Testing and Estimating Change-Points in the Covariance Matrix of a High-Dimensional Time Series

Abstract.

This paper studies methods for testing and estimating change-points in the covariance structure of a high-dimensional linear time series. The assumed framework allows for a large class of multivariate linear processes (including vector autoregressive moving average (VARMA) models) of growing dimension and spiked covariance models. The approach uses bilinear forms of the centered or non-centered sample variance-covariance matrix. Change-point testing and estimation are based on maximally selected weighted cumulated sum (CUSUM) statistics. Large sample approximations under a change-point regime are provided including a multivariate CUSUM transform of increasing dimension. For the unknown asymptotic variance and covariance parameters associated to (pairs of) CUSUM statistics we propose consistent estimators. Based on weak laws of large numbers for their sequential versions, we also consider stopped sample estimation where observations until the estimated change-point are used. Finite sample properties of the procedures are investigated by simulations and their application is illustrated by analyzing a real data set from environmetrics.

Key words and phrases:

Keywords: Big data, Change-point, CUSUM transform, Data science, High-dimensional statistics, Projection, Spatial statistics, Spiked covariance, Strong approximation, VARMA processes1991 Mathematics Subject Classification:

MSC: 62E20, 62M10, 62H991. Introduction

High-dimensional big data arise in diverse fields such as environmetrics, engineering and finance. From a data science viewpoint statistical methods and tools are needed, which allow to answer questions posed to the data, and mathematical results justifying their validity under mild regularity conditions. The latter especially requires asymptotics for the case that the data dimension is large in comparison to the sample size. In this paper, a high-dimensional time series is model is studied and all asymptotic results allow for increasing dimension without any constraint relative to the sample size. The proposed procedures are investigate by simulations and applied to real data from environmetrics.

We study methods for the detection of a change-point in a high-dimensional covariance matrix and estimation of its location based on a time series. The proposed procedures investigate estimated bilinear forms of the covariance matrix, in order to test for the presence of a change-point as well as to estimate its location. The bilinear forms use weighting vectors with finite - resp. -norms which may even grow slowly as the sample size increases. This approach is natural from a mathematical point of view and has many applications in diverse areas: Analysis of projections onto subspaces spanned by (sparse) principal directions, infering the dependence structure of high-dimensional sensor data, e.g., from environmental monitoring, testing for a change of the autocovariance function of a univariate series or financial portfolio analysis, to mention a few. These problems have in common that the dimension can be large and may be even larger than the sample size . The results of this paper allow for this case and do not impose a condition on the growth of the dimension. Multivariate versions of CUSUM statistics are also considered.

The problem to detect changes in a sequence of covariance matrices has been studied by several authors and recently gained increasing interest, although the literature is still somewhat sparse. Going beyond the binary segmentation approach, [Cho and Fryzlewicz, 2015] propose a sparsified segmentation procedure where coordinate-wise CUSUM statistics are thresholded to segment the second-order structure. But these results do not cover significance testing. To test for a covariance change in a time series, [Galeano and Peña, 2007], who also give some historical references, consider CUSUM and likelihood ratio statistics for fixed dimension assuming a parametric linear process with Gaussian errors. Their CUSUM statistics, however, require knowledge of the covariance matrix of the innovations when no change is present. [Berkes et al., 2009] studied unweighted and weighted CUSUM change-point tests for a linear process to detect a change in the autocovariance function, but only for a fixed lag. Further, their theoretical results are restricted to the null hypothesis of no change. Kernel methods for this problem have been studied by [Steland, 2005] and [Li and Zhao, 2013]. [Aue et al., 2009] studied break detection in vector time series for fixed dimension and provide an approximation of the limiting distribution of their test statistic, an unweighted CUSUM, if is large. Contrary, the approach studied in this paper allows for growing dimension without any constraint such as , as typically imposed in random matrix theory, for some increasing function , e.g., exponential growth as in [Avanesov and Buzun, 2018] (which is, however, constrained to i.i.d. samples), or (again for i.i.d. samples) asymptotics for the eigenstructure under the assumption for the spiked eigenvalues , [Wang and Fan, 2017], which allows for provided the eigenvalues diverge.

It is shown that, for the imposed high-dimensional time series model, (weighted) CUSUM statistics associated to the sample covariance matrix can be approximated by (weighted) Gaussian bridge processes. Under the null hypothesis this follows from [Steland and von Sachs, 2017] and one can also consider an increasing number of such statistics by virtue of the results in [Steland and von Sachs, 2018]. The asymptotics under a change-point regime, however, is more involved and is provided in this paper. Both single CUSUM statistics and multivariate CUSUM transforms corresponding to a set of projection vectors are studied. The dimension of the time series as well as the dimension of the multivariate CUSUM transform is allowed to grow with the sample size in an unconstrained way. The results of this paper extend [Steland and von Sachs, 2017, Steland and von Sachs, 2018], especially by studying weighted CUSUMs, providing refined martingale approximations and relaxing the conditions on the projection vectors.

Further, consistent estimation of the unknown variance and covariance parameters is studied without the need to estimate eigenstructures. As well known, this essentially would require conditions under which the covariance matrix can be estimated consistently in the Frobenius norm, which needs the restrictive condition on the dimension according to the results of [Ledoit and Wolf, 2004] and [Sancetta, 2008], or requires to assume appropriately constrained models. Estimators for the asymptotic variance and covariance parameters associated to a single resp. a set of CUSUM statistics have already been studied under the no-change hypothesis in [Steland and von Sachs, 2017] and [Steland and von Sachs, 2018]. These estimators are now studied under a change-point model, generalized to deal with two pairs of projection vectors describing the asymptotic covariance between pairs of (weighted) CUSUMs and studied from a sequential viewpoint which allows us to to propose stopped-sample estimators using the given sample until the estimated change point. This is achieved by proving a uniform law of large numbers for the sequential estimators.

Closely related to the problem of testing for a change-point is the task of estimating its location. It is shown hat the change-point estimator naturally associated to the weighted or unweighted CUSUM statistic is consistent. As a consequence, the well known iterative binary segmentation algorithm, dating back to [Vostrikova, 1981], can be used to locate multiple change points.

The organization of the paper is as follows. Section 2 introduces the framework, discusses several models appearing as special cases, introduces the proposed methods and discusses how to select the projection vectors. The asymptotic results are provided in Section 3. They cover strong and weak approximations for the (weighted) partial sums of the bilinear forms and for associated CUSUMs as well as consistency theorems for the proposed estimators of unknowns. Section 4 considers the problem to estimate the change-point. Simulations are presented in Section 5. In Section 6 the methods are illustrated by analyzing the dependence structure of ozone measurements from monitors across the United States over a five-year-period. Main proofs are given in Section A, whereas additional material is deferred to an appendix.

2. Model, assumptions and procedures

2.1. Notation

Throughout the paper for two arrays of real numbers means that there exists a constant , such that for all . denotes the underlying probability space on which the vector time series is defined. denotes expectation (w.r.t. ), the variance and the covariance. For a logical expression we let denote the associated indicator function. If is a set, then is the usual characteristic function, whereas for denotes the -vector with entries and is the null -vector. is the vector-2 norm, , , the -norm for sequences and the maximum norm for sequences or vectors. denotes the semi norm for a linear operator on a Hilbert space with inner product . denotes weak convergence of a sequence of càdlàg processes in the Skorohod space equipped with the usual metric.

2.2. Time series model and assumptions

Let us assume that the coordinates of the vector time series are given by

| (1) |

for coefficients and independent zero mean errors satisfying the following two assumptions.

Assumption (D): An array of real numbers satisfies the decay condition (D), if for some

| (2) |

Assumption (E): , is an array of independent mean zero random variables with and moment arrays , , satisfying

for some and sequences and .

The assumptions on and allow for a certain degree of inhomogeneity of the second and third moments. Especially, under the change-point model described below, where the coefficients of the linear processes change after the change-point , these assumptions cover weak effects of the change on the second resp. third moments. An example satisfying the conditions is given by

for two positive constants and , , with and .

2.3. Spiked covariance model

The spiked covariance model is a common framework to study estimation of the eigenstructure for high-dimensional data. For let and let , , be orthonormal vectors with for . Assume that

| (3) |

The leading eigenvalues of under model (3) are , , and represent spikes in the spectrum, which is otherwise flat and given by . The assumption that the eigenvectors are -bounded is common in high-dimensional statistics, especially when assuming a spiked covariance model: [Johnstone and Lu, 2009] have shown that principal component analysis (PCA) generates inconsistent estimates of the leading eigenvectors if , which motivated developments on sparse PCA. Minimax bounds for sparse PCA have been studied by [Birnbaum et al., 2013] under -constraints on the eigenvectors for . For example, the simple diagonal thresholding estimator of the th leading eigenvector of [Johnstone and Lu, 2009] satisfies and the iterated version of [Ma, 2013] attains the optimal rate , see also [Paul and Johnstone, 2007]. An sparseness assumption on the eigenvectors is weaker than the (joint) -sparseness condition on the row support of matrix of eigenvectors imposed in [Cai et al., 2015], who study optimal estimation under the spectral norm.

Model (3) can be described in terms of (1): Let , , , and , , . Then for i.i.d the MA() series have the covariance matrix (3). The decay condition (D) follows from .

We may conclude that our methodology covers the above spiked covariance under which sparse PCA provides consistent estimates of the leading eigenvectors, which are an attractive choice for the projection vectors on which the proposed change-point procedures are based on. The literature on such consistency results is, however, not yet matured and typically assumes i.i.d. data vectors, whereas the framework studied here considers time series.

2.4. Multivariate linear time series and VARMA processes

The above linear process framework is general enough to host classes of multivariate linear processes and vector autoregressive models with respect to a -variate noise process, . These processes are usually studied for a sequence of innovations, but since our constructions work for arrays, we consider this setting.

Multivariate linear processes: Let be integers and define the -variate innovations

based on . If have homogeneous variances, then iff. , , such that for large enough , , the innovations are arbitrarily close to white noise. Let , be -dimensional matrices with row vectors , , for . Then the -dimensional linear process

has coordinates which attain the representation

| (4) |

. If we assume that the elements of the coefficient matrices satisfy the decay condition

then the coefficients of the series (4) satisfy , i.e., Assumption (D) holds. In this construction the lags used to define the -variate innovation process may depend on .

We may go beyond the above near white noise -variate innovations and consider -dimensional linear processes with mean zero innovations , , with a covariance matrix close to some : Let

| (5) |

where

| (6) |

for , is a full rank matrix and are coefficient matrices as above, i.e., with elements satisfying the decay condition. is used to reduce the dimensionality. Let be the singular value decomposition of with singular values , left singular vectors and right singular vectors satisfying , , . Then and the element at position of the latter matrix is given by which is if the eigenvalues and eigenvectors are bounded. Therefore, the class of processes (A.1) is a special case of (1).

The case , especially leading to the usual definition of a -dimensional linear process, can be allowed for when imposing the conditions

| (7) |

with and assuming that the operators , , are trace class operators in the sense that , with eigenvectors satisfying . For we let such that are the eigenvectors and the eigenvalues of . Then verifying (D), as shown in the appendix. The constraint on the eigenvectors can be omitted when imposing the stronger condition on the coefficient matrices. For details see the appendix.

VARMA Models: Let us consider a -dimensional zero mean VARMA() process

with colored -variate innovations as in (A.1). and are coefficient matrices. Let us assume that each of these coefficient matrices satisfies (7) with for some , when denoting its elements by , . Recall that the process is stable, if for . Then the operator , where denotes the lag operator, is invertible, the coefficient matrices, , of are absolutely summable, and one obtains the MA representation As well known, the coefficient matrices, , can be calculated using the recursion where for . Using these formulas one can show that the coefficient matrices, , of the MA representation satisfy (7) when denoting its elements by , and therefore the VARMA coordinate processes , , with innovations (6) satisfy the decay condition (D).

Another interesting class of time series to be studied in future work are factor models, which are of substantial interest in econometrics. For detection of changes resp. breaks we refer to [Breitung and Eickmeier, 2011], [Han and Inoue, 2015] and [Horváth and Rice, 2019], amongst others.

2.5. Change-Point Model and Procedures

The change-point model studied in this paper considers a change of the coefficients defining the linear processes. Nevertheless, all procedures neither require their knowledge nor their estimation. So let and be two different coefficient arrays satisfying the decay assumption and put

It is further assumed that and are such that

| (8) |

We will study CUSUM type procedures based on quadratic and bilinear forms of sample analogs of those variance-covariance matrices, in order to detect a change from to . Let Assumption (8) ensures that .

The change-point model for the high-dimensional time series is now as follows. For some change-point it holds

| (9) |

with underlying error terms , , , satisfying Assumption (E). Our results on estimation of , however, assume that the change occurs after a certain fraction of the sample by requiring that

| (10) |

for some . We are interested in testing the change-point problem

which implies a change in the second moment structure of the vector time series when holds, and in estimation of the change-point to locate the change. Under the null hypothesis the covariance matrix of , , is given by whereas it changes unter the alternative hypothesis from to If , then the change is present in the sequence of the associated quadratic forms, which change from to if , and the change-point test below will be based on an estimator of that bilinear form. A natural condition to ensure that this relationship holds asymptotically, yielding consistency of the proposed test, is

| (11) |

We shall, however, also discuss in Section 3.2 more general conditions for the detectability of a change.

To introduce the proposed procedures, define the partial sums of the outer products ,

such that is the sample variance-covariance matrix using the data . Let

Consider the CUSUM-type statistic,

The large sample approximations for obtained in [Steland and von Sachs, 2017] under , and generalized in this paper, imply that can be approximated by a Brownian bridge process, . Hence, we can reject the null hypothesis of no change at the asymyptotic level , if

| (12) |

where is a consistent estimator for the asymtotic standard deviation associated to the series , and is the -quantile, , of the Kolmogorov distribution function, , . One may also use a weighted CUSUM test

for some weight function , whose role is to compensate for the fact that the centered cumulated sums get small near the boundaries. The results of Section 3.2 provide large sample approximations for a large class of weighting functions. An attractive choice would be the weight function , but the corresponding supremum of the standardized Brownian bridge, , , is not well defined due to the law of the iterated logarithm (LIL), requiring to use Gumbel-type extreme value asymptotics, [Csörgő and Horváth, 1997], known to converge slowly, see, e.g., [Ferger, 2018]. For a discussion of the class of proper weight functions ensuring that is a.s. finite we refer to [Csörgő and Horváth, 1993]. One may use the weight function for some or any weight function satisfying

| (13) |

Therefore, one rejects the no-change null hypothesis, if

| (14) |

where denotes the quantile function of the law of . As studied in [Ferger, 2018], one may also standardize the unweighted CUSUM statistic by its maximizing point, i.e., substitute by . The associated Brownian bridge standardized by its argmax attains a density wich has been explicitly calculated in [Ferger, 2018].

When the assumption that the vector time series has mean zero is in doubt, one may modify the above procedures by taking the cumulated outer products of the centered series, , where . The associated weigthed CUSUM statistics are then given by

and the null hypothesis is rejected using the rule (14) with replaced by .

To estimate the unkown change-point , we propose to use the estimator

Based on the estimator of the change-point, one may also estimate the nuisance parameter by .

For pairs of projection vectors , , consider the associated CUSUM transform

Observe that this transform differs from the transform studied in [Wang and Samworth, 2018], where the statistics are calculated coordinate-wise and the transform is given by the corresponding CUSUM trajectories.

We wish to test the null hypothesis of no change w.r.t. to

against the alternative hypothesis that, induced by a change at , at least one bilinear form changes (assuming the projections are appropriately selected),

As a global (omnibus) test one may reject at the asymptotic significance level , if

| (15) |

Here is a non-standard quadratic form, as it is based on the CUSUMs instead of a multivariate statistic which is asymptotically normal, , is the Moore-Penrose generalized inverse of and denotes the -quantile of the simulated distribution of using a Monte Carlo estimate of ; the estimators of the asymptotic covariance of the th and th coordinate of the CUSUM transform are defined in the next section, calculated from a learning sample. It is worth mentioning that the statistic can be used to test for a change in the subspace by putting , .

2.6. Choice of the projections

The question arises how to choose the projection vectors . Their choice may depend on the application. Here are some examples.

Example 1.

(Change of sets of covariances as in gene expression time series)

Time series gene expression studies investigate the gene expression levels of a large number of genes measured at several time points, in order to identify and analyze activated genes and their relationship in a biological process, see [Bar-Joseph et al., 2012]. Going beyond the expression levels and analyzing the dependence structure of gene expression is of interest. For example, a group of genes may be uncorrelated to others or the rest of the genome, but interactions inducing correlations may start after an external stimulus. To analyze two groups, e.g., the first and the last variables, one may use

corresponding to

the average covariance between the first and the last coordinates. Further, in order to compare the first variables with the remaining ones, one could use with .

Example 2.

(Spatial clustered sensors)

Suppose that the observed variables represent sensors of clusters or groups, e.g., sensors spatially distributed over geographic regions such as states. Such a classification is given by a partition with pairwise disjoint sets , . To analyze the within-region and between-region covariance structures, one may consider the orthogonal sytem given by the vectors , . Our results allow for the case of region-wise infill asymptotics where increases with the sample size. In our data example, the grouping is, however, determined by a sparse PCA instead of using geographic locations.

Example 3.

(Change in the autocovariance function (ACVF) of a stationary time series)

Our high-dimensional time series model also allows to analyze the ACVF of a stationary time series. Let be a stationary linear time series with coefficients , , satisfying Assumption (D) and define

Then is a special case of model (1), and the change-point model (9) analyzes a change of the coefficients of in terms of the ACVF up to the lag respectively a change of the ACVF due to a change of the underlying coefficients. Since then the sample covariance matrix consists of the sample autocovariance estimators, the proposed CUSUM tests consider a weighted averages of them and taking unit vectors for leads to a procedure closely related to the CUSUM test studied in [Berkes et al., 2009]. Changes in autocovariances have also been studied by [Na et al., 2011] from a parametric point of view and by [Steland, 2005] and [Li and Zhao, 2013] using kernel methods.

Example 4.

(Financial portfolio analysis)

In financial portfolio optimization one is given a stationary time series of returns of assets and seeks a portfolio vector representing the number of shares to hold from each asset. The variance-minimizing portfolio is obtained by minimizing the portfolio risk under the constraint . In order to keep transactions costs moderate, sparsity constraints can be added, see, e.g., [Brodie et al., 2009] where a -penalty term is added. For bounds and confidence intervals of the risk of the optimal portfolio see [Steland, 2018].

In some applications selecting them from a known basis may be the method of choice. In low- and high-dimensional multivariate statistics it is, however, a common statistical tool to project data vectors onto a lower dimensional subspace spanned by (sparse) directions (axes) . These directions can be obtained from a fixed basis or by a (sparse) principal component analysis using a learning sample. The projection is determined by the new coordinates , , for simplicity also called projections, and represent a lower dimensional compressed approximation of . The uncertainty of its coordinates, i.e., of its position in the subspace, can be measured by the variances . Clearly, it is of interest to test for the presence of a change-point in the second moment structure of these new coordinates by analyzing the bilinear forms , . Also observe that one may analyze the spectrum, since for eigenvectors the associated eigenvalue is given by .

The question under which conditions PCA or sparse PCA is consistent has been studied by various authors. The classic Davis-Kahan theorem, see [Davis and Kahan, 1970] and [Yu et al., 2015] for a statistical version, relates this to consistency of the sample covariance matrix in the Frobenius norm, which generally does not hold under high-dimensional regimes without additional assumptions, and minimal-gap conditions on the eigenvalues. Standard PCA is known to be inconsistent, if , where here and in the following discussion a possible dependence of on is suppressed. Under certain spiked covariance models consistency can be achieved, see [Johnstone and Lu, 2009] if , [Paul, 2007] under the condition and [Jung and Marron, 2009] for fixed and . Sparse principal components, first formally studied by [Jolliffe et al., 2003] using lasso techniques, are strongly motivated by data-analytic aspects, e.g., by simplifying their interpretation, since linear combinations found by PCA typically involve all variables. Consistency has been studied under different frameworks, usually assuming additional sparsity constraints on the true eigenvectors (to ensure that their support set can be identfied) and/or growth conditions on the eigenvalues (to ensure that the leading eigenvalues are dominant in the spectrum). We refer to [Shen et al., 2013] for simple thresholding sparse PCA when is held fixed and , [Birnbaum et al., 2013] for results on minimax rates when estimating the leading eigenvectors under -constraints on the eigenvectors and fixed eigenvalues, whereas [Cai et al., 2015] provide minimax bounds assuming at most entries of the eigenvectors are non-vanishing and [Wang and Fan, 2017] derives asymptotic distributions allowing for diverging eigenvalues and .

To avoid that a change is not detectable because it takes place in a subspace of the orthogonal complement of the chosen projection vectors, a simple approach used in various areas is to take random projections. For example, one may draw the projection vectors from a fixed basis or, alternatively, sample them from a distribution such as a Dirichlet distribution or an appropriately transformed Gaussian law. Random projections of such kind are also heavily used in signal processing and especially in compressed sensing, by virtue of the famous distributional version of the Johnson-Lindenstrauss theorem, see [Johnson and Lindenstrauss, 1984]. This theorem states that any points in a Euclidean space can be embedded into dimensions such that their distances are preserved up to , with probability larger than . This embedding can be constructed with -sparsity of the associated projection matrix, see [Kane and Nelson, 2014].

This discussion is continued in the next section after Theorem 2 and related to the change-point asymptotics established there.

3. Asymptotics

The asymptotic results comprise approximations of the CUSUM statistics and related processes by maxima of Gaussian bridge processes, consistency of Bartlett type estimators of the asymptotic covariance structure of the CUSUMs, stopped sample versions of those estimators and consistency of the proposed change-point estimator.

3.1. Preliminaries

To study the asymptotics of the proposed change-point test statistics both under and , we consider the two-dimensional partial sums,

| (16) |

and their centered versions,

| (17) |

for , where for brevity and are defined by

for and .

Introduce the filtrations , , . In Lemma 2 it is shown that can be approximated by a -martingale array with asymptotic covariance parameter defined in Lemma 1, see (48). Denote by , for , the associated asymptotic variance parameter.

As a preparation, let , , be a two-dimensional mean zero Brownian motion with variance-covariance matrix

| (18) |

For define the Gaussian processes

| (19) | ||||

Before the change, is the Brownian motion with variance and after the change it behaves as the Brownian motion with start in and variance . Further define

As shown in the appendix, it holds

| (20) |

3.2. Change-point Gaussian approximations

Closely related to the CUSUM procedures are the following càdlàg processes: Define

and the introduce the associated bridge process

Observe that its expectation is and vanishes, if . But a non-constant series , , may lead to . This particularly holds for the change-point model. Our results show that () can be approximated by a Brownian (bridge) process and lead to a FCLT under weak regularity conditions, and the same holds true for weighted version of theses càdlàg processes for nice weighting functions .

Define for

and

The following theorem extends the results of [Steland and von Sachs, 2017, Steland and von Sachs, 2018] and justifies the proposed tests (12) and (14) when combined with the results of the next section on consistency of the asymptotic variance parameters. This and all subsequent results consider the basic time series model (1), but all results hold for the multivariate linear processes and VARMA models introduced in Section 2 under the conditions discussed there.

Theorem 1.

Suppose that satisfies Assumption (E). Let be weighting vectors with -norms satisfying

| (21) |

and let and be coefficients satisfying Assumption (D). If the change-point model (9) holds, then, for each , one may redefine, on a new probability space, the vector time series together with a two-dimensional mean zero Brownian motion with coordinates , , , characterized by the covariance matrix (18) associated to the parameters , assumed to be bounded away from zero, and , such that for some constant the following assertions hold true almost surely:

-

(i)

, .

-

(ii)

, .

-

(iii)

, .

-

(iv)

, .

-

(v)

, .

-

(vi)

, .

If , then we also have

-

(vii)

, a.s., as ,

-

(viii)

, a.s., as ,

where , . Further, provided the weight function satisfies (13), the corresponding above assertions hold in probability, if . Especially,

| (22) |

and

| (23) |

Remark 1.

Provided the original probability space, , is rich enough to carry an additional uniform random variable, the strong approximation results of Theorem 1 can be constructed on .

When there is a change, the drift term yields the consistency of the test.

Note that Theorem 1 holds without the conditions (10) and (11). To discuss conditions of detectability of a change, observe that the drift of the approximating Gaussian process in (22) is given by

If this function is asymptotically constant, especially if for all but (which implies by (8) and Lemma 1) and , then the change is asymptotically not detectable, since the asymptotic law is the same as under the null hypothesis. Now assume . A change located in a measurable set with positive Lebesgue measure is detectable and changes the asymptotic law, if for some function on , since then the asymptotic law is given by , or if cf. Theorem 2. The case corresponds to a local alternative such as for some matrix such that exists. For example, if in the spiked covariance model (3) a new local spike term of the form appears after the change-point, then and . Condition (11) is then satisfied, if the weighting vectors are not asymptotically orthogonal to the direction of the new spike.

Observe that is linear in . Clearly, is maximized if is a leading eigenvector of . This can be seen from the spectral decomposition , where are the eigenvectors and the eigenvalues. When there is no knowledge about the change, e.g., in terms of the and/or or in terms of the model coefficients , it makes sense to select from a known basis or as leading (sparse) eigenvectors of , estimated from a learning sample, in order to obtain a procedure which is capable to react, if the dominant part of the eigenstructure of the covariance matrix changes. Clearly, a change in the orthogonal complement of chosen projection vectors is not detectable. This can be avoided by considering, in addition, random projection(s).

For the CUSUM statistics based on the centered time series we have the following approximation result.

Theorem 3.

Let the original probability space be rich enough to carry an additional uniform random variable. Assume the conditions of Theorem 1 and the strengthended decay condition for some hold. Suppose that the vector time series is centered at the sample averages , before applying the CUSUM procedures, leading to the statistics and . Then assertions (i) and (ii) of Theorem 1 hold true with an additional error term and (iii)-(vi) with an additional term. Finally, (vii) and (viii) hold in probability, if .

The above theorems assume that the projection vectors and have uniformly bounded -norm. When standardizing by a homogenous estimator , i.e. satisfying

| (24) |

for all , one can relax the conditions on the projections .

Theorem 4.

Suppose that satisfies Assumption (E). Assume that

| (25) |

or there are non-decreasing sequences with

| (26) |

Suppose that the estimator used by is ratio consistent and homogenous. Further, let and be coefficients satisfying Assumption (D). If the change-point model (9) holds, then, under the construction of Theorem 1 with , (vi) holds and we have for any weight function satisfying (13)

| (27) |

where , .

By Theorem 1, statistical properties of the CUSUM statistic can be approximated by those of . In view of Theorem 4, for the standardized CUSUM statistic one replaces by a process which is a Browninan bridge with covariance function up to and after the change. Especially, under the null hypothesis of no change, we have , for all and , and by (8) and Lemma 1. Then the asymptotics of the change-point procedures is governed by a standard Brownian bridge. Theorems 1, 4 and 3 (under the strenghtened decay condition) imply FCLTs.

Theorem 5.

(FCLT) If , for , and , as , then under the conditions of Theorem 1 (viii) or Theorem 4 it holds

with , , in the Skorohod space , for some Gaussian bridge process defined on with if or , and , if . Further, if are weighting vectors satsfying (21), (25) or (26) and if the constructions of Theorem 1 and Theorem 4, respectively, hold with , then for any weight function which satisfies (13) we have

3.3. Multivariate CUSUM approximation

Let us now consider CUSUM statistics where

, defined for pairs , , of projection vectors. When using no weights, i.e., , , the corresponding quantities are denoted .

Let , , be a -dimensional mean zero Brownian motion with covariance matrix

| (28) |

with blocks

where, for brevity, with , . Also put , , , see (48). Define the processes

where , and .

Theorem 6.

Suppose that satisfies Assumption (E). Let , , be weighting vectors satisfying (21) uniformly in , and let and be coefficients satisfying Assumption (D). Then, under the change-point model (9), one can redefine, for each , on a new probability space, the vector time series together with a -dimensional mean zero Brownian motion with covariance function given by (28), such that

| (29) |

and for a weight function satisfying (13), for any

| (30) |

where with , .

Observe that under the asymptotic covariance matrix of the approximating process and hence of is given by , whose diagonal is given by the elements and off-diagonal elements by , . For fixed the results of the next section show that can be estimated consistently, providing a justification for the test (15) when is regular.

3.4. Full-sample and stopped-sample estimation of and

Let us now discuss how to estimate the parameter for one pair of projection vectors, which is used in the change-point test statistic for standardization, and the asymptotic covariance parameters for two pairs and , which arise in the multivariate test for a set of projections. If there is no change, one may use the proposal of [Steland and von Sachs, 2017]. But under a change these estimators are inconsistent. The common approach is therefore to use a learning sample for estimation. Alternatively, one may estimate the change-point and use the data before the change. The consistency of that approach follows quite easily when establishing a uniform weak of large numbers of the sequential (process) version of the estimators which uses the first observations, , where is a fraction of the sample size so that for :

Fix and define for

where

for , with . The estimators and , , corresponding to two pairs of projection vectors, are defined analogously, i.e.,

| (31) |

with

| (32) |

for with , .

The weights are often defined through a kernel function via for some bandwidth parameter . For a brief discussion of common choices see [Steland and von Sachs, 2017].

The following theorem establishes the uniform law of large numbers. Especially, it shows that is consistent for if , whereas for a convex combination of and is estimated. A similar result applies to the estimator of the asymptotic covariance parameter.

Theorem 7.

Assume that with , as , and the weights satisfy

-

(i)

, as , for all , and

-

(ii)

, for some constant , for all , .

If the innovations are i.i.d. with , , for all and , satisfy the decay condition

for some , and , then under the change-in-coefficients model (9) with , , it holds for any

as , where for . Further,

where for for , as defined in Lemma 1.

Let us now suppose we are given a consistent estimator of the unknown change-point; in the next section we make a concrete proposal. In order to estimate the parameter it is natural to use the above estimator using all observations classified by the estimator as belonging to the pre-change period. This means, we estimate by . The following result shows that this estimator is consistent under weak conditions.

Theorem 8.

Suppose that is an estimator of satisfying a.s. and as . Then

4. Change-point estimation

In view of the change-point test statistic studied in the previous section, it is natural to estimate the change-point by

(By convention, denotes the smallest maximizer of some function .)

The expectation of is a function of , and we assume that the limit

| (33) |

exists. To proceed, we need further notation. Put

| (34) |

and introduce the associated rescaled functions

| (35) | ||||

| (36) |

and

| (37) |

If , then for the function is strictly increasing on and strictly decreasing on , and for the same holds for . The same applies for any weight function such that

| (38) | is continuous, increasing on and decreasing on . |

Obviously, this holds for a large class of functions whatever the value of the true change-point. Hence, we expect that the maximizers of , , and its estimator , , converge to the true change-point . But the maximizers of and of are related by

| (39) |

Therefore, since is constant on , and vanishes on , , as implies , as .

A martingale approximation and Doob’s inequality provide the following uniform convergence.

The consistency of the change-point estimator follows now easily from the above results.

5. Simulations

To investigate the statistical performance of the change-point tests a change from a family of AR() series to a family of (shifted) MA() series, which are, at lag , independent, was examined: We assume that these series, , are defined as follows. Fix and let

with , for and , i.i.d. standard normal and , , , so that the marginal variances of the time series do not change. The asymptotic variance parameter, , was estimated with lag truncation justified by simulations not reported here, using three sampling approaches: (i) Learning sample of size , (ii) full in-sample estimation and (iii) stopped in-sample estimation using the modified rule . Although this modification may lead to some bias, the actual number of observations was increased, since otherwise the sample size for estimation may be too small.

Both a fixed and a random projection were examined. The case of a fixed projection vector was studied by using . Random projections were generated by drawing from a Dirichlet distribution, such that the projections have unit norm and expectation , in order to study the effect of random perturbations around the fixed projections.

Table 2 provides the rejection rates for and dimensions when the change-point is given by with , to study changes within the central of the data as well as early and late changes. First, one can notice that the power is somewhat increasing in the dimension but quickly saturates. The results for stopped-sample and in-sample estimation are quite similar. The unweighted CUSUM procedure has very accurate type I error rate if a learning sample is present, whereas the weighted CUSUM overreacts somewhat under the null hypothesis. For stopped-sample and in-sample estimation the unweighted procedure is conservative, whereas the weighted CUSUM keeps the level quite well with only little overreaction. Although the unweighted CUSUM operates at a smaller significance level, it is more powerful than the weighted procedure when the change occurs in the middle of the sample, but the weighted CUSUM performs better for early changes. The results for a random projection are very similar.

The accuracy and power of the global test related to the CUSUM transform was examined for a change to a MA model after half of the sample for the sample size . The design of this study is data-driven as the principal directions calculated for the ozone data set were used in addition to random projections. The global test based on the weighted CUSUM transform using the weight function with was fed with the first poejctions for various values of . The results are provided in Table 1. Each entry is based on runs. According to these figures, the proposed global test is accurate in terms of the significance level and quite powerful.

| level | power | |

|---|---|---|

6. Data example

To illustrate the proposed methods, we analyze daily observations of 8 hour maxima of ozone concentration collected at monitors in the U.S.. The data corresponds to the 5-year-period from January 2010 to December 2014. We analyze mean corrected data, see [Schweinberger et al., 2017], namely residuals obtained after fitting cubic splines to the log-transformed data, in order to correct level and seasonal ups and downs.

| Fixed projection | ||||||||

|---|---|---|---|---|---|---|---|---|

| 10 | 100 | 200 | 10 | 100 | 200 | |||

| Method | Unweighted CUSUM | Weighted CUSUM | ||||||

| 10 | 100 | 200 | 10 | 100 | 200 | |||

| 0.10 | 0.03 | 0.02 | 0.02 | 0.10 | 0.15 | 0.14 | 0.14 | |

| 0.25 | 0.31 | 0.34 | 0.34 | 0.25 | 0.35 | 0.37 | 0.38 | |

| L=500 | 0.50 | 0.70 | 0.75 | 0.77 | 0.50 | 0.55 | 0.59 | 0.61 |

| 0.75 | 0.39 | 0.46 | 0.46 | 0.75 | 0.33 | 0.40 | 0.38 | |

| 0.90 | 0.07 | 0.08 | 0.08 | 0.90 | 0.09 | 0.08 | 0.09 | |

| 1.00 | 0.05 | 0.06 | 0.05 | 1.00 | 0.09 | 0.11 | 0.10 | |

| 0.10 | 0.14 | 0.14 | 0.09 | 0.10 | 0.79 | 0.98 | 0.99 | |

| 0.25 | 0.79 | 0.88 | 0.88 | 0.25 | 0.86 | 0.93 | 0.92 | |

| stopped-sample | 0.50 | 0.90 | 0.93 | 0.93 | 0.50 | 0.70 | 0.72 | 0.71 |

| 0.75 | 0.29 | 0.30 | 0.29 | 0.75 | 0.17 | 0.17 | 0.18 | |

| 0.90 | 0.03 | 0.02 | 0.02 | 0.90 | 0.04 | 0.03 | 0.04 | |

| 1.00 | 0.02 | 0.01 | 0.01 | 1.00 | 0.07 | 0.07 | 0.08 | |

| 0.10 | 0.14 | 0.13 | 0.11 | 0.10 | 0.79 | 0.98 | 0.99 | |

| 0.25 | 0.79 | 0.87 | 0.86 | 0.25 | 0.86 | 0.93 | 0.92 | |

| in-sample | 0.50 | 0.90 | 0.92 | 0.93 | 0.50 | 0.69 | 0.73 | 0.72 |

| 0.75 | 0.29 | 0.30 | 0.29 | 0.75 | 0.17 | 0.17 | 0.18 | |

| 0.90 | 0.03 | 0.02 | 0.02 | 0.90 | 0.04 | 0.04 | 0.04 | |

| 1.00 | 0.02 | 0.02 | 0.02 | 1.00 | 0.08 | 0.08 | 0.07 | |

| Random projection | ||||||||

| Method | Unweighted CUSUM | Weighted CUSUM | ||||||

| 10 | 100 | 200 | 10 | 100 | 200 | |||

| 0.10 | 0.02 | 0.02 | 0.02 | 0.10 | 0.14 | 0.14 | 0.14 | |

| 0.25 | 0.32 | 0.36 | 0.36 | 0.25 | 0.36 | 0.39 | 0.39 | |

| 0.50 | 0.71 | 0.77 | 0.76 | 0.50 | 0.54 | 0.60 | 0.61 | |

| 0.75 | 0.39 | 0.46 | 0.46 | 0.75 | 0.33 | 0.39 | 0.39 | |

| 0.90 | 0.08 | 0.08 | 0.08 | 0.90 | 0.09 | 0.09 | 0.10 | |

| 1.00 | 0.05 | 0.05 | 0.05 | 1.00 | 0.10 | 0.10 | 0.09 | |

| 0.10 | 0.13 | 0.15 | 0.11 | 0.10 | 0.80 | 0.98 | 0.99 | |

| 0.25 | 0.80 | 0.86 | 0.87 | 0.25 | 0.85 | 0.92 | 0.92 | |

| stopped-sample | 0.50 | 0.90 | 0.93 | 0.93 | 0.50 | 0.70 | 0.72 | 0.72 |

| 0.75 | 0.28 | 0.29 | 0.30 | 0.75 | 0.18 | 0.17 | 0.17 | |

| 0.90 | 0.03 | 0.03 | 0.03 | 0.90 | 0.04 | 0.04 | 0.04 | |

| 1.00 | 0.02 | 0.02 | 0.02 | 1.00 | 0.08 | 0.07 | 0.07 | |

| 0.10 | 0.14 | 0.14 | 0.11 | 0.10 | 0.80 | 0.98 | 0.98 | |

| 0.25 | 0.79 | 0.87 | 0.87 | 0.25 | 0.86 | 0.92 | 0.92 | |

| in-sample | 0.50 | 0.91 | 0.93 | 0.93 | 0.50 | 0.71 | 0.72 | 0.73 |

| 0.75 | 0.28 | 0.30 | 0.30 | 0.75 | 0.17 | 0.18 | 0.16 | |

| 0.90 | 0.03 | 0.03 | 0.02 | 0.90 | 0.04 | 0.04 | 0.04 | |

| 1.00 | 0.02 | 0.02 | 0.02 | 1.00 | 0.08 | 0.07 | 0.08 | |

The data of the first year was used to calculate a sparse PCA. We use the method of [Erichson et al., 2018] to get sparse directions instead of [Cai et al., 2015], since, according to the latter authors, their estimators leading to minimax rates are computationally infeasible.The sparse PCA was conducted as follows: Denote the data matrix by . [Erichson et al., 2018] propose to calculate an orthonormal matrix and a sparse matrix solving

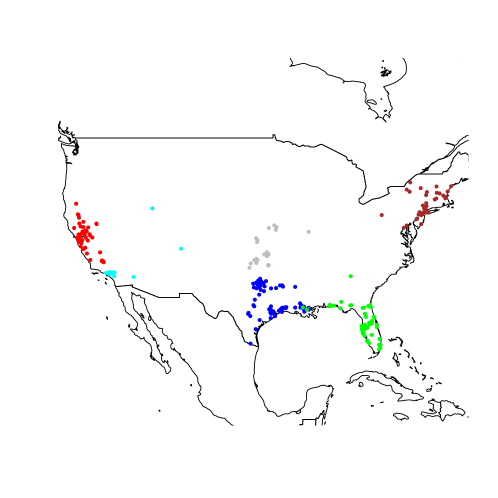

where we used an elastic net regularization with parameters , . This analysis shows that the supports of the leading six projections, where for , correspond to a spatial segmentation which eases interpretation. Figure 1 shows the geographic locations of these supports.

The data of the years 2011 to 2014, providing the test sample with , was now analyzed using the leading directions as projection vectors. The proposed change-point tests were applied to test for the presence of changes in the (co-) variances , , for . The asymptotic variance parameter was estimated using both the full in-sample and stopped-sample approach. The application of the unweighted CUSUM approach revealed no significances at the usual levels.

7. Proofs

The proofs are based on martingale approximations, which require several additional results and technical preparations. These results extend and complement the results obtained in [Steland and von Sachs, 2017].

7.1. Preliminaries

For an arbitray array of coefficients and vectors and with finite -norm, i.e., , define

for and . Put for .

Introduce for coefficients satisfying Assumption (D) and vectors and the -martingales

which start in , for each . Put

Notice that, by definitions (16) and (17),

| (42) |

for and , where . For brevity introduce the difference operator

for , which takes the lag forward difference at . Notice that for

coincides with the martingale . A direct calculation shows that

| (43) | ||||

for and .

7.2. Martingale approximations

The following lemma provides an explicit formula for the asymptotic covariance parameter related to the two CUSUMs, , using different pairs and of weighting vectors, abbreviated as . Especially, it follows from these results that the asymptotic variance of a single CUSUM detector under the no-change null hypothesis, , satisfies

The following general results hold under a mild condition on the error terms and especially show that (73) can be approximated by at the rate , uniformly in and , cf. [Steland and von Sachs, 2017, (3.18)] and [Kouritzin, 1995]. The proof extends these latter results and improves the bounds, but it is technical and thus deferred to the appendix. The improved bounds show that the -norms of the weighting vectors may grow slowly without sacrificing the convergence of the second moments, cf. the verification of (II) and (III) in the proof of Theorem 1.

Lemma 1.

Let , , be independent with variances and third moments satisfying

| (44) |

| (45) |

for constants and for some with . Then for , with ,

| (46) |

and for and

| (47) |

if

| (48) |

Lemma 2.

Let be independent mean zero random variables with variances and third moments satisfying Assumption (E). Let be coefficients satisfying the decay condition (D). Then we have for and

| (49) |

Further, for and

| (50) | ||||

| (51) |

such that

| (52) |

(50), (51) and (52) also hold (with obvious modifications), if and for two pairs of weighting vectors, where the bound in (52) then is given by .

Proof.

See appendix. ∎

The next lemma studies the conditional covariances of the approximating martingales. It generalizes [Steland and von Sachs, 2018, Lemma 2.2] to the change-point model and two different pairs of projection vectors.

Lemma 3.

Proof.

See appendix. ∎

7.3. Proofs of Subsection 3.2

After the above preparations, we are now in a position to show Theorem 1.

Proof of Theorem 1.

Put

| (53) |

such that for and . Let us consider the bivariate extension of the sums ,

Introduce the conditional covariance operators

and the unconditional covariance operator associated to the Brownian motion ,

We shall verify [Philipp, 1986, Th. 1], namely the validity of the following conditions: For , ,

-

(I)

for some .

-

(II)

For some it holds

-

(III)

There exists a covariance operator , namely , such that the conditional covariance operator converges to in the semi-norm in expectation in the sense that for some .

Remark: As the construction is for fixed , one could consider in (II) and (III). But since we are interested in and (II) and (III) yield the moment convergence with rate for the partial sum of interest (for large ), we show and consider the case . This includes the real sample size and (21) then ensures the bound we shall use.

Write , , and observe that where is obtained from by replacing by and by . The -inequality and Cauchy-Schwarz yield

and the second component is estimated analogously. Following the arguments in [Kouritzin, 1995, p. 343], for and , one can show that for and

where , uniformly in uniformly -bounded and , such that and, in turn, . Eventually, we obtain for any

| (54) |

Now Jensen’s inequality yields

verifying (I). To show (II) recall that the martingale approximation for is given by see Lemma 2. Using

it follows that

by Lemma 2 and (21), such that (II) holds with . It remains to show (III). Observe that

Noting that , we obtain

Therefore, (III) follows, if

a.s., which is shown in Lemma 3, since then assumption (21) ensures the estimate . Hence, from [Philipp, 1986], we may conclude that there exists a constant and a universal constant , such that

| (55) |

a.s., which implies

| (56) |

a.s., for . Recalling that where satisfies

we have the following crucial representation in terms of ,

for all . Since

(56) yields, by definition of , see (19),

for , a.s.. This implies

| (57) |

as , a.s., which in turn leads to (iii), since

as , a.s., and (iv) follows from the reverse triangle inequality. Recalling that and , we obtain

as , a.s., which shows (v). (vi) now follows easily from the reverse triangle inequality. For a weight function satisfying (13) the arguments are more involved and as follows: Let be a non-decreasing sequence specified later. Then, using and for , we obtain a.s.

The maximum over is estimated analogously leading to

The right-hand side is , a.s., if we put . Further, the technical results of the appendix and the Hájek-Rényi inequality for martingale differences yield for any the tail bound

The first term tends to , as , uniformly in , since . Let be a Brownian bridge and note that . Using the estimates and on the law of the iterated logarithm for the Brownian bridge, [Shorack and Wellner, 1986, p.72], entails for and (thus for large )

by our choice of and since . The corresponding tail probabilities for the maximum over are treated analogously. Combining the above estimates shows (22). ∎

Proof of Theorem 2.

See appendix. ∎

Proof of Theorem 3.

See appendix. ∎

Proof of Theorem 4.

Since and satisfy property (21) and

we may conclude that . Consequently, all approximations for carry over. In particular, we obtain under the conditions of Theorem 1, cf. (23),

Note that is a standard Brownian on , cf. (20), whereas the scale factor changes from to on . This shows (27) for -bounded projections. The proof for uniformly -bounded projections uses the scaling and the fact that by Jensen’s inequality gives , where the sum is finite by assumption and the factor cancels by standardization, see also [Steland and von Sachs, 2018]. ∎

Proof of Theorem 5.

The conditions on ensure that is well defined, see [Csörgő and Horváth, 1993]. Further, and for each . Therefore, combining these facts, Lévy’s modulus of continuity, , of a Brownian bridge , i.e. , a.s., and the continuous mapping theorem the result follows from (23) ∎

Proof of Theorem 6.

Let us stack the statistics , as defined in (17), yielding the -dimensional random vector

Also put , . For sparseness of notation, we use the same symbols and and note that the quantities studied here coincide with the previous definitions if . We work in the Hilbert space and show (I) - (III) when , so that the additional scaling with , which can be attached to the ’s or put in front of the sums, is in effect. The equivalence of the vector norms and - recall that and - and Jensen’s inequality yield, in view of (54),

since the bounds for obtained above and leading to (54) are uniform in and uniform over the considered sets of projection vectors and coefficient arrays. This shows (I). (II) follows from

such that , by the assumptions on the growth of . Next consider the conditional covariance operators

and the covariance operator , . We need to estimate the operator norm of their difference and use Lemma 3 and similar arguments as in the proof of Theorem 2.2 of [Steland and von Sachs, 2018]. Denote the th coordinate of corresponding to the weighting vectors and by and let

By Lemma 3

where . Using the well known estimate for and , , we therefore obtain

which establishes condition (III). Hence, from [Philipp, 1986], we may conclude that there exists a constant and a universal constant , such that on a new probability space for an equivalent version of and a Brownian motion as described in the theorem

a.s.. The proof can now be completed along the lines of the proof of Theorem 1 with instead of by arguing coordinate-wise leading to

where the upper bound does not depend on , which establishes (29). For a positive weight function a similar bound applies when considering CUSUMs taking the maximum over for , . For a weight function satisfying (13) and CUSUMs taking the maximum over the required LIL tail bound and the martingale approximation used to apply the Hájek-Rényi inequality do not depend on or , such that

for any . ∎

7.4. Consistency of nuisance estimators

Proof of Theorem 7.

Fix . We can and will assume that is large enough to ensure that and . Denote by the estimator regarding the dimension as a formal parameter such that . In the same vain we proceed for and all other statistics arising below and write etc. The assertion will then follow by showing that the consistency is uniform in the dimension . By assumption satisfies for and if . Put and again let , if , and , if . By Lemma 1 and Lemma 2, with . Combining this with (59), we obtain Without loss of generality we fix and show that , as , where

Here and in the sequel we omit the dependence of and related quantities (namely and introduced below) on , for sake of readability.

Observe that for

Define for and

Then for ,

Using and for , uniformly in , we obtain

as , for , where the term is uniform in and . Consequently,

as , where the term is uniform in and , such that

| (58) |

as , where

for . As in [Steland and von Sachs, 2017, Th. 4.4] one can show that

| (59) |

for as well as and . This implies

| (60) |

since Therefore, we may further conclude that

yielding the representation

| (61) |

as well as

| (62) |

as , uniformly in and , where

The arguments used in the proof of [Steland and von Sachs, 2017, Th. 4.4] to obtain (A.11) therein show that, if applied to the subseries and ,

| (63) |

for constants not depending on , . Hence

| (64) |

for , and in turn

| (65) |

for constants . Now observe that where , . It holds

Again decomposing the sums as

and using (63), we obtain uniformly over , and . For example, for

We may conclude that as , and by boundedness of the weights it follows that

Now, having in mind (61) and (62), decompose

and combine (58), (60) and (65), see the appendix for details. ∎

7.5. Consistency of the change-point estimators

Proof of Theorem 9.

Observe that, by the definitions of and ,

with remainder . By (84) we have for

and the same bound holds for . Therefore for any

Hence, it suffices to show that for all and , where the first assertion follows from the latter maximal inequality. Of couse , since is the sum of martingale differences. Now an application of Doob’s maximal inequality entails which establishes

and in turn (40). Next consider

as , by (40). Clearly, for each fixed , and by monotonicity on and this implies uniform convergence, since is continuous, which completes the proof. ∎

Proof of Theorem 10.

Since is an isolated maximum of and converges uniformly to , the consistency follows from well known results, see, e.g., [van der Vaart, 1998], by virtue of Theorem 9 and (39). ∎

Appendix A Additional Results and Proofs

This section provides technical details of several proofs and additional auxiliary results. Especially, the proofs of the asymptotic results are based on martingale approximations which require several additional results and technical preparations. These results extend and complement the results obtained in [Steland and von Sachs, 2017].

A.1. Proofs for Subsection 7.1 (Preliminaries)

Consider the multivariate linear time series of dimension ,

with , cf. (5), which can be written as

Let be the SVD of with singular values , left singular vectors and right singular vectors , which satisfy , . Then and the element at position of the latter matrix is given by . Plugging the latter formula into equation (4) leads us to

i.e. the coefficients of the series (4) take now the form .

Lemma 4.

Suppose that

-

(i)

and ,

-

(ii)

,

-

(iii)

Then , i.e. (D) holds.

Proof of Lemma 4.

We can assume that the constants in (i) are equal to . By (i) for all . Using the inequality we obtain for all

Combining

| (66) |

with now yields

Using (iii) we may conclude that the coefficients satisfy

which completes the proof. ∎

Whereas the conditions of Lemma 4 rule out eigenvectors such as , the following set of conditions relaxes the assumptions on the eigenstructure by strengthening the requirements on the coefficient matrices.

Lemma 5.

Suppose that

-

(i)

and

-

(ii)

Then , i.e. (D) holds.

Proof of Lemma 5.

Recall that for all . The proof is similar as the proof of Lemma 4 noting that implies and using the estimate . ∎

Assumption (ii) is a weak localizing condition on the coefficient matrices of the multivariate linear process, as it limits the influence of the th innovation on the th coordinate process at all lags . Observe that a sufficient condition for (ii) is to assume that

for some .

Consider a stable VARMA model

| (67) |

as introduced in the main document with coefficient matrices and satisfying (element-wise) the decay condition (7) with for some . The coefficient matrices, , of the representation,

can be calculated using the recursion

where for . Denote and .

Lemma 6.

Suppose that the cofficient matrices of the VARMA model satisfy (7) with , i.e. for some

Then , such that (7) is satisfied with , and therefore the decay condition (D) holds for the coefficients, , in the representation (4) of the multivariate linear process associated to the VARMA model (67).

Proof of Lemma 6.

The proof is by induction. For the assertion follows from . For it suffices to show that

Since for

we have

Using the fact that for , we obtain , such that

Consequently,

and we may conclude that

such that

Using again the estimate (66), we may conclude that . ∎

We need the following lemma.

Lemma 7.

Under Assumption (D) it holds for weighting vectors with finite -norms

| (68) | ||||

| (69) | ||||

| (70) |

The constants arising in the above estimates do not depend on .

Proof.

Omitted for brevity. ∎

The following lemma provides estimates needed to study a change of the coefficients.

Lemma 8.

Under Assumption (D) it holds for vectors with finite -norms:

-

(i)

, .

-

(ii)

.

-

(iii)

.

Proof of Lemma 8.

By virtue of Assumption (D), we have for with

Hence . Since for , we obtain

Next we show (ii). Put . By (i) we have for

such that

which establishes (ii). To show (iii), observe that for

Therefore, for

∎

A.2. Proofs for Subsection 7.2 (Martingale Approximations)

Recall the following definitions: Introduce for coefficients satisfying Assumption (D) and vectors and the -martingales

which start in , for each . Put

Notice that, by definitions (16) and (17)

| (71) |

for and , where . For brevity introduce the difference operator

which takes the lag forward difference at . Notice that for

| (72) |

coincides with the martingale . A direct calculation shows that

| (73) | ||||

for and .

Proof of Lemma 1.

For and put

Then

by Lemma 8 (iii). We shall prove that one may replace by

with an error term of order . Then a further application of Lemma 8 (iii) shows that the range of summation for can be extended to and gives , such that the assertion follows. First observe the following fact: If , , satisfy for some , then

This follows from

which implies

since . Next observe that

| (74) |

and anolgous estimates hold for the triple . Because we have and therefore by using

| (75) |

and

| (76) |

for constants and for some with , and the decomposition

where , we obtain

| (77) |

Next we show that the second term of can be replaced by the second term of . Use

to otain

The first term of the last decomposition can be estimated as follows.

Similarly, for the second term we have

for ( exists, since by assumption). Putting things together, we arrive at

Combining the latter estimate with (77) shows that

which completes the proof. ∎

Proof of Lemma 2.

For brevity of notation, we omit the dependence on in notation. Put and note that , where

for . The result can now be shown along the lines of [Kouritzin, 1995, Lemma 2] noting the following facts. By independence of , for any fixed ,

By virtue of (68) - (70), which hold due to the decay assumption (D) on the coefficients of the vector time series, we obtain

since by assumption and , which entails that the rate also applies to innovation arrays satisfying Assumption (E). Analogously,

Lastly,

and therefore Fatou’s lemma leads to . Repeating the arguments provided in [Kouritzin, 1995] shows that can be decomposed in three terms which are bounded by the expressions listed in (68) - (70), which are . Observing that the dependence on the vectors is only through the coefficients , the remaining assertions follow by recalling (71). ∎

Observe that for i.i.d. error terms with and for all

| (78) |

We write , . If , , then for projections these quantities do not depend on .

Proof of Lemma 3.

We may apply the method of proof of [Kouritzin, 1995]. Define for a sequence satisfying Assumption (D) the following approximation for ,

and let

denote the associated approximation error, for , and , if . Then the lag martingale differences attain the representation

where

| (79) |

Using the fact that the lag difference operator is the sum of first order differences, i.e., , we obtain

Let us now estimate the four terms separately. For brevity of notation we omit the dependence on , as they are attached to and , respectively, and enter only through the coefficients . Using (79) we have

Noting that and the sums over are non-vanishing only if , we obtain by independence of for with the centered r.v.s.

a.s., since and are independent if and . Therefore

a.s.. Consequently, cf. (73),

a.s.. A lengthy calculation shows that such that, because is -measurable if and ,

such that the Cauchy-Schwarz inequality provides us with the bound

a.s.. This implies

since by virtue of the Jensen inequality and Lemma 8

Further,

leading to the estimate

Lastly, a direct calculation using similar arguments as above shows that

which is the th term of the first sum of as defined in the proof of Lemma 1. Since there it was shown that , we eventually obtain

Putting together the above estimates completes the proof of the first assertion. The second assertion is shown as in [Kouritzin, 1995, (4.23)] and is omitted for brevity. ∎

A.3. Proofs of Subsection 7.3

Lemma 9.

Under the change-point model (9) it holds

| (80) |

and

| (81) |

Proof of Lemma 9.

Proof of Theorem 2.

Observe that In Theorem 11 it is shown that , defined in (85), is a martingale which approximates , since , so that as well as hold. Using this fact, (83) and the triangle inequality, we obtain for any constant and

which entails . W.l.o.g. assume for large and observe that by (11) it holds as . Consequently, we have

∎

Proof of Theorem 3.

Observe that for and arbitrary coefficient arrays . By the strengthened decay condition, we have uniformly in , and

for . It follows that

and therefore

satisfies and . Put

where . Since , , we have for the estimates uniformly in . Consider the decomposition if . By Markov’s inequality , , such that for any . It follows that

In view of (55) we may conclude that, on a new probability space for equivalent versions, , , a.s.. By virtue of [Billingsley, 1999, Sec. 21, Lemma 2] this strong approximation can be constructed on the original probability space . Consequently, we obtain , , a.s.. Now it follows easily that assertions (i) and (ii) of Theorem 1 hold true with an additional error term and (iii)-(vi) with an additional term. Finally, (vii) and (viii) hold in probability, if . ∎

A.4. Proofs of Subsection 7.5

Theorem 11.

Under the change-point alternative model (9) with , , there exist a -martingale array , , , such that

| (82) |

and hence for and

| (83) |

Further, if , then

| (84) |

Proof of Theorem 11.

Recall (72) and put for each

| (85) |

It is clear that holds if and . In addition, for we have

because is a -martingale array. Since

the triangle inequality provides the upper bound

for , which is by virtue of Lemma 2, see (49) and (50), This verifies (82), i.e.,

As a consequence, for and

Lastly, since we may assume that is small enough to ensure , it holds for

| (86) |

∎

Proof of Theorem 7.

The proof is completed by considering the decomposition

where the term is uniform over and

has been already estimated in (60) and (62) implies , as . Denote the counting measure on by . Then by Fubini and (65)

Lastly, , as , follows by dominated convergence. ∎

Acknowledgments

The author acknowledges support from Deutsche Forschungsgemeinschaft (grants STE 1034/11-1, 1034/11-2).

References

- [Aue et al., 2009] Aue, A., Hörmann, S., Horváth, L., and Reimherr, M. (2009). Break detection in the covariance structure of multivariate time series models. Ann. Statist., 37(6B):4046–4087.

- [Avanesov and Buzun, 2018] Avanesov, V. and Buzun, N. (2018). Change-point detection in high-dimensional covariance structure. arxiv:1610.03783.

- [Bar-Joseph et al., 2012] Bar-Joseph, Z., Gitter, A., and Simon, I. (2012). Studying and modelling dynamic biological processes using time-series gene expression data. Nature Reviews Genetics, 13:552–564.

- [Berkes et al., 2009] Berkes, I., Gombay, E., and Horváth, L. (2009). Testing for changes in the covariance structure of linear processes. J. Statist. Plann. Inference, 139(6):2044–2063.

- [Billingsley, 1999] Billingsley, P. (1999). Convergence of probability measures. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons, Inc., New York, second edition. A Wiley-Interscience Publication.

- [Birnbaum et al., 2013] Birnbaum, A., Johnstone, I. M., Nadler, B., and Paul, D. (2013). Minimax bounds for sparse PCA with noisy high-dimensional data. Ann. Statist., 41(3):1055–1084.

- [Breitung and Eickmeier, 2011] Breitung, J. and Eickmeier, S. (2011). Testing for structural breaks in dynamic factor models. J. Econometrics, 163(1):71–84.

- [Brodie et al., 2009] Brodie, J., Daubechies, I., De Mol, C., Giannone, D., and Loris, I. (2009). Sparse and stable Markowitz portfolios. Proceedings the National Academy of Sciences of the United States of America, 106(30):12267–12272.

- [Cai et al., 2015] Cai, T., Ma, Z., and Wu, Y. (2015). Optimal estimation and rank detection for sparse spiked covariance matrices. Probab. Theory Related Fields, 161(3-4):781–815.

- [Cho and Fryzlewicz, 2015] Cho, H. and Fryzlewicz, P. (2015). Multiple-change-point detection for high dimensional time series via sparsified binary segmentation. J. R. Stat. Soc. Ser. B. Stat. Methodol., 77(2):475–507.

- [Csörgő and Horváth, 1993] Csörgő, M. and Horváth, L. (1993). Weighted approximations in probability and statistics. Wiley Series in Probability and Mathematical Statistics: Probability and Mathematical Statistics. John Wiley & Sons, Ltd., Chichester. With a foreword by David Kendall.

- [Csörgő and Horváth, 1997] Csörgő, M. and Horváth, L. (1997). Limit theorems in change-point analysis. Wiley Series in Probability and Statistics. John Wiley & Sons, Ltd., Chichester. With a foreword by David Kendall.

- [Davis and Kahan, 1970] Davis, C. and Kahan, W. M. (1970). The rotation of eigenvectors by a perturbation. III. SIAM J. Numer. Anal., 7:1–46.

- [Erichson et al., 2018] Erichson, N. B., Zheng, P., Manohar, K., Brunton, S. L., Kutz, J. N., and Aravkin, A. A. (2018). Sparse principal component analysis via variable projection. arXiv:1804.00341.

- [Ferger, 2018] Ferger, D. (2018). On the supremum of a Brownian bridge standardized by its maximizing point with applications to statistics. Statist. Probab. Lett., 134:63–69.

- [Galeano and Peña, 2007] Galeano, P. and Peña, D. (2007). Covariance changes detection in multivariate time series. J. Statist. Plann. Inference, 137(1):194–211.

- [Han and Inoue, 2015] Han, X. and Inoue, A. (2015). Tests for parameter instability in dynamic factor models. Economet. Theor., 31(5):1117–1152.

- [Horváth and Rice, 2019] Horváth, L. and Rice, G. (2019). Asymptotics for empirical eigenvalue processes in high-dimensional linear factor models. J. Multivariate Anal., 169:138–165.

- [Johnson and Lindenstrauss, 1984] Johnson, W. B. and Lindenstrauss, J. (1984). Extensions of Lipschitz mappings into a Hilbert space. In Conference in modern analysis and probability (New Haven, Conn., 1982), volume 26 of Contemp. Math., pages 189–206. Amer. Math. Soc., Providence, RI.

- [Johnstone and Lu, 2009] Johnstone, I. M. and Lu, A. Y. (2009). On consistency and sparsity for principal components analysis in high dimensions. J. Amer. Statist. Assoc., 104(486):682–693.

- [Jolliffe et al., 2003] Jolliffe, L., Trendafilov, N., and Uddin, M. (2003). A modified principal component technique based on the lasso. J. Comput. Graph. Statist., 12:531–547.

- [Jung and Marron, 2009] Jung, S. and Marron, J. S. (2009). PCA consistency in high dimension, low sample size context. Ann. Statist., 37(6B):4104–4130.

- [Kane and Nelson, 2014] Kane, D. M. and Nelson, J. (2014). Sparser Johnson-Lindenstrauss transforms. J. ACM, 61(1):Art. 4, 23.

- [Kouritzin, 1995] Kouritzin, M. A. (1995). Strong approximation for cross-covariances of linear variables with long-range dependence. Stochastic Process. Appl., 60(2):343–353.

- [Ledoit and Wolf, 2004] Ledoit, O. and Wolf, M. (2004). A well-conditioned estimator for large-dimensional covariance matrices. J. Multivariate Anal., 88(2):365–411.

- [Li and Zhao, 2013] Li, X. and Zhao, Z. (2013). Testing for changes in autocovariances of nonparametric time series models. J. Statist. Plann. Inference, 143(2):237–250.

- [Ma, 2013] Ma, Z. (2013). Sparse principal component analysis and iterative thresholding. Ann. Statist., 41(2):772–801.

- [Na et al., 2011] Na, O., Lee, Y., and Lee, S. (2011). Monitoring parameter change in time series models. Stat. Methods Appl., 20(2):171–199.

- [Paul, 2007] Paul, D. (2007). Asymptotics of sample eigenstructure for a large dimensional spiked covariance model. Statist. Sinica, 17(4):1617–1642.

- [Paul and Johnstone, 2007] Paul, D. and Johnstone, I. M. (2007). Augmented sparse principal component analysis for high dimensional data. Technical Report arXiv:1202.1242.

- [Philipp, 1986] Philipp, W. (1986). A note on the almost sure approximation of weakly dependent random variables. Monatsh. Math., 102(3):227–236.

- [Sancetta, 2008] Sancetta, A. (2008). Sample covariance shrinkage for high dimensional dependent data. J. Multivariate Anal., 99(5):949–967.

- [Schweinberger et al., 2017] Schweinberger, M., Babkin, S., and Ensor, K. B. (2017). High-dimensional multivariate time series with additional structure. J. Comput. Graph. Statist., 26(3):610–622.

- [Shen et al., 2013] Shen, D., Shen, H., and Marron, J. S. (2013). Consistency of sparse PCA in high dimension, low sample size contexts. J. Multivariate Anal., 115:317–333.

- [Shorack and Wellner, 1986] Shorack, G. R. and Wellner, J. A. (1986). Empirical processes with applications to statistics. Wiley Series in Probability and Mathematical Statistics: Probability and Mathematical Statistics. John Wiley & Sons, Inc., New York.

- [Steland, 2005] Steland, A. (2005). Random walks with drift—a sequential approach. J. Time Ser. Anal., 26(6):917–942.

- [Steland, 2018] Steland, A. (2018). Shrinkage for covariance estimation: Asymptotics, confidence intervals, bounds and applications in sensor monitoring and finance. Statistical Papers, 59:1441–1462.

- [Steland and von Sachs, 2017] Steland, A. and von Sachs, R. (2017). Large-sample approximations for variance-covariance matrices of high-dimensional time series. Bernoulli, 23(4A):2299–2329.

- [Steland and von Sachs, 2018] Steland, A. and von Sachs, R. (2018). Asymptotics for high-dimensional covariance matrices and quadratic forms with applications to the trace functional and shrinkage. Stochastic Process. Appl., 128(8):2816–2855.

- [van der Vaart, 1998] van der Vaart, A. W. (1998). Asymptotic Statistics. Cambridge University Press, Cambridge.

- [Vostrikova, 1981] Vostrikova, L. J. (1981). Discovery of disorder in multidimensional random processes. Dokl. Akad. Nauk SSSR, 259(2):270–274.

- [Wang and Samworth, 2018] Wang, T. and Samworth, R. J. (2018). High dimensional change point estimation via sparse projection. J. R. Stat. Soc. Ser. B. Stat. Methodol., 80(1):57–83.

- [Wang and Fan, 2017] Wang, W. and Fan, J. (2017). Asymptotics of empirical eigenstructure for high dimensional spiked covariance. Ann. Statist., 45(3):1342–1374.

- [Yu et al., 2015] Yu, Y., Wang, T., and Samworth, R. J. (2015). A useful variant of the Davis-Kahan theorem for statisticians. Biometrika, 102(2):315–323.