*\mathcal

An Efficient -BIC to BIC Transformation and Its Application to Black-Box Reduction in Revenue Maximization

Abstract

We consider the black-box reduction from multi-dimensional revenue maximization to virtual welfare maximization. Cai et al. [12, 13, 14, 15] show a polynomial-time approximation-preserving reduction, however, the mechanism produced by their reduction is only approximately Bayesian incentive compatible (-BIC). We provide two new polynomial time transformations that convert any -BIC mechanism to an exactly BIC mechanism with only a negligible revenue loss.

-

•

Our first transformation applies to any mechanism design setting with downward-closed outcome space and only requires sample access to the agents’ type distributions.

-

•

Our second transformation applies to the fully general outcome space, removing the downward-closed assumption, but requires full access to the agents’ type distributions.

Both transformations only require query access to the original -BIC mechanism. Other -BIC to BIC transformations for revenue exist in the literature [23, 38, 18] but all require exponential time to run in both of the settings we consider. As an application of our transformations, we improve the reduction by Cai et al. [12, 13, 14, 15] to generate an exactly BIC mechanism.

1 Introduction

Mechanism design is the study of optimization algorithms with the additional constraint of incentive compatibility. A central theme of algorithmic mechanism design is thus to understand how much this extra constraint hinders our ability to optimize a certain objective efficiently. In the best scenario, one may hope to establish an equivalence between a mechanism design problem and an algorithm design problem, manifested via a black-box reduction that converts any algorithm to an incentive compatible mechanism. In this paper, we study the black-box reduction of a central problem in mechanism design: multi-dimensional revenue maximization.

The problem description is simple: an auctioneer is selling a collection of items to one or more strategic bidders. We follow the standard Bayesian assumption, that is, each bidder’s type is drawn independently from a distribution known to all other bidders and the auctioneer. The auctioneer’s goal is to design a Bayesian incentive compatible (BIC) mechanism that maximizes the expected revenue.

In the special case of single-item auction, Myerson provides an elegant characterization of the optimal mechanism. Indeed, Myerson’s solution can be viewed as a black-box reduction from revenue maximization to the algorithmic problem of (virtual) welfare maximization [34]. However, whether the black-box reduction can be extended to multi-dimensional settings remained open after Myerson’s result. Recently, a line of work by Cai et al. [12, 13, 14, 15] showed that there is a polynomial-time approximation-preserving black-box reduction from multi-dimensional revenue maximization to the algorithmic question of (virtual) welfare optimization. However, this result still has the following two caveats: (i) the revenue of the mechanism is only guaranteed to be within an additive of the optimum; and (ii) the mechanism is only approximately Bayesian incentive compatible. Thus, an immediate open problem following their result is whether these two compromises are inevitable. In this paper, we show that approximately Bayesian incentive compatibility is unnecessary through our first main result:

-

Result I:

There is a polynomial-time approximation-preserving black-box reduction from multi-dimensional revenue maximization to the algorithmic question of (virtual) welfare optimization that generates an exactly Bayesian incentive compatible mechanism.

Result I is enabled by a new polynomial time -BIC to BIC transformation for revenue, which is our second main result:

-

Result II:

There is a polynomial-time -BIC to BIC transformation that converts any approximately Bayesian incentive compatible mechanism to an exactly Bayesian incentive compatible mechanism with a negligible revenue loss for any downward-closed environment with only sample access to the agents’ type distributions.

The transformation is applicable to any downward-closed mechanism design setting.222Roughly speaking, the setting is downward-closed if the agents have the choice to not participate in the mechanism. See Section 2 for the formal definition. We believe the transformation is of independent interest and would have numerous applications in mechanism design. Indeed, our black-box reduction follows straightforwardly from applying the transformation to the mechanism of Cai et al. [12, 13, 14, 15]. Furthermore, if we are given full access to the type distributions of the buyers, we can extend our transformation to the fully general outcome space, removing the downward-closedness assumption. Here is our third main result:

-

Result III:

There exists a polynomial-time -BIC to BIC transformation with oracle access to any approximately Bayesian incentive compatible mechanism and full access to the agents’ distributions, outputs an exactly Bayesian incentive compatible mechanism for any general outcome space with a negligible revenue loss.

Note that other -BIC to BIC transformations for revenue have been proposed in the literature [23, 38, 18], however, all of the existing transformations require solving a -hard problem repeatedly [28] and therefore cannot be made computationally efficient.

1.1 Our Results and Techniques

We first fix some notations to facilitate our discussion of the results. We consider a general mechanism design environment where there is a set of feasible outcomes denoted by .There are agents, and each agent has a type drawn from distribution independently. We use to denote the support of , and for every , is a valuation function that maps every outcome to a real number in [0,1]. A mechanism consists of an allocation rule and a payment rule . We slightly abuse notation to define . If we have query access to , then on any query bid profile , we receive an outcome and payments .

The outcome space is called downward-closed if each can be written as a vector where is the outcome for agent . And for every , any with or for every is also in . Here is a null outcome available to each agent , which represents the option of not participating in the mechanism.

Equiped with the notations, we are ready to discuss our -BIC to BIC transformations.

Informal Theorem 1 (-BIC to BIC transformation on downward-closed outcome space).

Given sample access to a collection of distributions on a downward-closed outcome space, and query access to an -BIC and individually rational (IR) mechanism with respect to . We can construct another mechanism that is exactly BIC and IR with respect to , and its revenue is at most worse than the revenue of . Moreover, for any bid profile , computes an outcome and payments in expected running time and makes in expectation at most queries to .

Informal Theorem 2 (-BIC to BIC transformation on general outcome space).

Given full access to the collection of distributions on a general outcome space such that for every , and query access to an -BIC and individually rational (IR) mechanism with respect to . We can construct a mechanism that is exactly BIC and IR with respect to . Moreover its revenue is within an additive of the revenue of . Furthermore, the running time of the constructed mechanism is and the mechanism makes at most queries to .

Previous transformations can produce an with similar guarantees in the downward-closed setting but require time to run [23, 38, 18]. In the special case, where there exists symmetry in the agents’ type distributions, the transformation can be improved to run in time , as the interim allocation probabilities and payments of the mechanism can be computed efficiently via a polynomial-size LP.333If the interim allocation probabilities and payments of are given, the edge weights in the Replica-Surrogate matching can be computed efficiently. See the next paragraph for more details. Our result achieves the running time without the symmetry assumption.

1.1.1 Our Result for the Downward-Closed Outcome Space

We first discuss our result for the downward-closed outcome space. To illustrate our new ideas, we first briefly review the constructions in the literature. In the heart of all the previous constructions lies the problem called replica-surrogate matching.

Replica-Surrogate Matching

For each agent , form a bipartite graph . The left hand side nodes are called replicas, which are types sampled i.i.d. from . In particular, the true type of agent is one of the replicas. On the right hand side, the nodes are called surrogates, which are also types sampled from . The edge between a replica with type and a surrogate with type is assigned weight 444The true weight is computed using a discounted price, but we can ignore the difference for now., which is the interim utility of agent when her true type is but reports to . Compute the maximum weight matching on . The true type selects a surrogate using the matching to compete in . Agent competes in using the type of the surrogate she is matched to in the maximum weight matching.

The intuition is that since is not BIC, the true type may prefer the outcome and payment from reporting some different type. The matching is set up to allow the true type to pick a more favorable type to compete in for it. But why wouldn’t the agent misreport in the matching? After all, the edge weights depend on the agent’s report. As it turns out, to guarantee incentive compatibility, one needs to find a matching with a maximal-in-range algorithm. Namely, the matched surrogate is selected to maximize the agent’s induced utility less some cost that only depends on the outcome. It is not hard to verify that the maximum weight matching is indeed maximal-in-range, and therefore the agent has no incentive to lie.

But why does the maximum weight matching take exponential time to find? The problem is that we are not given the edge weights. For each edge, we can only sample from a distribution whose mean is the weight of the edge: Sample from and compute . Even if we assume that we know the distributions , it still takes time to compute the weight of a single edge exactly, which is already an exponential on . But why can’t we first estimate the edge weights with samples and find the maximum matching using the estimated weights? The issue is that no matter how many samples we take, the empirical mean will be off by some estimation error. The maximal-in-range property is so fragile that even a tiny bit of estimation error can cause the algorithm to violate the property, making the whole mechanism not incentive compatible. See Example 2 below for a more detailed explanation.

Black-box Reduction for Welfare Maximization

To overcome the difficulty, we turn to another important problem in mechanism design, black-box reduction for welfare maximization, for inspiration. A line of beautiful results [29, 8, 28, 24] initiated by Hartline and Lucier shows that the mechanism design problem of welfare maximization in the Bayesian setting can be black-box reduced to the algorithmic problem of welfare maximization. The replica-surrogate matching is again the central piece in the reduction. Indeed, the idea of replica-surrogate matching was first proposed by Hartline et al. [27, 28], and later introduced by Daskalakis and Weinberg [23] to the study of -BIC to BIC transformation for revenue. The main difference of the two scenarios is the way the edge weights are defined. For welfare maximization, the edge weight between a replica and a surrogate is , namely, the interim value for agent when her true type is but reports to . We will refer to the one with interim utilities as edge weights the U-replica-surrogate matching and the one with interim values as edge weights the V-replica-surrogate matching. The main reason that we would like to distinguish the two settings is as follows: in a V-replica-surrogate matching all edge weights are nonnegative, while in a U-replica-surrogate matching the edge weights may be negative. The importance of the presence of negative edges will become clear soon. Obviously, it also takes exponential time to compute the exact maximum weight V-replica-surrogate matching due to the same reason discussed above.

A result by Dughmi et al. [24] shows how to circumvent this barrier for welfare maximization. Their solution has the following two main components: (i) a polynomial time maximal-in-range algorithm to solve the maximum entropy regularized perfect matching problem; (ii) the fast exponential Bernoulli race, a new Bernoulli factory 555A Bernoulli factory is an algorithm that with sample access to a -coin to simulate a -coin. In Section 2.1 we give a brief introduction to Bernoulli factories. We also refer the readers to [30, 35] and the references therein for more details., that allows them to execute the algorithm in (i) exactly with only sample access to distributions whose means are the edge weights. They use the algorithm to find a maximum entropy regularized V-replica-surrogate matching, and argue that this matching has approximately maximum weight, which allows them to conclude that their new mechanism loses at most a negligible fraction of the welfare.

Why is the mechanism by Dughmi et al. [24] unsuitable?

The reason turns out to be subtle. As the U-replica-surrogate matching contains negative edges and the algorithm by Dughmi et al. [24] always returns a perfect matching, some agent types may receive negative utilities from the matching. To guarantee individually rationality, the mechanism must compensate these types. However, due the incentive compatibility constraint, the mechanism must also compensate other agent types. One might think that the overall compensation can be shown to be negligible. Unfortunately, in the following example, we show that the overall compensation can in fact dramatically damage the revenue and may even drive the revenue to .

Example 1.

Consider the following instance with a single agent and outcome space . The agent has two possible types and with probability and respectively, where is sufficiently small. The agent’s valuation is: , . The given mechanism chooses outcome and charges if the agent reports , and chooses outcome and gives the agent if the agent reports . Clearly, is -BIC and IR. . Note that in the U-Replica-Surrogate matching, the edge between replica with type L and surrogate with type H has negative weight .

Denote the number of surrogates sampled from the above distribution. Let be the constructed mechanism that always selects a perfect replica-surrogate matching. Denote the payment function of . Then since is IR. Consider the following two scenarios when the agent has true type . In the first scenario she reports truthfully her type and in the second scenario she reports . With probability , none of the surrogates has type . In both scenarios the buyer must be matched to a surrogate with type in the perfect replica-surrogate matching and has value 1 for the result outcome . Thus the difference of the agent’s expected value between the two scenarios is at most . Since is BIC, we must have . Therefore . For any fixed and , when , the and revenue loss goes to 1. Note that our mechanism guarantees revenue loss at most for any type distribution, where is an absolute constant.

Let us take a closer look at what happens in the example above. With high probability, the agent with low type is matched to a surrogate with high type in the perfect matching and has negative utility. Thus to satisfy individual rationality, the mechanism has to compensate her. To guarantee incentive compatibility, the mechanism will also have to compensate the agent when her true type is . However, the total compensation is so large that it essentially drives the revenue of the constructed mechanism to . Our main challenge is to enforce both individually rationality and incentive compatibility in the presence of negative edges without sacrificing much of the revenue.

As Example 1 implies, to preserve revenue, it is crucial to avoid matching a replica with a negative weight edge with high probability in the U-replica-surrogate matching. Again the exact weight can not be computed efficiently. One may try to remove the negative edges using samples. However, removing edges based on the empirical means from samples could easily violate the maximal-in-range property. See Example 2.

Example 2.

Let be the number of samples that the algorithm uses to calculate the empirical expectation. Choose such that . Consider the following example with 1 node on each side. There are two instances. For the first instance, the random variable attached to this edge is w.p. , and with probability . The edge weight . For the second instance, is w.p. 1 and .

For the above example, both instances have the same edge weight and any maximal-in-range allocation will always output the same matching. However in the first instance, with probability the empirical expectation is negative and the two nodes are not matched. While in the second instance the algorithm will always match the two nodes. Thus the output matching is not maximal-in-range. It is well-known that if the allocation is maximal-in-range, there must exist a payment rule such that the agent is incentive-compatible. Thus the algorithm will violate the incentive-compatibility when applied to the replica-surrogate matching.

Our Solution for the Downward-Closed Outcome Space.

Our transformation on downward-closed environments is directly inspired by [24] but differs in several major ways. Our plan is to design an algorithm, for general graphs with arbitrary weights, that satisfies the following two properties:

-

1.

The algorithm produces a distribution of matchings whose expected weight is close to the maximum weight matching.

-

2.

For any LHS node, the expected weight of the edge matched to it is not too negative.

Note that for graphs with positive weights, the algorithm by Dughmi et al. [24] satisfies both properties. When the edges are negative, the first property is not satisfied by their algorithm in general. Even if we only consider U-replica-surrogate matching, their algorithm still violates the second property. Interestingly, we provide a reduction from the case of arbitrary edge weights to the case with only positive edge weights. Indeed, our reduction can be succinctly summarized by the following formula, if an edge has weight , set the new weight by applying the -softplus function to 666The function is known as the soft plus function.: , where is a parameter of our algorithm. Note that for any value of , is always nonnegative! Moreover, the maximum entropy regularized matching on weights can be shown to be close to the maximum weight matching on , and the second property also holds due to nice features of the algorithm and the softplus function. So it seems that we only need to run the algorithm from [24] on the new weights . An astute reader may have already realized that being able to run the algorithm on does not imply that one can run the algorithm on , as we can only sample from distributions whose means are but not . One idea is to construct a Bernoulli factory to simulate a -coin using a -coin. To the best of our knowledge, no such construction exists. We take a different approach and make use of a crucial property of the algorithm from [24]. Namely, if we run their algorithm with the same parameter , the algorithm only needs to sample from the softmax function over the weights. More specifically, with weights , it suffices to have the ability to sample an edge with probability exactly . Despite the fact that we cannot directly sample from distributions with means , we can indeed sample edge with exactly the right probability, as

which can be sampled efficiently using the fast exponential Bernoulli race given only sample access to distributions with means equal to the original edge weights .

Our second contribution is to show that an approximately maximum U-replica-surrogate matching suffices to guarantee only a small loss in revenue. Previous results [23, 38, 18] only prove the statement for the exactly maximum matching. We provide a more delicate analysis that allows us to extend the statement to approximately maximum matchings. Finally, as the agent may receive negative utility from certain surrogates, we sometimes need to subsidize the agent to ensure individual rationality. Due to the second property of our algorithm, we can argue that the total subsidy is small compared to the revenue. We emphasize that the U-replica-surrogate matching found in our mechanism may not be perfect. Thus the assumption being downward-closed is necessary, in order to allow the agent whose true type is unmatched in the matching to receive a outcome. See Mechanism 3 in Section 5 for more details.

1.1.2 Our Result for the General Outcome Space

Our result for the general outcome space is based on the regularized replica-surrogate fractional assignment mechanism by Hartline et al. [28]. They use this mechanism to provide a black-box reduction for welfare maximization, but this mechanism only applies to discrete type space and requires full access to all agents’ type distributions. We refer the readers to Section 7.1 for details of their mechanism.

The main barrier for applying their approach to transform an -BIC mechanism to a BIC mechanism is that their mechanism does not provide any guarantees on the revenue. More specifically, the prices of their mechanism are determined by a set of optimal dual variables of their problem. Although any set of optimal dual variables can guarantee the mechanism to be incentive compatible and individually rational, which is sufficient for welfare maximization, some choices could result in substantial revenue loss, making them unsuitable to preserve revenue. In fact, Example 4 illustrates that for some optimal dual variables, the revenue loss due to negative prices can be very high. Our main contribution is to show an efficient algorithm to find a set of optimal dual variables such that the induced prices only cause negligible loss in the revenue.

1.2 Application to Multi-dimensional Revenue Maximization

We next apply the -BIC to BIC transformation to obtain our black-box reduction for revenue maximization. We first introduce the problem formally.

Multi-Dimensional Revenue Maximization (MRM): Given as input type distributions and a set of feasible outcomes , output a BIC and IR mechanism who chooses outcomes from with probability and whose expected revenue is optimal relative to any other, possibly randomized, BIC, and IR mechanism with respect to .

To state our black-box reduction, we introduce the virtual welfare optimization problem.

Virtual Welfare Optimization (VWO) [15]: Given as input functions and a set of feasible outcomes , output an outcome . is considered as the weight function that depends on the agent’s real type. We refer to the sum as agent ’s virtual value for outcome .

Informal Theorem 3.

When the outcome space is downward-closed, given sample access to distribution and oracle access to an -approximation Algorithm for VWO, we can construct an exactly BIC and IR mechanism with respect to , that has expected revenue , where is the optimal revenue over all BIC and IR mechanisms with respect to . The running time is , where is the running time of , and is an upper bound on the bit complexity of for any agent , any type , and any outcome .

Note that a similar result holds for a general outcome space, given that we have full access to distribution . The modified running time and revenue loss can be found in Section 7.

1.3 Further Related Work

Multi-dimensional revenue maximization has recently received lots of attention from computer scientists. Significant progress has been on the computational front [19, 20, 1, 11, 2, 12, 13, 17, 15, 3, 9, 22, 31]. On the structural front, a family of simple mechanisms, i.e., variants of sequential posted price and two-part tariff mechanisms, have been shown to achieve constant factor approximations of the optimal revenue in quite general settings [5, 39, 38, 16, 21, 18]. -BIC to BIC transformation for revenue has been an instrumental tool in obtaining both the computational and structural results [23, 38, 18, 31].

There has also been significant interest in understanding the sample complexity for learning an almost revenue-optimal auction in multi-item settings. Last year, Gonczarowski and Weinberg [26] show that one can learn an almost revenue-optimal -BIC mechanism using samples under the item-independence assumption, where is the number of bidders and is the number of items. Brustle et al. [10] generalize the result to settings where the item values are drawn from correlated but structured distributions that can be modeled by either Markov random fields or Bayesian Networks. The mechanism they produce is still -BIC. Our transformation can certainly convert these mechanisms from [26, 10] into exactly BIC mechanisms, and the transformation requires many samples. Unfortunately, each is already exponential in in their settings. The dependence on is unavoidable for us, as our goal is to provide a transformation that is applicable to a general mechanism design setting. Nonetheless, the techniques we develop in this paper may be combined with special structure of the distribution to provide more sample-efficient -BIC to BIC transformations.

Recently, Gergatsouli et al. [25] proved that for the case where we have a single buyer with an additive valuation over independent items and the set of outcomes is downward-closed, an exponential (in ) query complexity is necessary for any black-box reduction for welfare maximization. It will certainly be interesting to see whether a similar lower bound on the sample complexity exists.

1.4 Organization of the Paper

In Section 2, we provide the notations we use throughout the paper. In Section 3, we mention the tools from the literature that are important for our constructions. In Section 4, we provide our new algorithm that solves the entropy regularized matching problem for graphs with arbitrary edge weights assuming the outcome space is downward-closed. In particular, we show the arbitrary edge weight case can be reduced to the nonnegative edge weight case. In Section 5, we describe our -BIC to BIC transformation when the outcome space is downward-closed. In Section 6, we show how to use our -BIC to BIC transformation to improve the black-box reduction for multi-dimensional revenue maximization. In Section 7 we state our result for the general outcome space. Note that in Sections 4 through 6 we focus on downward-closed outcome spaces, whereas in Section 7 we shift our attention to general outcome spaces.

2 Preliminaries

We specify a general mechanism design setting by the tuple . There are agents participating in the mechanism. Denote the set of all possible outcomes. We consider two types of outcome space.

-

1.

Downward-Closed Outcome Space: Each can be written as a vector where is the outcome for agent . We also assume that a null outcome is available to each agent . One can think of as the option of not participating in the mechanism. Throughout the paper, when we say the outcome space is downward-closed, then for every , any with or for every is also in . An example of the downward-closed outcome space is the combinatorial auction, where the outcome set contains all possible ways to allocate items to agents, and the null outcome represents allocating nothing to the agent. One setting that does not have a downward-closed outcome space is building a public project.

-

2.

General Outcome Space: is an arbitrary set. This is the most general outcome space, and it can capture settings such as building a public project.

Each agent has a type from type space , which is drawn independently from some distribution . We use to denote the support of . We use to denote . In the paper we consider discrete type spaces, we assume that every for some finite . Note that our results for the downward-closed outcome space can easily be extended to the continuous case using similar techniques as in [24], while our results for general outcome space requires the type space to be discrete. For every , is a valuation function that maps every outcome to a real number in . In a downward-closed outcome space, for all agent and type , if . Every agent is risk-neutral and has quasi-linear utility.

For any mechanism , denote the expected revenue of . We use for short when the agents’ distributions and valuation functions are clear. We use the standard definitions of BIC, -BIC, IR, and -IR:

Bayesian Incentive Compatible (BIC):

Individual Rational (IR):

-BIC:

-IR:

Coupling between Type Distributions:

In order to measure the difference between the two distributions, we will introduce the following definition. Fix every agent . A coupling of distribution and is a joint distribution on the probability space such that the marginal of coincide with and . In the paper we slightly abuse the notation, denoting a random variable that is distributed according to the conditional distribution of type over when . According to the definition of the coupling, when , .

We say is non-increasing w.r.t. the coupling if for all , outcome , and every realized type , . Intuitively, the coupling always maps a “higher” type to a “lower” type. Such coupling is common, for example in a combinatorial auction, rounding agent ’s value for each bundle of items down to the closest multiples of can be viewed as such a coupling.

Wasserstein Distance:

For any , let . The -Wasserstein Distance between distribution and w.r.t. is defined as the smallest expected distance among all couplings. Formally,

Finally, we use to denote the natural logarithm and to denote the set of all distributions over elements.

Definition 1 (Gibbs Distribution).

For any integer , define the Gibbs distribution over states with temperature as for all , where is the energy of element .

Definition 2 (Maximal-in-Range Algorithms).

An algorithm is maximal-in-range, if for every , there exists a cost function , which may depend on , such that the allocation for any , where is a set of all feasible allocations.

2.1 A Brief Introduction to Bernoulli Factories

Suppose we are given a coin with bias , can we construct another coin with bias using the original coin? If the answer is yes, then how many flips do we need from the original coin to simulate the new coin? A framework that tackles this problem is called Bernoulli Factories. We refer the reader to [33] for a survey on this topic.

Definition 3 (Keane and O’Brien [30]).

Given some function and black-box access to independent samples of a Bernoulli random variable with bias , the Bernoulli factory problem is to generate a sample from a Bernoulli distribution with bias .

A useful generalization of the previous model is the following777The model is called Expectations from Samples in [24].: given sample access to distributions with expectations , and a function , where is a set of feasible outcomes and is a set of probability distributions over these outcomes, how can we want generate a sample from ?

Below we state an important result from [24], which we use in this paper. It proposes an algorithm called Fast Exponential Bernoulli Race with . For every , it produce a sample from the Gibbs distribution with temperature and energy for each outcome , given only sample access to distributions .

Theorem 1.

[24] Given any parameter and sample access to distributions with expectations , there exists an algorithm that can sample from a Gibbs distribution in , where

using samples in expectation.

The fast exponential Bernoulli race [24] is a randomized algorithm that allows us to sample from the Gibbs distribution. We use the following result in the rest of our paper.

Lemma 1.

[Fast Exponential Bernoulli Race] For any integer , any , and any , given sample access to distributions with expectations , a sample from the following Gibbs distribution in :

can be drawn with samples from in expectation.

3 Tools from the Literature

3.1 Replica-Surrogate Matching

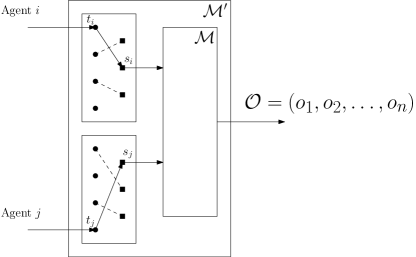

Now we provide a detailed description of the replica-surrogate matching mechanism used in [23, 38, 18]. For each agent , the mechanism generates a number of replicas and surrogates from , and maps the agent’s type to one of the surrogates via a maximum weight replica-surrogate matching, and charges the agent the corresponding VCG payment. Then let the matched surrogate participate in the mechanism for the agent. Formally, suppose we are given query access to a mechanism , we construct a new mechanism using the following two-phase procedure:

Phase 1: Surrogate Selection

For each agent ,

-

1.

Given her reported type , create replicas sampled i.i.d. from and surrogates sampled i.i.d. from . The value of is specified in Lemma 3.

-

2.

Construct a weighted bipartite graph between replicas (and agent ’s true type ) and surrogates. The weight between the -th replica and the -th surrogate is the interim value of agent when her true type is but reported to less the interim payment for reporting multiplied by :

(1) -

3.

Treat as the value of replica for being matched to surrogate . Run the VCG mechanism among the replicas, that is, compute the maximum weight matching w.r.t. edge weight and the corresponding VCG payments. If a replica (or type ) is unmatched in the maximum matching, match it to a random unmatched surrogate.

Phase 2: Surrogate Competition

Let be the surrogate matched with the agent ’s true type . Run mechanism under input . Let be a the outcome generated by . If agent is matched in the maximum matching, her outcome is and her expected payment is plus the VCG payment for winning surrogate in the first phase; Otherwise the agent gets the null outcome and pays .

In Figure 1 we illustrate the replica-surrogate scheme.

Proof.

We prove this in two parts, similarly to [18]. First we argue that the distribution of the surrogate that represents the agent, when the agent reports truthfully, is . Since we have a perfect matching, an equivalent way of thinking about the process is to draw replicas, produce the perfect matching (the VCG matching plus the uniform matching between the unmatched replicas and surrogates) and then pick one replica uniformly at random to be the agent. These two processes produce the same joint distribution between replicas, surrogates and the agents . So we can just argue about the second process of sampling. Since the agent is chosen uniformly at random between the replicas in the second process, the surrogate that represents the agent, will also be chosen uniformly at random between all the surrogates. Thus, the distribution of is .

We need to argue that for every agent reporting truthfully is a best response, if every other agent is truthful. In the VCG mechanism, agent faces a competition with the replicas to win a surrogate. If agent has type , then her value for winning a surrogate with type in the VCG mechanism is exactly the edge weight

Clearly, if agent reports truthfully, the weights on all incident edges between her and all the surrogates will be exactly her value for winning those surrogates. Since agent is in a VCG mechanism to compete for a surrogate, reporting the true edge weights is a dominant strategy for her, therefore reporting truthfully is also a best response for her assuming the other agents are truthful. It is critical that the other agents are reporting truthfully, otherwise agent ’s value for winning a surrogate with type may be different from the weight on the corresponding edge.

∎

Moreover, when is sufficiently large, the revenue of is close to the revenue of .

3.2 Online Entropy Regularized Matching

Now we describe the online entropy regularized matching algorithm developed by Dughmi et al. [24]. The original application is to find approximately maximum replica-surrogate matching in welfare maximization, but the algorithm is general and can be applied to any -to- bipartite matching with positive edge weights.

-to- Matching

For every integer , , consider the complete bipartite graph between left hand side nodes (called LHS-nodes) and right hand side nodes (called RHS-nodes). Let be the edge weight between LHS-node and RHS-node for . For ease of notation, let , , and . A matching is called a -to- matching if every LHS-node is matched to at most one RHS-node, and every RHS-node is matched to at most LHS-nodes. A -to- matching is called perfect if every LHS-node is matched to one RHS-node, and every RHS-node is matched to exactly LHS-nodes.

In this section, we focus on the case where all edge weights are nonnegative, and we refer to this case as the nonnegative weight -to- matching. In Section 4, we generalize the results to arbitrary weights.

The optimal -to- matching is simply a maximum weight bipartite matching problem. The challenge is that the weights are not given. For every edge , we only have sample access to a distribution whose expectation is . To the best of our knowledge, none of the algorithms for finding a maximum weight bipartite matching can be implemented exactly with such sample access to the edge weights. Moreover, as we require the replica-surrogate matching mechanism to be incentive compatible, the algorithm should be maximal-in-range. Therefore, finding the maximum weight matching using the empirical means is also not an option, as it violates the maximal-in-range property (see the discussion in Section 1.1).

Dughmi et al. [24] provide a polynomial time maximal-in-range algorithm (Algorithm 1) to compute an approximately maximum weight perfect -to- matching. The key idea is to find a “soft maximum weight matching” instead of the maximum weight matching by adding an entropy function as a regularizer to the total weight. We summarize the guarantees of Algorithm 1 in Theorem 2. We refer the readers to [24] for intuition behind Algorithm 1. However, to understand this paper, readers can simply treat Theorem 2 as a black box that guarantees that Algorithm 1 is maximal-in-range, and finds approximately maximum expected weight -to-1 matching, with only sample access to the distributions.

Definition 4.

Given parameter , the (offline) entropy regularized matching program (P) is:

| (2) |

Lagrangify the constraints . The Lagrangian dual of is:

The following lemma follows from the first-order condition: for any dual variables , the optimal solution for the Lagrangian is given by a collection of Gibbs distribution .

Lemma 4.

[24] For every dual variables , the optimal solution maximizing the Lagrangian subject to constraints is: .

If the optimal dual variables are known, by complementary slackness, the corresponding in Lemma 4 is the optimal solution of . The gap between the expected weight of and the maximum weight is at most the value of the maximum entropy , so we can simply use the matching sampled according to the distribution . However, as the optimal dual is unknown, the wrong dual variables may cause a loss of , which may be too large when is not computed based on the optimal dual variables. To resolve this difficulty, Dughmi et al. [24] introduce the second key idea – Online Entropy Regularized Matching algorithm (Algorithm 1). The online algorithm gradually learns a set of dual variables close to the optimum . When the algorithm terminates, it is guaranteed to find a close to optimal solution to program . From Lemma 5, the algorithm is also maximal-in-range for any choice of the parameters .

Lemma 5.

[24] For every , and parameter , the Gibbs distribution (specified in step 4) is maximal-in-range, as

Theorem 2.

[24] When 999The theorem applies to any bounded edge weights . For simplicity we normalize the edge weights to lie between . for all , Algorithm 1 satisfies the following properties:

-

1.

For any choice of the parameters, it always returns a perfect -to-1 matching.

-

2.

For any choice of the parameters, the algorithm is maximal-in-range. The expected running time and sample complexity of Algorithm 1 is .

-

3.

For every , if and , where is the optimum of program , the expected value (over the randomness of the Algorithm 1) of is at least .

Moreover, for every , if we set , and and satisfy the conditions above, then the expected total weight of the matching output by the algorithm is at most less than the maximum weight matching.

The only part of Algorithm 1 does not specified is how to choose a that is a constant factor approximation to . Dughmi et al. [24] show a polynomial time randomized algorithm that produces a that falls into with high probability, which suffices to find a close to optimum V-replica-surrogate matching. Please see Appendix A for details.

4 -to- Matching with Arbitrary Edge Weights

To obtain an approximately revenue-preserving -BIC to BIC transformation, we need to find a near-optimal U-surrogate-replica matching, where edge weights may be negative. Motivated by this application, we provide a generalization of Theorem 2 to general -to- matchings with arbitrary edge weights. We design a new algorithm (Algorithm 2) with guarantees summarized in Theorem 3.

In Example 1 we point out the issue of directly applying Algorithm 1 to the general -to- matching problem. A tempting way to fix the issue may be to first remove all edges with negative weights then run Algorithm 1. With only sample access to , one way to achieve this is to remove edges with negative empirical means. In fact, with a sufficiently large number of samples, with high probability, all edges with strictly positive weights will remain and all edges with strictly negative weights will be removed. However, with non-zero probability, some edges will either be kept or removed incorrectly causing the algorithm to violate the maximal-in-range property. See Example 2 for a concrete construction.

An alternative way is to relax the constraint to , so the algorithm no longer needs to find a perfect matching. However, Lemma 4 fails to hold as the optimal solution is no longer a Gibbs distribution and it is unclear how to sample efficiently from it with only sample access to .101010The issue is that may be strictly less than and has a complex expression. It is not clear whether we can sample efficiently from with only sample access to . Moreover, even if we can sample from the distribution, the guarantees in Theorem 2 may no longer hold. A similar attempt is to add a slack variable to , modifying the constraint to . It is equivalent to adding one dummy RHS-node, with weight on every incident edge. Now for every dual variable, the optimal solution for the Lagrangian follows from a Gibbs distribution. However, the program differs from , in particular the new dummy RHS-node has no capacity constraint, and as a result there is no dual variable that corresponds to this dummy node. It is not clear how to modify Algorithm 1 to accommodate the new dummy node and to produce a close to maximum matching.

4.1 Reduction from Arbitrary Weights to Non-Negative Weights

In this section, we provide a reduction from the -to- matching with arbitrary edge weight case to the non-negative edge weight case.

Definition 5.

For arbitrary edge weights and parameter , define the -softplus function:

Consider the entropy regularized matching program w.r.t. weights :

| (3) |

Note that for any , so the program is exactly a -to- matching with positive edge weights. We prove that the optimum of is close to the weight of the maximum weight -to- matching (See Lemma 6 and the proof of Theorem 3).

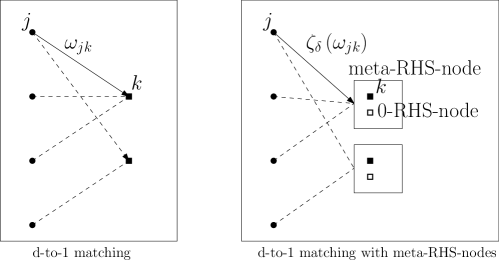

Thus in the rest of this section we will consider approximating the optimum of . Let be the solution produced by Algorithm 1 on . Program is the same as if we substitute the weight for each LHS-node and RHS-node with . Recall that our main goal is to avoid being matched with negative edges too often. Now for every RHS-node, we construct a dummy -RHS-node with weight 0 for all edges incident to it. Let the meta-RHS-node consists of the real RHS-node and the corresponding -RHS-node. The weight between the LHS-node and the meta-RHS-node is defined as . We will explain later why the weights are chosen in this way.

Think of the procedure that first executes Algorithm 1 to find a matching between LHS-nodes and meta-RHS-nodes. As a second step, when a LHS-node is matched to some meta-RHS-node , we further decide how to match it to the real RHS-node or the 0-RHS-node, according to the following “softmax” program between weight and (see Figure 2 for an illustration):111111Note that it’s also the entropy regularized matching program between a single LHS-node and two RHS-nodes (real RHS-node and 0-RHS-node ).

| (4) |

Let be the optimal solution. One can easily verify that the optimum of the softmax program is equal to . The two-step procedure finds a -to- matching in the original graph (by removing all edges matched to -RHS-nodes). Moreover, when the LHS-node is matched to the meta-RHS-node , its expected weight is at most less than . Thus by Theorem 2, the two-step procedure that executes Algorithm 1 w.r.t. indeed finds an approximately-optimal -to- matching w.r.t. weights and no LHS-node is matched to an edge with too negative weight.

The main issue with the above two-step procedure is that, to execute Algorithm 1 w.r.t. , we will have to sample from a distribution with mean with only sample access to the distribution whose mean is . To the best of our knowledge, no algorithm exists to sample exactly from such a distribution.

We present our algorithm (Algorithm 2) that solves this issue. The key conceptual idea is to merge the two steps into one. It directly matches LHS-nodes to either real RHS-nodes or 0-RHS-nodes. The reason that this is possible is because the distribution from the combined procedure is again a Gibbs distribution, which allows us to use the fast exponential Bernoulli race to sample directly from it (Observation 2).

We prove a coupling between executing Algorithm 2 over weights and executing Algorithm 1 over weights , with the same parameters . Note that both executions are online procedures. Thus the distribution of matching the current LHS-node depends on the previous matching. We carefully prove that the dual variables and the remaining capacities are the same for every round . Our result is summarized in Theorem 3.

Theorem 3.

When 121212Again the theorem applies to any bounded edge weights in . For simplicity we normalize the edge weights to lie in . for all , Algorithm 2 satisfies the following properties:

-

1.

For any choice of the parameters, dropping all the edges incident to any -RHS-nodes in the matching, the algorithm produces a feasible -to- matching (not necessarily perfect).

-

2.

For any choice of the parameters, the algorithm is maximal-in-range. The expected running time and sample complexity is .

-

3.

For every , if and , where is the optimum of program , then the expected value (over the randomness of the Algorithm 2) of is at least .

Moreover, for every , if we set , and and satisfy the conditions above, then the expected value of , the expected total weight of the matching output by the algorithm (dropping all the edges incident to any -RHS-nodes in the matching), has weight at most less than the maximum weight matching.

-

4.

For every LHS-node , the expected weight of the edge that matches is never too much smaller than . Formally, for every and every , .

Remark 1.

To prove Theorem 3, we consider the following auxiliary problem.

Definition 6.

For any parameter , we define the following auxiliary convex program :

| s.t. | |||

Let be the solution produced by Algorithm 2.

Observation 1.

For every , and parameter , match according to the Gibbs distribution to the available RHS-nodes in ,

maximizes

subject to the constraint .

Observation 2.

For every dual variables the optimal solution maximizing the Lagrangian of program subject to the constraints is

Hence

We prove in Lemma 6 that the optimum of is exactly the same as the optimum of .

Lemma 6.

For all and , if , then

| (5) |

This implies that the optimal objective values of and are equal.

Proof of Lemma 6:

For every , recall . Observe that . We have

| RHS | |||

Hence, Equation (5) holds. Since the optimal values satisfy the requirements by Observation 2, we have that the optimum of is at least as large as the optimum of . On the other hand, let be the optimal solution of , we can choose and so that and . Clearly, is a feasible solution to , therefore the optimum of is at most as large as the optimum of . Combining. the two claims, we prove that and have the same optimal objective values.

Lemma 7.

With parameter , let be the optimal solution of . The optimum of , , is no smaller than the weight of the maximum weight matching.

Proof.

Let be the maximum weight matching. It is not hard to see that we can construct a vector so that is a feasible solution of . As both and only take values in or , the entropy term . Hence, the optimum of is at least as large as the weight of the maximum weight matching .∎

Proof of Theorem 3: As the algorithm always produces a matching that respects the constraints of , the first property clearly holds. As the set of available RHS-nodes and the dual variables only depend on the first LHS-nodes but not the LHS-node , the maximal-in-range property follows from Observation 1. The algorithm runs in rounds, step 3 and 4 both take time. Step 5 takes expected time and -many samples from distributions to complete. Hence, the running time and sample complexity as stated in the second property.

If we execute Algorithm 1 on a -to- matching with weights and Algorithm 2 over weights with the same parameters , we can couple the two executions so that the dual variables and the remaining capacities are the same for every . We introduce the new notation which is exactly the set of available RHS-nodes in step 2 of both algorithm in round . Note that is deterministically determined by . If and are the same in both algorithms for every , then for every and . To verify this, simply observe that

How does the coupling work? We construct it by induction. In the base case where , clearly everything is the same in both algorithms. Suppose the dual variables and the remaining capacities are all the same for the first rounds, we argue that we can couple the two executions in round so that and remain the same in both algorithms. First, the set is the same, which implies that the dual variables are also the same. Next, Algorithm 1 samples a RHS-node according to distribution and Algorithm 2 samples a RHS-node according to distribution . Note that , so wherever Algorithm 1 matches the LHS-node to a RHS-node we match the LHS-node to the normal RHS-node with probability and to the -RHS-node with probability . Clearly, this coupling makes sure the new remaining capacities also remain the same. Combining the coupling with Lemma 6, we conclude that

By Theorem 2, the expected value of is a multiplicative approximation to , if we choose the parameters according to the third property of the statement. Therefore, the expected value of is a multiplicative approximation to . Since the optimum of , , is the same as (Lemma 6), the expected value of is also a multiplicative approximation to . Now, invoke Lemma 7, we know that the expected value of is at least a multiplicative approximation to the weight of the maximum weight matching, which we denote as OPT. Note that the entropy term is non-negative and at most , hence the expected weight of the matching produced by Algorithm 2, the expected value of , is at least .

If we choose , , then and as . Thus, the expected weight of the matching produced by Algorithm 2 is within an additive error of from the weight of the maximum weight matching. This completes our proof for the third property.

Now we are going to prove the final bullet of the theorem. We denote the entropy of as:

By Observation 1,

Therefore the objective of solution is a lower bound on the objective of solution :

Since , we can conclude that:

5 -BIC to BIC Transformation

In this section, we present our -BIC to BIC transformation. In Theorem 4, we prove a more general statement where the given mechanism is -BIC with respect to , while we construct an exactly BIC mechanism with respect to a different distribution . If , the problem is the -BIC to BIC transformation problem. We show that the revenue of under decreases gracefully with respect to the Wasserstein Distance of the two distributions. For every , we denote the -Wasserstein Distance of distributions , . We slightly abuse notation and let .

Our mechanism works in the following way. After some agent reports her type, we sample i.i.d. replicas, i.i.d. “real” surrogates and add 0-surrogates, for some appropriately chosen parameters . The true type is inserted into a random position in the replicas. We define the weight between a replica and a “real” surrogate to be (almost) the expected utility of type if she reported to the original mechanism . The weights between replicas and 0-surrogates are 0. Then, we run Algorithm 2 in order to get a -to-1 matching between the replicas and the surrogates. To ensure that this matching is truthful, we impose appropriately selected payments to the agent. This is the first phase of . Now, suppose that the true agent is matched to surrogate . In the second phase of the mechanism, we let participate in along with the matched surrogates of the other agents. If is a 0-surrogate, then the agent gets the outcome and pays nothing. Otherwise, she gets the outcome that the surrogate gets and pays the same price discounted by a factor of . We remark that a downward-closed outcome space is necessary here to allow a outcome.

A formal description of our mechanism is shown in Mechanism 3. In step 3, the parameter is estimated using an approach similar to Dughmi et al. [24]. See Lemma 17 in Appendix A for more details.

How do we compute the payment of Phase 1? Note that if any agent reports truthfully, then the surrogate who participates for agent in Phase 2 131313Agent may be matched to a -surrogate, then is the type of the corresponding normal surrogate. is exactly drawn from distribution . Therefore, if all the other agents report truthfully, agent ’s value for winning a normal surrogate is exactly and otherwise. In other words, Mechanism 3 is equivalent to a competition among replicas to win surrogates, and the edge weight between a replicas and a surrogate is exactly the replica’s value for the surrogate. To show that Mechanism 3 is BIC, it suffices to prove that the payment of Phase 1 incentivizes the replicas to submit their true edge weights. As Algorithm 2 is maximal-in-range, such payment rule indeed exists.

If the true type is the -th replica, and the reported type induces edge weights , charge the agent

| (6) |

where , , and is the set of dual variables in the -th iteration of Algorithm 2. Observation 1 implies that the payment rule is BIC. However, direct implementation of the payment requires knowing the edge weights which we only have sample access to. We use a procedure called the implicit payment computation [4, 29, 6, 7, 24] to circumvent this difficulty.

Definition 7 (Implicit Payment Computation).

For any fixed parameters ,, and , let be the edge weights on a size bipartite graph, we use to denote

, the allocation of the -th LHS-node/replica to the surrogates computed by Algorithm 2 on the bipartite graph. Now, fix r and s, we use to denote . Suppose agent ’s reported type is in position , that is, . To compute price , let surrogate be the surrogate sampled from by Algorithm 2 in step 6, where is the collection of edge weights in graph as defined in step 5 of Mechanism 3, and we sample a surrogate from , where contains all weights of the edges incident to the -th replica, and is simply multiplying each weight in by . Then we sample from , the price is

where if , otherwise .

In expectation over , and ,

if we also take expectation over ,

With Definition 7, our mechanism is fully specified. We proceed to prove that the mechanism is BIC and IR. Our transformation is quite robust. Even if the original mechanism is not -BIC or the estimated in step 3 is not a constant factor approximation of , the mechanism is still BIC and IR. The proof for truthfulness is similar to the one in Dughmi et al. [24]. However, as our edge weights may be negative, it is more challenging to establish the individually rationality compared to Dughmi et al. [24]. To make sure the mechanism is IR, we sometimes need to use negative payments to subsidize the agents, and at the same time guarantee that the total subsidy is negligible compared to the overall revenue. Note that this is also different from the previous -BIC to BIC transformations [23, 38, 18], as they essentially use the VCG mechanism to match surrogates to replicas, their mechanisms are clearly individually rational and use non-negative payments. The proof of Lemma 8 is postponed to Appendix B.

Lemma 8.

For any choice of the parameters , , , , and any IR mechanism , is a BIC and IR mechanism w.r.t. . In particular, we do not require to be -BIC. Moreover, each agent ’s expected Phase 1 payment is at least . Finally, on any input bid , computes the outcome in expected running time and makes in expectation at most queries to .

We are now ready to present our main result for this section (Theorem 4). To prove the theorem, it suffices to lower bound the revenue of from the second phase due to Lemma 8. In the previous transformations [23, 38, 18], the mechanism computes an exact maximum weight replica-surrogate matching, which allows them to bound the revenue from the second phase directly. Our mechanism only computes an approximately maximum weight replica-surrogate matching. As a result, we need to use a more delicate analysis to lower bound the revenue from Phase 2. We refer the readers to Appendix B.1 for more details about bounding the revenue loss and the complete proof of Theorem 4.

Theorem 4.

Let be a downward-closed outcome space. Given sample access to distributions and , and query access to an -BIC and IR mechanism w.r.t. distribution . We can construct an exactly BIC and IR mechanism w.r.t. distribution , such that

| (7) |

On any input bid , computes the outcome and payments in expected running time and makes in expectation at most queries to , where is the support of and .

Furthermore, for any coupling between and such that is non-increasing w.r.t. 151515Roughly speaking, is non-increasing w.r.t. a coupling if the coupling always couples a “higher” type to a “lower” type. Namely, for all , outcome , if the coupling produces type and , then . , the error bound can be improved as follows:

| (8) |

where is the allocation rule of and can be chosen to be an arbitrary constant in .

Inequality (7) is our main result, and provides a strong guarantee in very general settings. Even though the difference between Inequality (8) and (7) seems small, we like to point out that the difference can be substantial sometimes and there were indeed cases where one needed a sharper version similar to Inequality (8). In particular, one common application of bounds similar to Inequality (8) is when the coupling simply rounds values down. For example, the main results in [18, 31] heavily rely on inequalities similar to Inequality (8), and these results may not be possible if only an Inequality (7) type bounds are used.

When , , the following corollary states the -BIC to BIC transformation.

Corollary 1.

If , .

Another useful corollary is when we choose to be the optimal BIC, IR mechanism for , we conclude that the optimal revenue under is not far away from the optimal revenue under .

Corollary 2.

If for all , let and be the optimal revenue achievable by any BIC and IR mechanism w.r.t. and respectively. Then .

6 Black-box Reduction for Multi-Dimensional Revenue Maximization

In this section, we apply Theorem 4 to the multi-dimensional revenue maximization problem. Cai et al. [15] provide a reduction from MRM to VWO. More formally:

Theorem 5 (Rephrased from Theorem 2 of Cai et al. [15]).

Let be a general outcome space. Given the bidders’ type distributions . Let be an upper bound on the bit complexity of and for any agent , any type , and any outcome , and OPT be the optimal revenue achievable by any BIC and IR mechanisms. We further assume that types are normalized, that is, for each agent , type and outcome , .

Given oracle access to an -approximation algorithm for VWO with running time , where is the bit complexity of the input, there is an algorithm that terminates in time, and outputs a mechanism with expected revenue that is -BIC with probability at least . Recall that . On any input bid, the mechanism computes the outcome and payments in expected running time .

We can apply Theorem 4 to the final mechanism produced by Theorem 5 and obtain an exactly BIC mechanism with almost the same revenue.

Theorem 6.

Let be a downward-closed outcome space. Given the bidders’ type distributions . Let be an upper bound on the bit complexity of and for any agent , any type , and any outcome , and OPT be the optimal revenue achievable by any BIC and IR mechanisms. We further assume that types are normalized, that is, for each agent , type and outcome , .

Given oracle access to an -approximation algorithm for VWO with running time , where is the bit complexity of the input, there is an algorithm that terminates in time, and outputs an exactly BIC and IR mechanism with expected revenue

where . On any input bid, computes the outcome and payments in expected running time .

Proof of Theorem 6: When the mechanism computed by Theorem 5 is -BIC, our transformation converts it into a BIC mechanism with at most less revenue. The important property of our transformation as stated in Lemma 8 is that even if the initial mechanism is not -BIC, our transformation still produces an exactly BIC mechanism. In this case, we can still treat the given mechanism as -BIC and IR, and use the corresponding revenue guarantees provided by Theorem 4. Since the probability that the mechanism computed by Theorem 5 is not -BIC is exponentially small, we can absorb the loss from this exponentially small event in the error term . The time complexity follows from Theorem 4 and 5.

Since our Theorem 4 allows us to construct a close to optimal mechanism w.r.t. the type distribution , if is not too far away from the distribution that is designed , we can approximate the optimal revenue even when we only have sample access to the bidders’ type distributions. A byproduct of this result is that the running time of our algorithm no longer depends on the bit complexity of the probability that a particular type shows up.

Theorem 7.

Let be a downward-closed outcome space. Given sample access to bidders’ type distributions . Let be an upper bound on the bit complexity of and for any agent , any type , and any outcome , and OPT be the optimal revenue achievable by any BIC and IR mechanism. We further assume that types are normalized, that is, for each agent , type and outcome , .

Given oracle access to an -approximation algorithm for VWO with running time , where is the bit complexity of the input, there is an algorithm that terminates in time, and outputs an exactly BIC and IR mechanism with expected revenue

where . On any input bid, computes the outcome and payments in expected running time .

Proof of Theorem 7: We can create an empirical distribution for each bidder , such that , with probability at least using samples.

We first consider the case where . Then, , as the highest value for any outcome is at most . Apply Theorem 5 on and let be the produced mechanism, be the optimal revenue achievable by any BIC and IR mechanism w.r.t. . Clearly, Theorem 5 guarantees that . According to Corollary 2,

We set and , we apply Theorem 4 to , that is, the replicas are sampled from and the surrogates are sampled from . Let be the constructed mechanism, and Theorem 4 guarantees that

if is a -BIC and IR mechanism. Otherwise, we know that is a -BIC and IR mechanism, and this happens with exponentially small probability according to Theorem 5, so we can absorb the loss from this case in . To sum up, if , then .

With probability we may get unlucky and may be larger than for some . In that case we still construct in the same way, and we can apply Theorem 4 by upper bounding by and treating as a -BIC and IR mechanism, which shows .

7 General Outcome Space: Regularized Replica-Surrogate Fractional Assignment

In this section we consider general outcome space , removing the assumption that is downward-closed. We first demonstrate in Example 3 that only having sample access to the agents’ type distributions is not sufficient to transform an -BIC mechanism to exactly BIC, with a small revenue loss.

Example 3.

Consider the following -BIC to BIC transformation instance for a single buyer. Let

be the set of the buyer’s types, , where is the distribution with support and point-mass probability:

The output space is such that:

For each distribution we consider the mechanism : if the buyer reports , the mechanism outputs and charges the buyer , if the buyer reports , the mechanism outputs and charges the buyer , if the buyer reports , the mechanism outputs and charges the buyer . If the buyer reports anything else, the mechanism outputs and charges the buyer . Mechanism is -BIC and IR for distribution . The revenue of is .

The mechanism designer has oracle access to set and faces the following problem: There is an arbitrary distribution from the whole space , which is unknown to the designer. The buyer’s valuation distribution is realized to be some , the designer is given sample access to , oracle access to 161616In other words the mechanism designer does not know the outcome space . It can only put a input type into the mechanism and outputs the returned outcome. and she needs to output a truly BIC and IR mechanism w.r.t. the buyer’s realized distribution that approximately preserves the revenue. Note that . Therefore the size of each is at most .

In Lemma 9, we prove that with proper choice of , any BIC and IR mechanism with samples from the type distribution and queries from has revenue far less than .

Lemma 9.

For any choose and . For any , let be any BIC, IR mechanism w.r.t. , which only uses samples from and queries from (notice that is the size of the input). Then . As goes to 0, goes to 0 while goes to 1.

Proof.

Denote the output of mechanism if the agent reports type and the expected payment if the agent reports . Notice that the outcome of can only be , or . Thus the output of mechanism is also one of these three outcomes. Let for inputs be the following distributions

Then by BIC constraint we have that:

By the previous inequalities we can infer that:

Notice that either or . The claim holds because if is non-negative, then and if is negative we have that . Without loss of generality assume .

Now we are going to bound . Note that since the mechanism designer does not have access to the outcome space, the only way to find outcome is to use as input to the mechanism . To do that, the designer must sample either directly from the type space or the realized distribution 171717Note that if the designer does not sample uniformly at random from the set , since the distribution over is unknown, the adversary can make it more difficult for her to sample the right type by picking a different distribution.

With at most samples from the buyer’s distribution , with probability at least , none of the sampled types is . By assumption, which implies that with probability at least we are not be able to sample type , therefore we cannot find output by this method.

Moreover, notice that the output of is for all types . Thus by querying mechanism with at most types chosen uniformly at random from , with probability at least , none of the returned outcomes is . By assumption implies that with probability at least none of the returned outcomes is .

Hence, for any , by taking Union Bound over the two events described above, we cannot identify output with probability at least . This implies . Similarly we can prove that .

By IR constraints for type , we have . Thus . By we denote the utility of type in mechanism when she reports . Consider the BIC constraint for type when she reports type . We have

Thus . Notice that both and are at most since the agent’s value under these two types are at most . Thus . ∎

Throughout this section, we will assume that we have full access to the agents’ type distributions: Assume every agent’s type distribution is discrete with finite support. We denote the support of the distribution of the -th agent as and the probability that the -th agent has type as . When there is no confusion about the agent that we are referring to, we may drop the superscript in . The constructed mechanism knows and the exact value for every .

We first present the result in the ideal model, where the edge weights are known exactly. Then we show that if we only estimate the edge weights approximately, we can use an approach similar to [28] to still guarantee the mechanism is BIC and IR.

7.1 Regularized Replica-Surrogate Fractional Assignment

We now present the Regularized Replica–Surrogate Fractional Assignment (RRSF) introduced by [28]. There are two main differences between RRSF and the replica-surrogate matching: (i) the replicas and surrogates in RRSF are no longer samples from the agent’s type distribution; for each type of the agent, there is exactly one replica and one surrogate of that type in RRSF; (ii) RRSF finds the optimal fractional assignment rather than a maximum weight matching.

Definition 8 (Definition 4.6 of [28]).

Let . For agent and , let be any value in . We may drop the superscript when agent is fixed and clear from context. Consider the following convex program with coefficients , where the decision variables are .

| (9) |

Let be an optimal solution to the primal problem and be any Lagrange multipliers satisfying the KKT condition

-

1.

-

2.

-

3.

7.2 Ideal Model

RRSF Mechanism with parameters :

every agent reports her type . Let be a random surrogate type such that for every .

The RRSF mechanism runs mechanism under the random input . The outcome for is the random outcome generated from and agent ’s expected payment is plus some extra payment , where . We call the RRSF mechanism with respect to if for every , the parameters are obtained by the convex program with coefficients .

Similar to [28], in our proof each will be chosen to be the expected utility of agent for the outcome of the mechanism when her type is and she is matched to the surrogate of type . Formally,

They proved that the RRSF mechanism with respect to the W defined above is BIC and IR.

Theorem 8 ([28]).

Given any mechanism . For every agent and , let

Then RRSF mechanism defined in Definition 8 is BIC and IR.

As Hartline et al. [28] only care about the welfare of , Theorem 8 suffices. We care about the revenue of , so we need to argue that running does not cause the designer to lose a large fraction of the revenue. contains two parts: (i) the expected revenue from payments , which is exactly the same as ; (ii) the expected payments from . To prove that is not too much smaller than , we need to prove that the expected payments from are not too negative. We prove this claim with the following sequence of lemmas.

We will prove a more general result for any RRSF mechanism with respect to W that satisfies: , for some . Note that when W is chosen as in Theorem 8 and is -BIC and IR, we will have and . The more general result is useful in the proof of the non-ideal model in Section 7.3.

We first prove a structural result about the optimal solution of the convex program .

Lemma 10.

Fix any agent . Suppose for all , holds for some . Let be an optimal solution of the convex program . Then, it holds that

Proof.

For any type such that the statement holds.

Now assume there are some types such that . A sequence of types of length , where , is called a flow sequence if for each it holds that . Let be the set of types (including ) such that there exists some flow sequence that starts with type that reaches them. We are going to prove that .

Note that for each , if then . Thus the set . Since is feasible, we have

On the other hand,

Therefore, we must have and for every , . Since , we have . Let such that and be the shortest flow sequence from to . Then each type appears in at most once. Let (here ). We consider the following new solution :

We will verify that is a feasible solution to RRSF. For the first set of constraints: for every , notice that (i) and (ii) there exists a unique such that . Thus . For the second set of constraints: for every for some , notice that there exists a unique such that , we have

For the third set of constraints: for every pair , either (the second and third case), or as .

Therefore is a feasible solution to RRSF. Moreover since is the optimal feasible solution, its objective should be at least the objective value of . Observe that for every and every edge with the value is not equal to only when there is some with . The value of this edge drops by , whereas the value of increases by . Denote the value of the objectives for these two feasible solutions respectively. In the flow sequence , for every for some , denote . We have

Since we have

Thus

∎

Equipped with Lemma 10, we proceed to show that the convex program has a set of optimal Lagrange multipliers that will make the total expected payments from not too negative. First, we construct a new convex program that “removes” all the very negative edge weights from , that is, change every edge ’s weight to (see Definition 9). Then, we argue that convex program and are essentially equivalent. Namely, any optimal solution of is also an optimal solution for , and there is a straightforward mapping that transforms any optimal Lagrange multipliers of to a set of optimal Lagrange multipliers for (see Lemma 11). Finally, we show that if we compute using any set of the optimal Lagrange multipliers derived from convex program , then is not too negative (see Lemma 12) The main reason is that using the KKT condition, we can relate to the edge weights, and the edge weights in are not too small.

Definition 9.

Fix an agent and . For every , define

We solve the following convex program where the decision variables are .

| (10) |

Let be an optimal solution of and be any Lagrange multipliers satisfying the KKT conditions:

-

1.

-

2.

-

3.

Lemma 11.

Fix any agent . Suppose for all , holds for some . Let be any optimal solution of the convex program . Then is also an optimal solution of the convex program . Moreover let , , be any Lagrange multipliers satisfying the KKT conditions w.r.t. the convex program . Then there exists such that ,, satisfies the KKT conditions w.r.t. the convex program .

Proof.

We first prove that is also an optimal solution of the convex program . Clearly is a feasible solution of the convex program . To argue is an optimal solution, we first prove that . For every , Since , . If , then and we have since . On the other hand, suppose . Then . .

We apply Lemma 10 to convex program . For any such that , . Thus it must hold that and the solution has the same objective value in and . Moreover since for every , the optimal objective value of is no larger than the optimal objective value of . Thus is an optimal solution of the convex program .

For the second part of the statement, consider the following dual variables :

We now verify that satisfies the KKT conditions w.r.t. the convex program . When we have that and . This implies that:

-

1.

-

2.

-

3.

Now consider such that . In this case . By Lemma 10, if , then . This contradicts with the fact that , so . We have

-

1.

-

2.

-

3.

Thus satisfies the KKT conditions w.r.t. the convex program . ∎

As illustrated in the following example an arbitrary set of optimal dual variables that satisfy the KKT conditions can cause a big revenue loss.

Example 4.

We consider the following instance. There is one agent with two possible types and such that the agent has type with probability and with probability for some sufficiently small . The outcome space . and . The mechanism is defined as follows: it returns outcome with input and returns outcome with input . The payment of the mechanism is always . It’s a BIC mechanism and it holds that and .

We are going to prove through KKT conditions that for this instance, the following is the optimal solution for Convex Program : and . Consider the following set of dual variables: , , , and .

Note that , and , . One can verify that the dual variables satisfy the KKT conditions with respect to , which implies that is an optimal solution for .

Note that . According to the payment rule, the payment charged to the first agent if she has type is and the payment charged if she has type is .

Therefore the expected revenue of the RRSF mechanism with parameter is . When both and go to , the expected revenue of the mechanism is close to , which is far from the revenue of .

Lemma 12.