#1##1

A dynamic ordering policy for a stochastic inventory problem with cash constraints

Abstract

This paper investigates a stochastic inventory management problem in which a cash-constrained small retailer periodically purchases a product from suppliers and sells it to a market while facing non-stationary demands. In each period, the retailer’s available cash restricts the maximum quantity that can be ordered. There exists a fixed ordering cost for the retailer when purchasing. We partially characterize the optimal ordering policy by showing it has an structure: for each period, when initial inventory is above the s threshold, no product should be ordered no matter how much initial cash it has; when initial inventory is not large enough to be a threshold, it is also better to not order when initial cash is below the threshold . The values of may be state-dependent and related to each period’s initial inventory. A heuristic policy is proposed: when initial inventory is less than and initial cash is greater than , order a quantity that brings inventory as close to as possible; otherwise, do not order. We first determine the values of the controlling parameters , and based on the results of stochastic dynamic programming and test their performance via an extensive computational study. The results show that the policy performs well with a maximum optimality gap of less than 1% and an average gap of approximately 0.01%. We then develop a simple and time-efficient heuristic method for computing policy by solving a mixed-integer linear programming problem and approximate newsvendor models: the average gap for this heuristic is approximately 2% on our test bed.

Keywords: stochastic inventory; non-stationary demand; cash-flow constraint; policy

1 Introduction

Cash flow management is important to the survival and growth of many businesses, especially for small-to-medium-sized enterprises (SMEs), including start-up companies and small retailers. Cash shortage may disrupt a firm’s smooth operation and can even lead to insolvency (John, 2014). Smirat and Yousef (2016) sampled SMEs in Jordan and found that cash management practices had influence on the financial performance of those firms. A report compiled by the research firm CB Insights found that 29% of start-ups failed because of cash crisis (CBInsights, 2018). For some small retailers, the maximum number of products they can purchase depends on their available cash in this period. Some of those retailers are widely present in many developing countries and called nanostores (Boulaksil and van Wijk, 2018). On Chinese E-commerce platforms such as Taobao.com of Alibaba Group and Jd.com of JD Group, or on social software WeChat of Tecent Group, there are many small online retailers operated by only a few people or even a single individual. External financing is more difficult to obtain for those retailers than for larger business entities. Therefore, such small retailers must consider cash constraints during business operations.

An important class of inventory control problems is the single-item single-stocking location stochastic lot-sizing problem. This problem has been widely investigated since the 1950s (Wagner and Whitin (1958), Scarf (1960)). An interesting stream in the stochastic lot-sizing literature focuses on cash constraints. Cash constraints are different from order quantity capacity constraints in that cash flow is dynamic and related to the retailer’s revenues and costs, while order quantity capacity constraints simply impose a fixed upper bound on the ordering quantity. To the best of our knowledge, existing works on multi-item stochastic inventory problems considering cash constraints either focus on single-period problems (e.g. Bi et al. (2018)) or are solved by simulation in a multi-period setting due to the complexity of the problem (e.g. Boulaksil and van Wijk (2018)). This motivates our study on a single-item multi-period problem.

Another difference between our paper and previous works is that we consider a fixed ordering cost in the problem. In real-life transactions, fixed ordering costs do exist for some retailers. For example, small online retailers mentioned above usually purchase from their suppliers every few weeks. The transportation cost and some other expenses of each procurement can be viewed as a fixed ordering cost because they are not related to the order quantity.

As pointed out by Graves (1999), one major theme in the continuing development of inventory theory is to incorporate more realistic assumptions about product demand into inventory models. In this work, we consider the cash-constrained single-item single-stocking location lot-sizing problem for non-stationary stochastic demands. To the best of our knowledge, the optimal policy for the non-stationary stochastic lot-sizing problem under cash constraints has not been studied before. Moreover, the computation of optimal or near-optimal policy parameters for multi-period stochastic inventory problems remains a challenging task. Our contributions to the literature are as follows.

-

•

We investigate a cash-constrained stochastic inventory system with fixed ordering cost for the retailer.

-

•

We discuss the characteristics of the optimal ordering policy for the problem under non-stationary demand over a finite horizon, and discuss a partial characterisation of the optimal ordering strategy: if initial inventory is above the threshold , or if the initial cash is below when initial inventory is less then the threshold , then there is no need for the retailer to order.

-

•

Inspired by the former analysis, we propose an ordering policy: . We first introduce an effective heuristic for determining the values of , and based on the results of stochastic dynamic programming. A comprehensive numerical study shows the average optimality gaps for this policy are very small and the policy is near-optimal, with a maximum gap of less than 1%.

-

•

We finally develop an efficient algorithm to obtain the values of , and by mixed-integer linear programming and approximating each ordering cycle to newsvendor models. The method can solve the problem in fractions of a second, and the average gap on the test bed is approximately 2%.

The rest of this work is structured as follows. Section 2 reviews the related literature in detail. Section 3 describes the problem setting and formulates a stochastic dynamic programming model. Section 4 summarizes several characteristics of the optimal ordering pattern. We present a heuristic ordering policy and their computation methods in Section 5. A computational study and its results are detailed in Section 6. Finally, Section 7 draws conclusions and outlines future research directions.

2 Literature review

An important part of supply chain management is financial flow management(Cooper et al., 1997). Some works considered the Net Present Value (NPV) of the cash flow in the traditional inventory problems. For example, Helber (1998) built a NPV model for a multi-item capacity-constrained problem. Wu et al. (2016) made a discounted cash-flow analysis for inventory models with deteriorating items and partial trade credits. Working capital is another aspect that has been investigated by many scholars in recent years. Zeballos et al. (2013) discussed an inventory problem with working capital constraints and short-term debt. Bian et al. (2018) took working capital requirements into account in a single-item lot-sizing problem. Luo and Shang (2019) built a working capital maximization model for an inventory problem with trade credit and cash-related costs. There are also some works that addressed cash flow and maximize the long-term survival possibility for start-up firms, see e.g. Archibald et al. (2002), Tanrısever et al. (2012), Archibald et al. (2015).

Although the aforementioned works have considered cash flow, the available cash in their models does not affect the ordering quantity decisions, hence these works do not consider cash constraints. Among works considering cash constraint, Buzacott and Zhang (2004) noted the importance of jointly considering operational and financial decisions by analyzing a cash-constrained newsvendor model with financing behavior. Dada and Hu (2008) built a Stackelberg model between a bank, manufacturer and cash-constrained retailer. Raghavan and Mishra (2011) considered a two-level supply chain with a retailer and manufacturer both facing cash constraints. Kouvelis and Zhao (2012) gave a detailed discussion of optimal trade credit contracts in a game model. Moussawi-Haidar and Jaber (2013) developed a model for a cash-constrained retailer under delay payments. Tunca and Zhu (2017) discussed the role and efficiency of buyer intermediation in supplier financing through a game-theoretical model. Bi et al. (2018) addressed short-term financing in an inventory problem of multi-item setting.

Most of the literature focusing on multi-period stochastic inventory problems with cash constraints consider single-item problems. Chao et al. (2008) investigated a multi-period single-item self-financing newsvendor problem. They proved the optimal ordering pattern is an approximate base stock policy and presented a simple algorithm to solve the problem for stationary demands. Gong et al. (2014) extended this by considering short-term financing. Katehakis et al. (2016) analyzed non-stationary demand processes and time-varying interests. Boulaksil and van Wijk (2018) formulated a cash-constrained stochastic inventory model with consumer loans and supplier credits for nanostores.

Despite considering cash constraints, no fixed ordering cost is embedded in the aforementioned works. The existence of fixed ordering cost makes it difficult to analyze the structure of the optimal ordering policy. Chen and Zhang (2019) investigated cash flow constraints in a lot-sizing problem. However, their system operates under deterministic demand. Next, we will review some pioneering works dealing with the stochastic inventory problem with fixed ordering costs, which inspires us to develop the ordering policy in this paper.

Without a capacity constraint, Scarf (1960) proved that the optimal ordering policy for the general single-item stochastic lot-sizing problem is , where denotes the reorder point and is the order-up-to level. The optimality is proved through a property called -convexity. Optimal ordering patterns have not been thoroughly characterized for the capacitated stochastic lot-sizing problem. A key finding by Shaoxiang and Lambrecht (1996) proved that with stationary demand and fixed capacity, the optimal policy has a band structure pattern: when the initial inventory level is below , it is optimal to order at full capacity; when the initial inventory level is above , do not order. Gallego and Scheller-Wolf (2000) further clarified this structure with CK-convexity and divided the optimal ordering policy into four regions: in two of these regions the optimal policy is completely specified, while it is partially specified in the other two. Shaoxiang (2004) extended it for the infinite horizon model. Chao and Zipkin (2008) found the optimal policy for a capacitated problem with a special supply chain contract. Özener et al. (2014) relaxed the capacitated problem with linear holding and penalty cost, Poisson demand, and proposed a heuristic policy. Shi et al. (2014) developed approximation algorithms with worst-case performance guarantee for this problem. There are also some other related works such as Chan and Song (2003) and Yang et al. (2014). While most of the above works considered the capacity constraint as static exogenous, cash constraint is more complex because actually cash constraint is a function of operational decisions.

For the general policy, the computation of the values of , in each period has been considered to be prohibitively expensive for years. A number of existing works have attempted to solve this problem under stationary demands; see e.g. Federgruen and Zipkin (1984), Zheng and Federgruen (1991), Feng and Xiao (2000). For non-stationary demands, recent progress has been made by Bollapragada and Morton (1999) and Xiang et al. (2018). Nevertheless, those works are for the uncapacitated situation —- there are no upper bounds on ordering quantity.

A comparison between some of the aforementioned inventory problems and our research is presented in Table 1.

3 Problem setting

For convenience, the notations adopted in this paper are listed in Table 2. Other relevant notations will be introduced as needed.

| Authors | Demand | Multi items | Fixed | Multi | Capacity |

|---|---|---|---|---|---|

| pattern | ordering cost | period | constraints | ||

| Helber (1998) | Deterministic | ✓ | ✓ | ✓ | |

| Bian et al. (2018) | Deterministic | ✓ | ✓ | ||

| Chen and Zhang (2019) | Deterministic | ✓ | ✓ | cash | |

| Archibald et al. (2015) | Stochastic | ✓ | |||

| Luo and Shang (2019) | |||||

| Buzacott and Zhang (2004) | Stochastic | cash | |||

| Moussawi-Haidar and Jaber (2013) | |||||

| Bi et al. (2018) | Stochastic | ✓ | cash | ||

| Scarf (1960) | Stochastic | ✓ | |||

| Shaoxiang and Lambrecht (1996) | Stochastic | ✓ | fixed | ||

| Gallego and Scheller-Wolf (2000) | |||||

| Shaoxiang (2004) | |||||

| Chao et al. (2008) | Stochastic | ✓ | cash | ||

| Gong et al. (2014) | |||||

| Katehakis et al. (2016) | |||||

| Boulaksil and van Wijk (2018) | Stochastic | ✓ | ✓ | cash | |

| This work | Stochastic | ✓ | ✓ | cash |

3.1 Problem description

In our problem, a cash-constrained retailer periodically purchases one product from its suppliers and sells the product to customers. Customer demand is non-negative, discrete and independently distributed from period to period. The random demand for each period can be non-stationary and is represented by a variable . Its probability density function is and cumulative distribution function is . Like Shaoxiang (2004) and Shaoxiang and Lambrecht (1996), we also assume the maximum demand value is . Additionally, we also assume the minimum demand value is . Theoretically, can be zero, and can be a very large number. In many real-life cases, extremely large demands are low-probability events and can be neglected. This assumption also guarantees there are finite states in the stochastic dynamic programming of this problem.

| Notations | Description |

|---|---|

| Indices | |

| Period index | |

| Problem parameters | |

| Initial cash in the first period | |

| Initial inventory in the first period | |

| End-of-period inventory in period | |

| End-of-period cash in period | |

| Selling price | |

| Fixed ordering cost | |

| Overhead costs like rents or wages that the retailer needs to pay in each period | |

| Unit variable ordering cost | |

| Unit salvage value for remnant inventory in the final period | |

| Maximum possible demand value | |

| Minimum possible demand value | |

| A function of initial cash , representing the cash constraint | |

| Random variables | |

| Random demand in period , with probability density function , cumulative distribution function | |

| Decision variables | |

| Immediate inventory level after ordering in period |

At the beginning of the planning horizon, the retailer has an initial inventory of and an initial cash . Since we focus on a retail setting, we assume that customers usually do not wait for back-ordered items and that unmet demand is lost. Moreover, we assume that suppliers require immediate payment and that the order delivery lead time is zero. Excess stock is transferred to the next period as inventory, and the selling back of excess stock is not allowed. At the beginning of any period , the retailer has to decide the order quantity ; we let , where denotes the “order-up-to level.” The inventory flow function of the retailer can then be expressed as

| (1) |

The initial inventory of the retailer is , and the initial cash balance of the retailer is . The selling price of the item is , and the retailer receives payments only when its items are delivered to the customers. A fixed ordering cost is charged to the retailer when ordering from its suppliers; there is also a variable ordering cost charged on every ordered unit. We assume that the retailer needs to pay a fixed overhead cost at the beginning of each period, to operate the business and cover fixed costs such as rents or wages for staffs; while variable inventory holding cost charged on every item unit carried from one period to the next is assumed to be negligible.

In each period , the initial cash is , and the ordering quantity is . Define as a unit step function to determine whether the retailer makes an order in period : when , when . The total ordering cost in period is , which includes the fixed ordering cost and variable ordering costs. Because of the cash constraint, when the retailer purchases items, its available cash must be greater than the total costs in this period, namely, ordering costs plus overhead cost. This is shown by the constraint below.

| (2) |

The actual sales quantity in period is , and revenue is . End-of-period cash for period is defined as the initial cash balance plus the period’s revenue minus the period’s total costs . Any inventory left at the end of the planning horizon has a salvage value per unit. Therefore, the full expression of is given by Eq. (3).

| (3) |

The main difference between our problem and previous inventory literature about cash constraint in inventory problems, such as Chao et al. (2008) and Gong et al. (2014), is that we consider a fixed ordering cost for the retailer. Another difference is that we do not account for the deposit interest of each period’s cash balance because the deposit interest from the bank is generally very small compared with the retailer’s transaction volume and usually does not exert an effect on its operational decisions.

To avoid triviality, we assume . Our aim is to find a replenishment plan that maximizes the expected terminal cash increment, i.e., .

3.2 Stochastic dynamic programming modeling

We formulate a stochastic dynamic programming model for our problem to analyze its mathematical properties.

States. The system state at the beginning of period is represented by initial inventory and initial cash quantity . Note that since demand is assumed to be discrete and maximum demand value is , there are finite states for inventory and cash in our problem.

Actions. The action in period is the order-up-to level , given initial inventory and initial cash quantity . From the cash constraint (2), we use a function to show the upper bound for the ordering quantity.

| (4) |

The bounds for are represented by

| (5) |

State transition function. The state transition function for inventory is given by inventory flow equation (1), while the state transition function for cash is presented by cash flow equation (3).

Immediate profit. Let be the cash increment in period , expressed as

| (6) |

The immediate profit for period is the expected cash increment during this period given , and . can be expressed as

| (7) |

Optimality Equation. Define as the maximum expected cash increment during periods when the initial inventory and cash of period are and , respectively. The optimality equation for the problem is expressed as:

| (8) |

The boundary equation is:

| (9) |

For convenience, we define as follows.

| (10) |

is an obvious concave function. For ease of expression, we suppress , , in some expressions and use it only when required. Therefore, , , and can be written as:

| (11) | ||||

| (12) | ||||

| (13) | ||||

| (14) |

4 Ordering policy discussion

In this section, we provide some characteristics about the optimal ordering policy. We first show this by a numerical example, then analyze the optimal ordering policy in the last period, and finally obtain some theoretical expressions with proofs for the general periods.

4.1 Numerical findings

Since optimality function for the dynamic programming model is two-dimensional, it is difficult to detect its mathematical properties. By fixing or fixing and viewing as a function of a single decision variable, does not show K-convexity as in Scarf (1960) or K-concavity as in Chen and Simchi-Levi (2004), nor does it show CK-convexity (or CK-concavity) as in Gallego and Scheller-Wolf (2000) or (C, K)-convexity (or (C, K)-concavity) as in Shaoxiang (2004). This result can be easily confirmed by some numerical examples.

However, we can find some characteristics of the optimal ordering policy. We illustrate these characteristics with the following numerical example: there are 4 periods; demands follow Poisson distributions and the average values are 9, 13, 20, 16; fixed ordering cost , unit variable ordering cost , overhead costs , selling price and unit salvage value .

The optimal ordering quantities for different initial inventory and in the first period are given below:

| 21 | 23 | 25 | 27 | 29 | 31 | 33 | 35 | 37 | 39 | 41 | 43 | 45 | 47 | 49 | ||

| 0 | 0 | 0 | 0 | 7 | 9 | 11 | 13 | 14 | 14 | 19 | 21 | 23 | 24 | 24 | 24 | |

| 1 | 0 | 0 | 0 | 0 | 7 | 9 | 11 | 13 | 13 | 13 | 19 | 21 | 23 | 23 | 23 | |

| 2 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 19 | 21 | 22 | 22 | 22 | |

| 3 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 19 | 21 | 21 | 21 | 21 | |

| 4 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 19 | 20 | 20 | 20 | 20 | |

| 5 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 19 | 19 | 19 | 19 | 19 | |

| 6 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 18 | 18 | 18 | 18 | 18 | |

| 7 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 8 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

As an illustration of how to read the above results, suppose the initial inventory is 1 and the initial cash is 35, then, the optimal ordering quantity is 13 units. Several ordering characteristics can be observed directly from this numerical case:

-

•

The optimal ordering policy is not the type.

-

•

When the initial inventory is very large or initial cash is very small, the optimal ordering quantity is always zero. For example, when or , . Furthermore, the ordering threshold of is different for different initial inventory. When , it is optimal to not order when ; when , it is optimal to not order when .

-

•

When ordering, it is optimal for the retailer to order as close to some specified inventory level as possible. For a fixed initial inventory, there may be several order-up-to levels. We show the different order-up-to levels by drawing a vertical line segment below the ordering quantity values. For example, in this case, the order-up-to levels for are 14, and 24, and the order-up-to levels for are 24.

The above case suggests that at least two thresholds exist, and : if or , do not order; else, order up to some specified level. For ease of analysis, we first investigate the ordering pattern in the last period .

4.2 Ordering pattern in the last period

When , from Eq. (14), its optimality equation is

| (15) |

Recall that . Let

| (16) |

Here, we draw the picture of of a real numerical example in Figure 1.

Since is also an apparent concave function, it reaches optimal at:

| (18) |

From Eq. (17), we can obtain a smallest threshold for period . The threshold means when initial inventory is larger than , it is always better to not order. As shown in Figure 1, is smaller than for a fixed ordering cost .

| (19) |

When , there exists a threshold. When , it is optimal for the retailer to not order because the expected profit cannot cover the ordering costs. The maximum threshold is the cash level for which the retailer’s expected profit by ordering equals the fixed ordering cost plus the expected profit of not ordering. The threshold for an initial inventory can be obtained by the following equation. Recall that means the maximum ordering quantity under initial cash .

| (20) |

Note that is state-dependent and related with inventory level . For an initial inventory level , its minimum cash requirement for ordering is . Its maximum order-up-to level under initial cash is . The relation of , , and is shown in Figure 1. Since is increasing when , it is optimal for the retailer to replenish its inventory level as close to as possible when and . The optimal ordering policy in period can easily be expressed by the following equation:

| (21) |

4.3 Thresholds of and

When is not restricted to the final period , we provide some analytic expressions for the thresholds of and .

For any period , an s threshold can be obtained by the following equation, where is the cumulative distribution function of total demand from period to and is its inverse function.

| (22) |

Lemma 1

In any period , there exists a threshold such that if initial inventory , regardless of the initial cash, there is no need for the retailer to order. The threshold can be defined by Eq. (22).

Proof. The total demand from period to period follows a stochastic distribution. Let

where is the probability distribution function of total demand from period to . Since there is no inventory holding cost in our cost, ordering earlier would not bring extra costs. If the retailer has enough cash, it only needs to order at most once in period to meet all the later demands, which can save fixed ordering costs and result in a similar newsvendor problem. By the above description and Eq. (14), we know that

| (23) | |||

| (24) |

Since is a concave function and reaches optimal at , by Eq. (24), when , there is no need to order because the available inventory is enough to obtain maximum expected profit. Therefore, Eq. (22) is a threshold.

More conservative thresholds exist. For example, if , the initial inventory is sufficient to meet all the demands in later periods; thus, there is no need for the retailer to order. By Lemma 3 below, the maximum demand can also be a threshold (we omit the proof for brevity). Note that the s threshold defined by Eq. (22) is also conservative in real numerical tests.

As for the threshold of , we first bring two lemmas about the optimality equation . Proofs for the two lemmas are in Appendix A.

Lemma 2

For any period and fixed , is non-decreasing in .

Note that when is sufficiently large, there is no ordering quantity constraint for the retailer, and the problem is the same as the traditional problem in Scarf (1960). In this situation, for fixed , is constant.

Lemma 3

For any period , , .

Lemma 3 implies that the expected cash increment for state is larger than . Thus, for two initial states (, ) and (, ), if one state has less initial inventory but more initial cash, and the extra cash is sufficient to replenish the initial inventory to equal that of the other state (), then this state will result in a larger expected cash increment at the end of the planning horizon.

When initial inventory is below the s threshold, one may order or not depending on available cash. If the initial cash is small, the retailer cannot order up to its desired inventory level to make revenue cover the ordering costs. This situation leads to the existence of a threshold. When initial cash , it is better for the retailer to not order. We develop two forms of threshold .

| (25) | ||||

| (26) |

Lemma 4

Proof.

Eq. (25) is an apparent threshold. If initial cash is less than , it is always better for the retailer to not order because the retailer does not even have sufficient cash to cover the fixed ordering cost. For the initial cash defined by Eq. (26), because , it is better to order at full capacity since this ordering will result in the greatest cash increment. Thus, there are two scenarios:

-

(a).

do not order.

-

(b).

order units.

The rest of the proof is similar to that of Lemma 3. Since , . The cash increments for the two scenarios are as follows.

From Eq. (26), because . Define and as the expected cash increments of the two scenarios.

Since , and . By lemma 2, .

Therefore, , and it is better for the retailer to not order.

5 A heuristic ordering policy

With the existence of the threshold and threshold, the optimal ordering pattern is still very complex, except in the last period. Based on the above analysis and numerical tests, we propose a heuristic ordering policy.

policy:

| (27) |

Note that the values of and can vary by period, and the values of are state-dependent and related to initial inventory . policy indicates that if the initial inventory is less than and initial cash is above , the inventory level should be replenished to as close to as possible; otherwise, do not order.

5.1 Computation for , and

To compute values of , and we provide two methods here: the first involves searching the results of stochastic dynamic programming (SDP) with some heuristic techniques; the second is to approximate the problem with a mixed-integer model and solve the problem with some heuristic equations.

5.1.1 Obtaining , , and via SDP

Let represent the optimal ordering quantity for initial inventory and initial cash at period in the SDP results. The default values for and are zero, the default values for are fixed ordering cost .

For period , if , , , , if , , , can be fixed arbitrarily. When , the values of , and can be obtained by Eq. (19), (18), (20), respectively.

When , the method for obtaining , , is given below.

Find : is selected as the minimum initial inventory level that results in not ordering for all cash states in the SDP results.

Find : in a given period, when , there may be more than one order-up-to level, as shown by our previous numerical case. We adopt a heuristic step by selecting the most frequent order-up-to level as .

Find : for initial inventory in a given period and , is the maximum value of initial cash that results in not ordering in the SDP results.

The pseudo-code of this method is given in Algorithm 1 of Appendix B. Since this method is based on the results of SDP, it enumerates all the states in each period. This is very time-consuming when the planning horizon is large. For example, in our numerical tests, if the length of the planning horizon is 15, it may take more than one hour to compute one case. So this method is only suitable for the cases of small planning horizons.

5.1.2 Obtaining , , and values by mixed-integer programming (MIP) approximation

The method here adopts a similar idea of “static-dynamic uncertainty” strategy in Bookbinder and Tan (1988). Replenishment periods are first computed at the beginning of the planning horizon by a MIP model; then we decide the values of , and by approximating a newsvendor problem in each replenishment cycle.

The expected demand, end-of-period cash, and end-of-period inventory for period are represented by , and , respectively. The mixed-integer programming (MIP) model for the cash-constrained problem is as follows. The major role of the MIP model is to obtain a heuristic ordering plan by determining the values of binary variable that represents whether to order or not in period .

| (28) | ||||

| s.t. | ||||

| (29) | ||||

| (30) | ||||

| (31) | ||||

| (32) | ||||

| (33) | ||||

| (34) |

In the MIP model, decision variable is the order-up-to level in period . Objective function Eq. (28) is the expected cash increment in the planning horizon. The cash constraint is represented by (29), and expected cash flow is given by (30). Constraint (31) indicates that the order-up-to level should not be less than the period’s expected initial inventory. Constraint (32) represents the relationship of with and . Constraint (33) is the value of initial inventory and initial cash. Constraint (34) ensures the nonnegativity and/or the binary nature of the decision variables.

For the last period, , and are obtained by equations (18), (19) and (20). For , we compute them in the following.

-

1.

Compute .

Ordering cycles can be obtained from the results of in the MIP model. For example, if , there are two ordering cycles in this ordering plan: period 13 and period 45. This can by shown by Figure 2.

Figure 2: A sketch of two consecutive ordering cycles Because the demands in each period are independent, the demands in an ordering cycle follow a joint distribution. Assume that the beginning period for an ordering cycle is and that the end period for an ordering cycle is (). Let represent the joint probability density function from period to period and represent the joint cumulative distribution function. Then, in an ordering cycle, the expected cash increment without fixed ordering cost and overhead cost from period () to is similar to a newsvendor model, that is:

(35) Since is concave, it reaches its maximum at () or (). () can be computed by the following heuristic equation:

(36) In Eq. (36), is the approximate maximum order-up-to level for period . The relation of , and for a numerical case is shown in Figure 3, where the red line represents and in this case.

Figure 3: , , and -

2.

Compute .

In an ordering cycle , we use a heuristic step to compute () by the following equation.(37) -

3.

Compute .

When initial inventory , for period (), is computed by the following heuristic equation.(38) Note that is related to initial inventory . In Eq. (38), is the one-period expected cash increment without overhead cost for period , and is its maximum point, which is . The relationship of and is shown in Figure 4. Eq. (38) suggests that if the one-period maximum cash increment is less than the fixed ordering cost, the retailer should not order and is a large number ; otherwise, is the maximum cash such that the one-period expected cash increment minus the ordering costs of ordering full capacity is larger than the cost of not ordering.

Figure 4:

5.2 An illustrative example

To further illustrate the policy and our computational methods, we present a numerical example: there are 4 periods, and the demands in each period follow a Poisson distribution. The mean demand in each period is [20, 7, 2, 14]. Other relevant parameter values are fixed ordering cost , unit variable ordering cost , overhead cost , selling price , unit salvage value , initial inventory , and initial cash . The results of different methods are given in Table 3.

| Optimality gap | |||||

| SDP method | 0.00% | ||||

| MIP method | 3.49% | ||||

As Table 3 shows, the SDP method is near-optimal, while the MIP method has an optimality gap 3.49%.

6 Computational study

In this section, we present an extensive computational study on large test beds to investigate the effectiveness of the ordering policy and computational methods we proposed.

6.1 Test bed

The test beds are adopted from Rossi et al. (2015) with some modifications. There are 10 demand patterns for numerical analysis: 2 life cycle patterns (LCY1 and LCY2), 2 sinusoidal patterns (SIN1 and SIN2), 1 stationary pattern (STA), 1 random pattern (RAND), and 4 empirical patterns (EMP1, EMP2, EMP3, EMP4). To ensure that SDP can solve these instances in reasonable time, we rescale the original demand values, select 10 successive periods for testing, and make cash and inventory be integers. The expected demands for different patterns are given in Table 5 and Figure 5 in Appendix C.

Fixed ordering cost takes values in (10, 15, 20); unit variable ordering cost is 1, overhead cost and unit salvage value ; price takes values in (5, 6, 7), which results in product margin taking values in (4, 5, 6); and initial cash capacity takes values in (6, 8, 10), which means initial cash is sufficient to order 6, 8 or 10 items. For example, if initial cash capacity is 6, initial cash . The initial cash capacity settings guarantee that the retailer does not have enough cash in the first period for all the cases, which makes these cases different from uncapacitated situations. Demands follow a Poisson distribution and are independent in each period. Therefore, there are 270 numerical cases in total for each ordering policy.

The computational studies are coded in Java and run on a desktop computer with an Intel (R) Core (TM) i5-7500 CPU, at 3.40 GHz, 8 GB of RAM, and 64-bit Windows 7 operating system.

6.2 Results analysis

We compare this heuristic policy with the optimal results directly obtained by stochastic dynamic programming (SDP). After the values of , and of the different methods are obtained, we simulate them in 100,000 stochastic demand samples to obtain the expected final values and compare the gaps with respect to SDP. The average optimality gap (AVG) and maximum optimal gap (MAX) are adopted as performance metrics. Comprehensive comparison results are shown in Table 4.

| by SDP | by MIP | Cases | |||

| MAX | AVG | MAX | AVG | ||

| Fixed ordering cost | |||||

| 10 | 0.41% | 0.00% | 4.85% | 1.35% | 90 |

| 15 | 0.27% | 0.00% | 10.91% | 1.93% | 90 |

| 20 | 0.65% | 0.03% | 17.66% | 2.87% | 90 |

| Margin | |||||

| 4 | 0.65% | 0.03% | 17.66% | 2.87% | 90 |

| 5 | 0.27% | 0.00% | 10.55% | 1.89% | 90 |

| 6 | 0.02% | 0.00% | 5.49% | 1.39% | 90 |

| Cash capacity | |||||

| 6 | 0.65% | 0.02% | 17.66% | 2.47% | 90 |

| 8 | 0.45% | 0.01% | 7.85% | 1.99% | 90 |

| 10 | 0.33% | 0.00% | 8.17% | 1.70% | 90 |

| Demand pattern | |||||

| STA | 0.33% | 0.01% | 2.63% | 0.91% | 27 |

| LC1 | 0.00% | 0.00% | 2.50% | 1.14% | 27 |

| LC2 | 0.04% | 0.01% | 3.07% | 1.68% | 27 |

| SIN1 | 0.65% | 0.06% | 4.93% | 1.35% | 27 |

| SIN2 | 0.41% | 0.04% | 17.66% | 2.93% | 27 |

| RAND | 0.00% | 0.00% | 3.17% | 1.20% | 27 |

| EMP1 | 0.01% | 0.00% | 10.04% | 3.09% | 27 |

| EMP2 | 0.00% | 0.00% | 6.28% | 2.26% | 27 |

| EMP3 | 0.03% | 0.00% | 11.00% | 3.44% | 27 |

| EMP4 | 0.01% | 0.00% | 9.09% | 2.52% | 27 |

| Gap over 1% | 0 | 182 | |||

| Avg Time | 305s | 0 s | |||

| General | 0.65% | 0.01% | 17.66% | 2.05% | 270 |

As shown in the table, policy performs very well in terms of both the maximum gap (0.65%) and the average gap (0.01%) of the SDP method. The MIP method has a maximum gap of approximately 17.66% and an average gap of approximately 2.05%. Among all 270 numerical cases in the test bed, there are no instances for the SDP method that have an optimality gap greater than 1%. For the MIP method, 182 numerical cases have a gap exceeding 1%.

When fixed ordering cost increases, the numerical tests show that the MIP method performs worse with obvious increasing optimality gaps (average gap changes from 1.35% to 2.87%, maximum gap changes from 4.85% to 17.66%) and there are also slightly increasing optimality gaps for the SDP method (average gap changes from 0.00% to 0.03%). However, with an increasing margin of the product or cash capacity, both methods perform better with lower optimality gaps.

The results also suggest that demand patterns may have a large effect on the performance of the two methods. For example, the maximum gaps and average gaps all grow large in demand pattern EMP1, EMP2, EMP3, EMP4 for policy the MIP method. But for the SDP method, the demand patterns do not have a clear influence to its average gaps. Moreover, for the stationary demand pattern (STA) which has the least demand fluctuation, both methods show good performance with low maximum gap and average gap.

In terms of computational efficiency, the average running time for the SDP method exceeds 300 seconds. However, the MIP approximation method is very fast, with an average running time of less than 1 second. Adding that its average gap is very low (2.05%), the MIP method performs very well.

7 Conclusions

Cash flow management is a key concern for many small businesses. In this paper, we consider a cash-constrained retailer with fixed ordering costs to maximize its final expected cash increment. We find that the optimal ordering policy for this problem is complex but has a structure: when initial inventory is over the threshold, do not order; when initial inventory is lower than the threshold, but initial cash is less than the threshold, do not order either. We propose a heuristic ordering policy for this problem: . Computational experiments demonstrate that performs well featuring a very small optimality gap. A heuristic method that approximates this problem as a mixed-integer linear model and newsvendor problem is also developed to compute the values of , and . Tests show that this method can solve the problem rapidly with narrow optimality gaps. Future research could extend this work in several directions: the first extension is to consider lead time (time lag) in the problem; the second possible extension is to investigate the cash flow constraints in the multi-item stochastic inventory problem.

Acknowledgments

The research presented in this paper is supported by the Fundamental Research Funds for the Central Universities of China under Project SWU1909738, National Natural Science Foundation of China under projects 71571006.

References

- Archibald et al. (2002) Thomas W Archibald, Lyn C Thomas, John M Betts, and Robert B Johnston. Should start-up companies be cautious? inventory policies which maximise survival probabilities. Management Science, 48(9):1161–1174, 2002.

- Archibald et al. (2015) Thomas W Archibald, Edgar Possani, and Lyn C Thomas. Managing inventory and production capacity in start-up firms. Journal of the Operational Research Society, 66(10):1624–1634, 2015.

- Bi et al. (2018) Gongbing Bi, Lei Song, and Yalei Fei. Dynamic mixed-item inventory control with limited capital and short-term financing. Annals of Operations Research, pages 1–32, 2018.

- Bian et al. (2018) Yuan Bian, David Lemoine, Thomas G Yeung, Nathalie Bostel, Vincent Hovelaque, Jean-Laurent Viviani, and Fabrice Gayraud. A dynamic lot-sizing-based profit maximization discounted cash flow model considering working capital requirement financing cost with infinite production capacity. International Journal of Production Economics, 196:319–332, 2018.

- Bollapragada and Morton (1999) Srinivas Bollapragada and Thomas E. Morton. A simple heuristic for computing nonstationary (s, s) policies. Operations Research, 47(4):576–584, 1999.

- Bookbinder and Tan (1988) James H Bookbinder and Jin-Yan Tan. Strategies for the probabilistic lot-sizing problem with service-level constraints. Management Science, 34(9):1096–1108, 1988.

- Boulaksil and van Wijk (2018) Y. Boulaksil and A.C.C. van Wijk. A cash-constrained stochastic inventory model with consumer loans and supplier credits: the case of nanostores in emerging markets. International Journal of Production Research, 2018. doi: 10.1080/00207543.2018.1424368.

- Buzacott and Zhang (2004) John A Buzacott and Rachel Q Zhang. Inventory management with asset-based financing. Management Science, 50(9):1274–1292, 2004.

-

CBInsights (2018)

CBInsights.

The top 20 reasons startups fail.

https://www.cbinsights.com/research/startup-failure-reasons-top/, accessed 4 November 2018, 2018. - Chan and Song (2003) Gin Hor Chan and Yuyue Song. A dynamic analysis of the single-item periodic stochastic inventory system with order capacity. European Journal of Operational Research, 146(3):529–542, 2003.

- Chao and Zipkin (2008) Xiuli Chao and Paul H Zipkin. Optimal policy for a periodic-review inventory system under a supply capacity contract. Operations Research, 56(1):59–68, 2008.

- Chao et al. (2008) Xiuli Chao, Jia Chen, and Shouyang Wang. Dynamic inventory management with cash flow constraints. Naval Research Logistics, 55:758–768, 2008.

- Chen and Simchi-Levi (2004) Xin Chen and David Simchi-Levi. Coordinating inventory control and pricing strategies with random demand and fixed ordering cost: The finite horizon case. Operations Research, 52(6):887–896, 2004.

- Chen and Zhang (2019) Zhen Chen and Ren-qian Zhang. A cash-constrained dynamic lot-sizing problem with loss of goodwill and credit-based loan. International Transactions in Operational Research, 0(0), 2019. doi: 10.1111/itor.12675. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/itor.12675.

- Cooper et al. (1997) Martha C Cooper, Douglas M Lambert, and Janus D Pagh. Supply chain management: more than a new name for logistics. The international journal of logistics management, 8(1):1–14, 1997.

- Dada and Hu (2008) Maqbool Dada and Qiaohai Hu. Financing newsvendor inventory. Operations Research Letters, 36(5):569–573, 2008.

- Federgruen and Zipkin (1984) Awi Federgruen and Paul Zipkin. An efficient algorithm for computing optimal (s, s) policies. Operations research, 32(6):1268–1285, 1984.

- Feng and Xiao (2000) Youyi Feng and B Xiao. A new algorithm for computing optimal (s, s) policies in a stochastic single item/location inventory system. IIE Transactions, 32(11):1081–1090, 2000.

- Gallego and Scheller-Wolf (2000) Guillermo Gallego and Alan Scheller-Wolf. Capacitated inventory problems with fixed order costs: Some optimal policy structure. European Journal of Operational Research, 126(3):603–613, 2000.

- Gong et al. (2014) Xiting Gong, Xiuli Chao, and David Simchi-Levi. Dynamic inventory control with limited capital and short-term financing. Naval Research Logistics, 61(3):184–201, 2014.

- Graves (1999) Stephen C Graves. A single-item inventory model for a nonstationary demand process. Manufacturing & Service Operations Management, 1(1):50–61, 1999.

- Helber (1998) Stefan Helber. Cash-flow oriented lot sizing in mrp ii systems. In Beyond Manufacturing Resource Planning (MRP II), pages 147–183. Springer, 1998.

- John (2014) AKINYOMI Oladele John. Effect of cash management on profitability of nigerian manufacturing firms. International journal of marketing and technology, 4(1):129, 2014.

- Katehakis et al. (2016) Michael N Katehakis, Benjamin Melamed, and Jim Shi. Cash-flow based dynamic inventory management. Production & Operations Management, 25(9):1558–1575, 2016.

- Kouvelis and Zhao (2012) Panos Kouvelis and Wenhui Zhao. Financing the newsvendor: supplier vs. bank, and the structure of optimal trade credit contracts. Operations Research, 60(3):566–580, 2012.

- Luo and Shang (2019) Wei Luo and Kevin H Shang. Managing inventory for firms with trade credit and deficit penalty. Operations Research, 2019.

- Moussawi-Haidar and Jaber (2013) Lama Moussawi-Haidar and Mohamad Y Jaber. A joint model for cash and inventory management for a retailer under delay in payments. Computers & Industrial Engineering, 66(4):758–767, 2013.

- Özener et al. (2014) Okan Örsan Özener, Refik Güllü, and Nesim Erkip. Near-optimal modified base stock policies for the capacitated inventory problem with stochastic demand and fixed cost. Asia-Pacific Journal of Operational Research, 31(03):1450019, 2014.

- Raghavan and Mishra (2011) NR Srinivasa Raghavan and Vinit Kumar Mishra. Short-term financing in a cash-constrained supply chain. International Journal of Production Economics, 134(2):407–412, 2011.

- Rossi et al. (2015) Roberto Rossi, Onur A Kilic, and S Armagan Tarim. Piecewise linear approximations for the static–dynamic uncertainty strategy in stochastic lot-sizing. Omega, 50:126–140, 2015.

- Scarf (1960) Herbert Scarf. The optimality of (s, s) policies in the dynamic inventory problem. Mathematical Methods in the Social Sciences, pages 196–202, 1960.

- Shaoxiang (2004) Chen Shaoxiang. The infinite horizon periodic review problem with setup costs and capacity constraints: A partial characterization of the optimal policy. Operations Research, 52(3):409–421, 2004.

- Shaoxiang and Lambrecht (1996) Chen Shaoxiang and M. Lambrecht. X-y band and modified (s, s) policy. Operations Research, 44(6):1013–1019, 1996.

- Shi et al. (2014) Cong Shi, Huanan Zhang, Xiuli Chao, and Retsef Levi. Approximation algorithms for capacitated stochastic inventory systems with setup costs. Naval Research Logistics, 61(4):304–319, 2014.

- Smirat and Yousef (2016) AL Smirat and B Yousef. Cash management practices and financial performance of small and medium enterprises (smes) in jordan. Research Journal of Finance and Accounting, 7(2):98–107, 2016.

- Tanrısever et al. (2012) Fehmi Tanrısever, S Sinan Erzurumlu, and Nitin Joglekar. Production, process investment, and the survival of debt-financed startup firms. Production and Operations Management, 21(4):637–652, 2012.

- Tunca and Zhu (2017) Tunay I. Tunca and Weiming Zhu. Buyer intermediation in supplier finance. Management Science, 2017. doi: https://doi.org/10.1287/mnsc.2017.2863.

- Wagner and Whitin (1958) Harvey M Wagner and Thomson M Whitin. Dynamic version of the economic lot size model. Management science, 5(1):89–96, 1958.

- Wu et al. (2016) Jiang Wu, Faisal B Al-Khateeb, Jinn-Tsair Teng, and Leopoldo Eduardo Cárdenas-Barrón. Inventory models for deteriorating items with maximum lifetime under downstream partial trade credits to credit-risk customers by discounted cash-flow analysis. International Journal of Production Economics, 171:105–115, 2016.

- Xiang et al. (2018) Mengyuan Xiang, Roberto Rossi, Belen Martin-Barragan, and S Armagan Tarim. Computing non-stationary (s, s) policies using mixed integer linear programming. European Journal of Operational Research, 271(2):490–500, 2018.

- Yang et al. (2014) Yi Yang, Quan Yuan, Weili Xue, and Yun Zhou. Analysis of batch ordering inventory models with setup cost and capacity constraint. International Journal of Production Economics, 155:340–350, 2014.

- Zeballos et al. (2013) Ariel C Zeballos, Ralf W Seifert, and Margarita Protopappa-Sieke. Single product, finite horizon, periodic review inventory model with working capital requirements and short-term debt. Computers & Operations Research, 40(12):2940–2949, 2013.

- Zheng and Federgruen (1991) Yu-Sheng Zheng and Awi Federgruen. Finding optimal (s, s) policies is about as simple as evaluating a single policy. Operations research, 39(4):654–665, 1991.

Appendix A Proofs for Lemma 2 and Lemma 3

A.1 Proof for Lemma 2

Proof.

When , . It is intuitively clear that is non-decreasing in .

Now, suppose this property holds for period ; we prove the results for period .

When is increased to , decision variable has a larger domain. Assume the optimal for initial cash is . For initial cash , let its decision . Thus, . From Eq. (11) and (13), , , . In Eq. (14), because is not less than by supposition, is not less than .

Lemma 2 is thus proved by induction.

A.2 Proof for Lemma 2

Proof.

For two scenarios of states and , let and represent the one-period cash increment of the two scenarios, respectively. From Eq. (14),

Scenario (a):

| (39) |

Scenario (b):

| (40) |

By Eq. (4), . The domain for Scenario (a) is , and the domain for Scenario (b) is . The domain for Scenario (a) is larger than that of Scenario (b). For any decision in Scenario (b), let . Then,

Therefore, . The end-of-period cash of period for the two scenarios is:

Appendix B Algorithms to compute , and

Appendix C Demand patterns in the test bed

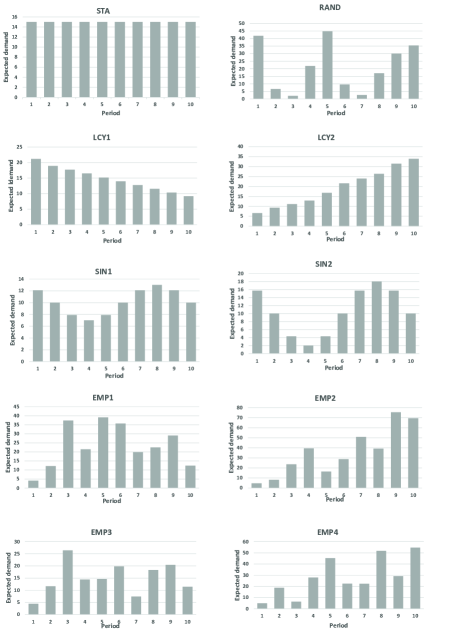

| Demand pattern | Expected demand values | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| STA | 15 | 15 | 15 | 15 | 15 | 15 | 15 | 15 | 15 | 15 |

| LC1 | 21.15 | 18.9 | 17.7 | 16.5 | 15.15 | 13.95 | 12.75 | 11.55 | 10.35 | 9.15 |

| LC2 | 6.6 | 9.3 | 11.1 | 12.9 | 16.8 | 21.6 | 24 | 26.4 | 31.5 | 33.9 |

| SIN1 | 12.1 | 10 | 7.9 | 7 | 7.9 | 10 | 12.1 | 13 | 12.1 | 10 |

| SIN2 | 15.7 | 10 | 4.3 | 2 | 4.3 | 10 | 15.7 | 18 | 15.7 | 10 |

| RAND | 41.8 | 6.6 | 2 | 21.8 | 44.8 | 9.6 | 2.6 | 17 | 30 | 35.4 |

| EMP1 | 4.08 | 12.16 | 37.36 | 21.44 | 39.12 | 35.68 | 19.84 | 22.48 | 29.04 | 12.4 |

| EMP2 | 4.7 | 8.1 | 23.6 | 39.4 | 16.4 | 28.7 | 50.8 | 39.1 | 75.4 | 69.4 |

| EMP3 | 4.4 | 11.6 | 26.4 | 14.4 | 14.6 | 19.8 | 7.4 | 18.3 | 20.4 | 11.4 |

| EMP4 | 4.9 | 18.8 | 6.4 | 27.9 | 45.3 | 22.4 | 22.3 | 51.7 | 29.1 | 54.7 |