Infinite time horizon

spatially distributed optimal control problems with pde2path –

algorithms and tutorial examples

Hannes Uecker1, Hannes de Witt2

1 Institut für Mathematik, Universität Oldenburg, D26111 Oldenburg,

hannes.uecker@uni-oldenburg.de

2 Institut für Mathematik, Universität Oldenburg, D26111 Oldenburg,

hannes.de.witt1@uni-oldenburg.de

Abstract

We use the continuation and bifurcation package pde2path to numerically analyze infinite time horizon optimal control problems for parabolic systems of PDEs. The basic idea is a two step approach to the canonical systems, derived from Pontryagin’s maximum principle. First we find branches of steady or time–periodic states of the canonical systems, i.e., canonical steady states (CSS) respectively canonical periodic states (CPS), and then use these results to compute time-dependent canonical paths connecting to a CSS or a CPS with the so called saddle point property. This is a (high dimensional) boundary value problem in time, which we solve by a continuation algorithm in the initial states. We first explain the algorithms and then the implementation via some example problems and associated pde2path demo directories. The first two examples deal with the optimal management of a distributed shallow lake, and of a vegetation system, both with (spatially, and temporally) distributed controls. These examples show interesting bifurcations of so called patterned CSS, including patterned optimal steady states. As a third example we discuss optimal boundary control of a fishing problem with boundary catch. For the case of CPS–targets we first focus on an ODE toy model to explain and validate the method, and then discuss an optimal pollution mitigation PDE model.

1 Introduction

We consider optimal control (OC) problems for partial differential equations (PDEs) of the form

| (1a) | ||||

| with initial condition , and suitable boundary conditions. Here denotes a (vector of) state variables, is a (distributed) control, is a diffusion matrix, and is the Laplacian. The goal is to find | ||||

| (1b) | ||||

for the discounted time integral

| (2) |

where is the spatially averaged current value objective function, with the local current value a given function, and is the discount rate which corresponds to a long-term investment rate. The discounted time integral is typical for economic problems, where “profits now” weight more than mid or far future profits. The (formally ) in (1b) runs over all admissible controls ; this will be specified in more detail in the examples below. Additionally, we also give one example of a boundary control, where , and where (1) and (2) are modified accordingly. In applications, and of course often also depend on a number of parameters, which however for simplicity we do not display here.111 in (1a) can in fact be of a much more general form, but for simplicity here we stick to (1a).

In this tutorial we explain by means of four examples how to numerically study problems of type (1) with pde2path222see [UWR14] for background, and [Uec19d] for download of the package, demo files, and various documentation and tutorials, including a quick start guide also giving installation instructions. The examples are from [Uec16, GU17, GUU19, Uec19a], and we mostly refer to these works and the references therein for modeling background and (bioeconomic) interpretation of the results, and for general references and comments on OC for PDE problems, here keeping these aspects to a minimum. In the first example, is the phosphate load in a model describing the phosphorus contamination of a shallow lake by a scalar PDE (1a) with homogeneous Neumann BCs , the outer normal. Similarly, in the second example, is the harvesting effort in a vegetation-water system, such that (1a) is a two component reaction diffusion, again with homogeneous Neumann BCs, while in the third example with is a boundary control, namely the fishing effort on (part of) the shore of a lake. In these examples, so–called canonical steady states (CSSs), i.e., steady states of the so–called canonical system (see below) play an important role. The fourth example considers optimal pollution (mitigation), where the states are the emissions of some firms and the pollution stock, and the control is the pollution abatement investment. Here, canonical periodic states (CPSs) play an important role. To keep this tutorial simple, for all examples we restrict to the 1D case of an interval. Generalizations to domains in are straightforward, and also straightforward to implement in pde2path, and for the shallow lake and the vegetation systems have also been studied in [Uec16, GU17] respectively.

In the remainder of this introduction, we first briefly review the derivation of the canonical system as a necessary first order optimality condition from (1) via Pontryagin’s maximum principle. Then we explain the basic algorithms to treat the canonical system, i.e., to first find CSSs and CPSs and then canonical paths (CPs), i.e., solutions of the canonical system which connect some given initial states to some CSS or CPS with the so–called saddle point property. These CPs yield candidates for solutions of (1). In §2 we present the example problems and the pde2path implementation details for controlling to a CSS, and in §3 for controlling to a CPS. In §4 we close with a brief summary and outlook. We assume that the reader has a basic knowledge of Matlab, has installed pde2path (see also [dWDR+18]), and also has some previous experience with the software. If this is not the case, then we recommend to at least briefly look at one of the simpler problems discussed in, e.g., [RU18].

Remark 1.1.

The pde2path library described here is in libs/oclib. There is also an older OC lib, namely libs/oc, which we mainly keep for downward compatibility, and the associated old demos are in ocdemos/legacy. The upgrade of oc to oclib includes the computation of CPs to CPSs, and the option to free the truncation time , and we strongly recommend to switch to this setting.

1.1 Pontryagin’s Maximum Principle and the canonical system

We first consider the case of spatially distributed controls , and assume homogeneous Neumann BCs for , i.e., on , the outer normal, and introduce the costates and the (local current value) Hamiltonian

| (3) |

By Pontryagin’s Maximum Principle (see Remarks 1.2 and 1.3) for the intertemporal Hamiltonian with the spatial integral

| (4) |

an optimal solution (or equivalently ) has to solve the canonical system (CS)

| (5a) | ||||

| (5b) | ||||

| where , which generally we assume to be obtained from solving | ||||

| (5c) | ||||

| Under suitable concavity conditions on this holds due to the absence of control constraints. The costates also fulfill zero flux BCs, and in the derivation of (5) we imposed the so called inter–temporal transversality condition | ||||

| (5d) | ||||

In principle we want so solve (5) for , but in (5a) we have initial data for only half the variables, and in (5b) we have anti–diffusion, such that (5) is ill–posed as an initial value problem. For convenience we set333the notation for the vector of state and costate variables is used here as generally denotes the vector of unknowns in pde2path; in optimal control is often used as the notation for the control, which here we denote by ;

| (6) |

and write (5) as

| (7) |

with BCs , where stands for parameters present, which for instance include the discount rate . A solution of the canonical system (7) is called a canonical path (CP), a fixed point of (7) (which automatically fulfills (5d)) is called a canonical steady state (CSS) and a time-periodic solution of (7) is called canonical periodic states (CPS). With a slight abuse of notation we also call with given by (5c) a canonical path.

Remark 1.2.

For general background on OC in an ODE setting with a focus on the infinite time horizon see [GCF+08] or [Tau15]. For the PDE see, [Trö10] and the references therein, or specifically [RZ99a, RZ99b] and [AAC11, Chapter5] for Pontryagin’s maximum principle for OC problems for semi-linear diffusive models. However, these works are in a finite time horizon setting, and often the objective function is linear in the control and there are control constraints, e.g., with some bounded set . Therefore is not obtained from the analogue of (5c), but rather takes the values from , which is often called bang–bang control. Here we do not (yet) consider (active) control or state constraints, and no terminal time, but the infinite time horizon. Our distributed OC models are motivated by [BX08, BX10], which also discuss Pontryagin’s maximum principle in this setting.

Remark 1.3.

The use of the Hamiltonian is the standard way of dealing with intertemporal OC problems in economics. Equivalently, the canonical system (5) is formally obtained as the first variation of the Lagrangian

| (8) |

where , and where can be identified as Lagrange multipliers to the constraint (1a), i.e., . Using integration by parts in with the Neumann BCs and we have and using integration by parts in with transversality condition (5d) yields Thus, can also be written as

| (9) | ||||

and (5) are the first variations of with respect to (using (8)) and (using (9)) with . Both computations (with and ) are somewhat formal, and in particular the necessity of the transversality condition (5d), is subject to active research. See also [GUU19] and the references therein for a discussion of rigorous results for infinite time horizon OC problems with PDE constraints.

1.2 The general setup and the algorithms for canonical paths

To study (7) we proceed in two steps, which can be seen as a variant of the “connecting orbit method”, see, e.g., [BPS01], [Gra15, Chapter 7] and Remark 1.5: first we compute (branches of) CSSs and CPSs, and second we compute CPs connecting some initial states to some CSSs or CPSs. Thus we take a somewhat broader perspective than aiming at computing just one optimal control, given an initial condition . Instead, we aim to give a somewhat global picture by identifying the optimal CSS/CPS and their respective domains of attraction.

(a) Branches of CSSs and CPSs.

We compute (approximate) CSSs of (7), i.e., solutions of

| (10) |

together with the spatial BCs, by discretizing (10) via the finite element method (FEM) and then treating the discretized system as a continuation/bifurcation problem.444The notation is often used in OC for CSS, and is not related to Fourier transform in any way; we use the notation for CPS in an analogous sense. This gives branches of solutions, parameterized by a (pseudo-) arclength, which is in particular useful to possibly find several solutions , at fixed . CPS are usually not computed directly, but via Hopf bifurcation from branches of CSS. Thus, after finding such Hopf bifurcations, we do a branch switching with an appropriate initial guess for the rescaled problem

| (11a) | ||||

| (11b) | ||||

where the period becomes an additional unknown, see [Uec19a].

By computing the associated we can identify which of the CSSs and CPSs is optimal amongst the CSSs and CPSs. Given a CSS , for simplicity we also write , and moreover have, by explicit evaluation of the time integral,

| (12) |

For a CPS with period length we evaluate the time integral

| (13) |

Due to the discounting this integral may highly depend on the phase of the CPS, and thus we do not have a single objective value for a CPS, but a continuum of objective values. However, when computing CPs to a CPS it generally turns out that the values of the CPs are independent of the chosen phase of the CPS, see Remark 3.1 below.

(b) Canonical paths to canonical steady states.

In a second step, using the results from (a), we compute CPs connecting chosen initial states to a CSS (or a CPS , see below), and the objective values of the canonical paths. For paths to a CSS we choose a truncation time and modify (5d) to the condition that and near , where denotes the stable manifold of . In practice, we approximate by the stable eigenspace , and thus consider the time-rescaled BVP

| (14a) | ||||

| (14b) | ||||

| (14c) | ||||

and small in a suitable sense, further discussed below. If the mesh in the FEM discretization from (a) consists of nodes, then , and (14a) yields a system of ODEs in the form (with a slight abuse of notation)

| (15a) | ||||

| while the initial and transversality conditions become555recall that we put the truncation time into such that the end point of a CP is at | ||||

| (15b) | ||||

| (15c) | ||||

Here, is the mass matrix of the FEM mesh, (15b) consists of initial conditions for the states, while the costates (and hence the control ) are free, and defines the projection onto the unstable eigenspace , where due to the convention that , the stable eigenspace is spanned by the (generalized) eigenvectors of to eigenvalues with positive real parts. Thus, to have BCs altogether we need dim. On the other hand, we always have dim, see [GU17, Appendix A]. We define the defect

| (16) |

and call a CSS with a CSS with the saddle–point property (SPP). At first sight it may appear that depends on the spatial discretization, i.e., on the number of of nodes. However, remains constant for finer and finer meshes, see [GU17, Appendix A] for further comments.

For with the SPP, and sufficiently small, we may expect the existence of a solution of (15), which moreover can be found from a Newton loop for (15) with initial guess . Here, as a first guess for the truncation time we may use the longest decay length of the stable directions, i.e.,

| (17) |

where is the stable eigenvalue with the smallest real part.

For larger a solution of (15) may not exist, or a good initial guess may be hard to find, and therefore we use a continuation process for (15). In the simplest setting, assume that for some we have a solution of (15) with (15b) replaced by

| (18) |

(e.g., for we have ). We then increase by some stepsize and use as initial guess for (15a), (15c) and (18), ultimately aiming at . To ensure that is small, the truncation time may be set free if

| (19) |

is violated, and the additional boundary condition

| (20) |

with fixed is added, where is a weighted (discrete) norm, and we initialize

| (21) |

which of course is only a rough estimate and highly problem dependent, and, like all numerical parameters, can be reset by the user. See Remark 1.4 for further comments.

To discretize in time and then solve (15a), (15c) and (18) (including (20) if is free) we use the BVP solver TOM [MS02, MT04, MST09]666see also www.dm.uniba.it/~mazzia/mazzia/?page_id=433, in a version mtom which accounts for the mass matrix on the lhs of (15a)777and which is also used for finding time-periodic orbits in pde2path, see [Uec19a, Uec19b].888We also use a simple BVP solver bvphdw, which we mainly set up for testing, but which is sometimes more robust than the sophisticated methods (error estimation and mesh refinement) of mtom. In the following discussion, we write mtom for the BVP solver, but bvphdw can similarly be used. This predictor () – corrector (mtom for ) continuation method corresponds to a “natural” parametrization of a canonical paths branch by . We also give the option to use a secant predictor

| (22) |

where and are the two previous steps. However, the corrector still works at fixed , in contrast to the arclength predictor–corrector described next.

It may happen that no solution of (15a), (15c) and (18) is found for for some , i.e., that the continuation to the intended initial states fails. In that case, often the CP branch shows a fold in , and we use a modified continuation process, letting be a free parameter and using a pseudo–arclength parametrization by in the BCs at . We set free and add BCs at continuation step ,

| (23) |

with the solution from the previous step, and appropriately chosen with , where is a suitable norm in , which may contain different weights of and . For and we find natural continuation with stepsize again. To get around folds we may use the secant

with small , and also a secant predictor

| (24) |

for with

| (25) |

This essentially follows [GCF+08, §7.2].

Finally, given , to calculate , at startup we solve the generalized adjoint eigenvalue problem

| (26) |

for the eigenvalues and (adjoint) eigenvectors , which also gives the defect by counting the negative eigenvalues in . If , then from we generate a real base of which we sort into the matrix . Algorithm 1 summarizes our method to compute a CP to a CSS.

0. Preparation.

Compute and the defect at the CSS.

If , then return (not a saddle point). Otherwise, set ,

and, if no initial guess for is given, compute from (17).

Repeat until or or until convergence failure.

1. BVP solution.

Solve (15) and check (19). If (19) is

violated (or from the start), then

augment (15) by (20), free , and solve again.

2. Next prediction (or stop).

If or then stop and return solution .

If no solution found:

If arc=0, then stop and return the last solution.

If arc=1 and (else stop and

return the last solution), then decrease

and go to 1 with new predictor from (24).

If solution found:

Let .

If arc=0, then let , let

, or set according

to (24) (secant predictor), and go to 1.

If arc=1, then make a new predictor via (24),

set , and go to 1.

Remark 1.4.

Writing (the discretized version of) (15) (and, if switched on, (20)) as

| (27) |

then is a (numerical) solution of (27) if , where the component of is essentially measured in the norm (for mtom we use the relative error), and thus we also use in (19). On the other hand, for the active condition (20) we choose the euclidean norm with derivative (as a row vector) instead of the at first sight more natural condition , because we thus altogether obtain a well conditioned Jacobian for the extended system (see (34)). For on the order of tol, (20) and are essentially equivalent, but the additional flexibility via (and derived from ) with for instance on the order of turns out to be useful to obtain fast and robust results. Finally, starting with such a possibly rather large then also allows to decrease a posteriori in a few steps, see the examples in §2. In detail, we solve

| (28) |

where is the number of spatial degerees of freedom (number of states, number of spatial discretization points), where denotes the number of time steps, where the boundary conditions are written as

| (32) |

where contains the arclength boundary condition (23), if switched on, and where is the discretization of . Thus, for CPs to CSSs with fixed time, and for CPs to CSSs with free time or CPs to CPSs, and (natural continuation) or (arclength). To solve (28), given a guess from a previous step, we use Newton’s Method, i.e.,

| (33) |

| (34) |

where the first line consist of rows, where the second line consists of rows, and the —row and the last column of are only present in the arclength setting.999We only indicate in the first line the dimension of the . Moreover, , , , where is the -th time step, and the field at time . Thus, for free, contains the row , which would be ill conditioned if , and (20) is much more robust. Of course, in (33) stands for the linear system solver used.

(c) Canonical paths to canonical periodic states.

For CPs to CPSs the basic idea is a BVP of style (14) again. However (14c) has to be adapted to the CPS case. The theoretical truncated BC is

| (35) |

where is the stable manifold of the CPS , and is some point on . In practice, to have a boundary condition analogous to (15c), we fix an end-point on the CPS. We then want a boundary condition of the form

| (36) |

with to yield boundary conditions. For a CPS, the analog to the linearization at a CSS is the monodromy matrix , which describes the linear effect of small deviations with respect to one period. It corresponds to the time (period of the CPS) map of the variational equation

| (37) |

The eigenvalues of are called Floquet multipliers, and are independent of the choice of , but the eigenvectors depend on . Since in (11a) we start with an autonomous system, we always have the (trivial) multiplier , which corresponds to a time shift of , and this trivial multiplier can be used for assessing the numerics.101010For instance, we give a warning if for the trivial multiplier we numerically have , with default setting .

The monodromy matrix can be computed (approximated) as the product of the linearizations of (14a) at every –mesh point of . However, for OC problems, in particular PDE OC problems, we often have both very large (due to the anti–diffusion in the co-states) and very small (due to diffusion in the states) multipliers111111for instance for the largest multiplier in a small scale PDE problem, and thus we need a particularly stable method for their computation. Here we use a periodic Schur decomposition, see [Kre01] and [Uec19a] and the references therein for details. This produces a set of matrices

| (38) |

with an orthogonal matrix and an upper triangular matrix with the multipliers on the diagonal. Moreover, the adjoint monodromy matrix can be computed without extra effort, and sorting of the multipliers in is possible, and as the first columns of are a basis of the span of the first eigenvectors, we can compute projections on eigenspaces this way.

The projection in (36) needs to provide boundary conditions by projecting onto the center–unstable eigenspace, associated with multipliers with , where the translational eigenspace associated with the trivial multiplier is included because we want to fix the truncation point on the CPS. As for the CSS case, the dimension of the center–stable eigenspace is at most and thus this is the only case in which a canonical path can be computed. This is called saddle point property (SPP) of the CPS, see [GCF+08]. Given a CPS with the SPP we thus compute the matrix as the projection on the center-unstable eigenspace, i.e. on the eigenspace spanned by Floquet-multipliers with .

Thus, altogether we have BCs (14b) for the initial states, BCs (36), and ODEs (14a) for the unknowns , and the free truncation time is the unknown, i.e.,

| (39a) | ||||

| (39b) | ||||

| (39c) | ||||

Moreover, as in (19) we additionally require, for a given ,

| (40) |

The continuation method in the initial states is the same as for CPs to CSS, i.e. we have natural parametrization with and without secant predictor, and arclength parametrization. This includes the adaptation of the truncation time to ensure (39c). Similar to (17), an estimate for can be obtained from the largest (in modulus) stable multiplier , which we denote by , with the trivial multiplier denoted by . In the linear regime (small deviation from ) we then have

| (41) |

However, for small we may use as default initialization, with rather small () and then for larger add periods of the CPS at the end of the canonical path within the continuation process if necessary, i.e., if the deviation from the CPS becomes to large. In detail, to ensure (40) (which is never used to extend (39)) we use an add hoc step additional to the discretization in time of (39) and the solution of the obtained algebraic system by Newton’s method:

| (42) |

This appears to be a new idea, which allows to start with rather small initial , and works very well in all our applications, see §3 for details and examples.

0. Preparation.

Choose a point on the CPS and

compute the projection

onto the center-unstable eigenspace of the monodromy matrix

at via (36), i.e. the eigenspace associated to

Floquet-multiplier with , including

the defect .

If , then return (not a saddle point CPS).

Let , and compute

a guess for a canonical path to , initially

( copies of, if ) the CPS itself. Set .

Repeat until or or until convergence failure.

1. BVP solution.

Solve (39) for .

2. Target check.

Check (40). If (40) is violated,

then proceed as in (42), i.e., extend and go to 1.

3. Next prediction (or stop).

If or then stop.

If no solution found:

If arc=0, then stop and return the last solution.

If arc=1 and (else stop and

return the last solution), then decrease

and go to 1. with new predictor from (24).

If solution found:

Let .

If arc=0, then let , let

, or set according

to (24) (secant predictor), and go to 1.

If arc=1, then make a new predictor via(24),

set , and go to 1.

Remark 1.5.

There are further (and more sophisticated) methods for computing connecting orbits, including (homo– and) heteroclinic orbits which also converge to some prescribed solutions as . See, e.g., [Bey90] for a detailed analysis of the ’standard’ projection boundary condition, [Pam01] and [BPS01] for the so-called boundary corrector method, and [DKvVK08, DKvVK09] for the special case of connecting orbits in . In particular, for connecting orbits to cycles (periodic orbits) these methods use a free truncation time together with certain phase conditions to ensure that is small, where may vary on the cycle.

Here, we fix and thus the (asymptotic) phase, and use (42) to ensure . From the application point of view, it is important to keep the defining systems for CPs as small as possible, and in particular to put the computation of the CPS and the projections at some target point on the CPS into a preparatory step. Algorithm 2 summarizes our method to compute a CP to a CPS.

2 Examples and implementation details for CPs to CSSs

To explain how to use pde2path to calculate CSS and canonical paths we consider three example problems of type (1): The sloc (shallow lake OC) problem from [GU17], the vegoc (vegetation OC) problem from [Uec16], and the boundary fishing problem lvoc (Lotka-Volterra OC) from [GUU19]. For all examples we first briefly sketch the models, and then summarize the contents of the respective demo folder and explain the most important files in some detail. For the first model we also explain the general setup how to initialize the spatial domain and discretization, the rhs, the computation of CSS, and the OC related routines of pde2path. For all models we give some plots, but for details and interpretation of the results we refer to the respective papers.

2.1 Optimal distributed control of the phosphorus in a shallow lake

Following [BX08], in [GU17] we consider a model for phosphorus in a shallow lake, and phosphate load as a control. In 0D, i.e., in the ODE setting, this has been analyzed in detail for instance in [KW10]. Here we explain how we set up the spatial problem in pde2path. The model reads

| (43a) | ||||

| where , as in (1b), and fulfills the PDE | ||||

| (43b) | ||||

| (43c) | ||||

The parameter is the phosphorus degradation rate, and are ecological costs of the phosphorus contamination . One wants a low for ecological reasons, but for economical reasons a high phosphate load , for instance from fertilizers used by farmers. Thus, the objective function consists of the concave increasing function , and the concave decreasing function . In the demo directory sloc we consider the parameters

| (44) |

With the co-state , the canonical system for (43) becomes, with ,

| (45a) | ||||

| (45b) | ||||

| (45c) | ||||

| (45d) | ||||

2.1.1 Canonical steady states

To compute CSS we use a standard pde2path setup for (the steady version) of (45). As an overview, Table 1 lists the scripts and functions in ocdemos/sloc; these will be explained in more detail below, but for new users of pde2path we refer to [RU18] for an introduction into the basic pde2path data structures and setup of elliptic systems.

| bdcmds1D | script to compute bifurcation diagrams of CSS |

| cpdemo1D | script to compute CPs |

| skibademo | script to compute Skiba paths, see §2.1.4 |

| slinit | init routine; set the pde2path parameters to standard values, then some parameters to problem specific values; initialize the domain, set an initial guess , and find a first steady state by a Newton loop |

| oosetfemops | set FEM matrices (stiffness K and mass M) |

| slsG; slsGjac | resp. the Jacobian for (45) |

| slcon; sljcf | extract control from states/costates; compute the current value |

| cssvalf; psol3D | print CSS value and characteristics; mod of psol3D to plot several solutions in one fig. |

The pde2path FEM setup converts the PDE (45) into the ODE system (or algebraic system for steady states)

| (46) |

In (46), is the mass matrix of the FEM, is the stiffness matrix, where is the 1–component stiffness matrix corresponding to the scalar (Neumann–)Laplacian, or, more precisely, , and we put ’everything but diffusion’ into the ’nonlinearity’ . As usual, our basic structure is a Matlab struct p as in problem, which has a number of fields (and subfields), e.g., p.fuha, p.pdeo, p.u, p.hopf, p.file, p.plot, p.sw, p.nc which contain for instance function handles to the right hand side (p.fuha), the FEM mesh (p.pdeo), the current solution p.u, data for Hopf orbits (CPS, p.hopf), filenames/counters (p.file), plotting controls (p.plot), and switches (p.sw) and numerical constants (p.nc) used in the numerical solution, such as p.nc.tol, where is taken as a solution of if . However, most of these can be set to standard values by calling p=stanparam(p). In standard problems the user only has to provide:

-

1.

The geometry of the domain , and in the OOPDE setting used here a function oosetfemops used to generate the needed FEM matrices.

-

2.

Function handles sG implementing , and, for speedup, sGjac, implementing the Jacobian.

-

3.

An initial guess for a solution of , i.e., an initial guess for a CSS.

Typically, the steps 1-3 are put into an init routine, here p=slinit(p,lx,ly,nx,sw,ndim), where lx,ly,nx and ndim are parameters to describe the domain size and discretization121212ly (irrelevant) and ndim(=1) play no role in this tutorial, but we kept them in slinit because the same init routine is also used in 2D, and sw is used to set up different initial guesses, see Listing 1. For CSS computations the only additions/modifications to the standard pde2path setting are as follows: (the additional function handle) p.fuha.jcf should be set to the local current value objective function, here p.fuha.jc=@sljcf (see Listing 2), and p.fuha.outfu to ocbra, i.e., p.fuha.outfu=@ocbra. This automatically puts at position 4 of the calculated output–branch. Finally, it is useful (for instance for plotting) to set p.fuha.con=@slcon, where q=slcon(p,u) (see Listing 2.1.1) extracts the control from the states , costates and parameters , all contained in the vector u.131313We do not use slcon in slsG. However, putting this function into p has the advantage that for instance plotting and extracting the value of the control can easily be done by calling some convenience functions of p2poc.

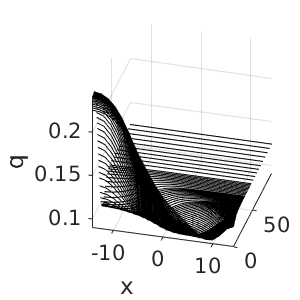

At the end of slinit, we call a Newton–loop to converge to a (numerical) CSS, which is called ’flat’, i.e., spatially homogeneous. By calling p=cont(p) we can continue such a state in some parameter. If p.sw.bifcheck>0, then pde2path detects, localizes and saves to disk bifurcation points on the branch. Afterwards, the bifurcating branches can be computed by calling swibra and cont again. These (and other) pde2path commands (continuation, branch switching, and plotting) are typically put into a script file, here bdcmds1D.m, see Listing 4, which we recommend to organize into cells. There are some modifications to the standard pde2path plotting commands, see, e.g., plot1D.m, to plot and simultaneously. These work as usual by overloading the respective pde2path functions by putting the adapted file in the current directory. See Fig. 1 for example results of running bdcmds1D.

| (a) BD of CSS | (b) BD, current values | (c) example CSS |

|---|---|---|

|

|

|

2.1.2 Canonical paths

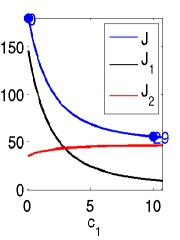

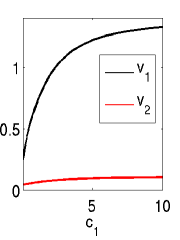

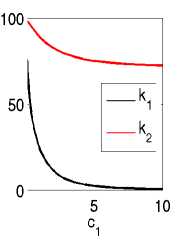

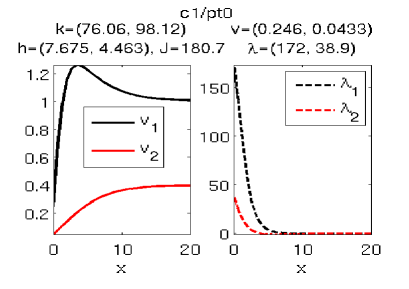

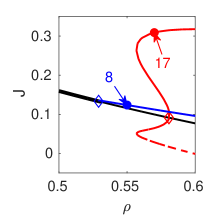

For OC problems, the computation of CSS is just the first step. The next goal is to calculate CPs from some starting state to a CSS with the SPP. For this we use the continuation algorithm isc which is essentially a wrapper for the BVP solvers mtom and bvphdw, and which for CSS as targets implements Algorithm 1. The data is again stored in a problem structure p which has a number of general options/parameters in p.oc, options specific to the behavior of the BVP solvers stored in p.tomopt, and solution data stored in p.cp. In particular, the oclib routines re–use the data and functions (FEM data, function handles) already set up for the computation of the CSS (or CPS), and no new functions need to be set up. The convenience function ocinit sets most OC parameters to standard values and, if provided with the corresponding data, the starting states and end point of the canonical path, i.e., the target CSS , or the target on a CPS . This function is the analog of stanparam in the CSS setting. For a first call the user only has to set the parameters at the top of Table 2, the estimated truncation time and the (initial) number of mesh points. However, as usual, the user can, and sometimes has to, change some of the standard options.

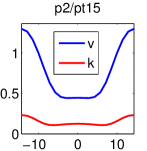

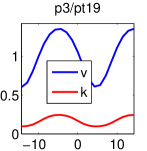

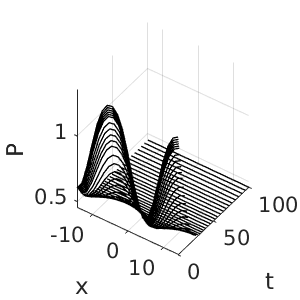

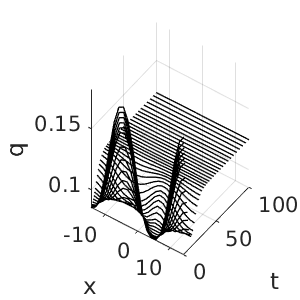

| (a) and on the CP from p3/pt19 to FSC | (b) diagnostics for (a) | (c) Using adaptation |

|---|---|---|

|

|

|

(d) Fold in for continuation for CP from p1/pt68 to FSS, and “upper” canonical path at

After setting up the data structures (via ocinit or modifications and possibly further commands) in the struct p, the computation of CPs is started by a call of p=isc(p,alvin,varargin) with default input parameters p and alvin, where alvin is a vector of continuation steps. For arclength continuation, the third input may contain the number of arclength continuation steps. For consecutive arclength calls, one can also set alvin=[] to directly start with arclength continuation. However a secant and two values for have to be given via p.oc.usec and p.hist.alpha (if natural continuation was done before, these fields are filled). See Section 2.1.3 for examples and further description of isc, other OC related pde2path functions, and the parameters in p.oc and p.tomopt. Here we continue with a brief description of CP results for the SLOC problem. The canonical path related computations are done in the command files cpdemo*. We first compute paths from a patterned CSS to a flat CSS and vice versa in cpdemo1D, see Listing 5 and Figure 2, while cpdemo2D does the same in . The file skibademo, to be run after cpdemo1D, computes some Skiba paths, see §2.1.4.

| struct/varname | default | description/comment |

|---|---|---|

| oc/ | struct with controls for isc external to the BVP solvers mtom and bvphdw | |

| nti | Initial number of mesh points. Highly problem dependent, so should be set by user. mtom has automatic mesh refinement, so rather try a small nti, while for bvphdw a somewhat larger nti should be used. | |

| T | first guess for truncation time - if empty it is set by isc | |

| nTp | 2 | for setting as a guess for for CPs to a CPS, period of CPS |

| freeT | 0 | if 1, then truncation time is set free for CPs to CSS, and (20) is included in the BVP, with in oc.tadev2 |

| tv | [] | initial t-mesh if not empty, otherwise generated by isc |

| retsw | 0 | return-switch for isc: 0: only final soln, 1: solutions for all |

| msw | 0 | predictor in natural continuation. 0: trivial, 1: secant |

| rhoi | 1 | pde2path index of the discount rate |

| tadevs | inf | target error in sup–norm, i.e., in (19). Can be set initially, but we recommend a first step without adaptation (small ), i.e., also freeT=0. |

| tadev2 | * | target error in euclidean norm, i.e., in (20), initialized by (21) once (19) is violated. Can be reset later to decrease the target deviation. |

| mtom | 1 | switch between mtom and bvphdw (in–house bvp solver) |

| sig | 0.1 | stepsize for arclength continuation |

| sigmin/sigmax | 1e-2,10 | minimal and maximal stepsizes for arclength continuation |

| fn | file–names, for instance for the initial and target states of the CP | |

| u0 | initial states; can be provided by file (see examples), or be set after ocinit | |

| s1 | classical pde2path data struct which will typically contain the data for the target (CSS in s1.u, or CPS in s1.hopf)) | |

| tomopt/ | struct with controls for the BVP solvers mtom and bvphdw | |

| lu | 0 | if 0, then use \ (usually faster) instead of decomposition in mtom |

| * | Standard mtom-parameters can be given here, e.g. Itlimax, Itnlmax and Nmax for maximal number of linear and nonlinear iterations and maximal number of mesh points. See mtom documentation. | |

| tol, maxIt | 1e-8,10 | tolerance (in norm) and max nr of iterations in bvphdw. |

| name | description |

|---|---|

| cp.u | solution (CP) generated by isc; used as initial guess for next continuation step, if already set by previous call to isc or if set externally. |

| cp.t | time mesh generated by isc (or set externally) |

| cp.par | solution parameters, i.e., truncation time in par(1), current in par(2) (for arclength) |

| hist.alpha | vector of the values in the continuation |

| hist.vv | vector of the objective values of the canonical path for the stored in hist.alpha |

| hist.u | CPs at continuation steps stored in hist.alpha |

| hist.t | time-meshes (normalized to ) of continuation steps |

| hist.par | parameter values ( and ) of the continuation steps |

2.1.3 Main oclib functions

The functions ocinit and isc are the main user interface functions for CP numerics. Essentially, after having set up p as in §2.1.1 for the CSS, including p.fuha.jcf, the user does not need to set up any additional functions to calculate canonical paths and their values. We give the signatures and some general remarks on the arguments and behavior of ocinit and isc, with the Cells referring to Listing 5.

-

p=ocinit(p,varargin) (Cell 1).

Convenience function (similar to p=stanparam(p)) to generate a standard problem structure p where most parameters are set to standard values. These are parameters for mtom (see tom/tomset.m), and parameters for isc, see Table 2 for an overview. If varargin={sd0,sp0,sd1,sp1}, then ocinit also sets the states of the solution stored in sd0/sp0 as the starting states and the solution stored in sd1/sp1 as the aimed CSS/CPS. Typically some of the options should be overwritten in the further setup.

-

p=isc(p,alvin,varargin) (Cell 1).

p is the problem structure containing the options/parameters described above in p.oc and p.tomopt, see Tables 2 and 3, and the solution in p.cp. alvin is the vector of desired values for the continuation, for instance alvin=[0.25 0.5]. If varargin=nsteps is given as a third input, arclength continuation is started after the last value of alvin with nsteps steps, or until is reached. If previous calls of isc are present, then we can directly start arclength continuation by calling isc with empty alvin. After the first call of isc some additional fields are set in p.oc, containing, e.g., the current secant, the last starting point in the continuation, and, if desired via p.oc.retsw=1, the solutions at different continuation steps, see Table 3.

Remark 2.1.

Concerning the original TOM options we typically run isc with weak error bounds and what appears to be the fastest monitor and order options, i.e., tomopt.Monitor=3; tomopt.order=2. Once continuation is successful (or also if it fails at some ), we can always postprocess by calling mtom again with a higher order, stronger error requirements, and different monitor options. See the original TOM documentation. The most convenient way to do so is to call isc with alvin=1 again after resetting TOM-related options.

There are a number of additional functions for internal use, and some convenience functions, which we briefly review as follows:

-

[Psi,mu,d,t]=getPsi(s1).

For CPs to CSSs only: compute , the eigenvalues mu, the defect d, and a suggestion for . This becomes expensive with large (number of spatial DoF).

-

[Fu1,Fu2,d]=floqpsmatadj(p.opt.s1).

For CPs to CPSs only: computes (by periodic Schur decomposition) the projection on the center-unstable eigenspace in Fu2 and the Floquet-multiplicators in d. Expensive, but has to be done only once for each CPS.

-

[sol,info]=mtom(ODE,BC,solinit,opt,varargin).

Modification of TOM, which allows for in (15a). Extra arguments and lu,vsw in opt. If opt.lu=0, then is used for solving linear systems instead of an LU–decomposition, which becomes too slow when becomes too large. See the TOM documentation for all other arguments included in opt, and note that the modifications in mtom can be identified by searching “HU” in mtom.m. Of course mtom (as any other function) can also be called directly, which for instance can be useful to postprocess the output of some continuation by changing parameters by hand.

-

sol=bvphdw(ODE,BC,solinit,tomopt,opt).

A simple Newton solver for CPs, which was mainly used for testing but is sometimes more robust than the sophisticated methods (error estimation and mesh refinement) of mtom.

-

f=mrhs(t,u,q,opt); J=fjac(t,u,opt); and f=mrhse(t,u,q,opt); J=fjace(t,u,opt).

The rhs and its Jacobian to be called within mtom resp. bvphdw (see the respective wrapper files). These are wrappers which calculate and by calling the resp. functions in the pde2path–struct p.opt.s1, which were already set up and used to calculate the CSS/CPS. Similar remarks apply to mrhse and fjace for the arclength continuation.

- bc=cbcf(ya,yb,opt);[ja,jb]=cbcjac(ya,yb,opt); bc=cbcfe(ya,yb);[ja,jb]=cbcjace(ya,yb).

-

[jval,jcav,jcavd]=jcaiT(s1,cp,rho) and djca=disjcaT(s1,cp,rho).

Computes the value

(47) of the solution in cp (with taken from s1.fuha.jcf), and also returns and along the CP for easy plotting, cf. Fig. 2(b).

- [di,d2]=tadev(p).

Remark 2.2.

There are also some plotting function in oclib, which however should be seen as templates for plotting of canonical paths, including diagnostic plots to check the convergence behavior of the canonical path as , cf. (d),(f) in Fig. 2. The function slsolplot(p,view) in the sloc demo directory can serve as a template how to set up such plots.

2.1.4 Skiba points

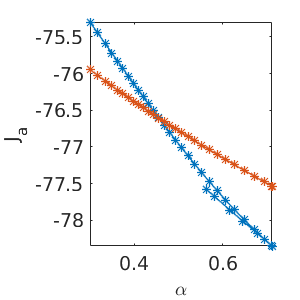

In ODE OC applications, if there are several locally stable CSS, then often an important issue is to identify their domains of attractions. These are separated by so called threshold or Skiba–points (if ) or Skiba–manifolds (if ), see [Ski78] and [GCF+08, Chapter 5]. Roughly speaking, these are initial states from which there are several optimal paths with the same value but leading to different CSS. Here we give an example for the SLOC model how to compute a patterned Skiba point between FSC and FSM.

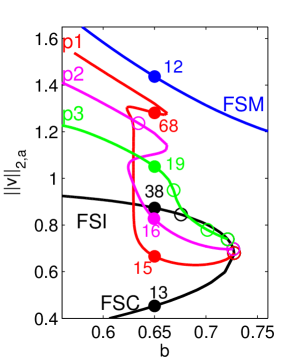

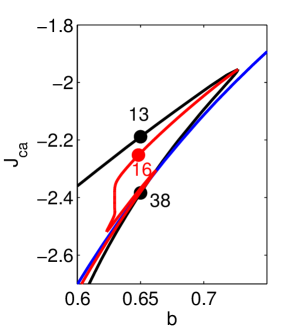

In Cell 3 of cpdemo1D.m we attempt to find a path from given by p1/pt68 to given by FSC/pt13; this fails due to the fold in . However, for given we can also try to find a path from the initial state to the FSM, and compare to the path to the FSC. For this, we can use the problem structure p computed in Cell 3. The initial states for the k’th value of p.hist.alpha are, due to p.opt.retsw=1, stored in p.hist.u{k}(:,1) i.e. as the starting point of the canonical path associated to the given value.

In skibademo.m (Listing 10, which is a rather elaborate application of the OC facilities of pde2path, and can be skipped on first reading) we find paths from these initial states from cpdemo1D.m to the other flat steady state with the SPP, namely FSM, and compare the values with the values of the paths to FSC, stored in p.hist.vv. See Fig. 3 for illustration.

| (a) A Skiba point at | (b) Paths to FSC (blue) and FSM (red) |

|---|---|

|

|

Remark 2.3.

The directory slocdemo also contains the script files bdcmds2D.m and cpdemo2D.m, used to compute CSS and canonical paths for (45) over the 2D domain (based on exactly the same init file slinit.m), and some modified plotting functions plotsolf.m and plotsolfu.m, see, e.g., [GU17, Fig. 4,5] for some 2D results.

2.2 Optimal harvesting patterns in a vegetation model

Our second example, from [Uec16], concerns the optimal control of a reaction diffusion system used to model harvesting (or grazing by herbivores) in a system for biomass (vegetation) and soil water , following [BX10]. Denoting the harvesting (grazing) effort as the control by , we consider

| (48a) | ||||

| (48b) | ||||

| (48c) | ||||

| with harvest , and current value objective function , which thus depends on the price , the costs for harvesting/grazing, and , in a classical Cobb–Douglas form with elasticity parameter . Furthermore, we have the boundary conditions and initial conditions | ||||

| (48d) | ||||

Again we want to maximize the discounted profit

| (49) |

For the modeling, and the meaning and values of the parameters we refer to [BX10, Uec16], and here only remark that the model aims at a realistic description of certain semi–arid systems, that, e.g., the discount rate is in the pertinent economic regime, and that, like in most studies of semi–arid systems, we take the rainfall as the main bifurcation parameter.

Denoting the co-states by we obtain the canonical system

| (50a) | ||||

| (50b) | ||||

| (50c) | ||||

| (50d) | ||||

| where . | ||||

The system (50) has a similar structure as (45), with the immediate difference that (50) has four components and many parameters, and thus looks somewhat complicated. However, it is still convenient to implement in pde2path, and leads to many patterned optimal steady states, see [Uec16] for further discussion. Thus, besides documenting the implementation of (50) underlying the results in [Uec16], our aim here is to illustrate that also rather complicated systems can be implemented and studied in the pde2path OC setting in a simple way. Writing (50) as , , we basically need to set up the domain, and the BCs, and the objective function. Table 4 lists and comments on the scripts and functions in ocdemos/vegoc. The implementation of (50) follows the general pde2path settings with the OC related modifications already explained in §2.1, and thus we only give a few remarks in the Listing captions.

| script/function | purpose,remarks |

|---|---|

| bdcmds, cpcmds | scripts to compute CSS and canonical paths |

| efu, vegjcf | functions to compute [E,H] from u, and the current value (by calling efu) |

| vegsolplot, vegdiagn | functions to plot CPs, and compute and plot diagnostics for CPs |

| vegcm.asc, watcm.asc | colormaps for CP plots (and state plots in 2D) |

Figure 4 shows a basic bifurcation diagram of CSS in 1D with , , from the script file bdcmds.m, which follows the same principles as the one for the SLOC demo. Again we start with a spatially flat (i.e., homogeneous) canonical steady FSS (black), on which we find a number of Turing-like bifurcations. The blue branch in (a) represents the primary bifurcation of PCSS (patterned canonical steady states), which for certain have the SPP, and, moreover, turn out to be POSS (patterned optimal steady states). See [Uec16] for more details, including a comparison with the uncontrolled case of so called “private optimization”, and 2D results for yielding various POSS, including hexagonal patterns.

(a) (b) (c)

The script files cpcmds.m for CPs, and skibacmds.m for a Skiba point between the flat optimal steady state FSS/pt13 and the POSS p1/pt34, again follow the same principles as in the the SLOC demo. See Figure 5 for an example output. We use customized colormaps for vegetation (green) and water (blue), which are provided as vegcm.asc, watcm.asc and whitecm.asc, respectively.

| (a) | (b) |

|---|---|

|

|

2.3 Optimal boundary catch as an example of boundary control

Our third example, taken from [GUU19], considers the optimization of the discounted fishing profit , . Here are the populations of two fish species (prey, predator) in a (1D) lake or ocean , are the fishing (harvesting) efforts (controls) of and , respectively, at the shore, and and are the prices for the fishes and the costs for fishing, respectively, and we again choose a Cobb–Douglas form for the harvests , with parameters . We assume that the fish populations evolve according to a standard Lotka-Volterra model, namely

| (51) |

in , with and growth function , with parameter . The controls (fishing efforts for species , respectively) occur in the BCs for (51), i.e., we assume the Robin BCs

| (52) |

and zero flux BCs at . Thus, in contrast to the sloc and vegoc examples we no longer have a spatially distributed control, but a (two component) boundary control.

Introducing the co-states , Pontryagin’s maximum principle yields the evolution and the BCs of the co-states (combining with (51), to have it all together)

| (53c) | |||

| (53f) | |||

| (53i) | |||

| and | |||

| (53j) | |||

Thus, we again have a 4 component reaction diffusion system (53a-c) for the states and the costates , but now the controls live on the boundary at , leading to nonlinear flux boundary conditions. Also, from the modeling point of view, the pertinent questions for (53) are slightly different than for (50), since for (53) we are not so much interested in bifurcations and pattern formation (which do not occur for the parameters chosen below), but rather in the dependence of the (unique) CSS on the parameters, and mostly in the canonical paths leading to these CSS.

In any case, we now focus on how to put the nonlinear BCs into pde2path. Table LABEL:lvoctab lists the scripts and functions in ocdemos/lvoc, and some further comments are given in the listing captions below.

| script/function | purpose,remarks |

| bdcmds,cpcmds | scripts to compute CSS and CPs |

| lvinit,oosetfemops | init routine, and setting of FEM matrices |

| lvsG | the rhs for (53a), also explicitly implementing the BC (53b), while (53c) are naturally fulfilled with K the Neumann Laplacian. |

| lvbra | branch-output, here substantially modified from stanocbra, i.e., writing specific data like profits/harvest/controls per fish-species on the branch |

| hfu | returns harvest , and derivatives (needed for lvsG) , ; straightforward implementation. |

| lvjcf | returns , as required in the standard pde2path setup for OC problems, but also the individual profits per fish-species. |

| jca | average, overloaded here since is on boundary, hence the default averaging by makes no sense |

| lvdiagn | diagnostics functions for canonical paths |

| stanpdeo1Dpde | classdef, overloads the pde2path classdef stanpdeo1D in order to have instead of (standard). |

| plotsol, psol3D | some more overloads of pde2path standard functions for plotting. |

Figure 6 gives some example plots from running bdcmds.m. This script is rather lengthy, with the main point here to illustrate how to plot various data of interest by first putting it on the branch (here via lvbra.m) and then choosing the pertinent component for plotting. The script cpcmds.m for computing canonical paths follows the same outline as those for the sloc and vegoc examples. Figure 7 shows a canonical path to the CSS at , starting from the homogeneous fixed point of (51). As already said, we refer to [GUU19] for discussion of the results.

| (a) and at ; continuation in | (b) CSS at |

|

|

|

3 Examples and implementation details for CPs to CPSs

The basic idea for the computation of CPSs and of CPs to CPSs is similar to that for the computation of CSSs and CPs to CSSs. We first search for CPSs, usually via Hopf bifurcations from CSSs, and then aim to compute CPs to such CPSs with the SPP, again using the main pde2path OC user interface isc, which now implements Algorithm 2. To illustrate the setup we first discuss an ODE toy model. Subsequently we come to a PDE model for pollution mitigation.

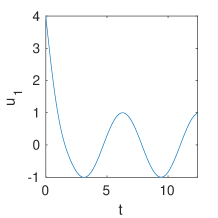

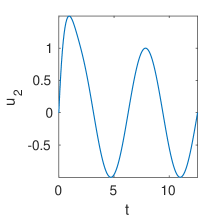

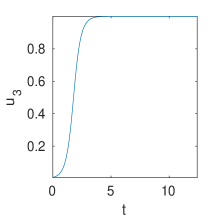

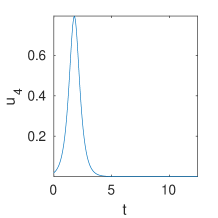

3.1 An ODE toy problem

We start with the ODE toy model

| (54a) | |||

| (54b) | |||

with parameters and . Although (54) is not derived as a canonical system for an OC problem, we interpret as states and as costates and call a time periodic solution of (54) a CPS.

3.1.1 Preliminary analytical remarks

Concerning our points of interest, the model (54) can almost completely be treated analytically and thus can be used to test our numerical methods. For fixed , the nonlinear system (54a) has the unstable periodic orbit of period , and (54a) is coupled to (or driven by) by the nonlinear pendulum (54b). In detail, by polar coordinates in , (54) transforms to

| (55a) | |||

| (55b) | |||

with and , with the phase portraits of the ODE (for fixed ) and the system sketched in Fig.8(a,b). Thus, to find a CPS we look for CSS of the reduced system

The costates are independent of the states and the system has the first integral , i.e. solutions of the system lie on contour lines of , see Fig.8(a). We choose , and , which yields a periodic solution in the full system. We fix and one of these CPS, namely

| (56) |

as our CPS of interest and aim to compute canonical paths to .

| (a) | (b) | (c) |

|---|---|---|

|

|

|

Now given an initial state with, e.g., and aiming at a CP to , i.e., the CPS associated with , we have the situation sketched in Fig.8(c). The only possible co-state choice to end in the CPS lies on the heteroclinic connection from to . Thus, which is the only costate which influences the states, can take values in . The state dynamics are sketched by the red triangles for with () for (). Since we need to choose sufficiently small such that to have , and at the same time we need on the black –heteroclinic to . The argument for works similarly.

We can also explicitly compute the Floquet multipliers of and the associated projections. In polar coordinates, the variational equation (37) is autonomous, namely

| (57) |

with eigenvalues . Since (57) is autonomous we obtain the multipliers by exponentiation of , namely

| (58) |

Clearly, additional to the trivial multiplier we have one stable multiplier and two unstable multipliers . Similarly, we can also compute the projection onto the center unstable eigenspace in Cartesian coordinates (which depends on the target point ) analytically. Moreover,

| as or , | (59) |

and conversely as or , and this (and the analytical projection, implemented in a testing function anaproj) can be used to tune and test the convergence behavior of the CPs in the numerics.

3.1.2 pde2path implementation and results

Table 6 lists the main files for the implementation of (54). Even though we do not need the bifurcation methods of pde2path, we implement the ODE (54) as a pde2path problem via the convenience function toyinit, because the OC routines reuse these basic pde2path data structures. To show the setup, in cmds_basic (Listing 11), we compute some CPs with easy parameter settings, namely , which yields for the “leading” Floquet multiplier, and hence fast convergence to the CPS. See Fig. 9 for some basic results, which were also used to generate the blue curve in Fig. 8(c). For convenience we outsourced the main setup in ocinit_sp, see Listing 12, which also recalls the meaning of the most important parameters. Additionally, there are some helper functions for plotting.

| cmds_basic | computes canonical paths with easy parameter setting. |

| cmds_advanced | canonical paths with advanced parameter setting, i.e. Floquet-multipliers near . |

| toyinit | init routine; set the limit cycle as a pde2path struct with standard parameters. |

| ocinit_sp | local extension of ocinit, resetting a number of parameters |

| sG, sGjac | rhs side of (54) resp. the Jacobian |

| anaproj | computes the monodromy matrix analytically |

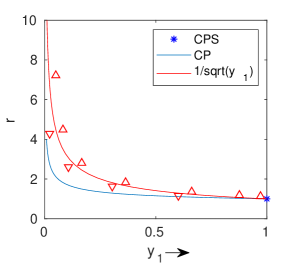

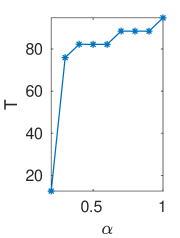

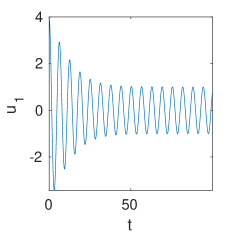

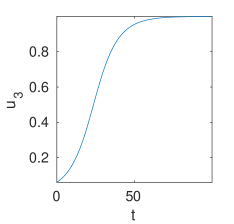

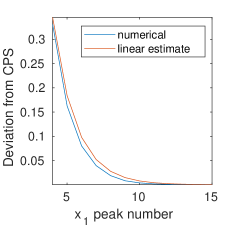

In cmds_advanced we essentially decrease (to ) which makes the problem more expensive due to slow convergence to , cf. (59). For we obtain for the leading stable multiplier. Intuitively, a change of correspond to a rescaling of time in the costates by , i.e., small reduces the speed of the costates. Then we expect that a canonical path spirals around the CPS several times while approaching it, and hence a long truncation time will be necessary for its computation. Figure 10(a) depicts typical results. We also compare the analytical and numerical Floquet multipliers, and generally find good agreement only for reasonably fine –discretizations. In Fig. 10(b) we compare the deviation of the –maxima of from with the asymptotic analytical prediction, showing rather good agreement, see Cell 2 of cmds_advanced.

| (a) | (b) | (c) |

|---|---|---|

|

|

|

3.2 Optimal pollution mitigation

As an example for an OC problem with Hopf bifurcations we consider

| (60a) | |||

| with discount rate , and where as in §2.1 and §2.2 is the spatially averaged current value function, with here the local current value, . The state evolution is | |||

| (60b) | |||

with Neumann BCs on , where models the emissions of some firms, and is the pollution stock, while the control models the firms’ abatement policies. In , and are the firms’ value of emissions and costs of pollution, and are the costs for abatement, and in (60b) is the recovery function of the environment. Again, the in (60a) runs over all admissible controls , meaning that , and we do not consider active control or state constraints. The associated ODE OC problem (no –dependence of ) was set up and analyzed in [TW96, Wir00]; in suitable parameter regimes it shows Hopf bifurcations of periodic orbits for the associated canonical (ODE) system. See also, e.g., [DF91, HMN92, Wir96, KGF+02, GCF+08] for results about the occurrence of Hopf bifurcations and optimal periodic solutions in ODE OC problems.

Setting , , and introducing the co–states (Lagrange multipliers)

and the (local current value) Hamiltonian , by Pontryagins Maximum Principle we obtain

| (61a) | ||||

| (61b) | ||||

where on , and

| (62) |

Finally we set , and write (61) as

| (63) |

where diag, .

For all parameter values, (63) has the spatially homogeneous CSS

We use similar parameter ranges as in [Wir00], namely

| (64) |

consider (63) over , and set the diffusion constants to .

Remark 3.1.

a) The motivation for the choice of is to have the first (for increasing ) Hopf bifurcation to a spatially patterned branch, and the second to a spatially uniform Hopf branch, because the former is more interesting from the PDE point of view. We use that the Hopf bifurcations for the model (63) can be analyzed by a simple modification of [Wir00, Appendix A]. We find that for branches with spatial wave number the necessary condition for Hopf bifurcation, from [Wir00, (A.5)], becomes . Since , a convenient way to first fulfill for is to choose , such that for the factor is the crucial one.

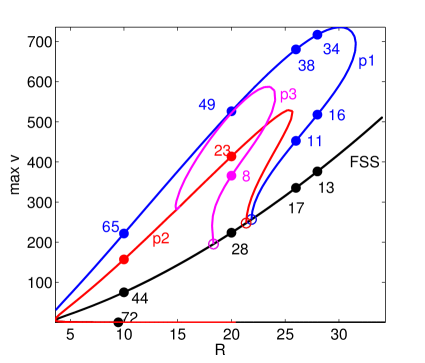

b) Even though we do not specify the units, may be considered quite large, in the following sense. Typical periods of the CPS will be between 20 and 40, and, moreover, CPs starting not close to these CPSs will need times scales (and larger) for convergence to the CPSs, but means that the large time () behavior of a CP hardly plays a role for the value of the CP, as the discounted current value drops to . Thus, our example turns out to be somewhat academic, but nevertheless it will show the robustness of our approach.

c) In the literature, most of the (ODE) OC examples with canonical periodic states show these at rather large discount rates, see, e.g., [HMN92, KGF+02]. An exception is for instance the resource management model in [BPS01], where (ODE) CPSs are found at discount rates near . We have also implemented this example, including a PDE setting, but its main drawback, already hinted at in [BPS01], is that already in the ODE setting it is extremely rich in CPSs, which undergo several period doubling and fold bifurcations, and the smaller is again offset by rather long periods (between 20 and 60). In summary, we focus on the pollution example because it gives a clear and robust bifurcation picture.

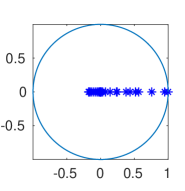

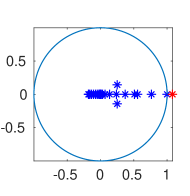

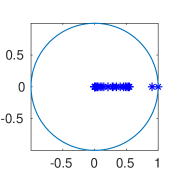

| (a) spectrum of , | (b) bifurcation diagram | (c) time series on h2/pt17 (spat. homogen. branch) | |

|

|

|

|

| (d) sample plots at h1/pt8 | |||

|

|

|

|

| (e) the smallest at h1/pt8 | (f) for the largest at h1/pt8 | (g) the smallest at h1/pt10 and at h2/pt17 | |

|

|

|

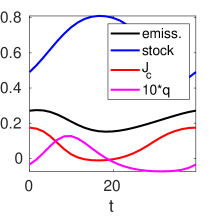

The implementation of (63) works as usual, and, moreover, the computation of the bifurcation diagram of CSS and CPS, and of the Floquet multipliers, is already explained in [Uec19a, Uec19c], and the novelty here is the computation of CPs to the CPSs in a full PDE setting. Table 7 gives a few comments on the used files. In Figure 11 (essentially already contained in [Uec19a]) we give some basic results for (63) with a coarse spatial discretization of by only points (and thus ). (a) shows the full spectrum of the linearization of (63) around at . (b) shows a basic bifurcation diagram. At there bifurcates a Hopf branch h1 with spatial wave number , and at a spatially homogeneous () Hopf branch h2 bifurcates subcritically with a fold at . (c) shows the pertinent time series on h2/pt17. As should be expected, is large when the pollution stock is low and emissions are high, and the pollution stock follows the emissions with some delay. In (b) we plot over . For the CSS this is again simply , but for the periodic orbits we take into account the phase, which is free for (63). If is a periodic solution of (63), then, for , we consider

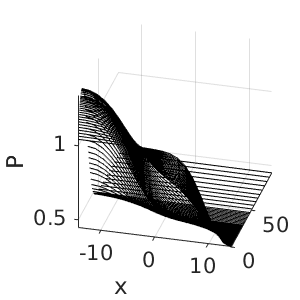

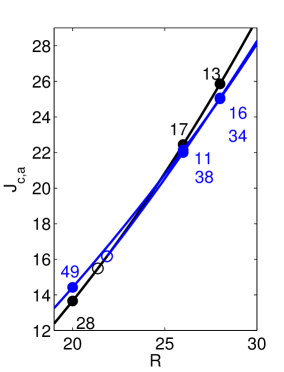

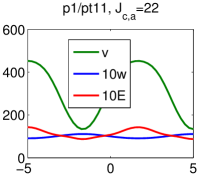

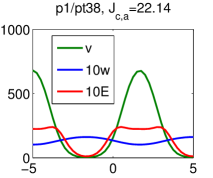

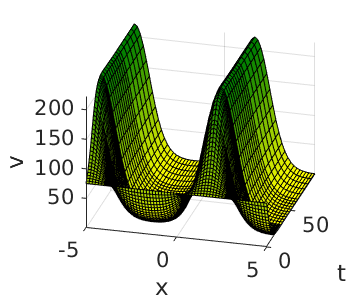

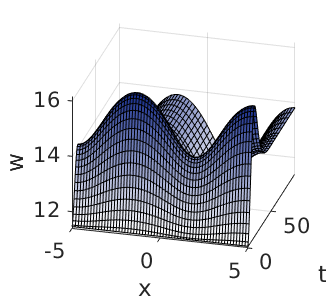

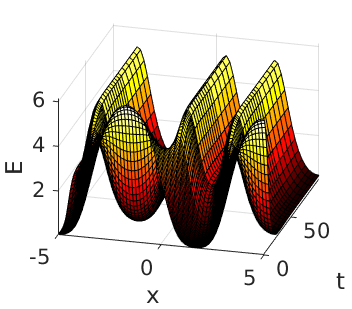

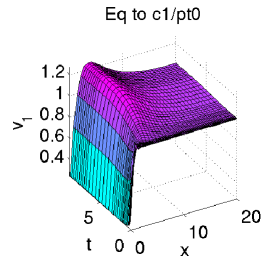

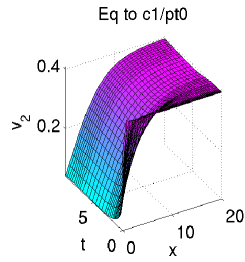

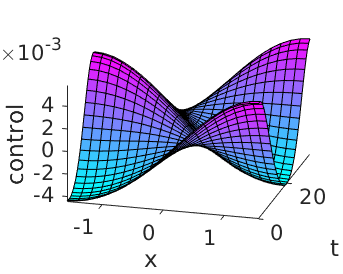

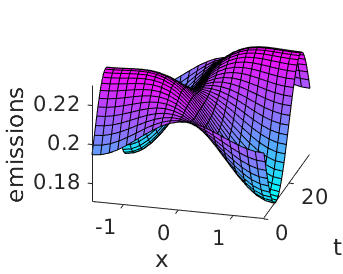

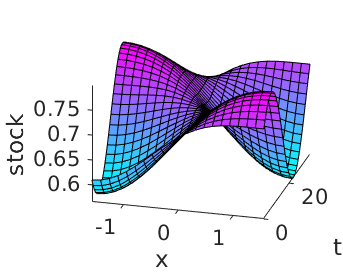

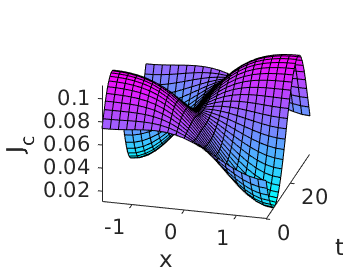

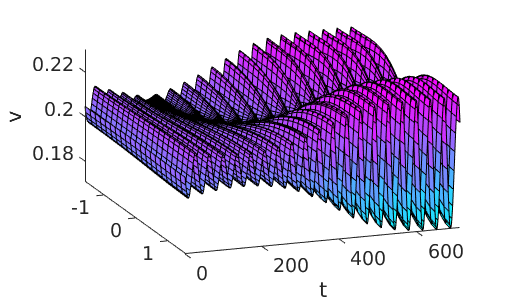

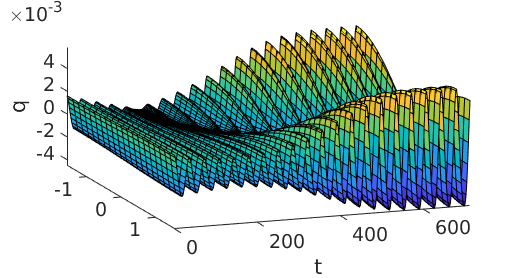

which in general may depend on the phase, and for h2 in (c) we plot for (full red line) and (dashed red line). For the spatially periodic branch h1, averages out in and hence only weakly depends on . Thus, we first conclude that for the spatially patterned periodic orbits from h1 give the highest , while for this is obtained from h2 with the correct phase. The example plots (d) at h1/pt8 illustrate the spatio-temporal dependence of , , and on the patterned CPS.

| bdcmds,cpcmds | bifurcation diagram of CSS and CPS, and computation of some CPs |

| cpplot, polldiagn | plot of CPs, computation and plotting of diagnostics for CPs. |

It remains to

-

•

compute the defects of the CSS and of periodic orbits on the bifurcating branches,

-

•

compute CPs to saddle point CSSs and CPSs.

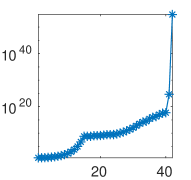

For we find that it starts with at , and, as expected, increases by 2 at each Hopf point. Below we shall focus on CPs to the CPSs h1/pt8 and h2/pt17, and in Fig. 11(e–g) we illustrate typical multiplier spectra, computed with pqzschur, which yields for all computations, i.e., a very accurate trivial multiplier, and hence we trust it. The large multipliers are very large, i.e., and larger, even for the coarse space discretization, as should be expected from the spectrum in Fig. 11(a).

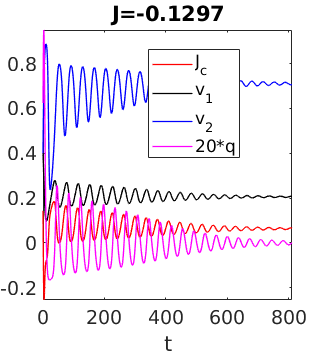

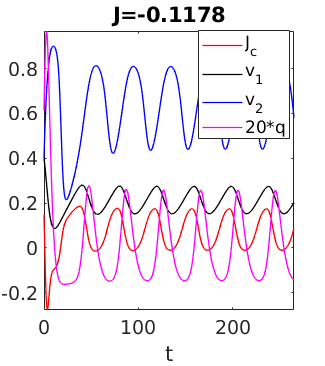

On h1 we find up to pt9, see (e) for the smallest multipliers at pt8, and (f) for for the large ones, which are mostly real. For larger the h1 branch looses stability by a (second) multiplier going through 1, and in fact at h1/pt8 we have , which suggests a slow convergence of CPs to the CPS. On h2 we start with , but after the fold until , after which increases again by multipliers going though 1. At pt17 we have , again suggesting slow convergence.

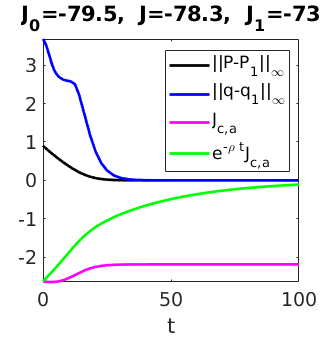

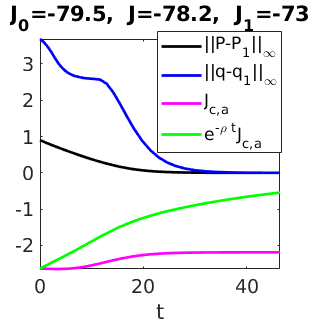

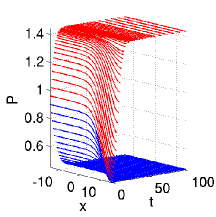

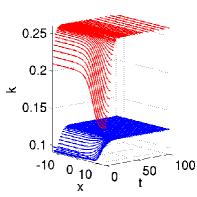

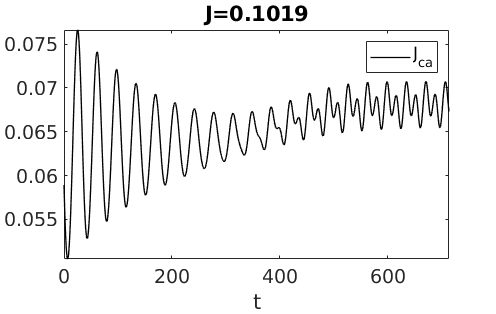

Nevertheless, the computation of CPs (from various initial states) to the CPSs works quite robustly, and in Fig. 12 we present some sample results from cpcmds, and from pollODE/cpcmdsode, which treats the same problem as an ODE. The idea is that the behavior of the spatially homogeneous CPs can be studied much faster in the ODE setting due to much less DoF. Also, for instance the ODE multipliers at h2/pt17 are , i.e., . The associated ODE paths then also exist in the PDE as spatially homogeneous paths, and show the same convergence behavioras long as the instability which yields the existence of the patterned CPS h1 plays no role.

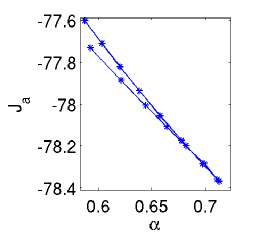

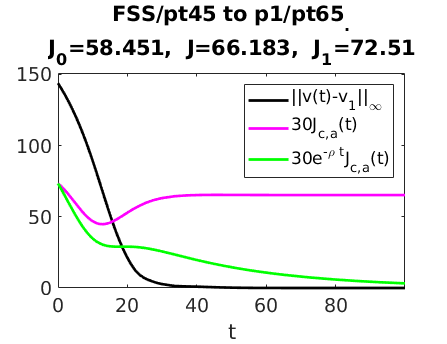

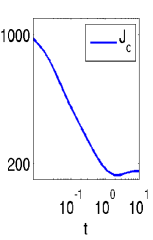

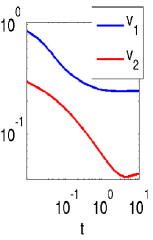

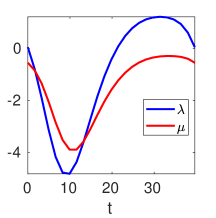

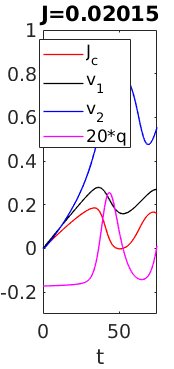

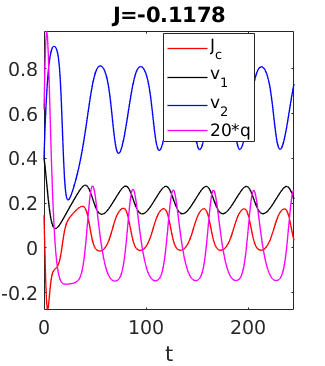

In Fig. 12(a)–(d) we show CPs to the CSS at (starting from two different initial states), and to the homogeneous CPS h2/pt17 at . The convergence to the CSS is very slow as we are close to the Hopf bifurcation and hence the slowest decay rate is . For (significant initial emissions and pollution) we obtain a negative value , as initially the emission are strongly reduced and the initial abatement investments are high. For (no initial emissions and pollution) we have due to increasing initial emission and negative initial abatement investments. To compute CPs to the CPS, we start with a rather small and for use the extension of the CP by copies of the CPS during the continuation in . This leads to the extension of to about , and to for the final deviation from the target , and we also illustrate how to a posteriori decrease this deviation to . We also run a few further tests, for instance computing CPs from the same ICs to shifted CPSs, e.g., h2 shifted by half a period. As expected, shifting the base point on the CPS just expands or shortens the truncation time by half a period, see Fig. 12(d).

| (a) | (b) | (c) | (d) |

|---|---|---|---|

|

|

|

|

| (e) |

|

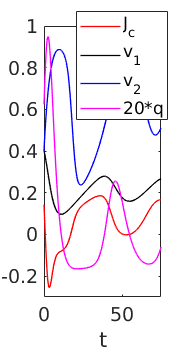

In Fig. 12(e) we give one exemplary CP to the inhomogeneous CPS at , starting with ICs . The ICs are thus quite close to the CSS, which is stable in the ODE, but (very weakly) unstable in the PDE, as we are beyond the primary Hopf bifurcation. Consequently, the associated CP transiently decays towards the CSS, before the inhomogeneous instability manifests and the CP converges to the inhomogeneous CPS. In summary, these examples show that our algorithms allow a robust control towards CSSs and CPSs with the SPP.

4 Summary and outlook

We explained how to study OC problems of class (1) in pde2path. The class (1) is quite general, and with the pde2path machinery we have a powerful tool to first study the bifurcations of CSS/CPS. For the computation of canonical paths to CSSs and CPSs, our Algorithms 1 and 2 implement for the class (1) variants of the connecting orbits methods explained for ODE problems in [GCF+08, Chapter 7]. For the CPS case, because of the very small and very large mutipliers present due diffusion and anti–diffusion, an important technical issue is the use of pqzschur to compute the projection onto the center–unstable eigenspace. Similarly, the idea to start with a rather small truncation time and then using (42), i.e., adding copies of the CPS to the CP to ensure convergence, seems crucial to have a fast and robust algorithm.

There also is a number of issues we do not address (yet), for instance inequality constraints that frequently occur in OC problems. In our examples we can simply check the natural constraints (such as in the sloc example) a posteriori and find them to be always fulfilled, i.e., inactive. If such constraints become active the problem becomes much more complicated.

References

- [AAC11] S. Aniţa, V. Arnăutu, and V. Capasso. An introduction to optimal control problems in life sciences and economics. Birkhäuser/Springer, New York, 2011.

- [Bey90] W.-J. Beyn. The numerical computation of connecting orbits in dynamical systems. IMA J. Numer. Anal., 10(3):379–405, 1990.

- [BPS01] W.J. Beyn, Th. Pampel, and W. Semmler. Dynamic optimization and Skiba sets in economic examples. Optimal Control Applications and Methods, 22(5–6):251–280, 2001.

- [BX08] W.A. Brock and A. Xepapadeas. Diffusion-induced instability and pattern formation in infinite horizon recursive optimal control. Journal of Economic Dynamics and Control, 32(9):2745–2787, 2008.

- [BX10] W. Brock and A. Xepapadeas. Pattern formation, spatial externalities and regulation in coupled economic–ecological systems. Journal of Environmental Economics and Management, 59(2):149–164, 2010.

- [DCF+97] E. Doedel, A. R. Champneys, Th. F. Fairgrieve, Y. A. Kuznetsov, Bj. Sandstede, and X. Wang. AUTO: Continuation and bifurcation software for ordinary differential equations (with HomCont). http://indy.cs.concordia.ca/auto/, 1997.

- [DF91] E. Dockner and G. Feichtinger. On the optimality of limit cycles in dynamic economic systems. Journal of Economics, 53:31–50, 1991.

- [DKvVK08] E. J. Doedel, B. W. Kooi, G. A. K. van Voorn, and Yu. A. Kuznetsov. Continuation of connecting orbits in 3D-ODEs. I. Point-to-cycle connections. Internat. J. Bifur. Chaos Appl. Sci. Engrg., 18(7):1889–1903, 2008.

- [DKvVK09] E. J. Doedel, B. W. Kooi, G. A. K. van Voorn, and Yu. A. Kuznetsov. Continuation of connecting orbits in 3D-ODEs. II. Cycle-to-cycle connections. Internat. J. Bifur. Chaos Appl. Sci. Engrg., 19(1):159–169, 2009.

- [dWDR+18] H. de Witt, T. Dohnal, J.D.M. Rademacher, H. Uecker, and D. Wetzel. pde2path - Quickstart guide and reference card, 2018.

- [GCF+08] D. Grass, J.P. Caulkins, G. Feichtinger, G. Tragler, and D.A. Behrens. Optimal Control of Nonlinear Processes: With Applications in Drugs, Corruption, and Terror. Springer, 2008.

- [Gra15] D. Grass. From 0D to 1D spatial models using OCMat. Technical report, ORCOS, 2015.

- [GU17] D. Grass and H. Uecker. Optimal management and spatial patterns in a distributed shallow lake model. Electr. J. Differential Equations, 2017(1):1–21, 2017.

- [GUU19] D. Grass, H. Uecker, and T. Upmann. Optimal fishery with coastal catch. Natural Resource Modelling, (e12235), 2019.

- [HMN92] R. F. Hartl, A. Mehlmann, and A. Novak. Cycles of fear: periodic bloodsucking rates for vampires. J. Optim. Theory Appl., 75(3):559–568, 1992.

- [KGF+02] P. Kort, A. Greiner, G. Feichtinger, J Haunschmied, A. Novak, and R. Hartl. Environmental effects of tourism industry investments: an inter‐temporal trade‐off. Optim. Control – Appl. and Methods, 23(1):1–19, 2002.

- [Kre01] D. Kressner. An efficient and reliable implementation of the periodic qz algorithm. In IFAC Workshop on Periodic Control Systems. 2001.

- [KW10] T. Kiseleva and F.O.O. Wagener. Bifurcations of optimal vector fields in the shallow lake system. Journal of Economic Dynamics and Control, 34(5):825–843, 2010.

- [MS02] F. Mazzia and I. Sgura. Numerical approximation of nonlinear BVPs by means of BVMs. Applied Numerical Mathematics, 42(1–3):337–352, 2002. Numerical Solution of Differential and Differential-Algebraic Equations, 4-9 September 2000, Halle, Germany.

- [MST09] F. Mazzia, A. Sestini, and D. Trigiante. The continuous extension of the B-spline linear multistep methods for BVPs on non-uniform meshes. Applied Numerical Mathematics, 59(3–4):723–738, 2009.

- [MT04] F. Mazzia and D. Trigiante. A hybrid mesh selection strategy based on conditioning for boundary value ODE problems. Numerical Algorithms, 36(2):169–187, 2004.

- [Pam01] Th. Pampel. Numerical approximation of connecting orbits with asymptotic rate. Numerische Mathematik, 90(2):309–348, 2001.

- [RU18] J.D.M. Rademacher and H. Uecker. The OOPDE setting of pde2path – a tutorial via some Allen-Cahn models, 2018.

- [RZ99a] J. P. Raymond and H. Zidani. Hamiltonian Pontryagin’s principles for control problems governed by semilinear parabolic equations. Appl. Math. Optim., 39(2):143–177, 1999.

- [RZ99b] J. P. Raymond and H. Zidani. Pontryagin’s principle for time-optimal problems. J. Optim. Theory Appl., 101(2):375–402, 1999.

- [Ski78] A. K. Skiba. Optimal growth with a convex-concave production function. Econometrica, 46(3):527–539, 1978.

- [Tau15] N. Tauchnitz. The Pontryagin maximum principle for nonlinear optimal control problems with infinite horizon. J. Optim. Theory Appl., 167(1):27–48, 2015.

- [Trö10] Fredi Tröltzsch. Optimal control of partial differential equations, volume 112 of Graduate Studies in Mathematics. American Mathematical Society, Providence, RI, 2010.

- [TW96] O. Tahvonen and C. Withagen. Optimality of irreversible pollution accumulation. Journal of Environmental Economics and Management, 20:1775–1795, 1996.

- [Uec16] H. Uecker. Optimal harvesting and spatial patterns in a semi arid vegetation system. Natural Resource Modelling, 29(2):229–258, 2016.

- [Uec19a] H. Uecker. Hopf bifurcation and time periodic orbits with pde2path – algorithms and applications. Comm. in Comp. Phys, 25(3):812–852, 2019.

- [Uec19b] H. Uecker. User guide on Hopf bifurcation and time periodic orbits with pde2path, 2019. Available at [Uec19d].

- [Uec19c] H. Uecker. User guide on Hopf bifurcation and time periodic orbits with pde2path, 2019.

- [Uec19d] H. Uecker. www.staff.uni-oldenburg.de/hannes.uecker/pde2path, 2019.

- [UWR14] H. Uecker, D. Wetzel, and J.D.M. Rademacher. pde2path – a Matlab package for continuation and bifurcation in 2D elliptic systems. NMTMA, 7:58–106, 2014.

- [Wir96] Fr. Wirl. Pathways to Hopf bifurcation in dynamic, continuous time optimization problems. Journal of Optimization Theory and Applications, 91:299–320, 1996.

- [Wir00] Fr. Wirl. Optimal accumulation of pollution: Existence of limit cycles for the social optimum and the competitive equilibrium. Journal of Economic Dynamics and Control, 24(2):297–306, 2000.