Department of Computer Science, Goethe University, Frankfurt am Main, Germany. bertschinger@fias.uni-frankfurt.de

Systemic Risk: Fire-Walling Financial Systems Using Network-Based Approaches

Abstract

The latest financial crisis has painfully revealed the dangers arising from a globally interconnected financial system. Conventional approaches based on the notion of the existence of equilibrium and those which rely on statistical forecasting have seen to be inadequate to describe financial systems in any reasonable way. A more natural approach is to treat fi- nancial systems as complex networks of claims and obligations between various financial institutions present in an economy. The generic frame- work of complex networks has been successfully applied across several dis- ciplines, e.g., explaining cascading failures in power transmission systems and epidemic spreading. Here we review various network models address- ing financial contagion via direct inter-bank contracts and indirectly via overlapping portfolios of financial institutions. In particular, we discuss the implications of the “robust-yet-fragile” nature of financial networks for cost-effective regulation of systemic risk.

1 Introduction

Over the past few decades, the generic framework of complex networks has been used to address problems in a variety of scientific disciplines. The study of evolutionary dynamics of populations lieberman2005 , spreading of diseases newman2002 , spreading of failures in power transmission systems dobson2007 , dynamics of opinion formation castellano2009 , working of genetic regulation hasty2001 ; all heavily rely upon viewing and understanding the underlying systems as complex networks which represent the interaction between their various constituent elements. It is now well-known that the emergent or collective behavior in these systems are greatly influenced by the topology of the underlying network of connections together with the particular kind of dynamic processes which run on it strogatz2001 ; amaral2004 ; boccaletti2006 .

One of the latest entry into the class problems to be analyzed using methods based on the theory of complex networks is the issue of spreading of failures in financial/economic systems. Often dubbed as systemic risk, this refers to the possibility of spread of initial distress at a single or a few financial institutions such as banks to a significant fraction of a financial network. Though earlier studies of such contagion exist, it is safe to say that it is only in the aftermath of the financial crisis of 2007-09 that viewing systems such as interbank markets from the standpoint of the theory of complex networks became mainstream schweitzer2009 ; haldane2015 .

More and more direct and indirect connections are being made everyday between financial institutions as the world increasingly becomes an economically globalized one. This together with modern day financial products such as CDS (credit default swaps) or CDO (collateralized debt obligations) make today’s financial systems a very complex one and hard to analyze. Conventional approaches based on the notion of the existence of equilibrium and those which rely on statistical forecasting have seen to be inadequate to describe financial systems in any reasonable way farmer2009 . Conventional theory often makes unrealistic assumptions and is capable of analyzing only simple situations. Most importantly, it cannot handle non-linearities and feedback mechanisms ubiquitous in financial systems catanzaro2013 . Inadequacy of the conventional approaches together with the spread of concepts from complex network theory to the economic/financial community lead to the conclusion that a more natural way to describe financial systems is to treat them as complex networks of claims and obligations between various financial institutions present in an economy. It is to be noted that a significant push towards this direction was provided by people working on ecological and epidemiological systems (e.g., Robert May may2008 ). The result is that there has been an exponential increase in the studies of financial networks employing ideas and tools from the complex networks literature and the terminology of latter nowadays finds commonplace in the discussions related to contagion in financial systems.

In the simplest form, the nodes of a financial network are institutions involved in financial intermediation (called banks in short hereafter) and the links between the nodes represent lending/borrowing relationships. The links are therefore directed (usually represented as directed from borrower to lender indicating the anticipated direction of cash flow after the link has been established) and weight of a link represents the amount of money involved in the transaction between the nodes connected by that link. The banks may have other kinds of direct and indirect connections between them which are discussed in section 2. Given such a financial network, the term systemic risk refers to the possibility of an initial financial distress at a single or a few banks (say their defaulting due to a loss of value of their asset holdings) to spread through the network causing the default of a significant number of other banks in the network. Such a system wide collapse has serious repercussions for the financial system and global economy in general and could affect the lives of millions in a negative way as painfully revealed in the crisis of 2007-09.

We can easily see the parallels of the problem of the collapse of a financial network with that of an ecological network or the spread of an infectious disease. Although all these problems deal with the transmission of a ‘failure’ at a node to its neighbors in a general sense, there are also marked differences between them may2011 . A feature which distinguishes financial networks from others is that unlike the failure of a node in an ecological network or an epidemiological network, the failure of a node in a financial network depends upon the ‘internal structure’ of that node (i.e., balance sheet structure of the bank) and the ‘cumulative health’ of its neighbors in the network. So unlike simple stochastic rules used to model for e.g., the spread of an infectious disease (as in SIR model), here we need to consider the internal balance sheet dynamics of a node in detail.

Our aim in this review is to give a broad overview of the various developments in the field of systemic risk of financial networks and discuss some future directions. In this respect, we will mainly focus on the literature that concentrates on the use of tools from the study of complex networks. There is an extensive literature on banking systems based on more traditional point of views like the ones using equilibrium models. We will occasionally mention other strands of research but will refrain from discussing them in any detail.

This review is organized as follows. In section 2, we give an account of the structure of a financial network and a detailed description of what constitutes its nodes and links. We describe the kind of questions one would like to answer about such networks. In section 3, we review various past efforts in modeling contagion via interbank credit networks and in section 4, we review contagion via fire-sale of commonly held assets by banks. We discuss some of our findings related to asset contagion. In section 5 we conclude and discuss some future possibilities.

2 Nodes and links of a financial network

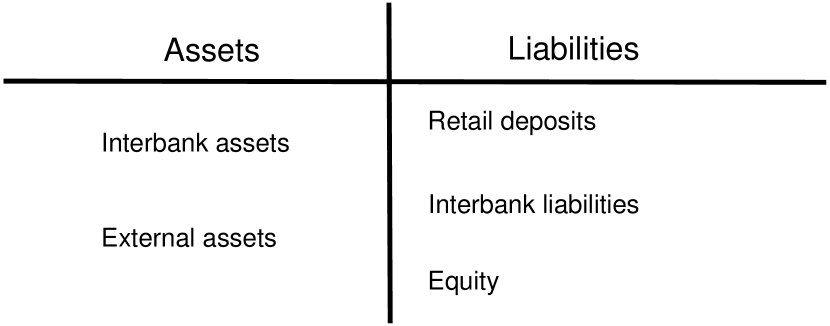

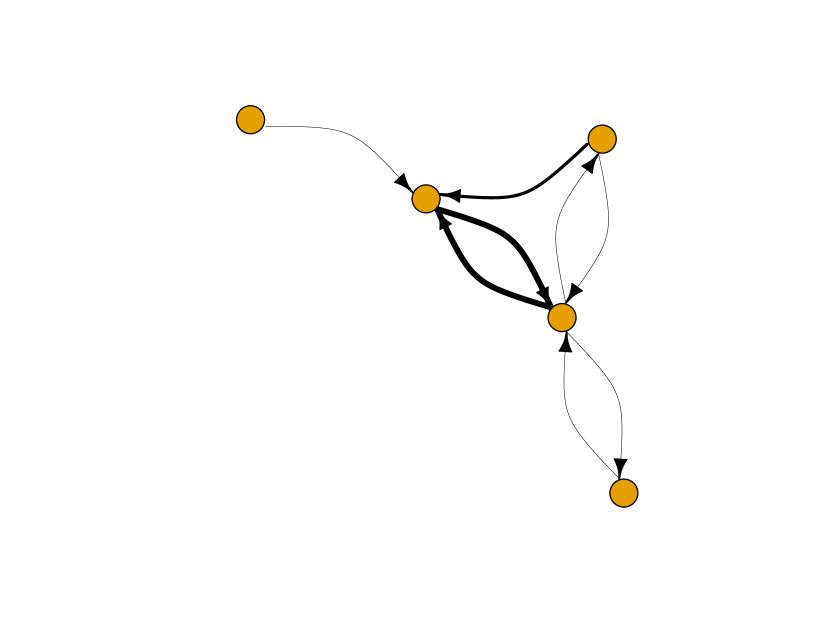

As mentioned in the introduction, the nodes of a financial network are banks, and the links represent various credit relationships. A sample financial network based on data from the European Banking Authority (EBA) is given in Fig. 1. To study the propagation of ‘failures’ or ‘defaults’ in a financial network, we may represent a bank by its balance sheet structure which lists its various assets and liabilities at any time. A schematic of a balance sheet is shown in Fig. 2. Broadly, we may classify the assets of a bank into two types; namely interbank assets (the money that the bank lent to other banks) and external assets (investments like the money that the bank lent to other parties such as business firms often receiving a collateral, deposits with a central bank, etc). The external assets can be further classified into liquid assets (assets for which there is a market and hence can be easily converted into cash. Examples include cash, central bank reserves, high-quality government bonds, etc.)) and illiquid ones (like secured or unsecured mortgages which cannot be used to raise cash quickly). More detailed classification of assets is possible by further considering divisions such as ‘Collateral assets’ (assets which may be used as collateral in repo transactions) and ‘Reverse repo assets’ (i.e., collateralized lending), etc. gai2011 . Considering such divisions is vital as the percentage of assets in various classes decides whether a bank in need of immediate cash for its promised payments can raise it in time or not. In general, the size of the balance sheet, i.e., the total value of assets (or equivalently liabilities) varies across banks. It is often found that the size distribution is heterogeneous having a heavy tail raddant2016 .

The liability side of the balance sheet usually consists of interbank liabilities (money that is owed to other banks) and retail deposits. Finer divisions such as ‘repo liabilities’ (i.e., borrowing secured with collateral) may also be considered gai2011 . The difference between the total assets and liabilities of a bank gives its equity, also commonly called net worth or capital. The equity is written on the liability side of the balance sheet indicating that it is money owed to promoters and shareholders of the bank.

There are two important considerations regarding the ‘health’ of a node.

-

•

Insolvency: A bank is considered insolvent if it has a negative net worth. The net worth may become negative, say for e.g., due to a drop in the prices of its assets (in a mark-to-market framework, the value of assets are updated according to its current market price) or due to failed investments. We may say that the bank cannot operate anymore as it cannot honor its liabilities and should close down with appropriate insolvency proceedings, though in reality, a number of things may happen like possible government intervention, etc.

-

•

Illiquidity: A bank is illiquid if its short term liabilities exceed liquid assets and hence it cannot honor the former.

In both cases, the bank is in trouble, and this will affect other banks to which it owes money. Also, the assets of the bank that is in trouble will face devaluation, thus affecting other banks holding the same class of assets on their balance sheets. Due to such feedbacks, initial distress can spread to other banks in the network and may affect a large part of it.

The links between nodes represent lending/borrowing relations between banks. They are directed and weighted, the weight of a link representing the value owed (See Fig. 3). Note that banks may interact with others not only through the above lending/borrowing relationship. Their balance sheet may be affected by the fact that they are exposed to common assets. A sell off or even a negative news about a bank might cause depreciation in the value of the assets it holds and other banks which have exposure to these assets will be affected. The sell off of an asset by a distressed bank will cause excess supply of that asset and if the market depth of that asset is shallow, will lower its value significantly. Such fire sale losses can quickly spread among the banks in the network. These two mechanisms of interbank lending and fire sale of assets form two important channels for spreading of crisis in a financial network. There are other channels possible and which ones are more relevant in reality is debatable. Upper upper2011 for e.g., argues that there is not much evidence for interbank channels propagating distress. In any case, these are possible channels of contagion under conceivable circumstances, and hence it is important to understand them from a regulatory and individual point of view.

Being able to understand the ‘behavior’ of a bank is crucial in the study of systemic risk. This is because the way a bank organizes its balance sheet and how they form connections will have a significant role in deciding whether or not an initial default will propagate in the network causing significant damage. An important factor which determines the actions of a bank is various regulatory constraints set by a central authority (like a central bank). For e.g., there could be a capital ratio constraint set by the authority stipulating that the activities of the bank should obey the constraint that its capital or net worth should be a minimum percentage of its illiquid assets (8% is now a typical figure under Basel III). Also the bank itself may have policies to keep its balance sheet structure in a specific way (For e.g., maintaining a constant leverage ratio adrian2010 ).

3 Contagion via interbank linkages

Lending and borrowing relationships with other banks serve the purpose of meeting the liquidity needs of a bank and profiting from the lending of idle liquid money. While lending, there is, of course, the risk of default. Presumably, forming more connections or dividing total exposure across several banks will reduce such risk. On the other hand, a bank with more number of connection will also have a higher probability of being hit by a defaulting counterparty. The interplay between these two effects determines whether the default of a single or a small set of banks will spread through the system.

3.1 Contagion via default spreading

One of the earlier works which explicitly incorporated the network aspects of interbank lending/borrowing is by Allen & Gale allen2000 . The interbank network they considered is rather simple compared to any real-world banking network and involved only four banks. Two different connectivity structures of the network are considered, and they showed that a complete network in which each bank is connected to every other bank readily absorbs any initial shock. However, an incomplete network structure makes the system prone to the spread of an initial default.

A pioneering work which considered the effects of varying the important features of interbank networks is by Nier et al. nier2007 . The network structures considered were Erdos-Renyi (ER) type and a tiered one. In the latter, a few large banks are connected to a large number of small banks where the latter are mostly connected to the large ones. The effect of level of capitalization of the banks, degree of the ER network, size of the interbank exposures, etc. on the number of defaults is determined using simulations. It is found that at smaller degrees of the network, a small increase in the degree of the network causes an increase in the number of defaults, but at relatively higher degrees, the effect of an initial default is contained. Predictably, higher capital levels found to reduce the risk of contagion, but the effect is found to be non-linear. The paper also briefly considers the ‘fire sale’ channel in which a distressed bank sells off its asset causing a depreciation in the market value of the assets.

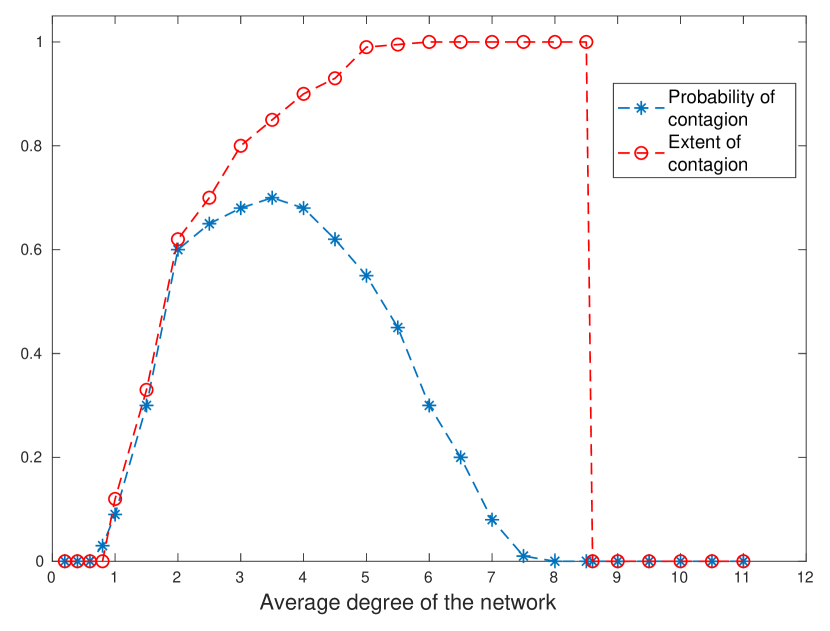

A landmark work is that of Gai & Kapadia gai2010 in which they formalized the above setting by Nier et al. nier2007 and distinguished probability of contagion from its extent (A comparison between these models is given in may2010 ). The former denotes the probability of a systemic event conditional on an initial shock while the latter denotes the percentage of banks affected conditional on a systemic event. One should note that what constitutes a systemic event is somewhat subjective. In this paper and several later works, a contagion is considered as systemic if more than 5% of the banks default. This might seem like a very low number, but reflects the fact that even the default of 5% of banks is a severe event in an economy affecting a large number of people and potentially wiping out millions of dollars. Their theoretical analysis closely follows the study of cluster size distribution in a complex network using generating functional formalism (see for e.g. newman2010 ). The key finding was that the phenomena of contagion in a financial network have a ‘robust-yet-fragile’ nature. i.e., even if the probability of contagion is very low, whenever a contagion happens, it wipes out most of the system. The typical dependency of probability and extent of contagion on the average degree of the ER network is as shown in Fig. 4. Note that when the average degree is below 1, there is no possibility of contagion as the network is a disconnected one and there is no large connected component present. After that, the probability of contagion increases with an increase in average degree, reaches a maximum value and then decreases. This clearly shows the interplay of the two effects of risk sharing and default spreading mentioned earlier. Higher degrees diffuses the initial impact among many neighbors thus reducing the possibility of contagion. However, once a contagion starts to spread, higher degrees can act as an ideal setting for the propagation of defaults since many counter-parties of a bank will be simultaneously affected. In a nutshell, this has the effect that the banking network may respond in entirely different ways to similar shocks at different nodes in the network.

The assumption made in gai2010 regarding the network structure as being ER type and that all banks are of the same size is not in line with empirical evidence about real-world banking networks which are found to have heavy-tailed distribution for both connectivity and size of banks huser2015 . Caccioli et al. caccioli2012 extended the Gai & Kapadia model to incorporate these effects. It was found that a heterogeneous degree distribution makes the network more resilient towards random defaults but more vulnerable to targeted attacks on well-connected nodes. It was also found that a power-law distribution for the size of the banks makes the contagion events more frequent. The effects of policies such as increased capital requirements are also considered which are seen to improve the resilience of the system. A recent work discussing the role of assumptions made about the connectivity and size of banks is by Raddant raddant2016 in which features of real-world empirical networks were considered in some detail.

3.2 Contagion via valuation adjustments

The seminal work of Eisenberg & Noe eisenberg2001 provides an alternative viewpoint on default contagion, namely as a problem of contract valuation. While each bank has promised the repayment of a nominal amount, it might be unable to hold up to its promise when the payment is due. As each repaid credit – in full or in part – is an income to the lending counterparty, Eisenberg & Noe proposed that the payments of all banks have to be considered simultaneously and solved in a self-consistent fashion. The resulting clearing vector can then be regarded as the value of all interbank contracts. Thus, instead of modeling the spread of defaults directly, the model provides a self-consistent solution for the final state when all payments are settled. This point of view readily connects with more standard approaches for financial valuation and has since spurred a range of theoretical glasserman2015 and computational research upper2011 .

In particular, the model of Suzuki suzuki2002 is noteworthy in this respect. It not only generalizes the above model allowing for cross-holdings of equity as well as interbank debt but also clearly formulates it as an extension of the Merton model to multiple firms. In his ground-breaking work, Merton merton1974 showed that liabilities and equity of a firm could be considered and valued as a short put and long call option on the firm’s assets respectively. Nowadays this insight forms the foundation of structural credit risk modeling and has been developed into established industry practice. Valuation in a network context is considerably more complicated as all option values are interdependent and have to be solved in a self-consistent fashion. Correspondingly, almost no analytic results are known, and only recently, some extensions including interbank liabilities of different seniorities fischer2014 or maturities kusnetsov2019 have been proposed.

From the perspective of a single firm, an approximate valuation can be obtained by taking into account the solvency risk of its counterparties. Barucca et al. barucca2016 have shown that several network valuation models, including the Eisenberg & Noe model and many of its extensions, can be unified in this way. In their framework, each firm locally adjusts the value of interbank contracts according to its expected recovery value. Different valuation models are then obtained via different assumptions about when nominal contract values are adjusted – either after an actual default or before an expected default. In the first case, the valuations obtained by each firm agree with the values derived from self-consistent network considerations whereas they only approximately reflect market values of interbank contracts in the latter.

Within the framework of network valuation, financial contagion is naturally quantified in marginal terms, i.e., as the impact of infinitesimal asset price shocks ota2014 . Demange demange2016 proposed a threat index considering a bank as systemically important to the extent that the values of all other banks are sensitive to devaluation of its assets. Taking this idea even further, Bertschinger & Stobbe bertschinger2018 have shown how to compute network Greeks, i.e., sensitivities with respect to several risk factors of interest besides asset prices. In principle, this allows to quantify the systemic impact of changes in interest rate, volatilities or asset correlations and naturally extends standard risk management practices. Indeed, the Greeks of single asset options are routinely used in order to asses and hedge the risk of trading portfolios.

3.3 Strategic reactions and network structure

An assumption that is made in the studies mentioned above is that the banks remain passive in the face of spreading of defaults. While there is some merit to this argument, it is doubtful that banks remain passive when aware of a possible default by a counterparty or news of trouble elsewhere in the financial system. There has been only minimal effort to model the effect of the response of banks on financial contagion. Anand et al. anand2012 incorporate a strategic decision-making component to the network which makes rewiring of connections a possibility. They model liquidity hoarding behavior of banks in which a bank refuses to roll over an interbank loan in fear of default of the counterparty. The outcome of a coordination game among the neighbors of a bank decides whether they roll over or withdraw loans made to that bank. Another work is by Arinaminpathy et al. arinaminpathy2012 in which confidence effects are included in the response of banks. Among other defining features of the model, it is assumed that long term loans can be made short term and interbank loans may be withdrawn.

A natural question is what kind of network structure will increase the stability of a financial system. The question has been a much debated one regarding all complex systems from the time of the influential article by Herbert Simon simon1962 . Stability of many benchmark network structures of financial systems has been studied by Battiston et al. battiston2013 with the conclusion that network topology plays a prominent role only when the liquidity is low, and there is no single optimal connection structure.

4 Contagion via fire sale of assets

As already mentioned, apart from the direct interbank claims and obligations, another way in which the balance sheets of banks influence each other is by carrying the same or similar asset classes. Portfolio overlaps thus produce another channel for initial defaults to spread, and evidence suggests that this one is more relevant than the direct channel in real-world systems. Though several earlier studies like that by Gai & Kapadia did consider minimally the effect of fire-sale of a single asset held by all banks, it is in more recent literature that this channel of contagion is analyzed more thoroughly. A general message here is that too much diversification may not be desirable for the health of the system even though it might appear as a wise strategy from an individual bank’s point of view. In fact, prior to the 2007-09 crisis, the prevailing view was that portfolio diversification by individual banks will make them safer and this will automatically translate into improved safety of the overall financial system. However, this ignored the crucial fact that diversification by firms will also create strong correlations across balance sheets thus rendering the whole system susceptible to price changes of commonly held assets.

4.1 Contagion via overlapping portfolios

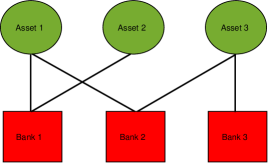

An early work which focuses on the network aspects of portfolio overlaps is by Caccioli et al. caccioli2014 who considered a bipartite network of banks and assets. In this network, banks have only connections to the assets they hold in their portfolio (see Fig. 5). Two kinds of initial shocks are considered namely 1) Devaluation of the price of a randomly chosen asset to zero and 2) Making a randomly selected bank default. The initial shock then causes defaulting banks to sell the assets in their portfolio en masse thereby depreciating their prizes. A specific functional form for the decrease in the price of an asset is assumed which in general could depend upon market depth and the volume of assets on sale. The depreciating prizes could cause further defaults thereby initiating a cascade. The effects of leverage (asset to equity ratio), market crowding (number of banks per assets), diversification (as measured by the average degree of banks) and market impact (price change of an asset as a function of its volume) on the cascading process is studied. A major finding is that there is a critical leverage below which financial networks are immune to systemic events, but above which there is a finite probability for them. A theory based on generalized branching process is also developed. A point to note here is that the probability and extent of contagion due to fire sales behaves more or less in a similar way to that in the case of direct counter-party contagion as depicted in Fig. 4.

Compared to interbank lending network, the asset contagion network can be more reliably constructed from the data available with regulatory authorities. Unlike interbank lending relations, the structure of the balance sheet of banks are partially publicly available and can be used to construct empirical banks-assets networks. Huang et al. huang2013 ran an asset contagion model on US Commercial banks asset network. The latter is constructed using data from US Commercial Banks Balance Sheet Data (CBBSD) which classifies assets into thirteen different types. By running simulations on the empirical network, they could reproduce a large portion of actually failed banks during the 2007-09 crisis. Similar balance sheet structure of major European Banks is made available by the European Banking Authority (EBA) and has been used in several studies.

Banwo et al. banwo2016 considered the effects of power-law distributions for the degree of the network as well as for balance sheet size. They found that the power-law degree distribution makes the system less resilient towards the initial default of a randomly chose bank. Targeted initial defaults of biggest or less connected banks increase the probability of a default cascade. A power-law distribution for the assets, on the other hand, increases the resilience of the network with respect to random initial defaults but not with respect to targeted defaults. Caccioli et al. caccioli2015 studied the effect of both interbank and asset contagion channels working together. It is found that systemic effects are amplified when both channels are present.

4.2 Fire-walling financial networks

By now it should be clear that a crucial question in these contexts is to determine which of the banks are most important as far as the stability of the network is concerned. Identifying systemic institutions is crucial in developing strategies and policies to protect the financial system from contagion. A simple answer to this is the “too-big-to-fail” paradigm in which it is proposed that the largest banks are the most important ones (which are also presumably well connected). A complimenting one to this is the “too-central-to-fail” paradigm introduced by Battiston et al. battiston2012 where they introduced a centrality measure called Debt rank. Another centrality measure is the Systemicness of a bank introduced by Greenwood greenwood2015 which is proportional to the product of the size of a bank, its leverage, and connectedness. Information regarding these variables may not be readily obtainable, and Gangi gangi2015 discusses how to obtain Systemicness based on only partial data about the network. A recent addition to the list of various centrality measures is the one proposed by Cont & Schaanning cont2016 which is based on liquidity weighted portfolio overlaps. Also, the threat index by Demange demange2016 and the network proposed by Bertschinger & Stobbe bertschinger2018 are noteworthy in this context.

Cost of preventing contagion

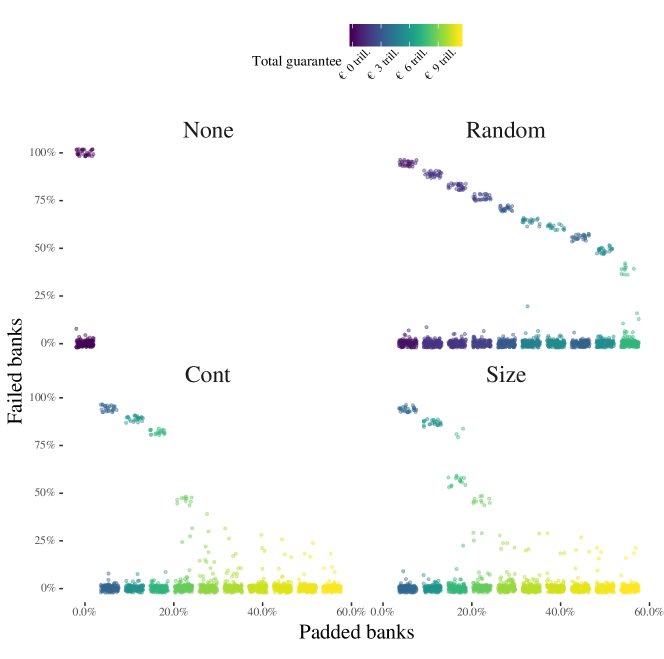

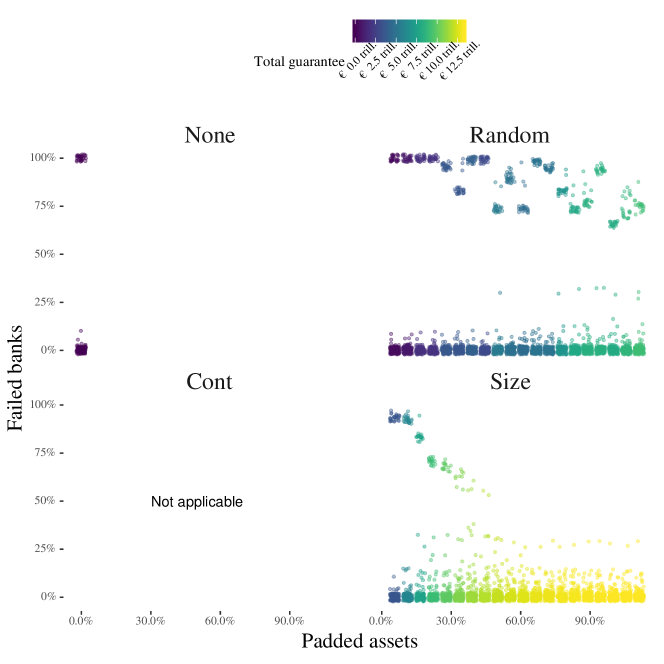

The proposed centrality measures should not just provide a better understanding of the systemic importance of financial institutions, but also should play a key role in designing cost-effective countermeasures to curtail the financial crisis. Here, we present a simulation study illustrating this idea. In particular, we study the model of Cont & Schaanning using portfolio holding data from the EBA (see cont2016 for additional details). The data set contains information about investments of the 90 largest European banks in about 140 asset classes, most finely disaggregated across European government bonds. We consider a shock scenario where a single asset is devalued by 30% and simulate ensuing banking defaults resulting from multiple rounds of fire-sale contagion. We investigate two ways of fire-walling the system against financial contagion: First via direct bail-out guaranties and second via asset price guaranties.

Fig. 6 shows the effectiveness of different bail-out strategies. Here, each dot corresponds to a shock scenario and is slightly jittered to reduce over-plotting. The all-or-nothing character of contagion is clearly visible with either almost no or all banks defaulting. Furthermore, providing bail-out guarantees to the most central banks first, i.e., 10% with the highest centrality, is more effective in preventing contagion than rescuing banks at random. Still, to fully avoid a systemic crisis guarantees on more than 5 trillion euros have to be granted towards more than 30 major banks (30% of 90 banks).

Fig. 7 shows the corresponding results of different buy-out strategies. In this case, instead of rescuing individual banks, prices of certain assets are guaranteed. Thus, even in case of a fire-sale, no price impact occurs on the guaranteed assets preventing any contagion via them. Again, providing buy-out guarantees in the order of decreasing systemic importance is found to be more effective than randomly buying them out. Still, at comparable sizes, buy-out guaranties are found to be less effective in preventing contagion than direct bank bail-outs. Note that the nominal size of the guarantee – as stated here and often quoted by the media during the financial crisis – can be much larger than the actual implementation cost sasi2019 especially if contagion is prevented.

5 Conclusion and Future directions

The rapidly increasing connectivity and complexity of the global financial system is a major concern in today’s world as it allows problems originating in one part to be quickly transmitted to seemingly distant and uncorrelated parts. Thus it has become ever more critical to understand the collective behavior of financial systems so that we can prevent or minimize contagious events. Viewing financial systems as complex networks is a significant step in this direction. The importance of macroprudential regulation in which more consideration is given to the health of the entire system than of individual institutions has now been recognized and is increasingly becoming a part of regulatory action.

In this review, we have tried to give a broad overview of various attempts to understand and model financial networks. A major theme arising out of these studies is the ‘robust-yet-fragile’ character of financial networks where contagious events are rare, but when they occur, they are widespread. Probability of contagion may be reduced by various regulatory measures such as requiring higher capital ratios and higher liquidity ratios. Identifying systemic institutions in a financial network is very important, and various centrality measures have been proposed for that. Protecting systemic institutions is crucial for the health of the entire system, but an issue here is how to set policies such that the institutions behave in a responsible way towards the health of the entire financial system. There is the problem of ‘moral hazard’ where a systemically important institution, with the full knowledge that it will be rescued in a crisis by taxpayers money, engages in reckless risk-taking behavior.

Financial networks are ever evolving and have continuously been subjected to many internal and external influences like regulatory constraints and factors from the economy. The technology underlying the formation of financial networks itself could change in the coming years with the use of Artificial Intelligence and formalizing financial contracts brammertz2018 . Another area to watch out for is the increasing presence of cryptocurrency borri2019 . All these have the potential to change the global landscape of financial networks. Including the effects of these and other future possibilities is a major challenge going forward. As we mentioned earlier, including the behavior of the banks in the face of a potential crisis is essential to model banking systems realistically. An area in which the current models lack realism is in the exclusion of central banks from modeling as the presence and actions of such a bank can have a significant effect on systemic risk georg2013 .

Banks and regulatory authorities often do not have a complete picture of various direct and indirect exposures of institutions in a financial network battiston2012a . Many recent studies try to integrate theoretical models with the available data to come up with conclusions about the possibility of systemic events and strategies or policies to contain them. With the availability of more and more real-time data and realistic models of bank behavior, it is expected that effective real-time monitoring of the health of financial systems will be a reality in the near future. Together with innovative taxation schemes, such as the one proposed by Poledna & Thurner poledna2016 , this might pave the way towards an economic future without systemic financial crises.

Acknowledgement

VS acknowledges support by University Grants Commission-BSR Start-up Grant No:F.30- 415/2018(BSR). NB thanks Dr. h.c. Maucher for funding his position.

References

- (1) Lieberman, E., Hauert, C., Nowak, M.A.: Evolutionary dynamics on graphs. Nature, 433(7023), 312 – 316 (2005).

- (2) Newman, M.E.: Spread of epidemic disease on networks. Physical review E, 66(1), 016128 (2002).

- (3) Dobson, I., Carreras, B.A., Lynch, V.E., Newman, D.E.: Complex systems analysis of series of blackouts: Cascading failure, critical points, and self-organization. Chaos: An Interdisciplinary Journal of Nonlinear Science, 17(2), 026103 (2007)

- (4) Castellano, C., Fortunato, S., Loreto, V.: Statistical physics of social dynamics. Reviews of modern physics, 81(2), 591 (2009).

- (5) Hasty, J., McMillen, D., Isaacs, F., Collins, J.J.: Computational studies of gene regulatory networks: in numero molecular biology. Nature Reviews Genetics, 2(4), 268 – 279 (2001)

- (6) Strogatz, S.H.: Exploring complex networks. Nature, 410(6825), 268 – 276 (2001)

- (7) Amaral, L.A., Ottino, J.M.: Complex networks. The European Physical Journal B, 38(2), 147 – 162 (2004)

- (8) Boccaletti,S., Latora, V., Moreno, Y., Chavez, M., Hwanga, D.U.: Complex networks: Structure and dynamic. Physics Reports, 424, 175 – 308 (2006)

- (9) Schweitzer, F., Fagiolo, G., Sornette, D., Vega-Redondo, F., Vespignani, A., White, D.R.: Economic networks: The new challenges. Science, 325, 422 – 425 (2009)

-

(10)

Haldane, A.G.: On microscopes and telescopes.

Speech retrieved from

www.bankofengland.co.uk/publications/Pages/speeches/default.aspx - (11) Farmer, J.D., Foley, D.: The economy needs agent-based modelling. Nature, 460, 685 – 686 (2009)

- (12) Catanzaro, M., Buchanan, M.: Network opportunity. Nature, 9, 121 – 123 (2013)

- (13) May, R.M., Levin, S.A., Sugihara, G.: Complex systems: ecology for bankers. Nature, 451, 893 – 895 (2008)

- (14) Haldane,A.G., May,R.M.: Systemic risk in banking ecosystems. Nature, 469, 351 – 355 (2011)

- (15) Gai, P., Haldane, A., Kapadia, S.: Complexity, concentration and contagion, Journal of Monetary Economics, 58, 453 – 470 (2011)

- (16) Karimi, F., Raddant, M. Cascades in real interbank markets. Comput. Econ., 47, 49 – 66 (2016)

- (17) Upper, C.: Simulation methods to assess the danger of contagion in interbank markets. Journal of Financial Stability, 7, 111 – 125 (2011)

- (18) Adrian, T., Shin, H.S.: Liquidity and leverage. J. Finan. Intermediation, 19, 418 – 437 (2010)

- (19) Allen, F., Gale, D.: Financial Contagion. Journal of Political Economy, 108(1), 1 – 33 (2000)

- (20) Nier, E., Yang, J., Yorulmazer, T., Alentorn, A.: Network models and financial stability. Journal of Economic Dynamics & Control, 31, 2033 – 2060 (2007)

- (21) Gai, P., Kapadia, S.: Contagion in financial networks. Proc. R. Soc. A, 466, 2401 – 2423 (2010)

- (22) May, R.M., Arinaminpathy, N.: Systemic risk: the dynamics of model banking systems. J. R. Soc. Interface, 7, 823 – 838 (2007)

- (23) Newman, M.: Networks: An introduction. Oxford University Press, Oxford (2010)

- (24) Huser, A.C.: Too interconnected to fail: A survey of the interbank networks literature. SAFE Working Paper No. 91, SSRN id 2577241 (2015)

- (25) Caccioli, F., Catanach, T.A., Farmer, J.D.: Heterogeneity, correlations and financial contagion. Advances in Complex Systems, 15(2), 1250058 (2012)

- (26) Eisenberg, L., Noe, T.H.: Systemic risk in financial systems. Management Science, 47(2), 236 – 249 (2001)

- (27) Paul Glasserman, P, Young, H.P., How likely is contagion in financial networks?, Journal of Banking & Finance, 50, 383 – 399 (2015)

- (28) Suzuki, T., Valuing corporate debt: The effect of cross-holdings of stock and debt. Journal of the Operations Research Society of Japan, 2, (2002)

- (29) Merton, R.C.: On the pricing of corporate debt: The risk structure of interest rates. Journal of Finance, 29(2), 449 – 470 (1974)

- (30) Fischer, T.: No-arbitrage pricing under systemic risk: Accounting for cross-ownership. Mathematical Finance, 24(1), 97–124 (2014)

- (31) Kusnetsov, M., Veraart, L.A.M.: Interbank clearing in financial networks with multiple maturities. SIAM Journal on Financial Mathematics, 10(1), 37 – 67 (2019)

- (32) Barucca, P., Bardoscia, M., Caccioli, F., D’Errico, M., Visentin, G., Battiston, S., Caldarelli, G.: Network Valuation in Financial Systems. SSRN id 2795583 (2016)

- (33) Ota, T.: Marginal contagion: A new approach to systemic credit risk. Bank of England, working paper (2014)

- (34) Demange, G.: Contagion in financial networks: A threat index. Management Science, 64(2), 955 – 970 (2016)

- (35) Bertschinger, N., Stobbe, J.: Systemic Greeks: Measuring risk in financial networks. arXiv:1810.11849 (2018)

- (36) Anand, K., Gai, P., Marsili, M.: Rollover risk, network structure and systemic financial crises. Journal of Economic Dynamics & Control, 36, 1088 – 1100 (2012)

- (37) Arinaminpathy, N., Kapadia, S., May, R.M.: Size and complexity in model financial systems. Proceedings of the National Academy of Sciences, 109(45), 18338 – 18343 (2012)

- (38) Simon, H.A.: The architecture of complexity. Proceedings of the American Philosophical Society, 106, 467 – 482 (1962)

- (39) Roukny, T., Bersini, H., Pirotte, H., Caldarelli, G., Battiston, S.: Default cascades in complex networks: Topology and systemic risk. Sci. Reports, 3, 2759 (2013)

- (40) Caccioli, F., Shrestha, M., Moore, C., Farmer, J.D.: tability analysis of financial contagion due to overlapping portfolios. Journal of Banking & Finance, 46, 233 – 245 (2014).

- (41) Huang, X., Vodenska, I., Havlin, S., Stanley, H.E.: Cascading Failures in Bi-partite Graphs: Model for Systemic Risk Propagation, Sci. Reports, 3, 1219 (2013)

- (42) Banwo, O., Caccioli, F., Harrald, P., Medda, F.: The effect of heterogeneity on financial contagion due to overlapping portfolios. Advances in complex systems, 19, 1650016-1 – 1650016-20 (2016)

- (43) Caccioli, F.,Farmer, J.D., Foti, N., Rockmore, D.: Overlapping portfolios, contagion, and financial stability. Journal of Economic Dynamics & Control, 51, 50 – 63 (2015)

- (44) Battiston, S., Puliga, M., Kaushik, R., Tasca, P., Caldarelli, G.: DebtRank: Too central to fail? Financial networks, the FED and systemic risk. Sci. Reports, 2, 541 (2012)

- (45) Greenwood, R., Landier, A., Thesmar, D.: Vulnerable banks. Journal of Financial Economics, 115, 471 – 485 (2015)

- (46) Gangi, D.D., Lillo, F., Pirino, D.: Assessing systemic risk due to fire sales spillover through maximum entropy network reconstruction. SSRN id 2639178 (2015)

- (47) Cont, R., Schaanning, E.: Fire sales, indirect contagion and systemic stress-testing. SSRN id 2541114 (2016)

- (48) Sasidevan, V., Bertschinger, N.: Fire-walling banks and assets: A network based approach. forthcoming (2019)

- (49) Brammertz, W., Mendelowitz, A.I.: From digital currencies to digital finance: the case for a smart financial contract standard. The Journal of Risk Finance, 19(1), 76 – 92 (2018)

- (50) Borri, N.: Conditional tail-risk in cryptocurrency markets. Journal of Empirical Finance, 50, 1-19 (2019)

- (51) Georg, C-P.: The effect of the interbank network structure on contagion and common shocks. Journal of Banking & Finance, 37, 2216 – 2228 (2013)

- (52) Battiston, S., Gatti, D.D., Gallegati, M., Greenwald, B., Stiglitz, J.E.: Default cascades: When does risk diversification increase stability?. Journal of Financial Stability, 8, 138 – 149 (2012).

- (53) Poledna, S., Thurner, S.: Elimination of systemic risk in financial networks by means of a systemic risk transaction tax. Quantitative Finance, 16(10), 1599 – 1613 (2016).