Extremal clustering in non-stationary random sequences

Abstract

It is well known that the distribution of extreme values of strictly stationary sequences differ from those of independent and identically distributed sequences in that extremal clustering may occur. Here we consider non-stationary but identically distributed sequences of random variables subject to suitable long range dependence restrictions. We find that the limiting distribution of appropriately normalized sample maxima depends on a parameter that measures the average extremal clustering of the sequence. Based on this new representation we derive the asymptotic distribution for the time between consecutive extreme observations and construct moment and likelihood based estimators for measures of extremal clustering. We specialize our results to random sequences with periodic dependence structure.

Keywords: Clustering of extremes, extremal index, interexceedance times, intervals estimator, non-stationary sequences, periodic processes.

1 Introduction

Extreme value theory for strictly stationary sequences has been extensively studied, initiated in the works of Watson (1954), Berman (1964), Loynes (1965), and continued by Leadbetter (1974, 1983) and O’Brien (1987) amongst others. One of the key findings in this line of research is that unlike in independent and identically distributed sequences where extreme values tend to occur in isolation, stationary sequences possess an intrinsic potential for clustering of extremes, i.e., several successive or close extreme values may be observed. Understanding the extremal clustering characteristics of a stochastic process is critical in many applications where a cluster of extreme values may have serious consequences. For example, if a sequence consists of daily temperatures at some fixed location then a cluster of extremes may correspond to a heatwave.

The extent to which extremal clustering may occur is naturally measured, for strictly stationary sequences, by a parameter known as the extremal index. Let be a sequence of random variables with common marginal distribution function , and let and . Also, let be a sequence of real numbers that we may informally think of as thresholds or levels. In the special case that and are independent, , then a necessary and sufficient condition for to converge to a limit in as is that in which case (Leadbetter et al., 1983, Theorem 1.5.1). More generally, if is a strictly stationary sequence, then is not sufficient to ensure the convergence of . However, in most cases of practical interest, provided that a suitable long range dependence restriction is satisfied, such as condition of Leadbetter (1974), one has where is the extremal index. Leadbetter (1983) showed that exceedances of the level occur in clusters with the limiting mean cluster size being equal to , and Hsing (1987) showed that distinct clusters may be considered independent in the limit.

Another characterization of that links it to the extremal clustering properties of a strictly stationary sequence can be found in O’Brien (1987). Defining , it was shown that the distribution function of satisfies

| (1.1) |

where

| (1.2) |

for some , and provided the limit exists, as . This result illustrates that smaller values of are indicative of a larger degree of extremal clustering, since the conditional probability in (1.2) is small when an exceedance of a large threshold is likely to soon be followed by another exceedance.

Early attempts at estimating were based on associating with the limiting mean cluster size. Different methods for identifying clusters gave rise to different estimators, well known examples being the runs and blocks estimators (Smith and Weissman, 1994). For the runs estimator, a cluster is identified as being initialized when a large threshold is exceeded and ends when a fixed number, known as the run length, of non-exceedances occur. The extremal index is then estimated by the ratio of the number of identified clusters to the total number of exceedances. A difficulty that arises when using this estimator is its sensitivity to the choice of run length (Hsing, 1991).

The problem of cluster identification was studied by Ferro and Segers (2003) who considered the distribution of the time between two exceedances of a large threshold. They found that the limiting distribution of appropriately normalized interexceedance times converges to a distribution that is indexed by . In particular, for a given threshold , they define the random variable , and found that as converges in distribution to a mixture of a point mass at zero and an exponential distribution with mean . Thus, by computing theoretical moments of this limiting distribution and comparing them with their empirical counterparts, they construct their so-called intervals estimator.

Motivated by the fact that many real world processes are non-stationary, in this paper we investigate the effect of non-stationarity on extremal clustering. Previous statistical works that consider extremal clustering in non-stationary sequences include Süveges (2007), who used the likelihood function introduced by Ferro and Segers (2003) for the extremal index together with smoothing methods to capture non-stationarity in a time series of temperature measurements. In a similar application, Coles et al. (1994) used a Markov model together with simulation techniques to estimate the extremal index within different months.

An early work that developed extreme value theory for non-stationary sequences with a common marginal distribution is Hüsler (1983), which focused on the asymptotic distribution of the sample maxima but did not consider extremal clustering. Hüsler (1986) considered the more general case where the margins may differ and also discussed the difficulty of defining the extremal index for general non-stationary sequences.

Here, we consider a sequence of random variables with common marginal distribution function , but do not assume stationarity in either the weak or strict sense. As we assume common margins, non-stationarity may arise through changes in the dependence structure. We show, under assumptions similar to O’Brien (1987), that

| (1.3) |

where

| (1.4) |

Thus, we find that the limiting distribution of the sample maximum at large thresholds is characterized by a parameter , provided the limit exists, which by analogy with equation (1.2), may be regarded as the average of local extremal indices. In this paper we develop methods for estimating these local extremal indices by adapting the methods of Ferro and Segers (2003) for the extremal index to our non-stationary setting. In the special case that the sequence is stationary, so that all terms in the summation (1.4) are equal, the formula for reduces to in (1.2).

The structure of the paper is as follows. Section 2 defines the notation and assumed mixing condition used throughout the paper and states the main theoretical results regarding the asymptotic distribution of the sample maxima and normalized interexceedance times. Section 3 discusses approaches to parameter estimation using the result from Section 2 on the distribution of the interexceedance times. Section 4 considers the estimation problem for two simple non-stationary Markov sequences with periodic dependence structures and Section 5 gives the proofs of the main theoretical results.

2 Theoretical results

2.1 Notation, definitions and preliminary results

Throughout the paper, when not explicitly stated otherwise, all limits should be interpreted as “as ”. We assume that all random variables in the sequence have common marginal distribution with upper endpoint , though we do not assume stationarity. In addition to the definitions for and given in the Section 1, we define where is an arbitrary set of positive integers, and write for the number of elements in . We also refer to a set of consecutive integers as an interval. If and are two intervals, we say that and are separated by if min() - max() = or min() - max() = , i.e., there are intermediate values between and . The set is denoted by . Equality in distribution of two random variables and is denoted by

We assume that the sequence satisfies the asymptotic independence of maxima (AIM) mixing condition of O’Brien (1987) which restricts long range dependence.

Definition 2.1.

The sequence is said to satisfy the asymptotic independence of maxima condition relative to the sequence of real numbers, abbreviated to “ satisfies AIM()”, if there exists a sequence of positive integers with such that for any two intervals and separated by we have

| (2.1) |

where the maximum is taken over all positive integers and such that , and .

Definition 2.1 states a slightly weaker condition than the widely used ) condition (Leadbetter, 1983) in that only certain intervals and need to be considered in (2.1) rather than arbitrary sets of integers, so that all examples in the literature of sequences satisfying ) also satisfy AIM(). For example, stationary Gaussian sequences with autocorrelation function satisfying Berman’s condition, (Berman, 1964), satisfy AIM() for any sequence such that is bounded and any (Leadbetter et al., 1983, Lemma 4.4.1). The analogous result for non-stationary Gaussian sequences is given in Hüsler (1983), where Berman’s condition is replaced by with and the correlation between and .

O’Brien (1987) showed that if is a stationary positive Harris Markov sequence with separable state space and is a measurable function then the sequence satisfies AIM() for any and with .

We note that Definition 2.1 states a property of the dependence structure of the sequence , with the specific marginal distributions playing essentially no role. In particular, if satisfies AIM() and is a monotone increasing function then satisfies AIM() with the same .

The assumption that satisfies AIM() ensures the approximate independence of the block maxima of two sufficiently separated blocks. Lemma 2.1 below provides an upper bound for the degree of dependence of block maxima for suitably separated blocks and will be useful in Section 2.2 when the limiting behaviour of is considered.

Lemma 2.1.

Let satisfy AIM() and let be distinct subintervals of where and , . Suppose that and are separated by for . Then

| (2.2) |

2.2 Asymptotic distribution of

In this section we investigate the limiting behaviour of , with the main result being Theorem 2.1. In addition to assuming that satisfies AIM(), we will assume that the rate of growth of the sequence is controlled via

| (2.3) |

In the case of continuous marginal distributions, (2.3) is immediately satisfied by . More generally, Theorem 1.7.13 of Leadbetter et al. (1983) guarantees the existence of a sequence satisfying (2.3) when is in the domain of attraction of any of the three classical extreme value distributions (Haan and Ferreira, 2006, Section 1.2).

We use the standard technique of block-clipping, see for example Section 10.2.1 in Beirlant et al. (2004), to split the interval into subintervals, or blocks, of alternating large and small lengths. Specifically, for sequences and such that and we define

| (2.4) | ||||

for , where .

If we take the sequence appearing in the construction of the blocks and to be the same as that in Definition 2.1, then Lemma 2.1 bounds the degree of dependence of the collection of random variables , and this allows us to prove Lemma 2.2 below which modifies Lemma 3.1 from O’Brien (1987) to allow for non-stationarity.

Lemma 2.2.

Remarks. Equation (2.6) follows easily from (2.2) by making the identification and using (2.3) and (2.5). Additionally, if satisfies AIM() then we can always find a sequence such that (2.5) holds, for example, by taking . Thus the only assumption in Lemma 2.2 beyond common margins is that satisfies AIM() for a sequence satisfying (2.3).

We can now state our main theorem.

Theorem 2.1.

As it was noted in Section 1, for independent sequences (2.3) implies that . For a random sequence satisfying the conditions of Lemma 2.2, the following result gives a necessary and sufficient condition for the convergence of

Corollary 2.2.

Corollary 2.2 follows from (2.8) since if and only which is easily seen by taking logs in the latter expression and using log( as .

A basic question regarding the constant appearing in Corollary 2.2 is whether it is independent of the particular value of in (2.3), i.e., do we obtain the same limiting value of regardless of the specific sequence and used in (2.3)? We will see in Section 2.3 that for sequences with periodic dependence this is indeed the case, and Theorem 2.3 gives sufficient conditions for this to hold more generally.

We now turn our attention to the conditional probabilities appearing in the summation (2.9), which contain local information regarding the strength of extremal clustering in the sequence .

Definition 2.2.

Under the same assumptions as in Lemma 2.2, let be the sequence of functions defined on by

| (2.10) |

We define the extremal clustering function of to be the function given by

| (2.11) |

provided the limit exists.

In the special case that the sequence is stationary, the extremal clustering function is simply a constant function equal to the extremal index of the sequence. In the general case, if we think of the index in as denoting time, then we may regard as the extremal index at time . The definition of entails pointwise convergence of the sequence of approximations in equation (2.10). When there is a uniformity in this convergence and the extremal clustering function is Cesàro summable we obtain the following result.

Theorem 2.3.

As with the constant in Corollary 2.2, we may inquire as to whether the extremal clustering function is independent of the value of and sequence used in (2.3). Although we do not attempt to answer this in full generality, we note that, as with the conditional probability formulation of the extremal index, for most sequences that are of practical interest, the formula defining may be reduced to a form that makes no explicit reference to the sequences and . For example, under the additional assumption due to Smith (1992) which requires that for any in Theorem 2.1 we have

| (2.14) |

for each , then (2.11) reduces to

| (2.15) |

Another common assumption for statistical applications is the condition of Chernick et al. (1991) which we define below in a slightly modified form for our non-stationary setting.

Definition 2.3.

A sequence as in Theorem 2.1 is said to satisfy the condition, where , if

| (2.16) |

for each . For the case , we define .

Note that it is assumed in Definition 2.3 that satisfies AIM in conjunction with (2.16). Whereas (2.1) limits the degree of long range dependence in the sequence, (2.16) is a local mixing condition that ensures that the probability of again exceeding the threshold in a block of observations, after dropping below it for consecutive observations falls to zero sufficiently rapidly as . The case where implies that in the limit, any exceedances of a high threshold occur in isolation and is implied in the stationary case by the condition of Leadbetter et al. (1983), Chapter 3. One might expect that a more natural condition in our non-stationary setting would be to replace the constant in (2.16) by to reflect possible variations in the strength of local dependence. However, when (2.16) holds for some particular , then it also holds for any other with and so provided that the sequence is bounded we may set and obtain (2.16) for each . Thus the assumption of a single value of in Definition 2.3 allows for variations in the strength of local dependence while at the same time restricting it to not persist too strongly to an arbitrary number of lags. If whenever is a sequence as in Theorem 2.1 and the condition holds then (2.11) reduces to

| (2.17) |

2.3 Periodic dependence

In this section we assume that the sequence has a more refined structure than in the previous sections, namely that of periodic dependence, under which the results of Section 2.2 may be simplified considerably.

Definition 2.4.

A sequence with common marginal distributions is said to have periodic dependence if there exists such that for all The smallest with this property is called the fundamental period.

Whereas for a strictly stationary sequence an arbitrary shift in time leaves the finite-dimensional distributions unchanged, for a sequence with periodic dependence only time shifts that are a multiple of the fundamental period leave finite-dimensional distributions unchanged. In particular, when Such sequences often mimic the dependence structure of certain environmental time series where we might expect a fundamental period of one year.

The following result concerning the convergence of shows that Theorem 3.7.1 of Leadbetter et al. (1983) for stationary sequences also holds for non-stationary sequences with periodic dependence.

Theorem 2.4.

Although Theorem 2.4 makes no reference to the extremal clustering function, when converges, the constant in Theorem 2.4 is identified by Corollary 2.2 as with as in equation (2.9). Due to periodicity we obtain the simplified formula and the extremal clustering function is determined by the values which repeat cyclically. Moreover, for sequences with periodic dependence, the convergence statement (2.12) can be strengthened to uniform convergence since

The following result is an immediate consequence of Theorem 2.4.

Corollary 2.5.

Let have periodic dependence with common marginal distribution function . For each , let be a sequence such that and suppose that satisfies AIM for each such . If converges for a single then it converges for all , and in particular for some .

2.4 Interexceedance times

Ferro and Segers (2003) provided a method for estimating the extremal index of a stationary sequence without the need for identifying independent clusters of extremes. This was achieved by considering the distribution of the time between two exceedances of a threshold , i.e.,

| (2.18) |

as approaches . In particular, it was shown that the normalized interexceedance time converges in distribution as to a mixture of a point mass at zero, with probability , and an exponential random variable with mean , with probability . The mixture arises from the fact that the interexceedance times can be classified in to two categories: within cluster and between cluster times. The mass at zero stems from the fact that the within cluster times, which tend to be small relative to the between cluster times, are dominated by the factor .

In the stationary case, conditioning on the event in equation (2.18) may be replaced with and replaced by for any without affecting the distribution of . In the non-stationary case we consider for each and threshold , the random variable defined by

| (2.19) |

whose distribution in general depends on . We find that the distribution of converges as to a mixture of a mass at zero, with probability , and an exponential random variable with mean , with probability . As in Ferro and Segers (2003), a slightly stronger mixing condition is required to derive this result than was needed for Theorem 2.1. We denote by , the -algebra generated by the events , , and we define the mixing coefficients

| (2.20) |

where the supremum is over all with and We will assume the existence of a sequence such that for all . This implies that satisfies AIM() with the same choice of and so we may find a sequence so that (2.5) is satisfied. We define to be as in equation (2.10) and assume a slightly stronger form of convergence than in (2.12) but weaker than uniform convergence

The limiting distribution of the normalized interexceedance times is given in Theorem 2.6.

Theorem 2.6.

Let be a sequence of random variables with common marginal distribution and a sequence of real numbers such that . Suppose that there is a sequence of positive integers such that and for all Then, if is Cesàro summable we have, for each fixed and

| (2.21) |

3 Estimation with a focus on periodic sequences

In this section we consider moment and maximum likelihood estimators for and based on the limiting distribution of normalized interexceedance times given in Theorem 2.6. We first show that the intervals estimator of Ferro and Segers (2003) may be used to estimate and then consider likelihood based estimation along the lines of Süveges (2007). For simplicity, we focus our discussion on the case of periodic dependence as in Definition 2.4. Such an assumption reduces estimation of the extremal clustering function to estimating the vector with where is the fundamental period which, for simplicity, we assume to be known a-priori. Such an assumption is important for the moment based estimators of Section 3.1 where one needs replications of interexceedance times in order to use the estimators, but can easily be relaxed for likelihood based inference.

3.1 Moment based estimators

Theorem 2.6 implies that the first two moments of satisfy and as . Assuming the threshold is chosen to be suitably large so that the terms can be neglected, these two equations can be solved with respect to the unknown parameters to give

| (3.1) |

A complication that arises in the non-stationary setting is that, since is defined via a conditional probability given the event if does not exceed the threshold then there are no interexceedance times to estimate . This problem doesn’t arise in the stationary case where every interexceedance time may be used to estimate the extremal index .

In order to estimate then, it is natural to assume that the extremal clustering function is structured in some way, e.g., periodic or piecewise constant. Making such an assumption allows us to use multiple interexceedance times to estimate . Focusing on the case where has periodic dependence with fundamental period , all exceedances of the threshold occuring at points that are separated by a multiple of give rise to interexceedance times that may be used to estimate the same value of the extremal clustering function. More precisely, suppose that is a sample of size of the process with exceedance times and corresponding interexceedance times with as in equation (2.19). The set of interexceedance times that may be used for estimating is the subset defined by If , then we may relabel the elements of as where now the subscript remains fixed. Making further, more refined assumptions regarding the nature of the periodicity of the process under consideration may give rise to different sets . For example, in an environmental time series setting it may be reasonable to assume that the extremal clustering function is piecewise constant within months or seasons, so that all interexceedance times that correspond to exceedances within the same calendar month or season belong to the same .

Equation suggests the estimator

| (3.2) |

whose bias we now investigate. From (2.21) we have that for

which motivates consideration of the positive integer valued random variable defined by

where and and we may identify with In a similar manner to Ferro and Segers (2003), we find that and , so that upon simplification we find that

| (3.3) |

A Taylor expansion of the right hand side of equation (3.3) around gives

so that the first order bias of is . On the other hand, since

this motivates the estimator

| (3.4) |

whose first order bias is zero. This estimator forms the key component of the intervals estimator of Ferro and Segers (2003), which we can use to estimate . We note that may take values greater than 1 and is not defined if max as then the denominator in (3.4) is zero. In order to deal with these cases, the intervals estimator of is defined as

While equation (3.1) also suggests an estimator for , this is based only on the interexceedances relevant to estimating and also requires an estimate of . One possibility is to obtain such estimates and take the mean of these as the estimate of . However, this estimator need not respect the relation , a consequence of the fact that we dropped the terms when solving the first two moment equations. In the examples that we consider in Section 4, we estimate using the mean of the estimates for the values.

3.2 Maximum likelihood estimation

Theorem 2.6 also allows for the construction of the likelihood function for the vector of unknown parameters. This is an attractive approach due to the modelling possibilities that become available, however, as discussed in Ferro and Segers (2003) in the stationary case, problems arise with maximum likelihood estimation due to uncertainty in how to assign interexceedance times to the components of the limiting mixture distribution. Since the asymptotically valid likelihood is used as an approximation at some subasymptotic threshold , all observed normalized interexceedance times are strictly positive. Assigning all interexceedance times to the exponential part of the limiting mixture means that they are all being classified as between cluster times. This is tantamount to exceedances of a large threshold occuring in isolation, and so the maximum likelihood estimator based on this, typically misspecified, likelihood converges in probability to 1 regardless of the true underlying value of .

This problem was addressed in Süveges (2007) for sequences satisfying the condition, i.e., the case in (2.16). For such sequences, in the limit as , exceedances above cluster into independent groups of consecutive exceedances, so that all observed interexceedance times equal to one are assigned to the zero component of the mixture likelihood. On the other hand, all interexceedance times greater than one are assigned to the exponential component of the likelihood. It was found that, when the condition is satisfied, maximum likelihood estimation outperforms the intervals estimator in terms of lower root mean squared error. The consecutive exceedances model of clusters implied by is in contrast to the general situation where within clusters, exceedances may be separated by observations that fall below the threshold.

If we were to make the assumption in our non-stationary setting, so that the consecutive exceedances model for clusters is accurate, then with the interexceedance times relevant for estimating as in Section 3.1, we obtain the likelihood function as

where is the set of all interexceedance times and

The full log-likelihood is then

| (3.5) |

where and in practice must be replaced with an estimate. Unlike in the stationary case, the likelihood equations don’t have a closed form solution, essentially due to the dependence of on all the . Equation (3.5), however, is easily optimized numerically provided is not too large. If is large, it is more natural to parameterize in terms of a small number of parameters which we may estimate by maximum likelihood or consider non-parametric estimation along the lines of Einmahl et al. (2016).

We may generalise this idea and assign all interexceedance times less than or equal to some value to the zero component of the likelihood, so that the corresponding expression for becomes

| (3.6) |

This may be justified by the assumption that the sequence satisfies the condition. Selection of an appropriate value of is equivalent to the selection of the run length for the runs estimator, and this problem is considered in the stationary case in Süveges and Davison (2010) and Juan Cai (2019). However, in a non-stationary setting, where the clustering characteristics of the sequence may change in time, the appropriate value of may also be time varying, so that may be replaced with in equation (3.6). Although, as was discussed in Section 3.1, we may take a constant value of in the definition of for the purposes of estimating , one wants to select for each , the smallest such that (2.16) is satisfied (Hsing, 1993). If too small a value is selected for then some of the interexceedance times may be wrongly assigned to the exponential component of the likelihood leading to an overestimate of whereas if is selected to be too large then we tend to underestimate .

4 Examples

In this section we consider two simple examples of non-stationary Markov sequences with a periodic dependence structure and common marginal distributions. The first example we consider is the Gaussian autoregressive model

| (4.1) |

where , and . In our second example, we consider a model where follow a bivariate logistic distribution with joint distribution function

| (4.2) |

and so that For the Gaussian model, no limiting extremal clustering occurs at any point in the sequence, so that for each , in contrast to the logistic model where for each .

For sufficiently well behaved stationary Markov sequences, mixing conditions much stronger than those considered in Section 2 hold. For example, for the stationary Gaussian autoregressive sequence, with in (4.1) for all Theorems 1 and 2 from Athreya and Pantula (1986) give that the mixing conditions of Theorem 2.1 and Theorem 2.6 hold for any sequence such that , , for any . Analogous results also hold for the non-stationary models that we consider in this section, see for example Bradley (2005) Theorem 3.3 and Davydov (1973) Theorem 4.

4.1 Gaussian autoregressive model

Stationary sequences where each is a standard Gaussian random variable, are extensively studied in Chapter 4 of Leadbetter et al. (1983). It is shown there that if the lag autocorrelation satisfies , then the extremal index of the sequence equals one and so no limiting extremal clustering occurs. Thus, the stationary autoregressive sequence with in (4.1) for all has extremal index one, provided This is a special case of the more general result that a stationary asymptotically independent Markov sequence has an extremal index of one (Smith, 1992). We say that the stationary sequence is asymptotically independent at lag if where

and asymptotically independent if for all (Ledford and Tawn, 2003).

Here, we consider the non-stationary autoregressive model (4.1) and specify a periodic lag one correlation function for . Applying Theorem 6.3.4 of Leadbetter et al. (1983), and comparing the non-stationary sequence to an independent standard Gaussian sequence, we deduce that as where is the standard Gaussian distribution function, and thus conclude that and for The same conclusion may also be drawn by applying Theorem 4.1 of Hüsler (1983), which shows that if satisfies (2.3) then

We simulated 1000 realizations of this sequence of length and, for each realization, estimated and for a range of high thresholds, using both the intervals estimator and maximum likelihood with in equation (3.6) equal to zero and one. We then repeated this procedure for sequences of length and . We found that the maximum likelihood estimator with gave by far the best performance as measured by root mean squared error in . In fact, in this case the 0.025 and 0.975 empirical quantiles of the estimated values of were both 1 to two decimal places in all simulations. This is not surprising since selecting ensures that all interexceedance times have the correct asymptotic classification as between cluster times. However, in a real data example such a level of prior knowledge regarding asymptotic independence is not realistic and would render estimation redundant. Although maximum likelihood estimation with performed slightly poorer than the intervals estimator, both methods produced broadly similar results.

Table 1 shows the 0.025 and 0.975 empirical quantiles of the parameter estimates obtained using the intervals estimator. In the table, corresponds to the threshold that there is probability of exceeding at each time point i.e., . Although the true value of each is 1, so that no extremal clustering occurs in the limit as , clustering may occur at subasymptotic levels. Moreover, there will tend to be more subasymptotic clustering in the sequence at points with a larger lag one autocorrelation, i.e., larger . This point has been thoroughly discussed in the context of stationary sequences and estimation of the extremal index (Ancona-Navarrete and Tawn, 2000; Eastoe and Tawn, 2012) and leads to the notion of a subasymptotic or threshold based extremal index.

| .66, .82 | |||||||||

| .75, .97 | |||||||||

| .65, .69 | |||||||||

| .70, .75 | |||||||||

| .78, .88 | |||||||||

| .71, .73 | |||||||||

| .81, .84 | |||||||||

| .86, .95 |

4.2 Bivariate logistic dependence

The stationary logistic model, that is, (4.2) with for all , has been thoroughly studied (Smith et al., 1997; Ledford and Tawn, 2003; Süveges, 2007). The parameter controls the strength of dependence between adjacent terms in the sequence, with corresponding to independence and giving complete dependence. Such a sequence exhibits asymptotic dependence provided , in particular, By exploiting the Markov structure of the sequence, precise calculation of can be achieved using the numerical methods described in Smith (1992), where it is found for example that the sequence with has and moreover, equation (2.14) is shown to hold for all . The case of is also considered in Süveges (2007) where, based on diagnostic plots, it is concluded that the condition is not satisfied for this sequence, and moreover, the maximum likelihood estimator for based on a run length of has bias of around . Süveges and Davison (2010) find that a more suitable run length is , and in this case the maximum likelihood estimator for has lower root mean squared error than the intervals estimator. Smaller values of will tend to be associated with larger values of the run length , though the precise nature of this relation is unclear.

We consider the non-stationary logistic model (4.2) with for Note that although we have specified the same parametric form for the dependence parameters as in the previous example for , the two parameters are not directly comparable. We simulated 1000 realizations of this process, of lengths and , and estimated using maximum likelihood with at a range of different thresholds. Table 2 shows, for the different sample sizes and thresholds considered, the 0.025 and 0.975 empirical quantiles of the parameter estimates obtained from this simulation. Although the exact values of the parameters are unknown, making evaluation of any estimators performance impossible, an upper bound for is easily obtained as . In our case this gives the bounds and where the relation is interpreted componentwise. It is conceivable that the methods in Smith (1992) could be adapted to the non-stationary case to allow exact computation of though we do not pursue this direction here.

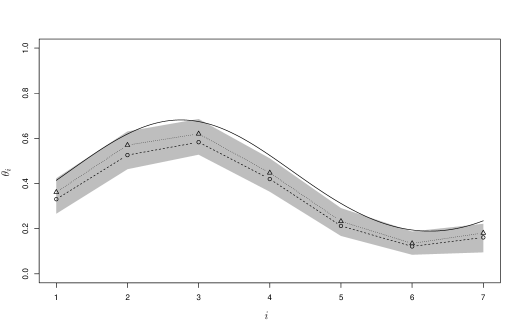

We also considered estimation of using the intervals estimator and obtained similar results to the maximum likelihood estimates. The median value of the 1000 estimates for each parameter using the different methods of estimation are shown in Figure 1 for the sample size of and threshold . The estimators clearly recover the periodicity in the dependence structure of the sequence and, on average, respect the upper bound for of .

| .28, .35 | |||||||||

| .29, .39 | |||||||||

| .27, .48 | |||||||||

| .29, .33 | |||||||||

| .32, .37 | |||||||||

| .33, .40 |

5 Proofs

5.1 Auxiliary results

In this section we state and prove some Lemmas that are required in the proof of Theorem 2.1.

Lemma 5.1.

Let be a sequence of positive integers and , an array of non-negative real numbers such that and as . Then,

| (5.1) | ||||

| if and only if | ||||

| (5.2) | ||||

Proof.

Using the fact that where , for sufficiently small , for some , we have and

| (5.3) |

so that or equivalently

| (5.4) |

from which the result follows. ∎

Lemma 5.2.

Let be a sequence of positive integers and , an array of non-negative real numbers such that , and is bounded above as . Then,

| (5.5) |

Proof.

This follows from Lemma 5.1 by considering subsequences along which converges. ∎

Lemma 5.3.

Let be a bounded function. If and then as .

Proof.

As is bounded, such that . Now let As such that

Then for

∎

Lemma 5.4.

Proof.

We first note that Lemma 2.2 also holds with blocks of length , i.e., with in place of in the definition of in equation (2.4) and in place of . Thus from equation (2.6), with blocks of length , we have that so that or equivalently

| (5.7) |

Now we note that since and and . Thus, using as , (5.7) may be written

| (5.8) |

Now it is easily seen that the second sum in converges to zero since

and so (5.8) implies Now, decomposing the event as a disjoint union we get

| (5.9) |

Again, the second sum in (5.9) goes to zero since it is bounded above by from which (5.6) follows. ∎

5.2 Proof of Lemma 2.1.

We use induction on the number of subintervals, . The case is just the fact that satisfies AIM(). Assuming that the result is true for such arbitrary subintervals, we will verify it also holds for the intervals . Let be the interval separating and and let , and we note that is an interval with and since we have,

| (5.10) |

so we may write where the remainder satisfies . We then have

| (5.11) | ||||

| (5.12) | ||||

| (5.13) | ||||

| (5.14) | ||||

| where and we have used our induction hypothesis to get (5.13) since is a union of intervals with adjacent intervals separated by . Now note that since we have and we may write where . Thus from (5.11) and (5.14) we have | ||||

as required.

5.3 Proof of Lemma 2.2.

5.4 Proof of Theorem 2.1.

In addition to the notation defined in Section 2.1, we also define

| (5.17) |

Now, for we have

and so

| (5.18) |

Now we note that

| (5.19) |

since the difference between the two sums is

so that (5.18) gives

| (5.20) |

Now we prove the reverse inequality of (5.20), i.e.,

| (5.21) |

We will show that (5.21) holds under the assumption that converges to some in , with the more general case following by considering subsequences along which converges and repeating the following argument. By Lemma 2.2, specifically equation (2.6), and Lemma 5.2 with we see that , and since (5.21) trivially holds when we may assume . Following O’Brien (1987), introduce a new sequence which plays the role of such that and let which now plays the role of and note that and the definitions in (5.17) and (2.4) are modified by replacing with . Then for , we have

and consequently, since Lemma 2.2 holds with in place of and in place of

| (5.22) |

Now, with we have, for all , and so as and . Also, which is bounded above as . Thus we may apply Lemma 5.2 to (5.22) to get

| (5.23) |

with (5.23) following from Lemma 5.4. Now Lemma 5.3 reduces (5.23) to

| (5.24) | ||||

| (5.25) |

with (5.25) following from (5.24) by the inclusions and the union bound. A similar argument that was used to show (5.19) gives

| (5.26) |

so that (5.25) becomes

| (5.27) |

and so (5.20) and (5.27) together prove (2.7). Also, since

with , this also gives (2.8).

5.5 Proof of Theorem 2.3.

Throughout we let . From Corollary (2.2) we know that with which is easily seen to converge to the same value as since

| (5.28) |

This establishes the first part of the Theorem.

5.6 Proof of Theorem 2.4.

The first step in the proof is to show that we have, for each integer ,

| (5.30) |

where . To do this we define intervals and , of alternating large and small lengths as follows,

| (5.31) |

We show that

| (5.32) | ||||

| (5.33) | ||||

| (5.34) | ||||

| and | ||||

| (5.35) | ||||

from which (5.30) follows by the triangle inequality.

(5.32) follows from and so since and

(5.33) follows immediately from Lemma 2.1 as are distinct subintervals of , and and are separated by .

(5.34) follows from and so that for .

For (5.35), we first note that Since is an interval of length , , we have by periodicity that for some Then for , we have

Hence which establishes (5.30).

Now we note that since satisfies AIM() with , it also satisfies AIM( whenever . This follows in the exact same way as for the condition, see, e.g., Lemma 3.6.2. in Leadbetter et al. (1983). This fact together with (5.30) allows the proof to proceed in exactly the same manner as the proof of Theorem 3.7.1. in Leadbetter et al. (1983).

5.7 Proof of Theorem 2.6.

For and , we define the mixing coefficients by

where the maximum is taken over intervals and that are separated by , with , and max.

We first note that since both and , we can find a sequence of positive integers such that and so that the conditions of Theorem 2.1 are satisfied.

Let and write so that for sufficiently large . Now, fix . For sufficiently large we have

| so that | ||||

In a similar way, since we have

so that Now we can derive the limiting distribution of . We have

| (5.36) |

Now we focus on the term appearing in (5.36). Since we have Since we have and so also. Thus we may find a sequence such that and , e.g., we may take Then applying Theorem 2.1 to the first terms we get where with .

We now verify that has limiting value . Define sequences , and by and and note that . Then with the usual notation , we have for all that, for sufficiently large , where we have used the fact that for sufficiently large and is non-decreasing in for fixed and . Therefore, and so and have the same limit which equals since

Finally, we have since implies that which in turn implies that . Substituting in (5.36) then gives the result.

Acknowledgements. The authors would like to express their gratitude to an anonymous reviewer whose helpful comments have greatly improved this paper.

Data availability. The datasets generated and analysed during the current study are available from the corresponding author upon request.

References

- (1)

- Ancona-Navarrete and Tawn (2000) Ancona-Navarrete, M. and Tawn, J. (2000), ‘A comparison of methods for estimating the extremal index’, Extremes 3, 5–38.

- Athreya and Pantula (1986) Athreya, K. B. and Pantula, S. G. (1986), ‘Mixing properties of Harris chains and autoregressive processes’, Journal of Applied Probability 23, 880–892.

- Beirlant et al. (2004) Beirlant, J., Goegebeur, Y., Segers, J. and Teugels, J. (2004), Statistics of Extremes, Theory and Applications, Wiley.

- Berman (1964) Berman, S. M. (1964), ‘Limit theorems for the maximum term in stationary sequences’, Ann. Math. Statist. 35, 502–516.

- Bradley (2005) Bradley, R. C. (2005), ‘Basic properties of strong mixing conditions. A survey and some open questions’, Probability Surveys 2, 107–144.

- Chernick et al. (1991) Chernick, M., Hsing, T. and McCormick, W. (1991), ‘Calculating the extremal index for a class of stationary sequences’, Advances in Applied Probability 23, 835–850.

- Coles et al. (1994) Coles, S. G., Tawn, J. A. and Smith, R. (1994), ‘A seasonal Markov model for extremely low temperatures’, Environmetrics 5, 221–239.

- Davydov (1973) Davydov, Y. A. (1973), ‘Mixing conditions for Markov chains’, Theory of Probability and its Applications 18, 312–328.

- Eastoe and Tawn (2012) Eastoe, E. F. and Tawn, J. A. (2012), ‘Modelling the distribution of the cluster maxima of exceedances of sub-asymptotic thresholds’, Biometrika 99, 43–55.

- Einmahl et al. (2016) Einmahl, J. H. J., de Haan, L. and Zhou, C. (2016), ‘Statistics of heteroscedastic extremes’, J. R. Statist. Soc. B 78, 31–51.

- Ferro and Segers (2003) Ferro, C. A. T. and Segers, J. (2003), ‘Inference for clusters of extreme values’, J. R. Statist. Soc. B 65, 545–556.

- Haan and Ferreira (2006) Haan, L. and Ferreira, A. (2006), Extreme Value Theory: An Introduction, Springer Series in Operations Research and Statistics, Springer.

- Hsing (1987) Hsing, T. (1987), ‘On the characterization of certain point processes’, Stochastic Processes and their Applications 26, 297–316.

- Hsing (1991) Hsing, T. (1991), ‘Estimating the parameters of rare events’, Stochastic Processes and their Applications 37, 117–139.

- Hsing (1993) Hsing, T. (1993), ‘Extremal index estimation for a weakly dependent stationary sequence’, Ann. Statist. 21, 2043–2071.

- Hüsler (1983) Hüsler, J. (1983), ‘Asymptotic approximation of crossing probabilities of random sequences’, Wahrscheinlichkeitstheorie verw Gebiete 63, 257–270.

- Hüsler (1986) Hüsler, J. (1986), ‘Extreme values of nonstationary random sequences’, Journal of Applied Probability 23, 937–950.

- Juan Cai (2019) Juan Cai, J. (2019), ‘A nonparametric estimator of the extremal index’, arXiv e-prints p. arXiv:1911.06674.

- Leadbetter (1974) Leadbetter, M. R. (1974), ‘On extreme values in stationary sequences’, Z. Wahr-sch. verw. Gebiete 28, 289 – 303.

- Leadbetter (1983) Leadbetter, M. R. (1983), ‘Extremes and local dependence in stationary sequences’, Z. Wahr-sch. verw. Gebiete 65, 291 – 306.

- Leadbetter et al. (1983) Leadbetter, M. R., Lindgren, G. and Rootzén, H. (1983), Extremes and Related Properties of Random Sequences and Series, Springer–Verlag, New York.

- Ledford and Tawn (2003) Ledford, A. W. and Tawn, J. A. (2003), ‘Diagnostics for dependence within time series extremes’, J. R. Statist. Soc., B 65, 521–543.

- Loynes (1965) Loynes, R. M. (1965), ‘Extreme values in uniformly mixing stationary stochastic processes’, Ann. Math. Statist. 36, 993–999.

- O’Brien (1987) O’Brien, G. L. (1987), ‘Extreme values for stationary and Markov sequences’, Ann. Probab. 15, 281–291.

- Smith (1992) Smith, R. L. (1992), ‘The extremal index for a Markov chain’, Journal of Applied Probability 29, 37–45.

- Smith et al. (1997) Smith, R. L., Tawn, J. A. and Coles, S. G. (1997), ‘Markov chain models for threshold exceedances’, Biometrika 84, 249–268.

- Smith and Weissman (1994) Smith, R. L. and Weissman, I. (1994), ‘Estimating the extremal index’, J. R. Statist. Soc. B 56, 515–528.

- Süveges (2007) Süveges, M. (2007), ‘Likelihood estimation of the extremal index’, Extremes 10, 41–55.

- Süveges and Davison (2010) Süveges, M. and Davison, A. C. (2010), ‘Model misspecification in peaks over threshold analysis’, Ann. Appl. Stat. 4, 203–221.

- Watson (1954) Watson, G. S. (1954), ‘Extreme values in samples from -dependent stationary stochastic processes’, Ann. Math. Statist. 25, 798–800.