Event Ticket Price Prediction with Deep Neural Network

on Spatial-Temporal Sparse Data

Abstract.

Event ticket price prediction is important to marketing strategy for any sports team or musical ensemble. An accurate prediction model can help the marketing team to make promotion plan more effectively and efficiently. However, given all the historical transaction records, it is challenging to predict the sale price of the remaining seats at any future timestamp, not only because that the sale price is relevant to a lot of features (seat locations, date-to-event of the transaction, event date, team performance, etc.), but also because of the temporal and spatial sparsity in the dataset. For a game/concert, the ticket selling price of one seat is only observable once at the time of sale. Furthermore, some seats may not even be purchased (therefore no record available). In fact, data sparsity is commonly encountered in many prediction problems. Here, we propose a bi-level optimizing deep neural network to address the curse of spatio-temporal sparsity. Specifically, we introduce coarsening and refining layers, and design a bi-level loss function to integrate different level of loss for better prediction accuracy. Our model can discover the interrelations among ticket sale price, seat locations, selling time, event information, etc. Experiments show that our proposed model outperforms other benchmark methods in real-world ticket selling price prediction.

1. Introduction

Promotional campaign, a series of advertisements using various marketing tools to promote an event (such as a concert or sports match), plays an important role in reaching out to potential customers. It can make the event better known in the relevant circles and promote event ticket sales. A successful advertising campaign cannot be executed in a vacuum and therefore, brands and businesses should carefully launch the campaign at the right moment. This is important because timing is crucial to the success of any public campaign. Among all the factors, predicting future ticket sale price of the targeted event is one of the most important ones, since it will lead to profit maximization if a campaign run right before the ticket selling price reaching its peak. So the team can decide when to get the most out of limited resources to promote the event in advance.

However, predicting ticket sale price for a concert or sports match is nontrivial, and it is different from traditional ticket price prediction such as airline price prediction (Mottini and Acuna-Agost, 2017; Lu, 2017; Groves and Gini, 2013). Airline ticket price prediction focus on predicting the average price of a flight, or a particular class (such as Economy Class), which doesn’t distinguish the spatial difference between seats. But match/concert ticket price is relevant to seat location since price can vary a lot for different seats, and it is important to predict each seat’s selling price so that the campaign plan can be more oriented to specific groups of potential customers. Therefore predicting event ticket selling price is a spatio-temporal analysis problem.

Spatio-temporal prediction has become a popular problem for a wide range of settings ranging from weather/climate forecasting (Liu et al., 2018; Xu et al., 2018), video prediction (Oh et al., 2015; Singh et al., 2017), traffic flow forecasting (Zhang et al., 2017; Yao et al., 2019; Yu et al., 2017b; Yu et al., 2017a) to taxi demanding prediction (Yao et al., 2018; Ke et al., 2017). In spatio-temporal prediction, measurements are often taken over space and time, while the model is required to predict future target value at any location and time.

Different from the traditional spatio-temporal prediction problem, our problem has the following challenges:

-

(1)

The available records of ticket transaction are sparse in both space and time, in the sense that for any historical event i) the selling price for one seat was only observable once at the time of sale, ii) it is not unusual that some seats didn’t get sold, iii) the distribution of the transaction time is very uneven.

-

(2)

Event ticket selling price is relevant to multiple types of information including temporal (transaction time), spatial (seat locations) and event information (event date, number of team stars, team’s recent performance, etc.).

Unfortunately, there is few research that aim at predicting the event ticket selling price to solve these challenges.

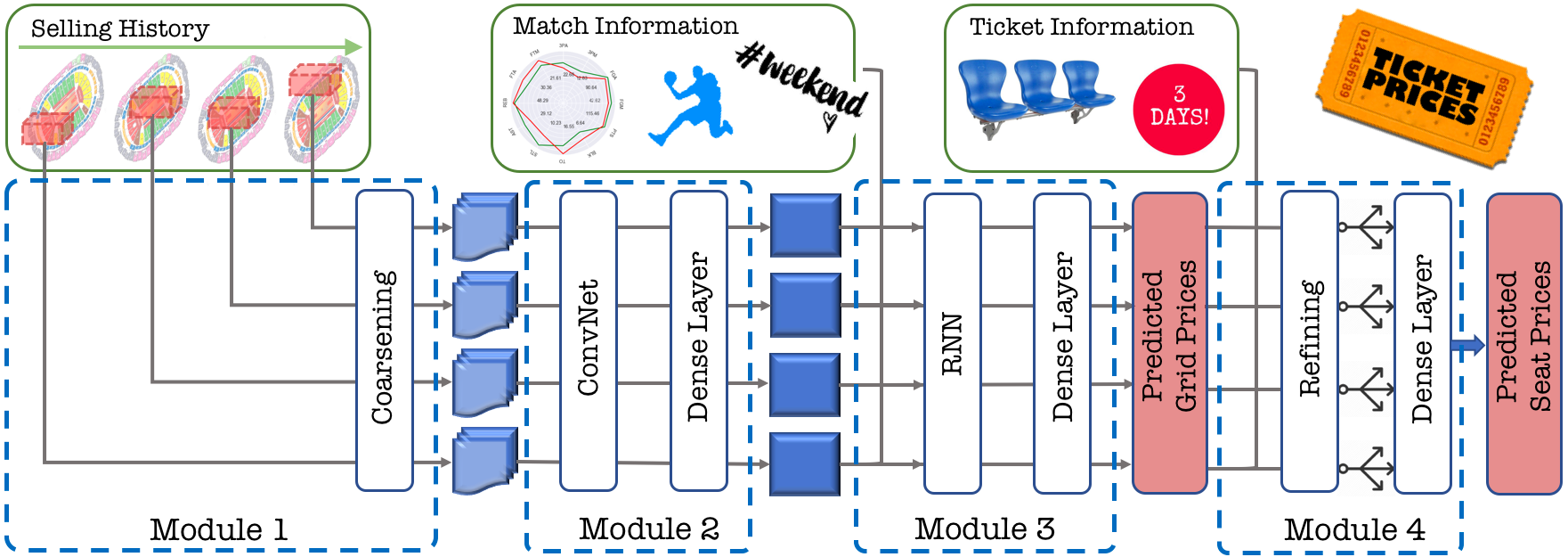

In this paper, we target to solve the above challenges by proposing Event Ticket Price Prediction (ETPP). The framework is shown in Figure 1. Our research has the following contributions:

-

(1)

We resolve the data sparsity problem by proposing data coarsening and refining layers on both spatial and temporal dimension. The coarsening layer converts the original sparse input to a coarse but much less sparse format, so to avoid the zero weighting problem of deep neural network on sparse data. The refining layer maps the coarse resolution back to original input level, so that the predicted value can be directly compared with ground truth.

-

(2)

Integrating the predicted values on both coarsened and original level, we propose a bi-level optimization method, and design a bi-level loss function that involves two levels of predicted output, which provides better prediction accuracy.

-

(3)

Our ETPP model systematically combines data coarsening and refining layers, spatial and temporal modeling and a special loss function. It considers multiple types of input (ticket transaction history, event information, ticket information, etc.), and outputs accurate prediction results on a real world ticket transaction dataset.

2. Our ETPP Framework

In this section, we first define the problem formally, and then elaborate our ETPP in details. As shown in Figure 1, ETPP consists of four modules. Module converts the input data into coarse format to mitigate the data sparsity. Then convolutional net (ConvNet) and fully connected layers are applied in Module to extract the spatial dependency. Module focuses on modeling temporal dependency by recurrent neural network (RNN). Finally, Module projects the data resolution back to the original level and calculates the final loss function.

2.1. Problem Statement

Given the historical records of ticket transactions, we want to predict the seats’ sale price at any time before the event. Each transaction record includes the selling price, the transaction time and the location of the corresponding seat, and the corresponding event information (such as event date, team’s recent performance, number of team stars, etc.).

Suppose there are historical events and the location has number of seats 111We assume that all the events were held at the same location, which can be a stadium (for sports match) or hall (for concert).. For any event , we denote as the ticket price of the seat at the -th row and the -th column, with date-to-event as the transaction time. We use to denote all the seat prices at date-to-event (nans for certain seats if there were no corresponding transactions at ).

Our goal is to design a model to predict () ahead given all the available historical transactions and event information (event date, team’s recent performance, number of team stars, etc.) where .

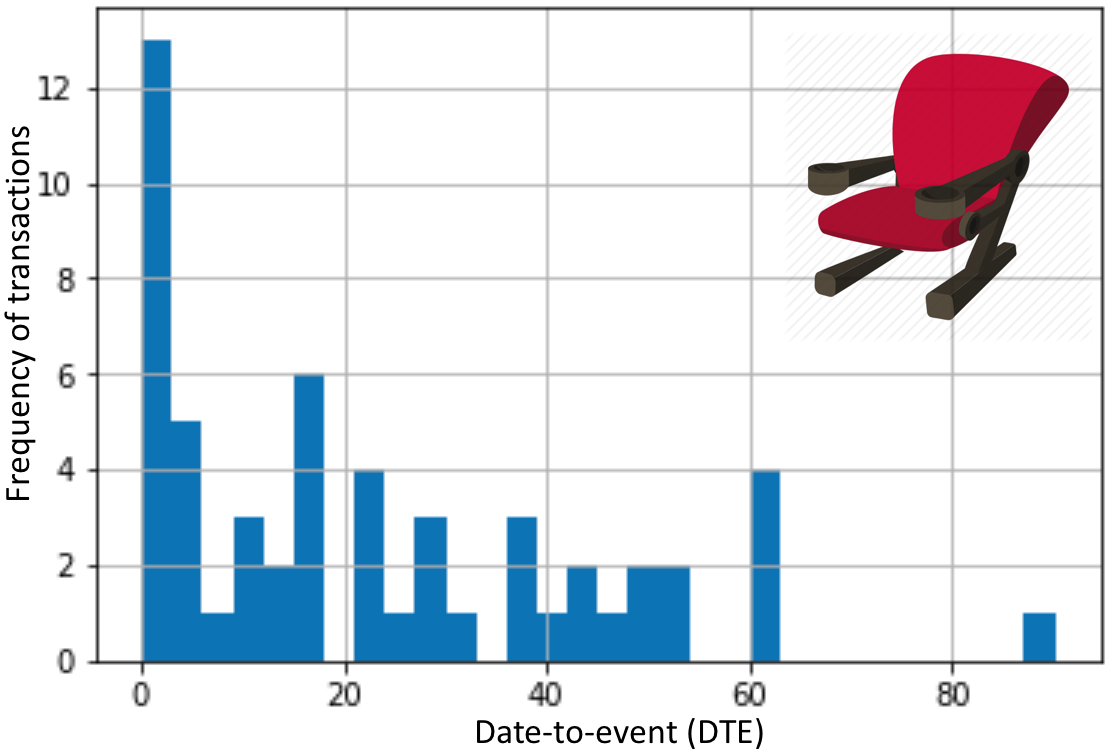

However, the historical record of ticket transaction is usually very sparse in time and space, and most of are with empty values because few transactions happened at , or some seats didn’t even get sold for that event. Figure 2 shows the transaction histogram across date-to-event of a certain seat for historical events. Obviously, the distribution is quite uneven, where most transactions happened right before the event date, and very few happened three months ahead. It is also not difficult to see that could be extremely sparse at certain date-to-event . On the other hand, any seat of an event can be only purchased once (assume there is no cancellation or reselling). Therefore, the historical data is very sparse in both time (date-to-event) and space (seat), which makes traditional regression methods inapplicable. And existing deep neural network also suffer from zero weighting problem on such sparse data. To solve this problem, our first step is to propose a coarsening layer on both temporal and spatial dimensions as described in Section 2.2.

2.2. Module 1: Data Coarsening

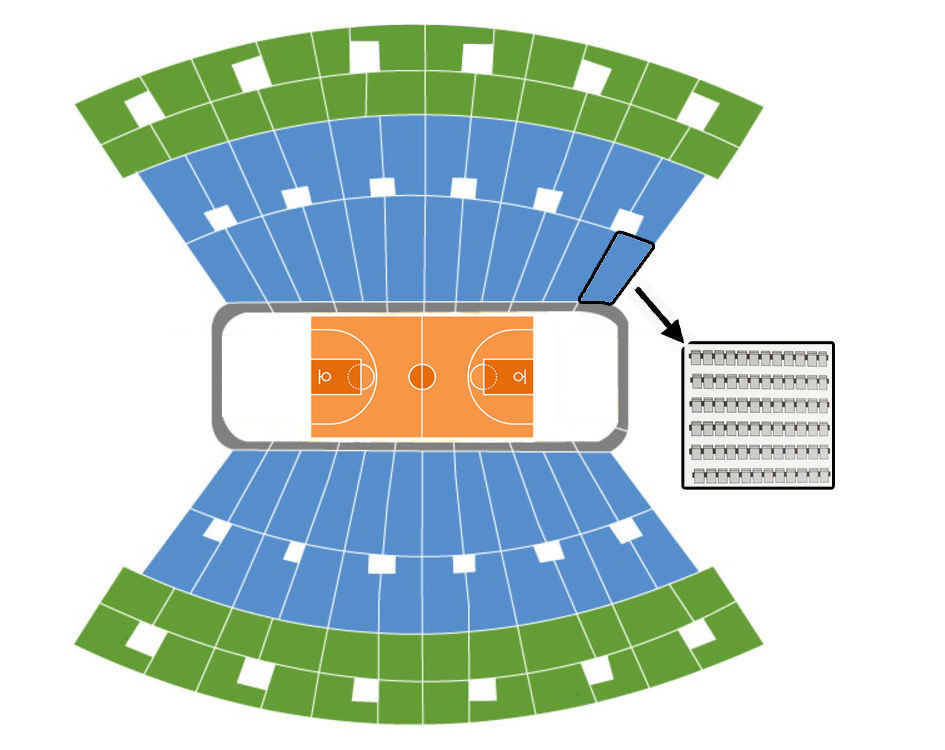

To solve the data sparsity problem, here we introduce a data coarsening layer on both spatial and temporal dimension. Assuming the event location is an auditorium, which has seats in total, we first deal with spatial sparsity by splitting seats into non-overlapping grids . Each grid () consists of a few seats where denotes the seat in -th row and -th column in grid . This is illustrated in Figure 3.

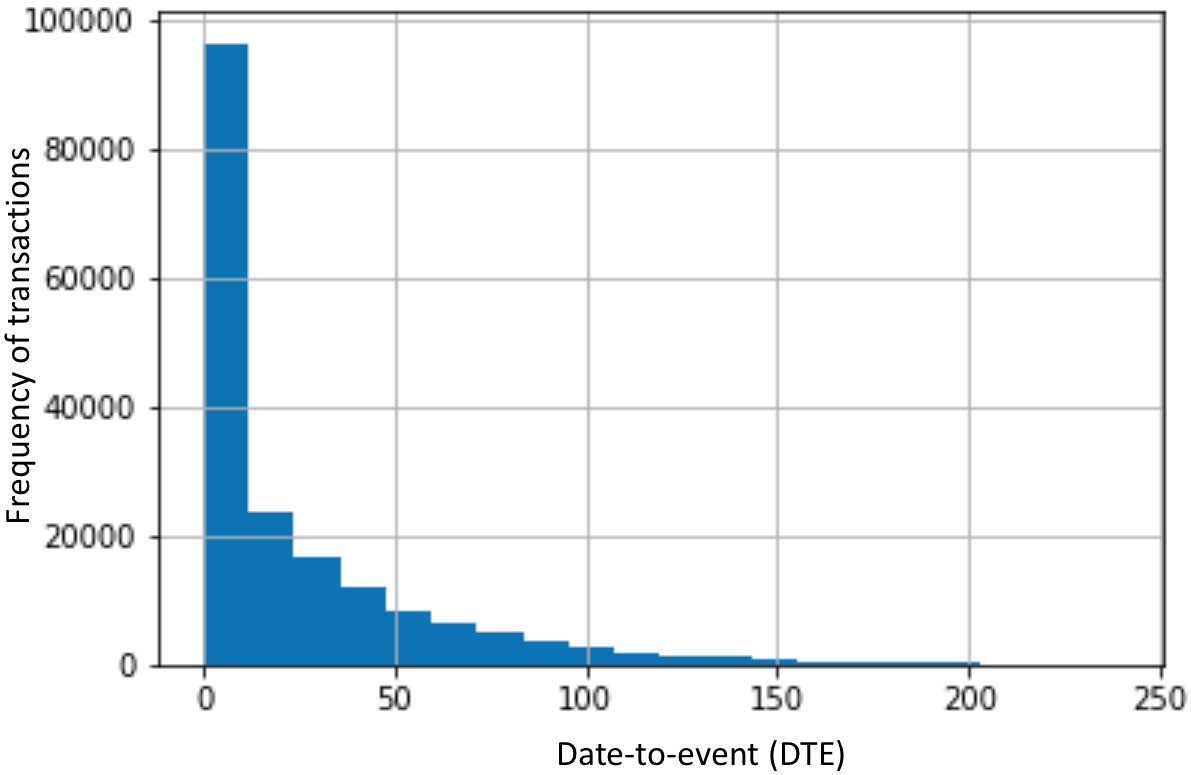

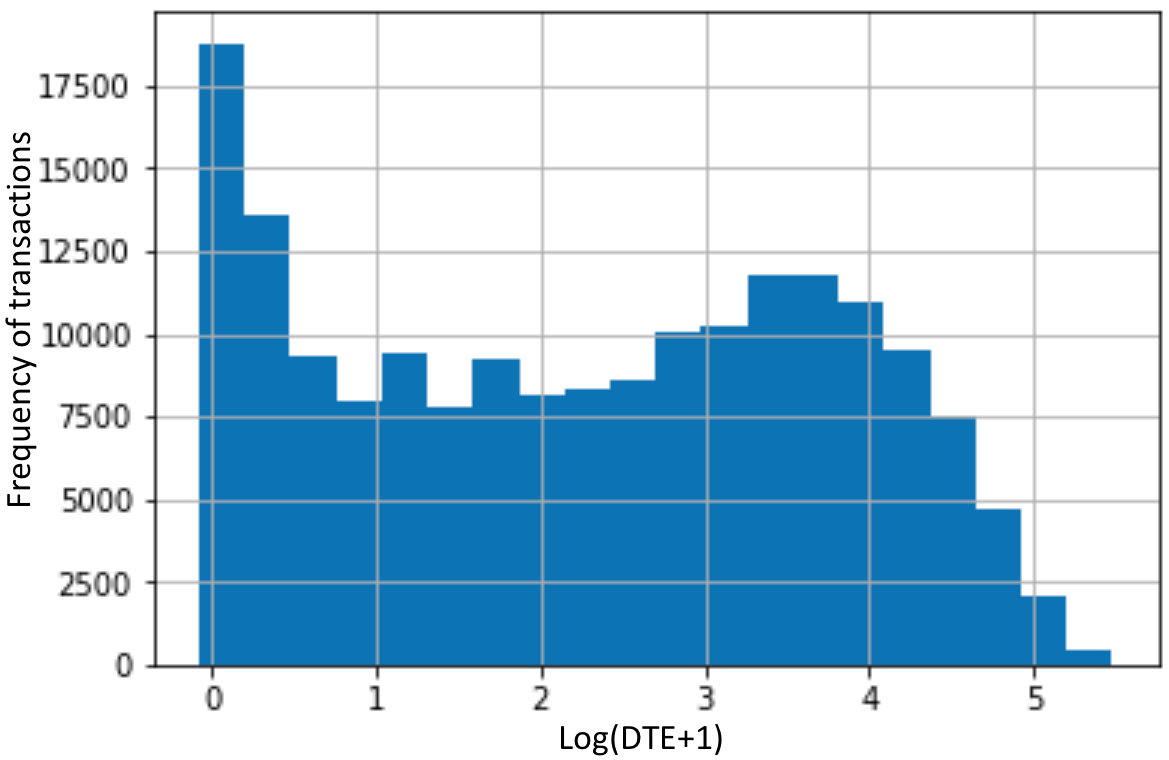

In temporal dimension, the data availability is not evenly distributed. Figure 4(a) shows the date-to-event (DTE) histogram of all the transactions in historical events. Obviously it is not reasonable to coarsen temporal data with one fixed-size. We notice from Figure 4(a) that ticket transactions are rare when DTE is large, and the frequency increases almost exponentially as DTE becomes smaller (closer to the event). Visually speaking, the distribution shape in Figure 4(a) is very similar to the function of , therefore we convert the scale in axis from DTE to 222Since DTE can be smaller than 1, therefore we use to make everything positive. as shown in Figure 4(b). Now the values become more evenly distributed. We equally divide into non-overlapping bins 333We let the whole range of cover of data, and all the data are added to their closest bin respectively.. Each time-bin represents a certain range in scale.

From now on, we denote as the ticket price of grid at time bin for event , which is computed by the median of all the available transactions for the seats at grid at time-bin . We denote , i.e. the median price collections of all the grids at .

To conclude, this layer coarsens the seat-time to grid-bin resolution. It is similar to average pooling layer which is usually used in image modeling. However, there are two differences: 1) unlike pooling layer, it doesn’t only compress spatial information but also temporal information; 2) the motivation of pooling layer is to reduce the model size, but our coarsening layer is to mitigate the spatio-temporal sparsity in the input data.

2.3. Module 2: Spatial Modeling

In Module 2, we employ a convolutional neural network (ConvNet) to explore the spatial dependency of ticket selling prices.

First of all, we reorganize into a two dimensional matrix with the first dimension as the row-wise coordinate and the second as the column-wise coordinate of grids (refer to Figure 3).

Then, we set the as , and feed it to a number of convolutional layers. Assuming that denotes the feature maps in the -th convolutional layer, the output of -th layer is given by:

| (1) |

where denotes the convolutional operation, is the activation function of ReLU, denotes the convolutional filter and is a bias term at the -th layer. The convolutional filters we used are three kernels of size , three kernels of size and three kernels of size , and they all have zero-padding. The output of the last convolutional layer is flattened to a vector, which we denote as . Then a fully connected layer is applied as below:

| (2) |

where is a weight layer, and is a bias term. The spatial dependency of grid prices is now captured by .

2.4. Module 3: Temporal Modeling

The spatial feature maps generated by Module is temporally dependent on the previous time bins. In Module we use recurrent neural network (RNN) to explore this temporal dependency. Specifically, we choose Gated Recurrent Units (GRUs) among all the RNN methods due to its comparable/better performance and less amount of parameters (Chung et al., 2014; Ugurlu et al., 2018).

Given the output from Module , we concatenate with the event information . We denote the concatenated data as , where and is dimensions of event information (such as event time, team’s recent performance and so on) 444We use OneHotEncoder to convert categorical features (if there is any) into numerical..

Specifically, given the previous hidden state , the current hidden state is updated with:

| (3) |

where the GRU cell (Chung et al., 2014) is formulated as:

| (4) | ||||

where is the update gate vector, is the reset gate vector, is tanh function, is sigmoid function, , and are the weight matrices of size , , and are the weight matrices of size , and , and are the bias vectors of size .

We then feed the output of GRU at each time bin to a fully connected dense layer:

| (5) |

where and . So is the output of Module , which is the predicted grid price at time bin .

Essentially, Module and Module jointly model the spatial patterns of ticket transactions with temporal dependency.

2.5. Module 4: Data Refining

In Module , we expand the data from grid-level to seat-level. Firstly, we expand to a vector of size , where is the total number of seats. Each grid is expanded to the full size of its number of seats by duplicating the predicted grid price. Then we concatenate the new vector with the corresponding seats’ coordinates and date-to-event of the transactions column-wisely (as additional channels), and denote the whole matrix as , where the columns include the predicted seat prices (expanded from ), the date-to-event of transactions and the spatial coordinates of the seats.

Finally, we apply a series of fully connected layers:

| (6) |

where , , and .

2.6. Our Loss Function

Here we design a special bi-level loss function to integrate the two-level prediction output. The model has intermediate output on grid-level prediction and final output on seat-level prediction. Although our final objective is to get better prediction of seat price, we found that combining the grid-level into loss function helps in getting better performance on the seat-level prediction. We will provide further analysis in the experiment section.

Our final loss function consists of two parts, one for the coarsened targets (grid level), and one for the original targets (seat level):

| (7) | ||||

where

| (8) |

The first part is to measure the residuals between the predicted and the actual grid price, while the second part is to measure the residuals between the predicted and the actual seat price. In the grid level, the sparsity is low and therefore most of the are . But on the seat level, the ground truth is much more sparse and therefore only a small portion of data will be involved. Moreover, our final objective is to get better accuracy on the seat level prediction, therefore in practice we set . We employ Adam optimizer to minimize .

3. Related Work and Discussion

Price prediction is a great challenge due to the fact that it is an immensely complex, chaotic and dynamic problem. There are many studies from various areas aiming to take on that challenge and machine learning approaches have been the focus of many of them. Particularly, a consensus has been reached that price prediction is a highly nonlinear and time-variant problem (Adebiyi et al., 2014).

Modern nonlinear machine learning methods have often been used in price prediction. For stock market price prediction (Patel et al., 2015; Khaidem et al., 2016), random forest is claimed to have better performance than Artificial Neural Network (ANN), Support Vector Machine (SVM), and naive-Bayes model. Specifically in the work of (Khaidem et al., 2016), random forest is proved to be robust in predicting future direction of stock movement. On the other hand, Gradient Boosting Machine based methods like XGBoost have shown good performance on price prediction of crude oil, electricity and gold market (Pierdzioch et al., 2015; Hong et al., 2016; Gumus and Kiran, 2017). It is popular because it has comparatively low variance and is able to recognize trends and fluctuations, and it can simultaneously handle variables of the nature of time indexes and static exogenous variables.

Recently, Deep Neural Networks have been successfully used in many real world applications. Among all these methods, Recurrent Neural Networks (RNNs) have been proposed to address time-dependent learning problems. In particular, Long Short Term Memory (LSTM) and Gated Recurrent Units (GRU) are tailor-made for time series price estimation (Nelson et al., 2017; Chen et al., 2017; Ugurlu et al., 2018).

However, event ticket price prediction is very special compared with other price prediction problems, in the sense that the training data is extremely sparse. For each historical event, there is at most one transaction for any seat across time. And there are many timestamps that have no transaction available at all. The data sparsity is a deteriorating factor for all training based methods, but in particular for neural network based methods, of which performance heavily depends on the availability of large training data (Ugurlu et al., 2018). For example, Convolutional Neural Network (ConvNet/CNN) discovers the spatial dependency in the neighborhood content. But simply applying it to the sparse transaction data at each timestamp will lead to all zero weights due to the weight sharing problem. Therefore, although there are many recent research that explore deep learning in the direction of spatio-temporal prediction (Liu et al., 2018; Xu et al., 2018; Yao et al., 2018; Yao et al., 2019; Zhang et al., 2019), none of them is applicable for event ticket price prediction due to the zero weighting problem.

4. Experiment

In this section, we demonstrate the performance of our ETPP by a thorough comparison with a number of popular baselines and its variants on actual ticket transaction dataset.

4.1. Experiment Setup

A Ticket Transaction Dataset from NBA

Over the last couple of years, National Basketball Association (NBA) is growing in popularity. It is the most followed sports league on social media with more than 150 million followers. The average NBA ticket price for the season is up from the average ticket price of during the season. Therefore there is urgent need for any of the NBA teams to design a ticket price prediction model for successful promotional campaign.

We use nine datasets to test our model. The data we use is from one NBA team’s ticket transaction database. It involves all the available transactions from season to . In total there are over transaction records from historical matches. Each record has the ticket sale price, seat location, and the information of the corresponding match. It is also worth to mention that the input and the price are all standardized during preprocessing.

To simulate practical use, backtesting is used in the experiment to test our prediction accuracy. We build nine different datasets to backtest our model by selecting nine representative dates to separate the data. For each season we define three dates to represent starting of the season (Nov 1st), mid-season (Jan 1st), and late season (Feb 1st). In total we choose nine representative dates, from Nov 1st 2016 to Feb 1st 2019. For each representative date, we choose the matches right after that date as testing set, matches before that date as validation set, and all the data before the validation set for training.

Evaluation Metric

We use Mean Squared Error (MSE) and Mean Absolute Percentage Error (MAPE) as the evaluation metrics in our experiment.

MSE is one of the most popular regression metrics. It is the second moment of the error, and thus incorporates both the variance of the estimator (how widely spread the estimates are from one data sample to another) and its bias (how far off the average estimated value is from the truth). We include it here since we apply MSE-like loss function in our model design, and for the other baselines we also use MSE as the loss function.

MSE loss is defined as:

| (9) |

where () is the actual (predicted) price of the transaction and is the total number of transactions.

On the other hand, MAPE is included to account for the big differences in ticket price for different matches. This metric takes the relative errors of ticket price into consideration, since some ticket prices are in the thousands while some are as low as less than 100 dollars. Especially, the data doesn’t contain any zero (there is no free ticket). So it is always meaningful to calculate MAPE. MAPE loss is defined as:

| (10) |

where () is the actual (predicted) price of the transaction and is the total number of transactions.

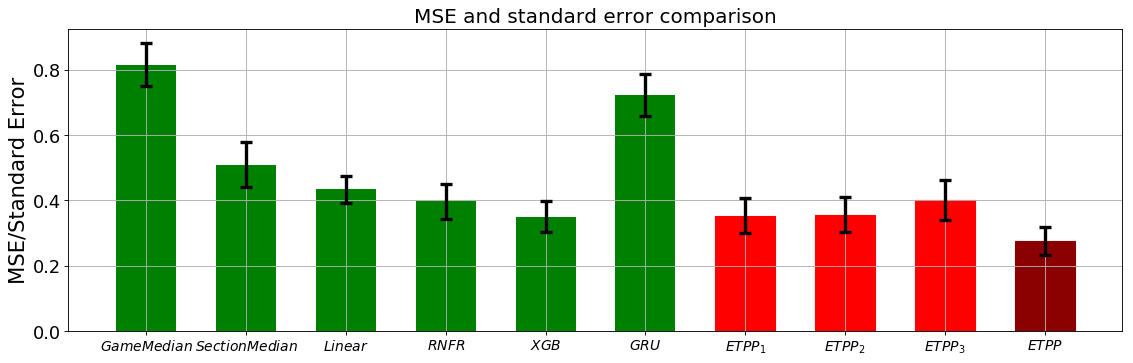

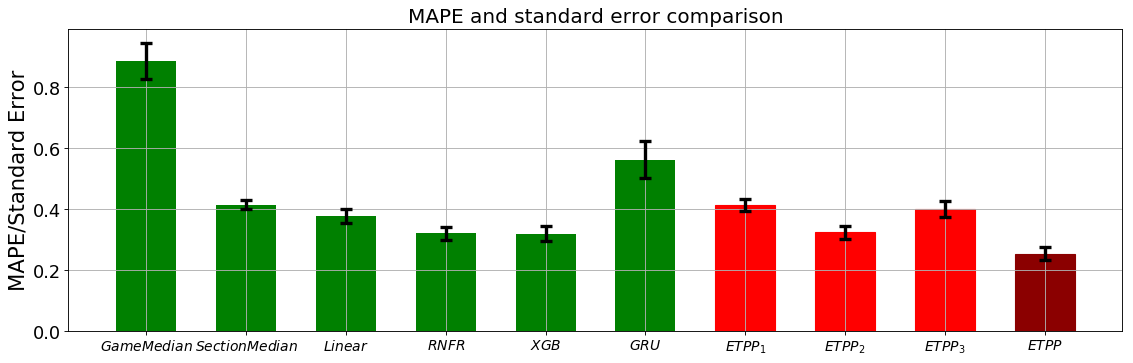

Since not all the baselines we included generate grid-level output, we only compare the seat-level output which are available in all models. For each of the nine datasets, we run every method times and calculate the average MSE and MAPE. And we also measure the standard error of MSE and MAPE across the nine datasets for each method.

Baseline Methods

We compare our ETPP method with the following six baselines.

-

•

GameMedian: Tickets sales usually start long before the match date. Therefore we are able to use the median of the sold tickets of each game as a naive prediction model.

-

•

SectionMedian: A slightly-improved but still naive model treats the median for loge and balcony seats separately. However, any further area segregation is difficult due to data sparsity.

-

•

Linear Model (Linear): It is a multiple linear regression approach for modeling the relationship between ticket prices, seat location and match information. But it treats transactions temporal-independently with each other.

- •

- •

-

•

Gated Recurrent Unit Network (GRU) (Ugurlu et al., 2018): GRU is a popular RNN model that has been used for price prediction (Ugurlu et al., 2018). For each game we concatenate all the ticket transactions to formulate a time series and feed these time series into the GRU model used in (Ugurlu et al., 2018).

Besides comparing against popular baselines, we are also interested in verifying the necessity of the key components of our design. Therefore we include the following variants of ETPP in our comparison:

-

•

: ETPP framework without Module (temporal modeling).

-

•

: ETPP framework without Module (spatial modeling).

-

•

: ETPP framework with seat-level loss function only (no grid-level loss).

-

•

: The whole ETPP framework.

The hyper-parameters of our ETPP are tuned according to the best performance on validation set. Specifically, the number of bins is set to , the hidden dimensions () in GRU is set to , in Module is set to , and in our loss function (Equation (LABEL:eq:loss)) are set to and . For all the baselines, we tune the parameters according to validation set performance and to the best of our effort.

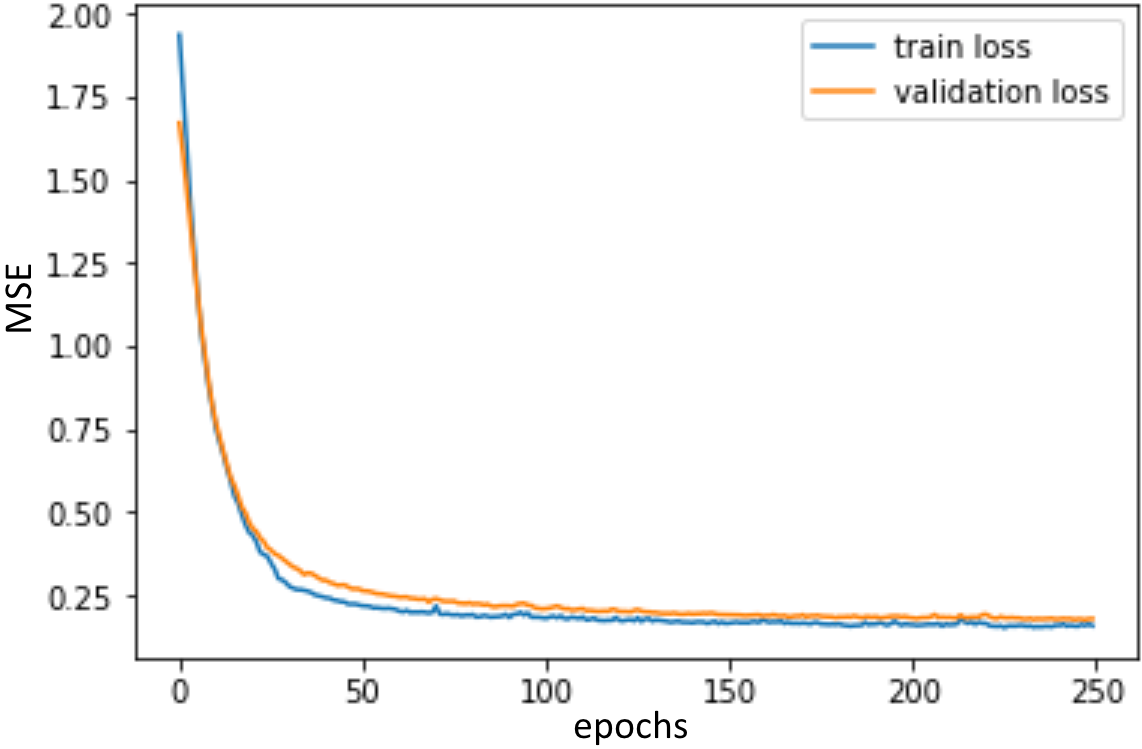

4.2. Convergence of Our ETPP

Before comparing against different baselines, it is necessary to show the convergence of our ETPP method. We plot the training loss and validation loss across training epochs in Figure 5. It shows that both the training loss and validation loss converge well, proving that our ETPP model is reasonably stable.

4.3. Comparison of Prediction Performance

Figure 6 shows the full comparison result on the average MSE and MAPE together with the standard error on the nine datasets. We have the following observations:

-

i)

Obviously, our ETPP is superior to all the baselines, on both MSE and MAPE. Specifically, ETPP’s MSE and MAPE is over lower than XGB, which performs the best among all baselines. Meanwhile, our standard error is also lower or comparable to the best performance from the other methods.

-

ii)

It is not surprising that GameMedian has the worst performance, since it does not use any information from historical matches. SectionMedian improves a lot from the local spatial statistics in seat neighborhood. This proves that spatial dependency is one of the key factors in ticket price prediction.

-

iii)

At first it may be surprising to see that popular RNN model like GRU fails miserably in this problem. But it can be explained by the curse of data sparsity. The concatenation of all the ticket transactions along time axis without any coarsening returns extremely sparse data. Besides, any two consecutive transactions are probably far away with each other in spatial position. RNN model is unable to explore the temporal dependency with such sparse and intermittent data.

-

iv)

Among the traditional regression methods, nonlinear ones like Random Forest (RNFR) and XGBoosting (XGB) clearly outperform linear regression (Linear), which shows that the ticket prediction is (closer to) a nonlinear problem. XGB is slightly better than RNFR, which may be because that in terms of training objective, Boosted Trees(GBM) tries to add new trees that compliment the already built ones. This normally gives better accuracy with less trees.

-

v)

From the comparison between different variants of ETPP, we can clearly see that the two-level loss function, spatial modeling (ConvNet) and temporal modeling (GRU) all contribute to the superior performance of ETPP.

4.4. Effect of Different Coarsening Resolution

In Section 2.2 we describe the coarsening in both spatial and temporal dimensions. Here we discuss the effect of different coarsening resolution.

While splitting space into grids is usually with prior knowledge or guidance (e.g. by the auditorium layout), there can be different options to split along the temporal dimensions. We already explained our strategy in Section 2.2 of using log-scale in time axis. Here we want to show the effect of using different number of bins (L). Figure 7 shows MAPE of our ETPP with different values of . The best result comes with the setting that is not too big or small. The reason is that: very small leads to much less sparsity but fewer samples in time series, which results in dropping useful information; On the other hand, setting too big increases sparsity and makes model unstable. In our experiment we find that gives the best prediction performance for the real-world dataset we used here.

5. Conclusion

In this work, we target on solving the curse of sparsity in predicting event ticket sale price. We design a deep neural network framework which first coarsens the sparse input to dense format, then explores the spatial and temporal dependency, and finally expands the intermediate output back to the original format. Furthermore a bi-level loss function is proposed to get better prediction accuracy. Experiments on real world ticket transaction data proves that our method outperforms the popular baselines in price prediction.

References

- (1)

- Adebiyi et al. (2014) Ayodele Ariyo Adebiyi, Aderemi Oluyinka Adewumi, and Charles Korede Ayo. 2014. Comparison of ARIMA and artificial neural networks models for stock price prediction. Journal of Applied Mathematics 2014 (2014).

- Castilla (2017) Pablo Castilla. 2017. Predict house prices with XGBoost regression.. In https://www.kaggle.com/pablocastilla/predict-house-prices-with-xgboost-regression.

- Chen and Guestrin (2016) Tianqi Chen and Carlos Guestrin. 2016. Xgboost: A scalable tree boosting system. In Proceedings of the 22nd acm sigkdd international conference on knowledge discovery and data mining. ACM, 785–794.

- Chen et al. (2017) Weiling Chen, Yan Zhang, Chai Kiat Yeo, Chiew Tong Lau, and Bu Sung Lee. 2017. Stock market prediction using neural network through news on online social networks. In 2017 International Smart Cities Conference (ISC2). IEEE, 1–6.

- Chung et al. (2014) Junyoung Chung, Caglar Gulcehre, KyungHyun Cho, and Yoshua Bengio. 2014. Empirical evaluation of gated recurrent neural networks on sequence modeling. arXiv preprint arXiv:1412.3555 (2014).

- Groves and Gini (2013) William Groves and Maria Gini. 2013. Optimal airline ticket purchasing using automated user-guided feature selection. In Twenty-Third International Joint Conference on Artificial Intelligence.

- Gumus and Kiran (2017) Mesut Gumus and Mustafa S Kiran. 2017. Crude oil price forecasting using XGBoost. In 2017 International Conference on Computer Science and Engineering (UBMK). IEEE, 1100–1103.

- Hong et al. (2016) Tao Hong, Pierre Pinson, Shu Fan, Hamidreza Zareipour, Alberto Troccoli, and Rob J Hyndman. 2016. Probabilistic energy forecasting: Global energy forecasting competition 2014 and beyond.

- Ke et al. (2017) Jintao Ke, Hongyu Zheng, Hai Yang, and Xiqun Michael Chen. 2017. Short-term forecasting of passenger demand under on-demand ride services: A spatio-temporal deep learning approach. Transportation Research Part C: Emerging Technologies 85 (2017), 591–608.

- Khaidem et al. (2016) Luckyson Khaidem, Snehanshu Saha, and Sudeepa Roy Dey. 2016. Predicting the direction of stock market prices using random forest. Applied Mathematical Finance 0, 0 (2016), 1–20.

- Liu et al. (2018) Xi Liu, Pang-Ning Tan, Zubin Abraham, Lifeng Luo, and Pouyan Hatami. 2018. Distribution Preserving Multi-task Regression for Spatio-Temporal Data. In 2018 IEEE International Conference on Data Mining (ICDM). IEEE, 1134–1139.

- Lu (2017) Jun Lu. 2017. Machine learning modeling for time series problem: Predicting flight ticket prices. arXiv preprint arXiv:1705.07205 (2017).

- Mottini and Acuna-Agost (2017) Alejandro Mottini and Rodrigo Acuna-Agost. 2017. Deep choice model using pointer networks for airline itinerary prediction. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. ACM, 1575–1583.

- Nelson et al. (2017) David MQ Nelson, Adriano CM Pereira, and Renato A de Oliveira. 2017. Stock market’s price movement prediction with LSTM neural networks. In 2017 International Joint Conference on Neural Networks (IJCNN). IEEE, 1419–1426.

- Oh et al. (2015) Junhyuk Oh, Xiaoxiao Guo, Honglak Lee, Richard L Lewis, and Satinder Singh. 2015. Action-conditional video prediction using deep networks in atari games. In Advances in neural information processing systems. 2863–2871.

- Patel et al. (2015) Jigar Patel, Sahil Shah, Priyank Thakkar, and K Kotecha. 2015. Predicting stock and stock price index movement using trend deterministic data preparation and machine learning techniques. Expert Systems with Applications 42, 1 (2015), 259–268.

- Pierdzioch et al. (2015) Christian Pierdzioch, Marian Risse, and Sebastian Rohloff. 2015. Forecasting gold-price fluctuations: a real-time boosting approach. Applied Economics Letters 22, 1 (2015), 46–50.

- Singh et al. (2017) Gurkirt Singh, Suman Saha, Michael Sapienza, Philip HS Torr, and Fabio Cuzzolin. 2017. Online real-time multiple spatiotemporal action localisation and prediction. In Proceedings of the IEEE International Conference on Computer Vision. 3637–3646.

- Ugurlu et al. (2018) Umut Ugurlu, Ilkay Oksuz, and Oktay Tas. 2018. Electricity price forecasting using recurrent neural networks. Energies 11, 5 (2018), 1255.

- Xu et al. (2018) Jianpeng Xu, Xi Liu, Tyler Wilson, Pang-Ning Tan, Pouyan Hatami, and Lifeng Luo. 2018. MUSCAT: Multi-Scale Spatio-Temporal Learning with Application to Climate Modeling.. In IJCAI. 2912–2918.

- Yao et al. (2019) Huaxiu Yao, Xianfeng Tang, Hua Wei, Guanjie Zheng, and Zhenhui Li. 2019. Revisiting spatial-temporal similarity: A deep learning framework for traffic prediction. In AAAI Conference on Artificial Intelligence.

- Yao et al. (2018) Huaxiu Yao, Fei Wu, Jintao Ke, Xianfeng Tang, Yitian Jia, Siyu Lu, Pinghua Gong, Jieping Ye, and Zhenhui Li. 2018. Deep multi-view spatial-temporal network for taxi demand prediction. In Thirty-Second AAAI Conference on Artificial Intelligence.

- Yu et al. (2017b) Bing Yu, Haoteng Yin, and Zhanxing Zhu. 2017b. Spatio-temporal graph convolutional networks: A deep learning framework for traffic forecasting. arXiv preprint arXiv:1709.04875 (2017).

- Yu et al. (2017a) Haiyang Yu, Zhihai Wu, Shuqin Wang, Yunpeng Wang, and Xiaolei Ma. 2017a. Spatiotemporal recurrent convolutional networks for traffic prediction in transportation networks. Sensors 17, 7 (2017), 1501.

- Zhang et al. (2017) Junbo Zhang, Yu Zheng, and Dekang Qi. 2017. Deep spatio-temporal residual networks for citywide crowd flows prediction. In Thirty-First AAAI Conference on Artificial Intelligence.

- Zhang et al. (2019) Junbo Zhang, Yu Zheng, Junkai Sun, and Dekang Qi. 2019. Flow Prediction in Spatio-Temporal Networks Based on Multitask Deep Learning. IEEE Transactions on Knowledge and Data Engineering (2019).