R-estimators in GARCH models; asymptotics, applications and bootstrapping

Acknowledgements

The quasi-maximum likelihood estimation is a commonly-used method for estimating GARCH parameters. However, such estimators are sensitive to outliers and their asymptotic normality is proved under the finite fourth moment assumption on the underlying error distribution. In this paper, we propose a novel class of estimators of the GARCH parameters based on ranks, called R-estimators, with the property that they are asymptotic normal under the existence of a more than second moment of the errors and are highly efficient. We also consider the weighted bootstrap approximation of the finite sample distributions of the R-estimators. We propose fast algorithms for computing the R-estimators and their bootstrap replicates. Both real data analysis and simulations show the superior performance of the proposed estimators under the normal and heavy-tailed distributions. Our extensive simulations also reveal excellent coverage rates of the weighted bootstrap approximations. In addition, we discuss empirical and simulation results of the R-estimators for the higher order GARCH models such as the GARCH () and asymmetric models such as the GJR model.

Keywords: R-estimation, Empirical process, Higher order GARCH models, Weighted bootstrap.

JEL classification: C13, C14, C22.

1 Introduction

1.1 Robust estimation based on ranks

Consider observations from a financial time series with the following representation

where are unobservable i.i.d. non-degenerate error r.v.’s with mean zero and unit variance and

| (1.1) |

with , , . In the literature, such models are known as the GARCH () model and we assume that is stationary and ergodic.

Estimation of parameters based on ranks of the residuals was discussed by Koul and Ossiander (1994) for the homoscedastic autoregressive model and Mukherjee (2007) for the heterscedastic models. Andrews (2012) proposed a class of R-estimators for the GARCH model using a log-transformation of the squared observations and then minimizing a rank-based residual dispersion function. However, such square-transformation may lead to loss of information under an asymmetric innovation distribution which is undesirable. This motivates us to define R-estimators for the GARCH model that uses the data directly without requiring such transformation. As shown in the motivating example of Section 1.2, our proposed R-estimators can be more efficient than those of Andrews (2012) when asymmetry is introduced for the innovation distribution while retaining efficiency for symmetric innovation distributions. Similar to the linear regression and autoregressive models, the asymptotic normality of R-estimators are derived under smoothness conditions of the innovation probability density function instead of that of the logged and squared innovation as in Andrews (2012).

As expected, the proposed class of R-estimators turns out to be robust and relatively efficient. Unlike the commonly-used quasi-maximum likelihood estimator (QMLE) which is asymptotically normal under the finite fourth moment assumption of the error distribution, the R-estimators turn out to be asymptotically normal under the assumption of only a finite -th moment for some . The efficiency property of the R-estimators is further confirmed based on the simulated data from the GARCH () model and the higher order GARCH () model to fill some void in the literature since the computation and empirical analysis for the higher order GARCH models are not considered widely. Analysis of real data shows that the numerical values of R-estimates can be different from the QMLE and the subsequent analysis of the GARCH residuals shows that such difference may be attributed to the infinite fourth moment of the innovation distribution, which leads to the failure of the QMLE.

Robust estimation of the GARCH parameters has been studied extensively in the literature although the attention has been focused exclusively on the class of M-estimators except in Andrews (2012). See, for example, Berkes and Horváth (2004), Mukherjee (2008), Francq et al. (2011), Fan et al. (2014) and Zhu and Ling (2011) and the references in those papers. One conspicuous issue with previous studies is related to the estimation of an identifiable scale parameter that leads to often more than one stage of estimation. As pointed out by Fan et al. (2014, Section 7.2), such estimation is important for comparing the bias performance. Some simulation study by Fan et al.(2014, Section 7.2) to compare M-estimators with the R-estimators proposed by Andrews (2012) revealed that these two classes of estimators have almost indistinguishable asymptotic performance while the rank-based estimators are slightly better and this provides another motivation for considering R-estimators. However, one problem unaddressed in Andrews (2012) was that the scale was not estimated. In Section 2.3 of this paper, we propose a simple consistent estimate of the scale based on R-estimators and the general principle can be applied for M-estimation as well.

Since the proposed class of the R-estimators are shown to converge to normal distributions, of which the covariance matrices do not have explicit forms, we employ a bootstrap method to approximate the distributions of the R-estimators. Chatterjee and Bose (2005) used the weighted bootstrap method for an estimator defined by smooth estimating equations. We consider weighted bootstrap of R-estimator where the equations are non-smooth functions because the residual ranks are integer-valued and non-smooth. Our extensive simulation study provides evidence that the weighted bootstrap has good coverage rates even under heavy-tailed innovation distribution and with moderate sample size.

Finally, we use the R-estimators for estimating parameters of the GJR () model proposed by Glosten et al. (1993), which is used to estimate the asymmetry effect of financial time series. Simulation results demonstrate good performance of the R-estimators for the GJR model.

The main contributions of the paper are threefold. First, a new class of robust and efficient estimators for the GARCH model parameters is proposed. Second, the asymptotic distributions of the proposed estimators are derived based on weak assumption on the error moments. Third, weighted bootstrap approximations of the distribution of the R-estimators are investigated through extensive simulations. In particular, we propose algorithms for computing the R-estimators and the bootstrap replicates, which are computational friendly and easy to implement.

1.2 A motivating example

|

|

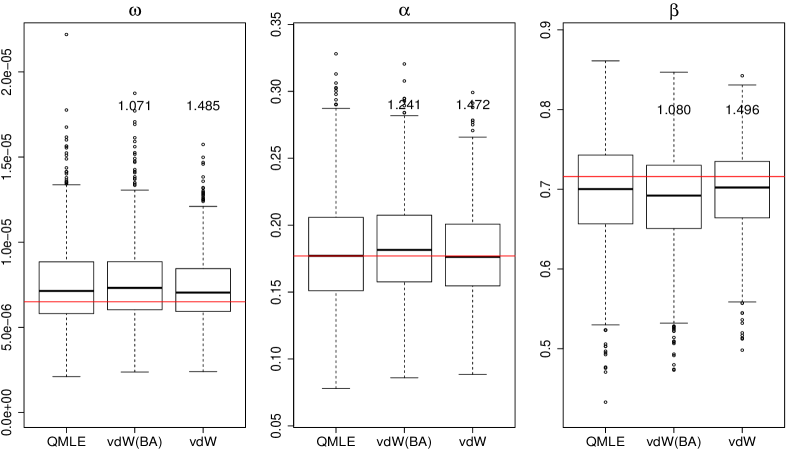

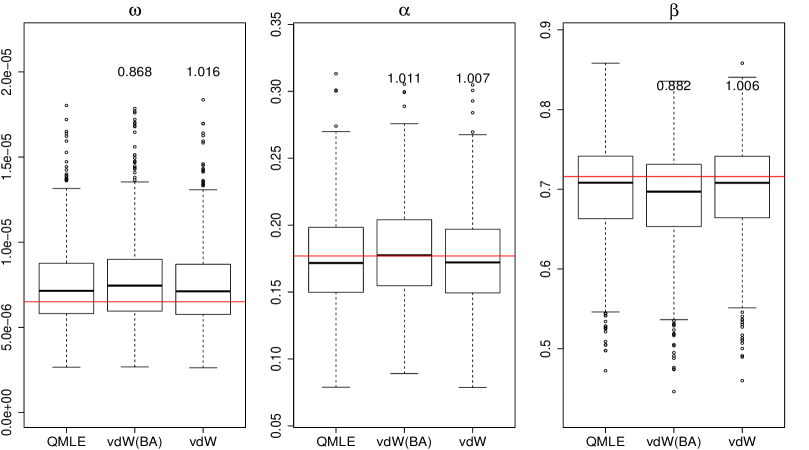

To illustrate the advantages of our proposed R-estimator over the commonly-used QMLE and R-estimator of Andrews (2012) (BA, henceforth), we consider below some simulation results corresponding to the GARCH () model with underlying standardized innovation density being (i) the standard normal distribution and (ii) the skew normal distribution (see e.g. Azzalini and Dalla Valle (1996) for details of such distribution). We generate samples of size with parameter values as in Section 3.2. Simulation results described below are similar to various other choices of the true parameters. To make a fair comparison, for both R-estimators we use the van der Waerden score (vdW, henceforth); our vdW score is given in Section 2.4 while BA’s one has a different form; see Andrews (2012, Section 3) and Section 2.3 for how to obtain a consistent estimator of the unknown parameters. Note that, only R-estimator of is given in Andrews (2012); to compare each component, we provide a consistent estimator of for her R-estimator in Section 2.3. The resulting boxplots of all estimators are displayed in Figure 1 under the skew normal (upper panel) and standard normal (lower panel) innovation densities and the MSE ratios of the QMLE over other estimators are reported.

An inspection of these plots reveals superiority of our R-estimator over the QMLE and BA’s. Under the normal error distribution, the distribution patterns of the R-estimators are quite similar to the QMLE around the true parameter value, and the MSE ratios of the QMLE over the R-estimators are all close to one. However, under the skew normal errors where asymmetry is introduced, our R-estimator has the least dispersion and with a gain of around efficiency over the QMLE, while the BA’s R-estimator still has similar efficiency as the QMLE for and . Therefore, although the BA’s R-estimator achieves efficiency as ours under the normal distribution, it is not as efficient as ours under an asymmetric distribution.

1.3 Outline of the paper

The rest of the paper is organized as follows. Section 2 defines a class of scale-transformed R-estimators based on an asymptotic linearity result of a rank-based central sequence. A consistent estimator of the unknown scalar is provided, and the asymptotic distributions and efficiency of the resulting R-estimators are discussed. Also, we give an algorithm for computing the R-estimators. Section 3 contains empirical and simulation results of the R-estimators. Section 4 describes the weighted bootstrap for the R-estimators and includes extensive simulation results. Section 5 considers an application to the GJR model. Conclusion is given in Section 6. The technique used to establish the asymptotic distribution is included in Appendix A.

2 The class of R-estimators for the GARCH model

In this section, we first define a central sequence of R-criteria based on ranks of the residuals of the GARCH model. We prove the asymptotic uniform linear expansion (2.6) of this central sequence, which enables us to define one-step R-estimator in (2.8) as a root- consistent estimator of a scale-transformed GARCH parameter

| (2.1) |

with a constant satisfying (2.4). Based on and , we are able to derive a consistent estimator of and thus a root- consistent R-estimator of . We discuss some computational aspects and propose a recursive algorithm for computation in Section 2.5.

Notations: Throughout the paper, for a function , we use and to denote its first and second derivatives whenever they exist. We use , , to denote positive constants whose values can possibly change from line to line. Let be a generic random variable (r.v.) with the same distribution as and let and denote the cumulative distribution function (c.d.f.) and probability density function (p.d.f.) of , respectively. Let and be a generic r.v. with the same distribution as . Let and be the c.d.f. and p.d.f. of , respectively. A sequence of stochastic process is said to be (denoted by ) if for every , , where stands for the Euclidean norm.

2.1 Rank-based central sequence

From Lemma 2.3 and Theorem 2.1 of Berkes et al. (2003), of (1.1) has the unique almost sure representation , where are defined in (2.7)-(2.9) of Berkes et al. (2003).

Let denote the true parameter belonging to a compact subset of . A typical element in is denoted by

Define the variance function by

where the coefficients are given in (3.1) of Berkes et al. (2003) with the property , , so that the variance functions satisfy , and

Let be observable approximation of , which is defined by

Let . The maximum likelihood estimator (MLE) is a solution of , where

However, in is usually unknown and we therefore consider an approximation to .

Let be a score function satisfying some regularity conditions which will be discussed later. Examples of are given in Section 2.4. Let denote the rank of among . In linear regression models, the MLE has the same asymptotic efficiency as an R-estimator based on the score function . For the estimation of the scale parameters, the MLE corresponds to the central sequence

| (2.2) |

However, since is unobservable, we therefore replace it by . Let denote the rank of among . We define rank-based central sequence as

| (2.3) |

2.2 One-step R-estimators and their asymptotic distributions

As we will show in this subsection, our R-estimator of is obtained by estimating first and then the unknown scalar .

2.2.1 One-step R-estimators of

To define the R-estimator in terms of the classical Le Cam’s one-step approach as in Hallin and La Vecchia (2017) and Hallin et al. (2019), we derive the asymptotic linearity of the rank-based central sequence under the following assumptions. Let be defined by

so that

| (2.4) |

Define . Since , is strictly decreasing on with range and strictly increasing on with range . The functions on with ranges and are well-defined when the ranges are considered separately.

The following conditions on the distribution of are assumed for the proof of Theorem A.1 in Appendix on the approximation of a scale-perturbed weighted mixed-empirical process by its non-perturbed version.

Assumption (A1). (i). The function is bounded on (and consequently so are the functions and ); functions and are uniformly continuous on when the ranges are considered separately as in the definition of above;

(ii).

(iii). There is a such that .

We remark that Assumption (i) entails that is uniformly Lipschitz continuous in scale in the sense that for some constant and for every , we have .

A more easily verifiable condition for Assumption (ii) can be obtained, for example, when admits the derivative which satisfies that for some ,

In particular, Assumptions (i), (ii) and (iii) in (A1) hold for a wide range of error distributions, including normal, double-exponential, logistic and -distributions with degrees of freedom more than which are considered for simulation study.

We also need the following assumptions on the parameter space and the score function .

Assumption (A2). Denoting by the set of interior points of , we assume that

Assumption (A3). The score function is non-decreasing, right-continuous with only a finite number of points of discontinuity and is bounded on

We now compare our assumptions with those made by Andrews (2012), to be called as BA1, BA2 etc. Assumption BA1 states the stationarity and ergodicity of similar to what we assume but not necessarily finiteness of the variance of . However, estimation of the intercept parameter appearing in Andrews (2012, Equation (2.2)) is not considered there. In this paper, we estimate the intercept parameter under the finite variance assumption of as in (A4). Higher moment assumptions were also made in Fan et al. (2014) while estimating the equivalent scale parameter .

Assumptions BA2 and BA3 are related to the uniqueness of parameters and the existence of the non-degenerate errors and observations. We assume non-degenerate models as is common in the literature. Assumptions BA4 and BA7 are on the score functions which are bounded, non-decreasing and left-continuous. In (A3), we assume that the score functions are bounded, non-decreasing and right-continuous with finite number of discontinuity. Assumptions BA5 and BA6 are on the cdf and pdf of the log of the squared error distribution. We have made analogous assumptions on the error pdf itself and uniform continuity on the -transformed axis in (A1)(i) and (A1)(ii); the later came up as a part of the technical assumptions in using some convergence results of empirical processes to derive the asymptotic distribution of the R-estimators. Assumptions BA8, BA9 and BA10 describe various scenarios related to some of the component parameters equal to zero as in Francq and Zakoian (2007). In (A2), we assume that all parameters are positive as in Berkes and Horváth (2004), Mukherjee (2008) and Francq et al. (2011) in relation to the M-score and this corresponds to BA8.

To state the asymptotic linearity of , we introduce the following notation. Let

| (2.5) |

Let be the r.v. , where is the standard Brownian bridge. Then has mean zero and variance ; see the proof in Lemma A.5 for details. Let , be the empirical distribution function of (which is unobservable),

The following proposition states the asymptotic uniform linearity of .

Proposition 2.1.

Let Assumptions (A1)-(A3) hold. Then for with ,

| (2.6) |

Moreover,

| (2.7) |

where converges in distribution to with mean zero and covariance matrix and .

The above asymptotic linearity allows us to define a class of R-estimators through the one-step approach. Let be a sequence of consistent estimator of ; see Section 2.5 for a construction of . Let be a root- consistent estimator of and, for technical reasons, we assume is asymptotically discrete. More precisely, a sequence is called discrete if there exists such that independent of , takes on at most different values in

see Kresis (1987, Section 4) for details. We remark that here asymptotically discreteness is only of theoretical interest since in practice always has a bounded number of digits; see Le Cam and Yang (2000, Chapter 6) and van der Vaart (1998, Section 5.7) for more details. Then the one-step R-estimator is defined as

| (2.8) |

Note that strictly speaking, the R-estimators based on this definition are not functions of the ranks of the residuals only. However, we borrow the terminology from the regression and the homoscedastic-autoregression settings and still call them (generalized) R-estimators. When, for example, , is an analogue of the Wilcoxon type R-estimator.

The following theorem shows that the R-estimator defined in (2.3) is -consistent estimator of . The proof is given in Appendix A.

Theorem 2.1.

Let Assumptions (A1)-(A3) hold. Then, as ,

| (2.9) |

Hence as , is normal with mean and covariance matrix

2.3 Estimation of

To obtain a root- consistent estimator of , we estimate the unknown scalar under the following mild moment assumption on .

Assumption (A4).

From Bollerslev (1986), a sufficient condition for the GARCH model to be second-order stationary (hence to satisfy Assumption (A4)) is In this case,

Using the ergodicity property, can be estimated from the data by . Also, and can be estimated by and , respectively. Solving the following equation for

we obtain an estimate of as

| (2.10) |

Consequently write in its component-wise form

and let

The following theorem states that is a consistent estimator of and thus is a root- consistent estimator of with asymptotically normal distribution; see Appendix A for its proof.

Theorem 2.2.

Let Assumptions (A1)-(A3) hold. Then, as ,

and

| (2.11) |

Hence as , is normal with mean and covariance matrix

Note that by assuming (A4) and following similar approach as in the proof of Theorem 2.2, one can also obtain consistent estimators of unknown scalars for robust estimators in GARCH models (e.g., M-estimators of Liu and Mukherjee (2020) and R-estimator of Andrews (2012)). For illustration, recall that the R-estimator of Andrews (2012) is root- consistent estimator of

where is the intercept parameter that plays the role of the unknown scalar. Denoting the R-estimator of Andrews (2012) by

a consistent estimator of can be obtained following similar approach as in the proof of Theorem 2.2 as

2.4 Examples of the score functions

Below we cite examples of three commonly-used R-scores; for similar examples of scores in other models, see Mukherjee (2007) and Hallin and La Vecchia (2017).

Example 1 (sign score). Let . Then for symmetric innovation distribution, which coincides with the scale factor of the LAD estimator in Mukherjee (2008). Therefore, the sign R-estimator is expected to be close to the LAD estimator. This is demonstrated later in the real data analysis.

Example 2 (Wilcoxon score). Let so that the range of is symmetric.

Example 3 (van der Waerden (vdW) or normal score). One might also set with denoting the c.d.f. of the standard normal distribution. Notice that unlike the sign and Wilcoxon score, the vdW score is not bounded as and . It thus does not satisfy Assumption (A3). However, an approximating sequence of bounded score functions of on can be constructed as in Andrews (2012). For example, letting

with , then satisfies Assumption (A3) and converges pointwise to the vdW score on . It is demonstrated later using both real data analysis and extensive simulation that the vdW has superior performance compared with the QMLE.

We now provide heuristics for the definition of the R-estimator in (2.2). When the underlying error distribution is known, one can obtain efficient R-estimator by choosing the score function as . Since for large , the empirical distribution function of evaluated at is close to , we have

Therefore, the criteria function of the R-estimator gets close to the MLE which is efficient. This leads to the choice of the vdW, sign and Wilcoxon under the normal, double exponential (DE) and logistic distributions, respectively. This is observed later in simulation study of the R-estimator.

2.5 Computational aspects

Here we discuss some key computational aspects and propose an algorithm to compute and .

First, since depends on the unknown density , it is difficult to have a -consistent initial estimator of . However, due to finite sample size in practice, the one-step procedure is usually iterated a number of times, taking as the new initial estimate, until it stabilizes numerically. This iteration process would mitigate the impact of different initial estimates; see van der Vaart (1998, Section 5.7) and Hallin and La Vecchia (2017) for similar comments. In fact, we observed during our extensive simulation study that irrespective of the choice of the QMLE, LAD or as initial estimates, only few iterations result in the same estimates.

Second, to compute of (2.8), we need which is a consistent estimator of . The matrix can be consistently estimated by

For estimating which is a function of the density , we can use the asymptotic linearity in (2.6). Here with an arbitrarily chosen , we can substitute for and then solve the equation for based on (2.6). A more delicate approach for estimating can be found in Cassart et al. (2010) and Hallin and La Vecchia (2017, Appendix C). Based on our extensive simulation study and real data analysis, it appears that different values of would finally lead to same estimate after some iterations. Consequently, we set during the computation which is the value corresponding to the vdW score under the normal distribution.

In summary, we propose the following iterative Algorithm 1 to compute , with which we can obtain using (2.10) and hence . Codes are available upon request.

-

1.

Compute a preliminary root- consistent estimator and set .

-

2.

for to do

| (2.12) |

Compute using (2.10) and then .

2.6 Asymptotic relative efficiency

In the linear regression and autoregressive models, the asymptotic relative efficiency (ARE) of the R-estimators with respect to (wrt) the least squares estimator is high for a wide array of error distributions. For the GARCH model, we compare the ARE of the R-estimator wrt the QMLE based on Theorem 2.2.

Note that under assumption , the QMLE is asymptotic normal with mean zero and covariance matrix Hence, in view of Theorem 2.2, the ARE of the R-estimator wrt the QMLE is

| (2.13) |

For the sign R-estimator, , and are all zeros. Hence reduces to

where is the identity matrix. Consequently, the ARE of the sign R-estimator wrt the QMLE equals which is under the normal distribution. This corresponds to the classical result of the ARE of the mean absolute deviation wrt the mean square deviation; see, e.g., Huber and Ronchetti (2011, Chapter 1).

For the vdW and Wilcoxon R-estimators, the AREs are more difficult to calculate since and are non-zero. However, in the following simulation study in Table 2, the estimated AREs reveal that the vdW R-estimator, compared with the QMLE, does not lose any efficiency which is a reflection of the well-known Chernoff-Savage phenomenon in the literature on the R-estimation in linear models.

3 Real data analysis and simulation results

This section examines the performance of the R-estimators and compare them with the QMLE by analysing three financial time series and by carrying out extensive Monte Carlo simulation.

3.1 Real data analysis

In this section we fit GARCH () model to three financial time series and compare the proposed three R-estimators with the M-estimators QMLE and LAD discussed in Mukherjee (2008), where the unknown scalar of the LAD can also be estimated by (2.10).

In an earlier work, Muler and Yohai (2008) fitted the the GARCH () model to the Electric Fuel Corporation (EFCX) time series for the period of January 2000 to December 2001 with sample size . The parameters of the model are estimated by M-estimators based on various score functions. It turned out that the M-estimates of the parameter differ widely depending on the score functions and so it is difficult to assess which estimate should be relied on in similar situations. Here we compare various M-estimates and R-estimates of the GARCH () parameters for the EFCX series again shedding light on which could be some possible reasons for the difference in estimates and finally which estimation methods can be relied upon. We also compare M-estimates of the GARCH () parameters when fitted to two other dataset, namely, the S&P 500 stock index from June 2013 to May 2017 with and the GBP/USD exchange rate from June 2013 to May 2017 with to illustrate that the M- and R-estimates do not differ widely when the underlying theoretical assumptions hold in general.

In Table 1, we report the QMLE computed using the fGarch package in R program, the M-estimates QMLE and LAD and the R-estimates proposed in Examples 1-3 of Section 2.4. For the EFCX data, the R-estimates for all score functions are quite close to the LAD estimate, but they are very different than the QMLE. On the contrary, for the S&P 500 and GBP/USD data, M- and R-estimates are close to each other.

| fGarch | QMLE | LAD | sign | Wilcoxon | vdW | |

|---|---|---|---|---|---|---|

| EFCX | ||||||

| 1.89 | 6.28 | 1.22 | 1.23 | 1.22 | 1.24 | |

| 0.05 | 0.07 | 0.17 | 0.17 | 0.16 | 0.13 | |

| 0.92 | 0.84 | 0.66 | 0.65 | 0.67 | 0.69 | |

| S&P 500 | ||||||

| 6.50 | 7.02 | 5.31 | 5.32 | 5.32 | 6.19 | |

| 0.18 | 0.18 | 0.19 | 0.19 | 0.19 | 0.18 | |

| 0.72 | 0.70 | 0.73 | 0.73 | 0.73 | 0.72 | |

| GBP/USD | ||||||

| 5.32 | 1.02 | 6.83 | 6.76 | 7.29 | 9.10 | |

| 0.12 | 0.13 | 0.07 | 0.07 | 0.07 | 0.09 | |

| 0.88 | 0.85 | 0.91 | 0.91 | 0.91 | 0.89 |

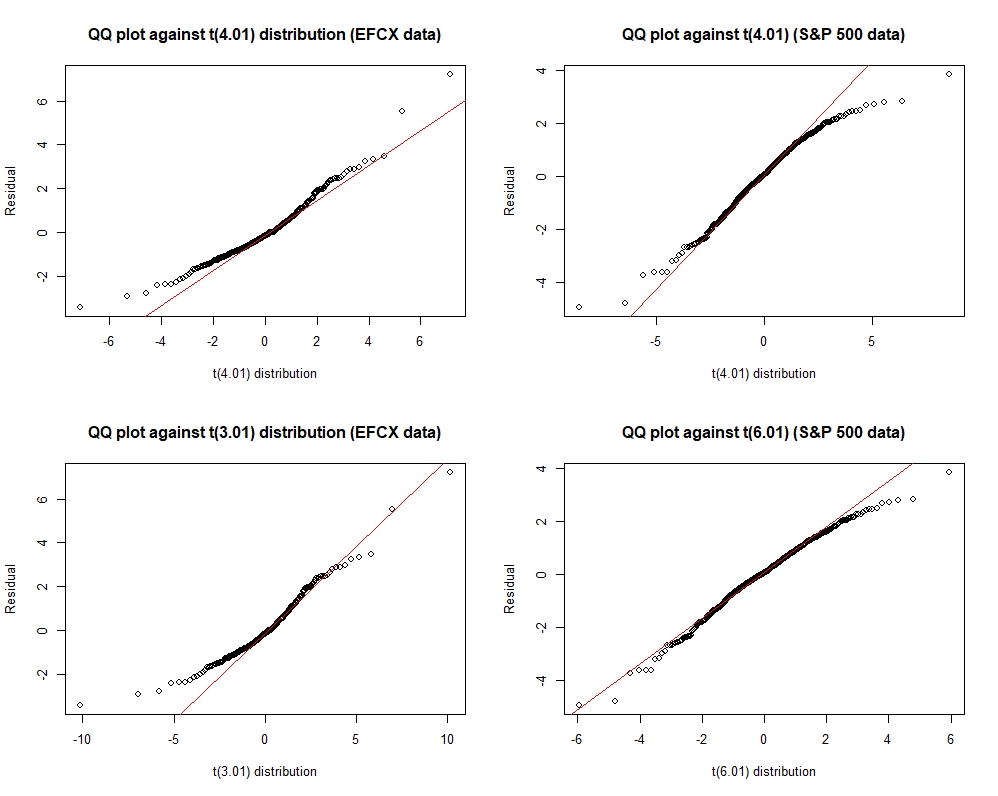

To investigate why the QMLE is different from the other R-estimates and LAD for the EFCX data, we check the assumption for this data by using the QQ-plots of the residuals (based on the vdW R-estimates) against distributions. We consider the vdW score only because the R-estimates based on two other score functions and the LAD are close to the vdW estimates. For comparison, we have also provided QQ-plots for the S&P 500 data. The main idea behind the QQ-plots of the residuals against the distribution is simple: Supposing distribution, then if and only if . Hence, residuals with heavier tail than the distribution correspond to the errors with the infinite -th moment while those with thinner tail than the distribution have the finite -th error moment.

The top-left panel of Figure 1 shows the QQ-plot of the residuals against the distribution for the EFCX data. The residuals have heavier right tail than the distribution which implies that the fourth moment of the error term may not exist. On the other hand, the QQ-plot against the distribution reveals lighter tail as shown at the bottom-left panel of Figure 1 and this implies that .

For the S&P 500 data, the QQ-plot against distribution at the top-right panel of Figure 1 shows that the residuals have lighter tails than distribution. For the QQ-plot against distribution, as shown at the bottom-right panel of Figure 1, the residuals fit the distribution better. Therefore, we may conclude that holds for the S&P 500 data.

3.2 Simulation study of the R-estimators

We now evaluate the performance of the R-estimators based on simulated data from various error distributions. Apart from the GARCH () model we consider the GARCH () model also as the computation for higher order models are not considered frequently in the literature. Let denote the number of replications and denote the R-estimator computed from the -th data, . We throughout compare the R-estimators with the QMLE by using the averaged bias and MSE. We also compare the relative efficiency of the R-estimators wrt the QMLE under a finite sample size, as an estimate of the ARE, by using the formula

Simulation for the GARCH () model. Here we run simulation with and where our choice of is motivated by the estimate given by the fGarch for the S&P 500 data in Table 1. The estimates of the bias and MSE of the R-estimators and QMLE under various error distributions are reported in Table 2, where the estimates of the ARE are shown in the parentheses. Notice that under distribution, the QMLE does not converge for many replications, while the R-estimators always converge. Therefore, the bias and MSE are obtained using the replications where the QMLE converges.

It is worth noting that the vdW achieves almost the same efficiency as the QMLE under the normal distribution, and the vdW is more efficient under heavier-tailed distributions. In general, the sign score is most efficient under the DE and distributions, while the Wilcoxon score is optimal under the logistic distribution. Under the distribution with infinite fourth moment, the R-estimators yield smaller bias and significantly smaller MSE than the QMLE.

To strengthen the point that the R-estimators behave better than the QMLE under a heavy-tailed distribution, we have reported simulation results for larger sample sizes and under distribution in Table 3. The QMLE failed to converge for large sample size; for example, with around 8% replications do not converge. From Table 3, when increases, the performance of the R-estimators becomes even better in terms of both the bias and MSE.

Overall, the vdW dominates the QMLE and other R-estimators sacrifice only small efficiency under the normal error distribution while they all achieve much higher efficiency when tails become much heavier. This provides a strong support for using the R-estimators.

| Standardized bias | Standardized MSE and ARE | ||||||

|---|---|---|---|---|---|---|---|

| Normal | |||||||

| QMLE | 8.96 | -4.42 | -1.54 | 6.45 | 1.41 | 4.14 | |

| Sign | 9.30 | 1.74 | -1.54 | 8.39 (0.77) | 1.62 (0.87) | 5.16 (0.80) | |

| Wilcoxon | 1.02 | 3.09 | -1.61 | 8.52 (0.76) | 1.54 (0.91) | 4.93 (0.84) | |

| vdW | 9.05 | 4.55 | -1.55 | 6.44 (1.00) | 1.43 (0.98) | 4.15 (1.00) | |

| DE | |||||||

| QMLE | 1.02 | 3.56 | -2.26 | 8.60 | 2.37 | 6.29 | |

| Sign | 5.82 | -3.42 | -1.69 | 6.22 (1.38) | 1.74 (1.36) | 5.15 (1.22) | |

| Wilcoxon | 6.24 | -2.93 | -1.74 | 6.34 (1.36) | 1.76 (1.35) | 5.12 (1.23) | |

| vdW | 6.22 | -4.13 | -1.96 | 6.51 (1.32) | 1.88 (1.26) | 5.45 (1.15) | |

| Logistic | |||||||

| QMLE | 1.05 | 2.51 | -1.51 | 7.44 | 1.63 | 4.28 | |

| Sign | 6.85 | -2.65 | -1.17 | 5.40 (1.38) | 1.42 (1.15) | 3.66 (1.17) | |

| Wilcoxon | 6.82 | -2.91 | -1.19 | 5.24 (1.42) | 1.38 (1.18) | 3.56 (1.20) | |

| vdW | 7.06 | -3.80 | -1.34 | 5.66 (1.31) | 1.42 (1.14) | 3.83 (1.12) | |

| QMLE | 9.96 | 2.99 | -5.46 | 2.53 | 2.74 | 2.81 | |

| Sign | 4.33 | 4.82 | -1.80 | 6.78 (3.73) | 3.72 (7.37) | 7.73 (3.64) | |

| Wilcoxon | 4.15 | 4.41 | -1.83 | 7.10 (3.57) | 3.86 (7.10) | 8.18 (3.44) | |

| vdW | 3.92 | 3.77 | -2.57 | 9.38 (2.70) | 5.33 (5.14) | 1.14 (2.47) | |

| Bias | MSE and ARE | ||||||

|---|---|---|---|---|---|---|---|

| n = 3000 | |||||||

| QMLE | 6.34 | 1.80 | -3.48 | 1.14 | 1.61 | 1.25 | |

| Sign | 1.52 | 1.46 | -9.99 | 1.65 (6.89) | 1.29 (12.47) | 2.10 (5.93) | |

| Wilcoxon | 1.61 | 1.47 | -1.03 | 1.76 (6.46) | 1.35 (11.95) | 2.22 (5.63) | |

| vdW | 1.58 | 1.01 | -1.39 | 2.46 (4.63) | 1.89 (8.49) | 3.15 (3.96) | |

| n = 5000 | |||||||

| QMLE | 3.66 | 1.20 | -2.07 | 8.21 | 1.20 | 8.22 | |

| Sign | 6.95 | -2.00 | -3.86 | 1.01 (8.09) | 7.21 (16.67) | 1.16 (7.10) | |

| Wilcoxon | -3.01 | -1.81 | -3.98 | 1.06 (7.73) | 7.56 (15.90) | 1.20 (6.85) | |

| vdW | -1.57 | -2.37 | -5.86 | 1.54 (5.33) | 1.13 (10.64) | 1.77 (4.64) | |

Simulation for the GARCH () model. It was reported in Francq and Zakoïan (2009) that higher order GARCH models may fit some financial time series better than the GARCH () model. Therefore, here we examine the performance of the R-estimators under the GARCH () model by running simulations with . To choose the true model parameter for simulation, we fitted the FTSE 100 data from January 2007 to December 2009 to the by GARCH () model using the fGarch package. It turned out that is significant with -value and the Akaike information criterion (AIC) of the GARCH () is smaller than that of the GARCH (). Since the fGarch estimate of the true parameter is , we choose this to generate sample from the GARCH () model with various error distributions. The R-estimators and QMLE are compared through the bias and MSE and the corresponding estimates are reported in Table 4. Similar to the GARCH () case, the advantage of the R-estimators over the QMLE becomes prominent under heavy-tailed distributions, especially under the distribution, where the bias and MSE of the R-estimators have smaller order of magnitude than the those of the QMLE.

| Bias | MSE | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Normal | |||||||||

| QMLE | 3.80 | 8.85 | -3.16 | -2.01 | 2.50 | 1.71 | 1.93 | 1.35 | |

| Sign | 3.79 | 1.05 | -5.76 | -1.84 | 2.65 | 1.90 | 2.19 | 1.30 | |

| Wilcoxon | 3.68 | 9.91 | -6.51 | -1.81 | 2.42 | 1.74 | 2.01 | 1.20 | |

| vdW | 3.95 | 1.03 | -7.49 | -1.96 | 2.67 | 1.74 | 1.94 | 1.25 | |

| DE | |||||||||

| QMLE | 2.61 | 4.43 | 2.14 | -1.99 | 3.11 | 2.53 | 4.01 | 2.33 | |

| Sign | 1.96 | 5.02 | 2.57 | -1.61 | 9.96 | 1.85 | 2.88 | 1.66 | |

| Wilcoxon | 1.85 | 3.03 | -2.03 | -1.65 | 9.57 | 1.79 | 2.85 | 1.73 | |

| vdW | 1.95 | 1.80 | -1.96 | -1.81 | 1.10 | 1.92 | 3.14 | 1.97 | |

| Logistic | |||||||||

| QMLE | 4.72 | 5.44 | 8.41 | -1.98 | 5.24 | 3.75 | 4.49 | 2.06 | |

| Sign | 3.17 | 3.23 | -2.32 | -1.49 | 2.09 | 1.75 | 2.50 | 1.39 | |

| Wilcoxon | 3.24 | 2.93 | -1.97 | -1.51 | 2.20 | 1.73 | 2.48 | 1.42 | |

| vdW | 3.62 | 2.49 | -1.97 | -1.72 | 2.76 | 1.91 | 2.67 | 1.72 | |

| QMLE | 1.78 | 3.06 | -2.07 | -3.12 | 2.85 | 7.88 | 7.65 | 1.08 | |

| Sign | 9.92 | 3.18 | -3.92 | -1.29 | 5.67 | 3.25 | 5.25 | 2.42 | |

| Wilcoxon | 9.78 | 3.69 | -4.87 | -1.28 | 5.70 | 3.51 | 5.58 | 2.50 | |

| vdW | 9.86 | 5.10 | -9.49 | -1.56 | 7.59 | 5.66 | 8.08 | 3.57 | |

4 Bootstrapping the R-estimators

Since the asymptotic covariance matrices of the R-estimators are of complicated forms, in this section we employ the weighted bootstrap technique discussed by Chatterjee and Bose (2005) in the context of M-estimators to approximate the distributions of the R-estimators and we compute corresponding coverage probabilities to exhibit the effectiveness of such bootstrap approximations. The weighted bootstrap in this context is attractive for its computational simplicity since at each bootstrap replication, only the weights need to be generated instead of resampling the data components to compute the replicates of the bootstrapped R-estimate.

In this context, the weighted bootstrap version of the rank-based central sequence is

where is a triangular array of r.v.’s which satisfies the following conditions:

(i) The weights are exchangeable and independent of the data and errors

(ii) For all where with being a constant.

Among various schemes of the weights satisfying the above conditions, we compare the following three types of weights:

(i) Scheme M: have a multinomial distribution, which is essentially the

classical paired bootstrap.

(ii) Scheme E: , where are i.i.d. exponential r.v.’s with mean .

(iii) Scheme U: ,

where are i.i.d. uniform r.v.’s on .

We propose the following Algorithm 2 to compute our bootstrap estimator, where the weighted version of (2.12) is used to compute the bootstrap estimator of and then with given in (2.10), we obtain the bootstrap estimator of through multiplying the and components by .

-

1.

Compute the R-estimator using (2.12) and set .

-

2.

for to do

| (4.1) |

Compute using (2.10), and then compute through multiplying the and components by .

4.1 Bootstrap coverage probabilities

Chatterjee and Bose (2005) proved the consistency of the bootstrap for an estimator defined by smooth estimating equation. Since ranks are integer-valued discontinuous functions, the proof of the asymptotic validity of the bootstrapped R-estimator is a mathematically challenging problem which is beyond the scope of this paper. Instead, we resort to simulations to evaluate the performance of the bootstrap approximation of the R-estimators by comparing the distribution of with that of in terms of coverage rates.

In particular, with the choice of the true parameter as in the simulation study of the GARCH () model of the previous section, we generate data each with sample size based on different error distributions. For each data, the exchangeable weights are generated times. We consider cases where the error distributions are normal, DE, logistic and . The bootstrap weights are based on Schemes M, E and U. The bootstrap coverage rates (in percentage) for nominal levels are reported in Table 5. Notice that all bootstrap schemes provide reasonable coverage rates under these error distributions. Scheme U is slightly better than the scheme M and E under the DE and distributions.

| nominal level | nominal level | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Normal | sign | Scheme M | 94.1 | 93.6 | 92.8 | 90.8 | 88.5 | 89.2 | |

| Scheme E | 93.5 | 93.3 | 92.8 | 90.3 | 88.1 | 88.8 | |||

| Scheme U | 94.8 | 94.7 | 93.7 | 91.7 | 90.2 | 89.6 | |||

| Normal | Wilcoxon | Scheme M | 96.4 | 96.3 | 93.7 | 93.8 | 90.3 | 89.7 | |

| Scheme E | 96.5 | 96.0 | 93.2 | 93.2 | 90.0 | 89.3 | |||

| Scheme U | 96.5 | 95.6 | 94.3 | 93.5 | 91.1 | 90.1 | |||

| Normal | vdW | Scheme M | 94.3 | 92.3 | 93.6 | 91.3 | 89.1 | 89.0 | |

| Scheme E | 94.2 | 92.2 | 92.7 | 90.5 | 88.5 | 88.7 | |||

| Scheme U | 95.3 | 94.1 | 93.7 | 91.4 | 90.5 | 89.2 | |||

| DE | sign | Scheme M | 90.8 | 90.5 | 91.6 | 87.8 | 86.0 | 86.8 | |

| Scheme E | 90.4 | 89.6 | 90.4 | 87.2 | 85.3 | 86.4 | |||

| Scheme U | 91.9 | 92.7 | 92.7 | 88.8 | 88.9 | 87.8 | |||

| DE | Wilcoxon | Scheme M | 91.0 | 91.0 | 91.5 | 87.6 | 86.9 | 87.6 | |

| Scheme E | 90.7 | 90.2 | 90.4 | 87.2 | 86.2 | 86.6 | |||

| Scheme U | 92.4 | 93.6 | 92.8 | 88.7 | 89.1 | 87.7 | |||

| DE | vdW | Scheme M | 90.9 | 87.6 | 89.7 | 87.5 | 83.9 | 85.3 | |

| Scheme E | 90.4 | 86.9 | 88.9 | 86.9 | 83.1 | 84.8 | |||

| Scheme U | 92.4 | 90.2 | 91.0 | 89.7 | 85.6 | 86.0 | |||

| Logistic | sign | Scheme M | 93.0 | 91.1 | 92.1 | 89.0 | 87.6 | 88.6 | |

| Scheme E | 93.4 | 92.3 | 92.5 | 89.8 | 86.3 | 88.4 | |||

| Scheme U | 93.0 | 92.3 | 91.9 | 88.7 | 87.5 | 87.1 | |||

| Logistic | Wilcoxon | Scheme M | 93.5 | 91.3 | 92.5 | 89.9 | 87.7 | 89.2 | |

| Scheme E | 93.7 | 89.4 | 91.7 | 90.0 | 85.8 | 87.1 | |||

| Scheme U | 94.1 | 92.2 | 92.8 | 88.9 | 88.1 | 86.4 | |||

| Logistic | vdW | Scheme M | 93.1 | 91.2 | 92.3 | 89.3 | 88.0 | 87.0 | |

| Scheme E | 92.4 | 91.1 | 91.7 | 88.5 | 87.6 | 86.4 | |||

| Scheme U | 94.4 | 93.6 | 92.2 | 90.4 | 90.8 | 86.8 | |||

| sign | Scheme M | 88.3 | 85.3 | 88.3 | 86.0 | 82.6 | 83.5 | ||

| Scheme E | 88.3 | 85.0 | 87.6 | 84.9 | 82.4 | 82.0 | |||

| Scheme U | 91.8 | 89.0 | 90.6 | 87.5 | 85.6 | 86.4 | |||

| Wilcoxon | Scheme M | 88.1 | 84.7 | 88.5 | 85.7 | 81.4 | 83.7 | ||

| Scheme E | 88.0 | 84.5 | 87.7 | 85.0 | 80.7 | 82.8 | |||

| Scheme U | 91.8 | 88.7 | 90.0 | 87.6 | 85.6 | 85.5 | |||

| vdW | Scheme M | 85.6 | 82.3 | 86.1 | 81.9 | 79.7 | 81.0 | ||

| Scheme E | 84.4 | 82.1 | 86.0 | 80.9 | 78.7 | 80.2 | |||

| Scheme U | 90.3 | 85.4 | 88.9 | 86.6 | 81.0 | 83.3 | |||

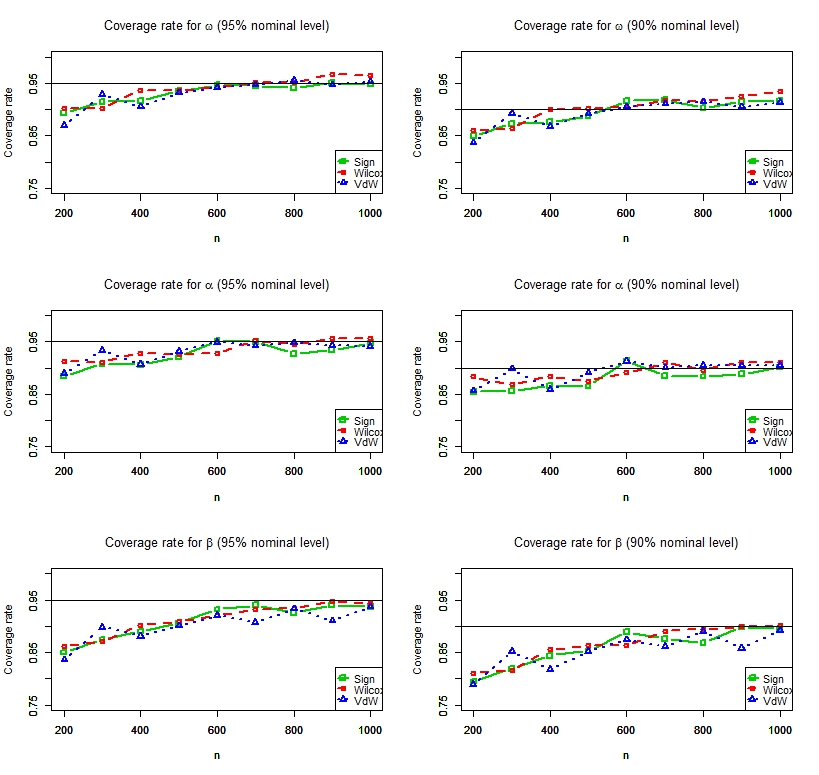

To check the performance of the bootstrap under different sample sizes, we run simulation with for the sign, Wilcoxon and vdW scores. There are replications being generated under the normal error distribution, and each replication is bootstrapped times with the scheme U. Figure 3 shows the bootstrap coverage rates for (first row), (second row), (third row) under nominal level (left column) and nominal level (right column). We notice that as the sample size increases, the coverage rates get close to the nominal levels for all parameters and all R-estimators, with only few exceptions. This tends to imply the consistency of the bootstrap approximation. With the sample size , the bootstrap coverage rates are generally close to the nominal levels.

5 Application of the R-estimator to the GJR model

The GJR model, proposed by Glosten et al. (1993), is used frequently for asymmetric financial data. Iqbal and Mukherjee (2010) considered a class of M-estimators to estimate model parameters. In a similar fashion, we have used the new class of R-estimators to analyze the GJR model and the relevant simulation results are available in Appendix B.

6 Conclusion

We propose a new class of R-estimators for the GARCH model and derive the asymptotic normality of these estimators under mild moment and smoothness conditions on the error distribution. We exhibit the robustness and efficiency of R-estimators with respect to the QMLE through simulation and real data analysis. We also consider a general type of weighted bootstrap for the R-estimators which is computational-friendly and easy-to-implement. The theoretical analysis such as the asymptotic validity of the weighted bootstrap is an interesting but challenging problem that can be explored in the future.

Acknowledgements

Hang Liu gratefully acknowledges the ESRC North West Social Science Doctoral Training Partnership (NWSSDTP Grant Number ES/P000665/1) for funding his PhD studentship.

References

- [1] Andrews, B. (2012). Rank-based estimation for GARCH processes. Econometric Theory, 28, 1037–1064.

- [2] Azzalini, A. and Dalla Valle, A. (1996). The multivariate skew-normal distribution. Biometrika, 83, 715–726.

- [3] Bahadur, R. R. (1966). A Note on Quantiles in Large Samples. Ann. Math. Statist., 37, 577–580.

- [4] Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 100, A307–A327.

- [5] Berkes, I., Horvath, L., and Kokoszka, P. (2003). GARCH processes: structure and estimation. Bernoulli, 9, 201-228.

- [6] Berkes, I. and Horvath, L. (2004). The efficiency of the estimators of the parameters in GARCH processes. Annals of Statistics, 32, 633-655.

- [7] Billingsley, P. (1968). Convergence of Probability Measures. Wiley Series in Probability and Mathematical Statistics. Wiley.

- [8] Cassart, D., Hallin, M., and Paindaveine, D. (2010). On the estimation of cross-information quantities in R-estimation. In J. Antoch, M. Hušková and P.K. Sen, Eds: Nonparametrics and Robustness in Modern Statistical Inference and Time Series Analysis: A Festschrift in Honor of Professor Jana Jurečková, I.M.S., 35–45.

- [9] Chatterjee, S. and Bose, A. (2005). Generalized bootstrap for estimating equations. Annals of Statistics, 33, 414–436.

- [10] Fan, J., Qi, L., and Xiu, D. (2014). Quasi-maximum likelihood estimation of GARCH models with heavy-tailed likelihoods. Journal of Business & Economic Statistics, 32, 178-191.

- [11] Francq, C., Lepage, G., and Zakoïan, J.-M. (2011). Two-stage non-Gaussian QML estimation of GARCH models and testing the efficiency of the Gaussian QMLE. Journal of Econometrics, 165, 246-257.

- [12] Francq, C. and Zakoïan, J.-M. (2007). Quasi-maximum likelihood estimation in GARCH processes when some coefficients are equal to zero. Stochastic Processes and their Applications, 117, 1265-1284.

- [13] Ghosh, J. K. (1971). A new proof of the Bahadur representation of quantiles and an application. Ann. Math. Statist., 42, 1957–1961.

- [14] Glosten, L.R., Jagannathan, R. and Runkle, D.E. (1993). On the relation between expected value and the volatility of the nominal excess return on stocks. Journal of Finance, 48, 1779-1801.

- [15] Hall, P. and Yao, Q. (2003) Inference in ARCH and GARCH models with heavy-tailed errors. Econometrica, 71, 285-317.

- [16] Hallin, M. and La Vecchia, D. (2017). R-estimation in semiparametric dynamic location-scale models. Journal of Econometrics, 2, 233–247.

- [17] Hallin, M., La Vecchia, D. and Liu, H. (2019). Center-Outward R-Estimation for Semiparametric VARMA Models. arXiv preprint arXiv:1910.08442.

- [18] Huber, P.J. and Ronchetti, E.M. (2011). Robust Statistics. Wiley Series in Probability and Statistics. Wiley.

- [19] Iqbal, F. & Mukherjee, K. (2010). M-estimators of some GARCH-type models; computation and application. Statistics and Computing 20, 435-445.

- [20] Koul, H. and Ossiander, M. (1994). Weak convergence of randomly weighted dependent residual empiricals with applications to autoregression. Annals of Statistics, 22, 540–562.

- [21] Kreiss, J.-P. (1987). On adaptative estimation in stationary ARMA processes, Annals of Statistics, 15, 112–133.

- [22] Le Cam, L. and Yang, G. L. (2000). Asymptotics in Statistics : Some basic concepts (2nd ed.). New York: Springer.

- [23] Liu, H. and Mukherjee, K. (2020). M-estimation in GARCH models without higher order moments. arXiv preprint arXiv:2001.10782.

- [24] Mukherjee, K. (2007). Generalized R-estimators under conditional heteroscedasticity. Journal of Econometrics, 141, 383–415.

- [25] Mukherjee, K. (2008). M-estimation in GARCH models. Econometric Theory, 24, 1530-1553.

- [26] Muler, N. and Yohai V. (2008). Robust estimates for GARCH models. Journal of Statistical Planning and Inference, 138, 2918-2940.

- [27] Tsay, R. (2010). Analysis of financial time series, Hoboken, N.J.: Wiley. 3rd edition.

- [28] van der Vaart, A. (1998). Asymptotic Statistics. Cambridge University Press.

- [29] Zhu, K. and Ling, S. (2011). Global self-weighted and local quasi-maximum exponential likelihood estimators for ARMA-GARCH/IGARCH models. Annals of Statistics, 39, 2131-2163.

APPENDIX

Appendix A Proofs of Proposition 2.1, Theorem 2.1 and 2.2

We will use the following facts from Berkes et al. (2003) for the proofs:

Fact 1. For any ,

| (A.1) |

and

Fact 2. There exist random variables , and , all independent of and a number , such that

| (A.2) |

| (A.3) |

Fact 3. Let be a sequence of identically distributed random variables. If , then for any ,

| (A.4) |

Idea of the proof of Theorem 2.1. We first derive the following Theorem A.1, Corollary A.1.1 and Theorem A.2 on empirical processes where a scale-perturbed weighted mixed-empirical process is approximated by its non-perturbed version. With

, we derive asymptotic expansion of the difference between two quantities and which are defined later. We then show that can be approximated by a r.v., which is asymptotic normal, plus a term linear in . Also, we use to approximate and show that asymptotically their difference is a r.v. with mean zero. Finally, we prove that the difference of and converges in probability to zero. Using these results, we are able to derive the asymptotic linearity of as shown in Proposition 2.1. Finally, using the definition of the one-step R-estimator in (2.8), we are able to derive the asymptotic distribution of .

Let be an array of -tuple r.v.’s defined on a probability space such that are i.i.d. with c.d.f. and is independent of for each . Let be an array of increasing sub--fields in both and so that , , , . Assume also that is measurable, and are measurable, . For , recall that and consider the following weighted mixed-empirical processes

| (A.5) | |||

Assume the following conditions on the weights and perturbations .

Let for some . Let with be such that

| (A.6) | |||

| (A.7) | |||

| (A.8) | |||

| (A.9) | |||

| (A.10) | |||

| (A.11) | |||

| (A.12) |

The following theorem shows that uniformly over the entire real line, the perturbed process can be approximated by .

Proof.

The proof is similar to the proof in Mukherjee (2007, Theorem 6.1). In particular, we show point-wise convergence for each and then invoke the monotone structure of the mean processes to achieve the uniform convergence. For weighted empirical, the monotonically increasing mean process is given by the distribution function. Although in the present case is not a monotone function on , we use its monotone property separately on and . ∎

We remark that this theorem is different from Koul and Ossiander (1994, Theorem 1.1) and Mukherjee (2007, Theorem 6.1) where weighted empirical processes were considered for the estimation of the mean parameters. For the estimation of the scale parameters, in this paper we consider weighted mixed-empirical process which is a weighted sum of the mixture of error and its indicator process.

The following corollary describes a Taylor-type expansion of the weighted sum of indicator functions .

Corollary A.1.1.

Proof.

The next theorem provides an extended version of (A.13) when the weights are functions on appropriately scaled parameter space. We define the following processes of two arguments as follows.

Probabilistic framework: Let be i.i.d. with the c.d.f. , be an array of measurable functions from to such that for every and , are independent of . For and , let

Here is a sequence of ordinary non-perturbed weighted mixed-empirical processes with weights and is a sequence of perturbed weighted mixed-empirical processes with scale perturbations . In Theorem A.2 below it is shown that can be uniformly approximated by under the following conditions (A.16)-(A.24) for and . Note that the statements on assumptions and convergence hold point-wise for each fixed .

There exist numbers and (both free from ) satisfying such that with ,

| (A.16) |

For some positive random process ,

| (A.17) | |||

| (A.18) | |||

| (A.19) | |||

| (A.20) | |||

| (A.21) | |||

| (A.22) | |||

| (A.23) | |||

| (A.24) | |||

Conditions (A.16)-(A.24) are regularity conditions on the weights and perturbations of the two-parameters empirical processes. Conditions (A.23)-(A.24) are smoothness conditions on the weights and perturbations. Under stationarity and ergodicity, many of these conditions reduce to much simpler conditions based on existence of the moments.

The following theorem generalizes (A.13) when the weights are functions of .

Theorem A.2.

Proof.

The following facts are useful in the proofs of various results of this paper. Let be the total number of parameters and fix . Let ,

| (A.26) |

Then satisfies (A.20) since

| (A.27) |

for some in the neighbourhood of for large . The -factor is used later for deriving convergence of some sequence of random vectors. Similarly, for some ,

| (A.28) |

say. Let . Then

where

For in Assumption (A1) and any ,

since all moments of are finite and and are independent for all . Therefore

| (A.29) |

If appears as the coefficients, we replace it by and the difference is controlled as follows. Notice that all derivatives below exist with bounded moments and so

| (A.30) |

where . Only the term is of our interest since others are of higher order than .

Take to be equal to the -th coordinate of

| (A.31) |

and as in (A.26). We now show that (A.17)-(A.24) hold with such choice.

For each with , are independent of . Using a Taylor expansion of at for each and noting the existence of all moments of and its derivatives of all higher orders, (A.17) and (A.18) hold. Existence of all higher moments of ensure conditions (A.19)-(A.21).

To verify (A.22), we use (A.27) and that for each , is a smooth function with derivatives of all order to conclude that

Conditions (A.23) and (A.24) can be verified using the mean value theorem.

The following lemmas and their proofs represent the intermediate steps in the proofs of Proposition 2.1 and Theorem 2.1.

Let

and note that the difference in the definitions of these two quantities lies only in the argument of . We show in Lemma A.3 below that . Using results on empirical processes in Theorem A.2, is linear in . Consequently, we obtain the following uniform approximations of over where .

Lemma A.3.

Let Assumptions (A1)-(A3) hold. Then, as ,

| (A.32) |

where .

Proof.

To use Theorem A.2 in the proof, let and for some . For simplicity, we use the notation to denote which is defined in the probabilistic framework above. Accordingly

and

With the choice based on (A.31) and (A.26) and using

Similarly,

Since

we get

and

Cancelling , equals

we have

Also,

Hence,

| (A.33) |

by recalling that . Finally, (A.32) follows from Theorem A.2. ∎

The following lemma states that the difference between and is asymptotically linear in .

Lemma A.4.

Let Assumptions (A1)-(A3) hold. Then, as ,

| (A.34) |

where

| (A.35) |

with .

Proof.

The difference between and lies in comparing and and involves smooth function of . So the proof follows easily with the details below. Notice that

Using (A.30),

Using the LLN, the first term in the above decomposition of is since

For the second term, using (A.28) we have factor of and consequently it is .

For , we approximate by and use to obtain . Hence (A.34) is proved.

Using the independence of and for each , is a sum of the vectors of martingale differences and so (A.35) follows from the martingale CLT. ∎

Now consider the rank-based counterpart of

The following lemma provides the difference between and . It shows that the effect of replacing observations in by ranks is asymptotically a r.v. with mean zero.

Lemma A.5.

Let Assumptions (A1)-(A3) hold. Then, as ,

| (A.36) |

Also, converges in distribution to , where has mean zero and variance .

Proof.

Consider the following decomposition

Using the -factor in (A.30) and (A.28), , and are . We next prove that in detail. Recall that is the empirical distribution function of . Let be the empirical distribution function of . Then

Since is the weighted sum of the difference of a c.d.f. evaluated at two different r.v.’s and integrated wrt , using the same technique for proving (A.33), .

Write . Since is the weighted sum of the difference of two different c.d.f.’s evaluated at two different r.v.’s and integrated wrt ,

Using (A.29), . Hence, by Theorem A.2,

Finally consider written as

where . We show that

| (A.37) |

| (A.38) |

For (A.37), note that converges weakly to a Brownian Bridge on since for each fixed , converges to a normal distribution using the martingale CLT and it is tight using the bound on the moment of the difference process in Billingsley (1968, Theorem 12.3).

Since , by the Arzela-Ascoli theorem,

and consequently, (A.37) is proved. For (A.38), we use the Bahadur representation; see Bahadur (1966) and Ghosh (1971) for details. Since is bounded and is positive on ,

Applying the mean value theorem,

| (A.39) |

Using ,

Since , and using van der Vaart (1998, Theorem 19.3),

we obtain (A.38) with the r.v. having mean zero. The variance of is given by

∎

Now recall the rank-based central sequence

which is an approximation to . We have the following lemma dealing with the difference between and .

Lemma A.6.

Let Assumptions (A1)-(A3) hold. Then, as ,

| (A.40) |

Proof.

Note that equals

| (A.41) | |||

| (A.42) | |||

| (A.43) |

Due to (A.2), (A.3) and , we have

| (A.44) |

Hence, in view of (A.1) and (A.4), for every ,

which implies that (A.41) is . Since is bounded, (A.42) is . For (A.43), since there is a factor from

it suffices to prove that

Let denotes the greatest integer less than or equal to . We split the sum in into two parts: in the first part, runs till where . We show that this part is by noting that its expectation is of the form multiplied by expectation of and a bounded quantity because is bounded. The number of summands in the second term is which is large but there we bound expectation of the sum of by a quantity of the form with and and this is . Accordingly

| (A.45) |

To show (A.45) is , we prove that for every ,

| (A.46) |

Since sequences and are permutations of , with the probability tending to one as , both and are at points of continuity of that has a finite number of the points of discontinuity. Therefore, to prove (A.46), it suffices to prove

| (A.47) |

For , we decompose ranks as

| (A.48) |

where the first sum is . For the second sum, writing

the modulus of (A.48) is bounded above by

Using , this is bounded above by

where the set is defined as

Therefore, it suffices to prove that uniformly with respect to both and . We show this with sets containing .

Recall that using (A.2), for a positive constant and so

Now using the triangular inequality,

| (A.49) |

Therefore (A.49) is bounded above by

In view of (A.49), we get

where .

Therefore, is a subset of

Consider r.v.s and with independent of . Then where the p.d.f. is bounded. Consequently,

Notice that since ,

due to and . Hence, converges in mean to zero uniformly with respect to both and , which entails uniformly.

∎

With all the results above, we can easily prove Proposition 2.1 and the asymptotic result for the R-estimator as follows.

Proof of Proposition 2.1.

Proof.

Combining (A.34), (A.36), (A.32) and (A.40), we get

| (A.50) |

which, by letting , entails

Hence, (2.6) follows by recalling that .

∎

Proof of Theorem 2.1.

Proof.

From the definition of in (2.8), (2.6) and (2.7) in Proposition 2.1, consistency of and the asymptotic discreteness of (which allows us to treat as if it were a bounded constant: see Lemma 4.4 in Kreiss (1987)), we have

In view of (2.7), we have

Now, it remains to obtain the asymptotic covariance matrix of . Recall (A.35) and (A.38). Since the asymptotic covariance matrices of and have been derived, it remains to obtain the covariance matrix . Note that equals

| (A.51) |

Using (A.39) and , as , (A.51) has the same limit as

where the first equality is due to independence of and for , independence of and , and Assumption (A1). The second equality is due to independence of and . The last equality is due to Assumption (A1).

∎

Proof of Theorem 2.2.

Appendix B R-estimators in GJR models and applications

Glosten et al. (1993) proposed the GJR () model for the asymmetric volatility observed in many financial dataset exhibiting asymmetry property. The GJR () model is defined by

where

with Since is linear in parameters, we define the R-estimators for the GJR model using the same rank-based central sequence as in (2.3). See also Iqbal and Mukherjee (2010) for the extension of M-estimators from the GARCH model to the GJR model. We do not prove any asymptotic theory for the R-estimators of the GJR model but present here empirical analysis using the same algorithm as in Algorithm 1 to compute the R-estimators. The following extensive simulation study, similar to the GARCH case, demonstrates the superior performance of the R-estimators compared to the QMLE that is often used in this model. We also carry out simulation with increasing sample sizes to show the consistency of the R-estimators. Three types of R-estimators and the QMLE are compared below under various error distributions. We run simulations with the sample size , number of replications and true parameter

which is motivated by the estimate in Tsay (2010) for the IBM stock monthly returns from 1926 to 2003. The estimates of the bias and MSE of the QMLE and R-estimators and those of the ARE of the R-estimators wrt the QMLE are reported in Table 6.

We remark that the results are consistent with those in Table 2: the vdW score still dominates the QMLE uniformly; the optimal scores under the DE and logistic distributions are also the sign and Wilcoxon, respectively. It is worth noting that under distribution, the R-estimators are much more efficient than the QMLE for the parameter

| Bias | MSE and ARE | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Normal | |||||||||

| QMLE | 8.70 | -2.03 | 7.47 | -2.03 | 4.17 | 7.63 | 1.53 | 3.80 | |

| Sign | 9.01 | -1.20 | 8.43 | -2.00 | 4.73 | 9.40 | 1.92 | 4.30 | |

| (0.88) | (0.81) | (0.80) | (0.88) | ||||||

| Wilcoxon | 9.35 | -8.15 | 8.65 | -2.00 | 4.96 | 8.72 | 1.76 | 4.24 | |

| (0.84) | (0.87) | (0.87) | (0.90) | ||||||

| vdW | 8.72 | -1.61 | 7.59 | -2.01 | 4.24 | 7.72 | 1.56 | 3.82 | |

| (0.98) | (0.99) | (0.98) | (0.99) | ||||||

| DE | |||||||||

| QMLE | 7.07 | -1.28 | 1.13 | -1.87 | 4.66 | 1.23 | 3.19 | 4.72 | |

| Sign | 4.91 | -2.26 | 6.99 | -1.62 | 3.44 | 9.58 | 2.36 | 4.10 | |

| (1.35) | (1.28) | (1.35) | (1.15) | ||||||

| Wilcoxon | 5.06 | -2.23 | 7.25 | -1.61 | 3.45 | 9.74 | 2.41 | 4.06 | |

| (1.35) | (1.26) | (1.32) | (1.16) | ||||||

| vdW | 4.98 | -3.35 | 6.73 | -1.71 | 3.54 | 1.02 | 2.50 | 4.23 | |

| (1.32) | (1.20) | (1.27) | (1.12) | ||||||

| Logistic | |||||||||

| QMLE | 8.01 | 7.88 | 8.85 | -1.62 | 3.86 | 1.07 | 2.40 | 3.46 | |

| Sign | 6.06 | -2.59 | 5.54 | -1.49 | 3.26 | 8.97 | 1.96 | 3.36 | |

| (1.18) | (1.19) | (1.23) | (1.03) | ||||||

| Wilcoxon | 5.97 | -5.22 | 5.38 | -1.44 | 3.07 | 8.76 | 1.93 | 3.18 | |

| (1.26) | (1.22) | (1.24) | (1.09) | ||||||

| vdW | 6.27 | -1.18 | 5.18 | -1.56 | 3.25 | 9.26 | 2.04 | 3.35 | |

| (1.19) | (1.15) | (1.17) | (1.03) | ||||||

| QMLE | 9.91 | -1.00 | 9.21 | -6.45 | 1.14 | 4.38 | 1.18 | 2.31 | |

| Sign | 5.68 | 4.23 | 2.71 | -2.77 | 3.78 | 1.35 | 4.69 | 6.33 | |

| (3.02) | (3.24) | (25.19) | (3.65) | ||||||

| Wilcoxon | 5.69 | 3.94 | 2.74 | -2.85 | 3.93 | 1.40 | 4.80 | 6.62 | |

| (2.91) | (3.12) | (24.57) | (3.49) | ||||||

| vdW | 6.12 | -1.61 | 3.43 | -3.71 | 5.13 | 1.93 | 7.45 | 9.58 | |

| (2.23) | (2.27) | (15.84) | (2.41) | ||||||

Simulation under different sample size. We next investigate behaviour of the R-estimators by carrying out simulations with different sample sizes. The number of replications and true parameter are the same as those used for Table 6 and the error distribution is normal. The estimates of the bias and MSE of the R-estimators for the GJR () model are shown in Table 7. In general, for all R-estimators, both the bias and MSE decrease when the sample size increases from to . This tends to reflect that the R-estimators are consistent estimators of for the GJR () model.

| Bias | MSE | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Sign | |||||||||

| 1.78 | 2.42 | 1.88 | -4.84 | 1.43 | 1.64 | 3.72 | 1.33 | ||

| 9.01 | -1.20 | 8.43 | -2.00 | 4.73 | 9.40 | 1.92 | 4.30 | ||

| 2.76 | -6.82 | 1.97 | -4.47 | 8.75 | 3.05 | 6.11 | 8.73 | ||

| 2.07 | -4.43 | 2.05 | -3.43 | 4.57 | 1.70 | 3.68 | 4.62 | ||

| Wilcoxon | |||||||||

| 1.77 | 2.52 | 1.88 | -4.75 | 1.37 | 1.52 | 3.45 | 1.26 | ||

| 9.35 | -8.15 | 8.65 | -2.00 | 4.96 | 8.72 | 1.76 | 4.24 | ||

| 3.01 | -2.94 | 2.68 | -4.30 | 8.18 | 2.82 | 5.60 | 7.85 | ||

| 2.45 | 1.52 | 2.82 | -3.54 | 4.50 | 1.63 | 3.55 | 4.29 | ||

| vdW | |||||||||

| 1.67 | 1.42 | 1.61 | -4.84 | 1.31 | 1.44 | 3.03 | 1.27 | ||

| 8.72 | -1.61 | 7.59 | -2.01 | 4.24 | 7.72 | 1.56 | 3.82 | ||

| 2.88 | -1.72 | 1.60 | -4.59 | 7.42 | 2.61 | 4.90 | 7.19 | ||

| 2.42 | 9.50 | 2.42 | -4.02 | 4.38 | 1.49 | 3.28 | 4.26 | ||