Asset Price Bubbles in markets with Transaction Costs

Asset Price Bubbles in market models with proportional transaction costs

Abstract

We study asset price bubbles in market models with proportional transaction costs and finite time horizon in the setting of [48]. By following [28], we define the fundamental value of a risky asset as the price of a super-replicating portfolio for a position terminating in one unit of the asset and zero cash. We then obtain a dual representation for the fundamental value by using the super-replication theorem of [49]. We say that an asset price has a bubble if its fundamental value differs from the ask-price . We investigate the impact of transaction costs on asset price bubbles and show that our model intrinsically includes the birth of a bubble.

Keywords: financial bubbles, fundamental value, super-replication, transaction costs, consistent price systems

Mathematics Subject Classification (2010): 91G99, 91B70, 60G44

JEL Classification: G10, C60

1 Introduction

In this paper we study financial asset price bubbles in market models with proportional transaction costs and finite time horizon. In the economic literature there are several contributions discussing the impact of transaction costs on the formation of asset price bubbles. It is apparent that bubbles may also appear in markets with big transaction costs, see [5], [22] and also [23], [43], [53] for the speficic case of the real estate market. Several approaches can be found in the literature to explain bubbles, like asymmetric information, see [2], [3], heterogenous beliefs, see [27], [52], and noise trading such as positive feedback activity [15], [54], [57], in combination with limits to arbitrage, see [1], [14], [55], [56]. In [52], the authors include transaction costs in an equilibrium model with heterogeneous beliefs and show that small transaction costs may reduce speculative trading and then prevent bubble’s formation. However, price volatility and size of the bubble are not reduced effectively. For an overview of heterogeneous beliefs, we refer to [60]. Also in [58], the authors show in an agent-based simulation that transaction costs can have positive impact by stabilizing the financial market model in the long run.

From a mathematical point of view, there is a wide literature on the theory of asset bubbles in frictionless market models. In general, a bubble is given by the difference of the market price of the asset and its fundamental value. While the market price can be observed, it is less obvious how to define the fundamental value. In the martingale theory of asset prices bubbles, see [12], [31], [36], [44], the fundamental value of a given asset is given by its expectation of future cash flows with respect to an equivalent local martingale measure. This definition has been criticized in [24] for its sensitivity with respect to model’s choice. Another approach defines the fundamental value of an asset by its super-replication prices, see [28], [29]. Other models explicitly describe the impact of microeconomic interactions on asset price formation, see [10], [35]. In [35], the fundamental value is exogenously given and asset price bubbles are endogenously determined by the impact of liquidity risk. In [10], microeconomic dynamics may at an aggregate level determine a shift in the martingale measure. Further references on asset price bubbles are [7], [8], [9], [30], [33], [34], [51]. For a comprehensive overview see also [46] and the entry “Bubbles and Crashes” of [41].

The aim of this paper is twofold. First, we wish to introduce and study the notion of asset price bubbles in market models with proportional transaction costs. In [24], the authors suggest a robust definition of asset price bubbles which can be interpreted as a bubble under proportional transaction costs. However, to the best of our knowledge a thorough study of this topic is still missing in the literature.

Secondly, we want to investigate in a mathematical setting the impact of transaction costs on asset bubbles’ formation and size. In particular, we can see that the presence of market frictions may prevent the birth of a bubble in some cases, but not always, and that we obtain that the introduction of transaction costs may not always reduce the size of a bubble, see (4.6), consistently with the results in the economic literature.

In market models with proportional transaction costs we distinguish between the ask price and the bid price for a given asset price . It is well-known that in the frictionless case the no-arbitrage condition no free lunch with vanishing risk (NFLVR) is equivalent to the existence of an equivalent local martingale measure, see [16]. In the presence of proportional transaction costs, the existence of consistent (local) price systems (Definition 2.1) for each guarantees that the corresponding market model is arbitrage-free in the sense of Definition 4 of [26]. Equivalence is obtained for continuous asset price processes. Furthermore, in [6], the authors establish an equivalence between the weaker notions of strictly consistent local martingale systems and the NUPBR111no unbounded profit with bounded risk and NLABPs222no local arbitrage with bounded portfolios conditions in the robust sense. Roughly speaking, a consistent (local) price system can be thought as a dual market model without transaction costs where the trading happens parallel. For a detailed overview of the theory of proportional transaction costs, we refer to the books [37] and [50].

Due to the presence of transaction costs, positions in cash and in the asset are asymmetric. By following [28], we define the fundamental value of a given asset as the price of a super-replicating portfolio for a position terminating in one unit of the asset and zero cash. More precisely, we are interested in super-replicating a position in the asset, and not in the liquidation value of the portfolio. First we study some properties of the fundamental value. We establish a dual representation for for any time based on the super-replication results from [11] and [49] and show time independence of the consistent (local) price system in the dual representation, see Theorem 3.9. In particular, in Theorem 3.15 we study when the fundamental value admits a right-continuous modification. An asset price bubble is defined as the difference of the ask price with respect to the fundamental value. For the frictionless case, if the NFLVR condition is satisfied in the setting of [28], one can apply the duality result from [42] and obtain that there is a bubble if and only if the price process is a strict local martingale under all equivalent local martingale measures. In particular, if there is at least one equivalent local martingale measure such that is a true martingale, there is no bubble in the market model. Analogously, in our framework there is no bubble in the market model if there exists a consistent price system in the non-local sense for any , see Proposition 3.11.

Further, we discuss this theoretical setting in several examples. In particular, the impact of proportional transaction costs is investigated by comparing our model to the frictionless framework of [28]. It is immediate to see that no bubble in the frictionless market model means no bubble in the analogous market model with transaction costs. On the other side, if there is a bubble in the market model with proportional transaction costs, there is also a bubble in the frictionless market model. However, if there is a bubble in the frictionless market model, the introduction of transaction costs can possibly eliminate the asset price bubble. Finally, we note that our definition of asset price bubble intrinsically includes bubbles’ birth, i.e., the possibility that there is no bubble at the initial time , but the bubble starts at some later time with positive probability, as in the settings of [7] and [28].

The paper is organized as follows. In Section 2, we outline the setting for market models with proportional transaction costs and extend the notion of admissible strategies. In Section 3, we introduce the definition of the fundamental value and of asset price bubbles, and establish a dual representation for the fundamental value. Further, we prove the main results, Theorem 3.9 and Theorem 3.15. In Section 4, the impact of proportional transaction costs on bubbles’ formation and size is investigated. In Section 5, we illustrate our results through concrete examples. In the Appendix, we state the super-replication results from [49] with small modifications.

2 The Setting

Let describe a finite time horizon and let be a filtered probability space where the filtration satisfies the usual conditions of right-continuity and saturatedness, with and . We consider a financial market model consisting of a risk-free asset , normalized to , and a risky asset . Throughout the paper we assume that is an -adapted stochastic process, with càdlàg and positive paths. For trading the risky asset in the market model, proportional transaction costs are charged, i.e., to buy one share of at time the trader has to pay and for selling one share of at time the trader receives . The interval is called bid-ask-spread. Further, we assume that for all . This assumption is needed in the proof of Lemma 3.6 and thus also for the main result, Theorem 3.9.

Definition 2.1.

For and a stopping time , we call (resp. ) the family of pairs such that Q is a probability measure on , , is a martingale (resp. local martingale) under Q on , and

| (2.1) |

A pair in (resp. ) is called consistent price system (resp. consistent local price system). By (resp. ) we denote the set of measures Q such that there exists a pair (resp. ). Further, we write and . By (resp. ) we denote the space of -valued random variables (resp. ).

A consistent (local) price system can be thought as a frictionless market with better conditions for traders, see [25]. The existence of a -consistent (local) price system for every implies that the corresponding market model is arbitrage-free in the sense of Definition 4 of [26]. Considering consistent price systems in the non-local or local sense corresponds in the frictionless case to the characterization of no arbitrage using true martingales or local martingales. In both cases the difference lies in the choice of admissible trading strategies. If there is no natural numéraire it seems reasonable to compare the portfolio with positions which may be short in each asset. On the other hand, if we fix a numéraire we control the portfolio only in units of the numéraire. In particular, we do not allow short positions in the risky asset. See Chapter 5 of [26] for a more detailed discussion. For the convenience of the reader we summarize the assumptions that we use through out the paper.

Assumption 1.

We assume that admits a consistent local price system for every .

In the sequel we will sometimes need a stronger assumption, namely, the existence of consistent price systems (in the non-local sense) for every .

Assumption 2.

We assume that admits a consistent price system for every .

Remark 2.2.

By following [26], [38], for we denote by the solvency cone at time , defined as

| (2.2) |

where are the unit vectors in , and by the corresponding polar cone, given by

| (2.3) | ||||

Definition 2.3.

We define (resp. ) as the set of processes such that is a P-martingale on and is a P-martingale (resp. local P-martingale) on and such that a.s. for all .

The following proposition from [26] provides a convenient representation of consistent (local) price systems by elements in (resp. ) and follows directly from the definition of in (2.3).

Proposition 2.4 (Proposition 3, [26]).

Let be a -dimensional stochastic process with . Define the measure by . Then (resp. ) if and only if is a consistent price system (resp. consistent local price system) on .

Next, we introduce the notion of self-financing strategies and admissibility, by extending Definition 3 and 5 of [48] to a general starting value.

Definition 2.5.

Let . A self-financing trading strategy starting with initial endowment is a pair of -predictable finite variation processes on such that

-

(i)

and ,

-

(ii)

denoting by and , the Jordan-Hahn decomposition of and into the difference of two non-decreasing processes, starting at , these processes satisfy

(2.4)

Definition 2.6.

Let .

-

(i)

Let . Then a self-financing trading strategy is called admissible in a numéraire-based sense on with if there is such that the liquidation value satisfies

(2.5) for all -valued stopping times .

-

(ii)

Let . Then a self-financing trading strategy is called admissible in a numéraire-free sense on with if there is such that

(2.6) for all -valued stopping times .

We denote by (resp. ) the set of all such trading strategies in the numéraire-free sense (resp. numéraire-based sense) on the interval . We also use the notation (resp. ).

For more details on the differential form of (2.4) we refer the interested reader to [48].

Note that both accounts, the holdings in the bond as well as the holdings in the asset are separately given in the definition of a trading strategy . Having an inequality in (2.4) allows for “throwing money away”, see [48]. As it is explained in [48] we could require equality in (2.4) in order to express in terms of . However, for our approach it is more convenient to specify both accounts separately.

Remark 2.7.

We now discuss the definition of admissible strategies. Since we are interested in considering strategies on a random interval with non-zero initial endowment, we need to extend Definitions 3 and 5 of [48], as we now explain for the numéraire-based case. The argument for the numéraire-free setting is analogous. In a first step we consider the case of zero initial endowments. Assume that and for all -valued stopping times and a constant . Then corresponds to an admissible strategy on according to Definition 3 of [48], where on and for all . Conversely, any strategy on with on , which is admissible in a numéraire-based sense in the sense of [48], also satisfies Definition 2.6. Suppose now to have a non-zero initial endowment. By translation, any admissible strategy on with initial endowments corresponds to an admissible strategy on without initial endowment. This correspondence is more delicate for strategies on . Let for some with and define for all . Then . Hence, it is not enough to bound the liquidation value of a strategy by a constant in order to have a one-to-one correspondence of admissible strategies with and without endowments on . Definition 2.6 allows to obtain from any admissible strategy on an admissible strategy on . Note that in the case of Definition 2.6 and Definition 3 of [48] coincide.

When we consider the definition of admissibility in a numéraire-based sense on from an economical perspective, the role of is to hedge the portfolio by units of the bond, see [48]. In particular, when we superhedge a portfolio on , it seems reasonable to use the information which are available up to time , namely, to superhedge the portfolio by units of the bond, where .

We now comment on the integrability conditions of the lower bound .

Remark 2.8.

We discuss the local and the non-local case separately.

In Definition 3 of [48] the liquidation value of an admissible strategy in the numéraire-based sense is required to be lower bounded by a constant. This guarantees that is an optional strong Q-supermartingale for all , see Proposition 2 of [48].

As explained in Remark 2.7 we wish to extend the definitions of [48] to include admissible strategies on an arbitrary interval with arbitrary initial endowment. To this propose we need to impose condition (2.5). However, we still obtain an arbitrage-free market model.

In the proof of Proposition 2 of [48] the lower bound is used to apply Proposition 3.3 of [4], respectively Theorem 1 of [59]. The conditions of these results are still fulfilled on if (2.5) holds, and thus is an optional strong Q-supermartingale for all .

In the non-local case, Definition 5 of [48] requires that the liquidation value of an admissible strategy in the numéraire-free sense satisfies

| (2.7) |

for all -valued stopping times . This guarantees that is an optional strong Q-supermartingale for all , see Proposition 3 of [48]. Following the proof of Proposition 3 of [48], we apply the following conditional version of Fatou’s lemma. Let be a sequence of real-valued random variables on converging almost surely to and such that the negative parts are uniformly Q-integrable. Then

In our case, the family is uniformly Q-integrable with respect to Q for all , as we have for

because for any and is a Q-martingale, and by assumption. Therefore, is an optional strong Q-supermartingale on for all and all trading strategies are admissible in a numéraire-free sense.

3 Asset price bubbles under proportional transaction costs

The notion of an asset price bubble consists of two components, namely, the market price of an asset and its fundamental value. We assume that the market price is given by the price process . For the fundamental value of an asset, we here follow the approach of [28] and define the fundamental value by means of the super-replication price of the asset.

In frictionless market models, it is equivalent to hold the asset or to have the (market) value of the asset in the money market account. This symmetry fails in the presence of transaction costs. A trader who wants to buy a share of the asset at time has to pay . A trader who wants to liquidate her position in the asset at time only receives per share of the asset. Therefore, a natural question arises.

Which position should we super-replicate in order to obtain a reasonable definition of the fundamental value in the presence of transaction costs?

Definition 3.1.

The fundamental value of an asset at time in a market model with proportional transaction costs is defined by

We say there is an asset price bubble in the market model with transaction costs if for some stopping time with values in . We define the asset price bubble as the process given by

| (3.1) |

Remark 3.2.

In Definition 4.2 of [24], the authors provide a robust definition of an asset price bubble, which can also be interpreted as a bubble under proportional transaction costs. A difference with respect to Definition 3.1 lies in the chosen specification of trading strategies. In [24], in the worst case scenario the strategy begins in cash, but the initial capital is all in stock, or analogously, the strategy ends in cash, but the trader has to deliver one share of the asset.

Specifying both components of the trading strategies in

our model allows to consider strategies starting in cash and ending in a position in the stock only.

Proposition 3.3.

Under Assumption 1, we have that the fundamental value is such that

and , . Moreover, the bubble has almost surely non-negative paths.

Proof.

Consider the buy and hold strategy starting at time . With an initial endowment it is possible to buy one share of the asset at time and keep it until time . Then for all . Therefore, the bubble has almost surely non-negative paths. The fact that follows by Remark 2.2. ∎

We now comment on Definition 3.1, which could be interpreted as the fundamental value for the ask price. Alternatively, we could consider to super-replicate the position which is the liquidation value of the asset at time , instead, or which is the price one has to pay to buy the asset at time . A trader who wants to super-replicate is only interested in cash, namely, in the liquidation value of the asset. However, it is not possible to re-buy at a share of the asset at price . On the other hand, a trader who wants to super-replicate is actually interested in having the asset at in the portfolio. So, super-replicating might be too expensive. Therefore, we consider the position and its corresponding super-replication price as fundamental value. This corresponds to the price a trader is willing to pay if she had to hold the asset in her portfolio until the terminal time , see [32]. Furthermore, this definition allows to model bubble birth, as in [7] and [28], as shown in Example 5.5.

3.1 Super-replication theorems and dual representation

We now provide a dual representation for the fundamental value , which allows to study further properties of and of the asset price bubble under transaction costs. To this purpose we extend some super-replication theorems.

In a frictionless market model there are well-known super-replication theorems which establish a dual representation, see e.g. [19], [42]. Analogously there are super-replication theorems for market models with proportional transaction costs to obtain a dual representation, see e.g. [13], [38], [40], [39]. We refer to the super-replication theorems of [11] and [49]. The formulations of Theorem 1.4 and Theorem 1.5 of [49] can be found in Appendix A.

Proposition 3.4.

Let Assumption 1 hold. We consider an -measurable contingent claim which pays many units of the bond and many units of the risky asset at time . Let . If

| (3.2) |

for some -measurable random variable satisfying , then the following assertions are equivalent

-

(i)

There is a self-financing trading strategy on with and which is admissible in a numéraire-based sense.

-

(ii)

For every we have

(3.3)

Proof.

It is possible to apply Proposition 2 of [48] although we consider the interval and initial endowment , see Remark 2.8. Then is an optional strong supermartingale and thus

For

we have

| (3.4) |

by equation (3.2), and for we get

| (3.5) |

by equation (3.3). Thus we can apply Theorem A.1 (Theorem 1.4 of [49]) which yields a strategy with on and which is admissible in a numéraire-based sense on . In particular, defined by and for , is an admissible strategy in the numéraire-based sense on according to Definition 2.6. ∎

From Proposition 3.4 we obtain a duality representation for the fundamental value.

Proposition 3.5.

Proof.

For and , condition (3.2) is satisfied and we get by Proposition 3.4 that

| (3.7) | ||||

By Definition 3.1 and (3.7) we have that

It is left to show that

| (3.8) |

For the first direction “” we note that , where we used that .

For the reverse direction “” we have that for all which implies by the definition of the essential supremum that

∎

Note that in the above proof can be replaced by a stopping time .

In Proposition 3.5 the essential supremum is taken over the set which depends on the initial time . In contrast, if we consider the frictionless case of [28] and assume that Theorem 3.2 from [42] applies, the fundamental value of an asset at time is given by

where denotes the set of equivalent local martingale measures for . The essential supremum is taken over all equivalent local martingale measure of , independently of the initial time . We now show that a similar independence property also holds for the fundamental value under transaction costs, see Theorem 3.9. In order to prove it, we need some preliminary results. We start with a local version of Lemma 6 and Corollary 3 of [26].

Lemma 3.6.

Let Assumption 1 hold. For each stopping time and each random variable such that

| (3.9) |

and for each there is an -consistent local price system with .

Proof.

The proof is partially based333The main difference with respect to the proof of Lemma 6 of [26] is that we cannot use the martingale property of consistent price systems as in [26], because we are now in the local setting. Hence we need some further technicalities. on the proof of Lemma 6 of [26]. Consider the sequence of stopping time , where

Note that defines a localizing sequence for all -consistent local price systems as for we have

| (3.10) |

for all and hence Proposition 6.1 of [49] can be applied. Further, it holds that a.s. Fix . First we consider the interval . Choose such that . By Assumption 1 there exists a -consistent local price system on the interval . We have

| (3.11) |

For define

Hence by (3.10) we get , and for we have

and

This implies that as well as by (3.9) and the fact that

Consequently, for and a stopping time with ,

thus using (3.11) we get

| (3.12) |

We show that converges almost surely to a random variable for all . We have that

By the Theorem of Monotone Convergence it follows that

| (3.13) |

For the second term we have

Since for all , we can apply the Theorem of Monotone Convergence to conclude

| (3.14) |

We define the process by (3.14). Since

is a -martingale, it admits a unique càdlàg modification. Further, has a unique càdlàg modification. Therefore, admits a unique càdlàg modification as a local -martingale. By (3.12) lies in the bid-ask spread for by construction. Thus is a -consistent local price system on satisfying . With the same construction as in the proof of Lemma 6 of [26] we can now show the existence of a consistent local price system such that . We refer to [47] for further details. We use this result to extend to a consistent local price system on the entire interval .

We now define which satisfies . Set by

and

Then and . ∎

Remark 3.7.

The following Corollary 3.8 can be proved in the same way as Corollary 3 in [26] because the construction does not use the martingale property of the consistent price systems.

Corollary 3.8.

Let Assumption 1 hold. For any stopping time , probability measure on and random variable with

there exists a -consistent local price system such that and .

We can now show time independence for the essential supremum in the definition of the fundamental value.

Theorem 3.9.

Under Assumption 1 the following identity holds:

Proof.

If , then . Thus, we immediately get that

Let be a sequence such that as tends to infinity. Fix an arbitrary with associated (local) P-martingales , as in Proposition 2.4. Then this can be approximated by a sequence satisfying

| (3.15) |

for each as follows. Define the set by

By Corollary 3.8 there exists for each a consistent local price system with associated (local) P-martingales , such that . We define by its associated (local) P-martingales by

Then satisfies (3.15) for all and converges to , for going to infinity. We now show that for each we can construct a pair with

| (3.16) |

Fix . By Lemma 3.6 and Corollary 3.8 there exists such that . Let be the associated (local) P-martingales as in Proposition 2.4. We define another -consistent local price system by

for . By construction it then holds that for all and

By (3.16) and because converges to , , as tends to infinity, we get that

| (3.17) |

Since was arbitrary, we can take the essential supremum over all (resp. ) on the right-hand side and conclude that

Note that the essential supremum over is equal to the essential supremum over . ∎

3.2 Properties of the fundamental value and asset price bubbles

In this section we study some basic properties of the fundamental value and of asset price bubbles in our setting.

Lemma 3.10.

The fundamental value is an adapted stochastic process, which is unique to within evanescent processes.

Proof.

By Proposition 3.5 we obtain that the fundamental value is given by

By Theorem A.33 of [21] we obtain that is an adapted process since all the probability measures are equivalent to P. As Proposition 3.4 and Theorem 3.9 hold for all stopping times , is unique to within an evanescent set because of the Optional Cross-Section Theorem, see Theorem 86 in Chapter IV of [17]. ∎

Proposition 3.11.

Let Assumption 2 hold. Then we have for all stopping times that

In particular, there is no asset price bubble in the market model.

Proof.

Let such that . By Assumption 2 there exists a for all . Define for . Then for all , since for we have

Further, it holds

where we have used the martingale property of . For the essential supremum we get

Hence we can conclude that

∎

Proposition 3.12.

Let Assumption 1 hold. If there exists such that there is no bubble in the market model with transaction costs , then there is no bubble in the market model with transaction costs .

Proof.

Let be such that

for all -valued stopping times , i.e., there is no bubble in the market model with transaction costs . Fix any . Note that . Then there exists such that . In particular, if , then . This yields

∎

Proposition 3.12 guarantees that a rise of transaction costs does not yield bubbles’ formation.

Lemma 3.13.

If the asset price is a semimartingale and the set of equivalent local martingale measures for is not empty, then for , and

| (3.18) |

Proof.

Definition 3.14.

Let be an open set in . A function is said to be upper semi-continuous at if

| (3.20) |

We say that is upper semi-continuous from the right at , if (3.20) holds for . Further, is called upper semi-continuous (from the right) if is upper semi-continuous (from the right) for all .

Theorem 3.15.

Suppose that Assumption 1 holds and assume that the function

| (3.21) |

is upper semi-continuous from the right. Then admits a right-continuous modification with respect to P.

Proof.

By Theorem 48 in [18], admits a right-continuous modification with respect to P if and only if for every decreasing sequence of bounded stopping times . For convenience, we write and in the sequel. Note that we use the representation of from Proposition 2.4. As in Proposition 4.3 of [42] we first show the identity

| (3.22) |

for all stopping times with values in . For the first direction we use monotonicity to obtain

| (3.23) |

For the reverse direction we use Theorem 3.9 to show that

is directed upwards, i.e. for there exists such that . We define

Let and be the processes associated to and respectively, as in Proposition 2.4. Then we define

| (3.24) |

and for ,

| (3.25) |

with corresponding

| (3.26) |

Obviously, satisfies all requirements from Definition 2.3, i.e., . Clearly, for all . For the local martingale property let be a localizing sequence for and . For we get

where we used that are measurable. In particular, by Theorem A.33 of [21], there exists an increasing sequence

| (3.27) |

Thus, we obtain by the Theorem of monotone convergence

| (3.28) |

The last equality in (3.28) holds due to similar arguments as in the proof of Theorem 3.9. This concludes the proof of (3.22).

Let now be a sequence of stopping times with values in such that as tends to infinity. We now prove that

Using (3.22), the Fatou’s lemma, and the fact that is right-continuous we obtain

| (3.29) | ||||

Since (3.29) holds for all we get that

| (3.30) | ||||

where the last equality follows by (3.22). By the assumption of upper semi-continuity from the right we directly obtain

| (3.31) |

Note that (3.31) also implies that the limit is finite, because

Putting (3.30) and (3.31) together yields by (3.22) that

This concludes the proof.

∎

Corollary 3.16.

Suppose that Assumption 1 holds and assume that there exists such that the function

| (3.32) |

is upper semi-continuous from the right. Then admits a right-continuous modification with respect to P.

Proof.

Since P and are equivalent we can conclude that if has a right-continuous modification with respect to , also has a right-continuous modification with respect to P. ∎

By Proposition 3.5, Lemma 3.10 and Theorem 3.15 we obtain that the fundamental price process is well-defined and admits a right-continuous modification.

Remark 3.17.

The assumption of upper semi-continuity from the right in Theorem 3.15 seems rather restrictive. In the frictionless case inequality (3.31) is automatically fulfilled because

for all is a Q-supermartingale for all . Then for any it holds that

See Proposition 4.3 of [42] for further details.

In the presence of transaction costs the supermartingale property of the fundamental value may fail. Additional regularity conditions on the family of consistent price systems must be required in order to guarantee the existence of a right-continuous modification for .

4 Impact of transaction costs on bubbles’ formation

In this section we study whether transaction costs can prevent bubbles’ formation and their impact on bubbles’ size. These issues, if market frictions may prevent bubbles’ formation or reduce their impact, has been thoroughly discussed in the economic literature, see the discussion in the Introduction. Here we study these problems from a mathematical point of view in our setting. In particular, we investigate the relation between asset price bubbles in market models with and without transaction costs.

To this purpose we use [28] as reference for the frictionless market case. We now briefly recall and re-adapt the framework of [28] to be coherent with our setting outlined in Section 2. In particular, we assume that the asset price is given by a càdlàg non-negative semimartingale such that . Under these assumptions, NFLVR holds, see [16]. Put . We denote by the set of all -valued processes which are predictable on and for which the stochastic integral process , , is defined in the sense of -dimensional stochastic integration, see [45, Section III.6].

Definition 4.1 (Definition 2.5, [28]).

Fix a stopping time . The space of self-financing strategies (for S) on consists of all -dimensional processes which are predictable on , belong to , and such that the value process of satisfies the self-financing condition

Definition 4.2 (Definition 3.1, [28]).

The fundamental value of the asset at time is defined by

| (4.1) |

We say that the market model has a strong bubble if and are not indistinguishable, i.e., if for some stopping and define the process by , .

Note that Definition 4.2 differs from Definition 3.1 of [28] since we require in (4.1) to be consistent with Definition 3.1. In this setting the duality from Theorem 3.2 of [42] holds and we get

| (4.2) |

In the more general framework of [28] it is possible that the duality does not hold, see Remark 3.11 of [28] and the comment before for more information.

Recall that, in the setting of [28] we assume that the asset price is a semimartingale and that . At time we obtain by Lemma 3.13 that

In particular, we have

| (4.3) |

From (4.3) we immediately obtain for that if , then and that if for . Let . Then

| (4.4) |

which means that the quotient of the bubbles is bounded by the factor . Furthermore, we have

| (4.5) |

It is easy to see that both bounds in (4.5) can be obtained. In Example 5.5 we get

| (4.6) |

Furthermore, we have in Example 5.4 that and thus we obtain the equality on the right hand side of (4.5). Further, we note that

| (4.7) |

By rearranging equation (4) we obtain then

| (4.8) |

Clearly, it holds . Consider Example 5.4, where is a -dimensional inverse Bessel process with respect to P and set . Then and

| (4.9) | ||||

where denotes the cumulative distribution function of the standard normal distribution, see [20]. For tending to infinity, then tends to .

Remark 4.3.

From equation (4.3) we can see that if a market model without transaction costs has no asset price bubble, then the analogue market model with transaction has no asset price bubble either. In other words, the introduction of transaction costs into a market cannot generate asset price bubbles. Conversely, by (4.3) it follows that, if a market model with transaction costs has an asset price bubble, the corresponding frictionless market model has an asset price bubble as well.

In our model the introduction of transaction costs can possibly prevent the occurrence of an asset price bubble. This can be seen in Example 5.4 where we have an asset price bubble in the sense of Definition 4.2 but no bubble in presence of transaction costs with respect to Definition 3.1. However, Example 5.5 shows that it is possible to have an asset price bubble in both market models, with and without transaction costs. In particular, the presence of transaction costs does not guarantee the absence of asset price bubbles.

5 Examples

In this section we provide several examples to illustrate our setting and the impact of transaction costs on asset bubbles. In Example 5.1 we start by showing a market model under transaction cost where the asset price, driven by a fractional Brownian motion, has a bubble in the sense of Definition 3.1. Due to well-known no-arbitrage arguments, a process driven by the fractional Brownian motion is not admissible as price process in a frictionless market model.

Then we study how the presence of an asset price bubble in a market model without transaction costs may be related to the appearance of a bubble in the analogous market model with transaction costs, and vice versa. To this purpose, we consider examples where the asset price is a semimartingale in the framework of [28] for frictionless market models. In Example 5.3 we illustrate a standard market model such that there is no bubble, neither with nor without transaction cost. This example suggests that the introduction of transaction costs cannot lead to bubble’s formation. In Example 5.4, the market model has no bubble under transaction cost but there is a bubble in the frictionless market model in the sense of [28]. In particular, this shows how transaction costs can possibly prevent the appearance of an asset price bubble. Example 5.3 and 5.4 illustrate the impact of transaction costs on bubbles’ formation. In Example 5.5 we see how bubble’s birth is already included in our model.

Example 5.1.

This example is based on Example 7.1 of [24]. Let be a fractional Brownian motion with Hurst index . We define

for . Let be the (completed) natural filtration of the process . Note that admits a consistent price system in the non-local sense on the interval for all by Proposition 4.2 of [25]. Define the stopping time

and set

Define , , and . Consider . We now show that there exists no consistent price system in the non-local sense for any . By contradiction assume that there exists a consistent price system for in the non-local sense for a . Then we have

| (5.1) |

for all , and hence also

| (5.2) |

which is not possible because is not bounded from above for . Thus, we can conclude that there is no consistent price system in the non-local sense. However, satisfies Assumption 1, i.e., for every there exists a consistent local price system for . Since admits for all a consistent local price system on for all , is also a consistent local price system for on . We now show that there is a bubble in this market model with transaction costs for . For any consistent local price system for we have

and because

This implies for

| (5.3) |

for all consistent local price systems. Thus, we have

| (5.4) |

Therefore, we can conclude by equation (5.4) that the the asset has a bubble under transaction cost at time .

Remark 5.2.

Due to the well-known arbitrage arguments, see [16], the process in Example 5.1 cannot be considered to describe asset price dynamics in a market model without transaction costs. Hence in the case a comparison with an analogous frictionless market model makes no-sense. Note also that the process can be replaced by any càdlàg process which is not bounded and admits a consistent local price system on for all and for all .

Example 5.3.

Let be a true -martingale for some probability measure . Then, is a true -martingale and is a consistent price system in the non-local sense for . For any stopping time we obtain by Proposition 3.3 that

| (5.5) |

Hence there is no bubble in the market model with transaction costs. Alternatively, we can observe that Assumption 2 is satisfied and thus we can apply Proposition 3.11.

From Definition 4.2 we have for any stopping time

So there is also no bubble in the market model without transaction cost in the sense of [28].

Example 5.4.

In this example we assume that is given by a three-dimensional inverse Bessel process, i.e.,

| (5.6) |

where is a three-dimensional Brownian motion with and consider the filtration defined by . Example 5.2 in [28], shows that there is a bubble in the market model without transaction cost in the sense of Definition 4.2. Note that there is also a P-bubble in the sense of [46] as in the case of a complete market model these definitions coincide. However, by Theorem 5.2 of [24] we have that for all there exists , where is a true Q-martingale such that

| (5.7) |

In the notation of [24], we say that is -close to . In particular, Assumption 2 is satisfied and thus we obtain by Proposition 3.11 that there is no bubble in any market model with proportional transaction costs . This example shows that proportional transaction costs can prevent bubbles’ formation.

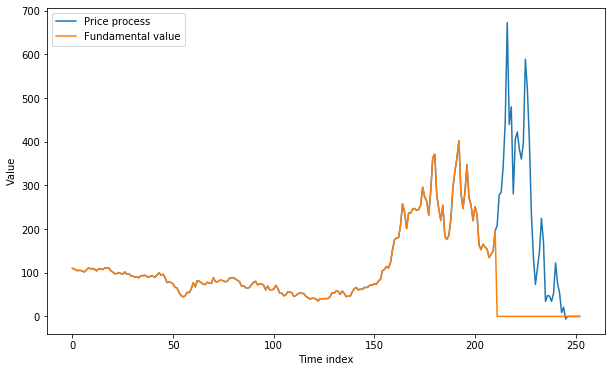

Example 5.5.

This example is based on Example 5.4 of [28]. It illustrates that bubble birth (see [46], [7]) is naturally included in our model.

Let be a random variable with values in , and for some and consider the filtration generated by . Then is a stopping time, which represents the time when the bubble is born. Further, let be a Brownian motion independent of . Denote by the natural filtration generated by and define the filtration by , , where denotes the P-nullsets of . Then is also an -stopping time. Let be the unique strong solution to the SDE

| (5.8) |

with and given by

| (5.9) |

for . Then is a geometric Brownian motion up to . At time the term starts to influence the volatility which explodes until time . This implies that converges to as tends to . We determine the fundamental value of at time . In particular, we see that there is no bubble before time but the bubble starts at . The fundamental value at time is given by

| (5.10) |

Note that for . We define the strategy on by

That is, using the initial capital we trade in such a way that we hold the asset at time . If at time , has already happened, we know that the volatility blows up and we can buy the asset at time at price . However, if happens strictly after we do not know if the volatility will blow up and thus we buy the asset at time at price in order to hold the asset at time . As this strategy super-replicates the position , we conclude that .

For the reverse direction, “” we use the duality from Proposition 3.4. By Example 5.4 of [28] we get

From this we obtain

Indeed, we have

This implies that on and on . In particular, we can conclude that is then the time at which the bubble is born.

We illustrate this example in Figure 1 below. Before the stopping time occurs the price process and the fundamental value are equal. The fundamental value drops immediately to when happens.

Appendix A Super-replication Theorems

For sake of completeness we provide the super-replication theorems (Theorem 1.4, Theorem 1.5) of [49]. Note that Theorem 1.5 of [49] coincides with Theorem 4.1 of [11].

Theorem A.1 (Theorem 1.5, [49]).

Let Assumption 2 hold. We consider a contingent claim which pays many units of the bond and many units of the risky asset at time . The random variable is assumed to satisfy

for some . Then the following assertions are equivalent

-

(i)

There is a self-financing trading strategy with on and which is admissible in a numéraire-free sense.

-

(ii)

For every we have

(A.1)

Theorem A.2 (Theorem 1.4, [49]).

Let Assumption 1 hold. We consider a contingent claim which pays many units of the bond and many units of the risky asset at time . The random variable is assumed to satisfy

| (A.2) |

for some . Then the following assertions are equivalent:

-

(i)

There is a self-financing trading strategy on with on and which is admissible in a numéraire-based sense.

-

(ii)

For every we have

(A.3)

Acknowledgement

We would like to thank Martin Schweizer for helpful remarks and insightful discussions.

References

- [1] Abreu, D., and Brunnermeier, M. K. Bubbles and crashes. Econometrica 71, 1 (2003), 173–204.

- [2] Allen, F., and Gorton, G. Churning bubbles. The Review of Economic Studies 60, 4 (1993), 813–836.

- [3] Allen, F., Morris, S., and Postlewaite, A. Finite bubbles with short sale constraints and asymmetric information. Journal of Economic Theory 61, 2 (1993), 206–229.

- [4] Ansel, J.-P., and Stricker, C. Couverture des actifs contingents et prix maximum. Annales de l’IHP Probabilités et Statistiques 30, 2 (1994), 303–315.

- [5] Anthony, J., Bijlsma, M., Elbourne, A., Lever, M., and Zwart, G. Financial transaction tax: review and assessment. CPB Netherlands Bureau For Economic Policy Analysis. CPB Discussion Paper (2012).

- [6] Bayraktar, E., and Yu, X. On the market viability under proportional transaction costs. Mathematical Finance 28, 3 (2018), 800–838.

- [7] Biagini, F., Föllmer, H., and Nedelcu, S. Shifting martingale measures and the birth of a bubble as a submartingale. Finance and Stochastics 18, 2 (2014), 297–326.

- [8] Biagini, F., and Mancin, J. Financial asset price bubbles under model uncertainty. Probability, Uncertainty and Quantitative Risk 2, 14 (2017).

- [9] Biagini, F., Mazzon, A., and Meyer-Brandis, T. Liquidity induced asset bubbles via flows of elmms. SIAM Journal on Financial Mathematics 9, 2 (2018), 800–834.

- [10] Biagini, F., and Nedelcu, S. The formation of financial bubbles in defaultable markets. SIAM Journal on Financial Mathematics 6, 1 (2015), 530–558.

- [11] Campi, L., and Schachermayer, W. A super-replication theorem in kabanov’s model of transaction costs. Finance and Stochastics 10, 4 (2006), 579–596.

- [12] Cox, A. M., and Hobson, D. G. Local martingales, bubbles and option prices. Finance and Stochastics 9, 4 (2005), 477–492.

- [13] Cvitanić, J., and Karatzas, I. Hedging and portfolio optimization under transaction costs: A martingale approach. Mathematical Finance 6, 2 (1996), 133–165.

- [14] De Long, J. B., Shleifer, A., Summers, L. H., and Waldmann, R. J. Noise trader risk in financial markets. Journal of political Economy 98, 4 (1990), 703–738.

- [15] De Long, J. B., Shleifer, A., Summers, L. H., and Waldmann, R. J. Positive feedback investment strategies and destabilizing rational speculation. the Journal of Finance 45, 2 (1990), 379–395.

- [16] Delbaen, F., and Schachermayer, W. A general version of the fundamental theorem of asset pricing. Mathematische Annalen 300, 1 (1994), 463–520.

- [17] Dellacherie, C., and Meyer, P.-A. Probabilities and Potential, vol. 29 of North-Holland Mathematics Studies. North-Holland Publishing Co., Amsterdam, 1978.

- [18] Dellacherie, C., and Meyer, P.-A. Probabilities and Potential B, vol. 72 of North-Holland Mathematics Studies. North-Holland Publishing Co., Amsterdam, 1982.

- [19] El Karoui, N., and Quenez, M.-C. Dynamic programming and pricing of contingent claims in an incomplete market. SIAM Journal on Control and Optimization 33, 1 (1995), 29–66.

- [20] Föllmer, H., and Protter, P. Local martingales and filtration shrinkage. ESAIM: Probability and Statistics 15 (2011), 25–38.

- [21] Föllmer, H., and Schied, A. Stochastic finance: an introduction in discrete time. Walter de Gruyter, 2011.

- [22] Gerding, E. F. Laws against bubbles: An experimental-asset-market approach to analyzing financial regulation. Wisconsin Law Review 977 (2007).

- [23] Gerding, E. F. Law, bubbles, and financial regulation. Routledge, 2013.

- [24] Guasoni, P., and Rásonyi, M. Fragility of arbitrage and bubbles in local martingale diffusion models. Finance and Stochastics 19, 2 (2015), 215–231.

- [25] Guasoni, P., Rásonyi, M., and Schachermayer, W. Consistent price systems and face-lifting pricing under transaction costs. The Annals of Applied Probability 18, 2 (2008), 491–520.

- [26] Guasoni, P., Rásonyi, M., and Schachermayer, W. The fundamental theorem of asset pricing for continuous processes under small transaction costs. Annals of Finance 6, 2 (2010), 157–191.

- [27] Harrison, J. M., and Kreps, D. M. Speculative investor behavior in a stock market with heterogeneous expectations. The Quarterly Journal of Economics 92, 2 (1978), 323–336.

- [28] Herdegen, M., and Schweizer, M. Strong bubbles and strict local martingales. International Journal of Theoretical and Applied Finance 19, 04 (2016), 1650022–1–44.

- [29] Heston, S. L., Loewenstein, M., and Willard, G. A. Options and bubbles. The Review of Financial Studies 20, 2 (2006), 359–390.

- [30] Jarrow, R., Kchia, Y., and Protter, P. How to detect an asset bubble. SIAM Journal on Financial Mathematics 2, 1 (2011), 839–865.

- [31] Jarrow, R., Protter, P., and Shimbo, K. Asset price bubbles in a complete market. Advances in Mathematical Finance 28 (2006), 105–130.

- [32] Jarrow, R. A. Asset price bubbles. Annual Review of Financial Economics 7 (2015), 201–218.

- [33] Jarrow, R. A., and Protter, P. Forward and futures prices with bubbles. International Journal of Theoretical and Applied Finance 12, 07 (2009), 901–924.

- [34] Jarrow, R. A., and Protter, P. Foreign currency bubbles. Review of Derivatives Research 14, 1 (2011), 67–83.

- [35] Jarrow, R. A., Protter, P., and Roch, A. F. A liquidity-based model for asset price bubbles. Quantitative Finance 12, 9 (2012), 1339–1349.

- [36] Jarrow, R. A., Protter, P., and Shimbo, K. Asset price bubbles in incomplete markets. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics 20, 2 (2010), 145–185.

- [37] Kabanov, Y., and Safarian, M. Markets with transaction costs: Mathematical Theory. Springer Science & Business Media, 2009.

- [38] Kabanov, Y. M. Hedging and liquidation under transaction costs in currency markets. Finance and Stochastics 3, 2 (1999), 237–248.

- [39] Kabanov, Y. M., and Last, G. Hedging under transaction costs in currency markets: a continuous-time model. Mathematical Finance 12, 1 (2002), 63–70.

- [40] Kabanov, Y. M., and Stricker, C. Hedging of contingent claims under transaction costs. In Advances in finance and stochastics. Springer, 2002.

- [41] Kaizoji, T., and Sornette, D. Bubbles and crashes. Encyclopedia of quantitative finance (2010).

- [42] Kramkov, D. O. Optional decomposition of supermartingales and hedging contingent claims in incomplete security markets. Probability Theory and Related Fields 105, 4 (1996), 459–479.

- [43] Levitin, A. J., and Wachter, S. M. Explaining the housing bubble. Geo. LJ 100 (2011), 1177.

- [44] Loewenstein, M., and Willard, G. A. Rational equilibrium asset-pricing bubbles in continuous trading models. Journal of Economic Theory 91, 1 (2000), 17–58.

- [45] Protter, P. Stochastic differential equations. Springer, Berlin, Heidelberg, 2005.

- [46] Protter, P. A mathematical theory of financial bubbles. Paris-Princeton Lectures on Mathematical Finance 2081 (2013), 1–108.

- [47] Reitsam, T. Asset price bubbles in market models with proportional transaction costs. PhD thesis, work in progress.

- [48] Schachermayer, W. Admissible trading strategies under transaction costs. Séminaire de Probabilités XLVI (2014), 317–331.

- [49] Schachermayer, W. The super-replication theorem under proportional transaction costs revisited. Mathematics and Financial Economics 8, 4 (2014), 383–398.

- [50] Schachermayer, W. Asymptotic theory of transaction costs. European Mathematical Society, 2017.

- [51] Schatz, M., and Sornette, D. Inefficient bubbles and efficient drawdowns in financial markets. Swiss Finance Institute Research Paper, 18-49 (2019).

- [52] Scheinkman, J. A., and Xiong, W. Overconfidence and speculative bubbles. Journal of political Economy 111, 6 (2003), 1183–1220.

- [53] Shiller, R. J. Irrational exuberance: Revised and expanded third edition. Princeton university press, 2015.

- [54] Shleifer, A. Inefficient markets: An introduction to behavioural finance. OUP Oxford, 2000.

- [55] Shleifer, A., and Summers, L. H. The noise trader approach to finance. Journal of Economic perspectives 4, 2 (1990), 19–33.

- [56] Shleifer, A., and Vishny, R. W. The limits of arbitrage. The Journal of finance 52, 1 (1997), 35–55.

- [57] Sornette, D. Critical market crashes. Physics Reports 378, 1 (2003), 1–98.

- [58] Šperka, R., and Spišák, M. Transaction costs influence on the stability of financial market: agent-based simulation. Journal of Business Economics and Management 14, sup1 (2013), 1–12.

- [59] Strasser, E. Necessary and sufficient conditions for the supermartingale property of a stochastic integral with respect to a local martingale. Séminaire de Probabilités XXXVII (2003), 385–393.

- [60] Xiong, W. Bubbles, crises, and heterogeneous beliefs. Tech. rep., National Bureau of Economic Research, 2013.