Stochastic proximal splitting algorithm for composite minimization

Abstract

Supported by the recent contributions in multiple branches, the first-order splitting algorithms became central for structured nonsmooth optimization. In the large-scale or noisy contexts, when only stochastic information on the objective function is available, the extension of proximal gradient schemes to stochastic oracles is heavily based on the tractability of the proximal operator corresponding to nonsmooth component, which has been deeply analyzed in the literature. However, there remained some questions about the difficulty of the composite models where the nonsmooth term is not proximally tractable anymore. Therefore, in this paper we tackle composite optimization problems, where the access only to stochastic information on both smooth and nonsmooth components is assumed, using a stochastic proximal first-order scheme with stochastic proximal updates. We provide sublinear convergence rates (in expectation of squared distance to the optimal set) under the strong convexity assumption on the objective function. Also, linear convergence is achieved for convex feasibility problems. The empirical behavior is illustrated by numerical tests on parametric sparse representation models.

1 Introduction

In this paper we consider the following convex composite optimization problem:

where is the smooth component and is a proper, convex, lower-semicontinuous function. In literature, many applications from statistics RosVil:14 or signal processing often motivate noisy contexts allowing access only to stochastic first order information on smooth function , having regularizer as a typical proximally-tractable convex function. By proximally-tractable we mean that the proximal map of a given function is computable in closed form or, at most, in linear time. Therefore, in these situations the following stochastic model

where is a random variable, express better the previous real assumptions. However, the recent dimensionality inflation of machine learning HaLes:15 ; ZhoKwo:14 ; ShiLin:15 and signal processing StoIro:19 ; ShiLin:15 models gave birth to optimization problems with complicated regularizers or complicated many constraints. As practical examples we recall: parametric sparse represention StoIro:19 , group lasso ZhoKwo:14 ; ShiLin:15 ; HaLes:15 , CUR-like factorization WanWan:17 , graph trend filtering SalBia:17 ; VarLee:19 , dictionary learning YanEla:16 ; StoIro:19 . Motivated by all these models, in this paper instead of assuming proximal-tractable regularizer , we consider that is expressed as an expectation of stochastic proximally-tractable components (i.e. ). Thus we focus on the following model:

| (1) |

where is a random variable associated with probability space . Functions are smooth with Lipschitz gradients and are proper convex and lower-semicontinuous, is the expectation over respective random variable. In general, many existing primal schemes encounter computational difficulties when a large (possibly infinite) number of constraints are present, since they are based on full projections onto complicated feasible set.

Contributions. We analyze a stochastic first-order splitting scheme relying on stochastic gradients and stochastic proximal updates, which naturally generalize the widely known Stochastic Gradient Descent (SGD) and Stochastic Proximal Point (SPP) algorithms toward composite models with untractable regularizations; we provide iteration complexity estimates which were previously unknown for this type of schemes. In particular, for convex feasibility problems, the analysis yields naturally linear convergence rates.

We briefly recall further the milestone results from stochastic optimization literature with focus on the complexity of stochastic first-order methods.

1.1 Previous work

Great attention has been given in the last decade to the behaviour of stochastic first order schemes, with special focus in stochastic gradient descent (SGD), on a variety of models under different convexity properties, see NemJud:09 ; MouBac:11 ; ShaSin:11 ; NguNgu:18 ; RosVil:14 ; Ned:10 ; Ned:11 . Since the analysis of SGD naturally require a typical smoothness, appropriate extensions are necessary to attack nonsmooth models. These extensions are embodied by the stochastic proximal point (SPP) algorithm, which has been recently analyzed using various differentiability assumptions, see TouTra:16 ; RyuBoy:16 ; Bia:16 ; PatNec:18 ; KosNed:13 ; WanBer:16 ; AsiDuc:18 and has shown surprinsing analytical and empirical performances. In TouTra:16 is considered the typical stochastic learning model involving the expectation of random particular components defined by the composition of a smooth function and a linear operator, i.e.: where . Their complexity analysis requires smoothness and strong convexity to obtain in the quadratic mean and an convergence rate, using vanishing stepsize. The generalization of these convergence guarantees is undertaken in PatNec:18 , where no linear composition structure is required and an (in)finite number of constraints are included in the stochastic model, i.e. . However, the analysis of PatNec:18 requires strong convexity and Lipschitz gradient continuity for each functional component . Note that our analysis surpasses this restriction and provides a natural generalization of PatNec:18 to nonsmooth composite models. Further, in Bia:16 a general asymptotic convergence analysis of slightly modified SPP scheme has been provided, under mild convexity assumptions on a finitely constrained stochastic problem. In WanBer:16 similar SPP algorithms are developed, which are also tailored for complicated feasible sets. The authors focus on mild convex models deriving optimal rates. Recently, in AsiDuc:18 , the authors analyze SPP schemes for stochastic models with ”shared minimizers” obtaining linear convergence results, for variable stepsize SPP. Also, without shared minimizers assumption, they obtain for SPP in convex Lipschitz continuous case and, furthermore, in strongly convex case.

Splitting first-order schemes received significantly attention due to their natural insight and simplicity in contexts when a sum of two components are minimized (see Nes:13 ; BecTeb:09 ). However, when the information access is limited only to stochastic samples of the two components, extending the existing guarantees is not straightforward. Notice that overall, on one hand, SPP avoids any splitting in composite models by treating the constrained smooth problems as black box expectations (see TouTra:16 ; PatNec:18 ; AsiDuc:18 ). On the other hand, until recently the composite nonsmooth models assumed proximal-tractable in order to extend proof arguments of the results related to stochastic smooth optimization RosVil:14 . Therefore, only recently the full stochastic composite models with stochastic regularizers have been properly tackled SalBia:17 , where almost sure asymptotic convergence is established for a stochastic splitting scheme, where each iteration represents a typical proximal gradient update with respect to stochastic samples of and . In our paper we analyze the nonasymptotic behaviour of this scheme and point the relations with other algorithms from the literature.

The stochastic splitting schemes are also related to the model-based methods developed in DavDru:19 . Here, the authors developed a unified algorithmic framework, which generates stochastic algorithms, for different models arising in learning applications. They assume their composite objective function to be the sum of a (weakly convex) stochastic component with bounded gradients and simple (proximally tractable) convex regularization. Although their framework is algorithmically more general, our analysis avoid these boundedness assumptions, allows objectives with a component having Lipschitz continuous gradient and do not require proximal tractability on regularizations.

Notations. We use notation . For denote the scalar product and Euclidean norm by . The projection operator onto set is denoted by and the distance from to the set is denoted . The indicator function of a set is denoted: . We use notations for the subdifferential set and for a subgradient of at . In differentiable case, is the gradient of component . Finally, we use for (conditional) expectation operator.

1.2 Preliminaries

We denote the set of optimal solutions with and any optimal point for (1).

Assumption 1.1

The objective function of our main problem (1) satisfies:

The function has -Lipschitz gradient, i.e. there exists such that:

and is strongly convex, i.e. there exists satisfying:

| (2) |

There exists subgradient mappings such that and

has bounded gradients on the optimal set: there exists such that for all .

For any there exists bounded subgradients such that and . Moreover, for simplicity, we assume throughout the paper .

The first part of the above assumption is natural in the stochastic optimization problems. The Assumption guarantee the existence of a subgradient mapping. The third part Assumption is standard in the literature related to proximal stochastic algorithms. Notice that most stochastic subgradient algorithms require bounded gradients on the entire domain MouBac:11 ; NemJud:09 ; NguNgu:18 , which is more restrictive than condition . The assumption needs a more consistent discussion, detailed in Pat:20 . However, for completeness we include it in the remark below.

Remark 1

Denote the set . In general, for convex functions it can be easily shown for all (see RocWet:82 ). However, is guaranteed by the stronger equality:

| (3) |

Discrete case. Let us consider finite discrete domains . Then (Roc:70, , Theorem 23.8) guarantees that the finite sum objective function from (1) satisfy (3) if . The can be further relaxed to for polyhedral components. In particular, let be finitely many closed convex satisfying qualification condition: , then also (3) holds, i.e. (see ( by (Roc:70, , Corrolary 23.8.1))). Again, can be relaxed to the set itself for polyhedral sets. As pointed by BauBor:99 , the (bounded) linear regularity property of implies the intersection qualification condition.

Under support of these arguments, observe that can be easily checked for most finite-sum examples arisen in convex learning problems.

Continuous case. In the nondiscrete case, sufficient conditions for (3) are discussed in RocWet:82 . Based on the arguments from RocWet:82 , an assumption equivalent to is considered in SalBia:17 under the name of integrable representation of (definition in (SalBia:17, , Section B)). On short, if is normal convex integrand with full domain then admits an integrable representation , and implicitly holds.

We mention that deriving a more complicated result similar to Lemma 3 we could avoid assumption . However, since facilitates the simplicity and naturality of our results and while our target applications are not excluded, we assume throughout the paper that holds.

Let closed convex sets and , then a favorable ”conditioning” property for most projection methods is the linear regularity property: there exists such that

| (4) |

Given some smoothing parameter , define Moreau envelope of and the prox operator as follows:

The approximate inherits the same convexity properties of and additionally has Lipschitz continuous gradient with constant , see RocWet:98 . In particular, when the prox operator becomes the projection operator .

2 Stochastic Splitting Proximal Gradient Algorithm

In the following section we present the Stochastic Splitting Proximal Gradient (SSPG) algorithm and analyze its nonasymptotic convergence towards the optimal set of the original problem (1). The asymptotic convergence of vanishing stepsize SSPG have been analyzed in SalBia:17 .

Let be a starting point and be a nonincreasing positive sequence of stepsizes.

Stochastic Splitting Proximal Gradient algorithm (SSPG): For compute

1. Choose randomly w.r.t. probability distribution

2. Update:

3. If the stoppping criterion holds, then STOP, otherwise .

The SSPG iteration is mainly a Stochastic Proximal Gradient iteration based on stochastic proximal maps SalBia:17 . Thus, the first step of algorithm SSPG consists of a varying-stepsize (vanilla) stochastic gradient update, while the second step rely on a stochastic proximal update, or equivalently a gradient step in the direction of the randomly sampled gradient of expected Moreau envelope . Further results will state that a diminishing stepsize is an appropriate choice to obtain convergence in expectation. By varying our central model, this general SSPG scheme recovers several well-known stochastic first order algorithms.

In the smooth case (), SSPG reduces to vanilla SGD MouBac:11 :

By considering proximal-tractable regularizers (i.e. ) or simple convex sets (i.e. , with computable in closed form), then we recover Proximal (or Projected, respectively) SGD RosVil:14 :

For nonsmooth objective functions, when , SSPG is equivalent with SPP iteration PatNec:18 ; AsiDuc:18 ; TouTra:16 :

For CFPs, i.e. , the SSPG iteration is simplified since and . Thus it recovers Randomized Alternating Projections scheme BauDeu:03 :

Therefore, the below results will implicitly represent unifying convergence rates for these algorithms, under stated assumptions.

3 Iteration complexity in expectation

In this section we assume that the function is strongly convex and derive convergence rates for this particular case. We recall a few elementary inequalities that will be used in our proofs. The proof of the following lemma can be found in Nes:04 .

A second elementary bound the we will use is: let and , then

| (5) |

We denote the history of index choices by .

Lemma 2

Let Assumption 1.1 hold and . Then the sequence generated by SSPG satisfies:

Proof

First notice that from the optimality conditions of the subproblem , the following relation holds:

| (6) |

Further we obtain the main recurrence:

| (7) | |||

By using in (7) the stepsize bound and Lemma 1, we obtain:

Further we take expectation w.r.t. in both sides and use the strong convexity property (2) (with and ) to finally derive the following:

Finally, by taking full expectation , over the entire index history, we obtain the above result.

Further we present some lower bounds on the second term from the right hand side, which will allow the synthesis of general complexity estimates over stochastic and deterministic contexts.

Lemma 3

Given , let Assumption 1.1 hold. Then satisfies the following relations: given

-

-

Let be convex sets satisfying linear regularity with constant , such that . Also let , then

Proof

In order to prove let and , by convexity of we have:

| (8) |

On one hand, based on Assumption 1.1 , we observe that the first term of the right hand side has null expectation:

| (9) |

On the other hand, for any , the second term can be lower bounded by (5):

| (10) |

We take full expectation (over the entire index history) in (8) and use relations (3)-(10) to get the first part .

To derive the second part , we proceed slightly different:

| (11) |

We proceed to bound each term of right hand side, similarly as in . By using the optimality condition (i.e. for all ), the expectation of the first term can be lower bounded as follows:

| (12) |

where in the second inequality we used Cauchy-Schwartz inequality and in the last one we used . After taking full expectation in (11) and using (5), (12) and the linear regularity property yields the following:

In the last inequality we also used (5).

Next we present the main recurrences which will finally generate our nonasymptotic convergence rates.

Theorem 3.1

Let Assumptions 1.1 hold, then the SSPG sequence satisfies:

-

Let for all , then:

where .

-

In particular, let such that are linearly regular sets with constant . Then the following recurrence holds:

where .

Remark 2

The above recurrences generates immediately the following convergence rates.

Corollary 3.2

Under Assumption 1.1, the following convergence rates hold:

Moreover, consider convex feasibility problem where , with linearly regular sets and constant stepsize . Then the SSPG sequence converges linearly as follows:

Proof

The proof for the first two results and follows similar lines with (PatNec:18, , Corrolary 15). However, for completeness we present it in appendix.

Remark 3

Although sublinear convergence rates for strongly convex objectives are typically obtained in literature for many first-order stochastic schemes MouBac:11 ; PatNec:18 , these rates are novel due to their generalization potential.

Regarding second rate , although it expresses a geometric decrease of the initial residual term, this rate states that, after iterations, the sequence will remain (in expectation) in a bounded neighborhood of the optimal point . This fact suggests that only sufficiently small constant stepsizes guarantee the convergence of SSPG sequence.

In the convex feasibility setting, SSPG reduces to Randomized Alternating Projections algorithm for which the obtained linear rate obeys the rates from the literature up to a constant. However, we believe that using some refinements of proof arguments there might be obtained optimal rates w.r.t. the constants.

4 Application to Parametric Sparse Representation

Sparse representation Ela:10 starts with the given signal and aims to find the sparse signal by projecting to a much smaller subspace through the overcomplete dictionary . Among the many Dictionary Learning techniques, we focus on the multi-parametric cosparse model proposed in StoIro:19 , since it could efficiently illustrates the empirical capabilities of SSPG. The multi-parametric cosparse representation problem is given by:

| (14) | ||||||

| s.t. |

where and correspond to the dictionary and, respectively, the resulting sparse representation, with sparsity being imposed on a scaled subspace with . In pursuit of (1), we move to the exact penalty problem . In order to limit the solution norm we further regularize the unconstrained objective using an term as follows:

| (15) |

The decomposition which puts the above formulation into model (1) consists of:

| (16) |

where represents line of matrix , and

| (17) |

To compute the SSPG iteration for the sparse representation problem, we note that the proximal operator is given by

Also, the gradient of the smooth function is given by

and with that we are ready to formulate the resulting particular variant of SSPG.

SSPG - Sparse Representation (SSPG-SR): For compute

1. Choose randomly w.r.t. probability distribution

2. Update:

3. If the stopping criterion holds, then STOP, otherwise .

We use randomly generated data with a standard normal distribution. 111Data generating code available at https://github.com/pirofti/SSPG In the following we present numerical simulations that show-case the application of SSPG to the multi-parametric sparse representation problem and compare it to CVX and Proximal Gradient method (denoted rox }) \cite{Nes:13}. Notice that at each iteration Proximal Gradient method requires, given current oint , the computation of:

-

•

gradient

-

•

proximal update

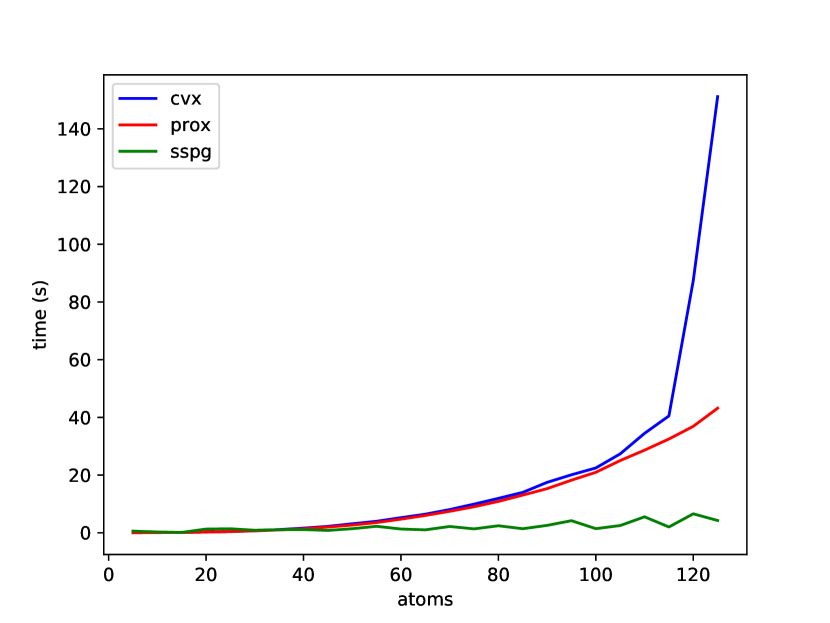

Our first experiment investigates the impact of the problem size on execution time. We vary the atoms in the dictionary starting from up to in increments of 5 and maintain a ratio of 4 features per atom such that . First CVX is used to determine within a margin. Then Proximal Gradient method and SSPG-SR are executed until is reached with the same approximation error. Figure 1 depicts the results. The experiment is stopped after when CVX execution times become too large. We can clearly see a similar yet gentler increasing trend for Proximal Gradient method (prox) and indeed other experiments have shown it to reach an impas shortly after. SSPG-SR on the other hand maintains a steady pace throughout the tests.

Next, we focus on the iterations of Proximal Gradient method and SSGP-SR. To this end we design a similar experiment consisting of 4 tests where we vary the problem size by increasing the number of features with a ratio of 6 features per atom (). As before, we use CVX to determine with . With identical parameters and initialization we execute 10 rounds of SSPG-SR and compare them to the Proximal Gradient method iterations. We time the execution of each iteration and record its progress . The result is shown in Figure 2. In all 4 panels it is clearly seen that the 10 SSPG-SR rounds perform much faster than Proximal Gradient method at least in a first phase. Further increases of the problem dimension lead to a stall in Proximal Gradient method. While SSPG-SR reaches a solution in less than a second in all the tests, Proximal Gradient method goes from 5 seconds in the first, to 9, 24 and 50 in the last. We note that even though the stopping criterion was the same for both methods (, Proximal Gradient method gets us much closer to because, in our parameter setting, the SR problem is well-conditioned.

5 Conclusion

In this paper we presented preliminary guarantees for stochastic gradient schemes with stochastic proximal updates, which unify some well-known schemes in the literature. For future work, would be interesting to analyze convergence rate on (non)convex functions satisfying more relaxed convexity conditions (i.e. quadratic growth) and the empirical behaviour of SSPG scheme under various stepsize choices.

References

- [1] Hilal Asi and John C Duchi. Stochastic (approximate) proximal point methods: Convergence, optimality, and adaptivity. SIAM Journal on Optimization, 29(3):2257–2290, 2019.

- [2] Heinz Bauschke, Frank Deutsch, Hein Hundal, and Sung-Ho Park. Accelerating the convergence of the method of alternating projections. Transactions of the American Mathematical Society, 355(9):3433–3461, 2003.

- [3] Heinz H Bauschke, Jonathan M Borwein, and Wu Li. Strong conical hull intersection property, bounded linear regularity, jameson’s property (g), and error bounds in convex optimization. Mathematical Programming, 86(1):135–160, 1999.

- [4] Amir Beck and Marc Teboulle. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM journal on imaging sciences, 2(1):183–202, 2009.

- [5] Pascal Bianchi. Ergodic convergence of a stochastic proximal point algorithm. SIAM Journal on Optimization, 26(4):2235–2260, 2016.

- [6] Damek Davis and Dmitriy Drusvyatskiy. Stochastic model-based minimization of weakly convex functions. SIAM Journal on Optimization, 29(1):207–239, 2019.

- [7] Michael Elad. Sparse and redundant representations: from theory to applications in signal and image processing. Springer Science & Business Media, 2010.

- [8] David Hallac, Jure Leskovec, and Stephen Boyd. Network lasso: Clustering and optimization in large graphs. In Proceedings of the 21th ACM SIGKDD international conference on knowledge discovery and data mining, pages 387–396, 2015.

- [9] Jayash Koshal, Angelia Nedic, and Uday V Shanbhag. Regularized iterative stochastic approximation methods for stochastic variational inequality problems. IEEE Transactions on Automatic Control, 58(3):594–609, 2012.

- [10] Eric Moulines and Francis R Bach. Non-asymptotic analysis of stochastic approximation algorithms for machine learning. In Advances in Neural Information Processing Systems, pages 451–459, 2011.

- [11] Angelia Nedić. Random projection algorithms for convex set intersection problems. In 49th IEEE Conference on Decision and Control (CDC), pages 7655–7660. IEEE, 2010.

- [12] Angelia Nedić. Random algorithms for convex minimization problems. Mathematical programming, 129(2):225–253, 2011.

- [13] Arkadi Nemirovski, Anatoli Juditsky, Guanghui Lan, and Alexander Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on optimization, 19(4):1574–1609, 2009.

- [14] Yu Nesterov. Gradient methods for minimizing composite functions. Mathematical Programming, 140(1):125–161, 2013.

- [15] Yurii Nesterov. Introductory lectures on convex optimization: A basic course, volume 87. Springer Science & Business Media, 2013.

- [16] Lam M Nguyen, Phuong Ha Nguyen, Marten van Dijk, Peter Richtárik, Katya Scheinberg, and Martin Takáč. Sgd and hogwild! convergence without the bounded gradients assumption. arXiv preprint arXiv:1802.03801, 2018.

- [17] Andrei Pătraşcu. New nonasymptotic convergence rates of stochastic proximal point algorithm for stochastic convex optimization. Optimization, pages 1–29, 2020.

- [18] Andrei Patrascu and Ion Necoara. Nonasymptotic convergence of stochastic proximal point methods for constrained convex optimization. The Journal of Machine Learning Research, 18(1):7204–7245, 2017.

- [19] R Tyrrell Rockafellar and Roger J-B Wets. Variational analysis, volume 317. Springer Science & Business Media, 2009.

- [20] R.T. Rockafellar. Convex Analysis. Princeton University Press, Princeton, New Jersey, 1988.

- [21] R.T. Rockafellar and R.J.-B. Wets. On the interchange of subdifferentiation and conditional expectation for convex functionals. Stochastics, 7(1):173–182, 1982.

- [22] Lorenzo Rosasco, Silvia Villa, and Bang Công Vũ. Convergence of stochastic proximal gradient algorithm. Applied Mathematics & Optimization, pages 1–27, 2019.

- [23] Ernest K Ryu and Stephen Boyd. Stochastic proximal iteration: a non-asymptotic improvement upon stochastic gradient descent. Author website, early draft, 2016.

- [24] Adil Salim, Pascal Bianchi, and Walid Hachem. Snake: a stochastic proximal gradient algorithm for regularized problems over large graphs. IEEE Transactions on Automatic Control, 64(5):1832–1847, 2019.

- [25] Shai Shalev-Shwartz, Yoram Singer, Nathan Srebro, and Andrew Cotter. Pegasos: Primal estimated sub-gradient solver for svm. Mathematical programming, 127(1):3–30, 2011.

- [26] Wei Shi, Qing Ling, Gang Wu, and Wotao Yin. A proximal gradient algorithm for decentralized composite optimization. IEEE Transactions on Signal Processing, 63(22):6013–6023, 2015.

- [27] Florin Stoican and Paul Irofti. Aiding dictionary learning through multi-parametric sparse representation. Algorithms, 12(7):131, 2019.

- [28] Panos Toulis, Dustin Tran, and Edo Airoldi. Towards stability and optimality in stochastic gradient descent. In Artificial Intelligence and Statistics, pages 1290–1298, 2016.

- [29] Rohan Varma, Harlin Lee, Jelena Kovacevic, and Yuejie Chi. Vector-valued graph trend filtering with non-convex penalties. IEEE Transactions on Signal and Information Processing over Networks, 2019.

- [30] Mengdi Wang and Dimitri P Bertsekas. Stochastic first-order methods with random constraint projection. SIAM Journal on Optimization, 26(1):681–717, 2016.

- [31] Xiao Wang, Shuxiong Wang, and Hongchao Zhang. Inexact proximal stochastic gradient method for convex composite optimization. Computational Optimization and Applications, 68(3):579–618, 2017.

- [32] Yael Yankelevsky and Michael Elad. Dual graph regularized dictionary learning. IEEE Transactions on Signal and Information Processing over Networks, 2(4):611–624, 2016.

- [33] Wenliang Zhong and James Kwok. Accelerated stochastic gradient method for composite regularization. In Artificial Intelligence and Statistics, pages 1086–1094, 2014.

6 Appendix

Proof (of Corollary 3.2)

For simplicity denote , then Theorem 3.1 implies that:

By using the Bernoulli inequality for , then we have:

| (18) |

On the other hand, if we use the lower bound

| (19) |

then we can finally derive:

By denoting the second constant , then the last relation implies the following bound:

Denote . To derive an explicit convergence rate order we analyze upper bounds on function .

First assume that . This implies that and that:

| (20) |

On the other hand, by using the inequality for all , we obtain:

Therefore, in this case, the overall rate will be given by:

If , then the definition of provides that:

When , it is obvious that and therefore the order of the convergence rate changes into:

Lastly, if , by using we obtain the second part of our result.