Credit risk with asymmetric information and a switching default threshold

Abstract

We investigate the impact of available information on the estimation of the default probability within a generalized structural model for credit risk. The traditional structural model where default is triggered when the value of the firm's asset falls below a constant threshold is extended by relaxing the assumption of a constant default threshold. The default threshold at which the firm is liquidated is modeled as a random variable whose value is chosen by the management of the firm and dynamically adjusted to account for changes in the economy or the appointment of a new firm management. Investors on the market have no access to the value of the threshold and only anticipate the distribution of the threshold. We distinguish different information levels on the firm's assets and derive explicit formulas for the conditional default probability given these information levels. Numerical results indicate that the information level has a considerable impact on the estimation of the default probability and the associated credit yield spread.

1 Introduction

Credit risk, or default risk, is the risk that a financial loss will be incurred if a counterparty does not fulfill its contractually agreed financial obligations in a timely manner. Quantitative credit risk models for measuring, monitoring and managing credit risk have become central in today's complex financial industry. The recent financial crisis has impressively demonstrated the need for effective credit risk management. Since then the evaluation of credit risk has been receiving increasing attention. For credit risk analysis it is crucial both from a theoretical and an empirical point of view to model the default of a default risky asset, i.e., a security that has a nonzero probability of defaulting on its contracted payments, and to forecast the associated default probability. A typical example of a credit risky asset is a corporate bond. A corporate bond promises its holder a fixed stream of payments but may default on its promise.

There are two classical types of modeling approaches for credit risk: the structural one and the reduced-form one. The structural approach is considered by Black & Scholes [3], Merton [18] and Black & Cox [2], among others. It provides a relationship between default risk and capital structure by using the evolution of the firm’s assets value to determine the time of default, i.e., the default event of a bond is triggered when the assets of the firm who issued the bond fall below some threshold. The important feature of the structural model is that it implicitly assumes that the modeler has complete knowledge about the dynamics of the firm's assets and the situation that will trigger the default event (i.e., the firm's liabilities). Despite the convincing economic interpretation in terms of the firm's assets and liabilities there are shortcomings when the firm's assets are modeled by a continuous-time asset value process. One is that credit yield spreads go to zero as maturity goes to zero regardless of the riskiness of the firm. This results from the investors' knowledge about the firm's true distance to default. Such credit spreads are uncommon in practice. Another disadvantage of the structural approach is that forecast bond prices continuously converge to their recovery value (the payment which is received if default occurs before maturity) which contradicts the price jump at default in empirical studies.

These issues do not occur in the second approach, the reduced-form approach, which is considered by Jarrow & Turnbull [13], Artzner & Delbaen [1], and Duffie & Singleton [7], among others. It treats the dynamics of default as an exogenous event. This implies knowledge of a less detailed information set compared to the structural approach and credit spreads become in general more realistic and are easier to quantify. Another advantage is that the reduced-form approach has proven to be very useful for the valuation of credit-sensitive securities. However, the approach is lacking economic insights as it does not connect credit risk to underlying structural variables.

To gain both the economic appeal of the structural approach and the empirical plausibility and the tractability of the reduced-form approach, structural models can be transformed into reduced-form models by changing its information set to a less refined one (see Jarrow & Protter [12]). One way is to model the default barrier as a random variable which is unobservable by bond investors (see Lando [17], Giesecke & Goldberg [8], Hillairet & Jiao [11]). Another way is to assume that the firm's assets are only partially observable by investors (see Duffie & Lando [6], Jeanblanc & Valchev [14], Lakner & Liang [16]).

This paper extends the traditional structural model to a dynamic setting by relaxing the assumption of a constant default threshold to the case of a piecewise constant threshold. Motivated by default events during the financial crisis where a firm's management has decided to close activities and the default occurs although the firm is in a relatively healthy situation (see Hillairet & Jiao [11]), the default threshold is modeled as a random variable whose value is chosen by the management of the firm and adjusted dynamically to react to changes in the economic environment or to account for the election of a new firm management. In literature, this generalization of the default model to a dynamic setting was proposed by Blanchet-Scalliet, Hillairet & Jiao [4]. The authors study the information accessible to the management of the firm and obtain explicit formulations for the survival probability given the information of the management by using a successive enlargement framework. Our approach is different and related to ordinary investors on the market who do not have access to the value of the threshold and only anticipate the distribution of the threshold. The objective is to analyze the impact of available information of public bond investors on the estimation of the default probability. We consider an investor who continuously observes the firm value and an investor who only observes the firm value at discrete dates. Explicit formulas for the default probabilities and associated credit yield spreads given the different information levels on the firm's assets are derived and, based on these formulas, as a direct application the valuation of bond prices is considered. Numerical examples are presented to illustrate and compare the conditional default probabilities and credit spreads.

The remainder of this paper is organized as follows. Section 2 sets up a model for credit risk based on a structural model but with an unobservable default barrier that is allowed to switch. In this setting different information structures are distinguished. The impact of asymmetric information on the default probability is studied in Section 3 where explicit formulas for the conditional survival probabilities given the different information structures are derived. Section 4 provides numerical results and a conclusion is given in Section 5. Finally, the Appendix contains proofs omitted from the main text.

2 Model for the default event

We introduce a structural model for credit risk where short-term default risk is included by making the default barrier unobservable. Further, the usual assumption of a constant default barrier is relaxed allowing the firm's management to adjust the barrier.

2.1 Default barrier

The default event is specified in terms of the firm's asset value process and the default threshold . Default occurs when the value of the firm decreases to the level of the default barrier for the first time. The random time of default is denoted by . Uncertainty in the economy is modeled by some fixed complete probability space which is endowed with the filtration generated by the asset process and satisfying the usual conditions, i.e., , where denotes the -null sets. The -algebra of describes the information of the market. We model the evolution of the value of the firm's assets by a geometric Brownian motion, i.e.,

| (1) |

where is a -Brownian motion, and . The solution to (1) is known to be

| (2) |

where . For the sake of easier notation we assume w.l.o.g. , i.e., we assume that the asset process starts at 1. We say that a firm defaults when it stops fulfilling a contractual commitment to meet its obligations stated in a financial contract. The firm's management decides whether and when to default. Thus, the management determines the default triggering barrier. The essential difference with a classical structural model is that the management is not constrained to decide on one fixed barrier but can dynamically adjust the default barrier. This reflects the management's possibility to react to changes in the economic environment or the election of a new firm management. The time points at which the management adjusts the default barrier are deterministic and denoted by , , with , where is a finite time horizon. The default barrier can be written as

where , are -measurable random variables representing the private information of the management on the default barrier and denotes the indicator function of the set . Public investors do not have any knowledge on the default barrier except that they know the adjustment time points and they agree on the joint probability distributions for , , which are denoted by . The associated probability density functions are denoted by for . We make the assumption that is independent of . The random default time is given by . The running minimum asset process is denoted by and given by

| (3) |

Further, the running minimum started from a certain time point is denoted by

| (4) |

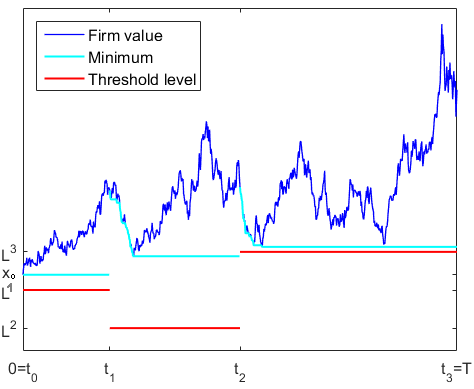

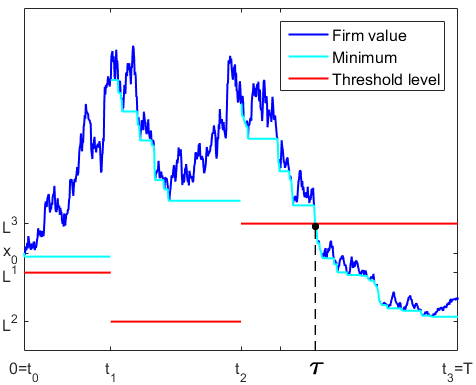

For we have . This model setup is illustrated by Figure 1 which shows two trajectories of the firm value , default barriers , and and the three running minimum processes , for . We consider two scenarios. In the first scenario shown in the left panel occurs no default whereas in the second scenario shown in the right panel default occurs between and .

2.2 Information structure

We distinguish the following three information structures.

Management's information

The management has complete information about the firm's asset process and obtains information on the default threshold at time . Thus, the management's information structure is a progressive enlargement of the filtration by the default threshold process , i.e.,

This insider information is considered in Blanchet-Scalliet, Hillairet & Jiao [4] and will not be considered in this paper.

For public bond investors we distinguish the following two information structures.

C-investor's information

The first type of investors continuously observe the firm value and the default in the moment it occurs but they do not have knowledge on the default threshold (because it is firm inside information of the management). We call an investor endowed with this information structure a C-investor. The C-investor's information structure on the bond market is described by a progressive enlargement of the filtration by the random default time , i.e.,

where is the default indicator process defined by . C-investors are uncertain about the firm's true distance to default although they have complete information about the firm value. This uncertainty is due to lacking knowledge on the threshold level. Thus, default arrives as a full surprise.

D-investor's information

The second type of investors observe the asset process only in discrete time and are called D-investors. The information structure of a D-investor is similar to the information structure of a C-investor in that both investors do not have any knowledge about the default barrier except that they observe the occurrence and timing of default. The difference is that the asset process is not completely observable but only at discrete dates denoted by , , where for . This is a realistic assumption, since investors usually observe the asset value at the times of corporate news release. The partial information on the asset process is described by a sub-filtration of , where

The D-investor's information structure can be described by a progressive enlargement of the filtration by the random default time , i.e.,

Assumption 2.1.

Every adjustment time , , of the default barrier coincides with one of the information dates , , i.e., .

3 Conditional survival probability

The conditional survival probability, i.e., the probability of not having experienced default by the finite time horizon given the accessible information, plays an important role in the valuation of credit risky securities (see Hillairet & Jiao [10]). The aim of this section is to derive explicit formulas for the conditional survival probability given the information of a C-investor, i.e., , and of a D-investor, i.e., .

We begin with reviewing classical results of the running minimum of a geometric Brownian motion.

Lemma 3.1.

Let be the asset value process given in (1) with and the running minimum process defined in (3).

-

1.

Given then the density function of is given by

(5) for and zero otherwise, where and denote the cumulative distribution function and the probability density function of the standard normal distribution, respectively.

-

2.

Given then the joint probability density function of and is given by

(6) for , , and zero otherwise.

-

Proof.

The above formulas are a corollary to the results given in Harrison [9, Ch. 1]. ∎

Lemma 3.2.

Under the assumptions of Lemma 3.1 the complementary distribution function of is given by

| (7) |

for , . Further, it holds for , and for .

-

Proof.

The proof is given in Jeanblanc & Valchev [14, Lemma 2]. ∎

3.1 C-investor's information case

The next theorem shows that the conditional survival probability given the information of a C-investor can be formulated in terms of -conditional survival probabilities for which we derive explicit formulas.

Theorem 3.3.

Let be the asset value process given in (1) with . Further, let be the associated running minimum started at zero defined in (3) and be the associated running minimum started at a certain time point defined in (4). Then, for the conditional survival probability given the information of a C-investor it holds

| (8) |

where the -conditional survival probabilities are given by the following formulas for :

- 1.

-

2.

For , , it holds

(11)

-

Proof.

We obtain Eq. (8) by using classical results of progressive enlargement (see Jeanblanc, Yor & Chesney [15, Sec. 7.3.3]). For the sake of simpler notation the proof of the -conditional survival probabilities is only given for , i.e., the threshold is in the interval and in the interval . The proof for is along the same line and skipped.

Eq. (2) yields that for the firm value can be expressed bywhere given by is a Brownian motion starting at zero and independent of . The process given by is independent of and it holds

Proof of (9): Let be fixed, then we can describe the event that no default occurs until the maturity time by

where given by with the Brownian motion given by is independent of and it holds . We denote by and the running minimum of and , respectively, i.e.,

Then it holds

Based on this representation the conditional survival probability until the maturity time given the information can be written as

We have exploited in the last equation the independence of from .

Proof of (10): Let be fixed, then we can describe the event that no default occurs until the maturity time byBased on this representation the conditional survival probability until the maturity time given the information can be calculated by

Proof of (11): The conditional survival probability until time given the information is obtained by

Finally, for it holds

∎

Remark 3.4.

For we obtain as a special case the model proposed by Giesecke & Goldberg [8], where the default barrier is constant but random, i.e., . The conditional survival probability is given by

| (12) |

Remark 3.5.

Let and assume that and are independent with probability distribution functions and , respectively. Then the conditional survival probability for is given by

on the no default set . For calculating the conditional survival probability reduces to the case of a constant but random barrier. We have

and

yielding the following simplified formula for the conditional survival probability

A direct application of the conditional survival probability is the pricing of credit derivatives such as defaultable bonds. For example, let us consider a zero-coupon bond that matures at and has zero recovery, i.e., the defaultable bond pays 1 at if there was no default by and zero otherwise. Assuming that the pricing probability is , then the price of such a financial product is given by

where is a discount factor. An important quantity in the credit risk analysis is the credit yield spread on a zero-coupon bond issued by a firm. It is the difference between the yield at time on a credit risky and a credit risk-free zero-coupon bond, both maturing at . Thus, the credit spread is given by

3.2 D-investor's information case

n this subsection we consider the case where the asset process is not completely observable by ordinary investors on the market. More precisely, the D-investor obtains information about the asset value only at discrete times which include the adjustment times , , of the default barrier. We denote the information dates between two adjustment times and by , , , where , , , and . Further, we introduce

| (13) |

for , .

Lemma 3.6.

-

Proof.

The proof is given in Jeanblanc & Valchev [14, Lemma 2]. ∎

The next theorem shows that the conditional survival probability given the information of a D-investor can be formulated in terms of -conditional survival probabilities for which explicit formulas are derived.

Theorem 3.7.

Under the assumptions of Theorem 3.3 for the conditional survival probability given the information of a D-investor it holds

| (14) |

where the -conditional survival probabilities are given by the following formulas for :

-

1.

For , , , it holds

(15) For , , it holds

(16) -

2.

For , , , it holds

(17)

-

Proof.

The proof is presented in Appendix A. ∎

Remark 3.8.

For the special case of a constant but random default barrier, i.e., and , the -conditional survival probabilities are given by the following formulas: Let , , where for , denote the times where the D-investor obtains information about the firm's asset value. For , , it holds

| (18) |

where

Remark 3.9.

Let be the price of a zero-coupon bond that matures at and has zero recovery. Assuming that the pricing probability is , then is given by

where is a discount factor. The credit spread is given by

4 Numerical examples

In this section we implement the formulas for the default probabilities derived in the previous section by evaluating the integrals using the Gauss–Kronrod quadrature formula (see Monegato [19]) and quantify numerically the impact of asymmetric information on the estimations of the default probabilities and credit spreads. More numerical examples can be found in Redeker [20].

The parameters for the firm's asset value process are taken from Blanchet-Scalliet, Hillairet & Jiao [4], i.e.,

We consider a time horizon of years and we suppose that a firm's management decides at on a default threshold . Further, we assume that the management adjusts the default threshold at from to . C-investors and D-investors only have knowledge on the (marginal and joint) laws of . The law of is modeled by a copula. In the following examples C-investors and D-investors assume that is beta distributed with parameters and is exponentially distributed with parameter . Further, investors assume that the law of is given by a Gumbel copula , i.e.,

for some (see Bluhm & Overbeck [5]). Thus, the correlation between and is modeled by the parameter , where corresponds to the case of independent default thresholds.

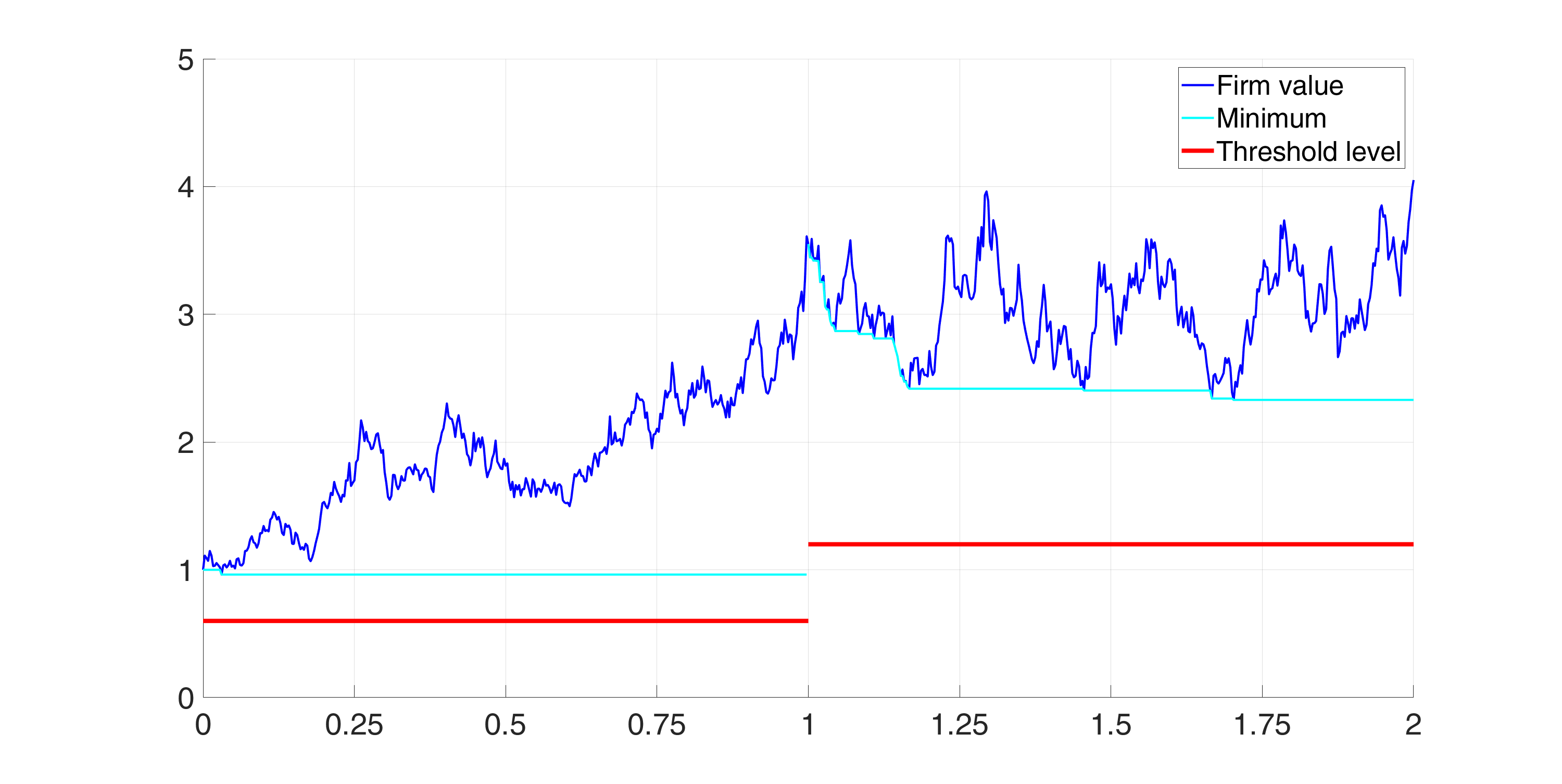

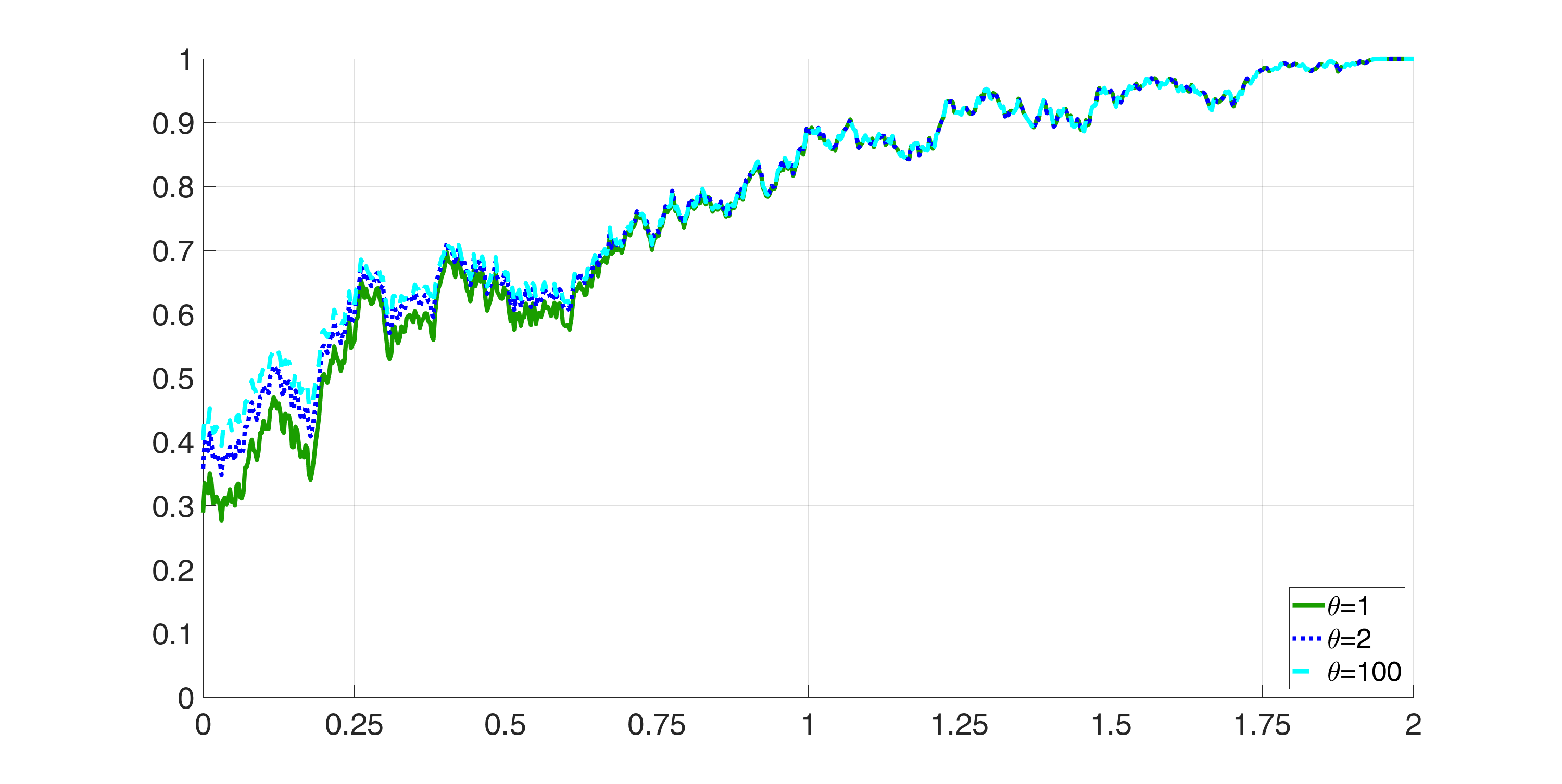

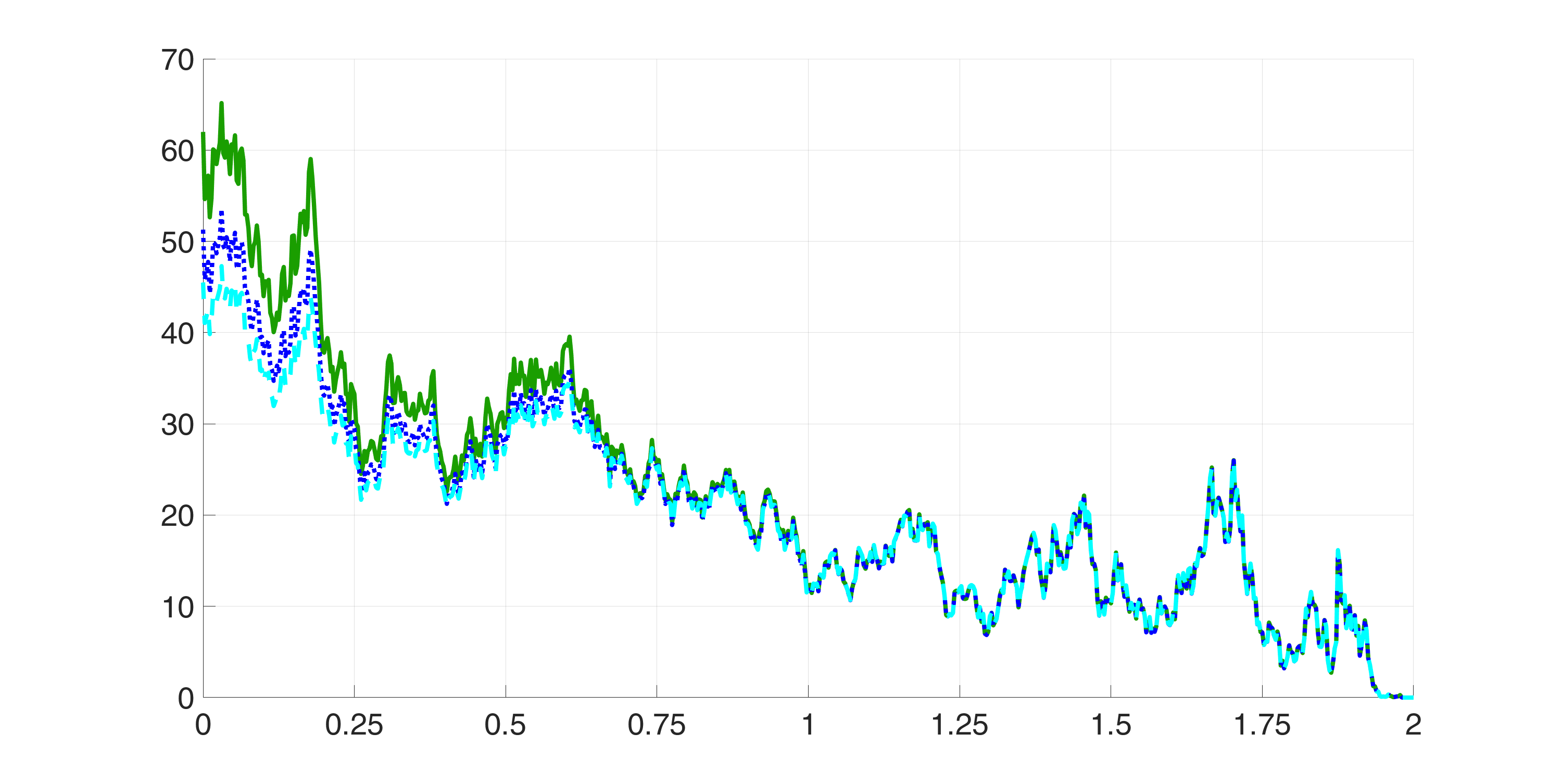

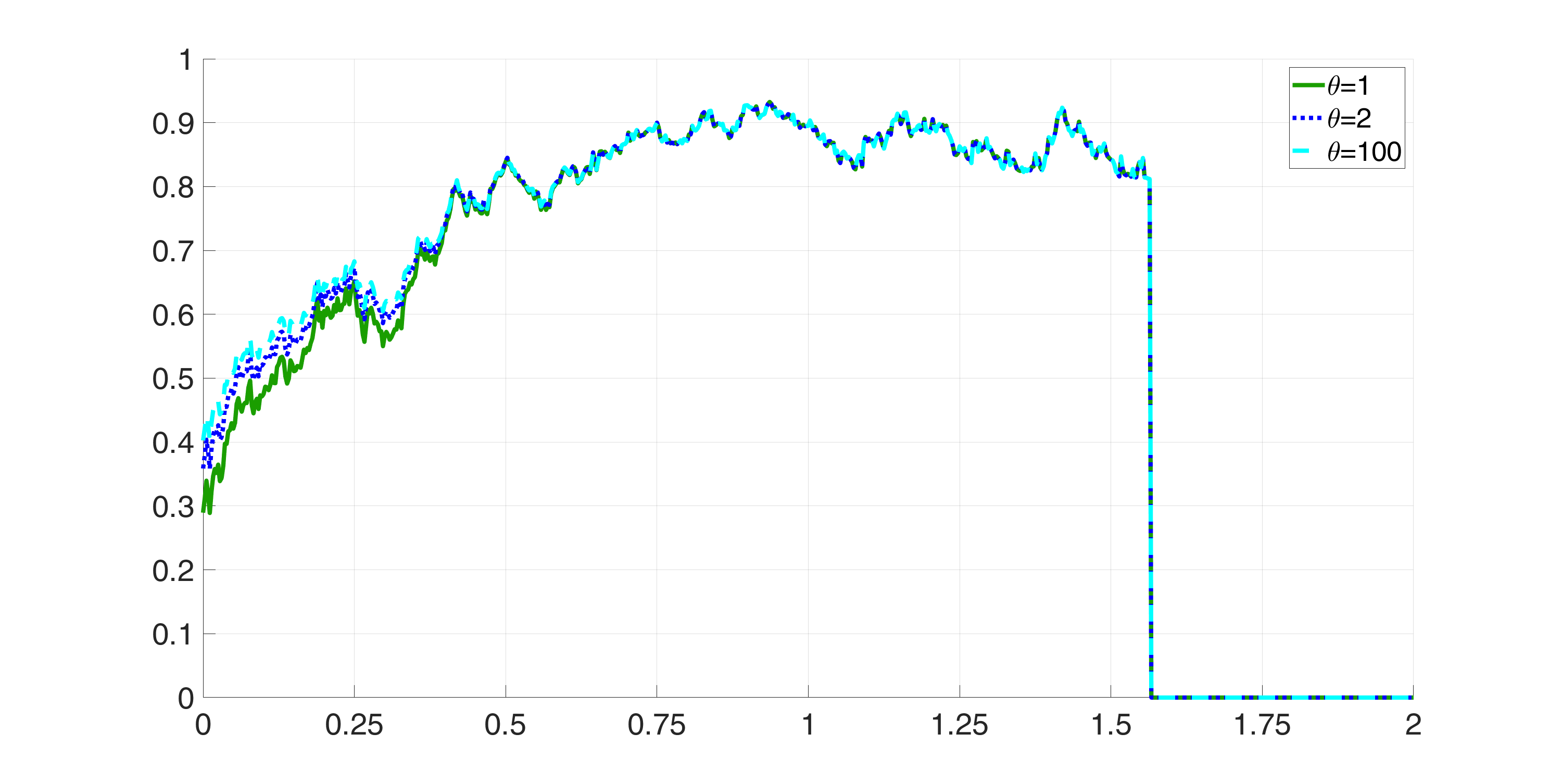

The top panel of Figure 2 presents a realized trajectory of the firm's asset process, the switching default threshold and the running minimum of the firm value which is restarted after adjustment of the default threshold. We observe that no default occurs before maturity and the realizations of the default thresholds are given by and . The middle panel of Figure 2 shows the associated conditional survival probability given the information of a C-investor for different values of (). We observe that the conditional survival probability converges to one, since no default has occurred by maturity. If and are independent, i.e., , the estimate of the survival probability is smaller compared to the cases of dependent and . However, differences in the conditional survival probability between , and become smaller with increasing time. The bottom panel of Figure 2 illustrates the associated credit yield spread given the information of a C-investor for different values of (). The credit spread tends to zero as the time approaches maturity since the C-investor has learned about the default threshold and knows that the firm is not subject to default in the next instance of time. If and are independent, i.e., , the credit yield spread is higher compared to the cases of dependent and .

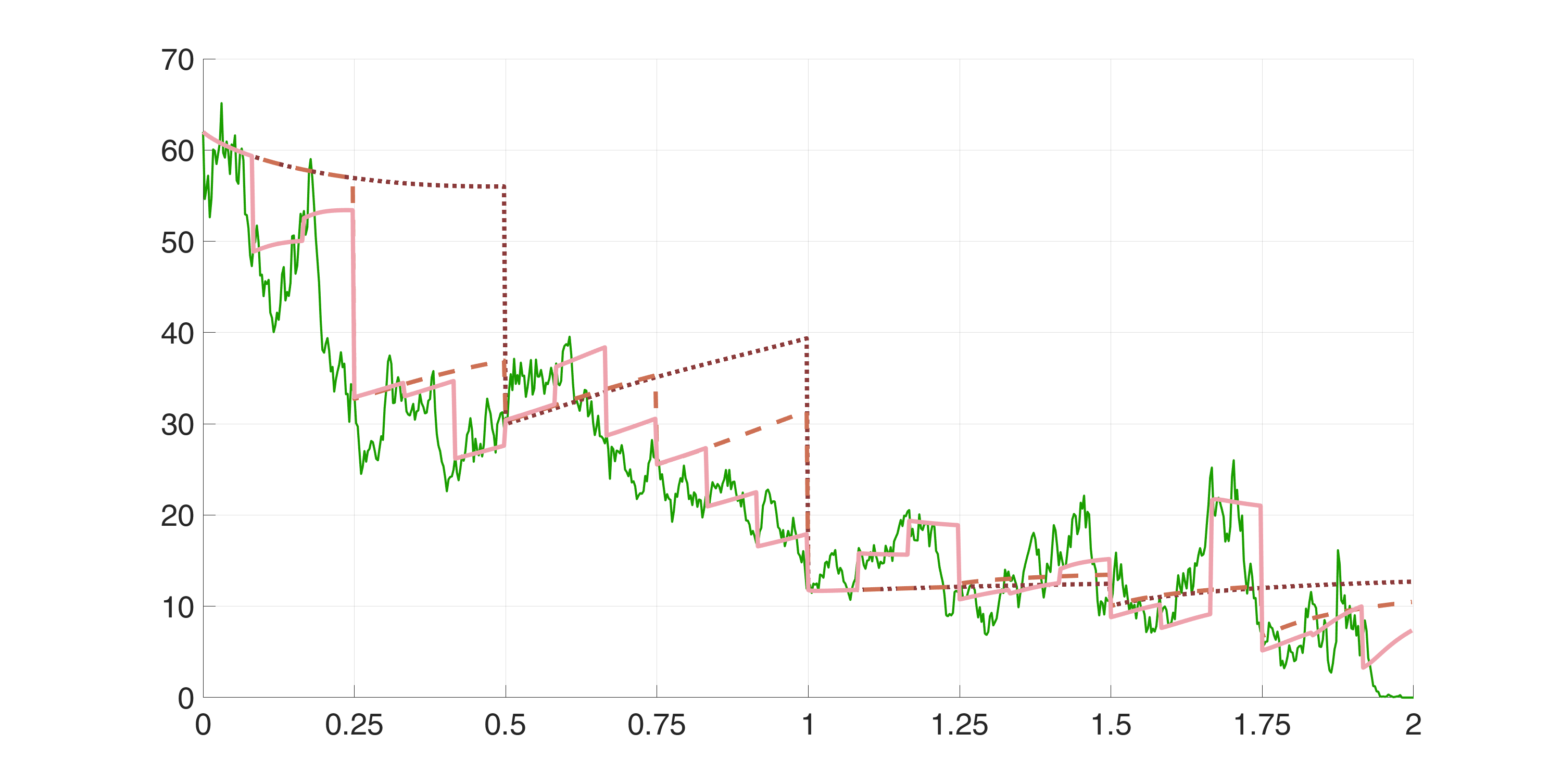

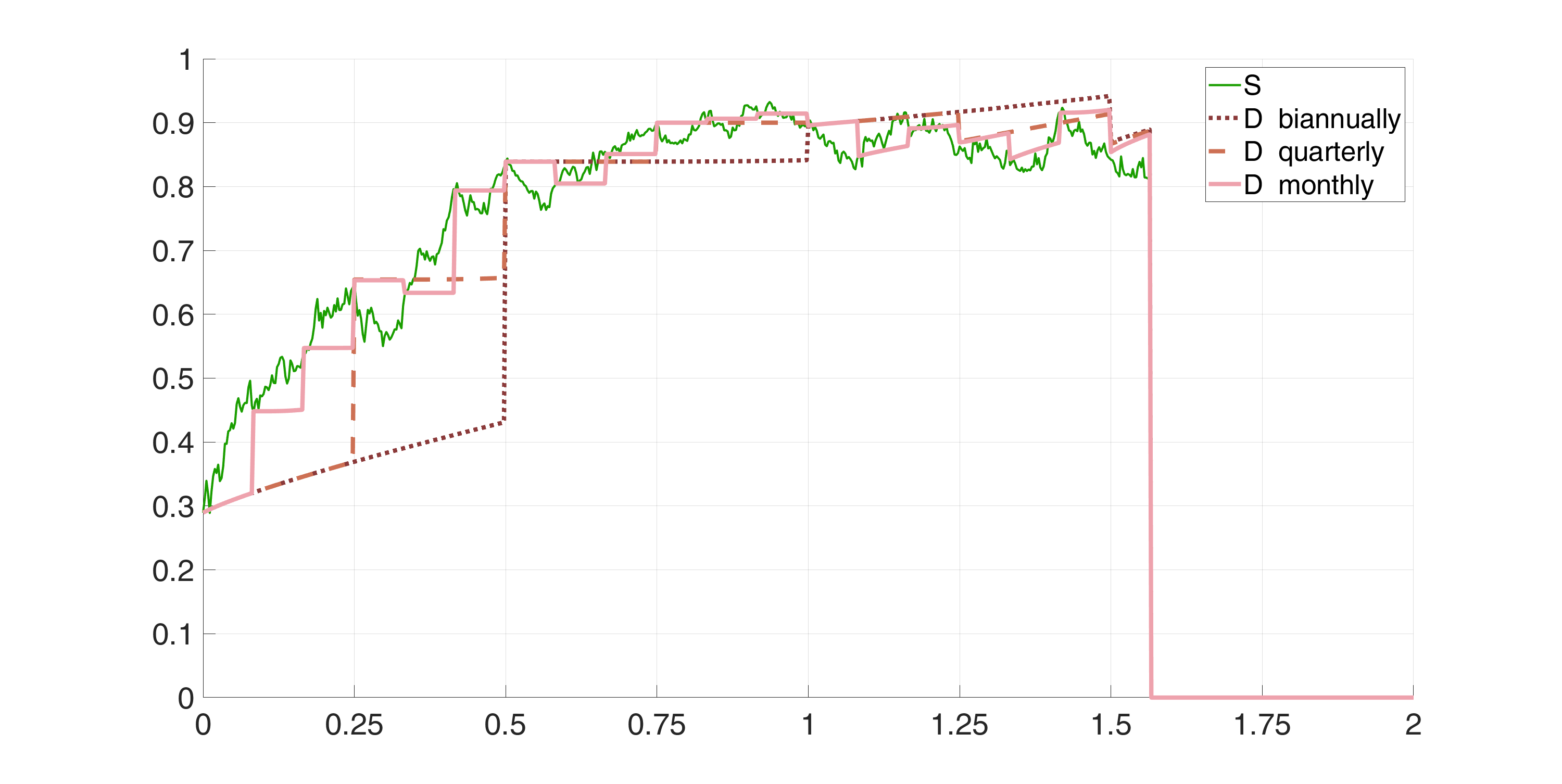

Figure 3 illustrates the conditional survival probability and the credit spread given the information of a D-investor for the case of independent default thresholds () and different information time points (biannually, quarterly, monthly).

We observe that the more frequently a D-investor obtains information about the firm value the closer are the D-investor's and C-investor's estimates of the survival probability. The credit yield spread given the information of a D-investor is non-zero at maturity, i.e., D-investors demand a risk premium for the default risk. D-investors who obtain information about the firm value twice a year demand the highest risk premium followed by D-investors who obtain that information every quarter. The lowest risk premium is demanded by D-investors who obtain information about the firm value every month. This indicates that the risk premium depends on the frequency of observations of the firm value and the associated time to maturity at the last information date. Recall that the D-investors who obtain information about the firm value twice a year, every quarter and every month receive the last information before at , and , respectively. At these time points the firm value is , and . Thus, the D-investor who observes the firm value every month demands the highest risk premium. Furthermore, the last observed firm value before is almost equal for the other two D-investors but the D-investor who obtains information twice a year demands a higher risk premium compared to the D-investor who observes the firm value every quarter. This indicates that the risk premium also depends on the frequency of observations of the firm value and the associated time to maturity at the last information date.

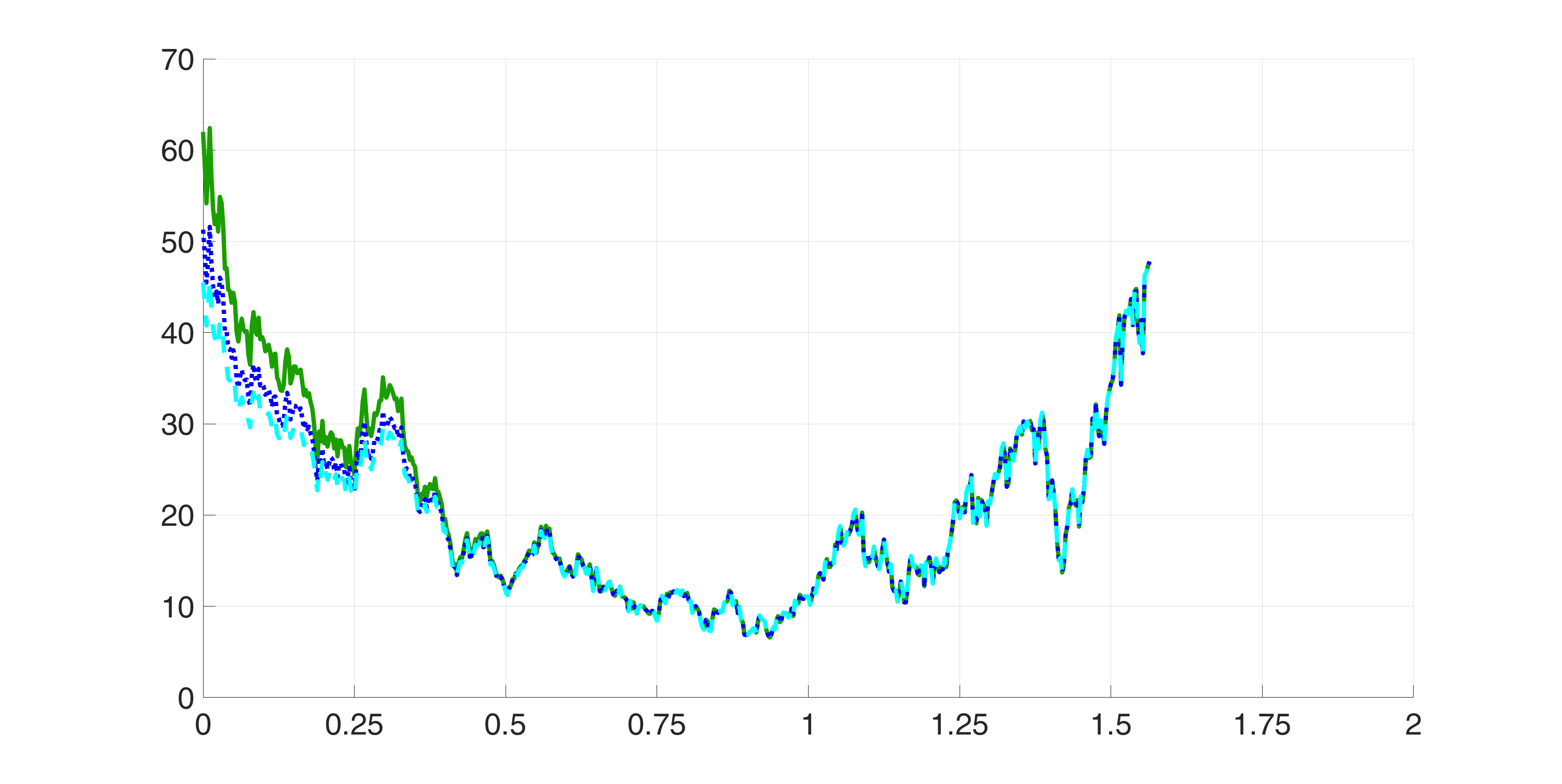

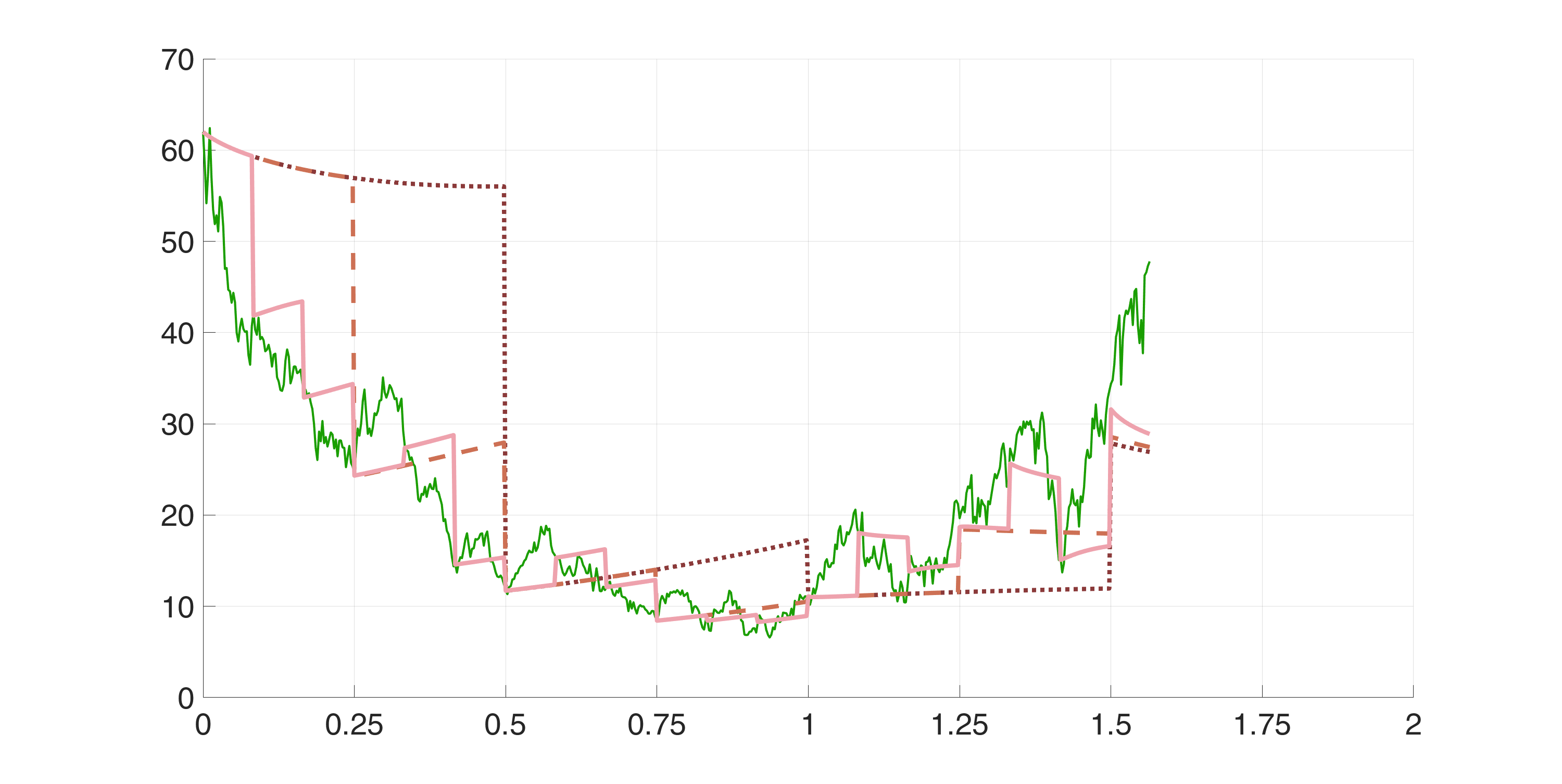

A second example is presented by Figure 4. The top panel shows a realized trajectory of the firm's asset process, the switching default threshold and the running minimum of the firm value which is restarted after adjustment of the default threshold. We observe that default occurs in the second year. The middle and bottom panel illustrate the associated conditional survival probability and credit yield spread given the information of a C-investor for different values of (). We observe that the conditional survival probability jumps to zero at the time of default.

Figure 5 illustrates the conditional survival probability and credit yield spread given the information of a D-investor for the case of independent default thresholds (). The D-investors obtain information about the firm value twice a year, every quarter and every month, respectively. We observe that the conditional survival probabilities jump to zero at the time of default.

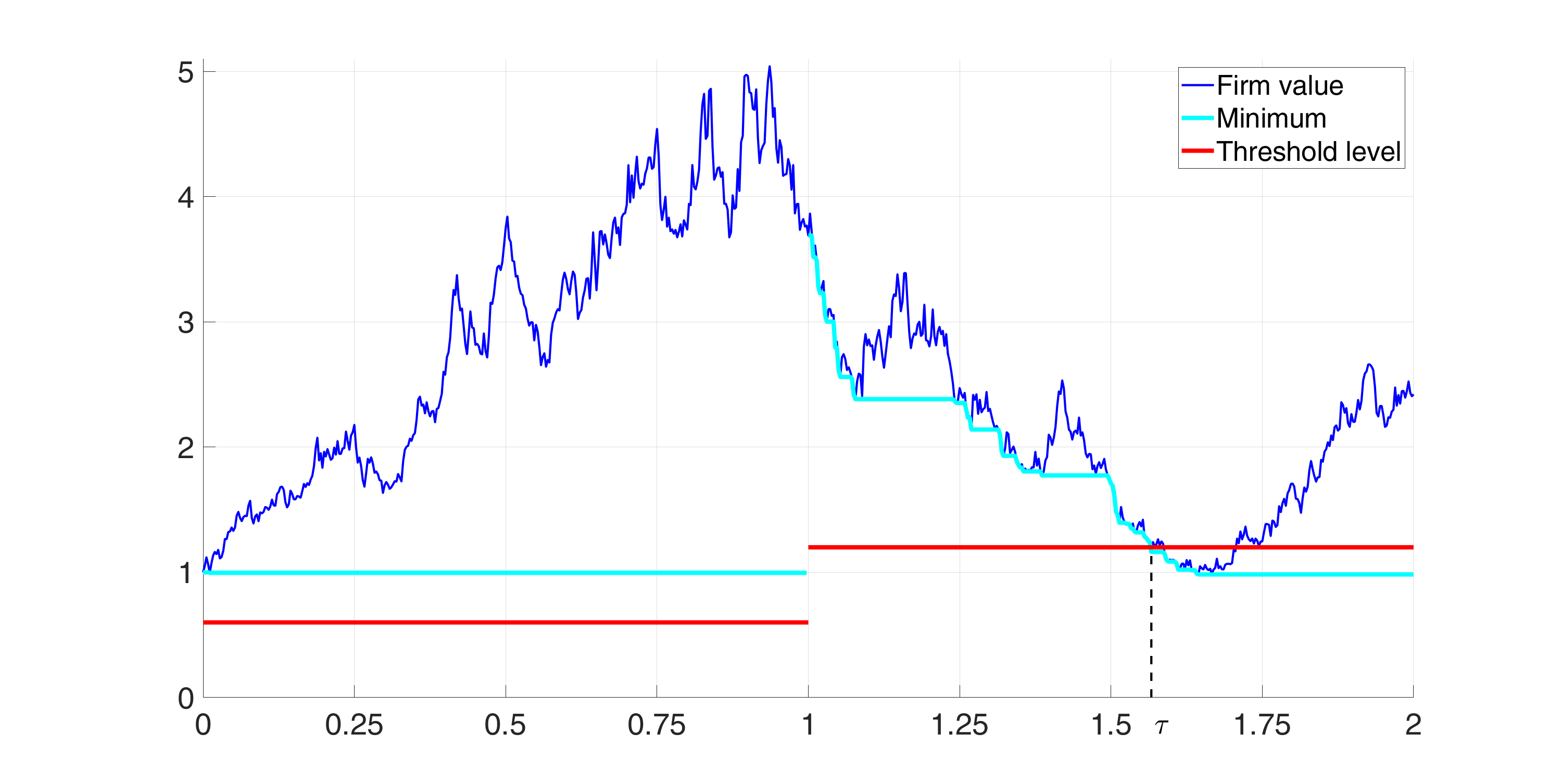

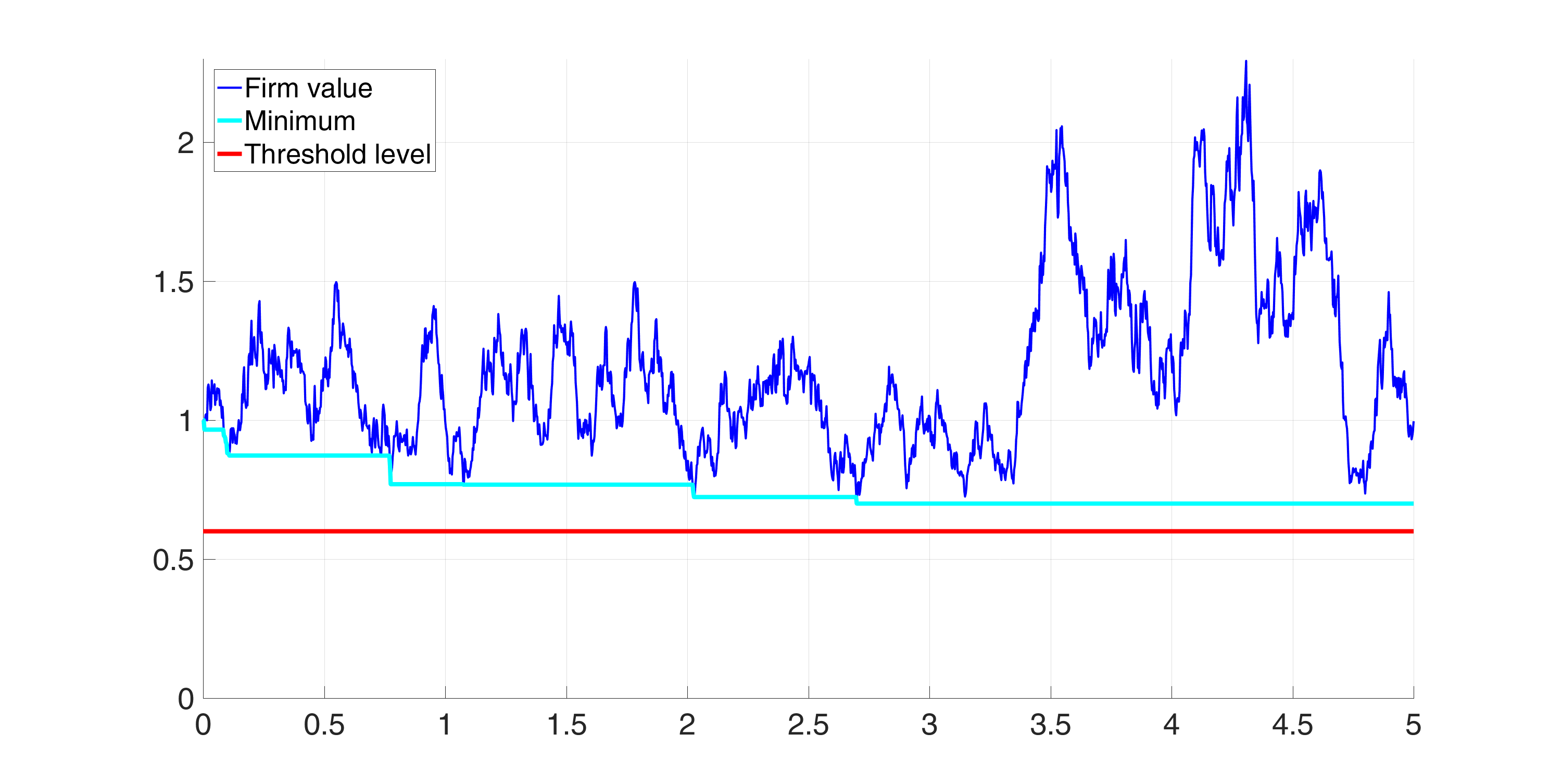

We note that the estimates of the conditional survival probabilities given the information of a C-investor and a D-investor are very close at the D-investor's information dates in the examples presented above. This is no longer the case if we extend the time horizon. We present a special case, where the default threshold is taken to be just a random constant of the form as proposed in Giesecke & Goldberg [8] and the time horizon is extended to years. C-investors and D-investors assume that follows a standard uniform distribution. The top panel of Figure 6 shows a realized trajectory of the firm value, the associated running minimum and a realization of the default threshold. The middle and bottom panel show the associated conditional survival probabilities and credit yield spreads given the information of a C-investor and a D-investor, respectively. The D-investor obtains information about the firm value once in 2.5 years. We observe that the C-investor's estimate of the conditional survival probability and the D-investor's estimate of the conditional survival probability are now visibly different at the information date of the D-investor. The credit yield spread at is zero given the information of the C-investor and nonzero given the information of the D-investor.

5 Conclusion

This paper extends the traditional structural model for credit risk. In the proposed model the default of a firm is triggered when the value of the firm's assets falls below a threshold which is modeled as a sequence of random variables whose values are chosen by the management of the firm and dynamically adjusted accounting for changes in the economy or the appointment of a new firm management. Investors on the market have no access to the value of the threshold and only anticipate its distribution. Different information levels on the firm value are distinguished and explicit formulas for the conditional default probability and associated credit yield spreads given these information levels are derived. Numerical illustrations are provided which show that the information level has a considerable impact on the estimation of the default probability and the associated credit yield spread. Investors who have perfect information on the value process of the firm learn about the default threshold, i.e., they learn that the default threshold must lie below the current running minimum of the firm value if default has not yet occurred. Thus, the larger the distance of the firm value to the running minimum the less likely is a default and investors adjust their estimation of the default probability accordingly. The associated credit yield spreads are high if the firm value is close to its running minimum and low otherwise. Especially, if the firm value is far above its running minimum just before maturity investors know that there will be no default in the next instance of time and they do not demand a default risk premium, i.e., the credit spread is zero. This is different for investors who do not have full access to the value process of the firm. Investors who only observe the firm value at specific dates cannot be certain about the firm value just before maturity and they demand a nonzero default risk premium. Furthermore, the credit spreads at maturity depend on their last observed firm value and the frequency of firm value observations. In future research the dynamics of defaultable bonds are studied in this model set-up.

Appendix A Proof of Theorem 3.7

Observe that . Then the proof of Eq. (14) is along the same line as the proof of Eq. (8) for the case of a C-investor. For the sake of a simple notation we prove the remaining formulas of the theorem for the case , i.e., the threshold is in the interval and in the interval . The proof for is along the same line and skipped. In order to keep the notation simple we denote the times at which the D-investor observes the asset process by , , where , and for some . The last term ensures that the D-investor obtains information about the asset process at the adjustment time of the default threshold. We define the processes by

where is a Brownian motion independent of and given by . Note that inherits the independence of and it has the same law as . Further we have the decomposition for . We denote by the running minimum of , i.e.,

Proof of (15): Let and with , i.e., , then

Then we have

where we have used in the second to last equation that is independent of . Since , for , and are given in (5) and (6), respectively. Before we calculate the probability in the above integrand we make the following notation

It holds

We have

where the last equation follows from the tower property of the conditional expectation since

We obtain

where we have used that is -measurable. The probability in the above equation is rewritten as

where last equation holds since is independent of . Finally, we obtain the following recursion formula

Lemma 3.6 yields

for and zero otherwise. Note that

for and otherwise. Then the probability can be recursively calculated by

since .

Eventually we obtain for and that

Proof of (16): Let and with , i.e., . Then

and we obtain

where is the complementary distribution function of given in Lemma 3.2.

Proof of (17):

Let and . Then

The second to last equation follows by the independence from of and the last equation holds since .

For and with , i.e., , it holds

Using the same arguments as above yields

References

- [1] P. Artzner and F. Delbaen. Default risk insurance and incomplete markets. Mathematical Finance, 5:187 – 195, 12 2006.

- [2] F. Black and J. Cox. Valuing corporate securities: Some effects of bond indenture provisions. The Journal of Finance, 31(2):351–367, 1976.

- [3] F. Black and M. Scholes. The pricing of options and corporate liabilities. Journal of Political Economy, 81(3):637–654, 1973.

- [4] C. Blanchet-Scalliet, C. Hillairet, and Y. Jiao. Successive enlargement of filtrations and application to insider information. Advances in Applied Probability, 49(3):653–685, 2017.

- [5] C. Bluhm and L. Overbeck. Structured Credit Portfolio Analysis, Baskets and CDOs. Chapman and Hall/CRC Financial Mathematics Series. CRC Press, 2006.

- [6] D. Duffie and D. Lando. Term structures of credit spreads with incomplete accounting information. Econometrica, 69:633–664, 2001.

- [7] D. Duffie and K. Singleton. Modeling term structures of defaultable bonds. The Review of Financial Studies, 12(4):687–720, 1999.

- [8] K. Giesecke and L. R. Goldberg. The market price of credit risk : the impact of asymmetric information. Working paper, 2008.

- [9] J. Harrison. Brownian motion and stochastic flow systems. John Wiley & Sons, 1985.

- [10] C. Hillairet and Y. Jiao. Information asymmetry in pricing of credit derivatives. International Journal of Theoretical and Applied Finance, 14, 02 2010.

- [11] C. Hillairet and Y. Jiao. Credit risk with asymmetric information on the default threshold. Stochastics, 84(2-3):183–198, 2012.

- [12] R. Jarrow and P. Protter. Structural versus reduced form models: A new information based perspective. J. Invest. Manag., 2, 07 2004.

- [13] R. Jarrow and S. Turnbul. Credit risk: Drawing the analogy. Risk Magazine, 9(5), 1992.

- [14] M. Jeanblanc and S. Valchev. Partial information and hazard process. International Journal of Theoretical and Applied Finance, 8(6):807––838, 2005.

- [15] M. Jeanblanc, M. Yor, and M. Chesney. Mathematical methods for financial markets. Finance, 31(1):81–85, 2010.

- [16] P. Lakner and W. Liang. Optimal investment in a defaultable bond. Mathematics and Financial Economics, 1(3-4):283–310, 2008.

- [17] D. Lando. On Cox processes and credit risky securities. Review of Derivatives Research, 2:99–120, 1998.

- [18] R. Merton. On the pricing of corporate debt: The risk structure of interest rates. The Journal of Finance, 29(2):449–470, 1974.

- [19] G. Monegato. A note on extended Gaussian quadrature rule. Mathematics of Computation, 30(136):812–817, 1976.

- [20] I. Redeker. Stochastic models in financial risk management. PhD thesis, Brandenburg University of Technology Cottbus-Senftenberg, available at https://opus4.kobv.de/opus4-btu/files/4801/redeker_imke.pdf, 2019.