Combined parameter and state inference with automatically calibrated approximate Bayesian computation

Abstract

State space models contain time-indexed parameters, termed states, as well as static parameters, simply termed parameters. The problem of inferring both static parameters as well as states simultaneously, based on time-indexed observations, is the subject of much recent literature. This problem is compounded once we consider models with intractable likelihoods. In these situations, some emerging approaches have incorporated existing likelihood-free techniques for static parameters, such as approximate Bayesian computation (ABC) into likelihood-based algorithms for combined inference of parameters and states. These emerging approaches currently require extensive manual calibration of a time-indexed tuning parameter: the acceptance threshold.

We design an SMC2 algorithm (Chopin et al., 2013, JRSS B) for likelihood-free approximation with automatically tuned thresholds. We prove consistency of the algorithm and discuss the proposed calibration. We demonstrate this algorithm’s performance with three examples. We begin with two examples of state space models. The first example is a toy example, with an emission distribution that is a skew normal distribution. The second example is a stochastic volatility model involving an intractable stable distribution. The last example is the most challenging; it deals with an inhomogeneous Hawkes process.

Keywords: Approximate Bayesian Computation, Sequential Monte Carlo, State Space Models, Particle Filter

1 Introduction

1.1 Approximate Bayesian computation (ABC)

Approximate Bayesian computation (Tavaré et al., 1997; Marin et al., 2012; Sisson et al., 2018) is a Monte Carlo method for performing parameter inference where the likelihood is intractable. Suppose we have some latent process , then Bayesian inference becomes more difficult when the multidimensional integral

cannot be computed explicitly. The output of ABC algorithms is a sample from an approximation of the posterior distribution . This approximation relies on parameter samples drawn from the prior, and samples of the latent process and the observed process drawn from the stochastic model given . Given these simulations, ABC algorithms derive approximations of the posterior and of other functionals of the posterior such as moments or quantiles. The most profound shortcoming with ABC is that approximating the conditional distribution of given requires that at least some simulations fall into the neighborhood of . If the data space is of high dimension, we face the curse of dimensionality, namely that it is almost impossible to get a simulated dataset near the observed . To circumvent this problem, ABC schemes perform a non-invertible mapping from the observed and simulated datasets onto a space of lower dimension via some summary statistics and , and set a metric on this space. Thus, ABC cannot recover anything better than . For instance, the accept-reject ABC algorithm samples the distribution given the event , i.e., , where is a threshold that has to be set by the user. This distribution tends to when . But, if we want a sample of size from , the accept-reject ABC algorithm requires on average a number of simulations from the prior given by . Since can decrease very quickly towards when , the ideal value may be difficult to achieve with the accept-reject ABC algorithm. In practice, corresponds to a quantile of the distances between the observed , the simulated : is set by the computational budget, and is the desired number of posterior samples. The threshold is set so that , which means that is the quantile of order of the distance to the observed dataset.

Various sampling algorithms that also target have been proposed in the literature to improve the accept-reject algorithm, particularly where the parameter space is high dimensional. The ABC-MCMC (Marjoram et al., 2003) is rather popular, but it can perform poorly if the threshold is small. Sequential Monte Carlo algorithms have been proposed as an alternative to these methods: Sisson et al. (2007), Beaumont et al. (2009), Drovandi and Pettitt (2011), Del Moral et al. (2012). These sequential algorithms decrease the threshold gradually and tune the proposal distribution for the parameter to get closer and closer to the approximate posterior . Yet these algorithms suffer from two problems: (i) at each iteration, they have to draw many complete datasets , which can be heavy in terms of computation time; (ii) they still require a summary function that projects the complete datasets into a space of much smaller dimension. With this projection, therefore, comes a possible loss of information, since we rarely have a theoretical guarantee that the statistic is sufficient.

State space models comprise one class of statistical inference problem where the parameter space is very high dimensional. There are Monte Carlo methods for Bayesian analysis of state space models, which we will explore in the next section. These methods usually target the distribution sequentially. The posterior distribution can then be recovered by trivial marginalisation of the final target. However, the thresholds are much more difficult to tune in this setting and may require multiple pilot runs before achieving acceptable results.

1.2 Combined parameter and state inference

In a typical state space model, two types of parameters coexist: one type varies on a time index (states), and the other type is independent of time (fixed static parameters, hereafter simply termed parameters). Observations are available on the same indexed time domain as the state. Common inference techniques perform inference on the state, conditional on known static parameters.

State inference is termed smoothing, filtering, or prediction depending on whether the state inference is earlier, cotemporal to, or later than the last observation respectively (Särkkä, 2013). Usually, interest lies in filtering, state inference conditional on all data processed thus far. The Kalman filter (Kalman, 1960) is a well-known analytic solution for filtering, but there are strict assumptions on , which is assumed to be Gaussian in nature. More complex cases typically require a Monte Carlo based approach, termed a particle filter (PF), where a vector of proposed states propagates along with the time index (Kitagawa, 1987; Gordon et al., 1993). For recent overviews of the subject see Fearnhead and Künsch (2018) and Naesseth et al. (2019).

Unknown static parameters add a surprising degree of complexity to the inference problem. Algorithms for combined parameter and state (CPS) inference have received less attention than filtering, see Kantas et al. (2015); Liu and West (2001) for comprehensive overviews. A straightforward approach introduces an artificial non-degenerate transition density for the static parameters and proceeds with the particle filter as though these static parameters were states, along with the genuine state parameters. This approach is problematic as the static parameter samples are no longer guaranteed to be from the true posterior. Furthermore, if the true parameter value is not within the initial draw of parameter proposals then the final weighted set of proposals will not contain the true value. This problem is not evident for the state proposals as they exhibit stochasticity naturally.

More recent techniques embed a PF for state parameters within a larger algorithm for static parameters. Examples include particle Markov chain Monte Carlo (PMCMC) (Andrieu et al., 2010; Drovandi et al., 2016), sequential Monte Carlo (SMC, SMC2) (Liu, 2008; Del Moral et al., 2012; Chopin et al., 2013; Drovandi and McCutchan, 2016), and Bayesian indirect inference (Martin et al., 2019). CPS inference techniques have many applications including ecology (Fasiolo et al., 2016), agent-based models (Lux, 2018), genetic networks (Mariño et al., 2017), and hydrological models (Fenicia et al., 2018).

1.3 Our contributions and plan

In this paper we develop an ABC sequential method that automatically tunes the time-indexed thresholds at each iteration of the algorithm. Section 2 provides some theoretical background for state space models, particle filtering and Bayesian static parameter inference within this framework.

The methodology we propose is given in Section 3, which is based on the efficient SMC2 algorithm proposed by Chopin et al. (2013). Our proposal includes the filtering algorithm of Jasra et al. (2012) to each particle of a larger SMC that takes into account the uncertainty about static parameters of the state space model. Our proposal is thus an adaptation of the SMC2 algorithm to approximate Bayesian computation. We take care of tuning automatically the time-index thresholds that are required by the algorithm. We investigate some theoretical properties of the method at the end of Section 3, and discuss the effect of the automatic calibration.

Our approach is illustrated on three different examples in Section 4: a state space model with skew normal distributions, a stochastic volatility model from the econometric literature, and a Hawkes process.

2 Background

2.1 State space model

The first example of a state space model was a hidden Markov models in the seminal paper by Baum and Petrie (1966). It is customary to use ‘state space’ notation for state parameters where refers to the value of the state parameter at time . We consider state space models where state transitions are Markovian, conditional on a static parameter :

where the notation denotes the subset of from time 1 to time . The state process is latent, but there is an observed process , also conditioned on :

| (1) |

termed the emission distribution. We can see, given and , that is independent of its history .

In nonlinear and non-Gaussian state space models, none of the distributions given below are explicitly available: (i) the filtering distribution: , (ii) the smoothing distributions: , with , and , moreover the likelihood is intractable. We briefly introduce particle filters in Section 2.2 and consider combined parameter and state space inference with the SMC2 in Section 2.3. Likelihood-free versions of these algorithms are discussed in Section 2.4.

2.2 Particle filters

Particle filters (PF) are Monte Carlo algorithms that target the filtering distribution . Two papers that conducted work in this area are Müller (1991) and Carpenter et al. (1999). More recently, Davey et al. (2015) re-create the path of the flight MH370 from satellite data using a state space model estimated with a PF. In this Section, we assume that the parameter is fixed and known and we proceed conditionally on this value. The target of PF is the filtering distribution . As a byproduct, it also computes an approximation of the marginalised likelihood . The main output is a weighted state sample of size whose empirical distribution

is an approximation of the filtering distribution. At each stage of the sequential algorithm, PF also produce an estimate of . Then the marginalised likelihood is given by

Importance sampling is at the core of PF: at time the states are sampled from a proposal distribution , and then the states are sampled from a Markovian kernel . The first reported version of this method (Gordon et al., 1993) sets to the Markovian kernel . This proposal may be far from the optimal kernel . More generally, such a particle filter is termed a sequential importance resampling filter by Doucet et al. (2000), see Algorithm 1. This filter is not necessarily ideal for targeting . Other approaches to particle filtering in literature include a multi-step MCMC kernel (Drovandi and Pettitt, 2011), and the alive particle filter (Del Moral et al., 2015).

2.3 Combined parameter and state inference

We consider now CPS inference, which targets the much more complex distribution . Such algorithms simultaneously filter the state and compute the posterior of the fixed parameter. We are interested in drawing samples from the joint distribution of and conditional on observations . Initial approaches addressed this problem by appending to the state vector , as though the static parameters were dynamic. This approach leads to error that is highly model specific and poorly understood. This led to the development of approaches which explicitly take the fixed nature of into account. Drovandi et al. (2016) and Drovandi and McCutchan (2016) address this problem by incorporating the alive particle filter into the PMCMC and SMC algorithms, respectively. Chopin et al. (2013) incorporate the sequential importance resampling filter (Algorithm 1) into a SMC approach, which they term SMC2 (Algorithm 2) since particle filters fall within the class of general SMC algorithms.

Algorithm 2 uses the sequential importance resampling filter (Algorithm 1) to estimate the likelihood update within a larger SMC algorithm to return weighted parameter samples . Since weights are updated rather than used within a resampling step at each time step, rejuvenation is necessary. Otherwise, will become degenerate. So-called sample impoverishment or particle degeneracy is a problem in sequential particle filters. In this paper, we use the classical measure of sample impoverishment called effective sample size (ESS, see, e.g., Djuric et al., 2003). This can be estimated by

| (2) |

Degeneracy is determined based on a fixed ESS threshold. Once degeneracy is detected, the values of are rejuvenated using a weighted kernel density , where is a Markov kernel with invariant distribution with a particle MCMC (Andrieu et al., 2010).

2.4 ABC and state space models

The sequential importance resampling particle filter (Algorithm 1), which forms part of the SMC2 algorithm (Algorithm 2), requires computation of the likelihood . This, in many cases, cannot be evaluated but can be used to draw model realisations. In the next section, we discuss approximate Bayesian computation (ABC), a likelihood-free approach to parameter inference that overcomes this limitation. We also review ABC adaptations of PFs and to CPS inference.

ABC particle filters based on the sequential importance resampling (Algorithm 1, see Jasra et al., 2012; Calvet and Czellar, 2014; Del Moral et al., 2015) substitute a likelihood approximator for within Algorithm 1. We give now an example of . Let us assume that we cannot evaluate , however, knowing and , we can simulate a set , , from this distribution. Then we have to replace the evaluation of this density with the proportion of that fall near the observation with respect to , i.e,

| (3) |

which is an unbiased estimate of

| (4) |

where is the indicator function. This could be replaced by any positive-valued decreasing function on , but we use for simplicity. Note that as a function of is a proper density function up to a normalising factor that depends only on . Finally, since we have values of at hand in the PF algorithm at a given time , we have to compute this ABC likelihood estimate times.

In some cases, the Markovian kernel of the state space model is intractable. In these cases, we can set the proposal to so that they cancel one another in the particle filter weights. This is the approach we take, in order to demonstrate the algorithm for fully intractable problems. In that case, all are equal to , and the ratio of Equation (7) is just the proportion of accepted simulations, weighted by , marginalised over parameters and states.

3 Methodology

We discuss now how an ABC particle filter, based on the sequential importance resampling, is incorporated into a likelihood-free CPS algorithm.

Likelihood-free CPS inference algorithms which have so far been developed (Drovandi and McCutchan, 2016; Drovandi et al., 2016), require that a sequence of thresholds be chosen before initialisation of the CPS algorithm. However, we develop a technique that bypasses this requirement to allow for automatic calibration.

3.1 Targets

We develop this algorithm (Algorithm 3) to provide a sample from the joint posteriors . However, since some distributions are intractable, we perform a likelihood-free approximation to sample from the approximate joint posteriors defined as follows. If , the target is given by

| (5) | |||

And, for any , the target is defined by induction as

| (6) |

where we set

We also introduce, for any ,

3.2 Proposed algorithm

The form of the integral in Equation (6) suggests to us a strategy for sampling from . Let us assume that, at time , we have a weighted sample that comprises

-

1.

a weighted sample of size , namely , with weights , …, , whose weighted empirical distribution is a Monte Carlo approximation of ; and

-

2.

for each value in that sample, a sample , with weights , whose weighted empirical distribution is a Monte Carlo approximation of .

State resampling is performed independently for each value of the parameter. Hence, for each , we still have an approximation of . For each value , we resample the states using their weights with the multinomial distribution . Note that other sampling choices, such as systematic sampling (Li et al., 2015), can be contemplated and incorporated in a straightforward manner. We move the resampled states according to to get the proposals. And we draw simulations , , for each , according to the emission distribution . Finally, the unnormalised weight of is

where denotes the index of the ancestor from the multinomial resampling. This allows us to estimate by taking an average from the particle approximation, where .

We discuss now the calibration of . In the standard application of ABC rejection, it is usual to calibrate as a quantile “acceptance probability” of the distances of the simulated values , see Section 1.1. To achieve this, the particles can be ordered according to their distances , , and the smallest value of can be found such that

| (7) |

is greater than .

With each ABCSMC2 update, more data are incorporated into the static parameter posterior . This leads to degeneracy of the weights . To check degeneracy, we use the ESS criteria in Equation (2), with threshold chosen prior to analysis. In order to propose new parameters and further improve the particle approximation to , we need an estimate of the ABC marginal likelihood . Following Chopin et al. (2013), the ABC likelihood can be estimated, in the following manner:

Once we have for each we can rejuvenate the particle system. The steps involved in parameter rejuvenation are the following:

-

1.

resample , to make non-degenerate,

-

2.

generate new parameter proposals for each , from a kernel around ,

-

3.

for each run an independent ABC particle filter, conditional on , with the previously computed thresholds , in order to compute the particle system at time , and

-

4.

accept each , with probability

It is important to recycle the previously computed thresholds so that the rejuvenation step preserves the distribution of the current particle set, i.e. from the approximate posterior .

The rejuvenation step means that the entire state space model, up to time , is re-evaluated, for proposed parameters , within the ABC particle filter whenever degeneracy occurs. This means that the computational complexity of our algorithm is not linear with time. This is also true for the algorithm of Chopin et al. (2013).

3.3 Theoretical results

In this Section, we set the following hypotheses.

-

(A1)

The sampling distributions are chosen such that, for all and ,

-

(A2)

The , , are never resampled.

-

(A3)

All have been set a priori.

The first assumption (A1) is quite classical and is necessary so that the importance sampling at each stage is unbiased. The second assumption (A2) is set to simplify the results below since the effects of the ’s resampling are well known. The last assumption will be alleviated in the last Proposition of this Section to understand the consequences of the threshold calibration.

The first results, in both following Propositions, show that the un-normalised ABC-SMC2 estimate is unbiased and consistent. Their proofs are given in Appendices A and B, respectively.

Proposition 1

Assume (A1), (A2) and (A3) hold. Consider a bounded function and set

We have

| (8) |

Proposition 2

With the same assumptions and notations of Proposition 1. When ,

The ABC-SMC2 estimate of the expected value of a bounded function with respect to the target (6) is

and is defined as in Propositon 1. We can now state the main result:

Theorem 3

Assume (A1), (A2) and (A3) hold. When ,

This Theorem is a direct consequence of Proposition 2 since is a special case of when the bounded function .

The theoretical results above show that the scheme is consistent even if . But the numerical accuracy at finite sample sizes depends on the values of and . In particular, at each stage, the total number of ’s simulations is the product . A larger number of these samples improves the calibration for the sequence of thresholds . See, for example, Del Moral et al. (2012) which also discussed a similar issue in Section 4.1.2 of their paper.

Assume now that (A1) and (A2) hold and that ,…, have been set a priori. With Propositions 1 and 2, for any value of , the numerator of Equation (7) is an unbiased, consistent estimate of

Likewise, the denominator of Equation (7) is an unbiased, consistent estimate of the same probability, but with . Thus, it estimates fairly , and the ratio in Equation (7) is a consistent estimate of . Hence, the rule we propose to tune is to choose a Monte-Carlo estimate of the quantile of order of the distance of to given the information we retrieved until time . Note that this probability is averaged over all values of from the ABC posterior recovered until time .

The estimate of the update of the marginal likelihood in Algorithm 3, namely , is the relative weights of simulations drawn from that satisfy the inequality . So, even if is calibrated on the whole set of simulations at stage , this estimate is a fair ABC surrogate of the update of the likelihood. In the extreme case of and a proposal , this estimate is

This is the standard ABC approximation of the likelihood. Increasing or sharpens the approximation of the likelihood.

4 Examples

We now demonstrate the use of our self-calibrated ABCSMC2 update (Algorithm 3) with some examples.

4.1 Skew normal distribution

4.1.1 Method

As a demonstration of our approach, we consider a simple state space model driven by an auto-regressive process. The emission distribution is the skewed version of the normal distribution as defined by Azzalini (1985). The skew normal distribution can be parameterised in a similar way to the normal distribution, with an additional parameter for skewness (see Azzalini (2005) for further details); we represent this distribution as SN(). The statistical model is as follows: ,

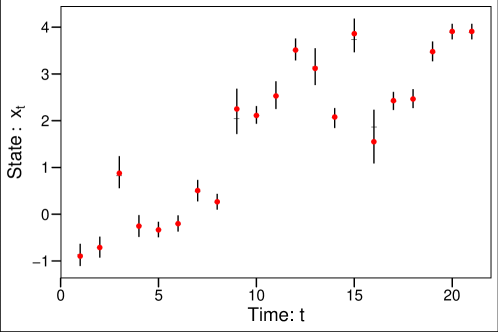

with initial state distribution , and where each observation comprises 100 independent and identically distributed observations of the skew normal distribution at each time step . The state parameter is the mean parameter of the SN distribution, and the parameters to be inferred are and . The priors are and . The true parameters used for the simulations are and .

The summary statistic for this example is composed of the sample mean , standard deviation and skewness . Skewness is calculated using a method discussed in Joanes and Gill (1998): , as implemented by the R package e1071 (Meyer et al., 2019), where is the sample third central moment. The distance is the weighted Euclidean distance between observed and simulated summary statistics. We implement this model with , , , and for time . The ESS threshold to rejuvenate the -particles is set to .

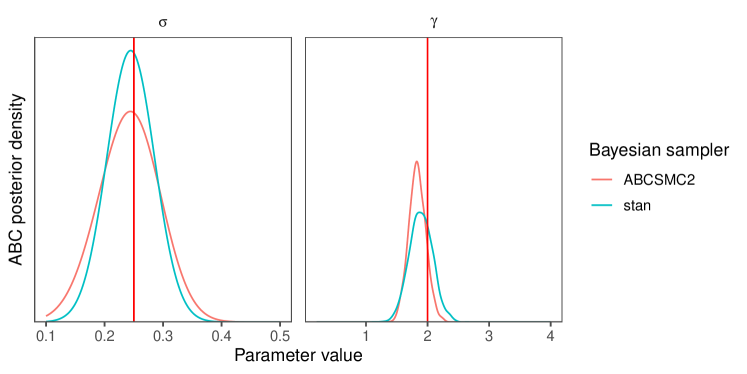

This example was intentionally made short on the time scale to make validation, with a Hamiltonian Montel Carlo likelihood-based sampler written in STAN (Carpenter et al., 2017), possible. The point of this is to validate our approach rather than to compare performance.

4.1.2 Results

Inference results for the marginalised filtering distribution for , as shown in Figure 1. We can see that the algorithm performs well in matching the true state. The posterior for the static parameters is shown in Figure 2. The results here are also good. The parameter is estimated well, with posterior mass concentrated near the true parameter, similarly for the parameter displays more posterior variance. We included a comparison with the likelihood-based Hamiltonian Monte Carlo Bayesian probabilistic programming language, stan. Of course the likelihood-based method outperforms our method, but the fact that our approximate posterior is close to the true posterior is highly encouraging.

4.2 Econometric model

Stochastic volatility models are one of the most common state space models in the econometric literature. Recently, Vankov et al. (2019) considered the case where the emission distribution is a stable distribution, that can take into account heavily tailed volatility. Assuming known values for static parameters of the model, they propose a likelihood-free particle filter to infer the states. But, up to our knowledge, no specific algorithm is available to take into account the uncertainty on the static parameters of the model. The model is as follows:

where is the stable distribution (Lombardi and Calzolari, 2009; Mandelbrot, 1963), with characteristic function

Note that is a stability parameter, a skewness parameter, and and are related to the scale and the position of the distribution. In particular, if and , the stable distribution is a Gaussian distribution; if and , it is a Cauchy distribution; if and , it is a Lévy distribution. Apart from these examples, the density of stable distribution is intractable (Lombardi, 2007). This has led to the development of ABC techniques for stable distributions (Peters et al., 2012).

4.2.1 Method

All static parameters are known except for . The prior of is . We define a transformation on the variables , where is the inverse CDF of the standard normal distribution. The transition kernel (Algorithm 3) is the following:

| (9) |

where is the weighted standard deviation of and is a fixed tuning parameter set to 0.1 to ensure high acceptance. The ratio which appears in the acceptance probability of Algorithm 3 is:

| (10) |

where is the standard normal probability density function, because the random walk is on the tranformed variable .

4.2.2 Results

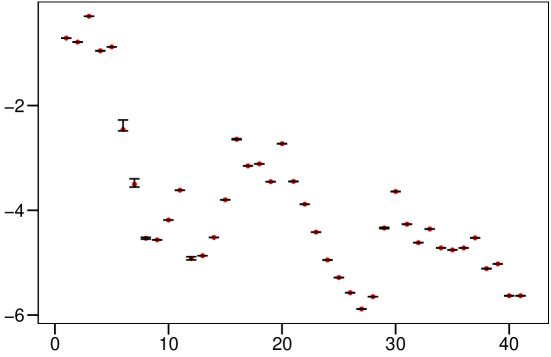

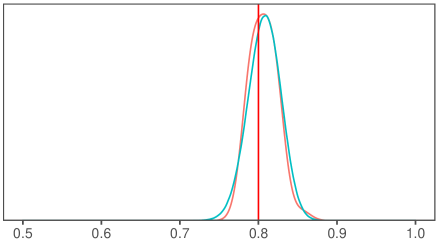

The tuning parameters were , . The acceptance probability to automatically tune the threshold was . The ESS threshold to rejuvenate the -particles was . The marginal filtering distribution follows the true state closely (Figure 3), despite taking into account the uncertainty on . The same is true for the posterior density in Figure 4.

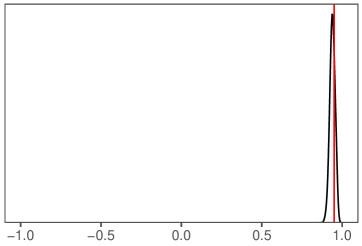

Very few alternatives exist to estimate the parameters of the stochastic volatility model including a general stable distribution because its density is intractable. But we can assume that we are in the special case where this distribution is Gaussian, so that the completed likelihood can be evaluated. We adapt the STAN sampling algorithm of Stan Development Team (2018) to sample from the true posterior on a smaller dataset of size . Figure 5 compares the posterior distribution on recovered by STAN and the one we get with our method. We clearly see that the approximate posterior takes the form of the true posterior, which provides an additional check as to the validity of our approach.

In this example, each is of size , and we did not need to summarise it to run our algorithm. The whole dataset is of size (general case) or of size (Gaussian case). Due to the curse of dimensionality, it would not have been possible to get decent results with a basic accept-reject ABC algorithm without introducing a summary statistic of much smaller dimension, thus without losing part of the information given by the data. Figure 5 is a demonstration that likelihood-free methods can return sharp results if we are able to run the algorithm without the resort to a non linear projection of the datasets, and without facing the curse of dimensionality.

4.3 Semi-parametric Hawkes process

Hawkes processes, as introduced by Hawkes (1971a, b) are a type of self-exciting point process on . The term self-exciting means that events are not independent. Assume that , are the ordered events. All previous events , raise the probability a new event occurring. The rate for a Hawkes process at time , given all past events , is

We use rather than to emphasise that this time variable is continuous. Here is some baseline rate function that is conditionally independent of ; and is the self-exciting kernel function evaluated over and time . We describe now the specifics of the Hawkes process we intend to study.

4.3.1 Method

We set a simple, nonparametric prior on the baseline rate . To that aim, we assume that this intensity is a step function. The time axis is divided into non-overlapping intervals, , and the levels of the baseline intensity are driven by an auto-regressive process of order 1, AR(1) and a coefficient . In other words,

We set , and and assume these values are known. Parameters and of the latent AR(1) control the regularity of the baseline intensity. The self-exciting kernel, , is of parametric form, namely, we use is the exponential decaying intensity (Dassios and Zhao, 2013):

| (11) | ||||

| (12) |

We have constructed the parameterisation so that controls the strength of the effect of past data and that controls the shape of the relationship with past data. Notice that, ignoring , is in the form of a probability distribution on . The baseline and the self-excitement kernel, once combined, give the overall Hawkes process rate at given the event before time :

| (13) |

The observed data generated by the Hawkes process with this intensity is a set of ordered events , ,…of random cardinal. The data can be sliced according to our partition of the real axis into nonoverlapping intervals:

The process , with the latent does not form a state space model: given the parameters, the set depends on , but also on the whole history . Nevertheless, the process forms a Markov chain, and it is clear that the process with the latent forms a state space model. Given and , the proposal which we use to simulate is as follows: we draw and we complete with the observed . Yet, the simulated are drawn as a realisation of the Hawkes process on given and .

Note that, in either case, it is possible that or is the empty set. This complicates definitions of summary statistics, so we append some imaginary events and : we set and , where and . The following summary statistics are now defined on (and likewise on ): the number of events in the interval, the sum of squares of inter-event times,

the sum of cubes of inter-event times,

and the minimum of inter-event times,

These summary statistics were used to construct estimators for , and , based on the summary statistics. To construct the estimators, we performed linear regression adjustment on these summary statistics (Beaumont et al., 2002). The distance is the Euclidean distance on these empirical estimators. Tuning parameters used in the SMC2 procedure were the following . The transition kernel (Algorithm 3) is defined in the following manner:

| (14) |

where is the maximum likelihood estimate of the covariance matrix of and is a fixed tuning parameter set to 0.1. Based on our definition of , the ratio of transition kernels is derived

4.3.2 Results

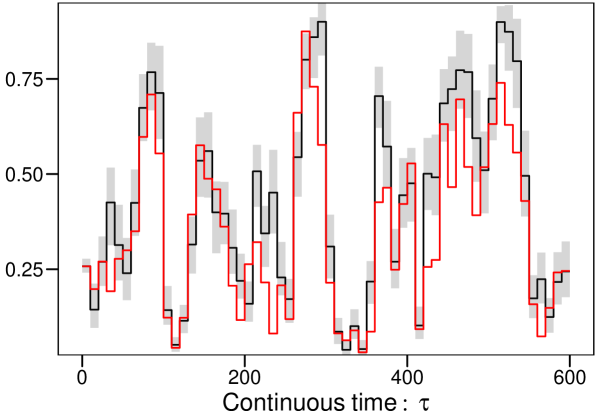

The synthetic dataset we consider as observed data is simulated with known parameter values . The observations are simulated up to . The true state is shown, in red, in Figure 6; along with the Bayesian prediction intervals for the marginalised filtering distributions. The results show very good correspondence with the true state, considering the complexity and dependencies within the Hawkes simulation, see Equation (13).

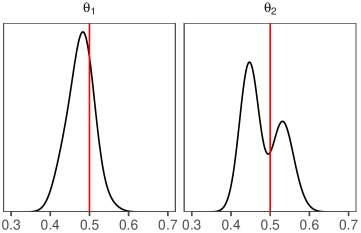

The priors were for both parameters. The posteriors are shown in Figure 7. The precision of the state inference is not reflected in the parameter inference, parameters. The posterior variance is slightly higher for , which may be related to how the distance was defined, with respect to estimators on and .

This example illustrates how a complex problem, with a nonparametric prior on the functional parameters of a stochastic process, can be included in a state space model. The inference problem is thus more challenging than the parametric problem studied by Rasmussen (2013). Despite the approximation due to an ABC approach, the results we obtained are interesting. They may deserve more numerical studies to compare carefully there accuracy with methods of proven accuracy such as Reynaud-Bouret et al. (2013).

5 Discussion and Conclusion

We have developed a CPS inference method (Algorithm 3) for likelihood-free problems without the need for any manual calibration of time-indexed tuning parameters. This algorithm, in some sense, resembles that from Chapter 4, where SABC transitions a set of parameter proposals through a sequence of decreasing and automatically calibrated thresholds. This is one example of the link between sequential algorithms for fixed parameters and particle filters for state parameters. In this chapter, we have constructed an algorithm which performs likelihood-free CPS inference with automatically tuned thresholds. The ABC thresholds are automatically calibrated as the algorithm progresses along the time index. It is important to store , as they are reused within the rejuvenation step to ensure that the resampling-move step preserves the intended approximate posterior distribution. We successfully retrieved the state trajectory, to a high level of precision, in all three examples and also retrieved the static parameters. Inference for the static parameters proved to be more difficult than the state parameters in all three examples.

As is the case for the SMC2 algorithm (Chopin et al., 2013), the computation time scales superlinearly with time . Recently, Crisan and Miguez (2018) developed a CPS algorithm which scales linearly with , with the disadvantage that the algorithm is no longer consistent for fixed . The memory requirements also became very high. For instance, the skew normal example, had , , and 20 time points. With 16 processors, the computation time was 37 minutes, with 14 GB of memory usage. More efficient data structures for storing full paths are discussed by Jacob et al. (2015).

Indexing of the variables within Algorithm 3 became very involved. This is because the algorithms are naturally written as object orientated programs, where the particle filter and SMC2 update communicate with one another while storing their evaluation environment. However, we wrote this algorithm as a functional program since this is the form most interpretable to statisticians.

Acknowledgements

Computing facilities were provided by the High Performance Computing (HPC), Queensland University of Technology. This work was supported by the ARC Centre of Excellence for Mathematical and Statistical Frontiers (ACEMS). This work was funded through the ARC Linkage Grant “Improving the Productivity and Efficiency of Australian Airports” (LP140100282) and the ARC Laureate Fellowship Program. At the beginning of this work, Kerrie Mengersen held the Jean-Morlet Chair at CIRM, Aix-Marseille University. The three first authors (Ebert, Pudlo, Mengersen) took advantage of the Chair’s invitation program to begin this research work. Christopher Drovandi was supported by an Australian Research Council Discovery Project (DP200102101).

References

- Andrieu et al. (2010) Christophe Andrieu, Arnaud Doucet, and Roman Holenstein. Particle Markov chain Monte Carlo methods. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 72(3):269–342, 2010.

- Azzalini (1985) Adelchi Azzalini. A class of distributions which includes the normal ones. Scandinavian Journal of Statistics, 12(2):171–178, 1985.

- Azzalini (2005) Adelchi Azzalini. The skew-normal distribution and related multivariate families. Scandinavian Journal of Statistics, 32(2):159–188, 2005.

- Baum and Petrie (1966) Leonard E Baum and Ted Petrie. Statistical inference for probabilistic functions of finite state Markov chains. The Annals of Mathematical Statistics, 37(6):1554–1563, 1966.

- Beaumont et al. (2002) Mark A. Beaumont, Wenyang Zhang, and David J. Balding. Approximate Bayesian computation in population genetics. Genetics, 162(4):2025–2035, 2002.

- Beaumont et al. (2009) Mark A Beaumont, Jean-Marie Cornuet, Jean-Michel Marin, and Christian P Robert. Adaptive approximate Bayesian computation. Biometrika, 96(4):983–990, 2009.

- Calvet and Czellar (2014) Laurent E Calvet and Veronika Czellar. Accurate methods for approximate Bayesian computation filtering. Journal of Financial Econometrics, 13(4):798–838, 2014.

- Carpenter et al. (2017) Bob Carpenter, Andrew Gelman, Matthew D Hoffman, Daniel Lee, Ben Goodrich, Michael Betancourt, Marcus Brubaker, Jiqiang Guo, Peter Li, and Allen Riddell. Stan: a probabilistic programming language. Journal of Statistical Software, 76(1), 2017.

- Carpenter et al. (1999) James Carpenter, Peter Clifford, and Paul Fearnhead. Improved particle filter for nonlinear problems. IEE Proceedings-Radar, Sonar and Navigation, 146(1):2–7, 1999.

- Chopin et al. (2013) Nicolas Chopin, Pierre E Jacob, and Omiros Papaspiliopoulos. SMC2: an efficient algorithm for sequential analysis of state space models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 75(3):397–426, 2013.

- Crisan and Miguez (2018) Dan Crisan and Joaquin Miguez. Nested particle filters for online parameter estimation in discrete-time state-space Markov models. Bernoulli, 24(4A):3039–3086, 2018.

- Dassios and Zhao (2013) Angelos Dassios and Hongbiao Zhao. Exact simulation of Hawkes process with exponentially decaying intensity. Electronic Communications in Probability, 18(62):1–13, 2013.

- Davey et al. (2015) Samuel Davey, Neil Gordon, Ian Holland, Mark Rutten, and Jason Williams. Bayesian Methods in the search for MH370. Springer, 2015.

- Del Moral et al. (2012) Pierre Del Moral, Arnaud Doucet, and Ajay Jasra. An adaptive sequential Monte Carlo method for approximate Bayesian computation. Statistics and Computing, 22(5):1009–1020, 2012.

- Del Moral et al. (2015) Pierre Del Moral, Ajay Jasra, Anthony Lee, Christopher Yau, and Xiaole Zhang. The alive particle filter and its use in particle Markov chain Monte Carlo. Stochastic Analysis and Applications, 33(6):943–974, 2015.

- Djuric et al. (2003) Petar M Djuric, Jayesh H Kotecha, Jianqui Zhang, Yufei Huang, Tadesse Ghirmai, Mónica F Bugallo, and Joaquin Miguez. Particle filtering. IEEE signal processing magazine, 20(5):19–38, 2003.

- Doucet et al. (2000) Arnaud Doucet, Simon Godsill, and Christophe Andrieu. On sequential Monte Carlo sampling methods for Bayesian filtering. Statistics and computing, 10(3):197–208, 2000.

- Drovandi and McCutchan (2016) Christopher C Drovandi and Roy A McCutchan. Alive SMC2: Bayesian model selection for low-count time series models with intractable likelihoods. Biometrics, 72(2):344–353, 2016.

- Drovandi and Pettitt (2011) Christopher C. Drovandi and Anthony N. Pettitt. Estimation of parameters for macroparasite population evolution using approximate Bayesian computation. Biometrics, 67(1):225–233, 2011.

- Drovandi et al. (2016) Christopher C Drovandi, Anthony N Pettitt, and Roy A McCutchan. Exact and approximate Bayesian inference for low integer-valued time series models with intractable likelihoods. Bayesian Analysis, 11(2):325–352, 2016.

- Fasiolo et al. (2016) Matteo Fasiolo, Natalya Pya, and Simon N Wood. A comparison of inferential methods for highly nonlinear state space models in ecology and epidemiology. Statistical Science, 31(1):96–118, 2016.

- Fearnhead and Künsch (2018) Paul Fearnhead and Hans R Künsch. Particle filters and data assimilation. Annual Review of Statistics and its Application, 5:421–449, 2018.

- Fenicia et al. (2018) Fabrizio Fenicia, Dmitri Kavetski, Peter Reichert, and Carlo Albert. Signature-domain calibration of hydrological models using approximate Bayesian computation: empirical analysis of fundamental properties. Water Resources Research, 54(6):3958–3987, 2018.

- Gordon et al. (1993) Neil J Gordon, David J Salmond, and Adrian FM Smith. Novel approach to nonlinear/non-Gaussian Bayesian state estimation. In Radar and Signal Processing, IEE Proceedings F, volume 140, pages 107–113. IET, 1993.

- Hawkes (1971a) Alan G Hawkes. Point spectra of some mutually exciting point processes. Journal of the Royal Statistical Society: Series B (Methodological), 33(3):438–443, 1971a.

- Hawkes (1971b) Alan G Hawkes. Spectra of some self-exciting and mutually exciting point processes. Biometrika, 58(1):83–90, 1971b.

- Jacob et al. (2015) Pierre E Jacob, Lawrence M Murray, and Sylvain Rubenthaler. Path storage in the particle filter. Statistics and Computing, 25(2):487–496, 2015.

- Jasra et al. (2012) Ajay Jasra, Sumeetpal S Singh, James S Martin, and Emma McCoy. Filtering via approximate Bayesian computation. Statistics and Computing, 22(6):1223–1237, 2012.

- Joanes and Gill (1998) DN Joanes and CA Gill. Comparing measures of sample skewness and kurtosis. Journal of the Royal Statistical Society: Series D (The Statistician), 47(1):183–189, 1998.

- Kalman (1960) Rudolph Emil Kalman. A new approach to linear filtering and prediction problems. Journal of Basic Engineering, 82(1):35–45, 1960.

- Kantas et al. (2015) Nikolas Kantas, Arnaud Doucet, Sumeetpal S Singh, Jan Maciejowski, and Nicolas Chopin. On particle methods for parameter estimation in state-space models. Statistical Science, 30(3):328–351, 2015.

- Kitagawa (1987) Genshiro Kitagawa. Non-Gaussian state-space modeling of nonstationary time series. Journal of the American Statistical Association, 82(400):1032–1041, 1987.

- Li et al. (2015) Tiancheng Li, Miodrag Bolic, and Petar M Djuric. Resampling methods for particle filtering: classification, implementation, and strategies. IEEE Signal Processing Magazine, 32(3):70–86, 2015.

- Liu and West (2001) Jane Liu and Mike West. Combined parameter and state estimation in simulation-based filtering. In Sequential Monte Carlo Methods in Practice, pages 197–223. Springer, 2001.

- Liu (2008) Jun S Liu. Monte Carlo strategies in scientific computing. Springer Science & Business Media, 2008.

- Lombardi (2007) Marco J Lombardi. Bayesian inference for -stable distributions: a random walk MCMC approach. Computational Statistics & Data Analysis, 51(5):2688–2700, 2007.

- Lombardi and Calzolari (2009) Marco J Lombardi and Giorgio Calzolari. Indirect estimation of -stable stochastic volatility models. Computational Statistics & Data Analysis, 53(6):2298–2308, 2009.

- Lux (2018) Thomas Lux. Estimation of agent-based models using sequential Monte Carlo methods. Journal of Economic Dynamics and Control, 91:391–408, 2018.

- Mandelbrot (1963) Benoit Mandelbrot. The variation of certain speculative prices. The Journal of Business, 36(4):394–419, 1963.

- Marin et al. (2012) Jean-Michel Marin, Pierre Pudlo, Christian P Robert, and Robin J Ryder. Approximate Bayesian computational methods. Statistics and Computing, 22(6):1167–1180, 2012.

- Mariño et al. (2017) Inés P Mariño, Alexey Zaikin, and Joaquín Míguez. A comparison of Monte Carlo-based Bayesian parameter estimation methods for stochastic models of genetic networks. PloS one, 12(8):e0182015, 2017.

- Marjoram et al. (2003) Paul Marjoram, John Molitor, Vincent Plagnol, and Simon Tavaré. Markov chain Monte Carlo without likelihoods. Proceedings of the National Academy of Sciences of the United States of America, 100(26):15324–15328, 2003. ISSN 0027-8424.

- Martin et al. (2019) Gael M Martin, Brendan PM McCabe, David T Frazier, Worapree Maneesoonthorn, and Christian P Robert. Auxiliary likelihood-based approximate Bayesian computation in state space models. Journal of Computational and Graphical Statistics, 28(3):508–522, 2019.

- Meyer et al. (2019) David Meyer, Evgenia Dimitriadou, Kurt Hornik, Andreas Weingessel, and Friedrich Leisch. e1071: Misc Functions of the Department of Statistics, Probability Theory Group (Formerly: E1071), TU Wien, 2019. URL https://CRAN.R-project.org/package=e1071. R package version 1.7-1.

- Müller (1991) Peter Müller. Monte Carlo integration in general dynamic models. Contemporary Mathematics, 115:145–163, 1991.

- Naesseth et al. (2019) Christian A Naesseth, Fredrik Lindsten, and Thomas B Schön. Elements of sequential Monte Carlo. arXiv:1903.04797, 2019.

- Peters et al. (2012) Gareth W Peters, Scott A Sisson, and Yanan Fan. Likelihood-free Bayesian inference for -stable models. Computational Statistics & Data Analysis, 56(11):3743–3756, 2012.

- Rasmussen (2013) Jakob Gulddahl Rasmussen. Bayesian inference for Hawkes processes. Methodology and Computing in Applied Probability, 15(3):623–642, 2013.

- Reynaud-Bouret et al. (2013) Patricia Reynaud-Bouret, Vincent Rivoirard, and Christine Tuleau-Malot. Inference of functional connectivity in neurosciences via Hawkes processes. In 2013 IEEE Global Conference on Signal and Information Processing, pages 317–320. IEEE, 2013.

- Sisson et al. (2007) S. A. Sisson, Y. Fan, and Mark M. Tanaka. Sequential Monte Carlo without likelihoods. Proceedings of the National Academy of Sciences of the United States of America, 104(6):1760–1765, 2007. ISSN 0027-8424.

- Sisson et al. (2018) Scott A Sisson, Yanan Fan, and Mark Beaumont. Handbook of approximate Bayesian computation. Chapman and Hall/CRC, 2018.

- Stan Development Team (2018) Stan Development Team. Stochastic volatility models. In Stan Modeling Language Users Guide and Reference Manual. mc-stan.org, 2018. URL https://mc-stan.org/docs/2_22/stan-users-guide/stochastic-volatility-models.html.

- Särkkä (2013) Simo Särkkä. Bayesian filtering and smoothing, volume 3. Cambridge University Press, 2013.

- Tavaré et al. (1997) Simon Tavaré, David J. Balding, Robert C. Griffiths, and Peter Donnelly. Inferring coalescence times from DNA sequence data. Genetics, 145(2):505–518, 1997.

- Vankov et al. (2019) Emilian R Vankov, Michele Guindani, and Katherine B Ensor. Filtering and estimation for a class of stochastic volatility models with intractable likelihoods. Bayesian Analysis, 14(1):29–52, 2019.

A Proof of Proposition 1

The proof is done by induction on .

Base case: .

A.0.1 Inductive step:

Let is the -field generated by all random draws of the ABC-SMC2 algorithm before entering the -th update. As above, since , we have

| (17) | ||||

And, during the -th update, we draw , and

Thus,

Thus,

Using the induction hypothesis, we get

This gives the desired results because of the inductive definition of the target given in (6).

B Proof of Propostion 2

We start by proving the consistency at . For the moment, fix and and consider the , , introduced in Equation (15). These random variables are iid and

because of Equation (16). By the strong law of large number, we obtain that

To obtain the desired result at , it is enough to average the above result over and .

We prove now the consitency at . Likewise, because of Equation (17), it is enough to prove that, for any fixed and ,

| (18) |

Let be the -field generated by , , , for , and . Since we assume that we never resample the ’s, these -fields are independant. Now, fix and . The random variables are -mesurable, thus they are independant. And it is clear that they are identically distributed. The strong law of large numbers concludes the proof.