Optimal reinsurance for risk over surplus ratios

Abstract

Optimal reinsurance when Value at Risk and expected

surplus is balanced through their ratio is studied, and it is demonstrated

how results for

risk-adjusted surplus can be utilized. Simplifications for large

portfolios are derived, and this large-portfolio study suggests a new condition

on the reinsurance pricing regime which is crucial for the results

obtained.

One or two layer contracts now become optimal

for both risk-adjusted surplus and the risk over expected surplus ratio, but

there is no second layer when portfolios are large or when

reinsurance

prices are below some threshold.

Simple

approximations of the optimum portfolio is considered, and

their degree of

degradation compared to the optimum is studied which leads to

theoretical degradation rates

as the number of policies grow.

The theory is supported by numerical experiments which suggest

that the shape of the claim severity distributions may not be of primary importance

when designing an optimal reinsurance program.

It is argued that the approach

can be applied to

Conditional

Value at Risk as well.

Key words and phases

Asymptotics, degradation rates, large portfolios, one- and two-layer

contracts, reinsurance pricing regimes, risk-adjusted surplus.

1 Introduction

Actuarial literature contains

countless formulations of what optimal reinsurance should mean,

for example, Borch (1960); Arrow (1963); Kaluszka (2001) and Cheung

et al. (2014). A criterion with much sense industrially

is to balance risk and profit through a ratio where a risk measure is

divided on expected surplus. Most of the paper makes use of Value at Risk

in this role.

That is how the insurance industry is regulated at present, but we shall argue

that the perhaps theoretically more appealing Conditional Value at Risk

could be handled in the same manner which would yield similar,

but not quite identical

results; see the companion paper Wang and

Bølviken (2019).

Ratios of risk and expected surplus are related to

risk-adjusted surplus under which many authors have examined how

reinsurance could be optimized, see Chi (2012); Asimit

et al. (2013); Cheung and

Lo (2017) and Chi

et al. (2017). Of particular

significance for the present paper is

Chi

et al. (2017) who were able to show

that the

reinsurance treaties maximizing risk-adjusted surplus are of the

multi-layer type. It is not tenable

to assume that reinsurance pricing is based on a fixed loading,

as noted already

by Borch (1960), and Chi

et al. (2017) made use of

a general formulation of reinsurance pricing

that goes back to Bühlmann (1980). Many other

researchers, for

example, Chi and

Tan (2013) and Zhuang

et al. (2016) have used

this scheme.

We follow in their track except that we argue for a modification.

The world of reinsurance is above all a market with

pricing offers from reinsurers

defining a supply curve for such risk, but

the variation in time is enormous with big events

like the World Trade Center terrorism in

having huge impact.

Details are not open to

the public in any case, and academic studies must therefore employ

‘premium principles’ as proxies for the real market prices. The

question is what conditions should be imposed on them. It is demonstrated

in this paper

that the original set-up in Bühlmann (1980) would enable the insurer

to reinsurance everything up to Value at Risk and for large portfolios

still obtain profit. No net

solvency capital would then be necessary, but is it likely

that the insurance

market should allow such a situation to exist? We think not and have

derived from this viewpoint a new condition that differs from

the one in current use.

All our results

depend on it. One of the consequences is that the multi-layer solution

for risk-adjusted surplus

in Chi

et al. (2017) is reduced to one or two layers with more than one

layer only when risk is expensive, and this result is a stepping stone

to similar results for the risk over surplus ratio.

One issue that does not seem to have been treated

in actuarial literature is what happens

when the portfolio size become infinite.

This is highly relevant for reinsurance of single risks

since many of them are sums of a large number of policies.

Such asymptotic studies have in

statistics or other branches of applied mathematics often

lead to simplification and clarity as indeed they do here.

We have limited ourselves to independent risks so that we can

lean on the central limit theorem

and its Lindeberg extension, but the approach can without doubt be extended

to dependent risks influenced by some common random factor; more on that

in the concluding section.

A part of all asymptotic studies is how well such approximations

perform for finite portfolio sizes. This is not in our case a question of error,

but rather one of degradation of the criterion in terms of how much

it changes compared to its value at the strict optimum.

Theoretical degradation studies are developed

in Section 4 through large portfolio analysis

which leads to approximate rates of decay as the number of policies grows.

The numerical side is examined in Section 5

though simulation studies and illustrates how large portfolios must

be for the large-portfolio approximations to perform well.

2 Basics and preliminaries

2.1 Notation and formulation

Let be the total claim losses of a single portfolio of non-life insurance policies over a certain period of time (often one year) and let be the net risk retained after having received from a reinsurer so that . Natural restrictions on are

| (2.1) |

where the first condition is obvious since the reinsurer will never pay out more than the original claim. The second condition is known as the slow growth property, and it opens for moral hazard if it isn’t satisfied; consult Cheung et al. (2014). Contracts satisfying (2.1) will be referred to as feasible.

Let be the distribution function of which starts at the origin. Risk measures that has attracted much interest are Value at Risk and Conditional Value at Risk with formal mathematical definitions

| (2.2) |

where is a given level. When these quantities apply to the retained risk we shall be using notation like . The right inequality in (2.1) implies that the retained risk is non-decreasing in so that if , then

| (2.3) |

Premia involved are collected by the cedent from its customers and for the reinsurance. Those are in their simplest form

| (2.4) |

with and given loadings (or coefficients) and with in practice. The reinsurance part is inadequate. Prices in that market is likely to increase with risk beyond the fixed coefficient in (2.4) right. In real life that would be captured by offers the cedent company receives from reinsurers, but such information isn’t available and for academic work we must instead supply a so-called premium principle which is dealt with in Section 2.3.

2.2 Expected surplus

We need a mathematical expression for the expected surplus for an insurer under a given reinsurance treaty. Into the account goes the premium collected from clients and out of it their net claims and the reinsurer premium . If the cost of holding solvency capital is subtracted too, a simplified summary of the balance sheet becomes

| (2.5) |

with the notation highlighting the dependence on the reinsurance function . The coefficient applies per money unit. It seems industrially plausible to attach cost to the entire solvency capital, not only to the part above the average, as in Chi et al. (2017). Alternatively such cost might be in terms of the Conditional Value at Risk with CVaRϵ replacing VaRϵ on the right in (2.5). Let and take expectations in (2.5). Inserting (2.3) and (2.4) left yield

| (2.6) |

with the last two terms depending on the reinsurance contract.

2.3 Reinsurance pricing

A standard formulation, used for example in Chi et al. (2017), is to introduce a market factor so that

| (2.7) |

where is a positive random variable correlated with and some function for which an exponential one will be used with the examples in Section 3.2. General models for is constructed through copulas. With the distribution function of let

| (2.8) |

with and the percentile functions of and and with a dependent pair of uniform variables. This yields an alternative expression for . By the rule of double expectation

with the last identity due to being fixed by . Hence

| (2.9) |

The impact of the dependency between to is taken care of by

where the distribution

function of doesn’t enter, and this will prove convenient

when depends on the underlying portfolio size in Section 4.

It is often assumed that ,

but that is hardly an obvious assumption.

It is being violated

when as in (2.4) right, and there is

in the present work no point in restricting the set-up so strongly, more

on that later. Note in passing

that if is a non-decreasing

function of , as

is plausible and assumed below, then

since and by (2.9) right. Hence

a non-decreasing guarantees

the reinsurance premium to be larger than the expected reinsurance

pay-out if

.

Much more general formulations of premium principles

can be found in Furman and

Zitikis (2009).

The price on reinsurance can also be expressed through the function

| (2.10) |

which is sketched in Figure 2.1 below. Consider the reinsurer expected surplus which by (2.9) left is

or since the derivative ,

But if if and otherwise. then

so that

after changing the order of integration. Since as , it follows that

| (2.11) |

2.4 Conditions on reinsurance pricing

The function will play a key role, and it is possible to extract

some useful properties of it if some restrictions are imposed on the

reinsurance pricing regime, notably:

Condition 1.

(i) is non-decreasing and (ii) .

The first assumption assumes a positive type of dependence

between the market factor and the risk , surely reasonable.

A sufficient condition for that is

being non-decreasing in and the model

for

in (2.8) based on a positive dependent copula for

in the sense that Pr is increasing in

for all . Most copulas satisfy this, and it

is under these circumstances a trivial matter to verify that

is monotone upwards.

The second assumption which will be needed

for the large-portfolio study in Section 4,

may seem less obvious since

many authors assume . This

condition goes

back to Bühlmann (1980) who derived it through

an economic equilibrium argument. Section 4.2 will present

alternative reasoning with some resemblance to arbitrage

which leads to Assumption (ii).

From (2.10)

and the assumption is the same as

| (2.12) |

which is the version that will be cited below.

To see what it mean suppose

there is a fixed loading in the reinsurance market

so that

. Then

,

and Assumption (ii) implies

with the loading

in the reinsurance market the larger one.

Some useful deductions on the form of the function

can be drawn under Condition 1:

Lemma 2.1.

Suppose Condition 1 is true. Then everywhere, and there is a unique real number between and so that

| (2.13) |

where is the derivative.

Proof.

Note that so that either is decreasing everywhere or, as in Figure 2.1, there is an between and so that which means that decreases to the left and increases to the right of . There is in either case a unique as in (2.13) with the derivative of negative at that point. That is immediate when since the integrand in (2.10) is positive (or zero) everywhere whereas we also have

which is when since the integrand now is negative. ∎

The function has been plotted in Figure 2.1 when it has a maximum. Its values at where it crosses the -line and its value at the Value at Risk level will in Section 4 play a main role in defining optimal or nearly optimal reinsurance for large portfolios with the and percentiles of the underlying risk variable being the lower and upper limit of one-layer contracts. It could happen that the -line crossing in Figure 2.1 takes place to the right of . If so, the upper and lower limits coincide, and reinsurance is so expensive that it is optimal for the insurer to carry all risk himself. It will be of some importance that , and in practice this inequality is sharp which is taken for granted in Proposition 4.2 below.

3 Optimization

3.1 Risk-adjusted surplus

Many contributors to reinsurance optimum theory work with Lagrangian set-ups of the form

| (3.1) |

with a risk measure and

a price on risk;

see Balbás

et al. (2009); Tan

et al. (2011); Jiang

et al. (2017) and Weng and

Zhuang (2017). This

risk-adjusted, expected surplus of the insurer is then maximized,

and as varies the solutions

define

an efficient frontier tracing out the minimum

obtainable for a given value of

. These solutions are

needed when the risk over surplus ratio is studied in Section 3.3.

Proposition 3.1.

Proof.

It isn’t assumed that as in Chi et al. (2017), but their ingenious argument still works. Insert (2.6) and into (3.1). This yields

which can be combined with (2.11) for the next to last term on the right and also

for the last one. Hence

| (3.3) |

with as in (3.2) right. The restrictions in (2.1) means that so that is maximized by selecting whenever and otherwise, and this yields in (3.2) as the optimum. ∎

The proposition shows that the optimum is of the multi-layer type. Let

| (3.4) |

where

is a vector of coefficients

for which . This is a single-layer contract

which is the solution in Proposition 3.1

when between and and elsewhere.

The general solution

depends on how many times in (3.2)

crosses zero. If there are

three or four crossings there is an additional layer

with , and the optimum is now

. In theory we may continue

to five or six crossings and a third layer and so on,

but arguably there are in practice at most two:

Corollary 3.1.

Degenerate situations are covered by this, for example leading to no reinsurance at all or with the reinsurer covering everything up to . The (perhaps surprising) -layer starting at occurs when is large enough; i.e. when the cost attached weights heavily enough compared to the expected gain .

Proof.

Note that if , then so that there is under no circumstances reinsurance above . On the other hand and starts below or at if . Since the derivative , Assumption (i) tells us that either decreases everywhere or start to increase and then decrease. In either case crosses zero from negative to positive at a single point or not at all. If there will be a layer starting at zero and a second one if there are two crossings below . ∎

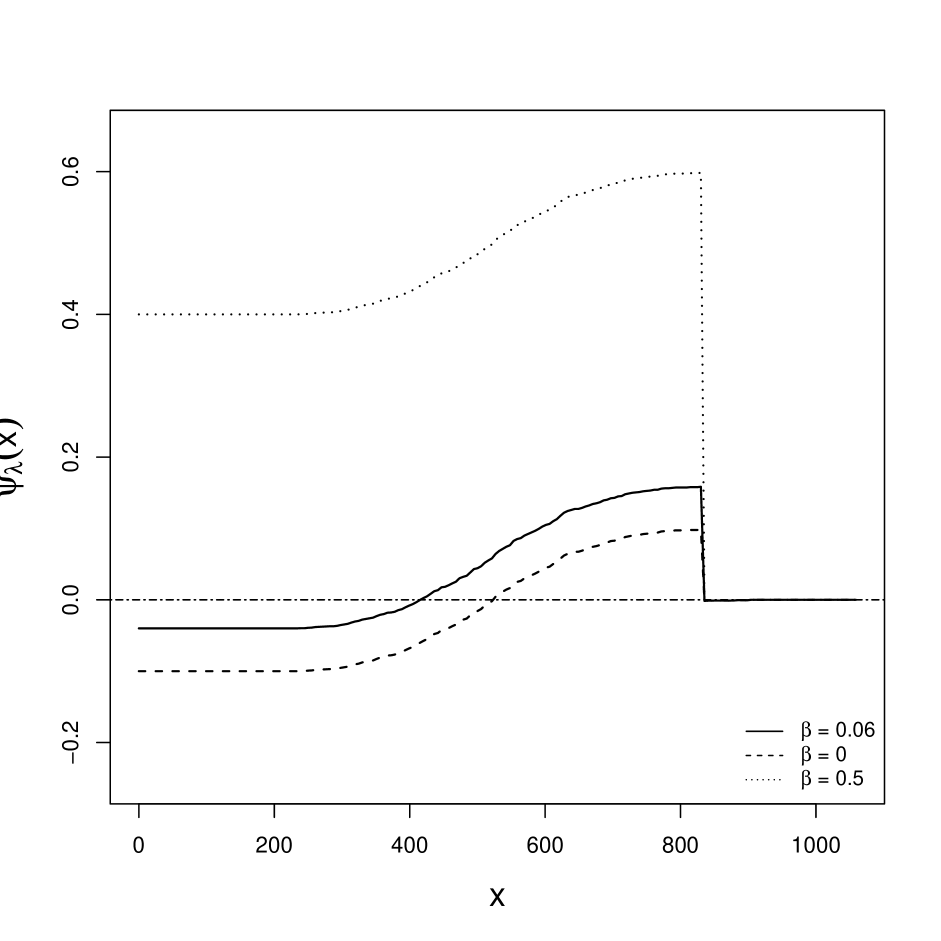

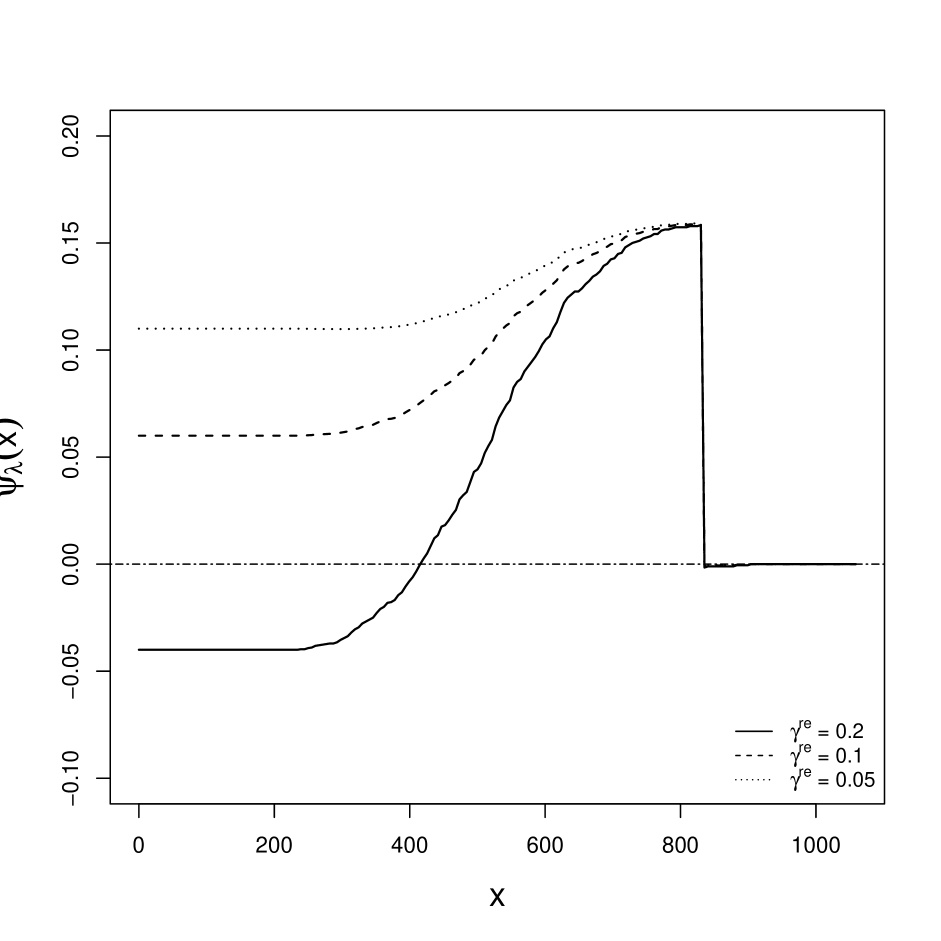

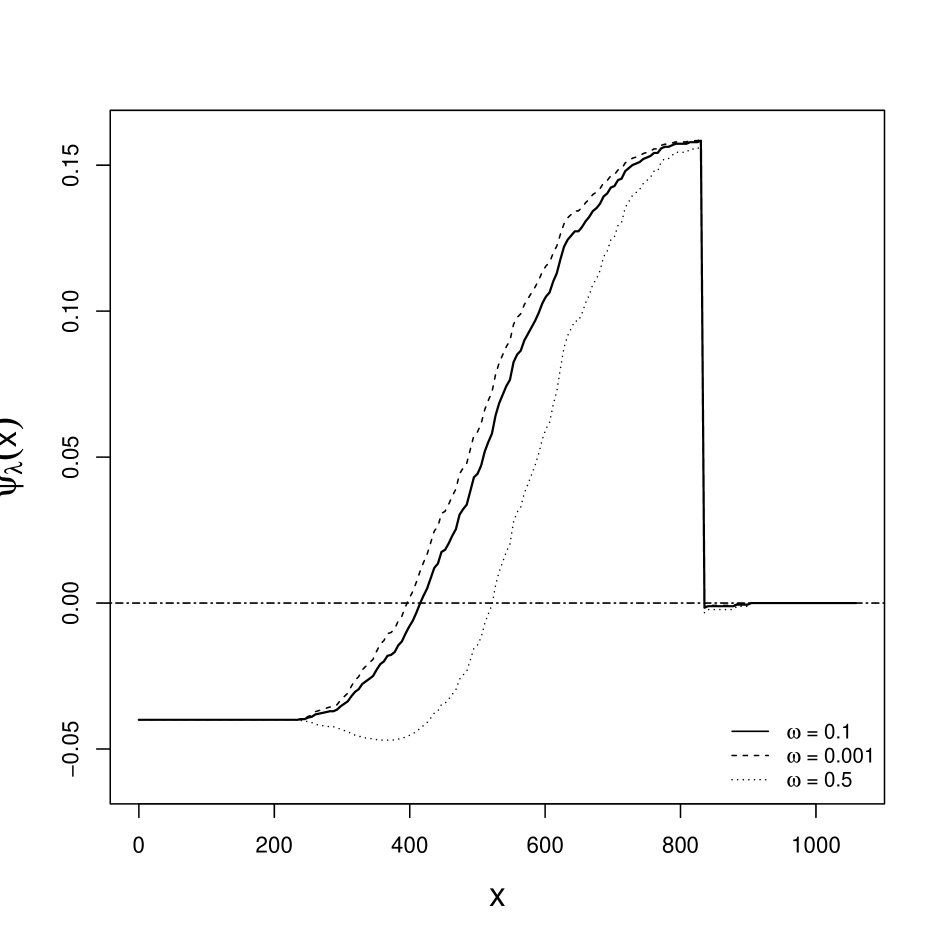

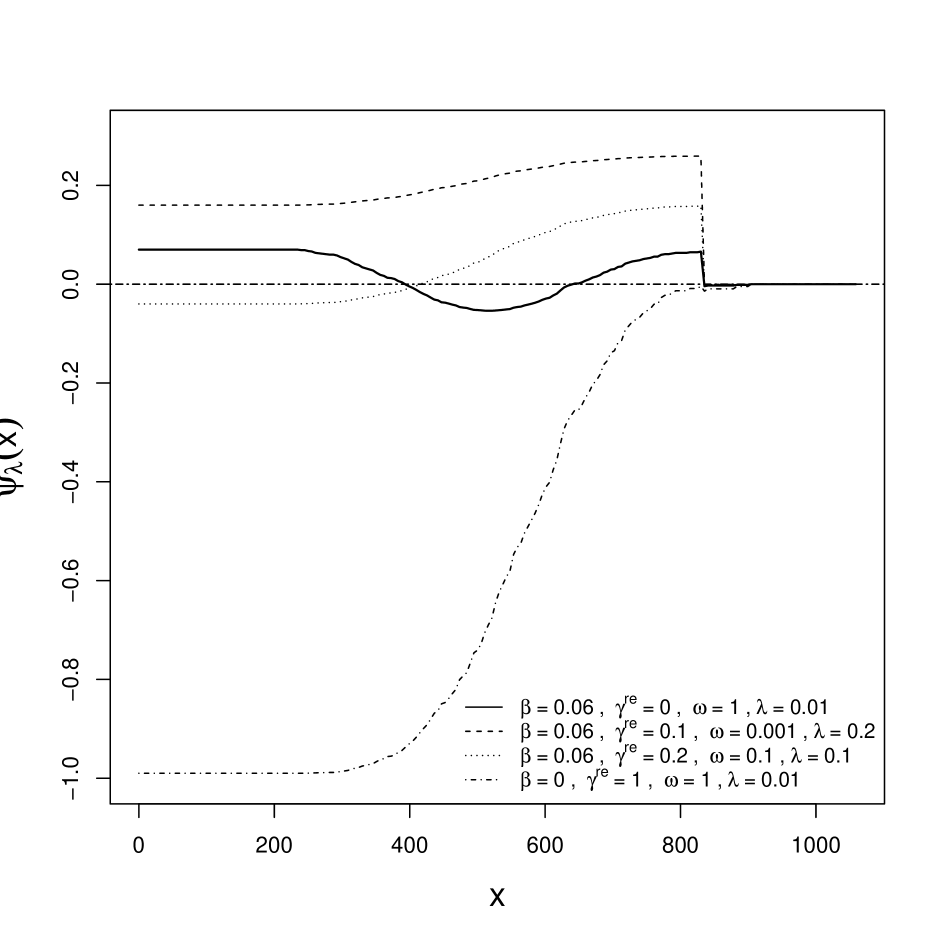

3.2 Numerical illustration

How in (3.2) varies with is shown in Figure 3.1 under different combinations of risk parameters. Detailed conditions and assumptions are recorded in Appendix B along with the simulation algorithm used. The portfolio is Poisson/Gamma with claims expected annually and with individual losses on average with standard deviation which allows for huge losses. The model for is based on the Clayton Copula (consult Appendix B) with a Gamma distribution for with mean and standard deviation . The market factor is

with and parameters that are varied. Note that , and the Bühlman condition corresponds to .

The default set of parameters in Figure 3.1 is , and the cost of capital is varied (top left), the price on risk (top right), (bottom left) whereas finally (bottom right) is shown for several parameter combinations. The optimum is in all but one case a one-layer solution ending at the percentile ( from some lower limit up to ) or reinsurance everywhere for ) or no reinsurance at all ( everywhere). The exception is the parameter combination with so that . Now , and there is a -layer in the beginning and then an -layer ending at .

3.3 Risk over expected gain

Another criterion and the main focus in this paper is the ratio of risk over expected surplus; i.e.

| (3.5) |

We search among insurance functions for which , and is to be minimized among such contracts. Inserting (2.3), (2.6) and (2.11) yields the more explicit form

| (3.6) |

where it is part of the optimization problem to keep the denominator positive.

Though not used much

in academic literature the criterion reflect

industrial thinking very well as a tool to

minimize risk per money unit expected gain. Its optimal solutions are

still located

on an efficient frontier of the Markowitz type

and belong to the same class as those maximizing risk-adjusted surplus as the

following

consequence of Proposition 3.1 shows:

Proposition 3.2.

Suppose Assumption (i) in Condition 1 is true. Then there exists for any feasible reinsurance function for which a one or two layer function so that , and .

Proof.

Let if and if . Value at Risk is then the same under both and whereas

since the contribution above is cut off on the right and . It follows from (3.6) that

The idea now is to construct a reinsurance function satisfying (3.2) for some so that . Then by Corollary 3.1 for some pair of coefficients and , and since this contract maximizes risk-adjusted surplus

denoting Value at Risk by and . Hence which implies

which was to be proved. To construct let , and note that implies for all so that Proposition 3.1 implies that the optimal reinsurance function when is cost of risk is everywhere. On the other hand if is large enough, for and the optimum contract now is for and for . The construction ensures that

since . It follows that . But if we allow to grow from to there will on continuity be a in between so that which completes the proof. ∎

4 Large portfolio asymptotics

4.1 Introduction

The search for an optimum reinsurance function was above reduced to the class

of two-layer ones with and ,

and the

aim now is to simplify further when portfolios are large. Suppose

with individual risks and

large.

It might be possible

to cover situations where

are dependent through some common random factor, but

that will not be done, and it is assumed that

are independent though not

identically distributed.

The distribution

function of then becomes Gaussian as

by the central limit theorem and its Lindeberg

extension which is almost always satisfied. We shall from now on

write to emphasize the importance of

, similarly for the

percentile,

,

and

and even and for the coefficients.

The detailed

mathematical calculations are relegated to Appendix A, but the

crux of the approach is

the centered and normalized variable

| (4.1) |

with average mean and average variance of the individual risks . For the ensuing argument it doesn’t matter that in reality and depend on as long as they converge to fixed values and as . This minor complication is ignored. The distribution function of with percentiles starts at (zero below), and we have the elementary relationships

| (4.2) |

The reason for introducing is that and as where and are distribution function and percentile for the standard normal. It is convenient to work with similar versions for the coefficients; i.e.

| (4.3) |

and when is the optimal upper cut-off point. Similar normalized coefficients and are introduced from and below.

4.2 A key condition

Consider the one-layer contract with limits and . The expected reinsurer surplus (2.11) is

or after changing the integration variable to in the last integral

| (4.4) |

Note that so that Value at Risk is which after inserting for and becomes

| (4.5) |

By (2.6)

and after inserting , (4.4) and (4.5).

| (4.6) |

which will be later needed to prove Proposition 4.1 below.

Suppose with still.

The reinsurer then takes all risk up to the

percentile so that Value at Risk for

the insurer is zero.

In (4.6) ,

and when this is inserted, vanishes (as it should) and

or

| (4.7) |

The limit follows from Lemma A.2 in Appendix A and

is also a simple consequence of l’Hpital’s rule if

so that

the integral in (4.7) becomes infinte as .

Surely this

suggests ?

Otherwise the insurer by expanding the portfolio and reinsuring everything up

to Value at Risk can earn money without having to put up any solvency

capital at all. This isn’t quite arbitrage since risk

above Value at Risk still rests with the insurer, but it is

for large portfolios

rather close to it. It seems

unlikely that the market should allow reinsurance risk to be priced

so cheaply that , and

becomes a fair assumption.

The formal condition in (2.12) excludes the

case .

Now Value at Risk is for large portfolios

when the insurer

reinsures everything below

so that its

ratio over expected surplus

is too (and hence minimized). For large portfolios

the situation has

become trivial and uninteresting and need not be considered.

4.3 Optima for large portfolios

It was shown above that is the upper cut-off point for the optimal reinsurance function, and it will now turn out that for large portfolios the percentile is the lower one where was defined in Lemma 2.1; consult, in particular (2.13) from which it follows that depends on the reinsurance pricing regime, but on not the actual distribution of risks. Define

| (4.8) |

and let .

Throughout this section

will represent different approximations to the

true optimum.

For the corresponding one-layer

reinsurance function under (4.8)

there is the following result:

Proposition 4.1.

In one word can’t in the limit exceed for any other feasible reinsurance function . The result provides a simple recipe for optimum reinsurance when portfolios are large with the second layer not included at all. Note that it could happen that so that in (4.8) which implies , and the optimum for the insurer is now to carry all risk. This happens when reinsurance is expensive. The extra assumption is always satisfied in practice; surely no insurer would operate if the loading in the primary insurance market didn’t exceed the cost per money unit of keeping solvency capital. The proposition is proved in Appendix A.

4.4 Degradation asymptotics

The one-layer reinsurance function with the two percentiles in (4.8) as limits is optimal as , but how much is the solution degraded for finite ? It may be measured against the true optimum based on the coefficients that minimizes . Note that this is the relevant comparison since there is by Proposition 4.1 no second layer when is large enough. The degree of degradation in is therefore

| (4.9) |

which is non-negative and

by Proposition 4.1

as . The following result provides

the rate:

Proposition 4.2.

Note that since by Lemma 2.1, and the

first term on the right in (4.10) is positive as it should.

Consult Appendix A.2 for the proof.

Simple, accurate calculation

of the coefficients in (4.8) is available through Monte Carlo.

If is an ordered sample of simulations of

take

and

where and

. But

what happens if Gaussian percentiles are used instead

so that no Monte Carlo is needed at all? Now

instead of (4.8)

| (4.12) |

Had the risk been strictly Gaussian,

Proposition 4.2 would still apply, but in practice

this is only an approximation, and we must suspect a lower degradation rate.

The following proposition is proved in Appendix A.3:

Proposition 4.3.

Note that Lemma 2.1 established that so .

The main contribution to the degradation is thus caused by the discrepancy at the upper percentile which may be approximated by the Cornish-Fischer correction

| (4.14) |

consult (for example) Section 2.5 in Hall (1992). The coefficient is the average skewness of the individual risk variables underlying the portfolio sum , and the usual situation is ; consult Chapter 10 in Bølviken (2014), for an expression for . Then as assumed in Proposition 4.3, and the degradation now becomes

| (4.15) |

Asymptotic results can also be derived when

which is so rare that it has little practical interest.

Proposition 4.3 indicates that the accuracy is enhanced when

a better approximation of than

is used.

Suppose

in a manner

resembling the Normal

Power method of reserving in property insurance (4.12)

right is replaced by

| (4.16) |

with the Cornish-Fisher correction term added. The error in the approximation

of is then of order , and it follows from

Proposition 4.3 that

the degradation now is of order .

These results also tell something about the impact of

model error.

The Poisson distribution, supported by the Poisson point process,

is often a reasonable choice for claim numbers, but there is

rarely much theory

behind the choice of a typical two-parameter family for claim size.

Suppose two such families are calibrated so that mean and standard

deviation match.

The same Gaussian distribution appears in the limit as

in either case, and the discrepancies

in the optimum value of the criterion are thus of order

and not very large for of some size.

5 Numerical study

5.1 Example and conditions

The Monte Carlo study presented is this section is based on the market factor independent of so that in (2.9) right which yields in (2.10)

and the -percentile

in Lemma 2.1

which is the solution of , becomes

.

Numerical values were and

so that which means that the

large-portfolio approximations of the optimal reinsurance function

use the percentile of as lower limit.

The other percentile was . Cost of capital was taken as

.

The claim number was Poisson distributed with claim frequency

per policy , and the portfolio

size varied between

and policies

representing small, medium and large portfolios

corresponding to and expected incidents. As model for the

individual losses we have taken three classic

distributions with strong skewness to the right; i.e

Gamma, log-normal and Pareto.

The probability density functions for Gamma and Pareto were

respectively

for whereas for the log-normal was normal with mean and variance . This way of parameterizing means that is mean loss per event in all three cases whereas determines variation. The models were calibrated so that and sd which mean that (Gamma), (log-normal) and (Pareto) with strong skewness in all three cases, respectively (Gamma), (log-normal) and (Pareto). The extreme right tail is heaviest for the Pareto distribution despite its skewness being lower than for the log-normal.

5.2 Results

The optimum Value at Risk over expected surplus had to be optimized numerically as a benchmark against which the approximations could be evaluated. Recall that the upper limit should be the percentile so the optimization was a simple one-dimensional one to find the lower limit. Monte Carlo was needed to compute the criterion. The number of simulations was , more than enough to keep Monte Carlo error at a comfortably low level.

| Model | |||||

|---|---|---|---|---|---|

| Gamma | 21.52 | ||||

| 12.46 | |||||

| 10.68 | |||||

| 10.21 | |||||

| Lognormal | 20.33 | ||||

| 12.39 | |||||

| 10.68 | |||||

| 10.21 | |||||

| Pareto | 20.30 | ||||

| 12.37 | |||||

| 10.67 | |||||

| 10.21 |

Main results are summarized in Table 5.1 for different values of the expected number of incidents and the three different loss distributions. All the three approximations (4.8), (4.12) and (4.16) have been evaluated and are recorded as , , , and these values in Columns must be judged against the optimum of the Value at Risk over surplus ratio in Column . What counts is the ratios. First note that the criterion itself is strongly dependent on portfolio size with much higher risk over surplus when the expected number of incidents are small. The approximations when are useless, but that changes for larger portfolios with the loss in Column and around when , when and perhaps when . The normal approximation in Column 5 is inferior to the two others as the results in Section 4.3 suggested. Decay rates as grows match the theoretical ones and are around for the Gaussian approximation in Column and around for the two others with the latter remarkably similar. Discrepancies between the three loss distributions are minor. Since they were calibrated so that mean and standard deviation are equal, the experiment testifies to the lack of importance of the shape of the distributions beyond the first two moments.

6 Concluding remarks

A large-portfolio approach has been introduced which leads

to

a modification for the

market factor in

the Bühlman

pricing regime for reinsurance.

Instead of imposing the usual we have assumed

where is the loading

in the primary market of the insurer. If this condition fails to hold,

insurers can in large portfolios

earn money with no net

solvency capital being needed, arguably

an unlikely state of affairs.

It was this new condition that

reduced the

optimum contracts for the Value at Risk adjusted surplus

in Chi

et al. (2017)

to one or two-layer ones, and that

applied to the Value at Risk over expected surplus

ratio as well. There was only one layer when the price on risk

is below a threshold. If prices in the reinsurance

market is of the expected premium principle type with loading

, the condition boils down to

with the cost of

solvency capital. Our judgment is that this condition

might often be satisfied, but against that view

there is the fact that the

prices in the reinsurance market

are distinctly volatile and nor do they have so simple a structure

as a fixed loading.

It has for large portfolios been shown that

one-layer contracts are close to optimum in any case, and

that the world of optimum reinsurance is under these circumstances

an orderly one.

The end points of the best layer is now defined as fixed percentiles

of the underlying risk variable

with the lower one determined by reinsurance prices. How far this

solution is from the true optimum was investigated theoretically

through large-portfolio studies that lead to degradation rates of order

when Monte Carlo approximations of the

exact percentiles are used and

for Gaussian ones with the number of policies.

There is even a Normal Power modification of the latter that achieves

too.

These results

were supported by numerical experiments in Section 5

which suggested considerable robustness

with respect to the shape of the underlying

claim severity distribution. The important thing for optimal

reinsurance seems to be to

get mean and variance right.

The studies in this paper can be extended along two lines. We conjecture

that similar results are obtained when Value at Risk is replaced by Conditional

Value at Risk. The main difference will be that the fixed percentile

for the upper limit will be replaced by larger one. Then there

is the condition of independent risks. They are in many situations

some common random factor influencing all of them, for example

a random claim frequency.

Now the central limit

theorem on which the present paper is based no longer holds. Portfolio losses

still have a limit

distribution, but it is very different from the one in Section 4.

It would be of

practical interest to develop theory in this situation and investigate

how optimal reinsurance is influenced.

References

- Arrow (1963) Arrow, K. J. (1963). Uncertainty and the welfare economics of medical care. The American economic review 53(5), 941–973.

- Asimit et al. (2013) Asimit, A. V., A. M. Badescu, and A. Tsanakas (2013). Optimal risk transfers in insurance groups. European Actuarial Journal 3(1), 159–190.

- Balbás et al. (2009) Balbás, A., B. Balbás, and A. Heras (2009). Optimal reinsurance with general risk measures. Insurance: Mathematics and Economics 44(3), 374–384.

- Bølviken (2014) Bølviken, E. (2014). Computation and Modelling in Insurance and Finance. International Series on Actuarial Science. Cambridge University Press.

- Borch (1960) Borch, K. (1960). An Attempt to Determine the Optimum Amount of Stop Loss Reinsurance. Norges Handelshøyskoles særtrykk-serie. Nr. 35. Uden forlag.

- Bühlmann (1980) Bühlmann, H. (1980). An economic premium principle. ASTIN Bulletin: The Journal of the IAA 11(1), 52–60.

- Cheung et al. (2014) Cheung, K., K. Sung, S. Yam, and S. Yung (2014). Optimal reinsurance under general law-invariant risk measures. Scandinavian Actuarial Journal 2014(1), 72–91.

- Cheung and Lo (2017) Cheung, K. C. and A. Lo (2017). Characterizations of optimal reinsurance treaties: a cost-benefit approach. Scandinavian Actuarial Journal 2017(1), 1–28.

- Chi (2012) Chi, Y. (2012). Reinsurance arrangements minimizing the risk-adjusted value of an insurer’s liability. ASTIN Bulletin: The Journal of the IAA 42(2), 529–557.

- Chi et al. (2017) Chi, Y., X. S. Lin, and K. S. Tan (2017). Optimal reinsurance under the risk-adjusted value of an insurer’s liability and an economic reinsurance premium principle. North American Actuarial Journal 21(3), 417–432.

- Chi and Tan (2013) Chi, Y. and K. S. Tan (2013). Optimal reinsurance with general premium principles. Insurance: Mathematics and Economics 52(2), 180–189.

- Furman and Zitikis (2009) Furman, E. and R. Zitikis (2009). Weighted pricing functionals with applications to insurance. North American Actuarial Journal 13(4), 483–496.

- Hall (1992) Hall, P. (1992). The bootstrap and edgeworth expansion. Springer.

- Jiang et al. (2017) Jiang, W., H. Hong, and J. Ren (2017, dec). On pareto-optimal reinsurance with constraints under distortion risk measures. European Actuarial Journal 8(1), 215–243.

- Kaluszka (2001) Kaluszka, M. (2001). Optimal reinsurance under mean-variance premium principles. Insurance: Mathematics and Economics 28(1), 61–67.

- Tan et al. (2011) Tan, K. S., C. Weng, and Y. Zhang (2011). Optimality of general reinsurance contracts under cte risk measure. Insurance: Mathematics and Economics 49(2), 175–187.

- Wang and Bølviken (2019) Wang, Y. and E. Bølviken (2019). How much is optimal reinsurance degraded by error? working paper.

- Weng and Zhuang (2017) Weng, C. and S. C. Zhuang (2017). Cdf formulation for solving an optimal reinsurance problem. Scandinavian Actuarial Journal 2017(5), 395–418.

- Zhuang et al. (2016) Zhuang, S. C., C. Weng, K. S. Tan, and H. Assa (2016). Marginal indemnification function formulation for optimal reinsurance. Insurance: Mathematics and Economics 67, 65–76.

Appendix A Proofs of asymptotics

A.1 Proposition 4.1

The following inequality is needed:

Lemma A.1.

If and are as in Section 2, and is a distribution function, then for all , and

| (A.1) |

Proof.

Lemma A.2.

If and is the distribution function of the normalized risk variable , then

| (A.2) |

Proof.

The next lemma shows that one-layer contracts

are better than two-layer ones when

portfolios are large:

Lemma A.3.

There exits for any some so that if Condition 1 is true,

| (A.3) |

where the sup is over all sequences of coefficients and so that .

Proof.

Consider the reinsurance function with coefficients as in the lemma for which . Hence Value at Risk becomes

after passing to the normalized coefficients. For the expected surplus of we need the expected net reinsurance surplus which from (2.11) is

or after substituting in the integral

so that the expected surplus for the insurer becomes

| (A.4) |

and

| (A.5) |

Elementary differentiation yields

with

After some straightforward calculations

where

Whether goes up or down with is determined by this function which can be examined through

| (A.6) |

where since

| (A.7) |

| (A.8) |

By Lemma A.1 with , and

where is over . Since , and the integral on the right are bounded, . To deal with the other quantity note that

Moreover, from (2.10)

which becomes after changing the order of integration

so that

But it follows from this that

| (A.9) |

where

We have to show that the right hand side of (A.9) as uniformly in when . Let and note that and recall that when . It follows that there exists a so that if , then when and under this condition

In the opposite case when the interval is bounded as , and in the denominator in (A.9) implies that uniformly in this interval too so that where the sup is over . Finally from (A.6)

where the sup is over all and for which . But since , this uniform bound establishes for sufficiently large that for all and which in turn implies that for such is an increasing function of for all so that the optimum is to remove the -layer completely. ∎

We need still another lemma which utilizes that

uniformly in as where is the standard

Gaussian distribution

function; consult Hall (1992) (for example) for this result.

Lemma A.4.

Let be the percentile of which satisfies and let be a sequence so that as . Then .

Proof.

Under Condition 1 there is a unique between and so that which implies that so that . But since uniformly this cannot occur unless . ∎

Finalizing the argument

Proposition 3.2 established that the

search for the optimal

reinsurance function can be carried out within the two-layer class

with

and , and for large portfolios Lemma A.3

further reduced the candidates

to the one-layer sub-class with .

The coefficient with its normalized version

is then the only remaining unknown to optimize over,

and

it is convenient to simplify notation so that

and (the same convention is used

everywhere below).

Value at Risk is now simply

so that the risk over surplus ratio becomes

where after removing the -layer in (A.4)

| (A.10) |

Differentiation yields

or after some straightforward calculations

where

| (A.11) |

Hence

| (A.12) |

By Lemma A.1, with ,

and

with the sup taken over all

.

Let be the

value minimizing

which from (A.12)

must satisfy that

and since uniformly in , it follows that . But , and by Lemma A.4 this can not occur unless . Hence so that as well, and there exists for any some so that for any

which completes the proof of Proposition 4.1.

A.2 Proposition 4.2

Part 1 We need asymptotic expressions for the first and second derivative of at . In (A.12) the first term in the numerator then vanishes since so that

| (A.13) |

whereas from (A.10)

and from (A.11) since

But , as and so that

and when the expressions for and are inserted in (A.13), it emerges that

| (A.14) |

The second derivative can be calculated from (A.12) and has a complicated expression. However, only the leading term is required, and this boils down to

where . But the central limit theorem on density form yields and as above

| (A.15) |

Part 2 We seek the asymptotic degradation when using the normalizing coefficients instead of the optimal with in both cases as upper limit. An elementary one-variable Taylor argument yields

with between and . Note that the linear term has vanished since is minimizing. The degradation in using instead of is then

| (A.16) |

where an assessment of is needed. The mean value theorem implies that

| (A.17) |

with between and . But the second order derivatives in (A.16) and (A.17) both tends to since and both and are squeezed in between. By combining (A.16) and (A.17) it follows that

| (A.18) |

where the error term is a consequence of those in (A.14) and (A.15), and inserting those leads after a straightforward calculation to

as claimed in Proposition 4.2.

A.3 Proposition 4.3

The normalized coefficients when the reinsurance function are using the Gaussian percentiles in (4.12) are and , and the upper limit deviates from the exact one which changes things considerably. Value at Risk is now

after inserting , and . Recall that we are assuming , and the degradation in using and instead of the optimal and then becomes

with and the expected surplus terms. This may be rewritten

| (A.19) |

where

| (A.20) |

| (A.21) |

| (A.22) |

The second of these terms represents degradation due to the difference between and with the upper limit the optimal and is on the argument that lead to Proposition 4.2 of order whereas must be examined further. Note that

| (A.23) |

where

Hence

after Taylor’s formula has been applied to the difference between the integrals. But as so that (A.23) after some straightforward calculations becomes

This is a quantity of the same order of magnitude as which by (A.20) can be rewritten

These two must be added whereas is of smaller order and can be ignored so that (A.19) is or after a little calculation

as claimed in Proposition 4.3.

Appendix B The simulation experiment in Section 3

Section 3.2 required the calculations of which is the main part of in (3.2). This requires a joint model for the uniform pair underlying . We have used the Clayton Copula

with , and and are then passed on through and where and are the distribution functions of and . From the definition of in (2.10) and in (2.9) right it follows that

which can be approximated by Monte Carlo through the following steps:

1. Generate simulations of .

2. Approximate through the kernel density estimate

with the

Gaussian integral, the standard deviation of

and .

3. Calculate , .

4. Generate

, .

5. Calculate

, .

6. Calculate , .

The approximations of then becomes

Note that all Monte Carlo simulations have been ∗-marked. The first step is carried out by an ordinary program for simulating portfolio losses whereas steps and is one of the ways the Clayton copula can be simulated; consult p.208 in Bølviken (2014). The final step makes use of the percentile function which is available for all standard distributions.