Meta-analysis of heterogeneous data: integrative sparse regression in high-dimensions

Abstract

We consider the task of meta-analysis in high-dimensional settings in which the data sources are similar but non-identical. To borrow strength across such heterogeneous datasets, we introduce a global parameter that emphasizes interpretability and statistical efficiency in the presence of heterogeneity. We also propose a one-shot estimator of the global parameter that preserves the anonymity of the data sources and converges at a rate that depends on the size of the combined dataset. For high-dimensional linear model settings, we demonstrate the superiority of our identification restrictions in adapting to a previously seen data distribution as well as predicting for a new/unseen data distribution. Finally, we demonstrate the benefits of our approach on a large-scale drug treatment dataset involving several different cancer cell-lines111Codes are available in https://github.com/smaityumich/MrLasso..

Keywords: Robust statistics, sparse-regression, meta-analysis

1 Introduction

We consider the task of synthesizing information from multiple datasets. This is usually done to enhance statistical power by increasing the effective sample size. However, as seen in many pooled studies, the inherent heterogeneity among the studies must be managed carefully. For example, in pooled genome-wide association studies (GWAS), differences in study populations and measurement methods may confound the association between the biomarkers and the outcome (Leek et al., 2010). To obtain meaningful conclusions, practitioners must properly model the heterogeneity in pooled studies.

In this paper, we consider the task of fitting high-dimensional regression models to similar, but non-identical datasets. To borrow strength across the datasets, we must distinguish between the common and idiosyncratic parts of the datasets. Let be the vector of regression coefficients for the -th dataset. Without loss of generality, we posit that the ’s are related through an additive structure:

| (1.1) |

This is a decomposition of the ’s into common and idiosyncratic parts: the global parameter represents the common part in the datasets, while the ’s represent the idiosyncratic parts. By itself, this decomposition does not identify the common and idiosyncratic parts because the decomposition is not unique: for any , and are different decompositions of the same ’s. Thus it is necessary to impose additional identification restrictions on and the ’s. Note that this identification issue is not specific to the additive decomposition (1.1); any parameterization of the ’s that introduces a global parameter (to model the common parts of the datasets) is overparameterized/underdetermined.

As we shall see, the choice of identification restriction is crucial to the efficacy of meta-analysis; an improperly defined global parameters may totally negate its benefits. For example, consider the common ANOVA identification restriction:

This restriction implies that the global parameter is the average of the ’s:

| (1.2) |

In some cases (e.g. when the ’s have disjoint supports), the global parameter can be up to -times denser than the local parameters, which negates any statistical efficiency gains from borrowing strength across the datasets. We defer a more comprehensive discussion of the inadequacies of common identification restrictions to Section 2.

In this paper, we define the global parameter as

| (1.3) |

where is a re-descending loss function (Huber, 1964). Intuitively, this definition separates into outlier and inliers and defines as the average of the inliers. Thus the definition identifies the location of the inliers as the common part of the datasets. This identification restriction is motivated by an -contamination model for the ’s:

| (1.4) |

where is the fraction of outliers, is the distribution of the inliers, and is the distribution of the outliers (among the -th regression coefficients). The two main benefits of this identification restriction are

-

1.

interpretability: if a majority of are zero, then is zero. More generally, if there is a majority value among (i.e. a common value shared by more than half of ), then is the majority value. Furthermore, if most of the local parameter coordinates are in a bulk (considered as inliers) and a few of them are significantly different (outliers), then is the average of only the inliers. This ensures that the global parameter is sparse and interpretable as the common part of the local datasets.

-

2.

statistical efficiency: can be estimated at a faster rate than the ’s. This ensures meta-analysis leads to gains in statistical efficiency.

We note that the ANOVA identification restriction does not share these two benefits.

The rest of this paper is organized as follows. In Section 2, we describe the pitfalls of several common definitions of the global parameter in integrative studies and propose a robustness-based definition to avoid such pitfalls. We design an estimator of the robustness-based global parameter in Section 3 and prove in Section 4 that it converges at a rate that depends on the total number of samples in all the datasets. Finally, we demonstrate the benefits of our approach in predicting the response of rare cancers to therapeutics with the Cancer Cell Line Encyclopedia (CCLE).

1.1 Related work

The goal of meta-analysis is borrowing strength from different datasets, and the most common approach is a two-step method in which the local parameters are first estimated from their respective datasets and then combined with (say) a fixed-effects model (Hedges and Olkin, 2014) or a random-effects model (DerSimonian and Laird, 1986). In the high-dimensional setting, we must also perform variable selection to reduce the prediction/estimation error and ensure that the fitted model is interpretable.

Gross and Tibshirani (2016); Asiaee et al. (2018) studied the case of heterogeneous linear regression models, where it is assumed that the underlying distribution of data sets are not the same. The former focuses on the prediction aspects of the problem, while the latter deals with the estimation aspects. Both papers reduce the problem of meta-analysis into a single lasso exercise, while the latter uses a version of the gradient descent algorithm to estimate parameters. Heterogeneity in the Cox model was studied by Cheng et al. (2015) where the likelihood was maximized using a suitable lasso problem. However, all these methods required the full data sets for analysis to be available on a single platform. This raises the question of communication efficiency and privacy concerns pertaining to the data sets. Cai et al. (2021) proposed a communication-efficient integrative analysis for high-dimensional heterogeneous data which addresses the issue of privacy preservation. In their two-step estimation procedure, they used lasso estimates and covariance matrices to obtain an estimator for the shared parameter, which, in a nutshell, is the average of the debiased lasso estimates.

There is a line of work on distributed statistical estimation and inference, e.g., Lee et al. (2017); Battey et al. (2018); Jordan et al. (2016), which is distinguished from our work by the additional assumption of no heterogeneity: i.e. the datasets are identically distributed. In this line of work, there are two general approaches: averaging local estimates of the parameters (Lee et al., 2017; Battey et al., 2018) and averaging local estimates of the score/sufficient statistic (Jordan et al., 2016). Although averaging the score has computational benefits over averaging the parameters, the latter is more amenable to meta-analysis because modeling the heterogeneity in the parameters is easier than modeling heterogeneity in the score.

2 Identifying the global parameter

We now quickly review the developments thus far. To distinguish between the common and idiosyncratic parts of the local parameters, we model the local parameters with an additive model:

By itself, this additive model does not identify the global parameter because the model is overparameterized. Thus it is necessary to impose additional identification restrictions to uniquely identify the global parameter. As we saw in Section 1, the choice of identification restriction is crucial to the statistical efficiency of meta-analysis. Recall we look for two properties in an identification restriction: interpretability and statistical efficiency. We describe them here again for the reader’s convenience:

-

1.

interpretability: if there is a majority value among (i.e. a common value shared by more than half of ), then is the majority value. This encourages sparsity in the global parameter because if a majority of are zero, then is zero.

-

2.

statistical efficiency: can be estimated at a faster rate than the ’s. This ensures meta-analysis leads to gains in statistical efficiency.

In the rest of this section, we show that standard identification restrictions do not satisfy the two preceding properties. After describing the inadequacies of standard identification restrictions, we present two that satisfy our desiderata.

2.1 Inadequacies of standard identification restrictions

Mean:

The usual approach to borrowing strength across heterogeneous datasets is to model the variation among the local parameters with a prior and consider the (hyper)parameter of the prior as the global parameter. The celebrated empirical Bayes approach is a prominent example. One of the simplest and most widely used priors is the Gaussian prior:

The standard estimator of is , which leads to the mean identification restriction (1.2). Unfortunately, this identification restriction does not satisfy our desiderata. Intuitively, the issue is it aggregates all local parameters in the definition of the global parameter regardless of whether a local parameter is similar to the other local parameters. This causes to lack interpretability because even a single non-zero local parameter is enough to nudge the global parameter away from zero. In the worst case (when the sparsity patterns of the local parameters are disjoint), the sparsity of the global parameter can be times the sparsity of the local parameters. This extra complexity of the global parameter negates any gains in statistical efficiency from meta analysis.

Median:

To address the sensitivity of the mean identification restriction to outliers, we consider identifying the global parameter with more robust centrality measures. One obvious choice is the median:

| (2.1) |

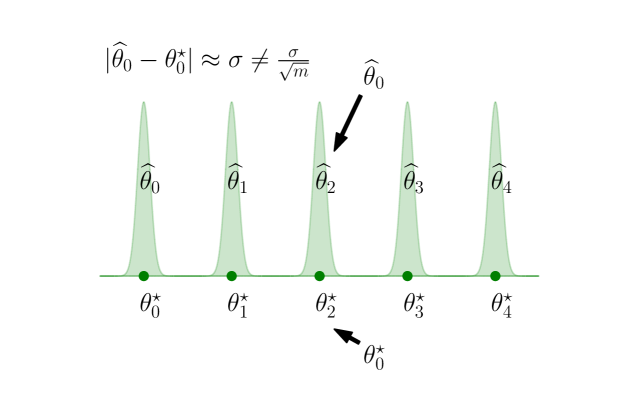

Unfortunately, in certain scenarios, the median may fail to borrow strength across datasets, making it statistically inefficient. If the local parameters are well-separated (see Figure 1), then the global parameter is one of the local parameters. In this case, it is impossible to estimate the global parameter at a faster rate than the equivalent local parameter. We provide a detailed example in Appendix A (see Example 1).

We note that Asiaee et al. (2018) and Gross and Tibshirani (2016) both considered identification restrictions similar to (2.1). In particular, they studied the estimator

where and are the features and responses in the -th dataset and is the total sample size. This estimator implicitly enforces the identification restriction

for some , which, unfortunately, suffers from a similar drawback as (2.1). We refer to Result 11 in Appendix A for the details. We note that this issue is reflected in Asiaee et al. (2018)’s theoretical results. In particular, they showed that

where is the sparsity of . If we assume , are all -sparse, then the right side simplifies to . While this is the fastest rate of convergence we expect for the left side, it suggests that the estimator of the global parameter converges at a rate that depends on the local sample size.

Huber loss:

As an alternative to the median, we consider minimizing Huber’s loss (Huber, 1964). Huber’s loss function is defined as

for some , and the global parameter is defined (coordinate-wise) as:

| (2.2) |

We hope that the quadratic part of Huber’s loss allows it to borrow strength effectively across datasets. Unfortunately, this leads to a loss of interpretability. Consider a problem in which all but one local parameter values are identically zero. It is possible to show that the global parameter is non-zero for any (see Example 2 in Appendix A).

2.2 Two interpretable and statistically efficient global parameters

The three examples presented in this subsection are hardly exhaustive. We list them here to illustrate the delicacy of the choice of identification restriction. In the rest of this section, we provide two examples of identification restrictions that satisfy our desiderata.

Both the examples have hyperparameters, that one must choose carefully, depending on the properties of the local datasets to satisfy our desiderata. At first, this seems unusual because the global parameter depends on the hyperparameters. However, the global parameter is defined by the data scientist to facilitate meta-analysis, and the hyperparameters reflect the discretion of the data scientist. Thus the dependence of the global parameter on the hyperparameters is natural. From another perspective, different values of hyperparameter lead to possible global parameters. However, not all the global parameters are interpretable and neither can they be estimated in a statistically efficient manner. We only consider global parameters that have these desirable properties.

Re-descending loss:

In this paper, we define the global parameter as the minimum of a re-descending loss function (Huber, 1964). More concretely, we consider the quadratic re-descending loss function: , and we define the global parameter as

| (2.3) |

It is possible to derive similar results for other re-descending loss functions, but we focus on the quadratic re-descending loss function here. As we shall see, is not only interpretable but also statistically efficient.

First, we check that (2.3) leads to an interpretable global parameter. The quadratic re-descending loss function has the property that its derivative vanishes outside , so (2.3) ignores any local parameters that are outside this interval. Thus local parameters that are far from the bulk of the local parameter values are considered outliers and ignored by (2.3), thereby ensuring that the global parameter is interpretable. For example, if there is a majority value among , then for a suitable choice of , (2.3) ignores all local parameters that are different from the majority value.

Second, we argue that it is possible to estimate at a fast rate. Consider as an -estimator in which the effective sample size is the number of local parameters in bulk (not considered outliers). This suggests that it is possible to estimate at a rate that depends on the number of local parameters in the bulk. As we shall see, the simple approach of replacing the local parameters with their estimates in (2.3) leads to an estimator that achieves this goal. We refer to Lemma 6 for a formal statement of a result to this effect.

We note that the choice of plays a crucial role in the interpretability and statistical efficiency of the global parameter . If is very large, then none of the local parameter values will be identified as outliers and (2.3) is equivalent to the mean identification restriction. This leads to a global parameter that is sensitive to outlier local parameters. On the other hand, if is small, then (2.3) ignores most local parameter values because it considers them as outliers. This reduces the statistical efficiency of borrowing strength across datasets because most datasets are ignored. Thus must be chosen in a way that balances interpretability and statistical efficiency.

We note that the quadratic re-descending loss has a close connection with the -contaminated model (1.4), where the inliers parameters are normally distributed:

| (2.4) |

In the absence of contamination (), it is not hard to check that minimizing the squared loss function leads to the maximum likelihood estimator for the global parameter . In the presence of outliers, we can avoid the corrupting effects of the outliers by using a robust version of the squared loss function. There are many choices of such robust loss; one such choice is a re-descending loss function (Hampel, 2005).

Quadratic + loss

As an alternative to the re-descending loss, we could also consider minimizing a convex combination of quadratic and loss functions:

| (2.5) |

This identification restriction combines the mean and the median identification restrictions, but in a different way than Huber’s loss function. It is not hard to check that this identification restriction satisfies our desiderata. The quadratic part of (2.5) allows us to borrow strength across datasets, while it is possible to pick in a way such that is interpretable. For example, if all but one of the local parameters are zero, it is possible to pick large enough so that the global parameter is zero, in contrast to the Huber loss function. That said, we focus on the re-descending loss here because it has better empirical performance (see Section 5).

3 Communication-efficient data enriched regression

In this section, we suggest a privacy-preserving communication-efficient estimator for the global parameter which borrows strength over different datasets. The privacy concern limits us to communicate with the datasets only through some summary statistics. So, the high-level idea to estimate is to start with some estimator of the local parameters computed from the datasets. Then the global parameter is estimated only using local estimates, without any further communication among datasets.

We describe the debiased lasso estimator for local parameters in the set-up of regularized M-estimators. The case of the linear regression model can be considered as a special case. Let be a loss function, which is convex in , and , be its derivatives with respect to . That is

Define , where the sum is only over the pairs on dataset . The lasso estimator for local parameter is given by

| (3.1) |

Since averaging only reduces variance, not bias, we gain (almost) nothing by averaging the biased lasso estimators. That is, the MSE of the naive average estimator is of the same order as that of the local estimators. The key to overcoming the bias of the averaged lasso estimator is to “debias” the lasso estimators before averaging.

The debiased lasso estimator as in van de Geer et al. (2014) is

| (3.2) |

where is an approximate inverse of . The choice of in the correction term crucial to the performance of the debiased estimator. In particuar, must satisfy

One possible approach to forming , as in van de Geer et al. (2014), is by nodewise regression on the weighted design matrix , where, is the design matrix for -th dataset, defined as and is diagonal matrix, whose diagonal entries are

That is, for that machine is debiasing, the machine solves

| (3.3) |

and forms

| (3.4) |

where

After calculating the debiased lasso estimators in local datasets, the integrated estimator is obtained using similar optimization problem as in (2.3). -th co-ordinate of the integrated debiased lasso estimator is obtained as

| (3.5) |

where, ’s used in the above equation are the same ones that are used to identify the global parameter. The integrated estimator calculated in (3.5) has a serious drawback. Loosely speaking, the use of quadratic re-descending loss to define gives us the co-ordinate wise mean of debiased lasso estimates, after dropping the outlier values. Since the debiased estimates are no longer sparse, is also dense. This detracts from the interpretability of the coefficients and makes the estimation error large in the and norms. To remedy both problems, we threshold Below we describe the hard-threshold and soft-threshold on :

| (3.6) | ||||

The final estimator is obtained by hard-thresholding or soft-thresholding at where, i.e., and the final estimators for ’s are obtained by hard-thresholding or soft-thresholding at a level i.e., or

A step by step process to obtain the global estimator for linear regression models is described in Algorithm 1. The Algorithm requires suitable choices of the parameters , and . In our numerical studies we pick these choices via the cross-validation approach, described in Algorithm 2. If appropriate choices of ’s are available from background knowledge then one can use those instead of picking them from cross-validation. In practice, cross-validating over might be computationally challenging since there are many unknown parameters for local datasets and as the covariate dimension; and specifically can be quite large. In our experiments we further simplify the choice by assuming ’s have equal value and . This simplifies the cross-validation parameters to just two parameters .

4 Theoretical properties of the communication-efficient estimator

To present the theoretical justification of consistency of the estimators we shall focus on and consistency of the estimators. Before getting into the assumptions and results, we first define some notations. We use , , and to denote usual -norm, -norm, and -norm respectively.

The performance of global estimator depends on the debiased lasso estimators from the local datasets. Hence, it is important to have a reasonable performance for local estimators. We study the error rate of the debiased lasso estimator for the parameter calculated form the dataset For a random vector , whose distribution is parametrized by we assume that is uniquely minimized at As before, the debiased lasso estimator is defined as where, for and is calculated according to (3.4). We assume that the actual parameter value is sparse, i.e., has many non-zero entries. Letting we assume the -th row of , which is denoted as is -sparse. Denote . We make the following assumptions on distributions of local datasets. These assumptions establish high probability bounds for the local debiased lasso estimates.

Assumption 1

Under the M-estimation setup, we assume the following.

-

1.

The pairs are iid and for some and the projection of on the row space of in the inner product is bounded: for any where

We define as

-

2.

It holds that

-

3.

The smallest eigenvalue of is bounded away from zero, and moreover,

-

4.

There exists a such that for any that satisfies it holds that stay away form zero and that . Furthermore, for any such and all

-

5.

With probability at least we have and .

-

6.

The derivative exists for all and for some -neighborhood, is locally Lipschitz: for some

Moreover,

-

7.

The diagonal entries of are bounded by .

The list of conditions in Assumption 1 are standard ones to establish convergence for the debiased lasso estimator and are adapted from (van de Geer et al., 2014, Assumptions (D1)-(D5)) and (Lee et al., 2017, Assumptions (B1)-(B7)). Condition 5 that directly assumes convergence of estimation and prediction error for lasso is implied by the other assumptions. We refer to (Bühlmann and Van De Geer, 2011, Chapter 6, Section 6.7) for the details, where the necessary compatibility condition is inherited from the condition 3. Here we state this to simplify the exposition. We refer to the corresponding literature (specifically Lee et al. (2017)) for further discussions about the conditions.

In the literature on debiased lasso for high-dimensional M-estimation, it is usually assumed that (see (van de Geer et al., 2014, Section 3.3.1), (Lee et al., 2017, Section 5)). For sub-gaussian covariates one can use a high-probability bound of the order . The high probability bound for local debiased lasso estimate follows.

Lemma 2

Under Assumption 1 the debiased lasso estimator satisfies the following high probability bound.

| (4.1) |

Remark 3

Under the Assumption 1 and we have a high probability bound

Before studying the theoretical properties of the integrated estimator defined in (3.5) one might notice that the identification restriction (2.3) may not lead to a unique global parameter, in general. The whole business of studying the theoretical properties of the global estimator is not meaningful if one cannot uniquely identify the global parameter. Hence, it is necessary to make some assumptions about the parameter values, with the goal that they will suffice unique identification of the global parameter. Here, we present the assumptions on the finite number of machines to have a uniquely identified parameter. For we assume

Assumption 4

-

(B1)

Let be the set of indices for ’s which are considered as inliers. We assume .

-

(B2)

Let Let be the smallest positive real number such that for all We assume that none of the ’s are in the intervals or

-

(B3)

Let is the minimum separation between inliers and outliers. Clearly, We choose such that

The Assumption 4 sets a co-ordinate wise clustering assumption for the local parameters. A visualization summary of the cluster Assumption 4 is seen in Figure 2. The conditions ensure enough separation between the bulk and the outliers such that the re-descending loss (2.3) uniquely identifies the global parameter at mean of the bulk values, as suggested by Result 5.

Result 5

Under the Assumption 4 the objective function has a unique minimizer

Result 5 implies that under the Assumption 4 the global parameter is uniquely identified at the mean of the inlier parameter values. This has the following nice implications: (1) the global parameter is not affected by outlier values; (2) the estimator of the global parameter can effectively borrow strength across datasets with inlier parameter values. The Lemma 6, where we study the coordinate-wise convergence rates for , is a step toward establishing effective borrowing strength for the estimator of global parameter.

Lemma 6

Let the following hold:

Then for sufficiently large we have the following bound for the co-ordinates of and bound for :

| (4.2) |

with probability at least

Condition in lemma 6 is needed to identify the global parameter uniquely, as suggested by Result 5. Condition provides a high probability bound for the local debiased lasso estimates (see lemma 4.1). Finally, the condition ensures the bias in local debiased estimates is of smaller order than the variance in integrated estimate. Since the bias term may not improve under averaging, violating this condition would result in higher-order for the bias in local estimates, and the estimation error for the global parameter stops improving (with a higher number of datasets).

In the following remark we introduce a weighted version of our data integration method (3.5).

Remark 7 (A weighted integration)

One may also consider a weighted version of the data integration

| (4.3) |

where is the weight corresponding to -th dataset with . In that case the uniqueness of the corresponding global parameter

| (4.4) |

at the value is established (in Result 17) by considering a weighted version of Assumption 4 (see Assumption 16) where we replace by in condition (B1), and let in condition (B2). Furthermore, under conditions (ii) and (iii) in Lemma 6, one can establish (see Theorem 18) the following high probability bound for :

Further details about the setup are provided in Appendix C.

An interesting special case arises when , and the above rate simplifies to and yields the fastest rate among all possible weights:

Note that the rate is faster than the corresponding one in (4.2), especially when the ’s are significantly different. The downside to the weighted formulation is that the corresponding structural assumptions on the local parameter values depends on the sample size, which can be perceived as strange.

Proof Here we shall provide a brief outline of the proof of Lemma 6. The detailed proof of this lemma is provided in appendix B. We start with the Remark 3, which gives us a high probability error bound for the individual local lasso estimators. From condition we see that the ’s satisfies Assumption 4. As long as concentrates around , also satisfies Assumption 4 (with different and ’s but identical ’s). Using Result 5 we see that the integrated estimator has the form

Finally, we use the decomposition on the individual lasso estimators in Lemma 12 and concentration bound for sums of independent random variables to get a high probability bound for the estimation error of

Before we study the theoretical properties of the thresholded estimators, we would like to make a few remarks about the rates of convergence for the coordinates of If there is reason to believe that none of the local parameters are outliers and we consider ’s large enough, then the global parameter is identified as mean of the local parameters, i.e. In that case, the rate of convergence for in Lemma 6 simplifies to:

where, implies with probability converging to This kind of rate is not surprising. Probably the simplest situation, under which this kind of convergence rate arises is ANOVA model. Let is a set of independent random variables, such that where are some real numbers. Under the assumption the estimator , where, follows distribution This gives us the following convergence rate for

We notice that and the equality holds when ’s are equal, which gives us the best possible rate. In this case the rate simplifies to:

Let and Notice that Hence, we can get the following simple (possibly naive) high probability bound for

The estimators in Lemma 6 are dense, they have higher and error. We threshold the estimators at a suitable level. The thresholding is usually done at a level of the error rate of the estimator. We recall the following result from Lee et al. (2017) which ensures probability convergence for such thresholding.

Lemma 8 (Lee et al. (2017), Lemma 11)

As long as satisfies the following.

-

1.

-

2.

-

3.

where, is the sparsity of The analogous results holds for

A combination of the Lemmas 6 and 8 establishes the rate of convergence for the estimates of global and heterogeneous effect parameters.

Theorem 9

Define Assume that the threshold for is set at and for ’s are set at respectively. Then under the conditions in Lemma 6 and for sufficiently large we have the following:

-

1.

-

2.

-

3.

-

4.

-

5.

-

6.

where, for a vector denotes its sparsity level.

It is not necessary to threshold all the co-ordinates of at a same level. Thresholding the -th co-ordinate of at may give us a faster rate of convergence for in terms of and errors. If one wish to use cross-validation to determine an appropriate choices of thresholding, setting different thresholding level for different co-ordinates may be computationally hectic. For computational simplicity, we consider same thresholding level for all the co-ordinates.

5 Computational results

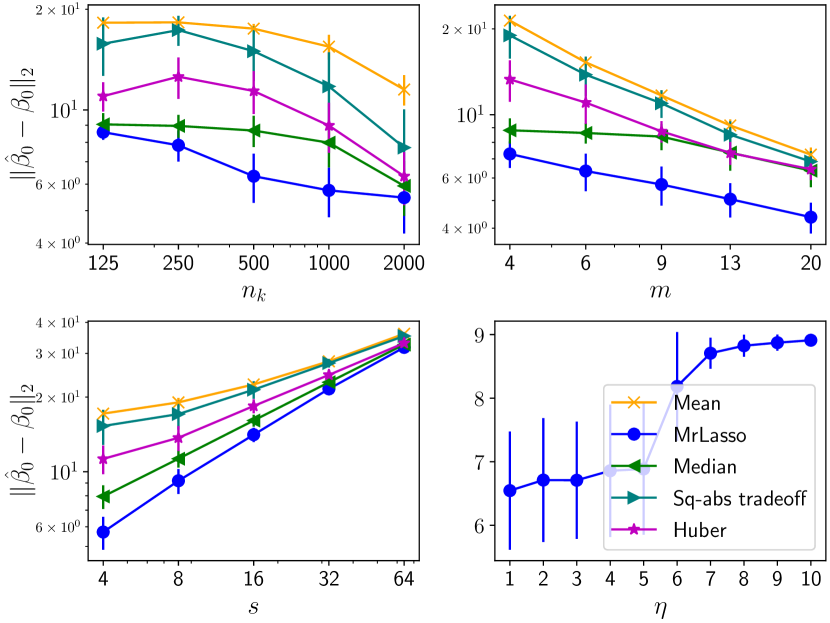

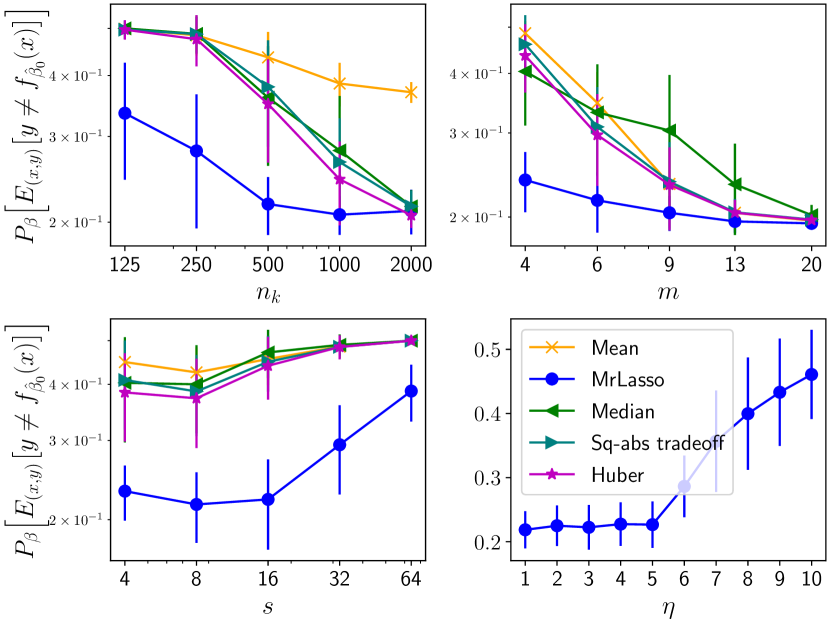

In this section, we compare the performance of MrLasso to several other global parameters considered in Section 2 on simulated data: the Mean (1.2), the Median (2.1), the square and absolute error trade-off in (2.5) and the Huber estimator in (2.2). The datasets are generated from a linear model with covariates. In our simulation, the covariates are generated from auto-regressive model (, , , and ) with the correlation , and the response in the -th local dataset is generated as

where is the vector of regression coefficients for the -th dataset. The first co-ordinates of ’s are independent random scalars. The next 20 coordinates of are drawn from the mixture distribution , where is the degenerate distribution at zero. This endows the local coordinates with the cluster structure of Assumption 4. This structure in the local coordinates highlights the difference between the identification restrictions in MrLasso and the other estimators.

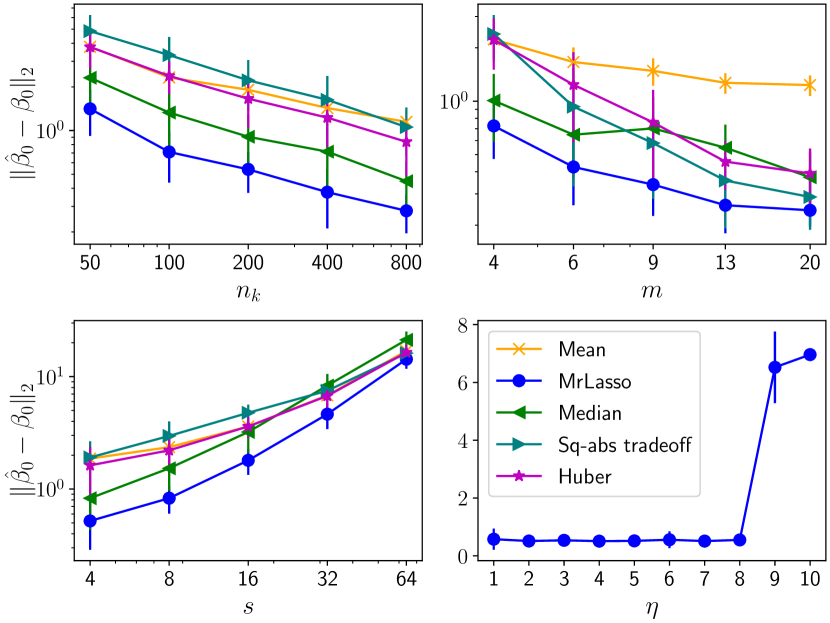

Note that the definition MrLasso, square and absolute loss trade-off and Huber loss require additional tuning parameters. In the simulation, we hold out of the dataset as a validation set and we pick those parameters to minimize test error on the validation set. The data dependent choice of tuning parameters are used to define the global parameters for square and absolute loss trade-off and Huber loss to keep the comparison fair, whereas for MrLasso the global parameters are identified with oracle tuning parameter values. The upper left plot in Figure 3 shows the -estimation error of the global parameter with respect to the sample size for each dataset (). We fix the number of datasets () at 5 and the sparsity of the MrLasso global parameter () at . Note that the global parameters are different for different identification restrictions. The convergence rate of MrLasso is faster than the others. For denser global parameters, the performance discrepancy between the estimators reduces. We see this behavior in the lower-left plot of Figure 3.

A study on the effect of for fixed and is presented in the upper right plot of Figure 3. All the estimates are able to borrow strength across datasets (-error decreases for higher ) but MrLasso produces lower -errors than others.

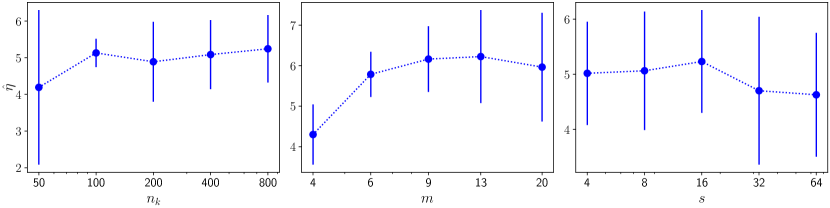

In the lower right panel of Figure 3 we study the sensitivity of MrLasso to the misspecification of . As seen in the plot, MrLasso produces a good estimate of the global parameter as long as falls within a reasonable range. This range depends on the separation between the bulk and outlier local coordinates (see Assumption 4, condition (B3)). The plot also suggests that (cross-)validation leads to a value of that falls in this range. We confirm this in Figure 4, which shows the chosen values of for the simulations in Figure 3.

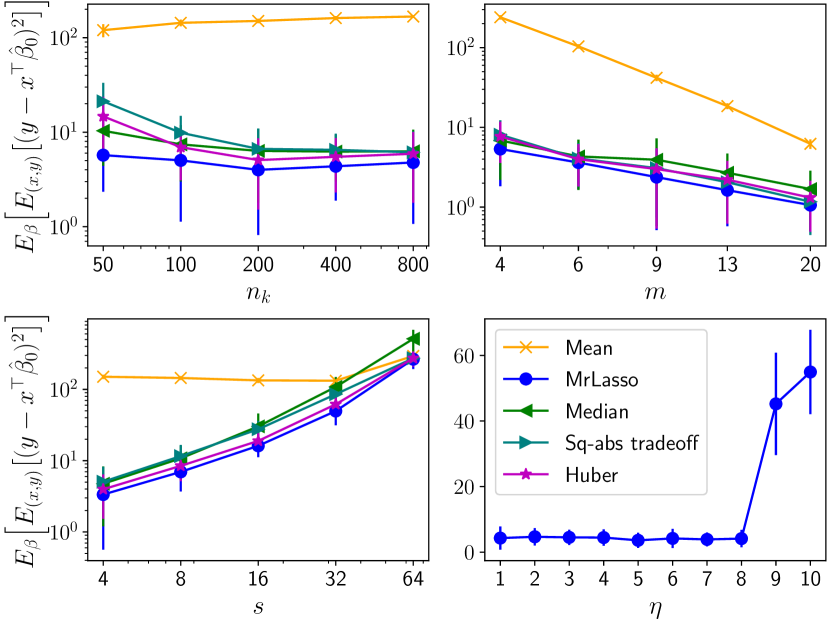

The errors in Figure 3 are calculated in terms of the corresponding global parameters of the estimators, but the global parameters are different. We complement this experiment by evaluating the prediction error of them on a test dataset that is generated without any outlier local regression coefficients. In particular, the first coordinates of the local regression coefficient vectors are generated independently from , while the rest of the coordinates are zero. In this setup, we expect the MrLasso global parameter to be closer to the population global parameter because it correctly identifies the coordinates of all but the first coordinates as zero. This is confirmed in Figure 5.

We finally note that our method is both privacy-preserving (no raw data is sent) and communication efficient (only scalars and vectors are sent). Even the model selection protocol for can be carried out without having to send the raw data: we only need to transfer scalars and vectors. We first send the local debiased estimates to the central machine to calculate and ’s for several choices of ’s. These estimates are sent back to the local machines to calculate prediction error on the holdout datasets. Finally these errors can be transferred back to the global machine to determine the choice of

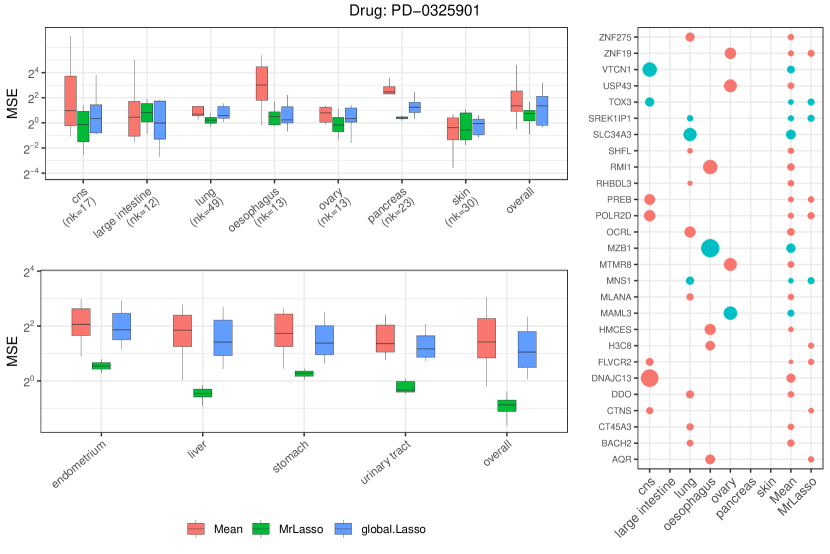

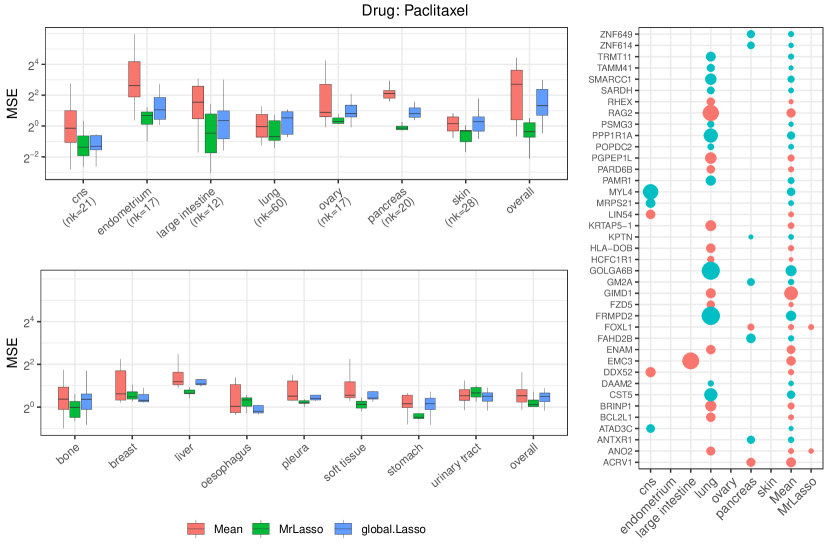

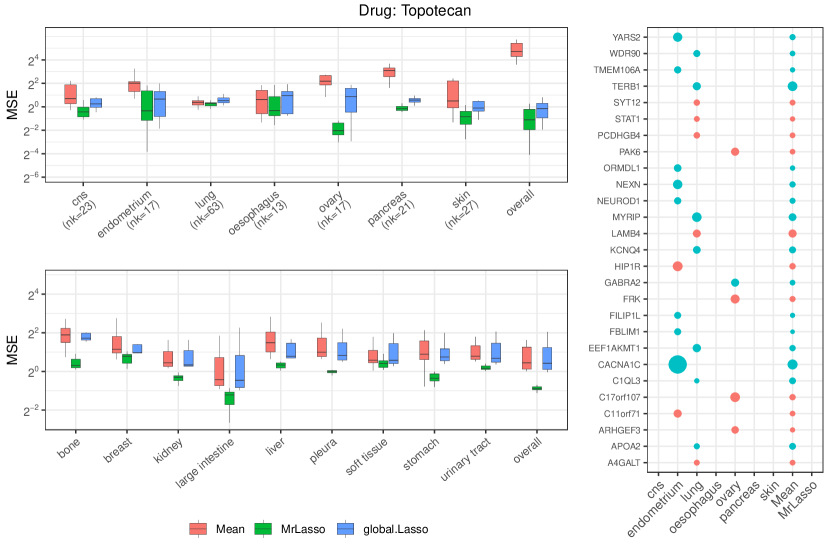

6 Cancer cell line study

The Cancer Cell Line Encyclopedia is a database of gene expression, genotype, and drug sensitivity data for human cancer cell lines. We use our method to study the sensitivity of cancer cell lines to certain anti-cancer drugs. We treat the area above the dose-response curve as the response variable (Barretina et al., 2012) and use expression levels of approximately genes () as features. More details about data source and pre-processing are provided in Appendix E. After prepossessing we have 482 cancer cell lines. Each of these cell lines comes from a cancerous organ and corresponds to a specific cancer type. The lines are divided into different machines () according to cancer types. For a given drug, our goal is to obtain a single regression coefficient vector which can be used to predict the response of different cancer types to that drug. We fit our model on the more common cancer cell types 222The number of local datasets () that are used in meta-analysis is same as the number of common cancer cell types shown in the upper left panel of the corresponding figures (for example the drug PD-0325901 has as seen in Figure 6), where the number of data-points (’s) in each of these common cancer types are also shown in the upper-left panel. with at least 10 samples and evaluate the prediction accuracy of the models on rare cancer types (those with less than 10 samples). The performance of three models are presented: soft thresholded mean of the local estimators (which we call Mean), the soft thresholded version of our integrated estimator (as in section 3), and a global lasso estimator that simply fits the lasso to an aggregate dataset consisting of samples from all common cancer types.

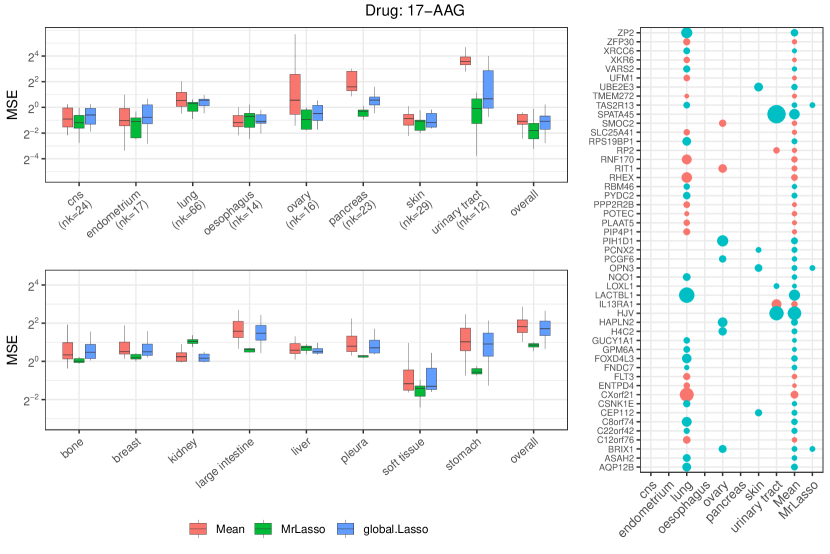

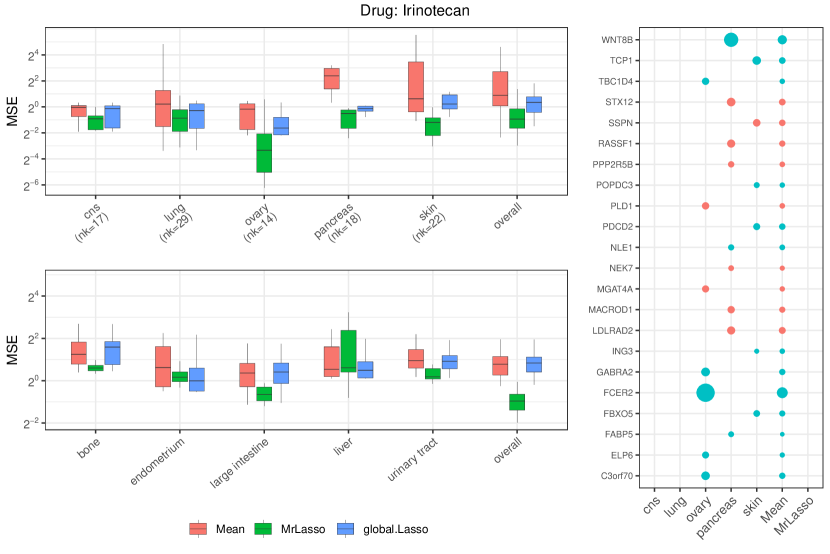

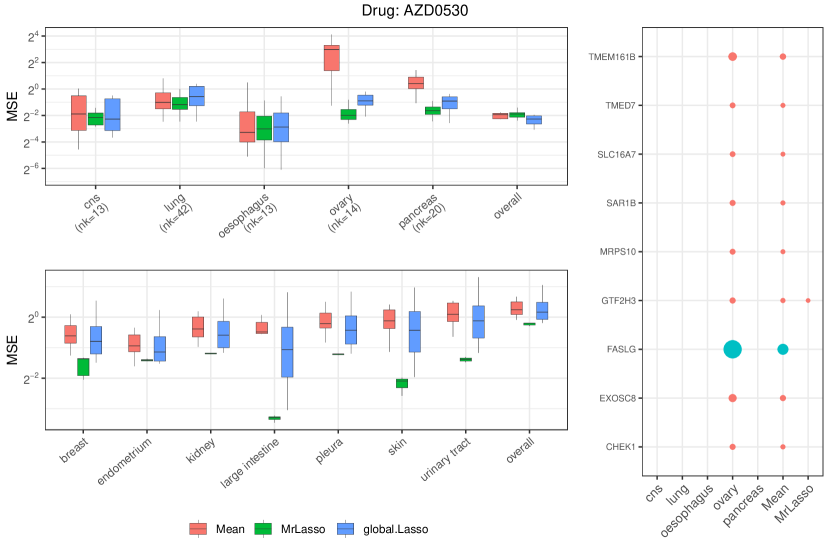

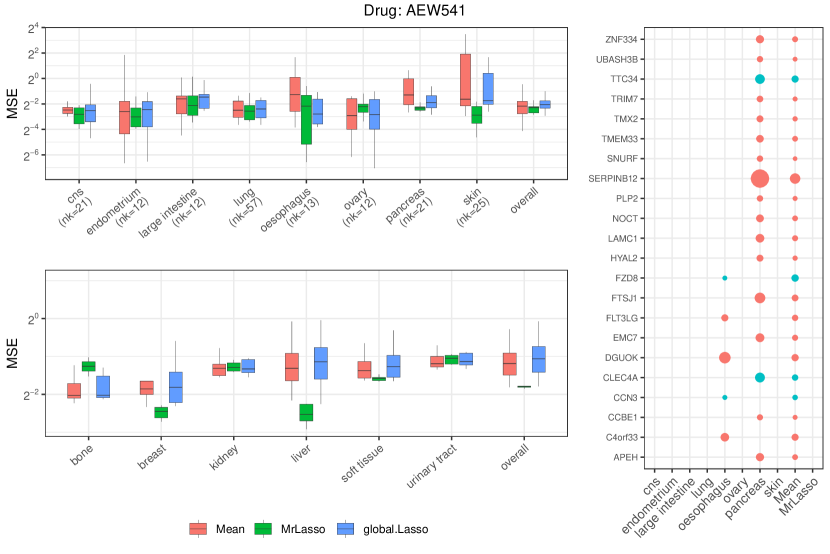

For integration purposes we first need to calculate the de-biased lasso estimate from each of these frequent cancer types. The regularization parameter for each of these cancer types is chosen using 7 fold cross-validation. After calculating the debiased lasso from each dataset, Mean is obtained by soft-thresholding their average, with the level of thresholding determined via 10 fold cross-validation. To calculate MrLasso, we assume that the parameters are identical over the gene expressions. Besides determining this common parameter we also require a proper soft-threshold level () for the integrated estimator. To this end the appropriate pair is again chosen via cross validation (see the discussion in last paragraph of Section 3). We compare the performances of the Mean, the MrLasso and the global lasso (obtained using combined data over the most-frequent cancer types with best regularization parameter chosen via 10-fold cross-validation) for drugs PD-0325901 (Figure 6), Paclitaxel (Figure 7) and Topotecan (Figure 8).

To evaluate the efficacy of this approach, we fit the global parameter using Mean, MrLasso, and a global lasso on the more common cancer types and evaluate its predictive accuracy on rare cancer types. The lower left panels in Figures 6, 7 and 8 give comparative plots for the prediction accuracy of drug-response of the three global parameter estimates (for the three drugs). The plots for several other drugs are provided in Appendix E. For completeness, we also evaluate the predictive performance of the fitted global parameters on held out data from the more common cancer types in the top left panels.

We see that the predictive performance of MrLasso is generally superior to that of Mean and the global lasso. This is mostly due to the heterogeneity in the relationship between drug sensitivity and genotype on different cancer types, as evinced by the considerable variation between the effect sizes of genetic variants on drug sensitivity from cancer to cancer: see for example, Figures 6, 7 and 8. This causes the global parameter fitted by the Mean to be considerably denser than the global parameter fitted by MrLasso. In other words, the Mean pools effect sizes across all cancer types regardless of whether the effect sizes are similar. This causes the global parameter fitted by the Mean to pick up many small effect sizes that are specific to certain cancer types, thereby detracting from the generalizability of the global parameter to other (rare) cancer types. On the other hand, MrLasso only aggregates effect sizes when the data suggests they are similar. In other words, the global parameter fitted by MrLasso only incorporates effects that persist across cancer types. This leads to a parameter whose prediction performance generalizes across cancer types. In some extreme cases (e.g. Figure 8), the effect sizes are so dissimilar that MrLasso does not borrow strength at all, but the Mean continues to pool the effect sizes. This leads to overall poor prediction performance. In comparison with Mean, we see that MrLasso can automatically adapt to the intrinsic level of heterogeneity across datasets, leading to a better generalization.

7 Discussion

We consider integrative regression in the high-dimensional setting with heterogeneous data sources. The two main issues that we address are (i) identifiability of the global parameter, and (ii) statistically and computationally efficient estimator of the global parameter. In many prior works on integrative regression in high dimensions, there is either no global parameter or a global parameter that is not properly identified (see Section 2 for a discussion of global parameters in prior work).

We suggest a way to identify the global parameter that addresses some of the drawback of prior approaches by appealing to ideas from robust location estimation. The main benefit of our suggestion is it is possible to estimate the global parameter at a rate that depends on the size of the combined dataset. We also proposed a statistically and computationally efficient estimator of the global parameter. By statistically efficient, we mean the estimation error vanishes at a rate that depends on the size of the combined datasets. By computationally efficient, we mean the communication cost of evaluating the estimator depends only on the dimension of the problem and the number of machines. Further, because no individual samples are communicated between machines, evaluating the proposed estimator does not compromise the privacy of the individuals in the data sources.

References

- Asiaee et al. (2018) A. Asiaee, S. Oymak, K. R. Coombes, and A. Banerjee. High Dimensional Data Enrichment: Interpretable, Fast, and Data-Efficient. arXiv:1806.04047 [cs, stat], June 2018.

- Barretina et al. (2012) J. Barretina, G. Caponigro, N. Stransky, K. Venkatesan, A. A. Margolin, S. Kim, C. J. Wilson, J. Lehár, G. V. Kryukov, D. Sonkin, et al. The cancer cell line encyclopedia enables predictive modelling of anticancer drug sensitivity. Nature, 483(7391):603–607, 2012.

- Battey et al. (2018) H. Battey, J. Fan, H. Liu, J. Lu, and Z. Zhu. Distributed testing and estimation under sparse high dimensional models. Annals of statistics, 46(3):1352, 2018.

- Bühlmann and Van De Geer (2011) P. Bühlmann and S. Van De Geer. Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media, 2011.

- Cai et al. (2021) T. Cai, M. Liu, and Y. Xia. Individual data protected integrative regression analysis of high-dimensional heterogeneous data. Journal of the American Statistical Association, pages 1–15, 2021.

- Cheng et al. (2015) X. Cheng, W. Lu, and M. Liu. Identification of homogeneous and heterogeneous variables in pooled cohort studies: Identification of Heterogeneity in Pooled Studies. Biometrics, 71(2):397–403, June 2015. ISSN 0006341X. doi: 10.1111/biom.12285.

- Consortium et al. (2015) C. C. L. E. Consortium, G. of Drug Sensitivity in Cancer Consortium, et al. Pharmacogenomic agreement between two cancer cell line data sets. Nature, 528(7580):84, 2015.

- Corsello et al. (2019) S. M. Corsello, R. T. Nagari, R. D. Spangler, J. Rossen, M. Kocak, J. G. Bryan, R. Humeidi, D. Peck, X. Wu, A. A. Tang, et al. Non-oncology drugs are a source of previously unappreciated anti-cancer activity. BioRxiv, page 730119, 2019.

- DepMap (2021) B. DepMap. DepMap 21Q2 Public, May 2021.

- DerSimonian and Laird (1986) R. DerSimonian and N. Laird. Meta-analysis in clinical trials. Controlled clinical trials, 7(3):177–188, 1986.

- Gross and Tibshirani (2016) S. M. Gross and R. Tibshirani. Data Shared Lasso: A novel tool to discover uplift. Computational Statistics & Data Analysis, 101:226–235, Sept. 2016. ISSN 01679473. doi: 10.1016/j.csda.2016.02.015.

- Hampel (2005) F. R. Hampel, editor. Robust Statistics: The Approach Based on Influence Functions. Wiley Series in Probability and Mathematical Statistics. Wiley, New York, digital print edition, 2005. ISBN 978-0-471-73577-9. OCLC: 255133771.

- Hedges and Olkin (2014) L. V. Hedges and I. Olkin. Statistical methods for meta-analysis. Academic press, 2014.

- Huber (1964) P. J. Huber. Robust Estimation of a Location Parameter. The Annals of Mathematical Statistics, 35(1):73–101, Mar. 1964. ISSN 0003-4851, 2168-8990. doi: 10.1214/aoms/1177703732.

- Jordan et al. (2016) M. I. Jordan, J. D. Lee, and Y. Yang. Communication-Efficient Distributed Statistical Inference. arXiv:1605.07689 [cs, math, stat], May 2016.

- Lee et al. (2017) J. D. Lee, Y. Sun, Q. Liu, and J. E. Taylor. Communication-efficient sparse regression: A one-shot approach. Journal of Machine Learning Research, 18, Jan. 2017.

- Leek et al. (2010) J. T. Leek, R. B. Scharpf, H. C. Bravo, D. Simcha, B. Langmead, W. E. Johnson, D. Geman, K. Baggerly, and R. A. Irizarry. Tackling the widespread and critical impact of batch effects in high-throughput data. Nature Reviews Genetics, 11(10):733–739, Oct. 2010. ISSN 1471-0064. doi: 10.1038/nrg2825.

- van de Geer et al. (2014) S. van de Geer, P. Bühlmann, Y. Ritov, and R. Dezeure. On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics, 42(3):1166–1202, June 2014. ISSN 0090-5364. doi: 10.1214/14-AOS1221.

Appendix A Identifiability

Lemma 10 (Contaminated normal model)

Let

where and is continuous density of contamination distribution. The expected redescending loss is minimized at if

and

where and are density and distribution functions of standard normal distribution.

Proof We note that

Here

where From the first order Taylor expansion

If is the density of then

From the requirement that

for any arbitrarily small , we have the lemma.

Example 1

Consider an one dimensional case where we have datasets each of size The local parameters of these datasets take the values for In this case the global parameter will be identified as Suppose we have some estimators for the local parameters which can be written as and for simplicity we assume are normal random variables with mean zero standard deviation The example can also be extended for sub-Gaussian random variables.

The parameter depends on the variances of observations. For simplicity we assume that is For some if sample sizes for each datasets then by union bound over sub-Gaussian inequality we get

We can see that with probability at least the local estimators are ordered as . Let this event be A natural choice for is the median of ’s under the identification condition (2.1). Clearly, under the event is and hence we have As is , we see that

For a fixed the above probability is larger than whenever This is a contradiction to the fact that rate of convergence for to is

Example 2

Let and For any choice of as defined in (2.2) is never zero.

Proof Define

Since

we note that

for and , we have

| (A.1) |

Note that is can never be zero, which concludes that the minimum is never achieved at zero.

Result 11

Suppose the covariate dimension is fixed. Assume

-

1.

-

2.

are same over different ’s,

-

3.

’s are invertible,

-

4.

has a unique minimizer

Define

for some independent of Then

in probability, with respect to norm, where, and

This result can be shown for any norm in

Proof Define

and

where, We define to be the closed ball around with radius Since, for each and is finite, in probability.

For any

So, by argmin continuous mapping theorem

in probability. Taking the radius we get

As Hence, in the minimization problem of becomes more and more important, and in the limiting case this becomes primary objective. Looking at the loss for primary objective we see that optimum achieved at for which for all Hence, where,

Appendix B Supplementary Results

Lemma 12

Under the Assumption 1 the followings hold.

-

1.

The debiased lasso estimator can be decomposed as

where, for and some ,

-

2.

For some

-

3.

There is some such that hold for any

Proof of Lemma 12. For the proof of 2. readers are suggested to see Theorem 3.2. in van de Geer et al. (2014).

Denote . To verify 1. we start with the Taylor expansion of :

where, is some number between and and We give a high probability bound for By triangle inequality

From KKT condition for nodewise lasso we get

where, This implies

Now

Hence This implies

By van de Geer et al. (2014), Theorem 3.2,

with probability at least Thus and by 6. in the Assumption 1

where, denotes with probability at least

We turn our attention to We see that

Again by van de Geer et al. (2014), Theorem 3.2,

which, by 1. in the Assumption 1 and van de Geer et al. (2014), Theorem 3.2,

From 3. in the Assumption 1 that the minimum eigen-value of is bounded away from zero for all we get that, for some which doesn’t depend on the largest eigne-value of Hence,

This shows 3. in lemma 12

From the fact that is the unique minimizer of we get

Using 3. in lemma 12 and 7. in the Assumption 1 we have for some Using Bernstein’s inequality we get,

where, For we get sub-Gaussian bound

By union bound

where, Setting we get Since, for sufficiently large we have such a choice for is justified.

Since, is bounded and zero mean random vectors, we get the following high probability bound for

Let the event that the followings hold:

-

1.

-

2.

-

3.

-

4.

Then Under the event We also notice that

Hence,

Proof of Result 5. We shall prove uniqueness of the global parameter for each co-ordinates separately. Fix For simplicity of the notation we ignore the index and denote and, as and, respectively.

For let us define and

When we have

which is uniquely minimized at

Under the case we must have We consider the case implies either is larger or smaller than ’s which are in . We assume that for all The other case will follow similarly. In that case,

for all where Since, we have

Notice that, for we have whenever Hence,

where the last inequality follows form the fact that for

Now, consider the case under which we have

Then

and

Since, the range of is less than we have This implies

and hence, is the unique minimizer in this case.

Proof of Lemma 6.

We start with remark 3 that under the assumption for sufficiently large we have

with probability at least By union bound, with probability simultaneously for all we have

If for all then there exists and such that the following holds,

Let where, is the indicator function over the set From Lemma 12

Hence,

To bound we notice that are zero mean random variables bounded by By Bernstein inequality,

where Let For we get a probability bound with subgaussian tail

Letting we get

with probability at least Taking union bound over all co-ordinates we get the above bound for each co-ordinates with probability at least

We shall apply Bennett’s concentration inequality 15 on Fix some For define and Then and where, from assumption (A5). Also, Let us define Now we apply Bennett’s inequality 15 on We notice that for we have the following bound:

For we get

We need to confirm that such a choice of is valid, i.e., or for some independent of and We notice that

and hence,

From assumption we get that asymptotically goes to infinity. Hence, such a choice of is valid.

We notice that is dependent of We define

To get a bound for we see that and We also notice that are mean zero bounded random vectors. Hence, by Bernstein inequality we can show that for sufficiently large ’s we can get a bound

with probability at least Hence, by union bound we get

with probability at least

Again by union bound, we get

| (B.1) |

with probability at least where is some constant. Since, for some from assumption we get Hence, for sufficiently large , the above high probability bound reduces to

with probability at least

Under the assumption we have which gives us the first result.

For the second inequality we get a bound for each of the form:

with probability at least Form the above bound and (B.1) we get

hence, for sufficiently large ’s, we have

with probability at least

Result 13

For each let where Then the assumptions 4 are satisfied for for , and

Proof

Let Consider the same as in assumption 4, Let Notice that for we have We further notice that

This implies assumption 4, and are satisfied with and

Result 14 (Bernstein’s inequality)

Let be independent random variables with Suppose for some and the following holds for all

Then for any and the following holds:

Lemma 15 (Bennett’s Inequality)

Let be independent random variables such that (1) (2) and (3) Then for any and for any

where

Proof Without loss of generality assume Let Set Then

For any

Hence

Therefor

By Markov’s inequality

We have to minimize

(1) Consider the case Then minimization with respect to gives us Since the minimum attains at under the condition we have Hence, for we get the upper bound

(2) Consider the case of This implies Then Choose such that Then Also from we get which gives us Hence, for we get the upper bound

So, there is an overlap in the interval under which we get both the tails. We just choose

Appendix C A weighted data integration

In this section we consider a setup of weighted data integration where the weight () are applied in integration step the debiased lasso estimators:

| (C.1) |

The corresponding global parameter is identified via weighted re-descending loss:

| (C.2) |

and the unique identification of such global parameter is guaranteed by a similar set of structural conditions as in Assumption 4. We state the conditions below:

Assumption 16

-

(P1)

Let be the set of indices for ’s which are considered as non-outliers. We assume .

-

(P2)

Let Let be the smallest positive real number such that for all We assume that none of the ’s are in the intervals or

-

(P3)

Let Clearly, We choose such that

Result 17

Under the conditions (P1)-(P3) in Assumption 16, the objective functions is uniquely minimized at for all

Proof

This proof is exactly same as the proof of Result 5 if we assume that there are proportitions of .

Theorem 18

Let the followings hold:

Then for sufficiently large we have the following bound for the co-ordinates of and bound for :

| (C.3) | |||

with probability at least

Proof

The proof is similar to the proof of Lemma 6 if we replace by

Appendix D Computational results: generalized linear model

In this section we perform synthetic experiments similar to Section 5 on binary classification setup. The covariates are dimensional and again generated from AR(1) model with correlation and variance 0.25 (, and , ), and the response for -th dataset is generated as:

We preform the debiased lasso on logistic regression to get the local estimates and keep rest of the setup exactly same as before.

In Figure 9 compare the -error of global parameter estimates with corresponding global parameters (note that they are different). The behaviors are similar to the linear models. For a fair comparison with the same baseline, we examine the prediction performance of the global parameters on new test data (not seen before), which one can find in Figure 10. The results for the logistic regression model have similar behavior as the linear regression model.

Appendix E Supplementary details for cancer cell line study

In the following section we provide the detail about cancer cell line dataset.

E.1 Data source and preprocessing

The Cancer Cell Line Encyclopedia is a database on gene expression, genotype and drug sensitivity data. As covariates, we use the RNAseq TPM gene expression data DepMap (2021) for just protein coding genes (DepMap 21Q2 Public release) and the pharmacologic profiles for 24 anticancer drugs Consortium et al. (2015) across 504 across lines as the responses. The cell-lines in the gene expression data and the drug response data are matched using the pairs of cell line name and depmap id from the secondary screen dose response curve parameters file Corsello et al. (2019) (secondary-screen-dose-response-curve.csv). These data files are publicly available in DepMap portal333Depmap portal: https://depmap.org/portal/

The gene expression data has genetic expression for genes across 1379 cell lines. After matching them with the drug response data we only keep the cell lines for which the dose-response curve was fitted using sigmoid function. We use the area above dose-response curve (ActArea) as the drug response measure. Finally we end up with cell lines in total. The codes are available in https://github.com/smaityumich/MrLasso.

E.2 Drug-response prediction plots

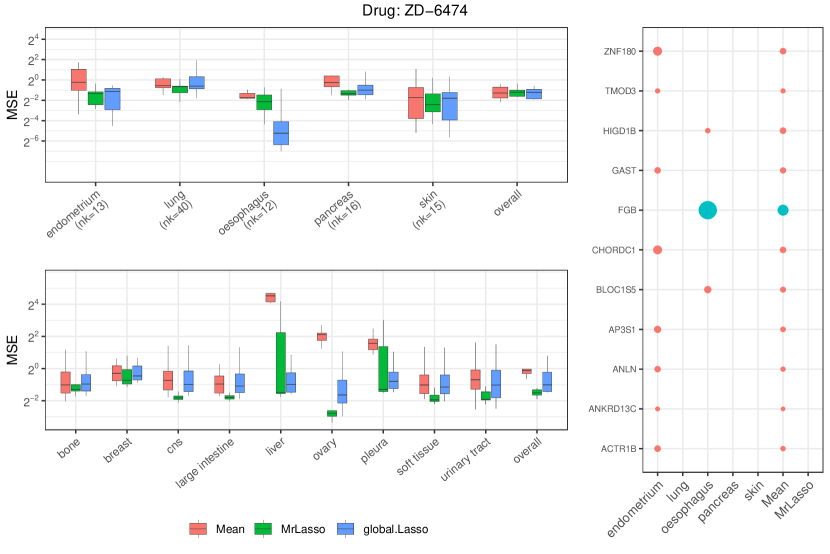

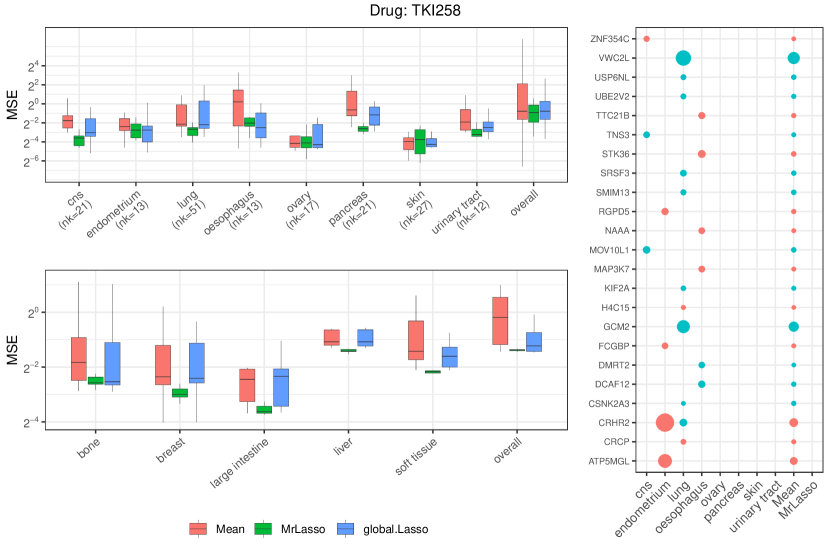

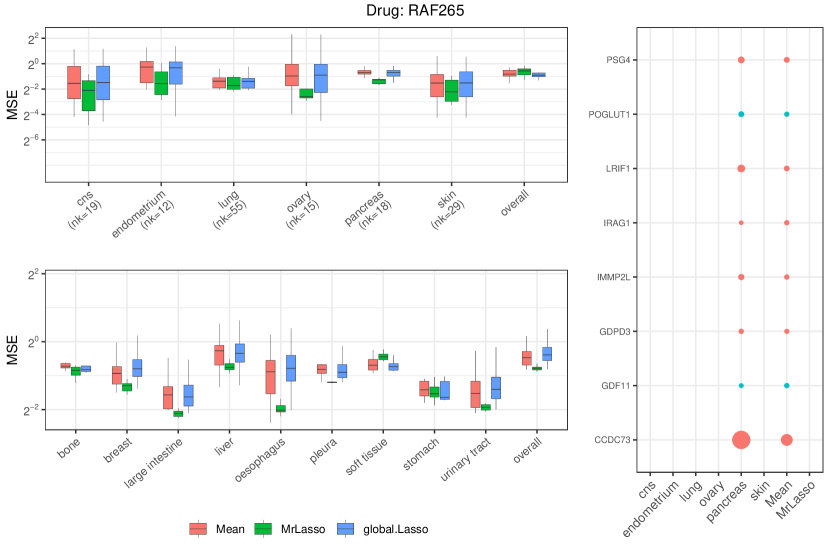

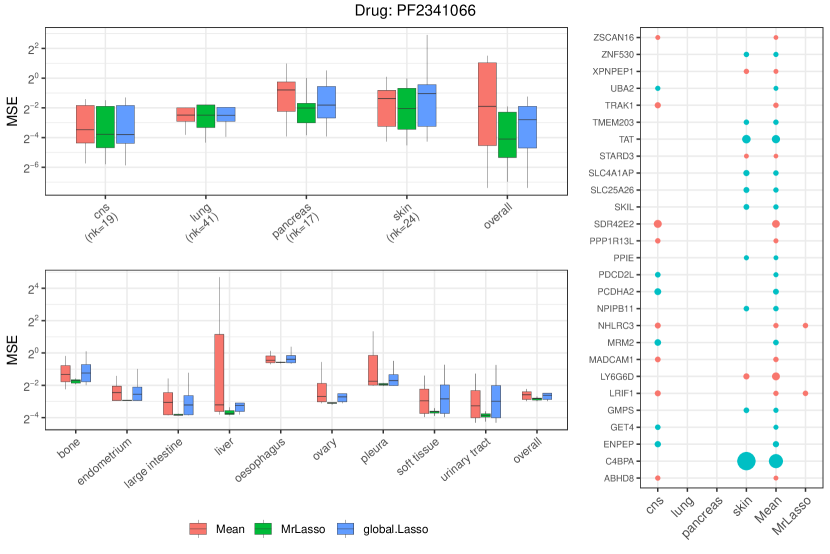

Next we present prediction error plots and gene selections for the drugs 17-AAG, Irinotecan, AZD0530, AEW541, ZD-6474, TKI258, RAF265 and PF2341066.