ITENE: Intrinsic Transfer Entropy Neural Estimator

Abstract

Quantifying the directionality of information flow is instrumental in understanding, and possibly controlling, 00footnotetext: J. Zhang, O. Simeone, and Z. Cvetkovic are with the Department of Engineering at King’s College London, UK (emails: jingjing.1.zhang@kcl.ac.uk, osvaldo.simeone@kcl.ac.uk, zoran.cvetkovic@kcl.ac.uk). E. Abela and M. Richardson are with the Department of Basic and Clinical Neuroscience at King’s College London, UK (emails: eugenio.abela@kcl.ac.uk, mark.richardson@kcl.ac.uk). J. Zhang and O. Simeone have received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 Research and Innovation Programme (Grant Agreement No. 725731). J. Zhang has also been supported by a King’s Together award. Code can be found at https://github.com/kclip/ITENE. the operation of many complex systems, such as transportation, social, neural, or gene-regulatory networks. The standard Transfer Entropy (TE) metric follows Granger’s causality principle by measuring the Mutual Information (MI) between the past states of a source signal and the future state of a target signal while conditioning on past states of . Hence, the TE quantifies the improvement, as measured by the log-loss, in the prediction of the target sequence that can be accrued when, in addition to the past of , one also has available past samples from . However, by conditioning on the past of , the TE also measures information that can be synergistically extracted by observing both the past of and , and not solely the past of . Building on a private key agreement formulation, the Intrinsic TE (ITE) aims to discount such synergistic information to quantify the degree to which is individually predictive of , independent of ’s past. In this paper, an estimator of the ITE is proposed that is inspired by the recently proposed Mutual Information Neural Estimation (MINE). The estimator is based on variational bound on the KL divergence, two-sample neural network classifiers, and the pathwise estimator of Monte Carlo gradients.

Index Terms:

Transfer entropy, neural networks, machine learning, intrinsic transfer entropy.I Introduction

I-A Context and Key Definitions

Quantifying the causal flow of information between different components of a system is an important task for many natural and engineered systems, such as neural, genetic, transportation and social networks. A well-established metric that has been widely applied to this problem is the information-theoretic measure of Transfer Entropy (TE) [1, 2]. To define it mathematically, consider two jointly stationary random processes with The TE from process to process with memory parameters is defined as the conditional Mutual Information (MI) [1, 3]

| (1) |

where and denote the past and samples of time sequences and . By definition (1), the TE measures the MI between the past samples of process and the current sample of process when conditioning on the past samples of the same process. Therefore, the TE quantifies the amount by which the prediction of the sample can be improved, in terms of average log-loss in bits, through the knowledge of samples of process when the past samples of the same process are also available. While not further considered in this paper, we note for reference that a related information-theoretic measure that originates from the analysis of communication channels with feedback [4, 5] is the Directed Information (DI). The DI is defined as

| (2) |

where we have normalized by the number of samples to facilitate comparison with TE. For jointly Markov processes111This implies the Markov chain . , with memory parameters and , the TE (1) is an upper bound on the DI (2) [6].

The TE, and the DI, have limitations as measures of intrinsic, or exclusive, information flow from to . This is due to the fact that conditioning on past samples of does not discount the information that the past samples of contain about its current sample : Conditioning also captures the information that can be synergistically obtained by observing both past samples and . In fact, there may be information about that can be extracted from only if this is observed jointly with . This may not be considered as part of the intrinsic information flow from to .

Example [7]: Assume that the variables are binary, and that the joint distribution of the variables is given as . It can be seen that observing both and allows the future state to be determined with certainty, while alone is not predictive of , since and are statistically independent. The TE with memory parameter is given as bit, although there is no intrinsic information flow between the two sequences but only a synergistic mechanism relating both and to .

In order to distinguish intrinsic and synergistic information flows, reference [7] proposed to decompose the TE into Intrinsic Transfer Entropy (ITE) and Synergistic Transfer Entropy (STE). The ITE aims to capture the amount of information on that is contained in the past of in addition to that already present in the past of ; while the STE measures the information about that is obtained only when combining the past of both and . Formally, the ITE from process to process with memory parameters is defined as [7]

| (3) |

In definition (3), auxiliary variables can take values without loss of generality in the same alphabet as the corresponding variables [8], and are obtained by optimising the conditional distribution . The quantity (3) can be shown to be an upper bound on the size (in bits) of a secret key that can be generated by two parties, one holding and the other , via public communication when the adversary has [9]. This intuitively justifies its use as a measure of intrinsic information flow. The STE is then defined as the residual

| (4) |

I-B TE and DI Estimation

The TE can be estimated using tools akin to the estimation of MI, including plug-in methods [10], non-parametric techniques based on kernel [1] or k-nearest-neighbor (k-NN) methods [11, 12], and parametric techniques, such as Maximum Likelihood [13] or Bayesian estimators [14]. Popular implementations of some of these standard methods can be found in the Java Information Dynamics Toolkit (JIDT) [15] and TRENTOOL toolbox [16]. For the DI, estimators have been designed that rely on parametric and non-parametric techniques, making use also of universal compressors [17, 18, 19]. In order to enable scaling over large data sets and/or data dimensions, MI estimators that leverage neural networks have been recently the subject of numerous studies. Notably, reference [20] introduced the Mutual Information Neural Estimator (MINE), which reduces the problem of estimating MI to that of classifying dependent vs. independent pairs of samples via the Donsker-Varadhan (DV) variational equality. Specifically, reference [20] proposes to train a neural network to approximate the solution of the optimization problem defined by the DV equality. The follow-up paper [21] proposes to train a two-sample neural network classifier, which is then used as an approximation of the likelihood ratio in the DV equality. Theoretical limitations of general variational MI estimators were derived in [22], which also proposes a variational MI estimator with reduced variance. We note that reference [21] also considers the estimation of the conditional MI, which applies directly to the estimate of the TE as discussed in Section II.

I-C Main Contributions, Paper Organization, and Notation

This work proposes an estimator, referred to as ITE Neural Estimator (ITENE), of the ITE that is based on two-sample classifier and on the pathwise estimator of Monte Carlo gradients, also known as reparameterization trick [23]. We also present numerical results to illustrate the performance of the proposed estimator. The paper is organized as follows. In Section II, we review the classifier-based MINE approach proposed in reference [21]. Based on this approach, we introduce the proposed ITENE method in Section III. Section IV presents experimental results. Throughout this paper, we use uppercase letters to denote random variables and corresponding lowercase letters to denote their realizations. represents the natural logarithm. represents the gradient of scalar function and the Jacobian matrix of vector function .

II Background: Classifier-based Mutual Information Neural Estimator (MINE)

In this section, we review the classifier-based MINE for the estimation of the MI between jointly distributed continuous random variables and . The MI satisfies the DV variational representation [24]

| (5a) | ||||

| (5b) | ||||

where the supremum is taken over all functions in (5a) and in (5b) such that the two expectations in (5a) are finite. Note that (5) contains expectations both over the joint distribution of and and over the product of the marginals and . Intuitively, the functions and act as classifiers of a sample being either generated by the joint distribution or by the product distribution . This is done by functions and ideally outputing a larger value in the former case than in the latter [25, Chapter 6]. More precisely, following [22], we can interpret function as an unnormalized estimate of the likelihood ratio , with being its normalized version. This normalization ensures the condition , which is satisfied by the true likelihood ratio [22]. Mathematically, the supremum in (5b) is achieved when is equal to the likelihood ratio [22, Theorem 1], i.e.,

| (6) |

This observation motivates the classifier-based estimator introduced in [21]. To elaborate, given a data set of data points from the joint distribution , we label the samples with a target value . Furthermore, we construct a data set approximately distributed according to the product distribution by randomly resampling the values of (see line 3 in Algorithm 1). These samples are labeled as . We use notation to represent the posterior probability that a sample is generated from the distribution when the hypotheses and are a priori equally likely. An estimate of the probability can be obtained by training a function parametrized as a neural network with input and , target output , and weight vector . This is done via the minimization of the empirical cross-entropy loss evaluated on the described data sets (see lines 8-10 in Algorithm 1) via Stochastic Gradient Descent (SGD) (see, e.g., [25, Chapter 6]). Having completed training, the likelihood ratio can be estimated as

| (7) |

This follows since, at convergence, if training is successful, the following equality holds approximately

| (8) |

Finally, the estimate (7) can be plugged into an empirical approximation of (5b) as

| (9) |

where represents the empirical distribution of the observed data sample pairs in an held-out part of data set , while and are the corresponding empirical marginal distributions for and (see line 11 in Algorithm 1); and the clip function is defined as with some constant [22]. Clipping was suggested in [22] in order to reduce variance of the estimate (9), and a similar approach is also used in [21]. The estimator (9) is known to be consistent but biased [20], and an analysis of the variance can be found in [22] (see also Lemma 1 below). Details are presented in Algorithm 1.

III Intrinsic Transfer Entropy Neural Estimator (ITENE)

In this section, inspired by the classifier-based MINE, we introduce an estimator for the ITE, which we refer to as ITENE. Throughout this section, we assume the availability of data in the form of time series generated as a realization of jointly stationary random processes . We use the notations , and and we also drop the subscript when no confusion may arise.

III-A TENE

We start by noting that, using the chain rule [26], the TE in (1) can be written as the difference

| (10) |

Therefore, the TE can be estimated by applying the classifier-based MINE in Algorithm 1 to both terms in (10) separately. This approach was proposed in [21] and found empirically to outperform other estimates of the conditional MI. Accordingly, we have the estimate

| (11) |

where the MINE estimates in (9) are obtained by applying Algorithm 1 to the data sets and , respectively (zero padding is used for out-of-range indices). We refer to the resulting estimator (11) as TENE. Following [21], TENE is consistent but biased. Furthermore, without using clipping, i.e., when , we have that the following lemma holds.

Lemma 1

Assume that the estimates and equal their respective true likelihood ratios, i.e., and . Then, under the randomness of the sampling procedure generating the data set , we have

| (12) |

The proof follows directly from [22, Theorem 1]. Lemma 1 demonstrates that, without clipping, the variance of TENE in (11) can grow exponentially with the maximum of the true values of and . Note that a similar result applies to MINE [22]. Setting a suitable value for is hence important in order to obtain reliable estimates.

III-B ITENE

We now move on to the estimator of the ITE (3). To this end, we first parameterize the distribution under optimization as

| (13) |

where and are disjoint sets of outputs of a neural network with weights ; is the element-wise product; and is a Gaussian vector independent of all other variables. Parameterization (13) follows the so-called reparameterization trick popularized by the variational auto-encoder [27]. An estimator of the ITE (3) can be defined by optimizing over the ITE (10) as

| (14) |

where we have made explicit the dependence of estimates and on . In particular, using (10), the first MINE estimate in (11) can be written as a function of as

| (15) |

where parameter is obtained from Algorithm 1 by considering as input the data set , where samples are generated using (13) as for i.i.d. samples . Furthermore, the empirical distributions in (15) are obtained from the held-out (estimation) data set in Algorithm 1. In a similar manner, the second MINE estimate in (14) is given as

| (16) |

where parameter is obtained from Algorithm 1 by considering as input the data set .

We propose to tackle problem (14) in a block coordinate fashion by iterating between SGD steps with respect to and updates of parameters using Algorithm 1. To this end, when fixing , the optimization over parameter requires the gradient

| (17) |

where, from (7), we have the gradient

| (18) |

and, from (13), we have the Jacobian . It also requires the gradient

| (19) |

where we have

| (20) |

We note that the gradients (17)-(19) are instances of pathwise gradient estimators [23]. The resulting ITENE is summarized in Algorithm 2. Due to the consistency of TENE, ITENE is also consistent if the capacity of the model is large enough.

IV Experiments

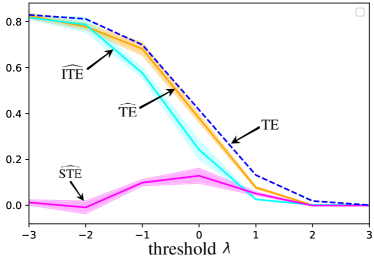

In this section, we provide some results to illustrate the type of insights that can be obtained by decomposing the TE into ITE and STE as in (4). To this end, consider first the following simple example. The joint processes are generated according to

| (23) |

for some threshold , where variables are independent and identically distributed as . Intuitively, for large values of the threshold , there is no information flow between and , while for small values, there is a purely intrinsic flow of information. For intermediate values of , the information flow is partly synergistic, since knowing both and is instrumental in obtaining information about . To quantify the intuition above, we apply the discussed estimators with . To this end, for all two-sample neural network classifiers, we consider two hidden layers with 100 hidden neurons with ELU activation functions, while for the probability , we adopt a neural network with hidden layer of 200 neurons with ELU activation functions and outputs and . The data set size is split into a -fraction for classifier training and a -fraction for estimation. We set learning rate and clipping parameter .

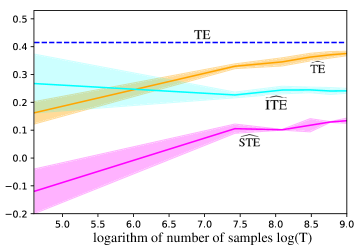

The computed estimates , , are plotted in Fig. 1 and Fig. 2 as a function of the threshold and the number of samples , respectively, along with the true TE. The latter can be computed in closed form as (nats), where is the standard complementary cumulative distribution function of a standard Gaussian variable. In a manner consistent with the intuition provided above, when is either small, i.e., , or large, i.e., , the ITE is seen in Fig. 1 to be close to the TE, yielding nearly zero STE. This is not the case for intermediate values of , in which regime a non-negligible STE is observed.

In Fig. 2, we investigate the impact of the number of samples when , at which point the gap between the ITE and the TE is the largest (see Fig. 1). As illustrated in the figure, the four estimates becomes increasingly accurate as increases, reflecting the consistency of the estimators.

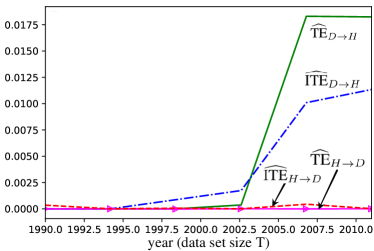

For a real-world example, we apply the estimators at hand to historic data of the values of the Hang Seng Index (HSI) and of the Dow Jones Index (DJIA) between 1990 and 2011. As done in [17], for each stock, we classify its values into three levels, namely , , and , where indicates an increase in the stock price by more than in one day, indicates a drop by more than , and indicates all other cases. As illustrated in Fig. 3, and in line with the results in [17], both the TE and ITE from the DJIA to the HSI are much larger than in the reverse direction, implying that the DJIA influenced the HSI more significantly than the other way around for the given time range. Furthermore, we observe that not all the information flow is estimated to be intrinsic, and hence the joint observation of the history of the DJIA and of the HSI is partly responsible for the predictability of the HSI from the DJIA.

V Conclusions

In this work, we have proposed an estimator for Intrinsic Transfer Entropy (ITE) between two time series based on two-sample neural network classifiers and the reparameterization trick. As future work, it would be interesting to apply the estimator to larger-scale data sets and to further investigate its theoretical properties.

Acknowledgements

Jingjing Zhang and Osvaldo Simeone have received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 Research and Innovation Programme (Grant Agreement No. 725731). Jingjing Zhang has also been supported by a King’s Together award.

References

- [1] T. Schreiber, “Measuring information transfer,” Phys. Rev. Lett., vol. 85, pp. 461–464, Jul. 2000.

- [2] R. Vicente, M. Wibral, and G. Lindner, Michaeland Pipa, “Transfer entropy—a model-free measure of effective connectivity for the neurosciences,” Journal of Computational Neuroscience, vol. 30, no. 1, pp. 45–67, Feb. 2011.

- [3] M. Wibral, N. Pampu, V. Priesemann, F. Siebenhühner, H. Seiwert, M. Lindner, J. T. Lizier, and R. Vicente, “Measuring information-transfer delays,” PLOS ONE, vol. 8, pp. 1–19, Feb. 2013.

- [4] J. L. Massey, “Causality, feedback and directed information,” in Proc. Int. Symp. Information Theory Applications (ISITA), Waikiki, Hawaii, Nov. 1990.

- [5] H. H. Permuter, Y. Kim, and T. Weissman, “Interpretations of directed information in portfolio theory, data compression, and hypothesis testing,” IEEE Trans. Inf. Theory, vol. 57, no. 6, pp. 3248–3259, Jun. 2011.

- [6] Y. Liu and S. Aviyente, “The relationship between transfer entropy and directed information,” in Proc. of Statistical Signal Process. Workshop (SSP), Michigan, USA, Aug. 2012, pp. 73–76.

- [7] R. G. James, B. D. M. Ayala, B. Zakirov, and J. P. Crutchfield, “Modes of information flow.” [Online]. Available: https://arxiv.org/abs/1808.06723

- [8] J. P. Crutchfield and D. P. Feldman, “Regularities unseen, randomness observed: levels of entropy convergence,” Chaos, vol. 13, no. 1, p. 25–54, 2003.

- [9] U. M. Maurer and S. Wolf, “Unconditionally secure key agreement and the intrinsic conditional information,” IEEE Trans. Inf. Theory, vol. 45, no. 2, pp. 499–514, Mar. 1999.

- [10] D. Freedman and P. Diaconis, “On the histogram as a density estimator: L2 theory,” Probability Theory and Related Fields, vol. 57, no. 4, pp. 453–476, Dec. 1981.

- [11] A. Kraskov, H. Stögbauer, and P. Grassberger, “Estimating mutual information,” Phys. Rev. E, vol. 69, Jun. 2004.

- [12] S. Frenzel and B. Pompe, “Partial mutual information for coupling analysis of multivariate time series,” Phys. Rev. Lett., vol. 99, p. 204101(4), Nov. 2007.

- [13] T. Suzuki, M. Sugiyama, J. Sese, and T. Kanamori, “Approximating mutual information by maximum likelihood density ratio estimation,” in Proc. of the Int. Conf. on New Challenges for Feature Selection in Data Min. and Knowledge Discovery, 2008, pp. 5–20.

- [14] D. H. Wolpert and D. R. Wolf, “Estimating functions of probability distributions from a finite set of samples,” Phys. Rev. E, vol. 52, pp. 6841–6854, Dec. 1995.

- [15] J. T. Lizier, “JIDT: An information-theoretic toolkit for studying the dynamics of complex systems,” Frontiers in Robotics and AI, vol. 1, p. 11, Dec. 2014.

- [16] M. Lindner, R. Vicente, V. Priesemann, and M. Wibral, “TRENTOOL: A matlab open source toolbox to analyse information flow in time series data with transfer entropy,” BMC Neuroscience 12, 119, Nov. 2011.

- [17] J. Jiao, H. H. Permuter, L. Zhao, Y. Kim, and T. Weissman, “Universal estimation of directed information,” IEEE Trans. Inf. Theory, vol. 59, no. 10, pp. 6220–6242, Oct. 2013.

- [18] C. J. Quinn, T. P. Coleman, N. Kiyavash, and N. G. Hatsopoulos, “Estimating the directed information to infer causal relationships in ensemble neural spike train recordings,” Journal of Computational Neuroscience, vol. 30, no. 1, pp. 17–44, Feb. 2011.

- [19] R. Malladi, G. Kalamangalam, N. Tandon, and B. Aazhang, “Identifying seizure onset zone from the causal connectivity inferred using directed information,” IEEE Journal of Selected Topics in Signal Process., vol. 10, no. 7, pp. 1267–1283, Oct. 2016.

- [20] M. I. Belghazi, A. Baratin, S. Rajeshwar, S. Ozair, Y. Bengio, A. Courville, and R. D. Hjelm, “Mutual information neural estimation,” in Proc. Int. Conf. on Machine Learning, Stockholm, Sweden, Jul. 2018.

- [21] S. Mukherjee, H. Asnani, and S. Kannan, “CCMI: Classifier based conditional mutual information estimation,” in Proc. the Conference on Uncertainty in Artificial Intelligence (UAI), Tel Aviv, Israel, Jul. 2019.

- [22] J. Song and S. Ermon, “Understanding the limitations of variational mutual information estimators,” 2019. [Online]. Available: https://arxiv.org/abs/1910.06222

- [23] S. Mohamed, M. Rosca, M. Figurnov, and A. Mnih, “Monte carlo gradient estimation in machine learning.” [Online]. Available: https://arxiv.org/abs/1906.10652

- [24] M. D. Donsker and S. R. S. Varadhan, “Asymptotic evaluation of certain markov process expectations for large time,” Communications on Pure and Applied Mathematics, vol. 36, pp. 183–212, 1983.

- [25] O. Simeone, A Brief Introduction to Machine Learning for Engineers. Foundations and Trends in Signal Processing, 2018. [Online]. Available: http://arxiv.org/abs/1709.02840

- [26] T. M. Cover and J. A. Thomas, Elements of Information Theory. New York, USA: Wiley-Interscience, 1991.

- [27] D. P. Kingma and M. Welling, “Auto-encoding variational bayes,” in Proc. Int. Conf. on Learning Representations (ICLR), Scottsdale, USA, May 2013.