*Corresponding author.

1. Introduction

This paper proposes a model in which a company can increase its current electricity production by irreversible investments in solar panels, while maximizing net profits. Irreversible investment problems have been widely studied in the context of real options and optimal capacity expansion. Related models in the economics literature are, for example, [6] and the monography [16]. Other relevant papers appearing in the mathematical literature are [1, 13, 15, 18, 19, 21, 30, 33, 34, 36], among many others.

We consider an infinitely-lived profit maximizing company which is a large player in the market. The company can install solar panels in order to increase its production level of electricity up to a given maximum level. The electricity generated will immediately be sold in the market, and while installing additional panels, the company incurs constant proportional costs. As it is assumed that the company is a large market player, its activities have an impact on the electricity price. In particular, we assume that the long-term electricity price level is negatively affected by the current level of installed power; that is, the electricity price will tend to move towards a lower price level if the electricity production is increased. Therefore, the company has to install solar panels carefully in order to avoid permanently low electricity prices which clearly decrease the marginal profits from selling electricity in the market.

The mathematical formulation of the model leads to a two-dimensional degenerate singular stochastic control problem (see, for example, [25, 26, 28] as early contributions) whose components are the electricity price and the current level of installed power which is purely controlled. To the best of our knowledge, this paper is the first which provides the complete explicit solution to a two-dimensional degenerate singular stochastic control problem in which the drift of one component of the state process (the electricity price) is linearly affected by the monotone process giving the cumulative amount of control (the level of installed power). In our model the electricity price evolves as an Ornstein-Uhlenbeck process, and dealing with such a process makes the problem more difficult in comparison to, for example, a geometric Brownian motion setting, due to the unhandy and non-explicit expressions of the fundamental solutions of the second-order ordinary differential equation involving the infinitesimal generator of the underlying Ornstein-Uhlenbeck process. It is worth noticing that our mathematical formulation shares similarities with the recent article [17] in which a central bank can choose a control of bounded variation for managing the inflation. The methodology and results of [17] are indeed different with respect to ours: in fact, in that paper the authors provide a theoretical study of the structure and regularity of the value function using viscosity theory and free-boundary analysis, but do not construct an explicit solution, as instead we do.

Price impact models have gained the interest of many researchers in recent years. Some of these works are also formulated as a singular stochastic control problem and study questions of optimal execution: [4] and [5] take into account a multiplicative and transient price impact, whereas [24] considers an exponential parametrization in a geometric Brownian motion setting allowing for a permanent price impact. Also, a price impact model working with singular stochastic controls has been studied by [2], motivated by an irreversible capital accumulation problem with permanent price impact, and by [20], in which the authors consider an extraction problem with Ornstein-Uhlenbeck dynamics and transient price impact. In all of the aforementioned papers on price impact models dealing with singular stochastic controls [2, 4, 5, 20, 24], the agents’ actions can lead to an immediate jump in the underlying price process, whereas in our setting, it cannot. Finally, [11, 12] show how to incorporate a market impact due to cross-border trading in electricity markets, and [35] models the price impact of wind electricity production on power prices.

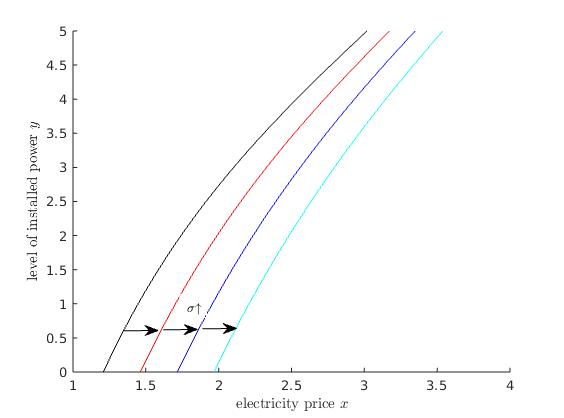

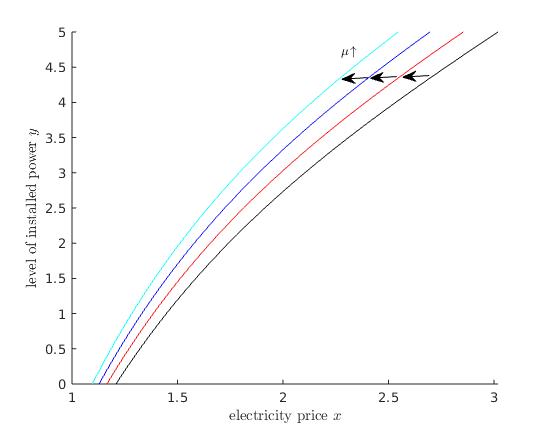

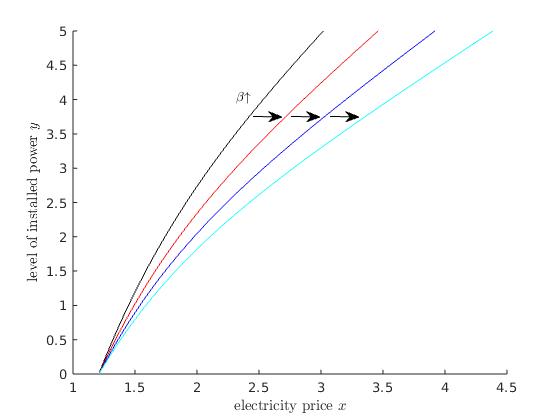

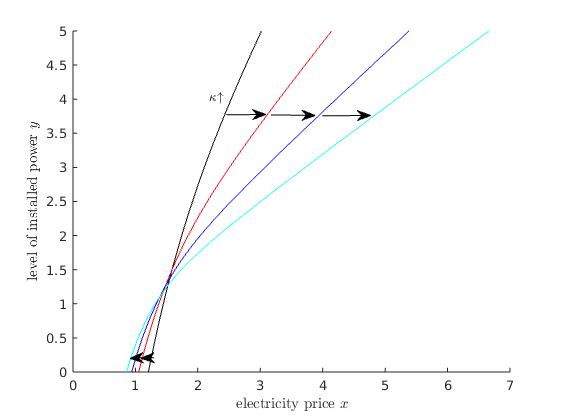

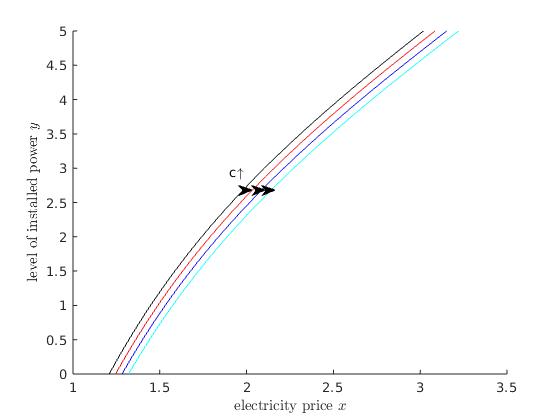

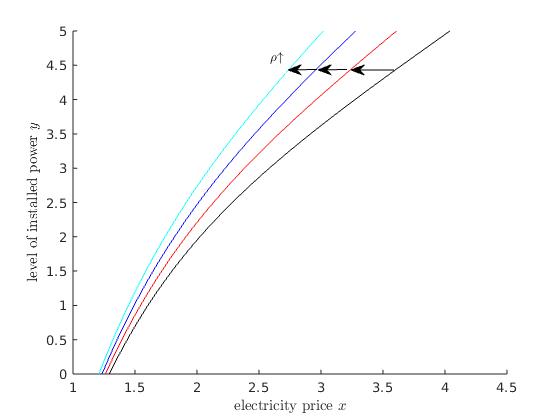

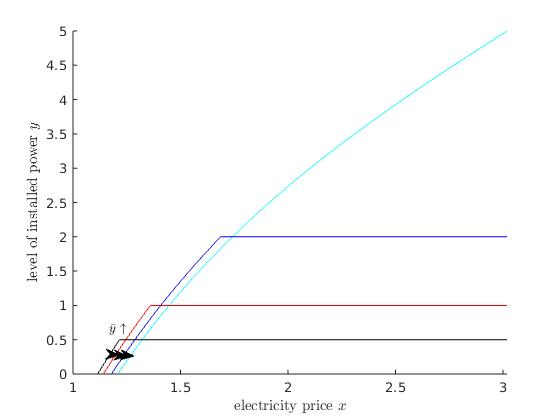

In our model the firm’s installation strategy is represented by an increasing control, possibly non-absolutely continuous, and we take into account a running payoff function which depends linearly on the level of installed power and on the electricity price. Following an educated guess for a classical solution to the associated Hamilton-Jacobi-Bellman (HJB) equation, and imposing regularity of the value function, we show that the optimal installation rule is triggered by a threshold which is a function of the current level of installed power, and we provide a closed-form expression of the value function. The threshold, also called free boundary, uniquely solves an ordinary differential equation (ODE) for which we implement a numerical solution. Then, we characterize the geometry of the waiting and installation regions. We show that the optimal installation strategy is such that the company keeps the state process inside the waiting region. In particular, the state process is pushed towards the free boundary by installing a block of solar panels immediately, if the initial electricity price is above the critical threshold (if the maximum level of installed power, that the company is able to reach, is not sufficiently high, the company will immediately install the maximum number of panels). Thereafter, the joint process will be reflected along the free boundary. The construction of the reflected diffusion relies on ideas in [14] that are based on the transformation of probability measures in the spirit of Girsanov. The uniqueness of the optimal diffusion process then follows by the global Lipschitz continuity of our free boundary. Our results are finally complemented by a numerical discussion of the dependency on the model parameters. We find, for example, that a higher mean-reversion level of the fundamental price process leads to a quicker installation of solar panels.

From the modeling point of view, it is common in the literature to represent electricity prices via a mean-reverting behavior, and to include (jump) terms to incorporate seasonal fluctuations and daily spikes, cf. [8, 10, 22, 37] among others. Here, we do not represent the spikes and seasonal fluctuations, with the following justification: the installation time of solar panels usually takes several days or weeks, which makes the company indifferent to daily or weekly spikes. Also, the high lifespan of solar panels and the underlying infinite time horizon setting allow us to neglect the seasonal patterns. We therefore assume that the fundamental electricity price has solely a mean-reverting behavior, and evolves according to an Ornstein-Uhlenbeck process. We are also neglecting the stochastic and seasonal effects of solar production. In fact, solar panels obviously do not produce power during the night, produce less in winter than in summer (these two effects could be covered via a deterministic seasonal component), and also produce less when it is cloudy (this should be modeled with a stochastic process). Since here we are interested in a long-term optimal behaviour, we interpret the average electricity produced in a generic unit of time as proportional to the installed power. All of this can be mathematically justified if we interpret our fundamental price to be, for example, a weekly average price as e.g. in [9, 23], who used this representation exactly to get rid of daily and weekly seasonalities.

The rest of the paper is organized as follows. In Section 2 we introduce the setting and formulate the problem. In Section 3 we provide preliminary results and a Verification Theorem. Then, in Section 4 we derive a characterization of the free boundary via an ODE, and the explicit solution is constructed. Finally, Section 5 provides a numerical implementation, and studies the dependency of the free boundary with respect to the model parameters.

2. Model and Problem Formulation

Let be a filtered probability space with a filtration satisfying the usual conditions, and carrying a standard one-dimensional -Brownian motion .

We consider an infinitely-lived company which installs solar panels and sells the electricity produced by those panels instantaneously in the spot market. In absence of the company’s economic activities, the fundamental electricity price evolves stochastically according to an Ornstein-Uhlenbeck dynamics

| (2.1) |

|

|

|

for some constants and .

The level of installed power can be increased at constant proportional cost due to the installation costs of panels. It is assumed that the firm cannot reduce the number of solar panels, thus the installation is irreversible. The current level of installed power is described by the process , which is given by

| (2.2) |

|

|

|

where the initial level of installed power is denoted by , and is identified as the company’s control variable: it is an -adapted nonnegative and increasing càdlàg process , where represents the total power installed within the interval . In the following, is also referred to as the installation strategy. Moreover, we assume that the level of installed power cannot exceed a given since, for example, only a finite number of solar panels can be installed. The set of admissible installation strategies is therefore defined as

|

|

|

|

|

|

|

|

We write in order to stress the dependency on both the initial level of installed power and the maximum possible level .

We assume that the current level of electricity production, which is proportional to , affects the electricity market price. In particular, when following an installation strategy , the mean level of the market price is instantaneously reduced at time by , for some , and the spot price thus evolves as

| (2.3) |

|

|

|

The company aims at maximizing the total expected profits from selling electricity in the market, net of the total expected costs of installation. That is, the company aims at determining

| (2.4) |

|

|

|

where for any

| (2.5) |

|

|

|

In (2.5), the parameter is the proportional factor between the average electricity produced in a generic unit of time and the current level of installed power. Thus, the running gain can be viewed as a weekly-averaged revenue deriving from solar production, here represented in continuous time as the life span of a typical solar panel is of several years.

For the sake of simplicity, we set in the following. In fact, the problem of finding an optimal control in (2.5) does not change for upon introducing a new cost factor

3. A Verification Theorem

The aim of this section is to provide a verification theorem which characterizes the solution to our problem.

A non-installation strategy is denoted by the function , and we indicate the electricity price process implied by by , that is . Then, the expected profits of the firm following a non-installation strategy is described by the function such that

| (3.1) |

|

|

|

The following preliminary result provides a growth condition and a monotonicity property of the value function , and its connection to the function . The proof of the proposition can be found in the appendix.

Proposition 3.1.

There exist a constant such that for all one has

| (3.2) |

|

|

|

Moreover, , and is increasing in .

In a next step we derive the Hamilton-Jacobi-Bellman (HJB), a particular partial differential equation which characterizes the solution to our problem.

For given and fixed , let be the infinitesimal generator of the diffusion given by the second order differential operator

| (3.3) |

|

|

|

where .

The HJB equation, for singular control problems as this one, follows this heuristic argument. At time zero, the firm has two possible options: either it waits for a short time period , in which the firm does not install additional panels and gains running profits from selling units of electricity in the market, or it can install solar panels immediately in order to increase its level of installed power. After each of these actions the firm behaves optimally. Suppose that the firm follows the first action. Since this action is not necessarily optimal,

it is associated to the inequality

| (3.4) |

|

|

|

Employing Itô’s formula to the last term of the right-hand side of (3.4), dividing by , and then letting , we obtain

|

|

|

Now, suppose the firm follows the second option, i.e. to increase its level of installed power by units and then to continue optimally. This action is associated to

|

|

|

which in turn, by dividing by and letting , implies

|

|

|

The previous observations suggest that should identify with an appropriate solution to the HJB equation

| (3.5) |

|

|

|

with boundary condition

|

|

|

With reference to (3.5), we introduce the waiting region

| (3.6) |

|

|

|

where we expect not to be optimal to install additional solar panels, and the installation region

| (3.7) |

|

|

|

where we expect it to be.

We move on by proving a Verification Theorem. It shows that an appropriate solution to the HJB equation (3.5) identifies with the value function, if an admissible installation strategy exists which keeps the state process inside the waiting region with minimal effort, i.e. by increasing the level of installed power whenever enters the installation region . Here, we have denoted by the closure of .

Theorem 3.2 (Verification Theorem).

Suppose there exists a function such that solves the HJB equation (3.5) with boundary condition , and satisfies the growth condition

| (3.8) |

|

|

|

for a constant . Then on .

Moreover, suppose that for all initial values , there exists a process such that

| (3.9) |

|

|

|

| (3.10) |

|

|

|

Then we have

|

|

|

and is optimal; that is, .

Proof.

Since we have by assumption, we let . In a first step, we prove that on , and then in a second step, we show that on and the optimality of satisfying (3.9) and (3.10).

Step 1. Let be given and fixed, and . For we set where . In the following, we write , , and denotes the continuous part of . By an application of Itô’s formula, we have

| (3.11) |

|

|

|

upon noticing that is continuous almost surely for any . Now, we find

|

|

|

|

|

|

|

|

which substituted back into (3.11) gives the equivalence

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

by adding on both sides of (3.11). Since satisfies (3.5) and (3.8), by taking expectations on both sides of the latter equation, and using that , we have

| (3.12) |

|

|

|

In order to apply the dominated convergence theorem in (3.12), we notice on the one hand that -a.s. for all , and therefore that

|

|

|

|

|

|

|

|

where we have used that -a.s. for all .

Also, one clearly has . Hence,

| (3.13) |

|

|

|

Now, we find that -a.s.

| (3.14) |

|

|

|

and the first expression on the right-hand side of (3.14) is integrable by (B-4). On the other hand, so to take care of the expectation on the right-hand side of (3.12), we employ again (3.13) to get for some constant

| (3.15) |

|

|

|

where we have used Hölder’s inequality in the last step.

As for the last expectation in (3.15), observe that by Itô’s formula we find

| (3.16) |

|

|

|

Then, by an application of the Burkholder-Davis-Gundy inequality (cf. Theorem 3.28 in [27]), we find that

| (3.17) |

|

|

|

for some constant . Then, since standard calculations show that for and some , we obtain from (3.16) and (3.17)

| (3.18) |

|

|

|

for some constant , and therefore, it follows with (3.15)

| (3.19) |

|

|

|

Hence, we can invoke the dominated convergence theorem in order to take limits as and then as , so to get

| (3.20) |

|

|

|

Since is arbitrary, we have

| (3.21) |

|

|

|

which yields by arbitrariness of in .

Step 2. Let satisfying (3.9) and (3.10), and . Employing the same arguments as in Step 1 all the inequalities become equalities and we obtain

| (3.22) |

|

|

|

|

Now, because is admissible and upon employing (3.8) and (3.19), we proceed as in Step 1 , and take limits as and in (3.22), so to find . Since clearly , then for all . Hence, using (3.21) on and is optimal.

∎

4. Constructing an Optimal Solution to the Installation Problem

In this section, we first construct a candidate value function and a candidate optimal strategy. Then, we move on by verifying their optimality.

We make the guess that there exists an injective function , called the free boundary which separates the waiting region and the installation region , such that

| (4.1) |

|

|

|

|

| (4.2) |

|

|

|

|

For all , the candidate value function should satisfy (cf. (3.6))

| (4.3) |

|

|

|

Recall (3.1). It is straightforward to check that a particular solution to (4.3) is given by the function . Moreover, the homogeneous differential equation

| (4.4) |

|

|

|

admits two fundamental strictly positive solutions (see pp. 18-19 of [7]). These are given by and , with strictly decreasing and strictly increasing, cf. Lemma A.1-(1),(5). Therefore our candidate value function takes the form

| (4.5) |

|

|

|

for some functions to be found. Notice that, for be given and fixed, grows to exponentially fast whenever , cf. Appendix 1 in [7]. In light of the linear growth of , see Proposition 3.1, and the structure of the waiting region , cf. (4.1), we must then have for all . Thus, we conjecture that

| (4.6) |

|

|

|

We move on to derive equations that characterize the function and the free boundary . With reference to (3.7), for all , should instead satisfy

| (4.7) |

|

|

|

implying

| (4.8) |

|

|

|

Now, we impose the so-called Smooth Fit condition, i.e. we suppose that , and therefore by (4.6),(4.7) and (4.8), should satisfy

| (4.9) |

|

|

|

and

| (4.10) |

|

|

|

Notice that the derivatives of can be easily obtained from (3.1), which gives

|

|

|

The following lemma provides essential properties of the function and a lower bound for that are needed for results of Section 4.1 and Section 4.2. Its proof can be found in the appendix.

Lemma 4.1.

The function is strictly positive and strictly decreasing. Moreover, admits the representation

| (4.11) |

|

|

|

and we have

| (4.12) |

|

|

|

4.1. The Free Boundary: Existence and Characterization

For the sake of simplicity, we introduce the function for a substitution, that is

| (4.13) |

|

|

|

We aim to prove the existence and a monotonicity property of , so to draw the implications for after.

We have

|

|

|

where is defined as

|

|

|

Notice that

|

|

|

From now on, we will often use the functions , , and their first derivatives, given by

| (4.14) |

|

|

|

Substituting for in both (4.9) and (4.10), and solving for and , gives

| (4.15) |

|

|

|

and

| (4.16) |

|

|

|

Lemma A.1-(3) ensures that is strictly positive for all , and therefore the denominator on the right-hand side of both (4.15) and (4.16) is nonzero.

In light of the boundary condition , cf. Theorem 3.2, the function should satisfy

| (4.17) |

|

|

|

Due to and (4.17), we must have that there exists a point solving , where is defined as

| (4.18) |

|

|

|

Lemma 4.2.

There exists a unique solution to the equation .

Proof.

We rewrite Now, the proof is a slight modification of the proof of Lemma 4.4 in [20] upon adjusting the cost factor in [20] by .

Differentiating (4.15), we find

| (4.19) |

|

|

|

|

where is given by

|

|

|

with defined as

| (4.20) |

|

|

|

Now, equating both expressions (4.16) and (4.19), we get

| (4.21) |

|

|

|

Letting be such that

| (4.22) |

|

|

|

we obtain from (4.21) the ODE

| (4.23) |

|

|

|

with boundary condition , cf. Lemma 4.2, and where is such that

| (4.24) |

|

|

|

The next goal is to prove that the ODE (4.23) admits a unique solution on such that . As a preliminary result we show that the previous property holds at , that is .

Lemma 4.3.

For any , we have

and it holds

| (4.25) |

|

|

|

Proof.

Recall the function from (4.18) which is such that . Therefore satisfies

| (4.26) |

|

|

|

We get from (4.20) and (4.26) that

| (4.27) |

|

|

|

upon recalling that . Now, Lemma A.2 implies . Hence, we find

| (4.28) |

|

|

|

∎

Now, we state the main result in this subsection. It guarantees the existence and uniqueness of a solution on of (4.23) which is such that for all . Its proof can be found in the appendix.

Proposition 4.4.

For any , there exists a unique solution on of the ODE (4.23) with boundary condition . Moreover,

|

|

|

Corollary 4.5.

The free boundary as in (4.1) and (4.2) is well defined. Moreover, it is strictly increasing and given by

|

|

|

Proof.

The existence and uniqueness is an implication of Proposition 4.4. It also ensures that

|

|

|

∎

4.2. The Optimal Strategy and the Value Function: Verification

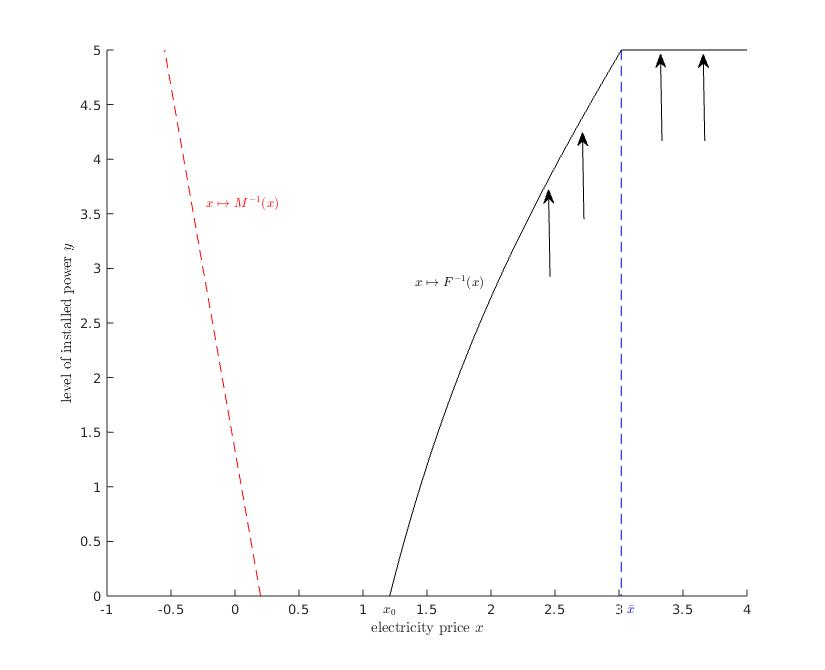

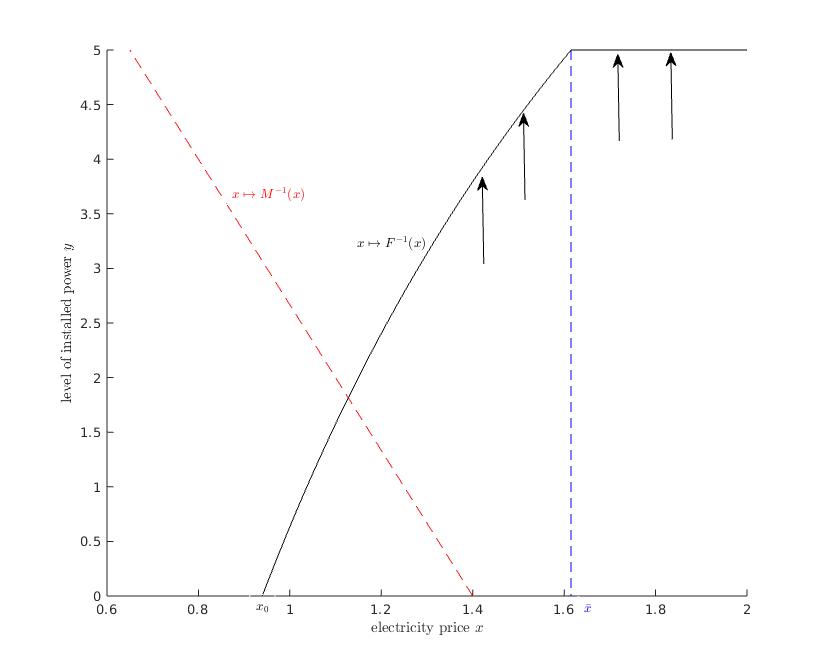

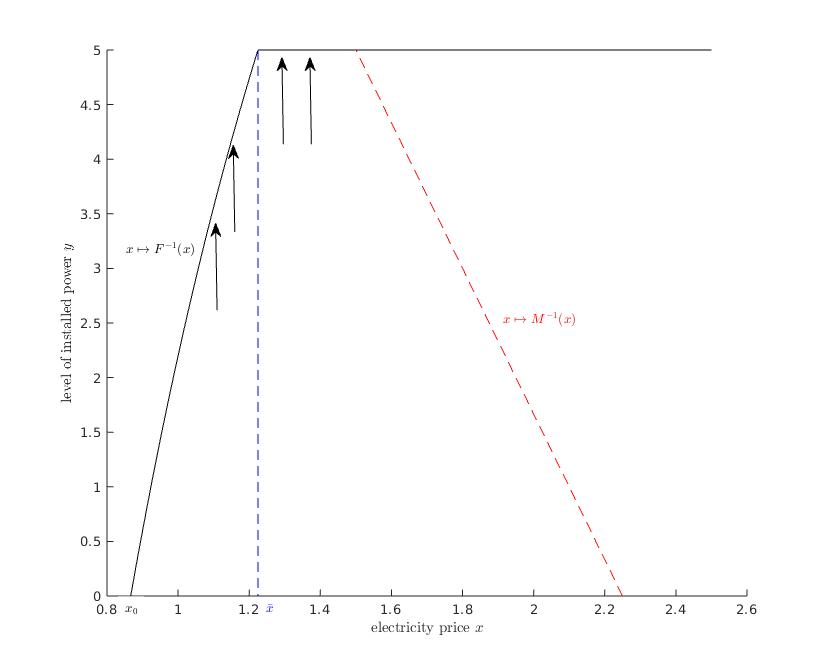

In the following, the initial price level at which the company starts to install solar panels is denoted by , and we define . Since is strictly increasing, its inverse function exists on and is denoted by .

We divide the (candidate) installation region into

|

|

|

and

|

|

|

An optimal installation strategy can be described as follows: in (cf. (4.1)), that is if the current price is sufficiently low such that , then the company does not increase the level of installed power. Whenever the price crosses , then the company makes infinitesimal installations so to keep the state process inside . Conversely, if the current price is sufficiently large such that (i.e. in , cf. (4.2)), then the company makes an instantaneous lump sum installation. In particular, on the one hand, whenever the maximum level of installed power , that the firm is able to reach, is sufficiently high (that is ), then the company pushes the state process immediately to the locus of points in direction , so to increase the level of installed power by units. The associated payoff to this action is then the difference of the continuation value starting from the new state and the costs associated to the installation of additional solar panels, that is . On the other hand, whenever the firm has to restrict its actions due to the upper bound (that is ), then the company immediately installs the maximum number of panels, so to increase the level of installed power up to units, and the associated payoff to such a strategy is .

In light of the previous discussion, we now define our candidate value function as

| (4.29) |

|

|

|

The next two results verify that is a classical solution to the HJB equation (3.5).

Lemma 4.6.

The function is .

Proof.

In the following, we denote by the interior of a set. Clearly, by (4.29) it holds for all that

| (4.30) |

|

|

|

|

| (4.31) |

|

|

|

|

| (4.32) |

|

|

|

|

and for all we have

| (4.33) |

|

|

|

To evaluate and inside , we need some more work. We find for all

| (4.34) |

|

|

|

| (4.35) |

|

|

|

| (4.36) |

|

|

|

|

where we have used (4.9) in (4.34), and (4.10) in (4.35). Notice that the functions and are continuous. The previous equations and (4.9) easily provide the continuity of the derivatives on . Letting be any sequence converging to , , we find the required continuity results along upon employing (4.9). Moreover, the boundary condition, cf. (4.17), ensures the continuity of and along , and we clearly have the continuity of along . .

∎

Proposition 4.7.

The function from (4.29) is a solution to

| (4.37) |

|

|

|

such that .

Proof.

Lemma 4.6 guarantees the claimed regularity of . Moreover, from (4.29) we see that since , and by construction, we clearly have for all , and for all . We prove the inequalities for all , and for all , in the following three steps separately. It is worth to bear in mind that by (3.1).

Step 1. Let be fixed. From the second line of (4.29), (4.34) and (4.35), we find

| (4.38) |

|

|

|

where we have employed that solves

|

|

|

For any , we have implying because , and hence , is strictly increasing, cf. Corollary 4.5. Thus, in order to show that (4.38) is negative on , it suffices to prove that the function

| (4.39) |

|

|

|

is negative for any . This can be accomplished in the same way as in Step 2 in the proof of Proposition 4.4. Due to the regularity of , we can use (4.34), and the fact that , to obtain

| (4.40) |

|

|

|

where the inequality holds by (4.12) with . Taking the total derivative of with respect to gives

| (4.41) |

|

|

|

where we have employed: , cf. (4.8), for the first equality, and (4.11) for the last equality (after rearranging terms).

Now, suppose that there exists a point such that . It follows from (4.39), together with (4.11) and (4.34), that satisfies

| (4.42) |

|

|

|

Then, exploiting the latter, one can find with (4.41) that

| (4.43) |

|

|

|

after using (A-4) with , and some simple algebra. We conclude from both (4.40) and (4.43) that there cannot exist a point such that . Therefore, we have for all .

Step 2. For all we find from the third line of (4.29) and (4.33)

|

|

|

|

|

|

|

|

|

where we have used that solves for the second equality, for any for the first inequality, and (4.12) with and for the last inequality.

Step 3. Let be fixed. We define

|

|

|

where the last equality holds true by (4.32). From (4.9) we clearly have . Hence, it suffices to show that because for all . Computing the derivative of with respect to gives

|

|

|

and from (4.10) we observe that . Moreover, we have

|

|

|

Recall (4.13) and (4.20). Lemma 4.3 and Proposition 4.4 imply that

| (4.44) |

|

|

|

Now, exploiting (4.15) and (4.16), we find

| (4.45) |

|

|

|

where the inequality is due to (4.44) and the fact that is (strictly) positive. Since is increasing by Lemma A.1-(3), and is positive for all by Lemma 4.1, we have for all

|

|

|

where we have employed (4.45) for the last inequality. Thus, we have , and therefore for all . This completes the proof.

∎

We conclude that identifies with the value function.

Theorem 4.8.

Recall from (4.29) and let , and defined on such that

| (4.46) |

|

|

|

with increasing , and starting point . Then, the function identifies with the value function from (2.4), and the optimal installation strategy, denoted by , is given by

| (4.47) |

|

|

|

Proof.

To prove the claim, we aim at applying Theorem 3.2. We already know that is a solution to the HJB equation (3.5) by Proposition 4.7. Moreover, the function satisfies the growth condition in (3.8) upon exploiting the facts that is continuous, is continuous and increasing, and for any and some constant .

In a next step, we show the existence of satisfying the stochastic differential equation (4.46). To do so, we borrow ideas from [14], cf. Section 5 therein. We let be a probability measure on a filtered probability space with a filtration satisfying the usual conditions, and be a -Brownian motion under . Define the processes such that

| (4.48) |

|

|

|

|

| (4.49) |

|

|

|

|

with starting point , and where is such that

| (4.50) |

|

|

|

Notice that the pair satisfies

|

|

|

for any . Since is increasing and for any , we apply Girsanov’s Theorem (cf. Section 3.5 in [27]), so to obtain an equivalent probability measure with respect to such that for any

|

|

|

and

|

|

|

is a standard Brownian motion on , where is the -algebra generated by , and . The pair constructed in this way is a weak solution to (4.46). We will prove in the following that is pathwise unique, hence a strong solution. Recall (4.23) and (4.24). Corollary (4.5) implies

|

|

|

because of the continuity of the functions and , and the fact that

|

|

|

which is due to Lemma 4.3, Proposition 4.4 and Lemma A.2. Therefore, is (globally) Lipschitz continuous. Now, fix , and let and be two solutions of (4.46). The (global) Lipschitz continuity of and the second line of (4.46) imply

| (4.51) |

|

|

|

for some constant . Then, again with the second line of (4.46) and (4.51), we find for some constant the estimate

| (4.52) |

|

|

|

where denotes the euclidean norm in . Now, Grönwall’s inequality yields

| (4.53) |

|

|

|

upon recalling that is continuous for any solution of (4.46). Thus, by (4.53), pathwise uniqueness holds, and (4.46) admits a unique strong solution.

Finally, since from (4.47) satisfies (3.9) and (3.10), we conclude that identifies with , and is an optimal installation strategy by Theorem 3.2.

∎

Appendix B Proofs of Results from Section 3 and Section 4

Proof of Proposition 3.1.

The proof employs arguments from the proof of Proposition 3.1 in [20] that are adjusted to our setting. In a first step we prove that (3.2) holds true, and then in a second step we show the monotonicity property of .

Step 1. In order to prove the lower bound of , we take the admissible (non-)installation strategy , so to obtain for all

| (B-1) |

|

|

|

for some .

To determine the upper bound of , recall the uncontrolled price process from (2.1), and notice that by an application of Itô’s formula we find for any

|

|

|

which in turn implies

| (B-2) |

|

|

|

for some . An application of the Burkholder-Davis-Gundy inequality (cf. Theorem 3.28 in Chapter 3 of [27]) yields

| (B-3) |

|

|

|

for a constant , and therefore

| (B-4) |

|

|

|

for some constant , since it follows from standard calculations that for a constant .

Now, for any we find by (B-4)

| (B-5) |

|

|

|

for some , and upon observing that -a.s. for any . Finally, from (B-1) and (B-5), we have that (3.2) holds with .

Step 2. If , then the only admissible strategy is , thus . In order to prove that is increasing, let , and notice that one has -a.s. for any and . Thus which implies .

Proof of Lemma 4.1.

In the following, Step 1 proves the positivity and the monotonicity property of the function , while Step 2 provides both the representation of and the lower bound of .

Step 1. Recalling that for all , we find from (4.10)

| (B-6) |

|

|

|

where is such that

|

|

|

In light of the boundary condition , cf. Theorem 3.2, we must have that

| (B-7) |

|

|

|

Due to (B-7) and the fact that is strictly negative as is strictly positive for any , cf. Lemma A.1-(2), we conclude that is both strictly positive and strictly decreasing.

Step 2.

Equations (4.9) and (4.10) lead to

| (B-8) |

|

|

|

Lemma A.1-(3) ensures that the denominator of is nonzero. Now, the numerator on the right-hand side of (B-8) writes as

|

|

|

|

|

|

|

|

upon using (A-4) with . Hence,

| (B-9) |

|

|

|

Since the denominator on the right-hand side of (B-9) is strictly negative by Lemma A.1-(3), we must have from the results of Step 1 that the numerator on the right-hand side of (B-9) is also strictly negative: this is possible only if

|

|

|

as is strictly positive for any . Hence, satisfies

| (B-10) |

|

|

|

Proof of Proposition 4.4.

The proof is organised in two steps: in a first step, we provide a representation of the function that is used after. Then, in Step 2, we show the existence of a strictly increasing maximal solution of the ODE (4.23), and prove (by a contradiction) that in fact exists on the interval .

Step 1. Recall (4.20), and let be a function which is given by

| (B-11) |

|

|

|

Then, where exists, we find upon employing (4.15) and (4.16)

| (B-12) |

|

|

|

Now, from (A-4), we derive

| (B-13) |

|

|

|

Using (B-12) and the latter equation (B-13) with , we obtain

| (B-14) |

|

|

|

where we have employed (4.9) and (4.10) for the last equality.

Step 2. Recall (4.23) and (4.24). In the following, we denote by the domain of , that is . Since is continuously differentiable for any , the functions and are continuously differentiable respectively. Therefore, is locally Lipschitz-continuous on its domain which is an open set. Hence, we find that the ODE (4.23) with boundary condition admits a unique maximal solution on an interval with . Since we want to show the existence and uniqueness of a solution on , it is enough to prove that . Following, for example, Theorem 2.10 in [3], is such that

-

(i)

either ,

-

(ii)

or ,

where is the boundary of the domain of , and is a norm in .

Now, suppose . Notice that for all by Lemma 4.3 and Lemma A.2, and therefore, we have on . Adjusting slightly the proof of Lemma 4.1, we find that is bounded from below on , and together with its monotonicity property, we must have that , for some . Thus, in order to have a contradiction, it is left to prove that condition (ii) above is not satisfied, so to show . Again, due to the boundedness of and the fact that both and are strictly positive, we find

|

|

|

for some . Therefore, upon recalling (B-11), we can complete the proof by showing that . Lemma 4.3 implies

| (B-15) |

|

|

|

Computing the total derivative of with respect to , upon using (B-14), gives

| (B-16) |

|

|

|

where the last equality holds by an application of (4.10). Next, we write the last coefficient in (B-16), that is , as a function of defined as

|

|

|

|

|

|

Employing (4.15), we get , and thus we have

| (B-17) |

|

|

|

Now, let be such that . We find from (B-11) that . Hence, upon recalling (4.20), it holds

| (B-18) |

|

|

|

Then, exploiting (B-18), we obtain

| (B-19) |

|

|

|

In (B-19) we have used: equation (A-4) with for the last equality, and the fact that and are strictly positive for the strict inequality.

Recalling that on , we conclude from (B-15), (B-17) and (B-19) that cannot tend to zero as . This completes the proof.

Acknowledgments. Financial support by the German Research Foundation (DFG) through the Collaborative Research Centre 1283 “Taming uncertainty and profiting from randomness and low regularity in analysis, stochastics and their applications” is gratefully acknowledged by the first author. We wish to thank Almendra Awerkin, Dirk Becherer, Tiziano De Angelis, Giorgio Ferrari, Markus Fischer, Wolfgang Runggaldier, Thorsten Schmidt and Mihail Zervos for useful comments.