The bivariate -finite normal mixture “blanket” copula

Abstract

There exist many bivariate parametric copulas to model bivariate data with different dependence features. We propose a new bivariate parametric copula family that cannot only handle various dependence patterns that appear in the existing parametric bivariate copula families, but also provides a more enriched dependence structure. The proposed copula construction exploits finite mixtures of bivariate normal distributions. The mixing operation, the distinct correlation and mean parameters at each mixture component introduce quite a flexible dependence. The new parametric copula is theoretically investigated, compared with a set of classical bivariate parametric copulas and illustrated on two empirical examples from astrophysics and agriculture where some of the variables have peculiar and asymmetric dependence, respectively.

Key Words: Bivariate copulas; Dependence structure; Kullback-Leibler distance; Mixtures of bivariate normal distributions.

1 Introduction

Multivariate response data abound in many applications including insurance, risk management, finance, health and environmental sciences. Data from these application areas have different dependence structures including features such as tail dependence (Joe,, 1993), that is dependence among extreme values. Modelling dependence among multivariate outcomes is an interesting problem in statistical science. The dependence between random variables is completely described by their multivariate distribution. One may create multivariate distributions based on particular assumptions thus, limiting their use. For example, most existing multivariate distributions assume margins of the same form (e.g., Gaussian, Poisson, etc.) or limited dependence (e.g., tail independence, positive dependence, etc.).

To solve this problem, copula functions (Joe,, 1997, 2014; Nelsen,, 2006) seem to be a promising solution. The power of copulas for dependence modelling is due to the dependence structure being considered separate from the univariate margins. Copulas are a useful way to model multivariate data as they account for the dependence structure and provide a flexible representation of the multivariate distribution. They allow for flexible dependence modelling, different from assuming simple linear correlation structures and normality, which makes them well suited to the aforementioned application areas. In particular, the theory and application of copulas have become important in finance, insurance and other areas, in order to deal with dependence in the joint tails (Joe et al.,, 2010).

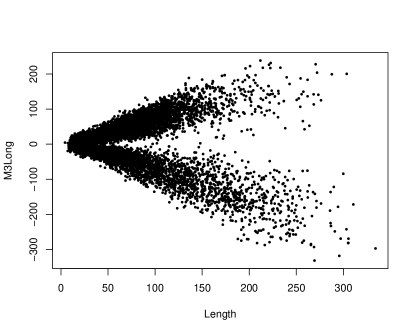

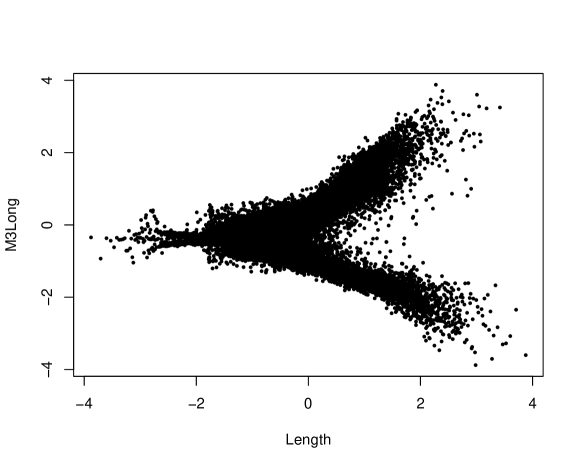

For the bivariate case, a rich variety of copula families is available and their properties are well-established (Joe,, 1997, 2014; Nelsen,, 2006). Nevertheless, a problem in practical applications is to identify the most plausible parametric family of bivariate copulas for dependence modelling (Durrleman et al.,, 2000; Huard et al.,, 2006; Nikoloulopoulos and Karlis,, 2008). Furthermore, sometimes none of the bivariate parametric copula families provides a good fit. For example, Nagler and Czado, (2016) and Czado, (2019) analysed the dependence between the Major Atmospheric Gamma Imaging Cherenkov (MAGIC) telescope variables (Bock et al.,, 2004) and pointed out the uncommon characteristics of the dependence structure between some of the variables, which do not correspond to any bivariate parametric copula. Figure 1 depicts, in particular the relationship between the length of the major axis of the ellipse (Length) and the third root of the third moment along the major axis (M3Long), and indeed reveals that none of the existing parametric families of bivariate copulas (see e.g., Joe, 1997, 2014) can model the joint distribution of these variables. Note in passing that in the right panel graph of Figure 1, we transform the data to the uniform scale by applying their empirical distributions, in order to isolate the effect of the marginal distributions and solely focus on the dependence structure.

|

|

In this paper, we propose a new parametric family of copulas that can represent the dependence structure between the aforementioned MAGIC variables. It can also remedy the copula selection issue as can “nearly” approximate any parametric family of bivariate copulas. A multivariate 2-finite normal mixture (FNM) copula has been proposed by Nikoloulopoulos and Karlis, (2009) to model multivariate discrete data. The correlation matrix for each mixture component was restricted to the identity matrix with the mixing operation introducing the dependence among the discrete responses. Therefore, it has a rather simple computational form, but suffers from a restricted range of attainable dependence. We will study the full dependence capacity of the bivariate -FNM copula, where is the number of mixture components, by using general correlation matrices for each mixture component and we will show that the the proposed -FNM is a “blanket” copula, i.e., a copula that can “nearly” approximate any bivariate parametric copula. A similar construction in the literature, which is called Bayesian non-parametric estimation of a copula (Wu et al.,, 2015; Dalla Valle et al.,, 2018), takes BVN copulas as the mixture components, hence it allows only for reflection symmetric dependence and is not as general as the proposed -FNM copula, which can allow reflection asymmetric dependence.

The remainder of the paper proceeds as follows. Section 2 introduces the bivariate -FNM copula, discusses its properties and provides computational details for maximum likelihood (ML) estimation. Before that it has a brief overview of relevant copula theory. Section 3 shows that the proposed copula is a “blanket” copula. Section 4 studies the small-sample efficiency of the proposed ML estimation technique. Section 5 illustrates the methods on two empirical examples from astrophysics and agriculture where some of the variables have peculiar and asymmetric dependence, respectively. We conclude with some discussion in Section 6.

2 The bivariate -finite normal mixture copula

In this section we will define the bivariate -FNM copula and study its properties. Before that, the first subsection has some background on bivariate copulas.

2.1 Overview and relevant background for copulas

A copula is a multivariate cumulative distribution function (cdf) with uniform margins (Joe,, 1997; Nelsen,, 2006; Joe,, 2014). If is a bivariate cdf with univariate margins , then Sklar’s (1959) theorem implies that there is a copula such that

The copula is unique if are continuous, but not if some of the have discrete components. If is continuous and , then the unique copula is the distribution of leading to

| (1) |

where are inverse cdfs. In particular, if is the bivariate normal (BVN) cdf with correlation and standard normal margins, and is the univariate standard normal cdf, then the BVN copula is

| (2) |

2.2 The bivariate -FNM copula

Let a bivariate -FNM distribution be defined as

where denotes the BVN distribution with mean vector and covariance matrix . Its cdf is given by

| (3) |

where is the cdf of the distribution.

From (1) if is the bivariate -FNM cdf in (3) and , where is the univariate -FNM cdf, then the bivariate -FNM copula is defined as

| (4) |

Subsequently, one can derive the bivariate -FNM copula density as below

| (5) |

where and is the univariate and bivariate density, respectively, of the -FNM distribution.

2.3 Dependence properties of the -FNM distribution

We study the dependence properties of the bivariate -FNM distribution as these will be inherited to the copula. The mean vector and covariance matrix of the -FNM are given respectively by

An aspect of mixture models is their lack of identifiability, but this can be overcome by imposing some restrictions in the parameters. In our approach, to overcome the typical identifiability issues we priory assume that , i.e., the mean vectors become

and that the variances of the mixture components are set to one, i.e., for .

The covariance matrix is then of the form where

and

As one can easily see, an identifiability problem still occurs. To overcome this, we set and .

Accordingly, the variance-covariance terms of reduce to

and

The Pearson’s correlation parameter is

and can attain the values.

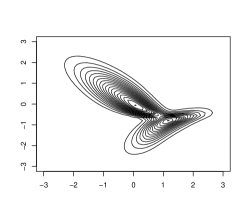

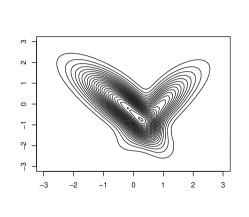

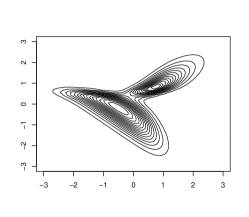

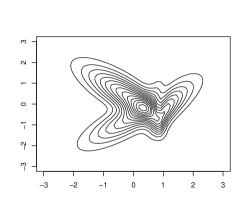

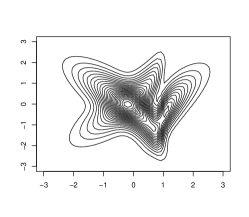

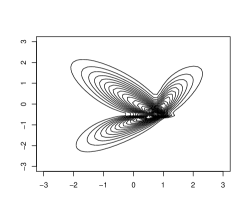

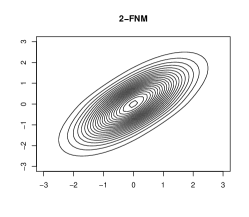

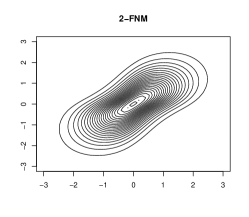

We depict some dependence shapes that can be imposed by the bivariate -FNM copula with the above parametrization in Figure 2.

|

|

|

|

|

|

2.4 Maximum likelihood estimation

In copula models, a copula is combined with a set of univariate margins. This is equivalent to assuming that variables have been transformed to uniform random variables . For data , we use either non-parametric or parametric univariate distributions to transform the data to copula data , i.e., data on the uniform scale. These semi-parametric and parametric estimation techniques have been developed by Genest et al., (1995) and Joe, (2005), respectively, and can be regarded as two-step approaches on the original data or simply as the standard one-step maximum likelihood (ML) method on the transformed (copula) data.

To this end, estimation of the -FNM copula parameters can be approached by maximizing the logarithm of the joint likelihood

where is the -FNM copula density given in (5). The estimated parameters can be obtained by using a quasi-Newton (Nash,, 1990) method applied to the logarithm of the joint likelihood. This numerical method requires only the objective function, i.e., the logarithm of the joint likelihood, while the gradients are computed numerically and the Hessian matrix of the second order derivatives is updated in each iteration. The standard errors (SE) of the ML estimates can be also obtained via the gradients and the Hessian computed numerically during the maximization process.

3 Is the bivariate -FNM a “blanket” copula?

In this section we will show that the -FNM copula is quite close to any parametric family of copulas. We will use the Kullback-Leibler methodology (Joe,, 2014, pages 234-241) to compare the new parametric copula family with existing parametric families of copulas. Before that, the first subsection provides choices of parametric bivariate copulas.

3.1 Existing parametric families of copulas

We will consider copula families that have different tail dependence (Joe,, 1993) or tail order (Hua and Joe,, 2011). A bivariate copula is reflection symmetric if its density satisfies for all . Otherwise, it is reflection asymmetric often with more probability in the joint upper tail or joint lower tail. Upper tail dependence means that as and lower tail dependence means that as . If for a bivariate copula , then , where is the survival or reflected copula of ; this “reflection” of each uniform random variable about changes the direction of tail asymmetry. Under some regularity conditions (e.g., existing finite density in the interior of the unit square, ultimately monotone in the tail), if there exists and some that is slowly varying at (i.e., as for all ), then is the lower tail order of . The upper tail order can be defined by the reflection of , i.e., as , where is the survival function of the copula and is a slowly varying function. With or , a bivariate copula has intermediate tail dependence if , tail dependence if , and tail quadrant independence if with being asymptomatically a constant.

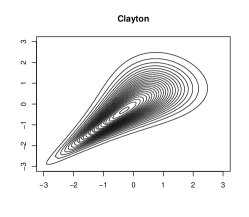

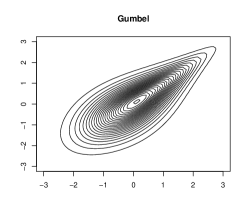

After briefly providing definitions of tail dependence and tail order we provide below a list of bivariate parametric copulas with varying tail behaviour:

-

•

Reflection symmetric copulas with intermediate tail dependence such as the BVN copula in (2) with , where is the copula (correlation) parameter.

-

•

Reflection symmetric copulas with tail quadrant independence (), such as the Frank copula.

-

•

Reflection asymmetric copulas with upper tail dependence only such as the Gumbel copula with () and (), where is the copula parameter.

-

•

Reflection asymmetric copulas with lower tail dependence only such as the Clayton copula with () and (), where is the copula parameter.

-

•

Reflection symmetric copulas with tail dependence, such as the copula with (), where is the correlation parameter of the bivariate distribution with degrees of freedom, and is the univariate cdf with degrees of freedom.

-

•

Reflection asymmetric copulas with upper and lower tail dependence that can range independently from 0 to 1, such as the BB1 copula with () and () or the BB7 copula with () and (), where and are the copula parameters.

The aforementioned bivariate copula families are sufficient for applications because tail dependence and tail order are properties to consider when choosing amongst different families of copulas, and the concepts of upper/lower tail dependence and upper/lower tail order are one way to differentiate families. Nikoloulopoulos and Karlis, (2008) and Joe, (2014) have shown that it is hard to choose a copula with similar tail dependence properties from real data because copulas with similar tail dependence properties provide similar fit.

3.2 Kullback-Leibler distance and sample size

For inferences based on likelihood, the Kullback-Leibler (KL) distance is relevant, especially as the parametric model used in the likelihood could be misspecified (Joe,, 2014). Typically, one considers several different models when analysing data, and from a theoretical point of view, the KL distance of pairs of competing models provides information on the sample size needed to discriminate them.

We will define the KL distance for two copula densities and the expected log-likelihood ratio. Because the KL is a non-negative quantity that is not bounded above, we use also the expected value of the square of the log-likelihood ratio in order to get a sample size value that is an indication of how different two copula densities are. Consider two copula densities (competing models) and with respect to Lebesgue or counting measure in . The KL distance between copulas with densities is defined as

| (6) |

The KL distance can be interpreted as the average difference of the contribution to the log-likelihood of one observation.

We use the log-likelihood ratio to get a sample size which gives an indication of the sample size needed to distinguish and with probability at least 0.95. If are similar, then will be larger, and if are far apart, then will be smaller. The calculation is based on an approximation from the Central Limit Theorem and assumes that the square of the log-likelihood ratio has finite variance when computed with being the true density (Joe,, 2014). If the variance of the log-density ratio is

then the KL sample size is

This is larger when is small or the variance is large.

3.3 Minimizing the KL distance

For a theoretical likelihood comparison between existing bivariate parametric families of copulas and the bivariate -FNM copula we minimize the KL distance in (6) where the true is the copula density of each of parametric bivariate copulas in Subsection 3.1 and is the copula density of the -FNM copula in (5), and hence (a) obtain the parameters of the -FNM copula that is quite close to the true copula in KL distance, (b) the KL sample size for these parameters. The minimized KL distances and resultant sample sizes will show the similarity or dissimilarity of the -FNM copula with the existing parametric families of copulas.

Numerical evaluation of or the variance can be approached using dependent Gauss-Legendre quadrature points (Nikoloulopoulos,, 2015) with the following steps:

-

1.

Calculate Gauss-Legendre quadrature points and weights in terms of standard uniform; see e.g., Stroud and Secrest, (1966).

-

2.

Convert from independent uniform random variables and to dependent uniform random variables and that have copula . The inverse of the conditional distribution corresponding to the copula is used to achieve this.

-

3.

Numerically evaluate

in a double sum:

With Gauss-Legendre quadrature, the same nodes and weights are used for different functions; this helps in yielding smooth numerical derivatives for numerical optimization via quasi-Newton (Nash,, 1990). Our comparisons show that is adequate with good precision to at least at four decimal places; hence it also provides the advantage of fast implementation.

| Copula | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| BVN | 0.1 | 0 | 0 | 0.000 | 0.500 | 0.090 | 0.134 | 0.134 | 5482651 |

| 0.2 | 0 | 0 | 0.000 | 0.500 | 0.179 | 0.267 | 0.267 | 248291 | |

| 0.3 | 0 | 0 | 0.000 | 0.500 | 0.269 | 0.398 | 0.398 | 47223 | |

| 0.4 | 0 | 0 | 0.000 | 0.500 | 0.359 | 0.526 | 0.526 | 16696 | |

| 0.5 | 0 | 0 | 0.000 | 0.500 | 0.451 | 0.647 | 0.647 | 8508 | |

| 0.6 | 0 | 0 | 0.001 | 0.500 | 0.544 | 0.758 | 0.758 | 5287 | |

| 0.7 | 0 | 0 | 0.001 | 0.500 | 0.642 | 0.855 | 0.855 | 3475 | |

| 0.8 | 0 | 0 | 0.002 | 0.500 | 0.746 | 0.931 | 0.931 | 2301 | |

| 0.9 | 0 | 0 | 0.003 | 0.493 | 0.864 | 0.982 | 0.982 | 1500 | |

| Frank | 0.1 | 0 | 0 | 0.000 | 0.500 | 0.149 | 0.060 | 0.060 | 14417 |

| 0.2 | 0 | 0 | 0.002 | 0.500 | 0.306 | 0.122 | 0.122 | 3729 | |

| 0.3 | 0 | 0 | 0.003 | 0.500 | 0.483 | 0.188 | 0.188 | 1814 | |

| 0.4 | 0 | 0 | 0.005 | 0.500 | 0.680 | 0.274 | 0.274 | 1175 | |

| 0.5 | 0 | 0 | 0.007 | 0.500 | 0.884 | 0.396 | 0.396 | 837 | |

| 0.6 | 0 | 0 | 0.011 | 0.500 | 1.096 | 0.549 | 0.549 | 537 | |

| 0.7 | 0 | 0 | 0.024 | 0.500 | 1.400 | 0.715 | 0.715 | 260 | |

| 0.8 | 0 | 0 | 0.067 | 0.500 | 1.161 | 0.860 | 0.860 | 111 | |

| 0.9 | 0 | 0 | 0.178 | 0.505 | 1.048 | 0.955 | 0.954 | 65 | |

| Clayton | 0.1 | 0.04 | 0 | 0.001 | 0.964 | 0.726 | 0.094 | -0.116 | 5262 |

| 0.2 | 0.25 | 0 | 0.003 | 0.917 | 0.794 | 0.171 | 0.285 | 1836 | |

| 0.3 | 0.45 | 0 | 0.005 | 0.869 | 0.863 | 0.248 | 0.591 | 1032 | |

| 0.4 | 0.59 | 0 | 0.008 | 0.812 | 0.915 | 0.326 | 0.762 | 669 | |

| 0.5 | 0.71 | 0 | 0.012 | 0.748 | 0.957 | 0.411 | 0.858 | 420 | |

| 0.6 | 0.79 | 0 | 0.020 | 0.687 | 0.991 | 0.519 | 0.921 | 247 | |

| 0.7 | 0.86 | 0 | 0.034 | 0.618 | 1.008 | 0.634 | 0.960 | 140 | |

| 0.8 | 0.92 | 0 | 0.061 | 0.538 | 1.010 | 0.755 | 0.983 | 79 | |

| 0.9 | 0.96 | 0 | 0.400 | 0.779 | 0.978 | 0.972 | 0.990 | 51 | |

| Gumbel | 0.1 | 0 | 0.13 | 0.000 | 0.012 | 1.075 | 0.638 | 0.129 | 104054 |

| 0.2 | 0 | 0.26 | 0.002 | 0.026 | 0.992 | 0.642 | 0.254 | 3962 | |

| 0.3 | 0 | 0.38 | 0.004 | 0.049 | 0.946 | 0.673 | 0.368 | 1891 | |

| 0.4 | 0 | 0.48 | 0.005 | 0.079 | 0.929 | 0.755 | 0.481 | 1405 | |

| 0.5 | 0 | 0.59 | 0.006 | 0.109 | 0.938 | 0.833 | 0.596 | 1153 | |

| 0.6 | 0 | 0.68 | 0.006 | 0.143 | 0.953 | 0.894 | 0.708 | 1004 | |

| 0.7 | 0 | 0.77 | 0.007 | 0.181 | 0.970 | 0.940 | 0.814 | 877 | |

| 0.8 | 0 | 0.85 | 0.008 | 0.221 | 0.986 | 0.973 | 0.905 | 758 | |

| 0.9 | 0 | 0.93 | 0.019 | 0.466 | 0.985 | 0.990 | 0.958 | 258 |

Table 1 shows the minimized KL distances and the corresponding 2-FNM copula parameters and KL sample sizes for comparing 1-parameter copula families, with symmetric or asymmetric dependence as the Kendall’s varies from 0.1 to 0.9, versus the bivariate 2-FNM copula. Table 2 shows the minimized KL distances and the corresponding 2-FNM or 3-FNM copula parameters and KL sample sizes for comparing the BB1 copula, with reflection asymmetric tail dependence () as the lower and upper tail dependence varies from 0.1 to 0.9 and from 0.9 to 0.1, respectively, versus the bivariate 2- or 3-FNM copula. Table 3 shows the minimized KL distances and the corresponding 2-FNM or 3-FNM copula parameters and KL sample sizes for comparing the copula for a small , with reflection symmetric tail dependence () as the Kendall’s varies from 0.1 to 0.9, versus the bivariate 2- or 3-FNM copula.

| 0.1 | 0.9 | 0.87 | 2 | 0.009 | 0.227 | 0.994 | 0.988 | 0.956 | 737 | |||

| 0.2 | 0.8 | 0.75 | 3 | 0.006 | 0.087 | 0.426 | 1.599 | -0.799 | 0.918 | 0.951 | 0.850 | 1271 |

| 0.3 | 0.7 | 0.66 | 2 | 0.006 | 0.081 | 0.978 | 0.932 | 0.821 | 1140 | |||

| 0.4 | 0.6 | 0.59 | 3 | 0.001 | 0.026 | 0.545 | 1.729 | -0.858 | 0.576 | 0.695 | 0.894 | 4437 |

| 0.5 | 0.5 | 0.55 | 3 | 0.005 | 0.005 | 0.537 | 3.565 | -1.765 | 0.670 | 0.654 | 0.881 | 909 |

| 0.6 | 0.4 | 0.54 | 2 | 0.007 | 0.923 | 0.986 | 0.687 | 0.853 | 963 | |||

| 0.7 | 0.3 | 0.56 | 2 | 0.006 | 0.839 | 0.973 | 0.642 | 0.889 | 979 | |||

| 0.8 | 0.2 | 0.63 | 2 | 0.013 | 0.728 | 0.994 | 0.643 | 0.934 | 414 | |||

| 0.9 | 0.1 | 0.77 | 2 | 0.042 | 0.580 | 1.009 | 0.743 | 0.977 | 120 |

The conclusion from the values in the tables are:

-

•

The -FNM copula is close to any parametric bivariate family of copulas and a large sample size is required to distinguish when the Kendall’s values range from 0.1 (weak dependence) to 0.5 (moderate dependence).

-

•

To approximate copulas with refection symmetric or asymmetric tail dependence, they are required up to mixture components, while for any 1-parameter family mixture components are sufficient.

-

•

Since the -FNM copula and each of the parametric families of copulas have the same strength of dependence as given by Kendall’s , the magnitude of the KL distance is related to the closeness of the strength of dependence in the tails. This is because copula densities can asymptote to infinity in a joint tail at different rates (tail order less than dimension d) or converge to a constant in the joint tail (if tail order is the dimension d or larger), see e.g, Joe, (2014).

-

•

Copula families with stronger dependence have larger KL distance with the -FNM copula than those with weaker dependence when strength of dependence in the tails are different based on the tail orders.

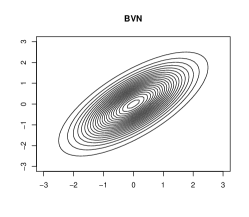

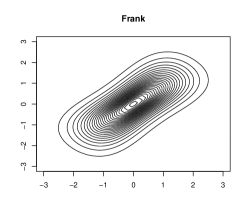

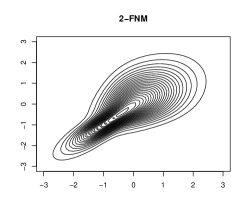

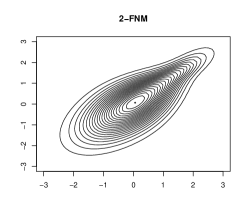

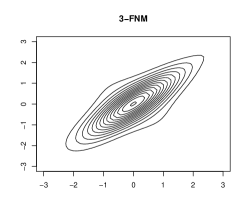

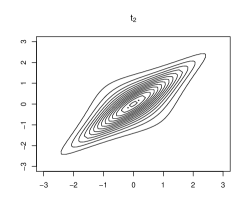

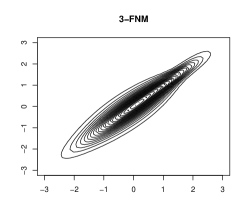

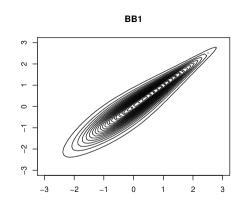

Figure 3 summarizes these results by depicting the contour plots of the 2- or 3-FNM copula with the parameters in Tables 1–3, i.e., the ones that the FNM copulas are close in terms of KL distance to the true copulas, and normal margins, along with the contour plots of the true copulas with normal margins. We summarize the case of ( for BB1).

| 2 | 0.1 | 0.24 | 0.24 | 3 | 0.004 | 0.004 | 0.436 | 2.003 | -0.986 | 0.756 | -0.582 | 0.689 | 1602 |

| 0.2 | 0.30 | 0.30 | 3 | 0.004 | 0.005 | 0.365 | 1.988 | -0.978 | 0.738 | -0.531 | 0.731 | 1535 | |

| 0.3 | 0.37 | 0.37 | 3 | 0.004 | 0.005 | 0.291 | 2.037 | -1.004 | 0.737 | -0.488 | 0.769 | 1338 | |

| 0.4 | 0.44 | 0.44 | 3 | 0.006 | 0.006 | 0.221 | 1.978 | -0.972 | 0.732 | -0.443 | 0.808 | 1002 | |

| 0.5 | 0.52 | 0.52 | 3 | 0.008 | 0.010 | 0.170 | 1.653 | -0.807 | 0.705 | -0.350 | 0.852 | 640 | |

| 0.6 | 0.61 | 0.61 | 3 | 0.012 | 0.010 | 0.166 | 1.906 | -0.938 | 0.735 | 0.057 | 0.906 | 375 | |

| 0.7 | 0.71 | 0.71 | 3 | 0.014 | 0.011 | 0.156 | 2.015 | -0.997 | 0.817 | 0.435 | 0.945 | 498 | |

| 0.8 | 0.80 | 0.80 | 3 | 0.026 | 0.000 | 0.108 | 1.666 | -0.819 | 0.599 | 0.441 | 0.976 | 181 | |

| 0.9 | 0.90 | 0.90 | 2 | 0.085 | 0.007 | 0.694 | 0.990 | 0.989 | 109 | ||||

| 3 | 0.1 | 0.16 | 0.16 | 3 | 0.001 | 0.003 | 0.411 | 2.103 | -1.037 | 0.688 | -0.498 | 0.589 | 10194 |

| 0.2 | 0.22 | 0.22 | 3 | 0.001 | 0.004 | 0.331 | 2.118 | -1.044 | 0.656 | -0.441 | 0.643 | 6923 | |

| 0.3 | 0.29 | 0.29 | 3 | 0.002 | 0.004 | 0.264 | 2.137 | -1.053 | 0.638 | -0.363 | 0.703 | 3576 | |

| 0.4 | 0.37 | 0.37 | 3 | 0.003 | 0.005 | 0.213 | 2.318 | -1.143 | 0.626 | -0.234 | 0.766 | 1865 | |

| 0.5 | 0.45 | 0.45 | 3 | 0.005 | 0.005 | 0.185 | 6.257 | -3.115 | 0.691 | 0.004 | 0.830 | 1050 | |

| 0.6 | 0.55 | 0.55 | 3 | 0.006 | 0.007 | 0.195 | 2.103 | -1.038 | 0.697 | 0.365 | 0.892 | 966 | |

| 0.7 | 0.66 | 0.66 | 3 | 0.006 | 0.008 | 0.206 | 2.085 | -1.035 | 0.801 | 0.650 | 0.940 | 983 | |

| 0.8 | 0.77 | 0.77 | 3 | 0.023 | 0.000 | 0.051 | 0.265 | -0.290 | 0.302 | 0.279 | 0.966 | 174 | |

| 0.9 | 0.88 | 0.88 | 3 | 0.050 | 0.001 | 0.000 | 0.761 | 0.621 | 0.154 | 0.171 | 0.987 | 123 | |

| 4 | 0.1 | 0.11 | 0.11 | 3 | 0.000 | 0.001 | 0.403 | 2.609 | -1.302 | -0.990 | -0.432 | 0.543 | 34841 |

| 0.2 | 0.17 | 0.17 | 3 | 0.000 | 0.003 | 0.315 | 2.372 | -1.172 | 0.626 | -0.369 | 0.593 | 119419 | |

| 0.3 | 0.23 | 0.23 | 3 | 0.001 | 0.003 | 0.247 | 2.683 | -1.326 | 0.545 | -0.276 | 0.662 | 15265 | |

| 0.4 | 0.31 | 0.31 | 3 | 0.002 | 0.005 | 0.213 | 2.858 | -1.409 | 0.545 | -0.085 | 0.739 | 4058 | |

| 0.5 | 0.40 | 0.40 | 3 | 0.003 | 0.005 | 0.222 | 2.609 | -1.288 | 0.611 | 0.229 | 0.820 | 2052 | |

| 0.6 | 0.50 | 0.50 | 3 | 0.003 | 0.006 | 0.259 | 2.596 | -1.287 | 0.675 | 0.531 | 0.890 | 1935 | |

| 0.7 | 0.61 | 0.61 | 3 | 0.002 | 0.007 | 0.266 | 1.981 | -0.985 | 0.775 | 0.738 | 0.938 | 3018 | |

| 0.8 | 0.74 | 0.74 | 2 | 0.025 | 0.951 | 0.925 | 0.949 | 0.848 | 256 | ||||

| 0.9 | 0.87 | 0.87 | 2 | 0.024 | 0.946 | 0.984 | 0.987 | 0.959 | 255 | ||||

| 5 | 0.1 | 0.08 | 0.08 | 3 | 0.000 | 0.001 | 0.470 | 2.725 | -1.345 | -0.990 | -0.315 | 0.532 | 168891 |

| 0.2 | 0.13 | 0.13 | 3 | -0.001 | 0.002 | 0.297 | 4.390 | -2.169 | 0.674 | -0.323 | 0.556 | 10836 | |

| 0.3 | 0.18 | 0.18 | 3 | 0.000 | 0.004 | 0.250 | 4.863 | -2.408 | 0.473 | -0.178 | 0.639 | 97784 | |

| 0.4 | 0.26 | 0.26 | 3 | 0.001 | 0.004 | 0.228 | 2.778 | -1.371 | 0.513 | 0.043 | 0.726 | 7140 | |

| 0.5 | 0.35 | 0.35 | 3 | 0.003 | 0.001 | 0.245 | 0.469 | -0.231 | 0.392 | 0.339 | 0.818 | 1450 | |

| 0.6 | 0.46 | 0.46 | 3 | 0.001 | 0.005 | 0.293 | 2.113 | -1.047 | 0.642 | 0.598 | 0.886 | 3961 | |

| 0.7 | 0.58 | 0.58 | 3 | 0.001 | 0.006 | 0.326 | 1.879 | -0.934 | 0.752 | 0.783 | 0.938 | 12785 | |

| 0.8 | 0.71 | 0.71 | 2 | 0.016 | 0.038 | 0.860 | 0.896 | 0.949 | 392 | ||||

| 0.9 | 0.85 | 0.85 | 2 | 0.015 | 0.035 | 0.970 | 0.967 | 0.987 | 394 |

If two copula models are applied to discrete variables and have the same strength of dependence as given by the Kendall’s , then the KL distance gets smaller. This is because the different asymptotic rates in the joint tails of the copula density do not affect rectangle probabilities for the log-likelihood with discrete response (Joe,, 2014). This means that a discretized -FNM copula model will be close to any copula model for discrete data even for strong dependence.

|

|

|

|

|

|

|

|

|

|

|

|

To show that we use ordinal response variables, say with regressions on a scalar covariate , which is assumed to take values equally spaced in . Let be a latent variable with cdf , such that if where is the number of categories of (without loss of generality, we assume and ), and is the slope of . From this definition, the ordinal response is assumed to have probability mass function (pmf)

Note that normal leads to the probit model and logistic leads to the cumulative logit model for ordinal response. With copula families, the bivariate pmf (see e.g., Nikoloulopoulos and Karlis, 2010) can be obtained as

| (7) | |||||

Let and denote the bivariate pmfs defined as in (7) for the bivariate Clayton and -FNM copula, respectively. Then the is

| 0.1 | 0.04 | 2 | 0.003 | 0.950 | 0.908 | 0.080 | -0.143 | 1788690 |

| 0.2 | 0.25 | 0.007 | 0.885 | 0.890 | 0.150 | -0.898 | 721543 | |

| 0.3 | 0.45 | 0.010 | 0.817 | 0.972 | 0.216 | -0.558 | 534811 | |

| 0.4 | 0.59 | 0.015 | 0.744 | 0.989 | 0.289 | 0.187 | 353990 | |

| 0.5 | 0.71 | 0.017 | 0.678 | 0.981 | 0.380 | 0.607 | 311204 | |

| 0.6 | 0.79 | 0.006 | 0.609 | 0.987 | 0.486 | 0.822 | 838516 | |

| 0.7 | 0.86 | 0.042 | 0.574 | 0.995 | 0.671 | 0.933 | 122823 | |

| 0.8 | 0.92 | 0.091 | 0.559 | 0.992 | 0.854 | 0.981 | 55142 | |

| 0.9 | 0.96 | 0.190 | 0.773 | 0.980 | 0.983 | 1.000 | 30454 | |

| 0.1 | 0.04 | 3 | 0.051 | 0.943 | 0.760 | 0.075 | -0.865 | 106069 |

| 0.2 | 0.25 | 0.139 | 0.884 | 0.863 | 0.145 | -0.430 | 39171 | |

| 0.3 | 0.45 | 0.247 | 0.816 | 0.905 | 0.213 | 0.056 | 22213 | |

| 0.4 | 0.59 | 0.331 | 0.746 | 0.916 | 0.284 | 0.470 | 16706 | |

| 0.5 | 0.71 | 0.248 | 0.674 | 0.944 | 0.358 | 0.720 | 22017 | |

| 0.6 | 0.79 | 0.196 | 0.609 | 0.990 | 0.467 | 0.856 | 27265 | |

| 0.7 | 0.86 | 0.503 | 0.555 | 1.022 | 0.625 | 0.938 | 9672 | |

| 0.8 | 0.92 | 0.791 | 0.503 | 1.022 | 0.802 | 0.981 | 5770 | |

| 0.9 | 0.96 | 0.690 | 0.554 | 1.018 | 0.959 | 1.000 | 8247 | |

| 0.1 | 0.04 | 4 | 0.114 | 0.945 | 0.755 | 0.075 | -0.608 | 47632 |

| 0.2 | 0.25 | 0.330 | 0.884 | 0.832 | 0.144 | -0.218 | 16580 | |

| 0.3 | 0.45 | 0.598 | 0.820 | 0.875 | 0.214 | 0.206 | 9236 | |

| 0.4 | 0.59 | 0.774 | 0.754 | 0.905 | 0.286 | 0.545 | 7137 | |

| 0.5 | 0.71 | 0.704 | 0.683 | 0.948 | 0.363 | 0.743 | 7673 | |

| 0.6 | 0.79 | 0.775 | 0.611 | 0.993 | 0.464 | 0.859 | 6808 | |

| 0.7 | 0.86 | 1.429 | 0.546 | 1.024 | 0.609 | 0.935 | 3410 | |

| 0.8 | 0.92 | 2.070 | 0.486 | 1.028 | 0.781 | 0.980 | 2213 | |

| 0.9 | 0.96 | 2.387 | 0.622 | 1.024 | 0.964 | 1.000 | 2833 | |

| 0.1 | 0.04 | 5 | 0.175 | 0.946 | 0.748 | 0.075 | -0.511 | 31010 |

| 0.2 | 0.25 | 0.525 | 0.886 | 0.817 | 0.144 | -0.121 | 10462 | |

| 0.3 | 0.45 | 0.956 | 0.823 | 0.861 | 0.214 | 0.280 | 5787 | |

| 0.4 | 0.59 | 1.216 | 0.757 | 0.899 | 0.285 | 0.582 | 4518 | |

| 0.5 | 0.71 | 1.186 | 0.687 | 0.948 | 0.362 | 0.757 | 4535 | |

| 0.6 | 0.79 | 1.449 | 0.615 | 0.996 | 0.464 | 0.864 | 3616 | |

| 0.7 | 0.86 | 2.583 | 0.549 | 1.027 | 0.606 | 0.936 | 1892 | |

| 0.8 | 0.92 | 3.752 | 0.482 | 1.029 | 0.772 | 0.979 | 1229 | |

| 0.9 | 0.96 | 3.729 | 0.490 | 1.020 | 0.941 | 1.000 | 1593 |

Table 4 shows the minimized KL distances, the corresponding 2-FNM copula parameters and KL sample sizes for comparing the discretized Clayton copula model, as the Kendall’s varies from 0.1 to 0.9, versus the discretized 2-FNM copula model. We show the comparison results versus the Clayton copula, as in Table 1 it was revealed that the Clayton copula is the 1-parameter copula family which is the most far apart from the 2-FNM copula for continuous responses. We used univariate ordinal regressions, but note that using ordinal probit regressions led to similar results.

The conclusions from the table and the other computations we have done for other copula families are:

-

•

The -FNM copula is close to any parametric bivariate family of copulas if two copulas models are applied to discrete variables.

-

•

With discrete response variables, it takes larger sample sizes to distinguish the -FNM copula (because tails of the copula densities would not be “observed”).

-

•

The KL distances (sample sizes) get larger (smaller) with less discretization, i.e., as increases.

4 Simulations

To gauge the small sample efficiency of the ML estimation method in Section 2.4 to estimate the -FNM copula parameters, we performed several simulation studies using -FNM copula models with various parameter choices for . We report here typical results from these experiments.

We randomly generated samples of size from the 2-and 3-FNM bivariate copulas with exponential margins and marginal parameters and . We have transformed the simulated data to uniform random variables using their empirical distributions, i.e., we have approached estimation of the -FNM copula parameters using the semi-parametric estimation (Genest et al.,, 1995). We have used as initial values the ones that resemble the independence copula.

Table 5 contains the copula parameter values, the bias, standard deviation (SD) and the root mean square errors (RMSE) of the ML estimates, along with the average of their theoretical SDs. The theoretical SD of the ML estimate is obtained via the gradients and the Hessian computed numerically during the maximization process. The conclusions from the table and the other computations we have done are that

-

•

ML is highly efficient according to the simulated biases, SDs and RMSEs as the sample size increases.

-

•

The SDs computed from the simulations are close to the asymptotic SDs as the sample size increases.

-

•

For small samples the estimates of the mean parameters have upward bias.

| Bias | 100 | 0.001 | 0.017 | 0.001 | -0.001 |

|---|---|---|---|---|---|

| 300 | -0.001 | 0.009 | 0.002 | -0.001 | |

| 500 | -0.001 | 0.005 | 0.001 | -0.001 | |

| SD | 100 | 0.074 | 0.170 | 0.090 | 0.048 |

| 300 | 0.039 | 0.086 | 0.042 | 0.026 | |

| 500 | 0.030 | 0.066 | 0.032 | 0.020 | |

| 100 | 0.046 | 0.111 | 0.066 | 0.039 | |

| 300 | 0.026 | 0.058 | 0.037 | 0.022 | |

| 500 | 0.019 | 0.042 | 0.028 | 0.017 | |

| RMSE | 100 | 0.074 | 0.171 | 0.090 | 0.048 |

| 300 | 0.039 | 0.087 | 0.042 | 0.026 | |

| 500 | 0.030 | 0.066 | 0.032 | 0.020 | |

| Bias | 100 | -0.028 | -0.018 | 0.704 | 0.258 | -0.093 | 0.088 | -0.069 |

|---|---|---|---|---|---|---|---|---|

| 300 | -0.002 | -0.001 | 0.113 | 0.041 | -0.009 | 0.006 | -0.005 | |

| 500 | -0.001 | 0.000 | 0.031 | -0.001 | 0.000 | 0.000 | 0.001 | |

| SD | 100 | 0.120 | 0.091 | 1.054 | 0.932 | 0.320 | 0.222 | 0.205 |

| 300 | 0.061 | 0.042 | 0.438 | 0.360 | 0.088 | 0.066 | 0.056 | |

| 500 | 0.041 | 0.031 | 0.209 | 0.182 | 0.064 | 0.038 | 0.030 | |

| 100 | 0.028 | 0.034 | 0.290 | 0.324 | 0.252 | 0.116 | 0.061 | |

| 300 | 0.022 | 0.024 | 0.089 | 0.086 | 0.060 | 0.041 | 0.031 | |

| 500 | 0.019 | 0.019 | 0.064 | 0.063 | 0.037 | 0.031 | 0.023 | |

| RMSE | 100 | 0.123 | 0.093 | 1.268 | 0.967 | 0.333 | 0.238 | 0.217 |

| 300 | 0.061 | 0.042 | 0.453 | 0.363 | 0.089 | 0.066 | 0.057 | |

| 500 | 0.041 | 0.031 | 0.211 | 0.182 | 0.064 | 0.038 | 0.030 | |

5 Empirical examples

In this section we illustrate the proposed methodology by analysing two real data examples with distinct dependence structures, the first in the area of astrophysics and the second in agriculture. In Section 5.1 we analyse the two aforementioned MAGIC variables with peculiar dependence that typical bivariate copulas fail to model, while in Section 5.2 we analyse three variables from the 1985 survey of nutritional habits commissioned by the United States Department of Agriculture that have strong reflection asymmetric dependence.

We estimate each marginal distribution non-parametrically by the empirical distribution function of , viz.

where denotes the rank of . Hence we allow the distribution of the continuous margins to be quite free and not restricted by parametric families. We use simple diagnostics to identify the suitable copula family. Although copula theory uses transforms to standard uniform margins, for diagnostics, we convert the original data to normal scores using the normal quantiles of their empirical distributions. With a bivariate normal scores plot (Nikoloulopoulos et al.,, 2012) one can check for deviations from the elliptical shape that would be expected with the BVN copula, and hence assess if tail asymmetry exists on the data.

Having discussed why more flexible dependencies are needed we proceed with the -FNM copula models and construct a plausible -FNM copula model, to capture any type of dependence. For a baseline comparison, we initially fit the typical copula families presented in Section 3.1. To make it easier to compare strengths of dependence, we convert the estimated copula parameters to Kendall’s ’s, lower tail dependence and upper tail dependence via the relations in Joe, (2014, Chapter 4). The estimated Kendall’s of the -FNM copula, viz.

has been calculated via adaptive bivariate integration over hypercubes (Narasimhan et al.,, 2018); is the -FNM copula cdf given in (3).

To find a copula model that provides a good fit we don’t use goodness-of-fit procedures (see e.g., Genest et al., 2009 and the references therein), but we rather adopt the Akaike’s information criterion (AIC). The goodness-of-fit procedures involve a global distance measure between the model-based and empirical distribution, hence they might not be sensitive to tail behaviours and are not diagnostic in the sense of suggesting improved parametric models in the case of small -values (Joe,, 2014). For vine copulas, Dissmann et al., (2013) found that pair-copula selection based on likelihood and AIC seem to be better than using bivariate goodness-of-fit tests. The AIC is

and a smaller AIC value indicates a copula model better approximates both the dependence structure of the data, and the strength of dependence in the tails.

5.1 MAGIC telescope

Ground-based atmospheric Cherenkov telescopes using the imaging technique are a useful addition to the variety of instruments used by astrophysicists. The MAGIC telescope, located on the Canary islands, observes high-energy gamma rays, detecting the radiation emitted by charged particles produced inside electromagnetic showers. Depending on the energy of the primary gamma, Cherenkov photons get collected, in patterns (called the shower image), allowing to discriminate statistically those caused by primary gammas (signal) from the images of hadronic showers initiated by cosmic rays in the upper atmosphere (background). Typically, the image of a shower is an elongated cluster; its long axis is oriented towards the camera center if the shower axis is parallel to the telescope’s optical axis, i.e. if the telescope axis is directed towards a point source. If the depositions were distributed as a BVN, this would be an equidensity ellipse. The characteristic parameters of this ellipse are among the image parameters. The energy depositions are typically asymmetric along the major axis (Bock et al.,, 2004).

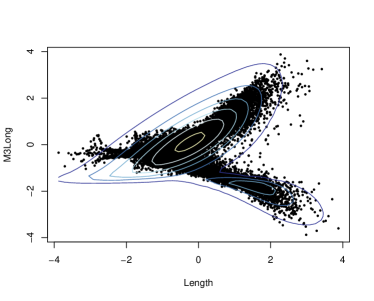

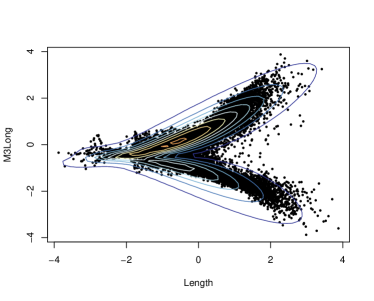

We apply the -FNM copula to 2 out of 10 MAGIC image parameters in Bock et al., (2004). Our objective is to describe the joint distribution of the Length and M3Long that have a peculiar dependence. The data set with the 10 MAGIC image parameters is available from the UCI Machine Learning Repository web page and comprises observations. In Figure 4 we depict the bivariate normal scores plot for the Length and M3Long. From the plot, it is revealed that none of the existing parametric families of copulas can adequately model the dependence structure between the variables.

Table 6 gives the AICs, estimated copula parameters and their SE, along with the family-based Kendall’s and tail dependence parameters for each fitted parametric family of copulas. The AICs show, that among the existing parametric families of copulas, the copula provides the best fit.

| Copula | AIC | SE | SE | |||||

|---|---|---|---|---|---|---|---|---|

| BVN | -648.1 | 0.183 | 0.007 | 0.117 | ||||

| -4590.3 | 0.352 | 0.008 | 2.159 | 0.042 | 0.229 | 0.302 | 0.302 | |

| Clayton | 2.1 | 0.000 | 0.002 | 0.000 | 0.000 | |||

| Gumbel | -3069.4 | 1.314 | 0.007 | 0.239 | 0.305 | |||

| Frank | -2004.5 | 2.167 | 0.049 | 0.230 | ||||

| BB1 | -3059.3 | 0.001 | 1.314 | 0.007 | 0.239 | 0.305 | ||

| BB7 | -4110.6 | 1.591 | 0.013 | 0.001 | 0.021 | 0.249 | 0.454 | |

| Survival Clayton | -3363.7 | 0.651 | 0.013 | 0.246 | 0.345 | |||

| Survival Gumbel | -228.1 | 1.102 | 0.007 | 0.093 | 0.125 | |||

| Survival BB1 | -3353.45 | 0.650 | 0.022 | 1.001 | 0.012 | 0.246 | 0.001 | 0.500 |

| Survival BB7 | -3355.2 | 1.001 | 0.013 | 0.651 | 0.014 | 0.246 | 0.001 | 0.345 |

| Est. | SE | Est. | SE | |||

| 0.127 | 0.001 | 0.001 | 0.000 | |||

| 0.334 | 0.000 | |||||

| -1.882 | 0.016 | -1.045 | 0.002 | |||

| -1.145 | 0.001 | |||||

| -0.784 | 0.006 | -0.470 | 0.103 | |||

| 0.747 | 0.003 | -0.854 | 0.003 | |||

| 0.901 | 0.001 | |||||

| 0.304 | 0.310 | |||||

| AIC | -17320.5 | -27064.1 | ||||

Then we exploit the use of the -FNM copula to construct a plausible copula family to represent the joint distribution of Length and M3Long. Table 7 gives the AICs, estimated copula parameters and their SE, along with the family-based Kendall’s for different numbers of components. The AICs show, that the 3-FNM copula provides the best fit and provides much better fit than the , since the AIC has been improved by . Note in passing that using , the estimated mixing probabilities for the extra components were close to zero, and, hence, there was no improvement in fit. In Figure 5 we depict the estimated contour plots of the 2- and 3-FNM copulas with standard normal margins, along with the bivariate normal scores plots. From the plots, it is revealed that the 3-FNM copula provides a realistic representation of the joint distribution.

|

|

The new-parametric family of copulas does not only allow to make accurate inferences that are based on the joint distribution, but also provides superior statistical inference for the parameters of interest, such as Kendall’s . From Table 9, it is revealed that the Kendall’s was underestimated using simple parametric families of copulas and a change from a -value of 0.23 (-based) to one slightly larger than 0.30 has been achieved.

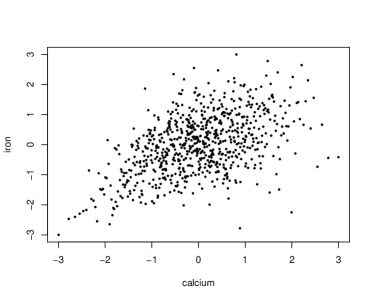

5.2 Nutritional habits

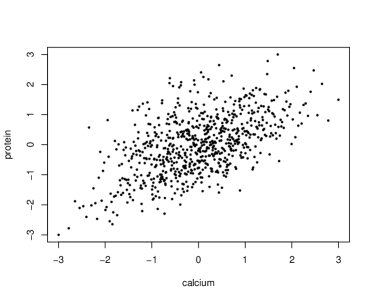

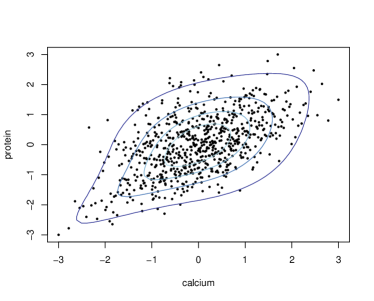

McNeil and Nešlehová, (2010) analysed three variables, namely daily calcium intake (in mg), daily iron intake (in mg) and daily protein intake (in g), of =747 female respondents aged between 25 and 50 years to the 1985 survey of nutritional habits commissioned by the United States Department of Agriculture. This dataset and its description can be found in the R package lcopula (Belzile et al.,, 2019). Genest et al., (2012) identified a strongly asymmetric dependence structure between the intakes of calcium and iron, and between the intakes of calcium and protein. In this section we apply the -FNM copula to the pairs identified as asymmetric to illustrate that it can sufficiently allow for reflection asymmetric dependence. In Figure 6 we depict the bivariate normal scores plots for the pairs identified as asymmetric. From the plots, it is revealed that there is more skewness in the lower tail.

|

|

| Calcium and Iron | ||||||||

|---|---|---|---|---|---|---|---|---|

| Copula | AIC | SE | SE | |||||

| BVN | -203.0 | 0.497 | 0.025 | 0.331 | ||||

| -216.6 | 0.492 | 0.030 | 6.563 | 2.026 | 0.328 | 0.149 | 0.149 | |

| Clayton | -230.7 | 0.885 | 0.069 | 0.307 | 0.457 | |||

| Gumbel | -162.0 | 1.412 | 0.040 | 0.292 | 0.366 | |||

| Frank | -173.0 | 3.140 | 0.238 | 0.319 | ||||

| BB1 | -238.3 | 0.684 | 0.091 | 1.115 | 0.043 | 0.332 | 0.403 | 0.138 |

| BB7 | -238.9 | 1.165 | 0.059 | 0.807 | 0.075 | 0.329 | 0.424 | 0.187 |

| Survival Clayton | -114.8 | 0.582 | 0.061 | 0.225 | 0.304 | |||

| Survival Gumbel | -239.6 | 1.490 | 0.043 | 0.329 | 0.408 | |||

| Survival BB1 | -237.7 | 0.016 | 0.063 | 1.480 | 0.057 | 0.330 | 0.403 | 0.626 |

| Survival BB7 | -240.6 | 1.611 | 0.069 | 0.270 | 0.070 | 0.320 | 0.462 | 0.077 |

| Calcium and Protein | ||||||||

| Copula | AIC | SE | SE | |||||

| BVN | -267.8 | 0.558 | 0.022 | 0.377 | ||||

| -268.9 | 0.553 | 0.025 | 12.323 | 6.752 | 0.373 | 0.072 | 0.072 | |

| Clayton | -261.7 | 0.965 | 0.071 | 0.325 | 0.487 | |||

| Gumbel | -217.2 | 1.499 | 0.043 | 0.333 | 0.412 | |||

| Frank | -227.2 | 3.657 | 0.244 | 0.362 | ||||

| BB1 | -282.3 | 0.633 | 0.091 | 1.196 | 0.049 | 0.365 | 0.401 | 0.215 |

| BB7 | -281.3 | 1.264 | 0.066 | 0.838 | 0.079 | 0.357 | 0.437 | 0.270 |

| Survival Clayton | -166.0 | 0.714 | 0.064 | 0.263 | 0.379 | |||

| Survival Gumbel | -283.3 | 1.567 | 0.045 | 0.362 | 0.444 | |||

| Survival BB1 | -284.4 | 0.115 | 0.068 | 1.493 | 0.060 | 0.367 | 0.409 | 0.629 |

| Survival BB7 | -284.6 | 1.632 | 0.073 | 0.407 | 0.074 | 0.354 | 0.471 | 0.182 |

Table 8 gives the AICs, estimated copula parameters and their SE, along with the family-based Kendall’s and tail dependence parameters for each fitted parametric family of copulas. The AICs show, that among the existing parametric families of copulas, the survival BB7 copula provides the best fit for both pairs identified as asymmetric.

| Calcium and Iron | Calcium and Protein | |||||

| Est. | SE | Est. | SE | |||

| 0.848 | 0.055 | 0.953 | 0.008 | |||

| 0.518 | 0.136 | 2.012 | 0.094 | |||

| 0.339 | 0.044 | 0.474 | 0.030 | |||

| 0.779 | 0.062 | 0.594 | 0.108 | |||

| 0.330 | 0.341 | |||||

| AIC | -243.7 | -291.7 | ||||

| 2-FNM | Survival BB7 |

|---|---|

|

|

| 2-FNM | Survival BB7 |

|

|

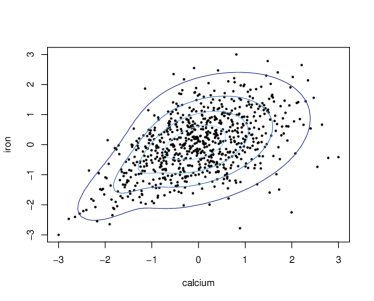

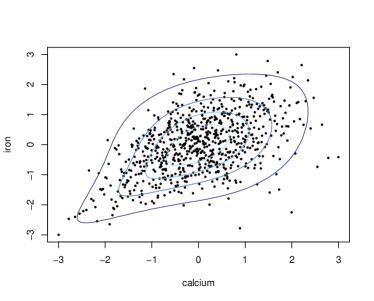

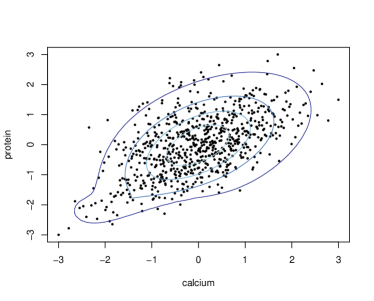

Then we exploit the use of the -FNM copula to construct a plausible copula family to represent the joint distribution of both pairs of variables. It has been revealed, that for both pairs mixture components are sufficient to describe their dependence. Table 9 gives the AICs and estimated 2-FNM copula parameters, along with their standard errors. The AICs show, that between the intakes of calcium and iron and between the intakes of calcium and protein the 2-FNM copula provides better fit than the survival BB7, since the AIC has been improved by and , respectively. In Figure 7 we depict the estimated contour plots of the 2-FNM and survival BB7 copulas with standard normal margins, along with the bivariate normal scores plot for the pairs identified as asymmetric in the nutrient data set. From the plots, it is revealed that the 2-FNM copula provides a nearly identical or even better representation of the joint distribution compared to the survival BB7 (best fit amongst the existing parametric families of copulas).

6 Discussion

We have proposed the -FNM parametric family of bivariate copulas and demonstrated that the new family is so flexible, it removes the ad-hoc constraints on the tails of existing parametric copula families, and is able to handle various dependence patterns that appear in the existing parametric bivariate copula families.

There exist many bivariate copula families, and as the new copula family can “nearly” approximate any of these, the selection of the appropriate copula family among many candidates can be subsided by solely using the -FNM copula. This applies when the data are continuous and have weak to moderate dependence and when the data are discrete for any different strength of dependence.

Given that bivariate copulas are building blocks for many multivariate dependence models such as the vine (e.g., Nikoloulopoulos et al., 2012; Panagiotelis et al., 2012; Dissmann et al., 2013) and factor (e.g., Krupskii and Joe, 2013; Nikoloulopoulos and Joe, 2015; Kadhem and Nikoloulopoulos, 2021) copula models, there is much potential of the proposed copula for building up more complex multivariate dependence models. Future research will focus on exploring this potential in modelling real multivariate datasets that have complex dependence structures.

Acknowledgements

The simulations presented in this paper were carried out on the High Performance Computing Cluster supported by the Research and Specialist Computing Support service at the University of East Anglia.

References

- Belzile et al., (2019) Belzile, L., Genest, C., McNeil, A. J., and Nešlehová, J. G. (2019). lcopula: Liouville Copulas. R package version 1.0.4. URL: http://CRAN.R-project.org/package=lcopula.

- Bock et al., (2004) Bock, R., Chilingarian, A., Gaug, M., Hakl, F., Hengstebeck, T., Jiřina, M., Klaschka, J., Kotrč, E., Savický, P., Towers, S., Vaiciulis, A., and Wittek, W. (2004). Methods for multidimensional event classification: a case study using images from a cherenkov gamma-ray telescope. Nuclear Instruments and Methods in Physics Research Section A: Accelerators, Spectrometers, Detectors and Associated Equipment, 516(2):511–528.

- Czado, (2019) Czado, C. (2019). Analyzing dependent data with vine copulas, volume 222 of Lecture Notes in Statistics. Springer.

- Dalla Valle et al., (2018) Dalla Valle, L., Leisen, F., and Rossini, L. (2018). Bayesian non-parametric conditional copula estimation of twin data. Journal of the Royal Statistical Society: Series C (Applied Statistics), 67(3):523–548.

- Dissmann et al., (2013) Dissmann, J., Brechmann, E., Czado, C., and Kurowicka, D. (2013). Selecting and estimating regular vine copulae and application to financial returns. Computational Statistics & Data Analysis, 59:52–69.

- Durrleman et al., (2000) Durrleman, V., Nikeghbali, A., and Roncalli, T. (2000). Which copula is the right one? Technical Report, Groupe de Researche Operationnelle Credit-Lyonnais.

- Genest et al., (1995) Genest, C., Ghoudi, K., and Rivest, L.-P. (1995). A semiparametric estimation procedure of dependence parameters in multivariate families of distributions. Biometrika, 82(3):543–552.

- Genest et al., (2012) Genest, C., Nešlehová, J., and Quessy, J.-F. (2012). Tests of symmetry for bivariate copulas. Annals of the Institute of Statistical Mathematics, 64(4):811–834.

- Genest et al., (2009) Genest, C., Rémillard, B., and Beaudoin, D. (2009). Goodness-of-fit tests for copulas: A review and a power study. Insurance: Mathematics & Economics, 44:199–213.

- Hua and Joe, (2011) Hua, L. and Joe, H. (2011). Tail order and intermediate tail dependence of multivariate copulas. Journal of Multivariate Analysis, 102(10):1454–1471.

- Huard et al., (2006) Huard, D., Évin, G., and Favre, A.-C. (2006). Bayesian copula selection. Computational Statistics & Data Analysis, 51(2):809–822.

- Joe, (1993) Joe, H. (1993). Parametric families of multivariate distributions with given margins. Journal of Multivariate Analysis, 46:262–282.

- Joe, (1997) Joe, H. (1997). Multivariate Models and Dependence Concepts. Chapman & Hall, London.

- Joe, (2005) Joe, H. (2005). Asymptotic efficiency of the two-stage estimation method for copula-based models. Journal of Multivariate Analysis, 94(2):401–419.

- Joe, (2014) Joe, H. (2014). Dependence Modeling with Copulas. Chapman & Hall, London.

- Joe et al., (2010) Joe, H., Li, H., and Nikoloulopoulos, A. K. (2010). Tail dependence functions and vine copulas. Journal of Multivariate Analysis, 101:252–270.

- Kadhem and Nikoloulopoulos, (2021) Kadhem, S. H. and Nikoloulopoulos, A. K. (2021). Factor copula models for mixed data. British Journal of Mathematical and Statistical Psychology. DOI: 10.1111/bmsp.12231.

- Krupskii and Joe, (2013) Krupskii, P. and Joe, H. (2013). Factor copula models for multivariate data. Journal of Multivariate Analysis, 120:85–101.

- McNeil and Nešlehová, (2010) McNeil, A. J. and Nešlehová, J. (2010). From Archimedean to Liouville copulas. Journal of Multivariate Analysis, 101(8):1772–1790.

- Nagler and Czado, (2016) Nagler, T. and Czado, C. (2016). Evading the curse of dimensionality in nonparametric density estimation with simplified vine copulas. Journal of Multivariate Analysis, 151:69–89.

- Narasimhan et al., (2018) Narasimhan, B., Koller, M., Johnson, S. G., Hahn, T., Bouvier, A., Kiêu, K., and Gaure, S. (2018). cubature: Adaptive multivariate integration over hypercubes. R package version 2.0.3. URL: http://CRAN.R-project.org/package=cubature.

- Nash, (1990) Nash, J. (1990). Compact Numerical Methods for Computers: Linear Algebra and Function Minimisation. Hilger, New York. 2nd edition.

- Nelsen, (2006) Nelsen, R. B. (2006). An Introduction to Copulas. Springer-Verlag, New York.

- Nikoloulopoulos, (2013) Nikoloulopoulos, A. K. (2013). Copula-based models for multivariate discrete response data. In Durante, F., Härdle, W., and Jaworski, P., editors, Copulae in Mathematical and Quantitative Finance, volume vol 213, pages 231–249, Berlin, Heidelberg. Springer.

- Nikoloulopoulos, (2015) Nikoloulopoulos, A. K. (2015). A mixed effect model for bivariate meta-analysis of diagnostic test accuracy studies using a copula representation of the random effects distribution. Statistics in Medicine, 34:3842–3865.

- Nikoloulopoulos and Joe, (2015) Nikoloulopoulos, A. K. and Joe, H. (2015). Factor copula models for item response data. Psychometrika, 80:126–150.

- Nikoloulopoulos et al., (2012) Nikoloulopoulos, A. K., Joe, H., and Li, H. (2012). Vine copulas with asymmetric tail dependence and applications to financial return data. Computational Statistics & Data Analysis, 56:659–3673.

- Nikoloulopoulos and Karlis, (2008) Nikoloulopoulos, A. K. and Karlis, D. (2008). Copula model evaluation based on parametric bootstrap. Computational Statistics & Data Analysis, 52:3342–3353.

- Nikoloulopoulos and Karlis, (2009) Nikoloulopoulos, A. K. and Karlis, D. (2009). Finite normal mixture copulas for multivariate discrete data modeling. Journal of Statistical Planning and Inference, 139:3878–3890.

- Nikoloulopoulos and Karlis, (2010) Nikoloulopoulos, A. K. and Karlis, D. (2010). Regression in a copula model for bivariate count data. Journal of Applied Statistics, 37:1555–1568.

- Panagiotelis et al., (2012) Panagiotelis, A., Czado, C., and Joe, H. (2012). Pair copula constructions for multivariate discrete data. Journal of the American Statistical Association, 107:1063–1072.

- Sklar, (1959) Sklar, M. (1959). Fonctions de répartition à dimensions et leurs marges. Publications de l’Institut de Statistique de l’Université de Paris, 8:229–231.

- Stroud and Secrest, (1966) Stroud, A. H. and Secrest, D. (1966). Gaussian Quadrature Formulas. Prentice-Hall, Englewood Cliffs, NJ.

- Wu et al., (2015) Wu, J., Wang, X., and Walker, S. G. (2015). Bayesian nonparametric estimation of a copula. Journal of Statistical Computation and Simulation, 85(1):103–116.