Numerical Schemes for Backward Stochastic Differential Equations Driven by -Brownian motion

Abstract. We design a class of numerical schemes for backward stochastic differential equation driven by -Brownian motion (-BSDE), which is related to a fully nonlinear PDE. Based on Peng’s central limit theorem, we employ the CLT method to approximate -distributed. Rigorous stability and convergence analysis are also carried out. It is shown that the -scheme admits a half order convergence rate in the general case. In particular, for the case of and , the scheme can reach first-order in the deterministic case. Several numerical tests are given to support our theoretical results.

Keywords. backward stochastic differential equation driven by -Brownian motion, -scheme, error estimates, CLT method

AMS subject classifications. 60H35, 65C20, 60H10

1 Introduction

In 1990, Pardoux and Peng in [19] proved the existence and uniqueness of the solution for nonlinear backward stochastic differential equations (BSDEs). Since then, the theory of BSDEs has grown into a indispensable tool in many areas. In particular, it is used to measure financial risk under uncertainty of probabilities. But this type of BSDE is difficult to price path-dependent contingent claims in the uncertain volatility model (UVM). To overcome this obstacle, Peng systemically established a time-consistent fully nonlinear expectation theory and introduced -expectation [20, 21, 22]. Under -expectation framework, a new type of Brownian motion called -Brownian motion was constructed and the corresponding stochastic calculus of Itô’s type was established. Hu et al. [13] obtained the existence and uniqueness of solution for the following fully nonlinear BSDE driven by -Brownian motion (-BSDE for short, in this paper we always use Einstein convention):

| (1.1) |

where is a -dimensional -Brownian motion, , are stochastic processes in for some . Under some regularity conditions on , and , the equation has a unique solution , is a decreasing -martingale. Furthermore, Hu et al. [14] studied nonlinear Feynman-Kac formula under the framework of -expectation (see Theorem 2.3), which built the relationship between -BSDEs and the fully nonlinear PDEs.

-expectation theory and its applications have been developed in recent research [4, 6, 7, 12, 25, 26]. Depending on the underlying volatility, it is well known that the Black-Sholes price can be presented by the solution of BSDEs. Hu and Ji [12] studied the pricing of contingent claims under -expectation. They found that the superhedging and subhedging prices of the given contingent claim are related to , which is the solution of the following -BSDE

where is the return on the riskless asset, and are bounded processes in . Indeed, in the Markovian case, the superhedging and subhedging prices are the Black-Scholes prices with volatilities and respectively. Therefore, proposing an efficient numerical approach to approximate the process has important practical significance.

Based on contingent claim pricing models, we devote to designing a numerical scheme for the following type of -BSDE

| (1.2) |

where is a -dimensional -Brownian motion defined in the -expectation space , and are bounded processes in , and , satisfy the following properties:

-

(H1)

There exists a constant such that for any ;

-

(H2)

There exists a constant such that

Tremendous efforts have been made on the numerical computing of BSDEs (see, e.g., [1, 2, 3, 5, 9, 10, 17, 18, 27, 28, 29, 30, 31] and references therein), but little attention has been paid to -BSDEs. There are some technical obstacles in developing numerical schemes for -BSDEs. On the one hand, owing to the sublinear nature of -expectation, many conclusions under linear expectation can not be extended to -expectation, which increases the difficulty of theoretical analysis. On the other hand, there is no integral representation for -normal distributed, traditional numerical integration methods of normal distribution are no longer applicable.

Zhao [29] proposed a -scheme to solve BSDEs directly, which is highly efficient and accurate. Unlike classical BSDEs, it is difficult to present a numerical scheme for -BSDEs directly. To overcome it, we construct an auxiliary extended -expectation space and design a new -scheme for solving of the -BSDE in this space. Furthermore, on the basis of Peng’s central limit theorem [23], we use the CLT method to approximate -distributed. Full stability and convergence analysis are also derived. It is shown that our -scheme admits a half order rate of convergence in the general case. In particular, for the case of and , our schemes can reach first-order convergence in the deterministic case. To the best of our knowledge, this is the first attempt to design numerical schemes for -BSDEs.

For simple representations, we introduce some notations that will be used extensively throughout the paper:

-

•

the standard Euclidean norm in and .

-

•

continuous functions such that , , , . Note: means that is a Lipschitz continuous function

-

•

continuously differentiable functions with uniformly bounded partial derivatives and for and .

-

•

the conditional -expectation of , under the -field , i.e. .

The paper is organized as follow. In Section 2, we recall some basic notations and results for stochastic calculus under -framework. In Section 3, we propose a class of -schemes for -BSDEs by choosing different parameters . The analysis of stability and convergence is separately discussed in Section 4 and 5. In Section 6, we employ the CLT method for -distributed simulation and conclude the paper in Section 7 with numerical examples that illustrate the performance of our schemes.

2 Preliminaries

The main purpose of this section is to recall some basic notions and results of -Expectation, -Brownian motion and -BSDEs, which are needed in the sequel. More details can refer to [20, 21, 22] and references therein.

2.1 -Brownian motion

Definition 2.1

Let be a given set and let be a linear space of real valued functions defined on , satisfies for each constant and if . is considered as the space of random variables. A sublinear expectation on is a functional : satisfying the following properties: for all , we have

-

Monotonicity: If then

-

Constant preservation:

-

Sub-additivity:

-

Positive homogeneity: for each

is called a sublinear expectation space. From the definition of the sublinear expectation , the following results can be easily obtained.

Proposition 2.2

For , we have

-

for each

-

If , then

-

i.e.

-

for with

Definition 2.3

Let and be two -dimensional random vectors defined respectively in sublinear expectation spaces and . They are called identically distributed, denoted by , if , for all , the space of bounded Lipschitz continuous functions on .

Definition 2.4

In a sublinear expectation space , a random vector , , is said to be independent from another random vector , under , denoted by , if for every test function we have .

Definition 2.5

A -dimensional random vector in a sublinear expectation space is called -normally distributed if for each we have

where is an independent copy of , denotes the function

where denotes the collection of symmetric matrices. We assume that is non-degenerate, i.e., there exist some constants such that for . Then there exists a bounded and closed subset such that

where denotes the collection of nonnegative elements in . In this paper, we also assume

Now we give definitions of -Brownian motion, -expectation and conditional -expectation.

Definition 2.6

Let , the space of real valued continuous functions on with , be endowed with the supremum norm. Set

-expectation on is a sublinear expectation defined by

for all , , where are identically distributed -dimensional -normally distributed random vectors in a sublinear expectation space such that is independent from , The corresponding canonical process is called a -Brownian motion and is called a -expectation space.

Definition 2.7

We assume that has the representation , define the conditional -expectation of , for some

where

Define for and . Then can be extended continuously to the completion of under the norm .

Proposition 2.8

For , we have

-

(I)

for

-

(II)

for

-

(III)

for

-

(IV)

2.2 -Itô’s formula and Feynman-Kac formula

Set

For and , let d and denote by the completion of under .

For each , we denote by the mutual variation process. We can define Itô’s integrals and , for two processes and (see [20, 21, 22]).

Consider the following -dimensional process:

| (2.1) |

where Now we give the following -Itô’s formula.

Theorem 2.9 ([22])

Let be a -function on such that satisfy polynomial growth condition for . Let and , be bounded processes in . Then for each we have

| (2.2) | ||||

Theorem 2.10 ([14])

Let the functions , be continuous with respect to and Lipschitz continuous with respect to , be an Lipschitz continuous function. Then the unique solution of -BSDEs can be represented as , where is the unique viscosity solution of the following PDE:

| (2.3) |

where

3 Numerical schemes for -BSDEs

3.1 Explicit expression of

Without loss of generality, we only consider the case of . The results still hold for the case . Let , the space of -valued continuous functions on with . we consider the following type of -BSDE defined in the -expectation space

| (3.1) |

where satisfy (H1)-(H2), and are bounded processes in .

To get the explicit expression of excluding , we construct an auxiliary extended -expectation space with and

To simplify presentation, we still denote by the extended -expectation in the sequel. Let be the canonical process in the extended space, it is easy to check that

Now, introducing the following linear -SDE:

| (3.2) |

it is easy to verify that

| (3.3) |

Applying Itô’s formula to , we obtain

By Lemma 3.4 in [13], is a -martingale. Thus we get the explicit expression of excluding

| (3.4) |

where .

3.2 The semi-discrete scheme

For the time interval , we introduce the following partition:

| (3.5) |

with and . We denote and with and , respectively, for . We also denote quadratic variation processes and , for .

Let and . From we can obtain

| (3.6) |

where

| (3.7) |

It is easy to verify that satisfies the following -SDE

| (3.8) |

Similar to numerical integration methods, using the -scheme to approximate the stochastic integrals in , we have

| (3.9) |

where , with

| (3.10) | ||||

and

| (3.11) | ||||

In the meanwhile, we employ Euler’s method to approximate the stochastic integrals in , denoted by , then

| (3.12) | ||||

Replacing with in , we get the following reference equation

| (3.13) |

where

| (3.14) | ||||

Let denote the numerical approximation to the analytic solution at time level . To maintain the consistency of representation, we use to denote . Based on , we propose the following semi-discrete -scheme for solving of the -BSDE .

Scheme 1

Given random variables , solve random variables , from

| (3.15) |

with the deterministic parameters .

Remark 3.1

Usually, we pay more attention to the solution of the -BSDE , which reflects the hedging price of a given contingent claim. By introducing the -SDE, we obtained the scheme 1 for solving , which can be excluded completely.

Remark 3.2

By choosing different , we can obtain a class of different -schemes for solving the solution of the -BSDE. Our -schemes can admit a first order rate of convergence when and in the deterministic case, which will be confirmed in later numerical experiments.

4 Stability analysis

In this section, we focus on the stability analysis of the numerical scheme. In what follows, represents a generic constant, which may be different from line to line.

Lemma 4.1

Let , be bounded processes. Then for all , ,

-

1.

and ;

-

2.

and ,

where is a constant independent of , and are defined in and , respectively.

Proof. 1. For all from we know

| (4.1) |

Notice that , applying -Itô’s formula to , we get

| (4.2) |

From the proposition 2.2, we have . Through the properties of quadratic variation and , , we have

Similar to the above process, we can deduce

| (4.3) |

It is easy to verify that , . Therefore, for bounded processes , and sufficiently small , we draw the conclusion 1. Similarly, we can prove 2.

Theorem 4.2

Let be the solution of the -BSDE and defined in the Scheme 1, and are defined in and , respectively. Assume that and satisfy (H1)-(H2) with Lipschitz constant Then for sufficiently small time step we have

| (4.4) |

for , is a constant just depending on and upper bounds of and .

Proof. Let , and , for . Subtract from , by Proposition 2.2 , we get

| (4.5) |

Using , implies

| (4.6) |

where is the Lipschitz constant. From the inequality , we obtain

| (4.7) | ||||

Taking square on both side of , using the inequalities , Hölder’s inequality and Lemma 4.1, we deduce

| (4.8) |

Taking -expectation on both sides of and substituting , recursively, we consequently deduce that

| (4.9) |

The proof is complete.

5 Error estimates

In this section, we will discuss the error estimates of Scheme 1 for the -BSDE with Under some regularity conditions on and , we first give the estimates of truncation errors and defined in and -. Then we come to the conclusion based on Theorem 4.2.

Lemma 5.1

Let be the local truncation error derived from . Then for sufficiently small time step and , we have the following conclusions:

-

1.

If , are bounded stochastic processes on and , we have

(5.1) -

2.

In particular, if , are Lipschitz continuous functions on and , we have

(5.2)

Here is a constant just depending on , , upper bounds of and .

Proof. 1. From the definition of in and Proposition 2.2 , we can deduce

| (5.3) | ||||

| (5.4) | ||||

Firstly, we give the estimate of . can be similarly obtained. According to , and Proposition 2.8 , it is worth noting that

| (5.5) |

Then, by Proposition 2.2 , we obtain

| (5.6) |

Under the conditions and Theorem 2.10, it is easy to check that . By Hölder’s inequality, we obtain

| (5.7) |

Notice that

| (5.8) |

and

| (5.9) |

Combing , , and , we have

| (5.10) | |||

Similar to Lemma 4.1, we can prove . Using Hölder’s inequality again, we obtain

| (5.11) | |||

If and are bounded stochastic processes in , due to , , by simple calculation, we get

| (5.12) |

Combing and , from Gronwall’s inequality, it follows that

| (5.13) |

Then from , and , we have

In the same way above, we can also obtain and , follows from

2. In particular, if , applying Itô’s formula to on and taking the conditional -expectation , we have

| (5.14) |

From and Hölder’s inequality, we can deduce

| (5.15) | |||

Since , are Lipschitz continuous functions on , from and , we can easily obtain

Similarly to prove above, holds.

Lemma 5.2

Assume that is a process in and , is a constant. Then

| (5.16) |

Remark 5.3

Lemma 5.4

Let be the local truncation error derived from -. Assume and are bounded processes. Then for sufficiently small , it holds that:

-

1.

For if , we have

(5.21) -

2.

In particular, for and , if , we have

(5.22)

Here is a constant just depending on , , upper bounds of and , upper bounds of derivatives of and .

Proof. 1. From the definition of and , we have

| (5.23) | ||||

and

| (5.24) |

We just give the estimate of the first part of , the second part can be similarly obtained. If , from Theorem 2.10, we know . Then

| (5.25) | |||

Combining , and Lemma 4.1, it is easy to check that . Similarly, we have . Thus, is proved.

2. If , , , by Theorem 2.10, we define and . Applying Itô’s formula to , we have

| (5.26) |

From , we can deduce

| (5.27) | |||

Notice that and , which implies

| (5.28) | |||

Then, . When , applying Itô’s formula to , we can similarly obtain

| (5.29) | |||

From Lemma 5.2, we have

| (5.30) |

Then, from , , and , by a simple computation similar to , it is straightforward to obtain . Therefore, holds.

Based on the discussion above, let us show the error estimates of Scheme 1.

Theorem 5.5

Let be the solution of the -BSDE and defined in the Scheme 1. Then for sufficiently small , it holds that:

-

1.

For if and , are bounded stochastic processes in , we have

(5.31) -

2.

In particular, for and if and , are Lipschitz continuous functions on , we have

(5.32)

Here is a constant just depending on upper bounds of and , upper bounds of derivatives of and .

-

1.

For if , and are bounded stochastic processes in , we have

(5.33) -

2.

In particular, for and if , and are Lipschitz continuous functions on , we have

(5.34)

Using Theorem 4.2, the conclusion can be directly obtained.

6 -distributed simulation

In this section, we first present the CLT method to approximate the -distributed. Then we propose a fully discrete -scheme for solving of the -BSDE .

6.1 CLT method for -distributed

Before giving the CLT method, we first recall the definition of -distributed and Peng’s central limit theorem.

Definition 6.1

The pair -dimensional random vectors in a sublinear expectation space is called -distributed if for each we have

where is an independent copy of , denotes the binary function

From the definition above, it is easy to check that is a -distributed.

Theorem 6.2 ([22, 23])

Let be a sequence of -valued random variables on a sublinear expectation space . We assume that and is independent from for each We further assume that . Then for each function satisfying linear growth condition, we have

| (6.1) |

where the pair is -distributed. The corresponding sublinear function is defined by

Since Peng’s central limit theorem, a great deal of work has been done to prove the following rate of convergence (see [8, 16, 15, 25, 26])

| (6.2) |

where is a constant depending on , and .

CLT method. Assume is a positive integer. Using the property of independence, we have

| (6.3) |

Denote as the approximation of . By choosing appropriate random variables , the numerical approximation of can be obtained, we call it the CLT method for -distributed. The following error estimate is straightforward

| (6.4) |

with converge to 0 with the convergence rate , as . So we can select a proper in the CLT method to approximate the -expectation with the required accuracy.

6.2 The fully-discrete scheme

To propose a fully-discrete scheme, we introduce the following space partition :

| (6.5) |

with the space step and the maximum space step .

Now by , we solve at the time-space point in the following form:

| (6.6) |

where and are truncation errors defined in - and ,

Here is the interpolation value at the point . is an approximation of by using the CLT method, and corresponding approximation error converge to 0 as .

Based on , by omitting numerical errors , and , we propose the following fully-discrete -scheme for solving of the -BSDE :

Scheme 2

Denote as a numerical solution to the analytic solution of the -BSDE at the time-space point . Given the random variable , , solve by

| (6.7) |

with the deterministic parameters .

Here is the interpolation value of at the point . is grid discrete approximation of the with and . is the approximation of the conditional -expectation by using the CLT method. More precisely, we take the special case as an example:

where is the interpolation approximation of at spacial non-grid point , is a positive integer. In our numerical experiments, we choose the sequence of discrete random variables

| (6.8) |

with uncertainty , , and , for all . In the same way, the conditional -expectation in Scheme 2 can be defined.

Remark 6.3

Notice that the spacial mesh is essentially unbounded. However, in real computations, we are interested in acquiring certain values of at with belonging to a bounded domain. In fact, , where is the truncation error. If is a bounded function, the truncation error is negligible when see Section 4.2 in [24] for more details.

7 Numerical experiments

In this section, some numerical calculations have been carried out to illustrate the high accuracy of our numerical schemes. In our numerical experiments, we let and select a appropriate in the CLT method. We also apply cubic spline interpolation to compute spatial non-grid points. Set the initial time and terminal time . In the following tables, denotes the absolute error between the exact and numerical solution for at . We shall denote by ”CR” the convergence rate.

Example 7.1

Consider the following linear -BSDE

| (7.1) |

The analytic solution of is

| (7.2) |

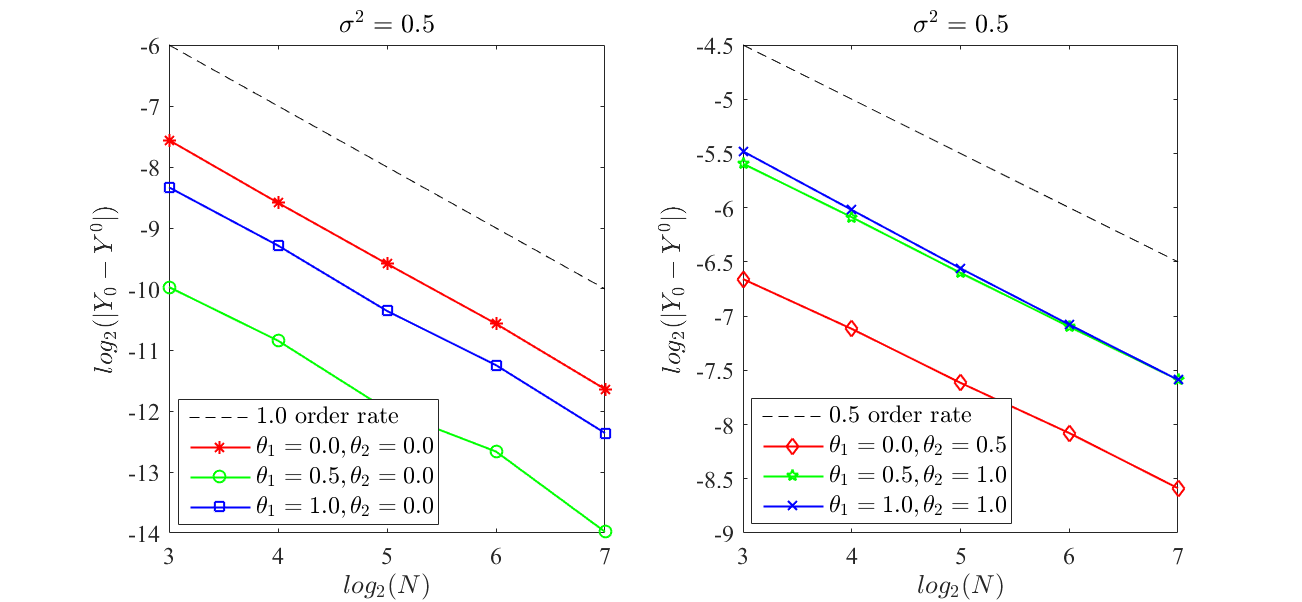

The solution at initial time is . Errors and convergence rates for different time partitions and different are listed in Table 1. Figure 1 shows the convergence rates of the -scheme for time step varying from to with different parameters . By contrast, we can clearly see that the convergence rate of the -scheme is highly correlated with . For , the scheme is half-order convergence with . When the scheme can achieve first order, which is consistent with our theoretical analysis.

Example 7.2

Consider the following nonlinear -BSDE

| (7.3) |

where , with the mollifier and the convolution

The analytic solution of is . Then at initial time is .

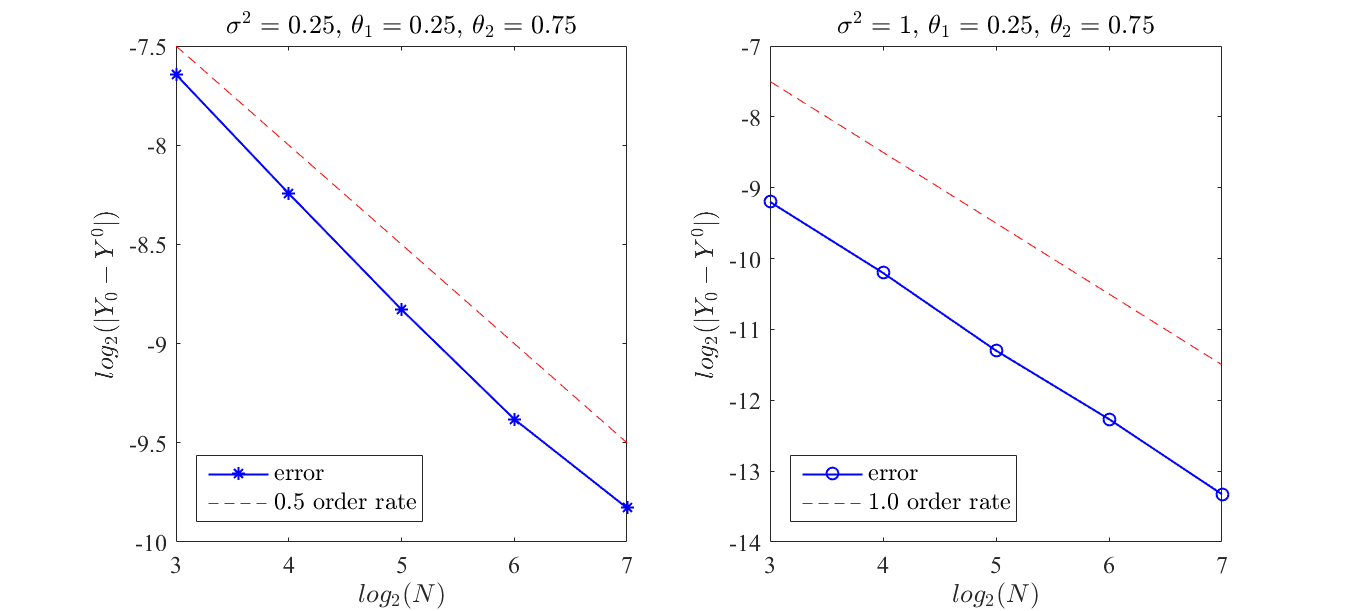

Errors and convergence rates for different time partitions of the -scheme with different parameters are listed in Table 2. Figure 2 presents convergence rates of the -scheme under different uncertainty . When , -Brownian motion is reduced to a standard Brownian motion, the -scheme can reach first order for , which coincides with Zhao [29].

8 Conclusions

In this paper, we design a new kind of -scheme to approximate the solution of the -BSDE . By choosing different , a class of numerical schemes have been obtained which provide useful tools for dealing with the pricing of contingent claims. We also analyze the stability of our numerical schemes and strictly prove the error estimates. As discussed in section 5, the -scheme admits a half order convergence rate in the general, and when , the scheme can reach first-order in the deterministic case. In addition, based on Peng’s central limit theorem, we employ the CLT method to approximate -distributed for the first time. Several numerical examples are presented to show the effectiveness of our numerical schemes.

References

- [1] V. Bally, Approximation scheme for solutions of BSDE, in Backward Stochastic Dfferential Equations, Pitman Res. Notes Math. 364, Longman, Harlow, UK, 1997, pp. 177-191.

- [2] C. Bender and R. Denk, A forward scheme for backward SDEs, Stochastic Process. Appl., 117 (2007), pp. 1793-1812.

- [3] D. Chevance, Numerical methods for backward stochastic differential equations, “Numerical Methods in Finance,” Publ. Newton Inst., Cambridge Univ. Press, Cambridge, (1997), pp. 232-244.

- [4] L. Denis, M. Hu, and S. Peng, Function spaces and capacity related to a sublinear expectation: application to GBrownian motion paths, Potential Anal., 34 (2011), pp. 139-161.

- [5] W. E, J. Han, and A. Jentzen, Deep Learning-Based Numerical Methods for High-Dimensional Parabolic Partial Differential Equations and Backward Stochastic Differential Equations, Commun. Math. Stat., 5 (2017), no. 4, pp. 349-380.

- [6] L. Epstein and S. Ji, Ambiguous volatility and asset pricing in continuous time, Review of Financial Studies, 26 (2013) pp. 1740-86.

- [7] L. Epstein and S. Ji, Ambiguous volatility, possibility and utility in continuous time. J. Math. Econom., 50 (2014), pp. 269-282.

- [8] X. Fang, S. Peng, Q. Shao, and Y. Song, Limit theorems with rate of convergence under sublinear expectations, Bernoulli, 25 (2019), pp. 2564-2596.

- [9] E. Gobet, J.-P. Lemor, and X. Warin, A regression-based Monte Carlo method for backward stochastic differential equations, Ann. Appl. Probab., 15 (2005), pp. 2172-2202.

- [10] E. Gobet and P. Turkedjiev, Linear regression MDP scheme for discrete backward stochastic differential equations under general conditions, Math. Comput., 85 (2016), pp. 1359-1391.

- [11] M. Hu, Explicit solutions of -heat equation with a class of initial conditions by -Brownian motion, Nonlinear Anal., 75 (2012), pp. 6588-6595.

- [12] M. Hu and S. Ji, A note on pricing of contingent claims under -expectation, 2013. arXiv:1303.4274 [math.PR].

- [13] M. Hu, S. Ji, S. Peng, and Y. Song, Backward stochastic differential equations driven by -Brownian motion, Stoch. Proc. Appl., 124 (2014), pp. 759-784.

- [14] M. Hu, S. Ji, S. Peng, and Y. Song, Comparison theorem, Feynman-Kac formula and Girsanov transformation for BSDEs driven by -Brownian motion, Stoch. Proc. Appl., 124 (2014), pp. 1170-1195.

- [15] S. Huang and G. Liang, A monotone scheme for -equations with application to the convergence rate of robust central limit theorem, 2019. arXiv:1904.07184 [math.PR] [math.NA].

- [16] N. V. Krylov, On Shige Peng’s central limit theorem, Stochastic Process, Appl., (2019), in press.

- [17] J. Ma and J. Zhang, Representations and regularities for solutions to BSDEs with reflections, Stochastic Process. Appl., 115 (2005), pp. 539–569.

- [18] G. N. Milstein and M. V. Tretyakov, Numerical algorithms for forward-backward stochastic differential equations, SIAM J. Sci. Comput., 28 (2006), pp. 561-582.

- [19] E. Pardoux and S. Peng, Adapted solution of a backward stochastic differential equation, Systems Control Lett., 14 (1990), pp. 55-61.

- [20] S. Peng, G-expectation, G-Brownian motion and related stochastic calculus of Itô type, in: Stochastic Analysis and Applications, in: Abel Symp., vol. 2, Springer, Berlin, 2007, pp. 541-567.

- [21] S. Peng, Multi-dimensional -Brownian motion and related stochastic calculus under -expectation, Stochastic Process. Appl., 118 (12) (2008), pp. 2223-2253.

- [22] S. Peng, Nonlinear expectations and stochastic calculus under uncertainty, 2010. arXiv:1002.4546v1 [math.PR].

- [23] S. Peng, Law of large numbers and central limit theorem under nonlinear expectations, Probab. Uncertain. Quant. Risk., 4 (2019), Paper No. 4, 8

- [24] S. Peng, S. Yang, and J. Yao, Improving Value-at-Risk prediction under model uncertainty, 2019. arXiv:1805.03890 [q-fin.RM].

- [25] Y. Song, Normal Approximation by Stein’s Method under Sublinear Expectations, 2017. arXiv:1711.05384 [math.PR].

- [26] Y. Song, Stein’s Method for Law of Large Numbers under Sublinear Expectations, 2019. arXiv:1904.04674 [math.PR].

- [27] J. Zhang, A numerical scheme for BSDEs, Ann. Appl. Probab., 14 (2004), pp. 459-488.

- [28] Y. Zhang and W. Zheng, Discretizing a backward stochastic differential equation, Int. J. Math. Math. Sci., 32 (2002), pp. 103-116.

- [29] W. Zhao, L. Chen, and S. Peng, A new kind of accurate numerical method for backward stochastic differential equations, SIAM J. Sci. Comput., 28 (2006), pp. 1563-1581.

- [30] W. Zhao, Y. Fu, and T. Zhou, New kinds of high-order multistep schemes for coupled forward backward stochastic differential equations, SIAM J. Sci. Comput., 36 (2014), pp. A1731-A1751.

- [31] W. Zhao, J. Wang, and S. Peng, Error Estimates of the -Scheme for Backward Stochastic Differential Equations, Dis. Cont. Dyn. Sys. B, 12 (2009), pp. 905-924.