded as the integrated long-run covariance matrix of For we define

| (5.11) |

We now discuss the power of the test under the following local alternative. For a given

where and as For instance, we can choose where is the quantile of the standard Gaussian distribution.

The above proposition states that under the power of our test will asymptotically be 1, i.e.,

5.2 Robust bootstrap procedure

It is difficult to directly use Proposition 5.4 to carry out the stability test since the quantities and are hard to estimate. Additionally, the high-dimensional Gaussian quadratic form converges at a slow rate. To overcome these difficulties, we extend the strategy of Zhou (2013b) and use a high-dimensional mulitplier bootstrap statistic to mimic the distributions of and . We focus on the discussion of Recall that

| (5.12) |

Recall (5.5). Denote

| (5.13) |

where are i.i.d. standard Gaussian random variables. Denote the bootstrap quadratic form

| (5.14) |

where with Since cannot be observed directly, we shall use the residuals

Accordingly, define and by replacing in and with , respectively.

We claim that mimics the distribution of asymptotically. Before formally introduce our results, we first introduce the following assumption, which states that diverges in a moderate way. Let .

Assumption 5.6.

Remark 5.7.

The above assumption is equivalent to

| (5.15) |

Therefore, when the above assumption can be read as

Hence, in the optimal case when Assumption 5.6 allows one to choose

Theorem 5.8.

For the detailed construction of we refer the reader to the proof of the above theorem. A theoretical discussion of the accuracy of the bootstrap can be found in Section S.1.

Finally, the following steps are proposed for practical implementation of the bootstrap:

-

1.

Select the tuning parameters , and by the methods demonstrated in Section 5.4.

-

2.

Compute using and the residuals

-

3.

Generate B (say 1000) i.i.d. copies of Compute correspondingly.

-

4.

Let be the order statistics of Reject at the level if where denotes the largest integer smaller or equal to Let The -value of the test can be computed as

5.3 Test of PACF for locally stationary time series

This subsection is devoted to testing whether a group of PACF are uniformly zero across time which is important when selecting a preliminary order of an AR model. We observe from Lemma 2.10 and Theorem 4.6 that the following statistic should be small under : , ,

where is a given sufficiently large lag. Consequently, can be used to test . However, in order to obtain the value of we need to do high-dimensional OLS regressions which is computationally intensive. The following lemma suggests that we can simply use

as our test statistic, where only one high-dimensional OLS regression is need in order to obtain its value.

Lemma 5.9.

For we have that

Similar to the discussion of Theorem 5.8, is normally distributed and so does . This is summarized as the following lemma. Denote where Similar to the discussion of (5.8), write

| (5.16) |

Denote the long-run covariance matrix as and the integrated long-run covariance matrix as For define

where and is a diagonal block matrix whose lower major part are identity matrices and zeros otherwise.

5.4 Choices of tuning parameters

In this subsection, we discuss how to choose the parameters in both the forecasting and testing procedures. We start with tuning parameter selection for forecasting. As we have seen from (4.2) and (4.6), we need to choose two important parameters in order to get an accurate prediction: and We use a data-driven procedure proposed in Bishop (2013) to choose such parameters.

For a given integer say we divide the time series into two parts: the training part and the validation part With some preliminary initial pair , we propose a sequence of candidate pairs in an appropriate neighbourhood of where are some given integers. For each pair of the choices we fit a time-varying AR() model (i.e., in (4.2)) with sieve basis expansion using the training data set. Then using the fitted model, we forecast the time series in the validation part of the time series. Let be the forecast of respectively using the parameter pair . Then we choose the pair with the minimum sample MSE of forecast, i.e.,

We will discuss how to choose some initial values of and in the testing procedure.

Next, we discuss how to choose the parameters and for the stability tests. In particular, the parameters and selected for the testing also serve as suitable preliminary initial values for the forecasting as we discussed above. Next, we will make use of the PACF to find a suitable where the sample PACF are uniformly insignificant after lag .

In light of Lemma 5.10, we can follow the bootstrapping procedure as discussed in the end of Section 5.2 by replacing with (c.f. (5.16)) in (5.13) to perform the test for . For a sufficiently large and a given nominal level denote

| (5.17) |

Then we can use for our test. Observe that the value of can be roughly determined by the PACF plot which is helpful in terms of reducing computational complexity. Also note that all PACF after lag are uniformly statistically insignificant and hence can be treated as 0.

Then we discuss the choice of using the criterion of cross-validation Hansen (2014). The key difference is that our observations are not i.i.d. samples, so we need to slightly modify the procedure. For a given large value such that

| (5.18) |

Denote as the estimation using the data points and basis functions. Denote cross-validation rule as

Therefore, we choose choose the estimate of using

| (5.19) |

Finally, we discuss how to choose for practical implementation. In Zhou (2013b), the author used the minimum volatility (MV) method to choose the window size for the scalar covariance function. The MV method does not depend on the specific form of the underlying time series dependence structure and hence is robust to misspecification of the latter structure Politis et al. (1999). The MV method utilizes the fact that the covariance structure of becomes stable when the block size is in an appropriate range, where is defined as

| (5.20) |

Therefore, it desires to minimize the standard errors of the latter covariance structure in a suitable range of candidate ’s.

In detail, for a give large value and a neighbourhood control parameter we can choose a sequence of window sizes and obtain by replacing with in (5.13), For each we calculate the matrix norm error of in the -neighborhood, i.e.,

where Therefore, we choose the estimate of using

Note that in Zhou (2013b) the author used and we also adopt this choice in the current paper.

6 Simulation studies

In this section, we perform extensive Monte Carlo simulations to study the finite-sample accuracy of the nonparametric sieve forecasting method and the finite sample accuracy and power of the stability test and compare them with those of some existing methods in the literature.

6.1 Simulation setup

We consider four different types of non-stationary time series models: two linear time series models, a two-regime model, a Markov switching model and a bilinear model.

-

1.

Linear AR model: Consider the following time-varying AR(2) model

where are i.i.d. random variables whose distributions will be specified when we finish introducing the models. It is elementary to see that when are constants, the prediction is stable.

-

2.

Linear MA model: Consider the following time-varying MA(2) model

- 3.

-

4.

Markov two-regime switching model: Consider the following Markov switching AR(1) model

where the unobserved state variable is a discrete Markov chain taking values and with transition probabilities It is easy to check that the above model is stable if the functions are constants and bounded by one Quandt (1972). In the simulations, the initial state is chosen to be 1.

-

5.

Simple bilinear model: Consider the first order bilinear model

It is known from Fan and Yao (2003) that when the functions are constants and bounded by one, has an ARMA representation and hence stable.

In the simulations below, we record our results based on 1,000 repetitions and for the bootstrapping procedure described in the end of Section 5.2, we choose For the choices of random variables we set to be student- distribution with degree of , i.e., (5) for models 1-2 and standard normal random variables for models 3-5.

6.2 Prediction of locally stationary time series

In this section, we study the prediction accuracy of our adaptive sieve forecast (4.2) by comparing it with some state-of-the-art methods. Specifically, we compare with the Tapered Yule-Walker estimate (TTVAR) in Roueff and Sanchez-Perez (2018), the non-decimated wavelet estimate (LSW) in Fryzlewicz et al. (2003), the model switching method (SNSTS) in Kley et al. (2016), the best linear prediction using the previous samples (SBLP) 222The prediction is based on the stationary assumption and an ARIMA model., the best linear prediction using recent samples (PBLP) and our adaptive sieve forecast (4.2). We implement TTVAR with constant taper function and the bandwidth is selected according to (Roueff and Sanchez-Perez, 2018, Corollary 4.2). For the wavelet method, we use the matlab codes from the first author’s website (see \urlhttp://stats.lse.ac.uk/fryzlewicz/flsw/flsw.html) and for the model switching method, we use the R package forecastSNSTS. For our sieve method, we use the orthogonal wavelets (4.11) with Daubechies-9 wavelet and the data-driven approach described in Section 5.4 to choose and

In Table 1, we record the mean square error over 1,000 simulations for one-step ahead prediction of the models 1-5 in Section 6.1. Specifically, we use

where for models 1-2 and for models 3-5. It can be seen that our sieve method outperforms the other methods in literature for five models in both sample sizes and . The forecasting accuracy improvement is more significant for non-AR type models such as the MA and bilinear models.

| Model | TTVAR | LSW | SNSTS | SBLP | PBLP | Sieve | Improvement |

|---|---|---|---|---|---|---|---|

| =256 | |||||||

| 1 | 0.24 | 0.21 | 0.45 | 0.284 | 0.24 | 0.189 | 10 |

| 2 | 0.28 | 0.27 | 0.28 | 0.273 | 0.283 | 0.22 | 18.5 |

| 3 | 0.21 | 0.185 | 0.198 | 0.241 | 0.194 | 0.178 | 3.8 |

| 4 | 0.207 | 0.195 | 0.2 | 0.247 | 0.199 | 0.187 | 4.1 |

| 5 | 0.22 | 0.22 | 0.24 | 0.246 | 0.273 | 0.176 | 20 |

| =512 | |||||||

| 1 | 0.21 | 0.2 | 0.2 | 0.233 | 0.209 | 0.181 | 9.5 |

| 2 | 0.26 | 0.26 | 0.264 | 0.276 | 0.283 | 0.196 | 24.62 |

| 3 | 0.207 | 0.183 | 0.192 | 0.213 | 0.194 | 0.18 | 1.7 |

| 4 | 0.205 | 0.175 | 0.188 | 0.211 | 0.181 | 0.17 | 2.86 |

| 5 | 0.23 | 0.21 | 0.24 | 0.23 | 0.22 | 0.183 | 12.86 |

6.3 Accuracy and power of the stability test

In this section, we study the performance of the proposed test (5.1). First, we study the finite sample accuracy of our test under correlation stationarity when

| (6.1) |

Observe that the simulated time series are not covariance stationary as the marginal variances change smoothly over time. We choose the values of and according to the methods described in Section 5.4. It can be seen from Table 2 that our bootstrap testing procedure behaves reasonably accurate for all three types of sieve basis functions even for a smaller sample size

Second, we study the power of the tests and report the results in Table 3 when the underlying time series is not correlation stationary. Specifically, we use

| (6.2) |

for the models 1-5 in Section 6.1. It can be seen that the simulated powers are reasonably good even for smaller and the sample size, and the results will be improved when and the sample size increase. Additionally, the power performances of the three types of sieve basis functions are similar in general.

| Basis/Model | 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|---|---|---|---|---|

| =256 | ||||||||||

| Fourier | 0.132 | 0.11 | 0.12 | 0.13 | 0.11 | 0.067 | 0.07 | 0.06 | 0.04 | 0.06 |

| Legendre | 0.091 | 0.136 | 0.13 | 0.12 | 0.13 | 0.06 | 0.059 | 0.041 | 0.07 | 0.07 |

| Daubechies-9 | 0.132 | 0.12 | 0.11 | 0.133 | 0.132 | 0.063 | 0.067 | 0.059 | 0.068 | 0.065 |

| =512 | ||||||||||

| Fourier | 0.09 | 0.13 | 0.11 | 0.13 | 0.127 | 0.05 | 0.06 | 0.067 | 0.068 | 0.069 |

| Legendre | 0.09 | 0.094 | 0.092 | 0.12 | 0.118 | 0.04 | 0.058 | 0.07 | 0.043 | 0.057 |

| Daubechies-9 | 0.091 | 0.11 | 0.098 | 0.11 | 0.118 | 0.048 | 0.052 | 0.054 | 0.053 | 0.054 |

| Basis/Model | 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|---|---|---|---|---|

| =256 | ||||||||||

| Fourier | 0.84 | 0.86 | 0.84 | 0.837 | 0.94 | 0.97 | 0.97 | 0.96 | 0.99 | 0.98 |

| Legendre | 0.8 | 0.806 | 0.81 | 0.84 | 0.83 | 0.97 | 0.968 | 0.95 | 0.97 | 0.91 |

| Daubechies-9 | 0.81 | 0.81 | 0.86 | 0.81 | 0.81 | 0.97 | 0.96 | 0.983 | 0.98 | 0.98 |

| =512 | ||||||||||

| Fourier | 0.91 | 0.9 | 0.96 | 0.9 | 0.93 | 0.96 | 0.97 | 0.973 | 0.98 | 0.97 |

| Legendre | 0.9 | 0.91 | 0.92 | 0.893 | 0.91 | 0.94 | 0.95 | 0.98 | 0.97 | 0.96 |

| Daubechies-9 | 0.87 | 0.88 | 0.93 | 0.91 | 0.91 | 0.96 | 0.99 | 0.97 | 0.97 | 0.96 |

6.4 Comparison with tests for covariance stationarity

In this subsection, we compare our method with some existing works on the tests of covariance stationarity: the distance method in Dette et al. (2011), the discrete Fourier transform method in Dwivedi and Rao (2011) and the Haar wavelet periodogram method in Nason (2013). The first method is easy to implement; for the second method, we use the codes from the author’s website (see \urlhttps://www.stat.tamu.edu/ suhasini/test_papers/DFT_covariance_lagl.R); and for the third method, we employ the R package locits, which is contributed by the author. For the purpose of comparison of accuracy, besides the five models considered in Section 6.1, we also consider the following two strictly stationary time series.

-

6.

Linear time series: stationary ARMA(1,1) process. We consider the following process

where are i.i.d. random variables.

-

7.

Nonlinear time series: stationary SETAR. We consider the following model

where are i.i.d. random variables.

Furthermore, for the comparison of power, we consider the following two non-stationary time series whose errors have constant variances.

-

.

Non-stationary linear time series. We consider the following process

where are i.i.d. standard normal random variables.

-

.

Non-stationary nonlinear time series. We consider the following process

where are i.i.d. standard normal random variables.

In the simulations below, we report the type I error rates under the nominal levels and for the above seven models in Table 4, where for models 1-5 we use the setup (6.1). Our simulation results are based on 1,000 repetitions, where refers to the distance method, DFT 1-3 refer to the discrete Fourier method using the imagery part, real part, both imagery and real parts of the discrete Fourier transform method, HWT is the Haar wavelet periodogram method and RB is our robust bootstrap method using orthogonal wavelets constructed by (4.11) with Daubechies-9 wavelet.

Since HWT needs the length to be a power of two, we set the length of time series to be 256 and 512. For the test, we use for and for For the DFT, we choose the lag to be as suggested by the authors in Dwivedi and Rao (2011). Since the mean of model 5 is non-zero, we test its first order difference for the methods mentioned above. Moreover, we report the power of the above tests under certain alternatives in Table 5 for models and models 1-5 under the setup (6.2).

| Model | DFT1 | DFT2 | DFT3 | HWT | RB | DFT1 | DFT2 | DFT3 | HWT | RB | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| =256 | ||||||||||||

| 1 | 0.08 | 0.148 | 0.057 | 0.13 | 0.18 | 0.132 | 0.024 | 0.067 | 0.017 | 0.063 | 0.083 | 0.063 |

| 2 | 0.081 | 0.097 | 0.068 | 0.12 | 0.085 | 0.12 | 0.038 | 0.04 | 0.07 | 0.057 | 0.028 | 0.067 |

| 3 | 0.171 | 0.183 | 0.04 | 0.137 | 0.227 | 0.11 | 0.087 | 0.103 | 0.011 | 0.033 | 0.093 | 0.059 |

| 4 | 0.2 | 0.163 | 0.05 | 0.12 | 0.176 | 0.133 | 0.077 | 0.087 | 0.013 | 0.034 | 0.113 | 0.068 |

| 5 | 0.46 | 0.293 | 0.077 | 0.19 | 0.153 | 0.132 | 0.29 | 0.21 | 0.03 | 0.14 | 0.12 | 0.065 |

| 6 | 0.11 | 0.105 | 0.096 | 0.09 | 0.087 | 0.088 | 0.047 | 0.053 | 0.053 | 0.039 | 0.052 | 0.057 |

| 7 | 0.051 | 0.097 | 0.08 | 0.092 | 0.085 | 0.127 | 0.018 | 0.04 | 0.06 | 0.047 | 0.038 | 0.061 |

| =512 | ||||||||||||

| 1 | 0.087 | 0.127 | 0.03 | 0.13 | 0.237 | 0.091 | 0.023 | 0.1 | 0.02 | 0.043 | 0.137 | 0.048 |

| 2 | 0.051 | 0.096 | 0.085 | 0.093 | 0.075 | 0.11 | 0.026 | 0.036 | 0.067 | 0.044 | 0.033 | 0.052 |

| 3 | 0.26 | 0.16 | 0.04 | 0.117 | 0.243 | 0.098 | 0.127 | 0.1 | 0.007 | 0.037 | 0.14 | 0.054 |

| 4 | 0.287 | 0.167 | 0.027 | 0.09 | 0.247 | 0.11 | 0.177 | 0.103 | 0.013 | 0.073 | 0.163 | 0.053 |

| 5 | 0.64 | 0.303 | 0.087 | 0.283 | 0.35 | 0.118 | 0.413 | 0.26 | 0.063 | 0.167 | 0.23 | 0.054 |

| 6 | 0.11 | 0.093 | 0.084 | 0.088 | 0.088 | 0.092 | 0.035 | 0.046 | 0.047 | 0.048 | 0.053 | 0.048 |

| 7 | 0.051 | 0.087 | 0.113 | 0.083 | 0.093 | 0.092 | 0.013 | 0.037 | 0.047 | 0.043 | 0.04 | 0.051 |

We first discuss the results for models 6-7 since they are not only correlation stationary but also covariance stationary. It can be seen from Table 4 that all the methods including our RB achieve a reasonable level of accuracy for the linear model 6. However, for the nonlinear model 7, we conclude from Table 4 that the method loses its accuracy due to the fact that the latter test is designed only for linear models. Regarding the power in Table 5, for model , when the sample size and are smaller, only our RB method is powerful. When and increases, the test starts to become powerful. Further, when both the sample size and increase, the HWT method becomes powerful. Similar discussion holds for model Therefore, we conclude that, when the marginal variance of the time series stays constant, even though other methods in the literature may be accurate for the purpose of testing for correlation stationarity, our RB method is generally more powerful when the sample size is moderate and/or the departure from stationary is small.

| Model | DFT1 | DFT2 | DFT3 | HWT | RB | DFT1 | DFT2 | DFT3 | HWT | RB | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| n=256 | ||||||||||||

| 1 | 0.263 | 0.14 | 0.03 | 0.07 | 0.3 | 0.81 | 0.503 | 0.113 | 0.053 | 0.089 | 0.4 | 0.97 |

| 2 | 0.183 | 0.497 | 0.08 | 0.092 | 0.585 | 0.81 | 0.68 | 0.14 | 0.06 | 0.047 | 0.38 | 0.96 |

| 3 | 0.44 | 0.153 | 0.04 | 0.16 | 0.393 | 0.86 | 0.7 | 0.14 | 0.05 | 0.09 | 0.64 | 0.983 |

| 4 | 0.603 | 0.16 | 0.04 | 0.203 | 0.44 | 0.81 | 0.86 | 0.2 | 0.07 | 0.12 | 0.647 | 0.98 |

| 5 | 0.92 | 0.243 | 0.143 | 0.24 | 0.57 | 0.81 | 0.997 | 0.347 | 0.193 | 0.397 | 0.797 | 0.98 |

| 0.697 | 0.12 | 0.093 | 0.11 | 0.327 | 0.86 | 0.923 | 0.16 | 0.15 | 0.15 | 0.563 | 0.94 | |

| 0.463 | 0.137 | 0.107 | 0.133 | 0.273 | 0.85 | 0.81 | 0.193 | 0.203 | 0.223 | 0.483 | 0.96 | |

| n=512 | ||||||||||||

| 1 | 0.477 | 0.173 | 0.04 | 0.08 | 0.52 | 0.87 | 0.857 | 0.137 | 0.03 | 0.1 | 0.75 | 0.96 |

| 2 | 0.51 | 0.297 | 0.082 | 0.092 | 0.385 | 0.88 | 0.918 | 0.24 | 0.06 | 0.047 | 0.838 | 0.99 |

| 3 | 0.657 | 0.24 | 0.05 | 0.083 | 0.61 | 0.93 | 0.96 | 0.17 | 0.24 | 0.113 | 0.95 | 0.97 |

| 4 | 0.84 | 0.23 | 0.043 | 0.143 | 0.773 | 0.91 | 0.987 | 0.293 | 0.053 | 0.19 | 0.97 | 0.97 |

| 5 | 0.963 | 0.297 | 0.127 | 0.263 | 0.87 | 0.91 | 0.983 | 0.523 | 0.24 | 0.478 | 0.994 | 0.96 |

| 0.847 | 0.147 | 0.087 | 0.103 | 0.67 | 0.88 | 0.95 | 0.13 | 0.09 | 0.133 | 0.963 | 0.95 | |

| 0.69 | 0.14 | 0.13 | 0.217 | 0.383 | 0.91 | 0.953 | 0.3 | 0.313 | 0.383 | 0.823 | 0.943 | |

Next, we study models 1-5 from Section 6.1. None of these models is covariance stationary. For the type I error rates, we use the setting (6.1) where all the models are correlation stationary. For the power, we use the setup (6.2). We find that DFT-3 is accurate for models 1-4 but with low power across all the models. Moreover, the test seems to have a high power for models 3-5. But this is at the cost of blown-up type I error rates. This inaccuracy increases when the sample size becomes larger. For the HWT method, even though its power becomes larger when the sample size and increase, it also loses its accuracy. Finally, for all the models 1-5, our RB method both obtain high accuracy and power. In summary, most of the existing tests for covariance stationarity are not suitable for the purpose of testing for correlation stationarity. From our simulation studies, our robust bootstrap method performs well for the latter purpose.

7 Empirical illustrations

7.1 Global temperature data

In this first application, we study the global temperature time series using the dataset Global component of Climate at a Glance (GCAG). As explained on the website of National Oceanic and Atmospheric Administration (NOAA) 333\urlhttps://www.ncdc.noaa.gov/cag/global/data-info, GCAG comes from the Global Historical Climatology Network-Monthly (GHCN-M) Data Set and International Comprehensive Ocean-Atmosphere Data Set (ICOADS), which have data from 1880 to the present. These two datasets are blended into a single product to produce the combined global land and ocean temperature anomalies. The term temperature anomaly means a departure from a reference value or long-term average.

The available time series of global-scale temperature anomalies are calculated with respect to the 20th century average Smith et al. (2008), while the mapping tool displays global-scale temperature anomalies with respect to the 1981-2016 based period. ( see \urlhttps://datahub.io/core/global-temp#readme for the dataset). This dataset is a global-scale climate diagnostic tool and provides a big picture overview of average global temperatures compared to a reference value.

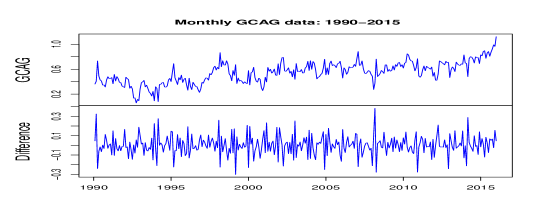

We study the monthly time series from this dataset for the time period 1990-2015 (Figure 2). As indicated from the above figure, the global temperature has an increasing trend and we consider its first order difference.

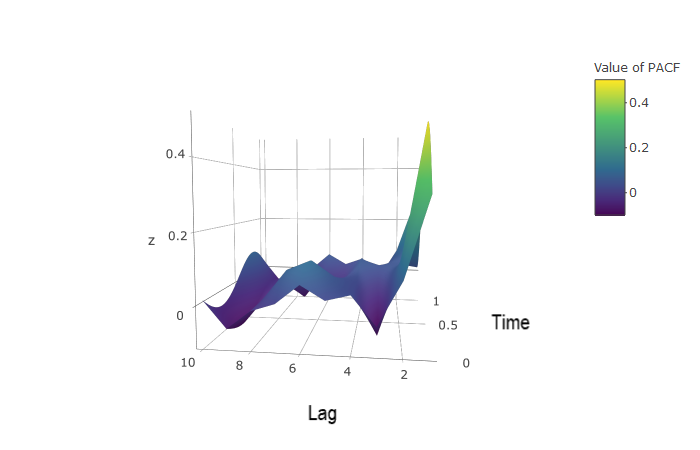

Then we apply the methodologies described in Sections 4 and 5 to study the time series. We first employ the methods from Section 5 to test whether this time series is correlation stationary. There are three parameters, and needed to be properly chosen. Especially, we make use of the PACF defined in Definition 2.9 to choose (c.f. Section 5.3). In Figure 3, we make a 3-D plot of the PACF for the time series (first order difference) between 1990 and 2015. It can be seen that the temporal dependence of this time series decays uniformly in time. For the sieve basis functions, we use the orthogonal wavelets constructed by (4.11) with Daubechies-9 wavelet. The tuning parameters and are chosen according to Section 5.4 which yields , (i.e. ) and . We apply the bootstrap procedure described in the end of Section 5.2 to test the stationarity of the correlation and find that the -value is . We hence conclude that the prediction is unstable during this time period.

Next, we use time series 1990-2015 as the training dataset to study the prediction performance over the year 2016, i.e., we do a one-step ahead prediction for each month of 2016 and take the average of the square error. We use the data-driven approach as described in Section 5.4 to choose and The MSE of our prediction is We compare this result with the methods mentioned in Section 6.2 and record the results in Table 6. We find that our prediction performs better than the other methods. Especially, we get a improvement compared to simply fitting a stationary model using all the time series from 1990 to 2015 (SBLP).

| Method | Sieve | TTVAR | LSW | SNSTS | SBLP |

| MSE | 0.381 | 0.3913 | 0.3851 | 0.3969 | 0.45706 |

7.2 Stock return data of Nigerian Breweries

In the second application, we study the stock return data of the Nigerian Breweries (NB) Plc. This stock is traded in Nigerian Stock Exchange (NSE). Regarding on market returns, the brewery industry in Nigerian has done pretty well in outperforming Brazil, Russia, India, and China (BRIC) and emerging markets by a wide margin over the past ten years. Nigerian Breweries Plc is the largest brewing company in Nigeria, which mainly serves the Nigerian market and also exports to other parts of West Africa. The data can be found on the website of morningstar (see \urlhttp://performance.morningstar.com/stock/performance-return.action?p=price_history_page&t=NIBRregion=ngaculture=en-US). We are interested in predicting the volatility of the NB stock. We shall study the absolute value of the daily log-return of the stock for the latter purpose.

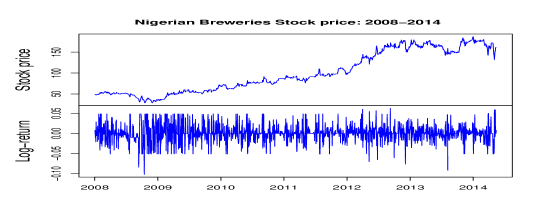

We perform our analysis on the time period 2008-2014 (Figure 4). This time series contains the data of the 2008 global financial crisis and its post period. As said in the report from the Heritage Foundation Sherk (2014), ”the economy is experiencing the slowest recovery in 70 years” and even till 2014, the economy does not fully recover.

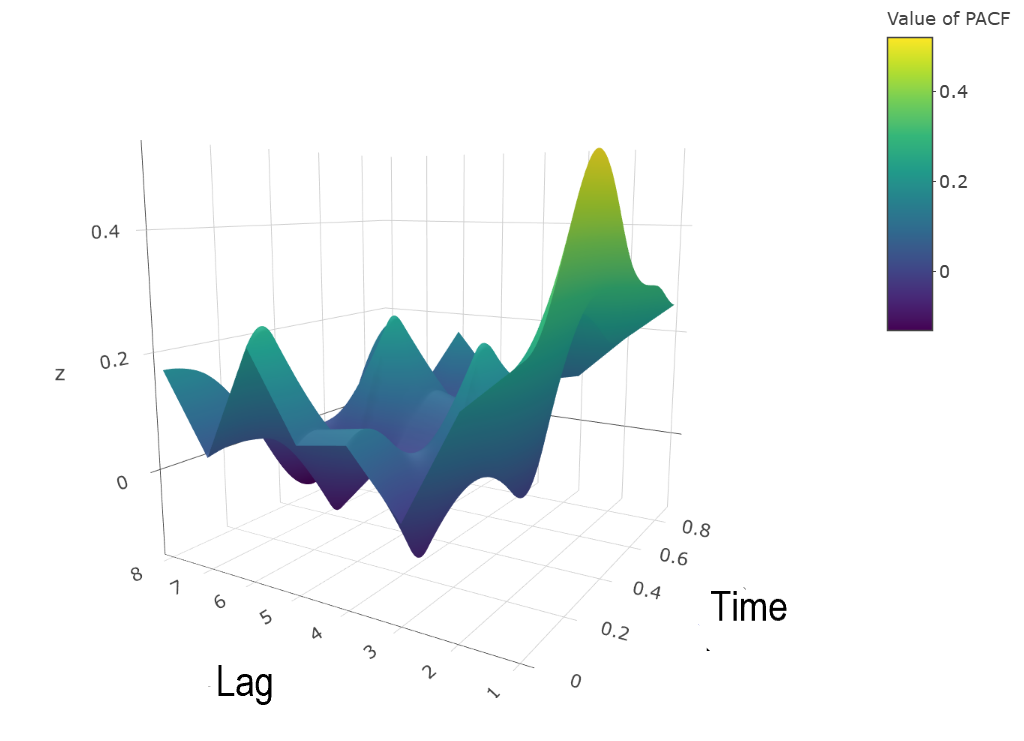

Then we apply the methodologies described in Sections 4 and 5 for the absolute values of log-return time series. It is clear that we need to fit a mean curve for this model. In Figure 5, we make a 3-D plot of the PACF for the time series between 2008 and 2014. It can be seen that the temporal dependence of this time series decays uniformly in time. Then we test the stability of the best linear prediction as described in Section 5. For the sieve basis functions, we use the orthogonal wavelets constructed by (4.11) with Daubechies-9 wavelet. We choose the parameters and based on the discussion of Section 5.4 which yields (i.e., ) and . We apply the bootstrap procedure described in the end of Section 5.2 and find that the -value is . We hence conclude that the prediction is likely to be unstable during this time period.

Next, we use the time series 2008-2014 as the training dataset to study the prediction performance over the first month of 2015. We employ the data-driven approach from Section 5.4 to choose and The MSE is We compare this result with the methods mentioned in Section 6.2 and record the results in Table 7. We find that our prediction performs better than the other methods. Especially, we get a improvement compared to simply fitting a stationary model using all the time series from 2008 to 2014.

| Method | Sieve | TTVAR | LSW | SNSTS | SBLP |

| MSE | 0.194 | 0.198 | 0.198 | 0.202 | 0.257 |

Finally, we further study the absolute value of the stock return from 2012 to 2014. We apply our bootstrap procedure described in the end of Section 5.2 to test correlation stationarity of the time series. We select (i.e., ) and for this sub-series and find that the -value is . We hence conclude that the prediction is stable during this time period. Therefore, we fit a best stationary ARMA model to this sub-series and do the prediction. This yields an MSE of 0.195. We find that our sieve method is still slightly better. The result from this sub-series shows an interesting trade-off between forecasting using a shorter and stationary time series and a longer but non-stationary series. The forecast model of the shorter stationary period can be estimated at a faster rate but at the expense of a smaller sample size. The opposite happens to the longer non-stationary period. Note that 2012-2014 is nearly half as long as 2008-2014 and hence the length of the shorter stationary period is substantial compared to that of the long period. In this case we see that the forecasting accuracy using the short period is comparable to that of the longer period. In many applications where the data generating mechanism is constantly changing, the stable period is typically very short and a nonparametric model for the longer period is preferred. Finally, we emphasize that the correlation stationarity test is an important tool to decide a period of prediction stability.

References

- Baxter (1962) G. Baxter. An asymptotic result for the finite predictor. Mathematica Scandinavica, 10:137–144, 1962.

- Baxter (1963) G. Baxter. A norm inequality for a “finite-section” wiener-hopf equation. Illinois J. Math., 7(1):97–103, 1963.

- Bell (2004) W. W. Bell. Special Functions for Scientists and Engineers (Dover Books on Mathematics). Dover Publications, 2004.

- Bishop (2013) C. Bishop. Pattern Recognition and Machine Learning. Information science and statistics. Springer, 2013.

- Brockwell and Davis (1987) P. Brockwell and R. Davis. Time series: Theory and Methods. Springer-Verlag, 1987.

- Brockwell and Davis (2002) P. Brockwell and R. Davis. Introduction to Time Series and Forecasting. Springer Texts in Statistics. Springer–Verlag, 2nd edition, 2002.

- Cai et al. (2016) T. T. Cai, W. Liu, and H. H. Zhou. Estimating sparse precision matrix: Optimal rates of convergence and adaptive estimation. Ann. Statist., 44:455–488, 2016.

- Chandrasekaran and Ipsen (1995) S. Chandrasekaran and I. C. F. Ipsen. On the sensitivity of solution components in linear systems of equations. SIAM Journal on Matrix Analysis and Applications, 16(1):93–112, 1995.

- Chen and Fang (2011) L. Chen and X. Fang. Multivariate normal approximation by stein’s method: The concentration inequality approach. arXiv preprint arXiv:1111.4073, 2011.

- Chen (2007) X. Chen. Large Sample Sieve Estimation of Semi-nonparametric Models. Chapter 76 in Handbook of Econometrics, Vol. 6B, James J. Heckman and Edward E. Leamer, 2007.

- Chen and Christensen (2015) X. Chen and T. M. Christensen. Optimal uniform convergence rates and asymptotic normality for series estimators under weak dependence and weak conditions. Journal of Econometrics, 188(2):447 – 465, 2015.

- Chen et al. (2013) X. Chen, M. Xu, and W. B. Wu. Covariance and precision matrix estimation for high-dimensional time series. Ann. Statist., 41(6):2994–3021, 2013.

- Cheng and Pourahmadi (1993) R. Cheng and M. Pourahmadi. Baxter’s inequality and convergence of finite predictors of multivariate stochastic processess. Probability Theory and Related Fields, 95(1):115–124, 1993.

- Das and Politis (2017) S. Das and D. Politis. Predictive inference for locally stationary time series with an application to climate data. arXiv preprint arXiv:1712.02383, 2017.

- Daubechies (1988) I. Daubechies. Orthonormal bases of compactly supported wavelets. Commun. Pure Appl. Math., 41:909–996, 1988.

- Daubechies (1992) I. Daubechies. Ten Lectures on Wavelets. SIAM series: CBMS-NSF Regional Conference Series in Applied Mathematics, 1992.

- Demko et al. (1984) S. Demko, W. Moss, and P. Smith. Decay rates for inverses of band matrices. Math. Comput., 43:491–499, 1984.

- Dette et al. (2011) H. Dette, P. Preubb, and M. Vetter. A measure of stationarity in locally stationary processes with applications to testing. J. Am. Stat. Assoc., 106:1113–1124, 2011.

- Dette et al. (2019) H. Dette, W. Wu, and Z. Zhou. Change point analysis of correlation in non-stationary time series. Statist. Sinica, 29(2):611–643, 2019.

- Ding and Zhou (2019) X. Ding and Z. Zhou. Estimation and inference for precision matrices of non-stationary time series. Ann. Statist. (to appear), 2019.

- Dwivedi and Rao (2011) Y. Dwivedi and S. S. Rao. A test for second–order stationarity of a time series based on the discrete Fourier transform. Journal of Time Series Analysis, 32:68–91, 2011.

- Fan and Yao (2003) J. Fan and Q. Yao. Nonlinear Time Series: Nonparametric and Parametric Methods. Springer, 2003.

- Fang (2016) X. Fang. A multivariate CLT for bounded decomposable random vectors with the best known rate. Journal of Theoretical Probability, 29(4):1510–1523, 2016.

- Fryzlewicz et al. (2003) P. Fryzlewicz, S. Van Bellegem, and R. von Sachs. Forecasting non-stationary time series by wavelet process modelling. Annals of the Institute of Statistical Mathematics, 55(4):737–764, 2003.

- Grenander and Szegö (2001) U. Grenander and G. Szegö. Toeplitz Forms and Their Applications. AMS Chelsea Publishing Series. University of California Press, 2001.

- Hansen (2014) B. Hansen. Nonparametric Sieve Regression: Least Squares, Averaging Least Sqaures, and Cross-Validation. Chapter 8: The Oxford Handbook of Applied Nonparametric and Semiparametric Econometrics and Statistics, 2014.

- Inoue et al. (2018) A. Inoue, Y. Kasahara, and M. Pourahmadi. Baxter’s inequality for finite predictor coefficients of multivariate long-memory stationary processes. Bernoulli, 24(2):1202–1232, 2018.

- Kac (1954) M. Kac. Toeplitz matrices, translation kernels and a related problem in probability theory. Duke Math. J., 21(3):501–509, 1954.

- Kley et al. (2016) T. Kley, P. Preuß, and P. Fryzlewicz. Predictive, finite-sample model choice for time series under stationarity and non-stationarity. arXiv preprint arXiv 1611.04460, 2016.

- Kreiss (1988) J.-P. Kreiss. Asymptotical inference for a class of stochastic processes. Habilitationsschrift, Universität Hamburg, 1988.

- Kreiss et al. (2011) J.-P. Kreiss, E. Paparoditis, and D. N. Politis. On the range of validity of the autoregressive sieve bootstrap. Ann. Statist., 39(4):2103–2130, 2011.

- Liu and Lin (2009) W. Liu and Z. Lin. Strong approximation for a class of stationary processes. Stochastic Process. Appl., 119:249–280, 2009.

- Meyer et al. (2015) M. Meyer, T. McMurry, and D. Politis. Baxter’s inequality for triangular arrays. Mathematical Methods of Statistics, 24(2):135–146, 2015.

- Meyer (1990) Y. Meyer. Ondelettes et opérateurs. I. Actualités Mathématiques. Hermann, Paris, 1990. Ondelettes.

- Nason (2013) G. Nason. A test for second–order stationarity and approximate confidence intervals for localized autocovariances for locally stationary time series. J.R. Statist. Soc. B, 75:879–904, 2013.

- Paparoditis (2010) E. Paparoditis. Validating stationarity assumptions in time series analysis by rolling local periodograms. Journal of the American Statistical Association, 105(490):839–851, 2010.

- Politis et al. (1999) D. Politis, D. Wolf, J. Romano, M. Wolf, P. Bickel, P. Diggle, and S. Fienberg. Subsampling. Springer Series in Statistics. Springer New York, 1999.

- Pourahmadi (2001) M. Pourahmadi. Foundations of Time Series Analysis and Prediction Theory. Wiley Series in Probability and Statistics. Wiley, 2001.

- Quandt (1972) R. Quandt. A new approach to estimating switching regressions. J. Am. Stat. Assoc., 67:306–310, 1972.

- Rosenblatt (1952) M. Rosenblatt. Remarks on a multivariate transformation. Ann. Math. Statist., 23(3):470–472, 1952.

- Roueff and Sanchez-Perez (2018) F. Roueff and A. Sanchez-Perez. Prediction of weakly locally stationary processes by auto-regression. Lat. Am. J. Probab. Math. Stat., 15:1215–1239, 2018.

- Sherk (2014) J. Sherk. Not Looking for Work: Why Labor Force Participation Has Fallen During the Recovery. \urlhttps://www.heritage.org/jobs-and-labor/report/not-looking-work-why-labor-force-participation-has-fallen-during-the-recovery, 2014.

- Smith et al. (2008) T. Smith, R. Reynolds, T. Peterson, and J. Lawrimore. Improvements to NOAA’s Historical Merged Land-Ocean Surface Temperature Analysis (1880–2006). J. Clim., 21:249–280, 2008.

- Stone (1982) C. J. Stone. Optimal global rates of convergence for nonparametric regression. Ann. Statist., 10(4):1040–1053, 1982.

- Tasaki (2009) H. Tasaki. Convergence rates of approximate sums of Riemann integrals. J. Approx. Theory, 161:477–490, 2009.

- Toeplitz (1911) O. Toeplitz. Zur Theorie der quadratischen und bilinearen Formen von unendlichvielen Veränderlichen. Math. Ann., 70(3):351–376, 1911.

- Tong (2011) H. Tong. Threshold models in time series analysis - 30 years on. Stat. Interface, 4:107–118, 2011.

- Wiener and Masani (1958) N. Wiener and P. Masani. The prediction theory of multivariate stochastic processes, II. Acta Mathematica, 99(1):93–137, 1958.

- Wu (2005) W. Wu. Nonlinear system theory: Another look at dependence. Proc Natl Acad Sci U S A., 40:14150–14151, 2005.

- Xiao and Wu (2012) H. Xiao and W. B. Wu. Covariance matrix estimation for stationary time series. Ann. Statist., 40(1):466–493, 2012.

- Xu et al. (2014) M. Xu, D. Zhang, and W. Wu. Asymptotics for High-Dimensional Data. arXiv preprint arXiv 1405.7244, 2014.

- Yuan (2010) M. Yuan. High dimensional inverse covariance matrix estimation via linear programming. J. Mach. Learn. Res., 11:2261–2286, 2010.

- Zhou (2013a) Z. Zhou. Inference for non-stationary time series auto regression. Journal of Time Series Analysis, 34:508–516, 2013a.

- Zhou (2013b) Z. Zhou. Heteroscedasticity and autocorrelation robust structural change detection. J. Am. Stat. Assoc., 108:726–740, 2013b.

- Zhou (2014) Z. Zhou. Inference of weighted V-statistics for nonstationary time series and its applications. Ann. Stat., 1:87–114, 2014.

- Zhou and Wu (2009) Z. Zhou and W. Wu. Local linear quantile estimation for non-stationary time series. Ann. Stat., 37:2696–2729, 2009.

- Zhou and Wu (2010) Z. Zhou and W. Wu. Simultaneous inference of linear models with time varying coefficents. J.R. Statist. Soc. B, 72:513–531, 2010.

Supplementary material for

Globally optimal and adaptive short-term forecasting of locally stationary time series and a test for its stability

This supplementary material contains further explanation, auxiliary lemmas and technical proofs for the main results of the paper.

Appendix S.1 A few further remarks

First, we will need the following further assumption in the paper.

Assumption S.1.1.

We assume that the following assumptions hold true for the sieve basis functions and parameters:

(1). For any denote whose -th entry is we assume that the eigenvalues of

are bounded above and also away from zero by a universal constant .

(2). There exist constants for some constant we have

(3). We assume that for defined in Assumption 2.2, defined in Assumption 3.3 and defined in (4.7), there exists a large constant such that

We mention that the above assumptions are mild and easy to check. First, (1) of Assumption S.1.1 guarantees the invertibility of the design matrix and the existence of the OLS solution. It can be easily verified that for the linear non-stationary process (3.7), (1) will be satisfied if (See (Ding and Zhou, 2019, Lemma 3.4) for detailed discussion.) Second, (2) is a mild regularity condition on the sieve basis functions and satisfied by the commonly used basis functions. We refer the readers to (Chen and Christensen, 2015, Assumption 4) for further details. (3) can be easily satisfied by choosing and accordingly. When the physical dependence is of exponential decay, we only need We refer the readers to (Ding and Zhou, 2019, Assumption 3.5) for more details.

Second, the accuracy of the robust bootstrap in Section 5.2 is determined by the closeness of its conditional covariance structure to that of . Following (Zhou, 2013b, Section 4.1.1), we shall use

| (S.1) |

where is defined in (5.20), to quantify the latter closeness. The following theorem establishes the bound for . Its proof will be given in Section S.3.

Theorem S.1.2 (Optimal choice of ).

Note that compared to (Zhou, 2013b, Theorem 4), the difference from Theorem S.1.2 is that we get an extra factor due to the high dimensionality. For instance, when we use the Fourier basis, normalized Chebyshev orthogonal polynomials and orthogonal wavelet, we shall have that which is the dimension of defined in (5.5). However, it will not influence the optimal choice of .

Appendix S.2 Some auxiliary lemmas

In this section, we collect some preliminary lemmas which will be used for our technical proofs. First of all, we collect a result which provides a deterministic bound for the spectrum of a square matrix. Let be a complex matrix. For let be the sum of the absolute values of the non-diagonal entries in the -th row. Let be a closed disc centered at with radius . Such a disc is called a Gershgorin disc.

Lemma S.2.1 (Gershgorin circle theorem).

Every eigenvalue of lies within at least one of the Gershgorin discs , where .

The next lemma provides a lower bound for the eigenvalues of a Toeplitz matrix in terms of its associated spectral density function. Since the autocovariance matrix of any stationary time series is a Toeplitz matrix, we can use the following lemma to bound the smallest eigenvalue of the autocovariance matrix. It will be used in the proof of Proposition 3.4 and can be found in (Xiao and Wu, 2012, Lemma 1).

Lemma S.2.2.

Let be a continuous function on Denote by and its minimum and maximum, respectively. Define and the matrix Then

The following lemma indicates that, under suitable condition, the inverse of a banded matrix can also be approximated by another banded-like matrix. It will be used in the proof of Theorem 2.5 and can be found in (Demko et al., 1984, Proposition 2.2). We say that is -banded if

Lemma S.2.3.

Let be a positive definite, -banded, bounded and bounded invertible matrix. Let be the smallest interval containing the spectrum of Set and set and Then we have

where

The following lemma provides an upper bound for the error of solutions of perturbed linear system. It can be found in the standard numerical analysis literature, for instance see Chandrasekaran and Ipsen (1995). It will be used in the proof of Theorem 2.5 and Lemma 5.9.

Lemma S.2.4.

Consider a matrix and vectors satisfying the linear system

Recall that the conditional number of is defined as

If we add perturbations on both and such that

Assuming that the linear system is well-conditioned, i.e., the conditional number satisfies that, for some constant

then we have that

The following lemma provides Gaussian approximation result on convex sets for the sum of an -dependent sequence, which is (Fang, 2016, Theorem 2.1). It will be used in the proof of Theorem 5.3.

Lemma S.2.5.

Let be a sum of -dimensional random vectors such that and Suppose can be decomposed as follows:

-

1.

such that is independent of , where

-

2.

such that is independent of

-

3.

such that is independent of

Suppose further that for each

where is the Euclidean norm of a vector. Then there exists a universal constant such that

where is a -dimensional Gaussian random vector preserving the covariance structure of and is the Kolmogorov distance defined in (5.9).

The following lemma offers a control for the summation of Chi-square random variables, which will be employed in the proof of Theorem 5.3. It can be found in (Xu et al., 2014, Lemma 7.2).

Lemma S.2.6.

Let such that let be i.i.d. random variables. Then for all we have