Dual Representation of Expectile based expected shortfall and Its Properties

Abstract.

The expectile can be considered as a generalization of quantile. While expected shortfall is a quantile based risk measure, we study its counterpart – the expectile based expected shortfall – where expectile takes the place of quantile. We provide its dual representation in terms of Bochner integral. Among other properties, we show that it is bounded from below in terms of convex combinations of expected shortfalls, and also from above by the smallest law invariant, coherent and comonotonic risk measure, for which we give the explicit formulation of the corresponding distortion function. As a benchmark to the industry standard expected shortfall we further provide its comparative asymptotic behavior in terms of extreme value distributions. Based on these results, we finally compute explicitly the expectile based expected shortfall for some selected class of distributions.

Keywords: Expectile; Expected Shortfall; Tail Conditional Expectation; Dual Representation; Coherent Risk Measure.

1. Introduction

Many risk measures proposed for the quantification of financial risks are given either directly or indirectly in terms of quantile of the distribution of the loss profile. This includes the value at risk and the derivation of is such as the tail conditional expectation and the expected shortfall

respectively. While the expected shortfall is coherent in the sense of Artzner et al. [2], the value at risk and tail conditional expectation are not sub-additive and hence not coherent, see [29, 15]. For diversification purposes, the expected shortfall is therefore preferred to these two quantile based risk measures. However, the expected shortfall is not elicitable, which has recently been discussed as a useful property from a backtesting viewpoint, see Gneiting [16], Ziegel [32], Emmer et al. [14], Chen [7]. In terms of elicitablity and coherency, the expectile which was first introduced by Newey and Powell [26] and defined as the unique solution of

is the only alternative coherent law invariant risk measure which is elicitable as shown by Weber [31], Ziegel [32] and Bellini and Bignozzi [4].

As discussed by Bellini et al. [5], the expectile can be seen as a generalization of quantile. We therefore revisit the former quantile based risk measure by considering the expectile instead of quantile, namely

thereafter referred to as expectile based tail conditional expectation and expectile based expected shortfall, respectively.

The notion of expectile based tail conditional expectation and expected shortfall is relatively new. Expectile based tail conditional expectation was first introduced in Taylor [30] for the estimation of the expected shortfall from expectile for loss profile with continuous distribution. Though it is positive homogeneous and cash invariant, it is however not monotone and sub-additive in general, see Daouia et al. [9]. For this reason, Daouia et al. [9] criticized the estimation from and propose which is coherent. They further showed that for Fréchet type of extreme value distribution, and are asymptotically equivalent.

In this paper we systematically study the properties of these expectile based risk measures under the light of recent results obtained in [13]. Since the expectile based expected shortfall turns out to be a coherent risk measure, we provide its dual set in terms of Bochner integral

where is the set of probability densities in , and is the set of strongly measurable functions such that is in the dual set of for almost every . We further bound from below in terms of combinations of expected shortfall, that is

where has an explicit expression given by relation (4.2). Though is not comonotonic, in the sense of Delbaen [11] we provide the smallest comonotonic risk measure dominating , that is

where the concave distortion function is explicitly given by Relation (4.1). To compare the value of with respect to the industry standard expected shortfall and value at risk, we provide their asymptotic relative behavior for each extreme value distribution type – Fréchet, Weibull and Gumbel. Finally, based on the present result we provide explicit expression for for several classical distributions.

The rest of the paper is organized as follows. In Section 2, we introduce some basic notations, and definitions of the quantile and expectile based risk measures. In Section 3, we address the dual representation of expectile based expected shortfall. In Section 4, we provide properties, bounds and asymptotic results for the expectile based expected shortfall. Section 5 illustrates those results with examples for some loss profiles with known distribution.

2. Basic Definition and Preliminaries

Let be an atomless probability space. Throughout, and denote the set of integrable and essentially bounded random variables identified in the almost sure sense, respectively. For each in , represents its cumulative distribution. We also denotes by , the set of densities in for probability measures that are absolutely continuous with respect to , that is,

We say is a coherent risk measure, if is

-

•

Monotone: whenever ;

-

•

Cash-invariant: for each in ;

-

•

Sub-additive: ;

-

•

Positive homogeneous: for every .

A coherent risk measure is further called Fatou continuous, if whenever is a sequence dominated in and converges to almost surely.

For in , we consider the quantile based functions

-

Value at Risk: for ,

-

Tail Conditional Expectation: for ,

-

Expected Shortfall: for ,

It is well known that the value at risk is not sub-additive – not even convex – and therefore not a coherent risk measure, see [29, 15]. While the expected shortfall is coherent and coincides with the tail conditional expectation for loss profiles with continuous distributions, in general and may not be sub-additive, see [2, 15, 1].

For risk level in , the expectile of in is defined as the unique solution of

| (2.1) |

It turns out that the expectile is a law invariant, finite valued, and the only elicitable and coherent risk measure, see [31, 32, 4, 12]. From [5], its dual representation is given by

where

| (2.2) |

Since expectile can be seen as a generalization of quantiles, if is replaced by in the definition of and , then we get the expectile based functions on defined as

-

Expectile based Tail Conditional Expectation: for ,

-

Expectile based Expected Shortfall: for ,

If is not identically constant, it holds that , where . It is also known that is not monotone and sub-additive in general and hence, not a coherent risk measure, see [9]. However, is coherent and has the following properties.

Proposition 2.1.

The expectile based expected shortfall is law invariant, valued, coherent and Fatou continuous.

Proof.

It is known that the map is continuous on , see [26, 5]. It implies that is measurable. Since for each , it holds that the integration is well defined and the range of is a subset of . The law invariance and coherent properties of directly follows from expectile. Let be a sequence dominated in and converging to almost surely. Since a finite valued coherent risk measure is Fatou continuous, it holds that is also Fatou continuous, see [20]. The Fatou continuity of together with Fatou’s Lemma yields

This ends the proof of the proposition. ∎

3. Dual Representation of expectile based expected shortfall

The expectile based expected shortfall is law-invariant, coherent and Fatou continuous. Hence, it admits a representation of the form

for some which is called the dual set of , see [20, 6, 8]. This section is dedicated to describe the set . Throughout this section, we consider the measurable space , where , is the Borel sigma algebra of and is the Lebesgue measure on . We denote by , the space of all step functions on with values in identified almost every where, that is,

where is the indicator function whose value is for in and , otherwise. We say a function is measurable (strongly), if there exist a sequence in such that almost every where . We also denote by , the spaces of all measurable functions on with values in . We extend the norm to as

where is a sequence in such that almost every where . Finally, denotes the space of all real valued random variables on identified almost every where. Throughout this section, all equalities and inequalities in are identified in the almost every where sense. Clearly, and with and are in . It also holds that is a function from to .

Proposition 3.1.

The expectile based expected shortfall admits the representation

| (3.1) |

where

Furthermore, in is optimal, if and only if is the optimal density of for -almost all in .

Proof.

As a result of Relation 2.2, it follows that in for -almost all in . This implies that for all in and therefore

| (3.2) |

For each in , we consider the partition of given by . Let

For in , it holds that and . Since , there exist in such that

for all . Define

It follows that in , and . Hence, and Relation (3.2) further implies that

| (3.3) |

where which is a sequence in such that almost everywhere. The monotone convergence theorem together with Relation (3.3) yields Relation (3.1).

Let in be given. By the definition of , we always have . If is optimal, then and hence, . The converse statement is clear ending the proof. ∎

Finally, to provide the dual representations of , we need the Bochner integral. The step function in is said to be Bochner integrable with respect to the measure , provide that . In this case, the Bochner integral of is denoted by and given by

A function in is also said to be Bochner integrable, if there exist a Bochner integrable sequence in such that almost every where and . In this case, the Bochner integral of with respect to is given by

It is well known that in is Bochner integrable if and only if is finite. For Bochner integrable function in , it also holds that

| (3.4) |

see [17] for instance. With this at hands, the dual representation reads as follows.

Theorem 3.2.

The expectile based expected shortfall admits the dual representation

where is the -closure of the non-empty and convex set

Furthermore, is optimal for if and only if in for which is optimal for Relation (3.1).

Proof.

Let be in , that is, for some Bochner integrable function in . Relation (3.4) and Proposition 3.1 yields

It follows that

| (3.5) |

For each in , it holds that

implying that every element of is Bochner integrable. Hence, Relation (3.3) and (3.4) yields

| (3.6) |

where

The last inequality follows from the fact that for all in . Relation (3.5) and (3.6) yields

Clearly, is non-empty and convex subset of . Hence, taking the -closure do not affect the supremum. The last assertion directly follows from Proposition 3.1. ∎

4. Properties of Expectile based expected shortfall

4.1. Comonotonicity

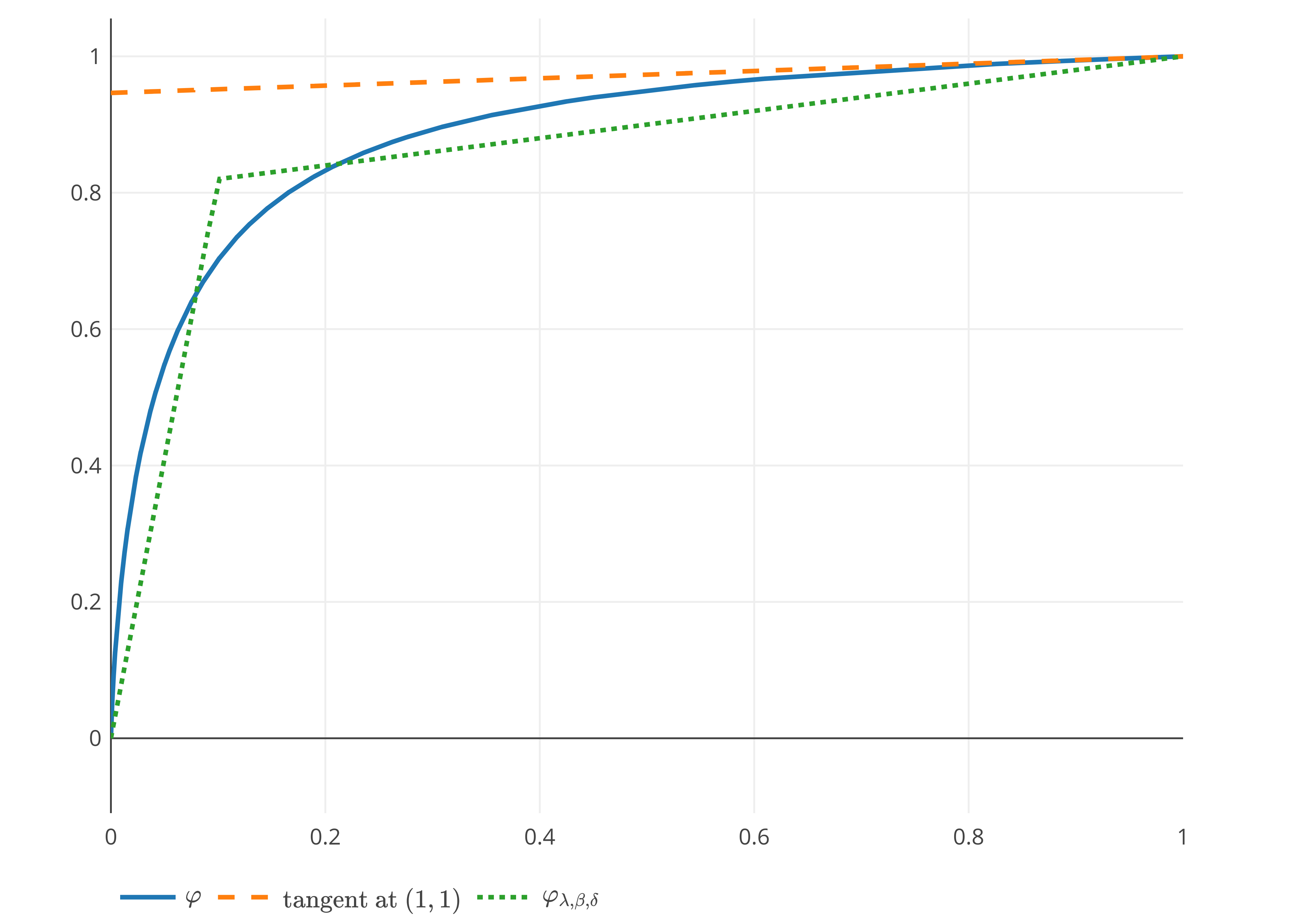

A coherent risk measure is said to be comonotonic, if for each comonotone pairs 111We say and in are comonotone, if for all . of loss profiles and . It is well known that the quantile based expected shortfall is comonotonic, while the expectile is not, see [27, 15, 14] for instance. It is therefore not astonishing that the expectile based expected shortfall is not comonotonic as shown in the following example.

Example 4.1.

In the spirit of [11, Theorem 6], the following proposition provides the smallest comonotonic risk measure that dominates uniformly on .

Proposition 4.2.

Let be the distortion function given by Relation (4.1), it holds that

Moreover, is the smallest law invariant coherent and comonotonic risk measure dominating uniformly for each in . In particular, for each .

Proof.

Following [11, Theorem 6], for each in , is dominated uniformly for each in by the smallest law-invariant, coherent and comonotonic risk measure as:

Using Fubini’s theorem yields

where

Clearly, is the smallest and law-invariant, coherent and comonotonic risk measure that dominates uniformly. From Example 5.1, we also have . ∎

4.2. Quantile Versus expectile based expected shortfall

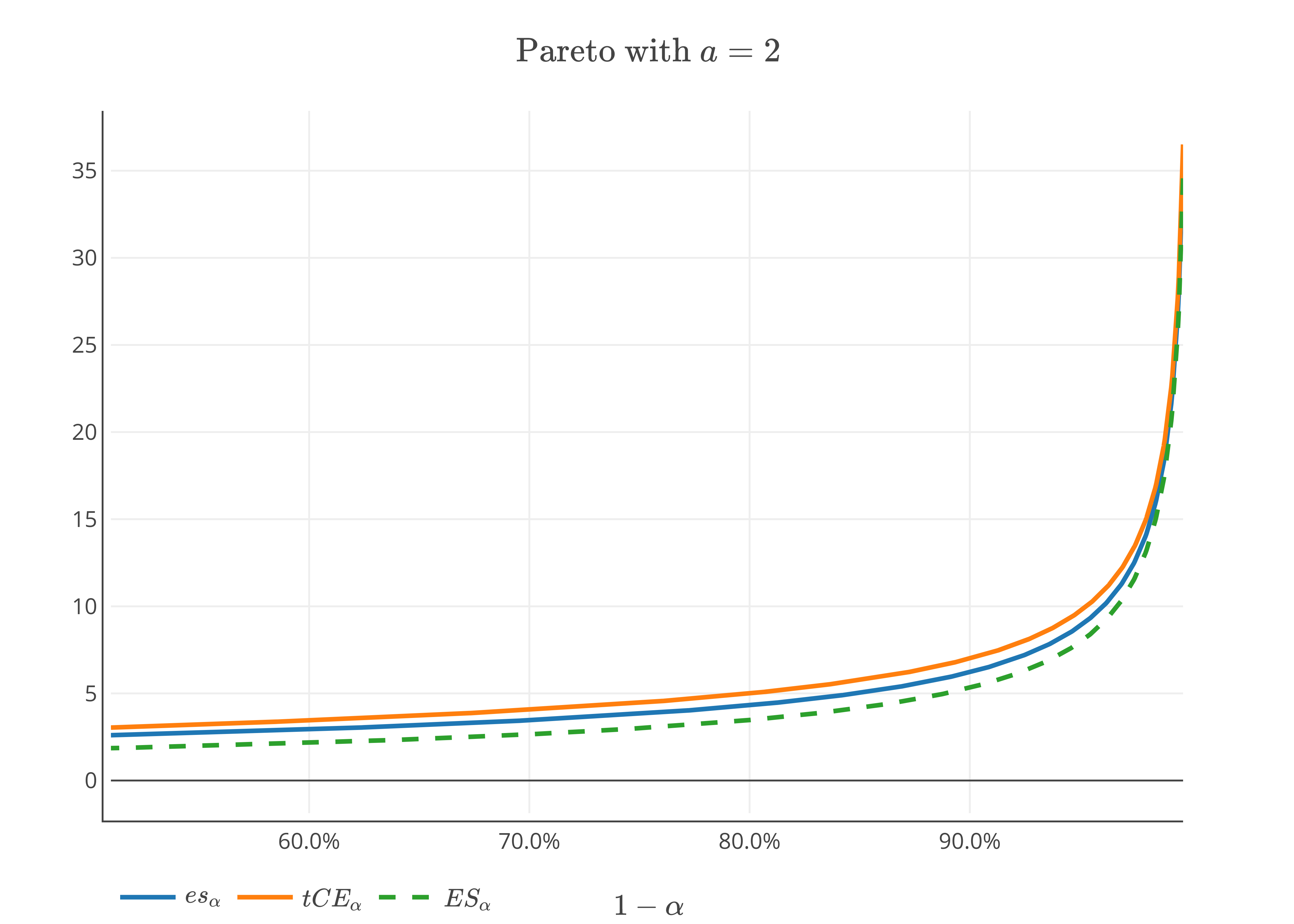

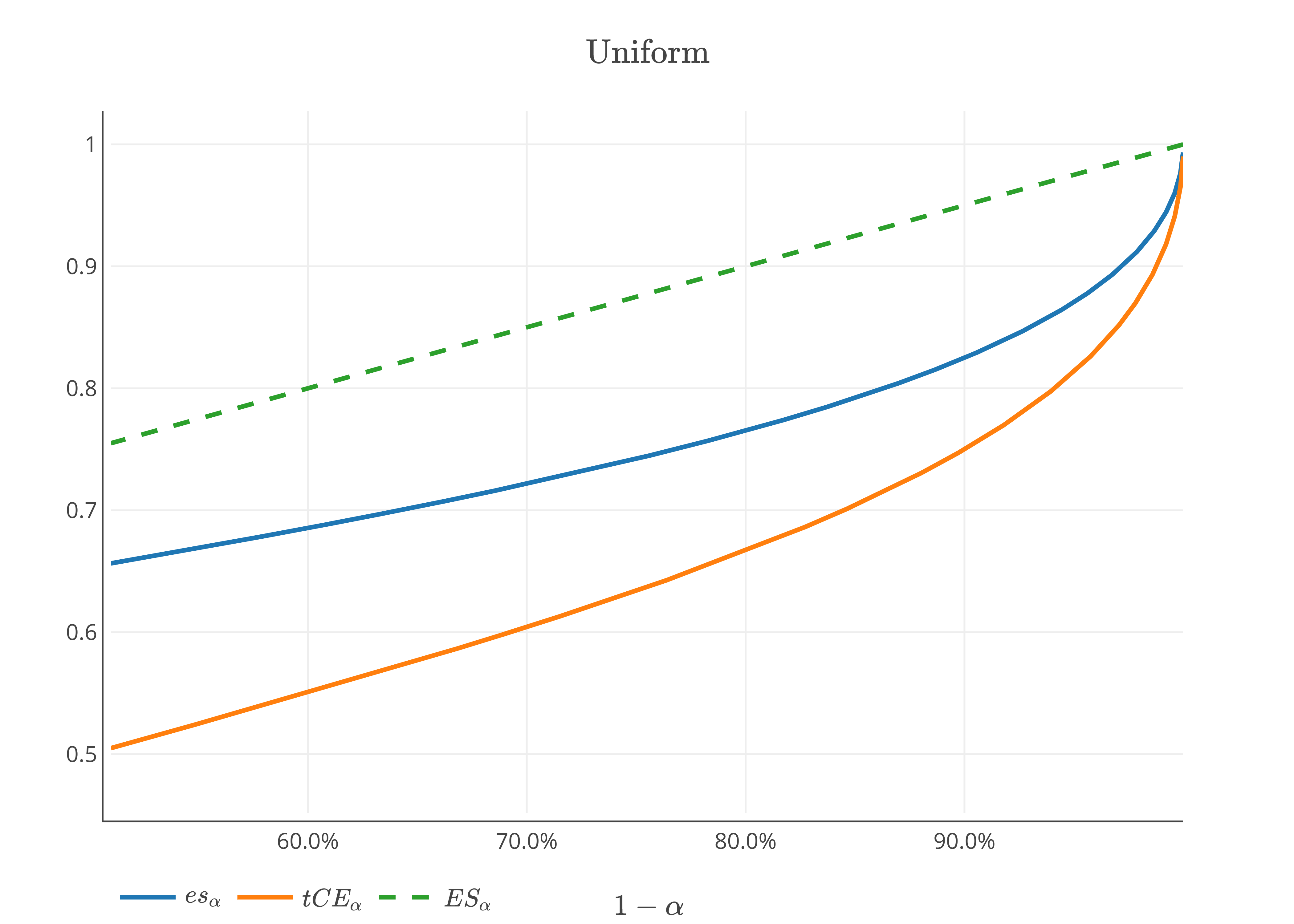

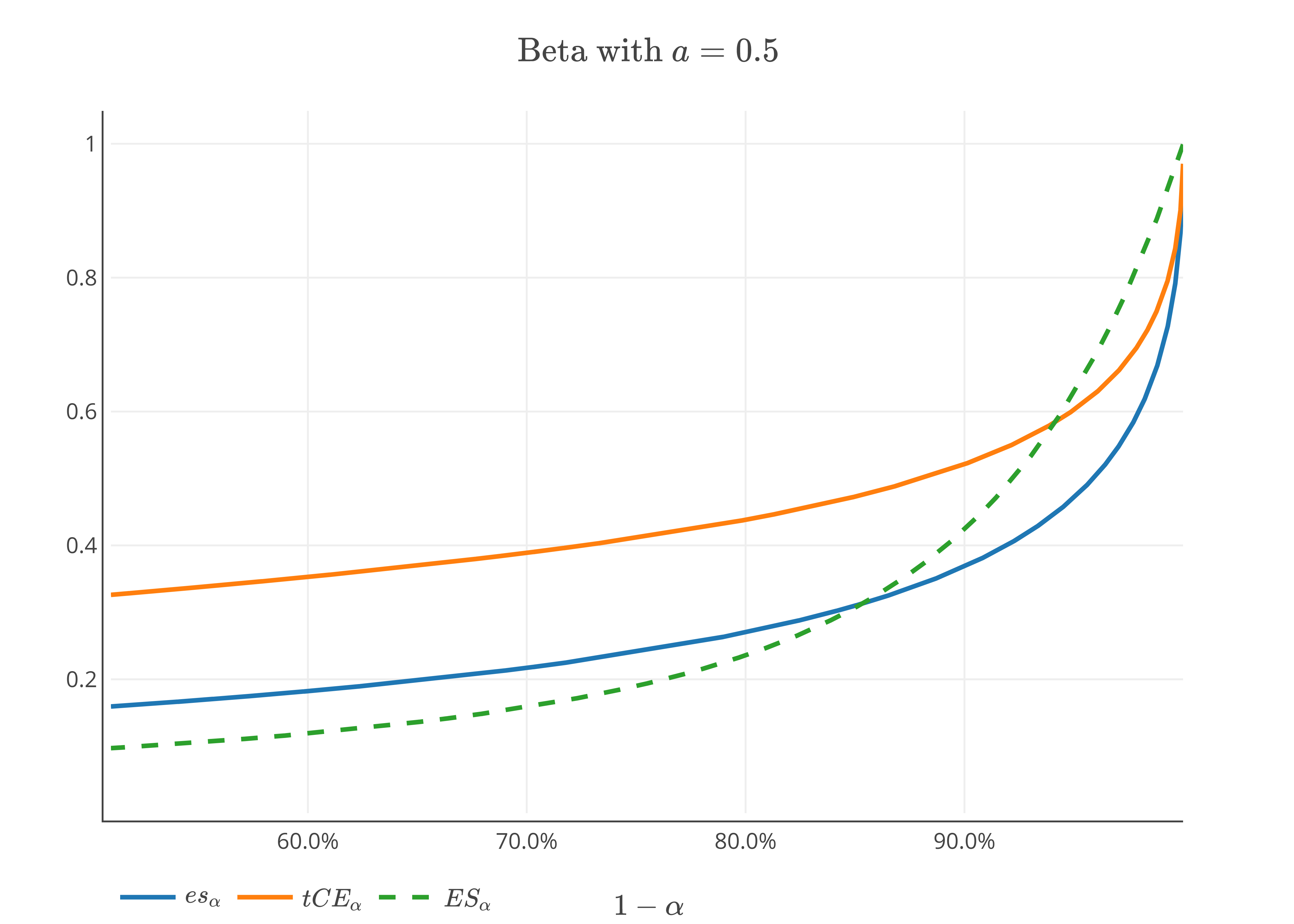

For a given risk level in , the expectile is less conservative than expectile based expected shortfall, that is, , see [9] for instance. However, as compared to the quantile based expected shortfall, it holds that or depending on the considered loss profile, see figure 1.

Using the lower bounds of expectile given in [13, Proposition 3.1], we provide a family of lower bounds for in terms of convex combination of expected shortfalls as follows.

Proposition 4.3.

For each in , it holds that

where

| (4.2) |

Furthermore, the risk measure defined as

is law invariant and coherent such that uniformly for in and for every .

Proof.

Let be in be given. From [13, Proposition 3.1], for each in we get

Integrating both sides of the above inequality with respect to gives the first result of the proposition. The law invariant and coherent property of directly follows from the properties of . Let be in such that with . A simple computation using yields . Hence, . ∎

Remark 4.4.

Note that the inequality can be strict as shown in Example 5.5.

The expectile can be uniformly dominated by the convex combination of expected shortfalls, see [13] for instance. However, this is not the case for the expectile based expected shortfall as shown by the following proposition.

Proposition 4.5.

The expectile based expected shortfall can not be dominated uniformly for in by coherent risk measures of the form

for some , and .

Proof.

We know that the concave distortion function that corresponds to

is given by . Furthermore, the tangent to at and is given by and , respectively. Suppose there exist a risk measure of the form dominating for some and . It follows that for each in . With out loss of generality we take the smallest one from these bounds, that is, is tangent to the graph of at and . This contradict the fact that the tangent to at is the -axis. Hence, our supposition is false and hence, there is no such upper bound, see Figure 2.

∎

4.3. Asymptotic Behavior of expectile based expected shortfall

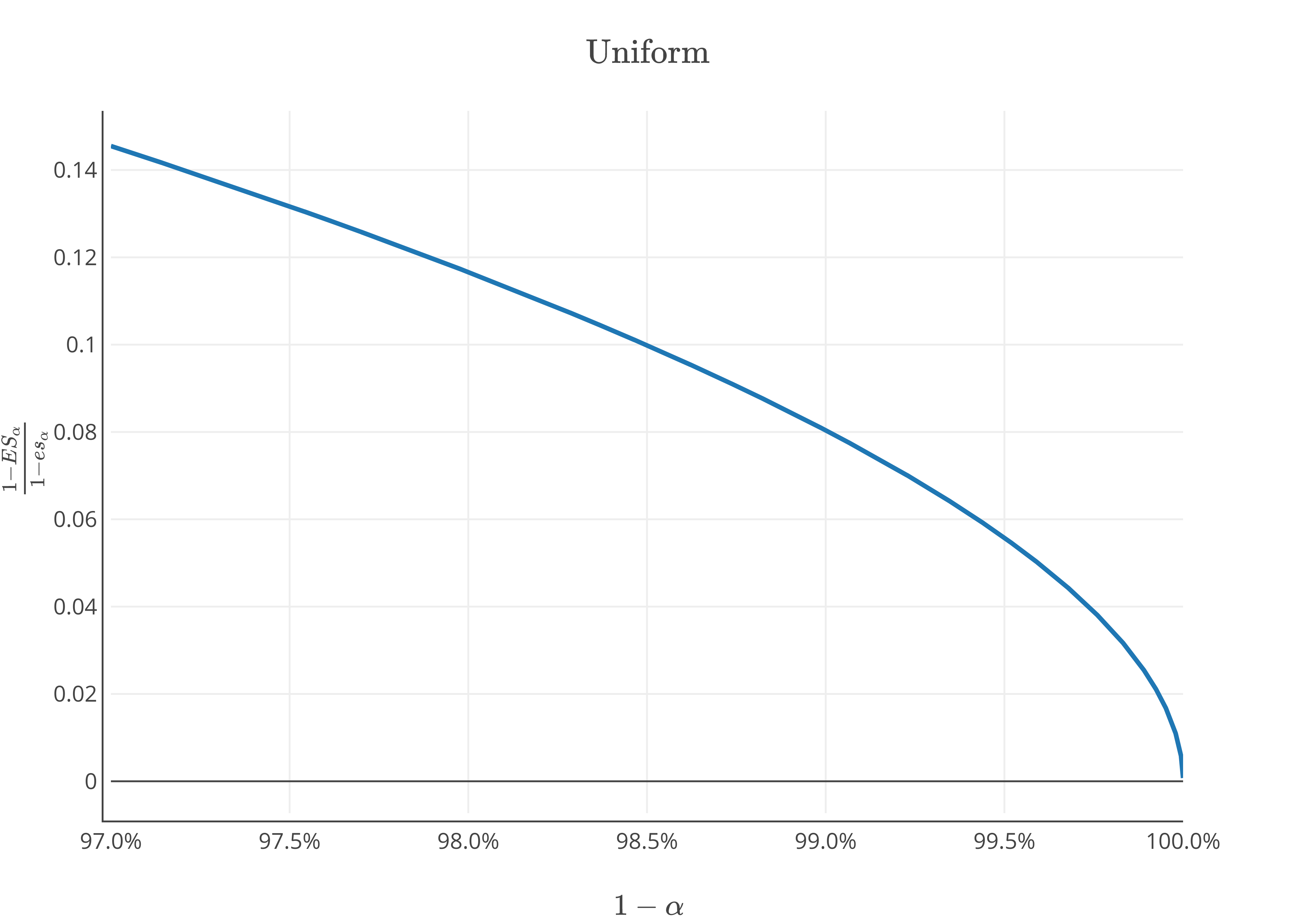

For a given risk level , the quantile based tail conditional expectation and expected shortfall coincides, that is , provided that the distribution of is continuous, see [29, 15]. However, this is not true in general for and neither of both even dominating the other depending on the considered loss profile, see Figure 1. As discussed in Section 4.2, it also holds that or , depending on the considered loss profile. When is attracted by extreme value distribution, [3] and [24] provide an asymptotic relationship between value at risk and expectile, [28] gives an asymptotic behavior of expected shortfall in terms of value at risk, [13] provides the asymptotic behavior of expectile in terms expected shortfall, and [9] also study the asymptotic behavior of in terms of and for Fréchet type distributions. Following these results, we are interested to provide the asymptotic behavior of with respect to and for loss profiles attracted 222We say is attracted by an extreme value distribution function and denoted by , if there exist constants and for each in such that by extreme value distribution . It is well known that can only be either Weibull (), Gumbel () or Fréchet () with parameter , where for , for , and for , see [25, 10] for instance.

The following proposition states the asymptotic relationship between , and based on each classes of extreme value distributions.

Proposition 4.6.

Let . If , as the risk level goes to , it holds that

-

()

(Fréchet:) If is in with ,

-

()

(Weibull:) If is in with ,

-

()

(Gumbel:) If is in ,

for the case and , respectively.

If further for some slowly varying function 333A measurable function is said to be slowly varying, if , for each in . and constant such that

(4.3) for some constant , it holds that

Proof.

The Fréchet case directly follows from [9, Proposition 3] and [13, Proposition 4.1]. For Weibull case, from [24, Proposition 3.3], we get as goes to . It follows that

for some function such that goes to as goes to . Hence,

That is, . Since , it follows that

Rearranging gives

| (4.4) |

Relation (4.4) can be re-written as

| (4.5) |

From [Lemma 3.2][23], as goes to we have that

Since as goes to , we have goes to , it follows that

Hence, Relation (4.5) yields

The relation for is due to [23, Theorem 3.4].

As for the Gumbel case, from Mao et al. [24, Relation 3.20], we have

| (4.6) |

The Relations (4.4), (4.5) and (4.6) together with [23, Theorem 3.4] yields

for the case and , respectively. The last asymptotic result holds as a result of under the given conditions, see [3, Proposition 2.4]. This ends the proof the proposition. ∎

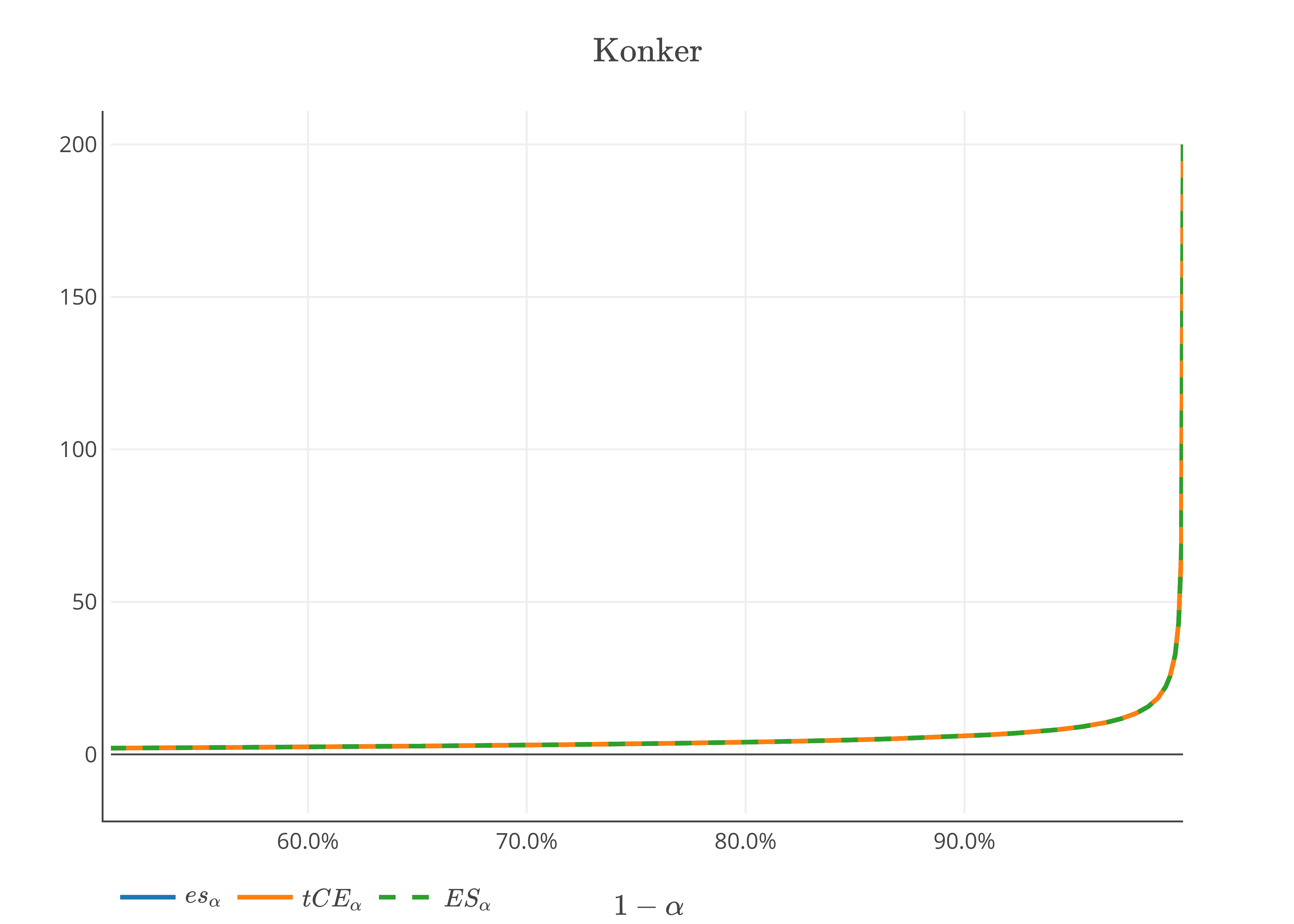

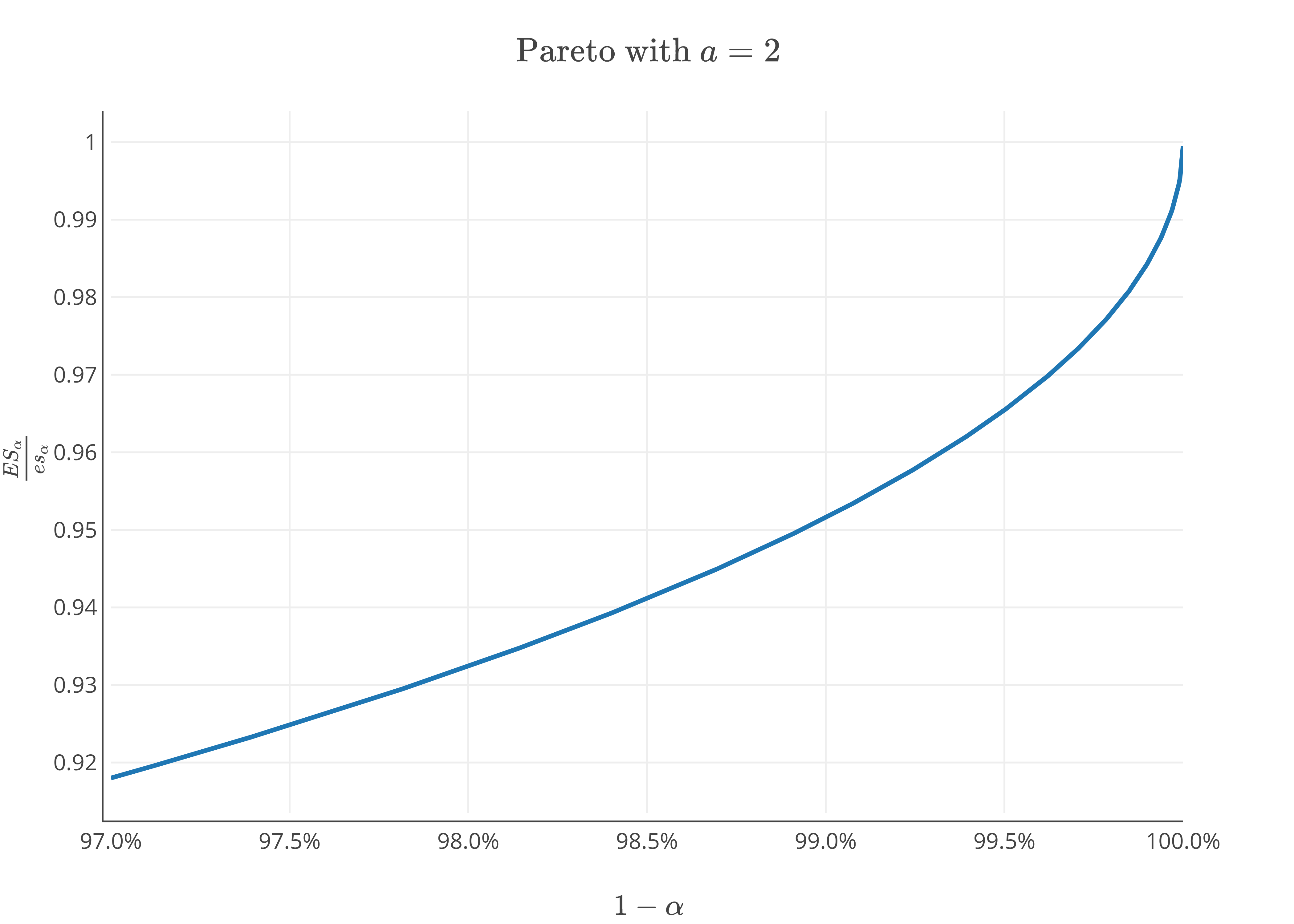

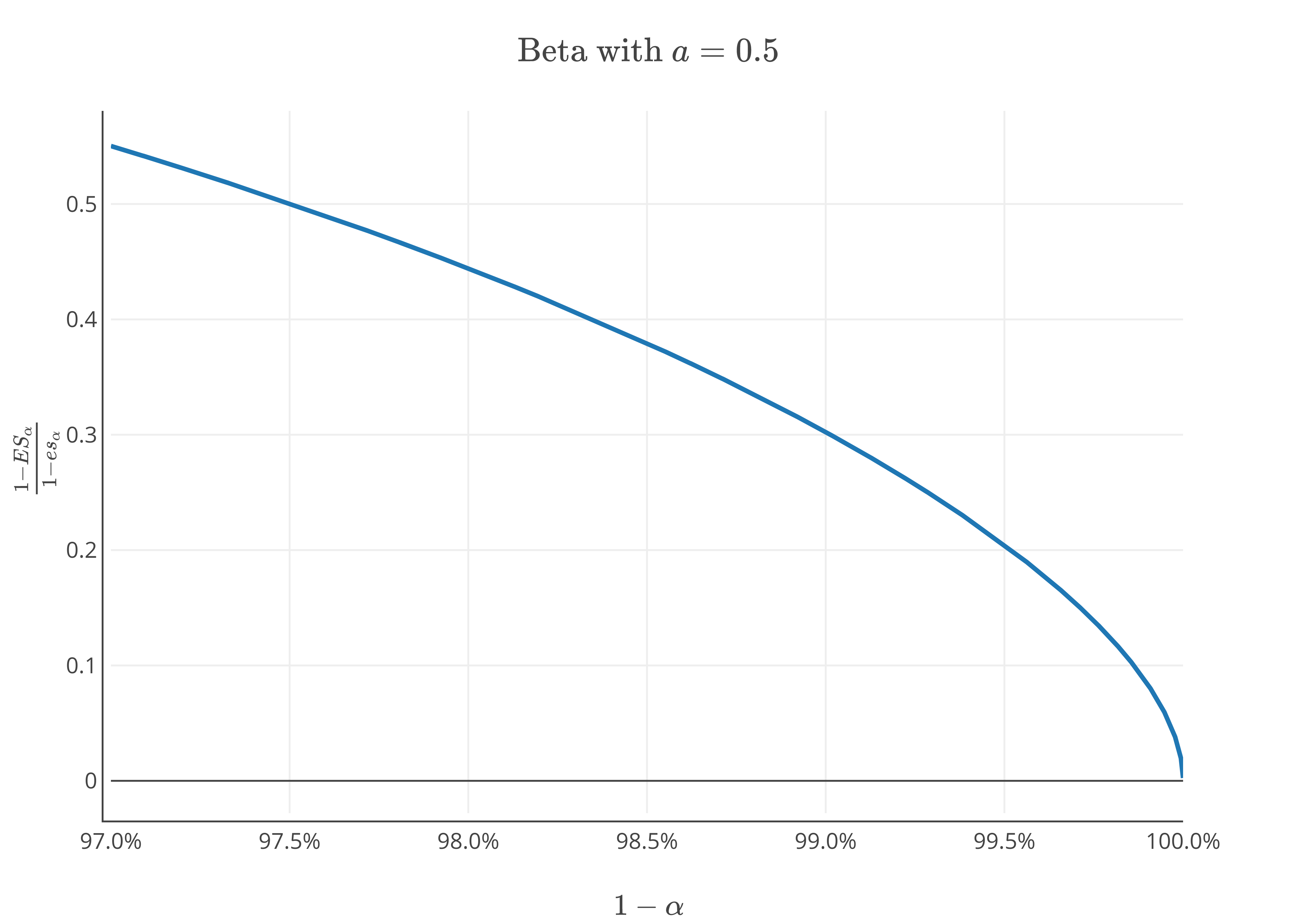

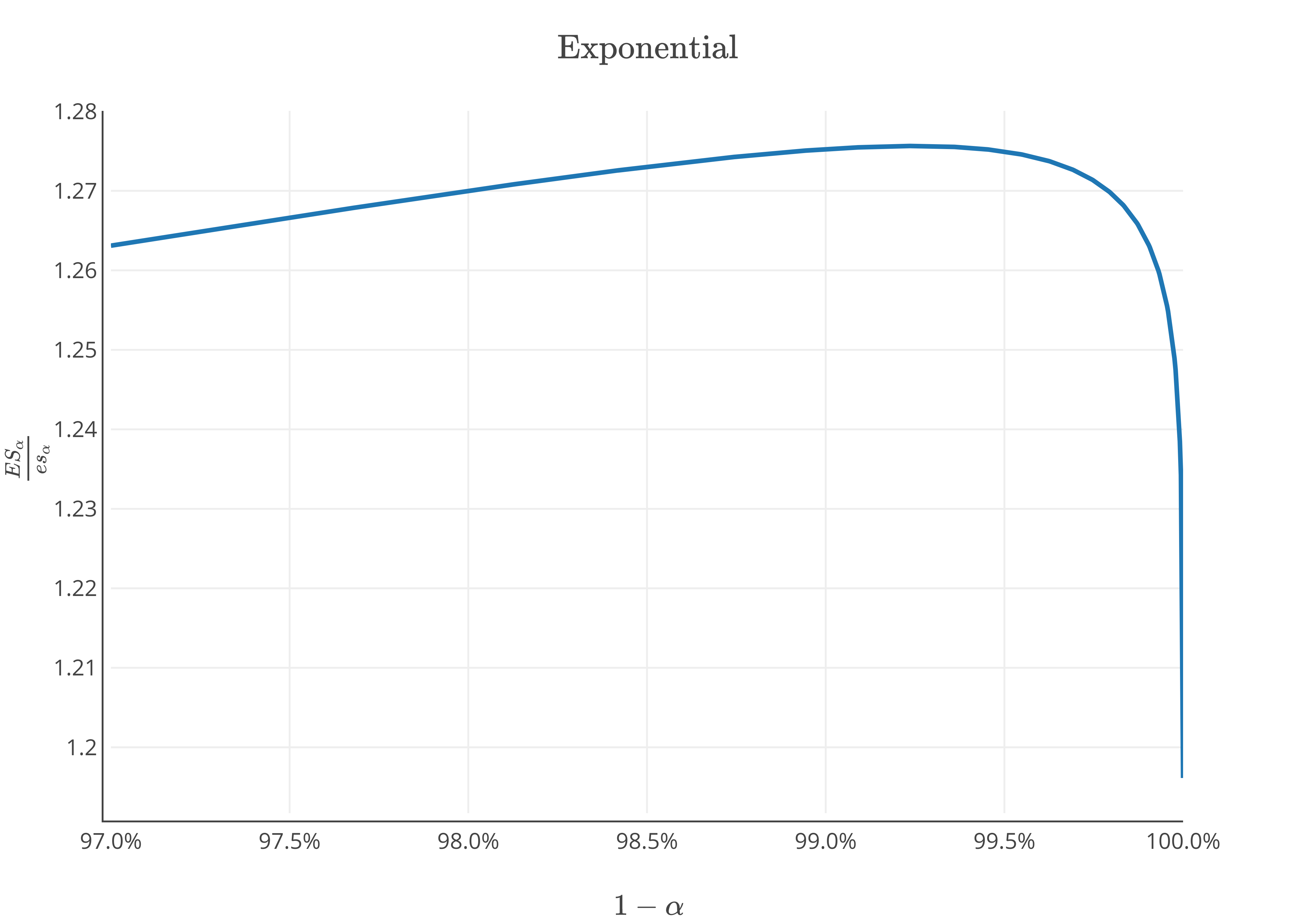

According to Proposition 4.6, for Fréchet and Gumbel (with condition (4.3) ) cases, as the risk level goes to , the expectile based tail conditional expectation and expectile based shortfall are equivalent. In this case, both and can be interpreted as the expectation of the loss under the event that the loss exceeds . Figure 3 provides a graphical illustration for the ratio of for Pareto, uniform, beta and exponential distributions. Notice that the Pareto distribution with parameter is attracted by Fréchet type , the uniform and beta distributions are attracted by Weibull type and the exponential distribution is attracted by the Gumbel type .

5. Examples

Example 5.2 (Uniform).

Example 5.3 (Beta).

For , let with in . From [13], we have

From [13] we also have that and , where solves

According to [19] and [25], , where is a random variable with probability density function given by

In the case of the Beta distribution, it follows that

which yields

It is known that belongs to the Weibull type , see [23, 24] for instance. We also have and as a result of Proposition 4.6, it holds

Example 5.4 (Exponential).

Let for . Then and , where is Lambert function444 is a function such that if and only if .. We also have

Hence,

From [3], we get . This implies that .

Example 5.5 (Konker distribution).

References

- Acerbi and Tasche [2002] C. Acerbi and D. Tasche. On the coherence of expected shortfall. Journal of Banking & Finance, 26(7):1487–1503, 2002.

- Artzner et al. [1999] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath. Coherent measures of risk. Mathematical Finance, 9(3):203–228, 1999.

- Bellini and Bernardino [2015] F. Bellini and E. D. Bernardino. Risk management with expectiles. The European Journal of Finance, 23(6):487–506, 2015.

- Bellini and Bignozzi [2015] F. Bellini and V. Bignozzi. On elicitable risk measures. Quantitative Finance, 15(5):725–733, 2015.

- Bellini et al. [2014] F. Bellini, B. Klar, A. Müller, and E. R. Gianin. Generalized quantiles as risk measures. Insurance: Mathematics and Economics, 54:41–48, 2014.

- Biagini and Frittelli [2009] S. Biagini and M. Frittelli. On the extension of the Namioka-Klee theorem and on the Fatou property for risk measures. In Optimality and Risk - Modern Trends in Mathematical Finance, pages 1–28. Springer Berlin Heidelberg, 2009.

- Chen [2018] J. Chen. On exactitude in financial regulation: Value at risk, expected shortfall, and expectiles. Risks, 6(2):61, 2018.

- Cheridito and Li [2008] P. Cheridito and T. Li. Dual characterization of properties of risk measures on orlicz hearts. Mathematics and Financial Economics, 2(1):29–55, 2008.

- Daouia et al. [2019] A. Daouia, S. Girard, and G. Stupfler. Tail expectile process and risk assessment. Preprint Hal, 2019.

- de Haan [2006] L. de Haan. Extreme Value Theory: An Introduction. Springer, 2006.

- Delbaen [2013] F. Delbaen. A remark on the structure of expectiles. Preprint ArXiV, 2013.

- Delbaen et al. [2016] F. Delbaen, F. Bellini, V. Bignozzi, and J. F. Ziegel. Risk measures with the cxls property. Finance and Stochastics, 20(2):433–453, 2016.

- Drapeau and Tadese [2019] S. Drapeau and M. Tadese. Relative bound and asymptotic comparison of expectile with respect to expected shortfall. Preprint ArXiV, 2019.

- Emmer et al. [2015] S. Emmer, M. Kratz, and D. Tasche. What is the best risk measure in practice? A comparison of standard measures. Journal of Risk, 18(2):31–60, 2015.

- Föllmer and Schied [2016] H. Föllmer and A. Schied. Stochastic Finance. An Introduction in Discrete Time. de Gruyter Studies in Mathematics. Walter de Gruyter, Berlin, New York, 4 edition, 2016.

- Gneiting [2011] T. Gneiting. Making and evaluating point forecasts. Journal of the American Statistical Association, 106(494):746–762, 2011.

- Hille and Phillips [1957] E. Hille and R. S. Phillips. Functional Analysis and Semi-groups. American Mathematical Society, 1957.

- Hua and Joe [2011] L. Hua and H. Joe. Second order regular variation and conditional tail expectation of multiple risks. Insurance: Mathematics and Economics, 49(3):537–546, 2011.

- Jones [1994] M. Jones. Expectiles and M-quantiles are quantiles. Statistics & Probability Letters, 20(2):149–153, 1994.

- Kaina and Rüschendorf [2008] M. Kaina and L. Rüschendorf. On convex risk measures on -spaces. Mathematical Methods of Operations Research, 69(3):475–495, 2008.

- Koenker [1993] R. Koenker. When are expectiles percentiles? Econometric Theory, 9(03):526, 1993.

- Lv et al. [2012] W. Lv, T. Mao, and T. Hu. Properties of second-order regular variation and expansions for risk concentration. Probability in the Engineering and Informational Sciences, 26(4):535–559, 2012.

- Mao and Hu [2012] T. Mao and T. Hu. Second-order properties of the Haezendonck–Goovaerts risk measure for extreme risks. Insurance: Mathematics and Economics, 51(2):333–343, 2012.

- Mao et al. [2015] T. Mao, K. W. Ng, and T. Hu. Asymptotic expansions of generalized quantiles and expectiles for extreme risks. Probability in the Engineering and Informational Sciences, 29(3):309–327, 2015.

- McNeil [2015] A. J. McNeil. Quantitative Risk Management: Concepts, Techniques and Tools - Revised Edition. Princeton University Press, 2015.

- Newey and Powell [1987] W. K. Newey and J. L. Powell. Asymmetric least squares estimation and testing. Econometrica, 55(4):819–847, 1987.

- Shapiro [2013] A. Shapiro. On kusuoka representation of law invariant risk measures. Mathematics of Operations Research, 38(1):142–152, 2013.

- Tang and Yang [2012] Q. Tang and F. Yang. On the Haezendonck–Goovaerts risk measure for extreme risks. Insurance: Mathematics and Economics, 50(1):217–227, 2012.

- Tasche [2002] D. Tasche. Expected shortfall and beyond. Journal of Banking & Finance, 26(7):1519–1533, 2002.

- Taylor [2008] J. W. Taylor. Estimating value at risk and expected shortfall using expectiles. Journal of Financial Econometrics, 6(2):231–252, 2008.

- Weber [2006] S. Weber. Distribution-invariant risk measures, information, and dynamic consistency. Mathematical Finance, 16(2):419–441, 2006.

- Ziegel [2014] J. F. Ziegel. Coherence and elicitablity. Mathematical Finance, 26(4):901–918, 2014.