Robust Parameter-Free Season Length Detection in Time Series

Abstract.

The in-depth analysis of time series has gained a lot of research interest in recent years, with the identification of periodic patterns being one important aspect. Many of the methods for identifying periodic patterns require time series’ season length as input parameter. There exist only a few algorithms for automatic season length approximation. Many of these rely on simplifications such as data discretization and user defined parameters. This paper presents an algorithm for season length detection that is designed to be sufficiently reliable to be used in practical applications and does not require any input other than the time series to be analyzed. The algorithm estimates a time series’ season length by interpolating, filtering and detrending the data. This is followed by analyzing the distances between zeros in the directly corresponding autocorrelation function. Our algorithm was tested against a comparable algorithm and outperformed it by passing 122 out of 165 tests, while the existing algorithm passed 83 tests. The robustness of our method can be jointly attributed to both the algorithmic approach and also to design decisions taken at the implementational level.

1. Introduction

In many areas of natural science and economics there exists an abundance data which can be used beneficially once they are processed. Often these data are collected at regular intervals to enable making statistical assumptions and predictions for numerous applications. Data collected repeatedly over a time span is referred to as time series.

The in-depth analysis of time series has been a central topic of research in recent years. Typically, time series are investigated to better understand their past behavior and to make forecasts for future data. To achieve this, identifying trends and regularities are particularly useful, as they allow one to generalize from the given data to a larger context.

A very natural approach to finding these relevant patterns is the Exploratory Data Analysis (Tukey, 1977). This method relies on visualizing the data, typically without making any prior assumptions about the data. An advantage of this procedure is that humans usually analyze visual data very effectively and thus identify many relevant features of the data.

While data visualization works well with many time series, there are also several cases where it is insufficient. When dealing with very complex data, it is often difficult to infer meaningful features. Furthermore, it is also frequently necessary to analyze dozens of time series, where manual analysis quickly becomes tedious or even infeasible. Therefore, an automated and robust approach that can deal with complex data is required.

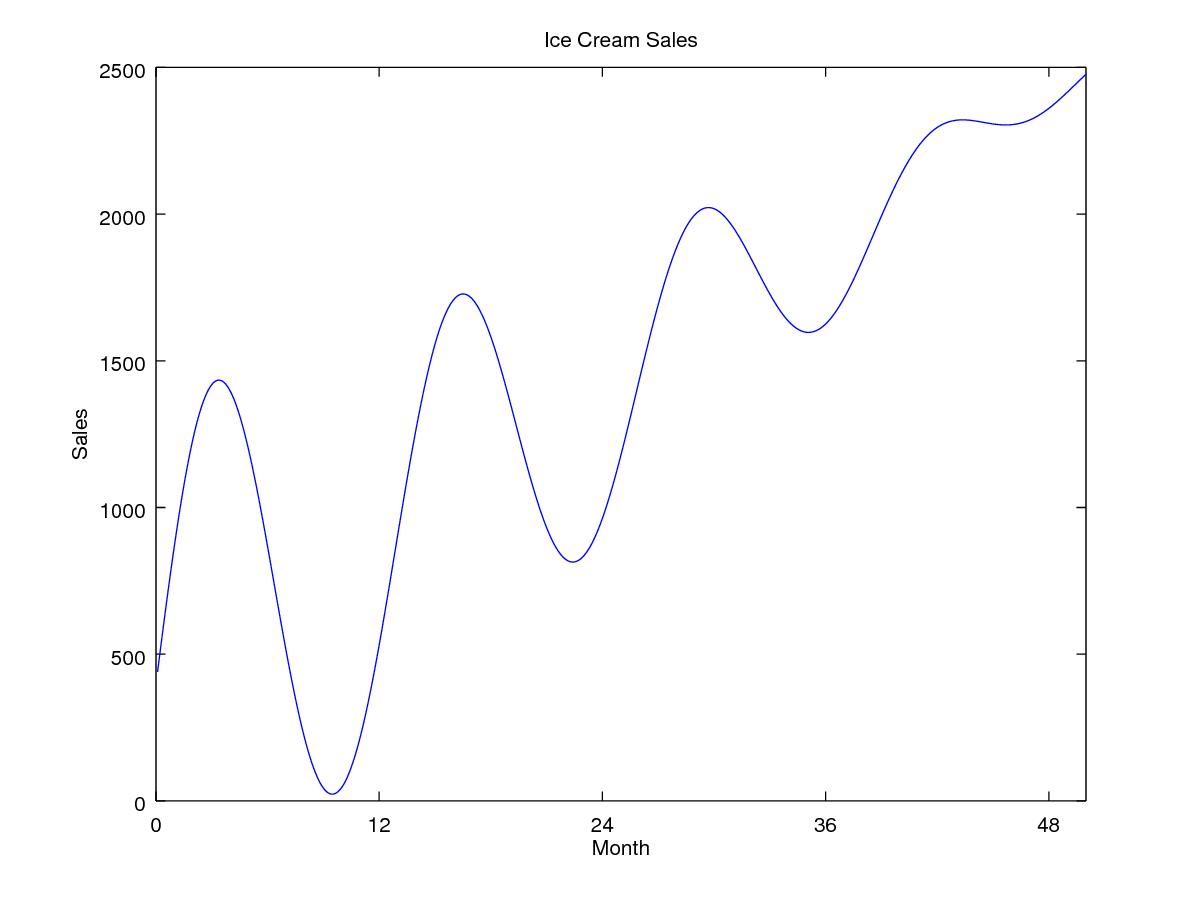

While there are many established algorithms for trend estimation (Draper et al., 1966) (Vamos and Craciun, 2012), methods for finding periodic patterns and features are much younger. One popular approach is the data cube concept (Han et al., 1998), which relies on constructing and employing a data cube for finding periodic features in a time series. This method would, for instance, successfully identify a peak of ice cream sales every summer given monthly sales data over several years. However, to achieve this, the algorithm requires the user to input the time series’ season length (or frequency). In the example depicted in Figure 1 the season length would be 12, as the sales pattern repeats every 12 months.

Today, there already exist a few algorithms for approximating season length. Most of them rely on data discretization before analysis, which is a simplification of data as seen above to discrete numbers such as 2, 4, and 6. For finding so-called symbol periodicity in discretized data one can for instance use suffix trees (Rasheed et al., 2011) or convolution (Elfeky et al., 2005). One downside of discretization is that it inevitably leads to a loss of information, which might change the result in some cases. A more significant disadvantage of discretization is that contemporary time series symbolization methods such as SAX (Lin et al., 2003) require the user to define the number of symbols to which the data is discretized. This is be problematic since data mining algorithms should in general have as few parameters as possible (Keogh et al., 2004).

A different approach that does not rely on data discretization is searching for local peaks and troughs in a time series’ autocorrelation function (Wang et al., 2006). This method works fully automated and efficiently computes the correct season length of many time series. Yet there are still several cases where this algorithm is not able to identify the correct frequencies - particularly in time series with noisy data or very long periods.

Due to the above mentioned algorithm’s disadvantages, it should be beneficial to find a more reliable method. Such an algorithm should not rely on user defined parameters or data discretization and still correctly identify a time series’ season length. A method that was designed to meets these requirements is presented in this paper. The source code of our system, the test data set and detailed test results can be accessed online111https://github.com/mtoller/autocorr_season_length_detection.

2. Background

The existing time series analysis literature has proposed several different approaches for seasonality detection. Often the term periodicity detection is used in literature for the same task. These methods can be split in three different categories: explicit season length, discretized time series, and single season length.

1. Explicit season length

The first type of algorithms depends on an external specification of the period length to extract periodic features. The previously mentioned data cube concept (Han et al., 1998) was a pioneer method for mining periodic features in time series databases. Other examples are the chi-squared test (Ma and Hellenstein, 2001) or binary vectors (Berberidis et al., 2002). The advantage of such procedures is their low time complexity and their reliable results. However, relying on an external specification of the period inherently prevents these methods from detecting an unknown period. In many applications a parameter-free method is being highly desired.

2. Discretized time series

The second type of algorithms for detecting periodic features test all possible periods of a time series. This is typically performed on a discretized time series, as otherwise such algorithms would quickly become computationally infeasible. Examples for such methods are suffix trees (Rasheed et al., 2011), convolution (Elfeky et al., 2005) and data sketches (Indyk et al., 2000). Unlike the previous type, these algorithms typically find all potentially relevant periodic patterns without previous specification of the period. However, since they depend on data discretization, they can only be as accurate as the underlying data discretization allows. Furthermore they may return more than one possible result. While this is often an accurate reflection of a time series periodic features, it is often advantageous in practice to provide a single dominant period for further automated processing of a time series.

3. Single season length

The third type of algorithms approximates a single season length from the raw data. While such an approach might be too limited for highly complex data, it can be useful in cases where time series have one dominant frequency. One popular algorithm (Hyndman, 2012) of this category can be found in the R forecast library and was derived from another method (Wang et al., 2006) which is based on autocorrelation. The algorithm presented in this paper belongs to the third type and focuses on improving the robustness of the season length detection.

Combination of methods

All three categories consequently serve different purposes in time series seasonality detection and also can be combined in useful ways. For example, an algorithm of type 3 can be used for season length detection, which can then be used as input for a type 1 algorithm to enable correct periodicity mining. Further, type 2 and 3 can be combined on the same time series to assess the effect discretization has on a specific time series.

3. Concepts

Let be a series of real-valued observations and the interval at which these observations are made. If has a subsequence of observations which occurs every observations after its first occurrence, is seasonal. Moreover, if is not part of a longer repeating subsequence of and it cannot be divided into shorter equal subsequences, then is perfectly seasonal with season length .

is negligible since it is independent from . The problem of finding season length can therefore be reduced to finding the characteristic subsequence which fulfills the following formal criteria 1 and 2. The first criterion is

| (1) |

which means the number of observations in must be equal to the number of observations in from one occurrence of to its next. The second criterion is

| (2) |

with being the power set (set of all subsets) of and ( followed by ). This means that must not contain a subsequence q that can be repeated times to create , i.e.

For example, given a time series

| (3) |

the sequence is repeated four times in . Sequence cannot be reduced to shorter equal sequences, as and the number of observations in is equal to the number of observations from one occurrence of to its next occurrence . Therefore and has a season length of .

If one extends the sequence by one element to then , which means it cannot be . Now considering sequence the first criterion is fulfilled: . Yet the second condition is violated as can be split into the equal subsequences , therefore can be divided into shorter equal sequences and also cannot be .

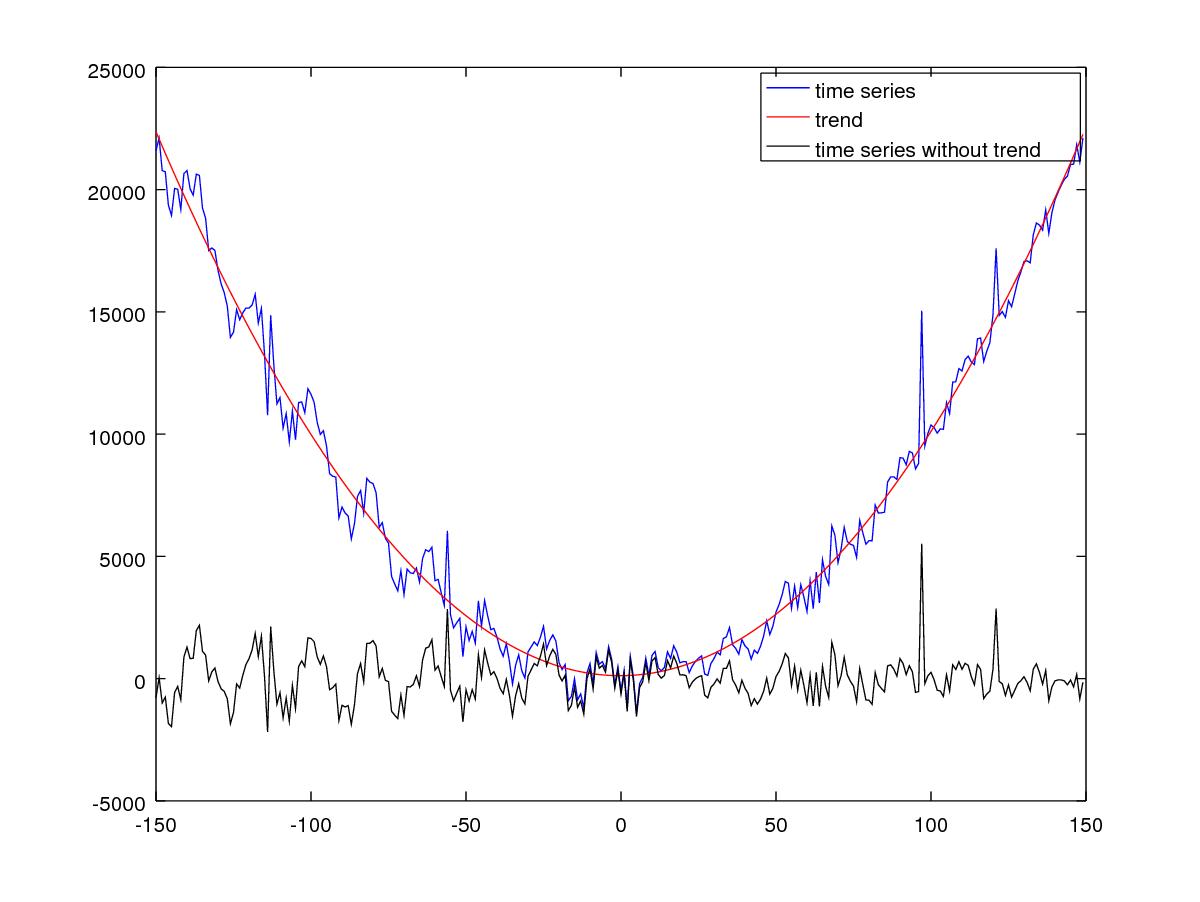

3.1. Detrending

Many time series have a trend in addition to its seasonality, which means that the seasonal influences revolve around a trend function. For instance, in the example in Equation 3 there could be a linear increase in the observations after every season, e.g.

In this case would be time-dependent:

with . However, the unscaled season length is identical for all and is therefore not time-dependent. Hence it is desirable to remove trend influences from a time series before analyzing seasonality.

Approximating the trend components can be achieved with regression analysis (Draper et al., 1966), which is a procedure for finding a function which minimizes the mean square error between the observations and the approximated function. Its cost function can be written as

| (4) |

where is the design matrix, the time series and the parameters of the regression. A design matrix is a matrix where each row describes one observation and each column models an assumed feature onto the corresponding observation. For instance, in polynomial regression can be written as

To find the parameters which minimize the cost function, one can use the analytical solution

| (5) |

The trend of time series can then be removed with

| (6) |

Removing all trend influences from a time series significantly facilitates investigating seasonal effects, as the characteristic subsequences then directly correlate with each other. This property allows one to investigate the time series’ autocorrelation instead of the time series itself. Such an approach is advantageous since the original observations are frequently much more difficult to analyze than autocorrelation.

3.2. Removing Noise

Before directly analysing the characteristic subsequence , another major component of many time series needs to be considered. Most non-discretized time series contain random inaccuracies, which are often named noise or residuals. Minimizing these random influences is desirable, since they tend to obscure the true nature of the observations. This is typically achieved by means of filters.

As noise typically affects every observation in a time series, it tends to have a shorter period than seasonality, which has a period of at least 2 observations. Such a shorter period leads to noise having a higher frequency than seasonality. Therefore, it is advantageous to apply a low-pass filter on the time series, which rejects any frequency higher than a given threshold. This smooths the curve while maintaining the original season length.

However, using a low-pass filter also has a negative effect on the observations. While removing white noise, filters likewise alter the observations’ correlation. To lessen these unwanted side effects, one may interpolate the data before applying the low-pass filter.

3.3. Analyzing Correlation

Only after removing most noise from the observations, it is possible to meaningfully investigate autocorrelation of a time series. A time series’ autocorrelation is the correlation of its observations at different times. Autocorrelation is formally defined as

| (7) |

where is the lag at which the observations are compared, and is the complex conjugate of . Since time series are time-discrete and real-valued, this can be further simplified to

| (8) |

After a further normalization the resulting values range from to . The former implies complete anti-correlation between the two observations, while the latter means full correlation.

In general, two objects and correlate, if a change in is likely to be linked with the same change in as well, whereas negative correlation would be associated with a change in in the opposite direction. In case of correlation, a change in is independent from .

Autocorrelation describes the correlation of with itself at a different point in time. If is seasonal, then its autocorrelation will be seasonal with the same season length. This property ensures that investigating autocorrelation leads to the same season length as analyzing the original observations, which is usually more challenging.

3.4. Interpolating the Observations

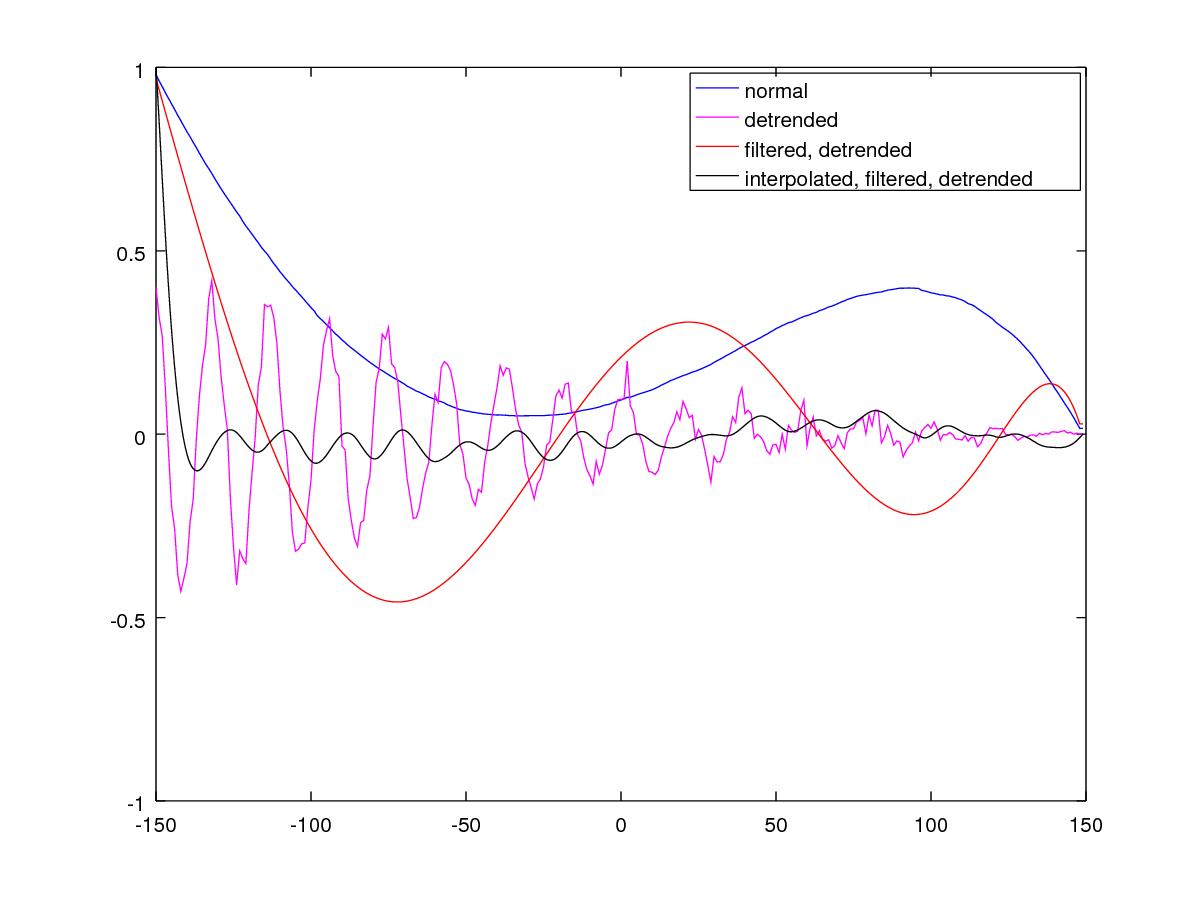

Autocorrelation should make it possible to observe seasonality. Yet when applied on time series being preprocessed via low-pass filters one will experience a negative side-effect: Its characteristic subsequence’s length no longer matches the length original subsequence . Instead, its unscaled season length is with and consequently a multiple of the original length, which makes finding the correct season length more difficult.

To avoid this side-effect, it is possible to linearly interpolate the observations before applying a filter. This means that between every neighboring observations, several intermediate observations are inserted. For example, the sequence could be interpolated to . The linear interpolation of two observations and can be written as

| (9) |

where is the time at which was observed and denotes a chosen point in time between these two observations. By interpolating all neighboring observations, can be expanded to its interpolated sequence

Interpolating the observations is advantageous, since it usually lessens the filters negative effect on the length of the characteristic subsequence. Let be after interpolation, filtering and detrending. The unscaled season length of its autocorrelation matches the unscaled season length of the original observations , which means

After interpolating, filtering and detrending the observations and calculating their autocorrelation, it is finally possible to directly compute the time series’ unscaled season length . This can be done by analyzing the zeros of . The distance between two zeros and with is equal to half the unscaled season length . Therefore, can be computed with

| (10) |

To calculate the true, scaled season length, one has to simply form the product , which is negligible in practice.

4. System

While the above mentioned concepts work well in theory, there are several challenges in practice which still need to be met:

-

•

Trends may change over time

-

•

Noise may vary

-

•

Machines have limited numeric precision

-

•

Seasonality is not always perfect

-

•

Presence of outliers

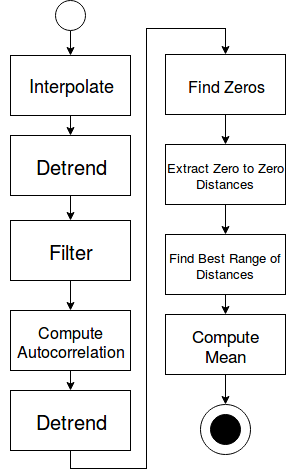

Dealing with these and other problems is imperative for robust parameter-free season length detection. An overview of the steps which our system takes to meet these challenges can be seen in Figure 4.

Another crucial practical aspect is runtime, since time series tend to contain thousands if not millions of observations. To be valuable in practice, it is desirable for the implementation to have a worst-case computational complexity of at the most , with being the number of observations in the time series.

4.1. Approximating the Trend

The seasonality of a time series typically revolves along a certain trend. However, this trend may follow an arbitrary function, which makes removing all trend in any time series impossible. Therefore, it is necessary to only consider trends which are particularly common in practice.

Linear trends occur frequently in mathematical functions, but are not very common in practice. Therefore, it is insufficient to assume that all time series will have a close to linear trend. However, as polynomials of higher order tend to over-fit the present data, linear trends can at least be compared with other assumptions without over-fitting the data. Consequently, it is useful to begin trend approximation by solving the 1st order polynomial linear regression.

Unlike linear tendencies, quadratic trends are fairly common. Many relations in nature follow the square - for instance the relation between speed and acceleration of moving objects. Therefore it is advantageous to attempt modeling the data with a quadratic trend. To compare such a model with a linear trend estimation one can compare the resulting mean square errors, which can be achieved with

| (11) |

where are the parameters which minimize the mean square error with a polynomial of th degree. The logarithm is applied since the difference tends to be very large. The constant determines the decision boundary between linear and quadratic trend estimation. In the context of this implementation it will be assumed that . This value was chosen empirically rather than theoretically, which obviously will not be appropriate in all cases. However, determining the correct value of this and a few other empirically chosen values for all cases would be beyond the scope of this paper.

4.2. Choosing the Correct Filter

A promising approach for detrending time series is high-pass filtering. An advantage of this approach is that it can effectively remove non-stationary trends from time series, which is difficult to achieve with linear regression. A disadvantage of high-pass filters is that they depend more strongly on threshold values, which limits their value to that of the chosen models’ constants.

There is a variety of ways to construct a low-pass filter, yet none of them can create the ideal low-pass filter, which rejects all frequencies higher than the cutoff frequency. It is only possible to approximate a close-to ideal filter, which removes most too high frequencies while changing the less frequent signals as little as possible. This can be achieved by generating a Butterworth low-pass filter, which can be obtained by choosing its order and cutoff frequency and then applying the corresponding algorithm.

However, choosing the correct order and cutoff frequency is problematic, as the amount and amplitude of noise vary in time series. In the context of our implementation, the order and cutoff-frequency were chosen empirically in preliminary tests.

4.3. Numeric Inaccuracies

Machines only have a finite numeric precision. Therefore, the theoretical method must be adjusted at several points.

Firstly, there usually is no exact in the autocorrelation, rather the data moves from positive to negative values or vice versa. Consequently, it is necessary to either create a tolerance interval around , or to interpolate the data until it is accurate enough. In case of our implementation, both strategies are applied.

Secondly, even after an almost ideal detrending, the autocorrelation will not have a linear trend of , but rather a tendency very close to . To deal with this, a second linear regression is performed after the autocorrelation was computed. The autocorrelation is then not searched for , but rather , where is the linear trend of the .

Thirdly, due to the consequential mentioned tolerance interval

| (12) |

there will be several solutions for which are in the same tolerance interval. Therefore, it is necessary to discard all and for which the following condition is true

| (13) |

This is obvious, since no time series can have a season length shorter than two observations and the difference between two zeros corresponds to half the season length.

4.4. Imperfect Seasonality

Another problem that exists in practice is that seasonality is rarely perfect, as assumed in theory. Frequently, seasonality outliers or a systematic seasonal change occur, which invalidate the above formula . To deal with these problems, it is possible to not only analyze and , but rather any pair of adjacent solutions for Equation 10.

Let be all values for so that Equation 10 is fulfilled and let be the distances between each pair of adjacent zeros in Equation 10. By removing all pairs that violate Equation 13 from one can compute all true distances between seasonal repetitions , which are further sorted in ascending order.

These true distances provide a better representation of the season length than an arbitrary pair of solutions and . However, simply taking an average of these values does not suffice, since many time series contain seasonality outliers. Further, numeric imprecision may cause the implementation to miss correct zeros, or any remaining noise might add incorrect zeros. Therefore, it is necessary to perform additional operations on .

To separate the correct values in from the incorrect, it is necessary to assume that contains a sufficiently large number of correct values. Since seasonality is stationary in time series, the correctly identified distances have a low variance in most cases, while erroneous values tend have a much higher sample variance.

When considering Equation 14, it can be observed that the intervals and have a low variance when compared to intervals including other values.

| (14) |

This suggests that the correct zero-to-zero distance is either or . By further considering that , it is intuitive to assume that these intervals are multiples of each other. Since Equation 2 must still be valid, it is safe to assume that a zero was missed between two zeros and thus caused the multiplied distance. Therefore, the correct zero-to-zero distance is very likely .

While the above example suggests taking the low-variance interval with the smallest mean, it is more reliable to rather search for the low-variance interval with the highest cardinality. The reason for this is the necessary assumption that a sufficiently large amount of the found zero-to-zero distances is almost correct, as otherwise reliably finding the true season length would be impossible.

To apply the above reasoning in a generalized way, it is necessary to reliably identify these low-variance intervals. This can be done by computing the quotients between the distances

| (15) |

These quotients describe the rate at which the distances between zeros change. A series of low values for implies a stable, low-variance interval of distances, while high values suggest a jump between intervals. These high and low values can be separated with

| (16) |

where is a constant which was chosen empirically in preliminary tests with and . This gives a series of integers where represents a low change of distances, and all other numbers the index of a high change. By then discarding all zeros with , the longest low-variance interval of distances can be found with

| (17) |

where is the index of the first distance in the interval, and the index of the last. If the resulting interval is long enough, it can be advantageous do further discard an upper and lower percentile of the values within the interval. However, in practice, we found that this alters the result very little in our experiments.

With the longest low-variance interval, an approximation of the season length can be computed by taking the average of these distances with

| (18) |

5. Evaluation

5.1. Data Set

To evaluate the implementation, it is necessary to test it with several different time series. For this purpose, two distinct time series databases were gathered. The first database contained extensive variations of synthetic data, while the second database consisted of real financial and climate data. The time series from these databases were tested in nine test runs, where our implementation was tested against the existing algorithm in the R forecast library. The test cases for runs 1 to 7 were taken from the synthetic database, while the test cases for runs 8 and 9 were taken from the real database and are briefly described below:

In the test, both algorithms were confronted with 20 time series, which strongly vary in trend, seasonality, noise and length. However, all these time series had a consistent season length, which does not vary within the series. This first testing was meant to compare the general applicability of the algorithm, which is achieved by challenging them with very different problems, which yet have a distinct solution.

In the test, the 20 test cases included many numeric outliers, largely changing season amplitude, season outliers and also varying noise. This had the purpose to assess the algorithms’ error tolerance.

The test included 20 examples with more than one correct solution. This aimed at observing the choices made by the algorithms and thus identifying their tendencies or preferences.

The test featured 4 time series, which were each presented in 5 variations. This was meant to assess the algorithms’ consistency.

The test started with a simple time series without any noise, which was then tested repeatedly with increasing amounts of noise. The goal of this run was to compare the noise resilience of the two algorithms.

The test also consisted of a single, simple time series, which was presented with varying season length. The purpose of this run was to test both algorithms in different result domains.

The test featured 10 examples with no seasonality. This had the purpose to explore the algorithms’ capability to distinguish between seasonal and non-seasonal time series.

The test consisted of 20 time series of seasonal economic data. These financial data were taken primarily from sectors which display seasonality, such as tourisms and restaurants. Three of these test cases contained both annual and quarterly seasonality, and several others only showed a very slight manifestation of seasonality.

The test contained 20 time series of seasonal climate data about temperature, precipitation, sun hours or storm counts.

5.2. Results

During testing, the R library algorithm which uses spectral density estimation was referred to as Spectral and our system using autocorrelation as Autocorr. For each test, the season length suggested by the algorithms was considered correct if it was within an error margin of of the reference value.

The accumulated test results are depicted in Table 1, while the results of the individual test runs can be seen in Figure 5. In the first 6 tests algorithm performed better than algorithm . The most significant difference was in the noise test, were passed 3 tests and 12 tests. The test, which only consisted of time series without seasonality, was the only test run were both algorithms passed the same number of tests. In all other test runs, including and , passed more tests than .

| Database | #Test Cases | Spectral | Autocorr |

|---|---|---|---|

| Synthetic | 125 | 62 | 96 |

| Real | 40 | 21 | 26 |

| 165 | 83 | 122 |

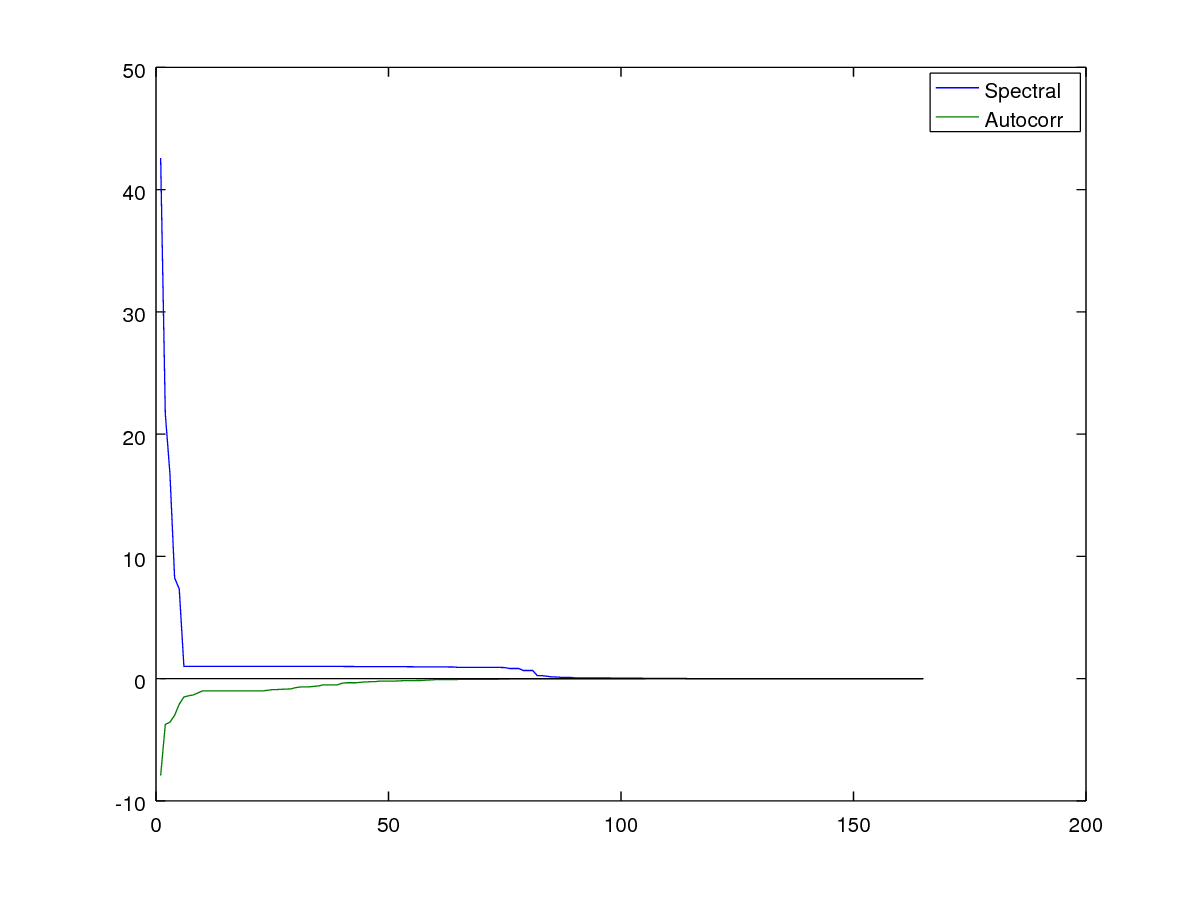

Figure 6 displays the relative difference between the detected season length and the reference value for all test cases. The area between the curves and zero represents the accumulated test error of the algorithms. Spectral had an accumulated error of 172%, while Autocorr’s relative errors add up to 57%.

6. Discussion

The purpose of this paper was to present an algorithm developed for identifying time series’ season length which is sufficiently reliable to be used in real-world applications. The conducted tests tried to cover many different aspects of time series behavior and our system compares favorably against the reference algorithm.

However, the overall results alone do not necessarily suggest that the methods applied in are preferable for identifying season length in all settings. Both implementations still rely on empirically chosen constants, which may have an influence on the outcome. For example, had the constant in for distinguishing linear and quadratic trends been chosen slightly higher, then several time series with quadratic trends may have been misclassified. This argument can be made for every empiric constant in both implementations.

The test, which was a repeated test of the same time series while increasing the noise component from test to test, has revealed a noise susceptibility of . This is likely an inherent property of working with spectral density estimates, as noise tends to hide the relevant frequencies. This is also supported by the test, where failed to disregard outliers induced on otherwise unchanged time series.

Another noteworthy observation is that frequently misclassified season lengths longer than . In fact, never suggested a season length longer than , although there were 18 cases where this would have been necessary. This suggests that the implementation of may not be the optimal choice for investigating seasonality in large time series with very long season lengths. Additional evidence for this assumption is provided by the test, which was designed to test this particular aspect of seasonality.

A dependency that greatly affects both algorithms is that they both rely on an adequate removal of trend from the time series. Algorithm always returned an erroneous result if it failed to correctly identify the trend. Moreover, neither nor were capable of detrending any non-linear or non-square trend. Correctly removing trends from time series is an active research field, fostering the hope that this issue will be addressed.

There is also a single case of a false positive in that is not directly apparent. While it did correctly analyze the season length of test case 5 in the the test, it was only coincidental that the result is correct. The reason for this is that perfectly removed all trend from this purely quadratic time series and then considered almost every not interpolated point in the autocorrelation as potential zero. Computing the mean distance between these obviously yields an average of 1, which is then discarded due to Equation 13. However, with an only slightly altered time series, the average distance could be rounded up to 2, which would not be discarded, yet still incorrect for a purely quadratic time series.

The most expensive operation in both implementations is computing the matrix-inverse required for detrending the data, which has a worst-case computational complexity of . This is far above the desirable computational complexity of , as for an exemplar time series with observations, in the ideal case operations would be required, whereas both implementations need in the worst case operations, which is a thousand times higher.

7. Conclusion

Detecting season length in time series without human assistance is challenging. The method presented in this paper attempts to complete this task by interpolating, filtering and detrending a time series and then analyzing the distances between zeros in its autocorrelation function. The implementation of this concept is still leaves room for improvement, as it still relies on several empirically chosen constants. However, the results demonstrated sufficient robustness in our evaluation.

Future work concerning automated season length detection might attempt to eliminate the algorithm’s constant-dependency by inferring them from the data. Further, the detrending can likely be improved by including high-pass filtering into the procedure. Another interesting concept would be to develop a season length detection algorithm based on a machine learning method like a neural network.

To advance automated seasonality and periodicity mining in general, it is important to develop automated procedures for a dynamic computation of otherwise static constants in contemporary algorithms. Achieving this is an interesting challenge for the future.

References

- (1)

- Berberidis et al. (2002) C. Berberidis, W.G. Aref, M. Atallah, I. Vlahavas, and A.K. Elmagarmid. 2002. Multiple and Partial Periodicity Mining in Time Series Databases. In Proceedings of European Conference on Artificial Intelligence.

- Draper et al. (1966) N.R. Draper, H. Smith, and E. Pownell. 1966. Applied Regression Analysis. Vol. 3. Wiley New York.

- Elfeky et al. (2005) M. G Elfeky, W. G Aref, and A. K Elmagarmid. 2005. Periodicity detection in time series databases. IEEE Transactions on Knowledge and Data Engineering 17, 7 (2005), 875–887.

- Han et al. (1998) J. Han, W. Gong, and Y. Yin. 1998. Mining Segment-Wise Periodic Patterns in Time Series databases. In Proceedings of Conference on Knowledge and Data Discovery.

- Hyndman (2012) R.J. Hyndman. 2012. Measuring Time Series Characteristics. (2012). https://robjhyndman.com/hyndsight/tscharacteristics/

- Indyk et al. (2000) P. Indyk, N. Koudas, and S. Muthukrishnan. 2000. Identifying Representative Trends in Massive Time Series Data Sets Using Sketches. In Proceedings of International Conference on Very Large Data Bases.

- Keogh et al. (2004) E. Keogh, S. Lonardi, and C. A. Ratanamahatana. 2004. Towards parameter-free data mining. In Proceedings of the tenth ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 206–215.

- Lin et al. (2003) J. Lin, E. Keogh, S. Lonardi, and B. Chiu. 2003. A symbolic representation of time series, with implications for streaming algorithms. In Proceedings of the 8th ACM SIGMOD workshop on Research issues in data mining and knowledge discovery. ACM, 2–11.

- Ma and Hellenstein (2001) S. Ma and J.L. Hellenstein. 2001. Mining Partially Reriodic Event Patterns with unknown Periods. In Proceedings of International Conference on Data Engineering. 205–214.

- Rasheed et al. (2011) F. Rasheed, M. Alshalalfa, and R. Alhajj. 2011. Efficient Periodicity Mining in Time Series Databases Using Suffix Trees. IEEE 23, 1 (2011).

- Tukey (1977) J. Tukey. 1977. Exploratory Data Analysis. Reading, Mass.

- Vamos and Craciun (2012) C. Vamos and M. Craciun. 2012. Automatic trend estimation. Springer Publishing Company, Incorporated.

- Wang et al. (2006) Xiaozhe Wang, Kate A. Smith, and R.J. Hyndman. 2006. Characteristic-based Clustering for Time Series Data. In Proceedings of Data mining and Knowledge Discovery.