Regression Discontinuity Design under Self-selection ††thanks: We would like to thank Zhuan Pei, Yanqing Fan, Peter Hull and participants in seminars and conferences at which this paper was presented. All remaining errors are ours.

Abstract

In Regression Discontinuity (RD) design, self-selection leads to different distributions of covariates on two sides of the policy intervention, which essentially violates the continuity of potential outcome assumption. The standard RD estimand becomes difficult to interpret due to the existence of some indirect effect, i.e. the effect due to self selection. We show that the direct causal effect of interest can still be recovered under a class of estimands. Specifically, we consider a class of weighted average treatment effects tailored for potentially different target populations. We show that a special case of our estimands can recover the average treatment effect under the conditional independence assumption per Angrist and Rokkanen (2015), and another example is the estimand recently proposed in Frölich and Huber (2018). We propose a set of estimators through a weighted local linear regression framework and prove the consistency and asymptotic normality of the estimators. Our approach can be further extended to the fuzzy RD case. In simulation exercises, we compare the performance of our estimator with the standard RD estimator. Finally, we apply our method to two empirical data sets: the U.S. House elections data in Lee (2008) and a novel data set from Microsoft Bing on Generalized Second Price (GSP) auction.

Keywords:

causal inference, regression discontinuity, weighted average treatment effect, inverse probability weighted estimator

1 Introduction

Regression discontinuity (RD) design is an important policy evaluation tool that has been widely used in empirical studies. Under the continuity assumptions (Lee, 2008), the RD design gives rise to many testable restriction similar to a randomized control trial, and it allows for the identification of causal effects (Hahn et al., 2001). Standard nonparametric tools like series expansion method or kernel regression method can be applied to estimate this quantity under this minimal assumption, see Imbens and Lemieux (2008) and Cattaneo and Escanciano (2017).

An implication of the continuity assumption is that the distribution of the covariates conditional on the assignment variable is continuous at the cutoff. To valid this assumption, a variety of statistical tests and nonparametric inference procedures have been proposed, including Cattaneo et al. (2015) and Canay and Kamat (2018). However, this assumption may not hold in many applications. In particular, we consider the following two motivating examples.

Example 1 (College scholarship).

Consider the classical scholarship example per Thistlethwaite and Campbell (1960). Students receive scholarships if their test score is higher than a threshold. The authors applied the RD framework to estimate the causal effect of the scholarship on student’s future education outcomes. In this example, the continuity assumption implies that the distributions of the covariate information for students whose score is just above and below the threshold are similar. However, if students are aware of this policy before they take the SAT exam, some of them may study harder to pass this threshold. As a result, students whose score is on two sides of the threshold may have distinct characteristics (e.g., gender).

Example 2 (Generalized Second Price (GSP) auction).

GSP is widely used by internet search engines like Google or Bing to allocate sponsored search advertisements. In reality, it is implemented through a reservation score system. Each bidder is assigned a score as a function of their bids and characteristics. The bidder’s advertisement is displayed if her score passes the reservation. However, due to design of the score system, bidders with low quality may be selected below the reservation score while bidders with high quality may be selected above the reservation score. Given that low quality bidders may have a high willingness to pay, we often observe the distribution of bids to be different on two sides of the reservation score. We will further elaborate this example in the real data analysis.

Due to different distributions of the covariates at the cutoff in these examples, the standard RD estimand is no longer valid. We show in those cases the standard RD estimand can be decomposed into a direct treatment effect and an indirect treatment effect. The indirect effect is due to the unbalanced covariates near the cut-off. For example, the policy intervention may result more boys than girls to receive scholarship. If in general boys perform different from girls in SAT test, the difference in SAT score due to gender will also be accounted into the standard RD estimand as if the policy intervention is selecting on genders. However as no direct causal mechanism is assumed between the unbalanced covariates and running variable, the selection could be generated due to an unknown equilibrium, completely reversed or purely spurious. For example, in a GSP auction, the reservation score is designed to separate the bidders by quality and in the meanwhile bidders may self-select such that low quality bidders may have incentive to bid higher. As a result, policy changes to move reservation score can be risky if the equilibrium between reservation score and quality of bidders are not disentangled.

In this paper, we propose a new framework to address this problem by adjusting unbalanced covariates due to self-selection. Consider the following sharp RD setup: is a binary treatment variable, and are the potential outcomes under and and is the running variable so that the treatment is fully determined by for a known threshold . In the classical RD framework, it is assumed that is continuous at for ; see Assumption 3. This essentially assumes away self-selection based on both observed and unobserved covariates. To account for the self-selection effect, we assume that further covariate information can be collected. In particular, we define and as the potential covariates with or without treatment. By using the potential “outcome” formulation, we allow the distribution of the covariates on two sides of the threshold to be different, i.e., discontinuity of the covariate distribution. By controlling all unbalanced covariates, we assume that is continuous in at the threshold; see Assumption 5. This is the main assumption made in this paper.

In the classical RD framework, the standard causal parameter of interest is the marginal treatment effect at the cutoff. In the presence of self-selection, the continuity assumption on may fail. Thus, the marginal treatment effect can be confounded by the discontinuity of the conditional mean of covariates at the cutoff, as seen in equation (2.4). In this paper, we propose a class of estimands for RD design in the framework of weighted average treatment effect (WATE). We show that our estimands can tease out the effect of discontinuity of the conditional distribution of covariates through re-weighting the marginal treatment effects. For instance, under the constant treatment effect model with unbalanced covariates, our estimands reduce to the direct treatment effect. One special case of our estimands is Frölich and Huber (2018). Another special case can be interpreted as the “global” average treatment effect (ATE) under the conditional independence assumption (CIA) as in Angrist and Rokkanen (2015). The CIA assumes that the treatment is mean independent of the running variable near the cutoff conditional on the covariates. Intuitively, after projecting the outcome variable onto a rich set of covariates (excluding running variable), the residual should not depend on the running variable and can be viewed as an experiment with randomly assigned treatment. We show that our method identifies ATE under CIA assumption, whereas the standard RD estimand remains a “local” treatment effect at the cutoff (Lee, 2008).

We further provide the nonparametric identification for our estimands and propose nonparametric estimators based on the inverse propensity score weighted (IPW) approach, see Horvitz and Thompson (1952) and Abadie and Imbens (2016). However, notice that the treatment assignment is degenerate with respect to the running variable. We get around this problem by considering the marginal effect of the treatment and re-weighting on the other covariates first. The kernel method is applied to estimate the conditional mean function. The consistency and asymptotic normality of the proposed estimator are established. We further extend our method to the fuzzy RD design where the treatment compliance is imperfect. Similarly, we provide the nonparametric identification of the causal effect under the fuzzy RD design, and propose a nonparametric estimator. The proposed estimator is similar to that of the local average treatment effect (LATE) in a fractional format but with numerator being adjusted to incorporate additional selections.

This work is connected to the growing literature on the RD design with covariates. In particular, two recent papers provide insightful guidance on the subject. Calonicoy et al. (2017) estimated the marginal treatment effect by a local linear regression with the linear-in-parameters specification for the covariates. The main advantage of their method is that the nonparametric estimation of is avoided. In another paper, Frölich and Huber (2018) proposed a fully nonparametric estimator of the marginal treatment effect by estimating nonparametrically. They allowed the conditional density of given to be discontinuous. Our work differs from the above papers by considering a different estimand that is less local under CIA and identifies the direct treatment effect under the constant treatment effect model. Unlike Calonicoy et al. (2017), we do not require the continuity of the conditional mean of given . Instead, our Assumption 5 is similar to assumption 1 (iv) in Frölich and Huber (2018) under the sharp RD design. The proposed IPW estimator is also different from the above regression based estimators.

The rest of the paper is organized as follows. In Section 2, we propose our new estimands in the form of weighted average treatment effects and establish its nonparametric identification. In Section 3, we propose a set of weighted local linear estimators. The theoretical properties are established in Section 4. In Section 5, we conduct simulation studies and also apply the method to two empirical data sets: the U.S. House elections data in Lee (2008) and a novel data set from Microsoft Bing on Generalized Second Price (GSP) auction. Finally, we consider the extension to the fuzzy RD case in Section 6. The proofs are deferred to the appendix.

2 Sharp RD Design

2.1 Problem Setup and Continuity Assumption

In the standard RD design setting, we observe i.i.d. random samples , where is the outcome variable of interest for the th sample, is the binary treatment variable, is the running variable and is the covariate. In the sharp RD design, the treatment is perfectly assigned through the running variable relative to a known cutoff . For example, we have

Adopting a potential outcome framework, we can write the observed outcome variable as

where and represent the potential outcomes without or with treatment. The average treatment effect is defined as . However, this estimand is not identifiable under the RD design as the treatment assignment is a deterministic function of . In this framework, Hahn et al. (2001), Lee (2008) and Cattaneo et al. (2015) showed that one can still identify the treatment effect at the cutoff

under the following continuity assumption.

Assumption 3 (Continuity Assumption of ).

are continuous in at .

This assumption implies that the conditional mean of the potential outcomes near the cutoff are similar. There is no discontinuity of the conditional mean functions at the cutoff. This assumption enables us to identify in the RD design. We refer to Hahn et al. (2001), Lee (2008) and Cattaneo et al. (2015) for further discussion on this assumption.

Now let us consider the case that additional covariates are observed. Denote

where and represent the potential covariates without or with treatment. In the presence of covariates , the causal parameter can be rewritten as

| (2.1) |

In a recent work, Calonicoy et al. (2017) proposed a kernel based estimator of by accounting for the additional covariates . In addition to the continuity Assumption 3, it is also assumed that for the consistency of the resulting kernel estimator, that is the potential covariates and have the same conditional mean at the cutoff .

However, in some applications we may observe , when self-selection based on the covariates exists. For example, consider the classical scholarship example. Students with SAT score higher than a threshold will receive scholarship. The treatment effect of interest is the effect of scholarship on the students’ first semester GPAs. If the cutoff is pre-released, it might be possible that students with some common characteristics (i.e. gender) may study harder to pass the bar. This leads to an ex-ante selection based on the covariates. Thus, one may observe that the conditional mean functions of given right below or above the threshold are different, i.e.,

| (2.2) |

The following simple lemma essentially says that the self-selection based on the covariates (i.e., eq 2.2) implies .

Lemma 4.

If is continuous at for , then

Proof.

By the continuity assumption on ,

and similarly . The lemma holds. ∎

The above lemma provides a convenient way to check whether holds in empirical studies. One may simply plot the observed covariates against and examine whether there is a discontinuity of the trend around . The method is applied in the real data analysis.

In the following, we investigate the consequence of . To be specific, we consider the following constant treatment effect model

| (2.3) |

for , where is an arbitrary continuous function. By (2.1), one can show that

| (2.4) |

The estimand can be decomposed into two terms. The first term represents the direct treatment effect after controlling the running variable and the covariates . The second term in the right hand side of (2.4) can be interpreted as the indirect effect of the policy due to the unbalanced covariates near the cutoff or self-selection, which is nonzero if and . In many applications, the direct treatment effect is usually more meaningful and interpretable than , as is confounded by the self-selection effect.

In this example, when the indirect effects in is assumed away by requiring the continuity of the conditional density of the covariates at the cutoff , the data around the cutoff can be viewed as a natural experiment and continuity on the covariates implies a balanced design for this experiment so that we can estimate a local average treatment effect. However when the self-selection exits, the experiment is no longer balanced and the average treatment effect will typically differ from the direct effect .

2.2 Weighted Average Treatment Effect

As seen in (2.4), if (i.e., the covariates are unbalanced at the cutoff) and , can be different from the causal parameter of interest. To overcome this difficulty, we propose a new class of causal parameters, called the weighted average treatment effect (WATE), which are defined as

| (2.5) |

where and denote different choices of weights to form the estimand, and and are the conditional density of and given . In order to interpret (2.5) as the WATE, we require the following normalization condition for and :

In particular, by choosing appropriate and , (2.5) can be interpreted as the average of the difference of the conditional mean functions corresponding to a target population. To see this, we consider the following examples. Denote

-

•

Average treatment effect over entire population:

where is the p.d.f of the covariates . In , we average the conditional mean difference over the entire population whose covariates follow from the marginal distribution . It is easy to see that WATE defined in (2.5) recovers by taking

-

•

Average treatment effect over locally untreated population:

In this causal parameter, we average the conditional mean difference over the untreated population right below the threshold whose covariates follow from the conditional distribution . Similarly, we obtain by taking

-

•

Average treatment effect over locally randomized population:

This is the estimand studied by Frölich and Huber (2018) in the sharp RD case. Under the proposed WATE framework, can be viewed as the average treatment effect over the population around the threshold which is randomized so that their covariates follow from and with equal probability. Similarly, we obtain by taking

-

•

Average treatment effect via classical RD estimand: We note that the proposed WATE reduces to the classical RD estimand (2.1) by taking . However, we note that unlike the previous three examples, may not be written as the average treatment effect over one well defined population. To see this, recall that when there exists self-selection, the conditional distributions and usually differ from each other. Then in (2.1) can be written as the difference of the average of over two populations (i.e., the population right below and above the threshold) with covariate distributions and respectively. This is the reason for which is confounded by the unbalanced covariates.

A summary of the first three estimands is provided in Table 1. In practice, which causal estimand in above examples to use should depend on the target population of interest and is often determined on a case-by-case basis. Indeed, our framework opens a door towards designing new causal parameters tailored to specific applications. For instance, similar to , one can define the average treatment effect over locally treated population i.e., . Since the goal of the paper is to deal with unbalanced covariates, to fix the idea we will mainly focus on the first three examples.

In the following, we comment on two properties of our estimands , and . First, under the constant treatment effect model (2.3), direct calculation shows that and thus equals to the direct treatment effect without any further assumption. In contrast, the classical RD estimand reduces to under the extra assumption that or .

Second, our estimand generalizes to the overall average treatment effect (ATE) under the conditional independence assumption (CIA) proposed by Angrist and Rokkanen (2015). Assume that are the pre-treatment covariates, i.e, . The CIA is defined as

| (2.6) |

which says that the potential outcomes are mean independent of the running variable conditional on the covariates. By controlling a rich set of covariates, CIA seems to be a reasonable assumption as the link between the running variable and outcomes can be blocked (Angrist and Rokkanen, 2015). Since the CIA (2.6) implies , our estimand reduces to

which is the overall ATE. In contrast,

remains a “local” treatment effect at the cutoff. It requires further conditions to generalize to the overall ATE. For instance, if the constant treatment assumption holds for some constant , then reduces to . Thus, the new estimand can represent a causal effect that is less local than the standard RD estimand .

| Estimand | ||||

2.3 Nonparametric Identification

In this subsection, we study the nonparametric identification of , and . Instead of Assumption 3, we impose the following continuity assumption.

Assumption 5 (Continuity Assumption of ).

are right and left continuous in at for any respectively.

Intuitively, this assumption says, once all unbalanced covariates are controlled, there is no further discontinuity between the running variable and outcomes at the threshold. This assumption is similar to assumption 1 (iv) in Frölich and Huber (2018) under the sharp RD design. In addition, this assumption is weaker than CIA, as (2.6) implies our Assumption 5 when the covariates are pre-determined.

The following theorem shows that is identifiable based on the distribution of the observed data under Assumption 5. In addition, and are identifiable under some extra continuity assumptions.

Theorem 6 (Nonparametric Identification).

Under Assumption 5, is identifiable:

where and . In addition, if is left continuous in at for any , then is identifiable:

where . Furthermore, if is right continuous in at for any , then is identifiable:

Proof.

To show the identifiability of , we note that Assumption 5 implies

By the definition of the potential outcome, we have for any . Thus,

Following the same step, we can show that

This implies is identifiable. To show is identifiable, similarly we have . In addition, by the left continuity of , we further have . Thus, we have

This implies is identifiable. The identifiability of follows from the same argument. This completes the proof. ∎

3 Nonparametric Estimation

In the causal inference literature, inverse propensity score weighting (IPW) is one of the most widely used tools to handle the unbalanced covariates in the treatment and control groups (Horvitz and Thompson, 1952). However, the standard IPW method is not directly applicable because in the sharp RD design the treatment assignment is a deterministic function of the running variable and thus the propensity score is degenerate. In this section, we propose a class of nonparametric estimators of , and by modifying the inverse propensity score weighting approach.

To motivate our nonparametric estimator, we consider the following notation. Denote by a function of the covariate to be chosen later, a symmetric kernel function and a bandwidth that shrinks to 0. The detailed conditions on the kernel function and bandwidth are deferred to the next section. Consider the following inverse weighted kernel estimator

| (3.1) |

for the estimand , where plays the same role as the propensity score in the IPW method. Since in the RD design the propensity score function is degenerate, in the following we will show that the choice of differs from the standard propensity score model. The rationale is to choose so that the estimator (3.1) is asymptotically unbiased,

| (3.2) |

Thus, it suffices to calculate the expectation of the kernel estimator as follows

| (3.3) |

where the first step follows from under and the last step follows from the definition . Thus, (3.3) implies

| (3.4) |

where the last step follows from the symmetry of the kernel function and can be made rigorous given the regularity conditions specified in the next section. Comparing with

we can see that (3.2) holds provided

| (3.5) |

where is the p.d.f of at . Following from the same argument, one can show that . In Table 1, we give the detailed expression of and for the proposed three estimands , and . Since the weight depends on the unknown density functions, we propose to estimate those densities by the following kernel estimators

| (3.6) |

| (3.7) |

| (3.8) |

where and are bandwidth parameters. Note that the kernel estimator is known to suffer from the curse of dimensionality and is only applicable when the dimension of is small. For the applications in which a large number of covariates can be collected, one may consider alternative parametric or semiparametric approaches for density estimation. In this work, we only focus on the above kernel estimators and leave the alternatives for future investigation.

Replacing the unknown density functions in and as shown in Table 1 with the corresponding kernel estimators, we can obtain and . While we can construct the final estimator by plugging into (3.1), for practical use and theoretical analysis we recommend the local linear estimator, since it has smaller asymptotic bias and better finite sample behavior near the boundary (Fan and Gijbels, 1996). Motivated by the formulation of the kernel estimator (3.1), we propose the following weighted local linear (WLL) estimator

| (3.9) |

Thus, we can estimate the WATE by

| (3.10) |

4 Theoretical Results

In this section, we study the asymptotic properties of the proposed estimator. We focus on the local linear estimator (3.9) for the estimand , due to the nice properties of as explained in Section 2.2. The analysis of the estimators for the other two estimands and is similar, but may require different technical conditions.

Let denote a small positive constant. For notational simplicity, define as the class of functions of and such that for any , is continuous, where . Here, the derivatives of with respect to at (say ) are interpreted as left derivatives. Similarly, we define as the class of functions of and such that for any , is continuous, where . The derivatives at correspond to the right derivatives. For simplicity, we only consider the case that . The generalization to multivariate covariates follows from the similar argument.

Assumption 7 (Smoothness condition).

Assume and . Denote for . Assume and .

Since the proposed method requires to estimate the unknown density functions and , we assume they are sufficiently smooth. In addition, we also need the smoothness of in order to study the local linear estimator (3.9). This assumption implies Assumption 5, which is required for identification purpose.

Assumption 8.

Assume the following conditions hold:

-

1.

such that and also has bounded support.

-

2.

The kernel is a non-negative, symmetric and bounded function with compact support which satisfies

The bivariate kernel is a product kernel , where satisfies the above conditions.

-

3.

is bounded way from 0 by a constant for and and is bounded way from 0 by a constant for and .

-

4.

for .

Assumption 8 has four parts. The first and second parts are standard assumptions in kernel density estimation problems. Since our RD estimator applies local linear estimators at the boundary, the uniform kernel or triangular kernel has been shown to have good performance under such scenario (Calonicoy et al., 2017). The third part requires and to be bounded away from 0 so that the inverse weights in the local linear estimator can be well controlled. This is similar to IPW estimator which requires the propensity score to be bounded away from 0. The last part assumes that the (homoscedastic) noise has finite variance.

Denote , and recall that . The main theorem in this section shows the rate of convergence of the local linear estimators and and their limiting distributions.

Theorem 1.

We note that from (4.1) the optimal choice of is of order and the corresponding convergence rate is due to the boundary effect. Specifically, the estimated weights and depend on the density estimators at the boundary. Since we only require and to be smooth from one side, the corresponding density estimators have a slower rate. So, the plug-in error becomes the dominant term when establishing the rate of . However, if are the pre-treatment covariates, i.e, , we can estimate the density by

| (4.2) |

The following corollary shows that in this case has an improved rate. With an optimal choice of the bandwidth parameters, we prove that , that is the boundary effect for estimating is automatically removed without applying any additional bias correction procedures.

5 Simulation and Empirical Examples

5.1 Simulation Study

In this first setting, consider the following data generating process:

where , , and are generated independently from distribution. The treatment is assigned at the cutoff 0: . In this case, there is no discontinuity of the conditional distribution of given . Thus, our estimaind equals the standard RD estimand (both are equal to 1). We vary from 0 to 5 and compare weighted local linear (WLL) estimator with the standard RD estimator (Imbens and Lemieux (2008)) in terms of bias, variance, root-mean-squared error (MSE), coverage probability of 95% confidence intervals (Coverage) and its length (CI length). When implementing both methods, we set the bandwidth parameter for standard RD estimator using cross-validation and then use the same bandwidth for WLL. The results based on 500 simulations are shown in Table 2. When , there is no covariates involved in the outcome function. Standard RD estimator performs neck to neck with our estimator. When , the standard RD estimator performs slightly better in terms of bias, however, our estimator consistently has smaller variance and MSE.

| bias | variance | MSE | Coverage | CI length | |||||||

| n | RD | WLL | RD | WLL | RD | WLL | RD | WLL | RD | WLL | |

| 500 | 0 | -0.0106 | -0.0102 | 0.3731 | 0.3767 | 0.3733 | 0.3768 | 0.9650 | 0.9750 | 1.6666 | 1.6853 |

| 1 | 0.0236 | 0.0226 | 0.6090 | 0.5423 | 0.6094, | 0.5427 | 0.9250 | 0.9400 | 2.2335 | 2.1753 | |

| 2 | -0.0583 | -0.0548 | 0.9004 | 0.7886 | 0.9023 | 0.7905 | 0.9600 | 0.9600 | 3.6103 | 3.2369 | |

| 5 | -0.0522 | -0.0423 | 2.1757 | 1.8264 | 2.1763 | 1.8268 | 0.8800 | 0.9000 | 7.1005 | 6.1439 | |

| 1000 | 0 | 0.0021 | 0.0034 | 0.2853 | 0.2841 | 0.2854 | 0.2841 | 0.9900 | 0.9900 | 1.3447 | 1.4083 |

| 1 | -0.0088 | -0.0118 | 0.4379 | 0.4387 | 0.4740 | 0.4388 | 0.9200 | 0.9450 | 1.6833 | 1.6661 | |

| 2 | 0.0380 | 0.0431 | 0.6046 | 0.5118 | 0.6058 | 0.5136 | 0.9400 | 0.9550 | 2.2516 | 2.2635 | |

| 5 | 0.1106 | 0.1129 | 1.4676 | 1.2770 | 1.4718 | 1.2820 | 0.9600 | 0.9850 | 6.3293 | 6.9139 | |

| 2000 | 0 | -0.0107 | -0.0111 | 0.2098 | 0.2096 | 0.2101 | 0.2099 | 0.9300 | 0.9200 | 0.7400 | 0.7229 |

| 1 | -0.0320 | -0.0225 | 0.3151 | 0.2920 | 0.3167 | 0.2929 | 0.9850 | 0.9850 | 1.3572 | 1.3237 | |

| 2 | -0.0177 | -0.0151 | 0.5234 | 0.4595 | 0.5237 | 0.4598 | 0.9500 | 0.9650 | 2.0911 | 1.9680 | |

| 5 | 0.1331 | 0.1360 | 1.1707 | 1.0019 | 1.1783 | 1.0111 | 0.9150 | 0.9200 | 4.2082 | 3.7723 | |

| 5000 | 0 | -0.0149 | -0.0136 | 0.1606 | 0.1616 | 0.1613 | 0.1622 | 0.9200 | 0.9250 | 0.5699 | 0.5725 |

| 1 | 0.0034 | 0.0049 | 0.2451 | 0.2275 | 0.2451 | 0.2275 | 0.9350 | 0.9400 | 0.9012 | 0.8793 | |

| 2 | -0.0130 | -0.0137 | 0.3301 | 0.2940 | 0.3304 | 0.2943 | 0.9450 | 0.9600 | 1.3654 | 1.2931 | |

| 5 | 0.0053 | 0.0139 | 0.8355 | 0.7016 | 0.8355 | 0.7018 | 0.9250 | 0.9750 | 3.1578 | 3.1535 | |

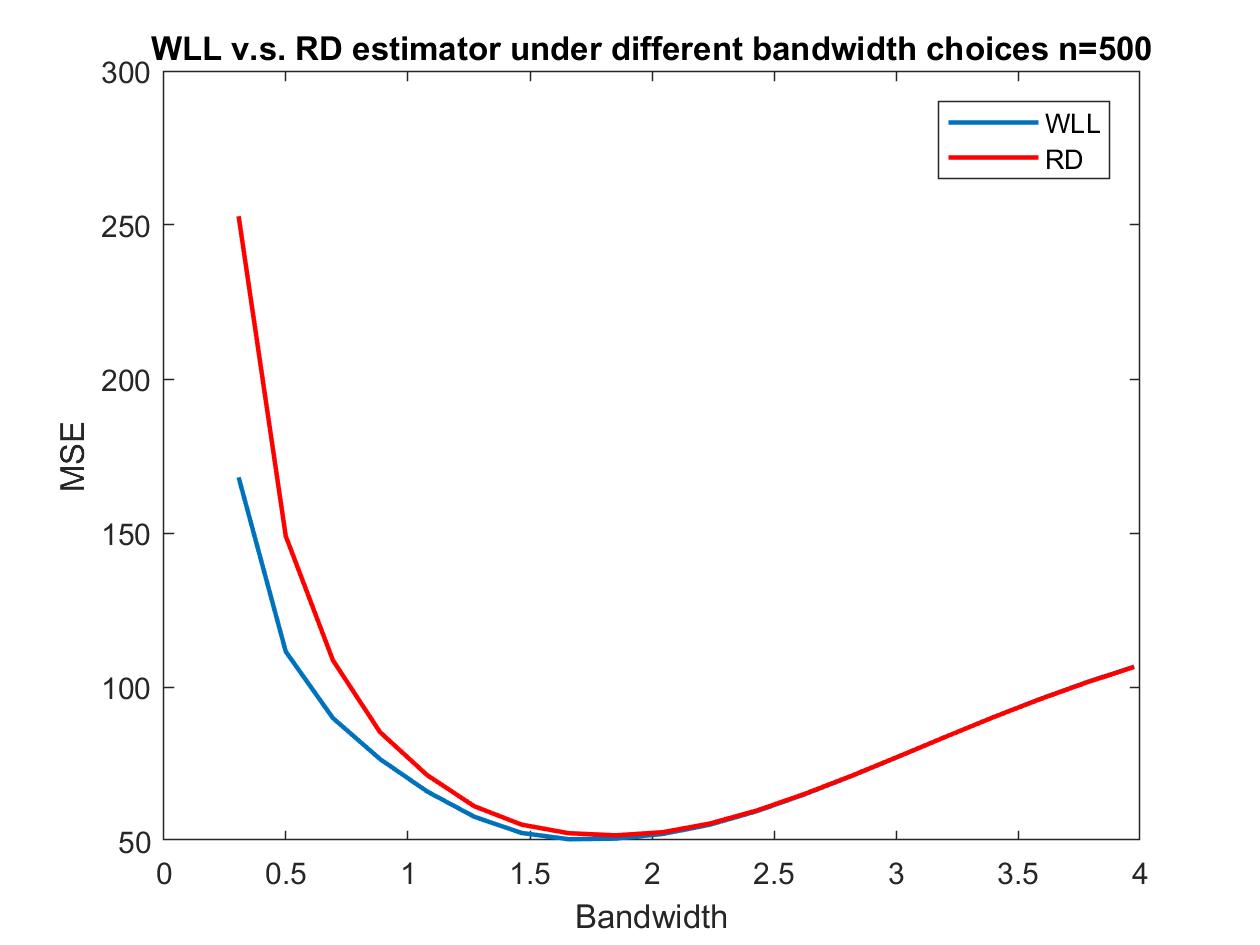

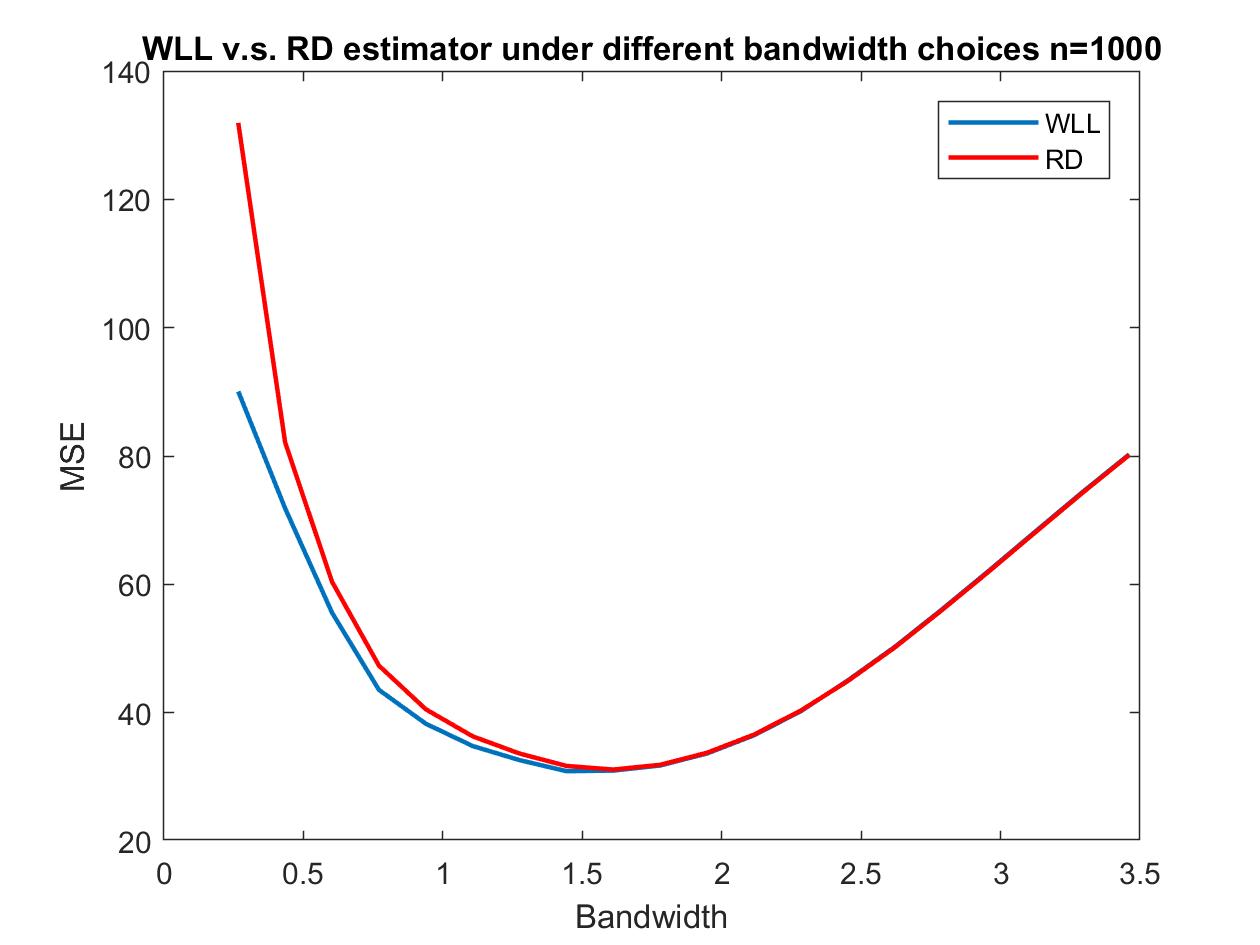

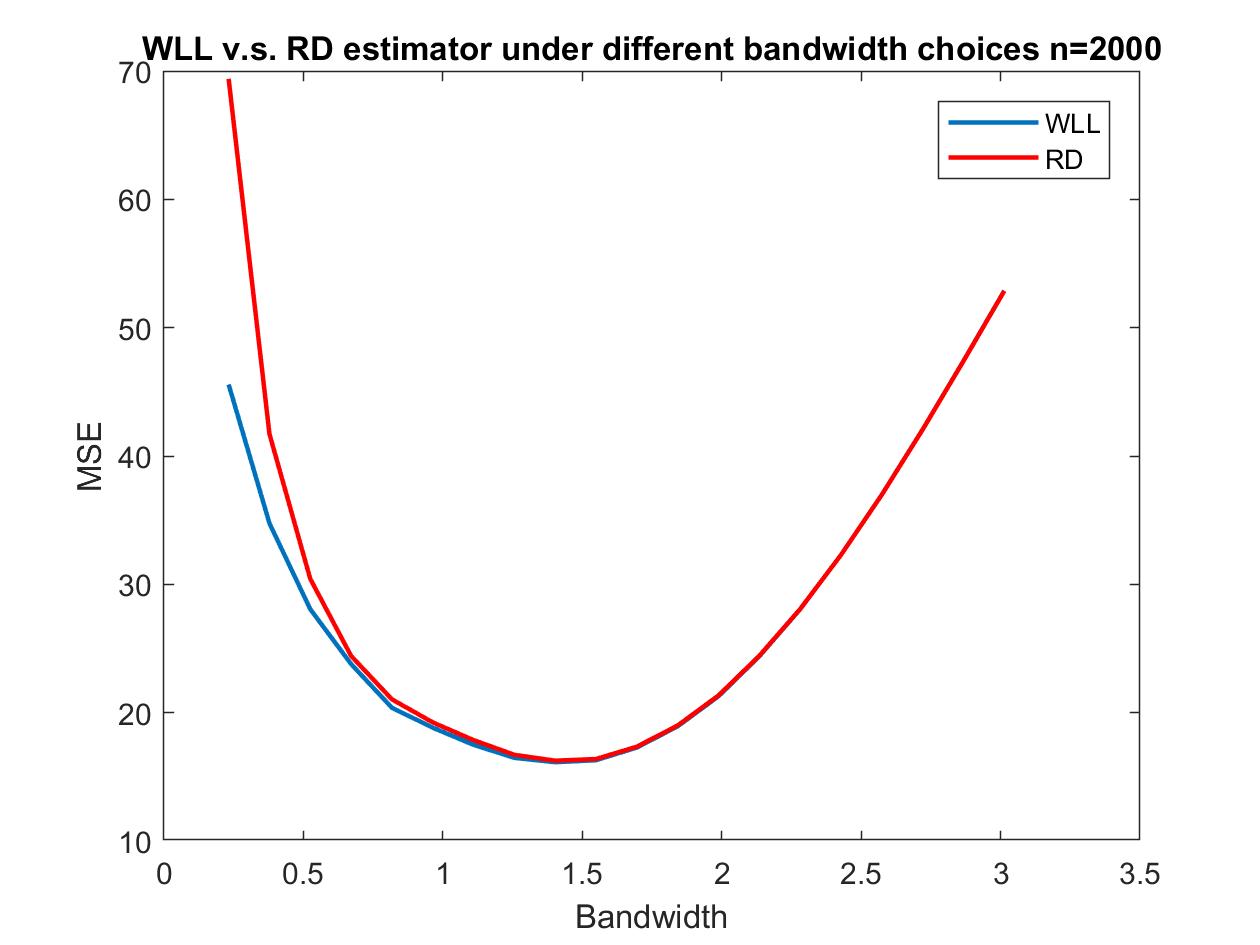

Figure 1 compares the MSE of the standard RD estimator with our WLL estimator across different bandwidth choices. The figure is consistent with corollary 1 as our estimator is asymptotically more efficient through including additional covariates into the estimation. Moreover, the advantage of WLL estimator is greater when perform under-smoothing and the difference of the two estimators becomes smaller as the bandwidth increases.

In the second setting, we consider the following data generating process:

where and are generated independently from distribution, however, is generated from another independent process with a discontinuity at , i.e. , where . The treatment is assigned at the cutoff 0: . When , again there is no discontinuity of the conditional distribution of given . Both our estimaind and the standard RD estimand are equal to 2. However, as differs from 0, the conditional distribution of given is discontinuous at . Our estimand is still equal to 2, which is the direct causal effect of interest. If we adopt the standard RD framework and ignore the discontinuity of the conditional distribution of given , we would expect that the standard RD estimator is biased for estimating the direct causal effect of interest (which is 2 in this example). In the data generating process, we vary from 0 to 1 and compare our estimator with the standard RD estimator. The results are shown in Table 3. The standard RD estimator has large bias and very poor coverage probability when is close to 1, which agrees with our expectation. In contrast, the proposed estimator has relatively small MSE and accurate coverage probabilities across different choices of the sample size and the parameter . In summary, our simulation studies confirm that one should apply the proposed framework to the RD study if there exists some potential discontinuity of the conditional distribution of the covariates given the running variable.

| bias | variance | MSE | Coverage | CI length | |||||||

| n | RD | WLL | RD | WLL | RD | WLL | RD | WLL | RD | WLL | |

| 500 | 0.2 | 0.1858 | 0.0762 | 0.6181 | 0.4318 | 0.4166 | 0.1922 | 0.9350 | 0.9550 | 2.4229 | 1.6925 |

| 0.4 | 0.4457 | 0.1150 | 0.5519 | 0.4327 | 0.5032 | 0.2005 | 0.8700 | 0.9450 | 2.1634 | 1.6963 | |

| 0.6 | 0.5721 | 0.1817 | 0.5898 | 0.4913 | 0.6751 | 0.2744 | 0.8500 | 0.9400 | 2.3119 | 1.9260 | |

| 0.8 | 0.7620 | 0.2445 | 0.5686 | 0.4698 | 0.9040 | 0.2805 | 0.7100 | 0.9250 | 2.2290 | 1.8416 | |

| 1 | 0.9753 | 0.3628 | 0.5346 | 0.4404 | 1.2369 | 0.3256 | 0.5750 | 0.8800 | 2.0956 | 1.7264 | |

| 1000 | 0.2 | 0.1851 | 0.0869 | 0.4124 | 0.4897 | 0.2044 | 0.2473 | 0.9200 | 0.9650 | 1.6168 | 1.9196 |

| 0.4 | 0.4082 | 0.1271 | 0.4101 | 0.3360 | 0.3349 | 0.1291 | 0.8450 | 0.9350 | 1.6077 | 1.3171 | |

| 0.6 | 0.5534 | 0.1795 | 0.4034 | 0.3428 | 0.4690 | 0.1497 | 0.7200 | 0.9200 | 1.5814 | 1.3437 | |

| 0.8 | 0.8240 | 0.2458 | 0.4625 | 0.3859 | 0.8930 | 0.2093 | 0.5750 | 0.900 | 1.8131 | 1.5125 | |

| 1 | 1.0130 | 0.3193 | 0.4445 | 0.5142 | 1.2237 | 0.3664 | 0.3950 | 0.9400 | 1.7423 | 2.0157 | |

| 2000 | 0.2 | 0.2052 | 0.0592 | 0.3162 | 0.2705 | 0.1421 | 0.0767 | 0.9050 | 0.9700 | 1.2393 | 1.0602 |

| 0.4 | 0.3755 | 0.0887 | 0.3072 | 0.2500 | 0.2354 | 0.0704 | 0.7550 | 0.9400 | 1.2042 | 0.9802 | |

| 0.6 | 0.5787 | 0.1697 | 0.3196 | 0.2568 | 0.4370 | 0.0947 | 0.5500 | 0.9000 | 1.2529 | 1.0067 | |

| 0.8 | 0.8448 | 0.2208 | 0.3173 | 0.2979 | 0.8143 | 0.1375 | 0.2450 | 0.9100 | 1.2438 | 1.1676 | |

| 1 | 1.0107 | 0.2234 | 0.2876 | 0.3556 | 1.1043 | 0.1763 | 0.0450 | 0.9500 | 1.1272 | 1.3938 | |

| 5000 | 0.2 | 0.2110 | 0.0418 | 0.2249 | 0.1748 | 0.0951 | 0.0323 | 0.8300 | 0.9450 | 0.8817 | 0.6852 |

| 0.4 | 0.4138 | 0.0650 | 0.2397 | 0.1947 | 0.2287 | 0.04212 | 0.6200 | 0.9450 | 0.9396 | 0.7631 | |

| 0.6 | 0.6099 | 0.1301 | 0.2319 | 0.2230 | 0.4257 | 0.06666 | 0.3000 | 0.9350 | 0.9091 | 0.8741 | |

| 0.8 | 0.8327 | 0.1826 | 0.2305 | 0.2741 | 0.7465 | 0.1085 | 0.0500 | 0.9150 | 0.9035 | 1.0744 | |

| 1 | 1.0259 | 0.2331 | 0.2250 | 0.2130 | 1.1032 | 0.0997 | 0.0050 | 0.9750 | 0.8821 | 0.8350 | |

5.2 Incumbency Advantage

We further apply our method to study the “incumbency advantage” in the U.S. House elections as in Lee (2008). The “incumbency advantage” states that current incumbent party in a district are more likely to win the next. The dataset contains 6560 observations on elections to the United States House of Representatives (1946-1998). We evaluate the probability a Democrat both running in and winning election as a function of the Democratic vote share margin of victory in election . The other covariates we are considering includes the Democratic vote share at time , Democrat winning at , Democrat’s political experience, opponent’s political experience, Democrat’s electoral experience, opponent’s electoral experience. This is the same setting as studied in Lee (2008) where he uses local 4th order polynomial RD estimates and includes these additional covariates as robustness check. We apply our method in the same five settings and results are reported in Table 4 below:

| Vote share | (1) | (2) | (3) | (4) | (5) | ||||||

| Polyn | WLL | Polyn | WLL | Polyn | WLL | Polyn | WLL | Polyn | WLL | ||

| Victory, election | 0.077 | 0.076 | 0.078 | 0.076 | 0.077 | 0.076 | 0.077 | 0.076 | 0.078 | 0.076 | |

| (0.011) | (0.010) | (0.011) | (0.011) | (0.011) | (0.010) | (0.011) | (0.010) | (0.011) | (0.010) | ||

| Dem. vote share | - | - | Y | Y | - | - | - | - | Y | Y | |

| Dem. win, | - | - | Y | Y | - | - | - | - | Y | Y | |

| Dem. political | - | - | - | - | Y | Y | - | - | Y | Y | |

| experience | |||||||||||

| Opp. political | - | - | - | - | Y | Y | - | - | Y | Y | |

| experience | |||||||||||

| Dem. electoral | - | - | - | - | - | - | Y | Y | Y | Y | |

| experience | |||||||||||

| Opp. electoral | - | - | - | - | - | - | Y | Y | Y | Y | |

| experience | |||||||||||

As shown in Table 4, there is no significant change on the estimated effect when using our method. The main reason is that the conditional densities of covariates are truly continuous at the cutoff in this data set. We expect that both standard RD estimator and our method are valid and therefore the results are very similar.

5.3 Generalized Second Price Auction (GSP)

Next we apply our method to study the generalized second price auction (GSP) problem. GSP is an auction mechanism for multiple items and it has been used widely for the assignment of advertisement positions by internet search engine like google and bing. Let be the number of bidders, and let be the bids from high to low. Denote by the bidders’ valuation associated with the rank of bids and the click through rate for the th position. The th bidder’s payoff in a GSP is given as .

An important metrics is the click through rate for the th position. Bidders are interested in the potential growth in their search traffic by winning the auction. And furthermore, in a Vickrey-Clarke-Groves (VCG) auction, will determine the total cost for placing each bidder in the sponsored advertisement region. In real world, GSP is usually implemented through a reservation score. A search score is formed for every bidder based on their bid and other quality measures. When the search score is bigger than a pre-set reservation score, the bidder’s link will be displayed in the sponsored area. Otherwise, they will be displayed after all the sponsored advertisements. The reservation score cut-off creates a natural regression discontinuity setting to evaluate .

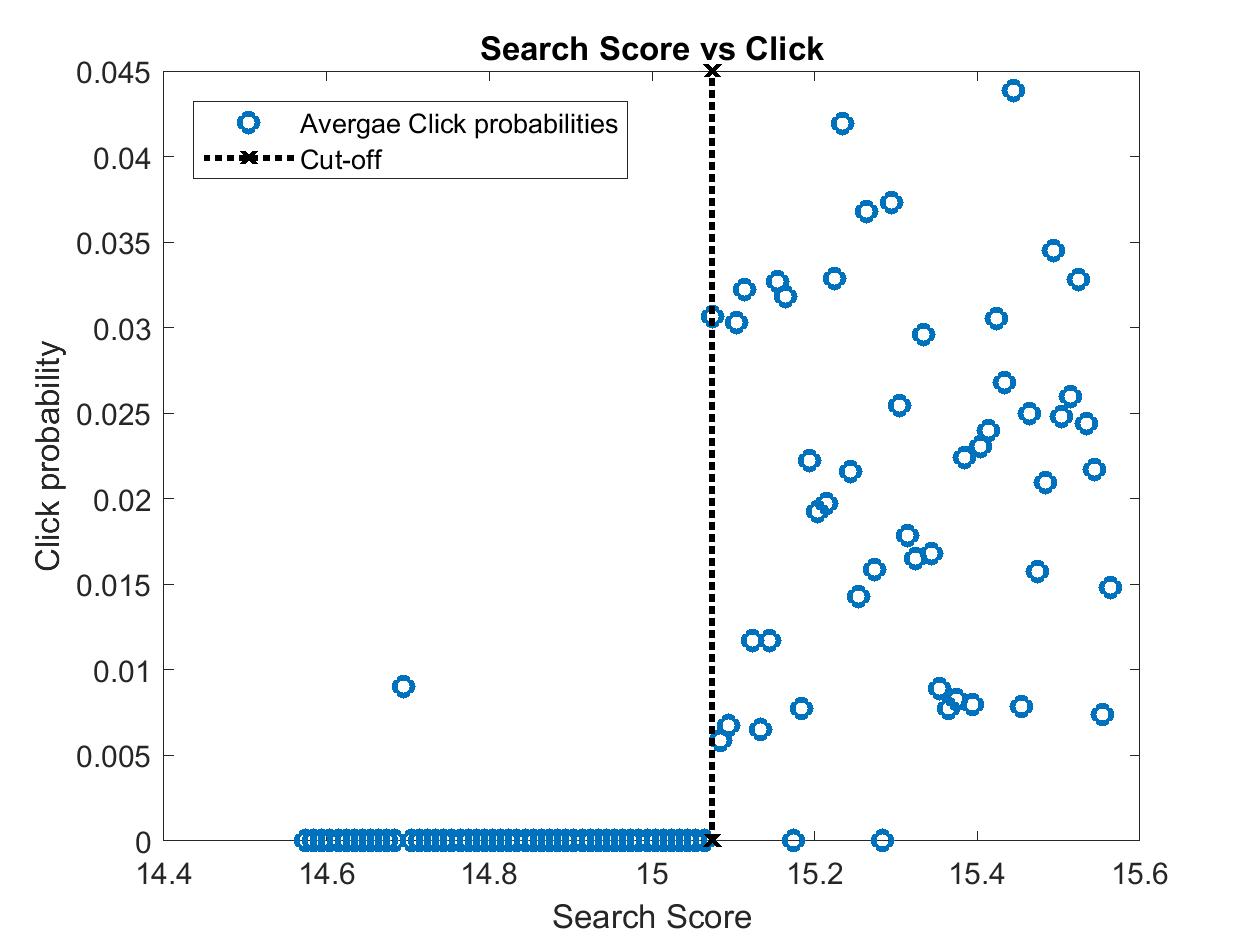

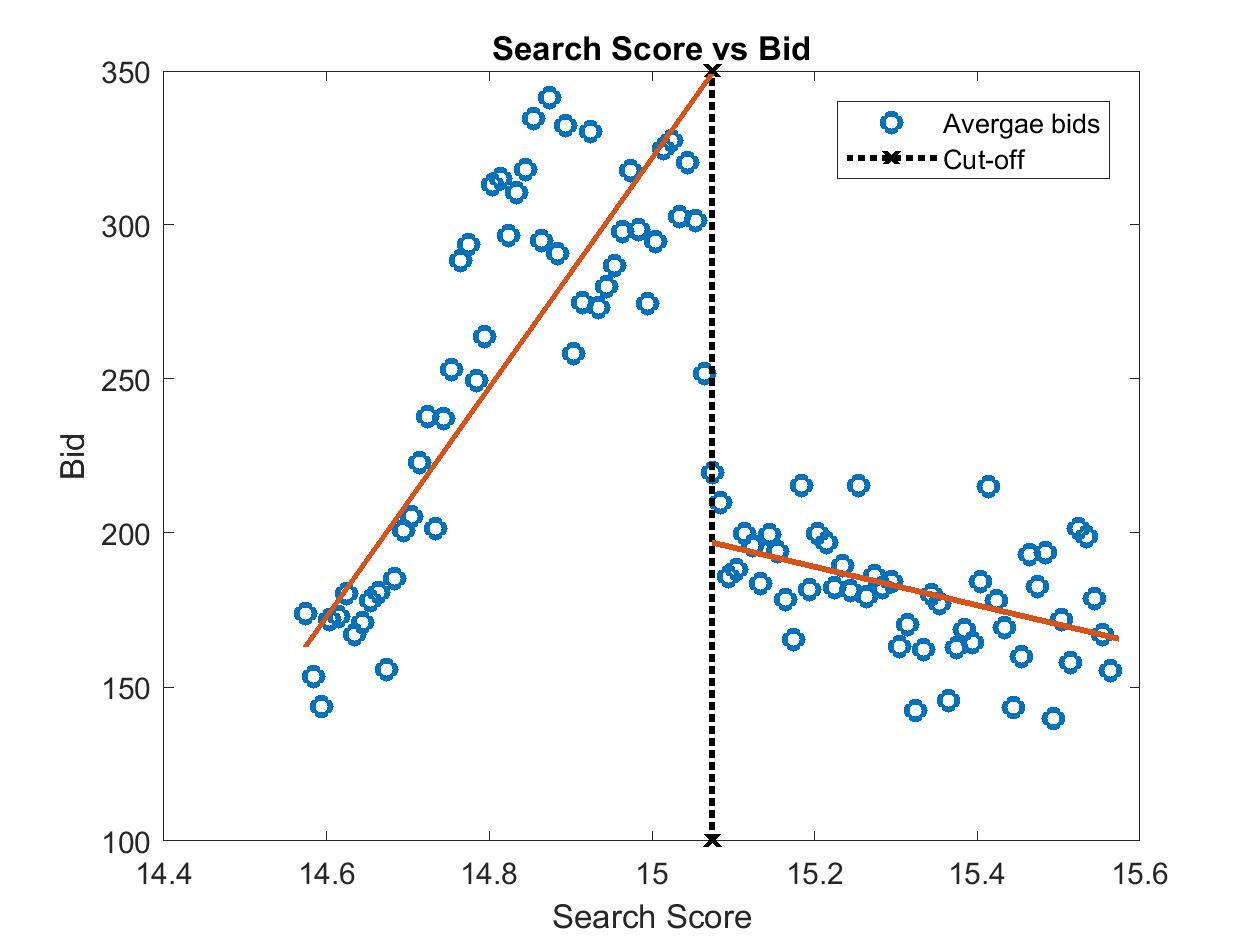

We study the Microsoft Bing search data from Oct 2nd to Oct 22nd in 2015 and estimate the effect of advertisement positions. We focus on a set of searches with first advertisement positions displayed but without third advertisement position displayed.111Microsoft Bing allows a maximum of 4 advertisement to be displayed at the time of study. This allows us to analyze the effect of second advertisement positions by comparing click-abilities for bidders near the search score cutoff. Figure 2 plots the connection between search score and click-ability for the second position in the sponsored advertisement area. Once the score passed the cut-off at 15.17, the customers’ links will be placed at the sponsored advertisement area and a significant increase in the click traffic can be observed.

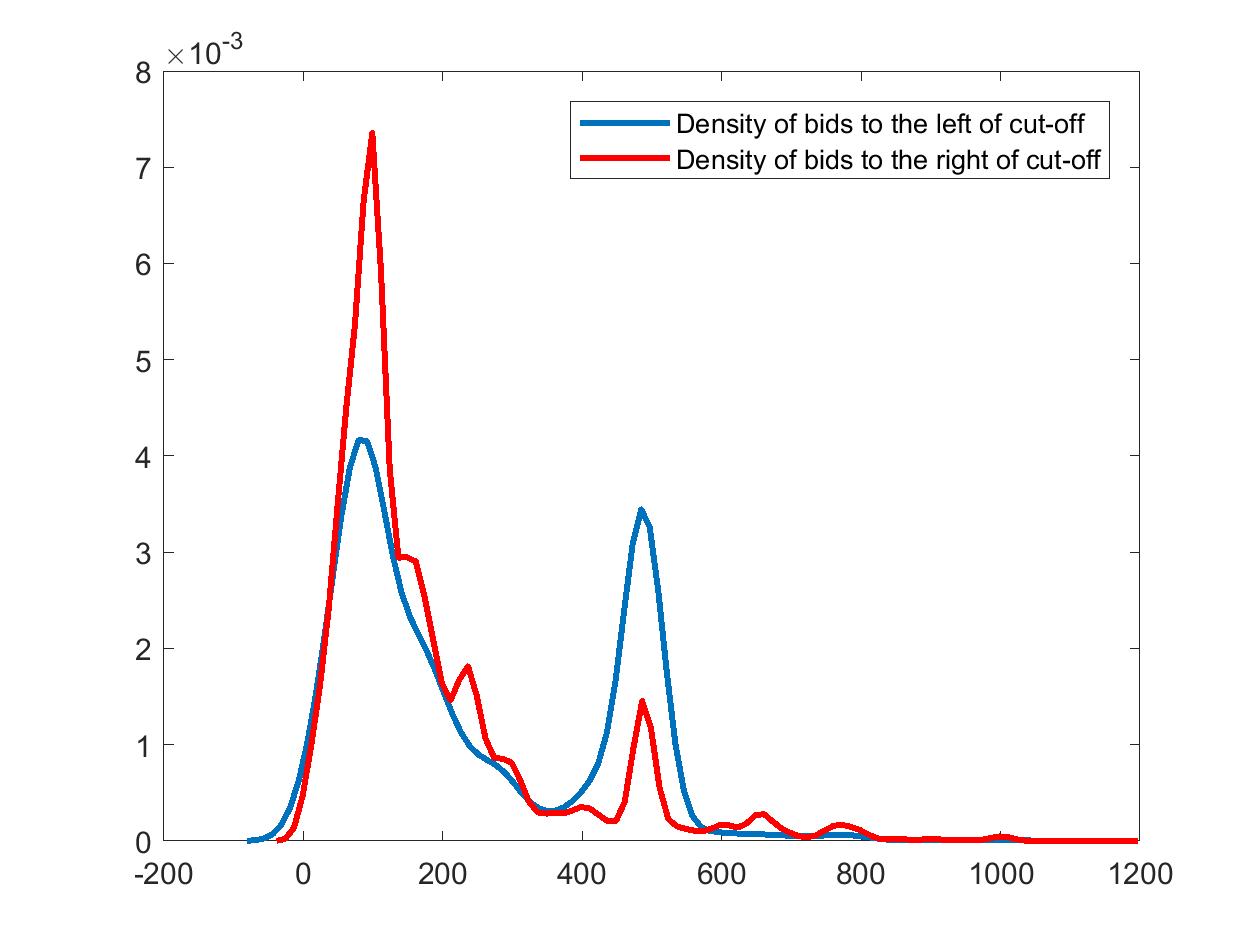

Consider the bid as a covariate. Figure 3 plots the mean bidding price before and after the search score cut-off. The mean bids before the cut-off is higher than the mean bids after the cut-off, implying the discontinuity of the conditional distribution of the covariate. See also Figure 4 for the conditional density of the covariate before and after the cut-off. Although a local envy free equilibrium exists when bidders are all bidding their true valuation (Edelman et al., 2007), information asymmetry or bidder inertia may still lead to bidder selections. For example, active bidders may have the incentive to bid more aggressively to take advantage of the bidders with high inertia.

Table 5 presents the results of our estimator and a polynomial RD estimator. The classic RD estimator may not be valid in this case due to the discontinuity in the covariates. It estimates that placing the advertisement on the second position can increase the click-ability by 1.91% and it is statistically significant. On the other hand, the proposed estimator delivers only 1.20%, 57% less than the RD estimator and it is not statistically significant at 5% level. The difference is mainly because low quality bidders with high willingness to pay have the incentive to bid higher to move their search scores pass the threshold. But when we match bidders with similar bids before and after the cut-off, the effect goes away.

| RD | WLL | |

| Estimates | 1.91%∗∗∗ | 1.20% |

| Standard Error | 0.0033 | 0.0090 |

6 Extension to Fuzzy RD Design

Fuzzy RD design refers to the case of a RD design when the treatment compliance is imperfect. Although is no longer a deterministic function of , there is still a discontinuity in . Hahn et al. (2001) showed the equivalence between the fuzzy RD design and local average treatment effect (LATE). Under independence and monotonicity assumption, the cutoff can be used as an instrument for the treatment status and the LATE can be interpreted as an intention-to-treat effect on the compliers: subjects take treatment as their assigned one.

Introducing self-selection under the Fuzzy RD design is the same as adding an additional endogenous variable. As a result, additional instrumental variable is required for identification. We consider a scenario when the self-selection is based on the cut-off instead of the treatment assignment mechanism. This setting allows us to deal with unobservables that affect the covariates. Let denote the type of individual: complier (), always-taker () and never taker (). A post-selection may exist and we can write

Notice that in sharp RD design, the self-selection based on the cut-off is the same as the selection on treatment assignment mechanism since the assignment mechanism is a deterministic function of . We study the selection based on the cut-off in fuzzy RD design as it is a more practical design. For example, students may notice that with SAT score higher than a threshold may increase their chance to receive scholarship, but the true assignment mechanism (gender, family income, etc.) may not be disclosed to them.

To consider self-selection under this setting, we first need to modify the independence and monotonicity assumption to incorporate additional covariates.

Assumption 9 (Fuzzy RD design).

.

-

1.

Independence: for .

-

2.

Monotonicity:

-

3.

Exclusion:

Due to self-selection, is discontinuous at , thus the independence assumption needs to be modified to insure individual types are remain constant under self-selection. Monotonicity assumption is essential to the identification by restricting the direction of selection. We may only have compliers, always-takers, never-takers in the population. As a result, we can view the treatment as an instrument as in Imbens and Angrist (1994).

By allowing types of individuals to depend on , our framework allows selection on treatment compliance to vary across . For example, individuals with family incomes less than a threshold are more likely to be always takers for the scholarship. An extreme scenario when is binary would be that always takers all have . In a similar spirit to the sharp RD design, we consider the following three estimands under our WATE framework:

| (6.1) |

| (6.2) |

| (6.3) |

where is a symmetric neighborhood around .

Theorem 2 (Identification under Fuzzy RD Design).

Under assumption 9, we have

| If we further have the conditional independence assumption (CIA), | ||

Theorem 2 proves the identification results for the three WATEs under the fuzzy RD design. The proof for the first two results are straightforward. The third result relies on the CIA in addition. This is because the sharp RD estimand is to ignore the conditioning on , however, the fuzzy RD has to condition on to cancel with the denominator. The CIA is to directly remove the conditioning on and thus is necessary for the results to hold. The local linear estimators of these three estimands can be developed following the argument in Section 3. However, the technical details and the theoretical results are much more involved, and are beyond the scope of this work. Given the practical importance of the fuzzy RD design, we think this is an important future research problem to explore.

7 Discussion

In this paper we study the RD problem when the conditional distribution of the covariates given running variables is discontinuous at the cutoff, for example, due to self-selection. The standard RD design is no longer valid as the continuity of potential outcomes assumption is violated. We show that casual effect can still be recovered when the covariates related to self-selection are observed. We thus propose a set of estimands under the framework of WATE and show that these estimands can be estimated using a class of weighted local linear estimators. We derive the theory for our estimators include consistency and asymptotic normality. We further compare our estimator with the standard RD estimator in simulation exercises to demonstrate its finite sample performance.

We apply our estimator to two empirical examples. First, we study the U.S. House elections data in Lee (2008), which is the classical data for RD estimator. Our estimator and local polynomial RD estimator have similar performance. Second, we apply our method to evaluate the effect of a GSP auction. We show that the result from our estimator is different from standard RD estimator due to self-selection. In particular, the obtained effect of advertising by using our estimator is smaller and statistically insignificant when self-selection is taking into account.

Appendix A Proofs

In the proof, we use to denote a generic constant which may change from line to line. Define the following notations:

For the ease of presentation, we introduce the following notations. Let , and denote the right derivatives , and . Denote

and

where . Define ,

Since all depend on , we denote the corresponding version with as .

Proof.

We will focus on the proof of (A.1). The remain results can be shown following the similar steps. By triangle inequality,

For term , we further decompose it into two terms,

| (A.2) |

The bias term is computed as

where the last step follows from the mean value theorem for some intermediate value . Our assumption implies that is bounded. In addition, by assumption is bounded away from 0 by a constant, thus the second term is of order . For the first term, by the choice of we get

| (A.3) |

which implies

Thus, we have . Now we consider . By the Markov inequality, . Thus, it suffices to compute ,

where the last step follows from the same argument in . Putting them together into (A.2), we have . For the last term , we have

where the last step holds by the bound for the term. This implies (A.1). ∎

Proof.

First, note that

Then, we have

which implies that is second order continuously differentiable by the continuously differentiable property of and in assumption 7. Thus, the standard calculation in nonparametric density estimation yields

To show the second result, following the similar argument, we get

where is a generic constant. The last two results follow from Fan (1993) together with the above bias calculation. ∎

A.1 Proof of Theorem 1

Since the local linear estimator is invariant to the scale of , we can simply take in the rest of the proof. It can be estimated by the following kernel estimator:

Start with the following minimization problem:

| (A.4) |

Recall that for any kernel estimates and , if is bounded away from 0, then

| (A.5) |

where and . Thus, if is bounded from above, then

Following the above discussion, we can show that

where Lemma 11 implies

The gradient of (A.4) can be written as the following -statistic:

where

implied by Lemma 11. Define

Thus,

| (A.6) |

where the first (leading) term is a -statistic after rescaling. By lemma 15 and Theorem 12.3 in Van der Vaart (2000), we have

| (A.7) |

where , and we use to denote the conditional expectation given the th sample. In the following, we approximate . Define . By Lemma 13, we have

The central limit theorem implies

| (A.8) |

where and . We now calculate the asymptotic variance as follows. Since , from lemma 13, we have

Similarly, we can show that

Recall that . Since , after some tedious calculation we can show that

And

Finally, note that in (A.6),

and therefore we obtain that

where

Following the similar argument, we can show the joint convergence

By the least squared formulation, the estimator satisfies

where . From lemma 10 and the matrix inversion formula,

Thus, the asymptotic bias of is

Similarly, the asymptotic variance of is

where

This completes the proof.

Lemma 12.

Proof.

Following the standard Taylor expansion, we can show that

where terms are valid uniformly over as the (mixed) third derivatives of are all bounded. ∎

Lemma 13.

Recall that

Under the same condition as in Theorem 1, and when

where terms are valid uniformly over or .

Proof.

From lemma 12,

where terms are valid uniformly over . Similarly, for Part.BII and Part.BIII, we can show that

where the last step follows from the definition of . Define . Combining the Part BI, BII and BIII, we obtain

Following the similar calculation, by lemma 11 we have

Finally, we calculate using Lemma 12,

where the terms are valid uniformly over and the last equality follows as

and

From Lemma 11, some tedious calculation implies

and

Thus when

This completes the proof. ∎

A.2 Proof of Corollary 1

In the case when , we can estimate by the following kernel estimator:

Similar as in theorem 1,

where Lemma 11 implies

The gradient in (A.4) can be written as the following -statistic:

where

Define

By Lemma 14, we have

The central limit theorem implies

| (A.9) |

where and . We now calculate the asymptotic variance as follows. Since , from lemma 13, we have

Similarly, we can show that

Recall that . Since , after some tedious calculation we can show that

Thus, choosing , we have

Finally, note that in (A.6),

and therefore we obtain that

where

Following the similar argument, we can show the joint convergence

By the least squared formulation, the estimator satisfies

where . From lemma 10 and the matrix inversion formula,

Thus, the asymptotic bias of is

Similarly, the asymptotic variance of is

where

This completes the proof.

Lemma 14.

Recall that

Under the same condition as in Theorem 1, and choose

where terms are valid uniformly over or .

Proof.

From lemma 12,

where terms are valid uniformly over . Similarly, for Part.EII and Part.EIII, we can show that

where the last step follows from the definition of . Define . Combining the Part EI, EII and EIII, we obtain

Following the similar calculation, by lemma 11 we have

Finally, we calculate using Lemma 12,

where the terms are valid uniformly over and the last equality follows as

and

From Lemma 11, some tedious calculation implies

and

Thus when

This completes the proof. ∎

A.3 Proof of Theorem 2

Proof.

Assume the treatment assignment function for individual is and only depends on directly. The assignment function is not known to the individual but they are aware of a jump in if . Thus a post selection may exist and we can write

Assume

Similarly

Assume and , then

| (A.10) |

Apply the same decomposition to

| (A.11) |

First notice that when integrating both sides with ,

Similarly, when integrating both sides with

And we obtain the estimand

Lastly under CIA, one can show that

| (A.12) |

and

| (A.13) |

when we integrating with both sides with ,

Thus

∎

Lemma 15.

When either or , the condition in Theorem 12.3 in Van der Vaart (2000) holds, such that

Proof.

is a linear combination of the following quantities:

| (A.14) | |||

| (A.15) | |||

| (A.16) | |||

| (A.17) | |||

| (A.18) | |||

| (A.19) |

∎

Lemma 16.

Proof.

Recall , thus

Following the standard Taylor expansion, we can show that

where terms are valid uniformly over as the (mixed) third derivatives of are all bounded. ∎

References

- Abadie and Imbens (2016) Abadie, A. and Imbens, G. W. (2016). Matching on the estimated propensity score. Econometrica 84 781–807.

- Angrist and Rokkanen (2015) Angrist, J. and Rokkanen, M. (2015). Wanna get away? regression discontinuity estimation of exam school effects away from the cutoff. Journal of the American Statistical Association 110 1331–1344.

- Calonicoy et al. (2017) Calonicoy, S., Cattaneo, M., Farrellx, M. and Titiunik, R. (2017). Regression discontinuity designs using covariates.

- Canay and Kamat (2018) Canay, I. A. and Kamat, V. (2018). Approximate permutation tests and induced order statistics in the regression discontinuity design. The Review of Economic Studies .

- Cattaneo and Escanciano (2017) Cattaneo, M. D. and Escanciano, J. C. (eds.) (2017). Regression Discontinuity Designs: Theory and Applications, vol. 38. Emerald Publishing Limited.

- Cattaneo et al. (2015) Cattaneo, M. D., Frandsen, B. R. and Titiunik, R. (2015). Randomization inference in the regression discontinuity design: An application to party advantages in the us senate. Journal of Causal Inference 3 1–24.

- Edelman et al. (2007) Edelman, B., Ostrovsky, M. and Schwarz, M. (2007). Internet advertising and the generalized second price auction: Selling billions of dollars worth of keywords. American Economic Review 97 242–259.

- Fan (1993) Fan, J. (1993). Local linear regression smoothers and their minimax efficiencies. Annals of Statistics 21 196–216.

- Fan and Gijbels (1996) Fan, J. and Gijbels, I. (1996). Local Polynomial Modelling and Its Applications: Monographs on Statistics and Applied Probability 66, vol. 66. CRC Press.

- Frölich and Huber (2018) Frölich, M. and Huber, M. (2018). Including covariates in the regression discontinuity design. Journal of Business & Economic Statistics o 0–0.

- Hahn et al. (2001) Hahn, J., Todd, P. and der Klaauw, W. V. (2001). Identification and estimation of treatment effects with a regression-discontinuity design. Econometrica 69 201–209.

- Horvitz and Thompson (1952) Horvitz, D. G. and Thompson, D. J. (1952). A generalization of sampling without replacement from a finite universe. Journal of the American Statistical Association 47 663–685.

- Imbens and Angrist (1994) Imbens, G. W. and Angrist, J. D. (1994). Identification and estimation of local average treatment effects. Econometrica 62 467–475.

- Imbens and Lemieux (2008) Imbens, G. W. and Lemieux, T. (2008). Regression discontinuity designs: A guide to practice. Journal of Econometrics 142 615–635.

- Lee (2008) Lee, D. S. (2008). Randomized experiments from non-random selection in u.s. house elections. Journal of Econometrics 142 675–697.

- Thistlethwaite and Campbell (1960) Thistlethwaite, D. L. and Campbell, D. T. (1960). Regression-discontinuity analysis: An alternative to the ex post facto experiment. Journal of Educational Psychology 51 309–317.

- Van der Vaart (2000) Van der Vaart, A. W. (2000). Asymptotic statistics, vol. 3. Cambridge university press.