From Robustness to Learnability: a General Approach to the Sample Complexity in Multi-item Auctions

Learnability and Robustness of Multi-Item Mechanisms without Item-Independence

Multi-Item Mechanisms without Item-Independence: Robustness implies Learnability

Multi-Item Mechanisms without Item-Independence: Learnability via Robustness

Abstract

We study the sample complexity of learning revenue-optimal multi-item auctions. We obtain the first set of positive results that go beyond the standard but unrealistic setting of item-independence. In particular, we consider settings where bidders’ valuations are drawn from correlated distributions that can be captured by Markov Random Fields or Bayesian Networks – two of the most prominent graphical models. We establish parametrized sample complexity bounds for learning an up-to- optimal mechanism in both models, which scale polynomially in the size of the model, i.e. the number of items and bidders, and only exponential in the natural complexity measure of the model, namely either the largest in-degree (for Bayesian Networks) or the size of the largest hyper-edge (for Markov Random Fields).

We obtain our learnability results through a novel and modular framework that involves first proving a robustness theorem. We show that, given only “approximate distributions” for bidder valuations, we can learn a mechanism whose revenue is nearly optimal simultaneously for all “true distributions” that are close to the ones we were given in Prokhorov distance. Thus, to learn a good mechanism, it suffices to learn approximate distributions. When item values are independent, learning in Prokhorov distance is immediate, hence our framework directly implies the main result of Gonczarowski and Weinberg [36]. When item values are sampled from more general graphical models, we combine our robustness theorem with novel sample complexity results for learning Markov Random Fields or Bayesian Networks in Prokhorov distance, which may be of independent interest. Finally, in the single-item case, our robustness result can be strengthened to hold under an even weaker distribution distance, the Lévy distance.

1 Introduction

A central problem in Economics and Computer Science is the design of revenue-optimal auctions. The problem involves a seller who wants to sell one or more items to one or more strategic bidders. As bidders’ valuation functions are private, no meaningful revenue guarantee can be achieved without any information about these functions. To remove this impossibility, it is standard to make a Bayesian assumption, whereby a joint distribution from which bidders’ valuations are drawn is assumed common knowledge, and the goal is to design an auction that maximizes expected revenue with respect to this distribution.

In the single-item setting, a celebrated result by Myerson characterizes the optimal auction when bidder values are independent [49]. The quest for optimal multi-item auctions has been quite more challenging. It has been recognized that revenue-optimal multi-item auctions can be really complex and may exhibit counter-intuitive properties [39, 40, 9, 22, 23]. As such, it is doubtful that there is a clean characterization similar to Myerson’s for the optimal multi-item auction. On the other hand, there has been significant recent progress in efficient computation of revenue-optimal auctions [18, 19, 2, 10, 3, 12, 13, 16, 14, 4, 8, 24]. This progress has enabled the identification of simple auctions (mostly variants of sequential posted pricing mechanisms) that achieve constant factor approximations to the optimum revenue [6, 56, 15, 20, 17], under item-independence assumptions.444Intuitively, item independence means that each bidder’s value for each item is independently distributed, and this definition has been suitably generalized to set value functions such as submodular or subadditive functions [53].

Making Bayesian assumptions in the study of revenue-optimal auctions is both crucial and fruitful. However, to apply the theory to practice, we would need to know the underlying distributions. Where does such knowledge come from? A common answer is that we estimate the distributions through market research or observation of bidder behavior in previously run auctions. Unavoidably, errors will creep in to the estimation, and a priori it seems possible that the performance of our mechanisms may be fragile to such errors. This has motivated a quest for optimal or approximately optimal mechanisms under imperfect knowledge of the underlying distributions.

This problem has received lots of attention from Theory of Computation recently. The focus has been on whether optimal or approximately optimal mechanisms are learnable given sample access to the true distributions. In single-item settings, where Myerson’s characterization result applies, it is possible to learn up-to- optimal auctions [32, 21, 46, 41, 48, 28, 52, 35].555The term “up-to- optimal” introduced in [36] means an additive approximation for distributions supported on . Under tail assumption on the distribution, it is also possible to obtain -multiplicative approximations. A recent paper by Guo et al. [37] provides upper and lower bounds on the sample complexity, which are tight up to logarithmic factors, thereby rendering a nearly complete picture for the single-item case.

In multi-item settings, largely due to the lack of simple characterizations of optimal mechanisms, results have been sparser. Recent work [48, 34, 11, 55] has shown how to learn simple mechanisms which attain a constant factor of the optimum revenue using polynomially many samples in the number of bidders and items. Last year, a surprising result by Gonczarowski and Weinberg [36] shows that the sample complexity of learning an up-to- optimal mechanism is also polynomial.666In particular, they learn a mechanism that is -truthful and has up-to- optimal revenue. However, all these results rely on the item-independence assumption mentioned earlier, which limits their applicability. A main goal of our work is the following:

-

Goal I:

Push the boundary of learning (approximately) optimal multi-item auctions to the important setting of item dependence.

Unfortunately, it is impossible to learn approximately optimal auctions from polynomially many samples under general item dependence. Indeed, an exponential sample complexity lower bound has been established by Dughmi et al. [31] for even a single unit-demand buyer. Arguably, however, in auction settings, as well as virtually any high-dimensional setting, the distributions that arise are not arbitrary. Arbitrary high-dimensional distributions cannot be represented efficiently, and are known to require exponentially many samples to learn or even perform the most basic statistical tests on them; see e.g. [25] for a discussion. Accordingly a large focus of Statistics and Machine Learning has been on identifying structural properties of high-dimensional distributions, which enable succinct representation, efficient learning, and efficient statistical inference. In line with this literature, we propose learning multi-item auctions under the assumption that item values are jointly sampled from a high-dimensional distribution with structure.

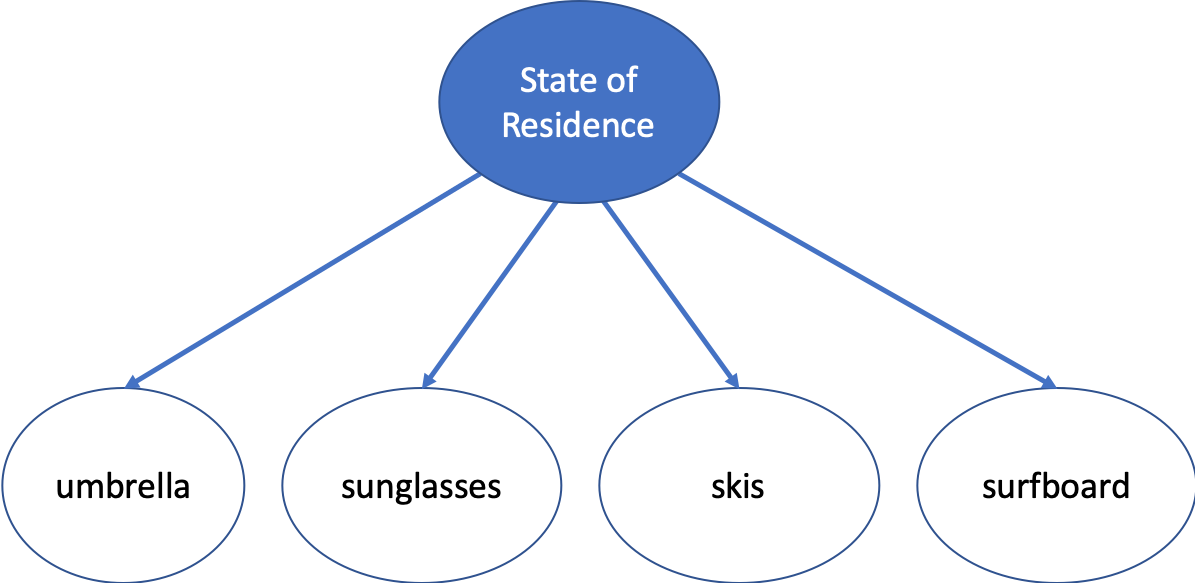

There are several widely-studied probabilistic frameworks which allow modeling structure in a high-dimensional distribution. In this work we consider two of the most prominent ones: Markov Random Fields (MRFs) and Bayesian Networks, a.k.a. Bayesnets, which are the two most common types of graphical models. Both MRFs and Bayesnets have been studied in Machine Learning and Statistics for decades. Both frameworks can be used to express arbitrary high-dimensional distributions. Their advantage, however, is that they are associated with natural complexity parameters which allow tuning the dependence structure in the distributions they model, from product measures all the way up to arbitrary distributions. In Figure 1, we show a very simple example illustrating how naturally these models express dependence structure in a distribution. The figure shows a Bayesnet, which samples the values of a buyer for four items. The structure of the Bayesnet implies (see Definition 8) that these values are sampled conditionally independently, conditioning on the value of the variable at the root of the Bayesnet which is the state of the buyer’s residence. The node is shaded because we assume that the corresponding variable is not observable. The pertinent question is how we might exploit the structure of the distribution, as captured by the natural complexity parameter of an MRF or a Bayesnet, to efficiently learn a good mechanism. At a high level, there are two components to the problem of learning approximately optimal auctions. One is inference from samples, i.e. extracting information about the distribution using samples. The other is mechanism design, i.e. constructing a good mechanism using the information extracted. A main goal of our work is:

-

Goal II:

Provide a modular approach for learning multi-item auctions which decouples the Inference and Mechanism Design components, so that one may leverage all techniques from Machine Learning and Statistics to tackle the first and, independently, leverage all techniques from Mechanism Design to address the second.

Unfortunately, the Statistical and Mechanism design components are complexly intertwined in prior work on learning multi-item auctions. Specifically, [47, 11, 55, 36] are PAC-learning approaches, which require a fine balance between (i) selecting a class of mechanisms that is rich enough to contain an approximately optimal one for a class of distributions; and (ii) having small enough statistical complexity so that the performance of all mechanisms in the class on a small sample is representative of their performance with respect to the whole distribution, and so that a small sample suffices to select a good mechanism in the class. See the related work section for a detailed discussion of these works and their natural limitations. Our goal in this work is to avoid a joint consideration of (i) and (ii). Rather we want to obtain a learning framework that separates Mechanism Design from Statistical Inference, based on the following:

-

(i)’

find an algorithm , which given a distribution in some family of distributions , computes an (approximately) optimal mechanism when bidders’ valuations are drawn from ;

-

(ii)’

find an algorithm , which given sample access to a distribution from the family of distributions learns a distribution that is close to in some distribution distance .

Achieving (i)’ and (ii)’ is of course not enough, unless we also guarantee the following:

-

(iii)’

given an (approximately) optimal mechanism for some there is a way to transform to some that is approximately optimal for any distribution that is close to under distribution distance .

Given (i)’–(iii)’, the learnability of (approximately) optimal mechanisms for a family of distributions can be established as follows: (a) Given sample access to some distribution we use to learn some distribution that is close to under ; (b) we then use to compute an (approximately) optimal mechanism for ; and (c) finally, we use (iii)’ to argue that can be converted to a mechanism that is (approximately) optimal for because is (approximately) optimal for any distribution that is close to .

Clearly, (iii)’ is important for decoupling (i)’—i.e. computing (approximately) optimal mechanisms for a family of distributions , and (ii)’—i.e. learning distributions in . At the same time, it is important in its own right:

-

Goal III:

Develop robust mechanism design tools, allowing to transform a mechanism designed for some distribution into a mechanism which attains similar performance simultaneously for all distributions that are close to in some distribution distance of interest.

The reason Goal III is interesting in its own right is that oftentimes we actually have no sample access to the underlying distribution over valuations. It is possible that we estimate that distribution through market research or econometric analysis in related settings, so we only know some approximate distribution. In other settings, we may have sample access to the true distribution but there might be errors in measuring or recording those samples. In both cases, we would know some approximate distribution that is close to the true distribution under some distribution distance, and we would want to use to identify a good mechanism for the unknown distribution that is close to . Clearly, outputting a mechanism that attains good performance under might be a terrible idea as this mechanism might very well overfit the details of . So we need to “robustify” . A similar goal was pursued in the work of Bergemann and Schlag [7], for single-item and single-bidder settings, and in the work of Cai and Daskalakis [11], for robustifying a specific class of mechanisms under item-independence. Our goal here is to provide a very general robustification result.

1.1 Our Results

We discuss our contributions in the setting of additive bidders, whose values for the items are not necessarily independent. Our results hold for quite more general valuations, including constrained additive and any family of Lipschitz valuations (Definition 2), but we do not discuss these here to avoid overloading our notation. We will denote by the number of bidders, and by the number of items. We will also assume that the bidders’ values for the items lie in some bounded interval .

Our Robustness Results (cf. Goal III above).

The setting we consider is the following. We are given a collection of model distributions , one for each bidder . We do not know the true distributions sampling the valuations of the bidders, and the only information we have about each is that , under some distribution distance —we will discuss distances shortly.

Our goal is to design a mechanism that performs well under any possible collection of true distributions that are close to their corresponding distributions under . We show that there are robustification algorithms, which transform a mechanism into a robust mechanism that attains similar revenue to that of under , except that ’s revenue guarantee holds simultaneously for any collection that is close to . Applying our robustification algorithm to the optimum mechanism for allows us to obtain the results reported in the first three columns of Table 1. DSIC and BIC refer to the standard properties of Dominant Strategy and Bayesian Incentive Compatibility of mechanisms, IR refers to the standard notion of Individual Rationality, and -BIC is the standard notion of approximate Bayesien Incentive Compatibility. For completeness these notions are reviewed in Appendix B.

Some remarks are in order. First, in multi-item settings, it is unavoidable that our robustified mechanism is only approximately BIC, as we do not know the true distributions. In single-item settings, the optimal mechanism is DSIC, and we can indeed robustify it into a mechanism that is DSIC. In the multi-item case, however, it is known that DSIC mechanisms sometimes can extract at most a constant fraction of the optimal revenue [57], so it is necessary to consider BIC mechanisms and the BIC property is fragile to errors in the distributions.

Second, we consider several natural distribution distances. In multi-item settings, we consider both the Prokhorov and the Total Variation distance. In single-item settings, we consider both the Lévy and the Kolmogorov distance. Please see Section 2 for formal definitions of these distances and a discussion of their relationships, and their relationship to other standard distribution distances. We note that the Lévy distance for single-dimensional distributions, and the Prokhorov distance for multi-dimensional distributions are quite permissive notions of distribution distance. This makes our robustness results for these distances stronger, automatically implying robustness results under several other common distribution distances.

Finally, en route to proving our robustness results, we show a result of independent interest, namely that the optimal revenue is continuous with respect to the distribution distances that we consider. Our continuity results are summarized in the last column of Table 1. Note that the continuity results are substantially easier to establish than the robustness results, please see Section 1.2 for details.

Setting Distance Robustness Continuity Single Item Kolmogrov is IR and DSIC (Theorem 2) (Theorem 2) Lévy is IR and DSIC (Theorem 1) (Corollary 1) Multiple Items TV is IR and - BIC w.r.t. , where (Theorem 12) (Theorem 11) Prokhorov is IR and - BIC w.r.t. , where (Theorem 12) where (Theorem 11)

Learning Multi-Item Auctions Under Item Dependence (cf. Goal I above).

In view of our robustness results, presented above, the challenge of learning near-optimal auctions given sample access to the bidders’ valuation distributions, becomes a matter of estimating these distributions in the required distribution distance, depending on which robustification result we want to apply.

When the item values are independent, learning bidders’ type distributions in our desired distribution distances is immediate. So we easily recover the guarantees of the main theorem of [36]. These guarantees are summarized in the second row of Table 2, and are expanded upon in Theorem 6.

But a main goal of our work (namely Goal I from earlier) is to push the learnability of auctions well beyond item-independence. As stated earlier, it is impossible to attain learnability from polynomially many samples for arbitrary joint distributions over item values so we consider the well-studied frameworks of MRFs and Bayesnets. These frameworks are flexible and can model any distribution, but they have a tunable complexity parameter whose value controls the dependence structure. This parameter is the maximum clique size of an MRF and maximum in-degree of a Bayesnet. We will denote this complexity parameter in both cases. Recall that we also used to denote distribution distances. To disambiguate, whenever we study MRFs or Bayesnets, we make sure to use , with parentheses, to denote distribution distances. Note that a small value of the complexity parameter does not mean that the corresponding MRF or Bayesnet does not have correlations among every pair of item values. Many natural MRF structures, with , and Bayesnet structures, with , permit distributions where all the variables are correlated, and indeed any pair of variables remain correlated even after conditioning on the values of all the other variables. In Figure 1, we show a simple such example where the values of a bidder on four items are sampled from a Naive Bayes Model, which is a very simple type of Bayesnet with . While even small values of allow all pairs of variables to be correlated even conditioning on everything else, the complexity parameter forbids arbitrary dependence structures. Indeed, this is the reason why MRFs and Bayesnets are so prevalent. They allow rich dependent structures but not arbitrary ones, unless their complexity parameter is tuned up to its maximum possible value, i.e. equal to the total number of variables, in which case they can express any dependence structure. In particular, a model of complexity can express arbitrary dependence on subsets of (for MRFs) or (for Bayesnets) variables, and it allows some dependence structures on larger subsets of variables depending on the graphical structure of the model.

Now, in order to learn near-optimal mechanisms when item values for each bidder are sampled from an MRF or a Bayesnet of certain complexity , our robustness results reassure us that it suffices to learn MRFs and Bayesnets under Total Variation or Prokhorov distance, depending on which multi-item robustenss theorem we seek to apply. So we need an upper bound on the sample complexity necessary to learn MRFs and Bayesnets. One of the contributions of our paper is to provide very general sample complexity bounds for learning these distributions, as summarized in Theorems 9 and 10 for MRFs and Bayesnets respectively. In both theorems, is the set of variables, is the complexity measure of the underlying distribution, and is the distance within which we are seeking to learn the distribution. Each theorem has a version when the variables take values in a finite alphabet , and a version when the variables take values in some interval . In the first case, we provide bounds for learning in the stronger notion of Total Variation distance. In the second case, since we are learning from finitely many samples, we need to settle for the weaker notion of Prokhorov distance. For the same reason, we need to make some Lipschitzness assumption on the density, so our sample bounds depend on the Lipschitzness of the MRF’s potential functions and the Bayesnet’s conditional distributions.

The sample bounds we obtain for learning MRFs and Bayesnets are directly reflected in the sample bounds we obtain for learning multi-item auctions when the item-values are sampled from an MRF or a Bayesnet respectively, as summarized in the last two rows of Table 2. Indeed, the sample complexity for learning auctions is entirely due to the sample complexity needed to learn the underlying item-distribution. In all cases we consider, the complexity is polynomial in number of variables and only depends exponentially in , the complexity of the distribution, and this is unavoidable. 777Note that the example by Dughmi et al. [31] can be captured by an MRF or Bayesnet with , and it is shown in [31] that the sample complexity for learning a mechanism that is a constant factor approximation to the optimal revenue in this example is at least .

Setting Revenue Guarantee and Sample Complexity Prior Result Technique Item Independence up-to- optimal, -BIC (Theorem 6) recovers main result of [36] Prokhorov Robustness + Learnability of Product Dist. (Folklore) MRF up-to- optimal, -BIC (Theorem 7) (Finite ) () unknown Prokhorov Robustness + Learnability of MRFs (Theorem 9) Bayesnet up-to- optimal, -BIC (Theorem 8) (Finite ) () unknown Prokhorov Robustness + Learnability of Bayesnets (Theorem 10)

Our sample bounds improve if the underlying graph of the MRF or Bayesnet are known and, importantly, without any essential modifications our sample bounds hold even when there are latent, i.e. unobserved, variables in the distribution. This makes both our auction and our distribution learning results much more richly applicable. As a simple example of the modeling power of latent variables, situations can be captured where an unobserved random variable determines the type of a bidder, and conditioning on this type the observable values of the bidder for different items are sampled.

Finally, it is worth noting that our sample bounds for learning MRFs (i.e. Theorem 9) provide broad generalizations of the bounds for learning Ising models and Gaussian MRFs presented in recent work of Devroye et al [30]. Their bounds are obtained by bounding the VC complexity of the Yatracos class induced by the distributions of interest, while our bounds are obtained by constructing -nets of the distributions of interest, and running a tournament-style hypothesis selection algorithm [29, 26, 1] to select one distribution from the net. Since the distribution families we consider are non-parametric, our main technical contribution is to bound the size of an -net sufficient to cover the distributions of interest. Interestingly, we use properties of linear programs to argue through a sequence of transformations that the net size can be upper bounded in terms of the bit complexity of solutions to a linear program that we construct.

1.2 Roadmap and Technical Ideas

In this section, we provide a roadmap to the paper and survey some of our technical ideas.

Single-item Robustness (Appendix 3)

We consider first the setting where the model distribution is -close to the true, but unknown distribution in Kolmogorov distance. In this case, we argue directly that Myerson’s optimal mechanism [49] for is approximately optimal for any distribution that is in the -Kolmogorov-ball around , which includes (Theorem 2). The idea is that the revenue of the optimal mechanism can be written as an integral over probabilities of events of the form: does lie in a certain interval ? Since and are -close in Kolmogorov distance, the probabilities of all such events are within of each other, which implies that the revenues under and are also close. Finally, note that Myerson’s optimal mechanism is DSIC and IR, so it is truthful and IR w.r.t. any distribution.

Unfortunately, the same idea fails for Lévy distance, as the difference in the probabilities of the event that a certain lies in some interval under and can be as large as even when and are -close in Lévy distance. (Indeed, consider two single point distributions: a point mass at and a point mass at ; their probabilities of falling in the interval are respectively and .) We thus prove our robustness result for Lévy distance via a different route. Given any model distribution , we first construct the “worst” distribution and the “best” distribution in the -Lévy ball around : this means that, for any that lies in the -Lévy ball around , first-order stochastically dominates and is dominated by (see Definition 3). We choose our robust mechanism to be Myerson’s optimal mechanism for . It is not hard to argue that ’s revenue under is at least , the optimal revenue under the “worst” distribution (Lemma 4), due to the revenue monotonicity lemma (Lemma 3) shown in [28]. The statement provides a lower bound of ’s revenue under the unknown true distribution . To complete the argument, we need to argue that cannot be too much larger than . Indeed, we relax to , and show that even the optimal revenue under the “best” distribution . To do so, we construct two auxiliary distributions and , such that (i) ; and (ii) and are -close in Kolmogorov distance, and and are -close also in Kolmogorov distance. Our robustness theorem under Kolmogorov distance (Theorem 2) implies then that and . Hence, , which completes our proof.

Multi-item Robustness (Section 4)

We first discuss our result for total variation distance. Unfortunately, our approach for Lévy distance—of simply choosing the optimal mechanism for the “worst,” in the first-order stochastic dominance sense, distribution in the -TV-ball around to be our robust mechanism—no longer applies. Indeed, it is known that the optimal revenue in multi-item auctions may be non-monotone with respect to first-order stochastic dominance [40], i.e. a distribution may be stochastically dominated by another but result in higher revenue. However, if and are -close in total variation distance, this means that there is a coupling between and under which the valuation profiles are almost always sampled the same. If we take the optimal mechanism for , and apply to bidders from , it will produce almost the same revenue under , and vice versa. Indeed, the only event under which may generate different revenue under the two distributions is when the coupling samples different profiles, but this happens with small probability. Similarly, the BIC and IR properties of under become slightly approximate under . We claim that we can massage , in a way oblivious to , to produce a -truthful and exactly IR mechanism for , which achieves an up-to- revenue (Theorem 3).

The main challenge is when and are only -close in Prokhorov distance. Note that two distributions within Prokhorov distance may have total variation distance . Just imagine two point masses: one at and another at . So Prokhorov robustness is not directly implied by TV robustness.

Why Standard Discretization Arguments are Insufficient?

Unlike standard algorithmic problems, discretization is subtle in mechanism design. Due to the presence of incentives, a small change in the bidders’ value distributions may change the distribution of outcomes of the mechanism dramatically. To perform discretization in mechanism design, a standard procedure goes as follows [5, 36, 45]: let be the true distribution, and be the distribution after discretization; design the optimal mechanism for ; to run on a bid vector from , discretize it to and apply mechanism on . This procedure can be generalized to any pair of distributions and as long as, we are given a coupling between and that maps any bid vector in the support of distribution to a bit vector in the support of . If for every bidder , and are close with all but small probability, we can apply similar arguments as in the total variation robustness result to massage the mechanism above to be nearly-truthful and exactly IR for , and argue it is approximately revenue optimal. Clearly, in the context of discretization, and are guaranteed to be close if the discretization is sufficiently fine.

At first glance, this procedure may seem applicable to our problem. A characterization of Prokhorov distance due to Strassen (Theorem 4) shows that: two distributions and are -close in Prokhorov distance if and only if there exists a (potentially randomized) coupling such that if random variable is distributed according to , then is distributed according to and . If is the optimal mechanism for the model distribution , and is the true distribution that is -close to , why can’t we combine the procedure above with the coupling to establish our Prokhorov robustness result?

Unfortunately, this approach is insufficient due to the following two issues: (i) The procedure relies on knowing the coupling . As we do not even know , how can we know the coupling? (ii) Even if we can identify the coupling between and a specific , the procedure above constructs a mechanism that depends on the coupling . However, may change for every different in the -Prokhorov-ball around , so the procedure generates a different mechanism for every possible true distribution. 888It is worth noting that the procedure can indeed be employed to prove the Prokhorov continuity, as the the pure existence of a good coupling between and suffices.

To satisfy our requirement for a robust mechanism in Goal III, we need to construct a single mechanism that is nearly truthful, IR, and near-optimal simultaneously for every distribution in the -Prokhorov-ball around . Our proof relies on a novel way to “simultaneously couple” with every distribution in the -Prokhorov-ball around . If we round both and any to a random grid with width , we can argue that the expected total variation distance (over the randomness of the grid) between the two rounded distributions and is (Lemma 7). Now consider the following mechanism: choose a random grid , round the bids to the random grid, apply the optimal mechanism that is designed for . Our robustness result under the total variation distance implies that for every realization of the random grid , is -truthful and up-to- revenue optimal for any . Since the expected value (over the randomness of the grid) of is for any in the -Prokhorov-ball of , our randomized mechanism is simultaneously -truthful and up-to- revenue optimal for all distributions in the -Prokhorov-ball around .999Since we round the bids to a random grid, we will also need to accommodate the rounding error. Please see Theorem 5 for details.

Sample Complexity Results

In Section 5, we apply our robustness theorem to obtain sample bounds for learning multi-item auctions under the item-independence assumption (Theorem 6). Our result provides an alternative proof of the main result of [36]. In Section 7, we combine our robustness theorem with our sample bounds for learning Markov Random Fields and Bayesian Networks discussed earlier to derive new polynomial sample complexity results for learning multi-item auctions when the distributions have structured correlation over the items. Theorem 7 summarizes our results when item values are generated by an MRF, and Theorem 8 our results when item values are generated by a Bayesenet.

2 Preliminaries

We first define a series statistical distances that we will use in the paper and discuss their relationships.

Definition 1 (Statistical Distance).

Let and be two probability measures. We use , , and to denote the total variational distance, the Kolmogorov distance, and the Lévy distance between and , respectively. See Appendix B for more details. Prokhorov Distance is a generalization of the Lévy Distance to high dimensional distributions. Let be a metric space and be a -algebra on . For , let . Then two measures and on have Prokhorov distance

We consider distributions supported on for some , so will be the -dimensional Euclidean Space, and we choose to be the -distance. We denote the Prokhorov distance between distributions , by .

Relationships between the Statistical Distances:

Among the four metrics, the Lévy distance and the Kolmogorov distance are only defined for single dimensional distributions, while the Prokhorov distance and the total variation distance are defined for general distributions. In the single dimensional case, the Lévy distance is a very liberal metric. In particular, for any two single dimensional distributions and ,

Note that a robustness result for a more liberal metric is more general. For example, the robustness result for single-item auctions under the Lévy metric implies the robustness under the total variation and Kolmogorov metric, because the -ball in Lévy distance contains the -ball in total variation and Kolmogorov distance. An astute reader may wonder whether one can find a more liberal metric in the single dimensional case. Interestingly, for the most common metrics studied probability theory, including the Wasserstein distance, the Hellinger distance, and the relative entropy, the Lévy distance is the most liberal up to a polynomial factor. That is, if the Lévy distance is , the distance under any of these metrics is at least . Indeed, the polynomial is simply the identity function or the quadratic function in most cases. Please see the survey by Gibbs and Su [33] and the references therein for more details.

The Prokhorov distance, also known as Lévy-Prokhorov Distance, is the generalization of the Lévy distance to multi-dimensional distributions. It is also the standard metric in robust statistical decision theory, see Huber [42] and Hampel et al. [38]. The Prokhorov distance is almost as liberal as the Lévy distance. 101010Note that for single dimensional distributions, the Prokhorov distance is not equivalent to Lévy distance. In particular, for any single dimensional distributions and . First, for any two distributions and ,

Second, if we consider other well studied metrics such as the Wasserstein distance, the Hellinger distance, and the relative entropy, the Prokhorov distance is again the most liberal up to a polynomial factor.

Multi-item Auctions:

We focus on revenue maximization in the combinatorial auction with bidders and heterogenous items. We use to denote the set of possible allocations, and each bidder has a valuation function/type . In this paper, we assume the function is parametrized by , where is bidder ’s value for item . We assume that bidder’s types are distributed independently. Throughout this paper, we assume all bidders types lie in . We adopt the valuation model in Gonczarowski and Weinberg [36] and consider valuations that satisfy the following Lipschitz property.

Definition 2 (Lipschitz Valuations).

There exists an absolute constant such that if type and are within distance , then for the corresponding valuations and , for all .

This for example includes common settings such as additive and unit demand with Lipschitz constant . More generally, holds for constrained additive valuations 111111 is constrained additive if , for some downward closed set system and . and even in some settings with complementarities. Please see [36] for further discussion.

A mechanism consists of an allocation rule and a payment rule . For any input bids , the allocation rule outputs a distribution over allocations and payments . If bidder ’s type is , her utility under input is .

Truthfulness and Revenue:

We use the standard notion -BIC and IR (see Appendix B for details). If is a -BIC mechanism w.r.t. some distribution , we use to denote the revenue of mechanism under distribution assuming bidders are bidding truthfully. Clearly, when is BIC w.r.t. . We denote the optimal revenue achievable by any -BIC (or BIC) mechanism by (or ). Although it is conceivable that permitting mechanisms to be -BIC allows for much greater expected revenue than if they were restricted to be BIC, past results show that this is not the case.

Lemma 1.

[27, 53] In any -bidder -item auction, let be any joint distribution over arbitrary -Lipschitz valuations, where the valuations of different bidders are independent. The maximum revenue attainable by any IR and -BIC auction for a given product distribution is at most greater than the maximum revenue attainable by any IR and BIC auction for that distribution.

Notations:

We allow the bidders to submit a special type , which represents not participating the auction. If anyone submits , the mechanism terminates immediately, and does not allocate any item to any bidder or charge any bidder. A bidder’s utility for submitting type is . We will sometimes refer to as the IR type.Throughout the paper, we use to denote the true type distributions of the bidders. We use to denote the model type distributions or our learned type distributions from samples. We use to denote the distribution induced by conditioned on being in the -dimensional cube , and to denote the support of distribution .

3 Lévy-Robustness for Single-Item Auctions

In this section, we show the robustness result under the Lévy distance in the single-item setting. If we are given a model distribution that is -close to the true distribution , in Lévy distance, for every bidder , we show how to design a mechanism only based on and extracts revenue that is at most less than the optimal revenue under any possible true distribution .

Theorem 1 (Lévy-Robustness for Single-item Auctions).

Given , where is an arbitrary distributions supported on for all . We can design a DSIC and IR mechanism based on such that for any product distribution satisfying for all , we have:

Let us sketch the proof of Theorem 1. We prove our statement in three steps.

-

•

Step (i): We first identify the “best” and “worst” distributions (Definition 3), in terms of the first-order stochastic dominance (Definition 4), among all distributions in the -Lévy-ball around the model distribution . We construct the optimal mechanism w.r.t. the “worst” distribution, and show that its revenue under any possible true distribution is at least ’s revenue under the “worst” distribution (Lemma 4). The statement provides a lower bound of ’s revenue under the unknown true distribution. Its proof follows from the revenue monotonicity lemma (Lemma 3) shown in [28].

-

•

Step (ii): We use the revenue monotonicity lemma again to show the optimal revenue under the true distribution is upper bounded by the optimal revenue under the “best” distribution(Lemma 5).

- •

3.1 Best and Worst Distributions in the -Lévy-Ball

We formally define the “best” and “worst” distributions in the -Lévy-ball around the model distribution.

Definition 3.

For every , we define and based on . is supported on , and its CDF is defined as . is supported on , and its CDF is defined as .

We provide a more intuitive interpretation of and here. To obtain , we first shift all values in to the right by , then we move the bottom probability mass to . To obtain , we first shift all values in to the left by , then we move the top probability mass to . It is not hard to see that both and are still in the -ball around in Lévy distance. More importantly, and are the “best” and “worst” distributions in the -Lévy-ball under first-order-stochastic-dominance.

Definition 4 (First-Order Stochastic Dominance).

We say distribution first-order stochastically dominates iff for all . We use to denote that distribution first-order stochastically dominates distribution . If and are two product distributions, and for all , we slightly abuse the notation to write .

Lemma 2.

For any , such that , we have .

Proof.

It follows from the definition of Lévy distance and Definition 3. For any ,

Clearly, , so we have for all . ∎

The plan is to construct the optimal mechanism for and show that this mechanism achieves up-to- optimal revenue under any possible true distribution .

Next, we state a revenue monotonicity lemma that will be useful. We first need the following definition.

Definition 5 (Extension of a Mechanism to All Values).

Suppose a mechanism is defined for all value profiles in . Define its extension to all values. We only specify , as can be determined by the payment identity given . first rounds the bid of each bidder down to the closest value in , and then apply allocation rule on the rounded bids. If some bidder ’s bid is smaller than the lowest value in , does not allocate the item to any bidder.

Observe that the extension provides a DSIC and IR mechanism for all values if the original mechanism is DSIC and IR.

Lemma 3 (Strong Revenue Monotonicity [28]).

Let be a product distributions. There exists an optimal DSIC and IR mechanism for such that, for any product distribution ,

is the extension of . In particular, this implies .

Combining Lemma 2 and 3, we show that if is the extension of the optimal mechanism for , it achieves at least under any distribution with .

Lemma 4.

Let be the extension of the optimal DSIC and IR mechanism for . For any product distribution with for all , we have the following:

Lemma 4 shows that with only knowledge of the model distribution , we can design a mechanism whose revenue under any possible true distribution is at least . Next, we upper bound the optimal revenue under with the optimal revenue under .

Lemma 5.

For any product distribution with for all , we have the following:

3.2 Comparing the Revenue of the Best and Worst Distributions

In this section, we show that our lower bound of ’s revenue under the true distribution and our upper bound of the optimal revenue under are at most away.

Lemma 6.

It is a priori not clear why Lemma 6 should be true, as is the “best” distribution and is the “worst” distribution in the -Lévy-ball around . We prove Lemma 6 by introducing another two auxiliary distributions and . In particular, we construct by shifting all values in to the right by , and construct by shifting all values in to the left by . There are two important properties of these two new distributions: (i) one can couple with so that the two random variables are always exactly away from each other; (ii) and are within Kolmogorov distance , and and are also within Kolmogorov distance . Property (i) allows us to prove that (see Claim 2). To make use of property (ii), we prove the following robustness theorem w.r.t. the Kolmogorov distance.

Theorem 2.

For any buyer , let and be two arbitrary distributions supported on such that . We have the following:

where and .

The proof of Theorem 2 is postponed to Appendix C. Equipped with Theorem 2, we can immediately show that and . Lemma 6 follows quite easily from Claim 2 and the two inequalities above. The complete proof of Lemma 6 can be found in Appendix C.

We are now ready to prove Theorem 1.

Proof of Theorem 1: We first construct based on and let be the extension of the optimal mechanism for . By Lemma 4, we know is at least for any . We also know that the optimal revenue under is at most by Lemma 5, and by Lemma 6. Therefore,

A simple corollary of Theorem 1 is the continuity of the optimal revenue under Lévy distance in single-item settings.

Corollary 1.

If and are supported on , and for all , then

where and .

4 Robustness for Multi-item Auctions

In this section, we prove our robustness results under the total variation distance and the Prokhorov distance in multi-item settings. As discussed in Section 1.2, the proof strategy for single-item auctions fails miserably in multi-item settings due to the lack of structure of the optimal mechanism. In particular, one of the crucial tools we relied on in single-item settings, the revenue monotonicity, no longer holds in multi-item settings [40]. Nevertheless, we still manage to provide robustness guarantees in multi-item auctions. The plan is to first prove the robustness result under the total variation distance in Section 4.1, then we show show to relate the Prokhorov distance with the total variation distance using randomized rounding in Section 4.2, and reduce the robustness under the Prokhorov distance to the robustness under the total variation distance in Section 4.3.

4.1 TV-Robustness for Multi-item Auctions

Theorem 3 (TV-Robustness for Multi-item Auctions).

Given any distribution , where each is a distribution supported on , and a -BIC and IR mechanism w.r.t. , we can construct a mechanism such that for any distribution , if we let for all and , then is -BIC w.r.t. and IR. Moreover, Note that our construction of only depends on and does not require any knowledge of .

We briefly describe the ideas behind the proof. If and share the same support, it is not hard to see that is already -BIC w.r.t. . The reason is that for any bidder and any type , her expected utility under any report can change by at most when the other bidders’ bids are drawn from rather than , as for all . The bulk of the proof is dedicated to the case, where and have different supports. We construct mechanism , which first takes each bidder ’s report and maps it to the “best” possible report from , then runs essentially on the transformed reports. We show that is -BIC w.r.t. and generates at most less revenue. The proof of Theorem 3 is postponed to Appendix D.1.

4.2 Connecting the Prokhorov Distance with the Total Variation Distance

In this section, we provide a randomized rounding scheme that relates the Prokhorov distance to the total variation distance. We first state a characterization of the Prokhorov distance due to Strassen [54] that is useful for our analysis.

Theorem 4 (Characterization of the Prokhorov Metric [54]).

Let and be two distributions supported on . if and only if there exists a coupling of and , such that where is the distance.

Theorem 4 states that and are within Prokhorov distance of each other if and only if there exists a coupling between the two distributions such that the two random variables are within of each other with probability at least . Next, we show that if and are close to each other in Prokhorov distance, then one can use a randomized rounding scheme to round both and to discrete distributions so that the two rounded distributions are close in total variation distance with high probability.

First, let us fix some notations.

Definition 6 (Rounded Distribution).

Let be a distribution supported on . For any and , we define function as follows: for all . Let be a random variable sampled from distribution . We define as the distribution for the random variable , and we call as the rounded distribution of .

Lemma 7.

Let and be two distributions supported on , and . For any , sample from the uniform distribution over ,

We only sketch the idea and postpone the formal proof to Appendix D.2. Let be a random variable sampled from and be a random variable sampled from . Since and are close in Prokhorov distance, we can couple and according to Theorem 4 such that they are within of each other with probability at least . The rounding scheme chooses a random origin from and rounds and to the corresponding random grid with width . More specifically, we round and to and respectively. For simplicity, consider . The key observation is that when and are within -distance of each other, they lie in the same grid with probability at least over the randomness of . If and are in the same grid, they will be rounded to the same point. In other words, the coupling between and induces a coupling between and such that, in expectation over the choice of , the event that the corresponding two rounded random variables have different values happens with probability at most . By the definition of total variation distance, this implies that the expected total variation distance between and is also at most . A similar argument applies to other choices of .

4.3 Prokhorov-Robustness for Multi-item Auctions

In this section, we show that even in multi-item settings, if every bidder’s approximate type distribution is within Prokhorov distance of her true type distribution , given any BIC and IR mechanism for , we can construct a mechanism that is -BIC w.r.t. , IR, and its revenue under truthful bidding is at most worse than .

Theorem 5.

Suppose we are given , where is an -dimensional distribution for each , and a BIC and IR mechanism w.r.t. . Suppose is the true but unknown type distribution such that for all . We can construct a randomized mechanism , oblivious to the true distribution , such that for any the followings hold:

-

1.

is -BIC w.r.t. and IR, where ;

-

2.

the expected revenue of under truthful bidding is

We postpone the formal proof of Theorem 5 to Appendix D.3. We provide a complete sketch here. Our construction consist of the following five steps.

-

•

Step (1): After receiving the bid profile, first sample from . For every realization of , we construct a mechanism and execute on the reported bids. In the next several steps, we show how to construct via two intermediate mechanisms and for every realization of based on . Since is a random variable, is a randomized mechanism.

-

•

Step (2): Round to for every bidder . We construct mechanism based on and show that is -BIC w.r.t. and IR. Moreover,

Here is the idea behind the construction: for any bidder and type drawn from , we resample a type from , which is the distribution induced by conditioned on being in the cube . We use the allocation rule of and a slightly modified payment rule on the resampled type profile. This guarantees that the new mechanism is -BIC w.r.t. and IR. The formal statement and analysis are shown in Lemma 8.

-

•

Step (3): We use to denote for our sample and every , and to denote . We transform into a new mechanism using Theorem 3. In particular, is -BIC w.r.t. and IR. Importantly, the construction of is oblivious to and . Moreover,

-

•

Step (4): We convert to so that it is -BIC w.r.t. , IR and

Here is the idea behind the construction of : for every bidder and her type drawn from , round it to (see Definition 6). We use the allocation rule of and a slightly modified payment rule on the rounded type profile. This guarantees that the new mechanism is -BIC w.r.t. and IR. Note that our construction only requires knowledge of , , and , and is completely oblivious to and . The formal statement and analysis are shown in Lemma 9.

-

•

Step (5): Since for every realization of , is -BIC w.r.t. and IR, must be -BIC w.r.t. and IR. According to Lemma 7, Therefore, is

-BIC w.r.t. and IR. Moreover,

Lemma 8.

Given any , , and a BIC and IR mechanism w.r.t. , we can construct a = -BIC w.r.t. and IR mechanism , such that

Lemma 9.

For any , , and distribution , if is a -BIC w.r.t. and IR mechanism, we can transform into a mechanism , so that is -BIC w.r.t. , IR, and has revenue under truthful bidding Moreover, the transformation does not rely on any knowledge of or .

4.4 Applications of Multi-Item Robustness

Lipschitz Continuity of the Optimal Revenue in Multi-item Auctions.

Equipped with Theorem 3 and 5, we can easily argue the Lipschitz continuity of the optimal revenue in multi-item auctions (Theorem 11) as stated in the last column of the second half of Table 1. Due to Theorem 3 and 5, we know that the optimal revenue of a -BIC and IR mechanism w.r.t. distribution is at least as large as the optimal revenue of a BIC and IR mechanism w.r.t. distribution , if or . According to Lemma 1, the optimal revenue of a -BIC and IR mechanism is at most larger than the optimal revenue of a BIC and IR mechanism. Hence, . Please see Appendix D.4 for the formal statement and the proof of Theorem 11.

Approximation Preserving Transformation.

One interesting implication of Theorem 11 is that the transformations of Theorems 3 and 5 are also approximation preserving. Given a a -approximation mechanism to the optimal revenue under distribution , applying the transformation in Theorem 5 (or Theorem 3) to , we obtain a new mechanism that is -BIC w.r.t. and IR if (or if ). Moreover, its revenue under truthful bidding is at least fraction of the optimal -BIC revenue under less a small additive term. The result is formally stated as Theorem 12 in Appendix D.5. Note that the third column of the second half of Table 1 is simply Theorem 12 with . Furthermore, if there is only a single bidder, the mechanism becomes exactly IC instead of approximately IC (Theorem 13).

Learning Multi-item Auctions under Item Independence.

Learning Multi-item Auctions under Structured Item Dependence.

Going beyond product measures, we initiate the study of learning multi-item auctions when every bidder’s item-values are dependent, but sampled from a joint distribution with structure. As we have already noted, arbitrary joint distributions are both unnatural from a modeling perspective, as they require exponentially many bits to describe, and are also known to require exponentially many samples to even learn approximately optimal auctions [31]. We thus propose studying the learnability of auctions under the assumption that each bidder’s item values are sampled from a Markov Random Field (MRF) or a Bayesian network (a.k.a. Bayeset). In fact, this is not really an assumption. These well-studied probabilistic frameworks, defined formally in Definitions 7 and 8 of Appendix 7 due to lack of space, are very flexible in that they can represent any distribution. The reason they are attractive from a modeling perspective is that they have a natural complexity parameter that controls how expressive they are, namely the maximum hyperedge size of an MRF and the maximum in-degree of a Bayesnet. Under the assumption that each bidder’s item-values are drawn from an MRF or a Bayesnet of complexity , we establish the results summarized in the last two rows of Table 2, whose main feature is that the sample complexity to learn an up-to- optimal auction is polynomial in the number of bidders , the number of items , the inverse approximation parameter , and other relevant parameters, and is only exponential in the complexity parameter of the bidders’ MRFs or Bayesian networks, as it should given the known lower bounds [31].

Our results for learning near-optimal auctions under MRF and Bayesnet assumptions are stated in more detail as Theorems 7 and 8 of Appendix 7, and can also accommodate unobservable variables which makes their applicability very broad. In turn, these results are proven by combining our robustness result (Theorem 12) with new learnability results for MRFs and Bayesnets that we also establish, namely Theorems 9 and 10 of Appendix 7 respectively. These results are of independent interest and provide broad generalizations of the recent upper bounds of [30] for Gaussian MRFs and Ising models. While this recent work bounds the VC dimension of the Yatracos class of these families of distributions, for our more general families of non-parametric distributions we construct instead covers under either total variation distance or Prokhorov distance, and combine our cover-size upper bounds with generic tournament-style algorithms; see e.g. [29, 26, 1]. The details are provided in Appendix F. While there are many details, we illustrate one snippet of an idea used in constructing a -cover, in total variation distance, of the set of all MRFs with hyper-edges of size at most and a discrete alphabet on every node. The proof argues that (i) the (appropriately normalized) log-potential functions of the MRF can be discretized to take values in the negative integers at a cost of in total variation distance; (ii) using properties of linear programming, it argues that using negative integers of bit complexity polynomial in , and suffices at another cost of in total variation distance. It thus argues that all MRFs can be covered by a set of MRFs of size exponential in , which is sufficient to yield the required sample bounds using the tournament algorithm.

5 Learning Multi-item Auctions under Item Independence

In this section, we show how to derive one of the state-of-the-art learnability results for learning multi-item auctions via our robustness results. We consider the case where every bidder’s type distribution is a -dimensional product distribution. We will show that a generalization of the main result by Gonczarowski and Weinberg [36] follows easily from our robustness result. The main idea is that it suffices to learn the distribution within small Prokhorov distance for every bidder , and it only requires polynomial many samples when each is a product distribution.

Theorem 6.

Consider the general mechanism design setting of Section 2. Recall that is the Lipschitz constant of the valuations. For every , and for every , we can learn a distribution with samples from , such that, with probability , we can transform any BIC w.r.t. , IR, and -approximation mechanism to an -BIC w.r.t. and IR mechanism , whose revenue under truthful bidding satisfies

If , the mechanism will be IR and IC, and

In particular, Gonczarowski and Weinberg [36] proved the case, and our result applies to any . The proof is given in Appendix E. We provide a proof sketch here. We first prove Lemma 12, which shows that polynomially many samples suffice to learn a distribution that is close to in Prokhorov distance. Now the statement simply follows from Theorem 12.

6 Missing Proofs from Section 5

We first show that for any product distribution , we can learn the rounded distribution of within small TV distance with polynomially many samples.

Lemma 10.

Let , where is an arbitrary distribution supported on for every . Given samples, we can learn a product distribution such that

with probability at least .

Proof.

We denote the samples as . Round each sample to multiples of . More specifically, let for every sample . Let be the uniform distribution over . Let . Note that is the empirical distribution of samples from . As , with samples, the empirical distribution should satisfy with probability at least . By the union bound for all with probability at least , which implies with probability at least . Observe that and can be coupled so that the two samples are always within in distance. When , consider the coupling between and by composing the optimal coupling between and and the coupling between and . Clearly, the two samples from and are within distance with probability at least . Due to Theorem 4, the existence of this coupling implies that . ∎

Proof of Theorem 6: We only consider the case, where . is an absolute constant and we will specify its choice in the end of the proof.

In light of Lemma 12, we take from and learn a distribution so that, with probability at least , for all . According to Theorem 12, we can transform into mechanism that is -BIC w.r.t. and IR. Choose in a way so that is -BIC w.r.t. . Moreover, ’s revenue under truthful bidding satisfies

If we choose to be sufficiently small, then

When there is only a single-bidder, we can apply Lemma 11 to transform to an IC and IR mechanism, whose revenue satisfies the guarantee in the statement.

7 Optimal Mechanism Design under Structural Item Dependence

In this section, we go beyond the standard assumption of item-independence, which has been employed in most of prior literature, to consider settings where, as is commonly the case in practice, item values are correlated. Of course, once we embark onto a study of correlated distributions, we should not go all the way to full generality, since exponential sample-size lower bounds are known, even for learning approximately optimal mechanisms in single-bidder unit-demand settings [31]. Besides those sample complexity lower bounds, however, fully general distributions are also not very natural. In practice, high-dimensional distributions are not arbitrary, but have structure, which allows us to perform inference on them and learn them more efficiently. We thus propose the study of optimal mechanism design under the assumption that item values are jointly sampled from a high-dimensional distribution with structure.

There are many probabilistic frameworks that allow modeling structure in a high-dimensional distribution. In this work we consider one of the most prominent ones: graphical models, and in particular consider the two most common types of graphical models: Markov Random Fields and Bayesian Networks.

Definition 7.

A Markov Random Field (MRF) is a distribution defined by a hypergraph . Associated with every vertex is a random variable taking values in some alphabet , as well as a potential function . Associated with every hyperedge is a potential function . In terms of these potentials, we define a probability distribution associating to each vector probability satisfying:

| (1) |

where for a set of nodes and a vector we denote by the restriction of to the nodes in , and is a normalization constant making sure that , as defined above, is a distribution. In the degenerate case where the products on the RHS of (1) always evaluate to , we assume that is the uniform distribution over . In that case, we get the same distribution by assuming that all potential functions are identically . Hence, we can in fact assume that the products on the RHS of (1) cannot always evaluate to .

Definition 8.

A Bayesian network, or Bayesnet, specifies a probability distribution in terms of a directed acyclic graph whose nodes are random variables taking values in some alphabet . To describe the probability distribution, one specifies conditional probabilities , for all vertices in , and configurations and , where represents the set of parents of in , taken to be if has no parents. In terms of these conditional probabilities, a probability distribution over is defined as follows:

It is important to note that both MRFs and Bayesnets allow the study of distributions in their full generality, as long as the graphs on which they are defined are sufficiently dense. In particular, the graph (hypergraph and DAG respectively) underlying these models captures conditional independence relations, and is sufficiently flexible to capture the structure of intricate dependencies in the data. As such these models have found myriad applications; see e.g. [43, 50, 51, 44] and their references. A common way to control the expressiveness of MRFs and Bayesnets is to vary the maximum size of hyperedges in an MRF and indegree in a Bayesnet. Our sample complexity results presented below will be parametrized according to this measure of complexity in the distributions.

In our results, presented below, we exploit our modular framework to disentangle the identification of good mechanisms for these settings from the intricacies of learning a good model of the underlying distribution from samples. In particular, we are able to pair our mechanism design framework presented in earlier sections with learning results for MRFs and Bayesnets to characterize the sample complexity of learning good mechanisms when the item distributions are MRFs and Bayesnets. Below, we first present our results on the sample complexity of learning good mechanisms in these settings, followed by the learning results for MRFs and Bayesnets that these are modularly dependent on.

7.1 Learning Multi-item Auctions under Structural Item Dependence

In this section, we state our results for learning multi-item auctions when each bidder’s values correlated. In particular, we consider two cases: (i) every bidder’s type is sampled from an MRF, or (ii) every bidder’s type is sampled from a Bayesnet. Our results can accommodate latent variables, that is, some of the variables/nodes of the MRF or Bayesnet are not observable in the samples. We show that the sample complexity for learning an -BIC and IR mechanism, whose revenue is at most less than the optimal revenue achievable by any -BIC and IR mechanisms, is polynomial in the size of the problem and scales gracefully with the parameters of the graphical models that generate the type distributions. If there is only a single bidder, the mechanism we learn will be exactly IC rather than approximately IC. We derive the sample complexity by combining our robustness result (Theorem 12) with learnability results for MRFs and Bayesnets (Theorem 9 and 10).

Theorem 7 (Optimal Mechanism Design under MRF Item Distributions).

Consider the general mechanism design setting of Section 2. Recall that is the Lipschitz constant of the valuations. Let , where each is a -dimensional distribution generated by an MRF , as in Definition 7, defined on a graph with nodes, hyper-edges of size at most , and . When , we say is generated by an MRF with latent variables. We use to denote .

For every , , and , we can learn, with probability at least , an -BIC w.r.t. and IR mechanism , whose revenue under truthful bidding is at most smaller than the optimal revenue achievable by any -BIC w.r.t. and IR mechanism, given

-

•

samples if the alphabet is finite; when the graph on which is defined is known for each bidder , then -many samples suffice, where is an upper bound on the number of edges in all the graphs;

-

•

samples if the alphabet , and the log potentials and for every node and every edge are -Lipschitz w.r.t. the -norm, for every bidder ; when the graph on which is defined is known for each bidder , then -many samples suffice, where is an upper bound on the number of edges in all the graphs.

If , the mechanism will be IR and IC, and

Theorem 8 (Optimal Mechanism Design under Bayesnet Item Distributions).

Consider the general mechanism design setting of Section 2. Recall that is the Lipschitz constant of the valuations. Let , where each is a -dimensional distribution generated by a Bayesnet , as in Definition 8, defined on a DAG with nodes, in-degree at most , and . When , we say is generated by an MRF with latent variables. We use to denote .

For every , , and , we can learn, with probability at least , an -BIC w.r.t. and IR mechanism , whose revenue under truthful bidding is at most smaller than the optimal revenue achievable by any -BIC w.r.t. and IR mechanism, with

-

•

samples if the alphabet is finite;

-

•

samples if the alphabet , and for every , the conditional probability of every node is -Lipschitz in the -norm (see Theorem 10 for the definition).

If , the mechanism will be IR and IC, and

7.2 Sample Complexity for Learning MRFs and Bayesnets

In this section, we present the sample complexity of learning an MRF or a Bayesnet. Our sample complexity scales gracefully with the maximum size of hyperedges in an MRF and indegree in a Bayesnet. Furthermore, our results hold even in the presence of latent variables, where we can only observe the values of variables, out of the total variables, in a sample.

Theorem 9 (Learnability of MRFs in Total Variation and Prokhorov Distance).

Suppose we are given sample access to an MRF , as in Definition 7, defined on an unknown graph with hyper-edges of size at most .

-

•

Finite alphabet : Given samples from we can learn some MRF whose hyper-edges also have size at most such that . If the graph on which is defined is known, then -many samples suffice. Moreover, the polynomial dependence of the sample complexity on cannot be improved, and the dependence on is tight up to factors.

-

•

Alphabet : If the log potentials and for every node and every edge are -Lipschitz w.r.t. the -norm, then given samples from we can learn some MRF whose hyper-edges also have size at most such that . If the graph on which is defined is known, then -many samples suffice.

Our sample complexity bounds can be easily extended to MRFs with latent variables, i.e. to the case where some subset of the variables are observable in each sample we draw from . Suppose is the number of observable variables. In this case, for all settings discussed above, our sample complexity bound only increases by a multiplicative factor.

Theorem 10 (Learnability of Bayesnets in Total Variation and Prokhorov Distance).

Suppose we are given sample access to a Bayesnet , as in Definition 8, defined on an unknown DAG with in-degree at most .

-

•

Finite alphabet : Given -many samples from we can learn some Bayesnet defined on a DAG whose in-degree is also bounded by such that . If the graph on which is defined is known, then -many samples suffice. Moreover, the dependence of the sample complexity on and is tight up to logarithmic factors.

-

•

Alphabet : Suppose that the conditional probability distribution of every node is -Lipschitz in the -norm, that is, , and . Then, given -many samples from , we can learn some Bayesnet defined on a DAG whose in-degree is also bounded by such that . If the graph on which is defined is known, then -many samples suffice.

Our sample complexity bounds can be easily extended to Bayesnets with latent variables, i.e. to the case where some subset of the variables are observable in each sample we draw from . Suppose is the number of observable variables. In this case, for all settings discussed above, our sample complexity bound only increases by a multiplicative factor.

In our proof of Theorem 9, we first carefully construct an -net over all MRFs with hyperedges of size at most in either total variation distance or Prokhorov distance, then apply a tournament-style density estimation algorithm [29, 26, 1] to learn a distribution from the -net that is at most away from the true distribution using polynomially many samples. Our proof of Theorem 10 follows a similar recipe. The main difference is how we construct the -net over all Bayesnets with in-degree at most . Both proofs are presented in Appendix F.

References

- [1] Jayadev Acharya, Ashkan Jafarpour, Alon Orlitsky, and Ananda Theertha Suresh. Sorting with adversarial comparators and application to density estimation. In Proceedings of the IEEE International Symposium on Information Theory (ISIT), 2014.

- [2] Saeed Alaei. Bayesian Combinatorial Auctions: Expanding Single Buyer Mechanisms to Many Buyers. In the 52nd Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2011.

- [3] Saeed Alaei, Hu Fu, Nima Haghpanah, Jason Hartline, and Azarakhsh Malekian. Bayesian Optimal Auctions via Multi- to Single-agent Reduction. In the 13th ACM Conference on Electronic Commerce (EC), 2012.

- [4] Saeed Alaei, Hu Fu, Nima Haghpanah, and Jason D. Hartline. The simple economics of approximately optimal auctions. In 54th Annual IEEE Symposium on Foundations of Computer Science, FOCS 2013, 26-29 October, 2013, Berkeley, CA, USA, pages 628–637, 2013.

- [5] Moshe Babaioff, Yannai A. Gonczarowski, and Noam Nisan. The menu-size complexity of revenue approximation. In Hamed Hatami, Pierre McKenzie, and Valerie King, editors, Proceedings of the 49th Annual ACM SIGACT Symposium on Theory of Computing, STOC 2017, Montreal, QC, Canada, June 19-23, 2017, pages 869–877. ACM, 2017.

- [6] Moshe Babaioff, Nicole Immorlica, Brendan Lucier, and S. Matthew Weinberg. A Simple and Approximately Optimal Mechanism for an Additive Buyer. In the 55th Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2014.

- [7] Dirk Bergemann and Karl Schlag. Robust monopoly pricing. Journal of Economic Theory, 146(6):2527–2543, 2011.

- [8] Anand Bhalgat, Sreenivas Gollapudi, and Kamesh Munagala. Optimal auctions via the multiplicative weight method. In ACM Conference on Electronic Commerce, EC ’13, Philadelphia, PA, USA, June 16-20, 2013, pages 73–90, 2013.

- [9] Patrick Briest, Shuchi Chawla, Robert Kleinberg, and S. Matthew Weinberg. Pricing Randomized Allocations. In the Twenty-First Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), 2010.

- [10] Yang Cai and Constantinos Daskalakis. Extreme-Value Theorems for Optimal Multidimensional Pricing. In the 52nd Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2011.

- [11] Yang Cai and Constantinos Daskalakis. Learning multi-item auctions with (or without) samples. In the 58th Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2017.

- [12] Yang Cai, Constantinos Daskalakis, and S. Matthew Weinberg. An Algorithmic Characterization of Multi-Dimensional Mechanisms. In the 44th Annual ACM Symposium on Theory of Computing (STOC), 2012.

- [13] Yang Cai, Constantinos Daskalakis, and S. Matthew Weinberg. Optimal Multi-Dimensional Mechanism Design: Reducing Revenue to Welfare Maximization. In the 53rd Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2012.

- [14] Yang Cai, Constantinos Daskalakis, and S. Matthew Weinberg. Understanding Incentives: Mechanism Design becomes Algorithm Design. In the 54th Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2013.

- [15] Yang Cai, Nikhil R. Devanur, and S. Matthew Weinberg. A duality based unified approach to bayesian mechanism design. In the 48th Annual ACM Symposium on Theory of Computing (STOC), 2016.

- [16] Yang Cai and Zhiyi Huang. Simple and Nearly Optimal Multi-Item Auctions. In the 24th Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), 2013.

- [17] Yang Cai and Mingfei Zhao. Simple mechanisms for subadditive buyers via duality. In Proceedings of the 49th Annual ACM SIGACT Symposium on Theory of Computing, STOC 2017, Montreal, QC, Canada, June 19-23, 2017, pages 170–183, 2017.

- [18] Shuchi Chawla, Jason D. Hartline, and Robert D. Kleinberg. Algorithmic Pricing via Virtual Valuations. In the 8th ACM Conference on Electronic Commerce (EC), 2007.

- [19] Shuchi Chawla, Jason D. Hartline, David L. Malec, and Balasubramanian Sivan. Multi-Parameter Mechanism Design and Sequential Posted Pricing. In the 42nd ACM Symposium on Theory of Computing (STOC), 2010.

- [20] Shuchi Chawla and J. Benjamin Miller. Mechanism design for subadditive agents via an ex-ante relaxation. In Proceedings of the 2016 ACM Conference on Economics and Computation, EC ’16, Maastricht, The Netherlands, July 24-28, 2016, pages 579–596, 2016.

- [21] Richard Cole and Tim Roughgarden. The sample complexity of revenue maximization. In Proceedings of the 46th Annual ACM Symposium on Theory of Computing, 2014.

- [22] Constantinos Daskalakis, Alan Deckelbaum, and Christos Tzamos. Mechanism design via optimal transport. In ACM Conference on Electronic Commerce, EC ’13, Philadelphia, PA, USA, June 16-20, 2013, pages 269–286, 2013.

- [23] Constantinos Daskalakis, Alan Deckelbaum, and Christos Tzamos. The complexity of optimal mechanism design. In the 25th Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), 2014.

- [24] Constantinos Daskalakis, Nikhil R. Devanur, and S. Matthew Weinberg. Revenue maximization and ex-post budget constraints. In Proceedings of the Sixteenth ACM Conference on Economics and Computation, EC ’15, Portland, OR, USA, June 15-19, 2015, pages 433–447, 2015.

- [25] Constantinos Daskalakis, Nishanth Dikkala, and Gautam Kamath. Testing ising models. In Proceedings of the Twenty-Ninth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1989–2007. Society for Industrial and Applied Mathematics, 2018.

- [26] Constantinos Daskalakis and Gautam Kamath. Faster and Sample Near-Optimal Algorithms for Proper Learning Mixtures of Gaussians. In Proceedings of the 27th Conference on Learning Theory (COLT), 2014.

- [27] Constantinos Daskalakis and S. Matthew Weinberg. Symmetries and Optimal Multi-Dimensional Mechanism Design. In the 13th ACM Conference on Electronic Commerce (EC), 2012.

- [28] Nikhil R Devanur, Zhiyi Huang, and Christos-Alexandros Psomas. The sample complexity of auctions with side information. In Proceedings of the forty-eighth annual ACM symposium on Theory of Computing, pages 426–439. ACM, 2016.

- [29] Luc Devroye and Gábor Lugosi. Combinatorial methods in density estimation. Springer Science & Business Media, 2012.

- [30] Luc Devroye, Abbas Mehrabian, and Tommy Reddad. The minimax learning rate of normal and ising undirected graphical models. arXiv preprint arXiv:1806.06887, 2018.

- [31] Shaddin Dughmi, Li Han, and Noam Nisan. Sampling and representation complexity of revenue maximization. In Proceedings of the 10th International Conference on Web and Internet Economics (WINE), 2014.

- [32] Edith Elkind. Designing and learning optimal finite support auctions. In Proceedings of the eighteenth annual ACM-SIAM symposium on Discrete algorithms, pages 736–745. Society for Industrial and Applied Mathematics, 2007.

- [33] Alison L Gibbs and Francis Edward Su. On choosing and bounding probability metrics. International statistical review, 70(3):419–435, 2002.

- [34] Kira Goldner and Anna R Karlin. A prior-independent revenue-maximizing auction for multiple additive bidders. In International Conference on Web and Internet Economics, pages 160–173. Springer, 2016.

- [35] Yannai A Gonczarowski and Noam Nisan. Efficient empirical revenue maximization in single-parameter auction environments. In Proceedings of the 49th Annual ACM SIGACT Symposium on Theory of Computing, 2017.

- [36] Yannai A Gonczarowski and S Matthew Weinberg. The sample complexity of up-to- multi-dimensional revenue maximization. In 2018 IEEE 59th Annual Symposium on Foundations of Computer Science (FOCS), pages 416–426. IEEE, 2018.

- [37] Chenghao Guo, Zhiyi Huang, and Xinzhi Zhang. Settling the sample complexity of single-parameter revenue maximization. In the 51st Annual ACM Symposium on Theory of Computing (STOC), 2019.

- [38] Frank R Hampel, Elvezio M Ronchetti, Peter J Rousseeuw, and Werner A Stahel. Robust statistics: the approach based on influence functions, volume 196. John Wiley & Sons, 2011.