2mm \textblockrulecolourNavy

Solution of option pricing equations using orthogonal polynomial expansion

Abstract

In this paper we study both analytic and numerical solutions of option pricing equations using systems of orthogonal polynomials. Using a Galerkin-based method, we solve the parabolic partial differential equation for the Black-Scholes model using Hermite polynomials and for the Heston model using Hermite and Laguerre polynomials. We compare obtained solutions to existing semi-closed pricing formulas. Special attention is paid to the solution of Heston model at the boundary with vanishing volatility.

Received 13 December 2019

Revised 27 February 2020, 23 June 2020

Keywords: orthogonal polynomial expansion; Hermite polynomials; Laguerre polynomials; Heston model; option pricing

MSC classification: 33C45; 65M60; 91G20; 91G60

JEL classification: C58; G12; C63

1 Introduction

One of the fundamental tasks in financial mathematics is the pricing of derivatives, in particular option pricing. An option is a contract between two parties which gives the holder the right (but not the obligation) to buy or sell the underlying asset under certain conditions on or before a specified future date. The price that is paid for the underlying when the option is exercised is called strike price and the last day on which the option may be exercised is called expiration date or maturity date. Whether the holder has the right to buy or sell the underlying asset depends on the type of option to which the contract is signed. There is either a call option which allows the holder to buy the asset at a stated price within a specific time-frame or a put option which allows the holder to sell the asset. In this article we will restrict ourselves to European options that can be exercised only on the expiration date.

In their Nobel-prize winning paper, Black and Scholes (1973) proposed a model for evaluating the fair value of the European call option that gives the right to buy a single share of common stock and derived a semi-closed formula for the option price, the so-called Black-Scholes formula. For the model they have assumed a frictionless market with ideal conditions like the absence of arbitrage and the possibility to borrow and lend any amount of money and to buy and sell any amount of stock, respectively. Volatility in the Black-Scholes (BS) model is assumed to be constant which has later become its most discussed feature. Constant volatility matches poorly with the observed implied volatility surface for real market data. Especially for out of the money options the market prices are significantly higher than what the model suggests. This phenomenon is widely known as the volatility smile. For a better fit to the data, Hull and White (1987) proposed to model volatility as another stochastic process. There are various stochastic volatility models from Hull and White (1987), Stein and Stein (1991), Heston (1993), and many others. Later on, additional jump components were included into the models, e.g. Bates (1996).

Up to this day, the Heston model is quite popular among economists and practitioners. Heston (1993) modelled the volatility using the mean-reverting Cox, Ingersoll, and Ross (1985) process (CIR), which allowed arbitrary correlation between volatility and spot asset returns. Heston also derived a semi-closed formula close to the BS formula. Both in BS and Heston model, one can derive the pricing partial differential equation (PDE) in several different ways, for example (Wilmott, 1998; Rouah, 2013; Hull, 2018) using arbitrage arguments with self-financing trading strategies, approaches with martingale measures or the Fokker-Planck equation for the transition probability density function. Although semi-closed formulas have been widely used in practice for a long time, only recently Daněk and Pospíšil (2020) showed that for certain values of model parameters these formulas can bring serious numerical difficulties especially in evaluation of the integrands in these formulas and their implementation therefore sometimes requires a demanding high precision arithmetic to be adopted.

Many different numerical methods can be used to solve option pricing problems such as Monte Carlo methods (including the Quasi Monte Carlo), Fourier based methods (including the Fast Fourier Transform method, Fourier method with Gauss-Laguerre quadrature, cosine series method), finite differences methods (with different time-stepping schemes, different grid refinements including the adaptive refinement or discontinuous Galerkin method), finite element methods (including the method with NURBS basis functions introduced by Pospíšil and Švígler (2019)) or for example radial basis function methods (RBF). We refer the reader to the references in the BENCHOP project report written by von Sydow et al. (2015), who implemented fifteen different numerical methods with the help of different advanced specialized techniques, and who compared all methods for different benchmark problems and consequently discussed advantages and disadvantages of each method.

The aim of this paper is to solve the pricing PDEs for both BS and Heston model using orthogonal polynomial expansions that are motivated by the Galerkin method. The expansion approach offers several advantages as we approximate the solution by smooth functions. Therefore, it gives more insight into how parameters influence prices and to what extent and hence give a better understanding of the solution than the semi-closed form or other approximation method especially for the Heston model. For the sake of clarity of the method we omit application of specialized techniques that could further improve the proposed method. Among the other mentioned methods, only FEM with smooth basis functions and RBF approximate the solution by smooth functions. One advantage of the orthogonal polynomial expansion is hence the independence of the space variable discretization (finite elements) or spacial node locations (RBF).

Aubin (1967) studied Galerkin type methods and their convergence for elliptic partial differential equations and Birkhoff, Schultz, and Varga (1968) used piecewise Hermite polynomials for this problem. Time-dependent equations were investigated with the usage of the Galerkin method by Swartz and Wendroff (1969). The initial value problem for a general parabolic equation of second order was first studied by Douglas and Dupont (1970). They used Galerkin type methods, both continuous and discrete in time, and established a priori estimates to control the error. These articles initiated several other papers by Dupont (1972), Fix and Nassif (1972), Wheeler (1973), Bramble and Thomée (1974), Bramble, Schatz, Thomée, and Wahlbin (1977), and Thomée (1977). Most of the a priori estimates are formulated with regard to the norm but Bramble, Schatz, Thomée, and Wahlbin (1977) offers estimates for the maximum norm, as well. Nonlinear parabolic equations were covered by Wheeler (1973). A survey of results can be found in Thomée (1978) and in the monograph Thomée (2006).

The application of orthogonal polynomial expansions in option pricing was to our knowledge for the first time suggested by Jarrow and Rudd (1982) who pioneered the use of Edgeworth expansions for valuation of derivative securities. Later Corrado and Su (1996) introduced the Gram-Charlier expansions. In the recent past, Hermite polynomial expansion approaches have been used in some interesting articles regarding different aspects of the option pricing problem.

Xiu (2014) studied a closed-form series expansion of European call option prices in the time variable and this series expansion was derived using the Hermite polynomials. Xiu introduced two approaches on vanilla option and binary option. The first one has been a bottom-up Hermite polynomial approach and the second one has been a top-down lucky guess approach. As the benchmark model he has chosen BS model but stated that square-root (SQR) models for the volatility like Heston (1993), quadratic volatility (QV) models, constant elasticity of variance (CEV) models, which introduces one additional parameter the elasticity of variance, or several jump-diffusion models can be considered, see for example a recent monograph by Lewis (2016).

Heston and Rossi (2017) showed that Edgeworth expansions for option valuation are equivalent to approximating the option payoff using Hermite polynomials and logistic polynomials. Consequently, the value of an option is equal to the value of an infinite series of replicating polynomials. Heston and Rossi provide efficient alternative moment-based formulas to express option values in terms of skewness, kurtosis and higher moments.

Polynomial expansions with Hermite and Laguerre polynomials play also a substantial role in Alziary and Takáč (2018). The authors rigorously formulate the Cauchy problem connected to the Heston model as a parabolic PDE with a special focus on the boundary conditions which are often neglected in the literature. \NoHyperAlziary and Takáč\endNoHyper provide the real analyticity of the solution which is directly connected to the problem of market completeness studied in Davis and Obłój (2008). The polynomial expansions are used in the proof of the main results of the article. Further investigations of the boundary conditions can be found in the forthcoming work Alziary and Takáč (2020).

Very recently, option pricing with orthogonal polynomial expansions has been studied by Ackerer and Filipović (2020), who derived option prices series representation by expansion of the characteristic functions rather than by solving the pricing PDE.

The structure of the paper is the following. In Section 2 we introduce system of orthogonal polynomials, studied models as well as other necessary terms and fundamental properties. In Section 3 we solve the Black-Scholes and Heston PDE using the orthogonal polynomial expansion. To solve the BS PDE we use Hermite polynomials and to solve the Heston PDE we use a combination of Hermite and Laguerre polynomials. In Section 4 we present all numerical results, especially comparison to the existing semi-closed form solutions. We conclude in Section 5.

2 Preliminaries and notation

2.1 Orthogonal polynomials

Standard theory for parabolic PDEs requires initial data in a Lebesgue space. In the PDE pricing approach for European-type derivatives the initial value corresponds to the payoff function of the contract but unfortunately the payoff of many European options, e.g., the European call option, is unbounded and not Lebesgue-integrable. For this reason we consider weighted Lesbesgue spaces with a positive weight function as studied in Kufner (1980), Kufner and Sändig (1987), Funaro (1992).

The weighted Lebesgue space is the space of all measurable functions for which

As usual, we consider representatives of classes of functions which are equal almost everywhere. We can also define weighted Sobolev spaces for . Again, we refer the reader to Kufner (1980), Kufner and Sändig (1987), and Funaro (1992), for details about such spaces.

We consider sequences of real polynomials in which are pairwise orthogonal with respect to the inner product defined by

| (1) |

It can be shown that for given and that are not both identically zero, there exist functions and such that the system of orthogonal polynomials satisfies the so called three-term recurrence relation

| (2) |

The relation (2) is arguably the single most important piece of information for the constructive and computational use of orthogonal polynomials. For more details about general systems of orthogonal polynomials and on the proof of the recurrence relation we refer the reader to the book by Gautschi (2004).

Throughout the paper we will work especially with Hermite and Laguerre polynomials. Their properties are rather extensively mentioned in many monographs, we refer the readers for example to the books by (Abramowitz and Stegun, 1964, chap. 22), (Lebedev, 1965, chap. 4), (Szegö, 1975, chap. 5), Thangavelu (1993) and (Olver, Lozier, Boisvert, and Clark, 2010, chap. 18) to name a few. The definition and basic properties of Hermite and Laguerre polynomials can be found in all of these monographs.

2.1.1 Hermite polynomials

Hermite polynomials are orthogonal polynomials on the real line. There exists two types of Hermite polynomials that differ slightly in the choice of weight function and that are called probabilists’ (weight function ) and physicists’ (weight function ) Hermite polynomials. Those two types can be easily converted into each other and we will consider physicists’ polynomials only.

Definition 2.1.

The system of Hermite polynomials is defined by the Rodrigues formula

The three-term recurrence (2) for Hermite polynomials reads

| (3) |

The Hermite polynomials form a complete orthogonal system in the weighted Lebesgue space with , where is the Kronecker delta, as well as an orthogonal set in the weighted Sobolev space for . See (Lebedev, 1965, Sec. 4.14) for the orthogonality and (Szegö, 1975, Sec. 5.7) for the completeness of the system, respectively.

In the following lemma we state several useful simplifications of integral terms that are consequences of Definition 2.1 and the three-term recurrence (3).

Lemma 2.2.

For all ,

| (4) | ||||

| (5) | ||||

| (6) | ||||

| (7) |

A proof can be found in the thesis (Filipová, 2019, chap. 2, Lemmas 2.5–2.9).

2.1.2 Laguerre polynomials

The volatility process in the Heston model is strictly positive provided that the Feller condition is satisfied. Hence, we need a system of orthogonal polynomials on the positive part of the real line for the expansion in the volatility variable. With the weight function , , on such a system is given by the Laguerre polynomials.

Definition 2.3.

The system of Laguerre polynomials is defined by

The three-term recurrence (2) for the Laguerre polynomials is

| (8) |

The Laguerre polynomials form a complete orthonormal system in the weighted Lebesgue space . The orthonormality of the system is studied in (Lebedev, 1965, Sec. 4.21) and the completeness in (Szegö, 1975, Sec. 5.7).

Lemma 2.4.

For all ,

| (9) | ||||

| (10) | ||||

| (11) | ||||

| (12) |

2.1.3 Finite–dimensional projections

In the following, we study orthogonal projections of functions in weighted Lebesgue spaces into finite–dimensional subspaces spanned by Hermite and Laguerre polynomials. See Funaro (1992) for details of the projection operators.

At first, we consider the weight function on the real line and denote by the vector space spanned by the first Hermite polynomials. The orthogonal projector with

| (13) |

satisfies

for every . Moreover, for each there exists a constant such that

| (14) |

and for every , see (Funaro, 1992, Theorem 6.2.6). We will later use the orthogonal projector defined in (13) to study the Black-Scholes model.

Next, we consider the weight function on and denote by the vector space spanned by the first Laguerre polynomials. The orthogonal projector with

satisfies the same approximation properties as and for each we have

| (15) |

for every with , , and a constant , see (Funaro, 1992, Theorem 6.2.5).

To treat models with non-constant volatility, we use a weighted Lebesgue space in two variables. A weighted Lebesgue space with the weight function is the space of all measurable functions for which

The inner product is defined in accordance with (1). For the Heston model, we will consider the weighted Lebesgue space with the weight . Due to (Reed and Simon, 1980, Sec. II.4), the products of Hermite and Laguerre polynomials for with for form a complete orthogonal set in . Let denote the vector space spanned by the products of the first Hermite polynomials and the first Laguerre polynomials. The orthogonal projector defined by

| (16) |

inherits the approximation properties from the projection operators and .

For practical reasons, we have to evaluate the finite-dimensional projections (13) and (16) numerically, where the Clenshaw’s algorithm (Press, Teukolsky, Vetterling, and Flannery, 2007, Sec. 5.4) will be of use. To evaluate the Fourier coefficients

| (17) |

in (13) and (16) precisely, it is necessary to choose the appropriate quadrature. Here we consider the Gauss–Hermite and Gauss–Laguerre quadratures, see for example in the books (Abramowitz and Stegun, 1964, Sec. 25.4), (Szegö, 1975, Sec. 14.5 – 14.7), (Olver, Lozier, Boisvert, and Clark, 2010, Sec. 3.5) or (Press, Teukolsky, Vetterling, and Flannery, 2007, Sec. 4.6).

2.2 Option pricing models

Since options are frequently traded contracts, the derivation of the option prices is an important task in mathematical finance. There exist several models for option pricing in an arbitrage-free setting. The prices that can be provided by these models give us an idea how the real market prices should behave. We will consider option pricing in the classical models by Black and Scholes (1973) with constant volatility and by Heston (1993) with a mean–reverting stochastic volatility process.

In this article, we restrict ourselves to the pricing of European call options, since the price of the corresponding European put options can be obtained by the put–call parity. A European option contract is characterized by two parameters, maturity and strike price . We introduce also a variable that is sometimes called moneyness and that measures a relative position of the price of an underlying asset (typically a stock) with respect to the strike price, i.e. . If , we say that the option is at-the-money (ATM), for the call option is in-the-money (ITM) and for it is out-of-the-money (OTM). For put options it is clearly the reverse.

In both models the money market is represented by a risk-free bond

with constant interest rate .

2.2.1 Black-Scholes model

Let be a complete probability space with a fixed filtration generated by a standard Wiener process . In BS model the stock price process is modelled as a continuous semimartingale with respect to and satisfies the stochastic differential equation

| (18) |

where drift and volatility are constant. The fair price of a European call option with maturity and strike price is defined by the risk-free pricing formula

| (19) |

where the conditional expectation is considered under the unique equivalent martingale measure provided that is continuous. The equivalent measure can be obtained from (18) by replacing by and keep . It can be shown that also satisfies the Black-Scholes partial differential equation

for with the terminal condition . There exit several approaches to obtain the PDE like replication of the derivative with a self-financing portfolio or delta hedging. For more details on replication strategies we refer to (Karatzas and Shreve, 1991, Chapter 5.8.B). We introduce new variables and , for the time till maturity and the logarithm of the stock price, respectively. For the function we obtain the parabolic Cauchy problem

| (BS) |

with the Black-Scholes operator

Black and Scholes (1973) formula for the fair price of a European call option reads

| (20) | ||||

| where | ||||

and denotes the cumulative distribution function of the standard normal distribution.

2.2.2 Heston model

Let be a complete probability space with a filtration and let and be two standard Wiener processes with respect to the filtration that are correlated by a factor . In contrast to BS model, in the Heston model the volatility is modelled as the square-root of a mean-reverting stochastic process . Both, the stock price process and are continuous semimartingales with respect to . The model dynamics are

| (21) | ||||

The drift and parameter (also called volatility of volatility) are constant. The mean-reverting stochastic variance process , also referred to as the Cox, Ingersoll, and Ross (1985) process, with constant rate of mean reversion and long-run mean level , both positive, is strictly positive provided that the so called Feller’s condition holds. Again, if the function of the option price is continuous then it is given by the pricing formula (19) for an equivalent martingale measure that we get from (21) by replacing , , by , , , respectively, and keep and . The parameter is referred to as the price of volatility risk. The price also satisfies a partial differential equation

for with the terminal condition which can be proved for instance with the help of a replicating self-financing portfolio, e.q., one could easily modify the proof in (Fouque, Papanicolaou, and Sircar, 2000, Section 2.4), where an Ohrnstein-Uhlenbeck process is used instead of the CIR process. Without loss of generality we set by using standard transformation techniques (Heston, 1993, Sec. 3).

As above, we introduce the new variables and . For the function we obtain the initial value problem

| (H) |

with the partial differential operator

In the book by Lewis (2000), the author presents the so called fundamental transform approach for solution of the initial value problem (H). We present here only the pricing formula that has among others one numerical advantage in the sense that we have to calculate only one numerical integral for each price of the option (compared to the two-integrals formula by Heston). The price of the European call option can be expressed as the so called Heston-Lewis formula

| (22) |

where and

where

3 Methodology

In this section we present our main results, in particular we introduce our Galerkin-based method. First, we establish the weak formulation of the Black-Scholes equation in a weighted Lebesgue space and show how we can solve the equation in finite-dimensional subspaces spanned by Hermite polynomials. The smooth solutions in the finite-dimensional subspaces approximate the weak solution of the Black-Scholes equation. Although the Black-Scholes model has already been studied in detail, Section 3.1 gives us a good understanding how the method should work for the more complicated Heston model. Second, we establish the method for the Heston model and study the equation for vanishing volatility.

As we have pointed out in the introduction, the Galerkin method for parabolic equations and their convergence properties were widely studied in the past. Even so, our applications are special in the sense that we have an unbounded domain and unbounded initial data. Most numerical schemes for unbounded domains just cut the domain at a certain point. Contrary to this, we use an orthogonal base on the whole unbounded domain. To treat the unbounded initial condition we consider weighted Lebesgue spaces.

3.1 Solution of the Black-Scholes PDE

Let us now consider the parabolic Cauchy problem for the function introduced in Section 2.2.1

| (23) |

with the Black-Scholes operator

The initial data is obviously not in but in the weighted Lebesgue space with the weight function and even in the weighted Sobolev space . We want to obtain a weak formulation of the problem in the weighted space. Therefore, we multiply the partial differential equation (23) with a test function and the weight function . If we integrate over then integration by parts yields

Following the standard procedure described for example in (Evans, 2010, p. 296), we define the bilinear form

| (24) |

for . We call

a weak solution of (23) if

| (25) |

for each test function and a.e. time , and . Here, is the dual space of the Sobolev space and can be canonically identified with it by the Riesz representation theorem. The existence of the unique weak solution in the weighted space can be obtained by modifying the proof of the Galerkin method in (Evans, 2010, Chapter 7.1, p. 349).

Following the Galerkin method, we want to approximate the weak solution with solutions of the Cauchy problem (23) in the finite–dimensional subspace , i.e., we look for a solution in the form

| (26) |

with a given initial condition

| (27) |

where is a column vector of Fourier coefficients , where T denotes the transposition (not to be confused with time ).

The natural choice for the initial condition is the orthogonal projection of the payoff function defined in (13). For instance, the coefficients in the initial condition (27) satisfy

| (28) |

or in vector form .

Let us now substitute into the bilinear form (24). In the view of Lemma 2.2 we can simplify the term and obtain the explicit form

| (29) |

We plug (26) into (25) and choose the Hermite polynomial as the test function

We make use of the orthogonality of the Hermite polynomials to obtain a system of ODEs

| (30) |

that possesses a unique solution to the initial data (28) by standard existence theory.

Let us introduce a matrix , , with elements

| (31) |

and denote by the transposed matrix111In the implementation, one can easily swap the arguments of the bilinear form in (31) in order to get an already transposed matrix. However, in the text we prefer the natural ordering and hence the transposition in the formulas below is needed.. From (29) we can easily see that is a three-diagonal matrix with entries on the main diagonal and two superdiagonals. With the matrix we can rewrite (30) in the matrix form as

| (32) |

We can write the solution in terms of the matrix exponential as

| (33) |

3.2 Solution of the Heston PDE

Let us now consider the Heston (1993) model with stochastic volatility. As above, we can use the Hermite polynomials for the polynomial expansion in the variable connected to the logarithm of the stock price. However, for the volatility variable we prefer Laguerre polynomials due to the fact that the volatility is strictly positive. The Cauchy problem connected to the model of Heston (1993) is

| (34) |

with the Heston operator

To obtain a weak formulation of the solution we multiply (34) with a test function and the weight function . Integration over the domain and application of Gauss’s theorem then yields the variational formulation of the problem

with the bilinear form defined by

| (35) | ||||

for all .

Similarly as for the BS model, we substitute the elements of the complete orthogonal set and into the bilinear form (35). For the purpose of better clarity, we study all seven integral terms separately. In particular, let

| (36) |

where each , = 1, 2, …, 7, represents individual integral terms.

Theorem 3.1.

Proof.

For the calculation of we apply (4) and (9). For we use (5) and (10). is derived with the help of a modification of (5)

| (37) |

and (10). For we need (11). In the calculation of we make use of (6), (9), and (37). For we need the same equations as for and (12). is trivial. More detailed calculations can be found in the thesis (Filipová, 2019, Sec. 3.2). ∎

In analogy to the BS case, we say that with is a weak solution of (34) if

| (38) |

for each test function and a.e. time , and for all . The existence and uniqueness of the weak solution is given by the Galerkin Method in (Evans, 2010, Chapter 7.1, p. 349). A detailed proof of the existence of the unique solution in a convenient weighted space considering the boundary conditions can be found in Alziary and Takáč (2018).

We study solutions of the Cauchy problem (34) in finite–dimensional subspaces , i.e. we look for the solution in the form

| (39) |

where

and , ; ; are (yet unknown) Fourier coefficients.

Let , , be a column vector of these coefficients, where , ; ; i.e.

For the initial data we choose the orthogonal projection of the payoff function , where for ,

| (40) |

or in vector form .

We use (38) with of the form (39) and the test function . Thanks to the orthogonality of the polynomials we obtain

Let us introduce a matrix , defined as

| (41) |

where . Using this assembly222Swapping the arguments in the bilinear form in (41) can again easily produce an already transposed matrix. it can be shown (by using Theorem 3.1) that the transposed matrix is an upper triangular matrix with elements on the main diagonal and superdiagonals if and 2 superdiagonals in the degenerate case like in the BS case. It is worth to mention that the BS PDE is not a special case of the Heston PDE. The superdiagonal is a contribution of the term , whose elements lie on seven superdiagonals ().

As above, we obtain a system of ODEs

| (42) |

The solution can also be written in terms of the matrix exponential as

| (43) |

3.2.1 Solution behaviour analysis near

We are interested in the behaviour of the solution of the Heston PDE for small volatility, especially at the boundary . Motivated by Alziary and Takáč (2020), we study the partial differential equation for .

The solution satisfies the Heston PDE

in and can be rewritten as

For the equation degenerates to the first order equation as shown in (Alziary and Takáč, 2020, cor. 4.3)

Since we want to study the problem for vanishing volatility, we replace the derivative with respect to by the differential quotient , where denotes a small distance to the boundary. By doing this, we obtain an initial value problem on the boundary

| (44) |

with the unknown function for fixed volatility and with the differential operator

We can derive a solution of the Cauchy problem in dependence of the inhomogeneity which consists of values of the solution of the Heston equation away from the boundary.

We introduce a new variable and the function that satisfies the inhomogeneous transport equation

with the initial condition . Following the standard procedure, we define the function

and obtain

| (45) |

We integrate (45) with respect to the time variable

Hence, we get the boundary solution that we denote as

and in particular

| (46) |

These formulas contain an integral over the finite interval . For the values of for we could make use of the polynomial expansion of the solution obtained in Section 3.2.

4 Results

In this section we present numerical results for several particular examples. All supporting codes are implemented in MATLAB. Parameter values in considered examples are chosen consistently with other cited resources in order to demonstrate the functionality of the proposed method. To provide a thorough analysis of the numerical solution for all possible parameter values combinations goes beyond the scope of present paper. When we refer to the error it is the error with respect to the norm of the weighted Lebesgue spaces and , respectively. For convenience, point-wise error is calculated for several selected nodes as well as the average absolute and relative error. We compare the newly proposed solution to existing closed formula (20) for BS model and semi-closed formula (22) for Heston model, respectively.

4.1 Black-Scholes model

In the following setting for BS model the parameters are chosen as follows:

-

•

volatility ,

-

•

risk free interest rate ,

and options parameters are the following:

-

•

maturity ,

-

•

strike price ,

-

•

stock price discretized with the equidistant step ,

and we impose (with being the smallest discretization point in variable). In the case of BS model, we choose Hermite polynomials as the complete orthogonal system of polynomials and focus on solving the Black-Scholes PDE. Our numerical solution of the BS PDE (23) is considered in the form (26). Fourier coefficients for are obtained by solving the system of ODEs (32) with given by (29) and (31). We use MATLAB ODE solver ode45 to solve this system since it leads to smaller values of errors then the numerical calculation of matrix exponential in (33) using MATLAB procedure expm. See (Filipová, 2019, Sec. 4.1) for a comparison of these two methods.

The BS formula and solutions obtained by ode45 for and are shown in Figure 1 on the left. For convenience the solution is plotted only for . The three vertical dashed lines represent moneyness respectively. On the right we can see the behaviour of the absolute error in this region.

| 20 | 0.22055 | 185.605 | 0.152195 | 0.027266 | 8.00953 | 0.243 |

|---|---|---|---|---|---|---|

| 40 | 0.0991825 | 83.4675 | 0.287501 | 0.0515061 | 1.38974 | 0.0421632 |

| 60 | 0.0875455 | 73.6744 | 0.249526 | 0.0447028 | 0.196272 | 0.00595466 |

| 80 | 0.0476676 | 40.1149 | 0.225168 | 0.0403392 | 0.542587 | 0.0164615 |

| 100 | 0.0209973 | 17.6704 | 0.229207 | 0.0410627 | 0.456833 | 0.0138598 |

| 120 | 0.00662291 | 5.57354 | 0.230279 | 0.0412547 | 0.312095 | 0.00946862 |

| error | |||||

|---|---|---|---|---|---|

| 20 | 3.11957e-09 | 2.81507 | 11.9282 | 5.29885 | 0.190209 |

| 40 | 5.23407e-10 | 1.00759 | 3.23288 | 1.57162 | 0.0630167 |

| 60 | 1.65443e-10 | 0.451035 | 3.10148 | 1.01331 | 0.0370747 |

| 80 | 7.21744e-11 | 0.274018 | 1.91442 | 0.575191 | 0.0220953 |

| 100 | 4.05356e-11 | 0.196393 | 1.02488 | 0.277925 | 0.0127912 |

| 120 | 2.93889e-11 | 0.152986 | 0.473851 | 0.17448 | 0.00880548 |

We measure the following errors. First and foremost we compute the error using the Gauss-Hermite quadrature with 251 Hermite points. In the second column of Table 2 we list the corresponding error for different polynomial orders. Convergence of the error is visually depicted in Figure 2 on the left. The set of nodes used on the right of Figure 2 and in Table 2 will be introduced below.

Next we measure the point-wise absolute and relative errors at selected nodes and their average. In particular, by we denote the absolute error with respect to the Black-Scholes formula (20) at the point ,

where is the moneyness introduced in Section 2.2. Similarly we measure the relative error

In Table 1, we list the values of both absolute and relative error at three different moneyness nodes () for different polynomial orders. The relative error for is high, because the option price is close to zero. For small values of , when the approximation is not optimal, the errors do not have to be strictly decreasing in , which is expected.

4.2 Heston model

We consider the following setting of Heston model. The parameters are chosen as in many examples in the book by Rouah (2013)

-

•

initial variance ,

-

•

variance discretized with the equidistant step ,

-

•

mean reversion rate ,

-

•

long-run variance ,

-

•

volatility of volatility ,

-

•

correlation ,

-

•

the price of volatility risk ,

-

•

risk free interest rate ,

and the parameters of the options are the same as for the BS model (Sec. 4.1). We also impose Combinations of Hermite and Laguerre polynomials are chosen for the orthogonal polynomial expansion. Our numerical solution of the Heston PDE (34) is considered in the form (39). Fourier coefficients for are obtained by solving the system of ODEs (42) with given by (36) and (41). For consistency reasons, we use MATLAB ODE solver ode45 to solve this system, that again leads to smaller values of error, although its speed is now much slower than the numerical calculation of matrix exponential in (43) using MATLAB procedure expm (Filipová, 2019, Sec. 4.1).

In order to evaluate

we repeatedly apply the Clenshaw’s recurrence formula as indicated. To numerically evaluate the error, we make use of the Gauss-Hermite (with 251 Hermite points) and Gauss-Laguerre (with 201 Laguerre points) quadratures. For pointwise comparison we make use of the same set of nodes and as in Section 4.1 with .

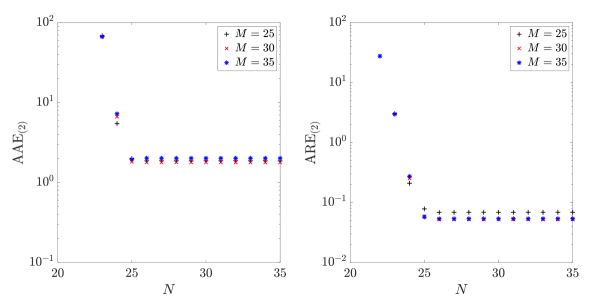

In Figure 3 on the left we can see the Heston-Lewis formula and numerical solution for and zoomed to the ITM region. This chosen combinations of polynomial orders present anticipated behaviour of the solution. The five dashed grid lines at the plane are plotted at . On the right we plot the relative error . For the same polynomial orders we plot the absolute error and relative error for different values of in Figure 4.

Similarly as in the BS case, we measure the error, absolute error and relative error calculated at given point and , i.e. now

and also average errors and for the two set of nodes and as described above. All results are summarized in Tables 3 and 4. Whereas the error is decreasing with increasing , the influence of increasing is not significant that can be seen also in Figure 5 where we depicted the for the ITM set of nodes . From the numerical analysis point of view it is also interesting to mention that very few Laguerre points used in the numerical quadrature lie within the considered region and experiments showed that the contribution from the majority of remaining points can be neglected.

| error | ||||||

|---|---|---|---|---|---|---|

| 25 | 26 | 0.238643 | 1.09888 | 0.390292 | 1.86799 | 0.0683568 |

| 25 | 28 | 1.1757e-06 | 1.1014 | 0.382943 | 1.87171 | 0.0686957 |

| 25 | 30 | 8.39452e-07 | 1.1014 | 0.382948 | 1.8717 | 0.0686954 |

| 30 | 26 | 0.238643 | 0.547496 | 0.288746 | 1.78832 | 0.0520266 |

| 30 | 28 | 1.18026e-06 | 0.547673 | 0.281325 | 1.7877 | 0.0522312 |

| 30 | 30 | 8.44246e-07 | 0.547673 | 0.28133 | 1.7877 | 0.052231 |

| 35 | 26 | 0.238642 | 0.493863 | 0.244035 | 2.01489 | 0.0535306 |

| 35 | 28 | 1.17799e-06 | 0.491256 | 0.236509 | 2.01206 | 0.0536491 |

| 35 | 30 | 8.42292e-07 | 0.491258 | 0.236514 | 2.01206 | 0.0536491 |

| 25 | 26 | 0.511921 | 3.51694 | 0.92327 | 0.0909802 | 0.844315 | 0.024334 |

|---|---|---|---|---|---|---|---|

| 25 | 28 | 0.497216 | 3.41591 | 0.936251 | 0.0922593 | 0.85614 | 0.0246748 |

| 25 | 30 | 0.497225 | 3.41598 | 0.936242 | 0.0922585 | 0.856132 | 0.0246746 |

| 30 | 26 | 0.386106 | 2.65258 | 0.539511 | 0.053164 | 0.939491 | 0.027077 |

| 30 | 28 | 0.371401 | 2.55155 | 0.552491 | 0.0544432 | 0.927665 | 0.0267362 |

| 30 | 30 | 0.37141 | 2.55162 | 0.552483 | 0.0544423 | 0.927673 | 0.0267364 |

| 35 | 26 | 0.331769 | 2.27928 | 0.418323 | 0.0412221 | 1.90743 | 0.0549739 |

| 35 | 28 | 0.317063 | 2.17825 | 0.431304 | 0.0425013 | 1.8956 | 0.0546331 |

| 35 | 30 | 0.317073 | 2.17831 | 0.431296 | 0.0425004 | 1.89561 | 0.0546333 |

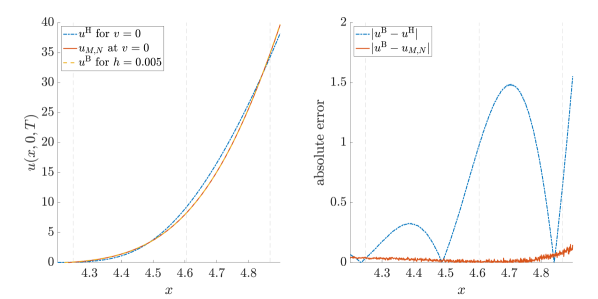

Following Section 3.2.1, we now analyse the solution close to the boundary . We consider and polynomial orders and . In Figure 6 on the left we can see the Heston–Lewis formula for , PDE solution at and the boundary solution gained by application of theory in Section 3.2.1 for . The vertical dashed grid lines are plotted again at . On the right we can see how the transport equation solution differs to the two remaining ones.

5 Conclusion

The analyticity of the solution of the Heston model has been shown in the recent paper of Alziary and Takáč (2018). A crucial step in their proof is the approximation of the payoff by a sequence of entire functions, in particular Hermite and Laguerre functions (Alziary and Takáč, 2018, sec. 11.1), with the Galerkin method (Alziary and Takáč, 2018, sec. 11.2). The aim of our paper was to make use of these theoretical results to study an alternative method for the option pricing problem for the Black and Scholes (1973) model and the Heston (1993) model. Moreover, we were interested in the behaviour of the solution near the zero volatility boundary and considered the equation for vanishing volatility. This approach was also motivated and theoretically justified by results of Alziary and Takáč (2020).

By the numerical implementation of Galerkin’s method in weighted Sobolev spaces we found an alternative representation of the solution to both BS and Heston models. The obtained representation is a smooth approximation of the solution that does not share the serious numerical difficulties of existing semi-closed formulas as they were presented by Daněk and Pospíšil (2020). Presented approach is also independent of the space variable discretization (used for example by Galerkin finite element methods) or spacial node locations (needed by radial basis function methods).

The presented experiments give a first insight into the performance of the method but thorough numerical analysis has to be performed in order to properly understand the behaviour of the solutions for higher polynomial orders. There are different possibilities how one could try to improve the method, for example to use other procedures to solve the system of ordinary differential equations especially such that take into consideration the specific triangular form of the matrix. A detailed error analysis and the application of additional procedures were beyond the scope of this paper and is left as an open issue.

A considerable advantage of the presented approach is that it can be easily adapted to other stochastic volatility models by following the steps at the beginning of Section 3.2 and using the calculations of Theorem 3.1. Aside from that, different payoff functions can be used as long as they are in the weighted Lebesgue space which applies to most of the generally used payoffs.

Funding

The work was partially supported by the Czech Science Foundation (GAČR) grant no. GA18-16680S “Rough models of fractional stochastic volatility”.

Acknowledgements

This work is based on the Master’s thesis Filipová (2019) titled Solution of option pricing equations using orthogonal polynomial expansion that was written by Kateřina Filipová and supervised by Jan Pospíšil. The thesis was also advised by Falko Baustian during the two months internship of Kateřina Filipová at the University of Rostock.

Our sincere gratitude goes to Prof. Peter Takáč from the University of Rostock, who introduced us to the problem and provided us with valuable suggestions and insightful criticism, and to both anonymous referees for their valuable comments and extensive suggestions.

Computational resources were provided by the CESNET LM2015042 and the CERIT Scientific Cloud LM2015085, provided under the programme “Projects of Large Research, Development, and Innovations Infrastructures”.

References

- Abramowitz and Stegun (1964) Abramowitz, M. and Stegun, I. A. (1964), Handbook of mathematical functions with formulas, graphs, and mathematical tables, vol. 55 of National Bureau of Standards, Applied Mathematics Series. Washington, D.C.: U.S. Govt. Print. Off., tenth printing, December 1972, with corrections, Zbl 0171.38503, MR0167642.

- Ackerer and Filipović (2020) Ackerer, D. and Filipović, D. (2020), Option pricing with orthogonal polynomial expansions. Math. Finance 30(1), 47–84, ISSN 0960-1627, DOI 10.1111/mafi.12226.

- Alziary and Takáč (2018) Alziary, B. and Takáč, P. (2018), Analytic solutions and complete markets for the Heston model with stochastic volatility. Electron. J. Differential Equations 2018(168), 1–54, ISSN 1072-6691, Zbl 1406.35415, MR3874931.

- Alziary and Takáč (2020) Alziary, B. and Takáč, P. (2020), The Heston stochastic volatility model has a boundary trace at zero volatility, available at arXiv: https://arxiv.org/abs/2004.00444.

- Aubin (1967) Aubin, J. P. (1967), Behavior of the error of the approximate solutions of boundary value problems for linear elliptic operators by Galerkin’s and finite difference methods. Ann. Sc. Norm. Super. Pisa, Sci. Fis. Mat., III. Ser. 21(4), 599–637, Zbl 0276.65052, MR0233068.

- Bates (1996) Bates, D. S. (1996), Jumps and stochastic volatility: Exchange rate processes implicit in Deutsche mark options. Rev. Financ. Stud. 9(1), 69–107, DOI 10.1093/rfs/9.1.69.

- Baustian, Mrázek, Pospíšil, and Sobotka (2017) Baustian, F., Mrázek, M., Pospíšil, J., and Sobotka, T. (2017), Unifying pricing formula for several stochastic volatility models with jumps. Appl. Stoch. Models Bus. Ind. 33(4), 422–442, ISSN 1524-1904, DOI 10.1002/asmb.2248, Zbl 1420.91444, MR3690484.

- Birkhoff, Schultz, and Varga (1968) Birkhoff, G., Schultz, M., and Varga, R. (1968), Piecewise Hermite interpolation in one and two variables with applications to partial differential equations. Numer.Math. 11(3), 232–256, DOI 10.1007/BF02161845, Zbl 0159.20904, MR0226817.

- Black and Scholes (1973) Black, F. S. and Scholes, M. S. (1973), The pricing of options and corporate liabilities. J. Polit. Econ. 81(3), 637–654, ISSN 0022-3808, DOI 10.1086/260062, Zbl 1092.91524, MR3363443.

- Bramble, Schatz, Thomée, and Wahlbin (1977) Bramble, J., Schatz, A., Thomée, V., and Wahlbin, L. (1977), Some convergence estimates for semidiscrete Galerkin type approximations for parabolic equations. SIAM J. Numer. Anal. 14(2), 218–241, Zbl 0364.65084, MR0448926.

- Bramble and Thomée (1974) Bramble, J. and Thomée, V. (1974), Discrete time Galerkin methods for a parabolic boundary value problem. Annali di Matematica 101(1), 115–152, ISSN 1618-1891, DOI 10.1007/BF02417101, MR0388805.

- Corrado and Su (1996) Corrado, C. J. and Su, T. (1996), Skewness and kurtosis in S&P 500 index returns implied by option prices. J. Financ. Research 19(2), 175, ISSN 0270-2592, DOI 10.1111/j.1475-6803.1996.tb00592.x.

- Cox, Ingersoll, and Ross (1985) Cox, J. C., Ingersoll, J. E., and Ross, S. A. (1985), A theory of the term structure of interest rates. Econometrica 53(2), 385–407, ISSN 0012-9682, DOI 10.2307/1911242, Zbl 1274.91447.

- Daněk and Pospíšil (2020) Daněk, J. and Pospíšil, J. (2020), Numerical aspects of integration in semi-closed option pricing formulas for stochastic volatility jump diffusion models. Int. J. Comput. Math. 97(6), 1268–1292, ISSN 0020-7160, DOI 10.1080/00207160.2019.1614174, MR4095540.

- Davis and Obłój (2008) Davis, M. and Obłój, J. (2008), Market completion using options. In Advances in mathematics of finance, vol. 83 of Banach Center Publ., pp. 49–60, Polish Acad. Sci. Inst. Math., Warsaw, DOI 10.4064/bc83-0-4, Zbl 1153.91479, MR2509226.

- Douglas and Dupont (1970) Douglas, J., Jr. and Dupont, T. (1970), Galerkin methods for parabolic equations. SIAM J. Numer. Anal. 7(4), 575–626, DOI 10.1137/0707048, Zbl 0224.35048, MR0277126.

- Dupont (1972) Dupont, T. (1972), Some error estimates for parabolic Galerkin methods. In A. Aziz, ed., The Mathematical Foundations of the Finite Element Method with Applications to Partial Differential Equations, pp. 491–504, Academic Press, ISBN 978-0-12-068650-6, DOI 10.1016/B978-0-12-068650-6.50022-8.

- Evans (2010) Evans, L. C. (2010), Partial differential equations, vol. 19 of Graduate Studies in Mathematics. American Mathematical Society, Providence, RI, second edn., ISBN 978-0-8218-4974-3, DOI 10.1090/gsm/019, Zbl 1194.35001, MR2597943.

- Filipová (2019) Filipová, K. (2019), Solution of option pricing equations using orthogonal polynomial expansion. Master’s thesis, University of West Bohemia.

- Fix and Nassif (1972) Fix, G. and Nassif, N. (1972), On finite element approximations to time-dependent problems. Numer.Math. 19(2), 127–135, DOI 10.1007/BF01402523, Zbl 0244.65063, MR0311122.

- Fouque, Papanicolaou, and Sircar (2000) Fouque, J.-P., Papanicolaou, G., and Sircar, K. R. (2000), Derivatives in financial markets with stochastic volatility. Cambridge, U.K.: Cambridge University Press, ISBN 0-521-79163-4, Zbl 0954.91025, MR1768877.

- Funaro (1992) Funaro, D. (1992), Polynomial approximation of differential equations, vol. 8 of Lecture Notes in Physics Monographs. Berlin Heidelberg: Springer-Verlag, ISBN 3-540-55230-8, Zbl 0774.41010, MR1176949.

- Gautschi (2004) Gautschi, W. (2004), Orthogonal polynomials: computation and approximation. Numerical Mathematics and Scientific Computation, Oxford University Press, New York, ISBN 0-19-850672-4, oxford Science Publications, Zbl 1130.42300, MR2061539.

- Heston (1993) Heston, S. L. (1993), A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 6(2), 327–343, ISSN 0893-9454, DOI 10.1093/rfs/6.2.327, Zbl 1384.35131, MR3929676.

- Heston and Rossi (2017) Heston, S. L. and Rossi, A. G. (2017), A spanning series approach to options. The Review of Asset Pricing Studies 7(1), 2–42, ISSN 2045-9920, DOI 10.1093/rapstu/raw006.

- Hull (2018) Hull, J. C. (2018), Options, Futures, and Other Derivatives. New York, NY: Pearson, 10th edn., ISBN 978-0-13-447208-9/hbk, 978-0-13-463149-3/ebook.

- Hull and White (1987) Hull, J. C. and White, A. D. (1987), The pricing of options on assets with stochastic volatilities. J. Finance 42(2), 281–300, ISSN 1540-6261, DOI 10.1111/j.1540-6261.1987.tb02568.x.

- Jarrow and Rudd (1982) Jarrow, R. and Rudd, A. (1982), Approximate option valuation for arbitrary stochastic processes. J. Financial Econ. 10(3), 347 – 369, ISSN 0304-405X, DOI 10.1016/0304-405X(82)90007-1.

- Karatzas and Shreve (1991) Karatzas, I. A. and Shreve, S. E. (1991), Brownian motion and stochastic calculus, vol. 113 of Graduate Texts in Mathematics. New York: Springer-Verlag, second edn., ISBN 978-0-387-97655-6, Zbl 0734.60060, MR1121940.

- Kufner (1980) Kufner, A. (1980), Weighted Sobolev spaces, vol. 31 of Teubner-Texte zur Mathematik [Teubner Texts in Mathematics]. Leipzig: BSB B. G. Teubner Verlagsgesellschaft, with German, French and Russian summaries, MR664599.

- Kufner and Sändig (1987) Kufner, A. and Sändig, A.-M. (1987), Some applications of weighted Sobolev spaces, vol. 100 of Teubner-Texte zur Mathematik [Teubner Texts in Mathematics]. Leipzig: BSB B. G. Teubner Verlagsgesellschaft, ISBN 3-322-00426-0, with German, French and Russian summaries, MR926688.

- Lebedev (1965) Lebedev, N. N. (1965), Special functions and their applications. Rev. English ed. translated and edited by Richard A. Silverman, Englewood Cliffs, N.J.: Prentice-Hall, Inc., MR0174795.

- Lewis (2000) Lewis, A. L. (2000), Option Valuation Under Stochastic Volatility: With Mathematica code. Finance Press, Newport Beach, CA, ISBN 9780967637204, Zbl 0937.91060, MR1742310.

- Lewis (2016) Lewis, A. L. (2016), Option Valuation Under Stochastic Volatility II: With Mathematica code. Finance Press, Newport Beach, CA, ISBN 978-0-9676372-1-1, Zbl 1391.91001, MR3526206.

- Olver, Lozier, Boisvert, and Clark (2010) Olver, F. W. J., Lozier, D. W., Boisvert, R. F., and Clark, C. W., eds. (2010), NIST handbook of mathematical functions. U.S. Department of Commerce, National Institute of Standards and Technology, Washington, DC; Cambridge University Press, Cambridge, ISBN 978-0-521-14063-8, MR2723248.

- Pospíšil and Švígler (2019) Pospíšil, J. and Švígler, V. (2019), Isogeometric analysis in option pricing. Int. J. Comput. Math. 96(11), 2177–2200, ISSN 0020-7160, DOI 10.1080/00207160.2018.1494826, MR4008120.

- Press, Teukolsky, Vetterling, and Flannery (2007) Press, W. H., Teukolsky, S. A., Vetterling, W. T., and Flannery, B. P. (2007), Numerical recipes. Cambridge University Press, Cambridge, third edn., ISBN 978-0-521-88068-8, the art of scientific computing, Zbl 1132.65001, MR2371990.

- Reed and Simon (1980) Reed, M. and Simon, B. (1980), Methods of modern mathematical physics. I. Academic Press, Inc. [Harcourt Brace Jovanovich, Publishers], New York, second edn., ISBN 0-12-585050-6, functional analysis, Zbl 0459.46001, MR751959.

- Rouah (2013) Rouah, F. D. (2013), The Heston Model and its Extensions in Matlab and C#, + Website. Wiley Finance Series, Hoboken, NJ: John Wiley & Sons, Inc., ISBN 9781118548257, Zbl 1304.91007.

- Stein and Stein (1991) Stein, J. and Stein, E. (1991), Stock price distributions with stochastic volatility: An analytic approach. Rev. Financ. Stud. 4(4), 727–752, ISSN 0893-9454, DOI 10.1093/rfs/4.4.727, Zbl 06857133.

- Swartz and Wendroff (1969) Swartz, B. and Wendroff, B. (1969), Generalized finite-difference schemes. Math.Comp. 23(105), 37–49, Zbl 0184.38502, MR0239768.

- Szegö (1975) Szegö, G. (1975), Orthogonal polynomials, vol. XXIII of Colloquium Publications. Providence, R.I.: American Mathematical Society, 4th edn., MR0372517.

- Thangavelu (1993) Thangavelu, S. (1993), Lectures on Hermite and Laguerre expansions, vol. 42 of Mathematical Notes. Princeton University Press, Princeton, NJ, ISBN 0-691-00048-4, Zbl 0791.41030, MR1215939.

- Thomée (1977) Thomée, V. (1977), Some error estimates in Galerkin methods for parabolic equations. In I. Galligani and E. Magenes, eds., Mathematical Aspects of Finite Element Methods, pp. 343–352, Springer-Verlag Berlin Heidelberg, ISBN 978-3-540-37158-8, MR0658321.

- Thomée (1978) Thomée, V. (1978), Galerkin-finite element methods for parabolic equations. In O. Lehio, ed., Proceedings of the International Congress of Mathematics, pp. 943–952, Academia Scientiarum Fennica, MR0562711.

- Thomée (2006) Thomée, V. (2006), Galerkin finite element methods for parabolic problems. Springer Series in Computational Mathematics, Springer-Verlag Berlin Heidelberg, 2 edn., DOI 10.1007/3-540-33122-0, MR2249024.

- von Sydow et al. (2015) von Sydow, L. et al. (2015), BENCHOP—the BENCHmarking project in option pricing. Int. J. Comput. Math. 92(12), 2361–2379, ISSN 0020-7160, DOI 10.1080/00207160.2015.1072172, Zbl 1335.91113, MR3417364.

- Wheeler (1973) Wheeler, M. (1973), A priori estimates for Galerkin approximations to parabolic partial differential equations. SIAM J. Numer.Anal. 10(4), 723–759, MR0351124.

- Wilmott (1998) Wilmott, P. (1998), Derivatives. Chichester: John Wiley&Sons, ISBN 978-0-47-198389-7/hbk, the theory and practice of financial engineering.

- Xiu (2014) Xiu, D. (2014), Hermite polynomial based expansion of European option prices. J. Econometrics 179(2), 158–177, ISSN 0304-4076, DOI 10.1016/j.jeconom.2014.01.003, Zbl 1298.91171, MR3170222.