Comparative Study of Two Extensions of Heston Stochastic Volatility Model

Abstract

In the option valuation literature, the shortcomings of one factor stochastic volatility models have traditionally been addressed by adding jumps to the stock price process. An alternate approach in the context of option pricing and calibration of implied volatility is the addition of a few other factors to the volatility process. This paper contemplates two extensions of the Heston stochastic volatility model. Out of which, one considers the addition of jumps to the stock price process (a stochastic volatility jump diffusion model) and another considers an additional stochastic volatility factor varying at a different time scale (a multiscale stochastic volatility model). An empirical analysis is carried out on the market data of options with different strike prices and maturities, to compare the pricing performance of these models and to capture their implied volatility fit. The unknown parameters of these models are calibrated using the non-linear least square optimization. It has been found that the multiscale stochastic volatility model performs better than the Heston stochastic volatility model and the stochastic volatility jump diffusion model for the data set under consideration.

Keywords. Stochastic volatility; Multiscale stochastic volatility; Mean reversion; Option pricing; Time scales; Jump diffusion

1 Introduction

The derivative pricing model proposed by Black and Scholes[5] assumes the volatility to be constant and asset log-return distribution as Gaussian. Empirically, the volatility is not constant but it smiles and the log-return distributions are non-Gaussian in nature characterised by heavy tails and high peaks. A wide range of research has been done to improve upon classical Black-Scholes model. The model has been extended to include either constant volatility with jumps(e.g. jump diffusion (JD) models of Merton[15] and Kou[13]) or to consider volatility itself as a continuous time stochastic process(e.g. stochastic volatility models given by Hull and White[11], Scott[17], Wiggins[21], Stein and Stein[20], Heston[10] and Ball and Roma[3], etc.). Stochastic volatility models allow the volatility to fluctuate randomly and are able to incorporate many stylized facts about volatility namely volatility smile and skew, mean reversion and leverage to name a few.

In the single factor stochastic volatility models, Heston stochastic volatility model is most popular as it gives a fast and easily implemented semi closed form solution for the European options and is relatively economical from the computational point of view. Despite its success and popularity, it has some shortcomings. The model is unable to fit implied volatility across all strikes and maturities particularity for the options with short expiry [12].

Also, Shu and Zhang[19] obtained that the Heston model overprices out-of-money (OTM) and short-term options and it underprices in-the-money (ITM) options.

In the option valuation literature, the shortcomings of one factor stochastic volatility models have traditionally been addressed by adding jumps to the stock price process(e.g. stochastic volatility jump diffusion (SVJ) models of Bates[4], Scott[18] and Pan[16], etc.).

Jumps are added to the stock price dynamics of a stochastic volatility model which improve its pricing performance for the short-term options [2]. An alternate approach is the consideration of multiscale stochastic volatility (MSV) models to address the shortcomings of one factor stochastic volatility models (see [9, 14]). In these models, volatility is driven by several factors varying at different time scales. Alizadeh et al.[1] found the evidence of two factors of volatility with one highly persistent factor and other quickly mean reverting factor. Extending this idea, Fouque et al.[8] proposed a two factor stochastic volatility model with one fast mean reverting factor and another slowly varying factor.

Christoffersen et al.[6] empirically showed that the two-factor models improve one factor models in the term structure dimension as well as in the moneyness dimension.

As both type of models (SVJ or MSV) are the extensions of classical single factor stochastic volatility models, this motivated us to study and compare these two approaches in context of Heston stochastic volatility model.

For this, we have considered two extensions of Heston stochastic volatility model. One is the stochastic volatility jump diffusion model proposed by Yan and Hanson[22] which is an extension of Heston stochastic volatility model by adding jumps to the stock price process with log-uniformly distributed jump amplitude.

The another model is the multiscale stochastic volatility model proposed by Fouque and Lorig[7], in which a fast mean-reverting factor is additionally considered in the framework of Heston stochastic volatility model.

These two models are compared with each other, and also with the Heston stochastic volatility model using SP index options data. Firstly, the model parameters are calibrated using non-linear least square optimization.

Then the models’ fit to the market implied volatility is captured against log moneyness at different time to maturity. The mean relative error of models’ prices with market data is also calculated. We have obtained that the multiscale stochastic volatility model performs better than the other two models.

The rest of the paper is organised as follows: The underlying models has been explained in Section 2. The empirical analysis has been conducted in Section 3, where the calibration of the models’ parameters, models’ fit to market implied volatility and mean relative error of model prices with market data has been reported and the results obtained are discussed. The conclusion has been given in Section 4.

2 Models Under Consideration

Firstly, the two models to be considered for the empirical analysis has been explained.

2.1 Stochastic Volatility Jump Diffusion Model

Yan and Hanson [22] proposed a SVJ model which considers the log-uniform distribution of the jump amplitudes in the stock price process. The model is explained below:

Let be the stock price at time whose dynamics under the risk-neutral probability measure is

| (1) |

where is the risk free interest rate and is the Poisson jump-amplitude with mean . The variance follows the CIR process given by

| (2) |

with as the rate of mean-reversion, as the long-run mean value and as the volatility of variance. The condition must be satisfied to ensure the positivity of the process (2). and are the standard Brownian motions for the stock price process and the volatility process respectively with correlation

is the amplitude mark process which is assumed to be uniformly distributed with density

and is given by

is the standard Poisson jump counting process with jump intensity , is the Poisson sum which is given as

here is the th jump-amplitude random variable and , the mean of jump-amplitude , is given as

Under this model, the pricing formula for the European call option, in terms of log stock price , is given as:

| (3) |

where is the variance at time , is the maturity time, is the strike price and is the risk free interest rate. The subscript in the price is just to specify the price obtained from SVJ model. The same convention is also followed for Heston and MSV model.

For ,

| (4) |

where the characteristic function of is

| (5) |

with and for and for . The other terms are

| (6) |

| (7) |

and

| (8) |

with

and

| (9) |

The unknown parameters of this model are and .

After the SVJ model, the MSV model of Fouque and Lorig [7] is given below.

2.2 Multiscale Stochastic Volatility Model

Fouque and Lorig [7] extended the Heston stochastic volatility model to a MSV model by considering an additional fast mean-reverting volatility factor in the Heston stochastic volatility model. This model is given below.

Under , the dynamics of stock price is given as

| (10) |

here . and are respectively the fast and the slow scale factors of volatility with their dynamics given as

| (11) |

and

| (12) |

, and are the standard Brownian motions for the stock price process and for the fast and the slow factors of volatility respectively with

and

.

and are constants which satisfy and .

The fast factor of volatility, follows the OU process with the mean-reversion rate and volatility of volatility parameter . is very small so that is fast mean-reverting towards its long-run mean . The slow volatility factor , as already explained for SVJ model, is the square root process. It slowly reverts to its long-run mean .

Fouque and Lorig[7] used the perturbation technique to obtain the expression for European call option prices. The asymptotic expansion of price in powers of is given as

| (13) |

They obtained the first order approximation to the price of the European call option as

This price approximation is clearly independent of the fast factor of volatility and depends only on the slow volatility factor . The approximated price is perturbed around the Heston price at the effective correlation , where is the average of with respect to long-run distribution of the volatility factor .

The first order approximation term is

| (14) |

where . For

| (15) |

The characteristic function of is

| (16) |

here

with

| (17) |

All the other terms are already given in Eq.(8) to Eq.(9). The unknown parameters of this model are and .

In the next section, the empirical analysis is conducted to compare these models.

3 Empirical Analysis and Discussion of Results

For the empirical analysis, the data111Data sharing is not applicable to this article as no new data were created or analyzed in this study. of SP index options is considered from January with maturity ranging from days to days and moneyness from to . The risk free rate of interest is the yield on -month U.S. government treasury bill. Firstly, the unknown parameters of each model are calibrated using non-linear least square optimization. Once the parameters are obtained, the models’ fit to the market implied volatilities for the SP index are captured and plotted against log moneyness. To compare the pricing performance, the mean relative error of each model price is calculated corresponding to the market option price data. These methods are explained in following subsections.

3.1 Calibration of Model Parameters

The unknown parameters of Heston stochastic volatility model, SVJ model and MSV model are calibrated using the data of SP index options. Let , and denote the parameter sets of unknown parameters of Heston, SVJ and MSV model respectively , such that

| (18) |

here all of these unknown parameters are already mentioned in Section 2 except ,

which is obtained from the condition of the CIR process (2) such that . Thus, the rate of mean-reversion is obtained from the calibrated values of and .

These parameters are calibrated by non-linear least square optimization using . The objective function is defined as:

| (19) |

| (20) |

| (21) |

where is the market price of call option with maturity . For each expiration , the available collection of strike prices is . Similarly, for a particular value of and , , and are the prices of the European call options with expiration date and exercise price , calculated from the Heston stochastic volatility model with parameter set , SVJ model with the parameter set and MSV model with the parameter set respectively.

The optimal set of parameters , and is obtained which satisfies

| (22) |

Firstly, the optimal parameter set for the Heston stochastic volatility model, , is calibrated.

Once the is obtained, the initial iteration for SVJ model is taken as with the lower and upper bounds for the last three components as and respectively. Similarly, the initial iteration for MSV model is taken as with the lower and upper bounds for last four components as and respectively.

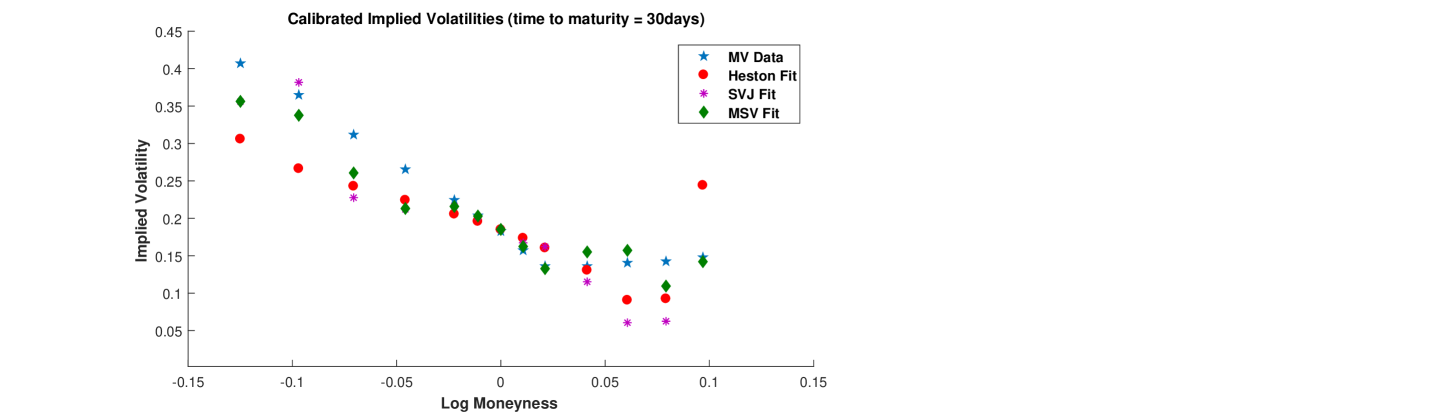

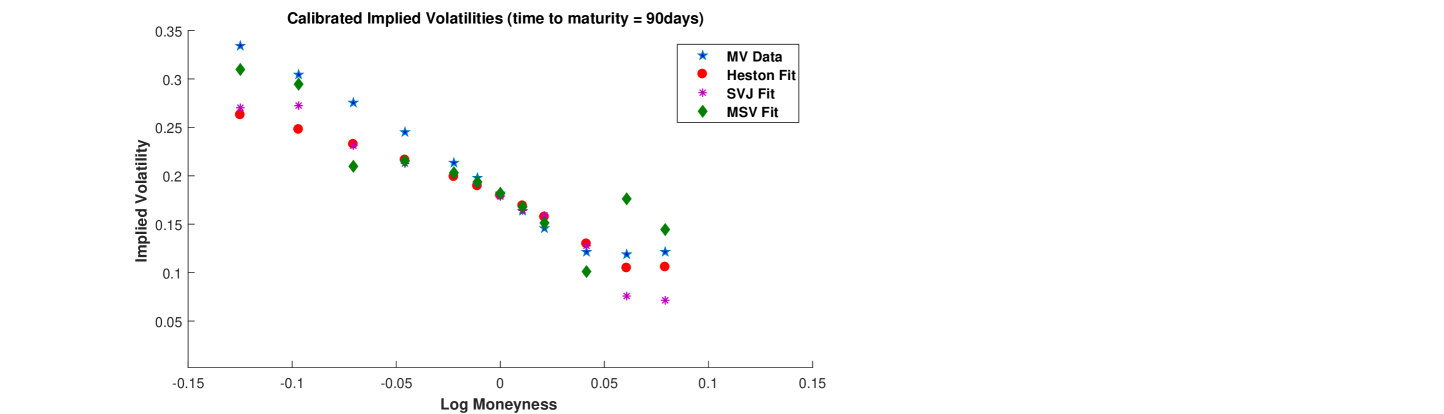

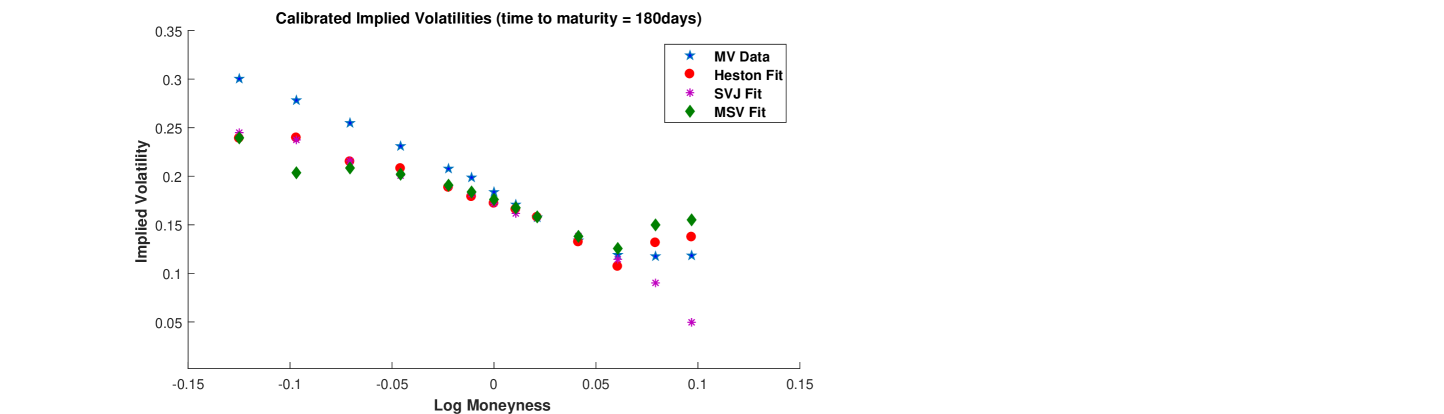

Using the optimal parameter set, the implied volatility fit for all the three models is obtained and is plotted against log moneyness (). The models fit are compared relative to market implied volatility (MV) data. It is given in Fig.1 to Fig.3 for time to maturity days, days and days respectively.

The parameters are calibrated from the whole data but the results are given and discussed for the different maturity times, separately.

Along with this, the mean relative error of the prices obtained from Heston stochastic volatility model, SVJ model and MSV model, with the market data of SP index option, is calculated at different maturity time. It is given in subsection 3.2.

3.2 Mean Relative Error

For a particular model with price at different values of and , the mean relative error (MRE) of model price with respect to market price, at time to maturity is given as

| (23) |

where is the different number of call options that has expiry at time , is the optimal parameter set for the given model.

The mean relative error of Heston stochastic volatility model, SVJ model and MSV model is calculated for SP index data set. The maturity time is taken from days to days. Corresponding to a particular maturity, the strike prices range from to . The results are given in Table 1.

| Models | |||

|---|---|---|---|

| Maturity Time (T) | Heston | SVJ | MSV |

| days | 0.0697 | 0.0499 | 0.0225 |

| days | 0.0874 | 0.0987 | 0.0456 |

| days | 0.0284 | 0.1070 | 0.0380 |

Now, we discuss the results obtained in

Fig.1 to Fig.3 and in Table1. From the models fit to the implied volatility given in Fig.1 to Fig.3, it is clearly observable that the MSV model performs in an improved way in comparison to Heston stochastic volatility model and the SVJ model. For at-the-money (ATM) and near the money options, all the three models give equivalent results. The difference is observable for ITM and OTM options.

In Fig.1, the maturity time is short, that is days. For such options, the Heston model fit to market implied volatility is not good. This supports the empirical findings that the Heston model poorly performs for short term options. The SVJ model performs better than Heston model and MSV model for deep ITM options, but as the log moneyness value increases, MSV model outperforms both Heston model and SVJ model.

In Fig.2, the maturity time is medium, that is days. The implied volatility fit of Heston model is improved for the OTM options. For ITM options, implied volatility fit of MSV model is better than the implied volatility fit of Heston model. The Heston model fit is equivalent to the SVJ model fit to market implied volatility.

In Fig.3, at the longer maturity, which is days, all of the three models give almost similar fit for ITM options but for OTM options the Heston model outperforms the other two models. The implied volatility fit of MSV model is better than the fit of SVJ model to the market implied volatilities. Thus, out of SVJ model and MSV model, the overall fit of MSV model to the market implied volatility is better than SVJ model.

Additionally, from Table1, the pricing performance of three models is compared in terms of mean relative error of models prices with the market option price data. For the short and medium term options with maturity and days respectively, the mean relative error of MSV model is least. Thus the MSV model performs better than the SVJ model and Heston model in pricing. For maturity time days, SVJ model performs better than Heston model in pricing, but for maturity days, Heston model gives better pricing performance.

For the long term options with maturity days, the MSV model performs better than SVJ model and Heston model outperforms the SVJ and MSV model.

Thus, out of SVJ model and MSV model, the overall pricing performance of MSV model is better than SVJ model for the data set under consideration.

4 Conclusion

The two extensions of Heston stochastic volatility model, already proposed in literature, are studied and compared in this paper on the basis of their fit to the market implied volatility and pricing performance. An empirical analysis is conducted on SP index options data and the results are obtained for all the three models. It has been obtained that for the data set under consideration, multiscale stochastic volatility performs better than the stochastic volatility jump model. Thus, the inclusion of additional volatility factor to a stochastic volatility model enhances its fit to the market implied volatility and improves its pricing performance in comparison to the addition of jump factors to the underlying stock price process.

References

- [1] Alizadeh, S., Brandt, M.W. and Diebold, F.X. (2002). Range-Based Estimation of Stochastic Volatility Models. Journal of Finance, 57, 1047 – 1091.

- [2] Bakshi, G., Cao, C. and Chen, Z. (1997). Empirical Performance of Alternative Option Pricing Models. Journal of Finance, 52, 2003 – 2049.

- [3] Ball, C.A. and Roma, A. (1994). Stochastic Volatility Option Pricing. Journal of Financial and Quantitative Analysis, 29, 589 – 607.

- [4] Bates,D. (1996). Jump and Stochastic Volatility:Exchange Rate Processes Implicit in Deutche Mark in Options. Review of Financial Studies 9, 69 – 107.

- [5] Black, F. and Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81, 637 – 654.

- [6] Christoffersen, P., Heston, S. and Jacobs, K. (2009). The Shape and Term Structure of the Index Option Smirk: Why Multifactor Stochastic Volatility Models Work So Well. Management Science, 55, 1914 – 1932.

- [7] Fouque, J.P. and Lorig, M.J. (2011). A Fast Mean-Reverting Correction to Heston’s Stochastic Volatility Model. SIAM Journal of Financial Mathematics, 2, 221 – 254.

- [8] Fouque, J.P., Papanicolaou, G., Sircar, R. and Solna, K. (2003). Multiscale Stochastic Volatility Asymptotics. Multiscale Modeling and Simulation, 2, 22 – 42.

- [9] Fouque, J.P., Papanicolaou, G., Sircar, R. and Solna, K. (2011). Multiscale Stochastic Volatility for Equity, Interest Rate and Credit Derivatives. New York, USA: Cambridge University Press.

- [10] Heston, S.L. (1993). A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options. The Review of Financial Studies, 6, 327 – 343.

- [11] Hull, J., White, A. (1987). The Pricing of Options on Assets with Stochastic Volatilities. Journal of Finance, 42, 281 – 300.

- [12] Gatheral, J. (2006). The Volatility Surface: A Practitioner’s Guide. Hoboken, NJ: Wiley.

- [13] Kou, S.G. (2002). A Jump Diffusion Model for Option Pricing. Management Science, 48, 1086 – 1101.

- [14] Malhotra, G., Srivastava, R. and Taneja, H.C. (2018). Quadratic Approximation of the Slow Factor of Volatility in a Multifactor Stochastic Volatility Model. Journal of Futures Markets, 38, 607 – 624.

- [15] Merton,R.C. (1976). Option Pricing when Underlying Stock Returns are Discontinuous. Journal of Financial Economics. 3, 125 – 144.

- [16] Pan, J. (2002). The Jump-Risk Premia Implicit in Options: Evidence from an Integrated Time-Series Study. Journal of Financial Economics, 63, 3 – 50.

- [17] Scott, L.O. (1987). Option Pricing When the Variance Changes Randomly: Theory, Estimation, and an Application. Journal of Financial and Quantitative Analysis, 22, 419 – 438.

- [18] Scott, L.O. (1997). Pricing Stock Options in a Jump-Diffusion Model with Stochastic Volatility and Interest Rates: Applications of Fourier Inversion Methods. Mathematical Finance, 7, 413 – 426.

- [19] Shu, J. and Zhang, J.E. (2004). Pricing SP Index Options under Stochastic Volatility with the Indirect Inference Method. Journal of Derivatives Accounting, 1, 171 – 186.

- [20] Stein, E.M. and Stein, J.C. (1991). Stock Price Distributions with Stochastic Volatility: An Analytic Approach. The Review of Financial Studies, 4, 727 – 752.

- [21] Wiggins,J. (1987). Option Values under Stochastic Volatilities. Journal of Financial Economics, 19, 351 – 372.

- [22] Yan, G. and Hanson, F.B. (2006). Option Pricing for a Stocahstic Volatility Jump-Diffusion Model with Log-Uniform Jump Amplitudes. Proceedings of the 2006 American control conference,USA, 2989 – 2994.