Certain Semi-Lévy Driven CARMA Processes: Estimation and Forecasting

Abstract

Continuous-time autoregressive moving average (CARMA) process driven by simple semi-Lévy process has periodically correlated property with many potential application in finance. In this paper, we study on the estimation of the parameters of the simple semi-Lévy CARMA (SSLCARMA) process based on the Kalman recursion technique.

We implement this method in conjunction with the state-space representation of the associated process. The accuracy of estimation procedure is assessed in a simulated study. We fit a SSLCARMA(2,1) process to intraday realized volatility of Dow Jones Industrial Average data. Finally, We show that this process provides better in-sample forecasts of these data than the Lévy driven CARMA process after deseasonalized them.

AMS 2010 Subject Classification: 62M10, 60H10, 62M09, 60G51.

Keywords: Periodically correlated process; Realized volatility; SSLCARMA process.

1 Introduction

Modeling of the continuous-time processes has a long history and has been carried out widely in financial econometrics. Early papers of Doop [10], Phillips [15] and Durbin [11] are dealt with properties and statistical analysis of Gaussian continuous-time ARMA (CARMA) processes. Brockwell [2] introduced the Lévy driven CARMA process for irregularly spaced data. These processes which are driven by non-decreasing Lévy processes constitute a general class of stationary processes [8]. Properties of second order Lévy driven CARMA processes and some of their financial applications in modeling stochastic volatilities are discussed by Brockwell [3].

Strongly consistent estimators for the parameters of the subordinator CARMA processes based on uniformly spaced observations are presented in [7].

The Lévy driven CARMA processes have the restriction that the underling process has stationary increments. In contrast, processes with periodically stationary increments such as semi-Lévy processes have a wider application and are more prominent.

The semi-Lévy processes have been extensively studied by Maejima and sato [13]. A class of CARMA processes driven by simple semi-Lévy process which is denoted as SSLCARMA process, introduced by Modarresi et al. [14]. They studied the properties of this process and show that it is periodically correlated (PC).

In this paper, we study a certain class of CARMA() process driven by simple semi-Lévy compound Poisson process. In order to estimate parameters of the SSLCARMA(), first we characterize the sampled process. It is shown that the sampled process is a class of weak ARMA() with independent and periodically identically distributed (ipid) noise. By the state-space representation of the sampled process, we compute the one-step linear prediction using Kalman recursion that is described in [6]. Numerical minimization of the sum of squares of errors gives least squares estimates of the parameters. The accuracy of estimation procedure is illustrated with simulated examples of some SSLCARMA(2,1) processes.

A growing number of research studies follow the intraday return that is determined by the availability of high-frequency financial data. Many of this data shows a PC structure in their squared log intraday returns [16]. For analysing such data, one approach is to remove the PC structure, then fit the corresponding stationary time series by the stationary process [9]. The proposed SSLCARMA(2,1) process provides much better fitting to the 30-minute realized volatility series of 5-minute Dow Jones Industrial Average (DJIA) data which is applied by Brodin and Klüppelberg [9]. For details on the determination of the realized volatility, see [1]. We show the competitive performance of the SSLCARMA process with the Lévy driven CARMA process. For this, we remove the periodicity of the 30-minute realized volatility series using filtering method [9], then fit a Lévy driven CARMA process. Then we show that the SSLCARMA process forecast the sample paths of the 30-minute realized volatility much better than CARMA process.

The rest of the paper is organized as follows. In section 2, the definition and properties of the second order SSLCARMA process are reviewed.

We provide a discrete characterization of the SSLCARMA model through some proper discretization in section 3. The estimation of the parameters is followed by using the Kalman recursion algorithm to present one step ahead predictor model in this section as well. We show the performance of the estimation method by simulated data and also by applying the model to a real data set in section 4. Finally, we analysis the performance of the introduced model in compare with the Lévy driven CARMA in some real data set. All proofs are given in Section 5.

2 Semi-Lévy driven CARMA process

In order to define the simple semi-Lévy driven CARMA, denoted by SSLCARMA process, first we present the simple semi-Lévy (SSL) process. We remind that a semi-Lévy process with period is a subclass of additive process with periodically stationary increments. Let be a partition of the positive real line where , , and for some , where denotes the length of interval . Also, for .

Definition 2.1

The random measure where is the Borel field on positive real line, is called simple semi-Lévy (SSL) random measure with partition and period for some fixed , if

where is a sequence of Lévy random measures that is a copy of for all . Moreover, is called SSL process.

If is a sequence of Poisson measures with rates where , then is a SSL Poisson process with period and rate

| (2.1) |

for , . Therefore,

| (2.2) |

where and is an independent and identically distributed (iid) sequence of random variables with probability distribution is called SSL compound Poisson process with drift.

So, and where , and .

Definition 2.2

Let be a second order semi-Lévy process with period defined by (2.2). The SSLCARMA process , , with parameters is the solution of the th order stochastic differential equation , where denotes differentiation with respect to . The polynomials and have no common factors and the coefficients for , . The corresponding observation and state equations can be written as

| (2.3) |

| (2.4) |

where

Every solution of equation satisfies the following relations for all ,

| (2.5) |

where the paths of have bounded variation on compact intervals. From equation and the independence of the increments of one can easily verify that is Markov. We characterized the moving average representation of the solution in (2.5) and presented some properties of it. Furthermore, we show that the SSLCARMA process is verified to satisfy in some properties, if the following condition hold,

Condition 1

The eigenvalues of the matrix have negative real parts and are distinct and the zeroes of the polynomial are distinct. The assumption of distinct zeroes is not critical since multiple zeroes of can be handled by replacing them with close but distinct zeroes and allowing each of these to converge to the multiple zero.

In the following we extend the state process to a process with index set . For this, we define the semi-Lévy process on the whole real line.

Definition 2.3

Remark 2.1

Proposition 2.1

For a proof, see [14].

Remark 2.2

(i) If is a SSL process defined by (2.6) and the Condition 1 is hold, then the SSLCARMA() process with equations (2.3) and (2.7) is defined as

where is called the kernel of the SSLCARMA process .

(ii) If the kernel is non-negative and the jumps are additionally non-negative, then the process will be non-negative. The kernel is non-negative

if and only if the ratio is completely monotone [17], where the polynomials and is defined in Definition 2.2. For SSLCARMA(2,1) process the condition is equivalent to the statement that the roots of , denoted by and , are both real and that , [7].

3 Estimation procedure

In this section, we concerned with inference for the non-negative SSLCARMA process and deal with the problem of estimation of the parameters of this process. The theoretical properties of the corresponding time varying discrete-time process with equally spaced observation are developed. We apply an estimation method to estimate the coefficients of such sampled process which leads to estimate the parameters of SSLCARMA process.

3.1 Characterization of the sampled process

Following the method of Brockwell et al. [7] and in order to estimate the parameters, we consider a discretization of the process. Let be the SSLCARMA process with period . We assume some equally spaced samples as where and . It is shown in [14] that is a PC with period , so is PC with period . Therefore, we have the following result.

Proposition 3.1

The proof, which is an immediate result of the decomposition of the integrand in (2.7) is the same as the one presented [7].

Corollary 3.2

For , a closed formula for the sampled process is

| (3.2) |

where is an independent and periodically identically distributed (ipid) noise.

Proof: see Appendix A, P1.

Now in the following lemma, assuming some conditions on autocovariance function, we show that any PC process can be represented as a moving average process with ipid noise. So, this lemma can be applied to the sampled SSLCARMA process which has been proved in [14] that is PC process and leads to a class of weak ARMA process with ipid noise.

Lemma 3.3

Let be a zero-mean PC process with period and while is greater than some integer . Then can be represented as a moving average process with ipid noise of order with constant coefficients of some uncorrelated and PC random variables as

Proof: see Appendix A, P2.

Theorem 3.4

Let be an operator and . By applying to each elements of and summing over , the sampled SSLCARMA process yields to

| (3.3) |

where for each fixed , is an ipid sequence with period defined by

Proof: see Appendix A, P3.

Remark 3.1

It follows from (3.3) that is a dependent sequence. So, if the PC process has zero mean, then by Lemma 3.3 there exists an uncorrelated PC noise such that is moving average process with ipid noise of order in which

where and coefficients , , are constant depending on the parameters of the SSLCARMA process. Therefore

| (3.4) |

So, is a class of weak ARMA process with ipid noise and from (3.3),

3.2 Kalman prediction

The Kalman filter is an optimal estimating method that infers parameters from indirect and uncertain observations. It is recursive so that new measurements can be processed as they arrive. This method minimizes the mean square error of the estimated parameters. For more details see [6], chapter 9. In order to present a prescription of the optimal filter we find the prerequisites of the algorithm such as the covariance matrix of the noise and linear predictors.

By Remark 3.1, the centered sampled process , where is period mean, satisfies the class of weak ARMA process (3.4) driven by ipid noise . It follows also from (2.3) that the process has the observation equation

| (3.5) |

where is the centered state vector of . It satisfies the state equation

| (3.6) |

where is a sequence of zero-mean ipid random vectors with covariance matrices

| (3.7) |

in which , and are jump-rates corresponding to the increments of the SSL Poisson random measure on partitions , as assumed in Definition 2.1. For more details regarding (3.6) and (3.7), see Appendix B, B1.

Remark 3.2

Since the sampled process is a PC process with period , the periodic mean is estimated by sample periodic mean

where in which denotes the integer part of , see [12], Chapter 9.

The inferential goal is to estimate of the SSLCARMA parameter vector . We do this by using the Kalman recursions in conjunction with the state-space representation in equations (3.5) and (3.6). We compute the one-step linear predictors in terms of , , based on the Kalman algorithm which is summarized in Table 1. Numerical minimization of the sum of squares of these one-step errors, , with respect to parameters of the model gives least squares estimates of the SSLCARMA coefficients. The Kalman filter algorithm can be roughly organized under the following steps.

| (a) The predictors of the state-space model (3.5) and (3.6) are determined by the one-step predictors , the error covariance matrices and the initial conditions (i) (ii) , where . For more details regarding , see Appendix B, B2. (b) For (i) , (ii) where is defined in (3.7), , and is the transpose of the vector . |

Remark 3.3

In this algorithm we assume that and and are not represented in the predictor but also in . Moreover, the parameter in is omitted. Then by minimizing the sum of the square errors with respect to the coefficients parameters of SSLCARMA process and , are estimated.

4 Data analysis

In this section, we conduct a simulation study to test the estimation procedure for the SSLCARMA parameters and to assess the quality of the estimates in subsection 4.1. Then in subsection 4.2, we apply the introduced model to the intraday realized volatility data for the Dow Jones Industrial Average (DJIA) and by minimization the sum of squared errors we estimate the parameters of the process. The estimation results are compared by the model which is introduced by Brodin and Klüppelberg [9] that is fitted by a Lévy-driven CARMA process after removing its periodicity in subsection 4.3.

4.1 Simulation study

The simulation of SSLCARMA process is followed by the moving average representation (2.7). For this, first we simulate the SSL process represented in (2.2). As a special case, we assume to be a SSL process with period and the lengths of the successive subintervals of each period interval are considered as and . The arrival rates of the semi-Lévy Poisson process on these subintervals are assumed as and Moreover, the jumps are assumed to be exponentially distributed with parameter . We simulate 1000 realizations of the SSLCARMA(2,1) that is specified by the equation

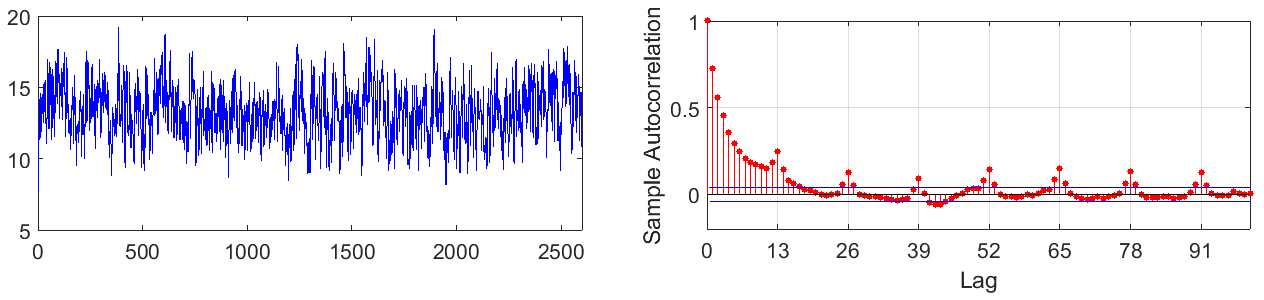

where , and is the SSL compound Poisson process with drift. In this case, the parameters are and and the simulation is for the duration of 200 period intervals. Then, each realization is sampled at spaces . Figure 1, shows the sample path and sample autocorrelation function (ACF) of this SSLCARMA(2,1) process.

For each realization we compute least squared estimators of the parameters of the SSLCARMA(2,1) process. As noted in Remark 3.3, it is not required to estimate the parameter of jump distribution . The sample mean, bias and standard deviation of these estimators are shown in Table 2.

| True | 3 | 0.5 | 2 | 10 | 15 | 3 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | 2.9146 | 0.5026 | 2.0106 | 10.1118 | 14.8977 | 3.1114 | |||||||||||

| Bais | 0.0854 | 0.0026 | 0.0106 | 0.1118 | 0.1023 | 0.1114 | |||||||||||

| Std. dev. | 0.0611 | 0.0145 | 0.0486 | 0.0269 | 0.0250 | 0.0222 |

4.2 Intraday realized volatility for the DJIA

Realized volatility is a non-parametric estimate of the return variation. The most obvious realized volatility measure is the sum of finely-sampled squared return realizations over a fixed time interval as

| (4.1) |

where in which is asset price. One of the striking features of financial time series is that the log returns have negligible correlation while its squared log returns are significantly correlated [4]. Many of high-frequency time series show a PC structure in their squared log returns [16], so according to relation (4.1) the intraday realized volatility have PC structure.

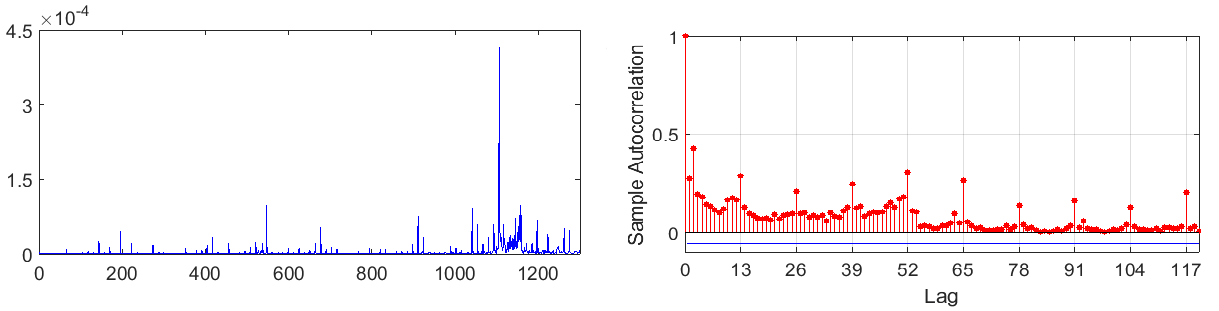

Here, we describe the application of the estimation procedure to the 30-minute realized volatility, denoted by , of the 5-minute DJIA data. This data set is recorded between 9:35 to 16:00 from October 3th, 2017 to February 27th, 2018. There was a total of trading days not including the weekends and holidays with 78 5-minute observations per day, resulting in the total of 7800 5-minute observations. We compute the form these data by (4.1) for . Figure 2 shows the sample paths and the sample ACF of the time series .

It is clear from ACF that the time series have a PC structure with period 13. We fit a SSLCARMA(2,1) model to . For this, we consider the SSL process , defined by (2.6), as the underlying process with period . Furthermore, the lengths of the successive subintervals of each period interval are 10, 2, 1 where corresponding arrival rates of the semi-Lévy Poisson process on these subintervals are and respectively. We use the Kalman algorithm which presented in Table 1 and compute the one-step predictions . By numerical minimization of the sum of squared errors, , where the centered realized volatility in which is followed from Remark 3.2, we estimate the parameters of the SSLCARMA(2,1) process. Table 3, shows the outcomes of estimating the parameters of the SSLCARMA(2,1).

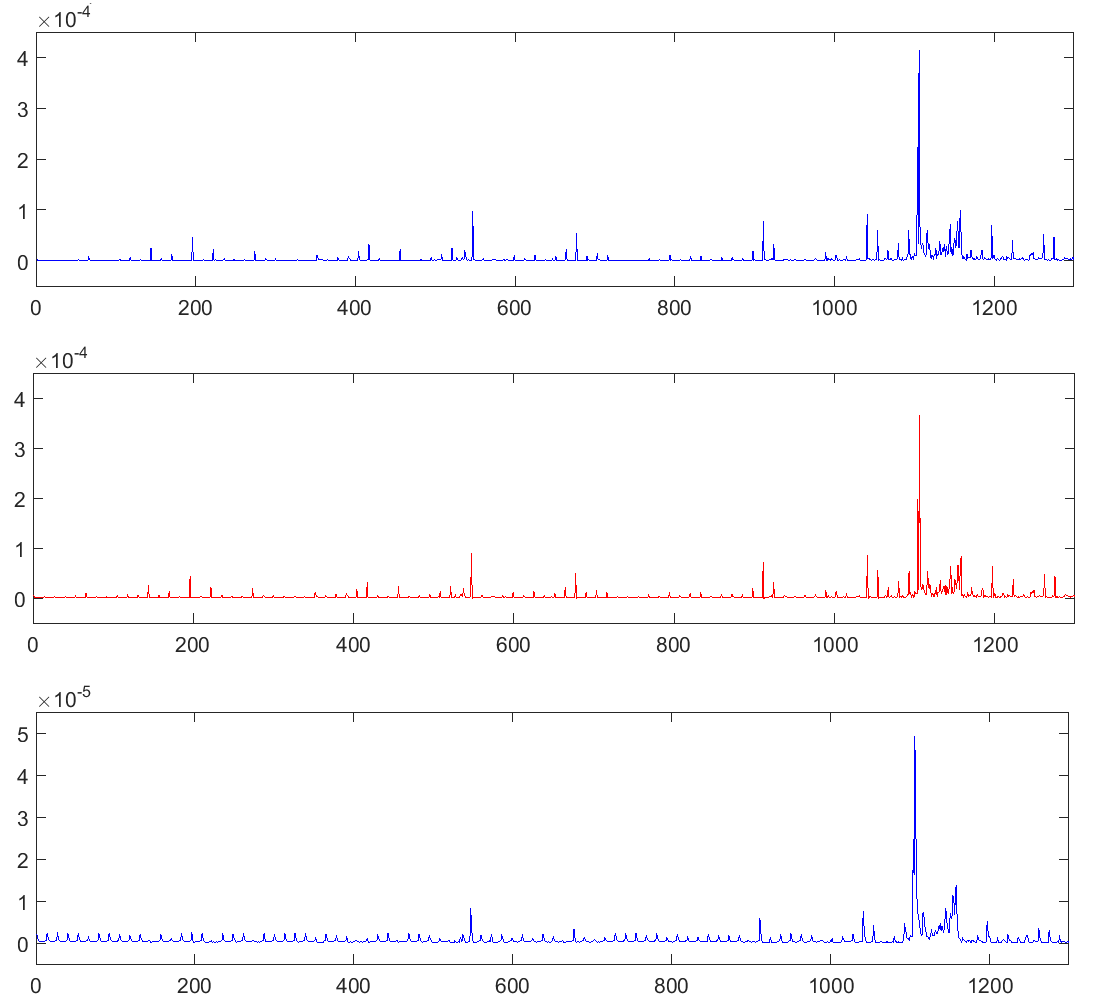

We use these estimators in state-space representation (3.5) and (3.6) and compute the one-step Kalman predictions of the . So, we can be compute the one-step predictions . Figure 3 shows the time series and the for .

4.3 In-sample performance analysis

To compare the performance of the SSLCARMA process with a Lévy driven CARMA process, we consider one-step Kalman prediction errors for the PC time series applied in subsection 4.2.

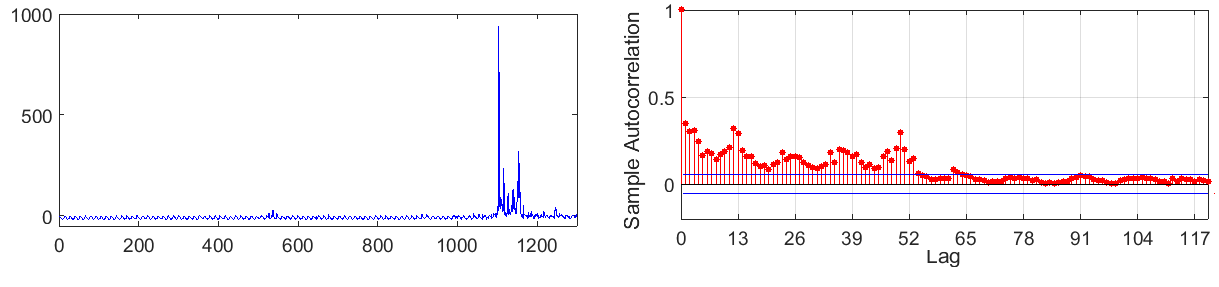

For modeling using the Lévy driven CARMA process, we follow the method of Brodin and Klüppelberg [9], and remove the period of this time series using filtering method in [9],

| (4.2) |

where is the sample mean of and are the seasonality coefficients estimated by

in which and . Figure 4 shows the sample paths and the sample ACF of the filtered time series which is defined by (4.2). As it is shown, the filtered data has no clear periodicity effect.

First, we model the time series by a Lévy driven CARMA() process using the method of the paper [7], based on the assumption that the Lévy process is a compound Poisson process with arrival rate and exponentially distributed jump size. It follows that the sampled process is the weak ARMA() process driven by the white noise sequence. So, the centered sampled process satisfies a weak ARMA process with state-space representation

| (4.3) |

where is a sequence of zero-mean iid random vectors with covariance matrix (for more details see Appendix B, B3). We use the state-space equation (4.3) with error covariance matrix (provided in Appendix B, B4) in Kalman algorithm which presented in Table 1 and compute the one-step predictions . By numerical minimization of the sum of squared errors, where in which , we estimate the parameters of the CARMA(2,1) process as and . We use these estimators in state-space equation (4.3) and compute the corresponding one-step Kalman predictions of the . So, from this and the filtering method (4.2), we predict the intraday realized volatility of the main data as by the followings. So,

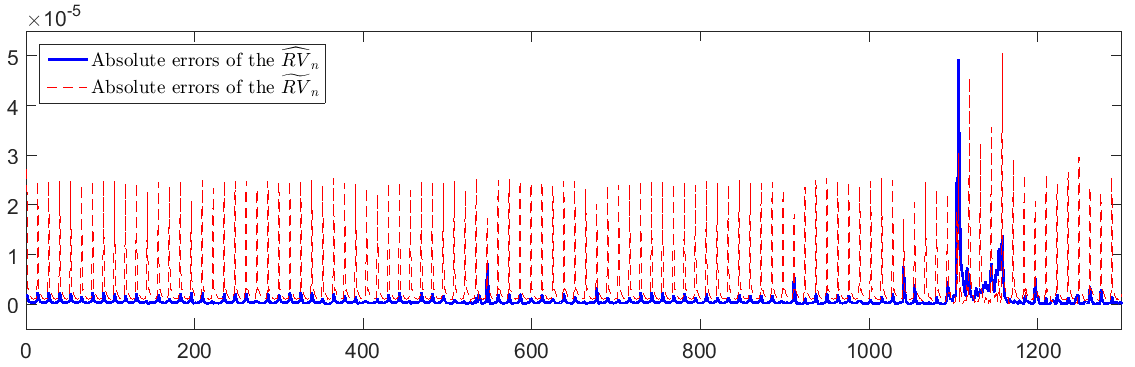

In Figure 5, we illustrate the absolute errors of the one-step Kalman predictions , which is computed from SSLCARMA(2,1), and . The mean absolute error of the and , respectively, are and .

5 Appendix

Appendix A

P 1

: Proof of Corollary 3.2

In discrete form, we can rewrite in (3.1) as

P 2

: Proof of Lemma 3.3

We define the subspace of for each and set

| (5.1) |

where denote the projection mapping onto subspace . Clearly and where is orthogonal complement of subset . Thus for , and and hence . For more details regarding the space and projection, see [5], chapter 2. Furthermore, we can show that

Since is PC with period and norm, , is continuous, we have that

We conclude that is a zero-mean noise with variance where . Now by (5.1), it follows that

The subspace can be decomposed into the two orthogonal subspaces and . Since by the assumption for , therefore and so by the properties of projection mappings and Theorem 2.4.1 in [5] we have

and by denoting and substituting in (5.1) we have .

P 3

: Proof of Theorem 3.4

It follows from that

By denoting and by (3.2), we have

| (5.2) |

Since , it follows from assumption of the theorem that

Therefore, by assuming , we have that, for ,

| (5.3) |

It follows from (5.2) that

| (5.4) |

By replacing the noise and (5.3) in (5.4) we have that

Appendix B

B 1

: According to relation (2.7) we have

| (5.1) |

where . Since and , one can easily check from (5.1) that . Furthermore, the covariance matrix of is

Now we find the covariance matrix in two cases. First when and belong to one subinterval as , so

| (5.2) |

Using (2.6) and the definition of in (2.2), the variance of the increment for is

| (5.3) |

and by changing the variable to we have the relation (3.7). Second, we consider in and in , so

Because of the independency of the increments . Therefore,

that by the same method in first case

by changing the variable to we have that

so we get to the result of relation (3.7).

B 2

: Since is the centered state vector and , it follows from (2.7) that

By a similar method in (5.2), we have . Therefore,

Similar to the relation (5.3), it follows from (2.6) and (2.1) that the variance of the increment for is

| (5.4) |

The last equality follows from the fact that . Let , then by (5.3) and (5.4), we have

By changing the variable to , we have the relation .

B 3

: According to relation , we have

By a similar method in (5.2), it follows that

By changing the variable to , we have .

B 4

: Since is the centered state vector and , we have that So, it follows from Proposition 1 in [7] that .

References

- [1] T. G. Andersen, L. Benzoni (2009). Realized volatility. In Handbook of Financial Time Series (eds T. G. Andersen, R. A. Davis, J.P. Kreiss and Th. Mikosch). Berlin, Heidelberg: Springer-Verlag, 555-75.

- [2] Brockwell, P. J. (2001). Continuous-time ARMA processes. Handbook of Statistics, 19, 249-276. Amsterdam: Elsevier.

- [3] P.J. Brockwell (2009). Lévy driven Continuous-time ARMA processes. Handbook of Financial Time Series, 457-480.

- [4] P.J. Brockwell, E. Chadraa, A. Lindner (2006). Continuous-time GARCH processes. Ann. Appl. Probab., 16(2), 790-826.

- [5] P.J. Brockwell, R.A. Davis (1991). Time Series: Theory and Methods. 2nd edn. New York: Springer-Verlag.

- [6] P.J. Brockwell, R.A. Davis (2016). Introduction to Time Series and Forecasting. 3nd edn. New York: Springer-Verlag.

- [7] P.J. Brockwell, R.A. Davis, Y. Yang (2011). Estimation for non-negative Lévy-driven CARMA processes. J. Bus. Econ. Stat., 29, 250-259.

- [8] P.J. Brockwell, A. Lindner (2015). CARMA processes as solutions of integral equations. Statistics Probability Letters, 107, 221-227.

- [9] E. Brodin, C. Klüppelberg (2009). Modeling, estimation and visualization of multivariate dependence for high-frequency data. Statistical Modelling and Regression Structures, 267-300.

- [10] T. L. Doob (1944). The elementary Gaussian processes. The Annals of Mathematical Statistics, 15, 229-282.

- [11] J. Durbin (1961). Efficient fitting of linear models for continuous stationary time series from discrete data. Bulletin of the International Statistical Institute, 38, 273-281.

- [12] H. L. Hurd, A. G. Miamee (2007). Periodically Correlated Random Sequences: Spectral Theory and Practice. Hoboken: Wiley.

- [13] M. Maejima, K. Sato (1999). Semi-selfsimilar processes. Journal of Theoretical Probability, 11, 347-373.

- [14] N. Modarresi, S. Rezakhah, S. Shoaee (2018). Structure of continuous-time ARMA process driven by semi-Lévy measure. arXiv:1610.01562v2.

- [15] A. W. Phillips (1959). The estimation of parameters in systems of stochastic differential equations. Biometrika, 46, 67-76.

- [16] J. R. Russell, R. F. Engle (2010). Analysis of High-Frequency Data, Handbook of Financial Econometrics: Tools and Techniques, volume 1 in Handbooks in Finance, 383-426.

- [17] H. Tsai, K.S. Chan (2005). A Note on Non-negative Continuous-Time Processes. Journal of the Royal Statistical Society, Ser. B, 67, 589-597.