Sharp hypotheses and bispatial inference

Russell J. Bowater

Independent researcher, Sartre 47, Acatlima, Huajuapan de León, Oaxaca, C.P. 69004,

Mexico. Email address: as given on arXiv.org. Twitter profile:

@naked_statist

Personal website:

sites.google.com/site/bowaterfospage

Abstract:

A fundamental class of inferential problems are those characterised by there having been a

substantial degree of pre-data (or prior) belief that the value of a model parameter was equal or

lay close to a specified value, which may, for example, be the value that indicates the absence of

an effect.

Standard ways of tackling problems of this type, including the Bayesian method, are often highly

inadequate in practice.

To address this issue, an inferential framework called bispatial inference is put forward, which

can be viewed as both a generalisation and radical reinterpretation of existing approaches to

inference that are based on P values.

It is shown that to obtain an appropriate post-data density function for a given parameter, it is

often convenient to combine a special type of bispatial inference, which is constructed around

one-sided P values, with a previously outlined form of fiducial inference.

Finally, by using what are called post-data opinion curves, this bispatial-fiducial theory is

naturally extended to deal with the general scenario in which any number of parameters may be

unknown.

The application of the theory is illustrated in various examples, which are especially relevant to

the analysis of clinical trial data.

Keywords:

Foundational issues; Gibbs sampler; Organic fiducial inference; Parameter and sampling

space hypotheses; Post-data opinion curve; Pre-data knowledge; Relative risk.

1 Introduction

Let us imagine that our aim is to make inferences about an unknown parameter on the basis of a data set that was generated by a sampling model that depends on the true value of . Given this context, we will begin with the following definition.

Definition 1: Sharp and almost sharp hypotheses

The hypothesis that the parameter lies in an interval will be defined as a sharp hypothesis if , and as an almost sharp hypothesis if the difference is very small in the context of our general uncertainty about after the data have been observed.

Clearly, any importance attached to a hypothesis of either of these two types should not generally have a great effect on the way that we make inferences about on the basis of the data if there had been no exceptional reason to believe that it would have been true or false before the data were observed. Taking this into account, it will be assumed that we are in the following scenario.

Definition 2: Scenario of interest

This scenario is characterised by there having been a substantial degree of belief before the data were observed, i.e. a substantial pre-data belief, that a given sharp or almost sharp hypothesis about the parameter could have been true, but if, on the other hand, this hypothesis had been conditioned to be false, i.e. if had been conditioned not to lie in the interval , then there would have been very little or no pre-data knowledge about this parameter over all of its allowable values outside of this interval. In this scenario, the hypothesis in question will be referred to as the special hypothesis.

Perhaps some may try to dismiss the importance of this type of scenario, however trying to make data-based inferences about any given parameter of interest in such a scenario represents one of the most fundamental problems of statistical inference that arise in practice. Let us consider the following examples.

Example 1: Intervening in a system

If is a parameter of one part of a system, and an intervention is made in a second part of the system that is arguably completely disconnected from the first part, then there will be a high degree of belief that the value of will not change as a result of the intervention, i.e. there is a strong belief in a sharp hypothesis about .

Example 2: A randomised-controlled trial

Let us imagine that a sample of patients is randomly divided into a group of patients, namely the treatment group, that receive a new drug B, and a group of patients, namely the control group, that receive a standard drug A. We will assume that patients in the treatment group experience a given adverse event, e.g. a heart attack, in a certain period of time following the start of treatment, and that patients in the control group experience the same type of event in the same time period. On the basis of this sample information, it will be supposed that the aim is to make inferences about the relative risk , where and are the population proportions of patients who would experience the adverse event when given drug B and drug A respectively. Now, if the action of drug B on the body is very similar to the action of drug A, which is in fact often the case in practice when two drugs are being compared in this type of clinical trial, then there may well have been a strong pre-data belief that this relative risk would be close to one, or in other words, that the almost sharp hypothesis that the relative risk would lie in a narrow interval containing the value one would be true.

It would appear that a common way to deal with there having been a strong pre-data belief that a sharp or almost sharp hypothesis was true is to simply ignore the inconvenient presence of this belief. However, doing so means that inferences based on the observed data will often not be even remotely honest. On the other hand, a formal method of addressing this issue that has received some attention is the Bayesian method. Let us take a quick look at how this method would work in a simple example.

Example 3: Application of the Bayesian method

Let us suppose that we are interested in making inferences about the mean of a normal density function that has a known variance , on the basis of a sample of values drawn from the density function concerned. It will be assumed that we are in the scenario of Definition 2 with the special hypothesis of interest being the sharp hypothesis that . Under the Bayesian paradigm, it would be natural to incorporate any degree of pre-data belief that equals zero into the analysis of the data by assigning a positive prior probability to this hypothesis.

However, the only accepted way of expressing a lack of knowledge about a model parameter under this paradigm is the controversial strategy of placing a diffuse proper or improper prior density over the parameter concerned. Taking this into account, let us assume, without a great loss of generality, that the prior density function of conditional on is a normal density function with a mean of zero and a largevariance .

The inadequacy of the strategy in question is clearly apparent in the uncertainty there would be in choosing a value for the variance , and this issue becomes very hard to conceal after appreciating that the amount of posterior probability given tothe hypothesis that is highly sensitive to changes in this variance. For example, the natural desire to allow the variance to tend to infinity results in the posterior probability of this hypothesis tending to one for any given data set and any given positive prior probability that is assigned to equalling zero.

It can be easily argued, therefore, that the application of standard Bayesian theory in the case just examined has an appalling outcome. Moreover, applying the Bayesian strategy just described leads to outcomes of a similar type in cases where the sampling density of the data given the parameter of interest is not normal, and/or the prior density of this parameter has a more general form, and also, importantly, in cases where the special hypothesis is an almost sharp rather than, simply, a sharp hypothesis. This clearly gives us a strong motivation to look for an alternative method for making inferences about in the scenario of interest. Following a similar path to that of Bowater and Guzmán-Pantoja (2019b), the aim of the present paper is to develop a satisfactory method for doing this on the basis of classical ideas about statistical inference. This method of inference will be called bispatial inference.

Before going further, let us summarise the structure of the paper. In the next section, a general theory of bispatial inference is broadly outlined. A special formalisation of this theory is then developed in detail in Section 3. Given that all reasonable objectives for making inferences about a parameter of interest can not be conveniently achieved by using this theory alone, a method of inference is put forward in Section 4 that is based on combining bispatial inference with a specific type of fiducial inference. In the final main section of the paper, namely Section 5, this combined theory is extended to cases where various model parameters are unknown.

2 General theory of bispatial inference

2.1 Overall problem

Let us now consider a more general problem of statistical inference to the one that was discussed in the Introduction. In particular, we now will be interested in the problem of making inferences about a set of parameters , where each is a one-dimensional variable, on the basis of a data set that was generated by a sampling model that depends on this set of parameters. Let the joint density or mass function of the data given the true values of the parameters be denoted as . This will be the overall problem of inference that we will be concerned with in the rest of this paper.

2.2 A note about probability

We will interpret the concept of probability under the definition of generalised subjective probability that was comprehensively outlined in Bowater (2018b). Given that it will not be necessary to explicitly discuss this definition of probability in the present paper, the reader is referred to this earlier work for further information. Nevertheless, in relation to the general topic in question, there is a specific issue that should not be overlooked. In particular, we observe that when events are repeatable, the concept of the probability of an event and the concept of the proportion of times the event occurs in the long term are often used interchangeably. However, this is not always appropriate. The reason for this is that a population proportion is a fact about the physical world, while under certain definitions of probability, e.g. the definition that will be adopted here, a probability is primarily always a measure of a given individual’s state of mind. Therefore, where necessary, we will denote the population proportion of times any given event occurs by , while the probability of the event will, as usual, be denoted by .

2.3 Parameter and sampling space hypotheses

The theory of inference that will be developed is based on a hypothesis that concerns an event in the parameter space, and an equivalent hypothesis that is stated in terms of the proportion of times an event in the sampling space will occur in the long run. The link that is made between the parameter and sampling spaces through the attention given to these two hypotheses is the reason that this type of inference will be called bispatial inference. More specifically, these two types of hypothesis will be assumed to have the following definitions.

Definition 3: Parameter space hypothesis

Given that, from now, : will denote the hypothesis that a given condition is true, the parameter space hypothesis is defined by:

where is a given subset of the entire space over which the set of parameters is defined.

Definition 4: Sampling space hypothesis

The two conditions that the sampling space hypothesis must satisfy are:

1) It must be equivalent to the hypothesis , i.e. if is true then must be true and if is true then must be true.

2) It must have the following form:

where is a statistic calculated on the basis of an as-yet-unobserved second sample of values drawn from the density function , which is possibly of a different size to the observed (first) sample , the set is a given subset of the entire space over which the statistic is defined, and the set is a given subset of the interval . To clarify, the hypothesis is the hypothesis that the unknown population proportion lies in the known set . Also, it should be clarified that the definition of the set will depend, in general, on the data set .

2.4 Inferential process

It will be assumed that inferences are made about the set of parameters by proceeding through the steps of the following algorithm:

Step 1: Formation of a suitable hypothesis . The choice of this hypothesis should be made with the goal in mind of being able to make useful inferences about the parameters .

Step 2: Assessment of the likeliness of the hypothesis being true using only pre-data knowledge about the parameters . It is not necessary that this assessment is expressed in terms of a formal measure of uncertainty, e.g. a probability does not need to be assigned to this hypothesis.

Step 3: Formation of a suitable hypothesis .

Step 4: Assessment of the likeliness of the hypothesis being true after the data have been observed. In carrying out this assessment, all relevant factors ought to be taken into account including, in particular, the assessment made in Step 2 and the known equivalency between the hypotheses and .

Step 5: Conclusion about the likeliness of the hypothesis being true having taken into account the data . This is directly implied by the assessment made in Step 4 due to the equivalence of the hypotheses and .

2.5 First example: Two-sided P values

In the next three sections, we will apply the method outlined in the previous section to the problem of inference referred to in Example 3 of the Introduction, i.e. that of making inferences about a normal mean when the population variance is known. In this case, it is clear that the set of unknown parameters will consist of just the mean .

To give a context to this problem, let us imagine that a patient is being constantly monitored with regard to the concentration of a certain chemical in his/her blood. We will assume that the measurements of this concentration are notably imprecise, and in particular, it will be assumed that any such measurement follows a normal density function with known variance centred at the true concentration. Also, let us suppose that the data is simply the measurement of this concentration at a time point minus the same type of measurement taken at a time point , where the time point is immediately before the patient is subjected to some kind of intervention and the time point is immediately after this intervention.

Now, if the intervention in question would not be expected to affect the concentration of the chemical of interest, there is likely to be a substantial degree of pre-data belief that the true change in this concentration in going from the time point to the time point , namely the change in this concentration, will be very small. In fact, to begin with, let us assume that these two time points are so close together that we find ourselves in the scenario of Definition 2 with the special hypothesis being the sharp hypothesis that . It can be seen therefore that we have effectively arrived at a specific form of Example 1 of the Introduction.

Under the assumptions that have been made, it is reasonable, as part of Steps 1 and 3 of the algorithm of Section 2.4, to define the hypotheses and as follows:

| (1) |

where is equal to an additional unobserved measurement of the concentration in question taken at time minus an additional unobserved measurement of the same type taken at time , while is the cumulative density of a standard normal distribution at the value . It can be easily appreciated that these two hypotheses are in fact equivalent. Observe that the quantity on the right-hand side of the equality in equation (1) would be the standard two-sided P value that would be calculated on the basis of the observation if was regarded as being the null hypothesis.

Now, in Step 4 of the algorithm of Section 2.4, although a small value for this two-sided P value would naturally disfavour the hypothesis , and in particular favour the left-hand side of the equality in equation (1) being greater than this P value, this would need to be balanced by how much the pre-data assessment in Step 2 of this algorithm favoured the hypothesis . Nevertheless, if the P value under discussion turns out to be very small then, even if the hypothesis was quite strongly favoured before the data value was observed, it may well be regarded as being rational to decide that hypothesis is fairly unlikely to be true. As will always be the case, the evaluation of the likeliness of the hypothesis in Step 5 of the algorithm in question should be the same as the evaluation of the likeliness of the hypothesis in Step 4 of this algorithm.

2.6 Second example: Q values

Let us now consider the more general case of the example being currently examined where the special hypothesis in the scenario of Definition 2 is the almost sharp hypothesis that lies in the interval , where is a small positive constant.

In this case, it is reasonable to define the hypotheses and as follows:

where

| (2) |

It can easily be shown that these two hypotheses are equivalent under the assumptions that have been made. Notice that the value as specified in equation (2) would be classified as the Q value for the hypothesis that according to the general definition of a Q value that was presented and discussed in Bowater and Guzmán-Pantoja (2019b), and therefore here will also be referred to as a Q value.

Similar to the previous example, although we would naturally disfavour the hypothesis , and as a result, the hypothesis if this Q value was small, this would need to be balanced by how much the hypothesis was favoured before the value was observed in order to make a sensible evaluation of the likeliness of the hypothesis being true.

2.7 Third example: One-sided P values

To give another example, let us look at an alternative way of defining the hypotheses and in the context of the specific problem of inference that is currently under discussion. In particular, let us now assume that, if , then these hypotheses would be defined as:

| (3) | |||

| (4) |

while if , then they would have the definitions:

| (5) | |||

| (6) |

Again, it can be easily shown that the hypotheses and in equations (3) and (4) are equivalent, and also that these hypotheses as defined in equations (5) and (6) are equivalent. In addition, observe that the quantities on the right-hand sides of the inequalities in equations (4) and (6) would be the standard one-sided P values that would be calculated on the basis of the observation if the null hypotheses were regarded as being the hypotheses that correspond to the hypotheses defined in these two equations.

Clearly, the substantial degree of pre-data belief that lies in the interval should be reflected in the pre-data assessment of the likeliness of the hypothesis as defined in either equation (3) or equation (5). Furthermore, similar to what was seen in the previous examples, a substantial degree of pre-data belief in whichever one of the hypotheses in these equations is applicable would need to be appropriately balanced by the information represented by the observation that is summarised by the one-sided P value that appears in the corresponding hypothesis , in order to make an adequate assessment of the likeliness of this latter hypothesis given the observed value of .

2.8 Discussion of examples

Although the methods that have just been outlined in Sections 2.5 to 2.7 can be applied to many other problems of inference than the simple one that has been considered, the latter method based on one-sided P values is much more widely applicable than the former two methods based on two-sided P values and on Q values, in particular, it is able to cope better with sampling densities that are multimodal and/or non-symmetric.

Also, it can be argued, not just in terms of the specific problem that has been discussed but more generally, that it is going to be less easy to evaluate, on the whole, the likeliness of hypotheses that are based either on two-sided P values or on Q values than those that are based on one-sided P values. With regard to the examples that have been presented, a simple observation that underlies the argument being referred to is that, for any given value of , one of the two open intervals over which either a two-sided P value or a Q value is determined by integration of the sampling density, i.e. one of the intervals or , will contain a proportion of the sampling density that always decreases in size as the mean moves away from zero, despite of course this change in always causing the total proportion of the sampling density contained in these two intervals to increase.

For the reasons that have just been given, we will not consider generalising in a formal way the methods based on two-sided P values and on Q values that were put forward in Sections 2.5 and 2.6. Instead, the type of method based on one-sided P values that was described in Section 2.7 and developments of this method, will constitute the main form of bispatial inference that will be explored in the rest of this paper. It should be pointed out that, although it is apparent from the example considered in Section 2.7 that possibly an important drawback of this method is that, in the scenario of Definition 2, it will not generally allow us to directly assess the likeliness of the special hypothesis that a parameter of interest lies in a narrow interval after the data have been observed, i.e. that lies in the interval in the example in question, it will be shown later how this difficulty can be overcome.

3 Special form of bispatial inference

3.1 General assumptions

Let us now formalise the specific type of bispatial inference that has just been identified.

For the moment, it will be assumed that the only unknown parameter on which the sampling density depends is the parameter , either because there are no other parameters in the model, or because all the other parameters are known. Also, we will assume that the scenario of interest is again the scenario outlined in Definition 2, with the unknown parameter now being of course , and that, in this scenario, the special hypothesis is the almost sharp hypothesis that lies in the narrow interval .

3.2 Test statistic

Let us begin by detailing how the concept of a test statistic will be interpreted. In particular, it will be assumed that a test statistic , which will also be denoted simply by the value , satisfies the following two requirements:

1) Similar to what in Bowater (2019a) was defined as being a fiducial statistic, it is necessary that the test statistic is a univariate statistic of the sample that can be regarded as efficiently summarising the information that is contained in this sample about the parameter , given the values of other statistics that do not provide any information about this parameter, i.e. ancillary statistics.

2) Let be the cumulative distribution function of the unobserved test statistic evaluated at its observed value given a value for the parameter , and conditional on being equal to , where are the observed values of an appropriate set of ancillary statistics of the data set of interest, i.e. equals the probability , and also let . On the basis of this notation, it is necessary that, over the set of allowable values for , the probabilities and strictly decrease as increases.

As far as the examples that will be considered in this paper are concerned, condition (1) will be satisfied, in a simple and clear-cut manner, by being a univariate sufficient statistic for . As a result, the set of ancillary statistics referred to in condition (2) will naturally be assigned to be empty in these examples, and in fact we could reasonably expect that it would usually be appropriate to assign this set to be empty when the choice of the test statistic is more general.

3.3 Parameter and sampling space hypotheses

If the condition

| (7) |

holds, where the values and are as defined in Section 3.1, then the hypotheses and will be defined as:

| (8) | |||

| (9) |

where is again an as-yet-unobserved sample of values drawn from the density function but now this sample will be assumed to be always of the same size as the observed sample , i.e. it must consist of observations, and where is the unknown population proportion of times that conditional on the ancillary statistics calculated on the basis of the data set being equal to the values , i.e. conditional on . On the other hand, if the condition in equation (7) does not hold, then the hypotheses in question will be defined as:

| (10) | |||

| (11) |

Given the way that the test statistic was defined in Section 3.2, it can be easily appreciated that the hypotheses and in equations (8) and (9) are equivalent, and also that these hypotheses as defined in equations (10) and (11) are equivalent. In addition, observe that the probabilities and that appear in the definitions of the hypotheses in equations (9) and (11) would be the standard one-sided P values that would be calculated on the basis of the data set if the null hypotheses were regarded as being the hypotheses that correspond to the two hypotheses in question.

We will assume that to make inferences about the parameter of interest , the same algorithm will be used as was outlined in Section 2.4. However, with regard to the use of this algorithm in the current context, let us make the following comments:

a) The set of parameters referred to in this algorithm will of course consist of only the parameter .

b) In Step 2 of this algorithm, it is evident that some special attention will often need to be placed in assessing the likeliness of the almost sharp hypothesis that lies in the interval based on only pre-data knowledge about , since we can see that this hypothesis will always be included in the hypothesis , but will not generally be equivalent to .

c) In assessing the likeliness of the hypothesis in Step 4 of this algorithm, one of the relevant factors that ought to be taken into account is clearly the size of the one-sided P value that appears in the definition of this hypothesis, i.e. the value or the value .

d) Also in Step 4 of this algorithm, it now will be assumed that the goal is usually to assign a probability to the hypothesis .

With reference to this last comment, the task of assigning a probability to the hypothesis may be made easier by first trying to determine what would be the minimum probability that could be sensibly assigned to this hypothesis. In particular, for a reason that should be obvious, it would not seem sensible to assign a probability to the hypothesis that is less than the probability that would be assigned to this hypothesis if nothing or very little had been known about the parameter before the data were observed. One way, but not as yet a widely accepted way, of making inferences about in this latter type of situation is to use the fiducial method of inference (which has its origins in Fisher 1935 and Fisher 1956) and, given the interpretation of the concept of probability being relied on in the present paper (see Section 2.2), it would seem appropriate to consider applying the form of this type of inference that has been called subjective, or more recently, organic fiducial inference, see Bowater (2017), Bowater (2018a) and Bowater (2019a). In this regard, let denote the post-data or fiducial probability that would be assigned to the hypothesis as a result of applying this latter method of fiducial inference if there had been no or very little pre-data knowledge about . Therefore, this value can be considered as being a minimum value for the post-data probability of the hypothesis being true in the genuine scenario of interest, i.e. the scenario of Definition 2. This method for placing a potentially useful lower limit on the probability of the hypothesis will be illustrated as a feature of the examples that will be described in the next two sections.

3.4 First example: Inference about a normal mean with variance known

Let us return to the example that was discussed in Section 2.7. We can see that this example fits within the special framework for bispatial inference that has just been outlined. In particular, the value , i.e. the observed change in concentration, is clearly a suitable test statistic , since it is a sufficient statistic for the mean that will satisfy condition (2) of Section 3.2 for any value it may possibly take. Also, the way that the hypotheses and were specified in Section 2.7 matches how these hypotheses would be specified by using the definitions in Section 3.3.

In this earlier example, let us now more specifically assume that , and . Under these assumptions, the relevant hypotheses and are as given in equations (5) and (6), and the one-sided P value on the right-hand side of the inequality in equation (6) is 0.0062. Since this P value is obviously small, but not very small, if a substantial probability of around would have been placed on the hypothesis that before the value was observed, it would seem possible to justify a probability in the range of say 0.03 to 0.08 being placed on the hypothesis being true, and as a result, on the hypothesis being true after the value has been observed.

The probability that would be assigned to this hypothesis after the value has been observed by applying the strong fiducial argument (see Bowater 2019a) as part of the method of organic fiducial inference would be equal to 0.0062, i.e. the one-sided P value of interest. We therefore can regard the probability referred to in the last section as being equal to 0.0062 in this example. Since the form of reasoning under discussion could be considered as justifying this value of 0.0062 as being a minimum value for the probability of the hypothesis in the genuine scenario of interest, it is therefore appropriate that the range of values for this probability that has been proposed is well above this minimum value.

3.5 Second example: Inference about a binomial proportion

Let us imagine that a random sample of patients are switched from being given a standard drug A to being given a new drug B. After a period of time has passed, they are asked which out of the two drugs A and B they prefer. The proportion of patients who prefer drug B to drug A, after patients who do not express a preference have been excluded, will be denoted by the value . Given this sample proportion, it will be assumed that the aim is make inferences about its corresponding population proportion . For a similar reason with regard to the nature of drugs A and B as that given in Example 2 of the Introduction, let us also suppose that the scenario of Definition 2 applies with the special hypothesis being the hypothesis that the proportion lies in a narrow interval centred at 0.5, which will be denoted as .

Observe that the sample proportion clearly satisfies the requirements of Section 3.2 to be a suitable test statistic . To give a more specific example, we will assume that there are twelve patients in the sample, of whom nine prefer drug A to drug B, one prefers drug B to drug A and two do not express a preference, and therefore . Also, let the constant be equal to 0.03. It now follows that, under the definitions of Section 3.3, the hypotheses and would be specified as:

| (12) |

where is the proportion of patients who would prefer drug B to drug A in an as-yet-unobserved sample of ten patients who express a preference between the two drugs.

We can see that again the one-sided P value, i.e. the value 0.0173 in equation (12), is reasonably small. Therefore, if a pre-data probability of say 0.3 would have been placed on the hypothesis that , it would seem possible to justify a probability in the range of say 0.03 to 0.08 being placed on the hypothesis being true, and as a result, on the hypothesis being true after the proportion has been observed.

The probability that would be assigned to the hypothesis after the value has been observed by using the strong fiducial argument, and a local pre-data (LPD) function for (see Bowater 2019a) defined by:

| (13) |

where is a positive constant, as part of the method of organic fiducial inference would be equal to 0.0070. Since this post-data probability can justifiably be regarded as the probability referred to Section 3.3, and therefore as being a minimum value for the probability of the hypothesis in the genuine scenario of interest, it is appropriate that, similar to the previous example, the range of values for the probability of this hypothesis that has been proposed is well above this minimum value.

3.6 Foundational basis of the theory

In the examples considered in the previous section and Section 3.4, it was inherently assumed that the smaller the size of the one-sided P value that appears in the hypothesis , the less inclined we should be to believe that this hypothesis is true. However, what is the foundational basis for this assumption? We will now try to offer some kind of answer to this question.

It can be seen that the two versions of the hypothesis in equations (9) and (11) can both be represented as:

| (14) |

where is a given condition and is a given one-sided P value. Therefore, the population proportion of times condition is satisfied will be less than or equal to if the corresponding hypothesis is true, or in other words, if the parameter is restricted in the way that is specified by this latter hypothesis. However, we could also calculate a post-data probability for condition being satisfied without placing restrictions on the parameter by using the fiducial argument. In particular, the post-data probability in question would be defined as:

| (15) |

where is an appropriate fiducial density function for the parameter . To clarify, the outer integral in this equation is over unobserved data sets that satisfy condition .

It will be helpful if we now look at a specific example, and so let us again consider the example discussed in Sections 2.7 and 3.4. In this case, the fiducial density of the parameter of interest , i.e. the density , obtained by using the strong fiducial argument is defined by the expression . On the basis of this fiducial density for , it is simple to show, by using equation (15), how we obtain the result that equals for any given observed value of , where as we know or , which of course is a special result that in fact could have been derived by using more direct fiducial reasoning. We could interpret this result as meaning that the probability that we should assign to condition being true if we had known nothing or very little about before the value was observed should be 0.5.

Taking into account this interpretation, if we were to propose assigning a large probability to the hypothesis being true when the P value in equation (14) was quite small, then it would seem fair if we were asked how we can justify doing this given the large difference between this P value and the probability . To be able to give a satisfactory answer to this question, it is reasonable to argue that the only situation we could be in would be one in which, before the value was observed, there had been a high degree of belief that the hypothesis was true, which in the context of the scenario of Definition 2, would mean a high degree of pre-data belief that lay in the interval . In this situation, we could argue that assigning a large probability to the hypothesis when the P value is quite small can be justified due to the importance that is attached to the probability as a benchmark or reference value being greatly diminished as a result of our strong pre-data opinion about .

Furthermore, let us suppose that a given probability of would be assigned to the hypothesis being true if the P value was equal to a given value that is less than say 0.05. Now, if we imagine a scenario in which the value of is less than , and therefore further away from the probability than , then it can be easily argued that the only way we could justify assigning the same probability to the hypothesis would be if, for an unrelated reason, it was decided that our pre-data belief that should be increased. Also, it is fairly uncontroversial to argue that for any fixed data value , the degree of pre-data belief that and the degree of post-data belief in the hypothesis should be positively correlated. As a logical consequence of these arguments, it follows that, if there is a fixed degree of pre-data belief that , then the probability we should wish to assign to the hypothesis after the value has been observed should decrease as the value that the P value is assumed to take is made smaller, on condition that this P value is already small. Therefore, we hope that an adequate answer to the question posed at the start of this section has been provided.

Another foundational issue that no doubt some would try to raise centres on the argument that the probability that is assigned, on the basis of the observed data, to the hypothesis as part of the method that has been outlined should be treated as a posterior probability that corresponds to the Bayesian update of some given prior density function for the parameter of interest , where the choice for this prior density, of course, does not depend on the data. However, to be able to sensibly use the Bayesian method being referred to some justification would need to be given as to why such a prior density function would have been a good representation of our beliefs about the parameter before the data were observed. The fact that, in the context of the scenario of interest in Definition 2, it is going to be extremely difficult, in general, to provide such a justification is consistent with the motivation for the method of bispatial inference that was given in the Introduction.

4 Bispatial-fiducial inference

The methodology of Sections 3.1 to 3.3 allows us to determine a post-data probability for the hypothesis being true. Clearly though, it would be preferable to have a post-data density function for the parameter of interest . For this reason, let us now consider generalising the methodology that has been proposed.

In particular, if

where is any given value of , then let us define the hypotheses and as:

| (16) |

otherwise, we will define these hypotheses as:

| (17) |

We can observe that a post-data distribution function for could be constructed if, for each value of within the range of allowable values for , we were able to consistently evaluate the post-data probability of the hypothesis that is applicable as defined by either equation (16) or (17). Obviously, it would be a little awkward to do this by directly assessing the likeliness of the hypothesis being true for all the values of concerned, however no assumption has been made regarding whether assessments of this type should be made directly or indirectly.

Therefore, we now will consider a strategy in which only one of these probability assessments is made directly, while all the other assessments of this type that are required will in effect be made indirectly by using again the method of organic fiducial inference. The application of this general strategy will be referred to as bispatial-fiducial inference.

4.1 First proposed method

Under the assumption that the hypothesis satisfies the more conventional definition of this type of hypothesis given in Section 3.3, let us assume that, after the data have been observed, we directly weigh up, and then determine a value for the probability of this hypothesis being true. This post-data probability will be denoted by the value , i.e. .

Furthermore, it will be assumed that the method of organic fiducial inference is used to derive a fiducial density function for conditional on not lying in the interval . In this approach to inference, the global pre-data (GPD) function (see Bowater 2019a) offers the principal, if not exclusive, means by which pre-data beliefs about a parameter of interest can be expressed. Given that it is being assumed that, under the condition that does not lie in the interval , nothing or very little would have been known about before the data were observed, it is appropriate to use a neutral GPD function for that has the following form:

| (18) |

where . On the basis of this GPD function, the fiducial density function of that is of interest can often be derived by applying what, in Bowater (2019a), was referred to as the moderate fiducial argument (when Principle 1 of this earlier paper can be applied). Alternatively, in accordance with what was also advocated in Bowater (2019a), this fiducial density can be more generally defined, with respect to the same GPD function for , by the following expression:

| (19) |

where is a normalising constant, and is a fiducial density for derived by applying the strong fiducial argument (as part of what is required by either Principle 1 or Principle 2 of Bowater 2019a) that would be regarded as being a suitable fiducial density for in a general scenario where it is assumed that there was no or very little pre-data knowledge about over all possible values of .

Given the assumptions that have been made, if the condition in equation (7) holds, which implies that is the hypothesis that , then it can be deduced that the post-data probability of the event is defined by:

| (20) |

where the probability is as defined at the start of this section, and is given by:

where denotes the fiducial probability of the event conditional on that is the result of integrating the fiducial density specified by equation (19) over those values of that satisfy the condition . Under the condition in equation (7), it also follows that the post-data density function of , which will be denoted simply as , is defined over all of its domain except for the interval by the expression:

| (21) |

where denotes the fiducial density specified by equation (19) conditioned on the event . To clarify, the density is being referred to as a post-data density because over the restricted space for in question it is defined on the basis of the post-data probability of the hypothesis , i.e. the value , and the fiducial density , which of course is a particular type of post-data density. While it has been assumed that the condition in equation (7) holds, it should be obvious, on the basis of symmetry, how to modify the definitions in equations (20) and (21) in cases where this condition does not hold, i.e. when is the hypothesis that .

Notice that the assignment of a probability to the hypothesis that is greater than or equal to the minimum value for this probability that was referred to at the end of Section 3.3 is a sufficient (but not a necessary) requirement for ensuring that the probability given in equation (20) is not negative. To clarify, the probability can be now more specifically expressed as:

| (22) |

where the fiducial density is defined as it was immediately after equation (19).

Furthermore observe that, if we are in the general case where , then although the definitions in equations (20) and (21) do not fully specify the form taken by the post-data density function of , this may not be a great problem if the aim is to only derive post-data probability intervals for , i.e. intervals in which there is a given post-data probability of finding the true value of . This is because the narrow interval over which this post-data density of is undefined may often lie wholly inside or outside of the probability intervals of the type in question that are of greatest interest. On the other hand, it will of course often be indispensible to have a full rather than a partial definition of the post-data density , e.g. for determining the post-data expectations of general functions of , and for simulating values from this kind of density function.

One way around this problem is to simply complete the definition of the post-data density function of by assuming that, when is conditioned to lie in the interval , it has a uniform density function over this interval. Therefore, the full definition of this post-data density would consist of what is required both by equation (21), and by the expression:

Again, since by definition the interval is narrow, this simple solution to the problem concerned may, in some circumstances, be considered adequate.

Nevertheless, it is a method that has two clear disadvantages. First, the post-data density function of that it gives rise to will, in general, be discontinuous at the values and . Second, the way in which the post-data density of conditional on the event is determined does not take into account our pre-data beliefs about , or the information contained in the data. Therefore, we will now try to enhance the methodology that has been considered in the present section with the aim of addressing these two issues.

4.2 A more sophisticated method

The method that has just been outlined is based on determining a fiducial density for conditional on lying outside of the interval using the neutral GPD function for given in equation (18). We now will attempt to construct a fiducial density for conditional on lying inside this interval using a more general type of GPD function for .

In particular, it will be assumed that this GPD function has the following form:

| (23) |

where is a given constant and is a continuous unimodal density function on the interval that is equal to zero at the limits of this interval. On the basis of this GPD function, the fiducial density of conditional on the event can often be derived by applying what, in Bowater (2019a), was referred to as the weak fiducial argument (see this earlier paper for further details). Alternatively, in accordance with what was also advocated in Bowater (2019a), this fiducial density can be more generally defined, with respect to the same GPD function for , by the following expression:

| (24) |

where the fiducial density is specified as it was immediately after equation (19) and is a normalising constant. Let us therefore make the assumption that this expression is used in conjunction with expressions identical or analogous to the ones given in equations (20) and (21) in order to obtain a full definition of the post-data density function of over all values of .

More specifically, though, it will be assumed that the constant in equation (23) is chosen such that this overall density function for is made equivalent to a fiducial density function for that is based on a continuous GPD function for over all values of . However, we will suppose that, except for the way in which the GPD function of is specified, this fiducial density is derived on the basis of the same assumptions as were used to derive the fiducial density . If the hypothesis is assigned a probability that is greater than the minimum value for this probability discussed in Section 3.3, i.e. the probability defined by equation (22), and the density is positive for all allowable values of , then the value of in question will always exist and be unique.

This criterion for choosing the value of will, in general, ensure that the post-data density function for being considered will be continuous over all values of . Also, if was conditioned to lie in the interval , then this post-data density would still be formed in a way that takes into account our pre-data beliefs about , and then allows these beliefs to be modified on the basis of the data. Therefore, the difficulties are avoided that were identified as being associated with the method that was proposed in the previous section.

Furthermore, there are two reasons why the criterion in question concerning the choice of the constant can be viewed as not being a substantial restriction on the way we are allowed to express our pre-data knowledge about the parameter . First, since going against this rule will in general lead to the post-data density of having undesirable discontinuities, it can be regarded as being a useful guideline in choosing a suitable GPD function for when is conditioned to lie in the interval . Second, any detrimental effect caused by enforcing this criterion may not be that apparent given the great deal of imprecision there will usually be in the specification of this GPD function.

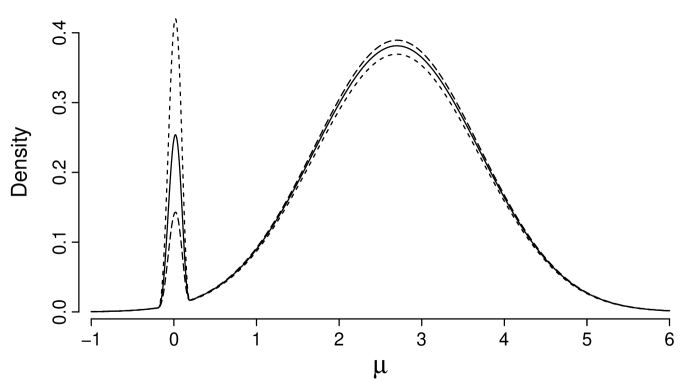

4.3 First example: Revisiting the simple normal case

To give an example of the application of the method proposed in the previous section, let us return to the problem of making inferences about the mean of a normal distribution that was considered in both Sections 2.7 and 3.4. All assumptions about the values of quantities of interest that were made in Section 3.4 will be maintained.

In this example, the fiducial density that was defined in Section 4.1, which now of course can be denoted as the density , can be directly derived by using the moderate fiducial argument (see Bowater 2019a), which implies that it is simply the normal density function of defined by the expression conditioned not to lie in the interval . To clarify, using the more general definition of the density in equation (19), the fiducial density , i.e. the density in the present case, would be the normal density of just mentioned.

Let us now make the assumption that the density function that appears in equation (23) is defined as being a beta density function for on the interval with both its shape parameters equal to 4. This density function clearly satisfies the conditions on the function that were given in Section 4.2. Furthermore, it is a reasonable choice for this function given that it is smooth, its mode is at and it is symmetric.

Given this assumption, if a sensible value was assigned to the probability of the hypothesis , then the precise form of the post-data density would be determined by the expression in equation (24) and expressions analogous to the ones given in equations (20) and (21). On the other hand, of course, this density function could have been defined according to the simple proposals for both its partial and full specification outlined in Section 4.1 without the need to have made an assumption about the form of the density .

The curves in Figure 1 represent the post-data density outside of the interval for all the definitions of this density function being considered, while, over the whole of the real line, they more specifically represent this function under its more sophisticated definition given in Section 4.2. The range of values for the probability , i.e. the probability , that underlies this figure is equal to what was proposed as being appropriate for this example in Section 3.4, i.e. the range of 0.03 to 0.08. In particular, the solid curve in Figure 1 depicts the post-data density when is 0.05, while the long-dashed and short-dashed curves in this figure depict this density when is 0.03 and 0.08 respectively. The accumulation of probability mass around the value of zero in these density functions is consistent with what we would have expected given the strong pre-data belief that would be close to zero, though as we know, the importance of this pre-data opinion about is assessed in the context of having observed the data value to obtain the density functions that are shown.

4.4 Second example: Revisiting the binomial case

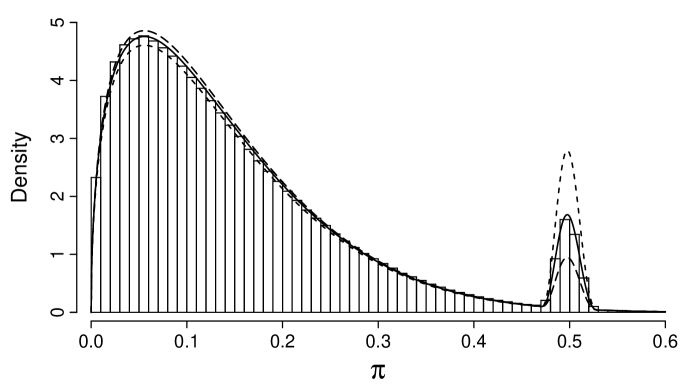

To give a second example of the application of the method being discussed, let us consider once more the problem of making inferences about a binomial proportion that was examined in Section 3.5, with the same assumptions in place about the values of quantities of interest that were made in this earlier section.

In using the method of organic fiducial inference in this example to derive the fiducial density that was specified for the general case immediately after equation (19) and which is required as an input in both this earlier equation and equation (24), it would again seem reasonable to define the LPD function as in equation (13). Also, as explained in Bowater (2019a), this fiducial density for will be fairly insensitive to the choice made for the LPD function in question. We will, in addition, assume that the density required by equation (23) is a beta density with both its shape parameters equal to 4, as it was in the previous example, but this time defined on the interval . As a result, we now can specify the post-data density using equations (20), (21) and (24), assuming again, of course, that a sensible value has been assigned to the probability of the hypothesis .

The histogram in Figure 2, which strictly speaking is a weighted histogram, represents this post-data density for the case where . The numerical output on which this histogram is based was generated by the method of importance sampling, more specifically by appropriately weighting a sample of three million independent random values from the fiducial density . On the other hand, the curves in Figure 2 represent approximations to the post-data density obtained by substituting the fiducial density used in its construction by the posterior density of the proportion that is based on the Jeffreys prior density for this problem, or in other words, based on choosing the prior density of to be a beta density function of with both its shape parameters equal to 0.5. Additional simulations showed that this method of approximation was satisfactory. In particular, the solid curve in Figure 2 approximates the density for the case where and, as was expected, it closely approximates the histogram in this figure. Similarly, the long-dashed and short-dashed curves in this figure approximate the density in question in the cases where is 0.03 and 0.08 respectively. Again, the range of values for being considered is 0.03 to 0.08, which is equal to what was proposed as being appropriate for this example in Section 3.5.

The accumulation of probability mass around the value of 0.5 in the density functions in Figure 2 is clearly an artefact of the strong pre-data opinion that was held about the proportion .

5 Extending bispatial-fiducial inference to multi-parameter problems

5.1 General assumptions

It was assumed in Section 2.1 that the parameter is the only unknown parameter in the sampling model. Let us now assume that all the parameters on which the sampling density depends are unknown.

More specifically, we will assume that the subset of parameters is such that what would have been believed, before the data were observed, about each parameter in this set if all other parameters in the model, i.e. , had been known, would have satisfied the requirements of the scenario of Definition 2 with being the parameter of interest . Furthermore, it will be assumed that the set of all the remaining parameters in the sampling model, i.e. the set , is such that, before the data were observed, nothing or very little would have been known about each parameter in this set over all allowable values of the parameter if all other parameters in the model, i.e. the set , had been known.

To derive the post-data density of any given parameter in the set conditional on all the parameters in the set being known, we can clearly justify applying the method outlined in Section 4.2, meaning that this density function would be defined by equation (24) and by expressions identical or analogous to the ones given in equations (20) and (21). The set of full conditional post-data densities that result from doing this for each parameter in the set would therefore be naturally denoted as:

| (25) |

It is also clearly defensible to specify the post-data density of any given parameter in the set conditional on all the parameters in the set being known as being the fiducial density that was defined immediately after equation (19). Doing this for each parameter in the set would therefore give rise to the following set of full conditional post-data densities:

| (26) |

5.2 Post-data densities of various parameters

If the complete set of full conditional densities of the parameters that results from combining the sets of full conditional densities in equations (25) and (26) determine a unique joint density for these parameters, then this density function will be defined as being the post-data density function of and will be denoted as . However, this complete set of full conditional densities may not be consistent with any joint density of the parameters concerned, i.e. these full conditional densities may be incompatible among themselves.

To check whether the full conditional densities of being referred to are compatible, it may be possible to use an analytical method. An example of an analytical method that could be used to try to achieve this goal was outlined in relation to full conditional densities of a similar type in Bowater (2018a).

By contrast, in situations that will undoubtedly often arise where it is not easy to establish whether or not the full conditional densities defined by equations (25) and (26) are compatible, let us imagine that we make the pessimistic assumption that they are in fact incompatible. Nevertheless, even though these full conditional densities could be incompatible, they could be reasonably assumed to represent the best information that is available for constructing a joint density function for the parameters that most accurately represents what is known about these parameters after the data have been observed, i.e. constructing, what could be referred to as, the most suitable post-data density for these parameters. Therefore, it would seem appropriate to try to find the joint density of the parameters that has full conditional densities that most closely approximate those given in equations (25) and (26).

To achieve this objective, let us focus attention on the use of a method that was advocated in a similar context in Bowater (2018a), in particular the method that simply consists in making the assumption that the joint density of the parameters that most closely corresponds to the full conditional densities in equations (25) and (26) is equal to the limiting density function of a Gibbs sampling algorithm (Geman and Geman 1984, Gelfand and Smith 1990) that is based on these conditional densities with some given fixed or random scanning order of the parameters in question. Under a fixed scanning order of the model parameters, we will define a single transition of this type of algorithm as being one that results from randomly drawing a value (only once) from each of the full conditional densities in equations (25) and (26) according to some given fixed ordering of these densities, replacing each time the previous value of the parameter concerned by the value that is generated. Let us clarify that it is being assumed that only the set of values for the parameters that are obtained on completing a transition of this kind are recorded as being a newly generated sample, i.e. the intermediate sets of parameter values that are used in the process of making such a transition do not form part of the output of the algorithm.

To measure how close the full conditional densities of the limiting density function of the general type of Gibbs sampler being presently considered are to the full conditional densities in equations (25) and (26), we can make use of a method that, in relation to its use in a similar context, was discussed in Bowater (2018a). To be able to put this method into effect it is required that the Gibbs sampling algorithm that is based on the full conditional densities in equations (25) and (26) would be irreducible, aperiodic and positive recurrent under all possible fixed scanning orders of the parameters . Assuming that this condition holds, it was explained in Bowater (2018a), how it may be useful to analyse how the limiting density function of the Gibbs sampler in question varies over a reasonable number of very distinct fixed scanning orders of the parameters concerned, remembering that each of these scanning orders has to be implemented in the way that was just specified. In particular, it was concluded that if within such an analysis, the variation of this limiting density with respect to the scanning order of the parameters can be classified as small, negligible or undetectable, then this should give us reassurance that the full conditional densities in equations (25) and (26) are, respectively according to such classifications, close, very close or at least very close, to the full conditional densities of the limiting density of a Gibbs sampler of the type that is of main interest, i.e. a Gibbs sampler that is based on any given fixed or random scanning order of the parameters concerned. See Bowater (2018a) for the line of reasoning that justifies this conclusion.

In trying to choose the scanning order of the parameters such that the type of Gibbs sampler under discussion has a limiting density function that corresponds to a set of full conditional densities that most accurately approximate the density functions in equations (25) and (26), we should always take into account the precise context of the problem of inference being analysed. Nevertheless, a good general choice for this scanning order could arguably be, what will be referred to as, a uniform random scanning order. Under this type of scanning order, a transition of the Gibbs sampling algorithm in question will be defined as being one that results from generating a value from one of the full conditional densities in equations (25) and (26) that is chosen at random, with the same probability of being given to any one of these densities being selected, and then treating the generated value as the updated value of the parameter concerned.

It is clear that being able to obtain a large random sample from a suitable post-data density of the parameters using a Gibbs sampler in the way that has been described in the present section will usually allow us to obtain good approximations to expected values of given functions of these parameters over the post-data density concerned, and thereby allow us to make useful and sensible inferences about the parameters on the basis of the data set of interest.

5.3 Post-data opinion curve

In constructing any one of the post-data densities in equation (25), there is, nevertheless, still one important issue that needs to be addressed, which is that the assessment of the likeliness of the relevant hypothesis in equation (9) or (11) will generally depend on the values of the parameters in the set . This of course will be partially due to the effect that the values of these parameters can have on the one-sided P value that appears in the definition of this hypothesis, i.e. the P value in terms of the notation used in equation (14). Therefore, in general, we will not need to assign just one probability to the hypothesis , but various probabilities conditional on the values of the parameters in the set .

Faced with the inconvenience that this can cause, it is possible to simplify matters greatly by assuming that the probability that is assigned to any given hypothesis , i.e. the probability , will be the same for any fixed value of the one-sided P value that appears in the definition of this hypothesis, no matter what values are actually taken by the parameters in the set . It can be argued that such an assumption would be reasonable in many practical situations. If this assumption is made then, the probability will clearly be a mathematical function of the one-sided P value . We will call this function the post-data opinion (PDO) curve for the parameter conditional on the parameters .

Notice that, when using the Gibbs sampling method outlined in the last section, we will only need to define this curve over the range of values of the P value that are likely to appear in the hypothesis having taken into account the data that have been observed. Also, it could be hoped that, in many cases, it would be possible to adequately specify this curve by first assessing the probability for a small number of carefully selected values of , and then fitting some type of smooth curve through the resulting points.

Furthermore, it is clear that there are rules which can be employed to ensure that any given PDO curve is chosen in a sensible manner. Perhaps the most obvious rule of this kind is that a PDO curve, in general, must be chosen such that, along this curve, the value of monotonically increases as the P value is increased from zero up to its maximum permitted value in the particular case of interest. Other characteristics that we would expect this type of curve to have will be discussed in the context of the examples that will be considered in the next two sections.

5.4 First example: Normal case with variance unknown

To give an example of the application of the method of inference that has just been proposed, i.e. bispatial-fiducial inference for multi-parameter problems, let us return to the example that was first considered in Section 3.5, however let us now assume that the difference in the performance of the two drugs of interest is measured by the difference in the concentration of a certain chemical (e.g. cholesterol) in the blood, in particular the level observed for drug A minus the level observed for drug B, rather than the preferences of the patients concerned. The set of these differences for all of the patients in the sample will be the data set . This example therefore also shares notable common ground with the example that was first considered in Section 2.5. Moreover, similar to this earlier example, it will be assumed that each value in the data set follows a normal distribution with an unknown mean , however, by contrast to this previous example, the standard deviation of this distribution will now also be assumed to be unknown.

For the same type of reason to that used in Example 2 in the Introduction, let us in addition suppose that, for any given value of , the scenario of Definition 2 would apply in relation to the parameter with the special hypothesis being the hypothesis that lies in the narrow interval . On the other hand, it will be assumed, as could often be done in practice, that nothing or very little would have been known about the standard deviation before the data were observed given any value for . Therefore, in terms of the notation of Section 5.1, the set of parameters will only contain , and the set will only contain .

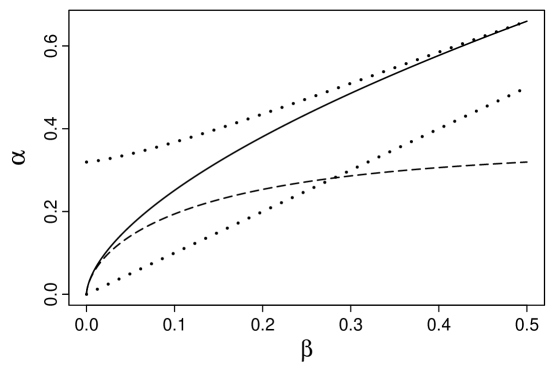

To determine the post-data density , the test statistic as defined in Section 3.2 will be assumed to be the sample mean , which clearly satisfies what is required to be such a statistic. Under this assumption, the hypotheses and will be as given in Section 2.7, except that now the mean takes the place of the value , the standard error takes the place of , and the random variable is substituted by , i.e. by the mean of an as-yet-unobserved sample of additional observations from the population concerned. If we more specifically assume, as we will do from now on, that , and , then it is evident that, since the condition in equation (7) does not hold in this case, the relevant hypotheses and can be defined as:

Clearly, the one-sided P value in the hypothesis depends on the standard deviation . Moreover, given that there is a one-to-one relationship between and this P value, the PDO curve for conditional on will completely describe the assessment of the probability of , i.e. the probability , in all possible circumstances of interest. To give a simple example, we will assume that this PDO curve has the algebraic form: . In Figure 3, this PDO curve is represented by the solid curve.

Similar to the example that was considered in Section 3.6, the fiducial density function of conditional on that is obtained by using the strong fiducial argument, i.e. the density , is defined by the expression . To clarify, what was referred to in Bowater (2019a) as being the fiducial statistic is here being assumed to be any sufficient statistic for , e.g. the sample mean . Using this simple analytical result, the lower dotted line in Figure 3 represents what the PDO curve under discussion would need to be so that the probability equals the probability that would be assigned to the hypothesis by the fiducial density . For the same reason that was given in Section 3.3, we would expect any choice for the PDO curve in question to be always higher than this dotted line, which is the case, as can be seen, for the PDO curve that has been proposed.

Using this proposed PDO curve, i.e. the function , and the fiducial density defined by equation (19) as inputs into the method described in Section 4.1 enables us to calculate, via equation (20), the post-data probability conditional on that lies in the interval , i.e. the probability , for any given value of the P value . The dashed curve in Figure 3 was constructed by plotting this post-data probability , rather than the probability , against different values for the P value . It can be seen that this curve is monotonically increasing, which is a desirable outcome. If this had not been the case, then it could have been quite reasonably concluded that the PDO curve on which this dashed curve is based does not represent logically structured beliefs about conditional on in the context of what has been assumed to have been known about before the data were observed.

Finally, the upper dotted curve in Figure 3 represents what the PDO curve of interest would need to be if, under the assumptions already made, we decided that independent of the size of the P value , we would place a post-data probability on lying in the interval that was equal to the limiting value assigned to this probability by the dashed curve as tends to 0.5, i.e. a probability of 0.32. Clearly, if this limiting value of the probability in question is regarded as being appropriate, then any sensible PDO curve in the case being considered would need to lie below this dotted curve and, as can be seen, the proposed PDO curve also satisfies this constraint.

If in addition we specify the density function , which is required by equation (23), i.e. the function in the present case, to be the same as it was in the example in Section 4.3, then the assumptions that have been made fully determine the post-data density in accordance with equation (24) and with expressions analogous to the ones given in equations (20) and (21). Furthermore, the fiducial density of conditional on that is obtained by using the strong fiducial argument, i.e. the density , is defined by the following expression:

where , i.e. it is a scaled inverse density function with degrees of freedom and scaling parameter equal to the variance estimator . If we assume, as we will do so from now on, that the sample variance is equal to 9, then under the other assumptions that have already been made, this fiducial density can be expressed as:

This density function will therefore be regarded as being the post-data density of conditional on in the example under discussion. Again to clarify, it has been assumed in deriving the fiducial density in question that the fiducial statistic is any sufficient statistic for , e.g. the variance estimator just defined.

To illustrate this example, Figure 4 shows some results from running a Gibbs sampler on the basis of the full conditional post-data densities of and that have just been defined, i.e. the densities and , with a uniform random scanning order of the parameters and , as such a scanning order was defined in Section 5.2. In particular, the histograms in Figures 4(a) and 4(b) represent the distributions of the values of and , respectively, over a single run of six million samples of these parameters generated by the Gibbs sampler after a preceding run of one thousand samples, which were classified as belonging to its burn-in phase, had been discarded. The sampling of the density was based on the Metropolis algorithm (Metropolis et al. 1953), while each value drawn from the density was independent from the preceding iterations.

![[Uncaptioned image]](/html/1911.09049/assets/x4.png)

In accordance with conventional recommendations for evaluating the convergence of Monte Carlo Markov chains outlined, for example, in Gelman and Rubin (1992) and Brooks and Roberts (1998), an additional analysis was carried out in which the Gibbs sampler was run various times from different starting points and the output of these runs was carefully assessed for convergence using suitable diagnostics. This analysis provided no evidence to indicate that the sampler does not have a limiting distribution, and showed, at the same time, that it would appear to generally converge quickly to this distribution.

Furthermore, the Gibbs sampling algorithm was run separately with each of the two possible fixed scanning orders of the parameters, i.e. the one in which is updated first and then is updated, and the one that has the reverse order, in accordance with how a single transition of such an algorithm was defined in Section 5.2, i.e. single transitions of the algorithm incorporated updates of both parameters. In doing this, no statistically significant difference was found between the samples of parameter values aggregated over the runs of the sampler in using each of these two scanning orders after excluding the burn-in phase of the sampler, e.g. between the two sample correlations of and , even when the runs concerned were long. Taking into account what was discussed in Section 5.2, this implies that the full conditional densities of the limiting distribution of the original Gibbs sampler, i.e. the one with a uniform random scanning order, should be, at the very least, close approximations to the full conditional densities on which the sampler is based, i.e. the post-data densities and defined earlier.

With regard to analysing the same data set , the curves overlaid on the histograms in Figures 4(a) and 4(b) are plots of the marginal fiducial densities of the parameters and , respectively, in the case where the joint fiducial density of these parameters is uniquely defined by the compatible full conditional fiducial densities and , which have already been specified in the present section, i.e. in the case where both the parameters and belong to the set referred to in Section 5.1. See Bowater (2018a) for further information about the general type of joint fiducial density of and in question, and to add a little more detail, let us clarify that the marginal fiducial density of being referred to is defined by:

The accumulation of probability mass around the value of zero in the marginal post-data density of that is represented by the histogram in Figure 4(a), and the fact that the upper tail of the marginal post-data density of that is represented by the histogram in Figure 4(b) tapers down to zero slightly more slowly than the aforementioned marginal fiducial density for are both clearly artefacts of the strong pre-data opinion that was held about .

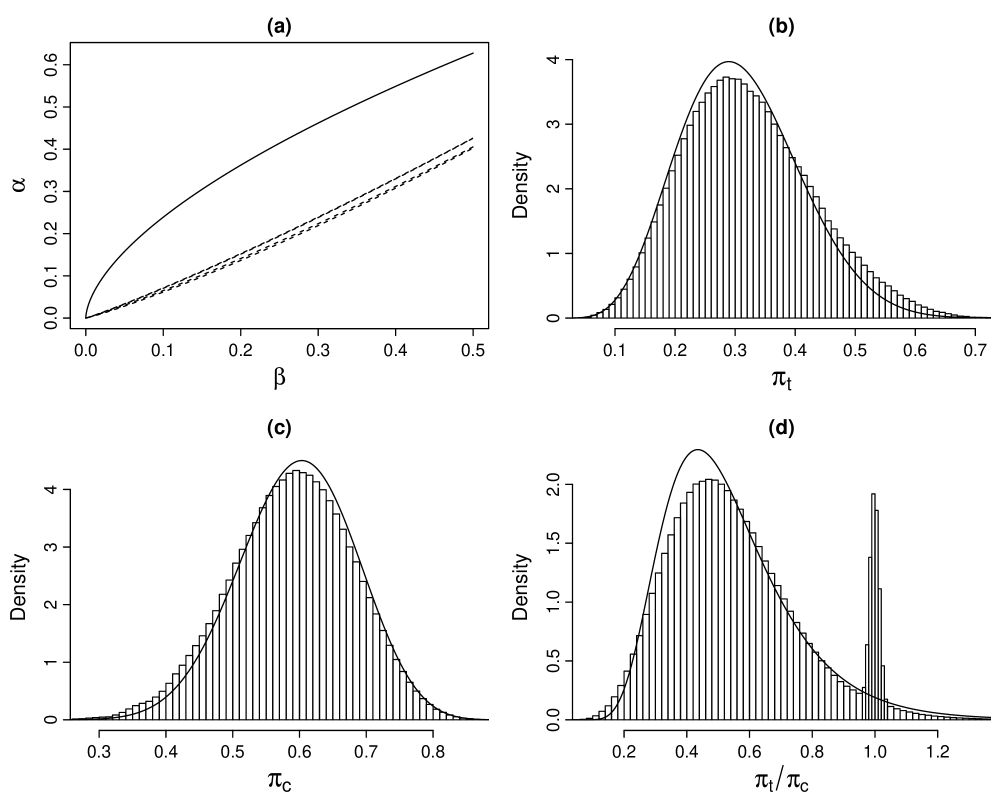

5.5 Second example: Inference about a relative risk

To go, in a certain sense, completely around the circle of examples considered in the present paper, let us now try to directly address the problem of inference posed in Example 2 of the Introduction, i.e. that of making inferences about a relative risk of a given adverse event of interest.

For the same reason as given in the description of this example, let us assume that the scenario of Definition 2 would apply if was unknown and was known, and also if was unknown and was known. In particular, if we define then, in the case where is the unknown parameter, the special hypothesis in this scenario will be assumed to be that , i.e. the odds of , lies in the following narrow interval:

where is a small positive constant, which is an interval that clearly contains , i.e. the odds of . In a symmetrical way, we will assume that, in the case where is the unknown parameter, the special hypothesis in the scenario of Definition 2 is that lies in the narrow interval . Of course, having a high degree of pre-data belief that logically implies that one should have a high degree of pre-data belief that , and also we can see that this is consistent with having a high degree of pre-data belief that the relative risk is close to one. As a result of what has just been assumed, it is clear that, in terms of the notation of Section 5.1, the set of parameters will contain both the parameters and , while the set will be empty.

In addition, we will assume that the full conditional fiducial densities and that were defined for the general case immediately after equation (19) are both specified such that they do not depend on the conditioning parameter concerned, and therefore are equivalent to the marginal fiducial densities and , respectively, which is a natural assumption to make given the independence of the data between the treatment and control groups. More specifically, let us suppose that each of these fiducial densities is defined in the same way as the fiducial density was defined in Section 4.4, i.e. on the basis of the LPD function given in equation (13).

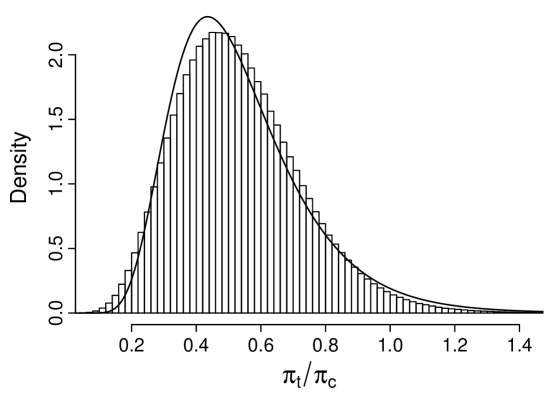

Although it would not of course be appropriate, given what was known about and before the data were observed, to use the joint fiducial density of and that is defined by the marginal fiducial densities and as a post-data density function of and in the present example, it would nevertheless be interesting to see what the marginal density of the relative risk over this joint fiducial density would look like. Therefore, the histogram in Figure 5 represents this marginal density of for the case where, in terms of the notation established for the present example in the Introduction, the observed counts are specified as follows: , , and . This histogram was constructed on the basis of a sample of three million independent random values drawn from the marginal fiducial density of concerned.