Empirical Bayes mean estimation with nonparametric errors via order statistic regression on replicated data

Abstract

We study empirical Bayes estimation of the effect sizes of units

from noisy observations on each unit. We show that it is possible to achieve near-Bayes optimal mean squared error, without any assumptions or knowledge about the effect size distribution or the noise. The noise distribution can be heteroskedastic and vary arbitrarily from unit to unit. Our proposal, which we call Aurora, leverages the replication inherent in the observations per unit and recasts the effect size estimation problem as a general regression problem.

Aurora with linear regression provably matches the performance of a wide array of estimators including the sample mean, the trimmed mean, the sample median, as well as James-Stein shrunk versions thereof. Aurora automates effect size estimation for Internet-scale datasets, as we demonstrate on data from a large technology firm.

Keywords: Empirical Bayes, Linear regression, Nonparametric regression, L-statistics, Asymptotic optimality

1 Introduction

Empirical Bayes (EB) (Efron, 2012; Robbins, 1956, 1964) and related shrinkage methods are the de facto standard for estimating effect sizes in many disciplines. In genomics, EB is used to detect differentially expressed genes when the number of samples is small (Smyth, 2004; Love et al., 2014). In survey sampling, EB improves noisy estimates of quantities, like the average income, for small communities (Rao and Molina, 2015). The key insight of EB is that one can often estimate unit-level quantities better by sharing information across units, rather than analyzing each unit separately.

Formally, EB models the observed data as arising from the following generative process:

| (1) |

The goal here is to estimate the mean parameters, for , from the observed data . If and are fully specified, then the optimal estimator (in the sense of mean squared error) is the posterior mean , which achieves the Bayes risk. Empirical Bayes deals with the case where or is unknown, so the Bayes rule cannot be calculated. Most modern EB methods (Jiang and Zhang, 2009; Brown and Greenshtein, 2009; Muralidharan, 2012; Saha and Guntuboyina, 2020) assume that is known (say, ) and construct estimators that asymptotically match the risk of the unknown Bayes rule, without making any assumptions about the unknown prior .

We examine the same problem of estimating the s when the likelihood is also unknown. Indeed, knowledge of is an assumption that requires substantial domain expertise. For example, it took many years for the genomics community to agree on an EB model for detecting differences in gene expression based on microarray data (Baldi and Long, 2001; Lönnstedt and Speed, 2002; Smyth, 2004). Then, once this technology was superseded by bulk RNA-Seq, the community had to devise a new model from scratch, eventually settling on the negative binomial likelihood (Love et al., 2014; Gierliński et al., 2015).

Unfortunately, there is no way to avoid making such strong assumptions when there is no information besides the one per . If is even slightly underspecified, then it becomes hopeless to disentangle from . To appreciate the problem, consider the Normal-Normal model:

| (2) |

Here, is marginally distributed as , and the observations only provide information about . Now, when is known, can be estimated by first estimating the marginal variance and subtracting . Indeed, Efron and Morris (1973) showed that by plugging in a particular estimate of into the Bayes rule , one recovers the celebrated James-Stein estimator (James and Stein, 1961). Yet, as soon as is unknown, then (and hence, ) is unidentified, and there is no hope of approximating the unknown Bayes rule.

However, as any student of random effects knows, the Normal-Normal model (2) becomes identifiable if we simply have independent replicates for each unit . The driving force behind this work is an analogous observation in the context of empirical Bayes estimation: replication makes it possible to estimate with no assumptions on or whatsoever. The method we propose, described in the next section, performs well in practice and nearly matches the risk of the Bayes rule, which depends on the unknown and .

2 The Aurora Method

First, we formally specify the EB model when replicates are available.

| (3) |

Again, the quantity of interest is the mean parameter . The additional parameter is a nuisance parameter that allows for heterogeneity across the units, while preserving exchangeability (Galvao and Kato, 2014; Okui and Yanagi, 2020). For example, is commonly taken to be the conditional variance to allow for heteroskedasticity. However, could even be infinite-dimensional—for instance, a random element from a space of distributions. The have no impact on our estimation strategy and are purely a technical device.

Given data from model (2), one approach would be to collapse the replicates into a single observation per unit—say, by taking their mean—which would bring us back to the setting of model (1). We could appeal to the Central Limit Theorem to justify knowing that the likelihood is Normal. An important message of this paper is that we can do better by using the replicates.

2.1 Proposed Method

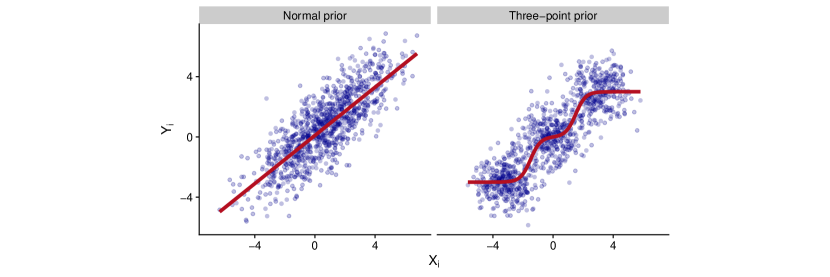

Since we have replicates, we can split the into two groups for each . First, consider the case of replicates so that we can write for . Now, and are conditionally independent given . Figure 1 illustrates the relationship between and under two different settings. The key insight is that the conditional mean is (almost surely) identical to the posterior mean , by the following elementary calculation (Krutchkoff, 1967). (For convenience, we suppress the dependence of the expected values on .)

| (4) |

This suggests that we can estimate the Bayes rule based on (i.e., the posterior mean ) by simply regressing on using any black-box predictive model, such as a local averaging smoother. Let be the fitted regression function; our estimate of each is then just .

To extend this method to , we can again split the replicates into two parts:

| (5) |

where is an arbitrary fixed index for now. (We suppress in the notation below.) Now, one approach is to summarize the vector by the mean of its values and regress on to learn (Coey and Cunningham, 2019). This works for essentially the same reason as the case. However, unless is sufficient for in model (2), then will be different from and suboptimal to .

Instead, we propose learning directly. The rationale is contained in the following result.

Proposition 1.

Proof.

The same argument as (4) shows that almost surely. Now, under exchangeable sampling, the order statistics are sufficient for and therefore it follows that almost surely, with no assumptions on . ∎

Equation (6) suggests that we should regress on the order statistics to learn a function that approximates the posterior mean. The fitted values can be used to estimate . There is one more detail worth mentioning. The estimate depends on the arbitrary choice of in (5). To reduce the variance of the estimate, we average over all choices of . This method, summarized in Table 1, is called Aurora, which stands for “Averages of Units by Regressing on Ordered Replicates Adaptively.”

| Aurora: “Averages of Units by Regressing on Ordered Replicates Adaptively.” | |

|---|---|

| For | |

| 1. | Split the replicates for each unit, , into and , as in (5). |

| 2. | For each , order the values to obtain . |

| 3. | Regress on using any black-box predictive model. Let be the fitted regression function. |

| 4. | Let . |

| end | |

| Estimate each by . | |

3 Related work

The Aurora method is closely related to the extensive literature on empirical Bayes, which we cite throughout this paper. One work that is worth emphasizing is Stigler (1990), who motivated empirical Bayes estimators, like James-Stein, through the lens of regression to the mean; for us, regression is not just a motivation but the estimation strategy itself. We were surprised to find a similar idea to Aurora in a forgotten manuscript, uncited to date, that Johns (1986) contributed to a symposium for Herbert Robbins (Van Ryzin, 1986). Although Johns (1986) used a fairly complex predictive model (projection pursuit regression (Friedman and Stuetzle, 1981)), we show theoretically (Sections 4,5) and empirically (Sections 6,7) that the order statistics encode enough structure that linear regression and -nearest neighbor regression can be used as the predictive model.

Models similar to (2) with replicated noisy measurements of unobservable random quantities have been studied in the context of deconvolution and error-in-variables regression (Devanarayan and Stefanski, 2002; Schennach, 2004). In econometrics, panel data with random effects are often modelled as in (2) with the additional potential complication of time dependence, i.e., indexes time, while may correspond to different geographic regions (Horowitz and Markatou, 1996; Hall and Yao, 2003; Neumann, 2007; Jochmans and Weidner, 2018). Fithian and Ting (2017) use observations from model (2) to learn a low-dimensional smooth parametric model that describes the data well. However, their goal is testing, while Aurora is geared for mean estimation.

The Aurora method is also related to a recent line of research that leverages black-box prediction methods to solve statistical tasks that are not predictive in nature. For example, Chernozhukov et al. (2017) consider inference for low dimensional causal quantities when high dimensional nuisance components are estimated by machine learning. Boca and Leek (2018) reinterpret the multiple testing problem in the presence of informative covariates as a regression problem and estimate the proportion of null hypotheses conditionally on the covariates. The estimated conditional proportion of null hypotheses may then be used for downstream multiple testing methods (Ignatiadis and Huber, 2018). Black-box regression models can also be used to improve empirical Bayes point estimates in the presence of side-information (Ignatiadis and Wager, 2019).

Finally, a crucial ingredient in Aurora is data splitting, which is a classical idea in statistics (Cox, 1975), typically used to ensure honest inference for low dimensional parameters. In the context of simultaneous inference, Rubin, Dudoit, and Van der Laan (2006) and Habiger and Peña (2014) use data-splitting to improve power in multiple testing.

4 Properties of the Aurora estimator

We provide theoretical guarantees for the general Aurora estimator described in Section 2. Throughout this section we split into and as in (5), and we write for the order statistics of . We also write and for the concatenation of all the and , respectively. As before, we omit whenever a definition does not depend on the specific choice of .

4.1 Three oracle benchmarks

In this section we define three benchmarks for assessing the quality of a mean estimator in model (2) (in terms of mean squared error). These benchmarks provide the required context to interpret the theoretical guarantees of Aurora that we establish in Section 4.2.

First, it is impossible to improve on the Bayes rule, so the Bayes risk serves as an oracle. We denote the Bayes risk (based on all replicates) by

| (7) | ||||

As explained in Proposition 1, the function we seek to mimic (for each in the loop of the Aurora algorithm in Table 1) is the oracle Bayes rule based on the order statistics of replicates,

| (8) |

The risk of is the Bayes risk based on replicates,

| (9) |

In the Aurora algorithm we average over the choice of held-out replicate . Thus, we also define an oracle rule that averages over all . We use the following notation for this oracle and its risk:

| (10) |

It is immediate that . Also, by the definition of in (10) and by Jensen’s inequality, it holds that,

so . This bound can be improved through the following insight: are jackknife estimates of the posterior mean and is their average. By a fundamental result for the jackknife (Efron and Stein, 1981, Theorem 2), it holds that111Here we use the fact that the entries of are independent conditionally on . This inequality is also known in the theory of U-statistics (Hoeffding, 1948, Theorem 5.2). . Armed with this insight, in Supplement A.1, we prove that:

Proposition 2.

Under model (2) with , it holds that:

| (11) |

Remark 1.

For sufficiently “regular” problems, will typically be of order , while will be of order ; we make this argument rigorous for location families in Section 5.2 and Supplement E. The correction term on the right hand side of (11) will also be of order in such problems. In our next example, we demonstrate the importance of this additional term.

Example 1 (Normal likelihood with Normal prior).

We consider the Normal-Normal model (2) from the introduction with prior variance and noise variance , and with replicates as in (2). In this case,222The details are given in Supplement D. we can analytically compute that , and so it follows that . The right-most inequality in (11) is an equality and . We conclude that, in the Normal-Normal model, the averaged oracle has risk closer to the full Bayes estimator than to the Bayes estimator based on replicates.

4.2 Regret bound for Aurora

In this section we derive our main regret bound for Aurora. The basic idea is that the in-sample prediction error of the regression method directly translates to bounds on the estimation error for the effect sizes , and thus, Aurora can leverage black-box predictive models. To this end, we define the in-sample prediction error for estimating the averaged oracle ,

| (12) |

When the predictive mechanism of the Aurora algorithm (Table 1) is the same for all ,333That is, the map is the same for all . This does not imply that for , since the training data changes. then Jensen’s inequality provides the following convenient upper bound on (12):

| (13) |

is the in-sample error from approximating by . We are ready to state our main result:

Theorem 3.

The mean squared error of the Aurora estimator (described in Table 1) satisfies the following regret bound under model (2) with .

| (Irreducible Bayes error) | ||||

| (Error due to data splitting) | ||||

| (Estimation error) |

(i.e., the Aurora estimator based on a single held-out response replicate) satisfies the above regret bound with replaced by .

As elaborated in Remark 1, the second error term in the above decomposition will typically be negligible compared to ; this is the price we pay for making no assumptions about and . Hence, beyond the irreducible Bayes error, the main source of error depends on how well we can estimate . Crucially, this error is the in-sample estimation error of , which is often easier to analyze and smaller in magnitude than out-of-sample estimation error (Hastie et al., 2008; Chatterjee, 2013; Rosset and Tibshirani, 2018).

4.3 Aurora with -Nearest-Neighbors is universally consistent

Theorem 3 demonstrated that a regression model with small in-sample error translates, through Aurora, to mean estimates with small mean squared error. Now, we combine this result with results from nonparametric regression to prove that under model (2), it is possible to asymptotically (in ) match the oracle risk (10) and in view of Proposition 2, to outperform the Bayes risk based on replicates.

Theorem 4 (Universal consistency with -Nearest-Neighbor (NN) estimator).

Consider model (2) with . We estimate with the Aurora algorithm where is the -Nearest-Neighbor (NN) estimator with , i.e., the nonparametric regression estimator which predicts444The definition below assumes no ties. In the proof we explain how to randomize to deal with ties.

and is the Euclidean distance. If satisfies , as , then:

This result is a consequence of universal consistency in nonparametric regression (Stone, 1977; Györfi, Kohler, Krzyzak, and Walk, 2006). It demonstrates that Aurora can asymptotically match the Bayes risk with substantial generality,555 Vernon Johns (1957) established a result similar to Theorem 4. We find this remarkable, since Johns (1957) anticipated later developments in nonparametric regression, independently proving universal consistency for partition-based regression estimators as an intermediate step. and suggests the power and expressivity of the Aurora algorithm.

To apply Aurora with NN, a data-driven choice of is required. In Supplement B.2 we describe a procedure that chooses the number of nearest neighbors per held-out response replicate through leave-one-out (LOO) cross-validation, and we study its performance empirically in the simulations of Section 6. Nevertheless, Aurora-NN tuned by LOO, is computationally involved. This motivates our next section; there we study a procedure that is interpretable, easy to implement and that scales well to large datasets.

5 Aurora with Linear Regression

In this section we analyze the Aurora algorithm when linear regression is used as the predictive model. That is, is a linear function of the order statistics

| (14) |

where are the ordinary least squares coefficients of the linear regression . We call the method Auroral, with the final “l” signifying “linear” and write for the resulting estimates of . Our main result is that Auroral matches the performance of the best estimator that is linear in the order statistics based on replicates. To state this result formally, we first define the minimum risk among estimators in class :

| (15) |

The class of interest to us specifically is the class of estimators linear in the order statistics:

| (16) |

This is a broad class that includes all estimators of based on that proceed through the following two steps: (1) summarization, where an appropriate summary statistic of the likelihood is used, that is linear in the order statistics, and (2) linear shrinkage, where the summary statistic is linearly shrunk towards a fixed location. Schematically:

| (e.g. James-Stein shrinkage) |

The summarization step can apply non-linear functions of the original data, such as the median and the trimmed mean, because the input to the linear model are the order statistics, rather than the original data. Such linear combinations of the order statistics are known as -statistics, which is a class so large that it includes efficient estimators of the mean in any smooth, symmetric location family, cf. Van der Vaart (2000) and Section 5.2.

We now show that Auroral matches asymptotically in .

Theorem 5 (Regret over linear estimators).

-

(i)

Assume there exists such that ,666 By the law of total variance, almost surely, it holds that (17) Thus, for example, when have bounded support, there exists such that almost surely and so, the stated assumption holds with . then:

-

(ii)

Assume there exists , such that , then:

If , then the conclusion of Theorem 3 holds for with the term bounded by (under Assumption (i)), resp. (under (ii)).

In datasets, we typically encounter . Then, Theorem 5 implies that Auroral will almost match the risk of the best -statistic based on replicates. This result is in the spirit of retricted empirical Bayes (Griffin and Krutchkoff, 1971; Maritz, 1974; Norberg, 1980; Robbins, 1983), which seeks to find the best estimator among estimators in a given class, such as the best Bayes linear estimators of Hartigan (1969). In these works linearity typically refers to linearity in and not ; Lwin (1976) however uses empirical Bayes to learn the best L-statistic from the class Lin, when the likelihood takes the form of a known location-scale family.

5.1 Examples of Auroral estimation

In this section we give three examples in which Auroral satisfies strong risk guarantees.

Example 2 (Point mass prior).

Suppose the prior on is a point mass at ; that is, . Then, the Bayes rule based on the order statistics, , has risk 0 and is trivially a member of , so . Therefore, by Theorem 5, provided that almost surely (), the risk of the Auroral estimator satisfies

Example 3 (Normal likelihood with Normal prior).

We revisit Example 1,777See Supplement D for details regarding the regret bounds we discuss here. wherein we argued that the averaged oracle (10) has risk equal to the Bayes risk plus . Auroral attains this risk, plus the linear least squares estimation error that decays as .

In addition to Auroral, we consider two estimators, that take advantage of the fact that is sufficient for in the Normal model with replicates:

CC-L implicitly uses the assumption of Normal likelihood by reducing the replicates to their mean, which is the sufficient statistic. Similar to Auroral, its risk is equal to plus and the least squares estimation error, which in this case is (only the slope and intercept need to be estimated for each held-out replicate). James-Stein makes full use of the model assumptions (Normal prior, Normal likelihood, known variance) and is expected to perform best. JS achieves the Bayes risk based on observations, plus an error term that decays as . The price Auroral pays compared to CC-L and JS for using no assumptions whatsoever, when reduction to the mean was possible, is modest.

Example 4 (Exponential families with conjugate priors).

Let be a -finite measure on the Borel sets of and be the interior of the convex hull of the support of . Let . Suppose is open, that both are non-empty and that is differentiable for with strictly increasing derivative .

Now, suppose are generated from model (2) as follows (with implicitly defined). First, is drawn from a prior with Lebesgue density proportional to on for some and . Next, and is drawn from the distribution with -density equal to , where . Diaconis and Ylvisaker (1979, Theorem 2) then prove that,

Thus, and Auroral matches the risk of up to the error term in Theorem 5.

5.2 Auroral estimation in location families

In this section we provide another example of Auroral estimation. In contrast to the rest of this paper, which treats as fixed, we consider an asymptotic regime in which both and tend to (with growing substantially slower than ). In doing so, we hope to provide the following conceptual insights: first, we provide a concrete setting in which Auroral dominates any method that first summarizes as . Second, we elaborate on the expressivity of the class (16).

We consider model (2) with for a smooth prior and , where has density with respect to the Lebesgue measure and is a density that is symmetric around .

We proceed with a heuristic discussion, that we will make rigorous in the formal statements below. Suppose for now that is sufficiently regular with Fisher Information,888 In location families, the Fisher information is constant as a function of the location parameter .

| (18) |

Then, by classical parametric theory, we expect that as 999Since , the likelihood swamps the prior. Furthermore, we will place regularity assumptions on the prior to rule out the possibility of superefficiency.. On the other hand, another classical result in the theory of robust statistics (Bennett, 1952; Jung, 1956; Chernoff, Gastwirth, and Johns, 1967; Van der Vaart, 2000) states that for smooth location families, there exists an L-statistic (i.e., a linear combination of the order statistics) that is asymptotically efficient. By Theorem 5, we thus anticipate that the risk of Auroral is equal to .

In contrast, if we first summarize by , then the best estimator we can possibly use is the posterior mean, . However, for large (so that the likelihood swamps the prior), , and so the risk will behave roughly as , where . We summarize our findings in the Corollary below, and provide the formal proofs in Supplement E.

Corollary 6 (Smooth location families).

Recalling that with equality when is the Gaussian density, we see that Auroral adapts101010 This adaptivity is perhaps expected, in light of existing theory on semiparametric efficiency in location families. For example, it is known that even for one can asymptotically (as ) match the variance of the parametric maximum likelihood estimator in symmetric location families, even without precise knowledge of (Stein, 1956; Bickel et al., 1998). However, the simulations of Section 6.1 demonstrate that Aurora adapts to the unknown likelihood already for , while semiparametric efficiency results are truly asymptotic in , requiring an initial nonparametric density estimate. to the unknown density and outperforms any estimator that first averages .

What about location families that are not regular? Below we give an example, namely the Rectangular location family with , in which a similar conclusion to Corollary 6 holds. The advantage of Auroral is even more pronounced in this case ( risk for Auroral, versus for any method that first averages ).

6 Empirical performance in simulations

In this section, we study the empirical performance of Aurora and competing empirical Bayes algorithms in three scenarios: homoskedastic location families (Section 6.1), heteroskedastic location families (Section 6.2) and a heavy-tailed likelihood (Section 6.3).

6.1 Homoskedastic location families

We start by empirically studying the location family problem from Section 5.2 for replicates and units. We first generate the means from one of two possible priors , parameterized by a simulation parameter : the normal prior and the three-point discrete prior that assigns equal probabilities to . Both prior distributions have variance .

We then generate the replicates around each mean from one of three location families: Normal, Laplace, or Rectangular. The parameters of these distributions are chosen so that the noise variance is .

We compare eight estimators of :

- •

-

•

Standard estimators of location: The mean , the median and the midrange (that is, ).

-

•

Standard empirical Bayes estimators applied to the averages : James-Stein (positive-part) shrinking towards (which we provide with oracle knowledge of ) and the nonparametric maximum likelihood estimator (NPMLE) of Koenker and Mizera (2014) (as implemented in the REBayes package (Koenker and Gu, 2017) in the function “GLmix”), which is a convex programming formulation of the estimation scheme of Kiefer and Wolfowitz (1956) and Jiang and Zhang (2009). For the NPMLE we estimate the standard deviation for each unit by the sample standard deviation over its replicates and use the working approximation .

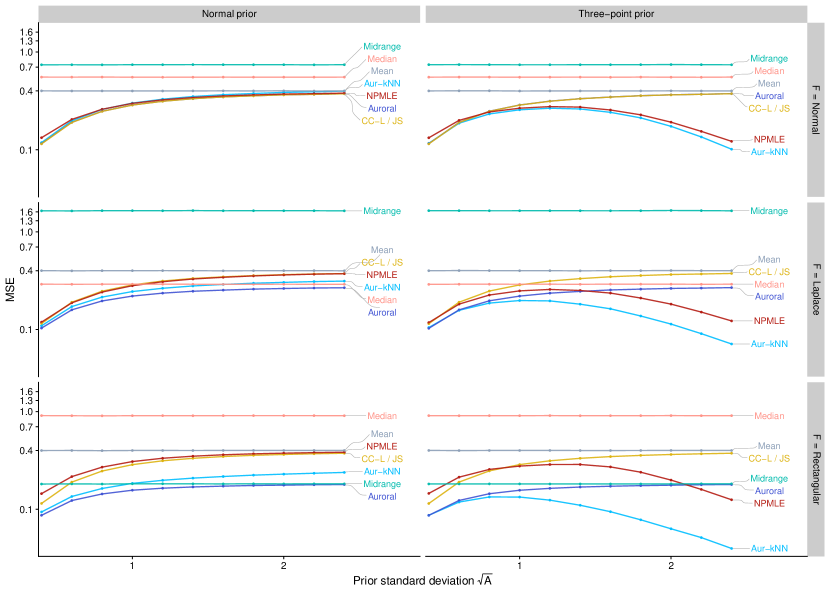

The results111111Throughout this section we calculate the mean squared error by averaging over 100 Monte Carlo replicates. are shown in Figure 2. The standard location estimators have constant mean squared error (MSE) in all panels, since they do not make use of the prior.

We discuss the case of a Normal prior first: here the MSE of all methods is non-decreasing in . Auroral closely matches the best estimator for every and likelihood. In the case of Normal likelihood, James-Stein (with oracle knowledge of ), CC-L and Auroral perform best,121212CC-L and James-Stein perform so similarly in the simulations of this subsection that they are indistinguishable in all panels of Figure 2 with the difference of their MSEs smaller than in all cases. In the first panel (Normal prior and likelihood) Auroral is also indistinguishable from CC-L and James-Stein. followed closely by Aurora-NN and the NPMLE. The standard location estimators are competitive when the prior is relatively uninformative (i.e., is large). Among these, the mean performs best for the Normal likelihood, the median for the Laplace likelihood and the midrange for the Rectangular likelihood.

The three component prior highlights a case in which non-linear empirical Bayes shrinkage can be helpful. Here, Aurora-NN performs best across all settings, closely followed by the NPMLE in the case of the Normal likelihood131313Even for the Normal likelihood, the assumptions of the implemented NPMLE are not fully satisfied, since we use estimated standard deviations for each unit.. The NPMLE is also the second most competitive method for the Laplace likelihood with large prior variance . The behavior of all other methods tracks closely with their behavior under a Normal prior.

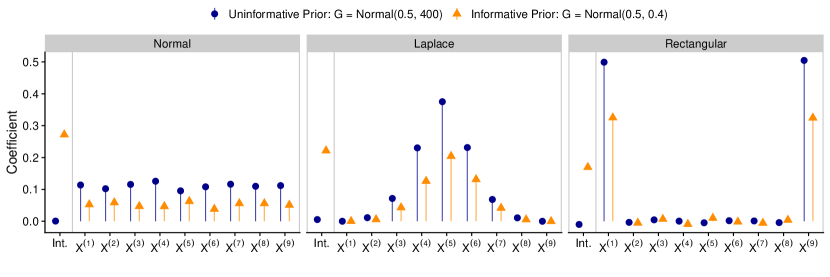

One may at this point wonder: How do the Auroral weights (coefficients) in equation (14) look like? In Figure 3, we show these weights from a single replication (with and ) for each of the three likelihoods considered above and for two Normal priors. First, we focus on the points in blue, which correspond to an uninformative prior (). When the likelihood is Normal, the Auroral weights are roughly constant and equal to . In other words, , that is the Auroral fit with held-out replicate , is (approximately) the sample mean of . When the likelihood is Laplace, the Auroral weights pick out the median and a few order statistics around it. When the likelihood is Rectangular, Auroral assigns approximately weight each to the minimum and the maximum and weight to all of the other order statistics. In other words, is (approximately) the midrange of . Notice that Auroral did not know the likelihood in any of these examples. Rather, it adaptively learned an appropriate summary from the data.

Next, we examine the difference between using informative versus uninformative priors . When the prior is informative (, orange in Figure 3), Auroral automatically learns a non-zero intercept, which is determined by the prior mean, and the remaining weights are shrunk towards zero.

6.2 Heteroskedastic location families

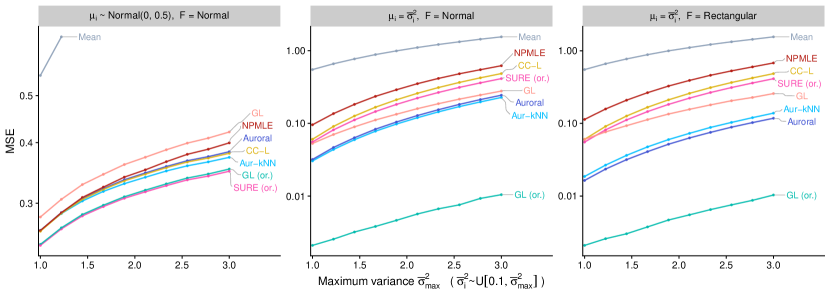

In our second simulation setting, we study location families where is also random and so we find ourselves in the heteroskedastic location family problem. Again we benchmark Auroral, Aurora-NN ( chosen by leave-one-out cross-validation from the set ), CC-L, the Gaussian NPMLE and the sample mean. We also consider two estimators which have been proposed specifically for the heteroskedastic Normal problem, the SURE (Stein’s Unbiased Risk Estimate) method of Xie et al. (2012) that shrinks towards the grand mean and the GL (Group-linear) estimator of Weinstein et al. (2018). We apply these estimators to the averages . Both of these estimators have been developed under the assumption that the analyst has exact knowledge of ; so we provide them with this oracle knowledge (SURE (or.) and GL (or.) — the other methods are not provided this information). Furthermore, we apply the Group-linear method that uses the sample variance calculated based on the replicates.

We use three simulations, inspired by simulation settings a), c) and f) of Weinstein et al. (2018): in all three simulations we let . First we draw , where is a simulation parameter that we vary. Then for the first setting we draw , while for the last two settings we let . Weinstein et al. (2018) use the latter as a model of strong mean-variance dependence. The methods that have access to can in principle predict perfectly (i.e., the Bayes risk is equal to ). Finally we draw where and is either the Normal location-scale family (first two settings) or the Rectangular location-scale family (last setting).

Results from the simulations are shown in Figure 4. The oracle SURE and oracle Group-linear estimators perform best in the first panel and oracle Group-linear strongly outperforms all other methods in the last two panels. This is not surprising, since oracle Group-linear has oracle access to and the method was developed for precisely such settings with strong mean-variance relationship. Among the other methods, Auroral and Aurora-NN remain competitive. In the first panel they match CC-L, while in the last two panels they outperform Group-linear with estimated variances. We point out that Auroral outperforms CC-L in the second panel, despite the Normal likelihood. This is possible, because the mean is no longer sufficient in the heteroskedastic problem.

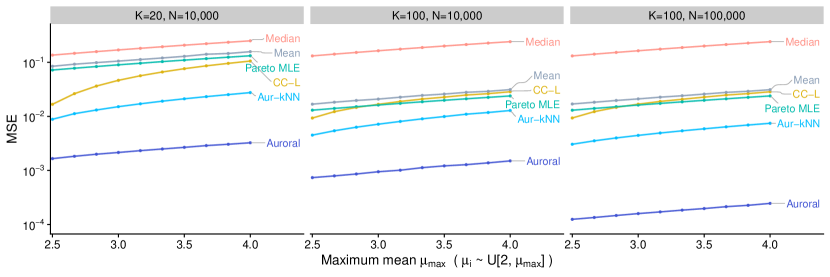

6.3 A Pareto example

For our third example we consider a Pareto likelihood, which is heavy tailed and non-symmetric. Concretely, we let (with a varying simulation parameter) and is the Pareto distribution with tail index and mean . We compare Auroral, Aurora-NN (Aur-NN) with chosen by leave-one-out cross-validation from the set (as described in Supplement B.2), CC-L, the sample mean and median, as well as the maximum likelihood estimator for the Pareto distribution (assuming the tail index is unknown). For this example we also vary . The results are shown in Figure 5. Throughout all settings, Auroral performs best, followed by Aurora-NN. All methods improve as increases. Auroral and Aurora-NN also improve as increases.

7 Application: Predicting treatment effects at Google

In this section, we apply Auroral to a problem encountered at Google and other technology companies —estimating treatment effects at a fine-grained level. All major technology firms run large randomized controlled experiments, often called A/B tests, to study interventions and to evaluate policies (Tang et al., 2010; Kohavi et al., 2013; Kohavi and Longbotham, 2017; Athey and Luca, 2019). Estimation of the average treatment effect from such an experiment (e.g., comparing a metric between treated users and control users) is a well-understood statistical task (Wager et al., 2016; Athey and Imbens, 2017). In the application we consider below, instead, interest lies in estimating treatment effects on fine-grained groups – a separate treatment effect for each of thousands of different online advertisers. In this setting, Empirical Bayes techniques, such as Auroral, can stabilize estimates by sharing information across advertisers.

To apply Auroral for the task of fine-grained estimation of treatment effects, we require replicates. Interestingly, the data from the technology firm we work with is routinely organized and analyzed using ‘streaming buckets’, i.e., the experiment data is divided into chunks of approximately equal size that are called streaming buckets. The buckets correspond to (approximately) disjoint subsets of users, partitioned at random, and so data across different buckets are independent to sufficient approximation. We refer to Chamandy et al. (2012) for a detailed description of the motivation for using streaming buckets to deal with the data’s scale and structure, as well as statistical and computational issues involved in the analysis of streaming bucket data. For the purpose of our application, each streaming bucket corresponds to a replicate in (2).

| Estimator | ||

|---|---|---|

| Aggregate | Baseline | Baseline |

| Mean | ||

| CC-L with Aggregate | ||

| CC-L with Mean | ||

| Auroral | ||

We model the statistical problem of our application as follows. The metric of interest is the cost-per-click (CPC), which is the price a specific advertiser pays for an ad clicked by a user. The goal of the experiment is to estimate the change in CPC before and after treatment. We have data for each advertiser ( advertisers) and two treatment arms; control () and treated (). The data is further divided into buckets. For each advertiser , bucket , and treatment arm , we record the total number of clicks and the total cost of the clicks . We define , the empirical cost-per-click for advertiser in bucket and treatment arm . In this application, the advertisers are the units and the buckets are the replicates. Each observation is , and the goal is to estimate the treatment effect

| (19) |

from model (2) capture advertiser-level idiosyncrasies. We consider the following estimation strategies:

-

1.

The aggregate estimate: we pool the data in all buckets and then compute the difference in CPCs, i.e., .

-

2.

The mean of the , i.e., .

-

3.

The CC-L estimator, wherein for each we use ordinary least squares to regress onto the aggregate estimate in the other buckets, i.e., onto .

-

4.

The CC-L estimator, wherein for each we use ordinary least squares to regress onto the mean of the other buckets, i.e., onto

-

5.

The Auroral estimator that (for each ) regresses on the order statistics .

We empirically evaluate the methods as follows: we use data from an experiment running at Google for one week, retaining only the top advertisers based on number of clicks, resulting in . The number of replicates is equal to . As ground truth, we use the aggregate estimate based on experiment data from the 3 preceding and 3 succeeding weeks. Then, we compute the mean squared error of the estimates (calculated from the one week) against the ground truth and report the percent change compared to the aggregate estimate.

The results are shown in Table 2. The table also shows the results of the same analysis applied to a second metric, the change in click-through rate (CTR), which is the proportion of times that an ad by a given advertiser which is shown to a user is actually clicked. We observe that the improvement in estimation error through Auroral is substantial. Furthermore, Auroral outperforms both variants of CC-L, which in turn outperform estimators that do not share information across advertisers (i.e., the aggregate estimate and the mean of the ).

8 Conclusion

We have presented a general framework for constructing empirical Bayes estimators from noisy replicates of units. The basic idea of our method, which we term Aurora, is to leave one replicate out and regress this held-out replicate on the remaining replicates. We then repeat this process over all choices of held-out replicate and average the results. We have shown that if the replicates are first sorted, then even linear regression produces results that are competitive with the best methods, which usually make parametric assumptions, while our method is fully nonparametric.

We conclude by mentioning some direct extensions of Aurora that are suggested by its connection to regression.

More powerful regression methods:

In this paper, we have used linear regression and -Nearest Neighbor regression to learn . But we can go further; for example, we could use isotonic regression (Guntuboyina and Sen, 2018) based on a partial order on . Or we could combine linear and isotonic regression by considering single index models with non-decreasing link function (Balabdaoui et al., 2019), i.e., predictors of the form , where and is an unknown non-decreasing function. Other possibilities include recursive partitioning (Breiman et al., 1984; Zeileis et al., 2008), in which linear regression is fit on the leaves of a tree, or even random forests aggregated from such trees (Friedberg et al., 2020; Künzel et al., 2019).

More general targets:

We have only considered estimation of in (2). As pointed out in Johns (1957, 1986) this naturally extends to parameters where is a known function. The only modification needed to estimate is that we fit a regression model to learn instead. We may further extend Vernon Johns’ observation to arbitrary U-statistics. Concretely, given and a fixed function , we can use Aurora to estimate . In this case we need to hold out replicates to form the response. For example, with and , we can estimate the conditional variance . Denoising the variance with empirical Bayes is an important problem that proved to be essential for the analysis of genomic data (Smyth, 2004; Lu and Stephens, 2016). However, these papers assumed a parametric form of the likelihood, while Aurora would permit fully nonparametric estimation of the variance parameter.

External covariates:

Model (2) posits a priori exchangeability of the units. However, in many applications, domain experts also have access to side-information about each unit. Hence, multiple authors (Fay and Herriot, 1979; Tan, 2016; Kou and Yang, 2017; Banerjee et al., 2020; Coey and Cunningham, 2019; Ignatiadis and Wager, 2019) have developed methods that improve mean estimation by utilizing information in the . Aurora can be directly extended to accommodate such side information. Instead of regressing on , one regresses on both and .

Software

We provide reproducible code for our simulation results in the following Github repository: https://github.com/nignatiadis/AuroraPaper. A package implementing the method is available at https://github.com/nignatiadis/Aurora.jl. The package has been implemented in the Julia programming language (Bezanson et al., 2017).

Acknowledgments

We are grateful to Niall Cardin, Michael Sklar and Stefan Wager for helpful discussions and comments on the manuscript. We would also like to thank the Associate Editor and the anonymous reviewers for their insightful and helpful suggestions.

References

- Athey and Imbens [2017] S. Athey and G. W. Imbens. The econometrics of randomized experiments. In Handbook of economic field experiments, volume 1, pages 73–140. Elsevier, 2017.

- Athey and Luca [2019] S. Athey and M. Luca. Economists (and economics) in tech companies. Journal of Economic Perspectives, 33(1):209–30, 2019.

- Azadkia [2019] M. Azadkia. Optimal choice of for -nearest neighbor regression. arXiv:1909.05495, 2019.

- Balabdaoui et al. [2019] F. Balabdaoui, C. Durot, and H. Jankowski. Least squares estimation in the monotone single index model. Bernoulli, 25(4B):3276–3310, 2019.

- Baldi and Long [2001] P. Baldi and A. D. Long. A Bayesian framework for the analysis of microarray expression data: regularized t-test and statistical inferences of gene changes. Bioinformatics, 17(6):509–519, 2001.

- Banerjee et al. [2020] T. Banerjee, G. Mukherjee, and W. Sun. Adaptive sparse estimation with side information. Journal of the American Statistical Association, 115(532):2053–2067, 2020.

- Bennett [1952] C. A. Bennett. Asymptotic properties of ideal linear estimators. In Unpublished dissertation, University of Michigan, 1952.

- Bezanson et al. [2017] J. Bezanson, A. Edelman, S. Karpinski, and V. B. Shah. Julia: A fresh approach to numerical computing. SIAM review, 59(1):65–98, 2017.

- Bickel et al. [1998] P. J. Bickel, C. A. Klaassen, Y. Ritov, and J. A. Wellner. Efficient and Adaptive Estimation for Semiparametric Models. Johns Hopkins series in the mathematical sciences. Springer New York, 1998.

- Boca and Leek [2018] S. M. Boca and J. T. Leek. A direct approach to estimating false discovery rates conditional on covariates. PeerJ, 6:e6035, 2018.

- Breiman et al. [1984] L. Breiman, J. Friedman, C. J. Stone, and R. A. Olshen. Classification and Regression Trees. CRC press, 1984.

- Brown and Greenshtein [2009] L. D. Brown and E. Greenshtein. Nonparametric empirical Bayes and compound decision approaches to estimation of a high-dimensional vector of normal means. The Annals of Statistics, pages 1685–1704, 2009.

- Carlsson et al. [2020] K. Carlsson, D. Karrasch, N. Bauer, T. Kelman, E. Schmerling, J. Hoffimann, M. Visser, P. San-Jose, J. Christie, A. Ferris, P. Anthony Blaom, C. Foster, E. Saba, G. Goretkin, I. Orson, O. Samuel, S. Choudhury, and T. Nagy. KristofferC/NearestNeighbors.jl: v0.4.8, Dec. 2020. URL https://doi.org/10.5281/zenodo.4301693.

- Chamandy et al. [2012] N. Chamandy, O. Muralidharan, A. Najmi, and S. Naidu. Estimating uncertainty for massive data streams. 2012.

- Chatterjee [2013] S. Chatterjee. Assumptionless consistency of the lasso. arXiv:1303.5817, 2013.

- Chernoff et al. [1967] H. Chernoff, J. L. Gastwirth, and M. V. Johns. Asymptotic distribution of linear combinations of functions of order statistics with applications to estimation. The Annals of Mathematical Statistics, 38(1):52–72, 1967.

- Chernozhukov et al. [2017] V. Chernozhukov, D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 2017.

- Chu and Hotelling [1955] J. T. Chu and H. Hotelling. The moments of the sample median. The Annals of Mathematical Statistics, pages 593–606, 1955.

- Coey and Cunningham [2019] D. Coey and T. Cunningham. Improving treatment effect estimators through experiment splitting. In The World Wide Web Conference, pages 285–295. ACM, 2019.

- Cox [1975] D. R. Cox. A note on data-splitting for the evaluation of significance levels. Biometrika, 62(2):441–444, 1975.

- Devanarayan and Stefanski [2002] V. Devanarayan and L. A. Stefanski. Empirical simulation extrapolation for measurement error models with replicate measurements. Statistics & Probability Letters, 59(3):219–225, 2002.

- Diaconis and Ylvisaker [1979] P. Diaconis and D. Ylvisaker. Conjugate priors for exponential families. The Annals of Statistics, pages 269–281, 1979.

- Efron [2012] B. Efron. Large-scale inference: empirical Bayes methods for estimation, testing, and prediction, volume 1. Cambridge University Press, 2012.

- Efron and Morris [1973] B. Efron and C. Morris. Stein’s estimation rule and its competitors—an empirical Bayes approach. Journal of the American Statistical Association, 68(341):117–130, 1973.

- Efron and Stein [1981] B. Efron and C. Stein. The jackknife estimate of variance. The Annals of Statistics, pages 586–596, 1981.

- Fay and Herriot [1979] R. E. Fay and R. A. Herriot. Estimates of income for small places: an application of James-Stein procedures to census data. Journal of the American Statistical Association, 74(366a):269–277, 1979.

- Fithian and Ting [2017] W. Fithian and D. Ting. Family learning: nonparametric statistical inference with parametric efficiency. arXiv:1711.10028, 2017.

- Friedberg et al. [2020] R. Friedberg, J. Tibshirani, S. Athey, and S. Wager. Local linear forests. Journal of Computational and Graphical Statistics, pages 1–15, 2020.

- Friedman and Stuetzle [1981] J. H. Friedman and W. Stuetzle. Projection pursuit regression. Journal of the American statistical Association, 76(376):817–823, 1981.

- Galvao and Kato [2014] A. F. Galvao and K. Kato. Estimation and inference for linear panel data models under misspecification when both n and t are large. Journal of Business & Economic Statistics, 32(2):285–309, 2014.

- Gierliński et al. [2015] M. Gierliński, C. Cole, P. Schofield, N. J. Schurch, A. Sherstnev, V. Singh, N. Wrobel, K. Gharbi, G. Simpson, and T. Owen-Hughes. Statistical models for RNA-seq data derived from a two-condition 48-replicate experiment. Bioinformatics, 31(22):3625–3630, 2015.

- Gill and Levit [1995] R. D. Gill and B. Y. Levit. Applications of the van Trees inequality: a Bayesian Cramér-Rao bound. Bernoulli, 1(1-2):59–79, 1995.

- Griffin and Krutchkoff [1971] B. S. Griffin and R. G. Krutchkoff. Optimal linear estimators: An empirical Bayes version with application to the binomial distribution. Biometrika, 58(1):195–201, 1971.

- Guntuboyina and Sen [2018] A. Guntuboyina and B. Sen. Nonparametric shape-restricted regression. Statistical Science, 33(4):568–594, 2018.

- Györfi et al. [2006] L. Györfi, M. Kohler, A. Krzyzak, and H. Walk. A distribution-free theory of nonparametric regression. Springer Science & Business Media, 2006.

- Habiger and Peña [2014] J. D. Habiger and E. A. Peña. Compound p-value statistics for multiple testing procedures. Journal of multivariate analysis, 126:153–166, 2014.

- Hall and Yao [2003] P. Hall and Q. Yao. Inference in components of variance models with low replication. The Annals of Statistics, 31(2):414–441, 2003.

- Hartigan [1969] J. Hartigan. Linear Bayesian methods. Journal of the Royal Statistical Society: Series B, 31(3):446–454, 1969.

- Hastie et al. [2008] T. Hastie, T. Robert, and J. H. Friedman. The Elements of Statistical Learning: Data Mining, Inference, and Prediction (2nd ed.). Springer Series in Statistics. Springer New York, 2008.

- Hoeffding [1948] W. Hoeffding. A class of statistics with asymptotically normal distribution. Annals of Mathematical Statistics, 19(3):293–325, 1948.

- Horowitz and Markatou [1996] J. L. Horowitz and M. Markatou. Semiparametric estimation of regression models for panel data. The Review of Economic Studies, 63(1):145–168, 1996.

- Ignatiadis and Huber [2018] N. Ignatiadis and W. Huber. Covariate powered cross-weighted multiple testing. arXiv:1701.05179, 2018.

- Ignatiadis and Wager [2019] N. Ignatiadis and S. Wager. Covariate-powered empirical Bayes estimation. In Advances in Neural Information Processing Systems, pages 9620–9632, 2019.

- James and Stein [1961] W. James and C. Stein. Estimation with quadratic loss. In Proceedings of the fourth Berkeley symposium on mathematical statistics and probability, volume 1, pages 361–379, 1961.

- Jiang and Zhang [2009] W. Jiang and C.-H. Zhang. General maximum likelihood empirical Bayes estimation of normal means. The Annals of Statistics, 37(4):1647–1684, 2009.

- Jochmans and Weidner [2018] K. Jochmans and M. Weidner. Inference on a distribution from noisy draws. arXiv:1803.04991, 2018.

- Johns [1957] M. V. Johns. Non-parametric empirical Bayes procedures. The Annals of Mathematical Statistics, pages 649–669, 1957.

- Johns [1986] M. V. Johns. Fully nonparametric empirical Bayes estimation via projection pursuit. In Adaptive statistical procedures and related topics, pages 164–178. Institute of Mathematical Statistics, 1986.

- Johnson and Barron [2004] O. Johnson and A. Barron. Fisher information inequalities and the central limit theorem. Probability Theory and Related Fields, 129(3):391–409, 2004.

- Jung [1956] J. Jung. On linear estimates defined by a continuous weight function. Arkiv für Matematik, 3(3):199–209, 1956.

- Kiefer and Wolfowitz [1956] J. Kiefer and J. Wolfowitz. Consistency of the maximum likelihood estimator in the presence of infinitely many incidental parameters. The Annals of Mathematical Statistics, pages 887–906, 1956.

- Koenker and Gu [2017] R. Koenker and J. Gu. REBayes: Empirical Bayes mixture methods in R. Journal of Statistical Software, 82(8):1–26, 2017.

- Koenker and Mizera [2014] R. Koenker and I. Mizera. Convex optimization, shape constraints, compound decisions, and empirical Bayes rules. Journal of the American Statistical Association, 109(506):674–685, 2014.

- Kohavi and Longbotham [2017] R. Kohavi and R. Longbotham. Online controlled experiments and A/B testing. Encyclopedia of machine learning and data mining, 7(8):922–929, 2017.

- Kohavi et al. [2013] R. Kohavi, A. Deng, B. Frasca, T. Walker, Y. Xu, and N. Pohlmann. Online controlled experiments at large scale. In Proceedings of the 19th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 1168–1176, 2013.

- Kou and Yang [2017] S. Kou and J. J. Yang. Optimal shrinkage estimation in heteroscedastic hierarchical linear models. In Big and Complex Data Analysis, pages 249–284. Springer, 2017.

- Krutchkoff [1967] R. G. Krutchkoff. A supplementary sample non-parametric empirical Bayes approach to some statistical decision problems. Biometrika, 54(3-4):451–458, 1967.

- Künzel et al. [2019] S. R. Künzel, T. F. Saarinen, E. W. Liu, and J. S. Sekhon. Linear aggregation in tree-based estimators. arXiv:1906.06463, 2019.

- Lehmann and Romano [2006] E. L. Lehmann and J. P. Romano. Testing statistical hypotheses. Springer Science & Business Media, 2006.

- Lönnstedt and Speed [2002] I. Lönnstedt and T. Speed. Replicated microarray data. Statistica Sinica, pages 31–46, 2002.

- Love et al. [2014] M. I. Love, W. Huber, and S. Anders. Moderated estimation of fold change and dispersion for RNA-seq data with DESeq2. Genome biology, 15(12):550, 2014.

- Lu and Stephens [2016] M. Lu and M. Stephens. Variance adaptive shrinkage (vash): flexible empirical Bayes estimation of variances. Bioinformatics, 32(22):3428–3434, 2016.

- Lwin [1976] T. Lwin. Optimal linear estimators of location and scale parameters using order statistics and related empirical Bayes estimation. Scandinavian Actuarial Journal, 1976(2):79–91, 1976.

- Maritz [1974] J. S. Maritz. Aligning of estimates: an alternative to empirical Bayes methods. Australian Journal of Statistics, 16(3):135–143, 1974.

- Muralidharan [2012] O. Muralidharan. High dimensional exponential family estimation via empirical Bayes. Statistica Sinica, pages 1217–1232, 2012.

- Neumann [2007] M. H. Neumann. Deconvolution from panel data with unknown error distribution. Journal of Multivariate Analysis, 98(10):1955–1968, 2007.

- Norberg [1980] R. Norberg. Empirical Bayes credibility. Scandinavian Actuarial Journal, 1980(4):177–194, 1980.

- Okui and Yanagi [2020] R. Okui and T. Yanagi. Kernel estimation for panel data with heterogeneous dynamics. The Econometrics Journal, 23(1):156–175, 2020.

- Rao and Molina [2015] J. Rao and I. Molina. Small Area Estimation. Wiley Series in Survey Methodology. Wiley, 2015. ISBN 9781118735787.

- Rider [1957] P. R. Rider. The midrange of a sample as an estimator of the population midrange. Journal of the American Statistical Association, 52(280):537–542, 1957.

- Robbins [1956] H. Robbins. An empirical Bayes approach to statistics. In Proceedings of the Third Berkeley Symposium on Mathematical Statistics and Probability, Volume 1: Contributions to the Theory of Statistics. The Regents of the University of California, 1956.

- Robbins [1964] H. Robbins. The empirical Bayes approach to statistical decision problems. Annals of Mathematical Statistics, 35:1–20, 1964.

- Robbins [1983] H. Robbins. Some thoughts on empirical Bayes estimation. The Annals of Statistics, pages 713–723, 1983.

- Rosset and Tibshirani [2018] S. Rosset and R. J. Tibshirani. From fixed-X to random-X regression: Bias-variance decompositions, covariance penalties, and prediction error estimation. Journal of the American Statistical Association, pages 1–14, 2018.

- Rubin et al. [2006] D. Rubin, S. Dudoit, and M. Van der Laan. A method to increase the power of multiple testing procedures through sample splitting. Statistical Applications in Genetics and Molecular Biology, 5(1), 2006.

- Saha and Guntuboyina [2020] S. Saha and A. Guntuboyina. On the nonparametric maximum likelihood estimator for gaussian location mixture densities with application to gaussian denoising. Annals of Statistics, 48(2):738–762, 2020.

- Schennach [2004] S. M. Schennach. Estimation of nonlinear models with measurement error. Econometrica, 72(1):33–75, 2004.

- Smyth [2004] G. K. Smyth. Linear models and empirical Bayes methods for assessing differential expression in microarray experiments. Statistical applications in genetics and molecular biology, 3(1):1–25, 2004.

- Stein [1956] C. Stein. Efficient nonparametric testing and estimation. In Proceedings of the Third Berkeley Symposium on Mathematical Statistics and Probability, Volume 1: Contributions to the Theory of Statistics. The Regents of the University of California, 1956.

- Stigler [1990] S. M. Stigler. The 1988 Neyman memorial lecture: a Galtonian perspective on shrinkage estimators. Statistical Science, 5(1):147–155, 1990.

- Stone [1977] C. J. Stone. Consistent nonparametric regression. The Annals of Statistics, pages 595–620, 1977.

- Tan [2016] Z. Tan. Steinized empirical Bayes estimation for heteroscedastic data. Statistica Sinica, pages 1219–1248, 2016.

- Tang et al. [2010] D. Tang, A. Agarwal, D. O’Brien, and M. Meyer. Overlapping experiment infrastructure: More, better, faster experimentation. In Proceedings of the 16th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 17–26, 2010.

- Tsybakov [2008] A. Tsybakov. Introduction to Nonparametric Estimation. Springer Series in Statistics. Springer New York, 2008. ISBN 9780387790527.

- Van der Vaart [2000] A. W. Van der Vaart. Asymptotic statistics, volume 3. Cambridge university press, 2000.

- Van Ryzin [1986] J. Van Ryzin. Adaptive statistical procedures and related topics: Proceedings of a symposium in honor of Herbert Robbins, June 7-11, 1985, Brookhaven National Laboratory, Upton, New York. Institute of Mathematical Statistics, 1986.

- Van Trees [1968] H. L. Van Trees. Detection, estimation, and modulation theory, part I: detection, estimation, and linear modulation theory. Wiley, New York, 1968.

- Wager et al. [2016] S. Wager, W. Du, J. Taylor, and R. J. Tibshirani. High-dimensional regression adjustments in randomized experiments. Proceedings of the National Academy of Sciences, 113(45):12673–12678, 2016.

- Weinstein et al. [2018] A. Weinstein, Z. Ma, L. D. Brown, and C.-H. Zhang. Group-linear empirical Bayes estimates for a heteroscedastic normal mean. Journal of the American Statistical Association, 113(522):698–710, 2018.

- Xie et al. [2012] X. Xie, S. Kou, and L. D. Brown. SURE estimates for a heteroscedastic hierarchical model. Journal of the American Statistical Association, 107(500):1465–1479, 2012.

- Zeileis et al. [2008] A. Zeileis, T. Hothorn, and K. Hornik. Model-based recursive partitioning. Journal of Computational and Graphical Statistics, 17(2):492–514, 2008.

Appendix A Proofs for Section 2

A.1 Proof for Proposition 2

Proof.

For the LHS inequality, it suffices to note that is a function of , and so is dominated by the Bayes rule in terms of mean squared error. For the RHS, we proceed as follows. First,

follows from the law of total variance and the other equalities are a consequence of the definition . Next,

By linearity,

In the last line we used again the fact that . We now proceed with the key step of our argument:

and follow from the law of total variance. For we used two results: for the right part, we used the fact that . For the left part, as announced in the main text, we used Theorem 2 of Efron and Stein [1981].

We conclude by combining the preceding displays. ∎

A.2 Proof for Theorem 3

Proof.

We first obtain a decomposition for a single coordinate . For simplicity, we suppress the dependence on and and first prove the result for , i..e, Aurora based on a single held-out response replicate .

| (S1) |

To see why the cross-term vanishes in the second equality above, observe that the factor is measurable with respect to . Therefore, the expectation conditional on is zero (almost surely), so the unconditional expectation (i.e., the cross-term) is also zero.

Next, we examine the quantity inside the expectation in the second term of (S1). By adding and subtracting and using the inequality , we obtain

| (S2) |

Now, we take the expectation of (S2). For the first term, we can repeat the argument from (S1) to obtain

which can be rearranged to show that

To summarize, we have the following result for a single coordinate :

Finally, we average over all to obtain the desired result:

The proof for is the same verbatim, if we replace by , by and by . ∎

Appendix B Aurora with Nearest Neighbors

B.1 Proof for Theorem 4

Proof.

Throughout the proof we assume that ties among the happen with probability . We avoid ties as follows. As in Chapter 6 of Györfi et al. [2006], we use NN to regress on , where are independently drawn from for some small, fixed . The regression function remains the same, since almost surely . We will however suppress the from our notation and assume ties do not occur for the ; otherwise the proofs go through verbatim by replacing by in all subsequent arguments.

We first claim that:

| (S3) | ||||

To see this, first note that:

| (S4) |

By the Cauchy–Schwarz inequality:

By definition it holds that . By (13) and permutation equivariance (with respect to permutations of the units) of the NN estimator (when there are no ties) it holds that:

Taking expectations in (S4), using the above results and rearranging, we conclude with the claim in (S3). Returning to the main proof, in view of (S3), it suffices to show that:

| (S5) |

By exchangeability of units in (2) and permutation equivariance of the NN estimator without ties, (S5) is equivalent to proving that:

We prove this by instead considering the NN estimator applied to all observations except the first; however still with the same number of nearest neighbors (instead of ). Then:

The first of these terms converges to by existing results on universal consistency in nonparametric regression, concretely Theorem 6.1 of Györfi et al. [2006]. We need to show that the second term also converges to . Let be the -th NN of among . Then

Consequently:

The first term goes to , since we assumed that and . We handle the second term as follows:

We elaborate on two steps: holds by exchangeability of the . holds for a constant that depends only on the dimension by Corollary 6.1. of Györfi et al. [2006]. To conclude we divide by and the result follows since we assumed that and .

∎

B.2 Tuning of Aurora-NN by cross-validation

Aurora-NN is a specific instantiation of the general Aurora algorithm (Table 1) with a specific choice of Step 3, which takes the form of leave-one-out cross-validated -Nearest Neighbor regression (see e.g., Azadkia [2019] and references therein). The box below presents the algorithm in detail:

Two remarks are in order:

-

1.

A naive approach to finding all nearest neighbors in step 3 of the algorithm (say, for a fixed held-out response replicate ) has computational complexity . By preprocessing all ordered samples (at the beginning of step 3), this computational complexity may be decreased, especially for small . In our default implementation we preprocess the data using a d-tree as implemented in the NearestNeighbors.jl [Carlsson et al., 2020] package when ,. For we use brute-force search of nearest neighbors.

-

2.

The leave-one-out calculation can be substantially sped up by reusing the computation from step when computing via the following elementary identity:

Appendix C Proof for Auroral estimator (Theorem 5)

Proof.

Throughout this proof we let be the orthogonal projection operator onto the linear space spanned by the columns of and the ones vector . We also use vectorized notation, e.g., , . With this notation it holds that

First, by Jensen’s inequality:

Thus it suffices to bound for a fixed . In doing so, we omit from the notation, e.g., we write instead of , instead of and instead of . We also (with slight abuse of notation) write . It then holds that:

It remains to bound the terms .

Bound on I: We claim that . This holds since:

Thus:

Bound on II: The argument here is similar to results on fixed design linear regression, see e.g., Theorem 11.1 in Györfi et al. [2006]. We have that:

where is the diagonal matrix with -th diagonal entry equal to . To conclude with the bound on , we provide two separate bounds on according to whether Assumption (i) or (ii) of Theorem 5 holds.

We start with (i). We note that in the positive semi-definite order. By trace properties and since is an orthogonal projection matrix, it thus holds that:

Integrating over and using assumption (i), we conclude that:

We turn to (ii). Let , then:

For the penultimate inequality we used Cauchy–Schwarz and for the last inequality, we used the following two intermediate results: first, and so by symmetry and . Second,

Bound on III: It remains to bound the cross-term III. We will show that . The crucial fact we use is that :

Integrating over we conclude. Let us justify .

follows because , since is orthogonal to the space spanned by . holds since for any vector , it holds that by positive semidefiniteness of .

Appendix D Normal prior and Homoskedastic Normal likelihood

We consider the more general case where . The results for the example may be recovered by taking . Throughout we assume that .

D.1 Oracle risks: Details for Example 1

The three oracle estimators are:

where is the sample average of . They have the following oracle risks:

Furthermore, the RHS of Proposition 2, equation (11), holds with equality, i.e.,

| where |

Proof.

The first two calculations are standard, and we provide the details for and its risk only. First, by definition of :

To evaluate the risk, let us write and (recall is the Bayes rule here). Then:

Furthermore:

∎

D.2 Data-driven risks: Details for Example 3

Recall that the Bayes risk is equal to . The upper bounds on the risk of the three estimators considered in this example are as follows:.

Auroral:

CC-L:

James-Stein:

Proof.

We consider each estimator separately.

Auroral: The result follows from Theorem 3 along with the bound on derived in Theorem 5. To apply the latter, we need to compute .

Thus:

| (S6) |

CC-L: The derivation is similar to the result for Auroral above and is omitted. The main difference is that we solve a linear least squares problem with an intercept and a single regressor (instead of an intercept and regressors).

James-Stein: The calculations are standard, e.g., see Chapter 1 of Efron [2012]. First, using Stein’s identity we get that:

Now notice that , where is the distribution with degrees of freedom, and so , which in turn yields:

Dividing by we get the required claim.

∎

D.2.1 Auroral and CC-L with a single held-out response

We conclude this section by noting that we can compute the risk of Auroral and CC-L exactly, if we omit the averaging over in the Aurora algorithm. In particular:

Proof.

We start with Auroral. Throughout we use the same notation as in Section C. Further, we write for . First:

Notice that . By conditioning on , we get:

Here we used that is homoskedastic. So as an intermediate result we conclude that:

For the remaining term we condition on and observe that and that is homoskedastic:

We conclude by using the expression for derived in (S6), by iterated expectation and by rearranging terms. The result for CC-L can be derived in a similar way. We note that the formula for CC-L appears (with a typo) as Corollary 1 in Coey and Cunningham [2019].

∎

Appendix E Location families: Formal statements for Section 5.2

E.1 Regularity assumptions

Assumption 1 (Regular prior).

The prior distribution has compact support , , and has density w.r.t. the Lebesgue measure. Furthermore, is absolutely continuous on , satisfies and also has finite Fisher information:

Assumption 2 (Regular location density).

We assume that has Lebesgue density with a fixed density and write (with some abuse of notation) for the corresponding distribution. We assume that:

-

(i)

is symmetric around .

-

(ii)

The fourth moment of exists, i.e., .

-

(iii)

is twice continuously differentiable and is an interval. The function is -Hölder continuous on for some ,141414 That is, there exist such that for all . where . The location Fisher information exists and is finite:

Remark S1.

Two examples of densities satisfying Assumption 2 are:

-

1.

The Gaussian density for . In this case, and .

-

2.

The logistic density, for . In this case, and .

The Laplace density does not satisfy the above regularity conditions. However, we may manually check that the conclusion of Corollary 6 holds in that case as well (see Remark S2 below for the proof in the Laplace case).

E.2 Proof of Corollary 6

We split up the proof over 3 individual parts, for each of the possible estimators considered.

E.2.1 Proof for CC-L estimator

Proof.

To simplify the exposition of the proof, we make a centering assumption that and we fit the linear regression without intercept (). The results are identical for the uncentered case where and we use an intercept.

Lower bound: The estimator takes the form,

Let us write:

| (S7) | ||||

We will justify below. From the Central Limit Theorem and Slutsky it follows that,

Then, by Fatou’s Lemma:

By exchangeability: and so we have established that:

It remains to show . It suffices to show that:

| (S8) |

For the first of these results, note that:

By the law of large numbers, it holds that . Furthermore, , since for any

For the second part of (S8), let us note that and , where . As a first consequence we have that , where:

Second, for any and any , we get that:

Next, fixing another , it holds that:

since . Thus:

We conclude by noting that

Upper bound: Repeating the argument of the proof of Theorem 5 and noting that for some by our assumptions on the support of and since is constant for location families, we get:

The first term is upper bounded by by plugging in and since we get:

We conclude, that

∎

E.2.2 Proof for estimator

Proof.

Lower bound: Let (it does not depend on for location families) and define the normalized sum . Since and , Johnson and Barron [2004, Theorem 1.6] prove that:

where is — with some abuse of notation — the location Fisher information of the Lebesgue density of conditionally on the location parameter .151515Part of the statement is also that exists and is finite for all large enough. Next, note that and so . By Corollary S1 below (van Trees inequality), applied for and one replicate,

Upper bound: The Bayes risk of is upper bounded by the risk of , i.e.,

Combining the upper and lower bounds, we find that,

∎

E.2.3 Proof for Auroral estimator

Proof.

Lower bound: By Corollary S1 below (van Trees inequality) it holds for the Bayes risk that,

So:

Upper bound: The first step consists of upper bounding the risk . We will do this by choosing an appropriate function from the class , cf. (16) and bounding its mean squared error for estimating . To this end, fix for the intercept and let , for a -Hölder continuous function to be chosen below. The L-statistic we study takes the form

| (S9) |

We may write where is -centered, so that:

Here . By Hölder continuity of :

Choosing to be , we thus get that (with the term being uniform over in the support of )

Van der Vaart [2000, Proof of Theorem 22.3] establishes that:

where the does not depend on . Now let us make the concrete choice . At the end of the proof, we will show that for this choice of :

| (S10) |

Thus we get that

and so,

| (S11) |

Therefore, by Theorem 5 and noting that for some (arguing as in the proof for CC-L), we get

The conclusion follows by taking since then , , i.e., we get that,

Fisher information calculations: It remains to prove (S10). First

For the second term, we first note that for the given choice of :

Thus we need to show that the numerator of the last expression is equal to , where . To this end, first let be an i.i.d. copy of . Then, since , it follows that . On the other hand, by absolute continuity of , we may write almost surely:

Applying the same argument formally with variable instead of and multiplying the results, we get:

Assume momentarily that we can apply Fubini’s theorem, then is equal to,

as claimed. To see why we may apply Fubini’s theorem, note that under the claimed assumptions, there exists a constant such that for almost all in the support of and so, almost surely:

The conclusion follows by Tonelli’s theorem, since .

∎

Remark S2 (Proof in the case of the Laplace distribution.).

Consider the Laplace location family with Lebesgue density , where

The scale parameterization is such that . We note that is absolutely continuous and is differentiable in quadratic mean with Fisher Information equal to [Lehmann and Romano, 2006, Example 12.2.4].

These properties of suffice for most steps of the proof of Corollary 6. The higher order smoothness is required only for deriving the upper bound for the Auroral estimator. In particular, the construction of a L-statistic in (S9) used to upper bound in (S11), no longer works. However, the following simple choice works instead: we choose as the median of . For simplicity we take limits over even , i.e., we assume that for and take and . Chu and Hotelling [1955] then prove that:

But and so (S11) holds, and the rest of the proof follows verbatim.

E.2.4 Proof of Corollary 7

As in the proof of Corollary 6, we need to bound the risk of each of the three estimators separately. It will be convenient to do the following preliminary calculation. In the rectangular location family,

CC-L: All steps of the proof in Section E.2.1 go through, and so we get,

Posterior mean based on average, : In this case the proof of Section E.2.2 goes through, and we get the same expression as for CC-L above. There is one subtlety involved in applying Johnson and Barron [2004, Theorem 1.6]: the Fisher information of the rectangular distribution is not well-defined. Nevertheless, the convolution of with itself, i.e., the density of , is equal to the triangular density, which has finite Fisher information and is absolutely continuous. Thus, we may apply Theorem 1.6 of Johnson and Barron [2004].

Auroral: Let be the sample midrange based on . is unbiased for and Rider [1957, Section 4] showed that . Since , it follows that . Applying Theorem 5 and noting that for some , we get

Since , we conclude that:

We conclude with the statement of the corollary by combining the results for the three estimators.

E.2.5 The van Trees inequality

Corollary S1 (The van Trees inequality for location families).

In the setting of Section 5.2, assume that:

-

(a)

The density w.r.t. the Lebesgue measure is absolutely continuous and symmetric around .

-

(b)

The location Fisher information for exists and is finite:

-

(c)

The prior distribution has compact support and has density w.r.t. the Lebesgue measure. Furthermore, is absolutely continuous on , satisfies and also has finite Fisher information:

Then, the Bayes risk for estimating satisfies:

Proof.

This is a direct corollary of the van Trees inequality [Van Trees, 1968, Gill and Levit, 1995]. Concretely, here we apply the form presented in Theorem 2.13 in Tsybakov [2008]. There results are phrased more generally for models , where is the Lebesgue density for a fixed parameter value . Here we have , which simplifies results. Concretely, we quickly verify the three assumptions (i),(ii),(iii) of Theorem 2.13 in Tsybakov [2008]:

For (i), joint measurability of in follows from absolute continuity of . For we use translation invariance of the Lebesgue measure to note that the Fisher information is constant as a function of the location parameter. We also use the fact that the Fisher Information in the experiment where we observe independent replicates is equal to -times the Fisher information in the experiment with a single replicate. Finally, assumption (iii) in Tsybakov [2008] is identical to assumption (c). ∎