\pkgsalmon: A Symbolic Linear Regression Package for \proglangPython

Alex Boyd, Dennis L. Sun \Plaintitlesalmon: A Symbolic Linear Modeling Package for Python \Shorttitle\pkgsalmon: A Linear Modeling Package \Abstract

One of the most attractive features of \proglangR is

its linear modeling capabilities. We describe a

\proglangPython package, \pkgsalmon, that brings the

best of \proglangR’s linear modeling functionality

to \proglangPython in a Pythonic way—by providing

composable objects for specifying and fitting linear

models. This object-oriented design also enables other

features that enhance ease-of-use, such as

automatic visualizations and intelligent model building.

\Keywordslinear regression, linear model, visualization, model building, \proglangPython

\Plainkeywordslinear regression, linear model, Python \Address

Dennis Sun

Department of Statistics

California Polytechnic State University

1 Grand Ave

San Luis Obispo, CA 93407

E-mail:

URL: http://dlsun.github.io/

1 Introduction

Linear models are ubiquitous in statistics, science, engineering, and machine learning. A linear model assumes that the expected value of a response variable is a linear function of explanatory variables, :

| (1) |

for coefficients . Model (1) is more flexible and general than it may first appear. For example, linear models do not necessarily have to be linear in the original explanatory variables. If we add higher-order polynomial terms to a linear model, then we can also model non-linear effects:

| (2) |

How are linear models used? First, they can be used for description. For example, we may want to emphasize trends in a scatterplot by superimposing a best-fit line on the points. Second, they may be used for prediction. Once the coefficients have been estimated, the linear model can be used to predict the value of the response for a new observation where only the explanatory variables are known. Finally, linear regression can be used for inference. The coefficients may encode information about nature, such as the causal effect of one variable on another, in which case we need hypothesis tests and confidence intervals for model parameters.

Because of these different use cases, several solutions for fitting linear models have emerged. Figure 1 illustrates the tradeoffs. At one extreme are point-and-click software packages, like \proglangJMP (jmp) and \proglangMinitab (minitab), which fit linear models and provide automatic visualizations. Although these packages have much built-in functionality, they are not easily extensible. For example, complicated data cleaning and wrangling often have to be done outside these software packages.

At the other extreme are programming languages for scientific computing, like \proglangMATLAB (matlab) and \proglangPython (python). To fit a linear model, users have to manually construct the matrices to be passed to a least-squares solver. To obtain predictions from the fitted model, users must implement the matrix multiplications. Although these environments can be powerful, users have to keep track of low-level details that distract from the modeling.

Libraries within these languages ease the burden somewhat. For example, \pkgscikit-learn is a \proglangPython library for machine learning that provides a consistent API for specifying, fitting, and predicting using a linear regression model. (pedregosa2011scikit) However, it provides little help with the other two uses of linear regression, description and inference, offering neither visualizations nor uncertainty estimates. Also, the \codeLinearRegression model in \pkgscikit-learn assumes that the explanatory variables have already been transformed into the numerical matrix that will be passed into a least-squares solver, so users must manually transform the variables or else define the transformations as part of the model.

R occupies a medium between the two extremes. (R) On the one hand, it is a full-fledged programming language. On the other, it provides a high-level API for specifying and fitting linear regression models through formulas and the \codelm function. For example, model (2) could be specified and fit in \proglangR as

{CodeInput}lm(y poly(x1, 3) + x2, data)

Although \proglangR provides automatic diagnostic plots, it offers limited visualizations of the fitted model, in comparison with point-and-click software packages such as \proglangJMP and \proglangMinitab.

Patsy (patsy) and \pkgstatsmodels (seabold2010statsmodels) are \proglangPython libraries that port \proglangR-style modeling to \proglangPython. Like \proglangR, \pkgstatsmodels provides some automatic diagnostic plots but not visualizations of the fitted model. However, \proglangR formula syntax is not interpretable by \proglangPython, so formulas have to be specified as strings:

{CodeInput}smf.ols("y poly(x1, 3) + x2", data)

This creates problems when the column names do not meet the language’s rules for variable names. For example, columns with names such as \code"weight.in.kg" or \code"person’s height" would need to be wrapped in Patsy’s “quote” object, \codeQ:

{CodeInput}smf.ols("y Q(’weight.in.kg’) + Q(’personś height’)", data)

Because the \codeQ constructor takes a string as input, we have strings within strings—hence the need for two different kinds of string delimiters. If the variable name itself includes an apostrophe or a quotation mark, then that character needs to be escaped. An object-oriented approach to model specification, described in this paper, avoids these complications, allowing any object that is a valid column name in a \pkgpandas \codeDataFrame to be used directly in the model specification, without requiring a workaround for problematic variable names. Furthermore, having objects associated with each variable in a model makes it easy to specify customization options for each variable (e.g., the baseline level for a categorical variable).

In this paper, we describe \pkgsalmon, a \proglangPython package for linear regression that offers an object-oriented interface for specifying linear models. The two main contributions of \pkgsalmon are:

-

1.

providing an \proglangR-like (but Pythonic) API for specifying models,

-

2.

producing appropriate visualizations of the models, bridging the gap with point-and-click packages, like \proglangJMP and \proglangMinitab.

Its philosophy and design is similar to other statistical packages in \proglangPython, such as \pkgSymbulate (ross2019symbulate). Throughout, we provide comparisons of model specification in \pkgsalmon with the similar formula syntax of \pkgR.

The easiest way to obtain \pkgsalmon is to install it via \codepip: {CodeInput} pip install salmon-lm but it can also be installed from source at http://github.com/ajboyd2/salmon.

2 Model building and fitting

We introduce the design and syntax of \pkgsalmon by way of a case study. We assume that all \pkgsalmon objects and methods have already been imported into the global namespace, as follows:

from salmon import Q, C, Log, Poly, LinearModel

We will use a sampled version of the Ames housing data set (de2011ames), which can be found within the repository for the package. The first five rows of this sampled data set are shown in Table 1.

| Neighborhood | Price($) | Style | Sq. Ft. | Fire? | |

|---|---|---|---|---|---|

| 0 | SawyerW | 162000 | 2 Story | 1400 | No |

| 1 | CollgCr | 195000 | 2 Story | 1660 | No |

| 2 | Crawfor | 164000 | Other | 1646 | Yes |

| 3 | NridgHt | 417500 | 1 Story | 2464 | Yes |

| 4 | SawyerW | 186800 | 1 Story | 1400 | No |

We will start with the simplest possible model, which assumes the sale price is a linear function of just the square footage:

| (3) |

This simple linear regression model can be specified in \pkgsalmon as follows:

>>> x = Q("Sq. Ft.") >>> y = Q("Price() 1 + Sq. Ft.

Notice that a quantitative variable is specified by creating a \codeQuantitative object, or \codeQ for short, with the name of the column in the \codeDataFrame. Alternatively, we could have created a generic variable using \codeV and let \pkgsalmon infer the type. Either way, these variable objects become the explanatory (\codex) and response (\codey) components of a \codeLinearModel object.

An intercept is added by default, as evidenced by the constant term \code1 in the printout. To specify a model without an intercept, we could either insert \code- 1 into the expression (which mirrors the formula syntax of \proglangR) or specify \codeintercept=False:

>>> no_intercept_model = LinearModel(x - 1, y) >>> no_intercept_model = LinearModel(x, y, intercept=False) >>> print(no_intercept_model) Price(tpβ_j = 0xxα1 - αPrice($)log(Price($))p(Sq. Ft.)^2I(⋅)α

3 Model diagnostics

The previous section explained how to build regression models; this section focuses on how to evaluate them. There are both visual and analytical diagnostics; we only attempt to highlight a few examples of each. For a full description of the API, please refer to the online documentation.

In the following examples, we will check whether the assumptions are satisfied for model (9), \codefull_model, as well as compare it to model (8), \codequant_cat_model, which is a nested model. Both models were defined in Section 2.

3.0.1 Visual Diagnostics

In equation (1), we only made assumptions about the conditional expectation of the response , given the explanatory variables . However, statistical inferences for linear regression require assumptions about the entire conditional distribution, not just the expectation. Perhaps the easiest way to specify this conditional distribution is to write

| (10) |

where the error term is independent of and assumed to follow a distribution. One can easily verify that this model is a special case of (1).

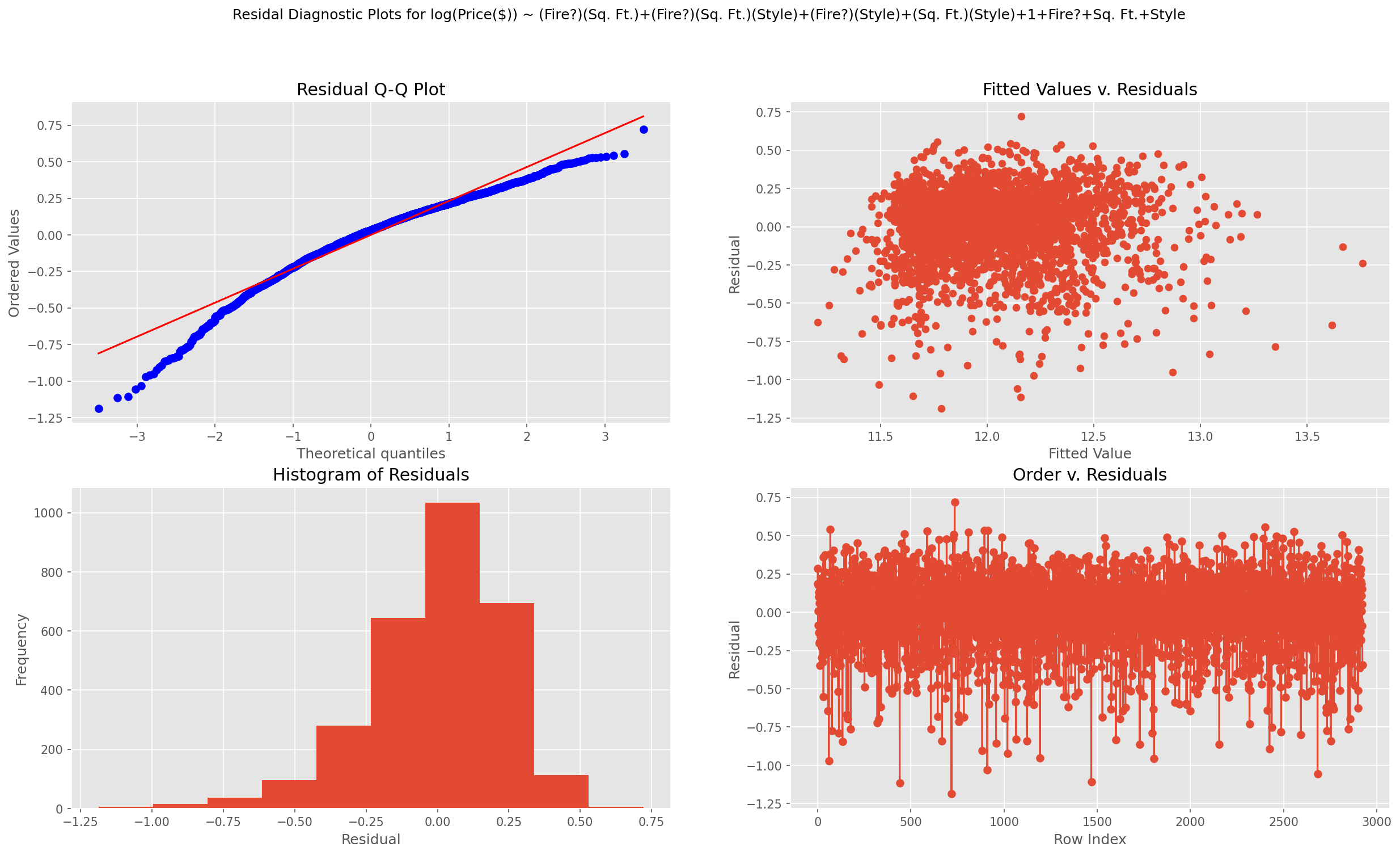

The assumption that the errors are independent and normally distributed with constant variance is usually assessed by inspecting the residuals. In \pkgsalmon, the residual diagnostic plots can be generated directly from the fitted model:

>>> full_model.plot_residual_diagnostics()

Four plots of the residuals are produced, as shown in Figure 11: a normal Q-Q plot, a histogram, a scatterplot of the fitted values versus the residuals, and a line plot of the residuals versus their order in the data set. The residuals appear to be skewed to the left, but otherwise there do not appear to be obvious violations of the assumptions. The line plot of the residuals versus their order is not as useful for this data set, since the row ordering is arbitrary, but it could potentially reveal violations of independence in data sets where row order is significant, such as time series data.

To further investigate assumptions, we can produce residual plots and partial regression plots by calling the methods \codemodel.residual_plots() and \codemodel.partial_plots() respectively. These will each produce one plot per explanatory variable.

3.0.2 Analytical Diagnostics

Visual diagnostics are in the eye of the beholder, so analytical diagnostics are equally important. One common, if not always the most useful, diagnostic of a model’s fit is the value.

>>> full_model.r_squared() 0.652748378553996

One problem with is that it is monotonically increasing in the number of variables in the model. A better diagnostic is Adjusted-, which accounts for the number of variables. To calculate Adjusted-, we specify the argument \codeadjusted=True. Besides , AIC and BIC are also available.

A more formal way of evaluating a model is to test it against another model. The \codeanova command, when called on a single model, returns the results of the omnibus -test, as well as the partial -test for the each individual variable in the model.

>>> from salmon import anova >>> anova(full_model)

| DF | SS Err. | SS Reg. | F | p | |

|---|---|---|---|---|---|

| Global Test | 11 | 309.578 | 309.578 | 500.765 | 0.000 |

| - (Style)(Sq. Ft.) | 2 | 169.819 | 303.415 | 54.828 | 4.2e-24 |

| - (Fire?)(Style) | 2 | 163.699 | 309.536 | 0.373 | 0.6883 |

| - Style | 2 | 166.776 | 306.458 | 27.755 | 1.1e-12 |

| - (Fire?)(Style)(Sq. Ft.) | 2 | 163.721 | 309.513 | 0.574 | 0.5630 |

| - Fire? | 1 | 163.731 | 309.503 | 1.333 | 0.2482 |

| - Sq. Ft. | 1 | 200.263 | 272.971 | 651.347 | 8e-130 |

| - (Fire?)(Sq. Ft.) | 1 | 163.796 | 309.438 | 2.477 | 0.1156 |

| Error | 2912 |

The inclusion of interactions between the quantitative variable (square footage) and the categorical variables (fireplace and house style) adds complexity to the model that may not be supported by the data. To test this, we can perform a partial -test comparing the full model to a reduced model without these interaction terms using the \codeanova command again, except passing in two fitted models. This mirrors the behavior of the \codeanova() function in \proglangR.

>>> anova(full_model, quant_cat_model)

| DF | SS Err. | SS Reg. | F | p | |

|---|---|---|---|---|---|

| Full Model | 11 | 163.657 | 309.578 | ||

| - Reduced Model | 5 | 179.015 | 294.219 | 54.655 | 2.0e-54 |

| Error | 2912 |

The results of the partial -test confirm that interactions significantly improve the fit of the model to the data.

4 Automatic model building

The \pkgsalmon package also provides functions to automate the model building process. In the following examples, we use \pkgsalmon to automatically select the “best” model, according to a metric of our choosing, from among the following variables: , , , , , plus interactions between all categorical and quantitative variables. The response variable in this scenario is .

To utilize the model building features of \pkgsalmon, we first specify a model that contains all of the variables under consideration:

>>> quant_vars = Poly(Cen(Q("Sq. Ft.")), 2) >>> all_terms_model = LinearModel( (1 + C("Style")) * (1 + C("Fire?")) * (1 + quant_vars), Log(Q("Price()) 1 + (Sq. Ft.-E(Sq. Ft.)) + (Sq. Ft.-E(Sq. Ft.))^2 + Fire? + (Fire?)(Sq. Ft.-E(Sq. Ft.)) + (Fire?)((Sq. Ft.-E(Sq. Ft.))^2) + Style + (Style)(Sq. Ft.-E(Sq. Ft.)) + (Style)((Sq. Ft.-E(Sq. Ft.))^2) + (Fire?)(Style) + (Fire?)(Style)(Sq. Ft.-E(Sq. Ft.)) + (Fire?)(Style)((Sq. Ft.-E(Sq. Ft.))^2)

Stepwise selection methods are supported through the \codestepwise function. Forward stepwise is specified by \codeforward=True, while backward stepwise is specified by \codeforward=False. Additionally, we specify what metric to optimize (e.g., AIC, BIC, ) using the \codemethod= parameter. For example, if we use forward stepwise to optimize for BIC, we obtain the following “best” model:

>>> from salmon import stepwise >>> results = stepwise( full_model=all_terms_model, metric