dcu

Semiparametric Quantile Models for Ascending Auctions with Asymmetric Bidders

Abstract

The paper proposes a parsimonious and flexible semiparametric quantile regression specification for asymmetric bidders within the independent private value framework. Asymmetry is parameterized using powers of a parent private value distribution, which is generated by a quantile regression specification. As noted in \citeasnounCantillon2008, this covers and extends models used for efficient collusion, joint bidding and mergers among homogeneous bidders. The specification can be estimated for ascending auctions using the winning bids and the winner’s identity. The estimation is in two stage. The asymmetry parameters are estimated from the winner’s identity using a simple maximum likelihood procedure. The parent quantile regression specification can be estimated using simple modifications of \citeasnounGimenes2017. Specification testing procedures are also considered. A timber application reveals that weaker bidders have less chances to win the auction than stronger ones. It is also found that increasing participation in an asymmetric ascending auction may not be as beneficial as using an optimal reserve price as would have been expected from a result of \citeasnounBulowKlemperer1996 valid under symmetry.

JEL: C14, D44

Keywords: Private values; asymmetry;

ascending auctions; seller expected revenue; quantile regression; two stage quantile regression estimation.

Nathalie Gimenes and Emmanuel Guerre acknowledge the British Academy and Newton Fund for generously funding this project (reference code: AF150085). Nathalie Gimenes thanks Ying Fan and Ginger Jin for very useful comments. Many comments from seminar and conference participants have helped to improve the paper.

1 Introduction

Asymmetry among bidders may arise from many factors, for example, differences in taste or specialization, degree of information, productivity, costs, firm size, joint bidding or collusion among a subgroup of buyers. It is, therefore, likely that symmetric bidding is only a theoretical approximation that may not fit well many auction markets. Within the independent private value paradigm (IPV hereafter), the revenue equivalence theorem no longer holds with asymmetric bidders and first-price auction can be inefficient, see \citeasnounKrishna2009 and the references therein. \citeasnounCantillon2008 supports the common belief that competition is reduced by bidders’ asymmetries. She shows that asymmetry decreases the seller expected revenue in first-price and second-price auctions, when compared to revenues achieved with a benchmark symmetric private value distribution. The timber auction revenue analysis of \citeasnounRobertsSweeting2016 shows that reducing the participation of strong bidders can considerably lower the seller expected revenue.

Myerson1981 suggests to depart from standard formats and describes an optimal auction which restores some competition by handicapping strong bidders. This mechanism critically involves the private value distribution and is difficult to implement. In an empirical study of snow removal contract sealed procurements, \citeasnounFlambardPerrigne2006 considered this optimal auction and an alternative subsidy policy. \citeasnounKrasnokutskayaSeim2011 studied a bid preference program for California highway auction, see also \citeasnounMarion2007. \citeasnounAtheyCoeyLevin2013 focused on set-asides and subsidies for timber auctions.

Among the aforementioned empirical works, the only papers adopting a nonparametric approach are \citeasnounFlambardPerrigne2006 and \citeasnounMarion2007, who studied first-price auctions. For first-price auctions, \citeasnounKrasnokutskayaSeim2011, \citeasnounAtheyLevinSeira2011 and \citeasnounAtheyCoeyLevin2013 all considered parametric specifications, as did \citeasnounRobertsSweeting2016 for ascending auctions.

There are, however, some works devoted to the nonparametric approach for ascending auctions with asymmetric bidders. A theoretical nonparametric identification result with a finite number of asymmetric types, due to \citeasnounKomarova2013a, shows that the asymmetric valuation distributions can be recovered from the winning bid and the identity of the winner under IPV, see also \citeasnounAtheyHaile2002. \citeasnounBendstrupPaarsch2006 have proposed a related semi-nonparametric estimation procedure. \citeasnounLamy2012 shows that nonparametric identification still holds under anonymity for second-price auctions when all the bids are observed. Set identification results are also available for affiliated models, which are not point identified as shown by \citeasnounAtheyHaile2002. For affiliated values and second-price auction, \citeasnounKomarova2013b gives bounds for joint private value distribution, assuming identities are available. \citeasnounCoeyLarsenSweeneyWaisman2017 consider a more difficult scenario, where only the winning bid is observed and anonymity is possible. They obtain bounds for the seller expected revenue and bidder surplus which extends upon the ones of \citeasnounAradillasGandhiQuint2013 for the symmetric case.

Developing nonparametric approaches for asymmetric bidders with a discrete number of types is difficult, because a different value distribution must be estimated for each types, as in \citeasnounFlambardPerrigne2006 or \citeasnounBendstrupPaarsch2006. Dividing the sample in subsamples defined by a given type may result in small subsamples in addition to poor nonparametric estimation rates due to the curse of dimensionality. Comparing the valuation distribution across types is not an easy task. In this paper, we tackle these two issues through a semiparametric approach allowing for a nonparametric component common to each type and using a parametric description of type heterogeneity. The common nonparametric component is a parent private value conditional distribution , where is an auction product-specific covariate. Following \citeasnounGimenes2017, we assume that corresponds to a quantile regression model, so that this rich and flexible specification can be estimated with a standard parametric rate independently of the dimension of . The asymmetry parameter, say , is an exponent specific to bidder , whose private value distribution is

The exponent can be an individual fixed effect which captures unobserved bidder characteristics. As developed in the paper, it can also be a parametric function of some observed bidder variables and fixed effect parameters. In our timber application, the buyers are either mill or logger, which are considered as weak and strong bidders respectively in all applications.

Cantillon2008 has used a similar specification for theoretical illustration purpose, noting that it has been used to “model efficient collusion, joint bidding and mergers among homogeneous bidders”, which can be relevant for many applications. Indeed, when is an integer number, is the distribution of the maximum value of symmetric bidders with independent valuations drawn from , as relevant, for instance, in joint bidding. This feature also shows that the asymmetry parameter is a measure of the “strength” of bidder . A small numerical experiment in the paper parallels \citeasnounCantillon2008, adopting an econometric point of view based on the symmetric private value distribution which would be estimated ignoring asymmetry by the quantile procedure of \citeasnounGimenes2017. Such a misspecification may lead to underestimation of the optimal reserve price and seller expected revenue.

The proposed estimation is in two stage, based upon the winning bid and identity of the winner. The first stage estimates the parameters appearing in the asymmetry exponent using a maximum likelihood procedure based upon the winner identity. The intuition behind this procedure is that the distribution of the winner identity only depends upon the relative buyers’ strength, and hence on asymmetry parameter and not upon the common parent distribution . The second stage estimates the quantile regression specification associated with . As in \citeasnounGimenes2017, it is based on a quantile regression estimation and uses individual transformations of quantile levels, which must be estimated under asymmetry. Accounting for asymmetry leads to considering a transformation which depends upon the estimated asymmetry parameter. This latter step parallels \citeasnounArellanoBonhomme1207, who similarly estimate a quantile level transformation in a three stage quantile regression procedure.

The empirical application illustrates the methodology using USFS timber ascending auctions. Two kinds of firms are competing: firms with manufacturing capacity (mills, usually considered as strong bidders in the literature) and firms lacking manufacturing capabilities (loggers). We take advantage of recent advances in the quantile-regression specification literature to illustrate how well the proposed model fits the data. The estimated asymmetry exponent of the loggers is less than the one of the mills, suggesting that, roughly speaking, two mills should be replaced by three loggers to generate an ascending auction with similar features. The empirical application also studies the seller expected revenue as a function of the proportion of loggers and the number of buyers. It reveals economically significant variations, in the range of between ascending auctions attended only by loggers or only by mills. In small auctions with two bidders, changing a logger by a mill can increase the seller optimal expected revenue by in some cases, and still as high as with 12 bidders. This suggests that seller expected revenue bounds that do not account for the proportion of each type can be considerably large, and that the ones averaging over types participation, as in \citeasnounCoeyLarsenSweeneyWaisman2017, can be less informative. Another finding relates to an important result of \citeasnounBulowKlemperer1996 stating that, under symmetry, increasing participation is more beneficial than using an optimal auction. Several violations of this result are observed, especially due to the presence of weak bidders.

The paper is organized as follows. Section 2 presents the auction setup and the asymmetric quantile specification. Sections 2.2 and 2.3 give the identification strategy and discuss identification of the parameter of asymmetry under several specifications. Section 3 shows how to design the optimal reserve price policy when bidders are asymmetric and studies the consequences of a symmetric misspecification for the seller’s expected revenue. The two-step estimator is proposed in Section 4 and its asymptotic distribution is obtained. A simulation of the methodology is given in Section 5 and an empirical application using USFS timber ascending auctions is studied in Section 6. The proofs of all the results given in the paper are grouped in the Appendix A. Appendix B details the test procedures used in the application. Appendix C contains tables not displayed in the application section to save space.

2 Semiparametric quantile specifications

A single and indivisible object with observed characteristics is auctioned to bidders through an ascending auction. Each bidder has a specific characteristic , . The auction covariates , the number of bidders participating in the auction and the associated bidder covariates , are common knowledge to buyers and sellers, and observed by the analyst. Within the IPV paradigm, each bidder is assumed to have a private value for the auctioned good, which is not observed by other bidders. The bidder only knows his own private value, but it is common knowledge for bidders and sellers that each private value has been independently drawn from a c.d.f. conditional upon , , or equivalently, with a conditional quantile function

| (2.1) |

It will be assumed later on that the analyst observes identically drawn auctions. For each auction , the winning bid and winner’s identity, the number of bidders, the product-specific covariate and the bidder characteristics are observed. As shown later, the assumption that the identity of the winner is observed can be relaxed when bidders are characterized using discrete types. In this case, it is sufficient to observe the type of the winner and the numbers of bidders within a given type.

As in the symmetric private value setting, the dominant strategy for non-winners is to bid up to their true valuation. It will, therefore, be assumed that

Assumption 1

The winning bid is the second-highest bidder’s private value.

See \citeasnounBendstrupPaarsch2006, \citeasnounAradillasGandhiQuint2013, \citeasnounCoeyLarsenSweeneyWaisman2017, and \citeasnounGimenes2017 for similar assumptions and related discussions, and \citeasnounHaileTamer2003 for a more general incomplete game framework.

2.1 Asymmetric private value quantile specification

The proposed model combines an asymmetry function known up to parameters

| (2.2) |

with a parent conditional distribution which only depends upon the product-specific covariates and is generated by a quantile-regression model111Our approach carries over with minor modifications for other quantile semiparametric specifications, such as the exponential one .

| (2.3) |

assuming that the first entry of is a constant term. In (2.2), the are bidder fixed effects parameter which can capture some unobserved bidder heterogeneity. In what follows .

The quantile regression specification (2.3) can be interpreted as follows. In the symmetric case where the private values are drawn from the parent distribution, the random quantile level , which indicates the rank of bidder in the private value distribution, is a measure of efficiency. As , the quantile regression model postulates an additive but linear contribution of the auction characteristics to bidder private value. This contribution is summarized by the slope coefficient , which does not need to be constant in most of its components as it would be for a regression model. This adds some flexibility and was found useful in our application. Under asymmetry, it holds by (2.5) below, so that a larger asymmetry coefficient gives a closer to , increasing the private value for a given efficiency .

Assumption 2

Cantillon2008 refers to distributions of the type of (2.4) as a class of distributions for which a quasi-ordering of potential bidders is available. This specification accommodates asymmetries that arise from merger, joint bidding or collusion among homogeneous bidders. See e.g. \citeasnounGrahamMarshall1987, \citeasnounMailathZemsky1991, \citeasnounMcafeeMcmillan1992, \citeasnounBrannmanFroeb2000 and \citeasnounWaehrerPerry2003.

Assumption 2 is equivalent to the quantile specification

| (2.5) |

which shows that asymmetry comes from a bidder specific transformation of the quantile level . As detailed below, the power specification is particularly convenient to establish identification. Examples of are given later on. The slope coefficient is the nonparametric element of the model. It can, however, be estimated with a parametric rate as expected from the quantile regression and shown later on. The asymmetric power exponent measures the bidder strength: if then bidder dominates bidder in a first-order stochastic dominance sense, i.e. with a strict inequality inside the common support of these distribution. Note that the private value distributions have the same support of the parent distribution. When goes to infinity, converges to while it goes to when goes to .

Additional standard assumptions on the parent quantile slope function and the function are as follows. In the last assumption, is the compact set of admissible asymmetry parameters and is the compact support of the bidder characteristic .

Assumption 3

The vector of auction specific variables, , has a dimension of . The random vector has a compact support . The matrix has an inverse.

Assumption 4

is continuously differentiable over with a derivative which is strictly positive for all in .

Assumption 5

It holds that . The function is twice continuously differentiable with respect to and . The true value of the asymmetry parameter lies in the interior of .

2.2 Identification

The proposed identification procedure is in two steps, which are constructive enough to develop a simple estimation procedure. The first step aims to identify the bidder asymmetry parameters and from the observed winner’s identity. Let be the c.d.f. of the winning bid given that bidder wins the auction, given covariates and . Define also

| (2.6) |

where

The next Lemma describes the joint distribution of the winner’s identity and the winning bid.

Suppose that the system of equations with unknowns and in

| (2.9) |

has a unique solution, and . Then, Lemma 1 shows that the winner’s identity distribution identifies the asymmetry parameters and . Identification on a case by case basis with examples of functions and parameter set ensuring identification of the asymmetry parameters is given in the next section. The probability of winning is very often used to assess the presence of asymmetry among the bidders, see \citeasnounLaffontOssardVuong1995, \citeasnounFlambardPerrigne2006 for first-price sealed bid auctions and \citeasnounBendstrupPaarsch2006 for ascending auctions.

Identification of the parent quantile regression slope follows in a second step, using the winning bid c.d.f. given that bidder wins the auction in (2.8). The proof of Proposition 2 yields that is strictly increasing. Therefore the conditional winning bid quantile function given that wins is

and then

| (2.10) |

Identification of easily follows as stated in the next Proposition.

2.3 Identified bidder asymmetry specifications

Establishing identification of the asymmetry parameter is essential, which holds for the following standard choice of the function under proper standardization of the asymmetry parameter. For the third and fourth examples given below, it is useful to assume that the bidder covariate varies across auctions.

Example 1: Bidder fixed effects.

In this example , and (2.9) shows that asymmetry parameter identification holds provided the system of equations with unknown in

has a unique solution. As well known, this is ensured when

that is, the parent private value distribution is the first bidder private value distribution.222It is however possible to identify , strengthening Assumption 4 to ensure exists and is strictly positive over . If so it holds for , is equivalent to , showing that is identified from the lower tail of the identified parent private value distribution. Implementing this in practice may however give nonparametric consistency rates and is therefore not attempted here. Alternatively the simplex is also possible.

Example 2: Linear regression.

The case of the regression specification is particularly useful when the covariate codes bidder types.333Alternatively, a fixed effects specification as in Example 1 can be used provided the fixed effects can only take unknown values , where is the number of types. An example of continuous is provided by construction procurement, where can group the bidder’s distance to the construction site and her capacity. When (2.9) gives the system

which is equivalent to or for all bidder pair . If the range of has a non-empty interior, differentiating with respect to the entries of this matrix gives for all pair . Hence, is identified up to a multiplicative constant and imposing that the first entry of is 1 or that ensures identification.

Example 3: Linear regression with bidder fixed effects.

The case of can be dealt as in Example 2, augmenting to code bidder identities.

Example 4: Exponential linear regression with bidder fixed effects.

When the entries can take negative values, a possible choice of the positive function is . For this choice, taking logarithm in (2.9) implies

If for some pair , it must hold that and then for all . Restricting the parameter space of the as in Example 1 then gives identification.

3 Seller revenue and asymmetry misspecification

The proposed specification is convenient to compute and analyze the seller revenue. The presence of a reserve price , where is the seller private value, requires changing Assumption 1 into

Assumption 6

There is no transaction if all private values are below the reserve price. Otherwise, the winning bid is the greater of the second-highest bidder’s private values and the reserve price.

For a reserve price in the common support , consider the quantile level of in the parent distribution. Under Assumption 4 it therefore holds that . It is convenient to abbreviate , , into , and , respectively. The seller payoff in an auction with reserve price is

where is the winning bid. The corresponding expected seller revenue is

3.1 Expected revenue and optimal reserve price

The next Proposition gives a quantile expression for the expected revenue and characterizes the optimal reserve price. Let and be as (2.6).

Proposition 3

-

(i)

The probability of selling the auctioned good is .

-

(ii)

The seller expected payoff is

(3.1) -

(iii)

The optimal reserve price satisfies

(3.2)

Compared to the case of symmetric bidders, Proposition 3-(ii) shows that the optimal reserve price depends upon the number of bidders and upon the bidder characteristics. The impact of the asymmetry coefficients on the expected seller revenue and on the optimal reserve price seems unclear. For , the ambiguity is due to the term which increases with , while the other terms decrease. Observe similarly that, in (3.2), decreases with while increases. Cantillon (2008, Theorem 2) gives condition that allows to rank two sets of asymmetry coefficients according to seller revenue.

In many cases, the seller must decide a reserve price before observing the number of bidders and the asymmetry parameter of the entrants. The expected revenue formula (3.1) is conditional on and on the asymmetry parameters of the entrant, an information which is not available but can be integrated out to produce a relevant expected revenue and optimal reserve price.

3.2 The effect of a symmetric misspecification

To analyse the effect of a symmetric misspecification on the optimal reserve price and seller revenue, we perform a numerical experiment with no covariate and two asymmetric bidders with private values , and . Higher gives private values closer to 1 and values of the curvature parameter ranging from to are considered. High and moderate asymmetry scenarios, with set to and respectively are considered.

To evaluate the effect of estimating a symmetric misspecified model, we derive the limiting symmetric private value distribution by matching the distribution of winning bids with the symmetric winning bid distribution. Under Assumption 1, the winning bid is equal to the minimum between , therefore, the winning bid distribution is

For symmetric bidders, the function does not depend upon and is equal to

Therefore, the symmetric private value c.d.f. which generates the winning bid distribution must satisfy so that

The c.d.f. is the limit of any nonparametric estimator obtained by matching the winning bid distribution of a misspecified symmetric bidder model with the observed one, see for instance \citeasnounGimenes2017. An optimal reserve price assuming symmetric bidders, where , solves the symmetric version of (3.2)

where the seller private value is set to for the sake of simplicity. The expected seller revenue achieved with under the true asymmetric private value distribution can then be computed using (3.1). The reserve price and the corresponding expected seller revenue are reported in the columns labeled “Misspecified” of the next table. The optimal reserve price and seller revenue using the true private value distribution are reported under the label “Asymmetry”.

| Optimal Reserve Price | Expected Seller Revenue | ||||||

|---|---|---|---|---|---|---|---|

| Asymmetry | Misspecified | Asymmetry | Misspecified | Percentage Loss | |||

Table 1 reveals that ignoring asymmetry can lead to substantial loss in terms of seller revenue, when the curvature parameter is high or in the high asymmetry scenario. Note that the optimal expected revenue computed under the misspecified symmetric model is always smaller than the one achieved with the correct asymmetric model. The optimal reserve price is also substantially higher in the correct model with strong asymmetry.

The analysis presented here differs from \citeasnounCantillon2008’s, who studies how presence of asymmetry impacts seller expected revenue. She compares auctions with asymmetric private value distributions with a symmetric benchmark, and finds that asymmetry is associated with lower expected revenue. Our comparison differs from hers in that we investigate what happens if a truly asymmetric model is misspecified as symmetric - in which case, we find that not accounting for asymmetry may lead to loss in revenue. In that sense, our analysis supports and extends her findings. To see this, consider different scenarios of asymmetry such that , with , as shown in Table 2.

| Optimal Reserve Price | Expected Seller Revenue | |||||

|---|---|---|---|---|---|---|

| Asymmetry | Misspecified | Asymmetry | Misspecified | Percentage Loss | ||

As can be seen, higher asymmetry when is (0.1,0.9) has lesser revenue than the symmetric case of (0.5,0.5), supporting Cantillon’s finding that “the expected revenue is lower the more asymmetric bidders are”. However, given ex-ante asymmetry among bidders, a misspecified symmetric model always has smaller expected revenue and higher the asymmetry, more is the potential loss in revenue due to misspecification.

4 Estimation and asymptotic inference

Suppose that for each auction , the analyst observes the winning bid , the product-specific covariate , the number of bidders , the bidder covariate and the identity of the winner.

4.1 Two step estimation

As stated in Lemma 1, the probability that bidder wins is

so that the asymmetry parameter can be estimated using the maximum likelihood estimator

| (4.1) |

The second step consists in the estimation of the parent quantile slope and is based upon (2.10), which identifies as shown in Proposition 2. Define, for as in (2.6),

The quantile level is an estimation of the (random) quantile level which is such that the quantile function of the winning bid given , , and satisfies

(see (2.10)). It suggests the quantile regression estimator

| (4.2) |

where , see e.g. \citeasnounKoenker2005.

4.2 Asymptotic distribution

While a joint estimation of the parameters , and may offer some potential efficiency gains, the proposed two step procedure is simple to implement. In addition, the first stage estimation of is not affected by a possible mispecification of the parent c.d.f. Note the second step slope estimator involves an estimated quantile level. As well known since \citeasnounMurphyTopel1985, the first step estimation can affect the second step asymptotic distribution, but not the rate of which is still the parametric rate. However, this can be easily captured using the proof techniques in \citeasnounPollard1991. Useful assumptions and notations are as follows. In the sequel, will be abbreviated in when convenient. Let be derivative of . Under Assumption 5, the Fisher information matrix for the asymmetry parameters can be defined as

or by using the Bartlett identity when has a compact support as assumed below.

Assumption 7

The auction variables are drawn identically and independently. The support of is compact.

Assumption 8

Assumption 7 is standard. Assumption 8 imposes that the auction model is correctly specified and that the asymmetry parameters are identified.

Consider now some additional notations for the second step estimator . Let the derivative of be denoted by , which exists and is strictly positive on as shown in the proof of Proposition 2. As the conditional quantile function of the winning bid is

the conditional p.d.f. of the winning bid is, under Assumption 4,

which is continuous and bounded away from infinity over . Let the derivative of be denoted by and define

The matrices and are specific to the infeasible quantile regression estimator of which uses the true asymmetry parameters instead of their estimates,

In particular, is the asymptotic variance of , see \citeasnounKoenker2005. The matrix is the asymptotic covariance of the infeasible and . Finally

is the derivative of the population version of the objective function which is used for .

The asymptotic variance of the asymmetry parameter estimator and of the feasible are given by the matrices and

The next Theorem gives the asymptotic joint distribution of and .

Theorem 4

While the asymptotic normality of the MLE is standard, the one of follows from modifying the approach of \citeasnounPollard1991 to account for the first step estimation. The asymptotic variance of these estimators can be estimated but it may be more suitable to rely on bootstrap, especially for the parent slope function . Indeed, bootstrap is more reliable for inference in quantile regression, see \citeasnounKoenker2005 and the reference therein.

4.3 Seller revenue and optimal reserve price estimation

Let , and be as (2.6). The estimated seller expected payoff derived from Proposition 3 is

In the integral upper bound above, is a small truncation index, set to in the Application Section, which accounts for the fact that the quantile regression estimator may not be defined for extreme quantiles. It follows that the argument must vary in . As in \citeasnounLiPerrigneVuong2003, an optimal reserve price estimation could be based on the maximization

instead of (3.2), as the latter would request an additional estimation of the derivative of . Note that the use of a truncation may affect the estimation of the optimal reserve price. As the values of relevant in our application were close to .5, we do not think it affects our empirical results.444Note also that the function vanishes at as long as , and at , since and . This also suggests that the lower and upper tails have a moderate contribution in the expected revenue integral, at least for reasonable value of .

A Functional Central Limit Theorem can be established for combining arguments used for Theorem 4 with empirical process theory as reviewed in \citeasnounvanderVaart1998. The Argmax Theorem can then be used to obtain the asymptotic distribution of and of . In the application, pairwise bootstrap is used to derive (pointwise) confidence intervals as proposed in \citeasnounKoenker2005.

5 Simulations

In this section, we present the results of a Monte Carlo simulation designed to evaluate the performance of the two-step estimation procedure.

Data Generating Process.

We simulate ascending auctions with bidders assigned to different classes: type 1 and type 2 with and . Bidders are assigned to each type with equal probability. Auction specific characteristics is a random draw from , for , with an expected value of and . The parent private value conditional quantile function is generated as

| (5.1) |

where the true quantile regression coefficients are

The number of simulation replications is set to 1000.

Estimation.

The estimation is conducted in two steps. In the first step, the type parameters are estimated using maximum likelihood estimation by maximizing (4.1) over a grid of points. The quantile regression slope are then estimated in a second step using (4.2). For the median , the estimated parent quantile function is given by .

Results.

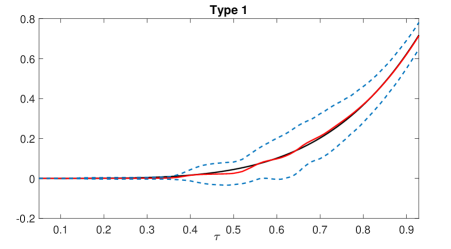

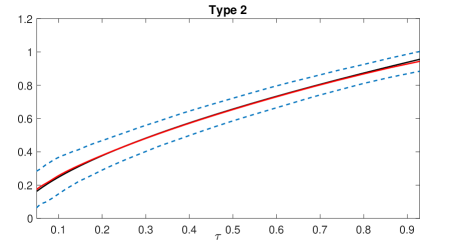

Figure 1(a) compares the true private value quantile function (in black) with the mean of the estimated private value quantile function across simulations (in red) for both type and type , considering a median auction. The bias and standard error (SE) for the private value quantile function for both types are reported in Table 3. The simulation results confirm that the two step estimation procedure works well.

True in black, mean of estimation across simulations in red, 95% confidence intervals in dotted lines

| Type 1 | Type 2 | |||

|---|---|---|---|---|

| Bias | SE | Bias | SE | |

6 Application

In this section, we investigate asymmetry in USFS timber auctions, as reported on Phil Haile’s website http://www.econ.yale.edu/pah29/timber/timber.htm, using the methodology developed in this paper. Bidders are classified as mill (with manufacturing capacity to process the timber) and logger (lacking manufacturing capabilities). For simplicity in the exposition, mills and loggers are abbreviated by and , respectively, when convenient. The dataset aggregates 7,462 ascending auctions (i.e., winning bids) that occurred in the western part of the US during the period of 1982-90. The sample contains a set of variables characterizing each timber tract including the estimated volume of the timber (measured in thousand of board feet - mbf) and its estimated appraisal value (given in Dollar per unit of volume). Mills won in about 72% of the auctions. The descriptive statistics can be found in Table LABEL:desc_stats. The auctioned tract exhibits significant heterogeneity in quality and size. The contracts to extract the timber last, on average, 2 years. Bidders participation is high. On average, there are 6 bidders attending the auctions in a range of 2 to 12.

| Mean | Std. Dev. | Max | Min | |

|---|---|---|---|---|

| Winning bids ($ per tbf) | 126.43 | 136.22 | 5,145.71 | 0.14 |

| Appraisal value ($ per tbf) | 58.65 | 60.35 | 793.62 | 0.25 |

| Volume (tbf) | 4,466.89 | 4,418.41 | 39,920 | 8 |

| Contract Length (years) | 1.96 | 1.3 | 42 | 0.1 |

| Number of bidders | 5.77 | 3.09 | 12 | 2 |

| Number of loggers | 1.74 | 2.10 | 11 | 0 |

| Number of mills | 4.03 | 3.02 | 12 | 0 |

| Bidders in the winner’s class | 4.52 | 2.73 | 12 | 1 |

As we do not observe individual bidders characteristics, we consider the private value quantile regression model

| (6.1) |

where stacks the constant, appraisal value and volume of the auctioned tract. In what follows, a median auction is an auction where the appraisal value and the volume are set to their median value. With the exception of Figure 3, all the figures and tables of this section and Appendix C are for a median auction.

6.1 Specification analysis

The fitted model (6.1) combines a power asymmetry specification, i.e. with a quantile regression for the parent distribution, which is identical here to the mill private value distribution. These two components are in fact quite different. Many options, such as adding interaction terms or adopting a sieve approach as in \citeasnounBelloniChernozhukovChetverikovFernandez-Val2019 can be used to improve the fit of the parent quantile regression. As for the “asymmetry” function , the considered asymmetry power specification is quite restrictive and may fail to provide a good approximation for . It is therefore of interest to develop a two-step analysis where the asymmetry specification is considered first, as this component of the model is the most likely to be misspecified. The correct joint specification of the two components in (6.1) is analyzed later.

6.1.1 Asymmetry power specification

Let and be the number of mills and loggers attending the auction. An implication of the asymmetry power specification already used for estimating is

Our power specification analysis is based on a test for , where the union is over the proportions with asymmetric auctions (i.e. , as the winner type distribution is degenerated otherwise), and with a number of auctions larger than . A statistic for is

| (6.2) | ||||

where is the number of asymmetric auctions in the sample, i.e. with or . In (6.2), is the sample estimator of the probability that a mill wins in an auction with mills and loggers. The -statistic is the studentized difference of to its model counterpart, which converges to a standard normal as shown in Proposition B.1 in Appendix B under standard assumptions.

Our asymmetry specification analysis relies on the maximum statistic over asymmetric auctions

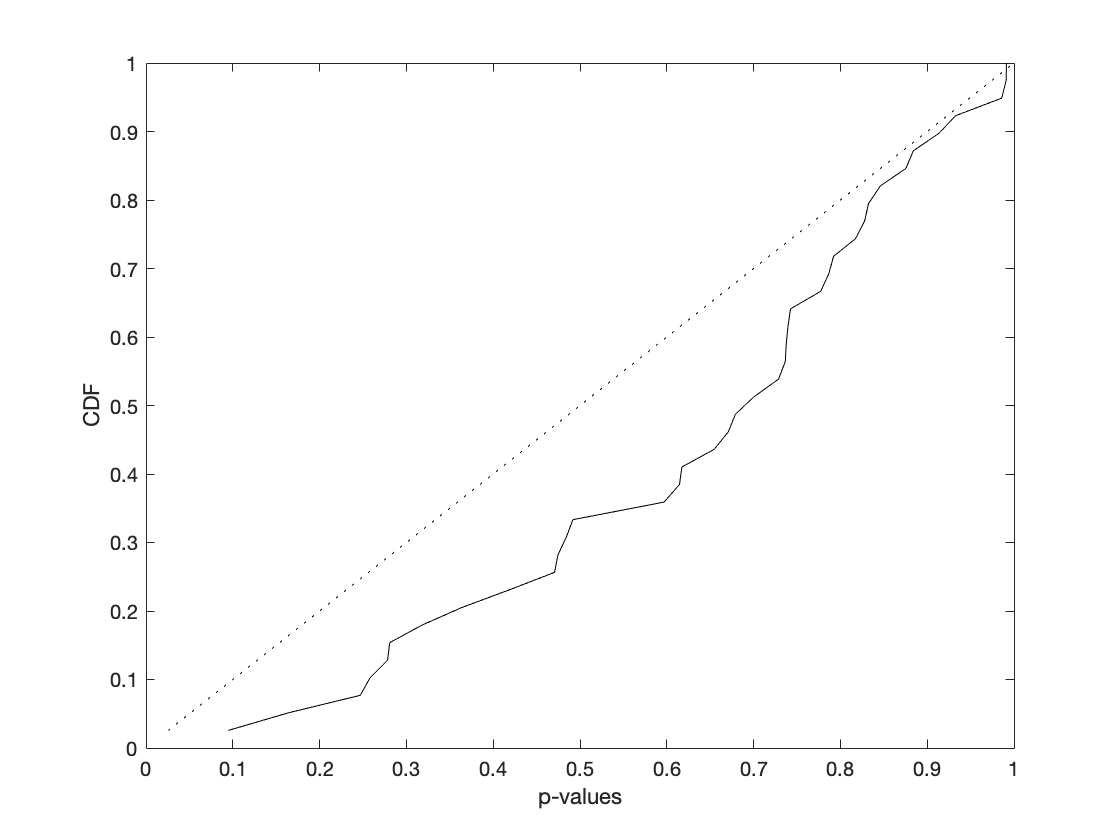

which is used to test . The value of is computed by the pairwise bootstrap as detailed in Appendix B. The result of this test is reported in Table LABEL:Xitest.

| Test statistic | -value | |

|---|---|---|

| 2.90 | 0.54 |

Appendix B also reports the pairwise bootstrap -values, which are all reasonably high.

6.1.2 Power and parent distribution specifications

Our estimation strategy is built on the winning bid quantile function given the type proportion , the winner type, say , and the auction characteristic . More specifically, (2.10) shows that the conditional winning bid quantile is

| (6.3) |

where, for if the winner is a mill and if a logger wins and ,

A recent literature considers quantile regression specification tests over a quantile interval , see \citeasnounEscancianoVelasco2010, \citeasnounRotheWied2013, \citeasnounEscancianoGoh2014 and the references therein. Their approach can be used to test whether the quantile regression (6.3) is correctly specified for each value of , building on a collection of statistics as done in the previous section for the winner type distribution. We adopt instead a more aggregated approach which follows \citeasnounRotheWied2013 and avoids to estimate the conditional winning bid cdf given . Let 555For a vector, means that for all . be the joint cdf of the winning bid and , which is estimated using the empirical cdf . The null hypothesis is

The null winning bid distribution is estimated using the winning bid quantile function (6.3) via

| (6.4) |

The Rothe and Wield (2013) statistic for is

| (6.5) |

We have conducted in parallel a conditional testing procedure reported in Appendix B, which computes a statistic as above for each type proportion observed in the sample, as done when analyzing the power specification. This was motivated by \citeasnounAradillasGandhiQuint2013, who mentioned that auctions with bidders may have more bidders.666See their Footnote 26. This was also pointed to us by an anonymous Referee. These auctions represent slightly less than of the sample. We therefore compute several versions of depending on whether auctions with were used or not to estimate the parent distribution and , and in empirical cdf summations. Appendix B details how to compute (6.4) in practice and to apply the bootstrap procedure of \citeasnounRotheWied2013 to obtain the -values of the next table.

| : all sample | : without | : without | ||||

| : all sample | : all sample | : without | ||||

| Test statistic | -value | Test statistic | -value | Test statistic | -value | |

| RW | .098 | 0.043 | .120 | .094 | .085 | .170 |

Table 6 shows that the Rothe and Wied (2013) test does not reject at the level but rejects at . Removing auctions with twelve bidders from the sample gives much higher p-values, which suggests that the proposed testing procedure supports the correct specification of the model. Further analysis reported in Appendix B shows that including or not auctions with twelve bidders gives a nearly identical estimation of as well as the intercept and appraisal value coefficients, and only slightly increases the estimation of the volume slope. We therefore use the whole sample in the rest of the empirical analysis.

6.2 Private value quantile functions

We use a type fixed effect specification for the asymmetry parameter , with if bidder at auction is a mill and if it is a logger. For identification, we normalize . The first step estimation gives with a 95% confidence interval computed by pairwise bootstrap given by , which shows that loggers are indeed significantly weaker than mills. In particular, the logger winning probability is when the types are in equal proportions, of the probability that a mill wins the ascending auction, which is .

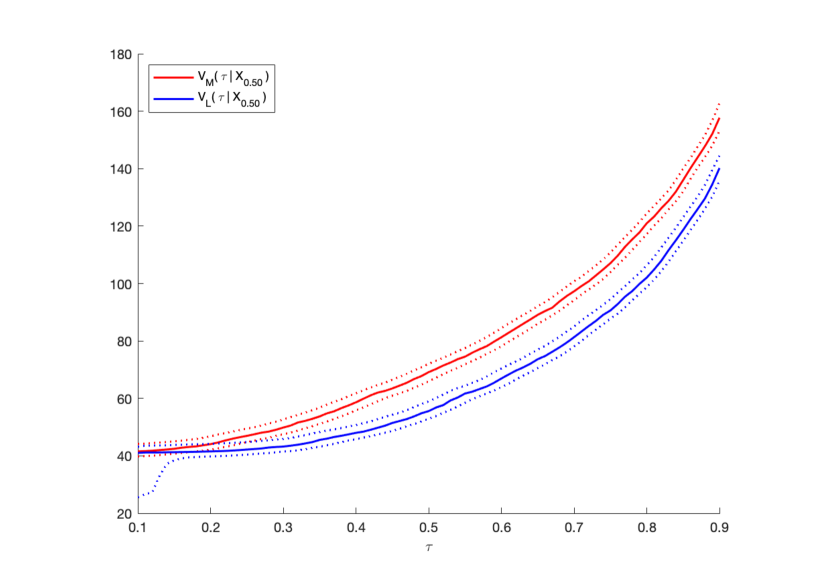

This is confirmed by Figure 2(a), which gives the estimated private value quantile functions of mills (red) and loggers (blue) and their 95% confidence bands computed via pairwise bootstrap method for a median auction. The private value conditional distribution of mills first-order stochastically dominates the one of loggers, especially in the upper part of the distribution.

The 95% confidence intervals for the quantile regression estimates were computed by resampling with replacement the ()-pair. Mills in red and loggers in blue.

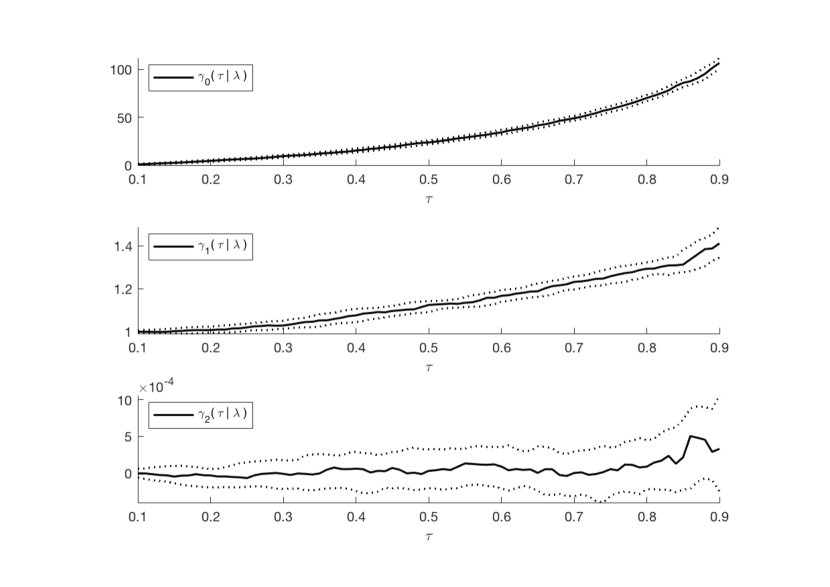

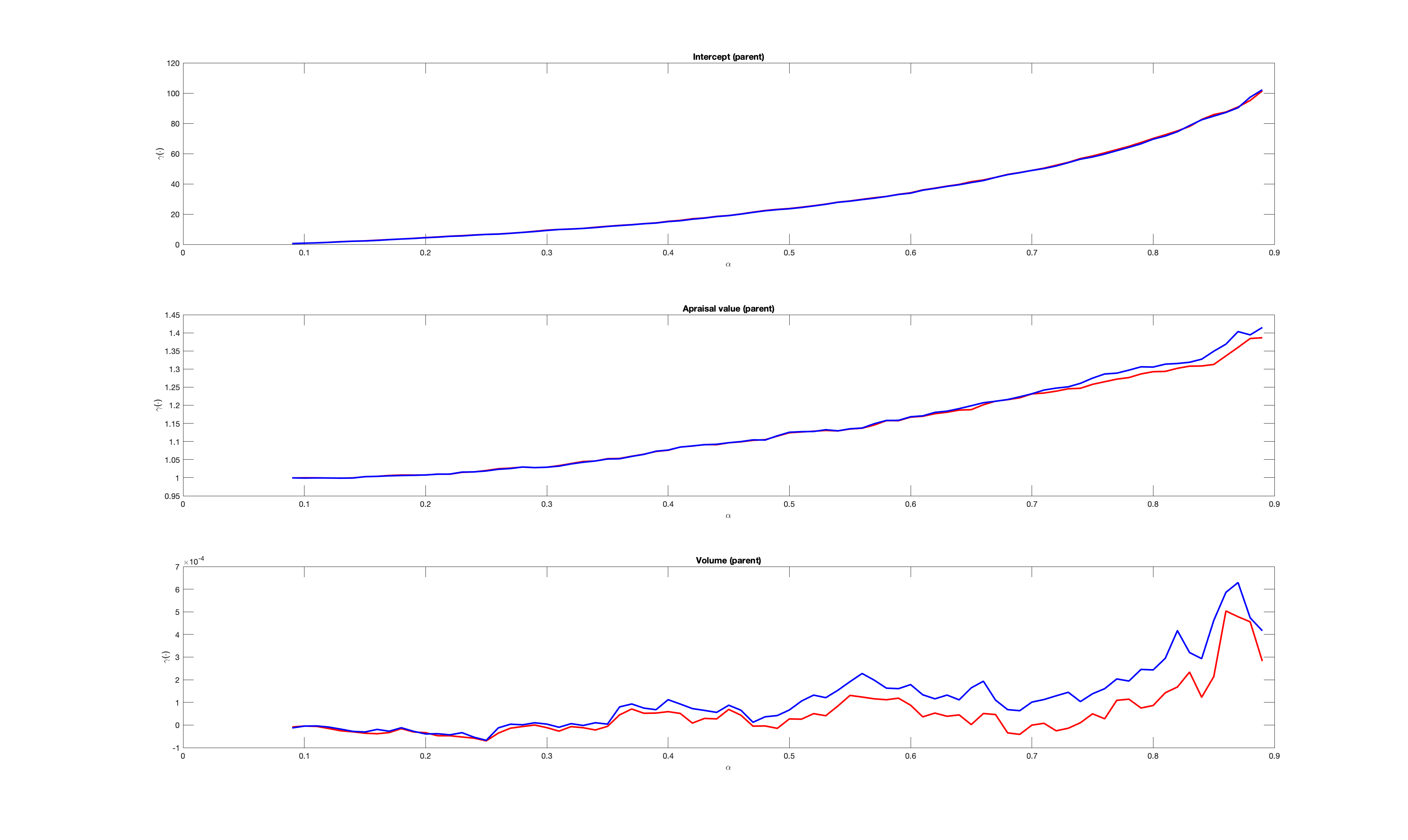

The power specification of the private value quantile functions allows to highlight which variable generates asymmetry. Indeed, a constant slope function in the parent private value quantile regression means that the impact of the associated variable is identical for each type of bidders. Figure 3 gives the quantile regression coefficients of the private value parent distribution. The estimated volume slope function looks constant, and possibly not significant. As the power transformation will not make bidders to differ in terms of volume slope functions, this suggests that capacity constraint is not binding for both types. In contrast, the parent appraisal value slope function does not look constant, and this variable is much likely to generate differences across mills and loggers. Figure 3, therefore, suggests that asymmetry is driven by qualitative (e.g. ability to improve on the appraisal value of the timber) and unobserved factors (captured by the intercept), instead of capacity constraints. Interestingly, coping for asymmetry gives appraisal value slope estimated functions that vary much less across quantile levels than in \citeasnounGimenes2017.

The 95% confidence intervals for the quantile regression estimates were computed by resampling with replacement the ()-pair. Top intercept, middle appraisal value and bottom volume estimated slope functions.

6.3 Expected revenue and optimal reserve price

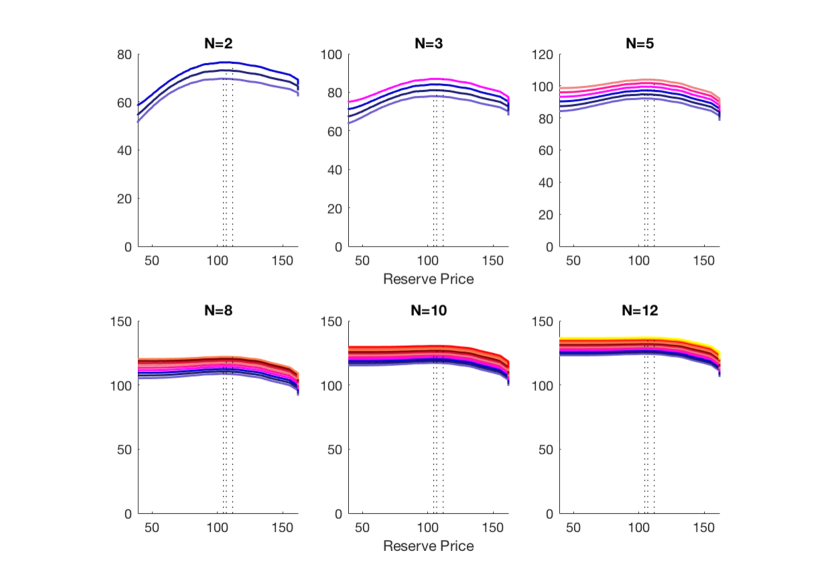

We now investigate the effect of asymmetry on the seller’s expected revenue and optimal reserve price. Given that we recover all the primitives of the game, we can evaluate the seller expected revenue as the proportion of types changes. This contrasts with \citeasnounCoeyLarsenSweeneyWaisman2017 who averages over the type proportion. In sections 6.3 and 6.4, the seller’s outside option value appearing in Proposition 3 is set to . Plotting gives a graph of the estimated seller’s expected revenue achieved with a reserve price .

Figure 4 shows estimates of the expected revenue as a function of the reserve price for each and type proportion. The dotted vertical lines give the optimal reserve price for each proportion of types. As the colors of the curves become warmer (from blue to red and yellow), loggers are replaced by mills and the revenue level increases in a parallel way. The expected revenue functions have clear maximas for small numbers of bidders (typically or ), contrasting with the estimation obtained with symmetric bidders in \citeasnounGimenesGuerre2019. For larger , the expected revenues look flat in their central part, a fact that cannot be seen from the estimation set strategy of \citeasnounCoeyLarsenSweeneyWaisman2017.

As a consequence, implementing an optimal reserve price is mostly useful when the probability of observing a small number of bidders is high. The optimal reserve prices shown in Figure 4 and detailed in the Appendix Table LABEL:count_prop_ORP depend upon and type proportion, but exhibit a moderate variation, staying in the interval and slightly increasing with the number of mills. As the expected revenues are flat around their maxima, using a reserve price in the range gives an expected revenue close to its maxima. This includes the optimal reserve price estimated from a symmetric specification, as in \citeasnounGimenes2017, given in LABEL:count_prop_ORP. As the expected revenue with no reserve price is mostly below when , as seen from Table LABEL:ERchanges_nonstrat below, using such a reserve price may mean not selling the auctioned lot if a small number of bidders participates.777To see this, observe that the probability of selling is the probability that the maximum private value is above the reserve price . The Markov inequality gives the bound for the latter. A proxy for is the non strategical revenue when the seller value is , suggesting to use the bound for the probability of selling.

6.4 Type variation and additional bidder effects

| One logger replaced by one mill | ||||

|---|---|---|---|---|

| Min ER | Max ER | Max | [ Min %, Max % ] | |

| 48.02 | 57.65 | 19.61% | [ 8.84%, 9.89% ] | |

| [46.37, 50.42] | [56.20, 59.70] | |||

| 63.59 | 75.04 | 18.01% | [ 5.42%, 5.83% ] | |

| [61.61, 66.03 | [73.30, 77.47] | |||

| 84.25 | 98.64 | 17.08% | [ 2.78%, 3.63% ] | |

| [81.82, 87.14] | [96.51, 101.45] | |||

| 105.28 | 120.17 | 14.14% | [ 1.35%, 2.02% ] | |

| [102.57, 108.42] | [117.68, 123.34] | |||

| 115.22 | 129.55 | 12.44% | [ 0.93%, 1.48% ] | |

| [112.45, 118.58] | [126.59, 132.95] | |||

| 123.05 | 136.52 | 10.95% | [ 0.66%, 1.12% ] | |

| [120.23, 126.19] | [133.61, 139.96] |

The 95% confidence intervals for the quantile regression estimates were computed by resampling with replacement the ()-pair.

| One logger replaced by one mill | ||||

|---|---|---|---|---|

| Min ER | Max ER | Max | [ Min %, Max % ] | |

| 69.65 | 76.44 | 9.75% | [ 4.57%, 4.95% ] | |

| [68.64, 70.92] | [75.45, 77.77] | |||

| 77.97 | 86.95 | 11.52% | [ 3.44%, 3.98% ] | |

| [76.60, 79.67] | [85.62, 88.73] | |||

| 92.16 | 103.9 | 12.74% | [ 2.14%, 2.75% ] | |

| [90.27, 94.45] | [102.06, 106.30] | |||

| 108.63 | 121.86 | 12.18% | [ 1.20%, 1.73% ] | |

| [106.32, 111.36] | [119.54, 124.84] | |||

| 117.16 | 130.37 | 11.28% | [ 0.86%, 1.33% ] | |

| [114.70, 119.99] | [127.76, 133.61] | |||

| 124.2 | 136.92 | 10.24% | [ 0.63%, 1.03% ] | |

| [121.63, 127.20] | [134.11, 140.35] |

The 95% confidence intervals for the quantile regression estimates were computed by resampling with replacement the ()-pair.

In this section, we study the effects of changes in the bidder’s type proportion and additional bidders on the expected revenue. For that, we set the largest to its maximal observed value 12, see tables LABEL:count_prop_ER_nonstr and LABEL:count_prop_ER in Appendix C. The boostrapped confidence intervals for the expected revenue given in these tables have a length ranging from to , corresponding to revenues varying between and 888The bootstrap confidence intervals for the optimal reserve price have a larger length, between and for an optimal reserve price between and . As a matter of comparison, \citeasnounCoeyLarsenSweeneyWaisman2017’s set identified confidence bounds for the seller revenue and optimal reserve price look huge, but they also allow for affiliated values.. The bootstrapped confidence intervals of the strategical seller expected revenue, achieved using an optimal reserve price, and the non strategical one, obtained with a non binding reserve price, does not overlap up to . Similarly, the revenue gain achieved when an additional bidder of any type enters looks significant, at least for auctions with up to initial bidders for additional logger and, for mill, up to some auctions with . Setting the largest to 12 is therefore expected to capture all the statistically significant policy effects delivered by the sample. We now focus on each of these effects.

Revenue and types.

Point estimation of bidders’ private value distributions permits investigation of changes in the number of bidders of a given type. Tables LABEL:ERchanges_nonstrat, LABEL:ERchanges_strat and LABEL:BK give a summary of all universe of changes, see also Tables LABEL:count_prop_ER_nonstr and LABEL:count_prop_ER in Appendix C.

Table LABEL:ERchanges_nonstrat considers a non strategical expected revenue, which means that reserve price is non binding, whereas Table LABEL:ERchanges_strat focuses on the optimal revenue999As suggested in \citeasnounCoeyLarsenSweeney2019, a comparison between a strategical and non strategical expected revenue can be fruitful to the seller due to the costs that a policy of setting an optimal reserve price may impose in practice. Recent works have highlighted the asymmetric effects on seller’s revenue due to mistakes in choosing reserve prices (see e.g. \citeasnounKim2013, \citeasnounOstrovskySchwarz2016, \citeasnounCoeyLarsenSweeney2019 and \citeasnounGimenes2017). All the results are obtained for a given . The second and third columns of both tables give the minimum and maximum values of the seller expected revenue across type proportions. The minimum and maximum values of the revenue in both cases are obtained when only loggers and only mills are participating, respectively. The percentage change in revenue when changing all loggers into mills is given in the fourth column and is an additional measure of asymmetry. It is, on average, 15.4% in the non strategical case and 11.3% in Table LABEL:ERchanges_strat. These order of magnitude are similar to the one found in \citeasnounRobertsSweeting2016 who employ a parametric specification.101010These authors also allow for entry decision but their estimate “indicate a moderate effect of selection”. The fifth column gives the maximum and minimum percentage changes obtained when replacing one logger by one mill. All these results suggest that the seller should either incentivize mills participation or subsidize higher loggers bid as studied in \citeasnounFlambardPerrigne2006, \citeasnounMarion2007 or \citeasnounKrasnokutskayaSeim2011 for the latter.

| (Logger,Mill) | Non strat. ER | Strat. ER | Additional Logger | Additional Mill | ||

| (2,0) | 48.02 | 69.65 | ||||

| (1,1) | 52.46 | 73.10 | ||||

| (0,2) | 57.65 | 76.44 | ||||

| (3,0) | 63.59 | 77.97 | ||||

| (2,1) | 67.30 | 81.07 | ||||

| (1,2) | 71.18 | 84.06 | ||||

| (0,3) | 75.04 | 86.95 | ||||

| (4,0) | 74.82 | 85.44 | ||||

| (3,1) | 78.23 | 88.24 | ||||

| (2,2) | 81.63 | 90.93 | ||||

| (1,3) | 84.96 | 93.53 | ||||

| (0,4) | 88.17 | 96.03 |

An underlined revenue indicates a violation of \citeasnounBulowKlemperer1996, ie the considered non strategical revenue obtained by adding a bidder of a given type is below the strategical one. A “*” indicates that the bootstrapped confidence interval of the strategical revenue and the non strategical one with an additional bidder of the considered type do not overlap.

Revenue and additional bidders.

An important result by \citeasnounBulowKlemperer1996 states that the seller expected revenue achieved in an ascending auction with no reserve price but an additional bidder is higher than the one of any allocation mechanism, which includes the case of an ascending auction with an optimal reserve price, under symmetry and a downward sloping marginal revenue condition.111111See \citeasnounCoeyLarsenSweeney2019 for a recent econometric application to entry exogeneity. Table LABEL:BK reports several violations of \citeasnounBulowKlemperer1996 arising in our asymmetric framework. The “Strat. ER” column of Table LABEL:BK indicates the estimated optimal expected revenue achieved with and bidders, with number of loggers or mills as indicated in the second column. The last two columns give the estimated non strategical expected revenue obtained when adding a logger or a mill.

Table LABEL:BK shows that using an optimal reserve price is always more profitable than adding a weak logger bidder. Adding a mill bidder is also less profitable than using the optimal auction but only when and in a much less significant way than adding a logger. Table LABEL:BK shows that the difference of revenue using the optimal auction and adding a logger decreases with , in average across type proportion. By contrast the revenue difference using the optimal auction and adding a mill increase with .121212Tables LABEL:count_prop_ER_nonstr and LABEL:count_prop_ER in Appendix C also report the revenues obtained for an estimation of a symmetric private value model as in \citeasnounGimenes2017. Interestingly violations of \citeasnounBulowKlemperer1996 occur for but not for larger . The systematic violations of \citeasnounBulowKlemperer1996 when adding a logger suggests that the logger private value distribution does not satisfy the downward sloping marginal revenue condition.131313The downwards sloping marginal revenue condition of \citeasnounBulowKlemperer1996 requires that increases with . If and , the leading term when goes to 0 of the derivative of this function is which is negative, so that the considered condition is not compatible with our estimation of . When , using the optimal reserve price is less profitable than participation of an additional bidder of any type, up to few minor exceptions. However, the differences of expected revenue between an optimal reserve price and an additional bidder are at best in the range of , which is close to the half length of the boostrapped confidence interval for the strategical and non strategical seller’s expected revenues.

7 Conclusion

The paper considers a semiparametric specification for asymmetric private value distribution under the independent private value distribution setup. The bidders share a common parent distribution, which is generated by a quantile regression model. Asymmetry is driven by powers applied to the parent distribution. These powers can depend upon individual and/or group fixed effects, bidder and/or auction specific variables. The specification can be estimated by a two stage procedure from the winning bid and winner’s identity. This quantile regression specification is not affected by the curse of dimensionality and can cope with data-rich environment. Unlike common parametric specifications, it is expected to be less affected by misspecification due to its nonparametric nature. Usual parametric rates nevertheless apply and estimation techniques remain standard. The parametric power component of the model allows for a simple evaluation of bidder’s asymmetry and of its economic implications.

A timber auction application has been used to illustrate the implication of asymmetry. The proposed specification tests do not reject the model. The estimated asymmetry parameter means that weaker bidders have less chances to win the auction than stronger ones. The quantile regression specification allows to detect the variables that affect the bidders in a symmetric way, here volume, suggesting that bidders face similar capacity constraints, and the other variables that represent characteristics of asymmetry. The shape of the expected revenue varies a lot with the number of bidders, being mostly flat for , with an optimal revenue close to the one achieved in the absence of a reserve price. For small , the choice of a reserve price does matter, but the estimated optimal one does not vary too much with and type proportion. The effect of asymmetry is mild here, and using the one estimated from a misspecified symmetric model should protect the seller against revenue loss occurring for small . On the other hand, and as expected, the proportion of small bidders may importantly affect the seller expected revenue. This suggests that the seller can benefit from preference policies which would strengthen the weak bidders. A striking finding is that, in small auctions with less than four bidders, increasing participation, as recommended by \citeasnounBulowKlemperer1996 in a symmetric environment, may give a smaller revenue than using an optimal reserve price, due to the presence of weak bidders. As a consequence, the choice of a proper reserve price may be a more important tool under asymmetry than when the bidders are symmetric.

References

- [1] \harvarditem[Aradillas-López et al.]Aradillas-López, Gandhi and Quint2013AradillasGandhiQuint2013 Aradillas-López, A., Gandhi, A., Quint, D., 2013, Identification and inference in ascending auctions with correlated private values, Econometrica 81(2), 489–534.

- [2] \harvarditem[Arellano and Bonhomme]Arellano and Bonhomme2017ArellanoBonhomme1207 Arellano, M., Bonhomme, S., 2017, Quantile selection models with an application to understanding changes in wage inequality, Econometrica 85(1), 1–28.

- [3] \harvarditem[Athey et al.]Athey, Coey and Levin2013AtheyCoeyLevin2013 Athey, S., Coey, D., Levin, J., 2013, Set-asides and subsidies in auctions, American Economic Journal: Microeconomics 5(1), 1–27.

- [4] \harvarditem[Athey and Haile]Athey and Haile2002AtheyHaile2002 Athey, S., Haile, P. A., 2002, Identification of standard auction models, Econometrica 70(6), 2107–2140.

- [5] \harvarditem[Athey et al.]Athey, Levin and Seira2011AtheyLevinSeira2011 Athey, S., Levin, J., Seira, E., 2011, Comparing open and sealed bid auctions: Evidence from timber auctions, The Quarterly Journal of Economics 126(1), 207–257.

- [6] \harvarditem[Belloni et al.]Belloni, Chernozhukov, Chetverikov and Fernández-Val2019BelloniChernozhukovChetverikovFernandez-Val2019 Belloni, A., Chernozhukov, V., Chetverikov, D., Fernández-Val, I., 2019, Conditional quantile processes based on series or many regressors, Journal of Econometrics 213(1), 4–29.

- [7] \harvarditem[Brannman and Froeb]Brannman and Froeb2000BrannmanFroeb2000 Brannman, L., Froeb, L. M., 2000, Mergers, cartels, set-asides, and bidding preferences in asymmetric oral auctions, Review of Economics and Statistics 82(2), 283–290.

- [8] \harvarditem[Brendstrup and Paarsch]Brendstrup and Paarsch2006BendstrupPaarsch2006 Brendstrup, B., Paarsch, H. J., 2006, Identification and estimation in sequential, asymmetric, english auctions, Journal of Econometrics 134(1), 69–94.

- [9] \harvarditem[Bulow and Klemperer]Bulow and Klemperer1996BulowKlemperer1996 Bulow, J., Klemperer, P., 1996, Auctions versus negotiations, American Economic Review 86(1), 180–194.

- [10] \harvarditem[Cantillon]Cantillon2008Cantillon2008 Cantillon, E., 2008, The effect of bidders’ asymmetries on expected revenue in auctions, Games and Economic Behavior 62(1), 1–25.

- [11] \harvarditem[Coey et al.]Coey, Larsen and Sweeney2019CoeyLarsenSweeney2019 Coey, D., Larsen, B., Sweeney, K., 2019, The bidder exclusion effect, The RAND Journal of Economics 50(1), 93–120.

- [12] \harvarditem[Coey et al.]Coey, Larsen, Sweeney and Waisman2017CoeyLarsenSweeneyWaisman2017 Coey, D., Larsen, B., Sweeney, K., Waisman, C., 2017, Ascending auctions with bidder asymmetries, Quantitative Economics 8(1), 181–200.

- [13] \harvarditem[Escanciano and Goh]Escanciano and Goh2014EscancianoGoh2014 Escanciano, J. C., Goh, S.-C., 2014, Specification analysis of linear quantile models, Journal of Econometrics 178, 495–507.

- [14] \harvarditem[Escanciano and Velasco]Escanciano and Velasco2010EscancianoVelasco2010 Escanciano, J. C., Velasco, C., 2010, Specification tests of parametric dynamic conditional quantiles, Journal of Econometrics 159(1), 209–221.

- [15] \harvarditem[Flambard and Perrigne]Flambard and Perrigne2006FlambardPerrigne2006 Flambard, V., Perrigne, I., 2006, Asymmetry in procurement auctions: Evidence from snow removal contracts, The Economic Journal 116(514), 1014–1036.

- [16] \harvarditem[Gimenes]Gimenes2017Gimenes2017 Gimenes, N., 2017, Econometrics of ascending auctions by quantile regression, Review of Economics and Statistics 99(5), 944–953.

- [17] \harvarditem[Gimenes and Guerre]Gimenes and Guerre2019GimenesGuerre2019 Gimenes, N., Guerre, E., 2019, Quantile regression methods for first-price auctions, arXiv e-prints.

- [18] \harvarditem[Graham and Marshall]Graham and Marshall1987GrahamMarshall1987 Graham, D. A., Marshall, R. C., 1987, Collusive bidder behavior at single-object second-price and english auctions, Journal of Political economy 95(6), 1217–1239.

- [19] \harvarditem[Haile and Tamer]Haile and Tamer2003HaileTamer2003 Haile, P. A., Tamer, E., 2003, Inference with an incomplete model of english auctions, Journal of Political Economy 111(1), 1–51.

- [20] \harvarditem[Kim]Kim2013Kim2013 Kim, D.-H., 2013, Optimal choice of a reserve price under uncertainty, International Journal of Industrial Organization 31(5), 587–602.

- [21] \harvarditem[Koenker]Koenker2005Koenker2005 Koenker 2005, Quantile Regression (Econometric Society monographs; no. 38), Cambridge university press.

- [22] \harvarditem[Komarova]Komarova2013aKomarova2013a Komarova, T., 2013a, A new approach to identifying generalized competing risks models with application to second-price auctions, Quantitative Economics 4(2), 269–328.

- [23] \harvarditem[Komarova]Komarova2013bKomarova2013b Komarova, T., 2013b, Partial identification in asymmetric auctions in the absence of independence, The Econometrics Journal 16(1), S60–S92.

- [24] \harvarditem[Krasnokutskaya and Seim]Krasnokutskaya and Seim2011KrasnokutskayaSeim2011 Krasnokutskaya, E., Seim, K., 2011, Bid preference programs and participation in highway procurement auctions, American Economic Review 101(6), 2653–86.

- [25] \harvarditem[Krishna]Krishna2009Krishna2009 Krishna, V., 2009, Auction theory, Academic press.

- [26] \harvarditem[Laffont et al.]Laffont, Ossard and Vuong1995LaffontOssardVuong1995 Laffont, J.-J., Ossard, H., Vuong, Q., 1995, Econometrics of first-price auctions, Econometrica 63, 953–980.

- [27] \harvarditem[Lamy]Lamy2012Lamy2012 Lamy, L., 2012, The econometrics of auctions with asymmetric anonymous bidders, Journal of Econometrics 167(1), 113–132.

- [28] \harvarditem[Li et al.]Li, Perrigne and Vuong2003LiPerrigneVuong2003 Li, T., Perrigne, I., Vuong, Q., 2003, Semiparametric estimation of the optimal reserve price in first-price auctions, Journal of Business and Economic Statistics 21(1), 53–64.

- [29] \harvarditem[Mailath and Zemsky]Mailath and Zemsky1991MailathZemsky1991 Mailath, G. J., Zemsky, P., 1991, Collusion in second price auctions with heterogeneous bidders, Games and Economic Behavior 3(4), 467–486.

- [30] \harvarditem[Marion]Marion2007Marion2007 Marion, J., 2007, Are bid preferences benign? the effect of small business subsidies in highway procurement auctions, Journal of Public Economics 91(7-8), 1591–1624.

- [31] \harvarditem[McAfee and McMillan]McAfee and McMillan1992McafeeMcmillan1992 McAfee, R. P., McMillan, J., 1992, Bidding rings, The American Economic Review pp. 579–599.

- [32] \harvarditem[Murphy and Topel]Murphy and Topel1985MurphyTopel1985 Murphy, K. M., Topel, R. H., 1985, Estimation and inference in two-step econometric models, Journal of Business & Economic Statistics 3(4), 370–379.

- [33] \harvarditem[Myerson]Myerson1981Myerson1981 Myerson, R. B., 1981, Optimal auction design, Mathematics of operations research 6(1), 58–73.

- [34] \harvarditem[Newey and McFadden]Newey and McFadden1994NeweyMcFadden1994 Newey, W. K., McFadden, D., 1994, Large sample estimation and hypothesis testing, Handbook of econometrics 4, 2111–2245.

- [35] \harvarditem[Ostrovsky and Schwarz]Ostrovsky and Schwarz2016OstrovskySchwarz2016 Ostrovsky, M., Schwarz, M., 2016, Reserve prices in internet advertising auctions: a field experiment. typescript.

- [36] \harvarditem[Pollard]Pollard1991Pollard1991 Pollard, D., 1991, Asymptotics for least absolute deviation regression estimators, Econometric Theory 7(2), 186–199.

- [37] \harvarditem[Roberts and Sweeting]Roberts and Sweeting2016RobertsSweeting2016 Roberts, J. W., Sweeting, A., 2016, Bailouts and the preservation of competition: The case of the federal timber contract payment modification act, American Economic Journal: Microeconomics 8(3), 257–88.

- [38] \harvarditem[Rothe and Wied]Rothe and Wied2013RotheWied2013 Rothe, C., Wied, D., 2013, Misspecification testing in a class of conditional distributional models, Journal of the American Statistical Association 108(501), 314–324.

- [39] \harvarditem[van der Vaart]van der Vaart1998vanderVaart1998 van der Vaart, A. W., 1998, Asymptotic Statistics, Cambridge University Press.

- [40] \harvarditem[Waehrer and Perry]Waehrer and Perry2003WaehrerPerry2003 Waehrer, K., Perry, M. K., 2003, The effects of mergers in open-auction markets, RAND Journal of Economics pp. 287–304.

- [41]

Appendix A - Proof section

A.1 Proof of Lemma 1.

Let

be the joint distribution of winning bids and winner’s identity. Due to private value independence, it holds, as shown in \citeasnounBendstrupPaarsch2006,

where the last line is obtained by integration by parts. Then, Assumption 2 gives

It follows

and

where is as in (2.6). This ends the proof of the Lemma.

A.2 Proof of Proposition 2

A.3 Proof of Proposition 3

Ignore, for the sake of brevity, the conditioning variables. Under assumption 6, the seller possible payoffs are

where is the th-lowest order statistics of private values, i.e. is the first highest order statistic and the second. Recall that , or equivalently . The next three points evaluate the contribution of each of the three events above to the seller revenue.

-

1.

. It follows that the probability of selling is , hence, Proposition 3-(i) is proven. The contribution of this event to the seller revenue is ;

-

2.

. The contribution of this second event to the seller revenue is ;

-

3.

Let denote the c.d.f. of the second-highest order statistic , which is

Under Assumption 2

The change of variable with then gives that the contribution of the third event to is

As , Proposition 3-(ii) is proved. It also follows that

Note that the optimal must belong to the open set . Hence the FOC gives that Proposition 3-(iii) holds.

A.4 Proof of Theorem 4

By Theorems 2.5 and 3.3, the proof of Theorem 3.2 in \citeasnounNeweyMcFadden1994, it holds under Assumptions 5, 7 and 8

| (A.6) |

For , define

which is such that and . The proof makes use of the following partial derivatives

Let be the -derivative of taken at

Define the objective function

which is such that

For simplicity of notation, denote . Arguing as in Pollard (1991, p.192) yields, for each fixed ,

| (A.7) |

where

contributes only to (A.7). To see this note that and denote and

Using Cauchy-Schwarz inequality

Denote .

Due to cancellation of cross-product terms

Lemma 2.4 in \citeasnounNeweyMcFadden1994 also gives

Hence, for each fixed ,

where the last line is from (A.6). Applying the convexity arguments in \citeasnounPollard1991 then gives, since ,

Then the joint asymptotic distribution of and is the one of and by (A.6), which by the CLT is a centered normal with covariance matrix

which can be written as in the Theorem.

Appendix B - Specification analysis

B.5 Power specification

Asymptotic normality.

The next Proposition establishes that the normalization used for the in (6.2) ensures they all have an asymptotic standard normal distribution.

Proposition B.1

Suppose Assumption 7 and (2.7) hold, and that there exists some real numbers such that , where the supremum is over the finite support of the distribution of and .

Then, for any type proportion with , converges in distribution to a standard normal when the sample size grows.

Note that the ’s are asymptotically dependent due to the common estimated parameter . Although it would be possible to derive their joint asymptotic distribution, it may be difficult to use in practice as, for instance, using it for a Chi-square statistic may give a very large asymptotic variance matrix, in the application, which may be difficult to estimate or to invert. Hence we prefer to use a maximum statistic in Section 6.1.1.

Proof of Proposition B.1.

Recall

and let , so that . Define also . Standard expansions give, standing for sum over asymmetric auctions,

Note also that

It follows that

where

observing that for symmetric auctions. As , the Proposition is proven.

Bootstrap procedure.

The values of Section 6.1.1 in the main text and of the next paragraph are computed using the following standard pairwise bootstrap procedure, which is valid under the Assumptions of Proposition B.1.

-

Step 1. Draw a bootstrap sample of winning bids auction covariates and types proportion with replacement from the realized values

. Iterate for -

Step 2. Compute the bootstrapped , , , ,

and .

-

Step 3. The bootstrapped -value for is given by

In the next paragraph, the bootstrapped -value for is given by .

Additional figure and table.

The next table gives the 39 selected type proportions with , the corresponding , and associated individual -values141414The total number of auctions with and is 3,290, about 44% of the original sample.. The -values are quite high and only one is lower than . If the statistics were computed using the true and instead of estimations, the -values would be, under , independent draws from the uniform distribution. Figure B.1 shows indeed that the -value cdf is close to the diagonal, as expected under the considered null.

| Type’s Proportion | p-value | |||

| 1 | 1 | 0.61 | 0.7005 | 223 |

| 1 | 2 | 0.33 | 0.8324 | 137 |

| 1 | 3 | 0.18 | 0.9136 | 133 |

| 1 | 4 | 0.41 | 0.7773 | 81 |

| 1 | 5 | 0.32 | 0.8279 | 49 |

| 1 | 6 | 1.76 | 0.2581 | 38 |

| 2 | 1 | 0.01 | 0.9910 | 205 |

| 2 | 2 | 0.22 | 0.8840 | 138 |

| 2 | 3 | 1.17 | 0.4707 | 99 |

| 2 | 4 | 0.79 | 0.6174 | 69 |

| 2 | 5 | 2.90 | 0.0947 | 46 |

| 3 | 1 | 0.48 | 0.7376 | 182 |

| 3 | 2 | 1.06 | 0.4918 | 113 |

| 3 | 3 | 0.71 | 0.6544 | 80 |

| 3 | 4 | 1.99 | 0.2469 | 39 |

| 3 | 5 | 0.79 | 0.6146 | 30 |

| 4 | 1 | 0.42 | 0.7425 | 160 |

| 4 | 2 | 1.01 | 0.4842 | 102 |

| 4 | 3 | 0.02 | 0.9859 | 55 |

| 4 | 4 | 0.35 | 0.8174 | 34 |

| 5 | 1 | 1.09 | 0.4183 | 127 |

| 5 | 2 | 0.52 | 0.7287 | 101 |

| 5 | 3 | 0.65 | 0.6790 | 58 |

| 6 | 1 | 1.26 | 0.2808 | 93 |

| 6 | 2 | 1.46 | 0.2783 | 81 |

| 6 | 3 | 0.36 | 0.7922 | 46 |

| 7 | 1 | 0.84 | 0.4746 | 83 |

| 7 | 2 | 0.11 | 0.9327 | 62 |

| 7 | 3 | 0.46 | 0.7396 | 34 |

| 7 | 5 | 0.44 | 0.7866 | 43 |

| 8 | 1 | 0.20 | 0.8755 | 69 |

| 8 | 2 | 0.55 | 0.6709 | 63 |

| 8 | 4 | 1.46 | 0.3639 | 50 |

| 9 | 1 | 1.61 | 0.1638 | 53 |

| 9 | 2 | 0.01 | 0.9913 | 37 |

| 9 | 3 | 0.28 | 0.8460 | 79 |

| 10 | 1 | 1.31 | 0.3181 | 35 |

| 10 | 2 | 0.44 | 0.7365 | 71 |

| 11 | 1 | 0.59 | 0.5968 | 92 |

B.6 Power and parent distribution joint specification analysis

Computation of in (6.4) and truncation in (6.5).

The testing procedure uses a quantile level grid , , and for each a value grid , . The parent cdf is estimated with the Riemann sum

The corresponding numerical computation of the winning bid quantile function is, using (6.3) and the rearrangement formula,

| (B.8) | |||||

The numerical approximation used for (6.4) is then

The sum (6.5) defining the Rothe and Wied statistic is restricted to auctions with transaction price in to avoid numerical errors at the boundaries, which may occur in view of the large sample size of 7,462 observations.

The bootstrap procedure analysis.

The two-step bootstrap procedure of \citeasnounRotheWied2013 is implemented as follows.

Preliminary to the bootstrap, we compute

over a larger quantile level grid

, , using the value grid , . Then

-

1.

Draw with replacement , from the initial auction sample. Use this bootstrap sample to estimate ;

-

2.

Draw with replacement transaction price from . Compute the statistic using the bootstrap sample ,

This is iterated for . The reported p-value is then .

Note that the first-step of this procedure assumes that the conditional winner type distribution is correctly specified, as tested earlier. Such mispecifications can however be detected if they affect the functional form of the winning bid quantile function used in the second step. This procedure can be easily restricted to subsamples and modified to ensure that the bootstrapped number of each type proportion is identical to the one achieved in the initial sample, as done in Table B.2 below.

| whole sample | w/o | ||||

|---|---|---|---|---|---|

| (Mills, Loggers) | p-value | p-value | |||

| (0,2) | 202 | .0159 | .8418 | .0152 | .8704 |

| (0,3) | 159 | .0359 | .1796 | .0355 | .1938 |

| (0,4) | 120 | .0346 | .1489 | .0322 | .1881 |

| (2,0) | 715 | .0799 | .1350 | .0798 | .1617 |

| (3,0) | 557 | .1755 | .0058 | .1745 | .0105 |

| (4,0) | 438 | .1133 | .0094 | .1151 | .0129 |

| (5,0) | 304 | .1039 | .0099 | .0947 | .0173 |

| (6,0) | 239 | .0532 | .0782 | .0476 | .1219 |

| (7,0) | 196 | .0250 | .5063 | .0263 | .4787 |

| (8,0) | 127 | .0358 | .2713 | .0328 | .3422 |

| (12,0) | 160 | .1447 | .0041 | .1805 | .0012 |

| (1,1) | 223 | .0170 | .8639 | .0170 | .8677 |

| (1,2) | 137 | .0297 | .5030 | .0290 | .5272 |

| (1,3) | 133 | .0156 | .8849 | .0160 | .8724 |

| (2,1) | 205 | .0400 | .2148 | .0407 | .2202 |

| (2,2) | 138 | .0130 | .9579 | .0145 | .9234 |

| (3,1) | 182 | .0215 | .6125 | .0208 | .6505 |

| (3,2) | 113 | .0557 | .0918 | .0606 | .0737 |

| (4,1) | 160 | .0202 | .6149 | .0195 | .6521 |

| (4,2) | 102 | .0307 | .4199 | .0326 | .3820 |

| (5,1) | 127 | .0102 | .9846 | .0104 | .9837 |

| (5,2) | 101 | .0411 | .2750 | .0448 | .2290 |

| Rest w/o | 2,175 | .0853 | .0257 | .1265 | .0123 |

| 449 | .2697 | .0000 | .3198 | .0000 | |

| .1755 | .0255 | .1745 | .0255 | ||

Type proportion conditional specification analysis.

The Rothe and Wied (2013) statistic , and to some extent the associated p-value, has a goodness of fit interpretation, as with a value of indicating that the model perfectly reproduces the sample distribution of . Computing a statistic with empirical and model cdf’s using subsamples given by a certain type proportion allows to analyze how well the model fits given mills and loggers participation, as done in Table B.2 where and are estimated over the whole sample or excluding the auction with twelve bidders. Table B.2 computes such statistics for subsamples with a number of observations larger than , the complement of these subsamples excluding auctions with twelve bidders, and a the remaining auctions with twelve bidders.

Table B.2 shows that the model has a poor fit for auctions with twelve bidders, which may confirm that participation is mismeasured for these data as reported in \citeasnounAradillasGandhiQuint2013. Otherwise the fit of the model seems quite good, except maybe for symmetric Mills auctions with and . Note that estimating and excluding auctions with twelve bidders seems to improve the fit, giving p-values higher than for these symmetric Mills auctions. Table B.2 also reports the bootstrapped p-values of maximum statistics, which are smaller than the ones obtained in Table 6, as expected since such maximum statistic is driven by the worst case, but still larger than .

Estimation impact of auction with twelve bidders.

Excluding auctions with twelve bidders gives an estimated at , which is virtually identical to the full sample one. The next figure reports the results for the estimation of the parent quantile coefficient . Only the volume slope function looks affected, but Figure 3 suggests that the volume slope function may not be significant.

Appendix C - Additional tables

This appendix displays tables that were commented on but not included in the empirical application. All tables are for median ascending auctions. The second column in all the three tables gives the corresponding estimates considering the methodology proposed in \citeasnounGimenes2017 with symmetric bidders for . If the econometrician does not take asymmetry into account, the seller’s expected revenue, is

and the optimal reserve price is with . The seller value is set to and the private value quantile function is estimated as in \citeasnounGimenes2017. Note that this differs from Section 3.2, where the true asymmetric distribution was used to compute the revenue achieved using a optimal reserve price from the misspecified symmetric model. Estimates taking into account asymmetry among the bidders, as discussed in this paper, are given on columns three to eight. They were computed using the expressions 3.1 and 3.2. The proportion of bidder’s types are given in parentheses following the rule .

| \citeasnounGimenes2017’s Approach | Asymmetric Approach | ||||||

|---|---|---|---|---|---|---|---|

| (2,0) | (1,1) | (0,2) | |||||

| 54.76 | 48.02 | 52.46 | 57.65 | ||||

| [53.42, 56.68] | [46.37, 50.42] | [51.07, 54.40] | [56.20, 59.70] | ||||

| (3,0) | (2,1) | (1,2) | (0,3) | ||||

| 70.69 | 63.59 | 67.30 | 71.18 | 75.04 | |||

| [69.12, 72.83] | [61.61, 66.03] | [65.72, 69.44] | [69.64, 73.31] | [73.30, 77.47] | |||

| (4,0) | (3,1) | (2,2) | (1,3) | (0,4) | |||

| 82.99 | 74.82 | 78.23 | 81.63 | 84.96 | 88.17 | ||

| [81.36, 85.29] | [72.59, 77.49] | [76.40, 80.58] | [80.03, 83.85] | [83.23, 87.32] | [86.19, 90.83] | ||

| (5,0) | (4,1) | (3,2) | (2,3) | (1,4) | (0,5) | ||

| 92.95 | 84.25 | 87.31 | 90.30 | 93.19 | 95.97 | 98.64 | |

| [91.05, 95.41] | [81.82, 87.14] | [85.27, 89.86] | [88.48, 92.62] | [91.42, 95.58] | [94.07, 98.54] | [96.51, 101.45] | |

| (6,0) | (5,1) | (4,2) | (1,5) | (0,6) | |||

| 101.14 | 92.31 | 95.02 | 97.65 | (…) | 104.93 | 107.16 | |

| [99.23, 103.68] | [89.76, 95.32] | [92.84, 97.71] | [95.68, 100.15] | [102.90, 107.64] | [104.87, 110.08] | ||

| (7,0) | (6,1) | (5,2) | (1,6) | (0,7) | |||

| 107.96 | 99.25 | 101.65 | 103.97 | (…) | 112.35 | 114.23 | |

| [105.97, 110.64] | [96.62, 102.31] | [99.32, 104.41] | [101.88, 106.60] | [110.18, 115.17] | [111.84, 117.24] | ||

| (8,0) | (7,1) | (6,2) | (1,7) | (0,8) | |||

| 113.72 | 105.28 | 107.41 | 109.47 | (…) | 118.57 | 120.17 | |

| [111.49, 116.55] | [102.57, 108.42] | [104.99, 110.26] | [107.26, 112.19] | [116.26, 121.51] | [117.68, 123.34] | ||

| (9,0) | (8,1) | (7,2) | (1,8) | (0,9) | |||