Mean-shift least squares model averaging

Abstract

This paper proposes a new estimator for selecting weights to average over least squares estimates obtained from a set of models. Our proposed estimator builds on the Mallows model average (MMA) estimator of Hansen (2007), but, unlike MMA, simultaneously controls for location bias and regression error through a common constant. We show that our proposed estimator– the mean-shift Mallows model average (MSA) estimator– is asymptotically optimal to the original MMA estimator in terms of mean squared error. A simulation study is presented, where we show that our proposed estimator uniformly outperforms the MMA estimator.

Keywords: Model averaging, Mallows criterion, series estimators, optimality.

1 Introduction

The goal of model averaging, where several models are averaged over, is to reduce estimation variance while controlling for bias arising from omitted variables (regression error). Hansen (2007) proposed the Mallows model averaging (MMA) estimator, which is shown to be asymptotically optimal with regard to the fitted estimates achieving the minimum squared error in a class of discrete model averaging estimators. However, while linear averaging (including MMA) can minimize regression error, it cannot simultaneously reduce regression error and location bias; the bias arising from non-zero expectation in the misspecification bias. In this paper, we propose a novel model averaging estimator that controls for location bias while reducing regression error. We call this new estimator the mean-shift Mallows model averaging (MSA) estimator. We relax the condition of discrete estimators to continuous estimators, similar to that of Wan et al. (2010), though under weaker conditions. We show that the proposed MSA estimator is asymptotically optimal to the MMA estimator.

Model averaging (or forecast combination/ensemble learning) has been a staple and necessary tool in the field of econometrics, statistics, and machine learning. Since the seminar paper by Bates and Granger (1969), the potency of model averaging has been proven over multiple applications and contexts. Recently, the field has received a surge of interest across many disciplines due to an increase in usage and availability of full forecast densities arising from more complex models. In the statistical literature, there is a large literature on model averaging, particularly for Bayesian methods. For example, Bayesian model averaging (BMA: Raftery et al. 1997; Hoeting et al. 1999) has become standard for Bayesians dealing with model uncertainty. In machine learning, ensemble methods, including bagging (Breiman 1996), boosting (Schapire 2003), and stacking (Džeroski and Ženko 2004), which are all linear model averaging (often equal weight), have been used extensively to alleviate overfitting. In econometrics, increased usage in density forecasts has stimulated the field for more advanced strategies for model combination (e.g. Terui and van Dijk 2002; Hall and Mitchell 2007; Amisano and Giacomini 2007; Hoogerheide et al. 2010; Kascha and Ravazzolo 2010; Geweke and Amisano 2011, 2012; Billio et al. 2012, 2013; Aastveit et al. 2014; Kapetanios et al. 2015; Pettenuzzo and Ravazzolo 2016; Negro et al. 2016; Yao et al. 2018; Aastveit et al. 2018a, b), with success in applications across many subdisciplines of economics.

While practical success of model averaging is abundant, theoretical considerations, in particular with regard to estimation of averaging weights, have been somewhat limiting. In terms of theoretical results for averaging models over model selection, Bates and Granger (1969) show that a combination of two forecasts can yield improved forecasts over the two individual forecasts, in terms of mean squared forecast error. In the machine learning literature, Louppe (2014) show that, for averaging regression trees (i.e. random forests), ensemble learning lowers variance while maintaining bias. In the Bayesian literature, when the true model is nested in the candidate models (-closed, as it is referred, following Bernardo and Smith 2009), BMA is known to asymptotically converge to the true model. However, under an -open setting, where the true model is not nested, BMA tends to converge to the “wrong” model, which is often not even the “best” model.

In terms of estimating the weights for model averaging, Hansen (2007) showed that minimizing the Mallows criterion is asymptotically optimal in a class of discrete model average estimators in terms of mean squared error. Wan et al. (2010) relaxes this assumption of discrete estimators to continuous estimators, and show that the optimality holds. Further theoretical results are developed for more complex settings (see, e.g., Hansen and Racine 2012; Zhang et al. 2013). While the MMA estimator is optimal for model averaging, it cannot simultaneously minimize the bias arising from omitted variables and location bias, due to its limited parameter dimension.

Building on the MMA estimator in Hansen (2007), we propose a new model averaging estimator that controls for both biases: the mean-shift Mallows model averaging estimator (MSA). Our main contribution is to show that our proposed MSA estimator is asymptotically optimal to the MMA estimator, achieving lower risk. While our MSA estimator is frequentist by nature, our motivation is, nonetheless, Bayesian. In particular, our development is inspired by the recent practical and theoretical success of Bayesian predictive synthesis (BPS); a coherent Bayesian framework to combine information– in particular, density forecasts– from multiple sources (see, e.g., McAlinn and West 2019; McAlinn et al. 2019; Takanashi and McAlinn 2019). Part of the success of BPS is in considering forecasts as “data” to be used in prior-posterior updating, treating them as latent factors. The flexibility of this framework, of which MMA is a special case, has lead to development of more elaborate model averaging approaches. One of which is to control for location bias arising from misspecification by incorporating a common constant, which shifts the mean to counteract the bias. This idea is central to our proposed MSA estimator.

2 Model averaging under misspecification

Let and be a countably infinite vector. The data generating process (DGP: following Hansen 2007) is

| (1) |

Note that the linearity of the DGP is not restrictive, as it includes series expansions. Consider each model, uses the first elements of , where , to construct an approximating model. This implies that the models are ordered, though this is not problematic when there are series expansions.

The misspecification bias (regression error) is

| (2) |

which is the component in the DGP that is never captured by any of the models, thus, under this setup, all models are misspecified. The predictive mean is,

| (3) |

where is the projection matrix and is the vector of least squares estimates. The full model, , is an integer for which is invertible.

The weights for model averaging is specified as

| (4) |

with the resulting linear averaged predictive mean being

| (5) |

Then, we have the following properties:

| (6a) | ||||

| (6b) | ||||

| (6c) | ||||

| (6d) | ||||

| (6e) | ||||

| (6f) | ||||

| (6g) | ||||

| (6h) | ||||

Define the risk (i.e. the conditional squared error), , as

where

following Hansen (2007) (Lemma 2). This shows that the risk is a quadratic function with regard to the weight vector, . From this, we have

The residual from the linear projection can be written as

When , the residual is

The Mallows criterion for the model average estimator is

where

is the vector of model dimensions and the collection of residuals is

For the MMA estimator, the weight vector is selected by minimizing the Mallows criterion. This has the expectation (Hansen 2007, Lemma 3),

The empirical weight vector is

for which Hansen (2007) showed that this criterion is optimal, as we summarize below.

Limiting the weight vector to a finite number of discrete values, where the possible values, , are the ,

The set of possible discrete weight vectors is denoted as . When , assume

almost surely. Additionally, assume

Then, the following holds (Hansen 2007, Theorem 1):

The theoretical results from Hansen (2007) shows that choosing by minimizing minimizes the loss (but not the risk), as well as achieve the optimal rate. However, limiting the weight vector to a finite number of discrete values is somewhat restrictive, which we will later relax.

While the MMA estimator is optimal for a class of discrete model averaging estimators, it does not mean that there is no room for improvement. This can be easily seen when we decompose the loss as

Since the linear projection, , will ultimately not be the conditional expectation of given and the averaged will not be the conditional expectation of given all the available information, this will leave to be improved.

This improvement can be expound further by decomposing the DGP and identifying the source of possible improvement. Consider decomposing the DGP into the full model, , and its misspecification bias;

Here, the covariates for , , and the covariates for misspecification bias, , are considered independent. The conditional expectation of the full model for , given all observable covariates, , is

The conditional expectation of the misspecification bias of , due to independence, is

If each are i.i.d., then does not depend on the sampling order , thus we denote it as . The best predictive value, in terms of MSE, can be written as,

which is to say that the DGP can be decomposed into its location bias, , and the optimal regression, . This can be written in matrix form (with elements corresponding to ) as

Note that is a vector of ones.

The expectation of the misspecification bias for each model, , using , is

The intercept, , is the estimate for for each model, . The predictive value, , for each model is,

where we separate the intercept. The matrix form (with elements corresponding to ) is

Note that is a vector of ones, and is minus the intercept.

Given the above, linear model averaging (including MMA) can be written as

The weights, are chosen to be as close to the best predictive value of ; . The optimal weight vector is . Then, except in rare situations, we have,

Since the weights, , must be selected by simultaneously minimizing the location bias and regression error, the weights on the location bias need not be zero. There might exist a vector of weights, , that satisfies , but that will likely worsen the regression error. This is due to the dimension for linear averaging missing one dimension with regard to optimizing the averaging weights. Thus, under linear averaging, there is always a tradeoff between the location bias and regression error, where minimizing one leads to an increase in the other, making all linear averaging estimators (MMA included) suboptimal.

3 Mean-shift least squares averaging

To simultaneously minimize the location bias and regression error, we propose a new estimator that includes a common constant (i.e. an intercept) to the set of models, which we call the mean-shift Mallows model averaging (MSA) estimator. Our MSA estimator has the following predictive mean:

| (7) |

where the empirical weights, , and intercept, , are estimated by minimizing the criterion we develop in this section.

When we include a common constant, the residual of the linear projection is

where

For the extra term , arbitrarily fixing the weight vector, , we have a quadratic function with regard to :

Since is downward convex and is zero when , the extra term can take a negative value. Then, the optimal is

Adding the mean-shift to linear averaging, the component for location bias can be written as

which uniformly improves the total error by fully controlling for location bias without compromising minimizing regression error. Additionally, adding changes the optimal solution with regard to the weights , which possibly improves the regression error as well.

3.1 Criterion

Since the loss is defined as

the expectation is

Then, the mean-shift Mallows criterion is

which can be written as

Comparing the criterion with and without an intercept, there exists an that satisfies

This can be seen by setting with regard to that satisfies .

3.2 Optimality

Given the extension, we now show that our proposed MSA is optimal to the MMA estimator in Hansen (2007). We set the parameter space for which the intercept can take values,

Here, is on including zero. Additionally, we assume

When , we assume,

almost surely. We additionally assume, for each point, ,

| (8) |

This condition is weaker than that of Wan et al. (2010). Compared to the conditions in Hansen (2007),

this might seem somewhat restrictive. However, we only need to add the following condition,

to the above, which is a reasonable condition to add.

Proposition 3.1.

Given the above assumptions, we have,

The proof roughly follows that of Li et al. (1987) and Hansen (2007), though the loss, risk, and criterion are dependent on the continuous parameter, , which makes the proof challenging. Note that Wan et al. (2010) provides the conditions to relax the discreteness of the weights. In contrast, we prove optimality using the convexity lemma by utilizing the fact that the loss and criterion is a convex function. This allows us to prove optimality with a weaker condition to that of Wan et al. (2010).

We first decompose as

Since the term does not affect model selection, this is equivalent to minimizing,

To prove optimality, we must show

which implies that

must uniformly hold with regard to and .

Since can be written as

and each term is

we need to show the following to prove optimality:

- 2.2

-

- 2.3

-

- 2.4

-

To show uniform convergence, it is sufficient to show pointwise convergence, following the below convexity lemma:

Theorem 3.1.

Proof of 2.2: From Chebyshev’s inequality, we have

which we evaluate the right hand side. From the inequality in Whittle (1960), the following

holds, thus,

where is some constant. Now, since

we have

Therefore, from assumption 8, we prove 2.2.

Proof of 2.3: Similarly to 2.2, applying Chebyshev’s inequality, we evaluate the moment of the right hand side. Applying the quadric version of Whittle’s inequality, we have

where, is a constant. Additionally, since

we prove 2.3.

Proof of 2.4: For this, it is sufficient to show convergence for the following:

thus,

Noting that

the first equation is equivalent to 2.2, and the second equation, utilizing the quadratic version of the Whittle’s inequality to evaluate the expectation,

and further noting that

for some constant, , we have the following:

The rest is the same as 2.3. Q.E.D.

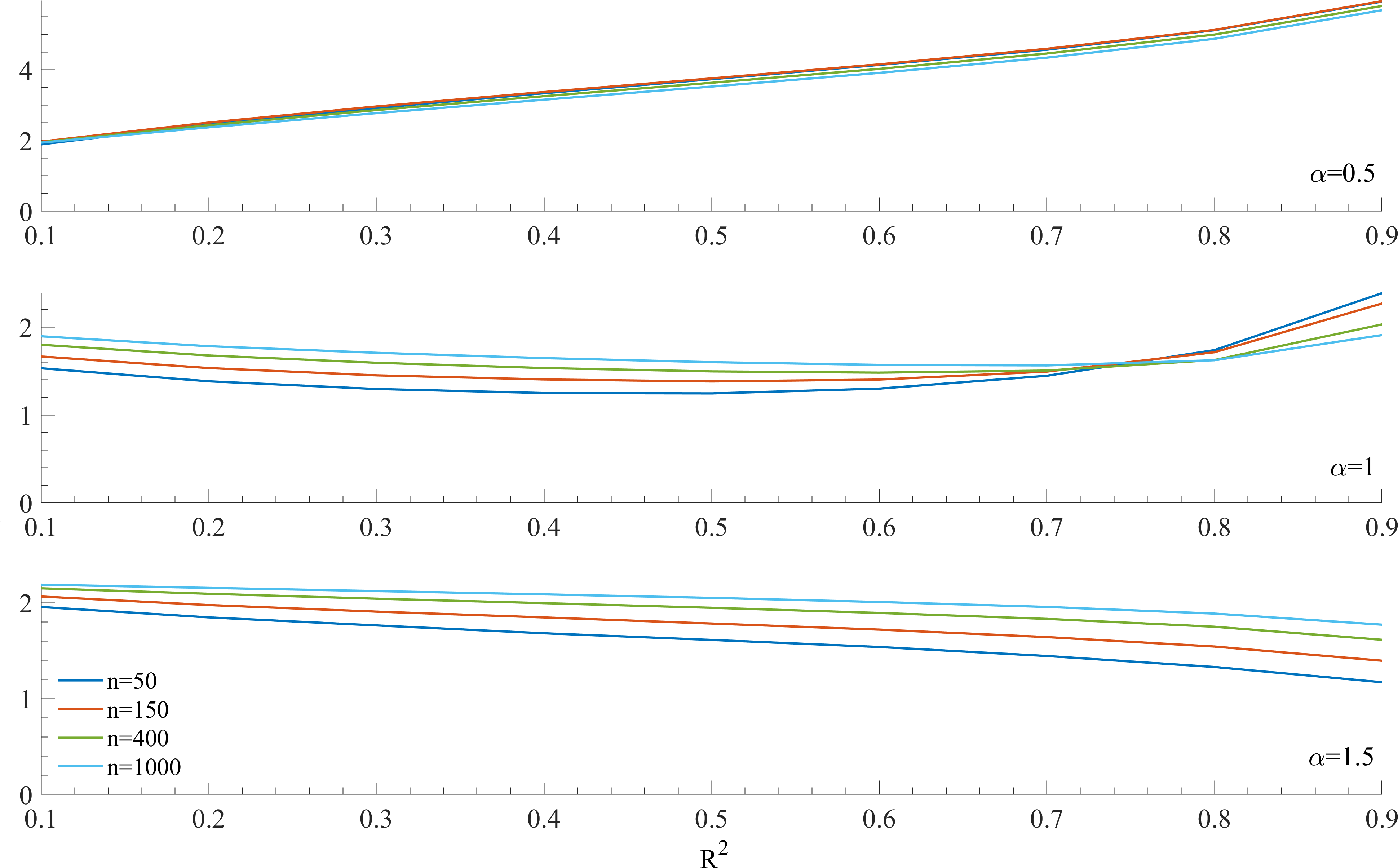

4 Finite sample investigation

We investigate the finite sample mean squared error of our proposed MSA estimator to that of the original MMA estimator in a simple simulation setting similar to Hansen (2007). Our data generating process is a slight modification of eq. (1), where the misspecification bias is positive:

where all are independent and identically distributed , the error, , is and independent of . The parameters are determined by the rule, , where . Though not reported, the results are robust to alternative specifications, except when the bias has expectation zero (i.e. no location bias), at which MSA is equivalent to MMA.

For the finite sample investigation, we vary the sample size by and . The parameter controls the rate of decline of the coefficients, , where a larger implies a steeper decline in . The number of models is determined by , which, for our four sample sizes, means . We vary so as varies from 0.1 to 0.9.

Unlike Hansen (2007), which compared the MMA estimator to AIC model selection, Mallows model selection, smoothed AIC, and smoothed BIC, we simply compare our MSA estimator to the MMA estimator, as Hansen (2007) convincingly show that the MMA estimator is superior to these methods. To evaluate the two estimators, we compute the log risk (expected squared error) for each and calculate the difference. The simulation is done for 1,000 iterations and averaged over.

The results of the finite sample investigation are shown in Fig. 1. The three panels display the difference in log risk between MMA and MSA for the varying , where the difference is displayed on the axis and the population is displayed on the axis. The different colored lines are for the different sample sizes, .

For all results, our proposed MSA estimator uniformly outperforms the MMA estimator to varying degrees. In the case of , the results are almost identical for all sample sizes. The relative performance of MSA increases as increases, which is expected as the increased , under a low , implies a more robust bias component. This bias component is captured in MSA, leading to improved performances. As increases, the results invert, in the sense that, for , the difference in log risk is bowed, while, for , the difference decreases as increases. This is not unexpected as, in Hansen (2007), the performance of the MMA estimator decreases in these cases. If anything, for , the MSA estimator seems more resilient for higher . Over all variations, the MSA estimator is superior to the MMA estimator.

References

- Aastveit et al. (2014) Aastveit, K. A., Gerdrup, K. R., Jore, A. S., Thorsrud, L. A., 2014. Nowcasting GDP in real time: A density combination approach. Journal of Business & Economic Statistics 32, 48–68.

- Aastveit et al. (2018a) Aastveit, K. A., Mitchell, J., Ravazzolo, F., van Dijk, H. K., 2018a. The evolution of forecast density combinations in economics. Tech. rep., Tinbergen Institute Discussion Paper.

- Aastveit et al. (2018b) Aastveit, K. A., Ravazzolo, F., Van Dijk, H. K., 2018b. Combined density nowcasting in an uncertain economic environment. Journal of Business & Economic Statistics 36 (1), 131–145.

- Amisano and Giacomini (2007) Amisano, G. G., Giacomini, R., 2007. Comparing density forecasts via weighted likelihood ratio tests. Journal of Business & Economic Statistics 25, 177–190.

- Bates and Granger (1969) Bates, J. M., Granger, C. W. J., 1969. The combination of forecasts. Operational Research Quarterly 20, 451–468.

- Bernardo and Smith (2009) Bernardo, J. M., Smith, A. F., 2009. Bayesian theory. Vol. 405. John Wiley & Sons.

- Billio et al. (2012) Billio, M., Casarin, R., Ravazzolo, F., van Dijk, H. K., 2012. Combination schemes for turning point predictions. Quarterly Review of Finance and Economics 52, 402–412.

- Billio et al. (2013) Billio, M., Casarin, R., Ravazzolo, F., van Dijk, H. K., 2013. Time-varying combinations of predictive densities using nonlinear filtering. Journal of Econometrics 177, 213–232.

- Breiman (1996) Breiman, L., 1996. Bagging predictors. Machine learning 24 (2), 123–140.

- Džeroski and Ženko (2004) Džeroski, S., Ženko, B., 2004. Is combining classifiers with stacking better than selecting the best one? Machine learning 54 (3), 255–273.

- Geweke and Amisano (2012) Geweke, J., Amisano, G. G., 2012. Prediction with misspecified models. The American Economic Review 102, 482–486.

- Geweke and Amisano (2011) Geweke, J. F., Amisano, G. G., 2011. Optimal prediction pools. Journal of Econometrics 164, 130–141.

- Hall and Mitchell (2007) Hall, S. G., Mitchell, J., 2007. Combining density forecasts. International Journal of Forecasting 23, 1–13.

- Hansen (2007) Hansen, B. E., 2007. Least squares model averaging. Econometrica 75 (4), 1175–1189.

- Hansen and Racine (2012) Hansen, B. E., Racine, J. S., 2012. Jackknife model averaging. Journal of Econometrics 167 (1), 38–46.

- Hoeting et al. (1999) Hoeting, J. A., Madigan, D., Raftery, A. E., Volinsky, C. T., 1999. Bayesian model averaging: a tutorial. Statistical science, 382–401.

- Hoogerheide et al. (2010) Hoogerheide, L., Kleijn, R., Ravazzolo, F., Van Dijk, H. K., Verbeek, M., 2010. Forecast accuracy and economic gains from Bayesian model averaging using time-varying weights. Journal of Forecasting 29, 251–269.

- Kapetanios et al. (2015) Kapetanios, G., Mitchell, J., Price, S., Fawcett, N., 2015. Generalised density forecast combinations. Journal of Econometrics 188, 150–165.

- Kascha and Ravazzolo (2010) Kascha, C., Ravazzolo, F., 2010. Combining inflation density forecasts. Journal of Forecasting 29, 231–250.

- Li et al. (1987) Li, K.-C., et al., 1987. Asymptotic optimality for , cross-validation and generalized cross-validation: Discrete index set. The Annals of Statistics 15 (3), 958–975.

- Louppe (2014) Louppe, G., 2014. Understanding random forests: From theory to practice. arXiv preprint arXiv:1407.7502.

- McAlinn et al. (2019) McAlinn, K., Aastveit, K. A., Nakajima, J., West, M., 2019. Multivariate bayesian predictive synthesis in macroeconomic forecasting. Journal of the American Statistical Association forthcoming.

- McAlinn and West (2019) McAlinn, K., West, M., 2019. Dynamic bayesian predictive synthesis in time series forecasting. Journal of Econometrics 210 (1), 155–169.

- Negro et al. (2016) Negro, M. D., Hasegawa, R. B., Schorfheid, F., 2016. Dynamic prediction pools: an investigation of financial frictions and forecasting performance. Journal of Econometrics 192(2), 391–405.

- Pettenuzzo and Ravazzolo (2016) Pettenuzzo, D., Ravazzolo, F., 2016. Optimal portfolio choice under decision-based model combinations. Journal of Applied Econometrics 31 (7), 1312–1332.

- Pollard (1991) Pollard, D., 1991. Asymptotics for least absolute deviation regression estimators. Econometric Theory 7 (2), 186–199.

- Raftery et al. (1997) Raftery, A. E., Madigan, D., Hoeting, J. A., 1997. Bayesian model averaging for linear regression models. Journal of the American Statistical Association 92 (437), 179–191.

- Rockafellar (1970) Rockafellar, R. T., 1970. Convex analysis. Vol. 28. Princeton university press.

- Schapire (2003) Schapire, R. E., 2003. The boosting approach to machine learning: An overview. In: Nonlinear estimation and classification. Springer, pp. 149–171.

- Takanashi and McAlinn (2019) Takanashi, K., McAlinn, K., 2019. Predictive properties of forecast combination, ensemble methods, and bayesian predictive synthesis. arXiv preprint arXiv:1911.08662.

- Terui and van Dijk (2002) Terui, N., van Dijk, H. K., 2002. Combined forecasts from linear and non- linear time series models. International Journal of Forecasting 18(3), 421–438.

- Wan et al. (2010) Wan, A. T., Zhang, X., Zou, G., 2010. Least squares model averaging by mallows criterion. Journal of Econometrics 156 (2), 277–283.

- Whittle (1960) Whittle, P., 1960. Bounds for the moments of linear and quadratic forms in independent variables. Theory of Probability & Its Applications 5 (3), 302–305.

- Yao et al. (2018) Yao, Y., Vehtari, A., Simpson, D., Gelman, A., et al., 2018. Using stacking to average bayesian predictive distributions (with discussion). Bayesian Analysis 13 (3), 917–1003.

- Zhang et al. (2013) Zhang, X., Wan, A. T., Zou, G., 2013. Model averaging by jackknife criterion in models with dependent data. Journal of Econometrics 174 (2), 82–94.