Focused Bayesian Prediction††thanks: We would like to thank a co-editor and two anonymous referees for very constructive comments on an earlier draft of the paper. We would also like to thank various participants at the following workshops and conferences for very helpful comments on earlier versions of the paper: the Casa Matemática Oaxaca Workshop on ‘Computational Statistics and Molecular Simulation: A Practical Cross-Fertilization’, Oaxaca, November, 2018; the Australian Centre for Excellence in Mathematics and Statistics Workshop on ‘Advances and Challenges in Monte Carlo Methods’, Brisbane, November, 2018; the International Symposium of Forecasting, Thessaloniki, June, 2019; the 13th RCEA Bayesian Econometrics Workshop, Cyprus, June 2019; the 12th International Conference on ‘Monte Carlo Methods and Applications’, Sydney, July, 2019; the Joint Statistical Meetings, Colorado, July, 2019; the ‘Frontiers in Research for Statistics’ Conference, Brisbane, October, 2019; and the ‘Statistical Methods in Data Science Workshop’, Mathematical Research Institute, Creswick, December, 2019. This research has been supported by Australian Research Council (ARC) Discovery Grants DP170100729 and DP200101414. Frazier was also supported by ARC Early Career Researcher Award DE200101070.

Abstract

We propose a new method for conducting Bayesian prediction that delivers accurate predictions without correctly specifying the unknown true data generating process. A prior is defined over a class of plausible predictive models. After observing data, we update the prior to a posterior over these models, via a criterion that captures a user-specified measure of predictive accuracy. Under regularity, this update yields posterior concentration onto the element of the predictive class that maximizes the expectation of the accuracy measure. In a series of simulation experiments and empirical examples we find notable gains in predictive accuracy relative to conventional likelihood-based prediction.

Keywords: Loss-based Bayesian forecasting; proper scoring rules; stochastic volatility; expected shortfall; Murphy diagram; M4 forecasting competition

MSC2010 Subject Classification: 62F15, 60G25, 62M20

JEL Classifications: C11, C53, C58.

1 Introduction

Bayesian prediction quantifies uncertainty about the future value of a random variable using the rules and language of probability. A probability distribution for a future value is produced, conditioned only on past observations; all uncertainty about the parameters of the prediction model, plus any uncertainty about the model itself, having been integrated, or averaged out via these simple rules. Inherent to this natural and coherent approach to prediction, however, is the assumption that the process that has generated the observed data is either equivalent to the particular model on which we condition, or contained in the set of models over which we average. Such a heroic assumption is clearly at odds with reality; in particular in the realm of the social and economic sciences where statistical data arises through complex processes that we can only ever intend to approximate.

In response to this limitation of the conventional paradigm, we propose an alternative approach to Bayesian prediction. A prior is placed over a class of plausible predictive models. The prior is then updated to a posterior over these models, via a criterion function that represents a user-specified measure of predictive accuracy. This criterion replaces the likelihood function in the conventional Bayesian update and, hence, obviates the explicit need for correct model specification. Summarization of the posterior so produced - via its mean, for example - yields a single, representative predictive distribution that is expressly designed to yield accurate forecasts according to the given measure. Alternatively, the full extent of the posterior variation that obtains can be quantified and visualized. Given this deliberate focus on a particular aspect of predictive performance in the building of predictions, we refer to the principle as focused Bayesian prediction, or simply FBP.

To quantify predictive accuracy we use the concept of a scoring rule. (See Gneiting et al.,, 2007, and Gneiting and Raftery,, 2007, for early expositions.) In short, a scoring rule rewards a probabilistic forecast for assigning a high density ordinate (or high probability mass) to the observed value (‘calibration’), subject to some criterion of ‘sharpness’, or some reward for accuracy in a particular part of the predictive support (e.g. the tails; Diks et al.,, 2011, Opschoor et al.,, 2017). Under appropriate regularity, we establish that this approach ensures, asymptotically, accurate performance according to the specified measure of predictive accuracy, and without dependence on correct model choice. Extensive numerical results support the theoretical results: focus on predictive accuracy, rather than correct model specification per se, leads to improved predictive performance.

This approach to Bayesian prediction has elements in common with the ‘probably approximately correct’ (PAC)-Bayes approach to prediction adopted in the machine learning literature; see Guedj, (2019) for a recent review and extensive referencing. The use of Bayesian updating per se without reference to a likelihood function also echoes the generalized inferential methods proposed by, for example, Bissiri et al., (2016), Giummolè et al., (2017), Knoblauch et al., (2019) and Syring and Martin, (2019), in which uncertainty about unknown parameters (in a given model) is updated via a general loss, or score, function. A major challenge in these generalizations of the standard Bayesian paradigm is the calibration of the scale of the loss (or score), which has a direct impact on the resultant variance of posterior of the parameters. Several methods for specifying this scale have been proposed (Bissiri et al.,; Giummolè et al.,; Holmes and Walker,, 2017; Lyddon et al.,, 2019; Syring and Martin,).111We note that Chernozhukov and Hong, (2003) also propose the use of quasi-posteriors based on updating a general loss function; however, the loss function is not calibrated as it is in the other literature referenced here. Whilst we draw some insights from this literature, we propose new approaches that are informed specifically by the prediction context in which we are working, and which ensure posterior concentration around the predictive that is optimal under the given accuracy measure.

The predictive distributions within the plausible class may characterize a single dynamic structure depending on a single vector of unknown parameters.222A related frequentist literature exists in which distributional forecasts produced via a particular model are ‘optimized’ according to a given form of predictive accuracy. Work in which this idea is implemented, or at least discussed, includes Gneiting et al., (2005), Gneiting and Raftery, (2007), Elliott and Timmermann, (2008) and Patton, (2019). However, they may also be weighted combinations of predictives from distinct models. As such, our approach represents a coherent Bayesian method for estimating weighted combinations of predictives via forecast accuracy criteria, and without the need to assume that the true model lies within the set of constituent predictives. Whilst an established literature on estimating mixtures of predictives exists (see Aastveit et al.,, 2019, for an extensive review) - including work that invokes Bayesian principles - our paper provides an alternative way of updating predictive combinations via non-likelihood-based Bayesian principles. We comment further on the connection of our work with the literature on predictive combinations, plus provide detailed referencing to this literature, in Section 4.2.

After establishing the theoretical validity of the new method, its efficacy and usefulness is demonstrated through a set of simulation exercises, based on alternative predictive classes for a stochastic volatility model for financial returns. These classes are deliberately chosen to represent, at one end, a very misspecified representation of the (known) true data generating process (DGP) and, at the other end, a less misspecified version. The comparator in all cases is the standard, and misspecified, likelihood-based Bayesian update of the given parametric class. The results are clear: within-sample updating based on a specific measure of predictive accuracy almost always leads to the best out-of-sample performance according to that measure. The degree of superiority depends on the interplay between the model class, including the manner in which the model is misspecified, and the desired measure of accuracy - with animated graphics used to illustrate this point. The differential impact of update choice on posterior variation is also highlighted, via an animated display of posterior distributions for the expected shortfall (ES) of both ‘long’ and ‘short’ portfolios in the financial asset.

Two empirical illustrations complete the analysis. In the first, we predict two different series of daily financial returns using predictive classes based on the Gaussian (generalized) autoregressive conditional heteroscedastic ((G)ARCH) class of volatility model, known to be misspecified for the more complex process driving returns. The series considered are returns on: the U.S. dollar currency index, and the S&P500 stock index. The empirical results mimic those produced by simulation, with predictive accuracy improved by using the focused update - rather than the conventional (likelihood-based) update - in virtually all cases. The increase in predictive accuracy translates into more accurate value at risk (VaR) forecasts: use of an update that focuses on tail accuracy leads to a better match of empirical to nominal VaR coverage (than does the likelihood update) in all cases, and more frequent support of the joint null of correct coverage and independent violations. Improved forecasts of ES also result in many cases.

In the second empirical example we pit FBP against the best performers in the Makridakis 4 (M4) forecasting competition. We perform the exercise using the 23,000 annual time series from the set of 100,000 series (of varying frequencies) used in the competition. We select as the predictive class, the exponential smoothing model of Hyndman et al., (2002) (referred to as ETS hereafter), which had ranked highly amongst all twenty-five competitors. Adopting the same preliminary model selection procedure as the authors to specify the components of the ETS class for each of the 23,000 series, we update the chosen class using the mean scaled interval score (MSIS). This measure of predictive accuracy penalizes a prediction interval if the observed value falls outside the interval (appropriately weighted by its nominal coverage), and rewards a narrow interval, and was one of the measures used to rank methods in the competition. As measured by MSIS, FBP not only almost always outperforms maximum likelihood-based implementation of ETS, but it outperforms all four predictive methods that were previously ranked best in the competition, in a large number of cases.

The rest of the article is organized as follows. In Section 2 we propose our new Bayesian predictive paradigm, and briefly illustrate its ability to produce more accurate predictions using a toy example. In Section 3 asymptotic validation of the method is provided, under the required regularity. More extensive illustration of the new approach via simulation, and visualization of the results, is the content of Section 4, whilst Section 5 illustrates the power of the method in empirical settings. In Section 6 we discuss the implications of our results and future lines of research. The proofs of all theoretical results, and certain computational details, are provided in appendices to the paper.

2 Focused Bayesian Prediction

2.1 Preliminaries and notation

Consider a stochastic process defined on the complete probability space . Let denote the natural sigma-field, and let denote the infinite-dimensional distribution of the sequence .

Throughout, we focus on one-step-ahead predictions and let denote a generic class of one-step-ahead predictive models for , which are conditioned on time information , and where the generic elements of are represented by The parameter indexes values in the predictive class, with defined on , and where measures our beliefs about . Our beliefs over - both prior and posterior - generate corresponding beliefs over the elements in the predictive class , in the usual manner and, therefore, throughout the remainder we abuse notation and refer to as indexing beliefs over the class .

Our goal is to construct a sequence of probability measures over , starting from our prior beliefs , such that hypotheses in that have ‘higher predictive accuracy’, are given higher posterior probability, after observing realizations from . Given a user-defined measure of accuracy, we demonstrate that such a probability measure can be constructed using a Bayesian updating framework.

Importantly however, we deviate from the standard approach to the production of Bayesian predictives in that the class only represents plausible predictive models for . At no point in what follows do we make the unrealistic assumption that the true one-step-ahead predictive is contained in .333The treatment of scalar and one-step-ahead prediction is for the purpose of illustration only, and all the methodology that follows can easily be extended to multivariate and multi-step-ahead prediction in the usual manner.

2.2 Bayesian updating based on scoring rules

Using generic notation for the moment, for a convex class of predictive distributions on , we measure the predictive accuracy of using the scoring rule , whereby if the predictive distribution is quoted and the value eventuates, then the reward, or positively-oriented ‘score’, is The expected score under the true predictive is defined as

| (1) |

We say that a scoring rule is proper relative to if, for all , and is strictly proper, relative to , if That is, a proper scoring rule is one whereby if the forecaster’s best judgment is indeed the true measure there is no incentive to quote anything other than (Gneiting and Raftery,, 2007).

Under the assumption that a given predictive class contains the truth, i.e. that , the expectation of any proper score , with respect to the truth , will be maximized at the truth, . Hence, maximization over of the expected scoring rule , will reveal the true predictive mechanism when it is contained in . In practice of course, the expected score is unattainable, and a sample estimate based on observed data is used to define a sample score-based criterion. Maximization of the sample criterion, which implicitly depends on the true predictive process through the observed data, will yield the member of the predictive class that maximizes the relevant sample criterion. However, asymptotically the true predictive distribution will be recovered via any proper score criterion (again, on the assumption that the true predictive lies in the class ).

The very premise of this paper is that, in reality, any choice of predictive class is such that the truth is not contained therein, at which point there is no reason to presume that the expectation of any particular scoring rule will be maximized at the truth or, indeed, maximized by the same predictive distribution that maximizes a different (expected) score. This does not, however, preclude the meaningfulness of a score as a measure of predictive accuracy, or invalidate the goal of seeking accuracy according to this particular measure. Indeed, it renders the distinctiveness of different scoring rules, and what form of forecast accuracy they do and do not reward, even more critical, and provides strong justification for driving predictive decisions by the very score that matters for the problem at hand.

With these insights in mind, we proceed as follows, reverting now to the specific notation that characterizes our problem, as defined in Section 2.1. Given observed data , our object of interest is , that is, the predictive distribution for , conditional on information known at time , . Given our prior beliefs , over , we update these beliefs using the following coherent posterior measure: for ,

| (2) |

where

| (3) |

and where the scale factor (indexed by ), used to define and index the posterior (via the notation ), is to be discussed in detail below.444The nature of the conditioning set differs according to the dynamic structure of For example, in a Markov model of order 1, comprises the observed only. In contrast, a predictive for a long memory model conditions on all available past observations. The conditioning set, , may also, of course, include observed values of covariates. Hence, we keep the notation for this conditioning set, , which is implicit in the definition of , distinct from that of the observed data, , that is used to build the posterior over the elements of Two more comments regarding notation are useful at this point. First, consistent with our earlier comment, we abuse notation by defining a prior directly over a predictive, here. In fact, the prior is placed over , and the prior over merely implied. Hence, the incongruous appearance of conditioning data in the prior (through the definition of ) is of no concern. It is simply used to define the particular function of () that is our ultimate object of interest, and that function conditions on (past) observed data, as it is a predictive distribution. Second, the criterion function that defines the update in (2) is, of course, comprised of the sequential one-step-ahead predictives, for

The use of the non-likelihood-based update in (2) mimics various generalizations of the standard Bayesian inferential paradigm that have been proposed. Such generalizations replace the likelihood with the exponential of a problem-specific loss function; the goal being to produce useful inference in the realistic setting in which the true DGP is unknown, and the correct likelihood function thus unavailable. This literature has its roots in the ‘Gibbs posteriors’ of Zhang, 2006a , Zhang, 2006b and Jiang and Tanner, (2008), in which the exponential of a general loss function replaces the likelihood function in the Bayesian update. However, it is arguably Bissiri et al., (2016), and the subsequent related work in (inter alia) Holmes and Walker, (2017), Lyddon et al., (2019) and Syring and Martin, (2019), that have given the method its recent prominence in the statistics and econometrics literature.

The PAC-Bayes algorithms used in machine learning are also characterized, in part, by exponential functions of general losses. The focus therein is on loss defined with respect to predictors, rather than parameters; hence the particular connection with our approach. Our work is, however, quite distinct from PAC-Bayes. Most notably, the updating mechanism in (2) is expressed in terms of a class of plausible conditional predictive distributions, rather than point predictors, and the ‘loss function’ defined explicitly in terms of a proper scoring rule. We also entertain predictive models that feature in the statistics and/or econometrics literature, and provide asymptotic validation of the method in this context.555The PAC-Bayes method also encompassess up-dates based on so-called ‘tempered’, or ‘power’ likelihoods, in which robustness to model misspecification is sought by raising the likelihood function associated with an assumed model to a particular power. See Grünwald and van Ommen, (2017), Holmes and Walker, (2017) and Miller and Dunson, (2019) for recent examples in which such modified likelihoods feature. We refer to Guedj, (2019) for a thorough review of PAC-Bayes, including the methods and terminology used in that setting.

The update in (2) is coherent in the sense that the posterior that results from updating the prior using two sets of observations in one step, is the same as that produced by two sequential updates. Proof of this property follows that of Bissiri et al., (2016) and exploits the exponential form of the first term on the right-hand-side of (2), in addition to certain conditions on to be made explicit below. Indeed, the appearance of serves to distinguish (2) from what would be an extension (to the predictive setting) of the loss-based inference approach adopted by Chernozhukov and Hong, (2003).666We note that a negatively-oriented score can be viewed as a relevant measure of ‘loss’ in a predictive setting. Moreover, it is also possible to define the loss associated with predictive inaccuracy using functions that are not formally defined as scoring rules (see, for example, Pesaran and Skouras,, 2004). However, we give emphasis to scoring rules in this paper, making brief note only of the applicability of our method to more general loss functions in the Discussion.

In the case where and with denoting the predictive density (or mass) function associated with the class , the update in (2) obviously defaults to the conventional likelihood-based update of the prior defined over . We refer hereafter to this special case as ‘exact Bayes’, and acknowledge that, given the presumption of misspecification, there is no sense in which exact Bayes remains the ‘gold standard’. This case remains, however, a critical benchmark in the numerical work, in which the degree of misspecification of will be seen to influence the relative out-of-sample performance of the conventional Bayesian update.

We can summarize the posterior in (2) by producing a simulation-based estimate of the mean predictive:

| (4) |

However, it is equally feasible to construct measures that capture the variability of the posterior, such as quantiles or the posterior variance. Moreover, we can use various graphical techniques to visualize the variation of the predictives themselves and understand the way in which posterior variation over the class impacts on predictive accuracy per se.

Before moving on, we quickly demonstrate the usefulness of this new approach to Bayesian prediction, and the predictive gains that it can reap, using a simple toy example.

2.3 A toy example: ARCH(1)

We produce predictive distributions for a financial return generated from a latent stochastic volatility model with a skewed marginal distribution, with precise details of this true DGP to be given in Section 4. The predictive class, , is defined by an ARCH model of order 1 (ARCH(1)) with Gaussian errors, with , and (with the indicator function) defining a prior density over .

For denoting the predictive density function associated with the Gaussian ARCH(1) class, we implement FBP using the following two scoring rules:

| (5) | ||||

| (6) |

As noted already, use of the log score (LS), (5), in (2) (with ) yields the conventional likelihood-based Bayesian update, and we label the results based on this score as exact Bayes as a consequence. The score in (6) is the censored likelihood score (CS) introduced by Diks et al., (2011), and applied by Opschoor et al., (2017) to the prediction of financial returns. This score rewards predictive accuracy over the region of interest (with indicating the complement of this region). Here we report results solely for defining the lower and upper tail of the predictive distribution, as determined respectively by the 10% and 90% quantile of the empirical distribution of . We label the results based on the use of (6) in (2) (also using ) as FBP-CS<10% and FBP-CS

Postponing discussion of the full design details until Section 4, we record in Table 1 out-of-sample results based on repeated computation of (4) using expanding windows to produce (via Markov chain Monte Carlo) draws from (2). Using a total of 2,000 out-of-sample values, the average LS (computed across the 2,000 mean predictives) and the average CS for the lower and upper 10% tail (denoted by CS<10% and CS>90% respectively) are computed for each of the three different updating methods. Recalling that we use positively-oriented scores, the largest average score, according to each out-of-sample evaluation method, is highlighted in bold.

| Out-of-sample score | ||||

|---|---|---|---|---|

| LS | CS<10% | CS>90% | ||

| Updating method | ||||

| Exact Bayes | -1.3605 | -0.4089 | -0.2745 | |

| FBP-CS<10% | -1.4420 | -0.3943 | -0.3833 | |

| FBP-CS>90% | -3.0067 | -1.4157 | -0.2397 | |

We see that use of the CS rule in the posterior update yields better out-of-sample performance, as measured by that score, in both the upper and lower tails. In absolute terms, the gain of ‘focusing’ is more substantial in the upper tail than the lower tail, and in Section 4 we shall see why this is so. The average LS produced by the exact Bayes (LS-based) update is also larger than the average LS produced by both FBP-CS<10% and FBP-CS>90%.

In summary, focusing works, and the following theoretical results give some insight into why.

3 Bayesian and Frequentist Agreement

Whilst the elements of may, in principle, be either parametric or nonparametric conditional distributions, in the remainder we focus on the parametric case to simplify the analysis, leaving rigorous analysis of nonparametric conditionals for later study. However, we remind the reader that this reduction to parametric conditionals covers both the canonical case where the elements of are indexed by a finite-dimensional parameter, in which case is a Euclidean space, as well as the case where the elements in are (a finite collection of) mixtures of predictives, in which case denotes either the weights of the mixture, or the combination of the weights and the unknown parameters of the constituent predictives.

3.1 Choosing

With reference to the conventional Bayesian approach to inference on the unknown parameters, , which characterize an assumed DGP, the posterior density,

| (7) |

where denotes the likelihood function, arises via a decomposition of the joint probability distribution for and the random vector As such, the representation of as proportional to the product of a density (or mass) function for , and the prior for , reflects the usual calculus of probability distributions, and provides a natural ‘weighting’ between the likelihood and the prior.

Once one moves away from this conventional framework, and replaces the likelihood with an alternative mechanism through which the data provides information about , this natural weighting is lost. Instead, a subjective choice must be made regarding the relative weight given to prior and data-based information in the production of the posterior, with the scale factor in (2) denoting this subjective choice of weighting. Bissiri et al., (2016) propose several methods for choosing , including annealing methods, hyper-parametrization of , and setting to ensure the equivalence of the expected ‘loss’ of the prior and data-based components of (2). The authors also suggest choosing to ensure correct frequentist coverage of posterior credible intervals, plus the use of priors that are conjugate to the weighted data-based criterion.777Further proposals on the choice of can be found in Holmes and Walker, (2017), Lyddon et al., (2019) and Syring and Martin, (2019).

In contrast, our interest is not in inference on per se, but in forecast accuracy. Given this goal, from a theoretical standpoint, our only concern is that, for a chosen scaling sequence, the FBP posterior measure concentrates onto the element of that is most accurate in the chosen scoring rule, which is defined by the following value in :

| (8) |

As the following result demonstrates, this concentration occurs for any reasonable choice of .

Lemma 1.

Remark 1.

The above result demonstrates that, if we restrict our analysis to a class of parametric predictives, FBP asymptotically concentrates, at rate , onto the predictive that is most accurate according to the scoring rule .

Remark 2.

The conditions for the above result are discussed in Appendix A and are similar to the standard regularity conditions for parametric -estimators, along with some uniform control on the tail of the prior . These conditions are similar to those used elsewhere in the literature, e.g., Chernozhukov and Hong, (2003). Interestingly, Lemma 1 is valid for a wide variety of . In Sections 4 and 5, we detail the particular values of that we use to produce our numerical predictions.

3.2 Merging

In the previous section, we have seen that, for a reasonable choice of , the FBP posterior concentrates on the element of that is most accurate for prediction under the chosen scoring rule. In this section, we compare the behavior of predictions obtained from the FBP posterior with those that would be obtained using direct optimization of an expected score criterion to produce a frequentist point estimate of , and the associated predictive that conditions on this point estimate.

Define the following predictive measures

| (9) | ||||

| (10) |

where denotes the Dirac measure at the point , for defined in (8). The mean predictive defines a distribution for the random variable , conditional on observed data , and where our uncertainty about the members of the predictive class, , is integrated out using the posterior , for some choice of tuning sequence .888The expression in (9) is just a more formal representation of (4). In contrast, the predictive in (10) denotes the optimal predictive obtained by maximizing the expected score. Clearly, obtaining is infeasible in practice. Instead, the following estimated value of , is generally used in place of . Under the same regularity conditions as in Lemma 1, we can derive the asymptotic behavior of .

Using the estimator , we can define the following frequentist equivalent to the FBP predictive:

| (11) |

where denotes the normal distribution function with mean and variance-covariance matrix . Using Lemmas 1 and 2, we can deduce the following relationship between the frequentist predictive in equation (11) and the FBP predictive in (9).

Remark 3.

Theorem 1 states that, for any sequence , the FBP predictive and the (feasible) optimal frequentist predictive will agree asymptotically. The above result is colloquially referred to as ‘merging’ (Blackwell and Dubins,, 1962). This result states that, in terms of the total variation distance, the predictions obtained by FBP and those obtained by a frequentist making predictions according to an optimal score estimator will asymptotically agree.

4 Simulation Study: Financial Returns

4.1 Overview of the simulation design

We first illustrate our approach with a simulation exercise that nests the toy example in Section 2.3. Adopting a simulation approach allows us to choose predictive classes that misspecify the (known) DGP to varying degrees, and to thereby measure the relative performance of FBP in different misspecification settings. We use both numerical summaries and animated graphics to illustrate the predictive accuracy of FBP, using a range of scores to define the update. With a slight abuse of terminology, in what follows we refer to FBP-LS solely as ‘exact Bayes’, reserving the abbreviation FBP for all other instances of the focused method.

We address three questions. First, what sample size is required in practice for the asymptotic results to be on display? That is, how large does have to be for FBP based on a particular scoring rule to provide the best out-of-sample performance according to that same rule? Second, does the degree of misspecification affect the dominance of FBP over exact Bayes? Third, does misspecification have a differential impact on FBP implemented via different scoring rules?

With the aim of replicating the stylized features of financial returns data, we generate a logarithmic return, , from

| (12) | ||||

| (13) | ||||

| (14) |

where and are independent processes, is a latent process with stochastic (logarithmic) variance, , and is the implied marginal distribution of (evaluated via simulation). The ‘observed’ return, , is then generated as in (14), via the (inverse) distribution function associated with a standardized skewed-normal distribution, .999For more details of the specific skewed-normal specification that we adopt see Azzalini, (1985). This process of inversion imposes on the dynamics of the stochastic volatility model represented by Equations (12) and (13) (via ) in addition to the negative skewness that is characteristic of the empirical distribution of a financial return.101010See Smith and Maneesoonthorn, (2018) for discussion of this type of implied copula model.

We adopt three alternative parametric predictive classes, i) Gaussian ARCH(1) (reproduced here for convenience and numbered for future reference):

| (15) |

ii) Gaussian GARCH(1,1):

| (16) |

and iii) a mixture of the predictives of two models: an ARCH(1) model with a skewed-normal innovation, and a GARCH(1,1) model with a Gaussian innovation. We represent the elements of class iii) as:

| (17) |

In (15) and (16) the respective parameter vectors, and , characterize the specific predictive model, with the GARCH(1,1) model being a more flexible (and, in this sense, ‘less misspecified’) representation of the true DGP than is the ARCH(1) model. In (17) the parameter vectors and that characterize the constituent predictives in the mixture are taken as known, and the scalar weight parameter is the only unknown. The component is specified according to the model in (16), whilst represents the predictive associated with the model in (15), but with distributed as a standardized skewed-normal variable with asymmetry parameter .111111The values imposed for and are the maximum likelihood estimators of these parameters. With the proviso made that the parameters of the constituent models are taken as given, the linear pool is arguably the most flexible form of predictive considered here, and defines the least misspecified predictive class in this sense. The prior over each of the three predictive classes is determined by the prior over the relevant parameter (vector) , respectively: i) (as defined earlier), ii) , and iii) (with uniform on ).

We now implement FBP using the two scoring rules in (5) and (6), plus the continuously ranked probability score (CRPS),

| (18) |

where denotes the predictive cumulative distribution function (cdf) associated with . Proposed by Gneiting and Raftery, (2007), CRPS is sensitive to distance, rewarding the assignment of high predictive mass near to the realized value of . It can be evaluated in closed form for the (conditionally) Gaussian predictive classes i) and ii), using the third equation provided in Gneiting and Raftery, (2007, p. 367). For predictive class iii), evaluation is performed numerically using expression (17) in Gneiting and Ranjan, (2011, p. 367). In the case of the CS in (6), all components, including the integral , have closed-form representations for predictive classes i) and ii). For the third predictive class, CS is computed as

where and correspond to the censored scores for the two constituent models, both having closed-form solutions.

As noted in Section 2.3, when either (5) or (6) is used in (2) a scale of is adopted. This is a natural choice, given that use of (5) defines the (misspecified) likelihood function induced by the predictive class, and that use of (6) is comparable to the specification of the likelihood function for a censored random variable (Diks et al.,, 2011). When (18) is used to define the posterior update however, the interpretation of as the (unnormalized) probability distribution of a random variable is lost, and must be chosen with reference to some criterion for weighting and . We choose to target a value for that ensures a rate of posterior update - when using CRPS - that is similar to that of the update based on LS, by defining

| (19) |

The subscript indicates that the expectation is with respect to the exact posterior distribution for . In practice, is estimated as

| (20) |

using draws of from the , , The link between specifying as in (19) and achieving a rate of posterior update that approximates that of exact Bayes, is detailed in Appendix B.1. All details of the Markov chain Monte Carlo (MCMC) scheme used to perform the posterior sampling are provided in Appendix B.2.

4.2 A comment on the role of predictive combinations

Before we proceed to document and discuss the simulation results in the following section, we comment briefly on the role played by predictive combinations in the simulation exercise and, subsequently, in certain of our empirical illustrations.

As noted in the Introduction, there is a well-established literature - invoking both frequentist and Bayesian principles - in which the weights in weighted combinations of predictives are either optimized (in the first case) or up-dated (in the second) according to predictive criteria. The frequentist literature includes work on linear combinations (or linear pools), in which various measures of predictive accuracy, including scoring rules, are used to define the criterion that is optimized to estimate the weights. Relevant references here include Hall and Mitchell, (2007), Kascha and Ravazzolo, (2010), Geweke and Amisano, (2011), Ganics, (2017), Opschoor et al., (2017) and Pauwels et al. (2019).121212Closely related work appears in Jore et al., (2010). Non-linear weighting schemes (or non-linear transformations of linear schemes) - again estimated via optimization of prediction-based criteria - are explored in Ranjan and Gneiting, (2010), Clements and Harvey, (2011), Gneiting and Ranjan, (2013) and Kapetanios et al., (2015). The Bayesian literature, having access as it does to posterior simulation schemes, has entertained more sophisticated (including time-varying) weighting schemes, in which predictive performance influences the posterior up-dates of the weights in one way or another. Key work here includes Billio et al., (2013), Casarin et al., 2015a , Casarin et al., 2015b , Casarin et al., (2016), Pettenuzzo and Ravazzolo, (2016), Bassetti et al., (2018), Baştürk et al., (2019) and Casarin et al., (2019).131313Conventional Bayesian model averaging (BMA) as applied to predictive distributions is effectively driven by a log score criterion, given the intrinsic connection between the predictive likelihood and the marginal likelihood that underlies each BMA weight. (See, for example, Geweke,, 2005, Chapter 2.)

In principle, any of the above combination schemes could be used to construct the predictive class , with the chosen measure of predictive accuracy used to define the update in (2). It is certainly the case that more sophisticated combination schemes for the constituent weights would require an alternative, and more computationally intensive, posterior sampling scheme than the straightforward MCMC algorithm we have adopted for the simple linear pool; nevertheless, beyond this issue, the principles that underpin our methodology would remain the same.141414We conjecture that the melding of the nonparametric Bayesian approach in Bassetti et al., (2018) and our generalized Bayesian updating would be a particularly fruitful avenue for future exploration; as would be a merging of the Bayesian predictive synthesis of Mike West and co-authors (e.g. Johnson and West,, 2018) and our focused prediction method.

However, the key point is that the goal of yielding a more accurate representation of the true DGP by employing more sophisticated weighting schemes is ancillary to the predictive philosophy underpinning our approach: we are not concerned with trying to find a model that more accurately represents the true DGP, but with ensuring that our chosen predictive delivers accuracy in terms of our chosen loss measure. Hence, we include predictive combinations in certain numerical illustrations not for the purpose of building a better representation of the DGP per se, but: first, to highlight the fact that such forms of distribution can be accommodated within our procedure; and second, as a way of illustrating the effect on the relative performance of FBP and exact Bayes of using a predictive class that more accurately captures the features of the true DGP than does any single model.

4.3 Simulation results

4.3.1 Summary results based on mean predictives

We generate observations of from the DGP in (12)-(14), using parameter values: , and , while defines the standardized skewed-normal distribution with shape parameter , which produces an empirically plausible degree of negative skewness. For each predictive class, and for each score update, the exercise begins by using the relevant computational scheme, as described in Appendix B.2, to produce (after thinning) posterior draws of , , and, hence, posterior draws of (at any point in the support of , which we denote simply by , as indexed by the draw of This first set of posterior draws is produced using the first values of in the update in (2). For each predictive class, six score updates are employed, corresponding to (5) and (18), plus (6) with the region A defining (approximately) four tails of the predictive distribution: lower 10%, lower 20%, upper 10% and upper 20%.151515As noted in Section 2.3, the set for any required tail probability, is determined via reference to the empirical distribution of ; hence the use of the word ‘approximately’. Hence, for each predictive class, draws from six different are produced.

Referencing the draws, , , from any one of the six distinct posteriors, we first estimate the mean predictive in (4) as: and compute the out-of-sample score of this single predictive, based on the observed value of , for period The same six scores used in the in-sample updates are used to produce these out-of-sample scores. The sample is then extended to , and the same exercise is repeated, with the out-of-sample scores computed using the observed value of , for time period This exercise is repeated 2,000 times, with the final set of out-of-sample scores computed using the observed value of for time period The average of the 2,000 scores is recorded in Table 2: for each update method, each out-of-sample evaluation method, and each predictive class.

Expanding on the results reported in Section 2.3, Panels A, B and C in Table 2 correspond respectively to the three predictive classes: ARCH(1), GARCH(1,1) and the mixture. The rows in each panel refer to the six distinct update methods, denoted in turn by: exact Bayes ( FBP-LS), FBP-CRPS, FBP-CS<10%, FBP-CS<20%, FBP-CS>80% and FBP-CS>90%. The columns refer to the out-of-sample measure used to compute the average scores: LS, CRPS, CS<10%, CS<20%, CS>80% and CS Numerical validation of the asymptotic results occurs if the largest average scores (bolded) appear in the diagonal positions in the table; that is, if using FBP with a particular focus yields the best out-of-sample performance according to that same measure of predictive accuracy.

| Panel A: ARCH(1) predictive class | ||||||||

| Out-of-sample score | ||||||||

| Center Focused | Left Focused | Right Focused | ||||||

| LS | CRPS | CS<10% | CS<20% | CS>80% | CS>90% | |||

| Updating method | ||||||||

| Exact Bayes | -1.3605 | -0.5299 | -0.4089 | -0.6687 | -0.4716 | -0.2745 | ||

| FBP-CRPS | -1.3663 | -0.5290 | -0.4206 | -0.6774 | -0.4723 | -0.2775 | ||

| FBP-CS<10% | -1.4442 | -0.5558 | -0.3943 | -0.6506 | -0.5755 | -0.3833 | ||

| FBP-CS<20% | -1.4660 | -0.5652 | -0.3933 | -0.6484 | -0.6002 | -0.4072 | ||

| FBP-CS>80% | -2.0422 | -0.5902 | -0.9655 | -1.3470 | -0.4365 | -0.2430 | ||

| FBP-CS>90% | -3.0067 | -0.6747 | -1.4157 | -2.0858 | -0.4592 | -0.2397 | ||

| Panel B: GARCH(1,1) predictive class | ||||||||

| Out-of-sample score | ||||||||

| Center Focused | Left Focused | Right Focused | ||||||

| LS | CRPS | CS<10% | CS<20% | CS>80% | CS>90% | |||

| Updating method | ||||||||

| Exact Bayes | -1.3355 | -0.5259 | -0.3941 | -0.6500 | -0.4710 | -0.2747 | ||

| FBP-CRPS | -1.3381 | -0.5258 | -0.3992 | -0.6532 | -0.4734 | -0.2788 | ||

| FBP-CS<10% | -1.3801 | -0.5341 | -0.3838 | -0.6387 | -0.5282 | -0.3317 | ||

| FBP-CS<20% | -1.4126 | -0.5480 | -0.3840 | -0.6375 | -0.5650 | -0.3710 | ||

| FBP-CS>80% | -2.0535 | -0.5918 | -0.9612 | -1.3530 | -0.4318 | -0.2387 | ||

| FBP-CS>90% | -3.1207 | -0.6818 | -1.4544 | -2.1502 | -0.4572 | -0.2347 | ||

| Panel C: Mixture predictive class | ||||||||

| Out-of-sample score | ||||||||

| Center Focused | Left Focused | Right Focused | ||||||

| LS | CRPS | CS<10% | CS<20% | CS>80% | CS>90% | |||

| Updating method | ||||||||

| Exact Bayes | -1.2901 | -0.5241 | -0.3898 | -0.6448 | -0.4363 | -0.2447 | ||

| FBP-CRPS | -1.2975 | -0.5234 | -0.3868 | -0.6418 | -0.4476 | -0.2557 | ||

| FBP-CS<10% | -1.3048 | -0.5236 | -0.3871 | -0.6422 | -0.4536 | -0.2610 | ||

| FBP-CS<20% | -1.3029 | -0.5235 | -0.3871 | -0.6421 | -0.4523 | -0.2599 | ||

| FBP-CS>80% | -1.2902 | -0.5250 | -0.3921 | -0.6472 | -0.4325 | -0.2407 | ||

| FBP-CS>90% | -1.2902 | -0.5250 | -0.3922 | -0.6472 | -0.4324 | -0.2406 | ||

The results in Table 2 broadly validate the asymptotic theory. With minor deviations, the expected appearance of bold figures on the main diagonal of each panel is in evidence - most notably in Panels A and B. Hence, with reference to the first question outlined at the beginning of Section 4.1: an initial sample size exceeding , expanded to in the production of 2,000 one-step-ahead predictions, is sufficient for the use of in-sample focusing to reap benefits out-of-sample.161616We reiterate that in this numerical assessment of predictive performance based on expanding estimation windows, there are two sample sizes that play a role: i) the size of the estimation period on which the posterior (over predictives) is based, and from which the mean (one-step-ahead) predictive and numerical score are extracted; and ii) the size of the out-of-sample period over which the average (one-step-ahead) scores are computed. With expanding estimation windows, an increase in the out-of-sample period goes hand-in-hand with a continued increase in the estimation period, i.e. an increase in . When there is a deviation from the strict diagonal pattern, such as in the CS<10% column of Panel A and in the CS<10%, CS<20% and CS>80% columns of Panel C, the difference between the relevant (non-diagonal) bold value and the value on the diagonal is negligible.

With reference to the second question, the out-of-sample dominance of FBP over exact Bayes declines as the predictive class becomes less misspecified. In particular, the results in Panel C - for the mixture predictive class - reveal that the average scores computed using a given out-of-sample measure are very similar for all six updating methods. The extent of the misspecification of the true DGP clearly does matter.171717For a large enough sample of course, for a predictive class that contains the true DGP, any updating method based on a proper score should (under regularity) recover the true predictive mechanism and, hence, should yield predictive performance out-of-sample (however measured) that matches that of an update based on an alternative proper score. See Gneiting and Raftery, (2007) for an early exposition of this sort of point, in the context of frequentist point estimation using scoring rules.

With respect to the third question: there are two notable results regarding the differential impact of the degree of misspecification on the different versions of FBP. First, when the degree of misspecification is most severe (as with the ARCH(1) and GARCH(1,1) predictive classes) use of the update that focuses on the upper tail (FBP-CS>80% or FBP-CS>90%) produces poor out-of-sample accuracy according to the LS and lower tail measures (CS<10% and CS<20%). We provide some graphical insight into this specific phenomenon in Section 4.3.2; however, the point is that focusing incorrectly can hurt, in particular when the predictive class is a poor match for the true DGP. Once misspecification of the predictive class is reduced, the performance of both FBP-CS>80% and FBP-CS>90% - according to all out-of-sample measures - broadly matches that of the other updating methods, as can be seen in Panel C.

The second differential impact of misspecification pertains to the exact (misspecified) Bayesian update, relative to all four tail-focused methods (FBP-CS<10%, FBP-CS<20%, FBP-CS>80% and FBP-CS>90%). For example, the values of CS>90% for FBP-CS>90% (the three bolded figures in the very last column of Table 2) change very little over the three panels, as the degree of misspecification lessens. A similar comment applies to the three values of CS<10% for FBP-CS In contrast, the improvement in performance in the tails (so the values of CS>90% and CS<10%) for exact Bayes, as one moves from the most to the least misspecified predictive class, is more marked; which makes sense. The focused methods do not aim to get the model correct; instead, they are deliberately tailored to a particular predictive task (accurate prediction of extreme values in this case). Hence, misspecification of the model per se matters less. The predictive performance of exact Bayes, on the other hand, depends entirely on the match between the model that underpins the method and the truth; there is nothing else that exact Bayes brings to the table; if the model is wrong, prediction (however measured) will be adversely affected by that error.

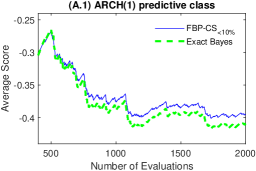

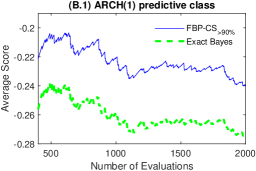

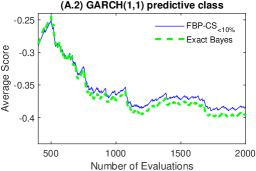

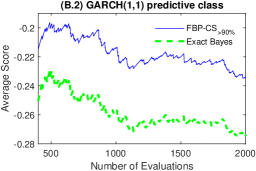

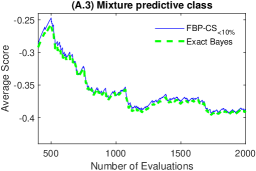

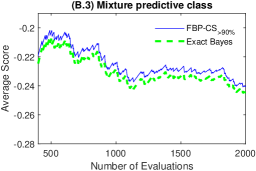

To gauge the sensitivity of the findings to the size of the out-of-sample evaluation period, we plot the average one-step-ahead score as a function of the latter. In the quest for brevity, we perform this task for two out-of-sample measures only: CS<10% and CS In Panel A of Figure 1 the cumulative average of CS<10% (for 400 to 2,000 out-of-sample periods) is plotted for two forms of in-sample updates only: exact Bayes (the dashed green line) and FBP-CS<10%, (the blue full line). Each of the three figures (A.1, A.2, A.3) corresponds respectively to results for each of the three predictive classes (ARCH(1), GARCH(1,1) and the mixture). In Panel B (B.1, B.2 and B.3) the corresponding results for the cumulative average of CS>90% are presented, based on exact Bayes (the dashed green line) and FBP-CS>90%, (the blue full line). In all figures, the final numerical values plotted correspond to the relevant values reported in Table 2.

Beginning with Figure A.1, we see that a sufficiently large of out-of-sample evaluation period (exceeding approximately 600) is needed for the dominant performance of FBP over exact Bayes to be in evidence visually; with in-sample estimation periods exceeding contributing to these average score results. However, beyond this point, the amount by which the full line exceeds the dashed one stabilizes, reflecting the extent to which FBP-CS<10% produces more accurate predictions of extreme (lower tail) returns than does exact Bayes, asymptotically. Tallying with the interpretation of the numerical results in Table 2, the extent to which FBP-CS<10% is superior to exact Bayes is successively less in Figures A.2 and A.3, with the dashed line ‘moving up’ to match the full line, as the misspecification of the predictive class is reduced. The size of the evaluation period required to produce a visual distinction between the out-of-sample performance of exact Bayes and FBP-CS<10% is larger, the less misspecified is the class.

| Panel A: | Panel B: |

|---|---|

| Lower tail accuracy | Upper tail accuracy |

|

|

|

|

|

|

In Panel B, the superiority of FBP-CS>90% over exact Bayes, in terms of accurately predicting extremely large returns is in stark evidence. In this case, the relative performance of the two updating methods is less affected by the move from the ARCH(1) to the GARCH(1,1) predictive class. However, once again, use of the more flexible mixture of predictives to underpin the exact Bayes update brings its performance much closer to that of the focused update, with the accuracy of the latter being reasonably robust to the choice of predictive class.

In the following section we provide some insight into why the focused update in the upper tail reaps more benefit out-of-sample than does the lower-tail update, relative to exact Bayes, and the role that misspecification plays here.

4.3.2 Animation of the mean predictives

In Figures 2 and 3 we display animated plots of the one-step-ahead mean predictives produced using expanding windows of to , and based solely on the (most misspecified) Gaussian ARCH(1) predictive class. The mean predictives produced by both updating methods (FBP and exact Bayes) are superimposed upon the true predictive, produced using simulation from (12)-(14). Figure 2 presents the results for lower tail focus (FBP-CS<10% versus exact Bayes) and Figure 3 the results for upper tail focus (FBP-CS>90% versus exact Bayes). The vertical lines in each plot indicate the return that defines the quantile in (6).

[controls,loop,scale =0.75]3Animate_out_low

[controls,loop,scale =0.75]3Animate_out_up

Two things are clear from Figure 2: one, the lower tails of both the FBP-CS<10% and exact Bayes predictives are quite similar; two, both tails are - for some time points - quite good at picking up the shape of the true predictive tail, but with the FBP-CS<10% predictive tail being a better match most of the time. These plots thus provide some explanation of the summary results in Panel A (column 3) of Table 2 and Panel A.1 of Figure 1, in which FBP-CS<10% dominates exact Bayes, but with the improvement in forecast accuracy being reasonably small, despite the misspecification of the predictive class.

In Figure 3 however, the animated display is very different. The upper tail of the exact Bayes predictive consistently fails to pick up the shape of the true: the misspecified nature of the Gaussian ARCH(1) model has a marked impact on predictive accuracy in this region of the support of In contrast, FBP-CS>90% has the flexibility to focus only what matters - upper tail predictive accuracy - and, as such, produces predictives with upper tails that are much closer in shape to the true, and which are often visually indistinguishable from the true. These plots thus explain the clear numerical dominance of FBP-CS>90% over exact Bayes in Panel A (column 6) of Table 2 and Panel B.1 of Figure 1.

We finish by noting that focus on upper tail accuracy does - as highlighted by the relevant figures in the middle columns of Panel A in Table 2 - impact quite severely on the ability of FBP- CS>90% to pick up the lower tail of the true predictive. This outcome highlights the fact that the ex-ante decision as to what form of accuracy to focus on is critical, and most notably so in the very misspecified case.

4.3.3 The differential effect of posterior variation

When adopting the conventional Bayesian paradigm for prediction, a single question needs to be addressed: which model (or set of models) is to be used to produce the predictive distribution? Once that model (or set of models) has been chosen, computational methods are used to integrate out the posterior uncertainty associated with that choice, and a single (marginal) predictive distribution thereby produced. Posterior parameter (and model) uncertainty affects the location, shape, and degree of dispersion of the marginal predictive, and any predictive conclusions drawn from it; however, it is not the convention to explicitly quantify the impact of posterior variation on prediction.

Our new proposal introduces an additional choice into the mix: which measure of predictive accuracy is to drive the production of a predictive distribution? Each different form of in-sample update serves as a different ‘window’ through which a choice of predictive model (or mixture of predictive models) - and all posterior uncertainty associated with that choice - impinges on predictive outcomes. For example, one choice of update may yield a posterior distribution over a given predictive class that is very diffuse; another choice may lead to a very concentrated posterior. Hence, finite sample posterior variation itself has import, since it is not unique, even given a particular choice of predictive class.

We illustrate this point using posterior draws from (2) for both FBP-CS<10% and FBP-CS>90%, using the Gaussian ARCH(1) predictive class, and for selected values of between and . From the draws from (2) based on the FBP-CS<10% update, we produce the corresponding values of the ES for period for a portfolio that is ‘long’ in the asset,181818See, for example, Embrechts et al., (1997).

| (21) |

The integral bound in (21) denotes the quantile, and ES denotes the (negative of the) mean of the random variable conditional on the future return falling into the lower 10% tail of ; that is, the (negative) expected return in a worst case scenario. For a ‘short’ portfolio, in which extremely large returns are harmful, the relevant function is:

| (22) |

where in (22) denotes the quantile, and ES denotes the mean of conditional on the future return falling into the upper 10% tail of In this case we produce values of ES using the draws from (2) based on the FBP-CS>90% update. For the Gaussian ARCH(1) predictive class, ES and ES have closed-form solutions, for any given value of

In each case we use kernel density estimation to produce an estimate of the marginal posterior of the scalar ES, based on the draws from (2). As a comparator in each case, we perform the same exercise but using the exact (likelihood-based) Bayes update to define (2). The ‘true’ values of ES0.1 and ES0.9, computed using simulation from (12)-(14), are reproduced on the respective plots as red vertical lines. All computations are performed for the selected values of , and animated graphics are used to illustrate how all quantities change over time.

[controls,loop,scale =0.75]1Animate_out_long \animategraphics[controls,loop,scale =0.75]1Animate_out_short

From Panel A in Figure 4 we see results that broadly confirm the lack of dominance of the FBP-CS<10% update over exact Bayes, in terms of accurately reproducing the lower tail of the true predictive. Neither the FBP-based posterior of ES (the full blue curve), nor the exact Bayes posterior (the dashed green curve) is located uniformly closer to the true vertical (red) value than the other, across time. That said, the posterior variation in the exact Bayes posterior is always less than that of the FBP posterior, for the selected time points considered.

In contrast, in Panel B in Figure 4 there is a much more marked tendency for the FBP posterior of ES to be located closer to the true value of ES0.9 than is the exact Bayes posterior, in addition to being much more concentrated. Hence, there are several instances over time in which the FBP posterior is extremely concentrated around - or very near to - the true ES: providing a further illustration of the benefits reaped by focusing on upper tail accuracy in the update.

5 Empirical Illustrations

We now illustrate the potential of the focused approach in empirical settings. In Section 5.1 we produce predictive results for two empirical return series, using the same predictive classes adopted in the simulation experiments above. We document the accuracy of the FBP posterior mean predictive in a similar manner to the documentation of the results in Table 2. Furthermore, we illustrate the practical benefits of FBP using two empirically relevant loss measures: one, empirical exceedances for predictive VaRs; two, out-of-sample accuracy for ES, as measured by a consistent class of scoring functions (Ziegel et al.,, 2020). In Section 5.2 we provide a quite different - and ambitious - empirical illustration, by using FBP to predict the 23,000 annual time series from the 2018 ‘M4’ forecasting competition. In all illustrations we estimate the mean predictive in (4) (for the relevant predictive class and updating rule) using (after thinning) 4,000 MCMC posterior draws of , and base all out-of-sample assessments on this mean predictive. The MCMC scheme remains as described in Appendix B.2, apart from certain minor modifications required for the ‘M4’ example, as detailed in Section 5.2.

5.1 Financial returns

5.1.1 Preliminary diagnostics

The two series used in the first empirical illustration are: i) observations of daily returns on the U.S. dollar currency index (DXY), from 3 Jan 2000 to 3 Nov 2015; and ii) observations of daily returns on the S&P500 index, from 3 Jan 1996 to 3 Feb 2012. Both series are supplied by the Securities Industries Research Centre of Asia Pacific (SIRCA) on behalf of Reuters. All returns are continuously compounded. To match the simulation exercise, the last 2,000 observations in each series are used to perform all out-of-sample assessments, with the one-step-ahead mean predictives produced in the same manner as described in Section 4.3.1 (using expanding estimation samples), apart from the fact that the first estimation sample for both empirical series is of length (rather than ). We also adopt the same three predictive classes, defined by the Gaussian ARCH(1), Gaussian GARCH(1,1) and mixture models.191919As in the simulation exercise, the parameters in the constituent models in the mixture are estimated via maximum likelihood.

As tallies with the typical features exhibited by financial returns, the descriptive statistics reported in Table 3 provide evidence of time-varying volatility (significant serial correlation in squared returns) and marginal non-Gaussianity (significant non-normality in the level of returns) in both series. Hence, we can conclude that the simple Gaussian ARCH(1) and GARCH(1,1) predictive classes are likely to be misspecified, and more so than the more flexible mixture class. As such, we would anticipate accuracy gains - by using FBP rather than exact Bayes - to be most in evidence for the ARCH(1) predictive class, with decreasing relative gains expected as the predictive class becomes less misspecified.

| Min | Max | Mean | Median | St.Dev | Range | Skewness | Kurtosis | JB stat | LB stat | |

|---|---|---|---|---|---|---|---|---|---|---|

| DXY | -2.913 | 1.645 | -0.010 | -0.007 | 0.316 | 4.558 | -0.303 | 4.517 | 3461 | 271 |

| S&P500 | -21.070 | 19.510 | 0.035 | 0.164 | 2.590 | 40.581 | -0.260 | 5.762 | 5579 | 2783 |

| Panel A: ARCH(1) predictive class | ||||||||

| Out-of-sample score | ||||||||

| Center Focused | Left Focused | Right Focused | ||||||

| LS | CRPS | FSR10% | FSR20% | FSR80% | FSR90% | |||

| Updating method | ||||||||

| DXY | ||||||||

| Exact Bayes | -0.2528 | -0.1701 | -0.2810 | -0.4113 | -0.3953 | -0.2729 | ||

| FBP | -0.2528 | -0.1689 | -0.2676 | -0.3921 | -0.3901 | -0.2692 | ||

| S&P500 | ||||||||

| Exact Bayes | -2.2984 | -1.3002 | -0.4975 | -0.8182 | -0.7209 | -0.4191 | ||

| FBP | -2.2984 | -1.2922 | -0.4661 | -0.7859 | -0.7100 | -0.4090 | ||

| Panel B: GARCH(1,1) predictive class | ||||||||

| Out-of-sample score | ||||||||

| Center Focused | Left Focused | Right Focused | ||||||

| LS | CRPS | FSR10% | FSR20% | FSR80% | FSR90% | |||

| Updating method | ||||||||

| DXY | ||||||||

| Exact Bayes | -0.1798 | -0.1664 | -0.2484 | -0.3712 | -0.3832 | -0.2660 | ||

| FBP | -0.1798 | -0.1659 | -0.2445 | -0.3656 | -0.3771 | -0.2582 | ||

| S&P500 | ||||||||

| Exact Bayes | -2.1257 | -1.2433 | -0.4251 | -0.7410 | -0.6531 | -0.3573 | ||

| FBP | -2.1257 | -1.2422 | -0.4213 | -0.7350 | -0.6510 | -0.3569 | ||

| Panel C: Mixture predictive class | ||||||||

| Out-of-sample score | ||||||||

| Center Focused | Left Focused | Right Focused | ||||||

| LS | CRPS | FSR10% | FSR20% | FSR80% | FSR90% | |||

| Updating method | ||||||||

| DXY | ||||||||

| Exact Bayes | -0.1859 | -0.1664 | -0.2559 | -0.3796 | -0.3795 | -0.2616 | ||

| FBP | -0.1859 | -0.1664 | -0.2566 | -0.3801 | -0.3791 | -0.2606 | ||

| S&P500 | ||||||||

| Exact Bayes | -2.1261 | -1.2437 | -0.4239 | -0.7397 | -0.6543 | -0.3586 | ||

| FBP | -2.1261 | -1.2428 | -0.4246 | -0.7401 | -0.6528 | -0.3575 | ||

| Panel A: Simulated dataset | Panel B: DXY | Panel C: S&P500 | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Out-of-sample exceedances | Out-of-sample exceedances | Out-of-sample exceedances | ||||||||||||

| VaR0.1 | VaR0.2 | VaR0.8 | VaR0.9 | VaR0.1 | VaR0.2 | VaR0.8 | VaR0.9 | VaR0.1 | VaR0.2 | VaR0.8 | VaR0.9 | |||

| Updating | ||||||||||||||

| method | ||||||||||||||

| Exact Bayes | 0.117 | 0.196 | 0.217 | 0.062* | 0.073* | 0.142* | 0.157* | 0.085 | 0.081* | 0.152* | 0.131* | 0.060* | ||

| FBP-CS<10% | 0.102 | 0.198 | 0.05* | 0.002* | 0.084 | 0.237* | 0.027* | 0.011* | 0.096 | 0.225* | 0.023* | 0.008* | ||

| FBP-CS<20% | 0.103 | 0.203 | 0.023* | 0.000* | 0.077* | 0.180 | 0.059* | 0.022* | 0.083 | 0.192 | 0.039* | 0.017* | ||

| FBP-CS>80% | 0.338* | 0.413* | 0.197 | 0.104 | 0.031* | 0.060* | 0.204 | 0.094 | 0.050* | 0.102* | 0.164* | 0.072* | ||

| FBP-CS>90% | 0.471* | 0.551* | 0.148* | 0.085 | 0.015* | 0.037* | 0.247* | 0.100 | 0.042* | 0.074* | 0.182* | 0.078* | ||

In the following sections we assess the relative performance of FBP and exact Bayes for these two series in terms of, respectively: average out-of-sample scores, VaR exceedances, and the average scoring function for ES proposed in Ziegel et al., (2020). For the third exercise, we assess the dominance of FBP over exact Bayes - in terms of predicting ES - by visually comparing the results using the Murphy diagrams proposed in Ehm et al., (2016).

5.1.2 Results: Average out-of-sample scores

In Table 4, we reproduce results for both the likelihood-based update (exact Bayes) and the FBP update that matches the out-of-sample accuracy measure used (as captured by the relevant scoring rule).202020The choice of for each FBP method remains as described in Section 4.1. That is, for each of the two empirical series, and for each predictive class, there is a single row of accuracy results labelled ‘FBP’, with the update underlying the FBP figure in any particular column matching the accuracy measure in the column label.

The results confirm our expectations. In Panel A, the figures based on the ARCH(1) predictive class tell a clear story: using an update that focuses on the measure that is assessed out-of-sample reaps accuracy gains. In all cases, and for both series, the exact (misspecified) Bayesian predictives are out-performed by FBP. In Panel B, FBP based on the GARCH(1,1) class continues to dominate exact Bayes uniformly; however the degree of dominance is less marked than in Panel A. The dominance of FBP over exact Bayes is no longer uniform in Panel C, for the case of the (least misspecified) mixture predictive class. Nevertheless, in all four instances, FBP still out-performs exact Bayes in the upper tail.

Hence, the empirical results mimic the patterns observed in the simulation setting, and continue to send the clear signal: when model misspecification is marked, FBP is beneficial, and particularly in terms of upper tail accuracy in the case of negatively skewed data. In the following sections we assess the practical significance of that benefit by conducting an out-of-sample assessment of the predictive VaR for period - or predictive quantile (denoted by VaRα) - and the ES (denoted by ESα), both computed from the relevant mean predictive, and for the most misspecified class only: Gaussian ARCH(1). For comparative purposes, we also perform the exercise for the simulated data analyzed in Section 4.3. Note that, for ease of notation we do not make explicit the dependence of both VaRα and ESα on a particular predictive distribution, unless this is necessary.

5.1.3 Results: VaR exceedances

To assess predictive accuracy of the VaR, for all updating methods and all return series (both empirical and simulated), we first compute the probability of ‘exceedance’, , as the proportion of realized out-of-sample values that are less than the predictive VaRα for and , as is relevant for a long portfolio. We then compute , as the proportion of realized values that are greater than the predictive VaRα for and , as pertains to a short portfolio. Table 5 reports the values of (or ), for the exact Bayes update and four different versions of FBP that focus explicitly on tail accuracy: FBP-CS<10%, FBP-CS<20%, FBP-CS>80% and FBP-CS The bold figure in each column indicates the empirical exceedance that is closest to the nominal tail probability. The asterisk then indicates whether the null hypothesis of (or ) and independence in the exceedances is rejected at the significance level by the Christoffersen, (1998) test. In this particular illustration there is, of course, no exact match between update and out-of-sample measure; however we would anticipate that the FBP methods that focus on accuracy in the lower tail would yield better predictions of VaR0.1 and VaR0.2 (and, hence, better associated performance statistics) than would both exact Bayes (with no lower tail focus) and the FBP methods that focus on accuracy in the upper tail; with the corresponding conclusions expected for upper tail focus, and accurate prediction of VaR0.8 and VaR0.9. Hence the usefulness of reproducing all five sets of results for each scenario.

Looking first at the bold figures in Table 5, a simple conclusion can be drawn: for all three series, an ‘appropriate’ form of FBP (i.e. with an update that rewards accuracy in the relevant tail) produces empirical exceedances that are closer to the nominal values than do both exact Bayes and the ‘inappropriate’ FBP (i.e. with an update that rewards accuracy in the opposite tail). By this measure, focussing correctly reaps VaR accuracy benefits for all three series. For the DXY series (Panel B) we can hone this conclusion further: the updates that focus on accuracy in a particular marginal tail (remembering that the threshold used in the CS score is based on an estimate of a marginal quantile) also yield the best empirical exceedances for the conditional VaRα with an equivalent probability. All four bold diagonal exceedances in Panel B are also insignificantly different from the nominal value, and are not associated with rejection of the null of independent violations. Indeed, with the exception of the FBP-CS>80% exceedance for FBP-CS>90%, these four diagonal figures are the only ones associated with a failure to reject the joint null of correct coverage and independent violations.

For the data simulated from (12)-(14) (Panel A), with one exception, all FBP methods that focus on the tail that is relevant for VaRα prediction - so the lower tail for VaR0.1 and VaR0.2, and the upper tail for VaR0.8 and VaR0.9 - yield statistics that fail to reject the joint null. Moreover, as is somewhat consistent with the particular dominance of FBP over exact Bayes in the upper tail illustrated in Section 4.3.1, there is a slight tendency for FBP to also be more superior to exact Bayes in terms of prediction of the upper tail VaRα’s. For the S&P500 data, the FBP methods that focus on lower tail accuracy (FBP-CS<10% and FBP-CS<20%) are the only ones that do not formally reject the joint null - when used to predict VaR0.1 and VaR However, again, in terms of raw exceedances for VaRα’s in a particular tail, the FBP methods that reward accuracy in that same tail outperform everything else.

5.1.4 Results: Murphy diagrams for ES predictions

Lastly, we compare the performance of FBP and exact Bayes in terms of the accuracy with which we predict ES. Reiterating that these results are based on the mean predictives (for both FBP and exact Bayes), for the Gaussian ARCH(1) class, this means that in the definition in equations (21)-(22), we replace with the mean predictive defined in (4), and for both FBP and exact Bayes updating.212121The lack of a closed-form solution for the mean predictive requires that ES must be estimated at each time point. Herein, ES is estimated via Monte Carlo integration based on a large number of draws from the mean predictive. We then follow Ziegel et al., (2020) and measure the out-of-sample accuracy of both forms of ES predictions using a class of scoring functions that are indexed by some known parameter , and which are consistent for the joint functional of VaR and ES. The specific details of the scoring function, as well as the definition of consistency are delayed until Appendix C.

With reference to a positively-oriented class of consistent scoring functions, Ziegel et al., (2020) say that predictive Method A, e.g. the mean predictive obtained under FBP, dominates predictive method B, e.g. the mean predictive obtained under exact Bayes, if on average predictions of ES obtained under Method A yield a score that is greater than or equal to the score that is obtained under Method B, uniformly over all scoring functions in the class (i.e., all ).222222A more formal definition of dominance is provided in Appendix C. Sampling variability aside, dominance can then be visualized using the Murphy diagram proposed in Ehm et al., (2016), which plots the average difference between the scores under Methods A and B, over the out-of-sample-evaluation period and across a range of values for . For the class of consistent scoring functions defined in Appendix C, and across a grid of values for , it is then feasible to evaluate if predictions made using FBP dominate those made under exact Bayes (when both approaches are based on the same predictive class) in terms of their accuracy in predicting ES.

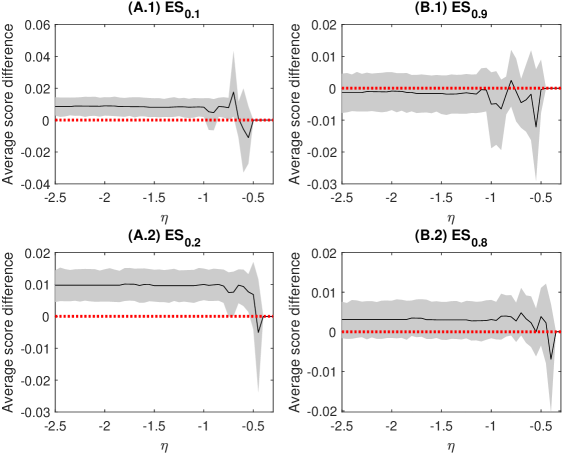

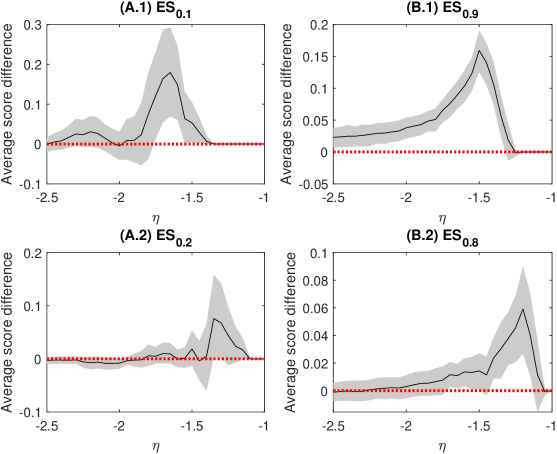

To this end, we produce and discuss Murphy diagrams for both the DXY and S&P500 return series. Panels A.1 and A.2 of Figure 5 present the Murphy diagrams for ES0.1 and ES0.2, respectively, for the DXY series. In each panel, predictions based on the ‘appropriate’ form of FBP are compared to exact Bayes. The black solid line displays the average difference (over the out-of-sample period) between the scores calculated under FBP and exact Bayes, across a grid of values for . The evaluation period used to calculate the average difference is the same as that used to compute the VaR exceedances in Section 5.1.3. The shaded region corresponds to a 95% bootstrap confidence interval for the average difference, calculated at each , based on a block bootstrap (Kunsch,, 1989) with block length of size and replications, while the red dashed line is the horizontal line at .232323We remind the reader that only sampling variability characterizes these out-of-sample computations; hence the production of a (bootstrap-based) confidence interval at each value of . From these two plots the black line indicates that, for virtually all values of , FBP outperforms exact Bayes, since the average score difference is generally positive and the confidence intervals usually do not encompass zero. This result supports the claim that FBP helps improve predictive performance in the lower tail of DXY returns. On the other hand, Panels B.1 and B.2 indicate that no such dominance is observed in terms of the upper-tail ES predictions, although in Panel B.1 the bulk of the confidence intervals do cover positive values, and the FBP forecasts are not dominated by exact Bayes in either panel.

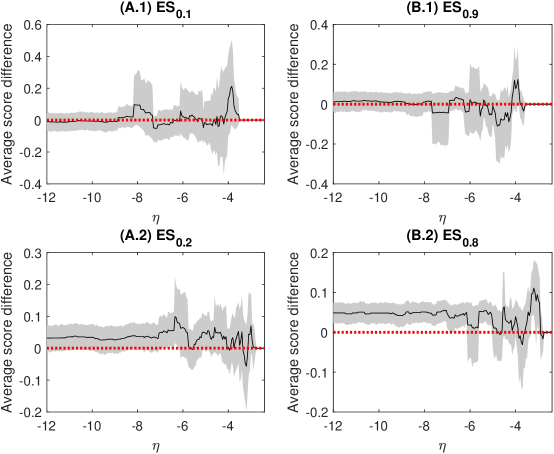

Figure 6 presents the corresponding results for the S&P500 returns. Panels A.1 and B.1 show that there is no dominance of FBP over exact Bayes for ES0.1 and ES0.9. On the other hand, Panels A.2 and B.2 show more evidence of FBP having better predictive performance than exact Bayes. In particular, in Panel B.2, for most values of FBP outperforms exact Bayes, with the average score difference being generally positive and most of the confidence intervals not encompassing zero. For completeness we also include the results for the data simulated from (12)-(14). In this case we have illustrated, in Section 4.3.3, the particular accuracy of the FBP-based ES results in the upper 10% tail (relative to exact Bayes). This finding is supported by the stark result in Panel B.1, in which virtually complete dominance of FBP over exact Bayes is on display.

| Panel A: | Panel B: |

| Lower tail expected shortfall | Upper tail expected shortfall |

|

|

| Panel A: | Panel B: |

| Lower tail expected shortfall | Upper tail expected shortfall |

|

|

| Panel A: | Panel B: |

| Lower tail expected shortfall | Upper tail expected shortfall |

|

|

5.2 M4 forecasting competition

The M4 competition was an exploration of forecast performance organized by the University of Nicosia and the New York University Tandon School of Engineering in 2018. A total of 100,000 time series - of differing frequencies and lengths - were made available to the public. Each forecasting expert (or expert team) was then to submit a vector of -step ahead forecasts, for each of the series. The winner of the competition in a particular category was the expert (team) who achieved the best average out-of-sample predictive accuracy according to the measure of accuracy that defined that category, over all horizons and all series.242424Details of all aspects of the competition can be found via the following link: M4 competition details.

One category was concerned with predictive interval accuracy, as measured by the mean scaled interval score (MSIS) proposed in Gneiting and Raftery, (2007). The MSIS formula used in the competition, defined over the % prediction interval, is given by

where denotes the longest predictive horizon considered, and denote the % and % predictive quantile, respectively, is the realized value at time , , and denotes the frequency of the data. The overall predictive accuracy according to this score was measured by the mean MSIS over the 100,000 series.