Network Data

Abstract

Many economic activities are embedded in networks: sets of agents and the (often) rivalrous relationships connecting them to one another. Input sourcing by firms, interbank lending, scientific research, and job search are four examples, among many, of networked economic activities. Motivated by the premise that networks’ structures are consequential, this chapter describes econometric methods for analyzing them. I emphasize (i) dyadic regression analysis incorporating unobserved agent-specific heterogeneity and supporting causal inference, (ii) techniques for estimating, and conducting inference on, summary network parameters (e.g., the degree distribution or transitivity index); and (iii) empirical models of strategic network formation admitting interdependencies in preferences. Current research challenges and open questions are also discussed.

(prepared for the Handbook of Econometrics, Volume 7A)

Bryan S. Graham111Department of Economics, University of California - Berkeley, 530 Evans Hall #3380, Berkeley, CA 94720-3880 and National Bureau of Economic Research, e-mail: bgraham@econ.berkeley.edu, web: http://bryangraham.github.io/econometrics/. Financial support from NSF grants SES #1357499 and SES #1851647 is gratefully acknowledged. I am grateful for comments provided by the co-editors and other participants at a conference held at the University of Chicago in August of 2017. Portions of the material presented below benefited from conversations with Peter Bickel, Michael Jansson and Jim Powell. I am especially grateful to Eric Auerbach, Seongjoo Min, Chris Muris, Fengshi Niu and Konrad Menzel, as well as an anonymous referee, for written feedback which greatly improved the chapter. All the usual disclaimers apply.

Initial Draft: June 2017, This Draft: September 2019

1 Introduction and summary

Many economic activities are embedded in networks: sets of agents and the (often) rivalrous relationships connecting them to one another. Firms generally buy and sell inputs not in anonymous markets, but via bilateral contracts (Kranton & Minehart,, 2001). In addition to public listings, individuals gather information about job opportunities from friends and acquaintances (Granovetter,, 1973). We similarly poll friends for information about new products, books, movies and so on (e.g., Jackson & Rogers,, 2007; Banerjee et al.,, 2013; Kim et al.,, 2015). Banks generally meet reserve requirements through peer-to-peer interbank lending. The structure of this interbank lending network has profound implications for the vulnerability of the financial system to large negative shocks (Bech & Atalay,, 2010; Gofman,, 2017). Additional examples abound (cf., Jackson et al.,, 2017).

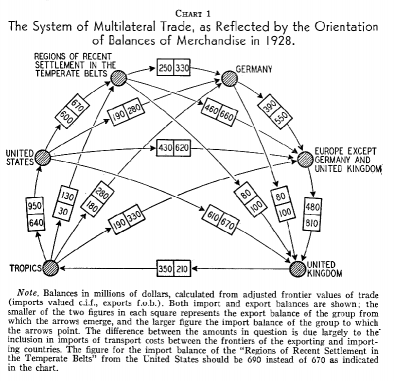

Notes: This figured appeared in Folke Hilgerdt’s 1943 American Economic Review article “The case for multilateral trade”. The figure shows aggregate trade balances between selected large countries and different regions of the world. The paper includes a narrative discussion of how the patterns of trade depicted in weighted digraph drawn in the figure developed historically.

Source: Reproduced from Hilgerdt, (1943, Chart 1).

Although important exceptions exists, some highlighted below, economists historically avoided the study networks (see Figure 1).222In contrast our colleagues in sociology studied networks from the outset of their discipline in its modern form. The monograph by Wasserman & Faust, (1994) provides a somewhat dated introduction to this literature. See also Granovetter, (1985). This is now changing, very quickly, and for several reasons. First, starting in the 1990s economic theorists applied the tools of game theory to formally study network formation (e.g., Jackson & Wolinsky,, 1996). In the resulting models agents add, maintain, and subtract links in order to maximize utility, with the realized network satisfying a pairwise stability equilibrium condition.333Other equilibrium concepts have been explored as well (cf., Bloch & Jackson,, 2006). Second, in parallel to this theoretical work, a lively empirical and methodological literature on peer group and neighborhood effects also arose (e.g., Manski,, 1993; Brock & Durlauf,, 2001; Graham,, 2008; Angrist,, 2014). Finally, largely driven by questions in empirical industrial organization, econometricians made substantial progress on the econometric analysis of games (cf., Bajari et al.,, 2013; de Paula,, 2013). Each of these literatures serve as foundations for material introduced below.

Outside of economics, two key initiators have been (i) the increasing availability of datasets with natural graph theoretic structure (see below for examples) and (ii) innovations in applied probability and theoretical statistics pertaining to random graph models (e.g., Diaconis & Janson,, 2008). These innovations provide a foundation upon which recent work in statistics and machine learning on networks is largely based.

A consequence of these developments is the emergence of a small methodological literature on the econometrics of networks. Empirical applications with substantial network content, spurred largely by access to new datasets, arose more quickly (e.g., Fafchamps & Minten,, 2002; De Weerdt,, 2004; Conley & Udry,, 2010; Atalay et al.,, 2011; Acemoglu et al.,, 2012; Banerjee et al.,, 2013; Barrot & Sauvagnat,, 2016). Furthermore, these applications now span the major fields of our discipline. Nevertheless many open questions in the econometrics of networks remain. In this chapter I attempt to provide an account of recent progress as well as make suggestions for future research. My audience is both econometricians and empirical researchers.

I divide my discussion into five parts. The discussion draws from recent contributions to the analysis of networks made in probability, econometrics, and statistics (including machine learning); approximately in that order. After an initial outline of recent empirical research with a network dimension in economics, Section 3 introduces some basic probability tools that will prove useful for what follows. Several of these tools are of quite recent origin. Next, in Sections 4 to 6 I turn to the analysis of dyadic regression models. Such models go back, at least, to the pioneering work of Tinbergen, (1962, Appendix VI) on gravity trade models. Although dyadic regression is a core empirical method in international trade, as well as in certain areas of political science and development economics, a coherent inferential foundation for empirical practice is only now emerging. My discussion, in addition to covering methods of inference, discusses how to incorporate unobserved heterogeneity into dyadic regression models (Section 6). Here I appropriate and extend insights from panel data (Chamberlain,, 1980, 1984, 1985; Hahn & Newey,, 2004; Arellano & Hahn,, 2007). This section also sketches out how to answer causal questions in dyadic settings.

Section 7 turns to the large network properties

of several common network statistics. I focus on so-called network

moments, or the frequencies with which certain low order subgraph

configurations (e.g., triangles

![]() )

occur within a network. Subgraph counts, in the form of the triad

census, were introduced by Holland & Leinhardt, (1970) almost

a half-century ago. Recent developments in probability and statistics

have substantially improved our understanding of these counts (e.g., Diaconis & Janson,, 2008; Bickel et al.,, 2011).

)

occur within a network. Subgraph counts, in the form of the triad

census, were introduced by Holland & Leinhardt, (1970) almost

a half-century ago. Recent developments in probability and statistics

have substantially improved our understanding of these counts (e.g., Diaconis & Janson,, 2008; Bickel et al.,, 2011).

Subgraph counts may be of direct interest, but also serve as the building blocks of several popular network statistics, such as transitivity or moments of the degree distribution. Jackson et al., (2017) survey the mapping between different network statistics and economic phenomena and questions. My interest in network moments also stems from their value as inputs into structural model estimation in a manner akin to the way sample moments are paired with model moments in the simulated method of moments (e.g., Gourieroux et al.,, 1993). This idea is developed in Section 8.

The discussion of dyadic regression in Sections 4 to 6 rules out interdependencies in link formation. In dyadic models the utility two agents generate by forming a link is invariant to the presence or absence of links elsewhere in the network. Beginning with the seminal work of Jackson & Wolinsky, (1996), the relaxation of this assumption is a central preoccupation of both theoretical and econometric researchers. When link formation decisions are interdependent, inefficient network structures may occur in equilibrium, making policy analysis interesting. Empirical network formation models allowing for interdependencies are also challenging to study. In a typical model many equilibrium network configurations can arise for any given parameter value; such models are incomplete (e.g., Tamer,, 2003). In principle, standard tools developed in the context of economic games between a small number of agents apply. Practically speaking such methods are computationally infeasible in the many agent context of networks. Recent research proposes a variety of ways of getting around this conundrum.

Economists’ interest in networks stems from the belief that their structure is consequential. For example, Loury, (2002) argues that differences in social networks across Blacks and Whites drives, in part, racial inequality (cf., Graham, 2018b, ). Acemoglu et al., (2012) argue that the Leontief input-output structure of the economy shapes technology shock propagation. Alatas et al., (2016) show that network structure influences the flow and aggregation of information within rural villages. Theorists also study the interplay between network structure and agent behavior on that structure (Jackson & Yariv,, 2011; Jackson & Zenou,, 2015). Methodological research relating network structure to economic outcomes builds-upon the line of peer effects research initiated by Manski, (1993). The paper by Bramoullé et al., (2009) is a nice, and influential, example of recent work along such lines.

This survey, however, does not review methods for the empirical analysis of behavior on networks. Instead I focus on modeling their formation. My motivation for this emphasis is two-fold. First, Blume et al., (2011) already survey work at the intersection of peer group effect identification and networks (cf., Blume et al.,, 2015; de Paula,, 2017). Second, the current state of research in this area suggests that a better understanding of how networks form is a prerequisite for more credible research on their consequences.

Current research on the effects of network structure on outcomes largely treats it as exogenously given (although this is not always made explicit). This decision is one reason why research on peer effects and networks remains controversial a quarter century after Manski’s foundational paper.444For example, Jackson et al., (2017, p. 81) argue that endogenous network formation, the tendency for the unobserved drivers of link formation and the behavior of interest to the econometrician to covary, poses a key challenge to “accurately estimating interactive effects in networked settings”. The focus maintained here, on formation, therefore seems to be a natural one. Ultimately, of course, the goal is to study the formation of networks and their consequences jointly, but such an integrated treatment remains largely aspirational at this stage. Although, Goldsmith-Pinkham & Imbens, (2013) provide one recent “proof of possibilities” example of such an integrated approach. Qu & Lee, (2015), Auerbach, (2016), Badev, (2017), and Johnsson & Moon, (2017) represent other steps in this direction.

2 Examples, questions and notation

The analysis of datasets with natural graph theoretic structure has a long history in the other social sciences (e.g., Moreno,, 1934), and more recently emerged as an area of focus within the statistics and machine learning community (e.g., Goldenberg et al.,, 2009; Kolaczyk,, 2009). Although we were late adopters, interest in these types of datasets now also extends across virtually all fields of economics. Nevertheless, as already noted, appropriate methods for the analysis of network data are not widely available. Ad hoc and/or heuristically motivated approaches to estimation and inference abound in empirical work. Networks are characterized by complex dependencies across agents, as well as other difficult modeling, estimation and inferential challenges. These challenges are just starting be understood and solved. Before discussing methods for the analysis of network data, I briefly introduce some recent examples of empirical network research in economics. These examples also serve to introduce some basic notation.

2.1 Empirical analysis of trade flows

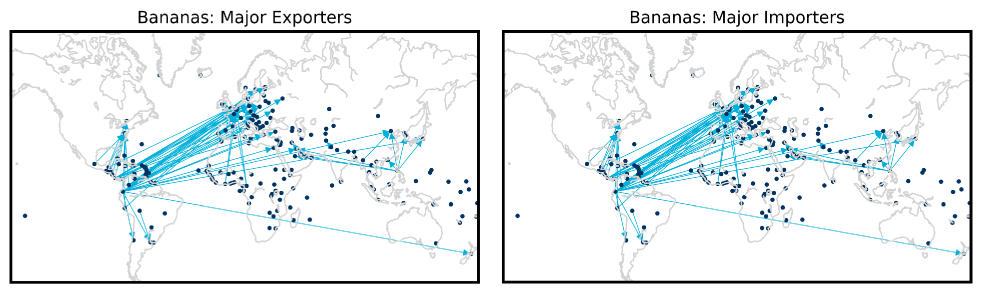

Figure 2 visually depicts international

trade in bananas, a widely-eaten tropical fruit, in 2015. Each dot

or node in the figure corresponds to a country. If, for example,

Honduras, exports at least 50,000 tons of bananas to the United States,

then there exists a directed edge

![]() from Honduras to the United States.555In constructing this network, I binarized the underlying trade flow

data to determine edge placement. The exporting country (left node) is called the tail of the

edge, while the importing country (right node) is its head.

The set of all such exporter-importer relationships forms ,

a directed network or digraph defined on

vertices or agents (here countries). The set

includes all agents (countries) in the network and

the set of all directed links (exporter-importer relationships of

50,000 tons or greater) among them.666Here denotes the Cartesian product

of the set and (i.e, ). Let be the order of the digraph and

its size. In what follows nodes may be equivalently referred

to as vertices, agents, individuals, countries and so on depending

on the context. Likewise edges may be called links, friendships, ties,

arcs, relationships and so on.

from Honduras to the United States.555In constructing this network, I binarized the underlying trade flow

data to determine edge placement. The exporting country (left node) is called the tail of the

edge, while the importing country (right node) is its head.

The set of all such exporter-importer relationships forms ,

a directed network or digraph defined on

vertices or agents (here countries). The set

includes all agents (countries) in the network and

the set of all directed links (exporter-importer relationships of

50,000 tons or greater) among them.666Here denotes the Cartesian product

of the set and (i.e, ). Let be the order of the digraph and

its size. In what follows nodes may be equivalently referred

to as vertices, agents, individuals, countries and so on depending

on the context. Likewise edges may be called links, friendships, ties,

arcs, relationships and so on.

There are countries in the banana network and hence up to directed trading relationships among them. How might an econometrician model the presence or absence of a trading relationship from country to ? Over fifty years ago Tinbergen, (1962, Appendix VI) introduced gravity models, suitable for data of the type shown in Figure 2. In a gravity model trade between two countries, a dyad in network parlance, is modeled as a function of exporter and importer attributes (e.g., their gross domestic products), as well as dyad-specific covariates (e.g., physical distance between them). Generalizations of Tinbergen’s approach are workhorses of modern empirical trade research (e.g., Santos Silva & Tenreyro,, 2006; Helpman et al.,, 2008; Anderson,, 2011).

Their ubiquity notwithstanding, serious open questions remain about how to estimate, and conduct inference on, the parameters of gravity trade models. Questions of particular interest here include how to account for the dependence across dyads sharing a country in common, how to incorporate country-specific (correlated) unobserved heterogeneity, and how to formalize causal policy effects in dyadic settings. As an example of the latter challenge, consider the effects of participation in multi-lateral trading agreements, such as the General Agreement on Tariffs and Trade (GATT) or its successor, the World Trade Organization (WTO), on trade flows. Does trade increase across participating countries (Rose,, 2004; Helpman et al.,, 2008)? While a mature literature on program evaluation suitable for single agent settings now exists (cf., Heckman & Vytlacil,, 2007; Imbens & Wooldridge,, 2009), a networked counterpart has yet to emerge.

2.2 Corporate governance

Next consider the affiliation network of (corporate board) directors and firms. This bipartite network consists of two sets of agents, the set of possible directors, , and the set of firms, . Edges, , match directors to firms (i.e., corporate boards), and hence may only run between and . A longstanding interest among corporate governance researchers centers on the implications of so-called board interlocks. When a single director sits on multiple corporate boards, then these corporations have interlocking directorates (Dooley,, 1969). Interlocking directorships may facilitate collusion and other anti-competitive activities as well as, perhaps more positively, the diffusion of innovations in corporate governance (Davis,, 1991, 1996).

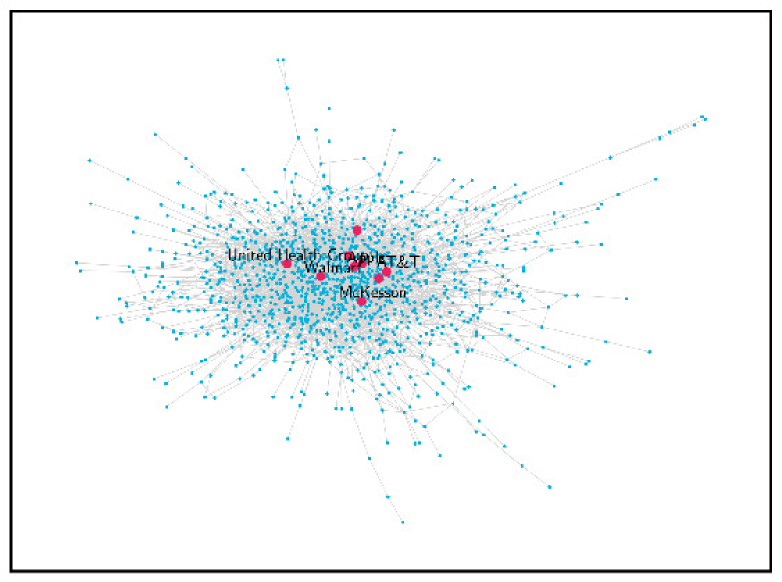

Figure 3 plots the one-mode projection of the directors-to-firms bipartite network for S&P 1,500 firms in 2016. This projection generates an undirected network on the set of all firms, with an edge between any two firms sharing at least one director in common (i.e., with interlocking corporate boards). Large firms in United States are inter-connected via overlapping corporate board membership. On average firms share at least one board member in common with four other firms and over 80 percent of S&P 1,500 firms form a giant connected component of board interlocks. The board interlock network is also highly transitive: two firms are much more likely to share a director in common, if they also share one in common with a third firm.

Chu & Davis, (2016) and Gualdani, ming provide recent analyses of board interlocks as well as references to earlier work.

2.3 Production networks

Atalay et al., (2011) study the production network of the United States economy. The sale and purchase of intermediate inputs between firms joins virtually all publicly traded corporations in the United States into one giant buyer-supplier network.

Serpa & Krishnan, (2017) present evidence of productivity spillovers across firms linked together via supply chain relationships (cf., Acemoglu et al., 2016a, ). Acemoglu et al., (2012) study the effect of the Leontief input-output structure of the US economy on shock propagation. Their analysis suggests that idiosyncratic technology shocks to critical input suppliers may have macro-level effects.

Bernard et al., (2018), using detailed supply-chain data from Japan, show how lowering supplier search costs allows firms to source inputs more efficiently, in turn lowering marginal production costs. The rich supply-chain data underlying the analysis of Bernard et al., (2018) is emblematic of the increasing availability of detailed supply chain network data from different countries (e.g., Dhyne et al.,, 2015). These datasets have the potential to dramatically improve our understanding of, for example the sources of heterogeneity in productivity across firms (e.g., Atalay et al.,, 2014) and the upstream and downstream implications of (horizontal) mergers (e.g., Fee & Thomas,, 2004; Bhattacharya & Nain,, 2011; Ahern & Harford,, 2014), among many other areas of industrial organization and regulation policy.

Source: BACI-CEPII International Trade Database (cf., Gaulier & Zignago,, 2010; De Benedictis et al.,, 2014) and author’s calculations.

Notes: International trade of bananas in 2015 (HS6 code 080390). Each node in the figure represents a country (nodes are positioned at capital cities) and an edge between two nodes indicates the presence of at least 50,000 tons of directed banana flows (the head of each directed edge corresponds to the importing nation). In the left-hand panel node size is proportional to the total exports of bananas by the relevant nation, while in the right it is proportional to its total imports.

2.4 Research collaboration

Jaffe, (1986), in a classic study, presented evidence of research and development (R&D) spillovers across technologically adjacent firms (Bloom et al.,, 2013; Acemoglu et al., 2016b, ). Such spillovers provide a motivation for firms to undertake collaborative R&D, a tendency which has increased over time (Hagedoorn,, 2002; Tomasello et al.,, 2017). König et al., (2019) model the formation of R&D partnerships across firms theoretically and empirically, exploring the implications of network structure for optimal R&D subsidy policies. The structure of spillovers across firms, as well as the mechanisms whereby they form R&D partnerships, determines optimal policies.

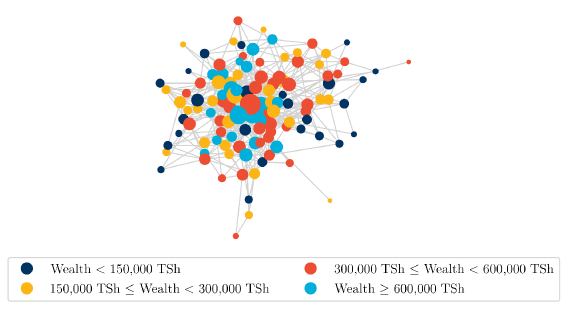

2.5 Risk-sharing across households

A classic question in development economics is whether households efficiently share risk through informal agreements (Townsend,, 1994; Udry,, 1994). Recently economists have directly collected information on risk-sharing relationships across households. For example, De Weerdt, (2004) collected data on risk-sharing links across households in a village in Tanzania and empirically modeled the determinants of these links (cf., Fafchamps & Lund,, 2003; Fafchamps & Gubert,, 2007). Ambrus et al., (2014) investigate how the precise structure of links across households determines the amount of risk that can be insured, as well as the form of second best, more local, network structures.

Network structure now informs many other areas of development economics, including research on technology adoption and program take-up in rural settings (e.g., Banerjee et al.,, 2013; Kim et al.,, 2015), the productivity of small traders and firms (e.g., Fafchamps & Minten,, 2002), and post-migration employment outcomes (Beaman,, 2011; Munski,, 2003), among other examples.

Source: Wharton Research Data Services (WRDS) - Institutional Shareholder Services (ISS) Directors dataset and author’s calculations (cf., Chu & Davis,, 2016).

Notes: The figure plots the largest connected component of the corporate board interlock network in 2016 among S&P 1,500 firms. The top 10 Fortune 500 firms in 2016 are the larger ‘Rose Garden’ colored nodes. A total of 1,216 firms belong to the largest connected component. See Newman, (2010, p. 124 - 127) for details on how to construct one-mode projections of bipartite graphs.

2.6 Insurer-provider and referral networks for healthcare

Many features of the health care market naturally map into graphs. For example, physicians may have admitting privileges across multiple hospitals, insurers typically offer preferential terms to selected networks of providers, and doctors vary in the intensity with which they refer patients to one another.777Barnett et al., (2011) and An et al., (2018) use patient referral patterns to map out relationships among physicians.

The welfare and economic implications of these networks are likely immense, given the magnitude of the health care sector in the United States economy. Ho, (2009) represents one attempt to grapple with the network structure of healthcare markets.

2.7 Employment search

Ioannides & Loury, (2004) survey the substantial literature on the interplay between social networks and job acquisition, a topic that has fascinated both sociologists and economists at least since Granovetter, (1973). The growing availability of longitudinal register data from various countries provides an opportunity to study the interface between networks and inequality in the labor market more carefully.

For example, Saygin et al., (2014) use the Austrian Social Security Database to construct a co-worker network for middle aged workers in Austria. A co-worker is anyone who an individual has ever worked with previously. They find that the structure of these co-worker networks predict the ease with which workers find employment after establishment closures (i.e., mass layoffs). This paper provides a nice example of how new data may facilitate the re-visiting of a classic networks question (cf., Hensvik & Skans,, 2016).

2.8 Questions

The examples outlined above represent only a small sample of recent appearances of network data in empirical economic research.888de Paula, (2017) and Jackson et al., (2017) provide additional references. What do we hope to learn from this growing body of research? As noted in the introduction, empirical research on networks can usefully be divided between that which studies the consequences of networks and that which studies their formation. The premise of this chapter is that network linkages across agents are consequential. That is, I take as given that networks are important venues for shock propagation, information diffusion, learning and various types of peer interactions. Maintaining this premise justifies my focus on the econometric modeling of network formation.

An analogy with the development of single agent models of discrete choice is useful. McFadden, (1974), in a pioneering paper, initiated a research program on identifying and estimating random utility models of discrete choice. Empirical application, computation, semiparametric identification and estimation, the inclusion of unobserved choice attributes, and allowing for strategic behavior, all have been important accomplishments of this research program. These econometric models are, in turn, routinely used in virtually all areas of economics.

The goal here is analogous. Relational data are ubiquitous in economics, but econometric models for such data are not. The goal, therefore, is to develop models for these data, preferably with (i) strong microeconomic foundations, (ii) that allow for unobserved agent-level heterogeneity, and (iii) incorporate interdependencies in preferences over links. Also required are feasible methods of estimation and inference (and in this area interesting and challenging questions are abundant). The availability of econometric methods for network analysis will, in turn, allow for counterfactual policy and welfare analysis. How would a particular horizontal merger affect upstream supply chain structure? What is the effect on trade flows of Eurozone membership? Could a school principal increase friendships across races, or raise average achievement, by structuring classrooms under her purview differently?

Some readers may wish to skip Section 3 initially and instead start with Sections 4 to 6. They could then return to Section 3 before tackling Sections 7 and 8. Graph theoretic concepts and notation appears throughout the chapter. While many terms and definitions are formally defined, others are not. Missing definitions can be found in any basic graph theory textbook.

3 Basic probability tools: random graphs, graphons, graph limits and sampling

This section provides an informal introduction to key ideas from the applied probability literature on exchangeable random graphs. The main concepts are (i) exchangeable random graphs and their representation, (ii) subgraph densities or network moments, (iii) limits of sequences of exchangeable random graphs, and (iv) sampling. These ideas underlie a substantial share of recent research on the statistics of networks (e.g., Airoldi et al.,, 2008; Diaconis et al.,, 2008; Bickel & Chen,, 2009; Bickel et al.,, 2011; Bhamidi et al.,, 2011; Chatterjee et al.,, 2011; Olhede & Wolfe,, 2014; Orbanz & Roy,, 2015; Gao et al.,, 2015).

Much of this statistics work has been motivated by research questions in computational biology and neuroscience (e.g., Picard et al.,, 2008). Link formation in these settings is not driven by purposeful agents. Consequently this research may initially appear rather distant from the concerns of econometricians. Nevertheless my view is that recent developments in probability and statistics have much to offer econometricians interested in networks (and also vice-versa, although making this second argument this is not on my agenda here).

The basic concepts introduced in this section appear frequently in later portions of the chapter.

3.1 Notation

Let be a finite undirected network or graph defined on vertices or agents; here denotes the set of all agents in the network.999If is a set, then denotes the cardinality of that set. If is a matrix of reals, then equals its (element-wise) absolute value. Any two agents may be connected or not. The set of such links is recorded in the edge list , consisting of the (unordered) indices of all connected agent pairs. Call the order of the network and its size. We can represent by the adjacency matrix with element

For an undirected network, with self-ties or loops ruled out, such that for , is a symmetric binary matrix with a diagonal of structural zeros. I focus on undirected networks initially, but also present some results for directed networks and bipartite networks. Specific notation for these special cases will be introduced as needed.

In settings where it is useful to emphasize the order of , I use the notation . This is especially useful when considering sequences of graphs. Let be an edge in ; sometimes I will abbreviate as . The complete graph on vertices is denoted by .

Following Jackson, (2008), let denote the network obtained by deleting edge from (if present), and the network one gets after adding this link. Let denote the adjacency matrix associated with the network obtained by adding/deleting edge from . Let denote the set of all possible adjacency matrices and the set of all possible -dimensional binary vectors.

Let be the set of agent ’s neighbors: agents to which she is directly linked. The degree of agent is given by the cardinality of this set. Equivalently agent ’s degree may be computed by summing the elements of the row of the adjacency matrix. Let be an vector of ones. The vector is called the degree sequence of the network (typically we re-arrange the order of agents such that the elements of this vector are in ascending order).

I informally call a network dense if its size, or number of edges, is “close to” and sparse if its size is “close to” . More precisely a sequence of graphs is sparse in the limit if the number of edges in it grows linearly with , dense if this growth is quadratic.

There are pairs of agents, or dyads, in a network consisting of agents. Triples, quadruples and quintuples of agents are call triads, tetrads and pentads respectively. A tuple of 17 agents, which arises rather rarely in everyday empirical work, is evidently called a septendecuple. Not having formally studied Latin, I offer the reader no guidance on pronunciation.

Let be shorthand for with similarly defined. The density of a network,

equals the proportion of connected dyads. Let be the element of the degree sequence. Average degree,

equals the average number of links per agent in the network.

In what follows random variables are (generally) denoted by capital Roman letters, specific realizations by lower case Roman letters and their support by blackboard bold Roman letters. That is , and respectively denote a generic random draw of, a specific value of, and the support of, . The abbreviations i.i.d., CLT , LLN and GGP stand for, respectively, “independent and identically distributed”, “central limit theorem”, “law of large numbers” and “graph generating process”. For the vector , denotes the Euclidean norm; for the matrix , denotes the Frobenius norm. I use to denote the identity matrix. denotes the set of natural numbers and an infinite two-dimensional array with element .

I use the big-Omega notation to denote that and . The notation denotes equality in distribution, a mathematical definition. Let be some parameter value in the space . Let be some statistic indexed by this parameter with population value . I let denote the statistic evaluated at . To economize on space I sometimes abbreviate as or and similarly for , etc.

3.2 Exchangeable random graphs

Initially assume the unavailability of agent-specific covariates, making it natural to assume that agents are exchangeable (models with covariates, and a correspondingly weaker notion of exchangeability, feature in Sections 4, 5, 6 and 8). Let be a permutation of the node labels of and the set of all such permutations. The random graph is jointly exchangeable if

| (1) |

for every permutation .

In settings where node labels have no meaning, exchangeability is an implication of a priori researcher belief (and hence a natural modeling assumption). Consider a researcher analyzing the adjacency matrix associated with a set of friendship links among adolescents in a high school (e.g., Currarini et al.,, 2009), in the absence of node-specific covariates, there is no reason to change one’s modeling approach after simultaneously applying a particular reshuffling of agents to both the rows and columns of (cf., Rubin,, 1981). Put differently, when node labels have no meaning, the probability attached to any isomorphism of should be the same as that attached to itself.

There are many interesting statistics of which are invariant to simultaneous row and column permutations. Examples include a network’s density, diameter and triangle count. A family of such statistics, network moments, is introduced below. Exchangeability suggests that a statistical model should attach different probabilities to networks with different values of such (permutation invariant) statistics, but the same probability to two networks which are isomorphic (which will share common values of any permutation invariant statistic).

An exchangeable model with strategic interaction

Most extant models of network formation satisfy condition (1). As an example, which will help to fix some ideas, consider the model of strategic network formation with bilateral transfers studied by Graham & Pelican, (2020). Let be a utility function for agent , which maps networks into utility. Define the marginal utility of edge for agent as

| (2) |

From Bloch & Jackson, (2006), a network is pairwise stable with transfers if the following condition holds.

Definition 1.

(Pairwise stability with Transfers)

The network is pairwise

stable with transfers if

(i)

(ii)

If the network in hand is a pairwise stable one, then any links actually present generate (weakly) positive utility (on net for the two agents on each side of a link). Unobserved links, in contrast, would not generate net positive utility if present.

Graham & Pelican, (2020) focus on a general family of parametric utility functions which includes, among others, the specification

| (3) |

with , and . Under (3), assuming , dyad will generate more utility when forming a link if they already share many links or “friends” in common (i.e., if is large). Here and are agent-specific “extroversion” and “popularity” parameters, the effect of which is to generate degree heterogeneity (cf., Graham,, 2017). The term is an idiosyncratic dyad-specific utility shifter. Graham & Pelican, (2020) leave the joint distribution of and unrestricted, but here I will assume that is an i.i.d. sequence which is independent of , also assumed i.i.d.

When the utility function is of the form given in (3) the marginal utility agent gets from a link with is

Pairwise stability then implies, conditional on the realizations of , , and the value of externality parameter, , that the observed network must satisfy, for and

| (4) |

with and . Equation (4) defines a system of nonlinear simultaneous equations. Any solution to this system – and there will typically be multiple ones – constitutes a pairwise stable (with transfers) network.101010Note that in this example existence of an equilibrium is easy to show using Tarski’s (1955) fixed point theorem.

As written, model (4) is incomplete (cf., de Paula,, 2013). Even if we assume that the observed network is a pairwise stable one, we have not specified a mechanism for selecting, when there are multiple ones, a specific equilibrium configuration. To complete the model, following the more careful development in Pelican & Graham, (2019), let equal the probability that configuration is selected. If is not an equilibrium – given , and – then . If is the unique equilibrium then . If is one of several equilibria, then etc.

For the net of all undirected adjacency matrices, we have that . The conditional likelihood of observing network wiring is therefore

The equilibrium conditions (4) indicate that if is an equilibrium, then so is . Hence as long as the equilibrium selection mechanism is also invariant to index permutations, as is natural to require, condition (1) holds.

Under the null of no strategic interaction, , the likelihood simplifies to

| (5) |

with

Since is i.i.d., if we further assume that , the logistic density, explicitly evaluating the integral in (5) yields

| (6) |

which is the likelihood associated with the so-called -model of Frank, (1997) and Chatterjee et al., (2011).

A feature of the -model is that links form independently conditional on the latent agent-specific effects . Equation (6) consists of a product of conditionally independent likelihood contributions.

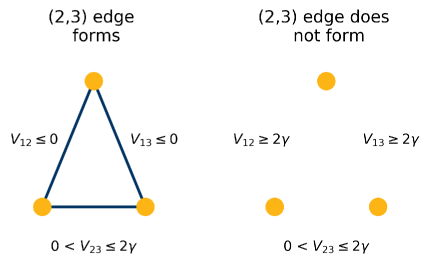

Evidently, this conditional independence structure is not typically a feature of the model when , such that strategic interaction is present. To see why by means of a simple example, consider a network consisting of just three homogenous agents (i.e., ). Initially assume that both and are less then zero, but that . This corresponds to edges and generating so much intrinsic utility that they will form irrespective of what other edges may or may not be present in the network. In contrast, the intrinsic utility attached to edge falls in an intermediate range: the edge forms if edges and are present – such that agents and share agent as a friend in common – and does not form if they are absent. This configuration of utility shocks is depicted in the left-hand panel of Figure 4. The unique equilibrium outcome in this case is a triangle network.

If, instead, and are both greater than , such that the and edges never form because of their low intrinsic utility (again irrespective of what other edges may or may not be present in the network), then the edge will not form either. This scenario is depicted in the right-hand panel of Figure 4. The unique equilibrium outcome in this case is an empty network.

This simple example shows that need not vary independently of and conditional on in the presence of strategic interaction () . Such conditional independence is a feature of the -model (). While the model is exchangeable both when and when , the conditional independence of edges only obtains under the no strategic interaction null.

Notes: Both panels depict the unique pairwise stable equilibrium associated with the shown triple of dyad-level utility shifters , and and agent-level heterogeneity parameters , and identically equal to zero. In both panels the realized value of is the same, but whether or varies with the realized values of and . If and are sufficiently low, then ; if they are sufficiently high, then . Links are not conditionally independent given .

3.3 Conditionally independent dyad (CID) models and the graphon

Having established that a network probability model should satisfy the joint exchangeability condition (1), it is important to articulate classes of models that do so. One such family of models, suggested by the last example, are conditionally independent dyad (CID) models (Chandrasekhar,, 2015; Shalizi,, 2016). In these models each agent is characterized by an unobserved latent attribute, . The agents in the network in hand are viewed as independent random draws from some population, such that the are independently and identically distributed. Conditional on the agent-specific latent variables edges form independently with

for every dyad with . Here for all is a symmetric edge probability function. In anticipation of results to come, call this function a graphon: short for graph function.

Conditional on the latent agent-specific effects the likelihood of the network is

Unconditional on , the likelihood equals

| (7) |

where is the density of . Importantly (7) allows for dependence across dyads which share agents in common. Independence holds only conditional on the latent agent attributes (Graham,, 2017). Similar independence restrictions play a prominent role in the econometrics of panel data (Chamberlain,, 1984; Arellano & Honoré,, 2001).

It is an easy exercise to show that (7) is compatible with the finite joint exchangeability restriction (1).

The -model, introduced above, belongs to the family of CID models with a graphon of

Random threshold graphs (e.g., Diaconis et al.,, 2008) are also members of this family with graphon

and the CDF of .

It is important to realize that CID models constitute only a subset of all jointly exchangeable random graph models when – the number of agents in the network – is finite. As shown by means of the example introduced above, strategic interaction in link formation can induce dependence across elements of the adjacency matrix that evidently cannot be eliminated by conditioning (see Figure 4 above). Although not all exchangeable models are CID ones, this family of models plays an outsized role in extant large sample theory for networks.

3.4 Aldous-Hoover representation theorem and the graphon

Joint exchangeability imposes more structure on the network probability distribution when there are an infinite number of agents. Specifically, if we strengthen (1) to hold for any permutation of a finite number of the indices of the infinite sequence , we have a generalization of de Finetti, (1931) type exchangeability of an infinite sequence, appropriate for infinite random graphs. In independent work Aldous, (1981) and Hoover, (1979) showed the following representation result for infinite random adjacency matrices (cf., Kallenberg,, 2005).

Theorem 1.

(Aldous-Hoover) A random adjacency matrix is jointly exchangeable if and only if there is a measurable function such that

for , , and independently and identically distributed random variables with .

Here is a mixing parameter, analogous to the one appearing in de Finetti’s (1931) classic representation theorem for exchangeable binary sequences.111111To make the connection with de Finetti, (1931) transparent Aldous, (1981, Lemma 1.5) also shows that an infinite sequence is exchangeable if and only if there exists a measurable function such that . Theorem 1 implies that if network agents are exchangeable for all , then we can proceed ‘as if’ edges formed according to a CID model or a mixture of such models.

Exploiting the fact that the elements of are binary, we can simplify Theorem 1 as follows. Averaging over yields

from which we get the more convenient representation, for ,

| (8) |

This is, of course, just a conditional edge independence model (or, more precisely, a mixture of such models). In what follows I focus on inference which conditions on the empirical distribution of the data; consequently can often safely be ignored. When this is the case I suppress the argument in the graphon, writing . See Bickel & Chen, (2009) and Menzel, (2017) for additional discussion.

Theorem 1 motivates an approach to nonparametric modeling of large networks that proceeds ‘as if’ links form independently conditional on the agent-specific latent variables . This is convenient because CID models induce a very particular dependence structure across the rows and columns of the network adjacency matrix.

Consider, without loss of generality, agents , and . In a CID model and may covary; the dyads and share the agent in common and hence both links form, in part, based on the value of . However and vary independently conditional on , and (hence the conditionally independent dyad nomenclature). Links involving pairs of dyads which share no agents in common, for example and , form independently.

The structured pattern of dependence, independence and conditional independence associated with CID models facilitates the development of LLNs and CLTs that can be applied to statistics of the adjacency matrix. A group of statistics for which some large network distribution theory is available are network moments.

3.5 Network moments

Almost fifty years ago Holland & Leinhardt, (1970) suggested that a network’s architecture could be usefully summarized by its average local structure. Agent exchangeability, in conjunction with Theorem 1, also motivates an approach to network modeling based on the frequency of low order subgraph configurations (i.e., the number of edges, two stars, triangles, squares, k-stars etc).

Consider, for example, the set of all triads

– unordered triples of agents – in a network; what fraction of

these triads take two-star

![]() or triangle

or triangle

![]() configurations? These frequencies, called network moments by

Bickel et al., (2011), feature prominently in research by sociologists

(e.g., Granovetter,, 1973; Coleman,, 1988; Gould & Fernandez,, 1989)

and computational biologists (e.g., Milo et al.,, 2002; Pržulj et al.,, 2004);

albeit in the context of two largely independent and desynchronized

literatures.

configurations? These frequencies, called network moments by

Bickel et al., (2011), feature prominently in research by sociologists

(e.g., Granovetter,, 1973; Coleman,, 1988; Gould & Fernandez,, 1989)

and computational biologists (e.g., Milo et al.,, 2002; Pržulj et al.,, 2004);

albeit in the context of two largely independent and desynchronized

literatures.

In economics, network moments play an increasingly important role in empirical research as well. Examples include Jackson et al., (2012), who explore, theoretically and empirically, how different triad configurations can support infrequent favor exchange between agents; Atalay et al., (2011), who calibrate a model of buyer-seller networks to the US economy by modeling its degree distribution121212Below I show that network moments and moments of the degree distribution are closely connected.; and de Paula et al., (2018), who present conditions under which (a variant of) network moments (partially) identify preferences in a structural model of strategic network formation.

Network moments, in addition to being important summary statistics for graphs, play an important role in (i) the distribution theory for dyadic regression discussed in Sections 4 and 5, (ii) understanding the degree distribution and (iii) structural model estimation. The material which follows is dense.

Subgraphs and isomorphisms

The exact sense in which a network is summarized by its moments can be made precise using the graphon, as introduced above, and the notion of a graph limit, which will be introduced below (Diaconis & Janson,, 2008; Lovász,, 2012). First we require a formal definition of a subgraph. There are two definitions used by empirical network researchers.

Definition 2.

(Partial Subgraph) Let be any subset of the vertices of and , then is a partial subgraph of .

A partial subgraph of consists of a subset of agents in and a subset of all edges among also appearing in . Counts of partial subgraphs are often referred to as network motif counts (e.g., Milo et al.,, 2002), although this terminology is not used consistently. The two star motif is a partial subgraph of . Note that in this example does not include the edge between agents, numbered clockwise from the top, and .

Definition 3.

(Induced Subgraph) Let be any subset of the vertices of and , then is an induced subgraph of .

An induced subgraph includes all edges in connecting any two agents in . Although is a partial subgraph of , it is not an induced one. Counts of induced subgraphs are often referred to as graphlet counts (e.g., Pržulj et al.,, 2004), although again not consistently so.

Consider two graphs, and , of the same order. Let be a bijection from the nodes of to those of . The bijection maintains adjacency if for every dyad if , then ; it maintains non-adjacency if for every dyad if , then . If the bijection maintains both adjacency and non-adjacency we say it maintains structure.

Definition 4.

(Graph Isomorphism) The graphs and are isomorphic if there exists a structure-maintaining bijection .

In what follows I use the notation to denote that “ is isomorphic to .”

Two special families of motifs/graphlets will play a prominent role in the analysis of network summary statistics presented in Section 7 below. First, a -cycle is order graphlet with nodes labeled (or relabeled) such that its edges form a cycle:

A -cycle is a connected graphlet with edges on nodes. As one transverses a -cycle graphlet no vertex is crossed more than once except for the first/last one. Important examples of -cycles are triangles () and 4-cycles ().

Second, a tree is a connected graph with no cycles. The number of edges on a order tree is ; a feature which will prove highly convenient. Important examples of trees are -star graphlets, such as two-stars () and three-stars (). Trees will feature in the analysis of the degree distribution given below. Trees are also called connected acyclic graphs.

Induced subgraph density

Using Definitions 3 and 4 we can formally introduce the induced subgraph density. This will be our first measure of the frequency with which a specific low-order local configuration of links appears within a network. Let be a -order graphlet of interest (e.g., or ), the group of isomorphisms of , and its cardinality. It is helpful to observe that equals the number of (partial) subgraphs of that are isomorphic to . For example, since there are three ways to draw a two-star configuration on three vertices. is the real world network under study.

Let be a set of integers. If we require that , then there are such integer sets; denote this set of integer sets by . If all that is required is that for , then there are such integer sets; denote this set of integer sets by

Let the vertex set of be . Let denote the induced subgraph of associated with vertex set . Since we wish to compare and it will be convenient to relabel the latter. Let be a relabelling of such that , so that if . Let ; the frequency with which equals is then

| (9) |

Call (9) the induced subgraph density of in . Alternatively we can write

| (10) |

The induced subgraph frequency of in equals the fraction of injective mappings that preserve both edge adjacency and non-adjacency. Direct computation of this fraction yields the equalities

| (11) | ||||

In order to understand the mechanics of computing (11) it is useful to reformulate, one again, its definition. Let be the sub-adjacency matrix constructed by removing all rows and columns of except those in We can check for whether is an isomorphism of by inspecting the elements of the sub-adjacency matrix.

Consider the two star triad , we can express in terms of as

| (12) |

We have

with the three terms to the right of the equality in (12)

equal to indicators for these three possible isomorphisms (on triad/vertex

set ). In general

may be defined in terms of

with the number of components equal to the number of possible isomorphisms

of . There is only one isomorphism of the

![]() configuration, yielding a second example of

configuration, yielding a second example of

Recognizing that is a functional of the adjacency matrix of allows us to easily compute its expectation when edges form according to the conditional edge independence model (8). Once again consider the two star configuration; iterated expectations and conditional independence of edges given yield

(and also that the value of is invariant to permutations of its indices). Finally we have, recalling that ,

for For a generic graphlet configuration we have

| (13) | ||||

where denotes the complement of the graph : the graph defined on the same nodes as with an edge present if, and only if, it is not present in . The graph sum of and therefore coincides with the complete graph .

Call the expectation of the induced subgraph density of in the graphon and write it as, in an abuse of notation, . Clearly is an unbiased estimate of when the true network generating process is of the CID type. Notice how the graphon provides a language for connecting empirical graphlet counts, first studied by Holland & Leinhardt, (1970), with well-defined probabilistic objects. This connection will prove useful for developing a procedure for conducting inference on using the sample graph . Since generally varies with the graphon , the idea is that by identifying for enough specific configurations (e.g., etc.), we may be able to identify itself (cf., Bickel et al.,, 2011).

Injective homomorphism density

A second notion of subgraph density also appears in some of the results which follow. Let denote that is a partial subgraph of . Using Definitions 2 and 4, we can also define what I will call, following Lovász, (2012), the injective homomorphism density.131313The Lovász, (2012) monograph presents several different notions of a subgraph density. The two introduced here were chosen for their connection to actual empirical practice. See also Diaconis & Janson, (2008). The homomorphism density gives the probability that a (partial) subgraph of , for chosen uniformly at random from , is equal to . Alternatively the homomorphism density equals the fraction of injective mappings that preserve edge adjacency. These mappings do not need to preserve non-adjacency.141414In contrast the induced subgraph density requires preservation of both adjacency and non-adjacency. The injective homomorphism density of in equals

| (14) | ||||

The two equivalent definitions are given to develop familiarity with notation. To understand expression (14) it is helpful to calculate the injective homomorphism density of in There are three isomorphisms of the two star configuration such that . Next consider the summation in the first line of (14). This summation is over all order partial subgraphs of which are isomorphic to . There are exactly two star partial subgraphs in (three for each of its four triads), a total of 8 of these configurations are subgraphs of such that . Note that the induced subgraph density of in is just .

Under an Aldous-Hoover GGP we have

Call the expectation of the injective homomorphism density of in the graphon and write it as .

3.6 Graph limits

Let be a finite exchangeable graph with adjacency matrix . Let

Observe that is a valid graphon and further that

for any of order (Chatterjee,, 2017, p. 28). This equality connects the definition of the induced subgraph frequency of in , denoted by in equation (11), with its “population” counterpart – equation (13). It also motivates the idea of the graphon as the appropriate limit object for a sequence of graphs, . If the subgraph frequency

converges to some limit for all fixed subgraphs , then we say that has a limit. Lovász & Szegedy, (2006) showed the natural limiting object is a graphon (i.e, heuristically, as ). Diaconis & Janson, (2008) connect this finding with the Aldous-Hoover representation theorem. Collectively these results motivate an approach to summarizing a network by the frequency of different low order subgraph configurations within it; by its average local structure. Lovász, (2012) provides a rigorous and compresensive introduction to theory of graph limits.

3.7 Sampling

In this chapter I will adopt two perspectives on “sampling”. In the first we view the network in hand as the one induced by a random sample of agents from some large (i.e., infinite) population. Let be an (infinite) exchangeable random graph. Let be a random sample of agents of size from . We assume that the observed network, , coincides with the subgraph induced by this random sample of vertices:

| (15) |

Let with be the adjacency matrix of . Exchangeability implies the characterization

| (16) |

with , and independent random variables (cf., Aldous,, 1981; Hoover,, 1979). Here is symmetric in its second and third arguments.

Under (15) the elements of , the adjacency matrix for the network in hand, also obey the characterization (16). The “sampling distribution” of some statistic of , say , is simply the one induced by repeated random sampling from the underlying infinite population. We calculate limit distributions by studying the sampling distribution of as .

An advantage of this first perspective it that is allows the econometrician to fully exploit the independence/dependence structure associated with the Aldous-Hoover Theorem. If the graph in hand is the one induced by a random sample of agents from some infinite exchangeable population, then we can proceed “as if”

| (17) |

for and . Although (17) is a nonparametric data generating process, it is a structured one. We can use this structure to our advantage.

An unattractive feature of this perspective is that if the density of the population graph is very low, then that of the sampled graph may be zero with high probability. To see this point heuristically assume that the population consists of agents, with very large. Assume that average degree, , is some small positive constant that does not dependent on . The probability of observing an edge between the two independent random draws from the population is thus

Boole’s inequality then gives a probability of observing at least one edge in our sampled network no greater than , which will be close to zero when . When the population graph is “sparse”, it is quite likely that the subgraph induced by a random sample of agents from it will be empty and hence completely uninformative. See Crane, (2018, Chapter 3) for more discussion and examples.

This example raises two questions. First, how does one sample from a large sparse graph in practice? I ignore this question here, but flag it as an interesting one which merits thought. The monograph by Crane, (2018) surveys extant work in this area. Second, if the sampling is fictitious (i.e., analysis is based upon the full graph), what mistakes might be made by proceeding “as if” we had randomly sampled from some (now entirely hypothetical) large graph?

To answer the second question is useful to return to an empirical example. Atalay et al., (2011) study the supply chain network of large publicly traded firms in the United States. Their network is not sampled, but rather constructed from Securities and Exchange Commission (SEC) reports filed by the entire universe of publically trade firms. If the model of network formation of interest is a conditional independent dyad (CID) one, then we are free to proceed “as if” the observed network were generated according to (17). If, instead, we view the network in hand as, for example, an equilibrium of a finite -player supply chain formation game, then it may be difficult to justify (17); strategic interaction may induce dependence across links that cannot be conditioned away. We cannot appeal directly to the Aldous-Hoover Theorem.

As in de Finetti, (1931), the Aldous-Hoover Theorem requires that the agent indices constitute an infinite sequence. However, just as the de Finetti result fails for finite sequences (e.g., Diaconis,, 1977), but approximately holds when the sequence is large enough (e.g., Diaconis & Freedman,, 1980), the hope is that in large (but finite) networks Theorem 1 remains useful (cf., Volfosky & Airoldi,, 2016).

One possibility would be to assume that is large enough such that a representation like (17) “approximately” holds. One could then conduct inference on model parameters by comparing observed network moments with model generated ones. The sampling distribution of the observed network moments would be calculated assuming an Aldous-Hoover DGP (which is appropriate for large enough). I sketch this idea in a bit more detail in Section 8 below. Many gaps in this discussion remain. Alternatively we could proceed along the lines of Menzel, (2016). In this approach we would approximate our finite player network formation game, with a limit game which is easier to deal with (see Section 8).

3.8 Adding sparsity: the Bickel & Chen, (2009) model

For any finite network of unlabelled agents, exchangeability is a natural, indeed unavoidable, modeling assumption. Unfortunately its extension to infinite exchangeability, as needed for Theorem 1, has the unattractive implication that the network is either empty or dense in the limit. Specifically a (random) agent will either never form links or do so infinitely often as . Denseness and sparseness are limit properties of infinite sequences of graphs. Any empirical network is neither “dense” nor “sparse”, it just is what it is. However, in most real world networks the numbers of agents and links are of similar magnitudes. This suggests that approximation results based on sequences of graphs that are sparse in the limit may be more useful than those with dense limits. Whether this is, in fact, the case remains an open question (Green & Shalizi,, 2017).

One way to model sequences of graphs with sparse limits, while still preserving the analytic convenience of conditional independence across edges, was proposed by Bickel & Chen, (2009). The Bickel-Chen model is the default one in the nonparametric statistics and machine learning literatures on random graphs.

Let be a random network of order generated according to (8). The expected average number of links an agent has in this network, that is average degree, equals

| (18) |

for . Average degree (18) either tends toward infinity or is zero, depending on whether is greater than or equal to zero.

To extend model (8) so that it can accommodate sparse graph sequences Bickel & Chen, (2009) define the conditional density

Next observe that since on we get can decompose the graphon as

| (19) |

With this parameterization, Bickel & Chen, (2009) and Bickel et al., (2011) argue that it is natural to let , but retain independence of from . Suppressing the argument (it is never identifiable), they write

| (20) |

The rate at which then controls the rate of average degree growth as grows large. If with as , then the graph is sparse. If we say the graph is dense, semi-dense etc. Many of the results presented below require that for some , despite the fact that might best describe real world networks (where average degree is generally low even when is very large). In what follows I will try to highlight those few known results which can accommodate sparse graph sequences.

3.9 Further reading

Orbanz & Roy, (2015) provide a non-technical introduction to the probability literature on exchangeable random arrays; the monograph by Kallenberg, (2005) a more complete development. Crane, (2018) also surveys this material, at a fairly accessible level, and with a somewhat contrarian point of view.

4 Dyadic regression

Jan Tinbergen’s 1962 report Shaping the World Economy, commissioned by Twenty Century Fund, featured, along with its sculptural title, a remarkable empirical analysis of trade flows (Tinbergen,, 1962). Table VI-1 in that report presented the results of a least squares fit of the logarithm of exports from country to country onto a constant, the (log) Gross National Product (GNP) of both countries and , the (log) distance between and , and a variety of other covariates capturing different relationships between and . Tinbergen’s (1962) analysis was based upon a sample of countries, or directed trading relationships.151515A second analysis, based upon a larger sample of countries, was also reported upon in Table VI-4 of the report.

Table VI-1 of Tinbergen, (1962) presents the results of what I will call a dyadic regression analysis. This particular analysis continues to serve as prototype for a substantial body of empirical work in international trade (Anderson,, 2011). Dyadic regression analyses also appear in other areas of social science research. They have been used, to give just a few recent examples, to study the onset of war among nation states (e.g., Russett & Oneal,, 2001), risk-sharing across households (e.g., De Weerdt,, 2004; Fafchamps & Gubert,, 2007; Attanasio et al.,, 2012), supply chain linkages across firms (e.g., Atalay et al.,, 2011, Table S3), the formation of commercial R&D collaborations (König et al.,, 2019, Table 4), and co-camping behavior among hunter-gathers (Apicella et al.,, 2012, Tables S2 to S49).

Familiar methods of econometric analysis appropriate for single agent models, typically utilizing a random sample from the population of interest, are ill-suited for dyadic settings (cf., Cameron & Golotvina,, 2005). Consequently, considerable confusion and controversy is associated with dyadic analyses in practice (e.g., Erikson et al.,, 2014). It is remarkable that, over a half-century after Tinbergen’s (1962) pioneering analysis of trade flows across countries, and also given the considerable empirical work that has followed, a textbook treatment of estimation and inference methods for gravity and other dyadic regression models remains unavailable.

4.1 Population and sampling framework

Let index agents in an infinite population of interest. Associated with each agent is the observable attribute . This attribute partitions the population into subpopulations which I will refer to as “types”. Let be the index set for type agents. Although may be very large, I assume that the size of each subpopulation, , is infinite with positive frequency (i.e., for ).

When all observable agent attributes are discretely-valued, then simply enumerates all distinct combinations of these attributes (e.g., might correspond to a Hispanic female, living in the Florida, with 12 years of schooling and two college-educated parents). More heuristically we can think of as consisting of the support points of a multinomial approximation to the support of a bundle of attributes, some of which might be continuously-valued. The finite support restriction is made in order to invoke a representation result due to Crane & Towsner, (2018); I do not think it is essential.

Associated with each ordered pair of agents is the scalar directed outcome . I will refer to agent as the “ego” of the directed dyad and agent as its “alter”. In the context of the trade example the ego agent is the exporting country, the alter the importing one. The adjacency matrix collects all such outcomes into an infinite random array.

From the standpoint of the econometrician, the indexing of agents within subpopulations homogenous in is arbitrary: agents of the same type are exchangeable. Exchangeability of agents within subpopulations homogenous in induces a particular form of exchangeability on the adjacency matrix. This form of exchangeability, in turn, induces a particular form of dependence across the rows and columns of . The structure of this dependence allows for the formulation of LLNs and CLTs.

Let be any permutation of a finite number of the agent indices which satisfies the restriction

| (21) |

Condition (21) constrains index permutations to occur among agents of the same type (i.e., we may permute the indices in , but not those within, for example, ). Crane & Towsner, (2018) call a network relatively exchangeable with respect to (or -exchangeable) if

| (22) |

for all permutations satisfying (21). -exchangeablility is a natural generalization of joint exchangeability, as introduced in the context of the Aldous, (1981) and Hoover, (1979) Theorem earlier.

A insightful way to think about condition (22) is in terms of vertex colored graphs. Associate with the color of a vertex; condition (22) states that all colored graph isomorphisms are equally probable. Since, when vertices of the same color are exchangeable, there is no reason to attach more or less probability to particular isomorphisms of a given vertex colored graph, any probability model for should be consistent with condition (22). As long as encodes all the vertex-specific information available to the econometrician, then -exchangeability is a nature a priori modeling restriction.

Let , and be (sequences of ) i.i.d. random variables, additionally independent of one another, and consider the random array generated according to the rule

| (23) |

with a measurable function (we normalize , and to have support on the unit interval without loss of generality). Clearly a graph generated according to (23) is -exchangeable (cf., Crane,, 2018, Chapter 8).

Here is a mixing parameter analogous to the one appearing in de Finetti’s (1931) original representation theorem. Since this parameter is unidentified, and the focus here is upon inference conditional on the realized data distribution, I will depress the dependence of on , defining the notation . Consistent with earlier terminology, the function will be referred to as a graphon.

Because doing so is convenient for the discussion of causal inference in dyadic settings which follows, (23) makes no presumption of independence between and . Of course we can always write

with equal to unit ’s rank among all those units of her type. The resulting sequence of 0-to-1 uniform random variables is independent of by construction (cf., Graham et al.,, 2010).

Depending on the context, it is fine to work with either or , but, as explained below, the former is more useful for making causal arguments; hence I allow for dependence between the observed covariate vector and the unobserved unit-specific effect in what follows (akin to a correlated random effects panel data analysis). The nuances involved will become clear as we proceed.

Networks generated by (23) exhibit a very particular pattern of dependence across the rows and columns of . Consider, without loss of generality, agents , , and . The outcomes and are independent of one another; the outcomes and are, however, dependent. These two outcomes share agent in common; the value of and influences both and , inducing dependence. But conditional on and , and are independent; if we condition on the observed covariates alone, however, they remain dependent. Finally and are dependent, this dependence holds even conditional on and because and may covary.

In words we have independence across dyads sharing no agents in common (exports from Japan to the United States and from Turkey to Germany), dependence across those sharing at least one agent in common (exports from Japan to the United States and from Japan to the United Kingdom), and “even more” dependence across dyads sharing both agents in common (e.g., exports from Japan to the United States and vice-versa).

Models with this type of dependence structure, as already noted, are called conditionally independent dyad (CID) models. The “conditionally independent” terminology reflects the fact that the outcomes and , associated with a pair of dyads sharing one agent in common, can be rendered independent of one another by conditioning on the observed covariates as well as the unobserved latent attributes .

Crane & Towsner, (2018), in an extension of the Aldous-Hoover representation result described earlier, show that for any -exchangeable random array there exists another array generated according to (23) such that the two arrays have the same distribution:

| (24) |

We can therefore use (23) as an ‘as if’ non-parametric data generating process for ; this will facilitate a variety of probabilistic calculations (e.g., computing conditional expectations, variances and, especially, covariances).

Let index a simple random sample from the target population. For each of the sampled units the econometrician observes and for each of the sampled dyads she observes . From hereon I will assume that is undefined (normalized to zero for convenience). Adapting what follows to accommodate self-loops is straightforward.

4.2 Composite likelihood

Let be a parametric family of distributions for the conditional distribution of given and . For example, Santos Silva & Tenreyro, (2006) model trade from exporter to importer given covariates as a Poisson random variable:

| (25) |

with and a known vector of functions of and . As an example, if , then setting

results in a basic gravity trade model specification.161616In practice distance is measured using the so-called great circle formula; which accounts for the curvature of the Earth’s surface.

Similar to Russett & Oneal, (2001), a researcher might model the conditional probability that country attacks country using logistic regression such that

| (26) |

with and .

An important feature of both (25) and (26) is that they only specify the marginal distribution of given and . The econometrician is not asserting, for example, that

since doing so would imply independence of and given covariates; but such dependence is precisely the complication under consideration. Formulating a conditional likelihood for the entire adjacency matrix given would require an explicit specification of the dependence structure across dyads sharing agents in common. In contrast , which is a model for the marginal distribution of alone, does not require modeling this dependence.

Let and consider the estimator which chooses to maximize:

| (27) |

Because its summands are not independent of one another – at least those sharing indices in common are not – (27) does not correspond to a log-likelihood function for given . Instead it corresponds to what is sometimes called a composite log-likelihood (e.g., Lindsey,, 1988; Cox & Reid,, 2004). A composite likelihood “is an inference function derived by multiplying a collection of component likelihoods” (Varin et al.,, 2011, p. 5). Although (27) fails to correctly represent the dependence structure across the elements of the adjacency matrix, if it is based upon a correctly specified marginal density, generally will be consistent for . This follows because the derivative of composite log-likelihood is mean zero at under correct specification of its components. While an appropriately specified composite log-likelihood typically delivers a valid estimating equation, accurate inference is more challenging, since the unmodeled dependence structure in the data does need to be explicitly taken into account at the inference stage.

4.3 Limit distribution

Consider a mean value expansion of the first order condition associated with the maximizer of (27).171717A general result on consistency of could be constructed by adapting the results of Honoré & Powell, (1994). Such an expansion yields, after some re-arrangement,

with a mean value between and which may vary from row to row and the superscript denoting a Moore-Penrose inverse. Here is the “score” vector

| (28) |

with for and . If the Hessian matrix converges in probability to the invertible matrix , as I will assume, then

so that the asymptotic sampling properties of will be driven by the behavior of .

As with the composite log-likelihood criterion function, the summands of are not independent of one another (cf., Cameron & Golotvina,, 2005; Fafchamps & Gubert,, 2007). A standard central limit theorem cannot be used to demonstrate asymptotic normality of . Fortunately , although not a U-Statistic, has a dependence structure similar to one. This insight can be used to derive the limit properties of .

Begin by re-writing as

| (29) |

where and While (29) has the cursory appearance of a U-Statistic it is, in fact not one: , which enters , varies at the dyad level, hence is not a function of i.i.d. random variables.

Let ; the projection of onto the observed covariate matrix and the unobserved vector of unit-specific effects equals:

| (30) |

with and The expression to the right of the equality in (30) follows from the Crane & Towsner, (2018) representation (23) and independence of from .

An important observation is that the projection (30) is a U-statistic of order two: specifically it is a summation over all dyads that can be formed from the i.i.d. sample . Unusually our U-statistic is defined in terms of a combination of both observed and unobserved random variables.

The projection error consists of a summation of conditionally uncorrelated summands; hence (as long as does not change as ). We also have that and are uncorrelated by construction.

Although we cannot numerically compute – even if is known – because the are unobserved, we can use the theory of U-statistics to characterize its sampling properties as . Decomposing into a Hájek projection and a second remainder term yields (e.g., Lehmann,, 1999; van der Vaart,, 2000):

where, defining and ,

| (31) | ||||

| (32) |

The superscript ‘e’ denotes ‘ego’ since it is the ego unit’s attributes which are being held fixed in the average used to compute . Similarly the ‘a’ denotes ‘alter’, since it is that unit’s attributes which are held fixed when defining . Conveniently is a sum of i.i.d. random variables to which, after scaling by , a CLT may be applied. Furthermore it can be shown that .

Putting these results together yields the asymptotically linear representation

and hence a limit distribution for of

| (33) |

where Although is not a U-statistic, under the assumptions maintained here, its limit distribution coincides with that of (which is a U-statistic).

Before turning to practicalities of variance estimation I will present a useful property of the kernel entering the Hájek Projection, above. By the usual conditional mean zero property of the score function we have that as long as marginal density of given and is correctly specified. This property can be used to show that the averages, and , are also conditionally mean zero. Taking the former we have that