X \IssueX \Year2020

Zero-Sum Differential Games on the Wasserstein Space∗

Abstract

We consider two-player zero-sum differential games (ZSDGs), where the state process (dynamical system) depends on the random initial condition and the state process’s distribution, and the objective functional includes the state process’s distribution and the random target variable. Unlike ZSDGs studied in the existing literature, the ZSDG of this paper introduces a new technical challenge, since the corresponding (lower and upper) value functions are defined on (the set of probability measures with finite second moments) or (the set of random variables with finite second moments), both of which are infinite-dimensional spaces. We show that the (lower and upper) value functions on and are equivalent (law invariant) and continuous, satisfying dynamic programming principles. We use the notion of derivative of a function of probability measures in and its lifted version in to show that the (lower and upper) value functions are unique viscosity solutions to the associated (lower and upper) Hamilton-Jacobi-Isaacs equations that are (infinite-dimensional) first-order PDEs on and , where the uniqueness is obtained via the comparison principle. Under the Isaacs condition, we show that the ZSDG has a value.

1 Introduction

In this paper, we consider a class of nonlinear two-player zero-sum differential games (ZSDGs), where the state process (dynamical system) depends on the random initial condition and the state process’s distribution (the law of the state process), and the objective functional includes the state process’s distribution and the random target variable. The main objectives of this paper are to establish dynamic programming principles (DPPs) for lower and upper value functions of the ZSDG, show that the value function is the unique viscosity solution of the associated Hamilton-Jacobi-Isaacs (HJI) equation, and prove that under the Isaacs condition, the ZSDG has a value.

(Deterministic and stochastic) ZSDGs and their applications have been studied extensively in the literature; see Basar2 ; Bardi_book_1997 ; Bensoussan_book_2007 ; Buckdahn_Cardaliaguet_DGAA_2011 ; Basar_Zaccour_book and the references therein. Specifically, Rufus Isaacs Isaacs_book was the first who considered (deterministic) ZSDGs with applications to pursuit-evasion games. Elliott and Kalton Elliott_1972 introduced the concept of nonanticipative strategies for the players, which was used in Evans_1984 ; Fleming_1989 to obtain DPPs for lower and upper value functions of the ZSDG, and show that the value functions are viscosity solutions to associated (lower and upper) HJI equations. The existence of the value of ZSDGs and the existence of saddle-point solutions were studied in Elliott_1972 ; Friedman_JDE_1970 ; Ghosh_JOTA_2004 .

Later, the results of Evans_1984 ; Fleming_1989 were extended to various other settings for ZSDGs. We mention here a few references that are relevant to our paper. The papers Buckdahn_SICON_2008 ; Li_AMO_2015 considered the class of games where the state and the objective functional are described by coupled forward-backward stochastic differential equations (SDEs). They used the so-called backward semigroup associated with the backward SDE to obtain DPPs and the viscosity solution property of the HJI equations. ZSDGs with unbounded controls were considered in Qui_ESIAM_2013 . The weak formulation of ZSDGs and the mean field framework of ZSDGs were studied in Pham_SICON_2014 ; Li_MIn_SICON_2016 ; Djehiche_AMO_2018 ; Averboukh_DGAA_2018 , where in Pham_SICON_2014 path-dependent HJI equations and their viscosity solutions were considered. Reference Averboukh_DGAA_2018 used the feedback approach to construct a suboptimal solution and prove the existence of the value function. (Deterministic and stochastic) linear-quadratic ZSDGs with Riccati equations were studied in Zhang_SICON_2005 ; Delfour_SICON_2007 ; YU_SICON_2015 ; Sun_SICON_2016 ; Moon_TAC_2019_Markov and the references therein. Maximum principles for risk-sensitive ZSDGs were established in Moon_TAC_Risk_2019 , and for nonzero-sum DGs in 5446378 .

There are numerous applications of ZSDGs. Pursuit-evasion games and their applications to characterization of reachable sets for dynamical systems were considered in Basar_Zaccour_book ; Buckdahn_Cardaliaguet_DGAA_2011 ; Mitchell_TAC_2005 ; Margellos_TAC_2011 . Optimal resource allocation, distributed control problems and their applications can also be considered within the framework of ZSDGs Yong_Book_2015 ; Basar_Zaccour_book . For particular applications of ZSDGs considered in this paper, see the discussion in Examples 2.1-2.3 of Section 2.2.

We should note that for the (lower and upper) value functions of ZSDGs and the associated HJI equations studied in Bardi_book_1997 ; Evans_1984 ; Fleming_1989 ; Buckdahn_SICON_2008 ; Li_AMO_2015 ; Qui_ESIAM_2013 ; Pham_SICON_2014 , the state space is the standard finite-dimensional space. In our formulation, however, the random initial condition and the law of the state process affect the dynamical system, and the objective functional includes the state process’s distribution as well as the random target variable. Hence, unlike Bardi_book_1997 ; Evans_1984 ; Fleming_1989 ; Buckdahn_SICON_2008 ; Li_AMO_2015 ; Qui_ESIAM_2013 ; Pham_SICON_2014 , in this paper the state arguments of the (lower and upper) value functions and the associated HJI equations belong to (the set of probability measures with finite second moments) and (the set of random variables with finite second moments) that are infinite-dimensional spaces. This inherent infinite-dimensional feature introduces a new technical challenge, which has not arisen in Bardi_book_1997 ; Evans_1984 ; Fleming_1989 ; Buckdahn_SICON_2008 ; Li_AMO_2015 ; Qui_ESIAM_2013 ; Pham_SICON_2014 . This is the challenge we tackle in this paper.111The ZSDG of the paper is closely related to mean field type games studied in Li_MIn_SICON_2016 ; Djehiche_AMO_2018 ; Averboukh_DGAA_2018 (see Example 2.1 in Section 2.2). However, Li_MIn_SICON_2016 ; Djehiche_AMO_2018 ; Averboukh_DGAA_2018 considered weak and open-loop formulations, where the DPPs, the HJI equations, and the viscosity solution property of the value functions naturally do not arise. The problem formulation, the approach used, and the main results of this paper are different from Li_MIn_SICON_2016 ; Djehiche_AMO_2018 ; Averboukh_DGAA_2018 .

The first main objective of the paper is to show that the (lower and upper) value functions defined on and , where is a fixed time horizon, are equivalent to each other. This leads to the law invariant property between the value functions on and , which were not considered in the finite-dimensional case in Bardi_book_1997 ; Evans_1984 ; Fleming_1989 ; Buckdahn_SICON_2008 ; Li_AMO_2015 ; Qui_ESIAM_2013 ; Pham_SICON_2014 . The (lower and upper) value functions on are called the lifted value functions. We also show that the (lower and upper) value functions on and their lifted version on are continuous. The proof of the continuity utilizes properties of the -Wasserstein metric and the flow (semigroup) property of the state distribution, which are not needed in the finite-dimensional cases studied in Bardi_book_1997 ; Evans_1984 ; Fleming_1989 ; Buckdahn_SICON_2008 ; Li_AMO_2015 ; Qui_ESIAM_2013 ; Pham_SICON_2014 ; Yong_book .

The second main objective of the paper is to establish lower and upper dynamic programming principles (DPPs) for the (lower and upper) value functions. This provides a recursive relationship of the (lower and upper) value function. Due to the law invariant property, the (lower and upper) DPPs on and the lifted (lower and upper) DPPs on are identical. For the proof, we need to consider the interaction between admissible control and nonanticipative strategies between the players.

The third main objective of the paper is to show that (lower and upper) value functions are viscosity solutions of the associated (lower and upper) Hamilton-Jacobi-Isaacs (HJI) equations that are first-order partial differential equations (PDEs) on and . Hence, unlike Bardi_book_1997 ; Evans_1984 ; Fleming_1989 ; Buckdahn_SICON_2008 ; Li_AMO_2015 ; Qui_ESIAM_2013 ; Pham_SICON_2014 , the HJI equations of this paper are infinite-dimensional. We use the notion of derivative of a function of probability measures in and its lifted version in with the associated chain rule introduced in Cardaliaguet ; Carmona_book_2018 to characterize the (lower and upper) HJI equations and the viscosity solution property of the (lower and upper) value functions. Furthermore, when the dynamics and running cost are independent of time, by constructing the test function and using the law invariant property, we prove the comparison principle of viscosity solutions, which leads to uniqueness of the viscosity solution. In addition, under the Isaacs condition, the lower and upper value functions coincide. This implies that the ZSDG has a value, which is further characterized by the viscosity solution of the HJI equation.

Finally, we provide numerical examples to illustrate the theoretical results of the paper. In particular, we observe that the value of ZSDGs considered in this paper is determined by the laws (distributions) of random initial and target variables, whereas the value of classical deterministic ZSDGs is obtained by explicit values of initial and target variables.

We note that different versions of the problem treated in this paper were considered earlier in Cardaliaguet_IGTR_2008 ; Cosso_JMPA_2018 . However, in Cardaliaguet_IGTR_2008 , the notion of nonanticipative strategies with delay was used, which is hard to implement in practical situations. Moreover, the objective functional does not have the running cost, and the state distribution and the random target variable were not considered in Cardaliaguet_IGTR_2008 . The stochastic version of the problem of this paper was considered in Cosso_JMPA_2018 . However, the comparison principle and therefore the uniqueness of viscosity solutions were not shown. Hence, there is no guarantee that the solution of the corresponding HJI equations characterizes the value function in Cosso_JMPA_2018 . In summary, the problem formulation, the approach used, and the main results of this paper are different from those of Cardaliaguet_IGTR_2008 ; Cosso_JMPA_2018 .

The rest of the paper is organized as follows. Notations including the notion of derivative in and its lifted version in , and the problem formulation are provided in Section 2. The DPPs and the properties of the (lower and upper) value functions are given in Section 3. The (lower and upper) HJI equations and their viscosity solutions (including existence and uniqueness) are given in Section 4. Numerical examples are provided in Section 5. Several potential future research problems are discussed in Section 6. Five appendices include proofs of the main results.

2 Problem Statement

In this section, we first describe the notation used in the paper, along with some notions and properties. The precise problem formulation then follows.

2.1 Notation

The -dimensional Euclidean space is denoted by , and the transpose of a vector by . The inner product of is denoted by , and the Euclidean norm of by .

Let be the set of all real-valued continuous functions defined on . Let be the set of real-valued functions defined on such that for , (the partial derivative of with respect to ) and (the partial derivatives of with respect to ) are continuous and bounded. Let and be Banach spaces with the norms and , respectively. A function is Frechet differentiable at (Luenberger_book, , page 172) if there exists a bounded linear operator such that .

Let be a complete probability space, and be the expectation operator with respect to . We denote by the distribution (or law) of a random variable . Let be the expectation for which the underlying distribution (or law) is . Let be the set of -valued random vectors such that for , . is a Hilbert space, with inner product and norm denoted by and , respectively Luenberger_book ; Conway_2000_book .

Let be the set of probability measures on , and be the set of probability measures with finite -th moment, , i.e., for any with , we have . We note that if and only if . For with the associated law , we can write . The -Wasserstein metric is defined by (see (Rachev, , page 40) and (Villani_book, , Chapter 6)):

where , and is the collection of all probability measures on with marginals and , i.e. and for any Borel sets Rachev . Note that can equivalently be written as (Villani_book, , Chapter 6)

One can easily show that is a metric; hence, endowed with , , is a metric space. For , let be the set of square-integrable functions with respect to .

We next provide the notion of derivative in , and its lifted derivative in , which are introduced in Cardaliaguet ; Carmona_book_2018 . Let , which implies . Let . We introduce the lifted (extended) version of , , that is, for (note that ), . While is a function of the random variable, is a function of the distribution (law) of . We say that is differentiable at , if its lifted version is Frechet differentiable at . Let be the corresponding Frechet derivative. Then is a bounded linear functional. Since is a Hilbert space and its dual space is , in view of Riesz representation theorem (Conway_2000_book, , Theorem 3.4), for any , there is a unique such that . This implies that the Frechet derivative can be viewed as an element of . In view of (Cardaliaguet, , Theorem 6.2), does not depend on , but depends on the law (distribution) of . Also, from (Cardaliaguet, , Theorem 6.5), there exists a function with such that is a derivative of in , which can be represented as . Finally, consider the dynamical system with . Let be the state distribution (or law) of the dynamical system. Let . From the notion of derivative in , the chain rule in is . Note that for the lifted chain rule in with , we have .

2.2 Problem Formulation

Consider the dynamical system on with the initial time :

| (1) |

where is the state with the random initial condition having the law , is the control of Player 1, and is the control of Player 2. We assume that and are compact. The set of admissible controls for Player 1, , is defined such that for , is a measurable function. The set of admissible controls for Player 2, , is defined in a similarly way. Let and . In (1), denotes the law (equivalently distribution) of the dynamical system at time that is dependent on the law of the initial condition (see Remark A.1 in Appendix A), as well as and . We introduce the following assumption:

-

(H.1)

is bounded, where is continuous in for each , and satisfies the Lipschitz condition: for , , , and and for , it holds that .

Then, for , (1) admits a unique solution on Rene_anals_2015 ; Jourdain_2008 .

Let with the law , which is independent of . Here, is the target variable in the objective functional (see (2) and Remark 2.1). Let with the law given by . The objective functional for the two-player ZSDG of this paper is then given by

| (2) | ||||

where is cost to Player 1 (minimizer) and payoff to Player 2 (maximizer). The notation in the first line of (2) indicates that is defined on , whereas the notation in the second line of (2) stands for as a functional on , and the two are equivalent because of the correspondence between and discussed in Section 2.1. Let . We have the following assumption:

-

(H.2)

is bounded, where is continuous in for each and satisfies the Lipschitz condition: for , , , and and for , it holds that . Also, is bounded, which is Lipschitz continuous in with Lipschitz constant .

Remark 2.1.

The random variable included in the terminal cost of (2) is called the target variable, which captures the constraint of the state process at the terminal time. Specifically, given , can be used such that the distance between the law of the state process and the target distribution (the law of ) can be optimized via the control processes and .

We next introduce the notion of nonanticipative strategies for Player 1 and Player 2; see also Bardi_book_1997 ; Evans_1984 ; Fleming_1989 ; Buckdahn_SICON_2008 ; YU_SICON_2015 .

Definition 2.1.

A strategy for Player 1 is a mapping . A strategy for Player 1 is nonanticipative if for any , and , for implies that for , this being true for each . The set of nonanticipative strategies for Player 1 on is denoted by . Let . A strategy for Player 2 is a measurable mapping . A nonanticipative strategy for Player 2 is defined in a similar way as Player 1’s. The set of nonanticipative strategies for Player 2 on is denoted by . Let .

Using Definition 2.1, for and , the lower value function for (2) is defined by with

| (3) |

and the upper value function is defined by with

| (4) |

Note that . Unlike the deterministic case, (3) and (4) are parametrized by the initial time, the initial distribution (law) of (1), and the target distribution in (2).

For and , define the lifted lower value function, with

| (5) |

and the lifted upper value function, with

| (6) |

Note that . As mentioned in Section 2.1, the lifted value functions depend on only the law of .222The value functions and their lifted versions are defined based on the notation in (2). Note that the value functions and their corresponding lifted versions are deterministic and identical, where the detailed proof of the latter is given in Lemma 3.1. As stated in Section 2.1 and Cardaliaguet ; Carmona_book_2018 , the motivation for introducing the lifted value functions on is to utilize the notion of derivative in , which allows us to characterize the explicit derivative of the (inverse-lifted) value function on . Note that is a Hilbert space, but with the Wasserstein metric is not.

Remark 2.2.

Unlike ZSDGs in Bardi_book_1997 ; Evans_1984 ; Fleming_1989 ; Buckdahn_SICON_2008 ; Li_AMO_2015 ; Qui_ESIAM_2013 ; Pham_SICON_2014 , the lower and upper value functions in (3)-(6) are defined on infinite-dimensional spaces and .

Before concluding this section, we provide a few examples of ZSDGs that fit into the framework laid out above.

Example 2.1.

The state dynamics in (1) can be regarded as a McKean-Vlasov dynamics, where the evolution of the state process depends on its distribution. This is closely related to mean-field games and mean-field type control, which have been studied extensively in the literature, particularly, for reducing variation of random effects on the controlled process and macroscopic analysis of large-scale interacting multi-agent systems Lasry ; Carmona_book_2018 ; Andersson_AMO_2010 ; 7047683 ; Cardaliaguet ; Rene_SICON_2013 ; Yong_SICON_2013_MF ; Bensoussan_Arxiv_2014 ; Rene_anals_2015 ; Cardaliaguet_MFE_2018 ; Djehiche_AMO_2018 ; Averboukh_DGAA_2018 ; Moon_DGAA_2019 . For example, we may take , and to optimize the objective functional under the mean-field effect. Notice that if and , then what we have is a class of mean-variance optimization problems.

Example 2.2.

In statistical learning theory and its applications, we often need to optimize the worst-case empirical criterion (or risk) Goodfellow_book . Specifically, assume that , , is an i.i.d. random pair sampled according to . Consider

Note that we have almost surely in view of the law of large numbers, which, together with (H.1) and (H.2) implies that . Hence, from the minimization point of view, the class of ZSDGs of this paper can be viewed as worst-case empirical optimization when the sample size is arbitrarily large.

Example 2.3.

Consider the two adversarial vehicles model:

where is the random initial condition, is the random target variable, are constants of the two vehicles and are velocities of the two vehicles Mitchell_TAC_2005 . When specialized to this setting, the class of ZSDGs in this paper can be seen as a pursuit-evasion game of two vehicles with random initial and target pair. Its deterministic version with different settings and applications to characterization of reachable sets were studied in Buckdahn_Cardaliaguet_DGAA_2011 ; Basar_Zaccour_book ; Mitchell_TAC_2005 ; Margellos_TAC_2011 , and the references therein.

3 Dynamic Programming Principles

In this section, we obtain the dynamic programming principles (DPPs) for the lower and upper value functions.

We first provide some properties of the value functions. The following lemma shows that the value functions are law invariant. The proof can be found in Appendix A.

Lemma 3.1.

Suppose that (H.1) and (H.2) hold. Then we have and for any with the law of being , i.e., .

The next lemma shows the continuity of the value functions. The proof is provided in Appendix A.

Lemma 3.2.

We now obtain in the following theorem the DPPs, whose proof is given in Appendix B.

Theorem 3.1.

Suppose that (H.1) and (H.2) hold. Then for any with and with , the lifted lower and upper value functions in (5) and (6), respectively, satisfy the following DPPs:

| (7) | ||||

| (8) | ||||

Equivalently, for any with the law and with , the lower and upper value functions in (3) and (4), respectively, satisfy the following DPPs:

| (9) | ||||

| (10) | ||||

4 HJI Equations and Viscosity Solutions

In this section, we address the issue of the lower and upper value functions being unique viscosity solutions of the associated Hamilton-Jacobi-Isaacs (HJI) equations, which are first-order partial differential equations defined on infinite-dimensional spaces, particularly and .

The lower HJI equation on is given by

| (11) |

and the upper HJI equation on is as follows:

| (12) |

where are the Hamiltonians:

| (13) | ||||

Viscosity solutions to (11) and (12) are defined as follows; see also Crandall_Lions_1983 ; Buckdahn_SICON_2008 ; Bardi_book_1997 ; Fleming_1989 ; Evans_1984 ; Li_AMO_2015 ; Yong_book and the references therein:

Definition 4.1.

-

(i)

A real-valued function is said to be a viscosity subsolution (resp. supersolution) of the lower HJI equation in (11) if (resp. ) for , and if further for all test functions and , the following inequality holds at the local maximum (resp. local minimum) point of :

- (ii)

The following theorem, whose proof is given in Appendix C, now establishes the viscosity solution property of the value functions in (3) and (4).

Theorem 4.1.

With the lifted value functions, the lifted lower and upper HJI equations are given by

| (14) | ||||

| (15) |

where are the (lifted) Hamiltonians defined by

| (16) | ||||

See Section 2.1 for the notion of derivative in and its relationship with the derivative in . As stated in Section 2.2, from the definition of the value functions (5) and (6), the lifted HJI equations (14) and (15) are dependent on the law of .

Remark 4.1.

- (i)

- (ii)

We have the following result, whose proof is similar to that of Theorem 4.1.

Proposition 4.1.

Next, we state the comparison results of the viscosity solutions in Theorem 4.1 and Proposition 4.1, with the proofs relegated to Appendix D. We need the following assumption:

-

(H.3)

and are independent of .

Theorem 4.2.

Assume that (H.1)-(H.3) hold. Then:

- (i)

- (ii)

Corollary 4.1.

Suppose that (H.1) and (H.2) hold, and that the (lower and upper) value functions are bounded. Then, the lower (resp. upper) value function in (3) (resp. (4)) is the unique viscosity solution to the lower (resp. upper) HJI equation in (11) (resp. (12)). Also, the lifted lower (resp. upper) value function in (5) (resp. (6)) is the unique viscosity solution to the lifted lower (resp. upper) HJI equation in (14) (resp. (15)).

Remark 4.2.

To proceed further, we now introduce the Isaacs conditions:

| (19) |

Note that due to the law invariant property, the conditions in (19) are equivalent. Then under the Isaacs condition, we have the following result, whose proof can be found in Appendix E.

Corollary 4.2.

5 Numerical Examples

This section provides two numerical examples. For the HJI equations in Section 4, assume that , , and . Also, , , and and are independent Gaussian random variables with mean zero and variance one (equivalently, and are Gaussian measures). Note that the target variable is included in the terminal cost . The ZSDG formulated in this section can be regarded as a class of mean-field type control (Example 2.1) and pursuit-evasion games (Example 2.3). Due to the random initial and target variables, and the dependence of and on , the problem cannot be solved using the existing theory for ZSDGs.

Note that (H.1)-(H.3) hold. Since the corresponding Hamiltonian is separable in and , the Isaacs condition in (19) holds. Hence, from Corollary 4.2, the ZSDG has a value that can be characterized by solving the following HJI partial differential equation (PDE) in (14) and (15)333It is the lifted HJI equations in (14) and (15) when . From the definitions of and , the PDE is obtained after carrying out the maximization with respect to and the minimization with respect to .:

Moreover, from (11) and (12), the HJI PDE above is equivalent to444It is the HJI equations in (11) and (12) when .

where is the Gaussian probability density function. Here, we have utilized the fact that for any mean zero and variance one Gaussian random variable with the law , and . We can easily see that is the unique solution to the above PDE, which is the value of the ZSDG. This shows that the value of the ZSDG of this example is zero, which is determined by the laws (distributions) of random initial and target variables. Note that, in this example, the game value is independent of explicit values of initial and target variables.

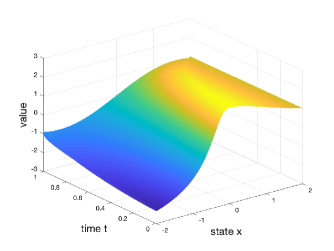

For the second example, with the same , and as in the first example, assume now that and are Dirac measures. Then the associated ZSDG is reduced to the classical deterministic ZSDGs studied in Bardi_book_1997 ; Evans_1984 ; Basar2 , where the state argument of the value function is in . The HJI equation then becomes

Its solution is depicted in Fig. 1 when , which is defined on . In this example, we have used the finite-difference method to approximate the viscosity solution Crandall_Lions_MC_1984 .

As seen from the two examples above and the results in the previous sections, the value of the class of ZSDGs considered in this paper depends on the laws (distributions) of random initial and target variables, whereas the values of the classical deterministic ZSDGs are determined by explicit values of initial and target variables.

6 Concluding Remarks

We have studied, in this paper, a class of two-player zero-sum differential games, where the dynamical system depends on the random initial condition and the distribution of the state process, and the objective functional includes the latter as well as a random target variable. The (lower and upper) value functions are defined on two infinite-dimensional spaces, and , which satisfy the dynamic programming principles. By using the notion of derivative in and its lifted version in , the (lower and upper) value functions are shown to be unique (continuous) viscosity solutions to associated (lower and upper) HJI equations that are first-order PDEs on infinite-dimensional spaces. Under the Isaacs condition, the lower and upper value functions are identical, which implies that the ZSDG has a value.

One possible future research topic would be to study the stochastic framework of ZSDGs in this paper as an extension of Cosso_JMPA_2018 , in which there is an additive Brownian noise in (1) and the corresponding diffusion term depends on the state, the law of the state process, and the control variables. This requires the notion of the second-order derivative in and its lifted version in to obtain DPPs, second-order HJI equations, and their viscosity solutions. Another direction would be the risk-sensitive ZSDGs. The problem of characterization of reachable sets, which can be viewed as an application of ZSDGs in this paper (see Example 2.3), would also be an interesting avenue to pursue. In this case, the major challenge would be to solve the HJI equation numerically in the infinite-dimensional space. Finally, the extension of the rational expectations models considered in Basar_Rational_1989 to the continuous-time framework is an interesting problem to study.

Appendix A Proof of Lemmas 3.1 and 3.2

Remark A.1.

-

(i)

For (1), let be the initial condition of (1) at the initial time . Assume that is distributed according to . Then the law of the state process is denoted by for . Then we can easily show that satisfies

(A.1) for any , and . That is, the law of the state process (A.1) satisfies the semigroup or flow property.

-

(ii)

We use the notation , , with to emphasize the initial condition and the initial time.

Proof of Lemma 3.1.

We prove (i) only, since the proof of (ii) is similar to that of (i). Consider the two initial pairs of random vectors having the same law (distribution), i.e., . Since the objective functional in (2) does not depend on the random variables, but depends on the law of the initial random pair, we have for and . This, together with the fact that and are not dependent on the law of the initial random pair, implies that for and . Then, from the definitions in (3) and (5), we have the desired result. ∎

Proof of Lemma 3.2.

We prove here the continuity of only the lower value functions ( and ), since the proof for the upper value functions ( and ) follows along similar lines. In the proof below, a constant can vary from line to line, which depends on the Lipschitz constant ((H.1) and (H.2)).

Let be the initial and target pair having the distribution (law) . We apply a similar argument to the notation and for . Let , with . Then by using (H.1), Gronwall’s lemma, and the fact that and (Villani_book, , Chapter 6), we have

| (A.2) |

In view of the definition of the Wasserstein metric, Hölder inequality, and the definition of the norm , the preceding estimates in (A.2) imply that

| (A.3) | ||||

where the inequality follows from (A.2). Moreover, we have

| (A.4) | ||||

where the inequality follows from (A.2), the definition of the -Wasserstein metric, and Hölder’s inequality. Then using (A.1), (A.4) and (A.3), together with the distance property of , we have

| (A.5) | ||||

Furthermore, with the estimates in (A.2), and (H.1) and (H.2), for any , and , we have for and ,

| (A.6) | ||||

| (A.7) | ||||

The convergence in implies convergence in with respect to , i.e., as implies as (Villani_book, , Theorem 6.9). Also, and . Then, from (A.6) and (A.7), and the definition of , we can easily see that is continuous in .

For the continuity of , we consider the following equivalent notation of the objective functional in terms of :

Then, with (H.1), (H.2), (A.2) and (A.5), we apply the definition of the Wasserstein metric and (Cardaliaguet_IGTR_2008, , Lemma 3) to show that

| (A.8) |

Note that (A.6) and (A.8) imply that is continuous in for any and . Then, by following the proof for the continuity of , we can show that is continuous in . This completes the proof. ∎

Appendix B Proof of Theorem 3.1

We prove (9) only, since the proofs for (7), (8) and (10) are similar to that for (9). Let with . For any , let

We need to show that .

For any , there exists such that

| (B.1) | ||||

Similarly, in view of the definition of the value function, for any , there exists such that for any with ,

| (B.2) | ||||

Define such that for , on and on . Then, from (A.1), (B.1) and (B.2), we can show that

which implies

| (B.3) |

On the other hand, for any and , there exists such that

| (B.4) | ||||

and by restricting to , we have

| (B.5) | ||||

The inequality in (B.5) implies that for each , there exists such that

| (B.6) | ||||

Similarly, for any , there exists such that for any with

| (B.7) | ||||

We define such that on and on . Consider with , i.e., on and on . Then, from (A.1), (B.6) and (B.7),

This, together with (B.4), implies that

| (B.8) |

Since was arbitrary, in view of (B.3) and (B.8), ; hence, we have the desired result.

Appendix C Proof of Theorem 4.1

In view of Lemma 3.2, . We now prove that the value function in (3) is a viscosity supersolution of (11). From the definition of the value function and (9) in Theorem 3.1, we have .

From the definition of the viscosity supersolution (Definition 4.1(i)), for any , for all with with some . Let and satisfying . Moreover, without loss of generality, we may assume .

Then in view of the DPP of (9) in Theorem 3.1,

and

| (C.1) | ||||

For and , , which implies that

Hence, with (C.1), we have

For each and small with , there exists such that for ,

We multiply the above expression by , and let and . Then, with the chain rule in in Section 2.1,

| (C.2) | ||||

which, together with (13), shows that is a viscosity supersolution to (11).

We now prove, by contradiction, that is a viscosity subsolution of (11). From the definition of the viscosity subsolution (Definition 4.1(i)), for any , for all with with some . Let , and satisfying . Moreover, without loss of generality, we may assume .

Let us assume that is not a viscosity subsolution of (11). Then, there exists a constant such that

Define . From (13), note that . Since and are (uniformly) continuous on , so is , which implies that there is a measurable function and such that for and ,

On the other hand, the DPP in (9) of Theorem 3.1 and the definition of the viscosity subsolution imply that

and by defining for , we have and

Then, for each , there exists such that

Multiplying the above expression by , and letting , together with the chain rule in in Section 2.1, yield

and by letting , we must have , which leads to a contradiction. This implies that

| (C.3) |

Hence, (C.2) and (C.3) taken together show that is a viscosity solution to (11). The proof of being a viscosity solution to (12) is similar. This completes the proof.

Appendix D Proof of Theorem 4.2

In the proof of Theorem 4.2, we need the following lemma, which follows from (H.1)-(H.3).

Lemma D.1.

Assume that (H.1)-(H.3) hold. Then, the following result holds: there is a constant , dependent on the Lipschitz constant, such that for any and , we have and .

The proof of Theorem 4.2 now proceeds as follows.

Proof of Theorem 4.2.

We first prove for . Note that both and are bounded by some constant . In the proof below, a constant can vary from line to line, depending on the bounds of and , and the Lipschitz constant in (H.1) and (H.2).

By a possible abuse of notation, we reverse the time by defining , where , . Then , . With the time reverse notation and Remark 4.1(ii) (see (Evans_Book, , Chapter 10)), for the lifted HJI equations, the inequality in Definition 4.1 has to be modified by

| (D.1) |

For , define

where . We can see that is continuous on , where is a Hilbert space and its dual space is Luenberger_book ; Conway_2000_book . For and , i.e., , let us define the linearly perturbed map of :

Then in view of Stegall’s theorem Stegall_1978 ; Fabian_NA_2007 and Riesz representation theorem Conway_2000_book , there exist such that , , , with , and has a maximum at a point .555In fact, is continuous, coercive and ; hence, in view of Fabian_NA_2007 , admits a minimum, i.e., admits a maximum. This implies that

which, together with Cauchy-Schwarz inequality and the fact that for , implies (note that and are bounded)

We apply the quadratic analysis to the above inequality. Then

| (D.2) | ||||

| (D.3) |

We show that either or by contradiction. Assume that for . By defining

we have , which admits a maximum at . Note that is the viscosity subsolution and is independent of (see (H.3)). This, together with (D.1), implies

| (D.4) |

The inequality is reversed due to the time reverse notation. Similarly, we have , where

which admits a maximum at , i.e., admits a minimum at . Then, from (D.1), we have

| (D.5) |

From (H.1)-(H.3), (D.2), (D.3), and Lemma D.1,

First, let and then and . Then, we can easily get a contradiction, since . This shows that we can select small positive , and such that either or .

Let us assume that . Then, the maximum property of and its definition yield

which implies

| (D.6) | ||||

Since and , we have

| (D.7) |

where the inequality follows from the Lipschitz property and (D.3). On the other hand, in view of (D.2) and Cauchy-Schwarz inequality,

| (D.8) | ||||

| (D.9) |

By first letting , and then and in (D.7)-(D.9), from (D.6) and the definition of , we have

which leads to the desired result in (18). Then for in (17) follows from Lemma 3.1. The proofs for in (18) and in (17) are similar. This completes the proof. ∎

Appendix E Proof of Corollaries 4.1 and 4.2

Proof of Corollary 4.1.

Suppose that and are value functions that are viscosity solutions to (14). In view of (18) in Theorem 4.2, Lemma 3.2, and the definition of the viscosity solution, we have and , which implies that . By Proposition 4.1, is the corresponding lifted lower value function. The proof of the remaining part is similar. This completes the proof. ∎

Proof of Corollary 4.2.

Set in (11) and (12), and in (14) and (15). Then, (11) and (12) become identical HJI equations, and so do (14) and (15). From Lemmas 3.1 and 3.2, Proposition 4.1 and Theorem 4.1, together with the uniqueness result in Corollary 4.1, we have for and , which is the value of the ZSDG and is the unique solution to the HJI equation. This completes the proof. ∎

References

- (1) T. Başar and G. J. Olsder, Dynamic Noncooperative Game Theory, 2nd ed. SIAM, 1999.

- (2) M. Bardi and I. Capuzzo-Dolcetta, Optimal Control and Viscosity Solustions of Hamilton-Jabobi-Bellman Equations. Birkhäuser, 1997.

- (3) A. Bensoussan, G. Da Prato, M. C. Delfour, and S. Mitter, Representation and Control of Infinite Dimensional Systems, 2nd ed. Birkhauser, 2007.

- (4) R. Buckdahn, P. Cardaliaguet, and M. Quincampoix, “Some recent aspects of differential game theory,” Dynamic Games and Applications, vol. 1, pp. 74–114, 2011.

- (5) T. Başar and G. Zaccour, Eds., Handbook of Dynamic Game Theory, Volumes I and II. Springer, 2018.

- (6) R. Isaacs, Differential Games. Dover Publications, 1965.

- (7) R. J. Elliott and N. J. Kalton, Existence of value in differential games. Memoirs of the Ametican Mathematical Society, 1972, vol. 126.

- (8) L. C. Evans and P. E. Souganidis, “Differential games and representation formulas for solutions of Hamilton-Jabobi-Isaacs equations,” Indiana Univ. Math. J, vol. 33, pp. 293–314, 1984.

- (9) W. H. Fleming and P. E. Souganidis, “On the existence of value functions of two-player zero-sum stochastic differential games,” Indiana Univ. Math. J, vol. 38, pp. 293–314, 1989.

- (10) A. Friedman, “Existence of value and of saddle points for differential games of pursuit and evasion,” Journal of Differential Equations, vol. 7, pp. 92–110, 1970.

- (11) M. K. Ghosh and A. J. Shaiju, “Existence of value and saddle point ininfinite-dimensional differential games,” Journal of Optimization Theory and Applications, vol. 121, no. 2, pp. 301–325, 2004.

- (12) R. Buckdahn and J. Li, “Stochastic differential games and viscosity solutions of Hamilton-Jabobi-Bellman-Isaacs equations,” SIAM Journal on Control and Optimization, vol. 47, no. 4, pp. 444–475, 2008.

- (13) J. Li and Q. Wei, “Stochastic differential games for fully coupled FBSDEs with jumps,” Applied Mathematics and Optimization, vol. 71, pp. 411–448, 2015.

- (14) H. Qui and J. Yong, “Hamilton-Jacobi equations and two-person zero-sum differential games with unbounded controls,” ESIAM: Control, Optimization and Calculus of Variations, vol. 19, pp. 404–437, 2013.

- (15) T. Pham and J. Zhang, “Two-person zero-sum game in weak formulation and path dependent Bellman-Isaacs Equation,” SIAM Journal on Control and Optimization, vol. 52, no. 4, pp. 2090–2121, 2014.

- (16) J. Li and H. Min, “Weak solutions of mean field stochastic differential equations and applications to zero-sum stochastic differential games.” SIAM Journal on Control and Optimization, vol. 54, no. 3, pp. 1826–1858, 2016.

- (17) B. Djehiche and S. Hamadene, “Optimal control and zero-sum stochastic differential game problems of mean-field type,” Applied Mathematics and Optimization, pp. 1–28, 2016.

- (18) Y. Averboukh, “Krasovskii-Subbotin approach to mean field type differential games,” Dynamic Games and Applications, pp. 1–21, 2018, https://doi.org/10.1007/s13235-018-0282-6.

- (19) P. Zhang, “Some results on two-person zero-sum linear quadratic differential games,” SIAM Journal on Control and Optimization, vol. 43, no. 6, pp. 2157–2165, 2005.

- (20) M. C. Delfour, “Linear quadratic differential games: Saddle point and Riccati differential equations,” SIAM Journal on Control and Optimization, vol. 46, no. 2, pp. 750–774, 2007.

- (21) Z. Yu, “An optimal feedback control-strategy pair for zero-sum linear-quadratic stochastic differential game: the Riccati equation approach,” SIAM Journal on Control and Optimization, vol. 53, no. 4, pp. 2141–2167, 2015.

- (22) J. Sun, X. Li, and J. Yong, “Open-loop and closed-loop solvability for stochastic linear quadratic optimal control problems,” SIAM Journal on Control and Optimization, vol. 54, no. 5, pp. 2274–2308, 2016.

- (23) J. Moon, “A sufficient condition for linear-quadratic stochastic zero-sum differential games for Markov jump systems,” IEEE Transactions on Automatic Control, vol. 64, no. 4, pp. 1619–1626, 2019.

- (24) J. Moon, T. Duncan, and T. Başar, “Risk-sensitive zero-sum differential games,” IEEE Transactions on Automatic Control, vol. 64, no. 4, pp. 1503–1518, 2019.

- (25) G. Wang and Z. Yu, “A Pontryagin’s maximum principle for non-zero sum differential games of BSDEs with applications,” IEEE Transactions on Automatic Control, vol. 55, no. 7, pp. 1742–1747, 2010.

- (26) I. M. Mitchell, A. M. Bayen, and C. J. Tomlin, “A time-dependent Hamilton-Jacobi formulation of reachable sets for continuous dynamic games,” IEEE Transactions on Automatic Control, vol. 50, no. 7, pp. 947–957, 2005.

- (27) K. Margellos and J. Lygeros, “Hamilton-Jacobi formulation for reach-avoid differential games,” IEEE Transactions on Automatic Control, vol. 56, no. 8, pp. 1849–1861, 2011.

- (28) J. Yong, Differential Games: A Concise Introduction. World Scientific, 2015.

- (29) J. Yong and X. Y. Zhou, Stochastic Controls: Hamiltonian Systems and HJB Equations. Springer, 1999.

- (30) P. Cardaliaguet, “Notes on mean field games,” Jan 2012, Technical Report.

- (31) R. Carmona and F. Delarue, Probabilistic Theory of Mean Field Games with Applications I. Springer, 2018.

- (32) P. Cardaliaguet and M. Quincampoix, “Deterministic differential games under probability knowledge of initial condition,” International Game Theory Review, vol. 10, no. 1, pp. 1–16, 2008.

- (33) A. Cosso and H. Pham, “Zero-sum stochastic differential games of generalized McKean-Vlasov type,” Journal de Mathématiques Pures et Appliquées, vol. 129, pp. 180–212, 2018.

- (34) D. G. Luenberger, Optimization by Vector Space Methods. John Wiley & Sons, 1969.

- (35) J. B. Conway, A Course in Functional Analysis. Springer, 2000.

- (36) S. T. Rachev and L. Ruschendorf, Mass Transportation Theory: Volume I: Theory. Springer, 1998.

- (37) C. Villani, Optimal Transport. Springer, 2009.

- (38) R. Carmona and F. Delarue, “Forward-backward stochastic differential equations and controlled McKean-Vlasov dynamics,” The Annals of Probability, vol. 43, no. 5, pp. 2647–2700, 2015.

- (39) B. Jourdain, S. Meleard, and W. Woyczynski, “Nonlinear SDEs driven by Levy processes and related PDEs,” ALEA, Latin American Journal of Probability, vol. 4, pp. 1–29, 2008.

- (40) J. M. Lasry and P. L. Lions, “Mean field games,” Jap. J. Math., vol. 2, no. 1, pp. 229–260, 2007.

- (41) D. Andersson and B. Djehiche, “A maximum principle for SDEs of mean-field type,” Applied Mathematics and Optimization, vol. 63, no. 3, pp. 341–356, 2010.

- (42) B. Djehiche, H. Tembine, and R. Tempone, “A stochastic maximum principle for risk-sensitive mean-field type control,” IEEE Transactions on Automatic Control, vol. 60, no. 10, pp. 2640–2649, 2015.

- (43) R. Carmona and F. Delarue, “Probabilistic analysis of mean-field games,” SIAM Journal on Control and Optimization, vol. 51, no. 4, pp. 2705–2734, 2013.

- (44) J. Yong, “Linear-quadratic optimal control problems for mean-field stochastic differential equations,” SIAM Journal on Control and Optimization, vol. 51, no. 4, pp. 2809–2838, 2013.

- (45) A. Bensoussan, K. C. J. Sung, S. C. P. Yam, and C. P. Yung, “Linear-quadratic mean field games,” 2014, https://arxiv.org/abs/1404.5741.

- (46) P. Cardaliaguet and C. A. Lehalle, “Mean field game of controls and an application to trade crowding,” Mathematics and Financial Economics, vol. 12, no. 3, pp. 335–363, 2018.

- (47) J. Moon and T. Başar, “Risk-sensitive mean field games via the stochastic maximum principle,” Dynamic Games and Applications, vol. 9, pp. 1100–1125, 2019.

- (48) I. Goodfellow, Y. Bengio, and A. Courville, Deep Learning. MIT Press, 2016.

- (49) M. G. Crandall and P.-L. Lions, “Viscosity solutions of Hamilton-Jacobi equations,” Transactions on American Mathematical Society, vol. 277, no. 1, pp. 1–42, 1983.

- (50) ——, “Two approximations of solutions of Hamilton-Jacobi equations,” Mathematics of Computation, vol. 43, no. 167, pp. 1–19, 1984.

- (51) T. Başar, “Some thoughts on rational expectations model, and alternative formulations,” Computers and Mathematics with Applications, vol. 18, no. 6/7, pp. 591–604, 1989.

- (52) L. C. Evans, Partial Differential Equations, 2nd ed. American Mathematical Society, 2010.

- (53) C. Stegall, “Optimization of functions on certain subsets of Banach spaces,” Mathematische Annalen, vol. 236, no. 2, pp. 171–176, 1978.

- (54) M. Fabian and C. Finet, “On Stegall’s smooth variational principle,” Nonlinear Analysis, vol. 66, p. 5, 2007.