Collectivised Pension Investment with Homogeneous Epstein–Zin Preferences

Abstract

In a collectivised pension fund, investors agree that any money remaining in the fund when they die can be shared among the survivors.

We compute analytically the optimal investment-consumption strategy for a fund of identical investors with homogeneous Epstein–Zin preferences, investing in the Black–Scholes market in continuous time but consuming in discrete time. Our result holds for arbitrary mortality distributions.

We also compute the optimal strategy for an infinite fund of investors, and prove the convergence of the optimal strategy as . The proof of convergence shows that effective strategies for inhomogeneous funds can be obtained using the optimal strategies found in this paper for homogeneous funds, using the results of [2].

We find that a constant consumption strategy is suboptimal even for infinite collectives investing in markets where assets provide no return so long as investors are “satisfaction risk-averse.” This suggests that annuities and defined benefit investments will always be suboptimal investments.

We present numerical results examining the importance of the fund size, , and the market parameters.

Introduction

A group of individuals may group together and invest income for their retirement in a collective fund. When an individual dies, any funds associated with that individual are then divided among the survivors. The paper [2] shows how to model the management of these funds mathematically and argues that they should yield significantly better results for investors than traditional pension investment models.

This paper complements [2] by computing the optimal investment strategy for collective investment under the following assumptions:

-

(i)

There are identical investors in the collective.

-

(ii)

The fund may invest in continuous time in a Black–Scholes–Merton market with one risky asset.

-

(iii)

The mortality of the individuals is independent: that is there is no systematic longevity risk. Mortality occurs with a known probability distribution.

-

(iv)

The preferences of each individual are given by homogeneous Epstein–Zin preferences with mortality (as defined in [2]).

-

(v)

Consumption occurs in discrete time (for example once per year).

We formulate the problem mathematically and are able to give analytical formulae for the optimal consumption and investment at each time.

Assumption (i), that the investors are identical, is not a significant restriction. The paper [2] shows that once one knows how to manage a fund of identical individuals, it is easy to devise very effective management strategies for inhomogeneous funds, i.e. funds of diverse individuals.

Assumption (ii), that the market is a Black–Scholes–Merton market is, of course, restrictive. This is the simplest type of market we could consider. We are trading full realism for analytic tractability. The assumption that the market has only one risky asset is not restrictive. It follows from the mutual fund theorem arguments of [1] that essentially the same strategy can be used in a Black–Scholes–Merton market with stocks.

Assumption (iv), that the preferences are given by homogeneous Epstein–Zin utility, is a central assumption to this paper, and is key to the analytic tractability of the problem. We consider different possible models for preferences over consumption with mortality in [2] and find that two models stand out as having particularly attractive properties. These models are called homogeneous Epstein–Zin preferences and exponential Kihlstrom–Mirman preferences in [2] and we will use the same terminology. As the results of this paper demonstrate, homogeneous Epstein–Zin preferences have the tremendous advantage of being analytically tractable. This stems from the homogeneity property of these preferences. By contrast, we can only expect to solve analogous problems with exponential Kihlstrom–Mirman preferences using numerical methods (we show how to do this in [3]). It is possible to define inhomogeneous Epstein–Zin preferences with mortality (see [2]). We believe that the techniques of [3] could be applied to such problems, but that one cannot, in general, expect analytical results without homogeneity.

Assumption (v), that consumption occurs in discrete time is not a significant restriction. Indeed one might argue it adds to the realism of the model.

The apparent mismatch between discrete time consumption and continuous time investment is the key technical trick required to obtain our analytic results. As is explained in [1], the Black–Scholes–Merton market is isomorphic to a linear market in continuous time and this explains the analytic tractability of many problems involving this market. However, in discrete time the Black–Scholes–Merton market is fundamentally non-linear, and this explains the analytic intractability of problems such as Merton’s investment problem in discrete time. We deduce that we must allow continuous time investment to obtain analytic results.

On the other hand, if we are to allow arbitrary mortality distributions and continuous time consumption, then there is no hope of obtaining analytic results as one wouldn’t even be able to write down the mortality distribution in general. Our assumption of discrete time consumption is essentially equivalent to assuming that mortality occurs in discrete time, and so restricts the set of mortality distributions we are considering to ensure tractability.

The advantage of analytic tractability is the insight it gives us into optimal pension investment.

For example, we can analyse how consumption varies over time. We find that except for very special cases, constant consumption is never optimal. This is interesting because many people see a defined-benefit pension which provides constant real-terms income as the “gold standard” for a pension fund. Our result shows that chasing constant income is, in fact, suboptimal.

It perhaps isn’t so surprising that if market returns are non-zero there are advantages to taking some risk by investing in equities.

Nor should it be surprising that delaying consumption to benefit from market returns can also be advantageous. We are able to make this precise by computing the elasticity of intertemporal substitution in our model.

It is perhaps, surprising that even if one assumes that both equities and bonds provide no return, it is still not optimal to receive a constant income, if one is satisfaction risk-averse (see below for a definition). Under these circumstances it can be optimal to spend earlier (if the primary risk one perceives is the risk of dying before one can consume one’s pension) or to spend later (if the primary risk one perceives is the risk of living for a long time on an inadequate pension).

Let us now describe the structure of the paper.

Section 1 reviews the definition of homogeneous Epstein–Zin preferences with mortality.

Section 2 states the optimal investment problems we will solve. The problem depends upon the number of individuals . We will also state an investment problem for a fund which is intended to represent the limiting case .

Section 3 solves the optimal investment problems analytically in the cases where and .

Section 4 computes how consumption and wealth vary over time, giving analytic descriptions of their probability distributions.

Section 5 generalizes the results to arbitrary fund sizes .

Section 6 uses our results to provide a rigorous justification for the claim that our models for finite converge to the case . This is of obvious theoretical interest in its own right, but we remark that the proof is essential to demonstrating that the strategies for inhomogeneous funds of described in [2] will be effective.

1 Homogeneous Epstein–Zin utility with mortality

Let us recall the definition of homogeneous Epstein–Zin utility with mortality given in [2]. In order to give a crisp definition, we first define a convention for how we will we handle algebra using infinite and infinitesimal values.

Definition 1.1.

The extended positive reals is the set

where is a symbol representing an infinitesimal value. We extend addition, multiplication and raising to a real power to in the obvious way:

We now assume that we are given a time grid where is some initial time, is a fixed time step and is the time by which we assume mortality is certain.

We will model the individual’s consumption as a non-negative stochastic process in a filtered probability space . The time of death is a stopping time taking values in . Our convention is that any consumption up to and including time may effect the individual’s utility, but any consumption occurring after time will be ignored.

Definition 1.2.

Homogeneous Epstein–Zin utility with mortality is defined for a non-negative consumption process and a stopping time taking values in . It depends on parameters , , and . It is the -valued random process defined recursively by

| (1.1) |

2 The optimal investment problem

A general optimal investment problem for a homogeneous collective fund was described mathematically in [2]. In this section we summarize the formulation of [2], specializing to the case of interest for this paper.

We model a collective fund of investors. The fund may invest in either a riskless bond which grows at a risk-free rate of or in a stock whose price at time , is denoted . The stock price at time is given. At subsequent times obeys the SDE

| (2.1) |

for a constant drift and volatility , and a -dimensional Brownian motion .

We will model consumption taking place in discrete time on a grid as described in the previous section. Since we are modelling consumption in discrete time, we may safely model mortality in discrete time. We let be a random variable modelling the time of death of a representative individual. We assume that has a probability distribution given by where is the measure given by adding the Dirac measures associated to the grid points of .

Let denote the survival probability between times and . That is

| (2.2) |

Write for the number of individuals individuals with a time of death greater than or equal to . The process is a Markov process, with initial value . Note, however, that will be measurable. We choose this convention for as it works well with our existing convention that individuals who die at age still consume at time .

For the case of a finite number of individuals, the transition probability of moving from a value of at time to the value at time is given by

| (2.3) |

We also wish to write down a formal optimal investment problem for the case of a fund with investors. In this case we will define for all times up to .

We will write for proportion of the fund invested in stock at time . We will write for the value of the fund per survivor at time before consumption. We will define if . Similarly, we will write for the value of the fund per survivor after consumption. We note that at time points . At intermediate times, , obeys the SDE

with initial condition given by the budget equation

| (2.4) |

unless in which case we define to be zero on . Note that this formula is based on our convention that an individual who dies at a time still consumes at that time and the corresponding convention for which ensures is measurable.

Let denote the time of death of individual .

For finite we let be the filtered probability space generated by and the time of death variables . We define to be the time of death variable for one specific individual whose time of death is greater than or equal to .

For we let be any random variable with the distribution . We let be the filtered probability space generated by and .

Let denote the space of admissible controls : that is -predictable processes such that and with . We define the value function of our problem starting at time to be

| (2.5) |

where is an Epstein–Zin utility function.

3 The cases and

To highlight the key ideas we will consider only the case when and in this section, leaving the case of general until Section 5. We define to distinguish these cases as follows

| (3.1) |

We write so that the positive-homogeneity of implies that

| (3.2) |

We note that we have not yet shown whether is finite, but equation (3.2) can still be interpreted for infinite values of .

Let denote the consumption rate at time , so for an individual who is still alive at time . The budget equation (2.4) can then be written as

| (3.3) |

We now let be the set of random variables representing the value of our investments at time that can be obtained by a continuous time trading strategy with an initial budget given by (3.3) with . Thus is the set of admissible investment returns given the budget and the consumption.

The Markovianity of Epstein–Zin preferences and the definition of to compute allow us to apply the dynamic programming principle to compute

| (3.4) |

The second line follows from the first by the positive homogeneity of Epstein–Zin utility (3.2).

If , we may compute the value of

by solving the Merton problem for optimal investment over time period , with initial budget , no consumption, and terminal utility function .

We find

| (3.5) |

where

| (3.6) |

For details see Merton’s paper [6] or [9] equations (3.47) and (3.48). Moreover the proportion invested in stock is given by which is a constant determined entirely by and the market. In the case where we must instead compute

However, apart from the change of a to an everything is algebraically identical, so the same formulae emerge.

Putting the value (3.5) into our expression (3.4) for the value function we obtain

| (3.7) |

where the last line follows from the budget equation (3.3). We define

| (3.8) |

so that (3.7) may be written as

| (3.9) |

Differentiating the expression in square brackets on the right-hand side, we see that the supremum is achieved in equation (3.7) when , where satisfies

or, if this yields a negative value for , we should take . Simplifying we must have

| (3.10) |

So

| (3.11) |

This expression for is non-negative, so it always gives the argument for the supremum in (3.7). We obtain

We conclude that

| (3.12) |

where is given by equation (3.8). We observe also that equation (3.11) for the optimal consumption rate per survivor simplifies to

| (3.13) |

We summarize our findings below.

Theorem 3.1 (Optimal investment with Epstein–Zin preferences).

Suppose that an individual has probability of dying in the interval . Individuals consume at fixed time points . By the time , death is certain. Between time points, we may trade in the Black–Scholes–Merton market (2.1). Let if we are interested in optimizing the consumption of an individual and if we are interested in the collectivised problem. The utility of each individual is given by Epstein–Zin utility of the form (1.1). Then

-

(i)

The optimal proportion of stock investments is determined entirely by the monetary-risk-aversion and the market. In particular it is independent of time and wealth. It is given by the value given in equation (3.6).

- (ii)

-

(iii)

The consumption for each survivor at time is given by where is given by (3.13).

4 Consumption over time

It is interesting to see how wealth and the consumption per individual vary over time.

Theorem 4.1.

Under the same conditions as 3.1, the optimal fund value per survivor at time , , follows a log normal distribution. Write and for the mean and standard deviation of so that

| (4.1) |

The standard deviation is given by

| (4.2) |

where is given by (3.6). The mean satisfies the difference equation

| (4.3) |

where is given by (3.12) and where we define by the same formula used to define but with set to zero, i.e.

| (4.4) |

The optimal consumption per survivor at time is also log normally distributed with

| (4.5) |

The mean of the log consumption per survivor satisfies the equation

| (4.6) |

where is given by equation (3.8).

Proof.

We suppose as induction hypothesis that the distribution of is as described at time .

The budget equation (3.3) then tells us that the wealth per survivor after consumption, , satisfies

Hence

Our investment strategy from to is a continuous time trading strategy where we hold a fixed proportion of our wealth in stocks at all time. So, in the interval , satisfies the SDE

By Itô’s lemma we find

| (4.7) |

We deduce that conditioned on the value of will follow a normal distribution with mean and standard deviation . Moreover the random variable is independent of .

The sum of independent normally distributed random increments yields a new normally distributed random variable, and one can compute the mean and variance by adding the mean and variance of the increments. Hence

where

| (4.8) |

and

| (4.9) |

Solving the recursion (4.9) yields equation (4.2). The result for now follows by induction.

To interpret Theorem 4.1 we specialize to the case of a market where and to preferences with . This represents the problem of consuming a fixed lump sum over time when there is no inflation but also no investment opportunities. While not financially reasonable, this problem highlights how longevity risk affects consumption, when considered in isolation from market risk.

In this case is a deterministic function. We find from equations (4.6) and (3.8) that

| (4.10) |

We note that is a non-zero probability, so . We may use equation (4.10) to compute whether increases or decreasing over time. We summarize the results in Table 1.

Perhaps surprisingly, we find that sometimes consumption increases over time rather than decreases. In the collectivised case, this can be explained by the fact that the pension will always be inadequate when . We say that a pension is inadequate if living an extra year on that pension decreases utility. If , living longer is considered negative by homogeneous Epstein–Zin preferences, so we may wish to compensate individuals who have the misfortune to live longer. We cannot identify these individuals in advance, so the only way to provide this compensation is to increase consumption over time. Thus the increasing consumption arises from the fact that when , the primary risk is the inadequacy of the pension, when , the primary risk is dying young. We believe that this mixing of the notion of pension adequacy with the risk aversion parameter is a significant shortcoming of homogeneous Epstein–Zin preferences. It is the price one must pay for analytic tractability.

In the individual case, the concern that one will die young is much more serious. This is why for the individual problem, the fear of an inadequate pension only dominates when both and .

The case when corresponds to the case of standard von-Neumann Morgernstern preferences, in which case constant consumption is optimal in the collectivised case as was proved in [2].

More significantly, our result also shows the converse. Constant consumption from one period to the next is only optimal if and only if either (i) the survival probability is one, or (ii) so one is satisfaction risk-neutral. Hence, even ignoring market effects constant consumption will be suboptimal for any realistic parameter choices.

We have not shown the case in Table 1 as in this case one has monetary-risk-aversion but not satisfaction-risk-aversion. We found the resulting behaviour to be difficult to interpret as rational, cautious (as understood intuitively) strategies. We see this simply as a evidence that satisfaction-risk-aversion is the correct operationalization of the intuitive notion of risk-aversion.

| Collectivised | Individual | |

|---|---|---|

| Increasing | Decreasing | |

| Increasing | Increasing | |

| Decreasing | Decreasing | |

| Constant | Decreasing | |

| Constant | Decreasing |

It is also interesting to calculate how consumption changes according to the available investment opportunities. If interest rates increase one may choose to defer consumption to a later date to benefit from the increased rate. To quantify this behaviour one wishes to calculate the elasticity of intertemporal substitution which is defined as follows.

Definition 4.2.

The elasticity of intertemporal substitution at time is defined to be

When is deterministic, this definition corresponds with the standard definition [5].

Theorem 4.1 allows us to calculate this elasticity.

Corollary 4.3.

For the optimal investment strategy of Theorem (3.1) we have

If this simplifies to

In the case of von Neumann-Morgernstern utility we have

5 General finite collectives

Let be the value function (2.5) for the optimal investment problem for individuals with homogeneous Epstein–Zin preferences. By positive homogeneity we may define , so that .

Let denote the event that both

-

(i)

there are survivors at time , i.e. .

-

(ii)

the individual whose utility we wish to calculate is one of those survivors, so .

Recall that denotes the value of the fund per survivor at time before consumption and mortality.

Hence

We now let be the set of random variables representing the value of the fund per survivor at time before consumption that can be obtained by a continuous time trading strategy given initial capital per survivor when . Writing for the rate of consumption and using the dynamic programming principle we find

We used positive homogeneity to obtain the last line. The argument of Section 3 tells us how to optimize over . Hence we find

where is as defined in equation (3.6). The optimal investment policy is also described in equation (3.6), and as before it depends only on the market and the monetary-risk-aversion parameter .

We may rewrite our expression for as follows:

| (5.2) |

where

| (5.3) |

Equation (5.2) is structurally identical to equation (3.9). Hence from equation (3.12) we may deduce similarly that

| (5.4) |

We state our results as a theorem.

Theorem 5.1.

Let denote the optimal Epstein–Zin utility, (2.5), for a collective of individuals investing an amount at time . The collective is allowed to invest in the Black–Scholes–Merton market (2.1) in continuous time. Individuals have independent mortality, with survival probability given by (2.2). Then equations (5.4) and (5.3) together with the initial condition allow us to compute the optimal Epstein–Zin utility by recursion. The value of is given in equation (3.6) and the value of is given in equation (2.3)

6 Convergence of as

In this section we will analyse the behaviour as to prove the following.

Theorem 6.1.

Let denote the maximum Epstein–Zin utility at time for the infinitely collectivized case then

Our proof strategy will be to approximate an expectation involving the binomial distribution with a Gaussian integral which we can then estimate using Laplace’s method. To get a precise convergence result, we need some estimates on the rate of convergence in the Central Limit Theorem. The estimates given in [4] suit our purposes well. For the reader’s convenience we will summarize the result we will need.

We begin with some definitions. A random variable is said to satisfy Cramér’s condition if its characteristic function satisfies

| (6.1) |

for all positive . Let be the standard normal distribution. Given a set , and a function , is defined to equal

The set is the ball of radius around .

Let be the appropriately normalized -th partial sum of a sequence of independent identically distributed random variables for which Cramér’s condition holds and which have finite moments have all orders. Appropriately normalized means normalized such that the central limit theorem implies converges to in distribution. Then there exists a constant such that for any bounded measurable function

| (6.2) |

The full result given in [4] is more general and more precise than we need. Let us explain how the statements are related. We have simplified our statement to the one-dimensional case, we have assumed the are identically distributed and we have assumed all moments of exist. The statement in [4] is therefore more complex, and in particular involves additional terms called defined in the one-dimensional case by

where

Our assumptions on guarantee that is independent of and so we have been able to absorb these terms into the constant . In addition, our statement uses Theorem 1 of [4], together with remarks at the end of the second paragraph on page 242 about Cramér’s condition.

We are now ready to prove the desired convergence result.

Proof of Theorem 6.1.

We proceed by a backward induction on . The result is trivial for the case . We now assume the induction hypothesis

We wish to compute , but only the sum in the expression (5.3) is difficult to compute. We will call this sum , so

| (6.3) |

Heuristically, one can approximate with a Gaussian integral using the Central Limit Theorem and then apply Laplace’s method to compute the limit as . This motivates the idea of decomposing the sum above into a “left tail” for small values of , a central term for values of near the mean of the Binomial distribution , and a “right tail” for larger values of . We will in fact bound the tails separately (Steps 1 and 2, below), and then we will be able to rigorously apply a Central Limit Theorem argument to the central term (Step 3).

We compute

| (6.4) |

We note that

So we define an integer by

and then equation (6.4) will ensure that we have exponential decay of as decreases

| (6.5) |

Step 1. We can now estimate the left tail of (6.3). There exists a constants , such that

| (6.6) |

To estimate this term, we observe that

Hence by equations (6.4) and (6.6) we find

which decays exponentially as . Our induction hypothesis ensures that the are bounded, so we may safely conclude that

| (6.7) |

Step 2. We apply the same strategy to the right tail. This time we compute

we define

to ensure that

Repeating the same argument as for the left tail tells us that

| (6.8) |

We note that is monotonic in and that and tend to finite, non-zero limits as . We deduce that there exists a constant such that

| (6.9) |

This implies that

Using this together with our induction hypothesis, we may obtain from (6.8) that

| (6.10) |

Step 3. In order to apply the bound (6.2), we define a Bernoulli random variable which takes the value if the -th individual survives at time and otherwise. Thus is the probability that . We define scaled random variables of mean and standard deviation by

and so the appropriately scaled partial sum is given by

We now wish to rewrite (6.10) as an integral.

We make the substitution to find

| (6.11) |

We may rewrite this as

| (6.12) |

where

From our expressions for and one readily sees that tends to at a rate proportional to as . Likewise tends to at a rate as . We will assume that is large enough to ensure that .

Let us define by

| (6.13) |

By (6.9), is bounded by a constant independent of . Hence is bounded independent of . We can bound the derivative of inside the interval , independent of . Hence for any and for sufficiently large , for some constant independent of . It follows that

| (6.14) |

Since tends to at a rate proportional to , since is bounded, and since the normal distribution has super-exponential decay in the tails, we have

| (6.15) |

and similarly

| (6.16) |

Estimates (6.14), (6.15), (6.16) together with the bound on allow us to apply the Central Limit Theorem estimate (6.2) to (6.12). We note that Cramér’s condition holds. The result is

We now apply Laplace’s method to estimate this Gaussian integral (see Proposition 2.1, page 323 in [10] ) and obtain

From the definition of in equation (5.3) and our definition of in (6.3) we obtain

We may now compare this with the definition of given in (3.8) for the infinitely collectivised case . We see that in this case

It now follows from the recursion relations for and (given in (3.12) and (5.4) respectively) together with our induction hypothesis that

This completes the induction step and the proof. ∎

7 Numerical Results

We illustrate our results with some numerical examples. We will restrict our attention to the case of von Neumann–Morgernstern preferences in this section. We refer the reader to the numerical results of [2] where we give numerical results for more general homogeneous Epstein–Zin preferences. In that paper we also compare the results with those obtained using exponential Kihlstrom–Mirman preferences.

For ease of comparison with [2] (and other pension models based on [8]) we choose the parameter values given in Table 2. Due to the positive homogeneity of our model, the choice of value for is unimportant.

| Parameter | Value |

|---|---|

The mortality distribution we use is for women retiring at age 65 in 2019. We obtained this distribution using the model “CMI_2018_F [1.5%]” as described in [7].

We define the annuity equivalent value of each investment-consumption approach. We define this to be the price of an annuity which would give the same gain. We define the annuity outperformance by

This gives a measure of the performance of the strategy relative to an annuity of the same cost.

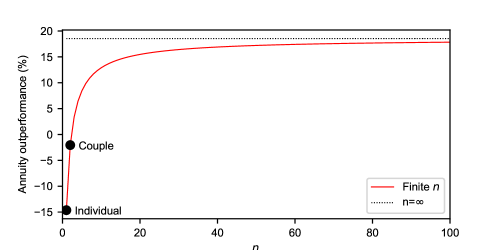

7.1 Dependence on the number of individuals,

In Figure 1 we show how the annuity outperformance depends upon the number of individuals in the collective. This plot shows that as few as individuals are required to obtain most of the benefits of collectivisation. One does not need a large fund to benefit from a collective investment: simply sharing risk with one’s partner brings a substantial benefit.

7.2 Dependence on market parameters

To compare the relative impact of investment in the stock market, inter-temporal substitution and collectivisation we have computed the annuity outperformance for a number of different fund and market scenarios. The results are shown in Table 3. Except where the table indicates a difference, the parameter values are described in the previous section.

| Scenario | Annuity outperformance | |||

|---|---|---|---|---|

| 1 | ||||

| 2 | ||||

| 3 | ||||

| 4 |

If scenarios and have an annuity outperformance of and then we will say that scenario gives an improvement of

over scenario .

So comparing Scenario 1 with Scenario 2 we see that the impact of collectivisation in this example is an improvement of . Comparing Scenarios and , the impact of investing in stock, rather than just bonds, is even more significant, yielding an almost improvement. Comparing Scenarios and , we see that exploiting inter-temporal substitution alone yields a relatively modest improvement.

References

- [1] John Armstrong. Classifying markets up to isomorphism. arXiv preprint arXiv:1810.03546, 2018.

- [2] John Armstrong and Cristin Buescu. Collectivised pension investment. arXiv preprint arXiv:1909.12730, 2019.

- [3] John Armstrong and Cristin Buescu. Collectivised pension investment with exponential Kihlstrom–Mirman preferences. arXiv preprint arXiv:1911.02296, 2019.

- [4] R. N. Bhattacharya. Rates of weak convergence and asymptotic expansions for classical central limit theorems. The Annals of Mathematical Statistics, pages 241–259, 1971.

- [5] Robert E Hall. Intertemporal substitution in consumption. Journal of Political Economy, 96(2):339–357, 1988.

- [6] Robert C Merton. Lifetime portfolio selection under uncertainty: The continuous-time case. The Review of Economics and Statistics, pages 247–257, 1969.

- [7] Mortality Projections Committee. Working Paper 119. CMI Mortality Projections Model: CMI_2018. Continuous Mortality Investigation, Institute and Faculty of Actuaries, 2019.

- [8] Office of Budget Responsibility (OBR). Supplementary forecast information release: Long-term economic determinants – March 2019. Office of Budget Responsibility, 2019.

- [9] Huyên Pham. Continuous-time stochastic control and optimization with financial applications, volume 61. Springer Science & Business Media, 2009.

- [10] Elias M Stein and Rami Shakarchi. Complex analysis, volume 2. Princeton University Press, 2010.