Approximate Factor Models with Strongly Correlated Idiosyncratic Errors

Abstract

We consider the estimation of approximate factor models for time series data, where strong serial and cross-sectional correlations amongst the idiosyncratic component are present. This setting comes up naturally in many applications, but existing approaches in the literature rely on the assumption that such correlations are weak, leading to mis-specification of the number of factors selected and consequently inaccurate inference. In this paper, we explicitly incorporate the dependent structure present in the idiosyncratic component through lagged values of the observed multivariate time series. We formulate a constrained optimization problem to estimate the factor space and the transition matrices of the lagged values simultaneously, wherein the constraints reflect the low rank nature of the common factors and the sparsity of the transition matrices. We establish theoretical properties of the obtained estimates, and introduce an easy-to-implement computational procedure for empirical work. The performance of the model and the implementation procedure is evaluated on synthetic data and compared with competing approaches, and further illustrated on a data set involving weekly log-returns of 75 US large financial institutions for the 2001–2016 period.

Keywords: convex optimization; alternating minimization; convergence; high-probability error bounds.

1. Introduction.

Factor models are widely used in a number of scientific fields for reducing the dimension of data sets comprising of a large number of variables (Anderson, 2003). A factor model assumes that each variable under consideration can be expressed as a linear combination of a small number of latent factors plus an idiosyncratic component (error term). Co-movements among the variables can be accounted for by these few factors thus aiding interpretation. When exact factor models are used in the analysis of cross-sectional data, it is assumed that the idiosyncratic components are mutually uncorrelated (Anderson, 2003). However, for time series data such assumptions are often too restrictive, especially if a large panel of time series is considered where the common factors may not fully capture all relationships among the observed time series; in this case, it is of interest to examine approximate factor models that also allow for correlations amongst the idiosyncratic components.

Such an approximate factor model was introduced in Chamberlain and Rothschild (1983) for the analysis of portfolios comprising of a large number of assets. Since then, a number of papers have appeared in the literature investigating properties of such approximate factor models, under the assumption that the correlations between the common factors and the idiosyncratic component, as well as those amongst the idiosyncratic components are weak. Formally, the approximate factor model is defined as

| (1) |

where is a vector of -dimensional time series, a -dimensional latent factor process, a matrix of factor loadings and the vector of idiosyncratic components. It is often further assumed that the factor process exhibits Vector Autoregressive dynamics, namely , where is a serially uncorrelated error process that is independent across its coordinates, and are transition matrices. The model in (1) is typically estimated through principal component (PC) decomposition, which operates under the assumption that as the time series panel size , the leading eigenvalues of diverge, whereas all eigenvalues of are bounded, thus enabling the separation between the common factors and the idiosyncratic components. Some key theoretical results for this model are given in Bai and Ng (2002); Bai (2003), where asymptotic normality of the estimated factors and factor loadings111up to some invertible transformation obtained from PC analysis is established, under a scaling for the former result and a scaling for the latter. Further, if , then the maximum time-indexed deviation of the estimated factors relative to their true values vanishes. In later work, Stock and Watson (2005) consider the same factor model representation, but each coordinate of is allowed to exhibit serial correlation, and assumed to be uncorrelated with across all time leads and lags. By decorrelating the coordinates of the error process222With a slight abuse of notion, here we use to denote the term that collects the lags of the actual factors that enter the model after decorrelation., the model can written in the form of

| (2) |

where is a diagonal matrix with each entry being the autoregressive polynomial corresponding to coordinates of , while is a pure noise term that is neither cross-sectionally nor serially correlated.

The presence of strongly correlated idiosyncratic components in the model can lead to distorted estimation and inference, resulting in overestimation of the number of factors (Greenaway-McGrevy et al., 2012) and is detrimental for forecasting purposes (Anderson and Vahid, 2007). Within the DFM framework, a common remedy entails the inclusion of lagged terms of (e.g. Anderson and Vahid, 2007; Carare and Mody, 2010; Liu and Spencer, 2013; Eichengreen et al., 2012), which however augments the number of model parameters at the rate of . To overcome the technical issues arising from jointly estimating a large number of parameters, these methods either implicitly assume a small panel size (e.g. Anderson and Vahid, 2007) so that their application does not suffer from the curse of dimensionality, or resort to estimating models based on pairwise univariate series from the components (e.g. Liu and Spencer, 2013).

In a related line of work, Forni et al. (2000) introduced the generalized dynamic factor model (GDFM) framework that dictates the existence of two mutually orthogonal processes that capture the common and idiosyncratic components, respectively. The dynamic factors spanning the common space can be general -integrable processes and estimated through principal components in the frequency domain (Forni et al., 2005, 2015).

Despite the generality of the GDFM framework, whose formulation ensures orthogonality between the independent and identically distributed noise process and the common space, its common space recovery relies on estimated spectral density matrices that can exhibit numerical instabilities when the dimensionality of becomes large (Fiecas et al., 2014). On the other hand, the aforementioned shortcomings of the DFM framework can be largely mitigated, through the inclusion of lagged terms and a formulation that jointly estimates model parameters via a computationally stable procedure. To this end, following Stock and Watson (2005), we write the approximate factor model in the form given in (2), but allow for to exhibit cross-correlation structure; i.e. is not restricted to be diagonal, but merely sparse. Hence, the dynamics of the time series in can be written in the form of a lag-adjusted static factor model, with the lag term impacting the current values through sparse transition matrices. Through cross-sectional de-correlation, becomes a strictly exogenous noise process comprising of independent and identically distributed shocks, and the model representation aligns with that under the GDFM framework, with the lagged term(s) and the factors collectively capturing the common space and accounting for all pervasive shocks. In the proposed model specification, two key quantities are the space spanned by the common factors (the “factor hyperplane” henceforth), and the sparse transition matrices of the time lags of the observable process. To obtain their estimates, we formulate a penalized maximum likelihood objective function, introduce a block-coordinate descent algorithm to solve the posited optimization problem and establish finite sample high-probability error bounds for the convergent solution estimates. Finally, note that the transition matrices of the lagged values can provide useful and interpretable information, as shown in our application study and noted in Eichengreen et al. (2012); Liu and Spencer (2013).

Together with the proposed model specification that allows for strongly correlated idiosyncratic components in approximate factor models, key contributions of this work entail the convex formulation that leads to joint estimation of the model parameters, as well as the technical developments that provide insights on appropriately handling the interaction between the latent factor space and the lagged space spanned by the past history of the observed process. In particular, the strategy used to establish error bounds is applicable to other high-dimensional statistical models involving simultaneously observed and latent components.

The remainder of this paper is organized as follows. In Section 2, we introduce our model setup, estimation procedure for model parameters, as well as steps for performing forecast. Theoretical properties of the proposed estimators are established in Section 3, including their high-probability statistical error bound, and convergence property. In Section 4, we introduce an empirical implementation procedure and present the performance evaluation of the estimates based on synthetic data. In Section 5, an application of our model to weekly stock return data of large US financial institutions for the period from 2001 to 2017 period is considered. Finally, Section 6 concludes the paper.

Notation. Throughout this paper, for some generic matrix of dimension , we use to denote its matrix norms, including the operator norm , the Frobenius norm , the nuclear norm , , and . We use and to denote the elementwise -norm and infinity norm. Additionally, we use to denote its spectral radius . For two matrices and of commensurate dimensions, denote their inner product by . Finally, we write if there exists some absolute constant that is independent of the model parameters such that .

2. Problem Formulation, Estimation and Forecast.

We start by introducing the model assuming that the idiosyncratic component follows the aforementioned sparse model, which simultaneously incorporates the cross-sectional and serial structure among its coordinates. To convey the main arguments, we assume without loss of generality that for the ease of exposition, and present the extension to the general lag case in the Supplement.

The starting point is the dynamic factor representation of the observable process , where is the common latent factor; is the idiosyncratic component whose dynamics satisfy with being the lagged matrix polynomial for some weakly sparse . Multiplying on both sides leads to the dynamic factor model consisting of (3) and (4), where collects the lags of so that it only enters the dynamics of contemporaneously, and is additionally assumed to follow some VAR model with lagged polynomial :

| (3) | ||||

| (4) |

is a mean zero noise process that is both serially and cross-sectionally uncorrelated. Moreover, it is strictly exogenous satisfying and , . The parameters of interest are the factor hyperplane (to be specified later) and the sparse transition matrix . Note that here we only require to be weakly sparse, the notion of which can be formalized through the definition of an ball with radius (c.f. Negahban et al., 2012):

| (5) |

The case of exact sparsity corresponds to where has at most nonzero entries; whereas for , the ball imposes constraints on the decay rate of ’s.

To ensure that is covariance stationary, we require that the spectral radius of satisfies without further restricting . Additionally, note that under the assumption that the spectral density of exists, the spectral density of the filtered process satisfies

Correspondingly, the spectral density of is given by

where and respectively denote the spectrum and cross-spectrum of some generic process and :

with and .

2.1 Estimation through a convex program.

Given a sample of the -dimensional observable process , denoted by , let

where and respectively denote the contemporaneous response matrix and the lagged predictor matrix, and denotes the latent factor matrix with the latent factor at time point stacked in its rows. The noise matrix is analogously defined. We additionally define the factor hyperplane associated with the latent factor as , and note that has rank at most . With the above notations, the model in (3) for the observed samples can be written as . With the transition matrix assumed sparse and the factor hyperplane being low rank, we formulate the following constrained optimization problem:

| (6) |

with the feasible region determined through a rank constraint imposed on and a sparsity-inducing norm constraint imposed on .

The rank constraint in (6) leads to a non-convex feasible region, making it particularly hard to characterize the obtained solution analytically as it depends on the initial values provided to the algorithm. Thus, as commonly undertaken in the literature (e.g. Agarwal et al., 2012b), we consider a tight convex relaxation of the rank constraint, and the solution to the convexified program has convergence guarantees independent of the initializer. Formally, we consider obtaining the estimator through the convex program in (7), which can be obtained from (6) by alternatively considering the nuclear norm constraint for the factor hyperplane and the norm constraint for the sparse transition matrix in Lagrangian form:

| (7) |

where and are tuning parameters. The solution can be obtained by a block-coordinate descent algorithm which alternately minimizes with respect to and , as outlined in Algorithm 1.

Reconstruction of the factors.

The solution to (9) provides an estimate of the factor hyperplane, based on which realizations of the -dimensional latent factors process can be reconstructed under certain identifiability restrictions. As mentioned in Section 1, for any invertible matrix , the following equality holds

hence, given a factor hyperplane and the latency of the factors, to fully identify the factors and the corresponding loading matrix from their observationally equivalent counterpart , a total number of restrictions is required to address their indeterminacy. Various choices for the identification restrictions have been discussed in the literature (e.g., Bai and Ng, 2008, and references therein), including the most popular PC estimator (Stock and Watson, 2002) which assumes orthogonality for both the factors and the loadings, as well as the ones that implicitly assume certain ordering of the factors and impose specific structural restrictions on the loading matrix (see PC2 and PC3 identification restrictions in Bai and Ng, 2013). Under these restrictions, the factors and the loading matrix can always be uniquely identified333For the PC estimator or under the PC2 restriction, where and is assumed lower-triangular, the identification is up to sign rotation; under the PC3 one, where the upper upper sub-matrix of is assumed an identity matrix and is left unrestricted, the identification is exact (see Bai and Ng, 2013). and obtained based on the SVD of the estimated hyperplane . It is worth noting that regardless of the identification restrictions that lead to different versions of the estimated factors, the space spanned by the estimated factors is invariant once is obtained. Specifically, forecasting future values of does not require an exact recovery of , as discussed next.

2.2 Forecasting.

Given estimates of the transition matrix and of the hyperplane, we consider the following procedure that first obtains forecasts of the filtered process through projection onto the factor space, followed by a lag adjustment to obtain those of the .

To this end, according to the model in (3), the filtered process can be represented as , whose -step-ahead best linear predictor based on is given by the projection , where denotes the linear space spanned by (Stock and Watson, 2002; Forni et al., 2005). In particular, based on estimate , the filtered process can be estimated through , whose common space estimate corresponds to . Using the surrogate process , let the sample covariance be ; the -step-ahead forecast of is then given by

| (8) |

where columns of are the right singular vectors of corresponding to nonzero singular values, and are effectively an orthonormal basis for the factor space. In the case where , ; in the case where , can be obtained inductively by sequentially estimating , for all . Algorithm 2 outlines the forecasting procedure.

Connections to GDFM.

To conclude this section, we discuss similarities of the proposed formulation to the GDFM (e.g., Forni et al., 2000, 2005). GDFM encompasses a broader class of factor models wherein the observed process admits a decomposition into two mutually orthogonal processes that respectively capture the common and the idiosyncratic component (Forni et al., 2000), with the former not limited to a VAR representation. From a modeling perspective, as pointed out in Lütkepohl (2014), the distinction between GDFM and the state-space form of DFM (e.g., Stock and Watson, 2005, which is also the factor model specification adopted in this paper) is not that substantial, since stationary processes can be approximated arbitrarily well by VAR processes with unrestricted order of lags. From the estimation perspective, however, to accommodate the potentially more complex dynamics of the factor processes, GDFM recovers the common space leveraging the spectral domain features of the processes, and the dynamic factors are obtained by solving a generalized eigen-equation w.r.t. estimated covariance matrices of the common and the idiosyncratic components (Forni et al., 2005). In our formulation, we posit an optimization that jointly estimates the factor space and the lagged space, which accounts for the lag information explicitly, under mild sparsity assumptions.

The empirical performance of the two procedures is considered and compared in Section 4 under various data generating mechanisms.

3. Theoretical Properties.

To establish statistical properties of the estimators, a ball constraint on the feasible region of is required to incur additional compactness on the low rank component that limits the spikiness of its entries, and this enables identification of the sparse component . To this end, throughout this section, we consider estimators that are solutions to the following convex program:

| (9) | ||||

where is a box constraint given by

is chosen such that the true value of the parameters is always feasible. We will provide further illustration on the interpretation of such a box constraint in Section 3.1 and Remark D.1. falls into the class of regularized -estimators, whose theoretical properties have been extensively studied in the statistical literature for diverse settings (e.g., Agarwal et al., 2012a; Loh and Wainwright, 2012).

A road map to establish properties of the estimators for is given next: first in Section 3.1 we derive non-asymptotic statistical error bounds of and under certain regularity conditions, when the proposed estimation procedure is based on a deterministic realization of the observable process . In particular, the required regularity conditions primarily entail the restricted strong convexity (RSC) condition (Agarwal et al., 2012b) and that the choice of and is in accordance with some deviation condition (Loh and Wainwright, 2012). Subsequently, in Section 3.2, we establish that the required conditions are satisfied with high probability, and provide probabilistic analogues of key model parameters’ error bounds for random realizations drawn from the underlying observable Gaussian process and the latent process . We also briefly discuss how the model identifiability issue is tackled through the constrained formulation adopted in (9). Finally in Section 3.3, from a numerical perspective, we establish the convergence of the proposed iterative algorithm to a stationary point. All proofs are deferred to Appendices A and C. Throughout our exposition, we use superscript to denote the true value of the parameters of interest, and denote the errors of the estimators by and , respectively.

3.1 Statistical Error Bounds with Deterministic Realizations.

We start by introducing some additional notation needed in the ensuing technical developments. Let denote the loss function, given by

The true number of latent factors is given by and thus . Further, given some (to be specified later), let denote the thresholded support set of , and we use to denote its cardinality, that is, and . Finally, let denote the sample covariance matrix of the error process and let be its maximum eigenvalue. Formally, the RSC condition (c.f. Agarwal et al., 2012b; Negahban et al., 2012) is defined as follows.

Definition 1 (Restricted Strong Convexity (RSC)).

For some generic data matrix , it satisfies the RSC condition with respect to norm with curvature and tolerance if

In our context, we consider the element-wise norm .

Further, for high dimensional sparse VAR models ( in the current setup), the tuning parameter needs to satisfy a deviation condition (Loh and Wainwright, 2012; Basu and Michailidis, 2015), namely,

which can be simplified to . Under the current model setup, however, the deviation condition is significantly more involved and requires proper modifications to incorporate quantities associated with the factor hyperplane, as seen in Theorem 1.

Before stating the main results, we provide a brief discussion on the box constraint on , which aims to “limit” the spikiness of the low rank component, and hence the interaction between the latent factor space and the observable lag space spanned by — in particular, for and to be properly recovered, such interaction can not be too large. Due to the basis vectors of the factor space being latent, a direct restriction on the interaction is impractical and conceptually unsatisfying, whereas the box constraint adopted effectively restricts the product of the signals from the two spaces and serves our objective, as shown in the proof of Theorem 1 and Remark 1. Note that this constraint is in the same spirit to similar ones in the literature (e.g., Agarwal et al., 2012b; Negahban and Wainwright, 2012), and the norm of is necessary since the two spaces have distinct bases.

Theorem 1 (Error bound for under fixed realizations).

Suppose fixed realizations of process satisfy the RSC condition with curvature and a tolerance such that

| (10) |

Then, for any matrix pair that generates the evolution of the process, for estimators obtained by solving the optimization (9) with regularization parameters and satisfying

| (11) |

the following error bound holds for some positive constants , and :

| (12) |

where ,

Next, we comment on the error bound in (12) and the required conditions in (10). The error bound encompasses three terms that are respectively associated with the transition matrix , the low rank factor space , and the tolerance which measures the extent to which the log-likelihood function deviates from strong convexity (see Definition 1). Both and depend on three components: (1) the overall curvature of the log-likelihood function as captured by , (2) the interaction structure between various components of the underlying process, as captured by the tuning parameters and , and (3) the inherent structure of the parameters as captured by , and — in particular, due to the approximately sparse structure of , both the density level of its strong support set and the magnitude of its “weak” entries play a role, with the two respectively reflecting the estimation error and the approximation error (c.f. Agarwal et al., 2012b) after proper scaling. The curvature as measured by dictates the constraint to which the tolerance needs to conform (see Equation (10)), and such a constraint is also interrelated to and : for (10) to be satisfied, neither nor can be too large. Moving to the tuning parameters, can be sub-divided into two terms: the cross-product term measures the maximum interaction between the design matrix and the noise , which according to model assumption (population level) should center around 0; where the term corresponds to an upper bound on the interaction between the latent (factor) space and the observed one (). For , we require that it dominates the maximum signal coming from the error process in the form of . Thus, a smaller is needed when interactions between associated terms are weaker and similarly a smaller is needed if the magnitude of the noise is weaker, thus leading to a tighter error bound for the estimates. Finally, it is worth noting that is a result of the approximately sparse structure of ; in the special case where is exactly sparse, this term would be 0.

Corollary 1 gives the bound of and with specific choice of the thresholded level , when the true value lies in the ball of radius (see definition in Equation (5)):

Corollary 1.

Under the same set of conditions as in Theorem 1, with , by choosing the thresholded level according to where , the following error bound holds for some positive constants and :

3.2 High Probability Bounds under Random Realizations.

Next, we provide high probability bounds/concentrations for key quantities associated with the derived error bound in Section 3.1, for random Gaussian realizations of the underlying factor and error processes. Specifically, this involves the verification of the RSC condition, as well as the examination of quantities associated with the deviation condition to which the choice of needs to conform, as shown in (11).

We introduce additional notation for the subsequent technical developments. For some generic process , in addition to the auto-covariance function and its spectral density , we define its maximum and minimum eigenvalue associated with the spectral density introduced in Section 2 as follows (Basu and Michailidis, 2015):

For two generic centered processes and that are assumed jointly covariance stationary, whose spectral density is given by where , the upper extreme for is analogously defined as

In general , but .

For the processes involved in our proposed model, recall that , and are mean zero Gaussian processes. In particular, is a noise process that does not exhibit temporal nor cross-sectional dependence, hence it is effectively a Gaussian random vector with covariance , and its spectral density simplifies to . Further, we define the shifted process for notation convenience.

The following lemma verifies that with high probability, for random realizations of the process , the RSC condition is satisfied provided that the sample size is sufficiently large:

Lemma 1 (verification of the RSC condition).

Consider whose rows are some random realization of the stable process with dynamic given in (3). Then there exist positive constants such that with probability at least , the RSC condition holds for with curvature and tolerance satisfying

provided that .

The next lemma establishes a high probability bound for the interaction term that influences the choice of through its elementwise norm.

Lemma 2 (High probability bound for ).

There exist positive constants such that for sample size , with probability at least , the following bound holds:

| (13) |

Note that with the definition of the shifted processes , we have , which implies . Hence, the term that measures the upper extreme of the cross-spectrum between and the shifted process in (13) can be replaced by its unshifted counterpart. Moreover, since , its upper extreme is given by .

The next lemma provides an upper bound for the maximum eigenvalue of the sample covariance matrix.

Lemma 3 (High probability concentration for ).

Consider whose rows are independent realizations of the mean zero Gaussian random vector with covariance . Then, for sample size , with probability at least , the following bound holds:

Up to this stage, we have verified the RSC condition and obtained the high probability bounds for quantities that are associated with the choice of , for random realizations from the underlying processes. Theorem 2 combines the results in Corollary 1 and Lemmas 1 to 3, and provides a high probability error bound of the estimates when the data are random realizations from the underlying processes, as stated next.

Theorem 2 (High probability error bound with random realizations).

Suppose we are given a snapshot of length from the -dimensional observable process , whose dynamics are described in (3) with . Then, there exist universal positive constants and such that for sample size , by solving convex problem (9) with regularization parameters

the solution has the following bound with probability at least , by choosing the thresholded level at with :

| (14) |

where are positive constants that are independent of and .

Remark 1.

Note that Theorem 2 requires that for relevant quantities to properly concentrate; as a consequence, the estimation errors for and are jointly bounded. The sample size requirement is of the same order as in classical factor analysis444In classical factor analysis, for both the factors and its loadings to be consistently estimated, both and are required to hold simultaneously. literature (e.g. Bai and Ng, 2008), and is standard under the context of recovering a low-rank component based on noisy data in high-dimensional statistics (e.g., Agarwal et al., 2012b). The nature of the upper bound provided is a consequence of being latent, and hence the low rank factor hyperplane and the error term become not perfectly distinguishable; in particular, the structure of the underlying optimization resembles a noisy matrix completion problem in which the restricted isometry property is violated (see also Candes and Plan, 2010). Further details on model identifiability issues are given in Appendix B.

3.3 Convergence Analysis of Algorithm 1.

The convergence property of Algorithm 1 can be established using familiar arguments and exploiting its convex nature. Specifically, define the objective function is given by

and is jointly convex in , with a convex feasible region . Thus, it directly follows from Tseng (2001) that the alternating minimization that generates the sequence converges to a stationary point which is also a global optimum, though the global optimum is not necessarily unique.

To conclude this section, we remark that the theoretical formulation in (9) can be solved in an analogous way to Algorithm 1. Specifically, the update of requires modification to satisfy the constraint on the feasible region of , and the partial minimization can be solved by employing the composite gradient descent algorithm of Nesterov (2007) that involves singular value thresholding steps. Nevertheless, the modified algorithm is also convergent, as the one in Algorithm 1.

4. Implementation and Performance Evaluation.

In this section, we present results for simulation studies under various settings to demonstrate the performance of our proposed model. As comparison, we also present the common space (to be defined later) recovery error and the one-step-ahead forecast error across our proposed method, the vanilla factor analysis using PC method a la Stock and Watson (2005), and the proposed method in Forni et al. (2005).

An empirical algorithmic relaxation.

The actual implementation of Algorithm 1 requires , as inputs, which in practice are challenging to select. On the other hand, the computation procedure designed for solving the convex program in (7) suggests that to obtain the estimates boils down to alternating between the following two steps: (1) a regularized regression (lasso) update on the rows of ; and (2) an SVT update on . This naturally motivates the following steps in the implemented version of the algorithm, outlined next in Algorithm 3.

Algorithm 3 outlines the algorithmic relaxation to obtaining in (7), and it can be viewed as an alternating minimization algorithm that solves

| (15) |

For each update, the partial minimization step with respect to or ensures that the value of the objective function is always non-ascending, which together with the fact that the objective function is bounded below guarantees convergence of the objective function iterates. In practice, the algorithm is terminated when the descent magnitude of the objective function between successive iterations is smaller than some pre-specified tolerance level. This algorithm does not provide guarantees of convergence to a stationary point of the sequence of iterates, which requires stronger assumptions — either the convexity of the objective function and the constraint region, or the uniform compactness of the generated sequence of iterates.

Choice of the tuning parameter and the rank constraint .

The implementation of Algorithm 3 requires a specific pair of as input. We consider choosing the optimal pair of based on the information criterion proposed in Ando and Bai (2015), called the Panel Information Criterion (PIC) and defined as:

| (16) |

where and are solutions to (15) with the specific pair of plug-in . The optimal pair is then selected in two steps: in step 1, we obtain that gives the smallest PIC over a lattice ; in step 2, we fix at where is the number of lags corresponding to the sparse model, and seek for over a grid that minimizes PIC. The optimal pair of tuning parameters is then given by .

Data generating mechanism.

Synthetic data are generated according to the lag-adjusted factor model representation . Starting from the standard approximate factor model representation , is serially correlated and follows a model555Throughout this section, we assume ; additional results for have been deferred to Supplement E., at each timestamp , the -dimensional factor is generated according to a model where ; decorrelating leads to following dynamic of :

where and .

We consider several simulation settings as listed in Table 1 to test various facets of the model, primarily encompassing the dimensionality of the system and the number of factors , as well as the sparsity structure of and its spectral radius that captures the level of autocorrelation. In addition to settings S0 to S4 where is Gaussian, to test the robustness of the proposed model to the presence of heavy tails, we consider also cases where follows some multivariate distribution (S5 to S7). Throughout all numerical experiments presented in this section, the sample size is fixed at 200 and the spectral radius of the system is set randomly from .

| sparsity structure of | structure of -dist. | factor space/lag space relative strength | |||||

| S0 | 100 | , exactly sparse | 2 | 1 | diagonal - | strong factor | |

| S1 | 100 | , weakly sparse | 0.7 | 2 | 1 | Toeplitz(0.2) - | strong factor |

| S2 | 300 | , weakly sparse | 0.7 | 5 | 1 | diagonal - | strong factor |

| S3 | 200 | , exactly sparse | 0.9 | 5 | 2 | diagonal - | strong lag |

| S4 | 200 | , weakly sparse | 0.7 | 5 | 4 | Toeplitz(0.2) - | strong factor |

| S5 | 100 | , exactly sparse | 0.7 | 5 | 1 | diagonal - | strong factor |

| S6 | 200 | , weakly sparse | 0.7 | 5 | 1 | Toeplitz(0.2) - | strong factor |

To generate the sparse transition matrix , for each row that corresponds to the coefficients of each single time series regression, its (strong) support set is randomly generated to meet the specified density level (i.e., or ), and nonzero entries are then generated from . In the case of a weakly sparse , entries in the weak support set are generated from . Finally, all entries are scaled to meet the specified level, to ensure that the system is stationary. For the dense factor loading matrix , its entries are generated from . It is worth noting that the value of and are set so that the factor/lag space relative strength is satisfied, measured by the empirical relative signal-to-noise ratio for the and the component.

Performance evaluation.

To measure the accuracy of the obtained estimates and forecast, we focus on the following four components of the model:

-

–

For the (weakly) sparse transition matrix we use sensitivity , specificity and relative error in Frobenius norm () as evaluation criteria. Note that in the case where is weakly sparse, despite the fact that entries in the weak support set are not exactly zero, they are effectively deemed as zeros for comparison purpose.

-

–

For the factor hyperplane , since we don’t separately identify the factors and in addition the factor space is invariant to identification restrictions, we measure its relative error in Frobenius norm (), as well as its relative projection error, defined as , where with being the orthonormal basis of ; can be analogously defined. Note that the following correspondence between distance and the projection error holds: ; moreover, this metric is not applicable in high-dimensional regimes () where it would stays at zero.

-

–

For the common space, in the case where it is estimated with the proposed lag-adjust DFM, at the population level it is captured by and hence its estimate is given by ; whereas in the case where the model is estimated based on the SW formulation or GDFM, the estimated factor space coincides with that of the common space. For all three models, we present the relative error in Frobenius norm of the estimates.

-

–

For the one-step-ahead forecast, we measure its squared norm w.r.t. the oracle , that is, , where the oracle is given by and can be viewed as the “denoised” version of .

| recovery (lag-adj DFM) | recovery (lag-adj DFM) | common space recovery | one-step-ahead forecast | |||||||||

| SEN | SPC | lag-adj DFM | SW | GDFM | lag-adj DFM | SW | GDFM | |||||

| S0 | 0.99 | 0.98 | 0.28 | 2 | 0.15 | 0.20 | 0.13 | 0.32 | 0.31 | 0.51 | 0.60 | 0.53 |

| S1 | 0.97 | 0.92 | 0.51 | 2 | 0.16 | 0.47 | 0.27 | 0.47 | 0.45 | 0.56 | 0.91 | 0.66 |

| S2 | 0.99 | 0.95 | 0.74 | 5 | – | 0.58 | 0.35 | 0.45 | 0.45 | 0.60 | 0.73 | 0.67 |

| S3 | 0.99 | 0.98 | 0.19 | 5 | – | 0.26 | 0.22 | 0.72 | 0.50 | 0.36 | 0.92 | 0.90 |

| S4 | 0.98 | 0.97 | 0.58 | 5 | – | 0.51 | 0.32 | 0.44 | 0.44 | 0.47 | 0.58 | 0.57 |

| S5 | 0.92 | 0.92 | 0.61 | 5 | 0.31 | 0.48 | 0.10 | 0.13 | 0.14 | 0.43 | 0.42 | 0.45 |

| S6 | 0.98 | 0.93 | 0.47 | 5 | – | 0.53 | 0.35 | 0.63 | 0.65 | 0.55 | 0.90 | 0.92 |

As Table 2 demonstrates, for all three components, estimates obtained from Algorithm 3 exhibit good performance. In particular, (i) the proposed method is robust to the sparsity structure of , as both exactly-sparse and weakly-sparse settings yield very satisfactory strong support recovery (see S1, S2 and S4). (ii) A larger panel size leads to improved factor hyperplane recovery, as manifested in the form of smaller relative error in magnitude estimation although it requires the sparsity of the transition matrix to decrease accordingly (recall that it is set to ); however, the performance deteriorates as the dynamics of become more complex (e.g., S4). (iii) A strong signal in the lag-space leads to improved recovery of , despite the presence of stronger temporal dependence which empirically incurs the algorithm to take more iterations to converge (e.g., S3). For all settings, PIC correctly selects the number of factors, which translates into the correct identification of the rank constraint.

Next, we compare the performance of common space recovery and forecasting for the following three methods: the posited model, standard SW formulation and GDFM. For SW (Stock and Watson, 2005), the reported error is based on the minimum error among estimates obtained under different rank constraints ranging between and ; for GDFM (Forni et al., 2005), the reported error is based on the minimum error among estimates obtained under different combinations of that determines the number of common factors when loaded dynamically and contemporaneously. For all settings, the proposed method (lag-adjusted DFM) outperforms the other two by explicitly incorporating the lag space spanned by ; specifically, it outperforms its competitors by a wide margin when the lag space possesses a stronger signal, in which case SW becomes particularly susceptible (e.g., S3 and S6). However, as the dynamics of becomes more involved, its advantage becomes less pronounced (S4).

Finally, the proposed model is relative robust to the presence of heavy tails, although the performance deteriorates compared to the Gaussian case. Specifically, when the distribution shows significant deviation from Gaussian (e.g., S5), the degradation manifests itself through less satisfactory recovery in the support of and larger error of the estimated factor space; whereas the forecasting performance isn’t affected. On the other hand, with lighter tails (e.g., S6), the performance becomes comparable to the Gaussian case.

4.1 Alternative DGPs.

To further compare the performance across all three methods, we consider settings where data generating processes deviate from the proposed model in (3). Specifically, we adopt the data generating mechanism in Forni et al. (2017, Model II), that is,

| (17) |

where coordinates of and are i.i.d standard Gaussian white noises processes, with capturing the structural shocks. Entries of and are drawn independently from ; entries of are first drawn independently from then scaled so that the spectral norm of satisfies some pre-specified target, with the latter drawn from . We focus on the performance of common space recovery and the one-step-ahead forecast, under various combinations of the model parameters, as listed in Table 3:

| common space recovery | one-step-ahead forecast | |||||||

|---|---|---|---|---|---|---|---|---|

| lag-adj DFM | SW | GDFM | lag-adj DFM | SW | GDFM | |||

| 100 | 2 | 4 | 0.212 (0.072) | 0.212 (0.072) | 0.208 (0.061) | 0.210 (0.812) | 0.210 (0.812) | 0.326 (4.528) |

| 100 | 4 | 4 | 0.144 (0.035) | 0.144 (0.035) | 0.143 (0.035) | 0.078 (0.324) | 0.078 (0.324) | 0.063 (0.768) |

| 200 | 4 | 6 | 0.119 (0.026) | 0.119 (0.026) | 0.121 (0.026) | 0.087 (0.302) | 0.087 (0.302) | 0.132 (1.679) |

| 300 | 6 | 6 | 0.100 (0.024) | 0.100 (0.024) | 0.085 (0.017) | 0.075 (0.351) | 0.075 (0.351) | 0.061 (0.263) |

As the results show, with the data generating procedure deviating from the proposed model in (3), with properly chosen tuning parameters, the performance of the proposed methodology matches that of SW by effectively having . Meanwhile, it is worth noting for all three methods, the performance of common space recovery shows significantly less variability compared with that of forecasting; in particular, the forecasting performance of GDFM exhibits the highest variance across replications, among the three methods.

5. Application to Returns of US Financial Assets.

Factor models have been widely used in financial applications. In particular, they have been employed in analyzing the dynamics of asset returns, either for the purpose of identifying risk factors, or for estimating the covariance structure amongst assets for better portfolio diversification and asset allocation (e.g., Fan et al., 2012). We applied the proposed modeling framework to a set of stocks return data corresponding to 75 large US financial institutions, which also exhibit strong (serial) correlation in the error terms. Specifically, we analyze the risk-free returns666The risk-free return of Stock at time is calculated as , where is its stock price at time and is the risk-free rate. of 25 banks, 25 insurance companies and 25 broker/dealer firms for the period of 2001-17. Note that this time period contains a number of significant events for the financial industry, including the growth of mortgage bank securities (Ashcraft et al., 2010) in the early 2000s, rapid changes in monetary policy in 2005-06, the great financial crisis (Eichengreen and O’rourke, 2010) in 2008-09 and the European debt crisis in 2011-12 and their aftermath. Our analysis identifies a number of interesting patterns, especially around the period 2007-09 encompassing the beginning, height and immediate aftermath of the US financial crisis, both through changes in the factor structure and the partial autocorrelation one governed by the VAR model transition matrix of the log-returns of these financial assets.

Data.

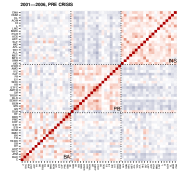

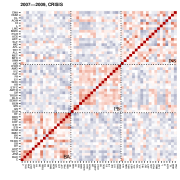

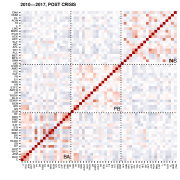

The data consist of weekly stock return data corresponding to 75 large financial institutions in terms of market capitalization, for the period of January 2001 to December 2017 and were obtained from the Center for Research in Security Prices (CRSP) database. The 75 companies are categorized into three sectors: banks (SIC code 6000–6199), broker/dealers (SIC code 6200–6299) and insurance companies (SIC code 6300–6499), with 25 in each sector (see also Billio et al., 2012). As we require that the data be available for the entire time span under consideration, 56 firms are kept for further analysis, since the remaining ones either went bankrupt or were forced to merge with financially healthier companies (e.g. Lehman Brothers and Merill Lynch in 2008, resp.). To get an overview of the correlation structure amongst the stocks after accounting for the first principal component that captures the weighted average return of the portfolio they constitute (Avellaneda and Lee, 2010), we plot the correlation among the principal component regression residuals. Specifically, the entire time span is broken into three sub-periods that have been previously considered in the literature (c.f. Billio et al., 2012): 2001–2006 (pre-crisis), 2007–2009 (crisis), 2010-2017 (post-crisis), and plot the correlation maps corresponding to samples in each period. As Figure 1 demonstrates, overall, we observe positive correlation within each sector and negative correlation across them. Such a structural pattern is predominant in the pre-crisis period especially within the insurance sector, and becomes significantly weaker in the post crisis one; whereas during the crisis, stronger negative correlation across blocks is present as well as scattered positive correlations. This suggests that different factor and auto-regressive structures emerge during the crisis period. Further, note that similar results hold if we examine the residuals after removing a second principal component, so as to capture a larger percentage of variance of the stock returns.

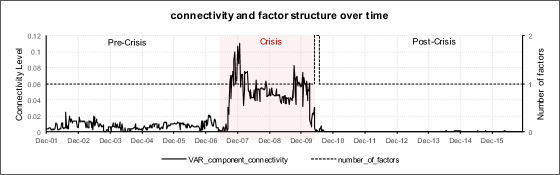

The analysis is based on 104-week-long rolling windows to avoid issues with non-stationarity that potentially depends on length of the period under consideration. This strategy has also been used in (Billio et al., 2012; Lin and Michailidis, 2017) and allows monitoring change in the number of factors over time, as well as the sparsity level of which measures the connectivity of the partial autocorrelation network across these financial institutions. Note that 48% of the rolling samples fail to reject the null hypothesis that they are multivariate normality777we consider the Henze-Zirkler’s multivariate normality test., with the exception of samples during the crisis period and those at the end of the sampling period post-crisis (around 2015–17). We fit the proposed lag-adjusted factor model in each time window, with tuning parameters selected according to a modified PIC criterion888The criterion is modified to . that does not depend on the range within which the number of factors is being searched.

As Figure 2 shows, sharp changes are observed in the temporal dependence structure of stock returns during the crisis period. In particular, two change points respectively correspond to the beginning of the 2007 sub-prime mortgage crisis and the ending of the 2008–2009 global financial crisis. Specifically, for the pre- and post-crisis periods, the density of the transition matrix stays at a level close to zero, suggesting that not much serial correlation exists in the idiosyncratic component after the common factor (proxy for the market portfolio) is accounted for. During the crisis period, however, the connectivity level of witnesses a sharp increase, reaching its maximum in the sampling window corresponding to Dec 2006–Dec 2008, during which period multiple major events of the financial crisis occurred. We also track the change in R-squared and the R-squared attributed to the factor over time, as a surrogate for the quality of the model fit, as shown in Table 4.

| pre-crisis | crisis | post-crisis | |

|---|---|---|---|

| Total Rsq | 42.11% | 58.18% | 56.76% |

| Factor Rsq | 41.29% | 54.39% | 56.50% |

In accordance with the connectivity level of the VAR component that captures the temporal dependence among the stocks, under normal market conditions, the majority fit of the model (R-squared) comes from the factor hyperplane; whereas during the crisis period, the gap between the total R-squared and the factor R-squared widens with the lag term explaining a non-negligible proportion of the R-squared, which indicates the presence of significant cross autocorrelations in the returns.

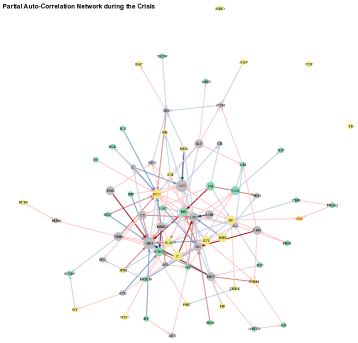

To further investigate the factor composition and the temporal dependence structure during the crisis period, we zoom in on the sampling frequency and focus on the year of 2008. Specifically, we consider daily data from January 2008 to December 2008 that cover 253 consecutive trading days and fit the proposed lag-adjusted factor model. Note that for this part of the analysis, the sample consists of 72 stocks. Using , 2 factors are identified, with the dominant one capturing 55% of the R-squared followed by 11% from the second. For reconstruction purposes, we assume they are orthogonal so that the factor composition can be retrieved from the singular vectors of .

As depicted in the left panel of Figure 3, all financial institutions contribute positively to the first factor, with dominating contributors spread in all sectors. The composition of the second factor shows an interesting pattern: two negative contributors are FRE (Freddie Mac) and FNM (Fannie Mae), and the positive ones are primarily in the insurance sector. However, AIG—unlike its peers—shows almost zero contribution to the second factor, albeit its strong contribution to the first one. The latter is consistent with other findings that it played a prominent role during the crisis.999According to an estimate as of January 2010, AIG accounted for 38% of the total losses incurred by insurance companies (98.2 out of 261.0 billions) since 2007. Source: Bloomberg, see also Schich (2010). In the right panel of Figure 3, we plot the partial auto-correlation network of the firms during the crisis after properly thresholding the entries that have small magnitudes, with red edges denoting positive links and with blue negative ones. Nodes that belong to the same sector are colored identically. A careful examination of the node weighted in/out-degrees shows that the top emitters are relatively uniform, in the sense that their weighted out-degrees do not differ by much; whereas the top receivers are dominant, since the weighted in-degrees for top receivers are significantly higher compared with the rest. Further top emitters heavily concentrate in the insurance sector. Meanwhile, some of the top receivers are also major contributors to the factors’ composition, e.g., AIG to the 1st factor, HIG to the 2nd, etc. This finding partially aligns with the role that many insurance companies played in magnifying the impact of the crisis on the overall stability of the financial system, due to their large insurance underwriting of Credit Default Swaps and subsequent exposure to accentuated risks (Eichengreen and O’rourke, 2010). However, this analysis points to the importance of insurance companies based on publicly available data and before their role in the crisis was fully revealed and understood. It is worth noting that with the same set of data, vanilla factor analysis using the information criterion proposed in Bai and Ng (2002) only identifies 1 factor, which further substantiates the aforementioned point that classical factor analysis may lead to skewed inference when strong correlation among the idiosyncratic component is present.

To conclude this section, we compare and contrast our results with those obtained in Billio et al. (2012), in which the authors consider 100 financial institutions comprising of the largest 25 among each of the four categories: hedge funds, broker/dealers, banks and insurers; thus, that data set is enhanced by the inclusion of big hedge funds for which publicly available stock quotes are not accessible. From the systemic risk standpoint, the authors measure the connectedness of the system based on principal component analysis (PCA) and Granger-causality network analysis during the 1994–2008 period, and identify increased level of interconnectedness during the crisis period and the asymmetry in the degree of connectedness amongst different sectors. Our results are qualitatively similar to these results, and the conclusions broadly match. However, we would like to highlight some key differences in both modeling and in the empirical results obtained. From the modeling perspective, Billio et al. (2012) consider two separate modeling strategies: (i) a Principal Components Analysis (akin to a static factor model) and (ii) a Granger-causality based analysis through fitting a VAR model for each pair of stocks returns. The PCA analysis examines a fixed number of principal components/factors and the authors argue that the increasing proportion of variation explained by them is an indication of the systematic response of the financial system to the crisis. Their pairwise based Granger-causal network also reveals increased connectivity during the crisis period. Our model considers latent factors and lead-lag relationships among stock returns simultaneously, thus gaining better and more informative insights. In addition, the lead-lag relationships are considered across all firms simultaneously rather than in a pairwise fashion. By incorporating the strong correlations present in the idiosyncratic component, our model is more parsimonious. Specifically, during the crisis, Billio et al. (2012) uses 10 principal components to account for 85% of the returns variance, whereas only 5 suffice in our model; further, the leading factor in their analysis only accounts 37% of the variance, compared to 50% in our model. Finally, extending the analysis period to 2017 shows that after 2011 the influence of banks and insurance companies on stock returns waned, as the marker slowly returned to normalcy. However, we are in broad agreement with the Billio et al. (2012) conclusion on the heightened role of banks and insurers up to 2009.

6. Discussion.

In this paper, we introduced a novel modeling framework that generalizes the classical approximate factor model to include lags of the observable process, so that stronger correlations among the idiosyncratic component can be accommodated. The autoregressive structure is assumed to be sparse, which enables its estimation for large time series panels. Estimation of the model parameters is based on a maximum likelihood formulation that leads to a convex optimization problem, and the resulting estimates come with high probability error bounds guarantees that can be expressed in terms of key structural parameters (, etc.), and exhibit superior empirical performance in synthetic data.

In addition to generalizing the model in Stock and Watson (2005), our proposed model can also be perceived as a robust treatment of endogeneity. Specifically, as noted by Anderson and Vahid (2007), in the presence of large values in and for a relatively small panel size , the factor estimates will be distorted as a result of this endogeneity. In this work, by explicitly taking into consideration the lagged terms in the dynamics of , the noise term becomes strictly exogenous. Our proposed model and estimation procedure has the capacity of handling much stronger correlation between and , although ultimately we do require to be indirectly bounded in some appropriate way.

References

- Agarwal et al. (2012a) Agarwal, A., S. Negahban, and M. J. Wainwright (2012a). Fast global convergence rates of gradient methods for high-dimensional statistical recovery. The Annals of Statistics 40(5), 2452–2482.

- Agarwal et al. (2012b) Agarwal, A., S. Negahban, and M. J. Wainwright (2012b). Noisy matrix decomposition via convex relaxation: Optimal rates in high dimensions. The Annals of Statistics 40(2), 1171–1197.

- Anderson and Vahid (2007) Anderson, H. M. and F. Vahid (2007). Forecasting the volatility of Australian stock returns: Do common factors help? Journal of Business & Economic Statistics 25(1), 76–90.

- Anderson (2003) Anderson, T. W. (2003). An Introduction to Multivariate Statistical Analysis, Volume 355. John Wiley & Sons.

- Ando and Bai (2015) Ando, T. and J. Bai (2015). Selecting the regularization parameters in high-dimensional panel data models: Consistency and efficiency. Econometric Review, 1–29.

- Ashcraft et al. (2010) Ashcraft, A., P. Goldsmith-Pinkham, and J. Vickery (2010). MBS Ratings and the Mortgage Credit Boom. https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr449.pdf.

- Avellaneda and Lee (2010) Avellaneda, M. and J.-H. Lee (2010). Statistical arbitrage in the US equities market. Quantitative Finance 10(7), 761–782.

- Bai (2003) Bai, J. (2003). Inferential theory for factor models of large dimensions. Econometrica 71(1), 135–171.

- Bai et al. (2016) Bai, J., K. Li, and L. Lu (2016). Estimation and inference of FAVAR models. Journal of Business & Economic Statistics 34(4), 620–641.

- Bai and Ng (2002) Bai, J. and S. Ng (2002). Determining the number of factors in approximate factor models. Econometrica 70(1), 191–221.

- Bai and Ng (2008) Bai, J. and S. Ng (2008). Large dimensional factor analysis. Foundations and Trends® in Econometrics 3(2), 89–163.

- Bai and Ng (2013) Bai, J. and S. Ng (2013). Principal components estimation and identification of static factors. Journal of Econometrics 176(1), 18–29.

- Basu and Michailidis (2015) Basu, S. and G. Michailidis (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics 43(4), 1535–1567.

- Billio et al. (2012) Billio, M., M. Getmansky, A. W. Lo, and L. Pelizzon (2012). Econometric measures of connectedness and systemic risk in the finance and insurance sectors. Journal of Financial Economics 104(3), 535–559.

- Candes and Plan (2010) Candes, E. J. and Y. Plan (2010). Matrix completion with noise. Proceedings of the IEEE 98(6), 925–936.

- Carare and Mody (2010) Carare, A. and A. Mody (2010). Spillovers of domestic shocks: Will they counteract the ”great moderation”? International Finance 15(1), 69–97.

- Chamberlain and Rothschild (1983) Chamberlain, G. and M. Rothschild (1983). Arbitrage, factor structure, and mean-variance analysis on large asset markets. Econometrica 51(5).

- Eichengreen et al. (2012) Eichengreen, B., A. Mody, M. Nedeljkovic, and L. Sarno (2012). How the subprime crisis went global: evidence from bank credit default swap spreads. Journal of International Money and Finance 31(5), 1299–1318.

- Eichengreen and O’rourke (2010) Eichengreen, B. and K. H. O’rourke (2010). A tale of two depressions: what do the new data tell us? VoxEU.org.

- Fan et al. (2012) Fan, J., Y. Li, and K. Yu (2012). Vast volatility matrix estimation using high-frequency data for portfolio selection. Journal of the American Statistical Association 107(497), 412–428.

- Fiecas et al. (2014) Fiecas, M., R. von Sachs, et al. (2014). Data-driven shrinkage of the spectral density matrix of a high-dimensional time series. Electronic Journal of Statistics 8(2), 2975–3003.

- Forni et al. (2000) Forni, M., M. Hallin, M. Lippi, and L. Reichlin (2000). The generalized dynamic-factor model: Identification and estimation. Review of Economics and statistics 82(4), 540–554.

- Forni et al. (2005) Forni, M., M. Hallin, M. Lippi, and L. Reichlin (2005). The generalized dynamic factor model: one-sided estimation and forecasting. Journal of the American Statistical Association 100(471), 830–840.

- Forni et al. (2015) Forni, M., M. Hallin, M. Lippi, and P. Zaffaroni (2015). Dynamic factor models with infinite-dimensional factor spaces: One-sided representations. Journal of econometrics 185(2), 359–371.

- Forni et al. (2017) Forni, M., M. Hallin, M. Lippi, and P. Zaffaroni (2017). Dynamic factor models with infinite-dimensional factor space: Asymptotic analysis. Journal of econometrics 199(1), 74–92.

- Greenaway-McGrevy et al. (2012) Greenaway-McGrevy, R., C. Han, and D. Sul (2012). Estimating the number of common factors in serially dependent approximate factor models. Economics Letters 116(3), 531–534.

- Lin and Michailidis (2017) Lin, J. and G. Michailidis (2017). Regularized estimation and testing for high-dimensional multi-block vector-autoregressive models. Journal of Machine Learning Research 18(117), 1–49.

- Liu and Spencer (2013) Liu, Z. and P. Spencer (2013). Modeling sovereign credit spreads with international macro-factors: The case of brazil 1998–2009. Journal of Banking & Finance 37(2), 241–256.

- Loh and Wainwright (2012) Loh, P.-L. and M. J. Wainwright (2012). High-dimensional regression with noisy and missing data: provable guarantees with nonconvexity. The Annals of Statistics 40(3), 1637–1664.

- Lütkepohl (2014) Lütkepohl, H. (2014). Structural vector autoregressive analysis in a data rich environment. Technical report, Deutsches Institut für Wirtschaftsforschung.

- Negahban and Wainwright (2012) Negahban, S. and M. J. Wainwright (2012). Restricted strong convexity and weighted matrix completion: Optimal bounds with noise. Journal of Machine Learning Research 13(May), 1665–1697.

- Negahban et al. (2012) Negahban, S., B. Yu, M. J. Wainwright, and P. K. Ravikumar (2012). A unified framework for high-dimensional analysis of -estimators with decomposable regularizers. Statistical Science 27(4), 538–557.

- Nesterov (2007) Nesterov, Y. (2007). Gradient methods for minimizing composite objective function. Technical report, Center for Operations Research and Econometrics (CORE), Catholic Univ. Louvain (UCL).

- Schich (2010) Schich, S. (2010). Insurance companies and the financial crisis. OECD Journal: Financial market trends 2009(2), 123–151.

- Stock and Watson (2002) Stock, J. H. and M. W. Watson (2002). Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association 97(460), 1167–1179.

- Stock and Watson (2005) Stock, J. H. and M. W. Watson (2005). Implications of dynamic factor models for VAR analysis. Technical report, National Bureau of Economic Research.

- Tseng (2001) Tseng, P. (2001). Convergence of a block coordinate descent method for non-differentiable minimization. Journal of Optimization Theory and Applications 109(3), 475–494.

- Wainwright (2009) Wainwright, M. J. (2009). Sharp thresholds for high-dimensional and noisy sparsity recovery using -constrained quadratic programming (lasso). IEEE Transactions on Information Theory 55(5), 2183–2202.

- Yu et al. (2015) Yu, Y., T. Wang, and R. J. Samworth (2015). A useful variant of the Davis–Kahan theorem for statisticians. Biometrika 102(2), 315–323.

Appendix A Proofs for Statistical Error Bounds.

Before presenting the proof of Theorem 1, we first define a few quantities associated with the regularizers. Given some (to be specified later), let denote the thresholded support set of , i.e., , and let the SVD of be , with and respectively denoting the first columns of and . Let , and their complements respectively be defined as follows:

and

Further, for some generic matrix , we define its projection on and (denoted by and , resp.) as

| (18) |

With the above definitions and projections, we can write

| (19) |

and note that the following inequality holds:

| (20) |

as has at most nonzero entries where . In an analogous way, for some generic matrix , its projections on and (denoted by and , resp.) are defined as

| (21) |

where is defined below and partitioned as:

Note that the following relationships hold

| (22) |

Next, we introduce concepts and lemmas regarding decomposable regularizers (Negahban et al., 2012). Define the weighted regularizer as

and let and .

Lemma A.2.

With the definition of (21), the following holds for some generic :

The proofs of these two lemmas are deferred to Supplement C. Based on the above preparatory steps, we present next the proof of Theorem 1.

Proof of Theorem 1.

We prove the bound for and under the imposed regularity conditions, where is the solution to the optimization problem (9). Using the optimality of and the feasibility of , the following basic inequality holds on:

| (23) |

The LHS can be equivalently written as

and by rearranging, (23) becomes

| (24) | ||||

Based on (24), the rest of the proof is divided into three parts: in part (i), we provide a lower bound for the LHS primarily using the RSC condition; in part (ii), we provide an upper bound for the RHS with the designated choice of and ; in part (iii), we align the two sides and obtain the error bound after some rearrangement.

Part (i).

In this part, we obtain a lower bound for the LHS of (24). Using the RSC condition for , the following lower bound holds for the LHS of (24):

| (25) |

To further lower-bound (25), consider an upper bound for with the aid of (23). By Hölder’s inequality, the following inequalities hold for the inner products:

| (26) |

and

| (27) |

By choosing and , the following inequality can be derived from the non-negativity of the RHS in (23):

where the first two terms in (1) come from (19), the next two terms come from (22) and the last three terms use Lemma A.1. After writing out and rearranging, we obtain

that is,

| (28) |

Note that for , using (20) and Lemma A.2,

| (29) |

Plug (29) into (28), and by the Cauchy-Schwartz inequality, we have

| (30) |

Combine (25) and (30), a lower bound for the LHS of (24) is given by

With the designated choice of satisfying , the above bound can be further lower bounded by

| (31) |

Part (ii).

Next, we obtain an upper bound for the RHS of (24). Using the triangle inequality and Hölder’s inequality, the first term satisfies

| (32) |

Using the fact that both and are feasible and satisfy the box constraint , the RHS of (32) is upper bounded by ; thus, by choosing , we have

With (26) and (27), by choosing and , the following upper bound holds for the RHS of (24):

| (33) |

where (1) uses (19) and (22); (2) is obtained by writing out and canceling terms; and (3) uses (29).

Part (iii).

A.1 The Error.

Theorem 1 establishes the error bound for the estimated factor hyperplane through the quantity . Here we provide an account for the error bound of the space spanned by the estimated latent factors relative to the true underlying one. To that end we derive an error bound for that measures the distance between the estimated factor space and the true factor space. In particular, we focus on analyzing the error between the leading rank- subspace spanned by and , although potentially could span an -dimensional subspace (whenever ) that depends on the value of the selected .

First we note that to examine the error of the estimated factor space is equivalent to examine the distance between and , where and are the first left singular vectors corresponding to and , respectively. Specifically, the angle between the spaces they span is defined as

| (34) |

where are singular values of . The following proposition associates the error of to that of .

Proposition 1 ( error of the estimated factor space).

Suppose the estimated factor hyperplane is obtained by solving (9), whose error is given by . Let and be the leading and the smallest nonzero singular values of . The following bound holds for the distance between the estimated and the true factor spaces:

| (35) |

The bound in (35) is obtained by considering as a -perturbation of , and the size of the perturbation is upper bounded in Frobenius norm given by given in Theorem 1. The stronger the minimum signal is for the true space (i.e., ), the tighter the error bound will be. Note that for the true space spanned by , although it is not observable, it can nevertheless be interpreted as a random (but fixed for this specific part of the analysis) realization drawn from the specified VAR model driving the dynamics of , which in turn directly influences the evolution of the observable process.

Proof of Proposition 1.

First, we note that for any given , it can be viewed as a -perturbation with respect to the true . As mentioned in the main text, as invertible linear transformations preserve the subspace, so does scaling (with a non-zero scale factor), it is equivalent to examining the distance between the first singular vectors of and (denoted by and , resp.). The rest follows seamlessly from the perturbation theory of singular vectors. Specifically, by applying Yu et al. (2015, Theorem 3) and assuming the singular values of are given by , the following bound holds for :

Note that the same bound holds for the distance between the factor spaces. ∎

Appendix B Proofs for Lemmas.

Proof of Lemma 1.

First, suppose we have

| (36) |

then, for all , and letting denote its th column, the RSC condition automatically holds since

Therefore, it suffices to verify that (36) holds. In Basu and Michailidis (2015, Proposition 4.2), the authors prove a similar result under the assumption that is a process. Here, we adopt the same proof strategy and state the result for a more general process .

Specifically, by Basu and Michailidis (2015, Proposition 2.4(a)), and ,

Applying the discretization in Basu and Michailidis (2015, Lemma F.2) and taking the union bound, define , and the following inequality holds:

With the specified , set , then apply results from Loh and Wainwright (2012, Lemma 12) with and , so that the following holds

with probability at least and note that since . Finally, let for some , and conclude that with probability at least , the inequality in (36) holds with

and so does also the RSC condition. ∎

Proof of Lemma 2.

We note that

where is the -dimensional standard basis with the th entry being 1. Applying Basu and Michailidis (2015, Proposition 2.4(b)), for an arbitrary pair of , the following inequality holds:

Take the union bound over all , and the following bound holds:

Set for and with the choice of , , then with probability at least , the following bound holds:

∎

Proof of Lemma 3.

For whose rows are iid realizations of a sub-Gaussian random vector , by Wainwright (2009, Lemma 9), the following bound holds:

where . In particular, by triangle inequality, with probability at least ,

So for , by setting , which yields so that with probability at least , the following bound holds:

∎

Appendix C Proofs of Auxiliary Lemmas.

In this section, proofs of auxiliary lemmas A.1, A.2 are provided. Variations of these Lemmas have been proved in Negahban et al. (2012) and Lin and Michailidis (2017); nevertheless, we provide them also here for the sake of completeness.

Proof of Lemma A.1.

Proof of Lemma A.2.

Let the SVD of be given by , where both and are orthogonal matrices. Assume . For , define as below and it is partitioned as:

Then by further defining

it is straightforward to see that . Moreover,

∎

Appendix D Model identifiability considerations.

In this section, we provided a detailed account of the model identifiability issue, due to the factor space being latent.

Consider the full identification of the given model . Similar to the analysis in Bai et al. (2016) for the informational series of a factor-augmented VAR model, there exist invertible matrices and such that

| (37) |

which are observationally equivalent to the original model. So for the model to be fully identifiable (including the factors), a total number of restrictions is required. If exact identification of the factors is not required, then restrictions are required to separate the space spanned by from that by . In low dimensional settings with a different model setup, an estimation procedure based on (37) that takes into consideration these restrictions can be carried out in a two step procedure involving estimation followed by rotation, with the aid of and the associated orthogonal projection operator (see Bai et al., 2016, for details). In the high-dimensional setting, however, neither auxiliary quantity is properly defined, and hence the above strategy can not be operationalized. As oppose to imposing additional model assumptions that would be stringent and only made for the sake of mathematical convenience, we incorporate these restrictions implicitly and approximately, through the assumption that the amount of interaction between the latent factor space and the lag space is controlled, which manifests itself in the technical developments as the product of the total signal present in these two spaces. In the formulated optimization problem, with properly selected tuning parameters, the global minimizer of the convex program exhibits good statistical behavior in terms of its error that does not grow with or , so that there is adequate control over the performance of the estimator, even though this upper bound of the error does not vanish asymptotically. This represents the price to be paid for handling strongly correlated idiosyncratic components in approximate factor models, under minimal identifiability restrictions.

Remark D.1 (Illustration on the additional box constraint).

In the same spirit as Agarwal et al. (2012b), to distinguish the low rank hyperplane from the lagged space from a theoretical standpoint , we restrict to be in the constrained set , where

is the dual norm of some regularizer . Note that the product measures the spikiness of w.r.t. ; in the setup of interest in this paper, it corresponds to the -norm regularizer associated with the sparse component; hence and . This constrained set leads to the box constraint given in (9).

Remark D.2.

For approximate factor models, a large panel size (large ) is helpful, since the estimated factors are obtained through cross-sectional aggregation. In particular, as discussed in Chamberlain and Rothschild (1983) and subsequent work, by assuming that the leading eigenvalues of diverge, whereas all eigenvalues of are bounded, separation between the common factors and the idiosyncratic components is achieved as the panel size goes to infinity. On the other hand, the Stock-Watson formulation (Stock and Watson, 2002) adopted in our work which accounts explicitly for strong correlations amongst the coordinates of the idiosyncratic component, leads to a high-dimensional sparse regression modeling framework. Hence, the estimates for the time-lags of the process suffer from the curse of dimensionality, if we do not compensate appropriately by an increase in the sample size. Hence, we need to strike a balance between these two competing forces. Specifically, when updating the estimate of the factor hyperplane by aggregating cross-sectional information and compress it to a subspace with reduced dimension through the SVD, a larger panel is helpful. On the other hand, when updating the estimate of the sparse transition matrix, a very high is detrimental, unless appropriately compensated by a larger sample size . In addition, the temporal dependence of the coordinates of the process along with the presence of the latent factors add further complications. Thus, careful balancing of these competing issues is needed to obtain estimates of the model parameters with adequate error control.

SUPPLEMENTARY MATERIAL

- Supplement to -lag dependence.

-

Generalization to dependence.

Appendix E Generalization to Dependence.

The proposed modeling framework and estimation procedure are easily generalizable to cases where the idiosyncratic error exhibits further into the past temporal dependence, and come with similar theoretical guarantees. Specifically, we use a sparse model to account for such dependency, that is,

with ’s assumed sparse. By stacking the lagged values of the factors and the corresponding loading matrices, the dynamic of the observable process can be written in the following form, in terms of the latent static factor :

| (38) |

Similar to the case, the condition required for stationarity is the same as cases where were a process, that is, all roots of should lie outside the unit circle: for all . Note that with the model specification in (38), the spectral density of takes the following form:

Estimation and theoretical guarantees.

Given a snapshot of the realizations from , denoted by , we can estimate and the factor hyperplane in an analogous way. Specifically, let the contemporaneous response and the lagged predictor matrices be and by stacking the observations in their rows with being the sample size. is similarly defined to . Further, letting , then with and identically defined to those in Section 2.1, we can write

and can be obtained by solving an analogously formulated optimization, that is

| (39) | ||||

Empirically at each iteration, is updated by SVT with hard-thresholding and each row of is updated via Lasso regression.

With deterministic realizations based on which we solve the optimization problem, we can obtain essentially the same error bound, with the conditions imposed on the corresponding augmented quantities. Formally, the error bound is given in the next corollary, with a superscript associated with the true value of the parameters, being analogously defined as the cardinality of the thresholded support set , and being the sample covariance matrix corresponding to .

Corollary 2 (Error bound under dependence).

Suppose the observations stacked in are deterministic realizations from process with dynamic given in (38), and satisfies the RSC condition with curvature and a tolerance such that . Then for any matrix pair that drives the dynamic of , for estimators obtained by solving (39) with and chosen such that

the following error bound holds for some constants and , with :

| (40) |