Controlling false discovery exceedance for heterogeneous tests

Abstract.

Several classical methods exist for controlling the false discovery exceedance (FDX) for large scale multiple testing problems, among them the Lehmann-Romano procedure Lehmann and Romano, (2005) ( below) and the Guo-Romano procedure Guo and Romano, (2007) ( below). While these two procedures are the most prominent, they were originally designed for homogeneous test statistics, that is, when the null distribution functions of the -values , , are all equal. In many applications, however, the data are heterogeneous which leads to heterogeneous null distribution functions. Ignoring this heterogeneity usually induces a conservativeness for the aforementioned procedures. In this paper, we develop three new procedures that incorporate the ’s, while ensuring the FDX control. The heterogeneous version of , denoted , is based on the arithmetic average of the ’s, while the heterogeneous version of , denoted , is based on the geometric average of the ’s. We also introduce a procedure , that is based on the Poisson-binomial distribution and that uniformly improves and , at the price of a higher computational complexity. Perhaps surprisingly, this shows that, contrary to the known theory of false discovery rate (FDR) control under heterogeneity, the way to incorporate the ’s can be particularly simple in the case of FDX control, and does not require any further correction term. The performances of the new proposed procedures are illustrated by real and simulated data in two important heterogeneous settings: first, when the test statistics are continuous but the -values are weighted by some known independent weight vector, e.g., coming from co-data sets; second, when the test statistics are discretely distributed, as is the case for data representing frequencies or counts.

1. Introduction

1.1. Background

When many statistical tests are performed simultaneously, a ubiquitous way to account for the erroneous rejections of the procedure is the false discovery proportion (FDP), that is, the proportion of errors in the rejected sets, as introduced in the seminal paper Benjamini and Hochberg, (1995). Most of the related literature studies the expected value of this quantity, which is the false discovery rate (FDR), e.g., building procedures that improve the original Benjamini-Hochberg procedure by trying to adapt to some underlying structure of the data. In particular, a fruitful direction is to take into account the heterogeneous structure of the different tests. Heterogeneity may originate from various sources. The two main examples we have in mind, and which have been intensively investigated in the statistical literature recently, is heterogeneity caused by -value weighting and discrete data.

The -value weighting is a popular approach that can be traced back to Holm, (1979) and that has been further developed specifically for FDR in, e.g., Genovese et al., (2006); Blanchard and Roquain, (2008); Hu et al., (2010); Zhao and Zhang, (2014); Ramdas et al., (2017). Here, the heterogeneity can be for instance driven by sample size, groups, or more generally by some covariates. In particular, finding optimal weighting in the sense of maximizing the number of true rejections has been investigated in Wasserman and Roeder, (2006); Rubin et al., (2006); Roquain and van de Wiel, (2009); Ignatiadis et al., (2016); Durand, (2019), either from independent weighting or from the same data set. As a result, the weighted -values have heterogeneous null distribution functions that must be properly taken into account by multiple testing procedures.

On the other hand, multiple testing for discrete distributions is a well identified research field Tarone, (1990); Westfall and Wolfinger, (1997); Gilbert, (2005) that has received a growing attention in the last decade, see, e.g., Heyse, (2011); Heller and Gur, (2011); Dickhaus et al., (2012); Habiger, (2015); Chen et al., (2015); Döhler, (2016); Chen et al., (2018); Döhler et al., (2018); Durand et al., (2019) and references therein. The most typical setting is the case for which each test is performed according to a contingency table. In that situation, the heterogeneity is induced by the fact that marginal counts naturally vary from one table to another. The approach is then to suitably combine the heterogeneous null distributions to compensate the natural conservativeness of individual discrete tests. Namely, Heyse’s approach Heyse, (2011) is to consider the transformation

| (1) |

and to apply BH to the transformed -values . Unfortunately, the latter does not rigorously control the FDR, as it has been proven in Döhler, (2016); Döhler et al., (2018). Appropriate corrections of the expression have been proposed in Döhler et al., (2018) in order to recover rigorous FDR control.

1.2. FDX control

A common criticism of FDR is that it captures only the average behavior of the FDP. In particular, controlling the FDR does not prevent the FDP from possessing undesirable fluctuations and we may aim to stochastically control of FDP in other ways. A classical approach is to control the false probability exceedance (FDX) in the following sense: for ,

| (2) |

This corresponds to control the -quantile of the FDP distribution at level , see, e.g., Genovese and Wasserman, (2004); Perone Pacifico et al., (2004); Korn et al., (2004); Lehmann and Romano, (2005); Genovese and Wasserman, (2006); Romano and Wolf, (2007); Guo et al., (2014); Delattre and Roquain, (2015). Let us also mention that the probabilistic fluctuation of the FDP process is of interest in its own, see, e.g., Neuvial, (2008); Roquain and Villers, (2011); Delattre and Roquain, (2011, 2015); Ditzhaus and Janssen, (2019).

Among multiple testing procedures, step-down procedures have been shown to be particularly useful for FDX control. Two prominent step-down procedures have been proven to control the FDX under different distributional assumptions:

-

•

The Lehmann-Romano procedure , introduced in Lehmann and Romano, (2005), is defined as the step-down procedure with critical values

(3) where we denote

(4) It has been shown to control the FDX under various dependence assumptions between the -values, e.g., when each -value under the null is independent of the family of the -values under the alternative (Theorem 3.1 in Lehmann and Romano, (2005)), which we will refer to (Indep0) below, or when the Simes inequality holds true among the family of true null -values (Theorem 3.2 in Lehmann and Romano, (2005)). 111Under the latter condition, it has also been proven later that the step-up version of , that is, the step-up procedure using the critical values (3) also controls the FDX, see the proof of Theorem 3.1 in Guo et al., (2014).

-

•

The procedure has been improved by the Guo-Romano procedure , see Guo and Romano, (2007), defined as the step-down procedure with critical values

(5) where denotes any variable following a binomial distribution with parameters and . While making more rejections, the procedure controls the FDX under a stronger assumption: the null -value family and the alternative -value family are independent and that the null -values are independent, which we will refer to (Indep) below.

1.3. Contributions

The global aim of the paper is to improve procedures and by incorporating the null distribution functions of the -values while maintaining rigorous FDX control. More specifically, the contributions of this work are as follows:

- •

- •

-

•

at the price of additional computational complexity, we introduce the Poisson-binomial procedure , which controls the FDX under (Indep) and is a uniform improvement of and ;

-

•

we apply this new technology to weighted -values to provide the first weighted procedures that control the FDX (to our knowledge), called and . They are able to improve their non-weighted counterparts and , respectively, see Section 4;

-

•

in the discrete context, our new procedures re-named , are shown to be uniform improvements with respect to the continuous procedures and , respectively. To the best of our knowledge, these are the first FDX controlling procedures tailored specifically to discrete -value distributions. The amplitude of the improvement can be substantial, as we show both with simulated and real data examples, see Section 5.

The paper is organized as follows: Section 2 introduces the statistical setting, the procedures and FDX criterion, as well as a shortcut to compute our step-down procedures without evaluating the critical values. Section 3 is the main section of the paper, which introduces the new heterogeneous procedures and their FDX controlling properties. Our methodology is then applied in two particular frameworks: new weighted procedures controlling the FDX are derived in Section 4 while Section 5 is devoted to the case where the tests are discrete. Both sections include numerical illustrations. A discussion is provided in Section 6 and most of technical details are deferred to Section 7. Appendix A gives additional numerical details for simulations.

2. Framework

2.1. Setting

We use here a classical formal setting for heterogeneous nulls, see, e.g., Döhler et al., (2018). We observe , defined on an abstract probabilistic space, valued in an observation space and of distribution that belongs to a set of possible distributions. We consider null hypotheses for , denoted , , and we denote the corresponding set of true null hypotheses by . We also denote by the complement of in and by the number of true nulls.

We assume that there exists a set of -values that is, a set of random variables , valued in . We introduce the following dependence assumptions between the -values:

| (Indep0) | for all , is independent of ; | ||

| (Indep) | (Indep0) holds and for all , consists of independent variables. |

Note that (Indep0) and (Indep) are both satisfied when all the -values , , are mutually independent in the model . The (maximum) null cumulative distribution function of each -value is denoted

| (6) |

We let that we supposed to be known and we consider the following possible situations for the functions in :

| (Cont) | for all , is continuous on | ||

| (Discrete) |

The case (Discrete) typically arises when for all and , . Throughout the paper, we will assume that we are either in the case (Cont) or (Discrete) and we denote , with by convention when (Cont) holds. For comparison with the homogeneous case, we also let

| (SuperUnif) |

2.2. False Discovery Exceedance and step-down procedures

In general, a multiple testing procedure is defined as a random subset which corresponds to the indices of the rejected nulls. For , the false discovery exceedance of is defined as follows:

| (9) |

In this paper, we consider particular multiple testing procedures, called step-down procedures. Given some -value family and some non-decreasing sequence , the step-down procedure with critical values rejects the null hypotheses corresponding to the set

| (10) | ||||

| (11) |

for which denotes the -values ordered increasingly (for some data-dependent permutation ).

2.3. Transformation function family and computational shortcut

In this paper, the critical values will be obtained by inverting some functional, that is,

| (12) |

for , , a given set of functions. In order for (12) to be well-defined and to be nondecreasing, we will say that the function set is a transformation function family if it satisfies the following conditions:

| (16) |

For instance, the critical values of the procedure can be rewritten as (12) for the functions

| (17) |

We easily check that the function set is a family of transformation functions (in the sense of (16)). Indeed, is non-increasing both in and . A second example is given by the procedure for which

| (18) |

can be proved to form a family of transformation functions. Indeed, the only non-obvious argument to prove (16) is that for a fixed , and we have . This comes from the fact that is non-increasing both in and .

Finally, because of the inversion, computing the critical values via (12) can be time consuming. Fortunately, computing the critical values is actually not necessary if we are solely interested in determining the rejection set given by (10). As the following result shows, we may determine by working directly with the transformation functions.

Proposition 2.1.

Let us consider any transformation function family and the corresponding critical values , , defined by (12). Then, for all , with -probability , the step-down procedure with critical values can equivalently written as

| (19) | ||||

| (20) |

3. New FDX controlling procedures

In this section, we introduce new procedures that control the false discovery exceedance at some level , that is,

| (21) |

while incorporating the family in an appropriate way.

3.1. Tool

Our main tool is the following bound: For any step-down procedure with critical values , we have

| (22) | ||||

| (23) |

Inequality (22) is valid under the distributional assumption (Indep0). This bound comes from a reformulation of Theorem 5.2 in Roquain, (2011) in our heterogenous framework, see Theorem 7.1 below. Our new procedures are derived by further upper-bounding via various probabilistic devices. More specifically, we will introduce several transformation function families such that for all ,

According to (22), the step-down procedure using the corresponding critical values (12) will then control the FDX in the sense of (21).

3.2. Heterogeneous Lehmann-Romano procedure

By using the Markov inequality, we obtain

| (24) |

where denotes the values of ordered decreasingly. Bounding the above quantity by entails the following procedure.

Definition 3.1.

The heterogeneous Lehmann-Romano procedure, denoted by , is defined as the step-down procedure using the critical values defined by

| (25) | ||||

| (26) |

where denotes the values of ordered decreasingly and is defined by (4).

The quantity is thus similar to , in which has been replaced by the average of the largest values of . To check that the functions form a transformation function family in the sense of (16), we note that is non-increasing in (averaging on smaller values makes the average smaller) and continuous in under (Cont) (because is continuous and is -Lipschitz).

3.3. Poisson-binomial procedure

Here, we propose to bound (23) by using the Poisson-binomial distribution. To this end, recall that the Poisson-Binomial distribution of parameters , denoted below, corresponds to the distribution of , where the are all independent and each follows a Bernoulli distribution of parameter for .

First note that for all and , we have that is stochastically upper bounded by a Bernoulli variable of parameter , see (6). As a consequence, by assuming (Indep), we have for all critical values ,

| (27) |

Bounding the latter by leads to the following procedure.

Definition 3.2.

The Poisson-binomial procedure, denoted by , is defined as the step-down procedure using the critical values

| (28) | ||||

| (29) |

where denotes the values of ordered decreasingly and is defined by (4).

Let us now check that is a transformation function family, that is, satisfy (16). The continuity assumption holds because, under (Cont), the mapping is continuous (argument similar to above) and the cumulative distribution function of is a continuous function of . The monotonic property comes from the fact that is non-increasing both in and .

Since under (SuperUnif), the distribution is stochastically smaller than the distribution , the following holds.

Proposition 3.2.

However, in general, the procedure is computationally demanding, even with the shortcut mentioned in Section 2.3. This comes from the computation of which involves the distribution function of a Poisson-binomial variable. In the next section, we make slightly more conservative for recovering the computational price of .

3.4. Heterogeneous Guo-Romano procedure

In this section, we further upper-bound (30) by using that any random variable is stochastically upper-bounded by a random variable (see Example 1.A.25 in Shaked, M. and Shanthikumar, J.G., (2007)). This yields

| (30) |

where we let

| (31) |

where denotes the values of ordered decreasingly.

This reasoning suggests another heterogeneous procedure, based on the binomial distribution. Since also uses the binomial device, we name this new procedure the heterogeneous Guo-Romano procedure.

Definition 3.3.

The condition (16) also holds in that case. However, the proof of monotonicity of is slightly more involved than above and is deferred to Lemma 7.1. In addition, since under (SuperUnif) we have , we deduce that , although more conservative than , is still a uniform improvement over .

Proposition 3.3.

Remark 3.1.

The numerical results in Sections 4 and 5 suggest that the conservatism of with respect to is usually quite small. In addition, since the computational effort required by is comparable to that of , the gain in efficiency may be great, especially for large . We therefore think that may be especially useful for very high dimensional heterogeneous data.

Remark 3.2.

We can also define a non-adaptive version of , defined as the step-down procedure of critical values (12) based on the transformation functional

where . While being more conservative than , it still controls the FDX in the sense (21) . So, while controlling the FDR is linked to the arithmetic average of the ’s (Heyse’s procedure, see text below (1)), this shows that controlling the FDX is linked to geometric averaging. In addition, this shows that the situation is even more simple for FDX, because no further correction is needed here, whereas the arithmetic average should be slightly modified in order to yield a rigorous FDR control Döhler et al., (2018).

4. Application to weighting

It is well known that -value weighting can improve the power of multiple testing procedures, see, e.g., Genovese et al., (2006); Roquain and van de Wiel, (2009); Ignatiadis et al., (2016); Durand, (2017); Ramdas et al., (2017) and references therein. However, to the best of our our knowledge, except for the augmentation approach described in Genovese et al., (2006), no methods are available that incorporate weighting for FDX control. We show in this section that such methods can be obtained directly from the bounds on introduced in Section 3.

Throughout this section, we assume that we have at hand a -value family satisfying (Cont) and (SuperUnif). As explained in our introduction section (see references therein), while the null distributions of the -values are typically uniform, the point is that they can have heterogeneous alternative distributions, so that it could be desirable to weigh the -values in some way. For this, we consider a fixed weight vector . The ordered weights are denoted , the average weight is denoted and the average over the largest weights is denoted by .

Since the heterogeneous procedures , and introduced in Section 3 yield valid control for any collection of distribution functions , it is possible to use very flexible weighting schemes. In order to limit the scope of this paper, we consider only two simple types of weighting approaches in more detail:

-

•

for arithmetic mean weighting (abbreviated in what follows as AM), we define the weighted -value family as

(34) The weighted -values thus have the heterogeneous distribution functions

(35) under the null. This corresponds to classical weighting approaches established for FWER and FDR control.

-

•

for geometric mean weighting (abbreviated as GM), we define

(36) The weighted -values therefore have the following heterogeneous distribution functions under the null:

(37)

Thus, combining these two weighting approaches with the three heterogeneous procedures introduced in the previous section yields a total of six weighted procedures which we discuss in more detail below. Note that a Taylor expansion provides for small values of . Therefore, we expect that AM and GM procedures will yield similar rejection sets for small -values.

4.1. Weighted Lehmann-Romano procedures

Using (22) and (24) (Markov device), we get that any step-down procedure using the weighted -values (34) and critical values has a FDX smaller than or equal to

Since the form a transformation function family, bounding the latter by leads to an FDX controlling procedure, that we call the AM-weighted Lehmann-Romano procedure, denoted by in the sequel. It thus corresponds to the step-down procedure using the weighted -values (34) and the critical values

In particular, if the weight vector is uniform, that is, for all , then reduces to .

Similarly to above, using the GM weighting (36) gives an FDX smaller than or equal to

This gives rise to the GM-weighted Lehmann-Romano procedure, denoted , defined as the step-down procedure using the weighted -values (36) and the critical values

In general, no domination relationship holds between and . Finally, again, in case of uniform weighting, reduces to .

4.2. Weighted Poisson-binomial procedures

Applying the strategy of Section 3.3 with the c.d.f. sets and , we can use the two transformation function families given by

to define new step-down procedures, denoted and respectively, that both ensure FDX control.

4.3. Weighted Guo-Romano procedures

We apply here the strategy of Section 3.4 for the c.d.f. sets and . According to (31), let us define

This gives rise to the transformation function families

Critical values and are obtained via (12) from families and , respectively. This yields two new FDX controlling step-down procedures that are denoted by and , respectively. Note that, similar to arithmetic weighting for the procedure, geometric weighting leads to a simple transformation of the original critical values, given by

| (38) |

Thus, this particular procedure combines simplicity with a close relationship to the original Guo-Romano procedure. By contrast, as for the heterogeneous version, the weighted Poisson-binomial procedures require the evaluation of the Poisson-binomial distribution function which may be computationally demanding for large . The weighted Guo-Romano procedures, on the other hand, while possibly sacrificing some power, only require evaluation of the standard binomial distribution.

4.4. Analysis of RNA-Seq data

We revisit an analysis of the RNA-Seq data set ’airway’ using results from the independent hypothesis weighting (IHW) approach (for details, see Ignatiadis et al., (2016) and the vignette accompanying its software implementation). Loosely speaking, this method aims to increase power by assigning a weight to each hypothesis and subsequently applying e.g. the Bonferroni or the Benjamini-Hochberg procedure to the weighted -values while aiming for control of FWER or FDR.

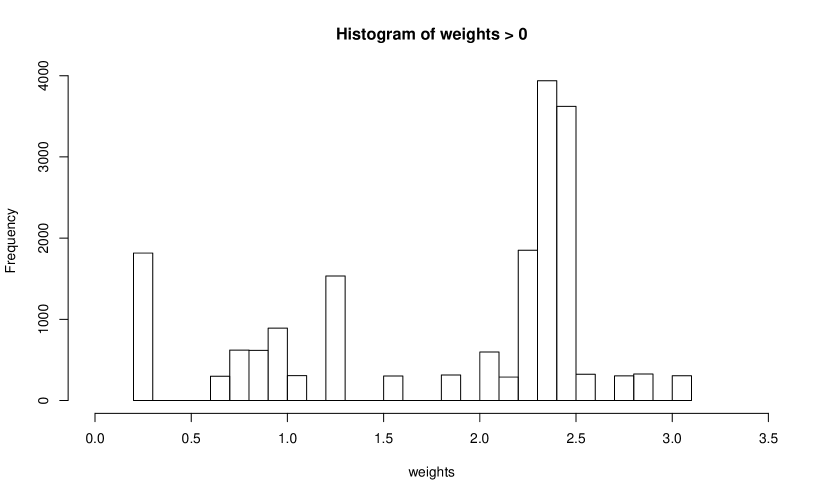

In what follows, we present some results for weighted FDX control, using the procedures introduced in Sections 4.2 and 4.3. For this data set we have and the weights are taken from the output of the ihw function from the bioconductor package ’IHW’. For the sake of illustration we assume the -values to be independent. A large portion (about ) of these weights are 0, Figure 1 presents a histogram of the (strictly) positive weights.

Table 1 shows that controlling the mean (i.e. FDR) or the median of the FDP leads to similar number of rejections.

| [wBH] | |||||||

|---|---|---|---|---|---|---|---|

| Rejections | 4099 | 4896 | 4243 | 4868 | 4865 | 4853 | 4852 |

For both error rates, incorporating weights leads to similar gains in power. For weighted FDX control, the more conservative weighted Guo-Romano procedures exhibit only a slight loss of power with respect to the weighted Poisson-binomial approaches. The difference between arithmetic and geometric weighting is negligible for this data.

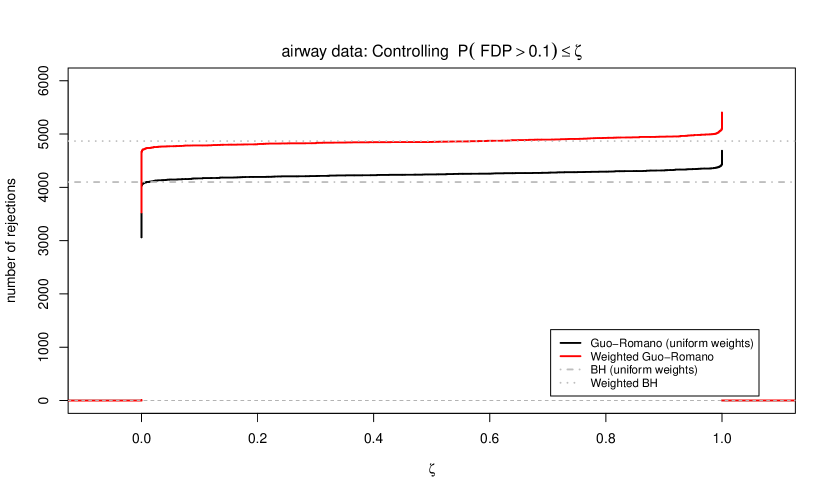

Figure 2 indicates that for the FDX controlling procedures, the mapping of the confidence level to the number of rejections is quite flat. This means that statements about the FDP can be made with high confidence without losing too much power. For instance, requiring that with confidence at least still allows for 4145 and 4771 rejections using the and procedures.

5. Application to discrete tests

5.1. Discrete FDX procedures

Discrete FDX procedures can be defined in a straightforward way by directly using the distribution functions of the discretely distributed -values. The prototypical example we have in mind are multiple conditional tests like Fisher’s exact test. In this case, discreteness and heterogeneity arise from conditioning on the observed table margins. We denote the resulting heterogeneous procedures from section 3 by (for ), (for [HPB]) and (for ).

5.2. Simulation study

We now investigate the power of the , and procedures in a simulation study similar to those described in (Gilbert,, 2005), (Heller and Gur,, 2011) and (Döhler et al.,, 2018). We focus on comparing the performance of the new discrete procedures to their continuous counterparts. Since the analysis with is computationally demanding, we are also interested in investigating the performance of the slightly more conservative, but numerically more efficient procedure. Finally, as above, we also include (Benjamini-Hochberg procedure) as a benchmark.

5.2.1. Simulated Scenarios

We simulate a two-sample problem in which a vector of independent binary responses (“adverse events”) is observed for each subject in two groups, where each group consists of subjects. Then, the goal is to simultaneously test the null hypotheses “”, , where and are the success probabilities for the th binary response in group 1 and 2, respectively. Before we describe the simulation framework in more detail, we explain how this set-up leads to discrete and heterogeneous -value distributions. Suppose we have simulated two vectors of dimension where each component represents a count in . This data can be represented by contingency tables. Now each hypothesis is tested using Fisher’s exact test (two-sided) for each contingency table, which is performed by conditioning on the (simulated) pair of marginal counts. Thus, we can determine for every contingency table the discrete distribution function of the -values for Fisher’s exact test under the null hypothesis. For differing (simulated) contingency tables, these induced distributions will generally be heterogeneous and our inference is conditionally on the marginal counts.

We take where and data are generated so that the response is at positions for both groups, at positions for both groups and at positions for group 1 and at positions for group 2 where represents weak, moderate and strong effects, respectively. The null hypothesis is true for the and positions while the alternative hypothesis is true for the positions. We also take different configurations for the proportion of false null hypotheses, is set to be , and of the value of , which represents small, intermediate and large proportion of effects, respectively (the proportion of true nulls is , , , respectively). Then, is set to be , and of the number of true nulls (that is, ) and is taken accordingly as .

For each of the 54 possible parameter configurations specified by and , Monte Carlo trials are performed, that is, data sets are generated and for each data set, an unadjusted two-sided -value from Fisher’s exact test is computed for each of the positions, and the multiple testing procedures mentioned above are applied at level . The power of each procedure was estimated as the fraction of the false null hypotheses that were rejected, averaged over the simulations (TDP, true discovery proportion). Note that while our procedures are designed to control the FDP conditionally on the marginal counts, our power results are presented in an unconditional way for the sake of simplicity. For random number generation the R-function rbinom was used. The two-sided -values from Fisher’s exact test were computed using the R-function fisher.test.

5.2.2. Results

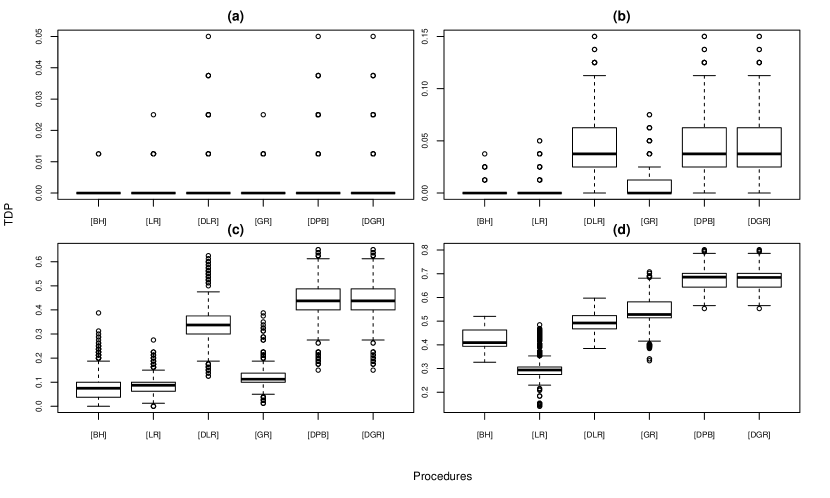

Table 3 in Appendix A shows that the (average) power of the compared procedures depends primarily on the strength of the signal . More specifically, Figure 3 contains some typical plots of the simulation results.

-

•

For , the power of , and is practically zero, whereas the discrete procedures are able to reject at least a few hypotheses, see panel (a) of Figure 3.

-

•

For , the power of and stays close to zero, performs slighty better and the discrete variants perform best as illustrated in panel (b) of Figure 3.

- •

-

•

There is no relevant difference in power between the procedures and .

In summary, these results show that for and , significant improvements are possible by using discreteness.

5.3. Analysis of pharmacovigilance data

We revisit the analysis of pharmacovigilance data from Heller and Gur, (2011) presented in Döhler et al., (2018). This data set is obtained from a database for reporting, investigating and monitoring adverse drug reactions due to the Medicines and Healthcare products Regulatory Agency in the United Kingdom. It contains the number of reported cases of amnesia as well as the total number of adverse events reported for each of the drugs in the database. For a more detailed description of the data which is contained in the R-packages Heller et al., (2012) and Durand and Junge, (2019) we refer to Heller and Gur, (2011). The works Heller and Gur, (2011) and Döhler et al., (2018) investigate the association between reports of amnesia and suspected drugs by performing for each drug a Fisher’s exact test (one-sided) for testing association between the drug and amnesia while adjusting for multiplicity by using several (discrete) FDR procedures. Applying the Benjamini-Hochberg procedure to this data set yields candidate drugs which could be associated with amnesia. Using the discrete FDR controlling procedures from Döhler et al., (2018) yields candidate drugs.

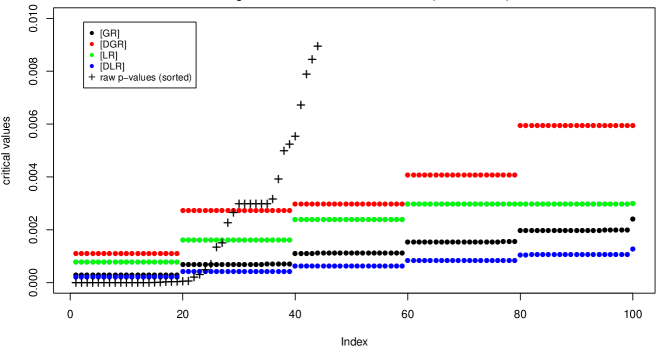

In what follows, we investigate the performance of the , , , and procedures for analyzing this data set. First, we compare these procedures when the goal is control of the median FDX instead of FDR at the level, i.e., we require . Figure 4 illustrates the data and the critical constants of the involved FDX controlling procedures.

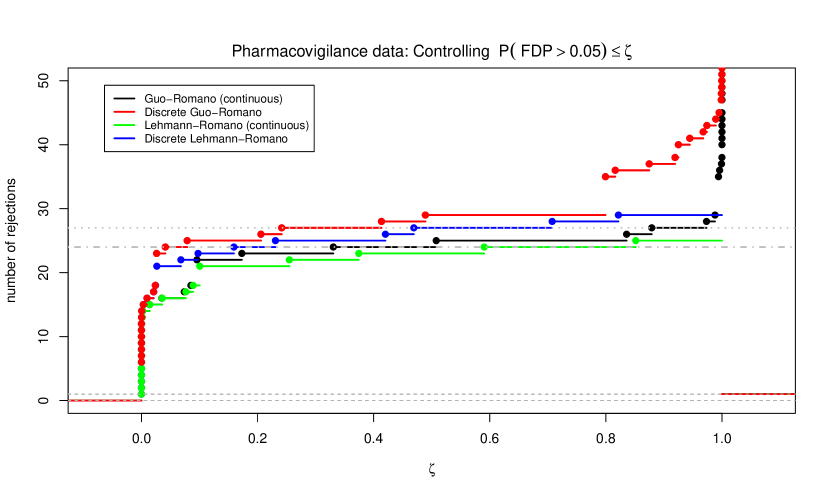

The benefit of taking discreteness into account is evident: the discrete critical values are considerably (by a factor of ) larger than their respective classical counterparts which leads to more powerful procedures, see also the first row of Table 2.

| Procedure controls | |||||

|---|---|---|---|---|---|

| 23 | 27 | 24 | 29 | 29 | |

| 16 | 21 | 16 | 24 | 24 |

Note that the critical values of are not displayed in Figure 4 since they are visually indistinguishable from the critical values. Figure 5 shows that this is in fact true for all indices, thus is not only an efficient, but also quite accurate approximation of the values, at least for the discrete distribution involved in this example.

We also compare the performance of the above procedures over the full range of possible values for . Figure 6 depicts the number of rejections when controlling for .

As expected from Propositions 3.1, 3.2 and 3.3, the discrete variants reject more hypotheses than their classical counterparts for all values of . For central values of , the gain is about three to four additionally rejected hypotheses, which corresponds roughly to the gain from using the discrete version of BH instead of (see Table 1 in Döhler et al., (2018)). Figure 6 also shows that for more extreme values of the gain may be more pronounced, e.g., when is to be guaranteed, the procedure rejects 16 hypotheses, whereas the procedure rejects 24 hypotheses (see the second row of Table 2).

6. Discussion

In this paper, we presented new procedures controlling the FDX while incorporating the (heterogeneous) family of null distribution . Markedly, it put forward that the geometric averaging of the ’s is a suitable operation for FDX control. This is new to our knowledge, as all previous works are mostly based on arithmetic averaging of the ’s (or variation thereof). Maybe more importantly, our approach led to a substantial power improvement in two common situations, under continuity of the tests statistics via weighting schemes, and for discrete test statistics when performing multiple individual Fisher’s exact tests.

This work opens several directions of research. First, the proofs of all our FDX bounds rely on using a kind of independence between the -values (see (Indep0) and (Indep)). While this assumption is classical, it is desirable to remove this condition to better stick to the reality of the experiments. This generalization seems however challenging, as FDX control under dependence is already delicate to study in the homogeneous case, see Delattre and Roquain, (2015). A second interesting avenue is to derive theoretical bounds for the true discovery proportion (TDP) of our procedure. In particular, a useful concern would be to assess whether our way to account for heterogeneity (via arithmetic or geometric averaging of the ’s) is optimal in some sense. Lastly, our work paves the way to control other simultaneous inference criteria based on an event probability, e.g., to establish post hoc bounds in the discrete heterogeneous case, see Genovese and Wasserman, (2006); Goeman and Solari, (2011); Blanchard et al., pear . While challenging, this is a very exciting direction for future research.

Acknowledgements

This work has been supported by ANR-16-CE40-0019 (SansSouci), ANR-17-CE40-0001 (BASICS) and by the GDR ISIS through the ”projets exploratoires” program (project TASTY). The authors thank Florian Junge for implementing the discrete FDX procedures and improved Poisson-binomial distribution functions in R, and for running the simulations.

References

- Benjamini and Hochberg, (1995) Benjamini, Y. and Hochberg, Y. (1995). Controlling the false discovery rate: A practical and powerful approach to multiple testing. Journal of the Royal Statistical Society. Series B, 57(1):289–300.

- (2) Blanchard, G., Neuvial, P., and Roquain, E. (to appear). Post hoc confidence bounds on false positives using reference families. Annals of Statistics.

- Blanchard and Roquain, (2008) Blanchard, G. and Roquain, E. (2008). Two simple sufficient conditions for FDR control. Electron. J. Stat., 2:963–992.

- Chen et al., (2018) Chen, X., Doerge, R. W., and Heyse, J. F. (2018). Multiple testing with discrete data: proportion of true null hypotheses and two adaptive FDR procedures. Biom. J., 60(4):761–779.

- Chen et al., (2015) Chen, X., Doerge, R. W., and Sarkar, S. K. (2015). A weighted FDR procedure under discrete and heterogeneous null distributions. arXiv e-prints, page arXiv:1502.00973.

- Delattre and Roquain, (2011) Delattre, S. and Roquain, E. (2011). On the false discovery proportion convergence under Gaussian equi-correlation. Statist. Probab. Lett., 81(1):111–115.

- Delattre and Roquain, (2015) Delattre, S. and Roquain, E. (2015). New procedures controlling the false discovery proportion via Romano-Wolf’s heuristic. Ann. Statist., 43(3):1141–1177.

- Delattre and Roquain, (2015) Delattre, S. and Roquain, E. (2015). On empirical distribution function of high-dimensional Gaussian vector components with an application to multiple testing. Bernoulli. To appear.

- Dickhaus et al., (2012) Dickhaus, T., Straßburger, K., Schunk, D., Morcillo-Suarez, C., Illig, T., and Navarro, A. (2012). How to analyze many contingency tables simultaneously in genetic association studies. Statistical applications in genetics and molecular biology, 11(4).

- Ditzhaus and Janssen, (2019) Ditzhaus, M. and Janssen, A. (2019). Variability and stability of the false discovery proportion. Electron. J. Statist., 13(1):882–910.

- Döhler, (2016) Döhler, S. (2016). A discrete modification of the Benjamini–-Yekutieli procedure. Econometrics and Statistics.

- Döhler et al., (2018) Döhler, S., Durand, G., and Roquain, E. (2018). New FDR bounds for discrete and heterogeneous tests. Electron. J. Statist., 12(1):1867–1900.

- Durand, (2017) Durand, G. (2017). Adaptive p-value weighting with power optimality. ArXiv e-prints.

- Durand, (2019) Durand, G. (2019). Adaptive -value weighting with power optimality. Electron. J. Statist., 13(2):3336–3385.

- Durand and Junge, (2019) Durand, G. and Junge, F. (2019). DiscreteFDR: Multiple Testing Procedures with Adaptation for Discrete Tests. R package version 1.2.

- Durand et al., (2019) Durand, G., Junge, F., Döhler, S., and Roquain, E. (2019). DiscreteFDR: An R package for controlling the false discovery rate for discrete test statistics. arXiv e-prints, page arXiv:1904.02054.

- Genovese and Wasserman, (2004) Genovese, C. and Wasserman, L. (2004). A stochastic process approach to false discovery control. Ann. Statist., 32(3):1035–1061.

- Genovese et al., (2006) Genovese, C. R., Roeder, K., and Wasserman, L. (2006). False discovery control with p-value weighting. Biometrika, 93(3):509–524.

- Genovese and Wasserman, (2006) Genovese, C. R. and Wasserman, L. (2006). Exceedance control of the false discovery proportion. J. Amer. Statist. Assoc., 101(476):1408–1417.

- Gilbert, (2005) Gilbert, P. (2005). A modified false discovery rate multiple-comparisons procedure for discrete data, applied to human immunodeficiency virus genetics. Journal of the Royal Statistical Society. Series C, 54(1):143–158.

- Goeman and Solari, (2011) Goeman, J. J. and Solari, A. (2011). Multiple testing for exploratory research. Statistical Science, pages 584–597.

- Guo et al., (2014) Guo, W., He, L., and Sarkar, S. K. (2014). Further results on controlling the false discovery proportion. The Annals of Statistics, 42(3):1070–1101.

- Guo and Romano, (2007) Guo, W. and Romano, J. (2007). A generalized Sidak-Holm procedure and control of generalized error rates under independence. Stat. Appl. Genet. Mol. Biol., 6:Art. 3, 35 pp. (electronic).

- Habiger, (2015) Habiger, J. D. (2015). Multiple test functions and adjusted -values for test statistics with discrete distributions. J. Statist. Plann. Inference, 167:1–13.

- Heller and Gur, (2011) Heller, R. and Gur, H. (2011). False discovery rate controlling procedures for discrete tests. ArXiv e-prints.

- Heller et al., (2012) Heller, R., Gur, H., and Yaacoby, S. (2012). discreteMTP: Multiple testing procedures for discrete test statistics. R package version 0.1-2.

- Heyse, (2011) Heyse, J. F. (2011). A false discovery rate procedure for categorical data. In Recent Advances in Bio- statistics: False Discovery Rates, Survival Analysis, and Related Topics, pages 43–58.

- Holm, (1979) Holm, S. (1979). A simple sequentially rejective multiple test procedure. Scand. J. Statist., 6(2):65–70.

- Hu et al., (2010) Hu, J. X., Zhao, H., and Zhou, H. H. (2010). False discovery rate control with groups. J. Amer. Statist. Assoc., 105(491):1215–1227.

- Ignatiadis et al., (2016) Ignatiadis, N., Klaus, B., Zaugg, J., and Huber, W. (2016). Data-driven hypothesis weighting increases detection power in genome-scale multiple testing. 13.

- Korn et al., (2004) Korn, E. L., Troendle, J. F., McShane, L. M., and Simon, R. (2004). Controlling the number of false discoveries: application to high-dimensional genomic data. J. Statist. Plann. Inference, 124(2):379–398.

- Lehmann and Romano, (2005) Lehmann, E. L. and Romano, J. P. (2005). Generalizations of the familywise error rate. Ann. Statist., 33:1138–1154.

- Neuvial, (2008) Neuvial, P. (2008). Asymptotic properties of false discovery rate controlling procedures under independence. Electron. J. Stat., 2:1065–1110.

- Perone Pacifico et al., (2004) Perone Pacifico, M., Genovese, C., Verdinelli, I., and Wasserman, L. (2004). False discovery control for random fields. J. Amer. Statist. Assoc., 99(468):1002–1014.

- Ramdas et al., (2017) Ramdas, A., Foygel Barber, R., Wainwright, M. J., and Jordan, M. I. (2017). A unified treatment of multiple testing with prior knowledge using the p-filter. arXiv e-prints, page arXiv:1703.06222.

- Romano and Wolf, (2007) Romano, J. P. and Wolf, M. (2007). Control of generalized error rates in multiple testing. Ann. Statist., 35(4):1378–1408.

- Roquain, (2011) Roquain, E. (2011). Type I error rate control for testing many hypotheses: a survey with proofs. J. Soc. Fr. Stat., 152(2):3–38.

- Roquain and van de Wiel, (2009) Roquain, E. and van de Wiel, M. (2009). Optimal weighting for false discovery rate control. Electron. J. Stat., 3:678–711.

- Roquain and Villers, (2011) Roquain, E. and Villers, F. (2011). Exact calculations for false discovery proportion with application to least favorable configurations. Ann. Statist., 39(1):584–612.

- Rubin et al., (2006) Rubin, D., Dudoit, S., and van der Laan, M. (2006). A method to increase the power of multiple testing procedures through sample splitting. Stat. Appl. Genet. Mol. Biol., 5:Art. 19, 20 pp. (electronic).

- Shaked, M. and Shanthikumar, J.G., (2007) Shaked, M. and Shanthikumar, J.G. (2007). Stochastic Orders. Springer Series in Statistics. Springer New York.

- Tarone, (1990) Tarone, R. E. (1990). A modified bonferroni method for discrete data. Biometrics, 46(2):515–522.

- Wasserman and Roeder, (2006) Wasserman, L. and Roeder, K. (2006). Weighted hypothesis testing. Technical report, Dept. of statistics, Carnegie Mellon University.

- Westfall and Wolfinger, (1997) Westfall, P. and Wolfinger, R. (1997). Multiple tests with discrete distributions. The American Statistician, 51(1):3–8.

- Zhao and Zhang, (2014) Zhao, H. and Zhang, J. (2014). Weighted -value procedures for controlling FDR of grouped hypotheses. J. Statist. Plann. Inference, 151/152:90–106.

7. Materials for the proofs

7.1. Proving the main tool

The proof is based on the following result, which is a reformulation of Theorem 5.2 in Roquain, (2011) in our context.

Theorem 7.1 (Roquain, (2011)).

In the setting defined in Section 2.1, consider any step-down procedure with critical values , . Then for all , we have

| (39) |

where (with if the set is empty).

Let us show that Theorem 7.1 implies (22) under (Indep0). Under (Indep0), is independent of the variable family

Hence, (39) provides that is smaller or equal to

which gives (22).

Finally, for completeness, let us now prove Theorem 7.1. Let for all . First, we have for any … such that :

by using the definition of . Assuming now for any , we obtain

where the last step uses the definition of . Moreover, if , again by definition of , we have . Hence, we obtain the following upper-bound for :

Since the above bound is also true when , it holds for any possible value of . Since in (11) satisfies both and for any , combining the above displays gives (39).

7.2. Proof of Proposition 2.1

First, we have with -probability , for all , , both under (Cont) or (Discrete). Hence, by (12), we have . By (11), this gives

where we have denoted for all . Now note that

hence it is sufficient to prove that for any . For this, let us fix and write , for . This is possible because, by definition, implies . Next, for any , we have both and , which entails and thus . Since and by the nonincreasing property of , we have . This gives for all . Therefore,

which leads to the result.

7.3. An auxiliary lemma

Lemma 7.1.

Proof.

First note that

in non-decreasing in (because the geometric average of larger numbers is larger). The quantity (40) is thus non-increasing with respect to , so that the only thing to check is that this quantity is non-increasing with respect to . For this, it is sufficient to prove that is stochastically larger than for any (which is not obvious because ). Let , , , , and . We easily check that and by (31),

Applying Example 1.A.25 in Shaked, M. and Shanthikumar, J.G., (2007) ( with the notation therein), we obtain that the sum of a variable and a variable (with independence) is stochastically smaller than a variable. In particular, a variable is stochastically smaller than a variable. This gives the result. ∎

Appendix A Additional numerical details

| [BH] | [LR] | [DLR] | [GR] | [DPB] | [DGR] | ||||

|---|---|---|---|---|---|---|---|---|---|

| 800 | 80 | 144 | 0.15 | 0 | 0 | 0.0025 | 0.0002 | 0.0025 | 0.0025 |

| 144 | 0.25 | 0.0004 | 0 | 0.043 | 0.0077 | 0.043 | 0.043 | ||

| 144 | 0.4 | 0.0803 | 0 | 0.3328 | 0.1195 | 0.4412 | 0.4406 | ||

| 360 | 0.15 | 0 | 0 | 0.0025 | 0.0002 | 0.0043 | 0.0043 | ||

| 360 | 0.25 | 0.0004 | 0 | 0.043 | 0.0077 | 0.0444 | 0.0444 | ||

| 360 | 0.4 | 0.0803 | 0 | 0.3766 | 0.1195 | 0.4512 | 0.4511 | ||

| 576 | 0.15 | 0 | 0 | 0.0071 | 0.0002 | 0.0076 | 0.0076 | ||

| 576 | 0.25 | 0.0004 | 0 | 0.0528 | 0.0077 | 0.077 | 0.077 | ||

| 576 | 0.4 | 0.0803 | 0 | 0.4474 | 0.1195 | 0.5141 | 0.5128 | ||

| 240 | 112 | 0.15 | 0 | 0 | 0.0025 | 0.0002 | 0.0025 | 0.0025 | |

| 112 | 0.25 | 0.0005 | 0 | 0.0289 | 0.0076 | 0.0422 | 0.0422 | ||

| 112 | 0.4 | 0.2148 | 0 | 0.425 | 0.1984 | 0.5153 | 0.5139 | ||

| 280 | 0.15 | 0 | 0 | 0.0025 | 0.0002 | 0.0025 | 0.0025 | ||

| 280 | 0.25 | 0.0005 | 0 | 0.0336 | 0.0076 | 0.0429 | 0.0429 | ||

| 280 | 0.4 | 0.2147 | 0 | 0.4413 | 0.1983 | 0.5728 | 0.5716 | ||

| 448 | 0.15 | 0 | 0 | 0.0025 | 0.0002 | 0.0037 | 0.0037 | ||

| 448 | 0.25 | 0.0005 | 0 | 0.0389 | 0.0076 | 0.043 | 0.043 | ||

| 448 | 0.4 | 0.2145 | 0 | 0.4609 | 0.1983 | 0.5921 | 0.5917 | ||

| 640 | 32 | 0.15 | 0 | 0 | 0.0018 | 0.0002 | 0.0025 | 0.0025 | |

| 32 | 0.25 | 0.001 | 0.0003 | 0.0203 | 0.0075 | 0.0212 | 0.0212 | ||

| 32 | 0.4 | 0.4243 | 0.0203 | 0.4908 | 0.5379 | 0.673 | 0.6724 | ||

| 80 | 0.15 | 0 | 0 | 0.002 | 0.0002 | 0.0025 | 0.0025 | ||

| 80 | 0.25 | 0.001 | 0.0003 | 0.0203 | 0.0075 | 0.0212 | 0.0212 | ||

| 80 | 0.4 | 0.4242 | 0.0203 | 0.4974 | 0.5374 | 0.6746 | 0.6743 | ||

| 128 | 0.15 | 0 | 0 | 0.0021 | 0.0002 | 0.0025 | 0.0025 | ||

| 128 | 0.25 | 0.001 | 0.0003 | 0.0203 | 0.0075 | 0.0212 | 0.0212 | ||

| 128 | 0.4 | 0.424 | 0.0203 | 0.5048 | 0.5369 | 0.6753 | 0.675 | ||

| 2000 | 200 | 360 | 0.15 | 0 | 0 | 0.0007 | 0 | 0.0022 | 0.0022 |

| 360 | 0.25 | 0.0001 | 0 | 0.0198 | 0.0029 | 0.0222 | 0.0222 | ||

| 360 | 0.4 | 0.073 | 0 | 0.3331 | 0.0792 | 0.4315 | 0.4311 | ||

| 900 | 0.15 | 0 | 0 | 0.0022 | 0 | 0.0024 | 0.0024 | ||

| 900 | 0.25 | 0.0001 | 0 | 0.021 | 0.0029 | 0.0373 | 0.0373 | ||

| 900 | 0.4 | 0.073 | 0 | 0.338 | 0.0792 | 0.4515 | 0.4515 | ||

| 1440 | 0.15 | 0 | 0 | 0.0024 | 0 | 0.0024 | 0.0024 | ||

| 1440 | 0.25 | 0.0001 | 0 | 0.0378 | 0.0029 | 0.0428 | 0.0428 | ||

| 1440 | 0.4 | 0.0729 | 0 | 0.432 | 0.0792 | 0.5173 | 0.5144 | ||

| 600 | 280 | 0.15 | 0 | 0 | 0.0007 | 0 | 0.0007 | 0.0007 | |

| 280 | 0.25 | 0.0001 | 0 | 0.0197 | 0.0029 | 0.0205 | 0.0205 | ||

| 280 | 0.4 | 0.2058 | 0 | 0.4093 | 0.196 | 0.5194 | 0.5176 | ||

| 700 | 0.15 | 0 | 0 | 0.0007 | 0 | 0.002 | 0.002 | ||

| 700 | 0.25 | 0.0001 | 0 | 0.02 | 0.0029 | 0.0205 | 0.0205 | ||

| 700 | 0.4 | 0.2058 | 0 | 0.4374 | 0.196 | 0.5678 | 0.5657 | ||

| 1120 | 0.15 | 0 | 0 | 0.0014 | 0 | 0.0024 | 0.0024 | ||

| 1120 | 0.25 | 0.0001 | 0 | 0.0201 | 0.0029 | 0.0206 | 0.0206 | ||

| 1120 | 0.4 | 0.2057 | 0 | 0.4545 | 0.1959 | 0.5908 | 0.5906 | ||

| 1600 | 80 | 0.15 | 0 | 0 | 0.0007 | 0 | 0.0007 | 0.0007 | |

| 80 | 0.25 | 0.0003 | 0.0001 | 0.009 | 0.0029 | 0.0172 | 0.0172 | ||

| 80 | 0.4 | 0.4223 | 0.0114 | 0.4823 | 0.5288 | 0.6665 | 0.6658 | ||

| 200 | 0.15 | 0 | 0 | 0.0007 | 0 | 0.0007 | 0.0007 | ||

| 200 | 0.25 | 0.0003 | 0.0001 | 0.009 | 0.0029 | 0.0184 | 0.0184 | ||

| 200 | 0.4 | 0.4222 | 0.0114 | 0.4866 | 0.5286 | 0.6689 | 0.6683 | ||

| 320 | 0.15 | 0 | 0 | 0.0007 | 0 | 0.0007 | 0.0007 | ||

| 320 | 0.25 | 0.0003 | 0.0001 | 0.009 | 0.0029 | 0.0194 | 0.0194 | ||

| 320 | 0.4 | 0.422 | 0.0114 | 0.4935 | 0.5283 | 0.6724 | 0.6715 |