Semilinear hyperbolic stochastic partial differential equations (SPDEs) find widespread applications in the natural and engineering sciences. However, the traditional Gaussian setting may prove too restrictive, as phenomena in mathematical finance, porous media, and pollution models often exhibit noise of a different nature. To capture temporal discontinuities and accommodate heavy-tailed distributions, Hilbert space-valued Lévy processes or Lévy fields are employed as driving noise terms.

The numerical discretization of such SPDEs presents several challenges. The low regularity of the solution in space and time leads to slow convergence rates and instability in space/time discretization schemes. Furthermore, the Lévy process can take values in an infinite-dimensional Hilbert space, necessitating projections onto finite-dimensional subspaces at each discrete time point. Additionally, unbiased sampling from the resulting Lévy field may not be feasible.

In this study, we introduce a novel fully discrete approximation scheme that tackles these difficulties. Our main contribution is a discontinuous Galerkin scheme for spatial approximation, derived naturally from the weak formulation of the SPDE. We establish optimal convergence properties for this approach and combine it with a suitable time stepping scheme to prevent numerical oscillations. Furthermore, we approximate the driving noise process using truncated Karhunen-Loève expansions. This approximation yields a sum of scaled and uncorrelated one-dimensional Lévy processes, which can be simulated with controlled bias using Fourier inversion techniques.

Keywords: Numerical Analysis of SPDEs – Stochastic Transport Equation – Infinite-dimensional Lévy Processes – Discontinuous Galerkin Method

In many applications in the natural sciences and financial mathematics partial differential equations (PDEs) are utilized to model dynamics of the underlying system. Often, the dynamical systems are subject to uncertainties for instance due to noisy data, measurement errors or parameter uncertainty. A common approach to capture this behavior is to model the source of uncertainty by continuous Gaussian processes, which are analytically tractable and straightforward to simulate. It turns out, however, that Gaussian distributions notoriously underappreciate rare events, thus heavy-tailed, discontinuous Lévy-processes are better suited, i.e., to model stock returns, interest rate dynamics and energy forward markets ([1, 29]).

Furthermore, Gaussian random objects are unfit to capture the impact of spatial and temporal discontinuities, for example in flows through fractured porous media or composite materials, see e.g. [49].

However, replacing Gaussian distributions by more general random objects comes at the cost of lower regularity (both, path-wise and in a mean-square sense) and advanced sampling techniques are required.

In this article we consider semilinear first order stochastic partial equations (SPDEs) with a random source term. The noise is modeled by a space-time Lévy process taking values in a suitable infinite-dimensional Hilbert space . Existence and uniqueness of weak solutions to this type of equations is ensured but in general no closed formulas or distributional properties are available.

Thus, we need to rely on numerical discretization schemes to estimate moments or statistics of the solution. The numerical approximation of SPDEs has been an active field of research in the last decade.

Most publications focus on second order parabolic equations, i.e. stochastic versions of the heat or Allen-Cahn equation, see for instance [9, 10, 25, 31, 32, 34, 35, 36, 40] and the references therein. In this setting, Lévy fields as driving noise of the SPDE have been investigated, among others, in [8, 12, 18, 27, 43].

Results on second order hyperbolic SPDEs may be found, e.g., in [2, 23, 37, 43, 48] and the references therein, nonlinear hyperbolic SPDEs are the subject of interest, for example, in [15, 39].

To model the dynamics in financial markets, however, it is more common to consider first order linear hyperbolic SPDEs, for example in the Heath-Jarrow-Morton model with Musiela parametrization for interest rate forwards, see [16, 20, 33]. Another example may be found in [7, 13], where the authors motivate a stochastic framework to model energy forward markets perturbed by infinite-dimensional noise.

The underlying SPDE is a semilinear hyperbolic transport problem, where the nonlinearity stems from a no-arbitrage condition and directly depends on the volatility in the market, represented by the integrand for the infinite-dimensional noise process.

Naturally, the numerical treatment is then more involved than in the parabolic case, as we face lower regularity of the solution and the transport semigroup is not analytic. Consequently, there is very little literature on the numerical analysis of stochastic transport problems as for example [6, 38]. More recently, in [14] the authors derived error estimates for a finite difference approximation of stochastic transport on a one-dimensional spatial domain.

Our contribution is a rigorous regularity analysis and a fully discrete approximation scheme for a stochastic transport equation on a one- and two-dimensional spatial domain, and driven by a trace class Lévy noise . We derive mean-square temporal continuity and spatial regularity of the solution in terms of fractional Sobolev norms under mild assumptions. The degree of spatial smoothness depends on the regularity of and is made explicit and outlined in detail for the important special case that is associated to a Matérn covariance function (see Examples 2.3 and 3.6 below). Furthermore, we consider the transport problem on a bounded domain with suitable inflow boundary conditions rather than on . This is of practical interest in terms of modeling and simulation, but the boundary naturally limits spatial regularity of the solution even for smooth noise and initial conditions.

To approximate the solution, we couple a stable time stepping scheme with a discontinuous Galerkin (DG) approach for the spatial domain, exploiting the weak formulation of the SPDE.

By imposing certain flow conditions on the mesh as in [21] (see Assumption 4.1 in Section 4 for details), we guarantee optimal spatial convergence.

This method has been proven to be successful for deterministic hyperbolic problems, but, to the best of our knowledge, has not been applied for the discretization of SPDEs.

Finally, to sample the paths of and to obtain a fully discrete scheme, we combine truncated Karhunen-Loève expansions with an arbitrary approximation algorithm for the one-dimensional marginal Lévy processes. In each step we provide bounds on the strong mean-squared error and give an estimate of the overall error between the unbiased solution and its fully discrete numerical approximation.

In Section 2, we present a comprehensive introduction to SPDEs with Lévy noise, establishing the existence and uniqueness of mild/weak solutions in a general setting. Moving on to Section 3, we introduce the stochastic transport problem associated with a first-order differential operator and outline the necessary assumptions for ensuring well-posedness. Subsequently, we demonstrate the spatial Sobolev regularity and mean-square temporal regularity of the solution in order to establish a rigorous error control framework for subsequent sections.

In Section 4, we introduce a discontinuous Galerkin spatial discretization method, which is then combined with a backward Euler time stepping scheme in Section 5. By utilizing a DG mesh that respects the flow direction of the transport operator, we derive optimal convergence rates for this spatio-temporal discretization approach.

Section 6 focuses on the sampling procedure of the infinite-dimensional driving noise. We provide an overall mean-squared error analysis that encompasses temporal, spatial, and noise approximation components. Finally, in Section 7, we present a numerical example that serves to support our theoretical findings.

2 Stochastic Partial Differential Equations with Lévy Noise

Let be a filtered probability space satisfying the usual conditions and let be a finite time interval.

Furthermore, let and be separable Hilbert spaces and let and denote the set of linear bounded operators and , respectively.

The space of Hilbert-Schmidt operators on is given by

where is an arbitrary orthonormal basis of .

The Lebesgue-Bochner space of all square-integrable, -valued random variables is defined as

For the remainder of this article, we omit the stochastic argument for notational convenience.

Solutions to the SPDEs are characterized by path-wise identities that hold almost surely, see Definition 2.4 below. Therefore, unless stated otherwise, all appearing equalities and estimates involving stochastic terms are in the path-wise sense and are assumed to hold almost surely.

We denote by a generic positive constant which may change from one line to another.

Whenever necessary, the dependency of on certain parameters is made explicit.

Our focus is on stochastic partial differential equations with Lévy noise, i.e. with a possibly infinite-dimensional, square-integrable Lévy process as driving noise.

Definition 2.1.

A -valued stochastic process is called Lévy process if

•

has stationary and independent increments,

•

almost surely, and

•

is stochastically continuous, i.e., for all and holds

is called square-integrable if holds for any .

We consider the SPDE

(1)

on , where is a -valued random variable and is an unbounded, densely defined linear operator generating a -semigroup on .

The coefficients and in Eq. (1) are possibly non-linear measurable mappings and , respectively.

The driving noise is modeled by a square-integrable, -valued Lévy process defined on with non-negative, symmetric and trace class covariance operator , satisfying the identity

By the Hilbert-Schmidt theorem, the ordered eigenvalues of are non-negative and have zero as their only accumulation point.

The corresponding eigenfunctions form an orthonormal basis of and we define the square-root of via

Since is not necessarily injective, the pseudo-inverse of is given by

With this, we are able to define the reproducing kernel Hilbert space associated to .

Definition 2.2.

Let be a square-integrable, -valued Lévy process with non-negative, symmetric, trace class covariance operator . Then, the set equipped with the scalar-product

is called the reproducing kernel Hilbert space (RKHS) of .

Note that forms an orthonormal system in the RKHS and hence the norm on the space of Hilbert-Schmidt operators is given by

Example 2.3.

An important special case is , where is an open and bounded spatial domain for and is the Matérn covariance operator with parameters , given by

(2)

Above, is the Gamma function, is the modified Bessel function of the second kind with degrees of freedom, and is an arbitrary norm on , for instance the Euclidean norm. We refer to as the correlation length of , while controls the spatial regularity of the paths generated by . More precisely, it holds that almost surely for each .

Solutions of Problem (1) are characterized in [43, Chapter 9]:

Definition 2.4.

The predictable -algebra is the smallest -field on containing all sets of the form , where and with .

A -valued stochastic process is called predictable if it is a --measurable mapping.

The set of all square-integrable, -valued predictable processes is denoted by

holds almost surely for all and , where are the adjoint operators to and , respectively.

In Eq. (3) is the semigroup generated by , thus and Eq. (3) may be interpreted as a variation-of-constants formula.

In the definition of weak solutions, we use the identification .

Hence, the integrand is a -valued process and we obtain

for any , see [43, Chapter 9.3].

Solutions to Problem (1) are infinite-dimensional processes, i.e. , where for some .

Therefore, in general .

To ensure that mild resp. weak solutions to (1) are well-defined and unique, we fix the following set of assumptions.

Assumption 2.5.

(i)

is a centered, square integrable, -valued Lévy process with trace class covariance operator .

(ii)

is a -measurable random variable.

(iii)

is densely defined and generates a -semigroup .

(iv)

The mappings and are measurable for each and there is a constant such that for all and

Remark 2.6.

•

We focus on mean-square type convergence results in this article and only consider square-integrable processes .

This enables us to use the Itô isometry in Lemma 2.10 for stochastic integrals with respect to Hilbert space-valued Lévy processes.

Details on non-square integrable martingales as integrator can be found in [43, Section 8.8].

•

If is of non-zero mean, then for some mean function . Hence, we may assume without loss of generality that and incorporate as part of the nonlinearity , if desired.

•

Under Assumption 2.5, all integrals in Definition 2.4 are well-defined, see [43, Remark 9.6].

•

The global Lipschitz condition (iv) with respect to the second argument is sufficient for existence and uniqueness of mild solutions.

In the literature (e.g.[41, 43]), slightly weaker assumptions of the form

for are imposed.

For the numerical analysis in the forthcoming chapters, however, we utilize the weak solution of the SPDE, and it is therefore advantageous to assume Lipschitz continuity of and .

We note that this condition on and implies the linear growth bound

Theorem 2.7.

Under Assumption 2.5, there exist a unique mild and weak solution to Problem (1).

Both solutions coincide and there exists , independent of , such that

Proof.

Existence and uniqueness of a mild solution as in Eq. (3) is proven in detail in [43, Theorem 9.29]. We only sketch the main idea here for later reference.

Let be arbitrary and define the norm

With this, is a Banach space, and, using as initial value, a sequence of fixed-point iterations on is given by

Under Assumption 2.5, and by choosing large enough, is a contraction, so that existence and uniqueness of mild solutions follow by Banach’s fixed-point theorem.

The equivalence of weak and mild solutions is shown in [43, Theorem 9.15].

∎

We further record the following bound on -semigroups for later reference.

Lemma 2.8.

[42, Chapter 1.2]

Let be a -semigroup with infinitesimal generator on a Banach space .

Then, there are constants such that for all and

In the remainder of this article, we investigate the case where is a first order differential operator and Eq. (1) is a (hyperbolic) transport equation with Lévy noise.

The next section establishes temporal and spatial regularity of in this scenario to pave the way for a numerical analysis in Sections 4-6.

To conclude this section, we record infinite-dimensional versions of Itô’s formula and the Itô isometry, that require some more notation as preparation.

Let be an orthonormal basis of the (separable) Hilbert space and denote by the corresponding tensor-product Hilbert space.

Let be the completion of with respect to the Hilbert-Schmidt norm

For a given -valued semimartingale , we consider a fixed decomposition , where is the local martingale part of and the process has paths of bounded variation.

For any real-valued semimartingale we denote the quadratic variation process of by . The quadratic covariation process of the two real-valued semimartingales is defined by the polarization identity

With this at hand, the quadratic variation proces of a given -valued (local) martingale is given by the -valued process

Lemma 2.9.

(Itô formula, [43, Theorem D.2])

Let be a -valued semimartingale and let be such that there holds for all and that the mapping

is uniformly continuous on any bounded subset of .

Then, is a local semimartingale and there holds -a.s. for all

(4)

Lemma 2.10.

(Itô isometry, [43, Corollary 8.17])

Let be a predictable, square integrable process and let satisfy Assumption 2.5(i).

Then, is an admissible integrand for , and for all it holds that

3 The Stochastic Transport Equation

Let us regard Eq. (1) with respect to a convex spatial domain with , i.e. the solution is a -valued process with .

We denote for the standard Sobolev space equipped with the norm, resp. seminorm

where is the mixed partial weak derivative (in space) with respect to the multi-index and .

The fractional order Sobolev spaces are defined by

where the last term

is the Gagliardo seminorm, see, e.g., [26].

Let be a fixed vector, and let in Eq. (1) be the first order differential operator. This yields the stochastic transport problem

(5)

The inflow boundary of is given by

where is the exterior normal vector to .

We further define

as the outflow and characteristic boundary, respectively.

We equip Eq. (5) with homogeneous inflow boundary conditions on for all .

Remark 3.1.

Homogeneous inflow boundary conditions are imposed for notational convenience, and are not restrictive in our setting.

In our example in Section 7, we examine an energy forward model with nonzero, but constant inflow boundary condition on for all .

To treat this case in our setting, let and be given, and let be a solution to Eq. (12), but with inhomogeneous boundary conditions on .

For any we define , as well as the modified coefficients

Note that if and satisfy Assumption 2.5(iv), then and also satisfy Assumption 2.5(iv).

It is then readily verified that on and for all it holds

To derive a weak formulation of Eq. (5) in , we follow the approach for deterministic transport problems from [24, Section 2.2]:

For any Green’s identity yields

where is the formal adjoint of .

Now let

For any we define , and note that is a norm on , since is injective on for ([24, Remark 2.2, case (i)]).

Furthermore, let

(6)

where signifies the closure of a set with respect to a given norm .

We extend from to in a distributional sense, so that and .

Lemma 3.2.

Let be the topological dual of as in (6) and let .

It holds that , the embeddings are dense, and that

are isometric, bounded linear operators.

Proof.

Let and .

As , we obtain from [24, Remark 2.2, case (i)] that is dense in .

Thus, there is a sequence such that

in as .

Hence, .

The remaining parts of the claim are given by [24, Remark 2.2 and Proposition 2.1].

∎

Clearly, for , and, since is an isometry, it follows that satisfies the inf-sup condition

(9)

see [24, Section 2.2] for a detailed derivation.

Moreover, partial integration shows that

(10)

As and on we may define the seminorm

(11)

The weak formulation of Eq. (5) is now to find such that for all it holds

(12)

The numerical schemes to approximate and the corresponding error estimates are based on the weak formulation from Eq. (12). As we see in Theorem 3.7, however, mild solutions to Eq. (5) are convenient to investigate the spatial regularity of .

To this end, we show that the operator is the infinitesimal generator of a semigroup on , namely the shift semigroup given by

(13)

Lemma 3.3.

The family of operators defined in Eq. (13) forms a -semigroup of bounded linear operators on . Furthermore, the infinitesimal generator of is given by .

Proof.

By the definition of , it is immediate that , , and for .

Hence, is a semigroup of bounded linear operators on .

To see that is strongly continuous, let be a compactly supported, continuous function on .

Furthermore, let be the zero-extension of on given by

(14)

This yields

Note that the interchange of limit and integral is justified, since is uniformly bounded on .

The last identity holds due to continuity of on , which is in turn given since is compactly supported in the open set .

By density of in , it follows that is a -semigroup on .

For the second part of the claim, we need to verify that for all it holds that

(15)

To this end, we observe that

It is therefore sufficient to verify (15) for .

Observe that

for any fixed , there is a such that for all .

Hence, multidimensional Taylor expansion yields for some

The last limit holds as is continuous on .

Thus, Equation (15) holds for

for all , and the claim follows since is dense in .

∎

Regarding the mild solution in (3),

we see that the shift by as in (13) may introduce (spatial) discontinuities or ”kinks” if and do not decay smoothly to zero at the inflow boundary.

To account for this and derive the spatial regularity of we have to strengthen Assumption 2.5:

Assumption 3.4.

For and given as in (5), and the orthonormal eigenpairs of let the following hold:

(i)

is a square integrable, -valued Lévy process with zero mean and trace class covariance operator . The eigenvalues of are in decreasing order and there are constants and such that for all .

(ii)

There are constants and such that is a -measurable random variable, and for all it holds that .

(iii)

and are Hölder continuous with exponent on and

globally Lipschitz on , i.e. for all and it holds that

and

(iv)

There are constants and such that for all and with it holds

(v)

There are constants , (where is as in (i)) and such that for all , and with it holds that

Remark 3.5.

•

For functions with arbitrary large , the shift by results in a discontinuous function and hence for any and . In our experiments in Section 7, we consider functions that vanish on , but have nonzero derivatives at , for which assumption 3.4(iv) and (v) holds with improved regularity .

•

Assumption 3.4(iii) on the Hölder continuity with respect to is necessary to ensure the rate of convergence of the time stepping scheme introduced in Section 5. This condition implies in particular that and are measurable with respect to .

Example 3.6.

Recall Example 2.3 with , as the Matérn covariance operator from Eq. (2)

with smoothness parameter and assume for any that

(16)

By [30, Proposition 9], Assumption 3.4(i) holds with .

Moreover, if , the proof of [30, Proposition 9] yields for all such that the estimate

Now let and , where is arbitrary small and .

By construction, satisfies and Ineq. (16) yields for that

Regarding the eigenpairs of , Assumption 3.4(v) is therefore satisfied for any and in the Matérn case, provided that . Thus, we may infer the (maximum) ”mean-square spatial regularity” of directly from (see Theorem 3.7).

Theorem 3.7.

Let Assumption 3.4 hold, define and .

There exists a unique solution to Eq. (12) and Eq. (3), and both solutions coincide almost surely. Moreover, there holds

and

Proof.

Existence, uniqueness and equivalence of a weak and mild solution follow by Theorem 2.7, since Assumption 3.4 implies in particular Assumption 2.5.

We recall that the mild solution is the unique fixed-point of the iteration

and with for all . To derive the spatial regularity of , we use a similar strategy of proof as for the existence and uniqueness proof of mild solutions.

We introduce the space

with the weighted norm

We first show by induction that holds for all . Then, we choose large enough so that is a contraction on to obtain a uniform (in ) estimate for .

Starting with , we note that by Assumption 3.4(ii), and obtain

Jensen’s inequality and Assumption 3.4(iv) yield similarly

Moreover, the Itô isometry from Lemma 2.10 shows for all the identity

Since by Assumption 3.4(v), it holds that , and we obtain

where is finite and uniformly bounded in .

We now iterate this estimate over and obtain

We choose so that (e.g., ), which gives a uniform bound with respect to for the last estimate.

Taking the limit and multiplying by yields the first part of the claim.

To prove the second part, observe that Assumption 2.5 implies for any and with that

Using that the stochastic integral in the fixed-point iteration for vanishes in expectation, we find by similar calculations as above for

that

The proof is then finished by again iterating the esimates over as there holds

∎

Theorem 3.8.

Let Assumption 3.4 hold.

There is a such that for all

Furthermore, if Assumption 3.4 holds with and , then there is a such that for all

In most cases, it is impossible to access analytically as the paths of are time-dependent random functions taking values in the infinite-dimensional Hilbert space . The time dependency of each sample may be reflected in the coefficients of a suitable basis expansions, but in general no tractable representations are available.

Even if closed form solutions with respect to and a given path of were known, it would still be unclear how to sample the infinite-dimensional Lévy process .

We address these issues by introducing a discontinuous Galerkin spatial discretization in Section 4 and suitable time stepping in Section 5.

Thereafter, we discuss an approximate sampling technique for , which yields a fully discrete approximation scheme for the stochastic transport problem.

4 Discontinuous Galerkin Spatial Discretization

In this section we discretize Eq. (12) with respect to the spatial domain .

To this end, let be a countable set and let be a sequence of uniform, shape-regular triangulations of , indexed by . We denote by the set of all faces of for fixed .

To achieve optimal spatial convergence rates, we follow the approach in [21] and consider triangulations that satisfy certain flow conditions with respect to transport direction . The face of any given triangle is called an inflow face if , and outflow face whenever .

Assumption 4.1.

The domain is polygonal with piecewise linear boundary (in case that ) and is a sequence of uniform, shape-regular triangulations of , such that .

For each , a given triangulation satisfies the following two conditions:

Each simplex has a unique inflow face, denoted by .

(21)

Each interior inflow face is included in an outflow face of another simplex .

(22)

We assume that is polygonal for convenience only, to omit errors due to the piecewise linear approximation of in this case. The ensuing numerical analysis shows that the flow conditions on the inflow/ouflow faces on are indeed crucial to obtain the maximum rate of convergence for . In case that , (21) and (22) are always satisfied when partitioning into intervals of arbitrary length.

The discrete discontinuous Galerkin (DG) space of piecewise linear polynomials is given by

Elements of are piecewise linear on the simplices , but allow for jumps at the interfaces of the triangulation.

Hence, the space of continuous, piecewise linear finite elements is enclosed by , whereas the DG approach yields additional stability with a suitably chosen numerical flux on the discontinuities.

Note that for , but in general , which is in line with the distributional extension from Section 3.

The ”broken version” of the -scalar product and the induced norm with respect to are denoted by

(23)

Clearly, and coincide on .

Analogously, we define the broken Sobolev norms and semi-norms for any via

The corresponding broken Sobolev spaces are given as

and we note that .

The key ingredient to prove optimal convergence rates for deterministic transport equations in [21] is a special projection , defined by the two properties

(24)

Lemma 4.2.

[22, Proposition 2.1]/[21, Lemma 2.1]

Under Assumption 4.1, the projection given by (24) is well-defined for any fixed .

Furthermore, for any there is a such that for any and there holds

In order to derive a discrete weak formulation for (5) with respect to , we define the bilinear form

(25)

Note that the homogeneous Dirichlet boundary conditions at have been imposed implicitly (25), as we do not sum over the inflow boundary edges.

As is not uniquely determined at the faces , it remains to determine a numerical flux on each face, that is not parallel to the flow direction or belongs to the outflow boundary .

To this end, consider two given simplices sharing a common interior face such that .

The outward normal vectors of and on are denoted by and , respectively.

Similarly, for a scalar function , we define by the trace of on , and is the trace of on .

We denote the jump resp. average across of by

Note that is a vector for scalar , and that conversely is scalar if is a vector-valued function.

As numerical flux on , we use the upwind flux given by

(26)

(for the second equality in (26) see, e.g., [17, Section 3]).

To treat the boundary edges , we define the numerical flux

with the convention that is the outward pointing normal of at .

For simplicity, we set the discrete initial condition as . The semi-discrete weak problem is now to find , such that for any and it holds that

(27)

As one of the main results of this article, we provide an estimate on the semi-discrete error :

Theorem 4.3.

Let Assumptions 3.4 and 4.1 hold such that , and denote by and (for any ) the solutions to Problem (12) and Problem (27), respectively.

Then, there is a constant such that for all and there holds

As a first step for our error analysis, we have to make sure that the true solution is actually in line with the weak formulation in (27). As , this is not obvious at first glance.

Lemma 4.4.

Let Assumption 3.4 hold such that .

Then, the unique weak solution to (12) satisfies for all and that

(28)

Proof.

Theorem 3.7 yields that for all and .

This implies in particular, that the trace is well-defined for any and coincides with the numerical flux on every face , in the sense that there holds on each face

(29)

Now assume first that for any and fix an arbitrary test function .

By density of in , partial integration yields on any that

We define the stochastic processes , and via , and for , so that .

Theorem 3.7 and Lemma 4.2 show that

(34)

and it thus remains to derive the corresponding bound for .

Lemma 4.4 and (27) yield together with for all that

We now follow the proof of [21, Theorem 2.2] to show that . For any , it holds by (25) that

The second and last identity follow by the defining properties of in (24), in the third and fourth step we have used the definition of the numerical flux in (29).

Thus, we obtain the error equation

where the operator is given by .

Note that the ”jump terms” in the second and third line in Eq. (4) vanish for the functional .

By Lemma 4.5 we have that , taking expectations thus yields the estimate

(36)

The first term is bounded by Young’s inequality and (34) by

To bound the second term , we use Assumption 3.4(iii) and (34) to obtain

For the final term , we first observe that the quadratic variation term is given for any orthonormal basis of by

Note that for all there holds

and all terms in the second line are centered and jointly uncorrelated random variables with respect .

As is an orthonormal basis of , we obtain by Parseval’s identity

where the last estimate holds by Lemma 4.2 and Assumption 3.4(iii).

By Item (v) in Assumption 3.4 and Theorem 3.7, we obtain further for some and that

Substituting the estimates on back into (36) thus yields

and the claim follows by Grönwall’s inequality.

∎

5 Temporal Discretization

We use equidistant time points to discretize , and define , for . We employ a backward Euler (BE) approximation for the linear part of Eq. (27), i.e.

The nonlinear parts with respect to and are approximated by the forward differences

(37)

where .

As the stochastic integral on the left hand side in Eq. (37) is an Itô integral, it is crucial to use forward differences that preserve the martingale property of the driving noise.

For the nonlinearity on the other hand, we could have chosen a backward difference or midpoint rule, but with the scheme (37) we avoid solving a nonlinear system in every time step without affecting the overall order of convergence.

The spatio-temporal-discrete version of the weak problem is then to find such that and for any and

(38)

We further interpolate linearly at the temporal nodes to obtain the continuous time approximation defined by

(39)

Our main result of this section bounds the resulting temporal discretization error:

Theorem 5.1.

Let Assumptions 3.4 and 4.1 hold such that , let , and denote by and the solutions to Problem (27) and Problem (39), respectively.

Then, there is a constant such that for all with and there holds

To prove Theorem 5.1, we first show mean-square continuity of the semi-discrete solution . For this, we record in turn the well-known inverse estimate

(40)

where is independent of and (see, e.g., [19, Remark 4.8/Corollary 4.24]).

Lemma 5.2.

Let Assumptions 3.4 and 4.1 hold such that , and denote by the solution to Problem (27).

Then, there is a constant such that for all and with there holds

Proof.

We use again the processes , and given by , and for .

Further, without of loss of generality, we assume that and show mean-square continuity of , the claim for then follows by the triangle inequality.

Fix such that and recall from (35) that for there holds

(41)

For the first part of the claim, we test against to obtain

The first term is bounded in expectation by Theorem 3.8

To bound the second term, we use (24) together with the inverse estimate (40), Lemma 4.2, and Theorem 4.3 to obtain

The last line follows since by Assumption 4.1 and with .

For the last two terms and , we proceed as in the proof of Theorem 4.3 to obtain that

and

As we have , there holds

and the first part of the claim follows with , since

To proof the second part of the claim, we first take expectations in (41), so that the stochastic integral vanishes, and then test against .

With the Cauchy-Schwarz inequality, Theorem 3.7 and similar arguments as for the first part, we arrive at

and the second part of the claim follows again by the triangle inequality.

∎

Since is a convex combination of in each sub-interval, it suffices to bound the error at the temporal grid points.

We assume again that for convenience.

Let for and observe that

.

By Eqs. (27) and (38) it holds for all that

To bound in expectation, we use the inverse estimate (40), Young’s inequality, and Lemma 5.2 to obtain

To bound , we use that and are independent to obtain

where we have again used (40) in the second step and Lemma 5.2 for the third line.

For the term , we then also use the splitting together with the inverse estimate (40) and Lemma 5.2 to obtain by similar calculations as for and that

Collecting the estimates for and using that then shows

The term is estimated by Young’s inequality, Assumption 3.4(iii) and Lemma 5.2 via

For the last term , we use independence of and together with the Cauchy-Schwarz/Young’s inequality and Itô’s isometry to obtain similarly

Substituting all estimates in (43), regrouping some terms and summing with respect to thus yields with that

The claim then follows by the discrete Grönwall inequality and Lemma 4.5.

∎

Remark 5.3.

For , the condition is satisfied by setting , which naturally yields the overall error equilibration

(44)

For the case that such an error balancing is not straightforward in view of the proof Theorem 5.1. However, our numerical results in Section 7 suggest that an overall error of order may also be recovered when with the parameters .

On the other hand, a suitable extension of Theorem 5.1 to the case is far from obvious, and requires a more involved analysis. In order to keep the length of this manuscript reasonable, we leave this as a subject for future work.

6 Noise Approximation

After discretizing the temporal and spatial domain of Problem (12), it is in general necessary to derive a numerically tractable approximation of the infinite-dimensional driving noise .

For this, we will utilize a series representation of and truncate the expansion after a finite number of terms.

Since the covariance operator of is symmetric and of trace class, admits the Karhunen-Loève expansion

(45)

The scalar products are one-dimensional uncorrelated, but not independent, Lévy processes with zero mean and variance (see [43]).

In general, infinitely many of the eigenvalues are strictly greater than zero, hence we truncate the series in Eq. (45) after terms to obtain

It can be shown, see for example [11], that converges to in mean-square uniformly on with the truncation error bounded by

When simulating , it is vital to generate as uncorrelated, but stochastically dependent Lévy processes for fixed .

Besides the truncation, another bias may occur when sampling the one-dimensional processes .

For , consider the normalized processes

(46)

with unit variance at . Denoting by equality in distribution,

the identity

holds with respect to probability law of .

For a general one-dimensional Lévy process , it is not possible to sample from the exact distribution of for arbitrary .

There are a few important exceptions, for instance normal-inverse Gaussian (NIG) or variance Gamma (VG) processes (see [46]), in any other case, however, one is forced to use approximate simulation algorithms.

The most popular technique is the compound Poisson approximation (CPA), see for instance [3, 27, 28, 45], which usually guarantees weak convergence. A drawback of the CPA methods is that it requires rather strong assumptions on the one-dimensional Lévy processes to bound the approximation error in a mean-square sense and is difficult to implement.

Another approach is to use the Fourier inversion (FI) technique introduced in [11], which ensures a strong error control in under relatively weak assumptions on . With the FI method, we are able to approximate very general types of Lévy noise and control the mean-squared error, for instance if stems from the important class of generalized hyperbolic (GH) Lévy processes introduced in [4, 5].

To allow for arbitrary approximation techniques, we formulate the following assumption.

Assumption 6.1.

Let be arbitrary approximations of (based on CPA, FI, etc.) such that the processes are jointly uncorrelated, but stochastically dependent, and let

be the approximated -valued Lévy field. There is a constant such that for all and

Remark 6.2.

Assumption 6.1 yields that the overall noise approximation error is bounded by

(47)

hence there is a separation between the truncation error with respect to and the simulation bias .

Often, an arbitrary small error may be achieved with sufficient computational effort and it is possible to reduce the noise approximation error in Eq. (47) to any desired amount by increasing the number of terms in the expansion and decreasing . This is for instance the case for GH Lévy fields approximated by FI as in [11].

Moreover, we achieve an equilibration between both types of errors in the sense that

Substituting by in Eq. (38) yields the fully discrete problem to find such that for all and it holds

(48)

where and .

To complete the error analysis, we derive the overall approximation error between and the unbiased weak solution to Eq. (12).

Theorem 6.3.

Let Assumption 3.4 hold with , let Assumption 6.1 hold, and denote by and the solutions to Problem (12) and Problem (48), respectively.

Then, there is a such that for any with and it holds that

Proof.

We define for , and obtain by in Eqs. (38) and (48) that

Testing against , taking expectations and using that is independent of and then yields with Young’s inequality that

Assumption 6.1 and the Itô isometry yield for the ”middle” term that

By analogous arguments as in the proof of Theorem 5.1 and the discrete Grönwall inequality, we obtain

where is independent of and .

The claim then follows as an immediate consequence of Remark 5.3 and the triangle inequality.

∎

7 Numerical Experiments

For the numerical experiments we consider the spatial domain with time interval , take , and let be the Matérn covariance operator from Examples 2.3 and 3.6:

We fix the correlation length to and vary the smoothness parameter throughout our experiments. The eigenpairs of may be approximated by solving a discrete eigenvalue problem and interpolation, see [44, Chapter 4.3].

Provided that , Remark 3.5 shows that Assumption 3.4(v) is satisfied for and .

We consider GH Lévy fields, i.e. the one-dimensional processes from Eq. 46 are uncorrelated GH Lévy processes. More importantly, for each the vector-valued process is a -dimensional GH Lévy process with parameters and , where and the matrix is symmetric, positive definite with unit variance. The characteristic function of is given for by

We achieve a zero-mean process by setting . An important class of the GH family are normal inverse Gaussian (NIG) processes, where .

For more details on multidimensional GH distributions and the simulation of GH Lévy fields we refer again to [11] and the references therein.

In all subsequent experiments, we use a NIG Lévy field with and for each truncation index .

The choice of NIG fields is motivated by the results from [1], where the authors pointed out that this class of Lévy fields is well-suited to fit empirical log-returns in electricity forward markets.

We are able to simulate multidimensional NIG processes without bias, i.e., Assumption 6.1 holds with .

As stochastic transport problem we consider a slight modification of the energy forward model from [7] (to include multiplicative noise) given by

(49)

For positive parameters we use the coefficient function

and matching initial/inflow boundary conditions given by

Note that Eq. (49) may be transformed to a problem with homogeneous boundary conditions by replacing and by

see Remark 3.1.

We fix the values and for our experiments.

The coefficients in Eq. (49) are time-independent and the relation is imposed to ensure the absence of arbitrage in the market, see [7].

This entails that is only locally Lipschitz with respect to , while Assumption 3.4 still holds for . Nevertheless, the quadratic growth of did not cause any problems in our experiments, and hence we stick to this particular example.

As and vanish near the outflow boundary for , but their derivatives do not, Assumption 3.4 is satisfied with and for all .

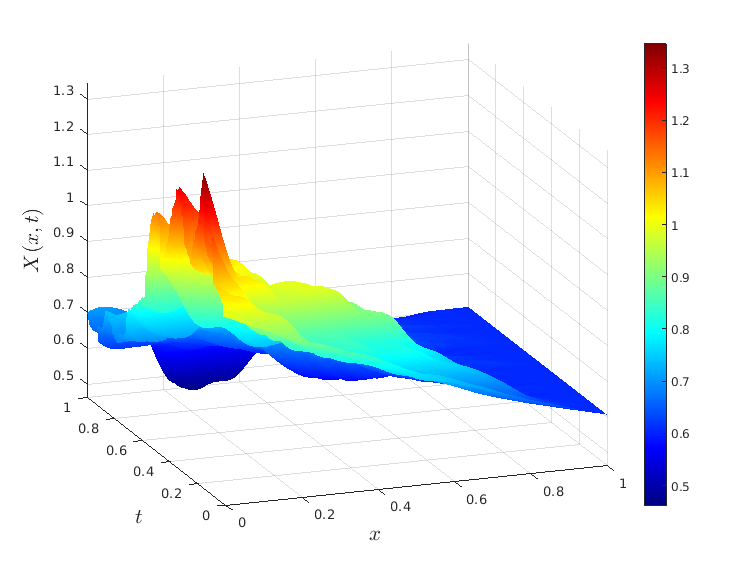

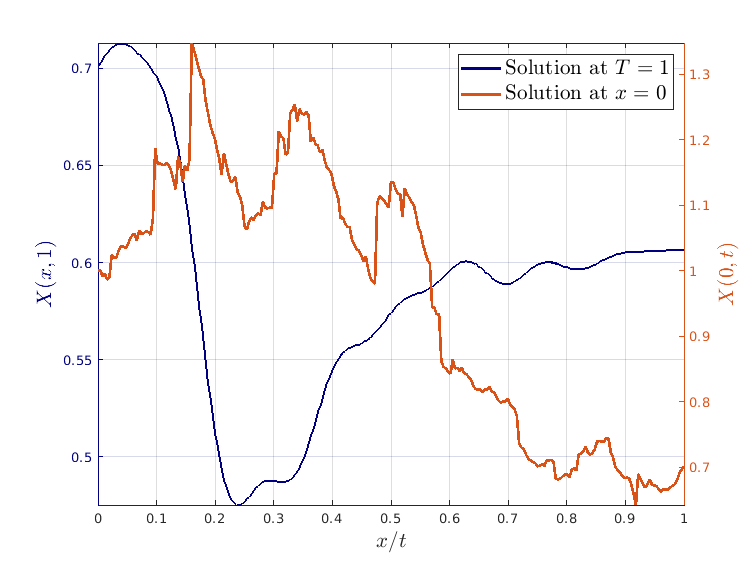

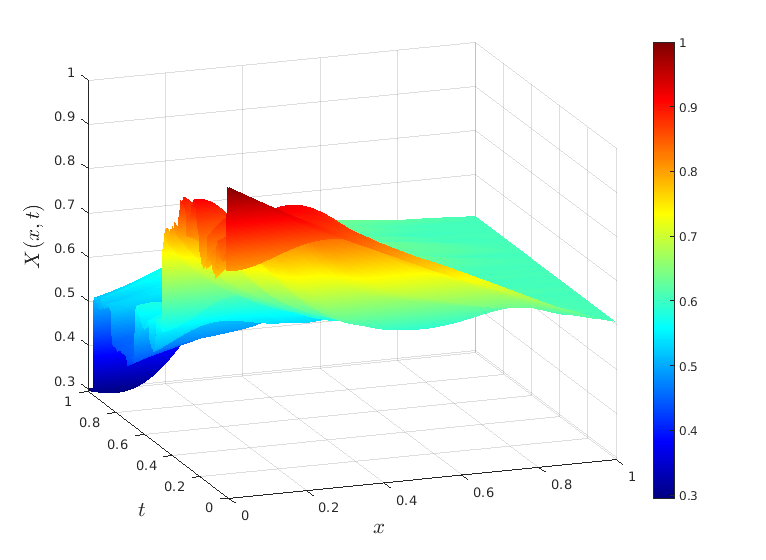

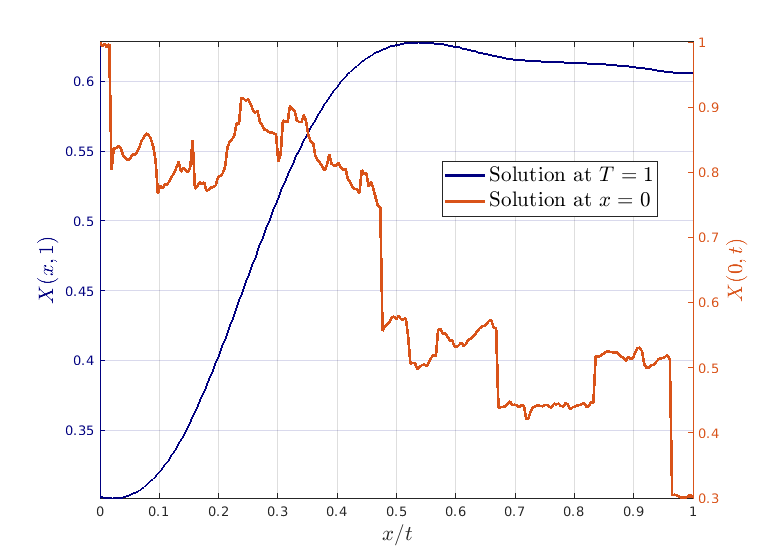

Samples of are given for and in Figure 1.

Figure 1: Left column: samples of the solution to the forward model. Right column: plots of the surface at the outflow boundary (blue) and for (orange). The smoothness parameters of the covariance function are in the top row and in the bottom row.

We use the fully discrete scheme (48) to discretize Eq. (49). The space consists of the piecewise linear DG functions with respect to an equidistant refinement of with mesh width .

Recalling that and , Theorem 6.3 predicts for an overall error of

We consider , assume for simplicity that ,

and use spatial refinements of for any given .

Based on Remark 5.3, we determine and such that

(50)

where the choice only applies in the case for the refinement .

We approximate by a reference solution that is generated with and and according to Eq. (50).

The overall root-mean-squared error (RMSE) from Theorem 6.3 is estimated by averaging 200 independent samples of , i.e.,

where the subscript denotes the -th Monte Carlo sample. The same realization of the Lévy noise is used for and in any of the 200 samples to estimate the pathwise, strong convergence of the algorithm.

By Eq. (50), we have for that

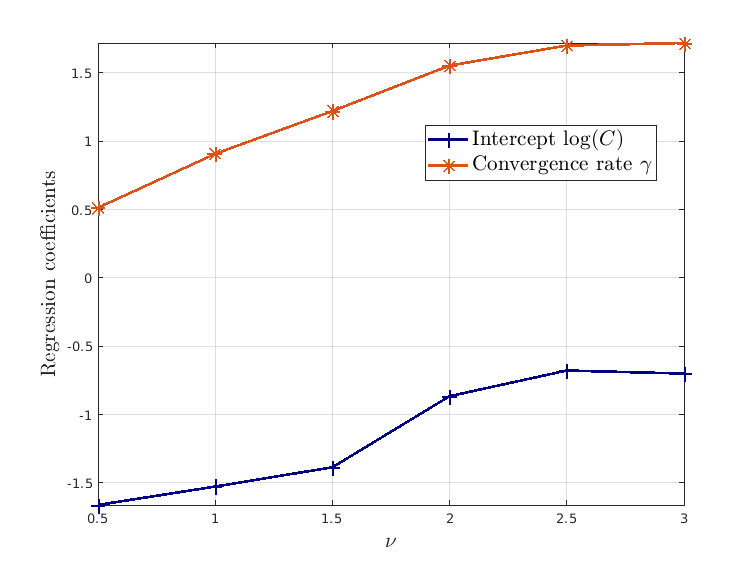

Hence, we perform a linear regression of the estimated log-RMSE on the log-refinement to obtain an empirical estimate of to compare with our theoretical findings.

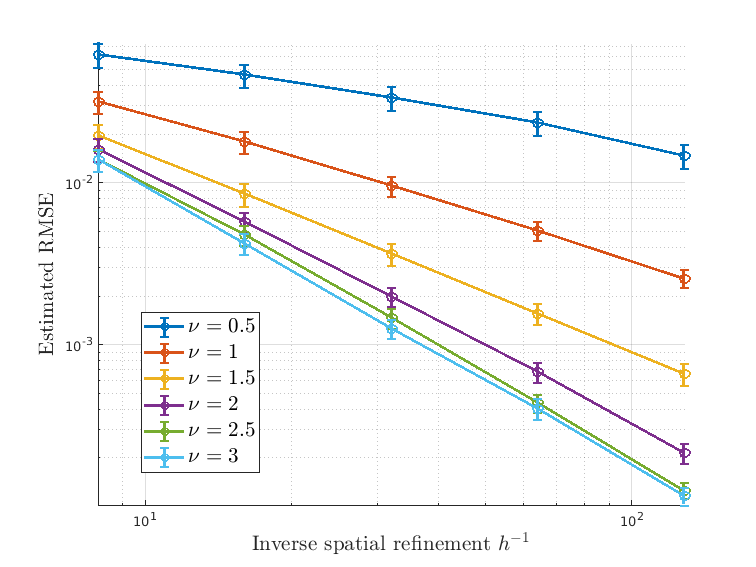

We display the results for and in Figure 2. As expected, a larger value of increases smoothness, and therefore causes a faster error decay with respect to . This effect saturates around , as the smoothness of the problem is not anymore limited by the noise, but by the ”kink” in the solution at the inflow boundary.

Moreover, the estimated empirical convergence rates in the right plot of Figure 2 are in line with our findings from Theorem 4.3 and the spectral analysis of the Matérn kernel in Example 3.6. The convergence rate is until its saturation point at , where it remains at , since the solution is at most -regular for . Finally, we remark that the discretization scheme also has an error decay with rate for the borderline case with , which is not covered by Theorem 5.1.

Figure 2: Left: RMSE vs. inverse spatial refinement , the bars on each RMSE curve indicate the 95-% confidence interval of the estimated error. Right: estimated convergence rates of the Backward Euler – Petrov-DG scheme for Eq. (49).

Acknowledgements

This work is partially funded by Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) under Germany’s Excellence Strategy - EXC 2075 - 39740016 and it is greatly appreciated. AS was partly funded by ETH Foundations of Data Science (ETH-FDS). We thank Prof. Dr. Christoph Schwab for insightful discussions that led to a significant improvement of the manuscript.

References

[1]

A. Andresen, S. Koekebakker, and S. Westgaard.

Modeling electricity forward prices using the multivariate normal

inverse Gaussian distribution.

Journal of Energy Markets, 3(3):3–25, 2010.

[2]

R. Anton, D. Cohen, S. Larsson, and X. Wang.

Full discretization of semilinear stochastic wave equations driven by

multiplicative noise.

SIAM Journal on Numerical Analysis, 54(2):1093–1119, 2016.

[3]

S. Asmussen and J. Rosiński.

Approximations of small jumps of Lévy processes with a view

towards simulation.

Journal of Applied Probability, 38(2):482–493, 2001.

[4]

O. E. Barndorff-Nielsen.

Exponentially decreasing distributions for the logarithm of particle

size.

Proceedings of the Royal Society of London. Series A,

Mathematical and Physical Sciences, 353(1674):401–419, 1977.

[5]

O. E. Barndorff-Nielsen.

Hyperbolic distributions and distributions on hyperbolae.

Scandinavian Journal of Statistics, 5(3):151–157, 1978.

[6]

A. Barth.

A finite element method for martingale-driven stochastic partial

differential equations.

Communications on Stochastic Analysis, 4(3):355–375, 2010.

[7]

A. Barth and F. E. Benth.

The forward dynamics in energy markets – infinite-dimensional

modelling and simulation.

Stochastics: An International Journal of Probability and

Stochastic Processes, 86(6):932–966, 2014.

[8]

A. Barth and A. Lang.

Milstein approximation for advection-diffusion equations driven by

multiplicative noncontinuous martingale noises.

Applied Mathematics and Optimization, 66(3):387–413, 2012.

[9]

A. Barth and A. Lang.

Simulation of stochastic partial differential equations using finite

element methods.

Stochastics, 84(2-3):217–231, 2012.

[10]

A. Barth, A. Lang, and C. Schwab.

Multilevel Monte Carlo method for parabolic stochastic partial

differential equations.

BIT Numerical Mathematics, 53(1):3–27, 2013.

[11]

A. Barth and A. Stein.

Approximation and simulation of infinite-dimensional Lévy

processes.

Stochastics and Partial Differential Equations: Analysis and

Computations, 6(2):286–334, 2018.

[12]

A. Barth and T. Stüwe.

Weak convergence of Galerkin approximations of stochastic partial

differential equations driven by additive Lévy noise.

Mathematics and Computers in Simulation, 143:215–225, 2018.

[13]

F. E. Benth and S. Koekebakker.

Stochastic modeling of financial electricity contracts.

Energy Economics, 30(3):1116–1157, 2008.

[14]

F. E. Benth, G. Lord, G. Di Nunno, and A. Petersson.

The heat modulated infinite dimensional heston model and its

numerical approximation.

arXiv preprint arXiv:2206.10166, 2022.

[15]

D. Blomker and A. Jentzen.

Galerkin approximations for the stochastic Burgers equation.

SIAM Journal on Numerical Analysis, 51(1):694–715, 2013.

[16]

A. Brace and M. Musiela.

A multifactor Gauss Markov implementation of Heath, Jarrow,

and Morton.

Mathematical Finance, 4(3):259–283, 1994.

[17]

F. Brezzi, L. D. Marini, and E. Süli.

Discontinuous Galerkin methods for first-order hyperbolic problems.

Mathematical models and methods in applied sciences,

14(12):1893–1903, 2004.

[18]

Z. Brzeźniak and J. Zabczyk.

Regularity of Ornstein–Uhlenbeck processes driven by a Lévy

white noise.

Potential Analysis, 32(2):153–188, Feb 2010.

[19]

A. Cangiani, Z. Dong, and E. Georgoulis.

hp-version discontinuous galerkin methods on essentially

arbitrarily-shaped elements.

Mathematics of Computation, 91(333):1–35, 2022.

[20]

R. Carmona and M. R. Tehranchi.

Interest Rate Models: An Infinite Dimensional

Stochastic Analysis Perspective.

Springer Science & Business Media, 2007.

[21]

B. Cockburn, B. Dong, and J. Guzmán.

Optimal convergence of the original DG method for the

transport-reaction equation on special meshes.

SIAM Journal on Numerical Analysis, 46(3):1250–1265, 2008.

[22]

B. Cockburn, B. Dong, and J. Guzmán.

A superconvergent ldg-hybridizable galerkin method for second-order

elliptic problems.

Mathematics of Computation, 77(264):1887–1916, 2008.

[23]

D. Cohen and L. Quer-Sardanyons.

A fully discrete approximation of the one-dimensional stochastic wave

equation.

IMA Journal of Numerical Analysis, 36(1):400–420, 2016.

[24]

W. Dahmen, C. Huang, C. Schwab, and G. Welper.

Adaptive Petrov–Galerkin methods for first order transport

equations.

SIAM Journal on Numerical Analysis, 50(5):2420–2445, 2012.

[25]

A. Debussche and J. Printems.

Weak order for the discretization of the stochastic heat equation.

Mathematics of Computation, 78(266):845–863, 2009.

[26]

E. Di Nezza, G. Palatucci, and E. Valdinoci.

Hitchhiker’s guide to the fractional Sobolev spaces.

Bulletin des Sciences Mathématiques, 136(5):521–573, 2012.

[27]

T. Dunst, E. Hausenblas, and A. Prohl.

Approximate Euler method for parabolic stochastic partial

differential equations driven by space-time Lévy noise.

SIAM Journal on Numerical Analysis, 50(6):2873–2896, 2012.

[28]

N. Fournier.

Simulation and approximation of Lévy-driven stochastic

differential equations.

ESAIM: Probability and Statistics, 15:233–248, 2011.

[29]

R. Gençay and F. Selçuk.

Extreme value theory and value-at-risk: Relative performance in

emerging markets.

International Journal of Forecasting, 20(2):287–303, 2004.

[30]

I. G. Graham, F. Y. Kuo, J. A. Nichols, R. Scheichl, C. Schwab, and I. H.

Sloan.

Quasi-Monte Carlo finite element methods for elliptic PDEs with

lognormal random coefficients.

Numerische Mathematik, 131(2):329–368, 2015.

[31]

I. Gyöngy and A. Millet.

On discretization schemes for stochastic evolution equations.

Potential Analysis, 23(2):99–134, 2005.

[32]

I. Gyöngy, S. Sabanis, and D. Šiška.

Convergence of tamed Euler schemes for a class of stochastic

evolution equations.

Stochastics and Partial Differential Equations: Analysis and

Computations, 4(2):225–245, 2016.

[33]

D. Heath, R. Jarrow, and A. Morton.

Bond pricing and the term structure of interest rates: A new

methodology for contingent claims valuation.

Econometrica: Journal of the Econometric Society, pages

77–105, 1992.

[34]

A. Jentzen and P. E. Kloeden.

The numerical approximation of stochastic partial differential

equations.

Milan Journal of Mathematics, 77(1):205–244, 2009.

[35]

P. E. Kloeden, G. J. Lord, A. Neuenkirch, and T. Shardlow.

The exponential integrator scheme for stochastic partial differential

equations: Pathwise error bounds.

Journal of Computational and Applied Mathematics,

235(5):1245–1260, 2011.

[36]

M. Kovács, S. Larsson, and F. Lindgren.

On the backward Euler approximation of the stochastic

Allen-Cahn equation.

Journal of Applied Probability, 52(2):323–338, 2015.

[37]

M. Kovács, F. Lindner, and R. L. Schilling.

Weak convergence of finite element approximations of linear

stochastic evolution equations with additive Lévy noise.

SIAM/ASA Journal on Uncertainty Quantification,

3(1):1159–1199, 2015.

[38]

M. Krivko and M. V. Tretyakov.

Numerical integration of the Heath–Jarrow–Morton model of

interest rates.

IMA Journal of Numerical Analysis, 34(1):147–196, 2014.

[39]

I. Kröker and C. Rohde.

Finite volume schemes for hyperbolic balance laws with multiplicative

noise.

Applied Numerical Mathematics, 62(4):441–456, 2012.

[40]

R. Kruse.

Optimal error estimates of Galerkin finite element methods for

stochastic partial differential equations with multiplicative noise.

IMA Journal of Numerical Analysis, 34(1):217–251, 2014.

[41]

W. Liu and M. Röckner.

Stochastic Partial Differential Equations: An

Introduction.

Springer, 2015.

[42]

A. Pazy.

Semigroups of Linear Operators and Applications to Partial

Differential Equations, volume 44.

Springer Science & Business Media, Applied Mathematical Sciences, 2

edition, 1983.

[43]

S. Peszat and J. Zabczyk.

Stochastic Partial Differential Equations with Lévy Noise.

Cambridge University Press, 2007.

[44]

C. E. Rasmussen and C. K. Williams.

Gaussian Processes for Machine Learning.

The MIT Press, 2006.

[45]

T. H. Rydberg.

The normal inverse Gaussian Lévy process: simulation and

approximation.

Communications in Statistics. Stochastic Models,

13(4):887–910, 1997.

Heavy tails and highly volatile phenomena.

[46]

W. Schoutens.

Lévy Processes in Finance: Pricing Financial

Derivatives.

John Wiley and Sons, 2003.

[47]

H. Triebel.

Theory of Function Spaces.

Modern Birkhäuser Classics. Birkhäuser/Springer Basel AG,

Basel, reprint of the 1983 edition, 2010.

[48]

J. B. Walsh.

On numerical solutions of the stochastic wave equation.

Illinois Journal of Mathematics, 50(1-4):991–1018, 2006.

[49]

D. Zhang and Q. Kang.

Pore scale simulation of solute transport in fractured porous media.

Geophysical Research Letters, 31(12), 2004.