22email: yq1995@zju.edu.cn 33institutetext: Yu-Ning Li 44institutetext: School of Mathematical Sciences, Zhejiang University, Hangzhou 310027, China.

44email: mark_li@foxmail.com 55institutetext: Yi Zhang 66institutetext: School of Mathematical Sciences, Zhejiang University, Hangzhou 310027, China.

66email: zhangyi63@zju.edu.cn

Change Point Detection for Nonparametric Regression under Strongly Mixing Process

Abstract

In this article, we consider the estimation of the structural change point in the nonparametric model with dependent observations. We introduce a maximum-CUSUM-estimation procedure, where the CUSUM statistic is constructed based on the sum-of-squares aggregation of the difference of the two Nadaraya-Watson estimates using the observations before and after a specific time point. Under some mild conditions, we prove that the statistic tends to zero almost surely if there is no change, and is larger than a threshold asymptotically almost surely otherwise, which helps us to obtain a threshold-detection strategy. Furthermore, we demonstrate the strong consistency of the change point estimator. In the simulation, we discuss the selection of the bandwidth and the threshold used in the estimation, and show the robustness of our method in the long-memory scenario. We implement our method to the data of Nasdaq 100 index and find that the relation between the realized volatility and the return exhibits several structural changes in 2007–2009.

Keywords:

Change point detection CUSUM statistic Nonparametric regression Strongly mixing process Structural changeMSC:

Primary 62G05; Secondary 62G0862G2062M101 Introduction

Structural change is a variation of a system over time, which is usually unexpected but can lead to a huge estimation and prediction error when we specify a time-invariant model. To deal with this, one can divide the sample set into two sub-samples on the time interval, and model each sub-sample separately. The key issue here is how to detect the changes and separate samples. More specifically, one should judge whether the change point exists, and, if it exists, where it is located. Change point detection methods are divided into two main branches: on-line methods, which aim to detect changes as soon as they occur in a real-time setting, and off-line methods that retrospectively detect changes when all samples are received. The former task is often referred to as event or anomaly detection, while the latter is sometimes called signal segmentation. In this paper, our research core is off-line problem with all samples already collected. In addition, we will only focus on abrupt change, though gradual change is another kind of structure change that has attracted extensive attention and research. Readers can refer to Hušková and Steinebach (2002) for the hypothesis test of gradual change.

Structural change, as suggested by the name, is always related to a specific structure. When a parametric model is specified, some of the parameters in the model may change over time. More general, any feature of a structure such as mean, variance and quantile can exhibit changes. Readers can refer to the excellent literature published recently such as Eichinger and Kirch (2018), Wang, Wang and Zi (2019) and Enikeeva and Harchaoui (2019) for mean changes, Xu, Wu and Jin (2019) for variance changes, Zhang and Lavitas (2018) for other quantities of interest, and Zou, Yin, Feng and Wang (2014) for distribution changes. Recently, an analogous mean-change-point setup became very popular in the functional data framework and motivated the new development, see, for instance, Dette, Kokot and Aue (2017) and Aue, Rice and Sönmez (2018).

Regression functions, which describe the relationship between regressand and regressors, of course, can change over time. It is of great interest for researchers to detect the structural change of regression functions, especially the linear ones. For example, Brown, Durbin and Evans (1975) tested the instability of the regression parameters based on the CUSUM of recursive residuals and Ploberger and Krämer (1992) studied CUSUM tests based on OLS residuals without standardising it. More recently, Wu, Zhang, Zhang and Ma (2016) used the jackknife empirical likelihood method for detecting the change in the parameters of the linear regression. Chen and Nkurunziza (2017) studied the multiple change point problem with the change point numbers known. Kaul, Jandhyala and Fotopoulos (2019) considered a high-dimensional case without grid search and they added a change-inducing variable in their linear regression model. In terms of non-linear regressions, Gurevich and Vexler (2005) studied the structural change of the logistic regression.

The most researches are devoted to the structural change of the parametric model, resulting in relatively few results and literature in the field of the structural change of the nonparametric models. To detect the changes in the nonparametric model, Su and Xiao (2008) proposed a CUSUM test and Mohr and Neumeyer (2019) modified it to achieve consistency. However, they did not estimate the changes after the change points were found. Wang (2008) studied the weak consistency of the change point estimator for a long-memory process, which motivates our change-point estimation research. Recently, Mohr and Selk (2020) proposed an estimator based on Kolmogorov-Smirnov functional of the marked empirical process of residuals.

The existing change point literature usually falls into two main categories: the change point detection and the change point estimation. The change point detection is usually performed by the means of some statistical test, while the change point estimation tries to locate the change points. We investigate both aspects of the change point problem by using a threshold-based method, which was developed by Fryzlewicz (2014), Cho and Fryzlewicz (2015) and Cho (2016). This method does not require a prior knowledge that the change point is really present in the model. With some ad-hoc threshold, consistency of the estimator is guaranteed, and no formal statistical test is implemented to controls Type I errors. We emphasize that the threshold method is consistent in estimating the number of change points. If there are multiple change points, though it is not investigated in this paper, the binary segmentation method can be used. Interested readers can refer to Venkatraman (1992), Bai (1997), Cho and Fryzlewicz (2012), Killick, Fearnhead and Eckley (2012), Fryzlewicz (2014) and the references therein.

We will investigate the following nonparametric model with a structural change,

| (1.1) |

where is the regressand and is the regressor, and are two different regression functions, and is an unknown change point.

It is important to make it clear that the problem we focus on is different from regression discontinuity. Regression discontinuity assumes a discontinuous regression function, and is prevailing in the treatment-effect analysis, see Müller (1992) and Qiu, Zi and Zou (2018) for fixed-design setting, Huh and Park (2004) for random-design setting, Wu and Chu (1993) and Braun and Müller (1998) for multiple discontinuity points detection problem, and Choi and Lee (2017) for reviews. Discontinuity points in a regression function are sometimes referred to as change points as well, so they can be ambiguous. For instance, Hušková and Maciak (2017) considered a nonparametric regression with -mixing dependence, which seems similar to this paper, but they investigated the discontinuities, which is fundamentally different. Delgado and Hidalgo (2000) tried to estimate the change points and discontinuity points in a uniform framework by estimating the right and left limits of an extended regression function including the scaling time as an extra variable. This method is very common in regression discontinuity, but does not take into account the priori information that the regression function is indeed not changed in two subsamples. In other words, the extended regression function is flat in the direction of time variable. Therefore the locally comparison method is intuitively not optimal which only uses limited data and information. In comparison, our method still identifies two regression functions before and after the change point rather than one discontinuity but time-invariant regression function. To estimate the change point, two regression functions are estimated using subsamples and compared across the entire domain of the covariate.

We make the following contributions. Firstly, we construct a CUSUM statistic to detect the structural change in the nonparametric regression model. The CUSUM statistic is aggregated using the sum-of-squares, which does not focus on only one extremal point like Wang (2008). Secondly, we not only establish the consistency of the change point estimator but also derive an asymptotic upper bound of the CUSUM statistic when there is no change point and an asymptotic lower bound when there is a change point. This result leads to a threshold method that can judge whether there is a change point. We show in the simulation that our method makes few false positive and false negative determinations. Last but not least, we show a surprising result that the CUSUM statistic constructed by the Nadaraya-Watson (N-W) estimator performs better than that constructed by the local linear estimator, because the N-W estimator is more sensitive to the observations or outliers which do not belong to the same stable period.

In Section 2, we introduce the basic preliminary of the nonparametric model and propose a sum-of-squares aggregated CUSUM statistic to locate the position of change point. In Section 3, we propose a threshold method based on the CUSUM statistic to detect whether the regression function changes over time. Under strongly mixing assumption, some asymptotic results are established. In Section 4, we do simulations and show how the bandwidth and the threshold in the estimation can be selected in practice. We show that our method has a superb performance in comparison with Wang (2008)’s method and the method of the local linear estimation. Section 5 is an application of our method to real data. Section 6 concludes. To keep fluency, we relegate all proofs in the appendix.

For convenience, we unify the notations in the rest part of this paper as below:

-

1. Denote the largest integer not greater than as .

-

2. Let denote a bivariate function .

-

3. Denote the support of a variable as . Let denote the set composed by the interior points of a set .

-

4. Let denote the -norm, where is a measurable function on a measure space , and . When , we denote .

-

5. Suppose that and are two scalar sequences. Define when , where is some nonzero constant.

-

6. Suppose that and are two random variable sequences. Denote when there exists a positive constant satisfying that almost surely for large enough, and when almost surely.

Besides, all asymptotics are discussed when the sample size without any special statement.

2 Preliminary and methodology

We denote the number of change point as . If , there is no change. We can write the conventional nonparametric regression model without a change as below,

| (2.1) |

where is the stationary observation at time , is the conditional mean of on , that is, , and is the residual, that is, .

Let and be the joint density of and density of , respectively. Using the fact that the conditional mean function can be written as , where , one can construct the classical N-W kernel regression estimator (refer to Nadaraya (1964) and Watson (1964)) as follows (using the sample from time to in this case),

| (2.2) |

with

| (2.3) |

and

| (2.4) |

where is a kernel function, is a bandwidth, and . Note that and are the estimators of and , respectively.

Now we consider the case when there is only one change point, that is, . If the regression function is not invariant in the whole time period but changes after time , we can create a model as below:

| (2.5) |

where . Note that at this stage we allow the change of the distribution of at . In order to identify the model, an overlapping condition is necessary for the supports of before and after the change point. However, if the distribution of changes, the change point detection is much easier, which reduces to a distributional change problem. For this reason, we assume that the distribution of does not change over time. We refer to Mohr and Selk (2020) for the case that the distribution of may change as well. Similarly, we should not only focus on the change of the distribution of . There are many examples, e.g. , and , in which it is impossible to detect the regression function change by only detecting the distributional change of .

Next we construct a CUSUM statistic. Inspired by the statistic due to Wang (2008), which is defined by

| (2.6) |

we define a CUSUM statistic using sum-of-squares as follows,

| (2.7) |

for , where are chosen grid points at which the function is estimated to detect whether a change point exists.

The choice of using supremum or sum-of-squares to aggregate the CUSUM statistic depends on the behavior of the two regression functions. If the magnitude of the change is small in the whole domain of the function, then the cumulation by sum-of-squares is a better choice. If the change of the function is spiky and local, then the supremum method is better. Thus, the choice of the two methods depends on the model of research and the volatility of data.

We shall also note that when supremum is used to aggregate the CUSUM statistic, the maximum on pre-determined grid points is used in the algorithm for discretization. Therefore, no matter supremum or sum-of-squares is used, we have to introduce the grid points. The requirement for the grid points is that for some . In practice, we can use equidistant grid points to cover the whole support of . If we have prior information, it will be more efficient if we only use the grids points where the change of the regression function may occur. For simplicity, we assume that does not change with . If increases with , the theoretical results will be more complex and it will be more time-consuming during the computation when is large. We will show in the simulation that the number of does not matter much to the empirical results.

After we construct the detection statistic, we obtain the estimator for the change point by maximizing with respect to , that is,

| (2.8) |

where is an integer growing with , which is introduced to deal with the time-boundary effect. When is close to or , we will have inadequate samples to estimate either or . Then it will be unable to detect the change by using the CUSUM statistic. For this reason, we only detect change points which is not close to the time boundary. We note that the weight in the CUSUM statistic, similar to Wang (2008), is also introduced to deal with the time-boundary effect. These two strategies are commonly used, see discussion in Appendix D of Barigozzi, Cho and Fryzlewicz (2018) for and Cho (2016) for an alternative choice of weights.

3 Asymptotics

Before introducing the related theorems, we will make the following assumptions for the purpose of asymptotic analysis.

Assumption 1

(PSM) The process is strictly stationary and is strongly mixing dependent with the mixing coefficient decaying to zero at a polynomial rate, that is, with some constant and constant .

Assumption 2

(GSM) The process is strictly stationary and is strongly mixing dependent with the mixing coefficient decaying to zero at a geometric rate, that is, with some constant and constant .

Assumption 3

Suppose that , where satisfies that for PSM, or for GSM.

Assumption 4

Let the kernel function be a symmetric nonnegative function satisfying that and .

Assumption 5

Suppose that and defined in the model (2.1) are uniformly bounded and denote as the joint density of . Define the bivariate function , and

where and are the joint densities of and , respectively. Assume that for some constants and , and . In addition, if the data is PSM, we define and , and require that and , where is defined in Assumption 1.

Assumption 6

Suppose that and , where and are positive constants.

If there is a change point, and may change over time. Assumptions 5 and 6 should hold true separately on the subsamples before and after the change point. In addition, if a change happens, we assume that:

Assumption 7

Let the time-scaled change point located at with for some . Let and . We assume that is non-empty, and and , which are two bounded functions, do not change with .

Assumption 8

The grid points satisfy that and at least for some grid point . The number of grid points is not dependent on .

The condition of the mixing dependence on in Assumption 1 (or 2) is very common and covers some commonly-used time series models such as ARMA process (Bosq (1998)) and GARCH process (Basrak, Davis and Mikosch (2002)). Bosq (1998) investigated the nonparametric N-W estimation for GSM and Johannes and Rao (2011) extended it to PSM. The condition that is stationary guarantees that is stationary before and after the change, respectively. Assumptions 3 is some restrictions on the bandwidth. Given the order of , it holds true that , which has been used in Chapter 2 of Bosq (1998) to obtain the upper bound of defined in Lemma 1. The condition on the kernel function in Assumption 4 is very mild, which is satisfied by commonly-used kernels. Assumption 5 is a technique requirement which refers to the same assumption in Bosq (1998) and Johannes and Rao (2011), and it is used by us to bound the variance and covariance of and together with Assumption 6. If there is no change point, Assumptions 3–6 guarantee the uniform bound of and .

In Assumption 7, what one should note is that we do not have to require that , or are continuous or differentiable as many researchers did. If and are discontinuous functions, the local estimator estimates a smoothing version of and . We can still detect the change point by comparing the two estimates. Assumption 8 suggests that, if a change happens, it is enough for our detection method to locate the change point, as long as there is a grid point on which the values of and are not identical. This quality releases the selection of the grid points extremely. As we have mentioned before, we can choose the equidistant grid points covering the main region between the minimum and the maximum of the collected . In this case, the grid points can cover each local region and probably some of them lie in .

Recall that, if , it means that no change appears, and the structure is of form as the model (2.1). If , it means that a change appears, and the structure is of form as the model (2.5). We have the following results for these two cases.

Theorem 3.1

When there is a change point, define

for . Indeed, if and are differentiable functions, we have by integration and Taylor expansion that

Thus can be seen as a smooth version of . We have the following theorem.

Theorem 3.2

We can see from Theorem 3.2 that the CUSUM statistic is larger if is larger or if is close to 0.5. This means that it is easier to detect a change point if the change is larger in magnitude, or if the change point locates in the middle of the sample set.

With probability one, Theorem 3.1 shows the asymptotic order of the CUSUM statistic when . There exists a constant satisfying that asymptotically. Theorem 3.2 shows that our CUSUM statistic has an asymptotic lower bound when , and this lower bound is a constant and thus is larger than the order in Theorem 3.1 as . Therefore, we can find an appropriate threshold between and when is large enough. Since both and are unobservable, we will use a permutation method to set the threshold for our method in the simulation and real data analysis.

We determine the value of by comparing with the threshold . When , we set , otherwise . Then we derive the strong consistency of as follows.

Theorem 3.3

We will show the determination of the threshold in the simulation.

4 Practicalities and simulation studies

In Section 4.1, we discuss the choice of the bandwidth and the threshold . We compare the estimation precision of several detection methods in Section 4.2. The Epanechnikov kernel function is used in the N-W estimation throughout the whole simulation. In terms of the grid points, which are related to and in Assumption 7, we choose equidistant points between 5th percentile and 95th percentile of as the grid points, respectively, to construct the CUSUM statistic in (2.7). We figure out that the results are similar to each other and thus set hereafter.

Two data generation processes (DGP), the ARMA process and the ARFIMA process, are used throughout our simulation. The former is a strongly mixing process, see the argument in S.4 of Bosq (1998), which matches Assumption 2 in Section 3. The latter is not a strongly mixing process but a long-memory one which Wang (2008) has studied. That helps us to show the robust application of our proposed method. The long-memory assumption together with ARFIMA DGP (see Hosking (1981) for detail) is introduced to the nonparametric change-point-detection problem by Wang (2008). Because Wang (2008)’s method is based on the N-W estimation as we do but uses supremum to construct the CUSUM statistic, we denote it as “nwsup”. In contrast, our method is denoted as “nwss”, where “ss” means “sum-of-squares”.

During our research, we ever planed to replace the N-W estimator with the local linear estimator in constructing the CUSUM statistic. We replace the N-W estimators in “nwsup” or “nwss” by the local linear estimators in the change-point-detection procedure to obtain the new methods which we denote as “llsup” and “llss”, respectively. Nevertheless, we will see later in our simulation that it does not promote performance result, compared with our current method.

Two nonparametric structural changes are considered:

(i) The first DGP is

| (4.1) |

The relation between and changes from a linear pattern to a quadratic one. This DGP is constructed to show the detectable property of our method even if does not change.

(ii) To show the extent of detectable structural change, the second DGP allows different scales of the change of , which is given by

| (4.2) |

where determines the magnitude of the change of the regression function.

For each model, we simulate by an ARMA(1,1) process or an ARFIMA(0,0.15,0) process:

(i) The ARMA(1,1) process is given by

| (4.3) |

where is the time-shifting operator, is generated from an independent normal distribution with mean 0 and variance , and is generated from an independent normal distribution with mean 0 and variance 0.25. Note that in this case and , therefore in the model (4.1) does not change over time but changes in model (4.2).

(ii) The ARFIMA(0,0.15,0) process is given by

| (4.4) |

where is generated from an independent normal distribution with mean 0 and variance . In the meantime, is generated from an ARFIMA(0,0.35,0) process as follows,

| (4.5) |

where is generated from an independent normal distribution with mean 0 and variance 0.01. The setting of variance still leads that and (one can refer to the statement about the variance of ARFIMA process in Hosking (1981)). Thus in the model (4.1) does not change over time , while changes slightly in the model (4.2).

To quantify the performance of each method, before exhibiting our simulation, we introduce some notations. Let the change point estimate of the -th experiment be , for , where is the number of experiments. We show the consistency of the estimator by using “Bias”, which is defined as . We compare different methods by using absolute bias (ABias), which is defined as . The sample standard deviations of and are denoted as “BiasSd” and “ABiasSd”, respectively.

4.1 Selection of bandwidth and threshold

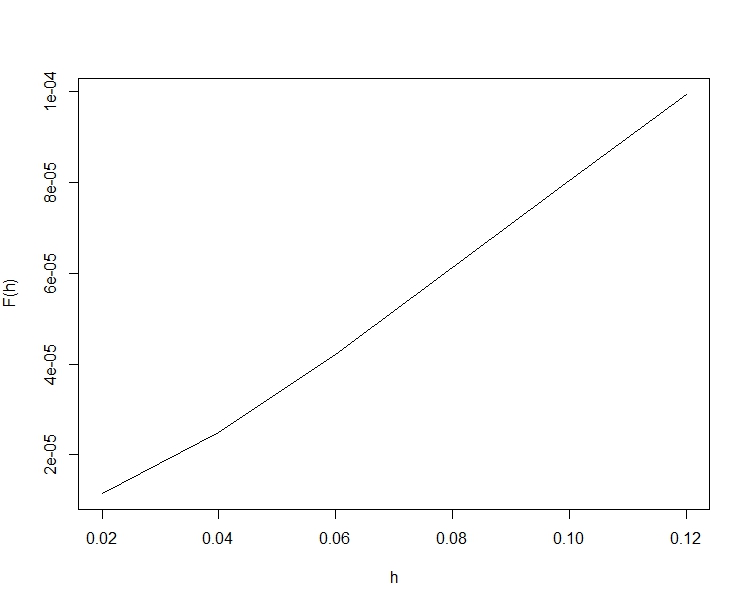

The bandwidth used in the change point detection can be different from that used in the nonparametric regression. Our aim is not to find a better regression curve, say in the sense of least MSE or some other criteria, but to make the change most detectable. In the case when the unconditional mean of changes, one can always benefit from choosing a large . This is because the nonparametric curve degenerates to a horizontal line when tends to infinity, and detecting the change point in the conditional mean is actually a parametric problem which naturally has a better solution in the sense of the asymptotics.

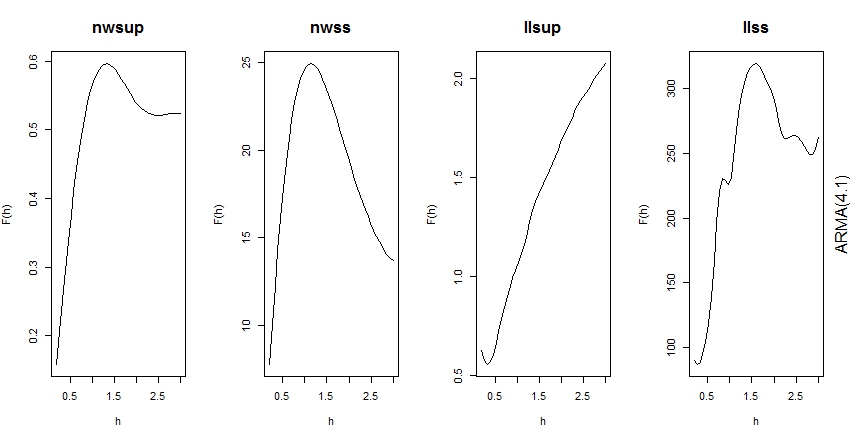

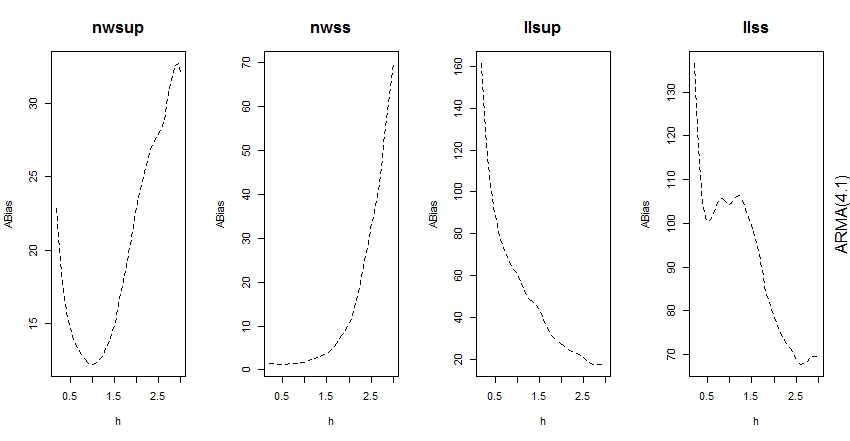

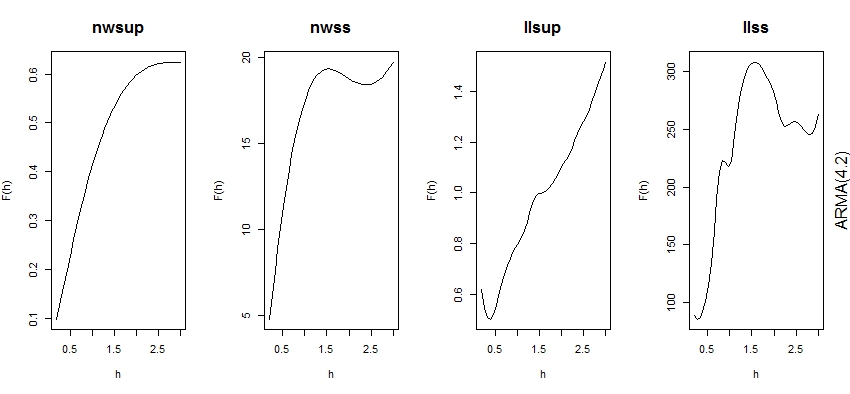

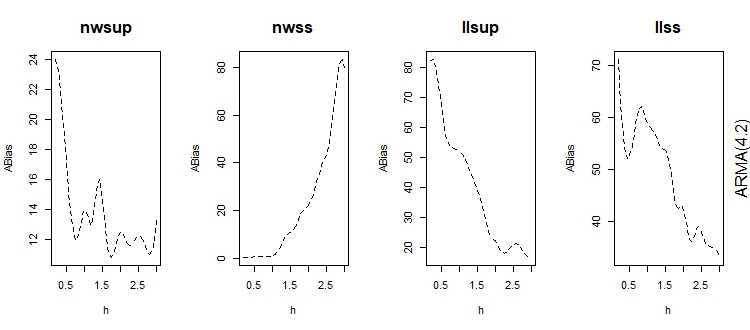

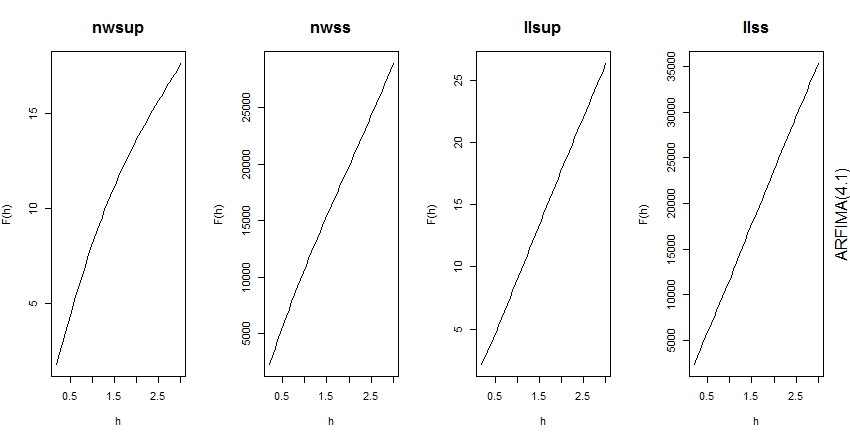

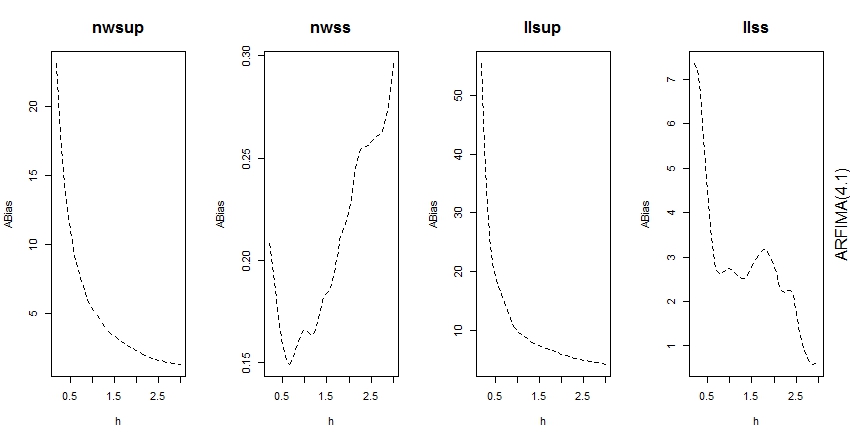

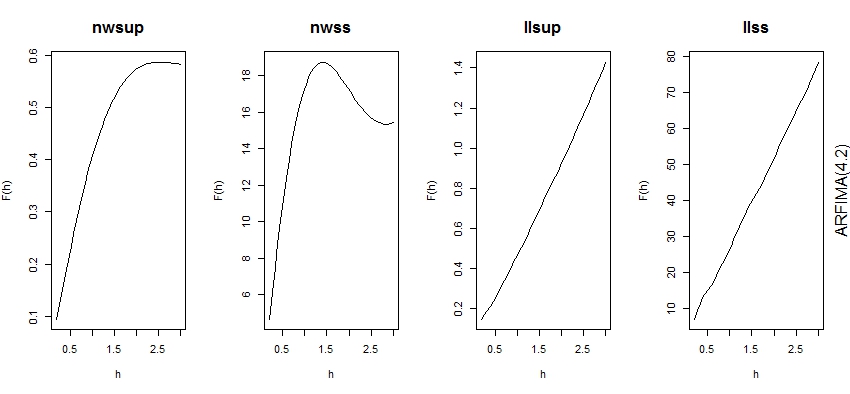

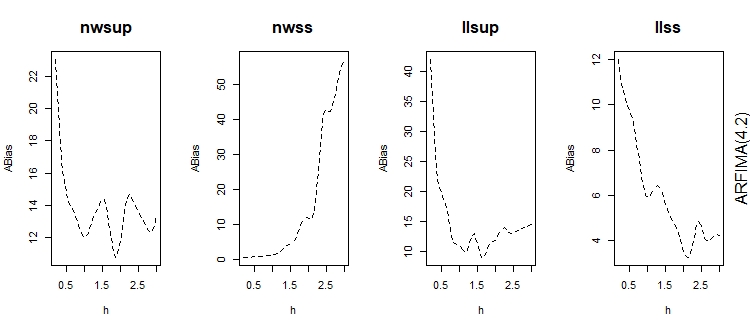

We want to find a data-driven procedure to select a bandwidth before knowing whether the unconditional mean of changes. We may find some clues from Theorem 3.1 and 3.2. When there is no change point, the order of is . The first idea one could think of is to find the that maximize . However, when there is no change point, this criterion leads to a tiny bandwidth. To fix it, we maximize to find a bandwidth. We have a.s. from Theorem 3.1, where is a positive constant, showing that the order of is no longer dependent on . Indeed, the procedure can be seen as trying to find the potential for the inequality. We avoid using too large and only consider smaller than . In Figure 1 and 2, we show that how the maximum point of and the minimum point of “ABias” match each other under different models and data. Specifically, we set sample size , in the model (4.2) and the relative position , and replicate experiments times for each . The average of experimental results is considered as for each . Note that we do not consider the threshold temporarily and determine the maximizer of as the change point.

In most cases, the maximizer of is near the minimizer of ABias. Particularly, when increases monotonically, ABias tends to decrease monotonically or retains in a range of low ABias. That is, we can take the maximizer of as the bandwidth to ensure the least or low ABias, which we cannot compute in reality. It seems to justify our bandwidth-choosing strategy. Thus, we use this method to determine the bandwidth of the real data demonstrated in the next section. In our simulation, without loss of generality, we take to proceed our simulation since each method has a relatively low ABias.

Now, we use bootstrap to determine the threshold of our method “nwss”. Specifically, we resample 200 sets of samples without replacing (which is a permutation essentially) and compute the 200 values of . Then we define the 99th percentile of ’s as the threshold, which is an approximation of the order in Theorem 3.1. To show the performance of our detection and threshold determination, we replicate 500 detection experiments for each specification defined in Section 4.1. For each case, the percentage of experiments determining a change happens, denoted as PDC, is shown in Table 1, that is, the percentage of . PDC shows the rate of the true positive results when there is a change point or the rate of the false positive results when the system is stable and it can measure the detection performance well.

From the table, we can see that: (i) When the structural change is large, e.g., the model (4.1) and the model (4.2) with or 0.5, our method can detect nearly all the changes. (ii) When there is no change point, the rate of the false positive results is approximately 2% for strongly mixing process. (iii) The accuracy increases with the sample size. (iv) When the change point is not around the center (), the rate of the true positive results is slightly inferior than that when but remains good as long as the sample size is relatively large. Note that the results are the same for and when .

These results are in compliance with the theoretical results. The larger the sample size is, the more accuracy our method is. It is possible to repeat the resample in the bootstrap procedures more times and select a larger threshold, for example 99.9th percentile. When sample size is large enough, we are able to find a proper threshold. According to Theorem 3.1 and 3.2, should be less than the threshold if there is no change and exceed the threshold when the change point exists.

We conclude that, although our research detection is performed by threshold method rather than hypothesis testing, our method still has a nice rate of the true positive and a low rate of the false positive to distinguish whether there is a change point.

| model | PDC() | PDC() | |||||

|---|---|---|---|---|---|---|---|

| ARMA | 4.1 | 0.982 | 1 | 1 | 0.940 | 1 | 1 |

| 0.888 | 0.998 | 1 | 0.722 | 0.956 | 1 | ||

| 0.678 | 0.924 | 1 | 0.562 | 0.748 | 0.942 | ||

| 0.036 | 0.264 | 0.108 | 0.014 | 0.234 | 0.064 | ||

| 0.018 | 0.012 | 0.016 | 0.018 | 0.012 | 0.016 | ||

| ARFIMA | 4.1 | 1 | 1 | 1 | 0.992 | 1 | 1 |

| 0.822 | 1 | 1 | 0.426 | 1 | 1 | ||

| 0.132 | 0.986 | 1 | 0.090 | 0.700 | 0.998 | ||

| 0.056 | 0.102 | 0.082 | 0.046 | 0.060 | 0.052 | ||

| 0.042 | 0.030 | 0.024 | 0.042 | 0.030 | 0.024 | ||

4.2 ARMA and ARFIMA processes with a change point

After judging whether there is a change point, to compare the estimation precision of the four methods,“nwss”, “nwsup”, “llss” and “llsup”, we do additional simulations under different model settings as below.

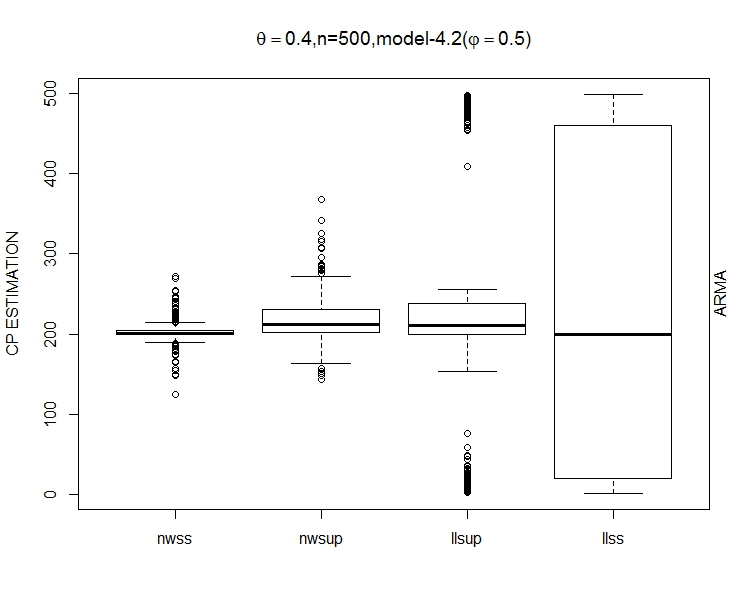

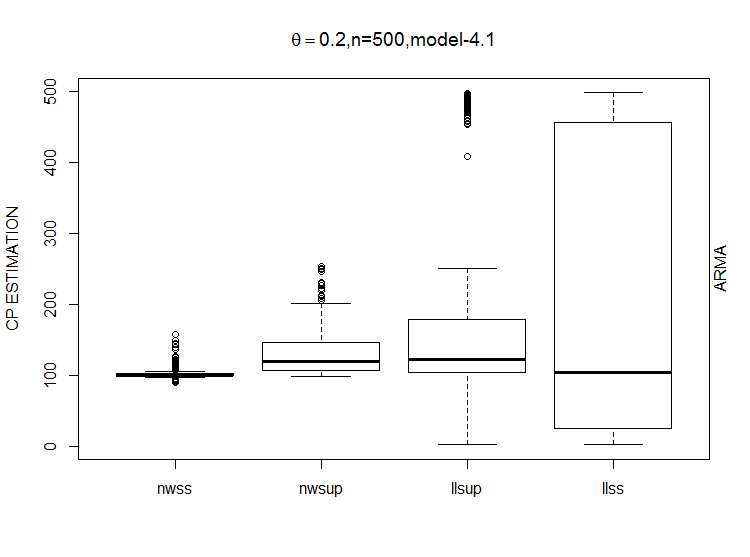

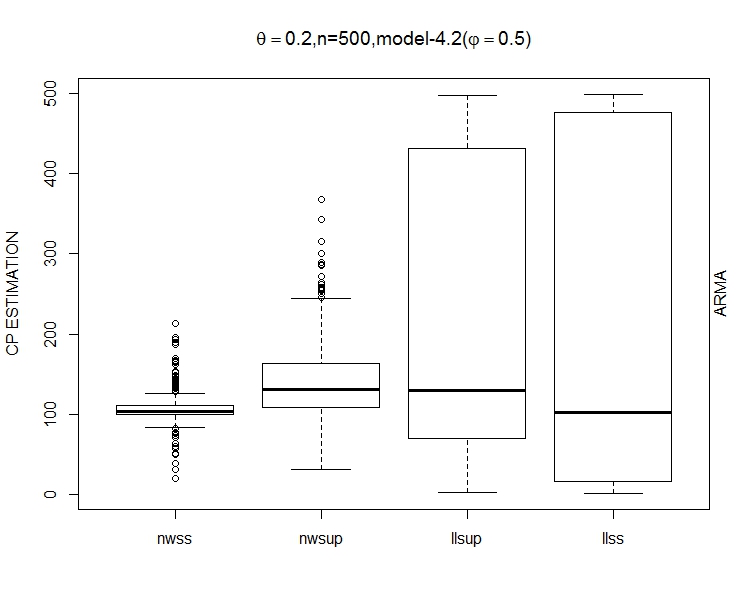

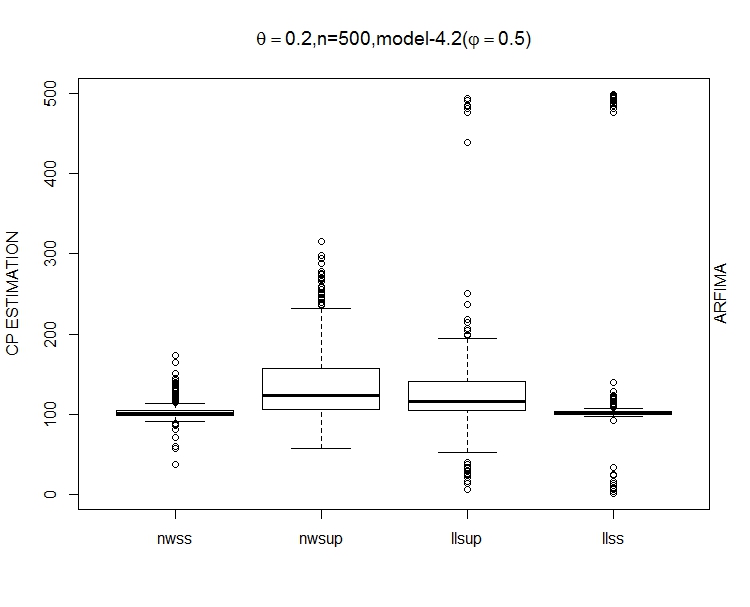

Firstly, we generate ARMA DGP with the change point at and 0.4, and take the sample size and . We replicate 500 experiments for each case. The Bias and ABias of the estimators are shown in Table 2. For saving space and because of similarity, we select the case when with the model (4.1) and the model (4.2) (), respectively, and plot the box-plots of the change point estimates in Figure 3. Note that the estimates outside from the median are marked by the void circle as outliers, where means the interquartile range.

We can see from the table that “nwss” performs best among all cases and “nwss” estimator has far smaller “Bias” and “ABias” than other three methods. When the change point is near time boundary (), the performance is still not bad as long as the structural change or sample size is not too small, despite it is inferior to that when the change point is about the central position. Intuitively, the local linear estimation may be superior to the N-W estimation. However, the result is opposite when they are introduced in the change-point detection procedure. Large “Bias”, “BiasSd”,“ABias” and “ABiasSd” are witnessed in most cases. We may call this phenomenon as the local linear paradox.

It is well known that the local linear fit is less influenced by outliers than the N-W fit, that is, the N-W estimation is more sensitive to outliers than the local linear estimation. Thus, we suspect that, when we use the local linear estimation, is flat around and probably reaches the maximum at other time point when some stochastic errors exist. Thus, we will get the wrong estimate of the change point. While using N-W estimation, decreases quickly at around because of its sensitivity property, and we can obtain the maximum at the change point . The stability advantage of the local linear fit develops disadvantage in this change-point detection and the local linear regression cannot be applied well to our detection in practice.

| n | Model | Method | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | BiasSd | ABias | ABiasSd | Bias | BiasSd | ABias | ABiasSd | |||

| n=200 | 4.1 | nwss | 2.126 | 7.233 | 2.802 | 6.998 | 5.278 | 14.034 | 5.938 | 13.767 |

| nwsup | 9.406 | 8.813 | 9.570 | 8.634 | 22.110 | 22.453 | 22.158 | 22.406 | ||

| llsup | 14.020 | 58.129 | 43.864 | 40.595 | 42.094 | 66.791 | 55.826 | 55.800 | ||

| llss | 12.686 | 68.348 | 51.760 | 46.343 | 42.170 | 76.537 | 60.950 | 62.590 | ||

| 4.2 | nwss | 2.013 | 16.465 | 8.963 | 13.951 | 8.313 | 22.781 | 12.722 | 20.638 | |

| () | nwsup | 9.646 | 17.357 | 14.086 | 13.988 | 28.978 | 28.889 | 30.434 | 27.347 | |

| llsup | 14.106 | 68.767 | 57.806 | 39.750 | 47.644 | 74.360 | 66.068 | 58.568 | ||

| llss | 14.362 | 74.272 | 61.334 | 44.201 | 43.322 | 80.185 | 65.522 | 63.313 | ||

| 4.2 | nwss | 2.0678 | 34.870 | 23.277 | 26.015 | 21.871 | 47.352 | 30.505 | 42.289 | |

| () | nwsup | 11.788 | 27.759 | 21.620 | 21.011 | 41.736 | 39.748 | 43.928 | 37.307 | |

| llsup | 16.316 | 76.542 | 69.908 | 35.050 | 53.682 | 79.217 | 74.818 | 59.615 | ||

| llss | 14.042 | 82.441 | 75.686 | 35.416 | 51.082 | 85.440 | 77.166 | 62.834 | ||

| n=500 | 4.1 | nwss | 1.192 | 3.463 | 1.788 | 3.196 | 2.728 | 6.877 | 3.236 | 6.653 |

| nwsup | 12.228 | 12.586 | 12.236 | 12.578 | 30.756 | 30.899 | 30.768 | 30.887 | ||

| llsup | 24.812 | 109.096 | 60.748 | 93.921 | 73.770 | 141.537 | 95.658 | 127.737 | ||

| llss | 16.688 | 158.394 | 104.268 | 120.308 | 77.944 | 183.979 | 126.028 | 154.986 | ||

| 4.2 | nwss | 3.098 | 12.404 | 6.889 | 10.767 | 6.845 | 18.480 | 10.949 | 16.381 | |

| () | nwsup | 17.996 | 26.223 | 21.656 | 23.286 | 43.352 | 46.817 | 45.264 | 44.968 | |

| llsup | 25.834 | 146.082 | 99.294 | 110.134 | 93.622 | 176.052 | 135.626 | 146.102 | ||

| llss | 21.488 | 174.659 | 126.644 | 122.056 | 87.646 | 197.860 | 144.898 | 160.649 | ||

| 4.2 | nwss | 4.359 | 46.524 | 24.038 | 40.055 | 14.403 | 69.204 | 32.088 | 62.967 | |

| () | nwsup | 19.922 | 46.556 | 35.034 | 36.542 | 71.740 | 79.929 | 76.080 | 75.801 | |

| llsup | 36.958 | 180.757 | 146.014 | 112.601 | 115.930 | 198.597 | 172.182 | 152.320 | ||

| llss | 27.194 | 204.130 | 173.426 | 110.786 | 108.079 | 217.664 | 182.138 | 160.752 | ||

| n=1000 | 4.1 | nwss | 1.732 | 4.743 | 2.280 | 4.505 | 2.188 | 5.593 | 2.504 | 5.462 |

| nwsup | 15.914 | 18.122 | 15.930 | 18.108 | 42.434 | 45.790 | 42.442 | 45.783 | ||

| llsup | 31.280 | 159.419 | 67.836 | 147.593 | 94.096 | 221.589 | 121.688 | 207.691 | ||

| llss | 41.962 | 282.981 | 160.130 | 236.959 | 132.434 | 342.388 | 202.526 | 306.112 | ||

| 4.2 | nwss | 3.464 | 9.112 | 5.616 | 7.965 | 6.730 | 16.901 | 9.570 | 15.469 | |

| () | nwsup | 25.676 | 35.052 | 28.544 | 32.754 | 61.428 | 72.720 | 62.800 | 71.536 | |

| llsup | 37.054 | 228.565 | 119.742 | 198.119 | 137.230 | 305.007 | 191.638 | 274.044 | ||

| llss | 45.342 | 312.549 | 196.314 | 247.246 | 148.852 | 373.300 | 243.264 | 319.779 | ||

| 4.2 | nwss | 4.404 | 33.797 | 16.152 | 30.005 | 6.615 | 38.622 | 22.373 | 32.154 | |

| () | nwsup | 32.278 | 59.658 | 46.874 | 49.005 | 96.584 | 113.546 | 100.448 | 110.136 | |

| llsup | 62.740 | 305.363 | 203.232 | 236.230 | 175.600 | 360.074 | 262.188 | 302.771 | ||

| llss | 64.268 | 384.523 | 299.620 | 249.088 | 202.762 | 425.231 | 332.922 | 333.103 | ||

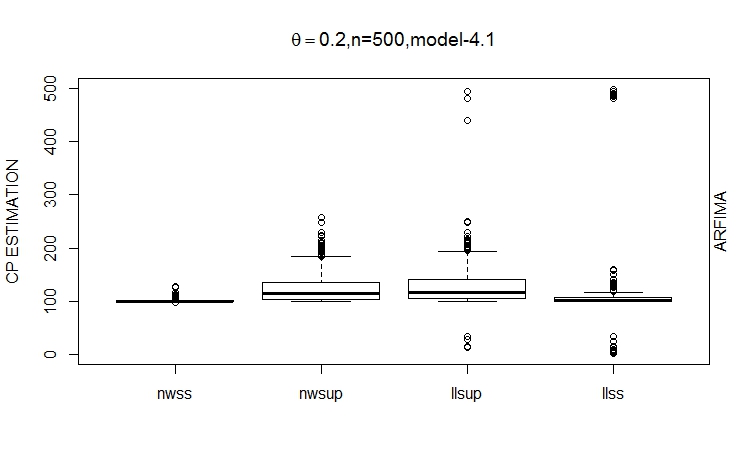

To compare our method “nwss” with “nwsup” in Wang (2008), we consider the long-memory DGP given by (4.4) and (4.5). The results are shown in Table 3 and Figure 4. Even for the long-memory data, “nwss” still has a superb performance with few big deviations as long as the structural change is not too tiny. While the method “nwsup” has relatively big bias and standard deviation. Also, the local linear paradox remains exist.

| n | Model | Method | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bias | BiasSd | ABias | ABiasSd | Bias | BiasSd | ABias | ABiasSd | |||

| n=200 | 4.1 | nwss | 0.786 | 1.870 | 0.858 | 1.838 | 1.745 | 4.203 | 1.806 | 4.177 |

| nwsup | 6.698 | 7.370 | 6.702 | 7.367 | 16.330 | 19.211 | 16.334 | 19.207 | ||

| llsup | 7.146 | 16.438 | 9.794 | 15.009 | 17.624 | 26.318 | 19.608 | 24.844 | ||

| llss | 0.700 | 21.658 | 6.056 | 20.804 | 8.528 | 30.962 | 11.856 | 29.844 | ||

| 4.2 | nwss | 1.673 | 10.756 | 4.861 | 9.737 | 6.807 | 22.572 | 9.718 | 21.475 | |

| () | nwsup | 7.106 | 14.642 | 10.890 | 12.090 | 23.486 | 27.060 | 24.798 | 25.860 | |

| llsup | 7.448 | 26.129 | 13.888 | 23.346 | 21.586 | 36.812 | 25.422 | 34.270 | ||

| llss | 1.394 | 28.162 | 9.482 | 26.551 | 7.820 | 34.338 | 12.140 | 33.056 | ||

| 4.2 | nwss | 4.227 | 40.089 | 23.409 | 32.693 | 23.933 | 53.243 | 32.733 | 48.216 | |

| () | nwsup | 9.984 | 25.850 | 18.652 | 20.482 | 33.624 | 36.117 | 35.928 | 33.821 | |

| llsup | 10.890 | 39.516 | 23.346 | 33.679 | 28.224 | 48.451 | 35.040 | 43.766 | ||

| llss | 5.010 | 41.815 | 19.53 | 37.298 | 16.232 | 51.461 | 24.752 | 47.941 | ||

| n=500 | 4.1 | nwss | 0.922 | 1.999 | 0.954 | 1.984 | 1.162 | 2.728 | 1.182 | 2.719 |

| nwsup | 8.904 | 9.966 | 8.904 | 9.966 | 24.362 | 27.943 | 24.370 | 27.936 | ||

| llsup | 11.076 | 24.188 | 13.168 | 23.114 | 28.236 | 39.803 | 29.464 | 38.901 | ||

| llss | 0.696 | 37.550 | 6.708 | 36.952 | 11.318 | 59.164 | 15.502 | 58.206 | ||

| 4.2 | nwss | 1.506 | 6.405 | 3.730 | 5.419 | 3.544 | 10.613 | 5.792 | 9.572 | |

| () | nwsup | 13.208 | 21.384 | 15.984 | 19.393 | 38.590 | 44.179 | 39.530 | 43.338 | |

| llsup | 10.114 | 29.557 | 12.210 | 28.753 | 27.186 | 52.429 | 32.262 | 49.462 | ||

| llss | 2.256 | 52.782 | 12.024 | 51.441 | 13.924 | 76.997 | 20.320 | 75.558 | ||

| 4.2 | nwss | 2.184 | 25.692 | 11.762 | 22.939 | 5.550 | 41.453 | 16.631 | 38.258 | |

| () | nwsup | 18.374 | 34.478 | 26.066 | 29.090 | 58.748 | 66.250 | 62.484 | 62.731 | |

| llsup | 8.156 | 53.917 | 21.940 | 49.914 | 39.048 | 83.426 | 49.576 | 77.620 | ||

| llss | 6.146 | 78.835 | 25.726 | 74.764 | 25.374 | 107.586 | 38.206 | 103.717 | ||

| n=1000 | 4.1 | nwss | 0.921 | 1.998 | 0.938 | 1.991 | 1.346 | 2.934 | 1.354 | 2.930 |

| nwsup | 11.548 | 13.829 | 11.548 | 13.829 | 33.014 | 38.612 | 33.014 | 38.612 | ||

| llsup | 15.088 | 28.843 | 15.088 | 28.843 | 39.944 | 53.390 | 40.628 | 52.871 | ||

| llss | 1.368 | 56.758 | 7.500 | 56.276 | 15.296 | 101.836 | 20.520 | 100.912 | ||

| 4.2 | nwss | 1.198 | 5.542 | 3.138 | 4.721 | 2.898 | 9.249 | 5.006 | 8.298 | |

| () | nwsup | 14.156 | 23.915 | 16.780 | 22.149 | 54.828 | 64.433 | 55.952 | 63.457 | |

| llsup | 9.540 | 36.459 | 12.492 | 35.554 | 39.848 | 64.470 | 41.912 | 63.145 | ||

| llss | 2.424 | 79.112 | 13.268 | 78.027 | 13.556 | 114.871 | 22.468 | 113.462 | ||

| 4.2 | nwss | 2.610 | 29.752 | 8.870 | 28.516 | 5.829 | 45.781 | 13.036 | 44.268 | |

| () | nwsup | 17.814 | 44.65646 | 29.966 | 37.582 | 75.358 | 90.264 | 77.698 | 88.253 | |

| llsup | 10.604 | 60.211 | 18.692 | 58.206 | 51.374 | 102.357 | 57.290 | 99.161 | ||

| llss | 9.254 | 127.826 | 32.570 | 123.945 | 34.000 | 177.884 | 49.164 | 174.296 | ||

In conclusion, on one hand, our method is superior to other methods in each case and it performs well as long as the structural change is not too tiny and the change point is not too close to the edge, and the robust application to the long-memory data has been shown by ARFIMA DGP. On the other hand, “nwsup” tends to have a relatively bad performance. Last but not least, “llss” does not promote the effect and even results in big deviations in most cases, which pushes us only to use the simpler N-W estimation.

5 Real data analysis

We apply our method to the Nasdaq 100 index for finding the structural change between the return volatility and the return. The relation between volatility and return is sometimes referred to as leverage effect, which can be illustrated as an asymmetric U-shaped curve. This relation can be time-varying, see for example Bandi and Renò (2012) and Jin (2017).

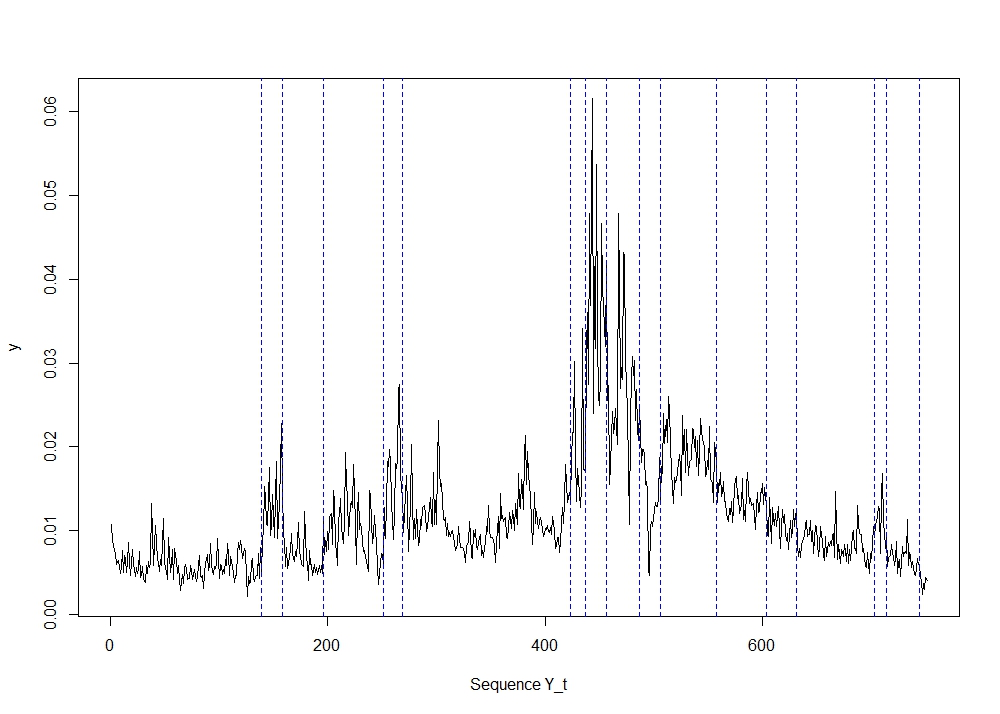

The volatility is inherently unobservable and we consider the realized volatility as the proxy of the return volatility. A discussion in gauging return-volatility regressions using different volatility measures can be found in Bollerslev and Zhou (2006). We take the three-year Nasdaq 100 index data from 2007–2009 as the sample (reader can acquire the data from the site https://realized.oxford-man.ox.ac.uk/data), and set its realized volatility as and return as . We plot the sequence and in Figure 6, and think that there probably exists multiple change points. The dotted vertical lines mark the change-point positions computed later.

In order to select the bandwidth, we plot the curve on the interval in Figure 5. It can be seen that increases monotonically, so we choose the bandwidth . Then we obtain the threshold by the permutation method as proposed in the simulation.

We detect the change point from the whole sample, and obtain the change point at 12/31/2007. Then we split the original sample to two sub-samples. Repeating the same steps for the left and right sub-samples, we detect the second change point 07/23/2007 and third one 06/02/2009. Note that the threshold is always changing because of the change of the sample size. Repeating the binary segmentation until the maximum of of each sub-sample is less than the threshold or the sub-sample sizes are too few, we totally detect 16 change points (dates). We investigate the corresponding big financial events resulting in stock market to fluctuate just near the date in Table 4. We can expect that during the financial crisis, prices and volatility will be unstable. From our analysis, we can see that the relationship between price and volatility is also fragile, and change points occur very frequently.

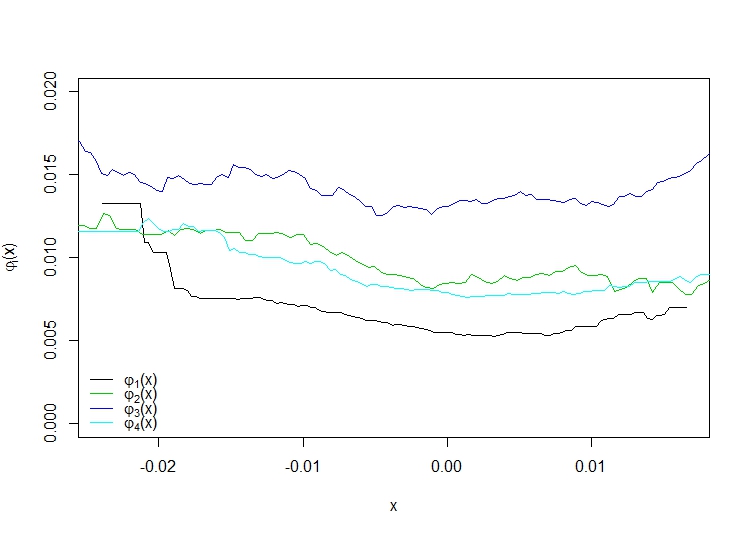

To see how the leverage curve changes visually, we choose the first three detected change points 07/23/2007, 12/31/2007 and 06/02/2009 as the split points, and plot the four corresponding classical N-W kernel regression curves in Figure 7 with the bandwidth . It is clear to find the obvious differences between and , and , and , respectively.

| date (change point) | event | date (change point) | event |

|---|---|---|---|

| 07/23/2007 | Largest US commercial mortgage company | 08/17/2007 | American FED cut the window discount |

| declared profit decreased by 33% | rate by 50 basis points to 5.75 | ||

| 10/10/2007 | The dow Jones closed at | 12/31/2007 | International agricultural futures |

| an all-time high of 14,165 | prices continue to set new records | ||

| 01/28/2008 | American FED provided $30 billion | 09/12/2008 | The 4th large US investment |

| to commercial bank | bank filed bankruptcy protection | ||

| 10/02/2008 | Bush signed a $700 | 10/29/2008 | American sub-prime mortgage crisis |

| billion financial rescue plan | developed to global financial crisis | ||

| 12/12/2008 | Many Banks in world cut | 01/12/2009 | The Finance of America injected |

| interest rates in tandem once more | $14.77 billion into 43 Banks | ||

| 03/26/2009 | American FED declared to use $200 billion | 06/02/2009 | General motors officially filed for |

| to help personal consumers and small enterprises | bankruptcy | ||

| 07/13/2009 | England bank announced it would | 10/22/2009 | The European debt crisis |

| maintain QE at the 120 billion pounds | officially erupted | ||

| 11/06/2009 | England bank announced it would | 12/21/2009 | US House of Representatives passed the biggest |

| increase QE 20 billion to 200 billion pounds | financial regulatory reform since 1930s |

6 Conclusion and discussion

In this paper, firstly, we construct a CUSUM statistic to detect the structural change in the nonparametric regression model. The CUSUM statistic is constructed using sum-of-squares but not supremum like Wang (2008) so that we can find the relatively small structural change, especially when the function difference is small in the whole domain. Secondly, with probability one, we derive an upper bound of the CUSUM statistic asymptotically when there is no change point as well as a lower bound asymptotically when there is a change point. We establish the strong consistency of the change point estimator. Although we detect the change point by the threshold method not usual hypothesis testing, we still show in the simulation that our method has a low rate of the false positive and high rate of the true positive even if the structural change of the regression function is not obvious. Last but not least, we demonstrate a surprising result that the CUSUM method constructed by the N-W estimator performs better than that constructed by the local linear estimator, because the N-W estimator is more sensitive to the observations or outliers which do not belong to the same stable period.

Although we only focus on the case of one regressor and one change point, our method can be extended without difficulties to the multivariate regression with multiple change points.

Acknowledgements.

The authors thank the professor Cai-Ya Zhang from ZUCC, senior brothers and many schoolmates for the vital comments and suggestions. Specially, we appreciate the editor and reviewers for their comments and suggestions to our research, which improve our work significantly.Appendix: Proofs

In this section, we provide the detailed proofs of the theoretical results in Section 3. Before proving the main theorems, we state and prove some lemmas.

The following lemma plays a crucial role in deriving some uniform bounds of an -mixing process.

Lemma 1 (Theorem 1.3 of Bosq (1998))

Let be a zero-mean real-valued process such that

. Let . Then

(i) For each integer and each ,

(ii) For each integer and each ,

with , ,

The following lemma demonstrates the bounds of the auto-covariances of and , that is, a truncated version of , which facilitates the application of Lemma 1 to the N-W estimator.

Lemma 2

Proof of Lemma 2

(i) Noting that , the density function of , is uniformly bounded and , we can prove that

with variable substitution and selecting . In terms of the covariance, we have

where is defined in Assumption 5. Letting satisfy and using Hölder inequality, we can prove that

| (6.5) |

where is equal to , noting that , which is implied by and in Assumption 4. Besides, by using the Billingsley’s inequality (c.f. Chapter 1 of Bosq (1998)), we have

| (6.6) | |||||

where . Note that we have in Assumption 2 for GSM or in Assumption 1 for PSM. Combining (6.5) and (6.6), and taking , we can prove (6.2).

(ii) We denote as for simplicity. Noting that , and by Assumptions 4, 5 and 6, respectively, we have

by selecting .

For the covariance, set , we have

where and are defined in Assumption 5. Note that the last step follows from the Hölder inequality similar to (6.5) with satisfying .

Next we prove the second part in the minimization function in (6.4). Note that, for any and ,

| (6.7) | |||||

and by Assumption 6 and Jensen inequality. By Corollary 1.1 in Bosq (1998) together with (6.7), we have, for any ,

with . Let tend to infinity, we have , thus

Using in Assumption 2 or in Assumption 1, and taking , we can prove (6.4).

The following lemma shows the uniform bound of the N-W estimator of a PSM process. Note that (i) the bandwidth is selected based on the sample size , (ii) the estimator is constructed based on subsample set , for , and (iii) the uniform bound is considered with respect to time .

Lemma 3

Proof of Lemma 3

It is clear that if for some ,

| (6.10) |

we can show (6.8) by using the Borel-Cantelli lemma. Next we prove (6.10). Actually,

noting that when . A sufficient condition is that for some and

| (6.11) |

when is large enough, where is a positive constant (we still use the notation for ).

Firstly, we want to derive the order of and defined in Lemma 1 with the sequence replaced by the sequence . Taking , , and , we have and for large n. Using the partition method similar to the proof of Theorem 3.3 in Johannes and Rao (2011), we have (define )

with the partition point . Then using Lemma 2, we can obtain for large n

| (6.12) | |||||

where the term is induced by substituting the sum with an integral and the last row follows from in Assumption 5. So for , we have

| (6.13) | |||||

for large enough, noting that when . Then using Lemma 1(ii) and (6.13), we have for

| (6.14) | |||||

Because and thereby , by selecting , we have . In terms of , noting that and , we can obtain

when for some .

The proof of (6.9) is similar to the proof of (6.8) by considering the sequence . Thus we omit the proof. Then we complete the proof of this lemma.

Lemma 4

Proof of Lemma 4

The proof of this lemma is similar to the proof of Lemma 3. Because of similarity, we only prove (6.15).

We need to prove (6.11) by Lemma 1(ii). Using the same notation with Lemma 3, we have , hence for large enough (see Lemma 2.1 of Bosq (1998)). Then we still have (6.14). By selecting , we have

| (6.17) |

In terms of , note that , which implies that and thus , and therefore and can be bounded by . We have

| (6.18) | |||||

where and are two positive constants, noting that . Combining (6.14), (6.17) and (6.18), we can prove (6.11). Thus we complete the proof of this lemma.

Lemma 5

Proof of Lemma 5

The proof of this lemma is similar to that of Lemma 3. The only difference is that may not be bounded, and we need to adopt the idea of truncation before using Lemma 1(ii). Analogously, our goal is to prove for some

which can be proved by

| (6.21) |

where and is a tiny positive constant.

Next, we prove (6.21). For , define and with , where is a positive constant which will be determined later. Then

| (6.22) | |||||

Denote the partial sums in (6.22) as and . To use Lemma 1(ii), set . Then (6.21) can be written as follows,

so we can prove this lemma by showing that

| (6.23) |

and

| (6.24) |

For (6.23), before using the similar method by the inequality in Lemma 1(ii) like before, we still need to show the bound of . Together with Lemma 2(ii), it immediately follows that, like (6.12) by using , for large n

when . Hence

when n is sufficiently large. Then we can use Lemma 1(ii) like the proof before and derive that for

For , we have

by selecting . For , we have

where the existence of in the last equality follows from Assumption 3. Then we have proved (6.23).

In terms of (6.24), using Cauchy-Schwarz and Markov inequality, we have

by letting , noting that , is uniformly bounded, , and .

Lemma 6

Proof of Lemma 6

We still use the notation in Lemma 5, and want to show (6.23) and (6.24). Together with Lemma 2(ii), it still holds that

noting that . So we only need to show the part containing mixing-coefficient as follows,

| (6.27) | |||||

where and are strictly positive constants, noting that the last second row is deduced like (6.18), and .

Lemma 7

Proof of Lemma 7

Because of similarity, we only show the first equation. Consider the decomposition

By Lemma 3, uniformly over . Since , the density function has a nonzero lower bound in a sufficient small neighbourhood of . We have for some positive constant if is small enough. Then, by Lemma 3 and 5, we have

noting that .

Hence we complete the proof of this lemma.

Proof of Theorem 3.1

Since there is no change point, we have and , and therefore by Lemma 7

We complete the proof of the theorem.

Proof of Theorem 3.2

By definition,

Note that is bounded. When , both and are bounded away from zero in a small neighbour of . Therefore is also bounded away from zero when is large enough.

Next we prove (3.2). Considering the special point , it is obvious that

Note that the sequences and are strictly stationary. By definition and Lemma 7, we have

| (6.30) | |||||

Thus, we complete the proof of this theorem.

Proof of Theorem 3.3

Now we prove (ii). From the statement in the proof of Theorem 3.2, we have

| (6.31) |

almost surely when . If we can show that

| (6.32) |

almost surely, for any small when , then (6.31) and (6.32) imply that almost surely when . Using the same method for the case when , we can obtain almost surely when . Combining these two inequalities we can show that by letting .

Next we prove (6.32). When , on the one hand, we have

| (6.33) |

uniformly in by Lemma 7. On the other hand,

We show that is negligible and is the leading term. Similar to the argument of proof for Lemma 5, we can show that the asymptotic order of is also , as the sample size is of order . Note that is bounded away from zero almost surely when is large enough. Since and , we have by Lemma 5 (or Lemma 6)

| (6.34) |

In terms of , we have by Lemma 3

Therefore,

| (6.35) | |||||

References

- Aue, Rice and Sönmez (2018) Aue A, Rice G and Sönmez O(2018)Detecting and dating structural breaks in functional data without dimension reduction. Journal of the Royal Statistical Society: Series B 80(3): 509–529

- Bai (1997) Bai J(1997)Estimating multiple breaks one at a time. Econometric theory 13(3): 315–352

- Bandi and Renò (2012) Bandi FM and Renò R (2012)Time-varying leverage effects. Journal of Econometrics 169(1): 94-113

- Barigozzi, Cho and Fryzlewicz (2018) Barigozzi M, Cho H and Fryzlewicz P(2018)Simultaneous multiple change-point and factor analysis for high-dimensional time series. Journal of Econometrics 206(1): 187-225

- Basrak, Davis and Mikosch (2002) Basrak B, Davis RA and Mikosch T(2002)Regular variation of GARCH processes. Stochastic Processes and their Applications 99(1): 95–115

- Bollerslev and Zhou (2006) Bollerslev T and Zhou H(2006)Volatility puzzles: a simple framework for gauging return-volatility regressions. Journal of Econometrics 131(1-2): 123-150

- Bosq (1998) Bosq D(1998)Nonparametric Statistics for Stochastic Processes: Estimation and Prediction, 2nd edn. Springer-Verlag, New York

- Braun and Müller (1998) Braun JV and Müller HG(1998)Statistical methods for DNA sequence segmentation. Statistical Science 13(2): 142–162

- Brown, Durbin and Evans (1975) Brown RL, Durbin J and Evans JM(1975)Techniques for testing the constancy of regression relationships over time. Journal of the Royal Statistical Society: Series B 37(2): 149–192

- Chen and Nkurunziza (2017) Chen F and Nkurunziza S(2017)On estimation of the change points in multivariate regression models with structural changes. Communications in Statistics-Theory and Methods 46(14): 7157–7173

- Cho (2016) Cho H(2016)Change-point detection in panel data via double CUSUM statistic. Electronic Journal of Statistics 10(2): 2000–2038

- Cho and Fryzlewicz (2012) Cho H and Fryzlewicz P(2012)Multiscale and multilevel technique for consistent segmentation of nonstationary time series. Statistica Sinica 22: 207–229

- Cho and Fryzlewicz (2015) Cho H and Fryzlewicz P(2015)Multiple-change-point detection for high dimensional time series via sparsified binary segmentation. Journal of the Royal Statistical Society: Series B 77(2): 475–507

- Choi and Lee (2017) Choi JY and Lee MJ(2017)Regression discontinuity: review with extensions. Statistical Papers 58(4): 1217–1246

- Dette, Kokot and Aue (2017) Dette H, Kokot K and Aue A(2017)Functional data analysis in the Banach space of continuous functions. Preprint on https://arxiv.org/abs/1710.07781

- Delgado and Hidalgo (2000) Delgado MA and Hidalgo J. (2000). Nonparametric inference on structural breaks. Journal of Econometrics 96(1): 113-144

- Eichinger and Kirch (2018) Eichinger B and Kirch C(2018)A MOSUM procedure for the estimation of multiple random change points. Bernoulli 24(1): 526–564

- Enikeeva and Harchaoui (2019) Enikeeva F and Harchaoui Z(2019)High-dimensional change-point detection under sparse alternatives. The Annals of Statistics 47(4): 2051–2079

- Fryzlewicz (2014) Fryzlewicz P(2014)Wild binary segmentation for multiple change-point detection. The Annals of Statistics 42(6): 2243–2281

- Gurevich and Vexler (2005) Gurevich G and Vexler A(2005)Change point problems in the model of logistic regression. Journal of Statistical Planning and Inference 131(2): 313-331

- Härdle, Müller, Sperlich and Werwatz (2004) Härdle W, Müller M, Sperlich S and Werwatz A(2004)Nonparametric and Semiparametric Models. Springer-Verlag, Berlin Heidelberg

- Hosking (1981) Hosking JRM(1981)Fractional differencing. Biometrika 68(1): 165–176

- Huh and Park (2004) Huh J and Park BU(2004)Detection of a change point with local polynomial fits for the random design case. Australian and New Zealand Journal of Statistics 46(3): 425–441

- Hušková and Maciak (2017) Hušková M and Maciak M(2017)Discontinuities in robust nonparametric regression with -mixing dependence. Journal of Nonparametric Statistics 29(2): 447–475

- Hušková and Steinebach (2002) Hušková M and Steinebach J(2002)Asymptotic tests for gradual changes. Statistics and Risk Modeling 20(1-4): 137–152

- Jin (2017) Jin X(2017)Time-varying return-volatility relation in international stock markets. International Review of Economics & Finance 51: 157-173.

- Johannes and Rao (2011) Johannes J and Rao SS(2011)Nonparametric estimation for dependent data. Journal of Nonparametric Statistics 23(3): 661–681

- Kaul, Jandhyala and Fotopoulos (2019) Kaul A, Jandhyala VK and Fotopoulos SB(2019)An efficient two step algorithm for high dimensional change point regression models without grid search. Journal of Machine Learning Research 20(111): 1–40

- Killick, Fearnhead and Eckley (2012) Killick R, Fearnhead P and Eckley IA(2012)Optimal detection of changepoints with a linear computational cost. Journal of the American Statistical Association 107(500): 1590–1598

- Masry (1996) Masry E(1996)Multivariate local polynomial regression for time series: uniform strong consistency and rates. Journal of Time Series Analysis 17(6): 571–599

- Mohr and Neumeyer (2019) Mohr M and Neumeyer N(2019)Consistent nonparametric change point detection combining CUSUM and marked empirical processes. Preprint on https://arxiv.org/abs/1901.08491

- Mohr and Selk (2020) Mohr M and Selk L(2020)Estimating change points in nonparametric time series regression models. Statistical Papers, online https://doi.org/10.1007/s00362-020-01162-8

- Müller (1992) Müller HG(1992)Change-points in nonparametric regression analysis. The Annals of Statistics 20(2): 737–761

- Nadaraya (1964) Nadaraya EA(1964)On estimating regression. Theory of Probability and Its Applications 9(1):141–142

- Ploberger and Krämer (1992) Ploberger W and Krämer W(1992)The CUSUM test with OLS residuals. Econometrica 60(2): 271–285

- Qiu, Zi and Zou (2018) Qiu P, Zi X and Zou C(2018)Nonparametric dynamic curve monitoring. Technomerics 60(3): 386–397

- Su and Xiao (2008) Su L and Xiao Z(2008)Testing structural change in time-series nonparametric regression models. Statistics and Its Interface 1(2): 347–366

- Venkatraman (1992) Venkatraman ES(1992)Consistency results in multiple change-point problems. Technical Report 24. Department of Statistics, Stanford University, Stanford

- (39)

- Wang (2008) Wang L(2008)Change-point estimation in long memory nonparametric models with applications. Communications in Statistics-Simulation and Computation 37(1): 48–61

- Wang, Wang and Zi (2019) Wang Y, Wang Z and Zi X(2019)Rank-based multiple change-point detecion. Communications in Statistics–Theory and Methods, online https://doi.org/10.1080/03610926.2019.1589515

- Watson (1964) Watson GS(1964)Smooth regression analysis. Sankhyā: The Indian Journal of Statistics: Series A 26(4): 359–372

- Wu and Chu (1993) Wu JS and Chu CK(1993)Kernel-type estimators of jump points and values of a regression function. The Annals of Statistics 21(3): 1545–1566

- Wu, Zhang, Zhang and Ma (2016) Wu X, Zhang S, Zhang Q and Ma S(2016)Detecting change point in linear regression using jackknife empirical likelihood. Statistics and Its Interface 9(1): 113–122

- Xu, Wu and Jin (2019) Xu M, Wu Y and Jin B(2019)Detection of a change-point in variance by a weighted sum of powers of variances test. Journal of Applied Statistics 46(4): 664–679

- Zhang and Lavitas (2018) Zhang T and Lavitas L(2018)Unsupervised self-normalized change-point testing for time series. Journal of The American Statistical Association 113(522): 637–648

- Zou, Yin, Feng and Wang (2014) Zou C, Yin G, Feng L and Wang Z(2014)Nonparametric maximum likelihhood approach to multiple change-point problems. The Annals of Statistics 42(3): 970–1002