High Dimensional Latent Panel Quantile Regression

with an Application to Asset Pricing

Supplementary Material for

“High Dimensional Latent Panel Quantile Regression with an Application to Asset Pricing”

Abstract

We propose a generalization of the linear panel quantile regression model to accommodate both sparse and dense parts: sparse means that while the number of covariates available is large, potentially only a much smaller number of them have a nonzero impact on each conditional quantile of the response variable; while the dense part is represent by a low-rank matrix that can be approximated by latent factors and their loadings. Such a structure poses problems for traditional sparse estimators, such as the -penalised Quantile Regression, and for traditional latent factor estimators such as PCA. We propose a new estimation procedure, based on the ADMM algorithm, that consists of combining the quantile loss function with and nuclear norm regularization. We show, under general conditions, that our estimator can consistently estimate both the nonzero coefficients of the covariates and the latent low-rank matrix. This is done in a challenging setting that allows for temporal dependence, heavy-tail distributions, and the presence of latent factors.

Our proposed model has a ”Characteristics + Latent Factors” Quantile Asset Pricing Model interpretation: we apply our model and estimator with a large-dimensional panel of financial data and find that (i) characteristics have sparser predictive power once latent factors were controlled (ii) the factors and coefficients at upper and lower quantiles are different from the median.

keywords:

[class=MSC2010]keywords:

,

and

1 Introduction

A central question in asset pricing is to explain why certain assets pay higher returns than others. The Arbitrage Pricing Theory ([70]) and the Fama-French three factors model ([37]) explains the asset return variations by a linear combination of common risk factors. Assets with similar exposure to a common factor shall rise and fall together ([29]). However, empirical evidence appears to indicate that the firm characteristics, rather than common factors, can also explain the variations in stock returns ([33]), which suggests a characteristic-based model.

We generalize both modeling approaches and propose a “Characteristics + Latent Factors” quantile asset pricing framework. By incorporating the “Characteristics”, we improve the economic interpretability and explanatory power of the model. On the other hand, the finance literature has documented a zoo of new characteristics, and the proliferation of characteristics in this “variable zoo” leads to a concern about which characteristics really provide independent information about returns ([30]). Our model addresses this issue by imposing a sparse structure, meaning although a large set of characteristics is available, only a much smaller subset of them might have predictive power. We also incorporate “Latent Factors” to capture the common variations in asset returns. One additional benefit of having this part is that it might help alleviate the “omitted variable bias” problem ([45]). As in the literature, typically, these latent factors are estimated via principal component analysis, which means all possible latent explanatory variables might be important for prediction although their individual contribution might be small, we term this as the dense part. 111More about sparse modeling and dense modeling can be found in [44]. See also [27]. Hence, our framework allows for “Sparse + Dense” modeling with large scale panel data that consist of a large number of asset returns that are allowed to be weakly correlated across time. In addition, we focus on understanding the quantiles (hence the entire distribution) of returns rather than just the mean, in line with the recent interest in quantile factor models (e.g. [3], [25], [61], [39], and [72]). Our quantile asset pricing framework also inherits micro-foundation from the seminal quantile preference framework([62, 71, 46]) and, in particular, the dynamic quantile preference framework of [35].

Specifically, with as the excess return of asset in period , as a -dimensional vector of observable characteristics such as return volatility and trading volume, we study the following high dimensional latent panel quantile regression model:

| (1) |

where is the vector of coefficients, is an -dimensional vector of unobservable factor returns, represents the factor loadings which captures the sensitivity of asset on the factors, is the quantile index. We allow for the possibility of quantile dependence of sensitivity to risk factors as such evidence has been reported in the literature (e.g., [3]). For notation simplicity, we often denote , then is a low-rank matrix with unknown rank . Thus, with is the cumulative distribution function of conditioning on , and , we model the quantiles of returns (instead of expected returns) as a linear combination of the characteristics and latent factors. Our framework allows for the possibility of lagged dependent data. Here, we allow for the number of characteristics , and the time horizon , to grow to infinity as grows. Throughout, we focus on the case where is large, possibly much larger than , but for the true model is sparse and has only non-zero components.

Our framework is flexible enough that allows us to jointly answer the following three questions in asset pricing: (i) Which characteristics are important to explain the time series and cross-section of stock returns, after controlling for the factors? (ii) How much would the latent factors explain stock returns after controlling for firm characteristics? (iii) Does the relationship of stock returns and firm characteristics change across quantiles? The first question is related to the recent literature on variable selection in asset pricing using machine learning ([58, 40, 49]). The second question is related to an classical literature starting from 1980s on statistical factor models of stock returns ([22, 31] and recently [60]). The third question extends the literature in late 1990s on stock return and firm characteristics ([33, 34]) and further asks whether the relationship is heterogenous across quantiles.

There are several key features of considering prediction problem at the panel quantile model in this setting. First, stock returns are known to be asymmetric and exhibit heavy tail, thus modeling different quantiles of return provides extra information in addition to models of first and second moments. Second, quantile regression provides a richer characterization of the data, allowing heterogeneous relationship between stock returns and firm characteristics across the entire return distribution. Third, the latent factors might also be different at different quantiles of stock returns. Finally, quantile regression is more robust to the presence of outliers relative to other widely used mean-based approaches. Using a robust method is crucial when estimating low-rank structures (see e.g. [73]). As our framework is based on modeling the quantiles of the response variable, we do not put assumptions directly on the moments of the dependent variable.

Our main goal is to consistently estimate both the sparse part and the low-rank matrix. Recovery of a low-rank matrix, when there are additional high dimensional covariates, in a nonlinear model can be very challenging. The rank constraint will result in the optimization problem NP-hard. In addition, estimation in high dimensional regression is known to be a challenging task, which in our frameworks becomes even more difficult due to the additional latent structure. We address the former challenge via nuclear norm regularization which is similar to [20] in the matrix completion setting. Without covariates, the estimation can be done via solving a convex problem, and similarly there are strong statistical guarantees of recovery of the underlying low-rank structure. We address the latter challenge by imposing regularization on the vector of coefficients of the control variables, similarly to [13] which mainly focused on the cross-sectional data setting. Note that with regards to sparsity, we must be cautious, specially when considering predictive models ([73]). Furthermore, we explore the performance of our procedure under settings where the vector of coefficients can be dense (due to the low-rank matrix).

We view our work as complementary to the low dimensional quantile regression with interactive fixed effects framework as of the very recent work of [39], and the mean estimation setting in [64]. However, unlike [64] and [39], we allow the number of covariates to be large, perhaps . This comes with different significant challenges. On the computational side, it requires us to develop novel estimation algorithms, which turns out can also be used for the contexts in [64] and [39]. On the theoretical side, allowing requires a systematically different analysis as compared to [39], as it is known that ordinary quantile regression is inconsistent in high dimensional settings (), see [13].

Related Literature

Our work contributes to the recent growing literature on panel quantile model. [1], [47], [4], considered the fixed asymptotic case. [51] formally derived the asymptotic properties of the fixed effect quantile regression estimator under large asymptotics, and [42] further proposed fixed effects smoothed quantile regression estimator. [41] works on dynamic panel. [53] proposed a penalized estimation method where the individual effects are treated as pure location shift parameters common to all quantiles, for other related literature see [59], [43]. We refer to Chapter 19 of [56] for a review. Furthermore, our framework can be viewed as a generalization of the model in [3] which considered panel quantile model with independent errors and low dimensional covariates.

Our work also contributes to the literature on nuclear norm penalisation, which has been widely studied in the machine learning and statistical learning literature, [38], [67, 57, 69], [65], [16]. Recently, in the econometrics literature [5] proposes a framework of matrix completion for estimating causal effects, [10] for estimating approximate factor model, [28] considered the heterogeneous coefficients version of the linear panel data interactive fixed model where the main coefficients has a latent low-rank structure, [7] for robust principal component analysis, and [11] for imputing counterfactual outcome.

Finally, our results contribute to a growing literature on high dimensional quantile regression. [77] considered quantile regression with concave penalties for ultra-high dimensional data; [82] proposed an adaptively weighted -penalty for globally concerned quantile regression. Screening procedures based on moment conditions motivated by the quantile models have been proposed and analyzed in [50] and [79] in the high-dimensional regression setting. We refer to [56] for a review.

To sum-up, our paper makes the following contributions. First, we propose a new class of models that consist of both high dimensional regressors and latent factor structures. We provide a scalable estimation procedure, and show that the resulting estimator is consistent under suitable regularity conditions. Second, the high dimensional and non-smooth objective function require innovative strategies to derive all the above-mentioned results. In particular, our paper allows for serial dependence and this flexibility is important for the panel data case. It is well known that dealing with data dependence is a non-trivial problem, and there are additional challenges for high dimensional models even for those without incorporating the latent factors: the extension of lasso-based methods with relaxing the i.i.d. assumption and other restrictive assumptions (for instance, Gaussianity), is just beginning to occur, e.g. for time series data some recent development along this line can be found in [78]. Those lead to the novel use in our proofs of some techniques from the high dimensional statistics and econometrics literature, such as the localization argument from [13], and the new loss function introduced in [66]; from spectral theory, namely, properties of nuclear norm studied in [36], and concentrations results by [23]; and from empirical process theory [80, 75]. We also generalize the sampling and smoothness assumption of [13] by considering panel data with weak correlation across time. In particular, we refer readers to [80] for thorough discussions on -mixing.

On the theoretical side, we also present multiple results that entirely differ from those in [13]. In addition to allowing time dependence and a latent factor structure, we can consistently estimate the conditional quantiles without requiring a minimum eigenvalue condition on the behavior of the design matrix, which is typically required in the literature (e.g. [13]). Relative to approaches that incorporate latent factor structure but relies on the squared loss, the proposed estimators inherit from quantile regression certain robustness properties to the presence of outliers and heavy-tailed distributions. Finally, we apply our proposed model and estimator to a large-dimensional panel of financial data in the US stock market and find that different return quantiles have different selected firm characteristics and that the number of latent factors can be also be different.

Outline

The rest of the paper is organized as follows. Section 2 introduces the high dimensional latent quantile regression model, and provides an overview of the main theoretical results. Section 3 presents the estimator and our proposed ADMM algorithm. Section 4 discusses the statistical properties of the proposed estimator. Section 5 provides simulation results. Section 6 consists of the empirical results of our model applied to a real data set. The proofs of the main results are in the Supplementary Material.

Notation

For , we write . For a vector we define its norm as , where takes value if the statement inside is true, and zero otherwise; its norm as . We denote the -norm weighted by ’s (defined in eq(14)). The Euclidean norm is denoted by , thus . If is a matrix, its Frobenius norm is denoted by , its spectral norm by , its infinity norm by , its rank by , and its nuclear norm by where is the transpose of . The th column is denoted by . Furthermore, the multiplication of a tensor with a vector is denoted by , and, explicitly, . We also use the notation , , . For a sequence of random variables we denote by the sigma algebra generated by . Finally, for sequences and we write if there exists positive constants and such that for sufficiently large .

2 The Estimator and Overview of Rate Results

2.1 Basic Setting

The setting of interest corresponds to a high dimension latent panel quantile regression model, where , and satisfying

| (2) |

where denotes subjects, denotes time, is the vector of coefficients, is a low-rank matrix with unknown rank , is the quantile index, and is the cumulative distribution function of conditioning on , and . Thus, we model the quantile function at level as a linear combination of the predictors plus a low-rank matrix. Here, we allow for the number of covariates , and the time horizon , to grow to infinity as grows. Throughout the paper the quantile index is fixed. We mainly focus on the case where is large, possibly much larger than , but for the true model is sparse and has only non-zero components. Mathematically, .

When , with , this immediately leads to the following setting

| (3) |

where we model the quantile function at level as a linear combination of the covariates (as predictors) plus a latent factor structure. This is directly related to the panel data models with interactive fixed effects literature in econometrics, e.g. linear panel data model ([6]), nonlinear panel data models ([24, 26]).

Note, for eq (3), additional identification restrictions are needed for estimating and (see [9]). In addition, in nonlinear panel data models, this creates additional difficult in estimation, as the latent factors and their loadings part induce a nonconvex quantile regression problem. However, we deal with this in the following subsection via using a nuclear norm constraint. 222 Different identification conditions might result in different estimation procedures for and , see [8] and [24].

2.2 Estimator

In this subsection, we describe the high dimensional latent quantile estimator. With the sparsity and low-rank constraints in mind, a natural formulation for the estimation of is

| (4) |

where is the quantile loss function as in [54], is a parameter that directly controls the sparsity of , and controls the rank of the estimated latent matrix.

While the formulation in (4) seems appealing, as it enforces variable selection and low-rank matrix estimation simultaneously, (4) is a non-convex problem due to the constraints posed by the and functions. We propose a convex relaxation of (4). Inspired by the seminal works of [74] and [20], we formulate the problem as the following

| (5) |

where and are tuning parameters, and are user specified weights (more on this in Section 4 ). Notice that is the nuclear norm defined on Page 4. The nuclear norm regularization works on the singular value of a matrix, the intuition is that via penalization with the nuclear norm, the resulting problem will be convex. Just as -minimization is the tightest convex relaxation of the combinatorial -minimization problem, nuclear-norm minimization is the tightest convex relaxation of the NP-hard rank minimization problem, see [18].

2.3 Summary of results

We now summarize our main results. For the model defined in (2):

-

•

Under (2), , an assumption that implicitly requires , and other regularity conditions defined in Section 4, we show that our estimator defined in Section 3 is consistent for . Specifically, for the independent data case (across and ), under suitable regularity conditions that can be found in Section 4, we have

(6) and

(7) Importantly, the rates in (6) and (7), up to logarithmic factor, match those in previous works. However, our setting allows for modeling at different quantile levels. We also complement our results by allowing for the possibility of lagged dependent data. Specifically, under a -mixing assumption, Theorem 4.2 provides a statistical guarantee for estimating . This result can be thought as a generalization of the statements in (6) and (7).

Let for and be the conditional quantiles. We show that, under weaker conditions than the ones needed for Theorem 4.2, our estimates satisfy

for the independent data case (across and ). This is a particular instance of Theorem 4.1 which allows the possibility of time dependence.

-

•

An important aspect of our analysis is that we contrast the performance of our estimator in settings where the possibility of a dense provided that the features are highly correlated. We show that there exist choices of the tuning parameters for our estimator that lead to consistent estimation.

- •

-

•

Section 6 provides thorough examples on financial data that illustrate the flexibility and interpretability of our approach.

Although our theoretical analysis builds on the work by [13], there are multiple challenges that we must face in order to prove the consistency of our estimator. First, the construction of the restricted set now involves the nuclear norm penalty. This requires us to define a new restricted set that captures the contributions of the low-rank matrix. Second, when bounding the empirical processes that naturally arise in our proof, we have to simultaneously deal with the sparse and dense components. Furthermore, throughout our proofs, we have to carefully handle the weak dependence assumption that can be found in Section 4.

3 High Dimensional Latent Panel Quantile Regression

In this subsection, we describe the main steps of our proposed ADMM algorithm, details can be found in Section S1. We start by introducing slack variables to the original problem (5). As a result, a problem equivalent to (5) is

| (8) |

To solve (8), we propose a scaled version of the ADMM algorithm which relies on the following Augmented Lagrangian

| (9) |

where is a penalty parameter.

Notice that in (9), we have followed the usual construction of ADMM via introducing the scaled dual variables corresponding to the constraints in (8) – those are , , , and . Next, recall that ADMM proceeds by iteratively minimizing the Augmented Lagrangian in blocks with respected to the original variables, in our case and , and then updating the scaled dual variables (see Equations 3.5–3.7 in [15]). The explicit updates can be found in the Supplementary Material. Here, we highlight the updates for , , and . For updating at iteration , we solve the problem

This can be solved in closed form exploiting the well known thresholding operator, see the details in Section S2.2. As for updating , we solve

| (10) |

via the singular value shrinkage operator, see Theorem 2.1 in [17].

Furthermore, we update , at iteration , via

| (11) |

which can be found in closed formula by Lemma 5.1 from [2].

Remark 1.

After estimating , we can estimate and via the singular value decomposition of and following equation

| (12) |

where and are of dimension . This immediately leads to factors and loadings estimated that can be used to obtain insights about the structure of the data. A formal identification statement is given in Corollary 4.3.

Finally, it is immediate to modify the proposed ADMM to the case when there are no covariates (), see Section S1.1 in the Supplementary Material. Hence, our proposed estimation procedure can be applied to settings (i) with low dimensional covariates, or (ii) without covariates. However, in what follows, we focus on the high dimensional covariates setting.

4 Theory

The purpose of this section is to provide statistical guarantees for the estimator developed in the previous section. We focus on estimating the quantile function, allowing for the high dimensional scenario where and can grow as grows.

4.1 Estimating the quantiles

We show that our proposed estimator is consistent for estimating the conditional quantiles.

Throughout, we treat as fixed parameters. As for the data generation process, our next condition requires that the observations are independent across , and weakly dependent across time.

Assumption 1.

We assume that

where . Furthermore, the following holds:

-

(i)

There exists a function for positive constants and such that, conditional on and , where are independent across . Also, for each , the sequence is stationary and -mixing with mixing coefficients satisfying for some . Moreover, there exists , such that

(13) Here,

-

(ii)

There exists satisfying

for some , where is the probability density function associated with when conditioning on , and with parameters and .

Note that Assumption 1 is related to the sampling and smoothness assumption of [13]. Furthermore, we highlight that similar to [13], our framework is rich enough that avoids imposing Gaussian modeling constraints. However, unlike [13], we consider panel data with weak correlation across time. In particular, we refer readers to [80] for thorough discussions on -mixing. Another difference with [13] is that we do not require any smoothness assumption on the condition density function of the response given the covariates.

It is worth mentioning that the parameter in Assumption 1 controls the strength of the time dependence in the data while parameter will relate to the tuning parameters and will impact the rates. As we decrease the value of condition (13) is easier to satisfy but the tuning parameters increase and slow down the rates of convergence. Furthermore, in the case that are independent our theoretical results will hold without imposing (13).

Next, we require that along each dimension the second moment of the covariates is one. We also assume that the second moments can be reasonably well estimated by their empirical counterparts.

Assumption 2.

We assume for all . Then

| (14) |

and we require that

Assumption 2 appeared as Condition D.3 in [13]. It is met by general models on the covariates, see for instance Design 2 in [13].

Using the empirical second order moments , we analyze the performance of the constrained estimator

| (15) |

Our main result of this subsection is provided next.

Theorem 4.1.

Theorem 4.1 shows that we can consistently estimate the conditional quantiles at a rate that combines the sparse and dense signal magnitudes. This result differs from [13] in several ways. First, [13] work with cross sectional data and focus on the estimation of the vector of parameter coefficients instead of the conditional quantiles. Therefore the assumptions for Theorem 4.1 and those in [13] are very different. For example, [13] required a minimum eigenvalue condition on the behavior of the design matrix, whereas we can avoid this. Furthermore, unlike [13], Theorem 4.1 allows for panel data with dependence across time. This translates into a technical challenge to arrive at Theorem 4.1, since it is not possible to use the analysis from [13] which relies heavily on independence. In fact, the minimum eigenvalue condition in [13] (Condition D.4) can be difficult to be verified in practice without the independence data assumption, and hence Theorem 4.1 has a different setting than those results in [13]. Also, our setting and estimator involve the latent factors which make both the estimator and theory more complex than the framework in [13]. Lastly, while some of the ideas in the proof of Theorem 4.1 come from [66], all of the technical steps involved in the proof of Theorem 4.1 are novel.

On another note, the rate of in Theorem 4.1 must be such that and satisfies (13). The parameter in (13) controls the terms and both of which determine the tuning parameters and imply specific rates of convergence. Cearly, . Moreover, the parameter measures the strength of the dependence in the data, whereas can be interpreted as the effective number of independent samples across time. In particular, when , we have that are basically independent across time, and so the final rate depends on . As a different example, since we would like , with we have and so that and . In this case condition (13) requires the parameter that governs the mixing speed to be such that .

4.2 Estimating the coefficients and latent factors

We show that our proposed estimator is consistent for estimating the vector of coefficients and latent factors separately in a broad range of models, and in some cases attains minimax rates, as in [19].

In order to obtain our main result of this subsection, we first provide some additional notation and assumptions. For a fixed , we assume that (2) holds. We also let be the support of , thus

and we write , and .

Assumption 3.

Conditional on , are independent across . Also, for each , the sequence is stationary and -mixing with mixing coefficients satisfying for some . Moreover, there exists , such that (13) holds. In addition, there exists satisfying

where is the probability density function associated with when conditioning on , and with parameters and . Furthermore, and are both bounded by and , respectively, uniformly in and in the support of .

As it can been seen in Lemma S4 from the Supplementary Material, the error of our estimator defined in (15), , belongs to a restricted set, which in our framework is defined as

| (16) |

for an appropriate positive constant .

Similar in spirit to other high dimensional settings such as those in [21], [14], [13] and [32], we impose an identifiability condition involving the restricted set which is expressed next and will be used in order to attain our main results. This is the key difference with the analysis in Section 4.1. Before arriving at our next condition, we introduce some notation.

For , we denote by the support ot the largest components, excluding entries in , of the vector . We also use the convention .

Assumption 4.

Few comments are in order. First, if then (17) and (18) become the restricted identifiability and nonlinearity conditions as of [13]. Second, the denominator of (17) contains the term . To see why this is reasonable, consider the case where , and are i.i.d.. Then

Hence, appears also in the numerator of (17) and it is not restrictive its presence in the denominator of (17).

We now state our result for estimating and .

Theorem 4.2.

Theorem 4.2 gives an upper bound on the performance of for estimating the vector of coefficients and the latent matrix . For simplicity, consider the case of i.i.d data. Then the convergence rate of our estimation of , under the Euclidean norm, is in the order of , if we ignore all the other factors. Hence, we can consistently estimate provided that . This is similar to the low-rank condition in [65]. In the low dimensional case , the rate matches that of Theorem 1 in [64]. However, unlike [64], our estimator is based on a loss function that is robust to outliers, and our assumptions also allow for weak dependence across time, making our framework potentially more general. Furthermore, the same applies to our rate on the mean squared error for estimating , which also matches that in Theorem 1 of [64].

With regards to the novelty of Theorem 4.2, we highlight that, while its proof is similar in spirit to that of Theorem 2 in [13], there are some significant differences. First, the construction of the restricted set used in Theorem 4.2 involves two different penalties which makes challenging to disentangle the behavior of and , whereas [13] only had to dealt with one penalty. Second, the empirical processes in [13] all involved independent data whereas as the proof of Theorem 4.2 handles the time dependence of our model and the latent factors.

Interestingly, it is expected that the rate in Theorem 4.2 is optimal. To elaborate on this point, consider the simple case where , , , and are mean zero i.i.d. sub-Gaussian(. The latter implies that

for a positive constant , and for all . Then by Theorem 2.3 in [19], we have the following lower bound for estimating :

| (22) |

Notably, the lower bound in (22) matches the rate implied by Theorem 4.2, ignoring other factors depending on , , , and . However, we highlight that the upper bound (21) in Theorem 4.2 holds without the perhaps restrictive condition that the errors are sub-Gaussian.

We conclude this section with a result regarding the estimation of the factors and loadings of the latent matrix . This is expressed in Corollary 4.3 below and is immediate consequence of Theorem 4.2 and Theorem 3 in [81].

Corollary 4.3.

Suppose that the all the conditions of Theorem 4.2 hold. Let be the singular values of , and the singular values of . Let and be matrices with orthonormal columns satisfying

and for . Then

| (23) |

and

| (24) |

Here, is the group of orthonormal matrices, and

A particularly interesting instance of Corollary 4.3 is when

a natural setting if the entries of are . Then the upper bound (23) becomes

whereas (24) is now

The conclusion of Corollary 4.3 allows us to provide an upper bound on the estimation of factors () and loadings () of the latent matrix . Notice that we are not claiming that we provide consistent estimation of the number latent factors, as Theorem 4.2 only guarantees consistent estimation of . However, other authors, e.g. [63], have observed that estimation can be possible even if is unknown.

4.3 Nearly low rank quantiles

We conclude our theory section by studying the case where the matrix has nearley low rank. We make this formal by imposing the condition that can be perturbed into a low-rank matrix. While the result in this subsection differs in the choice of tuning parameters from those in Theorem 4.2, our result here suggests that even in this low-rank setting there exists a choice of tuning parameters that allows our estimator to provide consistent estimation.

We view our setting below as an extension of the linear model in [28] to the quantile framework and reduced rank regression. The specific condition is stated next.

Assumption 5.

With probability approaching one, it holds that , and

with as defined in Theorem 4.2. Furthermore, .

Notice that in Assumption 5, is an approximation error. In the case , the condition implies that with probability close to one.

Next, exploiting Assumption 5, we show that (15) provides consistent estimation of the quantile function, namely, of .

Theorem 4.4.

Suppose that Assumptions 2–5 hold. Let be the solution to (15) with the additional constraint that , for a large enough positive constant . Then

where is a sequence with , and for choices

and

Interestingly, unlike Theorem 4.2, Theorem 4.4 does not show that we can estimate and separately. Instead, we show that , the estimated matrix of latent factors, captures the overall contribution of both and . This is expected since Assumption 5 states that, with high probability, has rank of the same order as of . Notably, is able to estimate via requiring that the value of increases significantly with respect to the choice in Theorem 4.2, while keeping .

As for the convergence rate in Theorem 4.4 for estimating , this is of the order , if we ignore , , and . When the data are independent, the rate becomes of the order . In such framework, our result matches the minimax rate of estimation in [18] for estimating an matrix of rank , provided that , see our discussion in Section 4.2.

5 Simulation

In this section, we evaluate the performance of our proposed approach (-NN-QR) with extensive numerical simulations focusing on the median case, namely the case when = 0.5. As benchmarks, we consider the -penalized quantile regression studied in [12], and similarly we refer to this procedure as -QR. We also compare with the mean case, which we denote it as -NN-LS as it combines the -loss function with and nuclear norm regularization. We consider different generative scenarios. For each scenario we randomly generate 100 different data sets and compute the estimates of the methods for a grid of values of and . Specifically, these tuning parameters are taken to satisfy and . Given any choice of tuning parameters, we evaluate the performance of each competing method, averaging over the 100 data sets, and report values that correspond to the best performance. These are referred as optimal tuning parameters and can be thought of as oracle choices.

We also propose a modified Bayesian Information Criterion (BIC) to select the best pair of tuning parameters. Given a pair , our method produces a score . Specifically, denote and ,

| (25) |

where is a constant. The intuition here is that the first term in the right hand side of (25) corresponds to the fit to the data. The second term includes the factor to emulate the usual penalization in BIC. The number of parameters in the model with choices and is estimated by for the vector of coefficients, and for the latent matrix. The latter is reasonable since is potentially a low rank matrix and we simply count the number of parameters in its singular value decomposition. As for the extra quantity , we have included this term to balance the dominating contribution of the . We find that in practice gives reasonable performance in both simulated and real data. This is the choice that we use in our experiments. Then for each of data set under each design, we calculate the minimum value of , over the different choices of and , and report the average over the 100 Monte Carlo simulations. We refer to this as BIC--NN-QR.

As performance measure we use a scaled version (see Tables 1-2) of the squared distance between the true vector of coefficients and the corresponding estimate. We also consider a different metric, the “Quantile error” ([55]):

| (26) |

which measures the average squared error between the quantile functions at the samples and their respective estimates. Since our simulations consider models with symmetric mean zero error, the above metric corresponds to the mean squared error for estimating the conditional expectation.

Next, we provide a detailed description of each of the generative models that we consider in our experiments. In each model design the dimensions of the problem are given by , and , and we also consider the instance . The covariates are i.i.d .

Design 1. (Location shift model) The data is generated from the model

| (27) |

where , and , with the Student’s t-distribution with 3 degrees of freedom. The scaling factor simply ensures that the errors have variance . In (27), we take the vector to satisfy

We also construct to be rank one, defined as

Design 2. (Location-scale shift model) We consider the model

| (28) |

where , and . The parameters in and in (28) are taken to be the same as in (27). The only difference now is that we have the extra parameter , which we define as for .

Design 3. (Location shift model with random factors) This is the same as Design 1 with the difference that we now generate as

| (29) |

where

| (30) |

| Design 1 | Design 2 | ||||||

|---|---|---|---|---|---|---|---|

| Method | Quantile error | Quantile error | |||||

| -NN-QR | 300 | 30 | 300 | 0.86 | 0.03 | 0.69 | 0.03 |

| BIC--NN-QR | 300 | 30 | 300 | 0.86 | 0.03 | 0.89 | 0.03 |

| -NN-LS | 300 | 30 | 300 | 2.58 | 0.05 | 1.03 | 0.04 |

| -QR | 300 | 30 | 300 | 8.18 | 4.19 | 6.81 | 4.18 |

| -NN-QR | 300 | 30 | 100 | 2.99 | 0.04 | 2.39 | 0.04 |

| BIC--NN-QR | 300 | 30 | 100 | 2.99 | 0.04 | 2.39 | 0.04 |

| -NN-LS | 300 | 30 | 100 | 8.06 | 0.12 | 3.11 | 0.08 |

| -QR | 300 | 30 | 100 | 41.0 | 4.19 | 26.0 | 4.19 |

| -NN-QR | 300 | 5 | 300 | 0.22 | 0.003 | 0.39 | 0.03 |

| BIC--NN-QR | 300 | 5 | 300 | 0.22 | 0.003 | 0.48 | 0.03 |

| -NN-LS | 300 | 5 | 300 | 0.37 | 0.01 | 0.69 | 0.03 |

| -QR | 300 | 5 | 300 | 2.6 | 4.19 | 3.27 | 4.19 |

| -NN-QR | 300 | 5 | 100 | 0.50 | 0.008 | 0.80 | 0.03 |

| BIC--NN-QR | 300 | 5 | 100 | 0.53 | 0.009 | 0.97 | 0.03 |

| -NN-LS | 300 | 5 | 100 | 1.12 | 0.02 | 1.46 | 0.04 |

| -QR | 300 | 5 | 100 | 7.87 | 4.19 | 8.56 | 4.19 |

| -NN-QR | 100 | 30 | 300 | 2.97 | 0.04 | 2.26 | 0.04 |

| BIC--NN-QR | 100 | 30 | 300 | 2.97 | 0.04 | 2.81 | 0.04 |

| -NN-LS | 100 | 30 | 300 | 9.77 | 0.12 | 3.39 | 0.06 |

| -QR | 100 | 30 | 300 | 40.0 | 4.23 | 24.0 | 4.23 |

| -NN-QR | 100 | 30 | 100 | 2.3 | 0.04 | 10.0 | 0.03 |

| BIC--NN-QR | 100 | 30 | 100 | 2.3 | 0.06 | 11.0 | 0.04 |

| -NN-LS | 100 | 30 | 100 | 8.4 | 0.79 | 13.0 | 0.16 |

| -QR | 100 | 30 | 100 | 229.0 | 4.23 | 177.0 | 4.23 |

| -NN-QR | 100 | 5 | 300 | 0.64 | 0.008 | 0.89 | 0.03 |

| BIC--NN-QR | 100 | 5 | 300 | 0.65 | 0.008 | 1.32 | 0.03 |

| -NN-LS | 100 | 5 | 300 | 1.25 | 0.02 | 1.67 | 0.05 |

| -QR | 100 | 5 | 300 | 8.79 | 4.23 | 8.61 | 4.23 |

| -NN-QR | 100 | 5 | 100 | 1.82 | 0.009 | 3.30 | 0.03 |

| BIC--NN-QR | 100 | 5 | 100 | 1.85 | 0.01 | 3.74 | 0.04 |

| -NN-LS | 100 | 5 | 100 | 4.06 | 0.03 | 4.45 | 0.14 |

| -QR | 100 | 5 | 100 | 32.0 | 4.23 | 27.0 | 4.23 |

| -NN-QR | 50 | 50 | 50 | 136.0 | 0.09 | 388.0 | 0.21 |

| BIC--NN-QR | 50 | 50 | 50 | 241.0 | 0.33 | 522.0 | 0.59 |

| -NN-LS | 50 | 50 | 50 | 2010 | 0.17 | 982 | 0.45 |

| -QR | 50 | 50 | 50 | 1258 | 4.27 | 2000.6 | 4.33 |

| Design 3 | Design 4 | ||||||

|---|---|---|---|---|---|---|---|

| Method | Quantile error | Quantile error | |||||

| -NN-QR | 300 | 30 | 300 | 2.17 | 0.17 | 1.58 | 0.11 |

| BIC--NN-QR | 300 | 30 | 300 | 2.17 | 0.29 | 2.81 | 0.26 |

| -NN-LS | 300 | 30 | 300 | 3.33 | 0.19 | 3.54 | 0.12 |

| -QR | 300 | 30 | 300 | 6.59 | 1.09 | 12.0 | 1.01 |

| -NN-QR | 300 | 30 | 100 | 10.0 | 0.18 | 4.61 | 0.13 |

| BIC--NN-QR | 300 | 30 | 100 | 11.0 | 0.26 | 4.61 | 0.16 |

| -NN-LS | 300 | 30 | 100 | 11.0 | 0.25 | 9.21 | 0.17 |

| -QR | 300 | 30 | 100 | 27.0 | 11.10 | 47.2 | 1.10 |

| -NN-QR | 300 | 5 | 300 | 1.13 | 0.17 | 0.27 | 0.03 |

| BIC--NN-QR | 300 | 5 | 300 | 1.56 | 0.33 | 0.74 | 0.13 |

| -NN-LS | 300 | 5 | 300 | 1.58 | 0.19 | 0.49 | 0.05 |

| -QR | 300 | 5 | 300 | 2.47 | 1.10 | 5.52 | 1.09 |

| -NN-QR | 300 | 5 | 100 | 3.04 | 0.19 | 0.69 | 0.05 |

| BIC--NN-QR | 300 | 5 | 100 | 4.37 | 0.27 | 1.11 | 0.15 |

| -NN-LS | 300 | 5 | 100 | 4.43 | 0.27 | 1.12 | 0.05 |

| -QR | 300 | 5 | 100 | 7.65 | 1.11 | 13.4 | 1.10 |

| -NN-QR | 100 | 30 | 300 | 11.0 | 0.18 | 7.06 | 0.15 |

| BIC--NN-QR | 100 | 30 | 300 | 12.0 | 0.27 | 7.29 | 0.24 |

| -NN-LS | 100 | 30 | 300 | 12.0 | 0.34 | 11.2 | 0.18 |

| -QR | 100 | 30 | 300 | 26.0 | 1.10 | 51.0 | 1.12 |

| -NN-QR | 100 | 30 | 100 | 6.12 | 0.17 | 32.1 | 0.10 |

| BIC--NN-QR | 100 | 30 | 100 | 6.64 | 0.22 | 35.4 | 0.15 |

| -NN-LS | 100 | 30 | 100 | 8.63 | 1.08 | 82.0 | 0.84 |

| -QR | 100 | 30 | 100 | 16.5 | 1.12 | 267.6 | 1.13 |

| -NN-QR | 100 | 5 | 300 | 2.99 | 0.18 | 0.86 | 0.05 |

| BIC--NN-QR | 100 | 5 | 300 | 4.19 | 0.26 | 1.43 | 0.14 |

| -NN-LS | 100 | 5 | 300 | 5.27 | 0.33 | 1.45 | 0.05 |

| -QR | 100 | 5 | 300 | 8.59 | 1.10 | 21.0 | 1.09 |

| -NN-QR | 100 | 5 | 100 | 12.3 | 0.16 | 2.15 | 0.04 |

| BIC--NN-QR | 100 | 5 | 100 | 13.1 | 0.20 | 2.43 | 0.07 |

| -NN-LS | 100 | 5 | 100 | 15.0 | 1.09 | 3.61 | 0.07 |

| -QR | 100 | 5 | 100 | 24.7 | 1.10 | 45.7 | 1.09 |

| -NN-QR | 50 | 50 | 50 | 386.7 | 0.32 | 511 | 0.27 |

| BIC--NN-QR | 50 | 50 | 50 | 898.1 | 0.97 | 1128.1 | 0.74 |

| -NN-LS | 50 | 50 | 50 | 605.2 | 0.44 | 967.3 | 0.49 |

| -QR | 50 | 50 | 50 | 1035.8 | 1.15 | 1697.5 | 1.18 |

Design 4. (Location-scale shift model with random factors) This is a combination of Designs 2 and 3. Specifically, we generate data as in (28) but with satisfying (29) and (30).

The results in Tables 1-2 show a clear advantage of our proposed method against the benchmarks across the four designs we consider. This is true for estimating the vector of coefficients, and under the measure of quantile error. Importantly, our approach is not only the best under the optimal choice of tuning parameters but it remains competitive with the BIC type of criteria defined with the score (25). In particular, under Designs 1 and 2, the data driven version of our estimator, BIC--NN-QR, performs very closely to the ideally tuned one -NN-QR. In the more challenging settings of Designs 3 and 4, we noticed that BIC--NN-QR performs reasonably well compared to -NN-QR.

6 Empirical Performance of the “Characteristics + Latent Factor” Model in Asset Pricing

Data Description

We use data from CRSP and Compustat to construct 24 firm level characteristics that are documented to explain the cross section and time series of stock returns in the finance and accounting literature. The characteristics we choose include well-known drivers of stock returns such as beta, size, book-to-market, momentum, volatility, liquidity, investment and profitability. Table LABEL:Table-names in the Supplementary Material lists details of the characteristics used and the methods to construct the data. We follow the procedures of [48] to construct the characteristics of interest. The characteristics used in our model are standardized to have zero mean and unit variance. Figure 1 plots the histogram of monthly stock returns and standardized firm characteristics. Each of them have different distribution patterns, suggesting the potential nonlinear relationship between returns and firm characteristics, which can be potentially captured by our quantile model.

Our empirical design is closely related to the characteristics model proposed by [33, 34]. To avoid any “data snooping” issue cause by grouping, we conduct the empirical analysis at individual stock level. Specifically, we use the sample period from January 2000 to December 2018, and estimate our model using monthly returns (228 months) from 1306 firms that have non-missing values during this period.

A “Characteristic + Latent Factor” Asset Pricing Model

We apply our model to fit the cross section and time series of stock returns ([60]). There are assets (stocks), and the return of the each asset can potentially be explained by observed asset characteristics (sparse part) and latent factors (dense part). The asset characteristics are the covariates in our model. Our model imposes a sparse structure on the characteristics so that only the characteristics having the strongest explanatory powers are selected by the model. The part that’s unexplained by the firm characteristics are captured by latent factors.

Suppose we have stock returns (,…,), and observed firm characteristics (,…,) over periods. The return quantile at level of portfolio in time is assumed to be the following:

where , e.g. or , is the -th characteristic (e.g. the book-to-market ratio) of asset in time . The coefficient captures the extent to which assets with higher/lower characteristic delivers higher average return. The term contains the latent factors in period which captures systematic risks in the market, and contains portfolio ’s loading on these factors (i.e. exposure to risk).

There is a discussion in academic research on “factor versus characteristics” in late 1990s and early 2000s. The factor/risk based view argues that an asset has higher expected returns because of its exposure to risk factors (e.g. Fama-French 3 factors) which represent some unobserved systematic risk. An asset’s exposure to risk factors are measured by factor loadings. The characteristics view claims that stocks have higher expected returns simply because they have certain characteristics (e.g. higher book-to-market ratios, smaller market capitalization), which might be independent of systematic risk ([33, 34]). The formulation of our model accommodates both the factor view and the characteristics view. The sparse part is similar to [33, 34], in which stock return are explained by firm characteristics. The dense part assumes a low-dimensional latent factor structure where the common variations in stock returns are driven by several “risk factors”.

Empirical Results

We first get the estimates and at three different quantiles, using our proposed ADMM algorithm. We then decompose into the products of its principal components and their loadings via eq(12). The -th element of , denoted as , can be interpreted as the exposure of asset to the -th latent factor (or in finance terminology, “quantity of risk”). And the -th elements of , denoted as , can be interpreted as the compensation of the risk exposure to the -th latent factor in time period (or in finance terminology, “price of risk”). The model are estimated with different tuning parameters and , and use our proposed BIC to select the optimal tuning parameters. The details of the information criteria can be found in equation (25).

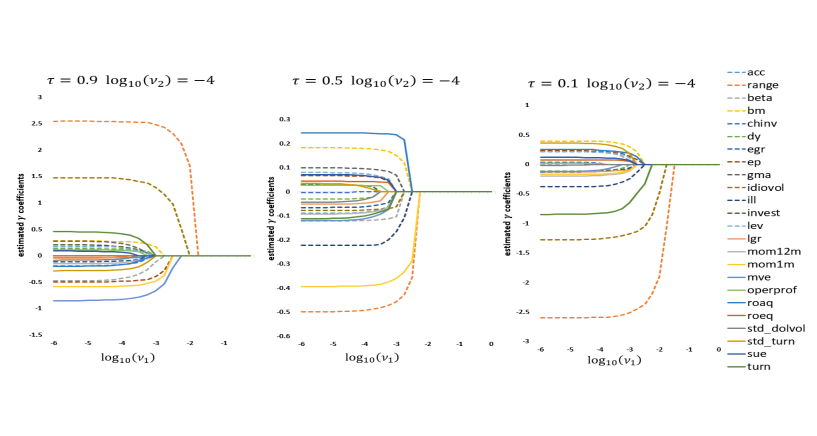

The tuning parameter governs the sparsity of the coefficient vector . The larger is, the larger the shrinkage effect on . Figure 2 illustrate the effect of this shrinkage. With fixed, as the value of increases, more coefficients in the estimated vector shrink to zero. From a statistical point of view, the “effective characteristics” that can explain stock returns are those with non-zero coefficient at relatively large values of .

Table 3 reports the relationship between tuning parameter and rank of estimated at different quantiles. It shows that the tuning parameter governs the rank of matrix , and that as increases, we penalize more on the rank of matrix through its nuclear norm.

| -6.0 | 228 | 228 | 228 |

|---|---|---|---|

| -5.5 | 228 | 228 | 228 |

| -5.0 | 228 | 228 | 228 |

| -4.5 | 164 | 228 | 168 |

| -4.0 | 1 | 7 | 2 |

| -3.5 | 1 | 1 | 1 |

| -3.0 | 0 | 0 | 0 |

-

•

Note: Estimated under different values of turning parameter , when is fixed. The results are reported for quantiles 10%, 50% and 90%.

The left panel of Table 4 reports the estimated coefficients in the sparse part when we fix the tuning parameters at and . The signs of some characteristics are the same across the quantiles, e.g. size (mve), book-to-market (bm), momentum (mom1m, mom12m), accurals (acc), book equity growth (egr), leverage (lev), and standardized unexpected earnings (sue). However, some characteristics have heterogenous effects on future returns at different quantiles. For example, at the 10% quantile, high beta stocks have high future returns, which is consistent with results found via the CAPM; while at and 90% quantile, high beta stocks have low future returns, which conforms the “low beta anomaly” phenomenon. Volatility (measured by both range and idiosyncratic volatility) is positively correlated with future returns at 90% quantile, but negatively correlated with future returns at 10% and 50% percentile. The result suggests that quantile models can capture a wider picture of the heterogenous relationship between asset returns and firm characteristics at different parts of the distribution ([52]).

| Fixed and | Optimal and (BIC) | |||||

|---|---|---|---|---|---|---|

| acc | -0.089 | -0.074 | -0.041 | 0 | 0 | 0 |

| range | -2.574 | -0.481 | 2.526 | -2.372 | -0.356 | 2.429 |

| beta | 0.174 | -0.116 | -0.406 | 0 | 0 | -0.115 |

| bm | 0.371 | 0.175 | 0.263 | 0 | 0 | 0.168 |

| chinv | 0 | 0 | -0.152 | 0 | 0 | 0 |

| dy | -0.086 | 0 | 0.119 | 0 | 0 | 0 |

| egr | -0.106 | -0.053 | -0.091 | 0 | 0 | 0 |

| ep | 0.199 | 0.057 | -0.479 | 0 | 0 | -0.391 |

| gma | 0 | 0.091 | 0.201 | 0 | 0 | 0 |

| idiovol | -1.229 | -0.071 | 1.438 | -1.055 | 0 | 1.286 |

| ill | -0.334 | -0.218 | 0 | 0 | 0 | 0 |

| invest | -0.097 | 0 | 0.146 | 0 | 0 | 0 |

| lev | 0.183 | 0.063 | 0.129 | 0 | 0 | 0 |

| lgr | -0.106 | -0.037 | 0 | 0 | 0 | 0 |

| mom12m | -0.166 | -0.077 | -0.117 | 0 | 0 | 0 |

| mom1m | -0.150 | -0.384 | -0.571 | 0 | -0.286 | -0.477 |

| mve | -0.038 | -0.093 | -0.811 | 0 | 0 | -0.667 |

| operprof | 0 | 0.025 | 0.088 | 0 | 0 | 0 |

| roaq | 0.221 | 0.242 | -0.147 | 0 | 0 | 0 |

| roeq | 0.073 | 0.041 | 0 | 0 | 0 | 0 |

| std_dolvol | 0 | 0 | -0.039 | 0 | 0 | 0 |

| std_turn | 0.310 | 0 | -0.247 | 0 | 0 | 0 |

| sue | 0.105 | 0.061 | 0.045 | 0 | 0 | 0 |

| turn | -0.796 | -0.083 | 0.386 | -0.330 | 0 | 0 |

-

•

Note: The left panel reports the estimated coefficient vector in the sparse part for quantiles 10%, 50% and 90%, when the tuning parameters are fixed at , . The right panel reports the estimated coefficient vector under the when the turning parameters are optimal, as selected by BIC (indicated in Table 5).

Table 5 reports the selected optimal tuning parameters and for different quantiles. The tuning parameters are selected via BIC based on (25) as discussed in Section 5. For every and , we get the estimates and and the number of factors . The vector is sparse with non-zero coefficients on selected characteristics. The 10% quantile of returns has only 1 latent factor, and 3 selected characteristics. The median of returns has 7 latent factors and 2 selected characteristics. The 90% quantile of returns has 2 latent factors and 7 selected characteristics. Range is the only characteristic selected across all 3 quantiles. Idiosyncratic volatility is selected at 10% and 90% quantiles, with opposite signs. 1-month momentum is selected at 50% and 90% percentiles, with negative sign suggesting reversal in returns.

| optimal | 1 | 7 | 2 |

|---|---|---|---|

| optimal | |||

| optimal |

-

•

Note: This table reports the selected optimal tuning parameter and that minimize the objective function in equation (25) for different quantiles.

Overall, the empirical evidence suggests that both firm characteristics and latent risk factors have valuable information in explaining stock returns. In addition, we find that the selected characteristics and number of latent factors differ across the quantiles.

Interpretation of Latent Factors

Table 6 below reports the variance in the matrix explained by each Principal Component (PC) or latent factor. At upper and lower quantiles, the first PC dominates. At the median there are more latent factors accounting for the variations in , with second PC explaining 13.8% and third PC explaining 6.8%.

| PC1 | 100.00% | 73.82% | 99.68% |

| PC2 | 13.71% | 0.32% | |

| PC3 | 6.78% | ||

| PC4 | 4.12% | ||

| PC5 | 1.11% | ||

| PC6 | 0.45% | ||

| PC7 | 0.01% | ||

| Total | 100.00% | 100.00% | 100.00% |

-

•

Note: Variance of matrix explained by each principal component for different quantiles.

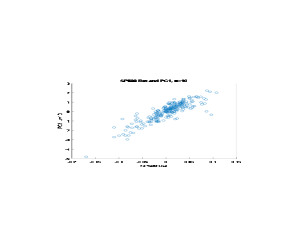

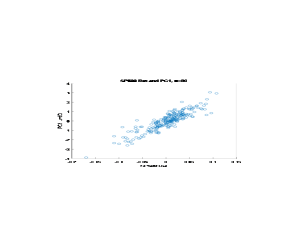

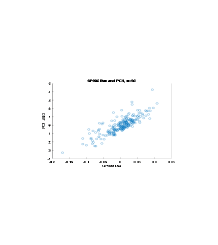

We also found the first PC captures the market returns in all three quantiles: Figure 3 plots the first principal component against the monthly returns of S&P500 index, showing that they have strong positive correlations.

Acknowledgements

We would like to thank the Editors, the Associate Editors and two anonymous referees for their detailed reviews, which helped to improve the paper substantially. We are also grateful to Victor Chernozhukov, Iván Fernández-Val, Bryan Graham, Hiroaki Kaido, Anna Mikusheva, Whitney Newey, Eric Renault, Jeremy Smith, and Vasilis Syrgkanis for helpful discussions.

References

- Abrevaya and Dahl [2008] {barticle}[author] \bauthor\bsnmAbrevaya, \bfnmJason\binitsJ. and \bauthor\bsnmDahl, \bfnmChristian M\binitsC. M. (\byear2008). \btitleThe effects of birth inputs on birthweight: evidence from quantile estimation on panel data. \bjournalJournal of Business & Economic Statistics \bvolume26 \bpages379–397. \endbibitem

- Ali, Kolter and Tibshirani [2016] {binproceedings}[author] \bauthor\bsnmAli, \bfnmAlnur\binitsA., \bauthor\bsnmKolter, \bfnmZico\binitsZ. and \bauthor\bsnmTibshirani, \bfnmRyan\binitsR. (\byear2016). \btitleThe multiple quantile graphical model. In \bbooktitleAdvances in Neural Information Processing Systems \bpages3747–3755. \endbibitem

- Ando and Bai [2020] {barticle}[author] \bauthor\bsnmAndo, \bfnmTomohiro\binitsT. and \bauthor\bsnmBai, \bfnmJushan\binitsJ. (\byear2020). \bjournalJournal of the American Statistical Association \bvolume115 \bpages266–279. \endbibitem

- Arellano and Bonhomme [2017] {barticle}[author] \bauthor\bsnmArellano, \bfnmManuel\binitsM. and \bauthor\bsnmBonhomme, \bfnmStéphane\binitsS. (\byear2017). \btitleQuantile selection models with an application to understanding changes in wage inequality. \bjournalEconometrica \bvolume85 \bpages1–28. \endbibitem

- Athey et al. [2018] {barticle}[author] \bauthor\bsnmAthey, \bfnmSusan\binitsS., \bauthor\bsnmBayati, \bfnmMohsen\binitsM., \bauthor\bsnmDoudchenko, \bfnmNikolay\binitsN., \bauthor\bsnmImbens, \bfnmGuido\binitsG. and \bauthor\bsnmKhosravi, \bfnmKhashayar\binitsK. (\byear2018). \btitleMatrix completion methods for causal panel data models. \endbibitem

- Bai [2009] {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. (\byear2009). \btitlePanel data models with interactive fixed effects. \bjournalEconometrica \bvolume77 \bpages1229–1279. \endbibitem

- Bai and Feng [2019] {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. and \bauthor\bsnmFeng, \bfnmJunlong\binitsJ. (\byear2019). \btitleRobust Principal Components Analysis with Non-Sparse Errors. \bjournalarXiv preprint arXiv:1902.08735. \endbibitem

- Bai and Li [2012] {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. and \bauthor\bsnmLi, \bfnmKunpeng\binitsK. (\byear2012). \btitleStatistical analysis of factor models of high dimension. \bjournalThe Annals of Statistics \bvolume40 \bpages436–465. \endbibitem

- Bai and Ng [2013] {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. and \bauthor\bsnmNg, \bfnmSerena\binitsS. (\byear2013). \btitlePrincipal components estimation and identification of static factors. \bjournalJournal of Econometrics \bvolume176 \bpages18–29. \endbibitem

- Bai and Ng [2017] {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. and \bauthor\bsnmNg, \bfnmSerena\binitsS. (\byear2017). \btitlePrincipal components and regularized estimation of factor models. \bjournalarXiv preprint arXiv:1708.08137. \endbibitem

- Bai and Ng [2019] {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. and \bauthor\bsnmNg, \bfnmSerena\binitsS. (\byear2019). \btitleMatrix completion, counterfactuals, and factor analysis of missing data. \bjournalarXiv preprint arXiv:1910.06677. \endbibitem

- Belloni and Chernozhukov [2009] {barticle}[author] \bauthor\bsnmBelloni, \bfnmAlexandre\binitsA. and \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV. (\byear2009). \btitleOn the computational complexity of MCMC-based estimators in large samples. \bjournalThe Annals of Statistics \bvolume37 \bpages2011–2055. \endbibitem

- Belloni and Chernozhukov [2011] {barticle}[author] \bauthor\bsnmBelloni, \bfnmAlexandre\binitsA. and \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV. (\byear2011). \btitle-penalized quantile regression in high-dimensional sparse models. \bjournalThe Annals of Statistics \bvolume39 \bpages82–130. \endbibitem

- Bickel, Ritov and Tsybakov [2009] {barticle}[author] \bauthor\bsnmBickel, \bfnmPeter\binitsP., \bauthor\bsnmRitov, \bfnmYa’acov\binitsY. and \bauthor\bsnmTsybakov, \bfnmAlexandre\binitsA. (\byear2009). \btitleSimultaneous analysis of Lasso and Dantzig selector. \bjournalThe Annals of Statistics \bvolume37 \bpages1705–1732. \endbibitem

- Boyd et al. [2011] {barticle}[author] \bauthor\bsnmBoyd, \bfnmStephen\binitsS., \bauthor\bsnmParikh, \bfnmNeal\binitsN., \bauthor\bsnmChu, \bfnmEric\binitsE., \bauthor\bsnmPeleato, \bfnmBorja\binitsB. and \bauthor\bsnmEckstein, \bfnmJonathan\binitsJ. (\byear2011). \btitleDistributed optimization and statistical learning via the alternating direction method of multipliers. \bjournalFoundations and Trends® in Machine learning \bvolume3 \bpages1–122. \endbibitem

- Brahma et al. [2017] {barticle}[author] \bauthor\bsnmBrahma, \bfnmPratik Prabhanjan\binitsP. P., \bauthor\bsnmShe, \bfnmYiyuan\binitsY., \bauthor\bsnmLi, \bfnmShijie\binitsS., \bauthor\bsnmLi, \bfnmJiade\binitsJ. and \bauthor\bsnmWu, \bfnmDapeng\binitsD. (\byear2017). \btitleReinforced robust principal component pursuit. \bjournalIEEE transactions on neural networks and learning systems \bvolume29 \bpages1525–1538. \endbibitem

- Cai, Candès and Shen [2010] {barticle}[author] \bauthor\bsnmCai, \bfnmJian-Feng\binitsJ.-F., \bauthor\bsnmCandès, \bfnmEmmanuel\binitsE. and \bauthor\bsnmShen, \bfnmZuowei\binitsZ. (\byear2010). \btitleA singular value thresholding algorithm for matrix completion. \bjournalSIAM Journal on Optimization \bvolume20 \bpages1956–1982. \endbibitem

- Candès and Plan [2010] {barticle}[author] \bauthor\bsnmCandès, \bfnmEmmanuel\binitsE. and \bauthor\bsnmPlan, \bfnmYaniv\binitsY. (\byear2010). \btitleMatrix completion with noise. \bjournalProceedings of the IEEE \bvolume98 \bpages925–936. \endbibitem

- Candès and Plan [2011] {barticle}[author] \bauthor\bsnmCandès, \bfnmEmmanuel\binitsE. and \bauthor\bsnmPlan, \bfnmYaniv\binitsY. (\byear2011). \btitleTight oracle inequalities for low-rank matrix recovery from a minimal number of noisy random measurements. \bjournalIEEE Transactions on Information Theory \bvolume57 \bpages2342–2359. \endbibitem

- Candès and Recht [2009] {barticle}[author] \bauthor\bsnmCandès, \bfnmEmmanuel\binitsE. and \bauthor\bsnmRecht, \bfnmBenjamin\binitsB. (\byear2009). \btitleExact matrix completion via convex optimization. \bjournalFoundations of Computational mathematics \bvolume9 \bpages717. \endbibitem

- Candès and Tao [2007] {barticle}[author] \bauthor\bsnmCandès, \bfnmEmmanuel\binitsE. and \bauthor\bsnmTao, \bfnmTerence\binitsT. (\byear2007). \btitleThe Dantzig selector: Statistical estimation when p is much larger than n. \bjournalThe annals of Statistics \bvolume35 \bpages2313–2351. \endbibitem

- Chamberlain and Rothschild [1983] {barticle}[author] \bauthor\bsnmChamberlain, \bfnmGary\binitsG. and \bauthor\bsnmRothschild, \bfnmMichael\binitsM. (\byear1983). \btitleARBITRAGE, FACTOR STRUCTURE, AND MEAN-VARIANCE ANALYSIS ON LARGE ASSET MARKETS. \bjournalEconometrica (pre-1986) \bvolume51 \bpages1281. \endbibitem

- Chatterjee [2015] {barticle}[author] \bauthor\bsnmChatterjee, \bfnmSourav\binitsS. (\byear2015). \btitleMatrix estimation by universal singular value thresholding. \bjournalThe Annals of Statistics \bvolume43 \bpages177–214. \endbibitem

- Chen [2014] {barticle}[author] \bauthor\bsnmChen, \bfnmMingli\binitsM. (\byear2014). \btitleEstimation of nonlinear panel models with multiple unobserved effects. \bjournalWarwick Economics Research Paper Series No. 1120. \endbibitem

- Chen, Dolado and Gonzalo [2018] {barticle}[author] \bauthor\bsnmChen, \bfnmLiang\binitsL., \bauthor\bsnmDolado, \bfnmJuan\binitsJ. and \bauthor\bsnmGonzalo, \bfnmJesús\binitsJ. (\byear2018). \btitleQuantile factor models. \endbibitem

- Chen, Fernández-Val and Weidner [2014] {barticle}[author] \bauthor\bsnmChen, \bfnmMingli\binitsM., \bauthor\bsnmFernández-Val, \bfnmIván\binitsI. and \bauthor\bsnmWeidner, \bfnmMartin\binitsM. (\byear2014). \btitleNonlinear panel models with interactive effects. \bjournalarXiv preprint arXiv:1412.5647. \endbibitem

- Chernozhukov, Hansen and Liao [2017] {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmHansen, \bfnmChristian\binitsC. and \bauthor\bsnmLiao, \bfnmYuan\binitsY. (\byear2017). \btitleA lava attack on the recovery of sums of dense and sparse signals. \bjournalThe Annals of Statistics \bvolume45 \bpages39–76. \endbibitem

- Chernozhukov et al. [2018] {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmHansen, \bfnmChristian\binitsC., \bauthor\bsnmLiao, \bfnmYuan\binitsY. and \bauthor\bsnmZhu, \bfnmYinchu\binitsY. (\byear2018). \btitleInference For Heterogeneous Effects Using Low-Rank Estimations. \bjournalarXiv preprint arXiv:1812.08089. \endbibitem

- Cochrane [2009] {bbook}[author] \bauthor\bsnmCochrane, \bfnmJohn H\binitsJ. H. (\byear2009). \btitleAsset pricing: Revised edition. \bpublisherPrinceton university press. \endbibitem

- Cochrane [2011] {barticle}[author] \bauthor\bsnmCochrane, \bfnmJohn H\binitsJ. H. (\byear2011). \btitlePresidential address: Discount rates. \bjournalThe Journal of finance \bvolume66 \bpages1047–1108. \endbibitem

- Connor and Korajczyk [1988] {barticle}[author] \bauthor\bsnmConnor, \bfnmGregory\binitsG. and \bauthor\bsnmKorajczyk, \bfnmRobert A\binitsR. A. (\byear1988). \btitleRisk and return in an equilibrium APT: Application of a new test methodology. \bjournalJournal of financial economics \bvolume21 \bpages255–289. \endbibitem

- Dalalyan, Hebiri and Lederer [2017] {barticle}[author] \bauthor\bsnmDalalyan, \bfnmArnak\binitsA., \bauthor\bsnmHebiri, \bfnmMohamed\binitsM. and \bauthor\bsnmLederer, \bfnmJohannes\binitsJ. (\byear2017). \btitleOn the prediction performance of the lasso. \bjournalBernoulli \bvolume23 \bpages552–581. \endbibitem

- Daniel and Titman [1997] {barticle}[author] \bauthor\bsnmDaniel, \bfnmKent\binitsK. and \bauthor\bsnmTitman, \bfnmSheridan\binitsS. (\byear1997). \btitleEvidence on the characteristics of cross sectional variation in stock returns. \bjournalthe Journal of Finance \bvolume52 \bpages1–33. \endbibitem

- Daniel and Titman [1998] {barticle}[author] \bauthor\bsnmDaniel, \bfnmKent\binitsK. and \bauthor\bsnmTitman, \bfnmSheridan\binitsS. (\byear1998). \btitleCharacteristics or covariances. \bjournalJournal of Portfolio Management \bvolume24 \bpages24–33. \endbibitem

- de Castro and Galvao [2019] {barticle}[author] \bauthor\bparticlede \bsnmCastro, \bfnmLuciano\binitsL. and \bauthor\bsnmGalvao, \bfnmAntonio F\binitsA. F. (\byear2019). \btitleDynamic quantile models of rational behavior. \bjournalEconometrica \bvolume87 \bpages1893–1939. \endbibitem

- Elsener and van de Geer [2018] {barticle}[author] \bauthor\bsnmElsener, \bfnmAndreas\binitsA. and \bauthor\bparticlevan de \bsnmGeer, \bfnmSara\binitsS. (\byear2018). \btitleRobust low-rank matrix estimation. \bjournalThe Annals of Statistics \bvolume46 \bpages3481–3509. \endbibitem

- Fama and French [1993] {barticle}[author] \bauthor\bsnmFama, \bfnmEugene F\binitsE. F. and \bauthor\bsnmFrench, \bfnmKenneth R\binitsK. R. (\byear1993). \btitleCommon risk factors in the returns on stocks and bonds. \bjournalJournal of financial economics \bvolume33 \bpages3–56. \endbibitem

- Fazel [2002] {barticle}[author] \bauthor\bsnmFazel, \bfnmMaryam\binitsM. (\byear2002). \btitleMatrix rank minimization with applications. \endbibitem

- Feng [2019] {barticle}[author] \bauthor\bsnmFeng, \bfnmJunlong\binitsJ. (\byear2019). \btitleRegularized Quantile Regression with Interactive Fixed Effects. \bjournalarXiv preprint arXiv:1911.00166. \endbibitem

- Feng, Giglio and Xiu [2019] {btechreport}[author] \bauthor\bsnmFeng, \bfnmGuanhao\binitsG., \bauthor\bsnmGiglio, \bfnmStefano\binitsS. and \bauthor\bsnmXiu, \bfnmDacheng\binitsD. (\byear2019). \btitleTaming the factor zoo: A test of new factors \btypeTechnical Report, \bpublisherNational Bureau of Economic Research. \endbibitem

- Galvao [2011] {barticle}[author] \bauthor\bsnmGalvao, \bfnmAntonio\binitsA. (\byear2011). \btitleQuantile regression for dynamic panel data with fixed effects. \bjournalJournal of Econometrics \bvolume164 \bpages142–157. \endbibitem

- Galvao and Kato [2016] {barticle}[author] \bauthor\bsnmGalvao, \bfnmAntonio\binitsA. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2016). \btitleSmoothed quantile regression for panel data. \bjournalJournal of econometrics \bvolume193 \bpages92–112. \endbibitem

- Galvao and Montes-Rojas [2010] {barticle}[author] \bauthor\bsnmGalvao, \bfnmAntonio\binitsA. and \bauthor\bsnmMontes-Rojas, \bfnmGabriel V\binitsG. V. (\byear2010). \btitlePenalized quantile regression for dynamic panel data. \bjournalJournal of Statistical Planning and Inference \bvolume140 \bpages3476–3497. \endbibitem

- Giannone, Lenza and Primiceri [2017] {barticle}[author] \bauthor\bsnmGiannone, \bfnmDomenico\binitsD., \bauthor\bsnmLenza, \bfnmMichele\binitsM. and \bauthor\bsnmPrimiceri, \bfnmGiorgio\binitsG. (\byear2017). \btitleEconomic predictions with big data: The illusion of sparsity. \endbibitem

- Giglio and Xiu [2018] {barticle}[author] \bauthor\bsnmGiglio, \bfnmStefano\binitsS. and \bauthor\bsnmXiu, \bfnmDacheng\binitsD. (\byear2018). \btitleAsset pricing with omitted factors. \bjournalChicago Booth Research Paper \bvolume16-21. \endbibitem

- Giovannetti [2013] {barticle}[author] \bauthor\bsnmGiovannetti, \bfnmBruno C\binitsB. C. (\byear2013). \btitleAsset pricing under quantile utility maximization. \bjournalReview of Financial Economics \bvolume22 \bpages169–179. \endbibitem

- Graham et al. [2018] {barticle}[author] \bauthor\bsnmGraham, \bfnmBryan S\binitsB. S., \bauthor\bsnmHahn, \bfnmJinyong\binitsJ., \bauthor\bsnmPoirier, \bfnmAlexandre\binitsA. and \bauthor\bsnmPowell, \bfnmJames L\binitsJ. L. (\byear2018). \btitleA quantile correlated random coefficients panel data model. \bjournalJournal of Econometrics \bvolume206 \bpages305–335. \endbibitem

- Green, Hand and Zhang [2017] {barticle}[author] \bauthor\bsnmGreen, \bfnmJeremiah\binitsJ., \bauthor\bsnmHand, \bfnmJohn\binitsJ. and \bauthor\bsnmZhang, \bfnmFrank\binitsF. (\byear2017). \btitleThe characteristics that provide independent information about average us monthly stock returns. \bjournalThe Review of Financial Studies \bvolume30 \bpages4389–4436. \endbibitem

- Han et al. [2018] {barticle}[author] \bauthor\bsnmHan, \bfnmYufeng\binitsY., \bauthor\bsnmHe, \bfnmAi\binitsA., \bauthor\bsnmRapach, \bfnmDavid\binitsD. and \bauthor\bsnmZhou, \bfnmGuofu\binitsG. (\byear2018). \btitleWhat Firm Characteristics Drive US Stock Returns? \bjournalAvailable at SSRN 3185335. \endbibitem

- He, Wang and Hong [2013] {barticle}[author] \bauthor\bsnmHe, \bfnmXuming\binitsX., \bauthor\bsnmWang, \bfnmLan\binitsL. and \bauthor\bsnmHong, \bfnmHyokyoung Grace\binitsH. G. (\byear2013). \btitleQuantile-adaptive model-free variable screening for high-dimensional heterogeneous data. \bjournalThe Annals of Statistics \bvolume41 \bpages342–369. \endbibitem

- Kato, Galvao Jr and Montes-Rojas [2012] {barticle}[author] \bauthor\bsnmKato, \bfnmKengo\binitsK., \bauthor\bsnmGalvao Jr, \bfnmAntonio F\binitsA. F. and \bauthor\bsnmMontes-Rojas, \bfnmGabriel V\binitsG. V. (\byear2012). \btitleAsymptotics for panel quantile regression models with individual effects. \bjournalJournal of Econometrics \bvolume170 \bpages76–91. \endbibitem

- Koenker [2000] {barticle}[author] \bauthor\bsnmKoenker, \bfnmRoger\binitsR. (\byear2000). \btitleGalton, Edgeworth, Frisch, and prospects for quantile regression in econometrics. \bjournalJournal of Econometrics \bvolume95 \bpages347–374. \endbibitem

- Koenker [2004] {barticle}[author] \bauthor\bsnmKoenker, \bfnmRoger\binitsR. (\byear2004). \btitleQuantile regression for longitudinal data. \bjournalJournal of Multivariate Analysis \bvolume91 \bpages74–89. \endbibitem

- Koenker [2005] {bbook}[author] \bauthor\bsnmKoenker, \bfnmRoger\binitsR. (\byear2005). \btitleQuantile regression. \bpublisherCambridge University Press, \baddressNew York. \endbibitem

- Koenker and Machado [1999] {barticle}[author] \bauthor\bsnmKoenker, \bfnmRoger\binitsR. and \bauthor\bsnmMachado, \bfnmJose AF\binitsJ. A. (\byear1999). \btitleGoodness of fit and related inference processes for quantile regression. \bjournalJournal of the american statistical association \bvolume94 \bpages1296–1310. \endbibitem

- Koenker et al. [2017] {bbook}[author] \bauthor\bsnmKoenker, \bfnmRoger\binitsR., \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmHe, \bfnmXuming\binitsX. and \bauthor\bsnmPeng, \bfnmLimin\binitsL. (\byear2017). \btitleHandbook of quantile regression. \bpublisherCRC press. \endbibitem

- Koltchinskii, Lounici and Tsybakov [2011] {barticle}[author] \bauthor\bsnmKoltchinskii, \bfnmVladimir\binitsV., \bauthor\bsnmLounici, \bfnmKarim\binitsK. and \bauthor\bsnmTsybakov, \bfnmAlexandre\binitsA. (\byear2011). \btitleNuclear-norm penalization and optimal rates for noisy low-rank matrix completion. \bjournalThe Annals of Statistics \bvolume39 \bpages2302–2329. \endbibitem

- Kozak, Nagel and Santosh [2019] {barticle}[author] \bauthor\bsnmKozak, \bfnmSerhiy\binitsS., \bauthor\bsnmNagel, \bfnmStefan\binitsS. and \bauthor\bsnmSantosh, \bfnmShrihari\binitsS. (\byear2019). \btitleShrinking the cross-section. \bjournalJournal of Financial Economics. \endbibitem

- Lamarche [2010] {barticle}[author] \bauthor\bsnmLamarche, \bfnmCarlos\binitsC. (\byear2010). \btitleRobust penalized quantile regression estimation for panel data. \bjournalJournal of Econometrics \bvolume157 \bpages396–408. \endbibitem

- Lettau and Pelger [2018] {btechreport}[author] \bauthor\bsnmLettau, \bfnmMartin\binitsM. and \bauthor\bsnmPelger, \bfnmMarkus\binitsM. (\byear2018). \btitleEstimating latent asset-pricing factors \btypeTechnical Report, \bpublisherNational Bureau of Economic Research. \endbibitem

- Ma, Linton and Gao [2019] {barticle}[author] \bauthor\bsnmMa, \bfnmShujie\binitsS., \bauthor\bsnmLinton, \bfnmOliver\binitsO. and \bauthor\bsnmGao, \bfnmJiti\binitsJ. (\byear2019). \btitleEstimation and inference in semiparametric quantile factor models. \endbibitem

- Manski [1988] {barticle}[author] \bauthor\bsnmManski, \bfnmCharles F\binitsC. F. (\byear1988). \btitleOrdinal utility models of decision making under uncertainty. \bjournalTheory and Decision \bvolume25 \bpages79–104. \endbibitem

- Moon and Weidner [2015] {barticle}[author] \bauthor\bsnmMoon, \bfnmHyungsik Roger\binitsH. R. and \bauthor\bsnmWeidner, \bfnmMartin\binitsM. (\byear2015). \btitleLinear regression for panel with unknown number of factors as interactive fixed effects. \bjournalEconometrica \bvolume83 \bpages1543–1579. \endbibitem

- Moon and Weidner [2018] {barticle}[author] \bauthor\bsnmMoon, \bfnmHyungsik Roger\binitsH. R. and \bauthor\bsnmWeidner, \bfnmMartin\binitsM. (\byear2018). \btitleNuclear norm regularized estimation of panel regression models. \bjournalarXiv preprint arXiv:1810.10987. \endbibitem

- Negahban and Wainwright [2011] {barticle}[author] \bauthor\bsnmNegahban, \bfnmSahand\binitsS. and \bauthor\bsnmWainwright, \bfnmMartin\binitsM. (\byear2011). \btitleEstimation of (near) low-rank matrices with noise and high-dimensional scaling. \bjournalThe Annals of Statistics \bvolume39 \bpages1069–1097. \endbibitem

- Padilla and Chatterjee [2020] {barticle}[author] \bauthor\bsnmPadilla, \bfnmOscar Hernan Madrid\binitsO. H. M. and \bauthor\bsnmChatterjee, \bfnmSabyasachi\binitsS. (\byear2020). \btitleRisk Bounds for Quantile Trend Filtering. \bjournalarXiv preprint arXiv:2007.07472. \endbibitem

- Recht, Fazel and Parrilo [2010] {barticle}[author] \bauthor\bsnmRecht, \bfnmBenjamin\binitsB., \bauthor\bsnmFazel, \bfnmMaryam\binitsM. and \bauthor\bsnmParrilo, \bfnmPablo\binitsP. (\byear2010). \btitleGuaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization. \bjournalSIAM review \bvolume52 \bpages471–501. \endbibitem

- Rigollet and Hütter [2015] {barticle}[author] \bauthor\bsnmRigollet, \bfnmPhillippe\binitsP. and \bauthor\bsnmHütter, \bfnmJan-Christian\binitsJ.-C. (\byear2015). \btitleHigh dimensional statistics. \bjournalLecture notes for course 18S997. \endbibitem

- Rohde and Tsybakov [2011] {barticle}[author] \bauthor\bsnmRohde, \bfnmAngelika\binitsA. and \bauthor\bsnmTsybakov, \bfnmAlexandre\binitsA. (\byear2011). \btitleEstimation of high-dimensional low-rank matrices. \bjournalThe Annals of Statistics \bvolume39 \bpages887–930. \endbibitem

- Ross [1976] {barticle}[author] \bauthor\bsnmRoss, \bfnmStephen\binitsS. (\byear1976). \btitleThe arbitrage theory of capital asset pricing. \bjournalJournal of Economic Theory \bvolume13 \bpages341–360. \endbibitem

- Rostek [2010] {barticle}[author] \bauthor\bsnmRostek, \bfnmMarzena\binitsM. (\byear2010). \btitleQuantile maximization in decision theory. \bjournalThe Review of Economic Studies \bvolume77 \bpages339–371. \endbibitem

- Sagner [2019] {bphdthesis}[author] \bauthor\bsnmSagner, \bfnmAndrés G\binitsA. G. (\byear2019). \btitleThree essays on quantile factor analysis, \btypePhD thesis, \bpublisherBoston University. \endbibitem

- She and Chen [2017] {barticle}[author] \bauthor\bsnmShe, \bfnmYiyuan\binitsY. and \bauthor\bsnmChen, \bfnmKun\binitsK. (\byear2017). \btitleRobust reduced-rank regression. \bjournalBiometrika \bvolume104 \bpages633–647. \endbibitem

- Tibshirani [1996] {barticle}[author] \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear1996). \btitleRegression shrinkage and selection via the lasso. \bjournalJournal of the Royal Statistical Society: Series B (Methodological) \bvolume58 \bpages267–288. \endbibitem

- van der Vaart and Wellner [1996] {bbook}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmAad W.\binitsA. W. and \bauthor\bsnmWellner, \bfnmJon A\binitsJ. A. (\byear1996). \btitleWeak convergence and empirical processes: with applications to statistics. \bpublisherSpringer. \endbibitem

- Vu [2007] {barticle}[author] \bauthor\bsnmVu, \bfnmVan\binitsV. (\byear2007). \btitleSpectral norm of random matrices. \bjournalCombinatorica \bvolume27 \bpages721–736. \endbibitem

- Wang, Wu and Li [2012] {barticle}[author] \bauthor\bsnmWang, \bfnmLan\binitsL., \bauthor\bsnmWu, \bfnmYichao\binitsY. and \bauthor\bsnmLi, \bfnmRunze\binitsR. (\byear2012). \btitleQuantile regression for analyzing heterogeneity in ultra-high dimension. \bjournalJournal of the American Statistical Association \bvolume107 \bpages214–222. \endbibitem

- Wong, Li and Tewari [2020] {barticle}[author] \bauthor\bsnmWong, \bfnmKam Chung\binitsK. C., \bauthor\bsnmLi, \bfnmZifan\binitsZ. and \bauthor\bsnmTewari, \bfnmAmbuj\binitsA. (\byear2020). \btitleLasso guarantees for -mixing heavy-tailed time series. \bjournalThe Annals of Statistics \bvolume48 \bpages1124–1142. \endbibitem

- Wu and Yin [2015] {barticle}[author] \bauthor\bsnmWu, \bfnmYuanshan\binitsY. and \bauthor\bsnmYin, \bfnmGuosheng\binitsG. (\byear2015). \btitleConditional quantile screening in ultrahigh-dimensional heterogeneous data. \bjournalBiometrika \bvolume102 \bpages65–76. \endbibitem

- Yu [1994] {barticle}[author] \bauthor\bsnmYu, \bfnmBin\binitsB. (\byear1994). \btitleRates of convergence for empirical processes of stationary mixing sequences. \bjournalThe Annals of Probability \bpages94–116. \endbibitem

- Yu, Wang and Samworth [2014] {barticle}[author] \bauthor\bsnmYu, \bfnmYi\binitsY., \bauthor\bsnmWang, \bfnmTengyao\binitsT. and \bauthor\bsnmSamworth, \bfnmRichard J\binitsR. J. (\byear2014). \btitleA useful variant of the Davis–Kahan theorem for statisticians. \bjournalBiometrika \bvolume102 \bpages315–323. \endbibitem

- Zheng, Peng and He [2015] {barticle}[author] \bauthor\bsnmZheng, \bfnmQi\binitsQ., \bauthor\bsnmPeng, \bfnmLimin\binitsL. and \bauthor\bsnmHe, \bfnmXuming\binitsX. (\byear2015). \btitleGlobally adaptive quantile regression with ultra-high dimensional data. \bjournalAnnals of statistics \bvolume43 \bpages2225. \endbibitem

Alexandre Belloni, Mingli Chen, Oscar Hernan Madrid Padilla, Zixuan (Kevin) Wang

S1 Implementation Details of the Proposed ADMM Algorithm

Denoting by and the element-wise positive and negative part operators, the ADMM proceeds doing the iterative updates

| (S1) | ||||

| (S2) | ||||

| (S3) | ||||

| (S4) | ||||

| (S5) | ||||

| (S6) |

where is the penalty, see [15].

The update for is

where

The update for is

where

Furthermore, for ,

Finally, defining

the remaining updates are

and

S1.1 Estimation without Covariates

Note, when there are no covariates, our proposed ADMM can be simplified. In this case, we face the following problem

| (S7) |