Mean skewness measures

Abstract

Skewness measures can be used to measure the level of asymmetry of a distribution. Given the prevalence of statistical methods that assume underlying symmetry, and also the desire for symmetry in order to make meaningful judgements for common summary measures (e.g. the sample mean), reliably quantifying asymmetry is an important problem. There are several measures, among them generalizations of Bowley’s well known skewness coefficient, that use sample quartiles and other quantile-based measures. The main drawbacks of many measures is that they are either limited to quartiles and do not take into account more extreme tail behavior, or that they require one to choose other quantiles (i.e. choose a value for different from 0.25) in place of the quartiles. Our objective is to (i) average the skewness measures over all and (ii) provide interval estimators for the new measure with good coverage properties. Our simulation results show that the interval estimators perform very well for all distributions considered.

Keywords: Bowley’s coefficient of skewness, quantile-based skewness

1 Introduction

Let and denote the quantiles of a population distribution, so that is the median, then the well-known Bowley’s coefficient (Yule,, 1912; Bowley,, 1920) given as is a robust measure of skewness. Note that when the distribution is symmetric, then since . The magnitude of grows as the difference between and increasing implies increasing skewness. A more general case of the Bowley’s coefficient (David & Johnson,, 1956) can venture further into the tails than when using the first and third quartiles. This measure has been considered further by Hinkley, (1975), Groeneveld & Meeden, (1984) and Staudte, (2014) who provided distribution free confidence intervals for the measure. Groeneveld et al. , (2009) introduced an improved version for right skewed distributions for which good point and interval estimators can be easily obtained. This measure is appropriate only when the direction of the skewness is known, although in practice simple data visualisations can be used to decide. However, as stated by Groeneveld et al. , (2009), the measure is easier to interpret and typically more sensitive to skewness.

The generalised Bowley’s and the Groeneveld et al. , (2009) measures require one to chose the extremity of the quantiles used. To overcome this, Groeneveld & Meeden, (1984) integrated both the numerator and denominator of the measure over . Motivated by this, we introduce integrated versions of the measures which have simple interpretations and for which interval estimators with good coverage properties are available.

In Section 2 we introduce notations and existing measures of skewness using quantiles. In Section 3 we consider integration of the measures over before comparing with other measures in Section 4. Point and interval estimators are provided in Section 5 with simulations assessing coverage and applications to some examples following in Section 6. We then conclude the work in Section 7.

2 Notations and some selected methods

Let denote the distribution function for random variable and denote the density function. For a , let the th quantile be so that, for example, is the population median and and the other quartiles. Let denote the quantile density function (Tukey,, 1965; Parzen,, 1979) and its reciprocal, which we denote , is the density quantile function. Also let denote a simple random sample of size from . Throughout let denote the estimator of where we use the Hyndman & Fan, (1996) quantile estimator which can be found as the Type 8 quantile estimator in R software (Development Core Team,, 2008).

2.1 Generalized skewness coefficients

Using the notations above, the generalized Bowley’s coefficient is defined as

| (1) |

for (Hinkley,, 1975; Groeneveld & Meeden,, 1984). For later use we define the th interquantile skewness to be and the th interquantile range as so that . We denote the estimator of as

where and .

Groeneveld et al. , (2009) introduced a variation of that is simple to interpret and often more sensitive to skewness. For right-skewed distributions, this measure is defined as

| (2) |

for . Let so that with estimator

where . For left-skewed distributions, the measure can be adapted to . For simplicity we will focus on the use of as defined in (2) noting that findings will similarly hold when re-defining for left-skewed distributions.

To overcome the need for choosing a for , Groeneveld & Meeden, (1984) integrated both the numerator and denominator with respect to finding

| (3) |

where is the mean for distribution .

3 New skewness measures

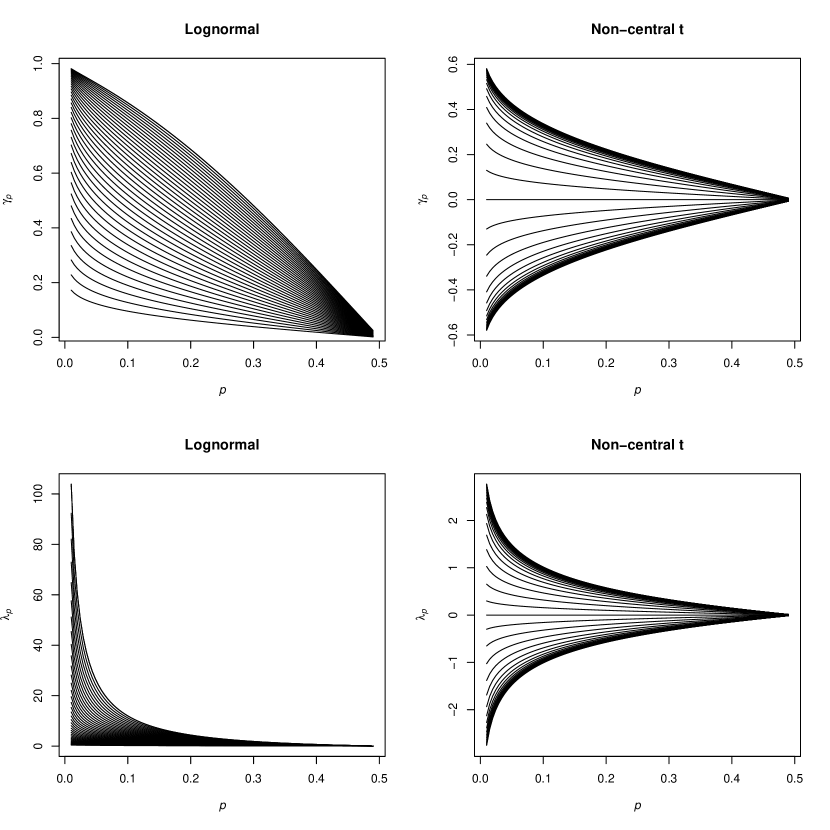

Note that and may be thought of as sensitivity curves over the domain of . In Figure 1 we plot the curves of (top row) and (bottom row) for two distributions: the lognormal distribution, LN, with varying from 0.01 to 2.0 and also the non-central distribution, with and non-centrality parameter (ncp) varying from to 10. For the lognormal, the curves are plotted for each choice of , where smaller are associated with the curves with smaller skew (lower vertical axis values). For the non-central , the curves with negative skewness are for (left skew), for the curve is constant at zero (symmetry) and for ncp the curves are for positive skew. Skewness increases with increasing ncp. In all cases skewness is maximised when the most extreme quantiles are used, i.e. smallest , and this is also when the distance between the curves is maximised suggesting greater sensitivity in detecting skewness for smallest . In practice, however, such extreme quantiles are difficult to estimate and so a not-so-small would be chosen.

3.1 Area under the skewness curve and mean skewness

One way to avoid choosing is to calculate the Area Under the sensitivity Curve (AUC) by integrating and over . That is, we define

| (4) |

An interpretation of the AUC above exists in the form of mean skewness. Let , then

| (5) |

so that the expected value for a point randomly chosen on the sensitivity curve is equal to one half of the AUC. This similarly true for the measures where .

Remark 1.

If one wanted the AUC and expected sensitivity above to be equal, then we could re-define

| (6) |

for so that . Then could be similarly defined with . We would then have that, for , and .

3.2 Weighting with respect to

Given that large values of and can result when is small, we could give less emphasis to the extremes by using and .

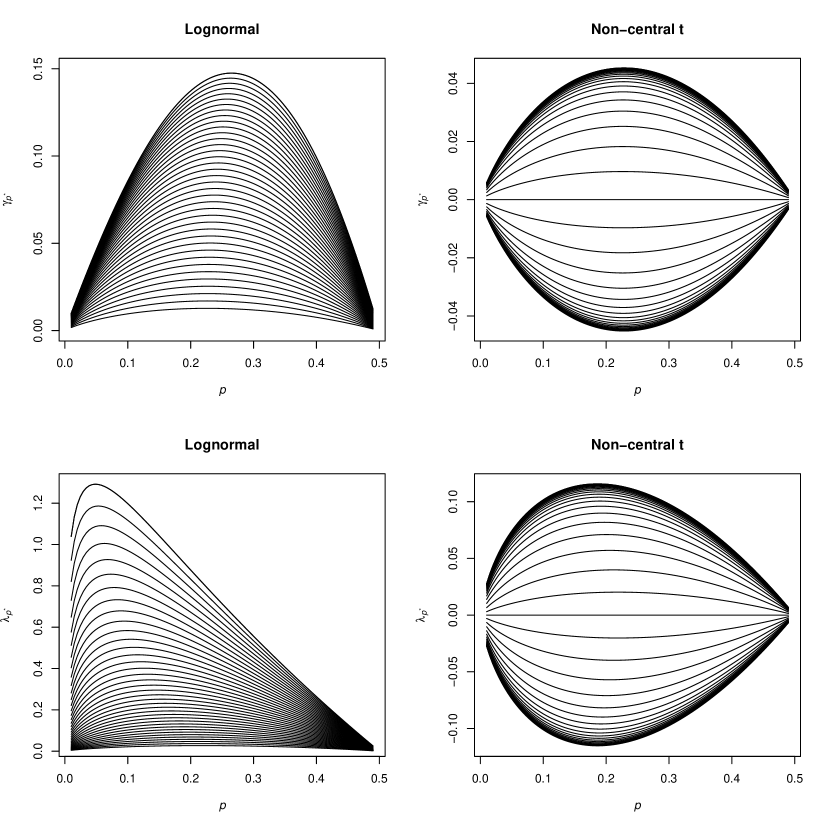

In Figure 2 we plot the curves for (top row) and (bottom row). Note that less weighting is now given to the extremes such that greater emphasis is placed on a choice of associated with greater density. For , that choice of is between 0.2 and 0.3 so that the peak in skew is approximately for when the measure is based on quartiles. For , the choice of is between approximately 0.05 and 0.1 depending on the chosen. This is in contrast to the other measures (see Figure 1), where peak skew occurred at the smallest (i.e. for the most extreme quantiles). Define the integrated , to be,

| (7) |

where, as before, these are one half of the mean skew over .

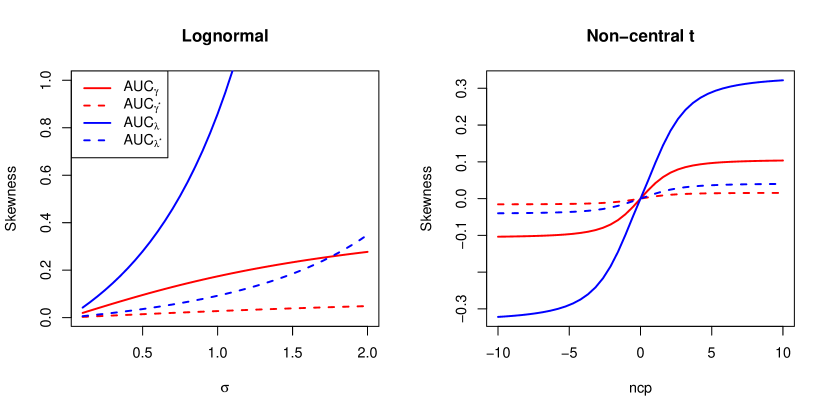

As example comparisons, all measures are depicted in Figure 3 for the lognormal with varying and the non-central with varying ncp.

4 Properties and comparisons with other measures

4.1 Properties

Oja, (1981) defined four desirable properties which are desirable for skewness measures. Let be a skewness measure where, for distribution function , is the measure of skewness for the distribution . Further, for denoting a random variable, for convenience we also let . These four properties are:

- P1.

-

for constants and .

- P2.

-

for symmetric .

- P3.

-

.

- P4.

-

If then .

| Property | ||||||

|---|---|---|---|---|---|---|

| P1 | + | + | + | + | + | + |

| P2 | + | + | + | + | + | + |

| P3 | + | + | + | |||

| P4 | + | + | + | + | + | + |

The notation ‘’, used by Groeneveld & Meeden, (1984) and Groeneveld et al. , (2009), is read as ‘ -precedes ’ meaning that distribution is at least as skewed to the right as distribution . Groeneveld & Meeden, (1984) has shown that satisfies Properties P1 - P4 while Groeneveld et al. , (2009) has shown that P1, P2 and P4 hold for . In both cases, for P4 to hold it is required that is convex. Given this, it is straightforward then to show that they also hold for the AUC measures and the properties are summarised in Table 1.

4.2 Comparisons of skewness for parametric families

We have carried out a comparison of the skewness measures , with our AUC measures over a wide range of distributions with different parameter choices.

| Distribution | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| LN(0, 1) | 0.676 | 0.565 | 0.476 | 0.398 | 0.325 | 4.180 | 2.602 | 1.819 | 1.320 | 0.963 | 0.175 | 0.858 | 0.028 | 0.092 |

| LN(1, 2) | 0.928 | 0.857 | 0.776 | 0.687 | 0.588 | 25.835 | 11.976 | 6.948 | 4.383 | 2.853 | 0.277 | 5.704 | 0.049 | 0.349 |

| Exp() | 0.564 | 0.465 | 0.388 | 0.322 | 0.262 | 2.587 | 1.738 | 1.269 | 0.950 | 0.710 | 0.144 | 0.540 | 0.022 | 0.065 |

| 0.564 | 0.465 | 0.388 | 0.322 | 0.262 | 2.587 | 1.738 | 1.269 | 0.950 | 0.710 | 0.144 | 0.540 | 0.022 | 0.065 | |

| 0.354 | 0.281 | 0.230 | 0.188 | 0.151 | 1.096 | 0.782 | 0.596 | 0.462 | 0.356 | 0.087 | 0.242 | 0.013 | 0.032 | |

| 0.156 | 0.122 | 0.099 | 0.080 | 0.064 | 0.369 | 0.277 | 0.219 | 0.175 | 0.138 | 0.038 | 0.085 | 0.006 | 0.012 | |

| PAR(1,4) | 0.680 | 0.568 | 0.477 | 0.398 | 0.325 | 4.250 | 2.625 | 1.827 | 1.322 | 0.963 | 0.175 | 0.872 | 0.028 | 0.092 |

| PAR(1,7) | 0.633 | 0.525 | 0.440 | 0.366 | 0.298 | 3.446 | 2.210 | 1.571 | 1.154 | 0.850 | 0.162 | 0.709 | 0.025 | 0.080 |

| PAR(1,100) | 0.325 | 0.469 | 0.392 | 0.325 | 0.264 | 0.963 | 1.768 | 1.289 | 0.963 | 0.719 | 0.145 | 0.551 | 0.023 | 0.066 |

| Beta(2,5) | 0.223 | 0.431 | 0.145 | 0.118 | 0.095 | 0.574 | 0.177 | 0.338 | 0.268 | 0.211 | 0.055 | 0.132 | 0.008 | 0.018 |

| Beta(5,10) | 0.106 | 0.083 | 0.068 | 0.055 | 0.044 | 0.238 | 0.182 | 0.145 | 0.117 | 0.092 | 0.026 | 0.056 | 0.004 | 0.008 |

| WEI(0.5) | 0.893 | 0.823 | 0.746 | 0.661 | 0.568 | 16.776 | 9.273 | 5.869 | 3.899 | 2.624 | 0.268 | 3.180 | 0.047 | 0.279 |

| WEI(1) | 0.564 | 0.465 | 0.388 | 0.322 | 0.262 | 2.587 | 1.738 | 1.269 | 0.950 | 0.710 | 0.144 | 0.540 | 0.022 | 0.065 |

| WEI(2) | 0.194 | 0.148 | 0.118 | 0.095 | 0.076 | 0.482 | 0.348 | 0.269 | 0.211 | 0.164 | 0.046 | 0.108 | 0.007 | 0.015 |

| WEI(10) | -0.099 | -0.148 | -0.121 | -0.099 | -0.080 | -0.180 | -0.257 | -0.215 | -0.180 | -0.147 | -0.046 | -0.080 | -0.007 | -0.013 |

| Gamma(2) | 0.397 | 0.929 | 0.260 | 0.213 | 0.172 | 1.317 | 0.929 | 0.702 | 0.541 | 0.414 | 0.098 | 0.287 | 0.015 | 0.037 |

| Gamma(5) | 0.248 | 0.195 | 0.158 | 0.129 | 0.104 | 0.660 | 0.484 | 0.377 | 0.296 | 0.231 | 0.061 | 0.149 | 0.009 | 0.020 |

| Gamma(10) | 0.174 | 0.136 | 0.111 | 0.090 | 0.072 | 0.423 | 0.316 | 0.249 | 0.198 | 0.156 | 0.042 | 0.097 | 0.006 | 0.014 |

| F(1, 6) | 0.829 | 0.735 | 0.645 | 0.556 | 0.466 | 9.717 | 5.552 | 3.640 | 2.503 | 1.742 | 0.232 | 1.929 | 0.039 | 0.178 |

| F(2, 8) | 0.398 | 0.568 | 0.477 | 0.398 | 0.325 | 1.322 | 2.625 | 1.827 | 1.322 | 0.963 | 0.175 | 0.872 | 0.028 | 0.092 |

Table 2 represents the values for , for and , , and for several distributions. Since the quantile function for the exponential distribution is a multiple of where is the rate parameter, skewness does not depend on the rate and so we provide the results for a general . Consequently the skewness measures for the distribution (the exponential distribution with rate 1/2) are also equal to these values. Other examples include the Pareto Type II distribution (PAR) with varying shape parameter where skewness decreases with increasing shape and similarly with the Gamma distribution. Increases and decreases among the skewness measures agree within and among distributions.

5 Estimation and inference

In this section we discuss estimation of the AUCs and provide confidence intervals.

5.1 Estimation

To estimate the th quantile, , we use the Hyndman & Fan, (1996) quantile estimator, which we denote , and which is a linear combination of two adjacent order statistics. It is readily available as the Type 8 quantile estimator in the R software package. We let , , , be the estimates of the skewness measures , , and .

For an arbitrary , closed-form expressions are not available for the AUCs of the skewness measures. Recent research integrating ratios of functions of quantiles over (e.g. Prendergast & Staudte,, 2016, 2018), used summation approximations over a finite number of different s. Approximate standard errors and subsequent confidence intervals were also found for the measures considered resulting in good coverage. We therefore consider this approach.

Let for so that we estimate the AUC for as

| (8) |

In the context of their estimators, Prendergast & Staudte, (2016, 2018), showed that provides an excellent approximation to the integral, including for the standard errors that follow. We too therefore choose . We define , and similarly. If the mean skewness measure over the curve is desired, then the AUC estimate simply needs to be halved.

5.2 Asymptotic variances

In this section we provide estimates of the asymptotic variances for the , and the AUC estimators. Staudte, (2014) has already derived the asymptotic variance of using the Delta method (e.g. Ch.3 of DasGupta,, 2006). It is

| (9) |

where the estimators and and population values and defined as in Section 2.

We similarly derived the asymptotic variance of estimator for finding

| (10) |

We have also derived asymptotic co-variances needed in the variances for the AUC measures where

where setting gives the asymptotic variances for the estimators of and . The formulas for the co-variances in the above are given in Appendix A. Then the asymptotic variance of our AUC estimators are given as

| (11) |

We also let and denote the asymptotic variances for the AUC estimators of and . We do not show them here, since each can be obtained by, for example, multiplying by in the above asymptotic variance expressions.

5.3 Interval estimators for the AUCs and differences of AUCs

Let denote the estimate of , denote the estimate of and similarly the estimate of . To obtain these, we need estimates of , and . These need estimates of the quantile density functions and where is the density function. To estimate the quantile density functions, we use a kernel density estimator studied by, e.g. Falk, (1986) and Welsh, (1988) with bandwidth determined by the quantile optimality ratio (QOR) of Prendergast & Staudte, (2016a). The bandwidth based on the QOR typically resulted in slightly conservative intervals for quantiles and so are favored by us for our simulations. Code is available on request, or if desired standard bandwidths and density estimators for could be used although our preference is to estimate the quantile density directly rather than thake the inverse of an estimated .

Let denote the quantile of the standard normal distribution. All our 100()% confidence intervals for measures of skewness will be of the form, e.g. for ,

| (12) |

where . If an interval for mean skewness over the interval was desired (which is half the AUC), then all that is required is to halve the lower and upper bounds of the AUC interval.

When there are two independent groups, we can construct interval estimators to compare the differences in skewness. E.g, an interval estimator for is,

| (13) |

where and the s are the variances of the respective AUCs.

6 Simulations and Examples

We now consider simulations to assess coverage of the interval estimators before considering two examples.

6.1 Simulations

A simulation study was conducted to compare the performance of interval estimator of with our new measures , , and by considering coverage probability (cp) and the average confidence interval width (w) as the performance measures. We have selected normal, log normal, exponential, chi-square and Pareto distributions with different parameter choices and the sample sizes . We used 10,000 simulation trials to our simulation study since the standard error of the estimated coverage probability for the nominal 0.95 level is less than 0.005 for 10,000 simulation trials (Staudte,, 2014).

| n | Dist. | |||||

|---|---|---|---|---|---|---|

| 50 | N(2,1) | 0.964(1.35) | 0.964(1.43) | 0.962(1.54) | 0.961(1.69) | 0.950(1.92) |

| LN(0, 1) | 0.955(12.91) | 0.960(7.35) | 0.963(5.66) | 0.961(4.82) | 0.955(4.47) | |

| EXP(1) | 0.959(6.23) | 0.960(4.58) | 0.958(3.95) | 0.955(3.66) | 0.952(3.56) | |

| 0.960(6.21) | 0.950(4.57) | 0.955(3.99) | 0.952(3.66) | 0.953(3.60) | ||

| PAR(1, 7) | 0.959(9.29) | 0.960(5.91) | 0.961(4.79) | 0.957(4.25) | 0.954(4.06) | |

| 100 | N(2,1) | 0.966(0.94) | 0.967(0.96) | 0.964(1.02) | 0.965(1.12) | 0.962(1.25) |

| LN(0, 1) | 0.963(7.78) | 0.964(4.58) | 0.968(3.53) | 0.965(3.02) | 0.958(2.72) | |

| EXP(1) | 0.963(4.02) | 0.962(2.98) | 0.960(2.54) | 0.960(2.33) | 0.955(2.24) | |

| 0.959(3.98) | 0.960(2.95) | 0.960(2.54) | 0.959(2.34) | 0.953(2.24) | ||

| PAR(1, 7) | 0.960(5.73) | 0.962(3.72) | 0.962(3.06) | 0.961(2.69) | 0.954(2.49) | |

| 200 | N(2,1) | 0.971(0.65) | 0.969(0.66) | 0.967(0.70) | 0.968(0.77) | 0.965(0.85) |

| LN(0, 1) | 0.961(4.93) | 0.967(3.02) | 0.965(2.33) | 0.963(1.98) | 0.965(1.80) | |

| EXP(1) | 0.961(2.66) | 0.964(1.99) | 0.966(1.70) | 0.959(1.56) | 0.959(1.49) | |

| 0.964(2.67) | 0.958(1.98) | 0.965(1.70) | 0.950(1.56) | 0.961(1.50) | ||

| PAR(1, 7) | 0.967(3.74) | 0.963(2.49) | 0.962(2.02) | 0.961(1.78) | 0.961(1.65) | |

| 500 | N(2,1) | 0.972(0.41) | 0.968(0.41) | 0.972(0.43) | 0.965(0.46) | 0.958(0.50) |

| LN(0, 1) | 0.962(2.89) | 0.959(1.80) | 0.962(1.40) | 0.962(1.19) | 0.964(1.08) | |

| EXP(1) | 0.961(1.60) | 0.960(1.21) | 0.956(1.04) | 0.957(0.95) | 0.960(0.91) | |

| 0.959(1.61) | 0.958(1.20) | 0.957(1.04) | 0.959(0.95) | 0.955(0.90) | ||

| PAR(1, 7) | 0.962(2.21) | 0.957(1.50) | 0.960(1.22) | 0.957(1.08) | 0.959(1.00) | |

| 1000 | N(2,1) | 0.972(0.28) | 0.965(0.28) | 0.963(0.29) | 0.959(0.32) | 0.959(0.35) |

| LN(0, 1) | 0.961(1.98) | 0.960(1.24) | 0.961(0.96) | 0.962(0.82) | 0.959(0.75) | |

| EXP(1) | 0.956(1.11) | 0.957(0.84) | 0.957(0.72) | 0.956(0.66) | 0.956(0.63) | |

| 0.958(1.11) | 0.957(0.84) | 0.958(0.72) | 0.955(0.66) | 0.956(0.63) | ||

| PAR(1, 7) | 0.958(1.52) | 0.956(1.04) | 0.958(0.85) | 0.958(0.75) | 0.958(0.69) | |

| 5000 | N(2,1) | 0.960(0.12) | 0.956(0.12) | 0.953(0.13) | 0.953(0.14) | 0.954(0.15) |

| LN(0, 1) | 0.957(0.85) | 0.954(0.54) | 0.955(0.42) | 0.952(0.36) | 0.955(0.32) | |

| EXP(1) | 0.957(0.49) | 0.952(0.37) | 0.953(0.32) | 0.952(0.29) | 0.953(0.28) | |

| 0.957(0.48) | 0.955(0.37) | 0.954(0.32) | 0.950(0.29) | 0.953(0.28) | ||

| PAR(1, 7) | 0.954(0.66) | 0.957(0.45) | 0.954(0.37) | 0.955(0.33) | 0.952(0.30) | |

| 10000 | N(2,1) | 0.955(0.08) | 0.956(0.08) | 0.954(0.09) | 0.956(0.10) | 0.952(0.11) |

| LN(0, 1) | 0.956(0.59) | 0.951(0.38) | 0.957(0.29) | 0.952(0.25) | 0.953(0.23) | |

| EXP(1) | 0.953(0.34) | 0.954(0.26) | 0.954(0.22) | 0.952(0.20) | 0.955(0.19) | |

| 0.951(0.34) | 0.954(0.26) | 0.951(0.22) | 0.950(0.20) | 0.957(0.19) | ||

| PAR(1, 7) | 0.954(0.46) | 0.954(0.32) | 0.953(0.26) | 0.952(0.23) | 0.955(0.21) |

Before we consider interval estimators for the AUCs, we provide simulated coverage probabilities for an interval estimator of using an estimated asymptotic variance from (10). We considered and the results are provided in Table 3. The interval provides very good coverage compared to the nominal 0.95 and the interval width decreases with increasing sample sizes. Groeneveld et al. , (2009) recommended to use since it does not ignore the tail behaviour of the distribution. Very good coverage probabilities are achieved for this .

| n | Dist. | ||||

|---|---|---|---|---|---|

| 50 | N(2,1) | 0.997(1.84) | 0.993(6.57) | 1.000(0.68) | 0.996(2.53) |

| LN(0, 1) | 0.998(2.60) | 0.953(11.44) | 0.999(0.89) | 0.987(3.05) | |

| EXP(1) | 0.996(2.42) | 0.964(6.94) | 0.999(1.50) | 0.988(2.63) | |

| 0.997(1.65) | 0.966(6.55) | 0.999(1.80) | 0.989(2.17) | ||

| PAR(1, 7) | 0.996(6.23) | 0.954(7.86) | 0.998(0.80) | 0.988(2.67) | |

| 100 | N(2,1) | 0.992(0.93) | 0.988(3.63) | 0.995(0.58) | 0.992(2.64) |

| LN(0, 1) | 0.994(1.43) | 0.953(4.72) | 0.997(0.39) | 0.984(1.95) | |

| EXP(1) | 0.991(1.42) | 0.966(3.70) | 0.996(0.42) | 0.982(1.52) | |

| 0.992(0.96) | 0.969(3.60) | 0.995(0.37) | 0.981(2.14) | ||

| PAR(1, 7) | 0.993(0.91) | 0.962(4.00) | 0.997(1.17) | 0.982(2.01) | |

| 200 | N(2,1) | 0.987(0.73) | 0.985(6.05) | 0.990(0.32) | 0.988(1.26) |

| LN(0, 1) | 0.989(0.77) | 0.954(2.96) | 0.992(0.35) | 0.982(1.01) | |

| EXP(1) | 0.986(0.81) | 0.971(2.26) | 0.991(0.32) | 0.982(0.83) | |

| 0.989(0.65) | 0.971(2.87) | 0.992(0.28) | 0.983(1.36) | ||

| PAR(1, 7) | 0.988(0.93) | 0.964(3.34) | 0.991(0.33) | 0.982(0.85) | |

| 500 | N(2,1) | 0.969(0.25) | 0.975(0.90) | 0.977(0.09) | 0.976(0.32) |

| LN(0, 1) | 0.974(0.24) | 0.959(1.55) | 0.979(0.09) | 0.975(0.43) | |

| EXP(1) | 0.974(0.24) | 0.967(1.24) | 0.978(0.09) | 0.976(0.39) | |

| 0.969(0.25) | 0.964(1.29) | 0.979(0.09) | 0.973(0.40) | ||

| PAR(1, 7) | 0.972(0.24) | 0.959(1.30) | 0.978(0.09) | 0.974(0.43) | |

| 1000 | N(2,1) | 0.964(0.17) | 0.970(0.41) | 0.969(0.06) | 0.973(0.15) |

| LN(0, 1) | 0.966(0.16) | 0.962(0.95) | 0.972(0.06) | 0.969(0.22) | |

| EXP(1) | 0.965(0.17) | 0.960(0.69) | 0.967(0.06) | 0.972(0.19) | |

| 0.964(0.17) | 0.959(0.70) | 0.960(0.06) | 0.967(0.19) | ||

| PAR(1, 7) | 0.966(0.17) | 0.960(0.81) | 0.967(0.06) | 0.965(0.19) | |

| 5000 | N(2,1) | 0.957(0.07) | 0.957(0.15) | 0.958(0.02) | 0.956(0.05) |

| LN(0, 1) | 0.958(0.07) | 0.947(0.38) | 0.958(0.02) | 0.962(0.07) | |

| EXP(1) | 0.957(0.07) | 0.952(0.28) | 0.955(0.02) | 0.961(0.07) | |

| 0.956(0.07) | 0.953(0.27) | 0.959(0.02) | 0.959(0.07) | ||

| PAR(1, 7) | 0.957(0.07) | 0.950(0.33) | 0.958(0.02) | 0.957(0.07) | |

| 10000 | N(2,1) | 0.953(0.05) | 0.953(0.10) | 0.953(0.02) | 0.951(0.04) |

| LN(0, 1) | 0.951(0.05) | 0.938(0.27) | 0.957(0.02) | 0.955(0.05) | |

| EXP(1) | 0.955(0.05) | 0.955(0.20) | 0.955(0.02) | 0.953(0.05) | |

| 0.955(0.05) | 0.955(0.20) | 0.955(0.02) | 0.952(0.05) | ||

| PAR(1, 7) | 0.951(0.05) | 0.944(0.23) | 0.955(0.02) | 0.954(0.05) |

Simulated coverages based on 10,000 trials for interval estimators of , , and are provided in the Table 4. The interval estimators of , , and provide good coverage compared to the nominal 0.95 for moderate to large and the interval width decreases with increasing sample sizes. For smaller , the coverages are conservative. Overall, the coverages for the AUC of the skewness measure are usually closer to nominal and approach nominal more quickly with increasing sample size. We have seen this across a broad range of distributions and the reader can verify this by using our web application detailed next.

6.1.1 A Shiny web application for the performance comparisons of the intervals

For further comparisons, we have developed a Shiny (Chang et al. ,, 2017) web application that readers can use to run the simulations with different parameter choices. This can be found at https://lukeprendergast.shinyapps.io/meanskew/. The user can change the distribution, parameters, sample size, probability and the number of trials according to their choices. Once the desired options are selected the ‘Run Simulation’ button can be pressed and the relevant estimates, coverage probability (cp) and the average width of the confidence interval (w) will be calculated according to their input choices.

6.2 Examples

We have selected two datasets as examples.

6.2.1 Computer price data

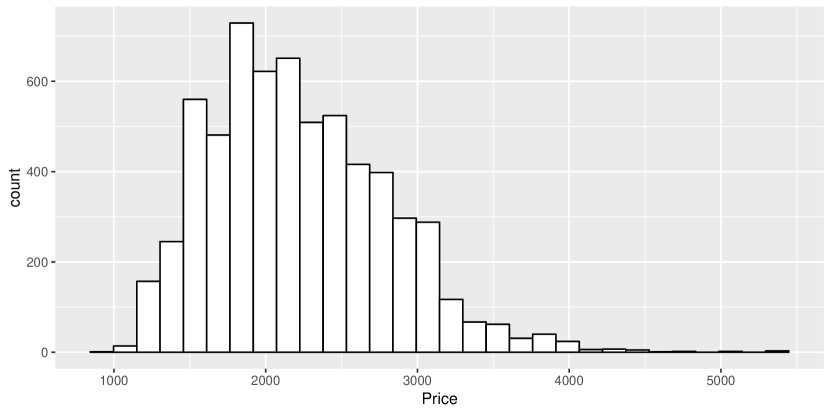

The “Computers” data set which is available in the “Ecdat” package (Croissant,, 2016) in R consists of prices for 6259 personnel computer which have been obtained from a cross section from 1993 to 1995 in the United States. Figure 4 depicts the computer price distribution which is clearly positively skewed.

| Measure | Estmate | CI | Measure | Estmate | CI |

|---|---|---|---|---|---|

| 0.1801 | (0.1531, 0.2072) | 0.4395 | (0.3589, 0.5200) | ||

| 0.1377 | (0.1128, 0.1626) | 0.3194 | ( 0.2523, 0.3865) | ||

| 0.1245 | (0.0967, 0.1524) | 0.2844 | (0.2117, 0.3571) | ||

| 0.1100 | (0.0783, 0.1417) | 0.2472 | (0.1671, 0.3273) | ||

| 0.1261 | (0.0906, 0.1616) | 0.2886 | (0.1957, 0.3814) | ||

| 0.1294 | (0.0726, 0.1861) | 0.2885 | (0.2052, 0.3718) | ||

| 0.0271 | (0.0025, 0.0516) | 0.0512 | (0.0257, 0.0768) |

6.2.2 Doctor visits data

The doctor visits data, used as an example in Heritier et al. , (2009), is a sub sample of 3066 individuals (987 males and 2079 females) of the AHEAD cohort born before 1924 for wave 6 (year 2002) from the Health and Retirement Study (HRS) (Heritier et al. ,, 2009). This study surveys more than 22,000 Americans over the age of 50 every 2 years. The response variable that we were are interested in is the number of doctor visits in the two gender groups. The doctor visits distributions of male and female are positively skewed, and the truncated histograms can be found in Staudte, (2014). There is one outlier in the female group (750 visits) and the ranges of visits, ignoring that outlier, for females is 0 to 365 and 0 to 300 for males. A complete analysis of descriptive statistics for the number of doctor visits in male and female can be found in Table 6 of Arachchige et al. , (2019).

| Male | Female | Male-Female (with outlier) | ||||

| Measure | Estimate | CI | Estimate | CI | Estimate | CI |

| 0.5172 | (0.4353, 0.5992) | 0.5758 | (0.5087, 0.6428) | -0.0585 | (-0.1644, 0.0474) | |

| 0.4545 | (0.4089, 0.5002) | 0.4545 | (0.4214, 0.4877) | 0.0000 | (-0.0564, 0.0564) | |

| 0.3333 | (0.2654, 0.4013) | 0.5238 | (0.4932 ,0.5544) | -0.1905 | (-0.2650, -0.1159) | |

| 0.2308 | (0.1202, 0.3413) | 0.5000 | (0.4542, 0.5458) | -0.2692 | (-0.3889, -0.1496) | |

| 0.2000 | (0.1035, 0.2968) | 0.2727 | (0.2044 ,0.3412) | -0.0727 | (-0.1910, 0.0455) | |

| 2.1429 | (1.4394, 2.8463) | 2.7143 | (1.9696, 3.4590) | -0.5714 | (-1.5959, 0.4530) | |

| 1.6667 | (1.3600, 1.9733) | 1.6667 | (1.4440, 1.8893) | 0.0000 | (-0.3790, 0.3710) | |

| 1.0000 | (0.6942, 1.3058) | 2.2000 | (1.9302 ,2.4699) | -1.2000 | (-1.6079, -0.7921) | |

| 0.6000 | (0.2264, 0.9736) | 2.0000 | (1.6333, 2.3667) | -1.4000 | (-1.9235, -0.8765) | |

| 0.5000 | (0.1985, 0.8015) | 0.7500 | ( 0.4915 ,1.0085) | -0.2500 | (-0.6471, 0.1471) | |

| 0.1741 | (0.1044, 0.2439) | 0.2610 | (0.2172, 0.3048) | -0.0869 | (-0.1692, -0.0045) | |

| 1.0676 | (0.6717, 1.4634) | 0.0296 | (0.0169, 0.0424) | -0.0265 | (-0.0512, -0.0018) | |

| 0.0031 | (-0.0180, 0.0243) | 0.0296 | (1.0733, 1.6754) | -0.3068 | (-0.8041, 0.1905) | |

| 0.0554 | (0.0120, 0.0987) | 0.1139 | (0.0786, 0.1493) | -0.0586 | (-0.1145, -0.0026) | |

Table 6 provides 95 confidence intervals for , , , , and for number of doctor visits for males, females and between males and females (with outlier). The intervals for each measure for males and females indicate skew. However, different conclusions about differences in skew between males and females can be made based on the different skewness measures. The intervals for and are sensitive to the choice of . However, the intervals for the AUC measures do indicate skew with the exception of the AUC for .

7 Summary and future work

We have introduced more powerful alternatives to the existing measures of skewness such as and which require a choice of . Here we introduce the integrated versions of the , , and as alternatives to measure the skewness. The simulation results show that the interval estimators perform well for all the selected distributions with moderate to large sample sizes and are typically conservative for smaller sample sizes.

While we refer to the AUCs as mean skew (i.e. mean of the skew curve over a uniform ), in truth the AUC itself is twice the mean. It is simple then to obtain point and interval estimates for the mean from the AUC estimates and vice versa. We favored AUC since it was more typically in the domain of skew values of and when is fixed to some value between 0 and 0.25 (which would typically be done in practice). The mean skew is typically less than the skewness at fixed since it is half the AUC and the AUC is taken over all . An alternative would also be to consider integrating over and dividing by 4. This would result in a mean more like the skew values for fixed in 0 to 0.25. We favored the AUC though since it considers the entire distribution, and not just a subset of it.

The influence function (IF Hampel,, 1974) can be used to study the robustness properties and sensitivity of estimators. Groeneveld et al. , (2009); Groeneveld, (1991) computed the IFs for the quantiles based measures and in doing so established typically greater sensitivity to right skew of compared to . A study of the IFs for the AUC measures may also reveal some advantage in weighting with respect to whereby the less weighting is applied to the extreme quantiles where estimation can be difficult. For examples of the IF, including the IF for quantiles as background, see e.g. Staudte & Sheather, (1990) and Clarke, (2018).

Appendix A Asymptotic variances and covariances

References

- Arachchige et al. , (2019) Arachchige, CNPG, Prendergast, LA, & Staudte, RG. 2019. Robust analogues to the coefficient of variation. arXiv preprint arXiv:1907.01110.

- Bowley, (1920) Bowley, AL. 1920. Elements of statistics. Vol. 2. PS King.

- Chang et al. , (2017) Chang, W, Cheng, J, Allaire, JJ, Xie, Y, & McPherson, J. 2017. shiny: Web application framework for r. R package version 1.0.5.

- Clarke, (2018) Clarke, BR. 2018. Robustness theory and application. John Wiley & Sons.

- Croissant, (2016) Croissant, Y. 2016. Ecdat: data sets for econometrics. r package version 0.3-1.

- DasGupta, (2006) DasGupta, A. 2006. Asymptotic Theory of Statistics and Probability. New York, NY: Springer.

- David & Johnson, (1956) David, FN, & Johnson, NL. 1956. Some tests of significance with ordered variables. Journal of the Royal Statistical Society. Series B (Methodological), 18(1), 1–31.

- David, (1981) David, HA. 1981. Order Statistics. New York: John Wiley & Sons.

- Development Core Team, (2008) Development Core Team, R. 2008. R: A language and environment for statistical computing. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0.

- Falk, (1986) Falk, M. 1986. On the estimation of the quantile density function. Statistics & Probability Letters, 4(2), 69–73.

- Groeneveld, (1991) Groeneveld, RA. 1991. An influence function approach to describing the skewness of a distribution. The American Statistician, 45(2), 97–102.

- Groeneveld & Meeden, (1984) Groeneveld, RA, & Meeden, G. 1984. Measuring skewness and kurtosis. The Statistician, 391–399.

- Groeneveld et al. , (2009) Groeneveld, RA, Meeden, G, et al. . 2009. An improved skewness measure. Metron, 67(3), 325.

- Hampel, (1974) Hampel, FR. 1974. The influence curve and its role in robust estimation. Journal of the American Statistical Association, 69, 383–393.

- Heritier et al. , (2009) Heritier, S, Cantoni, E, Copt, S, & Victoria-Feser, Maria-Pia. 2009. Robust methods in biostatistics. Vol. 825. John Wiley & Sons.

- Hinkley, (1975) Hinkley, DV. 1975. On power transformations to symmetry. Biometrika, 62(1), 101–111.

- Hyndman & Fan, (1996) Hyndman, RJ, & Fan, Y. 1996. Sample quantiles in statistical packages. The American Statistician, 50, 361–365.

- Oja, (1981) Oja, H. 1981. On location, scale, skewness and kurtosis of univariate distributions. Scandinavian Journal of Statistics, 154–168.

- Parzen, (1979) Parzen, E. 1979. Nonparametric statistical data modeling. Journal of the American Statistical Association, 74, 105–121.

- Prendergast & Staudte, (2016) Prendergast, LA, & Staudte, RG. 2016. Quantile versions of the lorenz curve. Electronic Journal of Statistics, 10(2), 1896–1926.

- Prendergast & Staudte, (2016a) Prendergast, LA, & Staudte, RG. 2016a. Exploiting the Quantile Optimality Ratio in finding Confidence Intervals for Quantiles. Stat, 5, 70–81.

- Prendergast & Staudte, (2018) Prendergast, LA, & Staudte, RG. 2018. A simple and effective inequality measure. The American Statistician, 1–16.

- Staudte, (2014) Staudte, RG. 2014. Inference for quantile measures of skewness. Test, 23(4), 751–768.

- Staudte & Sheather, (1990) Staudte, RG, & Sheather, SJ. 1990. Robust Estimation and Testing. New York: Wiley.

- Tukey, (1965) Tukey, JW. 1965. Which part of the sample contains the information? Proceedings of the National Academy of Sciences, 53, 127–134.

- Welsh, (1988) Welsh, AH. 1988. Asymptotically efficient estimation of the sparsity function at a point. Statistics & Probability Letters, 6(6), 427–432.

- Yule, (1912) Yule, GU. 1912. An introduction to the theory of statistics. London: Griffin.