Scaling limit for stochastic control problems in population dynamics

Abstract

Going from a scaling approach for birth/death processes, we investigate the scaling limit of solutions to non-Markovian stochastic control problems by studying the convergence of solutions to BSDEs driven a sequence of converging martingales. In particular we manage to describe how the values and optimal controls of control problems converge when the models converge towards a continuous population model.

Key words: stochastic control, population models, birth and death processes, backward stochastic differential equation (BSDE), stability of BSDEs, martingale properties.

1 Introduction

The sustainability of natural resources has become a major subject of interest in the last decades for public institutions. For instance, in 1983 the European Union has launched its common fisheries policy to manage European fish stocks. In August 2010, a report of European commission named Water Scarcity and Drought in the European Union, has emphasized that ”an adequate supply of good-quality water is a pre-requisite for economic and social progress, so we need to do two things: we must learn to save water, and also to manage our available resources more efficiently”. A large part of academic literature has dealt with such issues. For example, Reed in [Ree79], Clarke and Kirkwood in [CK86], Regnier and De Lara in [RDeL15] or Tromer and Doyen in [TD19] have studied the exploitation of a natural resource under uncertainty on its evolution in a multi-period model. May, Beddington, Horwood and Sherpherd in [MBHS78] have considered the problem by assuming that the intrinsic population growth rate is given by the difference between recruitment and mortality for general recruitment functions. These models have been extended to stochastic differential equations driven by a Brownian motion (see for instance the work of Saphores [Sap03]). Evans, Hening and Shreiber in [EHS15] or more recently Kharroubi, Lim and Ly Vath in [LKLV18] have modelled the dynamic of the natural resource as the solution of the logistic stochastic differential equation to solve a control problem under interaction between species and delayed renewal of the resource. We also refer to the book [DeLD08] for stochastic and deterministic models and resource management problems. All the models mentioned above use a Brownian motion to describe the uncertainty of the system evolution. We refer to this class of model as continuous models. On the other side of the literature, Getz in [Get75] has studied control problems related to a birth/death process. This work has been extended more recently by Claisse in [Cla18] to branching processes. We refer to those models as discrete models.

It is well known that some continuous population models can be seen as scaling limits of discrete models, see for example the work of Bansaye and Méléard in [BM15]. Hence continuous models can be considered as good approximations of the macroscopic evolution of a population size. Therefore it is relevant to consider continuous models for resources management purposes. Moreover those models are attractive from a tractability viewpoint compared to discrete models. Indeed solving control problems in Brownian driven model essentially boils down to solve a partial differential equation. Whereas for discrete models it leads to integral-partial differential equation, which are often more complex to solve. Yet the remaining question is the relevancy of designing a management policy based on a continuous modeling while the controlled population (or resource) is naturally discrete.

To try to give an answer to this question we are going to consider a sequence of discrete population models that converges towards a continuous population model. For each of those models we consider a control problem. Each of them are the natural adaptations of the same control problem to the different models. Therefore we expect the solutions of the discrete control problems to converge towards the solution of the continuous limit problem. From -convergence results adapted to stochastic control problems as in for instance the articles of Buttazzo and Del Maso [BDM82] and Belloni, Buttazzo and Freddi [BBF93], we expect to have convergence of value functions (see also for instance [DM12, Theorem 10.22]) and a kind of weak convergence of optimal controls (see for instance [BBF93, Proposition 2.8]). This is emphasized in a toy model (see Section 2) where besides convergence of the value functions we also get convergence in law of the state process under the optimal control. In this paper we prove the convergence of the controls as sequence of processes. This is stronger than convergence. Since we aim at dealing with non-Markovian stochastic control problems our problematic is to prove the convergence of solutions to a sequence of Backward Stochastic Differential Equations (BSDE for short) driven by a sequence of converging martingales.

We know from the seminal paper of Donsker [Don51] that a scaling in time procedure leads to the weak convergence of a random walk to a Brownian motion. Following the idea of Donsker, Pardoux in [Par99b, Par99a] has studied the weak convergence of Markovian BSDE driven by Brownian motions. Extending this result to the theory of non-Markovian BSDE with fixed time horizon , Briand, Delyon and Mémin in [BDM01] have provided a time discretization of the Brownian motion to get the convergence of a time discretized BSDE. More precisely, they consider a sequence of random walks converging towards a Brownian motion . Then they prove the convergence of the solutions of a sequence of BSDEs driven the towards the solution of a BSDE driven by . The main idea is to prove the convergence of the terms involved in the martingale representation with respect to when goes to infinity. For this they use the convergence, in the sense of Coquet, Mémin and Slominski [CMS01], of the filtrations associated to each of the towards the natural filtration associated to . Those results have been extended in [BDM02] to a more general situation, without assuming that has a predictable representation property, but assuming that the brackets of the martingales are uniformly bounded. In a more general case, preliminary results on the convergence of BSDEs driven by general martingales have been obtained in the PhD thesis of Alexandros Saplaouras, in for the Skorokhod distance, see [Sap17, Chapter IV].

In the present paper we aim at extending both the results of [Par99b, BDM01] to a wider class of martingale convergence and the results of [Sap17] to stronger convergence. Starting from a scaling result in [BM15] showing that a sequence of scaled birth/death processes with scaling parameter converges in law to the solution of a stochastic Feller diffusion, we begin to extend it to more general birth and death intensities. We then consider a sequence of BSDEs of the form

where is some general terminal random condition, the generator of the BSDE, a two dimensional martingale associated to the population model and denotes the measure associated to the angle bracket of . We also consider the continuous counterpart of ,

where is some terminal condition, is the generator of the BSDE, is a one dimensional martingale related to the diffusion term of and is its angle bracket. The existence and uniqueness of solutions to such BSDEs driven by general martingales have been studied, for instance, by El Karoui and Huang in [EKH97], Confortola and Fuhrman in [CF13] or more recently by Papapantoleon, Possamaï and Saplaouras in [PPS18] in a general framework. Inspired by [BDM02], we prove that when converges toward and towards , the solution of converges to the solution of . Moreover, since we are motivated by applying our results to stochastic control problems, we prove a stronger convergence, compared to [Sap17], for the solutions to the particular BSDEs considered. To obtain such stronger convergence, we however need to set stronger assumptions on the integrability of terminal conditions . The methods used are related to the so-called martingale problem as stated by Jacod and Shiryaev in [JS13] and to the double-Picard iterations craftly used in [BDM02]. Our results enable us to investigate the scaling limit of solutions to non-Markovian stochastic control problems applied to population monitoring.

Main Contributions.

Our approach extends the results in [Par99a, Par99b, BDM01, BDM02] to counting processes, beyond the convergence of a time discretization of the BSDE. This paper is also more focused on applications to stochastic control problems, dealing with examples in population monitoring. We prove that a sequence of solutions to BSDEs driven by birth/death processes converges to a BSDE driven by a one dimensional Brownian motion in tractable spaces to investigate the scaling limits of solutions to stochastic control problems. This also extends the preliminary results on the robustness of solutions to BSDEs in [Sap17, Chapter IV] to the convergence of solutions to our particular BSDE in different spaces. Moreover, the results obtained on the convergence of optimal controls in stochastic control problems go beyond convergence since we get a strong form of convergence for the optimal controls.

The structure of the paper is the following. In Section 2 we study the convergence of a rescaled birth/death process to the solution of a stochastic Feller type SDE by extending [BM15] to more general dynamics (see Theorem 1). We also provide fundamental properties of our state processes such as exponential moments (see Proposition 1 and Corollary 1). Section 3 introduces a toy model motivating our study and illustrated with numerical simulations. In Section 4, Theorem 2 gives convergence of the solutions to to the solution of . In Section 5 from our BSDE approach we deduce convergence of the values and optimal controls to a sequence of control problems. Section 6 gives the main proofs of our results. Minor proofs are given in the appendix.

The spaces considered are defined in Appendix A.

2 From a discrete to a continuous population model

In this section we define a sequence of discrete population models. We show that this sequence converges in law towards a continuous Feller population model by extending [BM15, Theorem III-3.2] to more general population dynamic models.

2.1 Definition of the discrete population models

We consider positive continuous functions , and defined from into that satisfy the following standing assumption.

Assumption 1.

-

(i)

The functions , and are null on and there exists non negative constants , , and such that for any

-

(ii)

and are Lipschitz continuous.

We note the set of piecewise continuous increasing positive functions with jumps equal to . We denote by the natural filtration associated to the canonical process of .

For a fixed and we define a population model on the stochastic basis . The initial population is and the processes and represent respectively the number of birth and death in the population. This means that when the process jumps there is a new individual in the population and when jumps there is one individual less in the population. Therefore at time the population size is . As we are interested in the large population limit (which corresponds to large) we consider the rescaled population process

We define the birth intensity in the model with parameter and initial population as

and the intensity of death

Remark 1.

Following Theorem 3.6 in [Jac75] there exists a unique probability measure on such that the processes

are local martingales. It means that under the probability the process (resp. ) has intensity (resp. ). Note that if then is absolutely continuous with respect to and we have:

| (1) |

where

We justify this change of measure in Appendix B.

For the rest of this work we fix an initial population and do not write anymore the superscript to lighten the notations. We write instead of when there is no ambiguity on the probability used. For any we consider the processes , and for

We note . The rescaled population process is now noted

2.2 Scaling limit of the sequence

Intuitively, and having in mind [BM15, Theorem 3.2], a continuous version of the processes , denoted by , would be an Ito diffusion with drift equal to and volatility given by . We formalize this intuition in the following result which extends [BM15, Theorem 3.2]. The proof is given in Section 6.1.

Theorem 1.

The sequence converges in law for the Skorokhod topology towards such that

-

(i)

there exists a bi-dimensional Brownian motions satisfying

-

(ii)

with , the process is the unique strong solution of

-

(iii)

.

Moreover, there exists a probability space and a sequence such that for any , has the law of under . Moreover on this space the sequence

converges in to when goes to .

According to the last point of Theorem 1 from now on we work under the probability space and we consider that the processes and are defined on this space. For any we note the natural filtration associated to and the natural filtration associated to .

Before going to the next section, we define some processes that we will extensively use in the rest of the paper. We note for

so that and that is written

We also consider the processes

Note that under the probability the random measure associated to the process interpreted as a compound jump process with values in admits as predictable compensator measure

with and where denotes the Dirac measure at point . This point of view is introduced in order to draw a parallel with the framework of [CF13] to which we will refer extensively in Section 4.2.

2.3 Uniform exponential moments

Finally we show that the sequence of processes admits exponential moments uniformly in if is linear. The proof of this result is postponed in Appendix F.

Proposition 1.

If there exists a positive constant such that there exists some positive constants , and such that for any we have

Without loss of of generality we assume that . From now we fix a positive constant strictly smaller than . As a consequence of Proposition 1, for any integer we have for any

and

We deduce from Fatou’s Lemma together with Proposition 1 that inherits from the exponential moments of as stated in the following corollary.

Corollary 1.

If there exists positive such that there exists some positive constants and such that for any we have

In order to benefit from those exponential moments we now assume that for some positive constant fixed.

3 Illustration of the study on a toy model

In this section, we illustrate the convergence result applied to optimization problems in population dynamics. We consider specific parameters and a sequence of control problems for which we are able to make explicit computations. Then, we show that the sequence of optimal controls converges in law to the optimal control of a continuous problem. In this section, we aim at providing the general main ideas of the paper rather than being perfectly accurate. Rigorous statements will be given in Section 5.

3.1 Discrete populations models

We consider a discrete birth/death model as studied in [BM15] by choosing:

-

-

the initial population ,

-

-

the birth rate for some ,

-

-

the death rate for some .

Recall from Remark 1 and from [BM15, Theorem 3.2] that converges in law for the Skorokhod topology towards the continuous diffusion process solution of the Feller stochastic differential equation

| (2) |

for a Brownian motion.

In this toy model, we assume that a resource manager regulates the population through an -predictable control . A control is admissible if

-

•

there exists a unique law under which the death intensity of the population is

and the birth intensity is . When this probability exists, it is the law of the population under the control .

-

•

is a non negative process almost surely.

We denote by the set of admissible controls.

The agent is assumed to be penalized if he fails at reaching a fixed level of the resource at time determined by a regulator. We model this penalization by the square of the difference between the effective population size at time and the target . So that the manager pays at time where is a positive constant. The manager payoff is also assumed to be penalized by the instantaneous amount per unit of time when its effort is . The problem of the resource manager is thus to solve

where denotes the expectation taken under the probability . We assume that and .

To solve this problem, as usual in stochastic control theory, we study the corresponding Hamilton-Jacobi-Bellman (HJB for short) equation and use a verification argument. The HJB equation associated to the control problem is

with Hamiltonian given by

and where

The maximizer of the Hamiltonian is , hence

Note that we do not actually care about the value of the control when since if the population reaches , it is stuck at this value. The partial differential equation (PDE for short) is quadratic, so we search for a solution under the form

Identifying the monomials, we get that is solution of if and only if is solution of the following systems of ODEs:

By Cauchy-Lipschitz theorem this system admits a unique solution. Thus the optimal effort of the agent is

and the corresponding death intensity is given by

Note that in view of and since is negative and positive, there exists a small enough, independent of , such that for any the control is in . We refer to Appendix C for more details on this point. We assume that we are considering such short enough time horizon here.

3.2 Continuous populations model

We now turn to the continuous version of the control problem. We assume that the manager controls the drift term in (2) through an predictable process . We say that is an admissible control when the following SDE admits a unique weak solution

When such solution exists we note its law that is the law of the population under the control . We denote by the set of admissible controls.

The control problem in the continuous framework is written

The associated HJB equation is given by

where the Hamiltonian is

The maximizer of the Hamiltonian is

As previously, we are looking for a quadratic solution of the form

Identifying the monomials, we get that is solution of if and only if is solution of the following system of ODEs.

Hence, the optimal control is given by

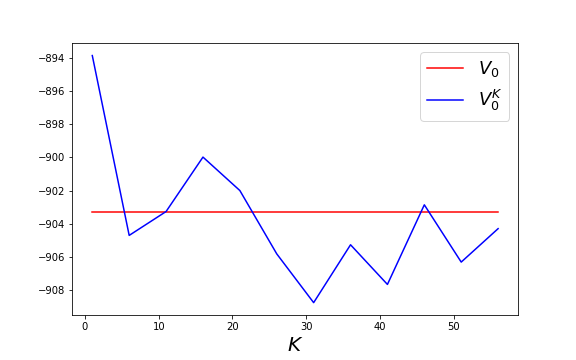

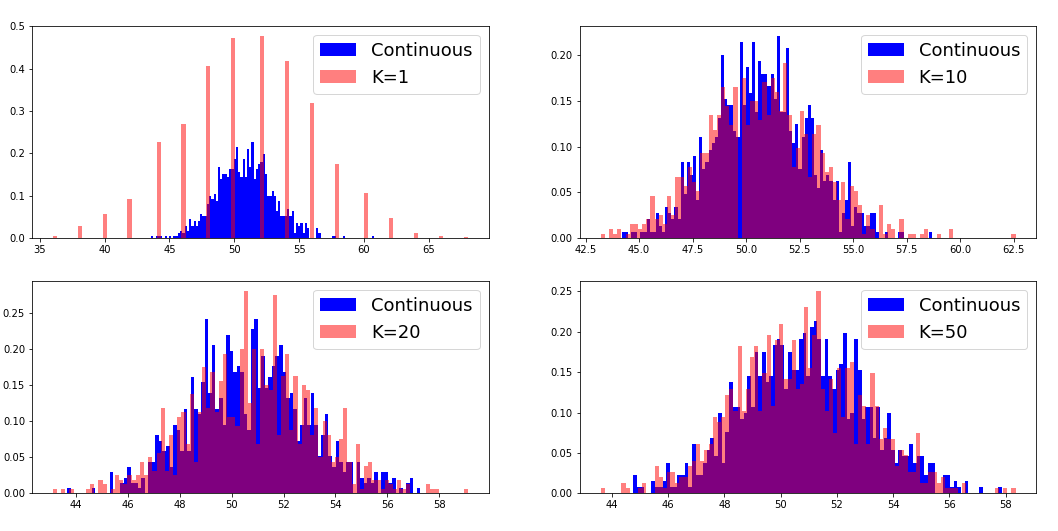

Note that in view of and since is negative and positive, there exists a small enough such that the control is in , see Appendix C for details. We assume that we are considering such time horizon here. We also note that and as consequence of Grönwall Lemma converges to when goes to . Consequently we get the convergence of the value of the control problems, . Moreover a direct adaption of the proof of Proposition 1 gives the convergence in law of the optimally controlled population:

Those convergences are illustrated in Figures 1 and 2 respectively.

.

4 Convergence of BSDEs

In this section we prove the main results of this paper. We recall a convergence result of a sequence of martingale representations given in [PPS19]. Then we extend it to the convergence of a sequence of BSDEs driven by the sequence of martingales .

4.1 Convergence of martingale representations

From Theorem 2 in [Dav76] we know any martingale has the representation property with respect to (in the sense of Definition III-4.22 in [JS13]). Moreover we prove in Appendix E that any martingale has the representation property relative to .

For any we consider an -measurable real random variable and an -measurable real random variable. We define the closed martingale by , a.s.. Since is an -martingale and , we know that there exists a unique process such that

Similarly considering the -martingale defined by , since we have existence and uniqueness of such that

We have the following result as a mere extension of [PPS19, Theorem 3.3].

Proposition 2 (martingale representations convergence).

If the sequence and are in and converges towards in for then

in for any .

Compared to Theorem 5 in [BDM02] or Theorem 3.3 [PPS19] we have assumed that the convergence of takes place in instead in . This is in order to extend the convergence of beyond . Indeed if we only assume that , is not squared integrable a priori. In [BDM02] the authors do not face this issue since they assume that the brackets of the martingales they consider are bounded, see Hypothesis . In our framework the sequence is not bounded in general. However, if we instead consider a sequence of models with a bounded population then would be bounded and we could get the same result assuming only the convergence of in only.

4.2 Convergence of BSDEs

We now extend the previous result to convergence of a sequence of BSDEs driven by .

For any we consider an random variable and two continuous functions and from into . We write for

Note that in the above equation, we implicitly use the decomposition . We will always assume such convention when we are dealing with a pair of elements such that one element of the pair is related to the birth in the population and the other is related to the death.

We introduce the BSDE with generator and terminal value by setting

Definition 1.

A solution to BSDE is a pair of processes such that the relation holds

As a consequence of Theorem 3.4 in [CF13] we have the following result.

Lemma 1.

Assume that

-

(i)

,

-

(ii)

there exists a positive constant such that and for any and we have for

-

(iii)

for ,

then the BSDE has a unique solution .

We also introduce a class of BSDE driven by the martingale . For an real valued random variable and a continuous function from into we consider the BSDE

Definition 2.

A solution to BSDE is a pair of processes such that the relation holds

We get the following result on existence and uniqueness of solution to which is a consequence of Theorem 6.1 in [EKH97] or Theorem 2.1 in [CFS08].

Lemma 2.

Assume that

-

(i)

,

-

(ii)

there exists a positive constant such that and for any we have:

-

(iii)

,

then the BSDE has a unique solution .

We are interested in the convergence of the solutions to when and converge. Therefore we make the following converging assumptions on the drivers of the BSDEs .

Assumption 2.

-

(i)

The sequence converges towards in for ,

-

(ii)

there exists a positive constant such that for any , and

-

(iii)

there exists a pair of continuous functions from and a positive sequence converging towards such that for any , and we have for :

Remark 2.

For any we consider the unique solution of . We have the following convergence result for the sequence whose proof is given in Section 6.2.

Theorem 2.

5 Application to a control problem

In this section we apply the results of Section 4 to the convergence of a sequence of controls problems.

5.1 The discrete problem

We first focus on the discrete control problem in the same spirit than Section 3. We consider that a resource manager monitors his harvesting intensity through a control , which is assumed to be bounded with bounds . We assume that his harvesting modifies the death rate of the natural resource according to a continuous function which satisfies the following assumption.

Assumption 3.

There exists a positive constant such that for any

with equality if .

The set of admissible controls is defined by

For any we define

where denotes the Doleans-Dade exponential process. We deduce from Assumption 3, Proposition 1 together with [Sok13, Corollary 2.6] that is a true martingale. Hence the law of the population process under the control is given by characterized by

Under the probability the death intensity of the population becomes

and the birth intensity is unchanged.

We assume that the manager receives at maturity a lump sum random compensation for his action. In addition, the manager receives continuous incomes along the time depending on the size of the population and on his control that is given by a function from into . This gain can be negative which corresponds to a cost related to the effort of the manager. This is what we have considered in Section 3. Therefore, the goal of the manager is to solve the following maximization problem

where denotes the expectation taken under the probability . Using the notations of Section 4.2 the BSDE associated to this control problem is

with for any

We need to assume that the functions and are chosen such that satisfies the assumptions (ii) and (iii) of Lemma 1 and that the maximizer in the above equation is unique. Formally we make the following assumption.

Assumption 4.

-

(i)

,

-

(ii)

there exists a positive satisfying and such that for any and we have

-

(iii)

For any there exists a unique such that

We thus have the following characterization of the optimal control (we refer to Appendix 6.3 for the proof).

Theorem 3 (Verification for ).

Let be the unique solution of . Then and solves the problem .

We now define the continuous version of this control problem.

5.2 The continuous problem

As previously the resource manager monitors his harvesting intensity through a control , assumed to be bounded with bounds . We assume that his harvesting modified the death rate of the natural resource according to a continuous function which is assumed to satisfy the following assumption.

Assumption 5.

There exists a positive constant such that for any

with equality if .

The set of admissible control is

Considering the process

where we recall that is given by . We deduce from Assumption 5 and Corollary 2.6 in [Sok13] that is a true martingale. Hence, we define the probability by

which is the probability measure corresponding to the control . Under the process is a strong solution of

where is a Brownian motion.

As in the discrete case we assume that the manager receives at maturity a lump sum random compensation for his action. In addition, the manager receives continuous incomes term depending on the size of the population and his control. This term is given by a function from into . Therefore, the goal of the manager is to solve the following maximization problem

where denotes the expectation taken under the probability . The BSDE associated to this control problem is

with for any

We need to assume that the functions and are chosen such that satisfies the assumptions (ii) and (iii) of Lemma 2 and that the maximizer in the above equation is unique. Formally we make the following assumption.

Assumption 6.

-

(i)

,

-

(ii)

there exists a positive satisfying such that for any and we have

-

(iii)

For any there exists a unique such that

We thus have the following characterization of the optimal control (we refer to Appendix 6.4 for the proof).

Theorem 4 (Verification for (P)).

Let be the unique solution of (BSDE). Then and solves the problem (P).

5.3 Convergence of the value functions and of the optimal controls

In this section, we show that under some natural assumptions the sequences of value functions and of controls converge respectively towards and . More precisely we consider the following assumptions.

Assumption 7.

-

(i)

converges to in for some ,

-

(ii)

there exists a positive sequence that converges towards such that for any and we have

and

-

(iii)

There exists a positive constant such that for any and we have

and for any and we have

Assumption 7 contains the natural assumptions ensuring that the problem is the version of the problems in the framework of the continuous population model .

Using a slight abuse we note the law of under the control and the law of under the control . We have the following convergence result which proof is given in Appendix 6.5.

Theorem 5.

-

(i)

We have in :

-

(ii)

The sequence converges for the Skorohod topology towards .

Since and a consequence of Theorem 5 (i) is that converges towards . The point (i) also implies that the sequence of controls converges towards the control . But this convergence is in a weak sense and we do not get the convergence of towards in law for the Skorohod topology.

6 Proofs of Theorems

6.1 Proof of Theorem 1

We introduce the process

The proof is divided in four main steps detailed below.

-

1.

We prove that admits a unique strong solution.

-

2.

We show that the sequence is C-tight.

-

3.

We show that for any limit point of the above sequence we have and is almost surely differentiable with derivative weak solution of .

-

4.

Finally, we prove that up to a probability space such that the above convergence holds in probability, the process actually converges to when goes to in .

Step 1: Pathwise uniqueness under existence.

The uniqueness result is a direct consequence of [RY13, IX-Theorem 3.5 (ii)] under Assumption .

Step 2: Tightness property.

In order to show tightness we first show that the sequence is bounded uniformly with respect to . We have

Hence, according to , there exists a positive constant (independent of ) such that

By using Grönwall’s inequality we deduce that is bounded uniformly with respect to .

We have

therefore is bounded and since then is also bounded. Moreover since the sequence bounded. Using Theorem VI-3.21 in [JS13] and that the processes , and for are nondecreasing for any we get that the sequences , , , and are tight.

Moreover since for and the processes , and are continuous for any following Proposition VI-3.26 in [JS13] we get that the sequences , , , and C-are tight.

The tightness of then follows from Theorem VI-4.13 in [JS13] since . We then get C-tightness since . Since marginal tightness implies tightness (Corollary IV-3.33 in [Jac75]) we get that is C-tight.

Step 3: convergence of the processes and existence of a solution to

We first show the following lemma:

Lemma 3.

For the process converges uniformly towards in probability.

Proof of Lemma 3.

Obviously we have so using the BDG inequality we have

that converges towards . We conclude using Markov inequality. ∎

In view of the tightness result obtained in Step 1, we denote by a limit point of with . By the Skorohod representation theorem since the limit of each marginal is continuous we can consider that converges almost surely and uniformly on towards , i.e.

and for any

According to Corollary IX-1.19 in [JS13] we have that is a local martingales. Moreover we have and so Corollary VI-6.29 in [JS13] gives and . Since is a continuous martingale we get

We also notice that is uniformly bounded in , so according to Fatou’s lemma is integrable, therefore is a true martingale.

We recall that

Then, converges almost surely and uniformly on towards

and converges almost surely uniformly on towards

Since we have

we get from Theorem V-3.9 in [RY13] that there exists a bi-dimensional Brownian motion such that

So finally we have shown that

This concludes the proof of the first part of Theorem 1 since converges in law for the Skorohod topology to .

Step 4: convergence of a copy in .

In view of the conclusion of Step 3, and by the Skorohod representation theorem, there exists a probability space and a copy in law of the sequence of processes that converges in probability toward a copy of when goes to . To prove that the convergence actually holds in we show that:

-

and are bounded in ,

-

and are bounded in ,

-

is bounded in ,

-

is bounded in .

Then we will get the convergence using dominated convergence.

Proof of . We write

Therefore we have for a positive constant independent of such that

Hence to conclude it is enough to show that is bounded. We have

So we get

Therefore by Proposition 1 and Grönwall lemma we get point (i) (since the same results follows for ).

Proof of . Using the Burkholder-Davis-Gundy inequality we get

Therefore because of point we get point . Same proof holds for .

Proof of . We write

So we have

taking the supremum over and then the expectation we obtain point as corollary of Proposition 1 and point .

6.2 Proof of Theorem 2.

We proceed in steps:

-

(i)

We show that there exists and some contracting functions and such that for any , the unique solution of is the fixed point of and the fixed point of is solution to .

-

(ii)

We introduce a double indexed sequence and prove a convergence result by induction.

-

(iii)

We conclude.

6.2.1 Step

For any we define the function

where is the unique solution of the BSDE:

Since and because of assumptions (ii) and (iii) in Lemma 1 we have . So we can properly define

and is the unique process in satisfying

Consider two pairs , and noting (resp. ). Using Ito’s formula on between and we get

Taking the expectation we get

Therefore using the assumptions of Lemma 1 together with Young’s inequality we get for any positive and that

or equivalently

Inspired by the proof of Theorem 3.4 in [CF13] we choose and such that

We can make such choice since . Therefore we obtain

Therefore for any the function is an contraction on for the norm equivalent to and defined by

In the continuous case we consider

where is the unique solution of the BSDE:

Since and because of Remark 2 we have . So we can properly define

and is the unique process in satisfying

Similarly we obtain that is an contraction for the equivalent norm on :

6.2.2 Step

For any we define the sequence satisfying

We similarly consider the sequence defined by

Since for any , is a contraction. For any the sequence converges towards in . In the same way converges towards in .

We use the following notation:

So that we can write:

| (3) |

and

| (4) |

We prove by induction that the following convergence holds for any :

in where .

Obviously the result holds for . We assume that the converge holds for and show that it implies the convergence for .

6.2.3 Step

Note that a consequence of Step is that for a certain positive constant we have

| (5) |

We write

Notice that according to the BDG inequality there exists a positive constant such that for any

which converges towards uniformly in when by Equation (5). Hence converges in towards .

Similarly we write

We proved in the previous section that the last term goes to when . Remark that we have

so using Jensen and Doob’s inequality we get

Therefore goes to when . In the same way we get that goes to when . So converges towards .

Finally notice that,

So the convergence

in follows from Proposition 2 in [BDM02] and from the convergence of in towards .

6.2.4 Convergence of towards

To prove the convergence we first prove that converges towards in probability for the uniform topology. Then we show that is bounded in where . We conclude by dominated convergence.

For any we note . We write

where for , we recall that ,

For the sequence obviously converges to in probability by almost sure convergence as goes to infinity.

The sequence converges towards in probability for the Skorohod topology and satisfy the P-UT condition by Proposition VI-6.12 in [JS13]. So for any , converges towards in probability (for the Skorohod topology) as a consequence of Theorem VI-6.22 in [JS13].

For the second term we write

So by assumptions of Lemma 1 and Assumption 2 we get:

Thus there exits

which obviously goes to in probability when according to Slutsky’s theorem, in view of the induction hypothesis and since goes to .

Finally we write:

So we have

Taking the average and going to the upper limit in we get by induction hypothesis and from Theorem VI-6.22 in [JS13] that

The RHS converges to when by dominated convergence. Hence we have shown that converges to in probability for the uniform convergence.

To conclude we show that is bounded in . We write

Using Kunita-Watanabe it is easy to see that the last term is bounded in . The other terms are bounded in by induction assumption and Proposition 1. So is bounded in . In the same way we show that . Therefore we obtain the convergence of towards in by dominated convergence.

6.3 Proof of Theorem 3

From Assumption 4 (i)-(ii) we get that the generator satisfies the conditions of Lemma 1. Therefore admits a unique solution . We consider , and show that solve the optimal control problem . Since is admissible according to Assumption 4 (iii) we have .

We now take any and show that

We write:

By definition the first integrand term is almost surely non negative and therefore we have

or equivalently

Taking the expectation with respect to we get the result.

6.4 Proof of Theorem 4

From Assumption 6 (i)-(ii) we get that the generator satisfies the conditions of Lemma 2. Therefore admits a unique solution . We consider , and show that solve the optimal control problem . Since is admissible according to Assumption 6 (iii) we have .

We now take any and show that

We write:

By definition the first integrand term is almost surely non negative and therefore we have

or equivalently

Taking the expectation with respect to we get the result.

6.5 Proof of Theorem 5

According to Assumption 7 the sequences and satisfy the assumptions of Lemma 4 for any and Assumption 2. So from Theorem 2 we have in

| (6) |

6.5.1 Proof of point (i)

We write

The second term converges towards by Theorem 1. The last one terms goes to from Assumption 7 (ii). Using Assumption 7 (iii) we can dominate the first term by

that goes to according to Theorem 1 and to the convergence (6).

In the same way, using that the control is bounded, we get that in probability

We then extend the convergences to by uniform integrability since the control is bounded. Thus we get the first statement of Theorem 5.

6.5.2 Proof of point (ii)

We consider and a bounded continuous function defined from into . We show that

where (resp. ) denotes the expectation under the control (resp. ). We write

and

Suppose we have shown that converges in probability surely towards . Then writing

we get that converges towards in by dominated converges and since

Then we conclude noticing that:

We finally prove the convergence of towards in probability. We introduce the following sequences

and show that they all converges to in probability.

For some independent of we have

The first term of the RHS converges towards in probability according to Markov inequality. The second one since converges almost surely towards from Assumption 7-(i). Remark that

Consequently using Assumption 7 (iii) and Tchebychev inequality we get that converges towards in probability. Notice that we have

The second and last terms go to in probability by Theorem 1, Assumption 7 (ii) and from Proposition VI-6.12 and Theorem VI-6.22 in [JS13]. As we did in the proof of Theorem 5 (i), the first term goes to from Cauchy Schwarz inequality Assumption 7 (iii) together with the convergence (6).

Finally we write

The second and last terms converge towards by Assumption 7 (ii), Theorem 1, Proposition VI-6.12, Theorem VI-6.22 in [JS13] and Theorem 5. Using Ito’s isometry, Cauch-Schwarz inequality, Assumption 7 (iii) together with Theorem 1 and Theorem 5 (i) we get that the first term goes to in probability. Therefore converges towards in probability.

Thus we conclude that converges toward in probability.

Appendix A Spaces and notations

-

•

the set of real valued random variable such that

-

•

is the set of -predictable valued process such that

-

•

For any we consider the sets:

-

–

is the set of predictable process valued such that

-

–

is the set of measurable valued random variable such that

-

–

is the set of -optional valued process such that

-

–

is the set of -predictable valued process such that

-

–

is the set of -predictable valued process such that

-

–

is the set of pair , we note .

-

–

-

•

We also consider the sets related to the continuous model:

-

–

is the set of predictable process valued such that

-

–

is the set of measurable valued random variable such that

-

–

is the set of -optional valued process such that

-

–

is the set of -predictable valued process such that

-

–

is the set of pair , we note .

-

–

-

•

Finally we consider the sets:

-

–

the set of real valued random variable such that

-

–

is the set of -predictable valued process such that

-

–

Appendix B Change of measure for initial population

We consider and and define the process

We have and therefore . Moreover from Assumption 1 we have for some constant positive

where is the lowest positive value that the process can take. Therefore by Theorem 2.4 in [Sok13] the process is a uniformly integrable martingale.

Moreover according to Theorem III-3.11 in [JS13] under the probability for the processes

are local martingales. Finally we conclude since

Appendix C Admissibility of the controls in the toy model

C.1 Discrete models

We show that the control is admissible. We have

By [Jac75] the probability exists. We recall that we have chosen small enough such that is negative and positive on . Hence we have

We can always assume that is small enough so that we can assume that for any , . So is almost surely non negative and the control is admissible.

C.2 Continuous models

We have

So the SDE

writes

Obviously this SDE admits a unique strong solution given by where is the unique strong solution of

Appendix D Feller property of the model

We consider a non negative real . We obviously have that when the converges almost surely towards . Now we consider a non negative sequence that converges towards and show that for any , converges in law towards . We fix larger than and any of the and a bounded continuous function on .

We write

and

The first term of the right hand side (RHS for short) goes to by dominated convergence. We can dominate the second on by

that converges towards according to Scheffé’s lemma. Therefore our model has the Feller property.

Appendix E Martingale representation with respect to

We show in this section that any martingale has the representation property relative to .

We set and , i.e. the probability measure on such that that . For a càdlàg process adapted to the filtration and and two -predictable processes with finite variation such that we recall the definition of the martingale problem associated with and (, , ).

Definition 3 (Definition III-2.6 in [JS13]).

A solution to the martingale problem associated with and is a probability measure on such that

-

•

the restriction of to equals ,

-

•

is a semi-martingale on with characteristics .

We denote by the set of solutions to this martingale problem.

From this definition we see that the projection of on is a solution of where

We have so that is a -adapted process and it makes sense to consider the set . We show that

| (7) |

and that is reduced to a singleton. This will be enough to conclude according to Theorem III-4.29 in [JS13].

Consider . We have and since and are continuous process with finite variation, we deduce that under the characteristics of are . Conversely, if then by recalling that we obtain . Hence, (7) holds.

Since admits a unique strong solution it admits a unique solution in law (see Theorem IX-1.7 [RY13]). Therefore from Theorem III-2.26 in [JS13] the set is reduced to a singleton. As a consequence of (7), the set is also reduced to a singleton. Therefore, we deduce from Theorem III-4.29 that all -martingales have the representation property relative to .

Appendix F Proof of Proposition 1

For two non negative reals and we say that is a linear branching process with birth rate and intensity if it can be written as where and are two counting processes with respective intensity and . This corresponds to a branching process as defined in Section III-3.3.1 in [Mél16] with parameters , and .

To prove Proposition 1 we proceed in two steps:

-

•

Step 1: We prove a result similar to Proposition 1 for linear branching process.

-

•

Step 2: We show that a under some assumption a population processes is almost surely dominated by a linear branching process.

-

•

Step 3: We conclude using the previous steps.

F.1 Step 1: exponential moments for linear branching processes

We consider a linear branching process with birth and death rate given by and .

We define the function from into by

where is the expectation taker under the probability law that corresponds to initial condition population of size . We have the following lemma:

Lemma 4.

For any consider

With those notations if satisfies we have for any

Note that since satisfies the above conditions, they also hold for and small enough.

Proof of Lemma 4.

Consider a population starting with one individual. We call the lifetime of this particle and or the size his offspring. Since all particles are independent and follow the same law we can consider that:

| (8) |

where are independent copies of .

Consider the stopping times

From Equation (8) we get

and taking the average we have

where . We therefore consider the following ODE:

We show that has a unique maximal solution defined on by

Using the change of variable , the ODE is equivalent to

By Cauchy-Lispchitz theorem this ODE admits a maximal solution . By hypothesis on we have

So for all such that we can write

| (9) |

We recognize the derivative of

So integrating on both sides of (9) we have

Therefore it is then easy to show that for any we have

Reciprocally it is easy to show that this function is a maximal solution of defined on .

The function being continuous a direct application of the Grönwall lemma gives that for any , . By monotone convergence we obtain that is finite and taking the average in Equation (8) we obtain that is solution of therefore we have

.

Finally if we consider a population starting with individual we can consider that

where are independent copies of the branching process starting with one individuals. Therefore for we get which concludes the proof. ∎

We now consider a sequence of branching process with initial condition and parameters

We consider such that and note

We assume that and satisfy . Those conditions imply that for large enough satisfies the assumption in Lemma 4.

To lighten the notations we use the under-script instead of . One can easily show the following convergence or equivalence:

| (10) |

| (11) |

The convergence of the sequence implies that for any and large enough is finite. Moreover from (10) and (11) we get that the sequence converges. More precisely it is easy to check that for any we have

where

Therefore we deduce that there exists , and such that for any we have

| (12) |

F.2 Step 2: domination of by linear process

We begin by showing the following lemma.

Lemma 5.

Consider two functions and from into such that

We consider two counting processes and with respective intensity and where . Then up to an extension of the probability space there exists a linear branching process with birth rate and death rate .

Proof of Lemma 5.

We proceed by thinning. We consider a multivariate point process with values in and let be its corresponding random measure. For any we define:

For and we note and

We set where . The measure is defined by:

where are Bernoulli random variable with parameters

For existence of the process see [Jac75]. Basically we get that the when there is an event either jump. If has jumped, then may jump or not and If has jumped, then may jump or not. So almost surely we have . According to Proposition 1. in [Oga81] for any the process is a counting process with intensity . This concludes the proof of the Lemma. ∎

F.3 Step 3: conclusion

As consequence of Lemma 5 for any up to an extension of the probability space we can consider that there exists a branching process with birth and death rate given by

that dominates almost surely. So according to Equation (12) in Step 2, there exists some positive constants , and such that for any

This conclude the proof of the proposition.

Acknowledgment:

The authors are gratefully thankful to Vincent Bansaye, Mathieu Rosenbaum, Sylvie Méléard, Dylan Possamaï and Nizar Touzi for many interesting discussions. The authors gratefully acknowledge the financial supports of the ERC Grant 679836 Staqamof, the Chaires Analytics and Models for Regulation and Financial Risk.

References

- [BBF93] Marino Belloni, Giuseppe Buttazzo, and Lorenzo Freddi. Completion by Gamma-convergence for optimal control problems. In Annales de la Faculté des sciences de Toulouse: Mathématiques, volume 2, pages 149–162, 1993.

- [BDM82] Giuseppe Buttazzo and Gianni Dal Maso. -convergence and optimal control problems. Journal of optimization theory and applications, 38(3):385–407, 1982.

- [BDM01] Philippe Briand, Bernard Delyon and Jean Mémin. Donsker-type theorem for BSDEs. Electronic Communications in Probability, 6(1):1–14, 2001.

- [BDM02] Philippe Briand, Bernard Delyon, and Jean Mémin. On the robustness of backward stochastic differential equations. Stochastic Processes and their Applications, 97(2):229–253, 2002.

- [BM15] Vincent Bansaye and Sylvie Méléard. Stochastic models for structured populations. Springer, 2015.

- [Cla18] Julien Claisse. Optimal control of branching diffusion processes: a finite horizon problem. The Annals of Applied Probability, 28(1):1–34, 2018.

- [CF13] Fulvia Confortola and Marco Fuhrman. Backward stochastic differential equations and optimal control of marked point processes. SIAM Journal on Control and Optimization, 51(5):3592–3623, 2013.

- [CFS08] Raffaella Carbone, Benedetta Ferrario, and Marina Santacroce. Backward stochastic differential equations driven by càdlàg martingales. Theory of Probability & its Applications, 52(2):304–314, 2008.

- [CK86] Colin W Clark and Geoffrey P Kirkwood. On uncertain renewable resource stocks: optimal harvest policies and the value of stock surveys. Journal of Environmental Economics and Management, 13(3):235–244, 1986.

- [CMS01] François Coquet, Jean Mémin, and Leszek Słominski. On weak convergence of filtrations. Séminaire de probabilités de Strasbourg, 35: 306–328, 2001.

- [Dav76] Mark HA Davis. The representation of martingales of jump processes. SIAM Journal on control and optimization, 14(4):623–638, 1976.

- [DeLD08] Michel De Lara and Luc Doyen, Sustainable management of natural resources: mathematical models and methods Springer Science & Business Media, Springer, 2008.

- [DM80] Claude Dellacherie and Paul-André Meyer. Probabilités et potentiel, chap. V-VIII., Hermann, Paris, 1980.

- [DM12] Gianni Dal Maso. An introduction to -convergence, volume 8. Springer Science, Business Media, 2012.

- [Don51] Monroe D Donsker. An invariance principle for certain probability limit theorems. Mem. Amer. Math. Soc. volume 6, 1951.

- [EHS15] Steven N Evans, Alexandru Hening, and Sebastian J Schreiber. Protected polymorphisms and evolutionary stability of patch-selection strategies in stochastic environments. Journal of mathematical biology, 71(2):325–359, 2015.

- [EKH97] Nicole El Karoui and Shaojuan Huang. A general result of existence and uniqueness of backward stochastic differential equations. Pitman Research Notes in Mathematics Series, pages 27–38, 1997.

- [Get75] Wayne M Getz. Optimal control of a birth-and-death process population model. Mathematical Biosciences, 23(1-2):87–111, 1975.

- [Jac75] Jean Jacod. Multivariate point processes: predictable projection, Radon-Nikodym derivatives, representation of martingales. Probability Theory and Related Fields, 31(3):235–253, 1975.

- [JS13] Jean Jacod and Albert Shiryaev. Limit theorems for stochastic processes, volume 288. Springer Science & Business Media, 2013.

- [LKLV18] Thomas Lim, Idris Kharroubi, and Vathana Ly-Vath. Optimal exploitation of a resource with stochastic population dynamics and delayed renewal. arXiv preprint arXiv:1807.04160, 2018.

- [MBHS78] Robert M May, John R Beddington, Joseph W Horwood, and James G Shepherd. Exploiting natural populations in an uncertain world. Mathematical Biosciences, 42(3-4):219–252, 1978.

- [Mél16] Sylvie Méléard. Modèles Aléatoires en Ecologie et Evolution. Springer, 2016.

- [Oga81] Yosihiko Ogata. On Lewis’ simulation method for point processes. IEEE Transactions on Information Theory, 27(1):23–31, 1981.

- [Par99a] Etienne Pardoux. BSDEs, weak convergence and homogenization of semilinear PDEs. Non linear analysis, differential equations and control. NATO Sci.Ser.C Math.Phys.Sci., 528, Kluwer Acad.Publ., 503–549, 1999.

- [Par99b] Etienne Pardoux. Homogenization of Linear and Semilinear Second Order Parabolic PDEs with Periodic Coefficients: A Probabilistic Approach. Journal of Functional Analysis, 167(2):498–520, 1999.

- [PPS18] Antonis Papapantoleon, Dylan Possamaï and Alexandros Saplaouras. Existence and uniqueness results for BSDE with jumps: the whole nine yards. Electronic Journal of Probability, 23(121), 2018.

- [PPS19] Antonis Papapantoleon, Dylan Possamaï and Alexandros Saplaouras. Stability results for martingale representations: The general case. Trans. Amer. Math. Soc., 372: 5891-5946, 2019.

- [Ree79] William J Reed. Optimal escapement levels in stochastic and deterministic harvesting models. Journal of environmental economics and management, 6(4):350–363, 1979.

- [RDeL15] Esther Regnier and Michel De Lara. Robust viable analysis of a harvested ecosystem model, Environmental Modeling &Assessment, 20(6):687–698, 2015.

- [RY13] Daniel Revuz and Marc Yor. Continuous martingales and Brownian motion, volume 293. Springer Science & Business Media, 2013.

- [Sap03] Jean-Daniel Saphores. Harvesting a renewable resource under uncertainty. Journal of Economic Dynamics and Control, 28(3):509–529, 2003.

- [Sap17] Alexandros Saplaouras. Backward stochastic differential equations with jumps are stable. PhD thesis, Technische Universität Berlin, 2017.

- [Sok13] Alexander Sokol. Optimal Novikov-type criteria for local martingales with jumps. Electronic Communications in Probability, 18(39), 2013.

- [TD19] Eric Tromeur and Luc Doyen. Optimal harvesting policies threaten biodiversity in mixed fisheries, Environmental Modeling & Assessment, 24(4):387–403, 2019