State Space Emulation and Annealed Sequential Monte Carlo for High Dimensional Optimization

Abstract

Many high dimensional optimization problems can be reformulated into a problem of finding the optimal state path under an equivalent state space model setting. In this article, we present a general emulation strategy for developing a state space model whose likelihood function (or posterior distribution) shares the same general landscape as the objective function of the original optimization problem. Then the solution of the optimization problem is the same as the optimal state path that maximizes the likelihood function or the posterior distribution under the emulated system. To find such an optimal path, we adapt a simulated annealing approach by inserting a temperature control into the emulated dynamic system and propose a novel annealed Sequential Monte Carlo (SMC) method that effectively generating Monte Carlo sample paths utilizing samples obtained on the high temperature scale. Compared to the vanilla simulated annealing implementation, annealed SMC is an iterative algorithm for state space model optimization that directly generates state paths from the equilibrium distributions with a decreasing sequence of temperatures through sequential importance sampling which does not require burn-in or mixing iterations to ensure quasi-equilibrium condition. Several applications of state space model emulation and the corresponding annealed SMC results are demonstrated.

Keywords: Emulation, State Space Model, Sequential Monte Carlo, Optimization, Simulated Annealing.

1 Introduction

High dimensional global optimization algorithms are being widely investigated since more and more applications involve high dimensional complex data nowadays. The gradient descent algorithm and its variations (Bertsekas, 1997) require the objective function to be convex or uni-modal so that the found local optimal is global. Recent research in machine learning involves many non-convex optimization problems (Anandkumar et al., 2014; Arora et al., 2012; Netrapalli et al., 2014; Agarwal et al., 2014). However, many non-convex problems remain NP-hard and the theory is only available for their convex relaxations (Jain et al., 2017). Deterministic optimization algorithms (for example, Hooke and Jeeves, 1961; Nelder and Mead, 1965; Land and Doig, 1960) may result in certain type of exhaustive search, which is computationally expensive in a high dimensional space. Stochastic optimization algorithms utilizes Monte Carlo simulations to explore the parameter space in a stochastic and often more efficient way (Kiefer et al., 1952; Kirkpatrick et al., 1983; Mei et al., 2018).

In this article, we propose an emulation approach that reformulates a high dimensional optimization problem into the problem of finding the most likely state path problem in a state space model. The state space models is a class of models that describes the behavior of a usually high-dimensional random variable in a form of dynamic evolution, with wide applications in mathematics, physics and many other fields. Many high-dimensional optimization problems can be transformed to finding the optimal state path under an equivalent state space model, whose likelihood function shares the same general landscape as the objective function of the original optimization problem. To be more specific, for a high-dimensional optimization problem with the objective function , we construct an emulated state space model whose likelihood function is proportional to a Boltzmann-like distribution , where is the inverted temperature.

There are several existing heuristic approaches using the emulation idea. Cai et al. (2009) transforms a regression variable selection problem with many predictors into an optimization problem over the high dimensional binary space , which can be further converted to the most likely path problem in a state space model with binary-valued states indicating the variable selection, even though the predictors have no chronological order in nature. Kolm and Ritter (2015) reformulates a portfolio optimization problem to a state space model by mapping the utility function to the log-likelihood function. The utility function is then optimized through finding the most likely path in the corresponding state space model by applying the Viterbi algorithm (Viterbi, 1967) over Monte Carlo samples. Similarly, Irie and West (2016) relates the multi-period portfolio optimization problem to the log-likelihood of a mixture of linear Gaussian dynamic systems and proposed an algorithm based on the Kalman filter (Kalman, 1960) and EM algorithm (Dempster et al., 1977) to find the most likely path.

These studies map high dimensional optimizations to a problem under state space model settings. However, it remains a challenging problem to find the most likely path analytically and numerically. For example, the approach in Cai et al. (2009) is difficult to be generalized to a continuous space. The Viterbi algorithm used in Kolm and Ritter (2015) requires the dynamic system to be Markovian and non-singular and it needs a large sample size in general to achieve high accuracy. The combination of Kalman filter and EM algorithm proposed in Irie and West (2016) works only when the underlying distribution can be represented as a mixture of Gaussian distributions.

In this paper, we propose a new Sequential Monte Carlo (SMC) based simulated annealing approach, named annealed SMC, to find the most likely path in a state space model. The SMC algorithm is a class of Monte Carlo methods that draws samples from the state space model systems in a sequential fashion. With the sequential importance sampling and resampling (SISR) scheme, SMC is extremely powerful in sampling from complex dynamic systems, especially for the state space models (Gordon et al., 1993; Kitagawa, 1996; Kong et al., 1994; Liu and Chen, 1995, 1998; Pitt and Shephard, 1999; Chen et al., 2000; Doucet et al., 2001). For a high-dimensional optimization problem with the objective function , we construct an emulated state space model whose likelihood function is proportional to a Boltzmann-like distribution , where is the inverted temperature. To mimic the (physical) annealing procedure in a non-interactive, non-quantum thermodynamic system (Kirkpatrick et al., 1983), we choose a sequence of decreasing temperatures , which corresponds to a sequence of emulated state space models.

We start from drawing sample paths from the base emulated state space model at a high base temperature . Samples from a low temperature (large ) system are close to the optimal sample path since the distribution is sharp at a low temperature, but drawing from such a distribution directly is usually difficult. With annealed SMC, samples of a low temperature system can be obtained by utilizing samples obtained at higher temperature. Eventually, all the SMC sample paths converge to the most likely one. The sequence of temperatures provides a slow-changing path from the base emulated state space model at , which is easy to sample from but not very useful for optimization, to the target emulated state space model at , which is difficult to sample but provides solutions to the optimization problem.

Four examples of state space emulation and their corresponding simulation experiments will be demonstrated. The smoothing spline optimization problem (Green and Silverman, 1993) is emulated by a state space model in which the function value and its first two derivatives of the spline function at every knot are formulated as a 3-dimensional vector AR process. A regularized regression problem with covariates, such as the ridge regression and LASSO (Tibshirani, 1996) setting, is transformed into a state space model of length , where the coefficients form the hidden states. The 1 trend filtering problem (Kim et al., 2009) is emulated by an AR(2) model with Laplace evolutions. In constructing an optimal stock trading strategy with transaction cost consideration (Kolm and Ritter, 2015), the hidden states of the emulated system consist of stock positions during the period of consideration, and the profit/loss is formulated into the observation part and the transaction costs are taken into state dynamics.

The rest of the paper is organized as follows. Section 2 first briefly reviews state space models then introduces the principles of state space emulation. Four emulation examples are provided in Section 2.3. Section 3 introduces the framework of annealed SMC designed to find the most likely path. The practical details of using the algorithm are discussed. Simulation results corresponding to the four examples in Section 2.3 are shown in Section 4. Section 5 concludes.

2 State Space Model and State Space Emulation

2.1 State Space Model

State space model is a class of models for describing the mechanism of a sequence of observations with a sequence of latent variables . The latent variables are assumed to follow a discrete-time stochastic process governed by the state equations

| (1) |

for , and follows its marginal distribution . When the distribution of conditioned on does not depend on such that , the system is Markovian. The observations are generated conditionally independently according to the corresponding latent variables through the observational equations

| (2) |

for . In inference problems, the formulas of the state equations and the observation equations are usually known except a set of unknown parameter of interest . In this paper, we assume and are completely known with no unknown parameters, and we are interested in inference on the latent states . Estimating from the observations under the likelihood principle is known as the most likely path problem in hidden Markov models.

In terms of estimating , the state equations provide the prior information

| (3) |

and the observation equations serve as the likelihood functions

| (4) |

A maximum-a-posterior (MAP) estimator can be obtained by maximizing the posterior function in (5).

| (5) |

When both and are Gaussian, the maximum of (5) can be obtained easily using Kalman filter and smoother (Kalman, 1960). In general cases when an analytic solution to optimize (5) is infeasible, the MAP estimator can be obtained by drawing sample paths from the posterior distribution . We will discuss details in estimating most likely path using Monte Carlo methods in Sections 3.2 and 3.3.

2.2 State Space Emulation

We propose a state space emulation approach for solving high dimensional optimization problems. The approach constructs a state space model so that the original optimization problem is equivalent to finding the most likely state path under the state space model.

Let be the objective function to be minimized and be a monotone decreasing function. Then minimizing is equivalent to maximizing such that

Furthermore, if there exists a state space model whose posterior function (5) is proportional to such that

with artificially designed state equations , and observation equations , we call the state space model an “emulated” state space model. The observations can be either certain observations involving in the original optimization problem (e.g. the observed points in the smoothing spline problem in Section 2.3.1) or artificially designed. Note that it is always possible to rewrite any joint distribution function in the form of (3) as

where and . Often such a series of conditional distribution is difficult to sample from or to be evaluated. However, in certain problems as our examples shown later, it is possible to reformulate the conditional distribution to , in which is easy to generate sample from and is easy to be evaluated, for some designed . Minimizing the objective function is then the same as finding the most likely path for the emulated state space model. The emulated state and observation equations provide guidance for annealed SMC implementation, even though they are artificial.

A common choice for the function is the Boltzmann distribution function

| (6) |

where is a positive constant that relates to the temperature in statistical physics. In statistics, the Boltzmann function in (6) links the least square method to the maximum likelihood approach with i.i.d. Gaussian noise. With this choice of , the system has a physical interpretation: The objective function is regarded as the possible energy levels in a non-quantum thermodynamic system. Assuming no interactions, the number of particles at the energy follows the Boltzmann distribution under thermodynamic equilibrium. The integrability of ensures the existence of the canonical partition function such that this physical canonical system is valid. The minimization of is now equivalent to find the base energy level, which inspires the use of simulate annealing of this thermodynamic system. More details will be discussed in Section 3.

2.3 Examples

2.3.1 Cubic Smoothing Spline

Consider a nonparametric regression model

with equally spaced . Without loss of generality, let and treat it as time.

The cubic smoothing spline method (Green and Silverman, 1993) estimates a continuous function by minimizing

| (7) |

The first term in (7) is the total squared tracking errors at the observation times and the second term is the penalty term on the smoothness of the latent function , where controls the regularization strength. Given the values of , the minimizer of the second term is a natural cubic spline that interpolates (see Green and Silverman (1993)). Hence, the solution to minimize (7) is a natural cubic spline, which is second-order continuously differentiable and is a cubic polynomial in all intervals for and is linear outside .

Define the derivatives of at each observation at time t as

By the constraints of natural cubic spline, we have the following recursive relationships:

with . Furthermore, by substituting with in the expressions of and , we have

| (8) | ||||

| (9) |

We will use the recursive relationships in (8) and (9) for the construction of state space emulation. With this notation, the second term in (7) can be expended as

In this case, the original optimization problem (7) over all second order differentiable functions becomes minimizing

| (10) |

where satisfies the recursive relationships (8) and (9) and the boundary condition . Note that completely defines the cubic smoothing spline solution .

With a positive inverted temperature , an emulated state space model is one such that whose likelihood of conditioned on is , with defined in (10). One possible way to decompose into the likelihood of a state space model is the following.

| (11) |

where , the “temperature” parameter, controls the shape of the distribution.

2.3.2 Regularized Linear Regression

LASSO (Tibshirani, 1996) is a widely-used regularized linear regression estimation procedure that can perform variable selection and parameter estimation at the same time.

Consider the regression model

where are the covariates that are used to model the dependent variable and . A LASSO estimator of is the minimizer of

| (14) |

For a fixed set of , for , define the partial residual as

| (15) |

and . Since

we have

| (16) |

Let and . An emulated state space model can be designed so that

| (17) |

The first term of (17) leads to the state equation

| (18) |

and the second term leads to the observation equation

| (19) |

where

with observation for all .

Note that is a function of as defined in (15) and is available at time . The observation equation and the observation value are imposed to incorporate in . The emulation for LASSO can be extended to other penalized regression with different penalty terms by changing accordingly.

2.3.3 Optimal Trading Path

In asset portfolio management, the optimal trading path problem is a class of optimization problems which typically maximizes certain utility function of the trading path (Markowitz, 1959). Kolm and Ritter (2015) and Irie and West (2016) proposed to turn such an optimization problem to an emulated state space model. To be more specific, let be a trading path in which represents the position held at time . Kolm and Ritter (2015) propose to maximize the following utility function.

| (20) |

where is a predetermined optimal trading path in an ideal world without trading costs, typically obtained by maximizing the risk-adjusted expected return under the Markowitz mean-variance theory (Markowitz, 1959). Kolm and Ritter (2015) provides a construction of based on the term structure of the underlying asset’s alpha (the excess expected return relative to the market). Let represent the transaction cost which is often assumed to be a quadratic function of the absolute position change . Without loss of generality, we parametrize it as

where is a non-negative constant related to the volatility and liquidity of the asset (Kyle and Obizhaeva, 2011). Let be the utility loss due to the departure of the realized path from the ideal path. We use the squared loss

Then the objective function is

Taking the position constraint into consideration as discussed in Cai et al. (2019), an emulated state space model can therefore be constructed as

| (21) | ||||

| (22) |

With the state equation (21) and the observation equation (22), the corresponding state space model has a likelihood function proportional to .

2.3.4 L1 Trend Filtering

L1 trend filtering (Kim et al., 2009) is a variation of Hodrick-Prescott filtering (Hodrick and Prescott, 1997). An 1 trend filtering on is defined to be the minimizer of the objective function

| (23) |

Minimizing (23) tends to produce a piece-wise linear function due to the penalty on second-order difference. An emulated state space model is designed to have the following Boltzmann likelihood function.

| (24) |

The first term of (24) leads to the observation equation

| (25) |

where with . The second term of (24) leads to the following second order auto-regressive process on the states

| (26) |

where with .

3 Annealed Sequential Monte Carlo

3.1 Sequential Monte Carlo (SMC)

The sequential Monte Carlo (SMC) method is a class of sampling methods designed for state space models. It utilizes the sequential nature of the state space model and draw samples incrementally with sequential importance sampling and resampling (SISR) scheme. A typical SMC approach is demonstrated in Figure 1.

Figure 1: Sequential Monte Carlo (SMC) Algorithm • Draw from and initialize all weights for . • At times : – Propagation: For , * Draw from distribution and set . * Update weights by setting – Resampling (optional): * Assign a priority score to each sample , . * Draw samples from the set with replacement, with probabilities proportional to . * Let and . * Return the new set . • Return the weighted sample set .

The function in the propagation step in Figure 1 is the proposal distribution. As discussed in Lin et al. (2013), the “perfect” choice for the proposal is the conditional distribution with full information set such that . However, in most cases, this conditional probability is impossible to evaluate or to sample from at time . The priority score is the weight used in the resampling step, which quantifies the sampler’s preference over different sample paths. The most common choice of is . Different variations of the SMC algorithm choose different proposal distributions and different priority scores. The Bayesian particle filter (Gordon et al., 1993) sets . It works well when the observations are relatively noisy compared with the state equation part. With accurate observations, the independent particle filter (Lin et al., 2005) uses . As an important (with certain additional cost) compromise over the Bayesian particle filter and the independent particle filter, Kong et al. (1994) and Liu and Chen (1998) suggests to adopt to reduce variance. Other sequential Monte Carlo methods focus on finding more appropriate priority scores in resampling with the help of future information. The auxiliary particle filter (Pitt and Shephard, 1999) conducts resampling with the priority score . The delayed sampling method (Chen et al., 2000; Lin et al., 2013) looks ahead steps further and uses .

In emulation for optimization, we are more interested in generating samples in the high probability region of , hence our problem is essentially a smoothing problem. Briers et al. (2010) proposed to use a generalization of two-filter smoothing formula to sample approximately from the joint distribution . Additional local MCMC moves can be adopted to fight degeneracy (Gilks and Berzuini, 2001). Many other SMC smoothing algorithm implementations are proposed to reduce the potential degeneracy in samples. See, for example, Godsill et al. (2004); Del Moral et al. (2010); Briers et al. (2010); Guarniero et al. (2017)

3.2 Finding the Most Likely Path

With emulation, finding the optimum of is now equivalent to finding the mode, or the most likely state path (MLP), of ,

| (27) |

with defined in (5) and being the common support for all latent variables. By construction, the mode, which is the optimum of , does not depend on used in (6).

In this article, we focus on finding the MLP from Monte Carlo samples. A set of weighted Monte Carlo samples from the distribution can be generated by Sequential Monte Carlo (SMC) and its various implementation schemes. Let be the samples drawn from the emulated state space model using the SMC algorithm in Figure 1. A natural and easy way is to use the empirical MAP path such that

| (28) |

Although the empirical MAP involves the least computation given the Monte Carlo samples, it usually requires a very large sample size to achieve high accuracy, especially when the dimension is large.

Note that when we use the Boltzmann-like target distributions as in the examples shown above, the MLP is the same under different . However the distribution is more flat for small (high temperature) and is more concentrated around the MLP for large . Hence the empirical MAP path tends to be more accurate if the Monte Carlo samples are generated from the target distribution with large . When is sufficiently large, the average sample path is also a good estimate of the MAP. However, it is much more difficult to generate Monte Carlo samples with large due to the tendency of being trapped in local optimum. Simulated annealing approach provides a natural bridge to link the high temperature system with easily generated samples with the low temperature system with more accurate estimates.

3.3 Annealed SMC

We propose a simulated annealing algorithm for sequential Monte Carlo on state space models. The idea comes from the thermodynamics analogue discussed in the previous section. When the function is chosen to be Boltzmann-like as in (6), the Monte Carlo samples from the emulated state space models correspond to a random sample set from the non-interacting particles in a thermodynamic equilibrium system as discussed in Section 2.2. If the temperature cools down to slowly enough such that the system is approximately in thermodynamic equilibrium for any temperature in between, all particles will condense to the base energy level. The idea of simulated annealing to analogize the physical system was proposed and discussed in Kirkpatrick et al. (1983).

To mimic the thermodynamic procedure, we propose the following system to simulate the annealing procedure for the SMC samples. Let be an increasing sequence of inverse temperatures. Suppose at , a base emulated state space model is constructed as

| (29) |

At a higher inverse temperature , an emulated state space model can be induced from (29) such that

| (30) |

where

are the corresponding state equations and observation equations at . The starting inverse temperature is usually chosen to be relatively small such that the function is relatively flat and is easy to sample from by SMC. We start with , draw from the base emulated state space model . For , new samples are drawn with respect to the distribution utilizing samples obtained at . The procedure is depicted in Figure 2. The annealed sequential Monte Carlo uses the following proposal distribution at temperature :

| (31) |

where the conditional distribution is an estimate of and can be obtained from the Monte Carlo samples under . We will discuss how to obtain such an estimate later. Since increases slowly, and are reasonably close.

Figure 2: Annealed Sequential Monte Carlo Algorithm • Draw from with SMC in Figure 1, using a set of proposal distributions . • For , draw from with SMC in Figure 1 using the proposal distribution where the right hand side is an estimate of . • Obtain an estimate of the most likely path from

With a sufficiently large , samples from the target distribution are highly concentrated around the true optimal path and hence are useful in inferring the most likely path. However, sampling from directly is usually difficult due to the challenge in finding appropriate proposal distributions, which significantly affects the Monte Carlo sample quality. Annealed SMC provides an iterative procedure to the difficult sampling problem under by utilizing the samples obtained at higher temperature. On one hand, annealed SMC provides a relatively “flat” and easy-sampling starting distribution and designs a slow-changing path connecting to the desired “sharp” distribution . On the other hand, for each iteration , annealed SMC adopts an optimal proposal distribution , which incorporates the full information set and is usually difficult to evaluate in conventional SMC implementations. In annealed SMC, the proposal distribution is estimated by sample paths from the previous iteration. The details in estimating the proposal distribution will be discussed in Section 3.4.

The conventional simulated annealing algorithm (Kirkpatrick et al., 1983) is a variation of Markov Chain Monte Carlo (MCMC), which adapts Metropolis-Hastings algorithm (Metropolis et al., 1953; Hastings, 1970) with an extra temperature control. The convergence of the conventional simulated annealing algorithm is given by Granville et al. (1994). However, different from the conventional simulated annealing, annealed SMC does not require for a mixing condition as usually shown in MCMC algorithms. At each iteration at , the samples are always properly weighted with respect to the target distribution because of the weight adjustments. The convergence of SMC samples is discussed in Crisan and Doucet (2000).

3.4 Practical Issues

In annealed SMC, at temperature , we need to estimate the proposal distribution with the sample paths from the previous iteration . Notice that, the weighted samples follow the distribution . Therefore, estimating the proposal distribution is equivalent to estimating the conditional distribution from a sample set drawn from the joint distribution. Here we mention two methods to sample from such a conditional probability.

Parametric Approach. For each time , suppose is a parametric family of distributions defined on and indexed by . The joint distribution of conditioned on under is approximated by one of the distributions in the family. Specifically, let

where is the corresponding probability density/mass function of . Denote the conditional probability induced from as . The joint distribution of is approximated by and the proposal distribution is estimated by .

One common choice for the distribution family is the multivariate Gaussian distributions. In this case,

The optimal parameter can be obtained by sample mean and sample variance such that

Denote

Then the induced conditional probability has the following closed-form:

where the parameters are

The results above for multivariate Gaussian distributions can be easily extended to mixture Gaussian distributions, which can approximate most distributions well.

Nonparametric Approach.

When there is no appropriate distribution family to describe the joint distribution of , one can sample from the conditional distribution of nonparametrically. Specifically, suppose and are kernel functions for and , respectively, and it is easy to sample from . For any given , Figure 3 depicts the nonparametric approach to draw from the conditional distribution when the samples properly weighted to are available.

Figure 3: Sample nonparametrically from a Empirical Conditional Distribution For given , • draw from with probabilities proportional to • draw from the density induced by . • return .

The parametric approach often requires the state space model to satisfy certain conditions. For example, when both state equations and observation equations are approximately linear and Gaussian, the multivariate Gaussian distribution family can be used to estimate the conditional distributions. The nonparametric approach can deal with general state space models. However, it often costs much more computing power than the parametric approach.

One issue for both approaches is the high dimensionality. Unless the system has a short memory, the conditional distribution at time involves the high dimensional and with potentially increasing dimension of parameter needed or the dimensions of spaces the nonparametric approach need to operate within. One solution for reducing dimension of the sampling problem is to use a low-dimensional sufficient statistics. Suppose is a low-dimensional sufficient statistic such that . Both parametric and nonparametric approaches can therefore be conducted on the joint distribution of , which is of lower dimension. In a Markovian system, and the problem reduces to sampling from a much simpler distribution. In an auto-regressive system with lag , , which is a -dimensional system. Note that since the estimated conditional distribution is used as a proposal distribution, it is often tolerable to use less accurate estimators for computational efficiency. Hence various approximation and dimension reduction tools can be used, including variational Bayes approximations (Tzikas et al., 2008).

Another issue in estimating the conditional distribution from sequential Monte Carlo samples is the sample degeneracy. In SMC, degeneracy refers to the phenomenon that the number of distinct values for some states such as can be less than the number of Monte Carlo samples, if resampling steps are engaged. The degeneracy problem is crucial for both approaches in sampling from the conditional distribution. Therefore, at , we suggest to conduct resampling only when all propagation steps are finished to prevent the samples from trapping into local maximums. When high degeneracy is persistent, we suggest to use post-MCMC steps (Gilks and Berzuini, 2001) to regenerate the samples. If the system is reversible and SMC can be implemented backward in , alternating forward and backward sampling through the annealing iterations may also reduce the degeneracy problem as it starts with more diversified samples in each temperature iteration.

3.5 Path refinement with Viterbi algorithm

A more accurate estimate of the mode can be obtained by using Viterbi algorithm (Viterbi, 1967) on the discrete space consisting of the SMC samples. Viterbi algorithm is a dynamic programming algorithm originally used to solve the MLP problem in hidden Markov models, where the hidden states are finite. Let be the grid points for and be the Cartesian product of the grid point sets. In state space models, the Viterbi algorithm searches for the maximum over all possible combinations of the grid points in . Specifically, the MLP obtained by the Viterbi algorithm is

| (32) |

The Viterbi algorithm for state space models based on the grid points is depicted in Figure 4.

Figure 4: Viterbi Algorithm for Markovian State Space Models • Let be a set of grid points for for . • At time 1, initialize and for . • At each time , for , set (33) and set , where is the optimal point of (33). • Let return .

The SMC samples drawn from the emulated state space model provides a set of grid points for the Viterbi algorithm. For example, one can set such that is the joint set of all SMC sample points. One can also add and remove grids points to expand coverage with more details around the more important state paths.

The Viterbi algorithm explores all combination of sample points and results in a better mode estimation compared with the empirical MAP in (28). However, it has its limitations for implementation with state space models. One limitation is that the Viterbi algorithm only works on Markovian state space models. In addition, it only works with a non-singular state evolution in which the degree of freedom is the same as the state variable dimension. Otherwise, state paths cannot be re-assembled as Viterbi algorithm tries to achieve. For example, in the cubic spline problem, the state evolution is singular. Although one can reduce the dimension of the state variable to make the evolution non-singular, the state evolution then becomes non-Markovian. Another limitation is the requirement for Monte Carlo sample size. The Monte Carlo samples induced provide a discretization of the support for each time . The accuracy of the Viterbi algorithm strongly dependents on the discretization quality, especially when is continuous. In general, the denser the Monte Carlo samples are around the true MLP, the more accurate the Viterbi algorithm solution is. As a result, it often requires a large Monte Carlo sample size to generate better discretization and to achieve high accuracy with Viterbi algorithm. To reduce the path error by half, the Monte Carlo sample size needs to be doubled, because the discretization size is reduced by half on average with doubled sample size. On the other hand, the computational cost increases quadratically with the sample size . One possible way to improve is to apply Viterbi algorithm iteratively by shrinking to the high value region of last iteration and regenerating grid points there. Similar to iterative grid search, the iterative Viterbi algorithm may result in a sub-optimal solution.

4 Simulation Results

4.1 Cubic Smoothing Spline

In this simulation study, we consider the cubic smoothing spline problem in Section 2.3.1. The observations are generated by

for , with and we fix in the objective function (7).

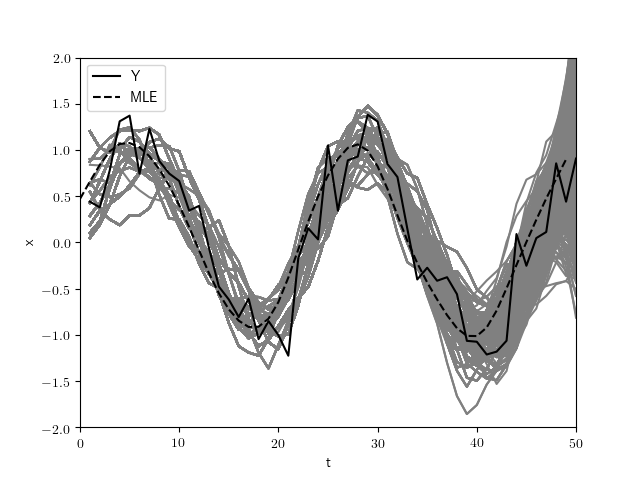

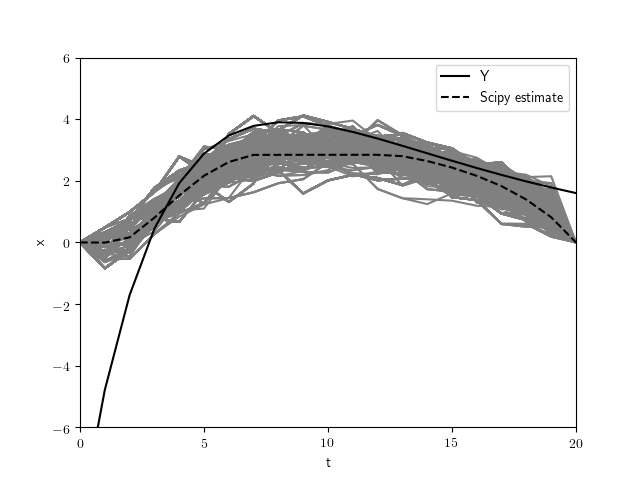

Since the dynamic system is linear and Gaussian, the most likely path is obtained by Kalman Smoother (Kalman, 1960). We use it as the benchmark. We start from the initial inverse temperature . Figure 5 demonstrates samples (in grey) drawn from the target distribution by the SMC algorithm described in Figure 1 along with the observations (the solid line) and the true most likely path (the dashed line).

The proposal distribution used at is chosen to be proportional to . At each time , is drawn from the proposal distribution , which is a Gaussian distribution in this case. Resampling is conducted when the effective sample size (ESS) defined in (34) is less than .

| (34) |

To find the most likely path stochastically and numerically, we apply the annealed SMC approach in Figure 2 with a predetermined sequence of inverted temperatures for . The proposal distribution for the anneal SMC is estimated by the parametric approach. Specifically, since the innovation in the state equation is of one dimension, at , we only need to generate proposal samples for . It is drawn by first fitting with a multivariate Gaussian distribution and then sampling from the conditional distribution. To prevent degeneracy, resampling step is only conducted in the end of each annealing SMC iteration and after each iteration, one step of post-MCMC move is conducted to regenerate sample states. The post-MCMC move uses blocked Gibbs sampling (Jensen et al., 1995), due to the special structure of the state dynamic. At each iteration of the Gibbs sampling, are updated together.

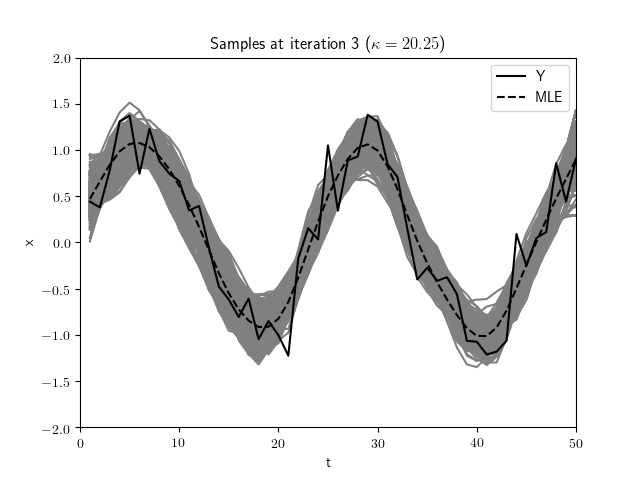

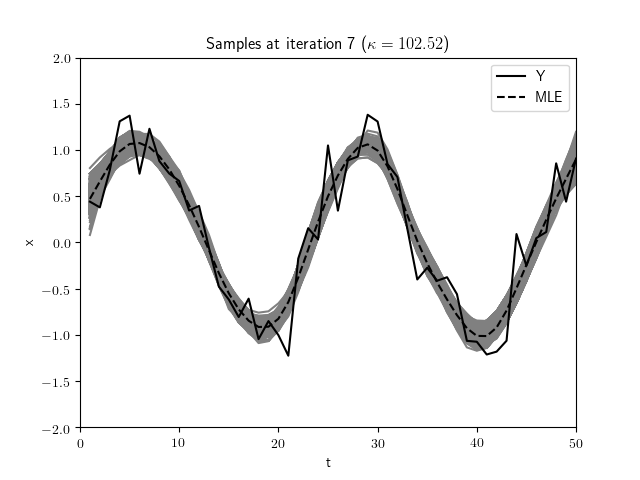

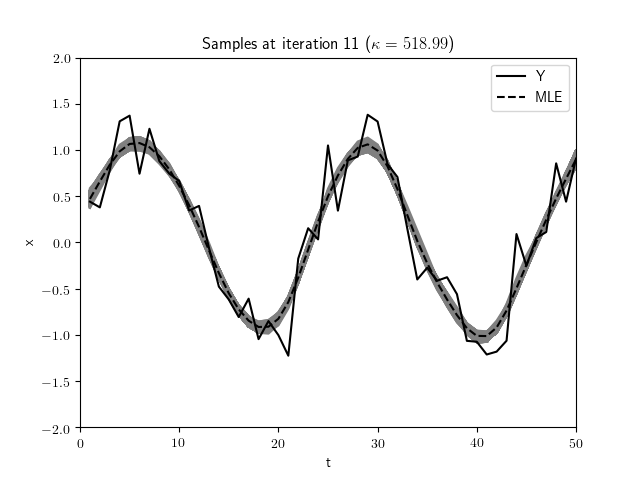

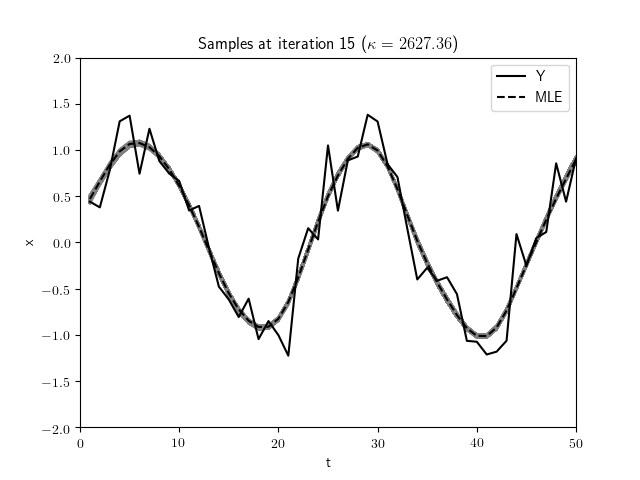

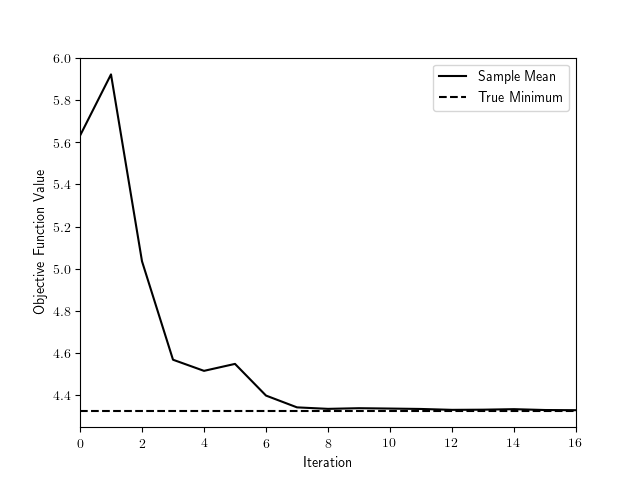

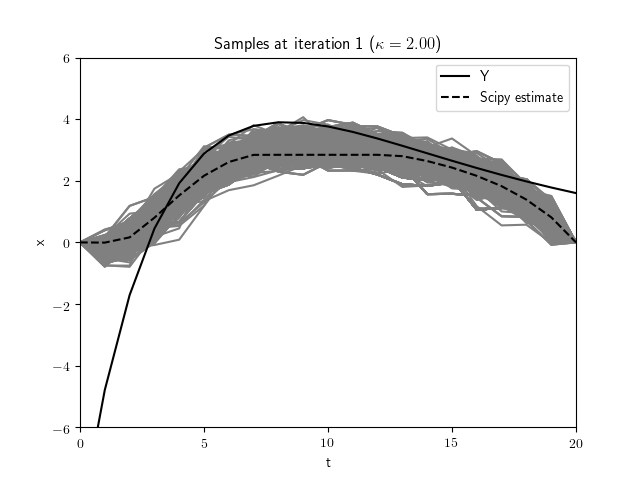

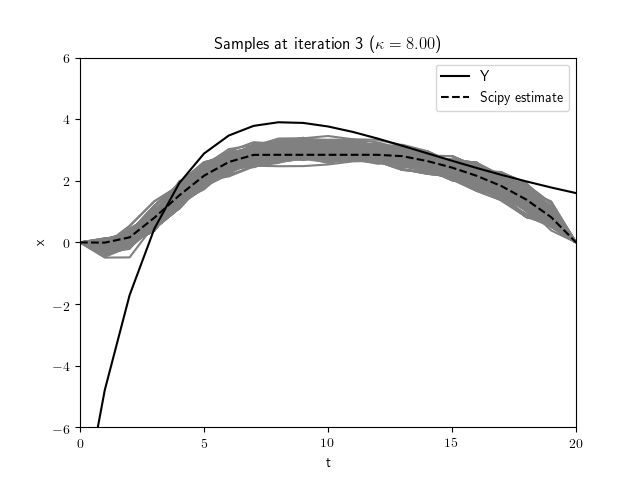

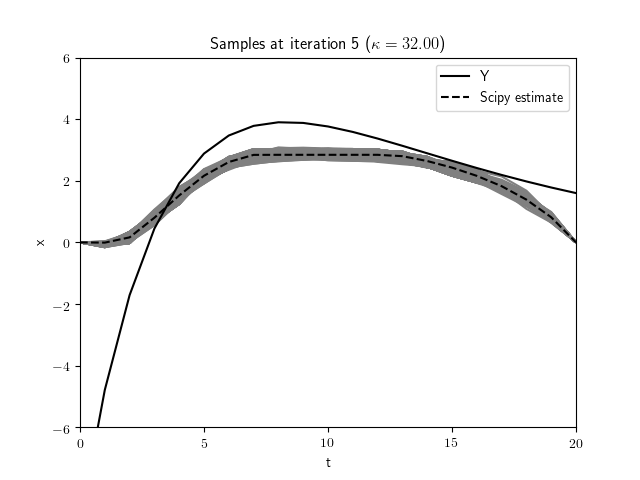

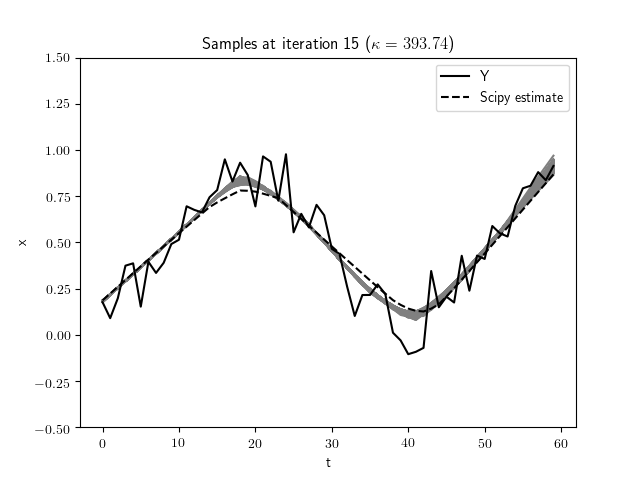

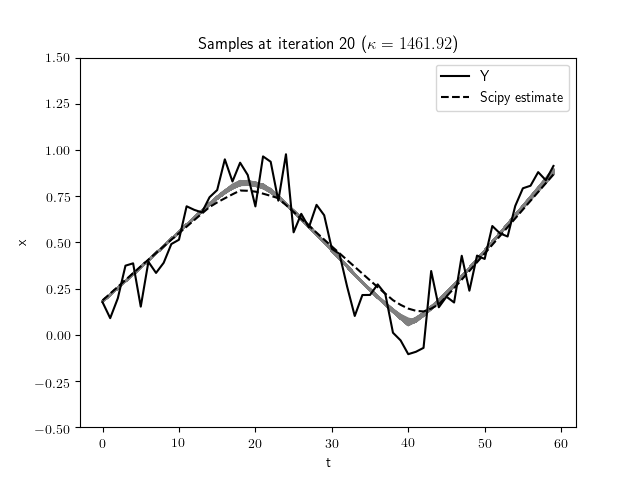

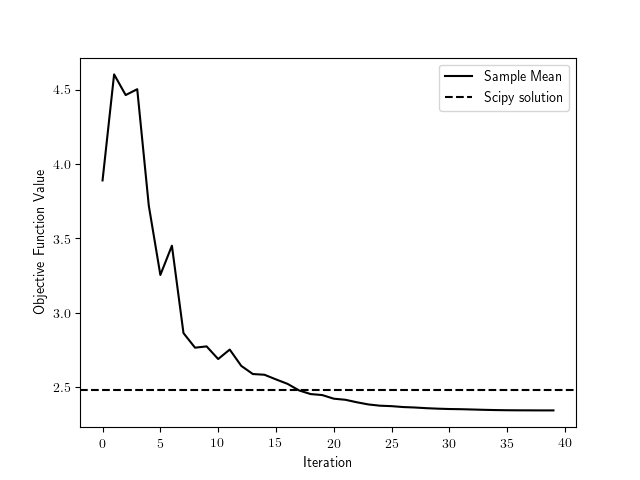

Figure 6 shows the sample paths (after the post-MCMC step) at the end of different anneal SMC iterations. When the temperature is shrinking to zero as increases, the sample paths move to a small neighborhood region around the true most likely path. Figure 7 shows the value of the objective function at the weighted average path of the samples as for different numbers of iterations. The true optimal value (the objective function value at the optimal path) obtained by the Kalman smoother is plotted as the dashed horizontal line. As the number of iteration increases, the objective function value at the averaged path decreases stochastically and convergences at roughly the 7th iteration.

To compare the computational efficiency, we record the computing time needed for different approaches, shown in Table 1. The Scipy approach uses the nonlinear optimizer provided by the python package Scipy (Jones et al., 2001), which implements the Broyden-Fletcher-Goldfarb-Shanno (BFGS) algorithm by default. The annealed SMC records the time until convergence (the time when the value of objective function is not improved by further iteration). Kalman Smoother is the fastest one due to its deterministic nature in finding the most likely path for linear Gaussian models. Annealed SMC is slower than the nonlinear solver program provided by Scipy, but achieves similar accuracy. We also note that this is a simple convex optimization problem in which a straightforward optimization algorithm such as the Scipy performs well. Our estimation approach is more flexible and this example serves as an illustration of how the algorithm works.

| Kalman Smoother | Scipy minimizer | Annealed SMC |

| 2.2 ms | 129.6 ms | 232.9 ms |

4.2 LASSO Regression

In this simulation study, we consider the LASSO regression problem as discussed in Section 2.3.2. We set observations, covariates and . The covariates are generated from a multivariate normal distribution where all diagonal elements of is 1 and all off-diagonal elements are 0.4. ’s are generated i.i.d. according to Bernoulli(0.2). is set to 5 in the objective function (14).

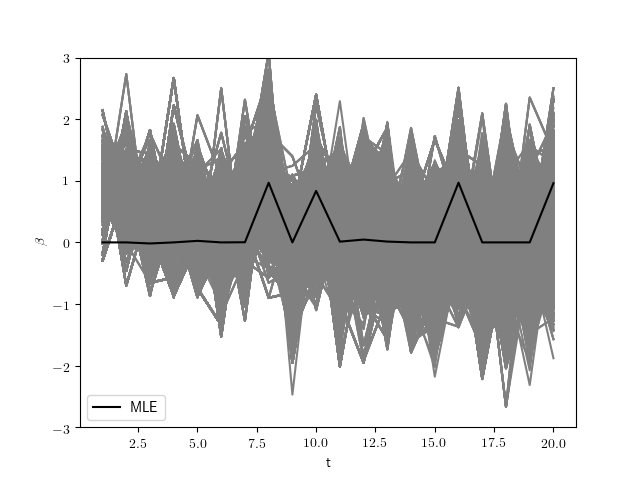

We start from the initial emulated model with the temperature parameter . samples are drawn from the standard SMC algorithm under the target distribution (17) with . The state equation (18) is used as the proposal distribution and the weight is from the observation equation (19) as a consequence. Resampling is done when the effective sample size (34) is below . The sampled state paths are plotted in Figure 8. The estimated path for solving the original LASSO problem (14) using the scikit-learn python package (Pedregosa et al., 2011) is treated as the benchmark. .

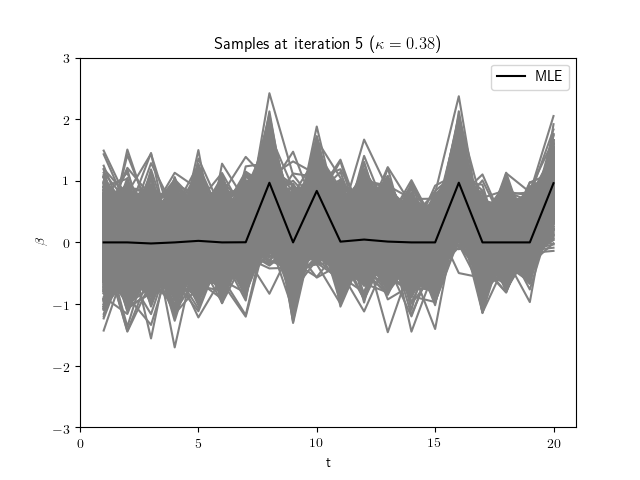

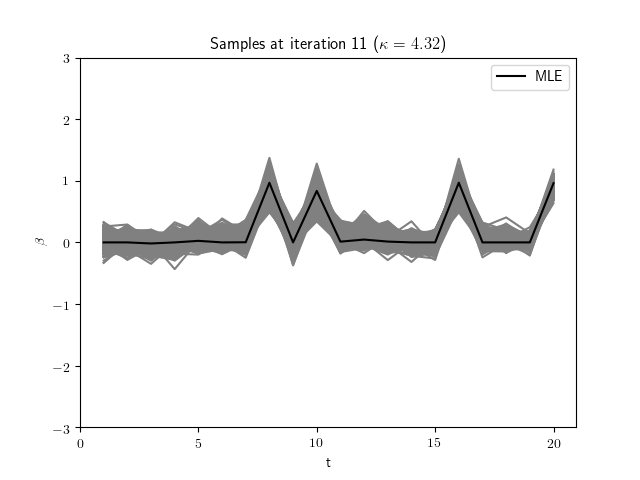

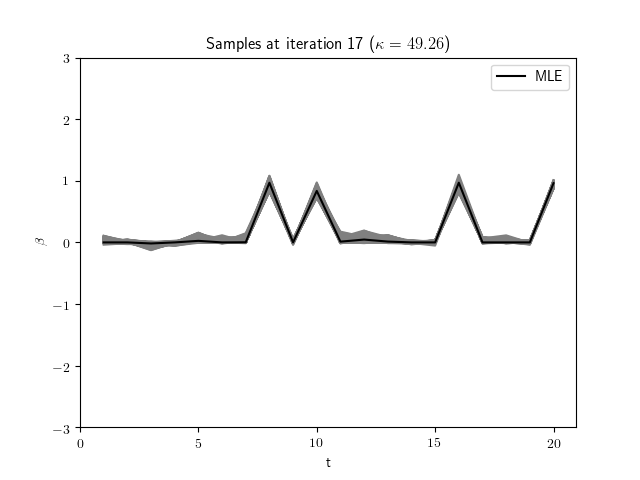

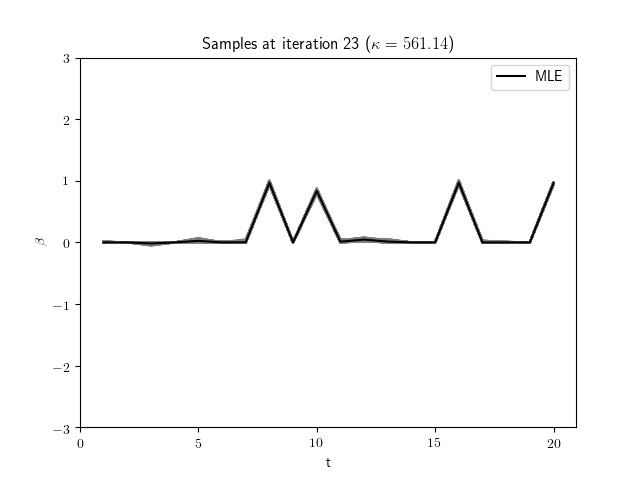

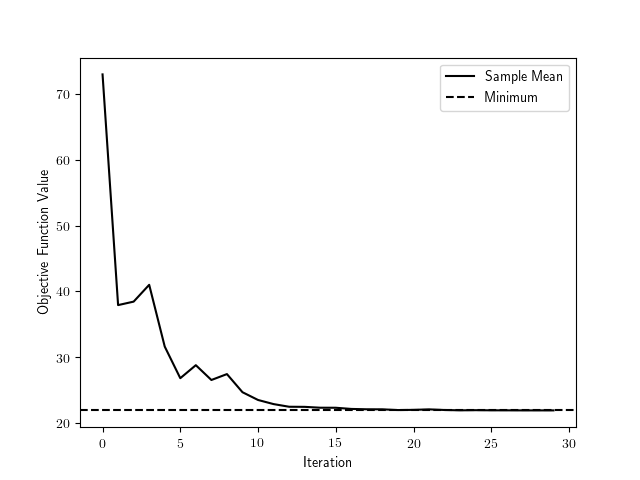

In the subsequent annealing procedure, we use samples and set for . The proposal distribution used in the annealing procedure is estimated with a multivariate normal approximation of the joint distribution of . Resampling is done only at the end of each iteration and 10 steps of post-MCMC runs are applied. The post-MCMC runs use the Gibbs sampling approach with the Metropolis-Hasting transition kernel (Metropolis et al., 1953; Hastings, 1970), where for and for , a new value for is proposed such that , where , and the proposed move is accepted with the probability with . Figure 9 plots the sample paths at four different levels of ’s. Again, it is seen that the procedure is able to gradually move the sample paths towards the optimal solution. Figure 10 shows the convergence of the values of the objective function in (14) evaluated at the weighted average of the sample paths.

After around 17 iterations, the weighted mean of the samples generated from the annealed SMC converges. Due to Monte Carlo variations, the sample paths and the average path cannot shrink the coefficients to exactly zero. It is tempting to run the Viterbi algorithm to refine the estimate, with zeros added to the set of allowed values of the state variables. Unfortunately the state space model designed for the LASSO problem is not Markovian hence Viterbi algorithm cannot be used. However, we used an additional refinement step by iteratively and greedily comparing each estimated state (using the average sample path) with zero under the original objective function. The refinement step (with additional 0.063ms in computing time) moved some of the states to zero, and improved the value of the objective function from 21.90356 to 21.899657. The minimum achieved by the Scikit solver is 21.899645. However, such a refinement is based on the knowledge that the solution of Lasso has exactly zero coefficients, and may not be used in other optimization problems. Note that, the emulation system can be easily generalized to other types of regularization on parameters by changing the penalty term in (19) without much efforts and can be adapted much more complex penalty structures.

4.3 Optimal Trading Path

In this simulation, we consider the optimal trading path problem in Section 2.3.3. Following Cai et al. (2019), we set , , and . The ideal trading path is given by

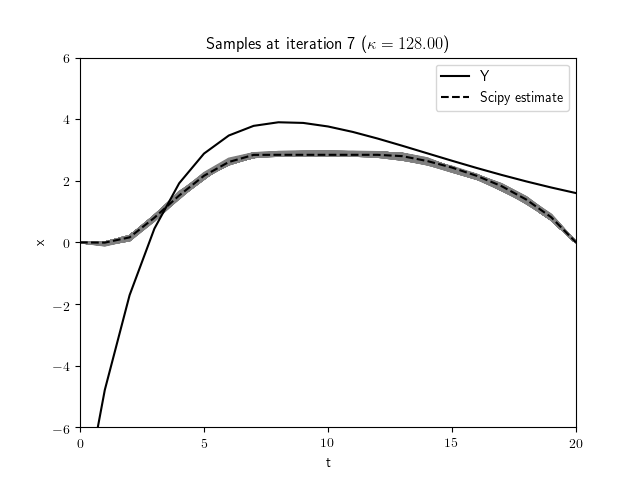

We start from the initial temperature . The sample paths at is drawn with the constrained SMC (Cai et al., 2019), where the resampling step is conducted with priority scores . The priority scores are estimated from a set of backward pilot samples (Cai et al., 2019). In this example, we use backward pilot samples. The resulting (forward) sample paths are shown in Figure 11. The observations , which represent the ideal optimal trading strategy without the trading cost, are plotted as the solid line. An estimated path, marked by dashed line, is provided by the Scipy nonlinear optimization algorithm.

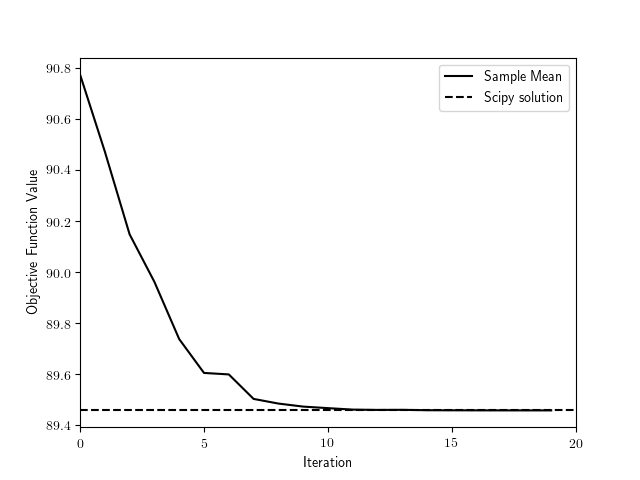

We use the following sequence of inverted temperatures for annealing: for . The proposal distribution in the annealed SMC is sampled with the parametric approach by approximating the joint distribution of and with a bivariate normal distribution. The annealed sample paths are resampled at the end of each iteration, and no post-MCMC step is conducted. Samples at several different inverted temperatures are shown in Figure 12. We use the sample average as our estimator for the most likely path. The value of the objective function at the sample average path decreases stochastically as shown in Figure 13. It eventually converges at around the 11th iteration. The optimal objective function value achieved by the annealed SMC is 89.459, while the one obtained by the Scipy nonlinear optimizer is 89.462. The values of the objective function at the sample paths at the 20th iteration has an average of and a standard deviation of . The annealed SMC gains some improvement in accuracy at the cost of extra computation. The Scipy nonlinear optimizer takes 78ms while the annealed SMC costs 1.820 seconds for the initial emulated model (including the time of backward sampling) and costs around 2ms for each subsequent iteration. Sampling from the base emulated model costs much more than subsequent iteration for two reasons. First, it requires a large sample size for the base model because of high degeneracy. Second, the end point constraint is imposed and an additional backward pilot run is needed to reduce degeneracy.

4.4 L1 Trend Filtering

In this simulation study, we consider the trend filtering problem in Section 2.3.4. We set , and

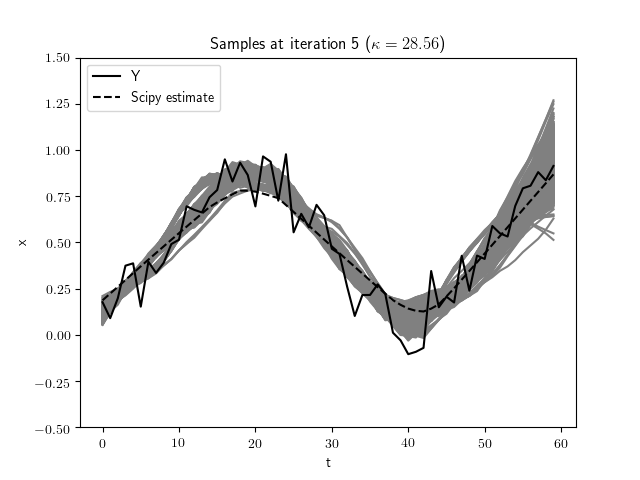

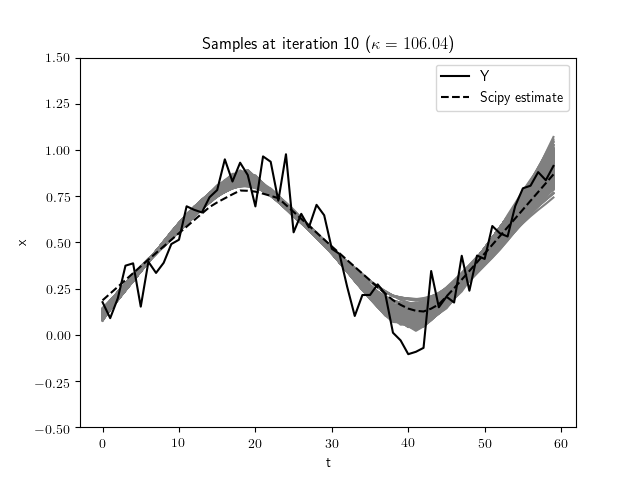

At , SMC paths are sampled using the state dynamics (26) as the proposal distribution. A resampling step is conducted when the effective sample size drops below . The approximate MLE marked as dashed line is the solution obtained by Scipy nonlinear solver. The solution shows a piece-wise linear behavior as the 1 type of penalty appears in the objective function.

We use the following designed annealing sequence for and use samples for annealing. In each annealing iteration, the proposal distribution used is where and are estimated from the samples from the last iteration . The Laplace distribution has a heavier tail than the normal distribution with the same variance. We found it more efficient to sample from the Laplace distribution to reduce sample degeneracy in this problem. The resampling step is conducted at the end of each iteration and is followed by 10 steps of post-MCMC moves. The post-MCMC steps follow the standard Gibbs sampling as in the LASSO example. Sample paths at four different ’s are displayed in Figure 14. Note that when , the sample paths are different from the nonlinear solver’s solution at . The value of the objective function at the sample average path shown in Figure 15 show that annealed SMC can obtained a smaller objective function value than the Scipy optimizer. The Scipy nonlinear optimizer takes 155ms while annealed SMC costs 22 ms for SMC sampling from the initial emulated model and costs around 160 ms for each subsequent annealing iteration including the post-MCMC runs.

5 Summary and Discussion

In this article, we propose a general framework of state space model emulation for high dimensional optimization problems. We demonstrated that, by constructing a proper state space model, many high dimensional optimization problems can be turned into the problem of finding the optimal (most likely) path under the state space model. And we propose an novel annealed sequential Monte Carlo method to solve the most likely path problem numerically through a simulated annealing scheme with SMC samples. We demonstrate the procedure of state space model emulation with four conventional problems and show how they can be solved using the proposed annealed SMC approach.

The proposed annealed SMC approach shares some similar properties with the traditional simulated annealing methods. Both can optimize a wide range of objective functions including non-convex functions and multi-modal functions, and both often require heavier computation cost than the simpler standard optimization algorithms such as the gradient descent algorithms. However, the annealed SMC approach for state space models is different to the traditional simulated annealing methods in association with MCMC for stochastic optimization in the following ways. First, emulating an optimization problem into a state space model has its advantage in many problems, especially when the problem is of high dimensional and when the system is inherently dynamic (such as the trading path problem or the trend filtering problem) or when the parameters to be estimated inherently play similar roles in the problem (such as the parameters in the regression problem). Second, SMC as an alternative to MCMC has certain advantages in many fixed dimensional problems such as in the problems when the “dependence” between the parameters in the emulated target distribution is local and (locally) very strong. In these problems, MCMC encounters slow mixing difficulties while SMC naturally takes advantage of such properties. Third, given any temperature, SMC samples target the equilibrium distribution, while MCMC samples often move towards the target distribution gradually. Hence annealed SMC may tolerate faster cooling schedule. Fourth, the inherited parallel structure of SMC allows faster computation. It also adapts to multi-modal problems better.

The state space model emulation and the annealed SMC provide an alternative way to solve high-dimensional optimization problems. Of course, the approach may not be suitable for all problems, due to its high computational cost and its requirement of certain structures. Nevertheless the approach adds to the high dimensional optimization toolbox a useful method for a wide range of complex problems for which the more traditional method may have difficulties to solve. Although the examples shown in this paper do not demonstrate great improvement of the state space emulation approach over the traditional one, they effectively shown how the approach can be implemented and can be used for other problems.

References

- Agarwal et al. (2014) Agarwal, A., Anandkumar, A., Jain, P., Netrapalli, P., and Tandon, R. (2014). Learning sparsely used overcomplete dictionaries. In Conference on Learning Theory, pages 123–137.

- Anandkumar et al. (2014) Anandkumar, A., Ge, R., Hsu, D., Kakade, S. M., and Telgarsky, M. (2014). Tensor decompositions for learning latent variable models. The Journal of Machine Learning Research, 15(1):2773–2832.

- Arora et al. (2012) Arora, S., Ge, R., Kannan, R., and Moitra, A. (2012). Computing a nonnegative matrix factorization–provably. In Proceedings of the forty-fourth annual ACM symposium on Theory of computing, pages 145–162. ACM.

- Bertsekas (1997) Bertsekas, D. P. (1997). Nonlinear programming. Journal of the Operational Research Society, 48(3):334–334.

- Briers et al. (2010) Briers, M., Doucet, A., and Maskell, S. (2010). Smoothing algorithms for state-space models. Annals of the Institute Statistical Mathematics, 62:61–89.

- Cai et al. (2009) Cai, A., Tsay, R. S., and Chen, R. (2009). Variable selection in linear regression with many predictors. Journal of Computational and Graphical Statistics, 18(3):573–591.

- Cai et al. (2019) Cai, C., Chen, R., and Lin, M. (2019). Resampling strategy in sequential monte carlo for constrained sampling problems. arXiv preprint arXiv:1706.02348.

- Chen et al. (2000) Chen, R., Wang, X., and Liu, J. S. (2000). Adaptive joint detection and decoding in flat-fading channels via mixture kalman filtering. IEEE Transactions on Information Theory, 46(6):2079–2094.

- Crisan and Doucet (2000) Crisan, D. and Doucet, A. (2000). Convergence of sequential monte carlo methods. Signal Processing Group, Department of Engineering, University of Cambridge, Technical Report CUEDIF-INFENGrrR38, 1.

- Del Moral et al. (2010) Del Moral, P., Doucet, A., and Singh, S. (2010). Forward smoothing using sequential monte carlo. arXiv preprint arXiv:1012.5390.

- Dempster et al. (1977) Dempster, A. P., Laird, N. M., and Rubin, D. B. (1977). Maximum likelihood from incomplete data via the em algorithm. Journal of the royal statistical society. Series B (methodological), pages 1–38.

- Doucet et al. (2001) Doucet, A., De Freitas, N., and Gordon, N. (2001). An introduction to sequential monte carlo methods. In Sequential Monte Carlo Methods in Practice, pages 3–14. Springer.

- Gilks and Berzuini (2001) Gilks, W. R. and Berzuini, C. (2001). Following a moving target—monte carlo inference for dynamic bayesian models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 63(1):127–146.

- Godsill et al. (2004) Godsill, S. J., Doucet, A., and West, M. (2004). Monte carlo smoothing for nonlinear time series. Journal of the American Statistical Association, 99(465):156–168.

- Gordon et al. (1993) Gordon, N. J., Salmond, D. J., and Smith, A. F. (1993). Novel approach to nonlinear/non-gaussian bayesian state estimation. IEE Proceedings F (Radar and Signal Processing), 140(2):107–113.

- Granville et al. (1994) Granville, V., Krivanek, M., and Rasson, J. . (1994). Simulated annealing: a proof of convergence. IEEE Transactions on Pattern Analysis and Machine Intelligence, 16(6):652–656.

- Green and Silverman (1993) Green, P. J. and Silverman, B. W. (1993). Nonparametric regression and generalized linear models: a roughness penalty approach. CRC Press.

- Guarniero et al. (2017) Guarniero, P., Johansen, A. M., and Lee, A. (2017). The iterated auxiliary particle filter. Journal of the American Statistical Association, 112(520):1636–1647.

- Hastings (1970) Hastings, W. K. (1970). Monte Carlo sampling methods using Markov chains and their applications. Biometrika, 57(1):97–109.

- Hodrick and Prescott (1997) Hodrick, R. J. and Prescott, E. C. (1997). Postwar us business cycles: an empirical investigation. Journal of Money, credit, and Banking, pages 1–16.

- Hooke and Jeeves (1961) Hooke, R. and Jeeves, T. A. (1961). “ direct search” solution of numerical and statistical problems. J. ACM, 8(2):212–229.

- Irie and West (2016) Irie, K. and West, M. (2016). Bayesian emulation for optimization in multi-step portfolio decisions. arXiv preprint arXiv:1607.01631.

- Jain et al. (2017) Jain, P., Kar, P., et al. (2017). Non-convex optimization for machine learning. Foundations and Trends® in Machine Learning, 10(3-4):142–336.

- Jensen et al. (1995) Jensen, C. S., Kjærulff, U., and Kong, A. (1995). Blocking gibbs sampling in very large probabilistic expert systems. International Journal of Human-Computer Studies, 42(6):647–666.

- Jones et al. (2001) Jones, E., Oliphant, T., Peterson, P., et al. (2001). SciPy: Open source scientific tools for Python.

- Kalman (1960) Kalman, R. E. (1960). A new approach to linear filtering and prediction problems. Journal of Basic Engineering, 82(1):35–45.

- Kiefer et al. (1952) Kiefer, J., Wolfowitz, J., et al. (1952). Stochastic estimation of the maximum of a regression function. The Annals of Mathematical Statistics, 23(3):462–466.

- Kim et al. (2009) Kim, S.-J., Koh, K., Boyd, S., and Gorinevsky, D. (2009). ell_1 trend filtering. SIAM review, 51(2):339–360.

- Kirkpatrick et al. (1983) Kirkpatrick, S., Gelatt, C. D., and Vecchi, M. P. (1983). Optimization by simulated annealing. Science, 220(4598):671–680.

- Kitagawa (1996) Kitagawa, G. (1996). Monte carlo filter and smoother for non-gaussian nonlinear state space models. Journal of Computational and Graphical Statistics, 5(1):1–25.

- Kolm and Ritter (2015) Kolm, P. N. and Ritter, G. (2015). Multiperiod portfolio selection and bayesian dynamic models. Risk. Available at SSRN: https://ssrn.com/abstract=2472768.

- Kong et al. (1994) Kong, A., Liu, J. S., and Wong, W. H. (1994). Sequential imputations and bayesian missing data problems. Journal of the American statistical association, 89(425):278–288.

- Kyle and Obizhaeva (2011) Kyle, A. and Obizhaeva, A. (2011). Market microstructure invariants: Theory and implications of calibration. Available at SSRN: https://ssrn.com/abstract=1978932.

- Land and Doig (1960) Land, A. H. and Doig, A. G. (1960). An automatic method of solving discrete programming problems. Econometrica, 28(3):497–520.

- Lin et al. (2013) Lin, M., Chen, R., and Liu, J. S. (2013). Lookahead strategies for sequential Monte Carlo. Statistical Science, 28:69–94.

- Lin et al. (2005) Lin, M. T., Zhang, J. L., Cheng, Q., and Chen, R. (2005). Independent particle filters. Journal of the American Statistical Association, 100(472):1412–1421.

- Liu and Chen (1995) Liu, J. S. and Chen, R. (1995). Blind deconvolution via sequential imputations. Journal of the American Statistical Association, 90(430):567–576.

- Liu and Chen (1998) Liu, J. S. and Chen, R. (1998). Sequential monte carlo methods for dynamic systems. Journal of the American statistical association, 93(443):1032–1044.

- Markowitz (1959) Markowitz, H. (1959). Portfolio selection, cowles foundation monograph no. 16. John Wiley, New York, 32:263–74.

- Mei et al. (2018) Mei, S., Montanari, A., and Nguyen, P.-M. (2018). A mean field view of the landscape of two-layer neural networks. Proceedings of the National Academy of Sciences, 115(33):E7665–E7671.

- Metropolis et al. (1953) Metropolis, N., Rosenbluth, A. W., Rosenbluth, M. N., Teller, A. H., and Teller, E. (1953). Equation of state calculations by fast computing machines. The Journal of Chemical Physics, 21(6):1087–1092.

- Nelder and Mead (1965) Nelder, J. A. and Mead, R. (1965). A simplex method for function minimization. The computer journal, 7(4):308–313.

- Netrapalli et al. (2014) Netrapalli, P., Niranjan, U., Sanghavi, S., Anandkumar, A., and Jain, P. (2014). Non-convex robust pca. In Advances in Neural Information Processing Systems, pages 1107–1115.

- Pedregosa et al. (2011) Pedregosa, F., Varoquaux, G., Gramfort, A., Michel, V., Thirion, B., Grisel, O., Blondel, M., Prettenhofer, P., Weiss, R., Dubourg, V., Vanderplas, J., Passos, A., Cournapeau, D., Brucher, M., Perrot, M., and Duchesnay, E. (2011). Scikit-learn: Machine learning in Python. Journal of Machine Learning Research, 12:2825–2830.

- Pitt and Shephard (1999) Pitt, M. K. and Shephard, N. (1999). Filtering via simulation: auxiliary particle filters. Journal of the American statistical association, 94(446):590–599.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288.

- Tzikas et al. (2008) Tzikas, D. G., Likas, A. C., and Galatsanos, N. P. (2008). The variational approximation for bayesian inference. IEEE Signal Processing Magazine, 25(6):131–146.

- Viterbi (1967) Viterbi, A. (1967). Error bounds for convolutional codes and an asymptotically optimum decoding algorithm. IEEE Transactions on Information Theory, 13(2):260–269.