April2018-BookCh-LPCopula

Nonparametric Universal Copula Modeling

Subhadeep Mukhopadhyay and Emanuel Parzen222 Shortly after finishing the first draft of this paper, Manny Parzen passed away. Deceased February 6, 2016.

Final Version

Abstract

To handle the ubiquitous problem of “dependence learning,” copulas are quickly becoming a pervasive tool across a wide range of data-driven disciplines encompassing neuroscience, finance, econometrics, genomics, social science, machine learning, healthcare and many more. At the same time, despite their practical value, the empirical methods of ‘learning copula from data’ have been unsystematic with full of case-specific recipes. Taking inspiration from modern LP-nonparametrics (Parzen and Mukhopadhyay, 2013a, b, Mukhopadhyay and Parzen, 2014, 2018, Mukhopadhyay, 2017, 2016), this paper presents a modest contribution to the need for a more unified and structured approach of copula modeling that is simultaneously valid for arbitrary combinations of continuous and discrete variables.

Keywords: Copula statistical learning, Unified nonparametric algorithm, Automated learning, Mixed data algorithm, Exploratory dependence modeling, LP transformation, Spectral expansion, Nonlinear dependence measure, Bernoulli copula paradox.

Notation Index

The following summarizes the most commonly used notation of this paper

| Symbol | Description |

|---|---|

| pair of random variables (RVs) | |

| cumulative distribution function (cdf) of | |

| mid-distribution function of | |

| quantile function of | |

| probability mass function (pmf) for discrete | |

| probability density function (pdf) for continuous | |

| joint cdf of | |

| copula cdf | |

| copula density function | |

| conditional comparison density of and | |

| th LP-comean | |

| The empirical cdf and mid-distribution function | |

| , | Expectation of with respect to and |

1 The Ubiquitous Learning Problem

How can investors estimate Value-at-Risk (VaR) of a portfolio (Embrechts et al., 2002)? How can financial firms assess the joint default probability of groups of risky assets (Frey et al., 2001)? How can econometricians study the interdependence between family insurance arrangements and health care demand (Trivedi et al., 2007)? How can neuroscientists delineate the dependence structure among neurons in the brain (Berkes et al., 2009)? How can actuary professionals describe the joint distribution of indemnity payments and loss expenses to calculate the premia (Frees and Valdez, 1998)? How can marketing managers figure out the association between duration of website visits and transaction data to combat low conversion rates (Danaher and Smith, 2011)? How can environmental engineers model the dependence structure between hydrologic and climatic variables (AghaKouchak, 2014)? As it turns out, the key statistical challenge to all of these applied multivariate problems lies in developing a method of copula density estimation that is simultaneously valid for mixed multivariate data. By ‘mixed,’ we mean any combination of discrete, continuous, or even ordinal categorical variables. Keeping this end goal in mind, we offer a ‘one-stop’ unifying interface for nonparametric copula modeling.

2 After 60 Years, Where Do We Stand Now?

Copula (or connection) functions were introduced in 1959 by Abe Sklar in response to a query of Maurice Fréchet. For a pair of random variables and , Sklar’s theorem states that every joint distribution can be represented as

| (2.1) |

where is defined as the joint cumulative distribution function with uniform marginals. For and both continuous (or discrete), Sklar’s copula representation theorem further enables us to decompose the joint density into a product of their marginals times copula density:

| (2.2) |

Some immediate remarks on copula density function :

-

•

Copula density can be interpreted as the “correction factor” to convert the independence pdf into the joint pdf. Hence, it acts as the building block of dependence learning.

-

•

When and are jointly continuous (or discrete), Copula density can also be expressed as , where the dependence function dep, pioneered by Hoeffding (1940), is defined as the joint density divided by the product of the marginal densities. A definition of for general mixed (X,Y) case will be discussed in Section 4.1.

-

•

From the statistical modeling perspective, copulas allow us to decouple and separately model the marginal distributions from the dependence structure.

For a detailed account of the theoretical properties and probabilistic interpretations of copulas, see the monographs by Schweizer and Sklar (2011), Nelsen (2007) and Joe (2014). In this paper, we shall focus primarily on the statistical modeling principles for fitting copula to the data:

Given a bivariate sample how can we estimate the copula density function ?

Typically, the choice of an appropriate statistical estimation algorithm depends on the data-type information (e.g., discrete or continuous) of and :

-

•

both continuous: A wide variety of parametric copulas exist (Nelsen, 2007, Table 4.1) for jointly continuous margins. Among them, elliptical copulas (including Gaussian and Student-t families), the Archimedean class (including the Clayton, and Frank families), and the extreme-value copulas (including Gumbel and Galambos) are the most commonly used types. Given this bewilderingly large collection, practitioners often face stiff challenges when choosing an appropriate one for their empirical problem. In addition, these parametric classes of copula models are notoriously less flexible when it comes to capturing real-world complex dependency structures. As a remedy, several nonparametric kernel-based procedures have been developed in recent times; see, e.g., Gijbels and Mielniczuk (1990), Chen and Huang (2007) and Geenens et al. (2017).

-

•

both discrete: Copula estimation is far more challenging for discrete margins that include binary, ordinal categorical, and count data. Some promising parametric approaches are discussed in Panagiotelis et al. (2012) and Smith and Khaled (2012). On the other hand, the current state of nonparametric copula estimation for discrete marginals is really grim, and still an open issue; see for example Genest and Neslehova (2007), which warns practitioners against “naive” rank-based estimators. Quite surprisingly, however, the paper offers no practical solution for the problems. Section 7 will discuss these issues in details.

-

•

discrete, continuous: The mixed discrete and continuous case is probably the most challenging regime for copula modeling. Existing parametric attempts (Craiu and Sabeti, 2012, Marbac et al., 2017, Zilko and Kurowicka, 2016) are indirect and forceful. They are based on continuous latent variables, which capture only limited dependence structure, due to their strong reliance on latent Gaussian or parametric copula assumptions. And they are often, computationally, extremely costly. Whereas, perhaps not surprisingly, the nonparametric tools and methods are very much in their nascent stage; see e.g., Racine (2015) and Nagler (2018a), which struggle to extend kernel density estimates for mixed data by introducing quasi-inverse or by adding noise (jittering) merely to make the data forcibly continuous-like. Consequently, this class of randomized methods not only makes the computation clumsy but also introduces artificial variability, leading to potential irreproducible findings.

The Motivating Question. It is evident that current best practices are overly specialized and suffer from “narrow intelligence.” They are carefully constructed for each combination of data-type on a case-by-case basis. Thus, a natural question would be:

Instead of developing methods in a ‘compartmentalized’ manner for each data-type separately, can we construct a more organized and unified copula-learning algorithm that will work for any combination of ?

A solution to this puzzle can have two major impacts on theory and practice of copula modeling. First, it can radically simplify the practice by automating the model-building process. This auto-adaptable property of our nonparametric algorithm (which adapts to different varieties of data automatically) could be especially useful for constructing higher-dimensional copulas according to a sequence of trees (vine copula; Joe (1996)), by using bivariate copulas as building blocks. Second, it can provide, for the first time, a unified and holistic understanding of the ‘science’ behind copula learning. It is somewhat remarkable that this question has not been posed in the copula literature before. In the sequel, we introduce a modern formulation of this problem. Our theory is based on a new nonparametric representation technique to provide a systematic and automatic learning pipeline for copula density function.

3 A Taste of Next-Generation Copula Learning

Before going into the main theory, here we present a glimpse of where we are headed in our effort to develop a practical and flexible copula model, LPCopula(X,Y)—a model that is exceptionally simple to use, due to its ability to adapt automatically to the underlying data type. We feel this is vital to ensure the safety of the proposed technology in the hands of applied researchers who are not trained in the esoteric theory of nonparametric data science.

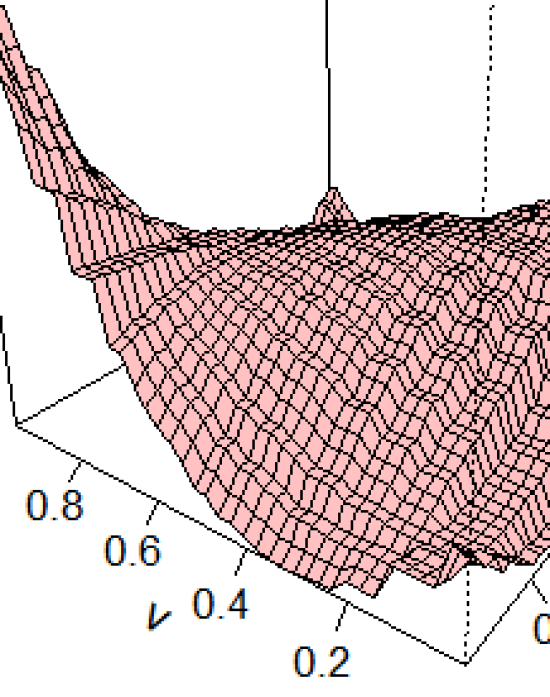

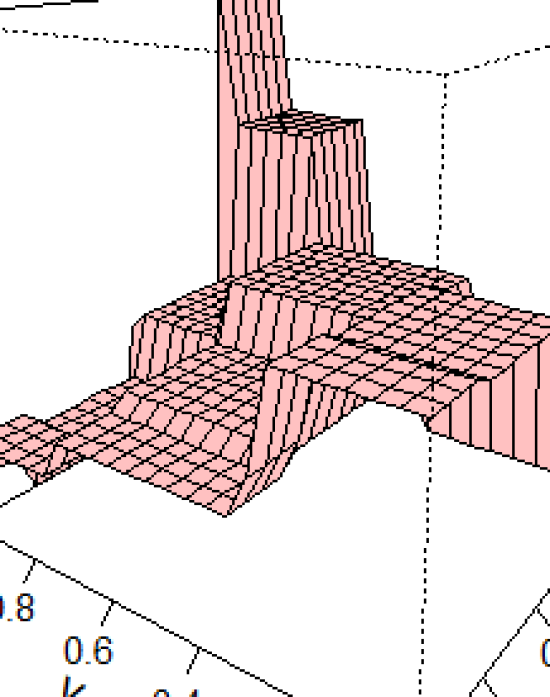

Using the methodology detailed in the next section, we estimate copula density function for four real data sets, covering the full spectrum of discrete, continuous, and categorical variables. The results are shown in Fig 1.

Example 1. Both continuous: This is the classic Loss-ALAE dataset from Frees and Valdez (1998), concerning indemnity payment (LOSS) and allocated loss adjustment expense (ALAE) from insurance claims. The estimated copula based on uncensored observations (1,466 in total) is shown in Fig. 1(a).

Example 2. Both discrete count: This data (Zelterman, 1987, Table 1) reports a survey of women employed as mathematicians or statisticians based on their monthly salary and years since their bachelor’s degree. The summarized data can be represented as a large, sparse contingency table. It is worthy of remark that estimating copula from this kind of data is known to be challenging. Fig. 1(b) displays the staircase . Example 3. Both ordinal: The dataset is based on the cross-classification of people in Caithness, Scotland, by eye color (blue, light, medium, dark) and hair color (fair, red, medium, dark, black), first analyzed by Fisher (1940). This is historically important data, and is believed to be the first example of measuring association in contingency tables. Fig. 1(c) displays the estimated piecewise-constant checkerboard copula function.

Example 4. Mixed variables: The data is cross-section wage data consisting of a random sample taken from the U.S. Current Population Survey for the year 1976 (Wooldridge, 2003). The copula density in Fig. 1(d) models the dependence between wages (continuous) and number of dependants (discrete). In contrast to the traditional copula-estimation techniques, the method presented here works across the board without a single modification or tuning in its architecture. It thereby achieves the important goal of automated learning in the mixed-data environment. A detailed description of the model specification, estimation, and exploratory analysis will be discussed in the ensuing sections.

4 United LP-Nonparametric Methods

This section provides a fundamentally new copula-representation theory, along with nonparametric estimation strategies that work for mixed data.

4.1 Generalized Copula and Conditional Comparison Density

United statistical theory aims to unify methods for continuous and discrete random variables. Thus it is important to introduce a bona fide definition of copula density that is valid for mixed(X,Y). This will be achieved via a new representation of Bayes’ theorem. We start by noting that when and are both continuous, or both discrete, their joint probability is described by joint probability density or by joint probability mass function . When is discrete and is continuous, the joint probability is described by either side of identity

| (4.1) |

which we call the Pre-Bayes theorem. Recall that the Bayes’ rule is given by .

Definition 1 (Comparison Density).

Define comparison density between and continuous as

and for and discrete, defined in terms of probability mass function:

We can now represent Bayes’ rule, after the quantile transformation using conditional comparison density notation:

| (4.2) |

Note that For continuous margins case, copula admits the following conditional distribution-based representation:

| (4.3) |

We now generalize this for mixed (X,Y) case in the following definition.

Definition 2 (Generalized Copula Density).

The key is to recognize that, for discrete and continuous, we can define generalized copula density through conditional comparison density as

| (4.4) |

Here Bayes’ theorem (4.2) asserts the equality of two comparison densities whose value is defined to be copula density. To the best of our knowledge, this is the first rigorous general-purpose definition of copula that is valid for arbitrary random variables.

Definition 3 (Sequential Multivariate Mixed Copula).

The next result generalizes formula (4.4) to multivariate case via successive conditional comparison densities:

| (4.5) |

For that reason we call this result “sequential” multivariate copula decomposition, valid for mixed discrete and continuous variables.

4.2 Notation and Background

Basics 1. Mid-Distribution Transform. The mid-distribution function of a random variable is defined as where is probability mass function. The has mean and variance . The empirical cdf will be denoted by . Basics 2. Pseudo-Observations Construction. Our nonparametric copula approach aims to model the distribution of . A major obstacle in applying and estimating copula densities is that the marginal of and are unknown. Our approach starts with the mid-distribution function of the sample marginal distribution functions of and to transform observed to

| (4.6) |

It is important to keep in mind that the empirical cdfs and are discrete, irrespective of the data-type of the original and .

Remark 4.1.

We recommend displaying the original as well as the copula scatter plots: and for a better understanding of the relationship.

Remark 4.2.

Note that our definition of pseudo-samples avoids the questionable practice of random tie-breaking using jittering, which is known to mask the real pattern in the data by injecting fake variation and randomness.

4.3 Theory and Approximation Methods

We present our nonparametric theory and methodology in a ‘programmatic’ style–by gradually introducing the essential tools and building blocks that is translatable into an algorithm.

Step 1: LP-Polynomials of Mid-Ranks. As is evident from Eq. (4.6), to model copula, we need to analyze discrete sample distributions and . Construct the LP-polynomial basis for the Hilbert space by applying Gram-Schmidt orthonormalization (see Supplementary Appendix A for more details) on the set of functions of the power of :

| (4.7) |

LP-bases obey the following orthonormality conditions with respect to the measure :

For data analysis, construct the empirical LP basis (in short eLP basis) , where is strictly less than the number of unique values in the sample . Note that our custom-constructed basis functions are orthonormal polynomials of mid-rank transform–for more details see Mukhopadhyay (2019), Mukhopadhyay and Wang (2019), and Mukhopadhyay and Parzen (2014). LP-orthonormal system plays a fundamental role in constructing expansions of our mixed generalized copula distributions (4.4).

Remark 4.3.

It is important to distinguish between parametric and nonparametric (or data-adaptive) orthonormal polynomials in order to appreciate the usefulness of eLP-basis functions. Traditional approaches construct separate orthonormal polynomials for standard parametric distributions like normal, exponential, Poisson, binomial, geometric, etc. on a case-by-case basis, each time solving the heavy-duty Emerson recurrence relation (Emerson, 1968). For details, see Rayner and Best (1989, Appendix 1) and Griffiths (2014). There are two practical disadvantages of this ‘parametric’ approach: (i) it quickly becomes fruitless (analytically laborious and computationally complex) for non-standard distributions; (ii) for real data analysis, this strategy completely breaks down, as we rarely know the underlying distribution. What we need is a ‘nonparametric’ mechanism that can provide an automatic and universal construction of tailor-made orthonormal polynomials for arbitrary . Applied data scientists would derive comfort from the fact that our LP-system of nonparametric polynomials serves exactly that purpose.

Step 2: Unit LP-Basis. Define the unit interval LP-polynomial basis functions

| (4.8) |

where refers to the quantile function of a random variable . The eLP-unit-bases are denoted simply as . Fig. 2 displays and for for the Wooldridge’s data. Notice the changing shape of LP-basis functions (the rows of Fig. 2)–a key characteristic property of nonparametric polynomials, as mention in Remark 4.3.

Step 3: LP-Comeans and LPINFOR. The next vital ingredients of our copula density estimation are LP-comeans defined as

| (4.9) |

where expectation is taken with respect to the joint distribution of . The LP-comeans are the nonparametrically derived “parameters” of our copula model, which can be interpreted as a dependence measure. For example, many traditional nonparametric statistics (Spearman rank correlation, Wilcoxon two-sample rank sum statistics, Pearson’s phi coefficient) are equivalent to ; for more details see Section 7 and Mukhopadhyay (2019). Given bivariate data, compute and display matrix of empirical LP-comeans (see Table 1) for .

Step 4: LP Representation of Copula Density. LP orthogonal series representation of generalized copula density function for arbitrary (X,Y) is given by

| (4.10) |

or, equivalently, LP-comeans are orthogonal coefficients of representations (estimators) of square integrable copula density

| (4.11) |

A proof of copula LP representation is provided by representations of conditional copula density and conditional expectations:

LP-representation theory provides a ‘smooth’ copula density estimate for mixed (X,Y) where the LP-comeans and custom-built orthogonal polynomials play the vital role.

Step 5: Estimation and Denoising. To estimate the LP-comeans, first note that Eq. (4.11) can be rewritten as follows after substituting and :

| (4.12) |

since and by construction. The expression (4.12) immediately leads to the following empirical estimate of the LP-comeans:

| (4.13) |

Using the theory of linear rank statistic (Ruymgaart, 1974, Parzen and Mukhopadhyay, 2013a), one can easily show that the sampling distribution (under the initial hypothesis of independence) of the empirical are i.i.d . Identify the significantly non-zero (“dominant” components) indices of by using the Schwarz model selection criterion, applied to the LP-comeans arranged in decreasing magnitude:

Choose to maximize for identifying the important LP-comeans. For other variants of penalty see Kallenberg (2008), Mukhopadhyay (2017), and references therein.

Step 6: LP-Spectral Expansion of Copula Density. Here we provide an alternative way of expressing (Karhunen-Loéve-type canonical representation) the fundamental LP-Fourier series expansion result (4.10).

Our canonical expansion is based on the singular value decomposition (SVD) of the LP-comean kernel (4.9) , where and are the elements of the singular vectors with singular values . For a square integrable copula density, we have the following orthogonal expansion result:

| (4.14) |

where the spectral basis functions are linear combinations of LP-polynomials: , and . We call these spectral-bases as copula-principal components–a potential tool for non-linear dimension reduction for mixed data.

Remark 4.4 (Trivariate Copula).

The LP-nonparametric theory of copula allows extension to higher-dimension. For example, a trivriate Bernoulli copula222Modeling multivariate binary data is an important problem in economics and health care. admits the following representation for :

where the higher-order LP-comeans are defined as follows:

As an anonymous reviewer pointed out, this multivariate LP-expansion result could be of “great importance,” since it is validity does not require assumptions like conditional independencies or constant conditional copulas. Some strategies on higher-dimensional generalizations are discussed in the next section.

5 Nonlinear Mixed Dependence Measure

How can we develop a copula-based nonparametric dependence measure that is: (i) capable of detecting complex nonlinear relationships between and , (ii) valid for mixed pairs of random variables, (iii) computationally fast enough to handle large datasets, and finally, (iv) able to provide insights into the ‘nature’ of the non-linear pattern that is present in the data. As a solution to this problem, we introduce a new class of dependence measure based on LP-comean matrix.

Definition 4.

Define LP-copula based nonparametric dependence measure LPINFOR

| (5.1) |

A few notable properties: (i) and are independent if and only if . (ii) It is invariant under monotone transformations (e.g., a logarithm/exponential) of the variables. (iii) Our LPINFOR statistic measures distance between true joint distribution and the independence model. Estimate LPINFOR by influential product LP-basis functions determined by BIC (or AIC).

Remark 5.1 (Information Measure).

The name LPINFOR arises from the observation that it can be interpreted as an INFORmation-theoretic measure belonging to the family of Csiszar’s f-divergence measures (Csiszár, 1975).

Remark 5.2 (Higher-dimensional Tree-Copula).

Our methodology provides rapid constriction of a multivariate dependence tree. It consists of two steps:

-

1.

Infer the maximum spanning tree (MST) by using the LPINFOR statistic as the edge-weight (indicating the degree of dependence between two variables) where denotes the edge sets.

-

2.

Approximate the multivariate copula density by:

(5.2) where each local bivariate copulas are estimated using the LP-method to ensure that the whole process can run automatically for mixed variables.

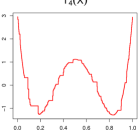

Example 5. Sinusoidal pattern: We consider the model with error . Fig 3 shows the relationship based on a sample of size generated from the model with . The associate empirical LP-comean matrix is given by

This yields the LPINFOR statistic value with p-value essentially zero, as follows under independence. However, an applied researcher might want to go beyond confirmatory test. In particular, the question of ‘how’ and are dependent (the nature of nonlinear coupling) could help domain scientists to generate refined hypothesis to investigate. To bring this exploratory side into our analysis, we introduce the concept of LP-maximal correlation and optimal transformations.

Definition 5.

Define LP-maximal correlation between and as

| (5.3) |

where ‘’ denotes the usual composition of functions; and were defined in (4.14).

Remark 5.3.

not only extends Breiman and Friedman (1985) to the mixed case, but also provides a more computationally friendlier scheme.

Fig. 3 shows the estimated optimal transformations and their embedding with the empirical . The remarkable thing about our algorithm is how accurately it recovers the optimal transformations: the sinusoidal function of and almost linear function for , and above all the simplicity of the computation (requiring only the SVD of the LP-dependence matrix; see Step 6 of Sec 4.3).

Remark 5.4.

Our LP-theoretic approach provides copula-based unified algorithms to measure as well as explore complex correlations, without any significant computational cost. Another approach of inferring the ‘shape’ of dependency will be discussed next.

6 Exploratory Modeling: The ‘Shape’ of Dependence

The LP-copula approach provides a model and explanation both. The LP-comeans provide insights into ‘how’ and are dependent. In order to better understand the exploratory side of our approach, consider the Wechsler Intelligence Scale (WAIS) data in Table 1. The question of particular interest to us: Whether age (discrete variable) and IQ (continuous variable) are dependent? If so, what can we say about the nature of their relationship?

| 16-19 | 20-34 | 35-54 | 55-69 | 70 |

|---|---|---|---|---|

| 8.62 | 9.85 | 9.98 | 9.12 | 4.80 |

| 9.94 | 10.43 | 10.69 | 9.89 | 9.18 |

| 10.06 | 11.31 | 11.40 | 10.57 | 9.27 |

The LP-comean matrix, displayed in Table 1, immediately implies the following:

-

•

There exists a significant (non-linear) dependence between Age and IQ score (LPINFOR-based p-value being ).

-

•

The only significant LP-component is , which indicates interaction between linear-IQ and quadratic-age effect.

-

•

In addition, the negative sign of suggests there is an umbrella-like trend of IQ as a function of age. This statistically confirms the common belief that the ability to comprehend ideas and learn is an increasing function of age up to a certain point, and then it declines with increasing age. This is also verified from the boxplot in Fig. 4. We feel this exploratory side of our method could be valuable for applied users to better interpret the pattern in the data.

-

•

The final estimated (mixed: IQ score is continuous; Age groups is a discrete variable) LP-copula density is shown in the left panel of Fig. 4.

7 Bernoulli Copula: Paradox and Its Resolution

“Surely discrete marginal dfs must cause problems. Believe me, they do! be prepared that everything that can go wrong, will go wrong.”—Embrechts (2009).

Developing a nonparametric copula-based dependence measure for discrete data (i.e., where the probability of a tie is positive) is known to be a challenging problem. However, an even more ambitious target is to design a truly automated correlation-learning algorithm for mixed variables that can adapt itself intelligently without having the data-type information from the user.

The problem comes from the fact that, while concordance measures like Kendall’s or Spearman’s are margin-free for continuous random variables, the same does not hold for discrete cases. As a consequence, the range of copula-based correlation measures for discrete become marginal-dependent, and do not attain the bound . This creates a significant complication, since we can not compare the ‘strength’ of dependence by solely comparing it’s magnitude. The following example, taken from Genest and Neslehova (2007, p. 492) illustrates this non-intuitive unpleasant phenomena.

Example 6. The Bernoulli table paradox: Consider Bernoulli random variables with marginal and joint distribution , which implies almost surely, still the traditional . Similarly, for the case , despite almost surely, the traditional yields counter-intuitive answer. This shows the surprising phenomenon that discrete and with perfect monotone functional dependence does not guarantee .

Generalized Spearman Correlation. We now show the (linear-rank) statistic not only resolves these inconsistencies but also provides one single computing formula for Spearman correlation that is valid for mixed (discrete or continuous) marginals without any additional adjustments.

Step 1. For binary with : we have and the correction factor . Step 2. Thus we have the mid-distribution-based LP-polynomial: , and . Remember that as is binary (takes two distinct values), we have one LP-basis function. Step 3. The LP-basis for is , and , since has the same marginals as with . Step 4. Now we are in a position to compute the :

A similar calculation goes through for the second case, where we have , yielding .

Remark 7.1.

In summary, generalized LP-correlations circumvent the mammoth challenges and technicalities required to build a valid copula-based dependence measure for mixed data. We end this section with a real example.

Example 7. Hellman’s Infant Data (Yates, 1934): Table 2 shows cross-tabulation of infants based on whether the infant was breast-fed or bottle-fed.

| Normal teeth | Malocclusion | |

|---|---|---|

| Breast-fed | 4 | 16 |

| Bottle-fed | 1 | 21 |

The scientific question of interest here is whether the type of feeding is associated with malocclusion. For this data we estimate the LP-comean:

with the pvalue , indicating an absence of any notable correlation.

8 Tests of Symmetry and Direction

In the previous section, we have seen how LP-comean dependence matrix helps to uncover the functional relationship between and . Now we will venture to go one step further and ask: does LP-comean matrix inform the user of the ‘shapes’ of copula density function? In particular, we are interested in the following question: Can we transform the problem of checking the symmetry of bivariate copula density for all , as testing symmetry of the corresponding LP-comean matrix? For the purposes of illustration, consider the following two empirical LP-comean matrices, computed from the Gaussian() copula and its asymmetric version produced by Khoudraji’s device (Khoudraji, 1996) with :

| (8.1) |

At a first glance, looks very close to symmetry (in a stochastic sense), whereas a clear asymmetry is visible in the matrix. We can test the hypothesis of symmetry of the LP-comean matrix by constructing the following statistic:

| (8.2) |

where follows chisquare distribution under null. We apply this test for our toy examples, leading to p-values and respectively.

Example 8. Geyser data: We are given observation of waiting time between eruptions and the duration of the eruption for the Old Faithful geyser in Yellowstone National Park. The left panel of Fig. 5 displays the data whose LP-comean matrix is displayed below:

Few notable features are clear from the LP-matrix:

-

•

The significant higher-order LP-comeans indicate strong presence of nonlinear correlation. Terence Speed in IMS Bulletin 15 (March 2012 issue) asked whether the dependence between eruption duration and waiting time is linear.

-

•

The matrix looks very “close” to symmetrical. In order to assess this, we apply the test. The resulting pvalue turns out to be . The conclusion of symmetry is not surprising looking at the scatter plot.

-

•

The right panel shows the estimated LP-copula density for geyser data, which indicates the presence of tail-dependence.

Remark 8.1.

The problem of symmetry is interesting for a few reasons: (i) this can be used to guide the suitable parametric model (e.g., Archimedean vs meta-elliptical copulas) for the data; (ii) the asymmetry might hint at a causal direction between and .

Remark 8.2.

LP-dependence matrix acts as both confirmatory and exploratory diagnostic tool in the sense that it contains information about the ‘strength’ (departure from uniformity) and ‘shape’ of the copula density.

Remark 8.3.

Note that, in contrast to most other schemes (Junker et al., 2019, Genest et al., 2012), our approach does not require empirical estimation of copula as an intermediate problem to understand the (a)symmetry, leading to computationally extremely efficient algorithm. This could be a huge advantage for large-scale problems. In general, LP-comean dependence matrix provides a fast and elegant way to nonparametrically diagnose different shapes of copula density. This will be explored further in the future.

9 Simulation Study

We perform numerical comparisons with state-of-the-art nonparametric copula density estimation methods, implemented in the R package kdecopula (Nagler, 2018b):

-

•

Probit transformation estimator with log-quadratic local likelihood estimation and nearest-neighbor bandwidths (Geenens et al., 2017).

-

•

The classical mirror-reflection estimator proposed by Gijbels and Mielniczuk (1990).

-

•

The penalized Bernstein polynomial-based estimator (Sancetta and Satchell, 2004).

-

•

The beta kernel estimator of Charpentier et al. (2007).

We restrict ourselves to continuous margins, as the competing methods are not generalizable for mixed data-type. Our numerical setting closely follows Geenens et al. (2017, Sec. 5). We simulate independent random copula-samples of size from the following copula distributions:

-

•

Gaussian copula with parameter ;

-

•

Student’s t-copula with 5 degrees of freedom, with ;

-

•

Frank copula with parameter .

-

•

Plackett Copula with parameter .

-

•

Clayton copula with parameter .

-

•

Ali-Mikhail-Haq copula with parameter .

-

•

Joe copula with parameter .

-

•

Gumbel copula with parameter .

We assess the fit of an estimator using the mean integrated absolute error (MIAE) or -distance criterion , which is estimated by the average over Monte Carlo replications on the grid . The results are shown in Table 3. To better interpret the numbers, we have reported the MIAE of the competing methods relative to our proposed LP-method. Thus, any number greater than one indicates the superiority of the LP-copula method.

| Copula family | Probit | MR | Bernstein | Beta | LP |

|---|---|---|---|---|---|

| Gaussian (0.70) | 0.677 | 1.200 | 1.110 | 1.221 | ✓ |

| Student’s-T4 (-.30) | 0.865 | 1.533 | 1.074 | 1.187 | ✓ |

| Frank (6) | 1.055 | 1.493 | 1.811 | 1.658 | ✓ |

| Frank (-2) | 1.215 | 1.615 | 1.423 | 1.669 | ✓ |

| Plackett (6) | 1.197 | 1.951 | 1.860 | 1.843 | ✓ |

| Plackett (0.10) | 1.576 | 1.580 | 1.779 | 1.573 | ✓ |

| Clayton (3) | 0.688 | 0.993 | 1.047 | 0.842 | ✗ |

| Clayton (-0.50) | 1.282 | 1.147 | 0.954 | 0.975 | ✗ |

| AMH (0.85) | 0.966 | 1.327 | 1.052 | 1.240 | ✓ |

| AMH (-0.85) | 0.988 | 1.012 | 1.041 | 1.226 | ✓ |

| Joe (1.5) | 0.875 | 1.166 | 0.906 | 0.933 | ✗ |

| Gumbel (1.5) | 0.740 | 1.112 | 1.095 | 1.016 | ✓ |

As we can see from Table 3, more often than not, the LP-method occupies the best or second-best position. For Ali-Mikhail-Haq (AMH) copulas, all methods work equally well. For the Joe copula, the mirror-reflection kernel estimator performs quite well. For the Clayton copula family the beta-kernel estimator is very efficient. However, the probit-transformation-based kernel density method (combined with local log-quadratic approximation and K-NN-type bandwidth matrix) appears to be the most prominent competitor. All in all, considering computational efficiency, ease of implementation222which, by the virtue of (4.10), only requires computation of LP-comeans. This can be done in one line R-code: Cov(), where and denote the matrix of LP-polynomials for and ., and power of generalizability, the proposed technique has the potential to become a ‘default algorithm’ for copula dependence modeling.

10 Conclusion

The ultimate goal of copula statistical learning is to construct a simple yet flexible mathematical model with interpretable parameters that can adequately describe the essential dependence structure of the data. Taking inspiration from the recent progress on ‘LP-United Data Science’ (Parzen and Mukhopadhyay, 2013a, Mukhopadhyay and Parzen, 2014, Mukhopadhyay, 2016, 2017, 2018, Mukhopadhyay and Parzen, 2018, Mukhopadhyay and Fletcher, 2018), this article presents a modern unifying copula learning program that is valid for any data-type. This philosophy of algorithm design is a significant milestone compared to the existing culture of building ‘well-tuned’ retail procedures on a case-by-case basis.

“Efficiency for the user needs to be interpreted quite differently for the user than the tool forger. All efficiencies between 90% and 100% are NEARLY the SAME for the user…The Tool-forger, on the other hand, should pay attention to another 1/2% of efficiency.”— John Tukey (1979, p. 104)

We hope that the advances presented here will make copula-based data analysis more attractive by making it self-consistent and easy to apply for practitioners, who like to have an automated versatile tool in their statistical repository that works reasonably well for a wide range of scenarios.

Acknowledgement

The authors thank the editor, associate editor, and reviewers for their constructive comments and suggestions, which helped improve the paper.

Supplementary Material

To better highlight the main points of the paper, we have relegated additional details on computation, methods, and numerical simulations to the supplement. All data used in this research are publicly available through R-software.

References

- AghaKouchak (2014) AghaKouchak, A. (2014). Entropy–copula in hydrology and climatology. Journal of Hydrometeorology 15, 2176–2189.

- Berkes et al. (2009) Berkes, P., Wood, F., and Pillow, J. W. (2009). Characterizing neural dependencies with copula models. In Advances in neural information processing systems, pages 129–136.

- Breiman and Friedman (1985) Breiman, L. and Friedman, J. H. (1985). Estimating optimal transformations for multiple regression and correlation. Journal of the American Statistical Association 80, 580–598.

- Charpentier et al. (2007) Charpentier, A., Fermanian, J.-D., and Scaillet, O. (2007). The estimation of copulas: Theory and practice. Copulas: From theory to application in finance pages 35–60.

- Chen and Huang (2007) Chen, S. X. and Huang, T.-M. (2007). Nonparametric estimation of copula functions for dependence modelling. Canadian Journal of Statistics 35, 265–282.

- Craiu and Sabeti (2012) Craiu, V. R. and Sabeti, A. (2012). In mixed company: Bayesian inference for bivariate conditional copula models with discrete and continuous outcomes. Journal of Multivariate Analysis 110, 106–120.

- Csiszár (1975) Csiszár, I. (1975). I-divergence geometry of probability distributions and minimization problems. The Annals of Probability 3, 146–158.

- Danaher and Smith (2011) Danaher, P. J. and Smith, M. S. (2011). Modeling multivariate distributions using copulas: Applications in marketing. Marketing Science 30, 4–21.

- Embrechts (2009) Embrechts, P. (2009). Copulas: A personal view. Journal of Risk and Insurance 76, 639–650.

- Embrechts et al. (2002) Embrechts, P., McNeil, A., and Straumann, D. (2002). Correlation and dependence in risk management: properties and pitfalls. Risk management: value at risk and beyond 1, 176–223.

- Emerson (1968) Emerson, P. L. (1968). Numerical construction of orthogonal polynomials from a general recurrence formula. Biometrics 24, 695–701.

- Fisher (1940) Fisher, R. A. (1940). The precision of discriminant functions. Annals of Eugenics 10, 422–429.

- Frees and Valdez (1998) Frees, E. W. and Valdez, E. A. (1998). Understanding relationships using copulas. North American actuarial journal 2, 1–25.

- Frey et al. (2001) Frey, R., McNeil, A., and Nyfeler, M. (2001). Copulas and credit models. Risk 10, 111–114.

- Geenens et al. (2017) Geenens, G., Charpentier, A., Paindaveine, D., et al. (2017). Probit transformation for nonparametric kernel estimation of the copula density. Bernoulli 23, 1848–1873.

- Genest and Neslehova (2007) Genest, C. and Neslehova, J. (2007). A primer on copulas for count data. Astin Bulletin 37, 475–515.

- Genest et al. (2012) Genest, C., Nešlehová, J., and Quessy, J.-F. (2012). Tests of symmetry for bivariate copulas. Annals of the Institute of Statistical Mathematics 64, 811–834.

- Gijbels and Mielniczuk (1990) Gijbels, I. and Mielniczuk, J. (1990). Estimating the density of a copula function. Communications in Statistics-Theory and Methods 19, 445–464.

- Griffiths (2014) Griffiths, R. (2014). Orthogonal expansions. Wiley StatsRef:Statistics Reference Online .

- Hoeffding (1940) Hoeffding, W. (1940). Massstabinvariante korrelationstheorie. Schriften des Mathematischen Seminars und des Instituts fr Angewandte Mathematik der Universitt Berlin 5, 179–233.

- Hollander et al. (2013) Hollander, M., Wolfe, D. A., and Chicken, E. (2013). Nonparametric statistical methods. John Wiley & Sons.

- Joe (1996) Joe, H. (1996). Families of m-variate distributions with given margins and m (m-1)/2 bivariate dependence parameters. In Distributions with Fixed Marginals and Related Topics (L. Rüschendorf, B. Schweizer and M. D. Taylor, eds.) pages 120–141.

- Joe (2014) Joe, H. (2014). Dependence modeling with copulas. CRC Press.

- Junker et al. (2019) Junker, R. R., Griessenberger, F., and Trutschnig, W. (2019). A copula-based measure for quantifying asymmetry in dependence and associations. arXiv:1902.00203 .

- Kallenberg (2008) Kallenberg, W. C. (2008). Modelling dependence. Insurance: Mathematics and Economics 42, 127–146.

- Khoudraji (1996) Khoudraji, A. (1996). Contributions à l’étude des copules et à la modélisation de valeurs extrêmes bivariées. PhD thesis, Universiè Laval, Quèbec, Canada.

- Marbac et al. (2017) Marbac, M., Biernacki, C., and Vandewalle, V. (2017). Model-based clustering of gaussian copulas for mixed data. Communications in Statistics-Theory and Methods 46, 11635–11656.

- Mukhopadhyay (2016) Mukhopadhyay, S. (2016). Large scale signal detection: A unifying view. Biometrics 72, 325–334.

- Mukhopadhyay (2017) Mukhopadhyay, S. (2017). Large-scale mode identification and data-driven sciences. Electronic Journal of Statistics 11, 215–240.

- Mukhopadhyay (2018) Mukhopadhyay, S. (2018). Decentralized nonparametric multiple testing. Journal of Nonparametric Statistics 30, 1003–1015.

- Mukhopadhyay (2019) Mukhopadhyay, S. (2019). United statistical algorithms and data science: An introduction to the principles. Topics in Nonparametric Statistics, Springer, New York, NY, (forthcoming) .

- Mukhopadhyay and Fletcher (2018) Mukhopadhyay, S. and Fletcher, D. (2018). Generalized empirical Bayes modeling via frequentist goodness of fit. Scientific Reports 8, 1–15.

- Mukhopadhyay and Parzen (2014) Mukhopadhyay, S. and Parzen, E. (2014). LP approach to statistical modeling. Preprint arXiv:1405.2601 .

- Mukhopadhyay and Parzen (2018) Mukhopadhyay, S. and Parzen, E. (2018). Nonlinear time series modeling: A unified perspective, algorithm, and application. Journal of Risk and Financial Management, Special Issue on “Applied Econometrics” 8, 1–18.

- Mukhopadhyay and Wang (2019) Mukhopadhyay, S. and Wang, K. (2019). A nonparametric approach to high-dimensional k-sample comparison problem. Biometrika (in press), preprint arXiv:1810.01724 .

- Nagler (2018a) Nagler, T. (2018a). A generic approach to nonparametric function estimation with mixed data. Statistics & Probability Letters 137, 326–330.

- Nagler (2018b) Nagler, T. (2018b). kdecopula: An R package for the kernel estimation of bivariate copula densities. Journal of Statistical Software 84, 1–22.

- Nelsen (2007) Nelsen, R. B. (2007). An introduction to copulas. Springer-Verlag New York.

- Panagiotelis et al. (2012) Panagiotelis, A., Czado, C., and Joe, H. (2012). Pair copula constructions for multivariate discrete data. Journal of the American Statistical Association 107, 1063–1072.

- Parzen and Mukhopadhyay (2013a) Parzen, E. and Mukhopadhyay, S. (2013a). United Statistical Algorithms, LP comoment, Copula Density, Nonparametric Modeling. 59th ISI World Statistics Congress (WSC), Hong Kong .

- Parzen and Mukhopadhyay (2013b) Parzen, E. and Mukhopadhyay, S. (2013b). United Statistical Algorithms, Small and Big Data, Future of Statisticians. arXiv:1308.0641 .

- Racine (2015) Racine, J. S. (2015). Mixed data kernel copulas. Empirical Economics 48, 37–59.

- Rayner and Best (1989) Rayner, J. and Best, D. (1989). Smooth tests of goodness of fit. Oxford University Press: New York.

- Ruymgaart (1974) Ruymgaart, F. (1974). Asymptotic normality of nonparametric tests for independence. The Annals of Statistics 2, 892–910.

- Sancetta and Satchell (2004) Sancetta, A. and Satchell, S. (2004). The bernstein copula and its applications to modeling and approximations of multivariate distributions. Econometric theory 20, 535–562.

- Schweizer and Sklar (2011) Schweizer, B. and Sklar, A. (2011). Probabilistic metric spaces. Courier Corporation.

- Sklar (1959) Sklar, M. (1959). Fonctions de répartition à n dimensions et leurs marges. Publ. Inst. Statistique Univ. Paris 8, 229–231.

- Smith and Khaled (2012) Smith, M. S. and Khaled, M. A. (2012). Estimation of copula models with discrete margins via bayesian data augmentation. Journal of the American Statistical Association 107, 290–303.

- Trivedi et al. (2007) Trivedi, P. K., Zimmer, D. M., et al. (2007). Copula modeling: an introduction for practitioners. Foundations and Trends® in Econometrics 1, 1–111.

- Tukey (1979) Tukey, J. W. (1979). Robust techniques for the user. In Robustness in statistics, pages 103–106. Elsevier.

- Wooldridge (2003) Wooldridge, J. M. (2003). Introductory econometrics thomson, south-western. Mason, Ohio .

- Yates (1934) Yates, F. (1934). Contingency tables involving small numbers and the test. Supplement to the Journal of the Royal Statistical Society 1, 217–235.

- Zelterman (1987) Zelterman, D. (1987). Goodness-of-fit tests for large sparse multinomial distributions. Journal of the American Statistical Association 82, 624–629.

- Zilko and Kurowicka (2016) Zilko, A. A. and Kurowicka, D. (2016). Copula in a multivariate mixed discrete–continuous model. Computational Statistics & Data Analysis 103, 28–55.

Supplementary Information for “Nonparametric Universal Copula Modeling”

Subhadeep Mukhopadhyay∗ and Emanuel Parzen

∗ To whom correspondence should be addressed; E-mail: deep@unitedstatalgo.com

This supplementary document contains three Appendices, presenting some additional methodological and numerical details.

A. Gram-Schmidt Orthonormalization

We start by explicitly defining orthonormal polynomials. As the name suggests, these are polynomials that are orthonormal to each other with respect to weighted inner product, i.e.,

| (E.1) |

Orthogonal polynomials can be obtained by applying the Gram-Schmidt orthogonalization process to the basis . Gram-Schmidt orthogonalization works as follows: Step 1. Select and the weight function . For constructing eLP-polynomials choose to be the empirical cdf and

| (E.2) |

Step 2. We then iteratively construct the next degree polynomial by removing the components in the directions of the previous ones: , where

| (E.3) |

There are several functions available in R to perform the numerical calculation of Gram-Schmidt algorithm. Note that our custom-constructed LP-basis functions are orthonormal polynomials of mid-rank transform instead of raw -values, thus provide robustness.

B. Additional Simulation Results: n=500 Case

| Copula family | Probit | MR | Bernstein | Beta | LP |

|---|---|---|---|---|---|

| Gaussian (0.70) | 0.624 | 1.217 | 1.162 | 1.261 | ✓ |

| Student’s-T4 (-.30) | 0.824 | 1.329 | 1.028 | 1.094 | ✓ |

| Frank (6) | 1.051 | 1.422 | 1.684 | 1.573 | ✓ |

| Frank (-2) | 1.171 | 1.477 | 1.282 | 1.509 | ✓ |

| Plackett (6) | 1.088 | 1.762 | 1.652 | 1.657 | ✓ |

| Plackett (0.10) | 1.394 | 1.623 | 1.827 | 1.620 | ✓ |

| Clayton (3) | 0.595 | 0.967 | 1.122 | 0.930 | ✗ |

| Clayton (-0.50) | 1.164 | 1.168 | 1.030 | 1.051 | ✓ |

| AMH (0.85) | 0.807 | 1.093 | 0.888 | 1.029 | ✗ |

| AMH (-0.85) | 1.003 | 0.976 | 1.035 | 1.185 | ✓ |

| Joe (1.5) | 0.685 | 1.064 | 0.767 | 0.873 | ✗ |

| Gumbel (1.5) | 0.869 | 1.049 | 1.064 | 1.100 | ✓ |

C. Computational Time and Implementation Ease

| Methods | Size of the data sets | |||

|---|---|---|---|---|

| Probit | 0.3592 | 0.5828 | 2.4472 | 4.8352 |

| MR | 0.0504 | 0.1160 | 1.1644 | 3.5976 |

| Bernstein | 0.2944 | 0.6560 | 4.6060 | 10.9684 |

| Beta | 0.4016 | 0.7676 | 3.9548 | 8.9556 |

| LP | 0.0040 | 0.0108 | 0.1916 | 0.6536 |

For moderately large problems it seems: LP is almost 50x faster than Probit, 10x faster than MR, 60x faster than Bernstein, and 70x faster than Beta method. This should not come as a surprise, because the implementation of LP-method is remarkably simple (no optimization required; only simple Cov operation of LP-transformed RVs) compared to other kernel based methods which require several level of tuning and pre-processing. Moreover, keep in mind, the other methods are not automatable for mixed data problems.

D. WAIS Data: Shapes of LP-Basis Functions