Double-Counting Problem of the Bonus-Malus System

Abstract

The bonus-malus system (BMS) is a widely used premium adjustment mechanism based on policyholder’s claim history. Most auto insurance BMSs assume that policyholders in the same bonus-malus (BM) level share the same a posteriori risk adjustment. This system reflects the policyholder’s claim history in a relatively simple manner. However, the typical system follows a single BM scale and is known to suffer from the double-counting problem: policyholders in the high-risk classes in terms of a priori characteristics are penalized too severely (Taylor,, 1997; Pitrebois et al.,, 2003). Thus, Pitrebois et al., (2003) proposed a new system with multiple BM scales based on the a priori characteristics. While this multiple-scale BMS removes the double-counting problem, it loses the prime benefit of simplicity. Alternatively, we argue that the double-counting problem can be viewed as an inefficiency of the optimization process. Furthermore, we show that the double-counting problem can be resolved by fully optimizing the BMS setting, but retaining the traditional BMS format.

keywords:

Bonus-malus system , Ratemaking , Double counting , Optimization JEL Classification: C3001 Introduction

The bonus-malus system (BMS), also called the merit rating system, or no-claim bonus system, is a widely used experience rating system in auto insurance. The system corrects a priori risk classification by reflecting the policyholder’s claim history a posteriori. In a typical auto insurance rating system, the rate is first determined by the observable characteristics of the policyholder a priori, and then adjusted under the BMS from the policyholder’s unobservable information embedded in the claim history. Bonus-malus (BM) is a very important rating factor. Lemaire, (1998) states that “if insurers are allowed to use only one rating variable, it should be some form of merit-rating,” and this is indeed true in practice.

The design and implementation of the BMS vary significantly across countries and insurers, involving from nonexistent to highly complex systems. Highly complex systems may achieve the goal of accurately predicting future claims but might increase the computational burden of insurers and make their communication with policyholders and regulators difficult. They may also challenge the effectiveness of supervision and increase consumer complaints. This study suggests that the BMS might enable a simple presentation to insurance consumers and still be as accurate as a very complex system by resolving the so-called double-counting problem of the traditional systems.

A traditional Asian-European auto insurance BMS (the traditional BMS hereafter) consists of finite discrete risk levels, rules for transition between the levels, and BM relativity assigned to each level. Policyholders can navigate between the risk levels by following the transition rules based solely on their claim history. A single BM relativity or scale assigned to each level determines the magnitude of the bonus (discount) or malus (penalty). This BM relativity revises the rate based on a priori risk classification (see Lemaire and Zi, (1994) for numerous examples).

This simple yet effective system is found to have a challenging double-counting problem due to a technical bias in the traditional BMS from the a priori characteristics such as age and gender affecting both the a priori and a posteriori risk classifications. For example, a young male driver is first penalized by the age and gender factors due to the high probability of having claims, and then again penalized from the realized claim records and the BMS. This critical problem was first raised by Taylor, (1997) in their seminal paper, and then well presented by Brouhns et al., (2003); Pitrebois et al., (2003); Lemaire et al., (2015). In an attempt to resolve the double-counting problem, Pitrebois et al., (2003) proposed a fair system, where each a priori class has its own BMS (individualized BMS hereafter), through a simple example, and Brouhns et al., (2003) suggested a computer-intensive individualized BMS method incorporating the interactions between the a priori and a posteriori mechanisms.

Since the 1990s, several countries have deregulated their BMS, moving away from a strict national system in which all insurers use the same levels, transition rules, and BM relativities. European and Asian insurers began to use intermediate or total freedom systems, designing their own systems that diverged significantly from the traditional systems (Lemaire,, 1998). Considering the effectiveness and significance of the BMS for auto insurance rates, deregulation of the BMS can be viewed as promoting price competition among insurers. In addition, deregulation of the BMS enables insurers to utilize more complex systems, such as those suggested by Brouhns et al., (2003); Pitrebois et al., (2003), and thus resolve the double-counting problem affecting actuarial equity.

However, this also indicates the transition from simple to more complex and opaque systems. Most insurers do not have a clear transition rule or relativities as seen in simple national systems. Therefore, in countries with a total freedom system, the only way for consumers to know the impact of new claim(s) on their insurance rates is from the quotes of insurers after the claim(s) are settled. Some regulators and consumers have found the lack of transparency in the BMS affecting consumer protection, with increased complexity making the supervision of rates a challenging task. For example, the New York Insurance Law section 2334 states that it ”shall continue to encourage competition among insurers, but shall discourage merit rating plan provisions which may tend to create confusion or misunderstanding among insureds. Section 2334 further requires insurers to clearly present the surcharge due to claim history in the declarations page or premium bill for transparency. The European Consumer Organization BEUC asks all insurers to mandate the BMS, requiring them to present their BM policies in a standardized template in order to increase policy transparency and comparability. Furthermore, in spite of the double-counting problem, several Asian countries still follow the national system in the traditional BMS format, possibly for socio-economic or practical reasons.

This paper presents a simple BMS system that reduces the double-counting problem and yet maintains its simple traditional format. We propose a new optimization process to set the a priori rate and a BM relativity attached to each BM level after revisiting the classical BMS considered in (Taylor,, 1997; Pitrebois et al.,, 2003; Lemaire et al.,, 2015; Tan et al.,, 2015). Thus, we have a new premium that can be considered appropriate for the classical BMS model, but with modified numerical values for the a priori rate and BM relativities. The main difference of the proposed premium is that the a priori rate contributes to the optimization process as well as BM relativities. In the classical premium, only BM relativities contribute to the optimization process, and the a priori rate is set to a fixed value based on a statistical estimation procedure. The new premium’s immediate result is better prediction of future premiums compared to the classical premium. Surprisingly, we find that the new premium hardly faces the double-counting problem. We explain that the double-counting problem in the classical premium arises from inefficiency in the optimization process, where the a priori rate is not allowed to participate in the optimization process.

The remainder of this paper is organized as follows. Section 2 reviews the frequency random effects model and the classical BMS. Section 3 investigates the double-counting problem in the classical BMS. Specifically, we formally define the double-counting problem mathematically and propose an index to quantify the problem. In Section 4, we propose a new premium under the full optimization process. We also explain the double-counting problem in the classical BMS as mainly due to the constrained a priori rate, which we allow to participate in the new optimization process in this study. Using a real data analysis in Section 5, we show that the double-counting problem in the classical premium can be resolved by adjusting the a priori rate and BM relativities.

2 Review of the Classical BMS

2.1 Definition and Notations

We consider the policyholders’ portfolio in the short-term insurance context, where the policyholders can decide whether or not to renew their policy at the end of each policy year, and insurers can adjust their premium at the beginning of each policy year based on the policyholders’ claim history. We denote , , , and as the sets of natural numbers, non-negative integers, real numbers, and positive real numbers, respectively. We define to indicate the -th policyholder’s number of claims in the -th policy year. The actuarial science literature often refers to as the insurance claim frequency. Furthermore, we define the -th policyholder’s claim history at the end of year as

Let be the a priori risk characteristics of the -th policyholder observable at the time of contract, and be the residual effect, or the policyholder’s characteristics not included in the a priori risk classification. In the BMS context, we distinguish between the a priori and a posteriori risk classification. The a priori rate function is based solely on the policyholders’ a priori risk characteristics, without considering their claim history , and the a posteriori risk classification is related to the policyholders’ residual effect based on their claim history .

Following the classical settings in the BMS, we assume constant a priori risk characteristics and residual effects, making it convenient to analyze the stationary frequency distribution. Thus, for and , we do not have the subscript . To model the insurance claim frequencies, we use the generalized linear model (GLM) format applied to Poisson distribution. Nonetheless, this paper’s arguments can apply to any counting distribution, including the Poisson and negative binomial distributions as well as the distributions for excess zeros, such as the zero-inflated or hurdle models (McCullagh and Nelder,, 1989; Yip and Yau,, 2005; De Jong and Heller,, 2008).

2.2 Frequency Random Effects Model

This section presents the general frequency modeling framework. Assume that defines the a priori risk characteristics of the -th risk class, and is the weight of the corresponding risk class; that is,

| (1) |

Denote as the a priori rate for the -th policyholder, determined by the a priori risk characteristics based on equation

| (2) |

where is the link functions and is the vector of parameters to be estimated. The residual effect , assumed to be independent of the a priori risk characteristics , has the distribution :

| (3) |

where denotes the continuous marginal distribution function for . We use to denote the density function corresponding to . Further, for identification purposes, we assume that

| (4) |

Now, we are ready to present the frequency random effect model, which is assumed throughout the study unless specified otherwise.

Frequency Random Effect Model. Consider the a priori risk characteristics described in (1) and (2), and the residual effect in (3) and (4). We assume that the a priori risk characteristics and the residual effect are independent. Assuming the a priori risk characteristics and residual effect , we construct the frequency model for using the count regression model

| (5) |

where the non-negative integer distribution function has the mean parameter of with . Clearly, the regression model in (5) can be similarly written as

for the random variable independent of and satisfying .

The mean of for the given claim history up to time , denoted by , is the Bayesian premium in an insurance setting. The formal mathematical definition of the Bayesian premium is

| (6) | ||||

where the Bayesian estimator of the residual effect, , can be interpreted as the residual effect estimator for the given a priori rate and claim history up to time . Thus, we can say that the Bayesian premium is unbiased in that

| (7) |

Similarly, we can say that the Bayesian estimator of the residual effect is unbiased if the estimator mean conditioned on the a priori risk characteristics is 1:

| (8) |

For brevity and clarity, we omit the subscript in the remaining part of the study.

2.3 BMS and Optimal Relativity

In the classical BMS, the transition rule is common, where one BM level is lowered for a claim-free year and BM levels are increased for a claim. We assume the transition rule in the remainder of this study unless specified otherwise.111Note that our assumption of the transition rule is only for expository convenience, with the main idea of this study valid for the general transition as long as it is based on the Markovian claim history. From this transition rule, the BM level for each policyholder would evolve in a Markov chain. Especially, we use as a random variable representing the BM level (from to ) for a randomly chosen policyholder in the stationary state. The stationary distribution of BM level is determined as

where is the stationary distribution for the policyholder, with frequency expected in level . The relativity associated with this BM level is denoted as , and is called BM relativity. Under this BMS, the premium denoted as is a function of the a priori rate and BM level . Throughout this study, we present various types of premium .

From among the various types of BMSs, we review the classical BMS, where all the policyholders share the same BM relativity table

| (9) |

and the premium is determined as

where is the a priori rate function determined from the policyholder’s a priori risk characteristics . This BMS, in which all the policyholders share the relativity table in (9), is called the BMS with shared BM relativity table. Because of its simplicity, the BMS with shared BM relativity table is a common experience ratemaking system in auto insurance. We formally describe this BMS as follows.

Bonus-Malus System 1 (BMS with shared BM relativity table).

Consider the BMS where the policyholder’s premium at the BM level and a priori rate is given as

| (10) |

This BMS is with shared BM relativities.

The canonical choice of the a priori rate function in the BMS with shared BM relativity table in the literature (Norberg,, 1976; Denuit et al.,, 2007; Lemaire,, 2012; Tan et al.,, 2015) is

or equivalently

| (11) |

The (optimal) BM relativity is determined from the various optimization settings. For the various optimal BM relativity versions, we refer to Norberg, (1976); Pitrebois et al., (2003); Tan et al., (2015). From among the various optimization settings, we prefer the premium minimizing the objective function

| (12) |

as in Tan et al., (2015), since one of the main tasks of the BMS is to estimate the predictive mean of . We formally present this in Criteria 1. For the given premium , the mean square error in (12) is the hypothetical mean square error (HMSE), denoted by

Criteria 1.

Under Criteria 1, Tan et al., (2015) obtain the optimal BM relativity

| (13) |

where the right-hand side (RHS) of the non-negative function is optimized, to obtain the solution

Now, we can provide the specific premium method classified in the BMS with shared BM relativity table. The premiums are commonly utilized in the BMS literature.

Premium from Partial Optimization of Shared BM Relativity Table (PPOS). From among the various type of premiums in the BMS with shared BM relativity table, we consider the premium at the BM level with the a priori rate , given as

where the a priori rate function is determined before optimization, as in (11), while the BM relativity function is determined after optimization, as in (13). This premium is the PPOS, in that only the BM relativity table is optimized while the a priori rate function is predetermined.

The PPOS is the same as the premium in Tan et al., (2015). The premiums in the classical BMS (Norberg,, 1976; Pitrebois et al.,, 2003) can be regarded as the PPOS with some variation in specification of the optimization process. Therefore, without loss of generality, the PPOS can be considered as the premium under the classical BMS. As a base premium method, we can conveniently utilize the following premium with no a posteriori risk classification (PNO).

Premium with No a Posteriori Risk Classification (PNO). Consider the policyholder’s premium at the BM level with the a priori rate given as

where the a priori and a posteriori rate functions are given as

respectively. This premium is the PNO. Note that the PNO can be classified as the BMS with shared BM relativity table, where the BM relativity function is given by the constant function of .

From the definition of PPOS, compared to PNO, the PPOS provides a better prediction in that

| (14) |

3 Double-Counting Problem in the BMS with Shared BM Relativities

From our investigation, the most common premium type in the classical BMS literature is that from the BMS with shared relativity table, especially with the a priori rate function determined as

While such premiums are convenient and easy to understand, they are unfair in that the policyholders with bad/good a priori risk characteristics pay more/less than the actual premium.

This unfairness in tariff is due to the double-counting problem, and is studied in the literature in various contexts (Taylor,, 1997; Lemaire et al.,, 2015; Tan et al.,, 2015). As briefly discussed in Pitrebois et al., (2003), the double-counting problem can be solved with the BMS with individualized BM relativity table, where policyholders have their own BM relativity table depending on their a priori risk characteristics. However, the BMSs with individualized BM relativity table are not widely accepted in practice, mainly because the insurer does not want to complicate the BMS.

Motivated from the literature, we provide the formal mathematical definition of the double-counting problem in this section, and propose an index that can detect the unfairness of a given BMS. In other words, we present the double-counting problem index. With these mathematical tools, we can confirm that the BMS with individualized BM relativity tables can fully solve the double-counting problem.

3.1 Double-Counting Problem

First, we define the unbiasedness of experience ratemaking in the BMS. As with the case of in (6), the unbiasedness of premium in the BMS is defined as follows.

Definition 1.

Under the BMS with the transition rule, the premium is unbiased if it satisfies

| (15) |

Otherwise, the premium is biased.

Now, we explain the double-counting problem in the classical BMS, that is, the PPOS. First, recall that the PPOS satisfies

Hence, the unbiased condition in (15) is equivalent to

| (16) |

We can show that (16) is not true for the PPOS. Consider two policyholders and with the a priori rates and , respectively, where . While their residual effects and are unknown, the -th policyholder tends to have a higher mean frequency than the mean frequency of the -th policyholder on average. Thus, the -th policyholder on average shows higher BM levels than the -th policyholder. Consequently, the policyholder with higher a priori rate tends to have a higher BM relativity on average,

| (17) |

The equivalence between (15) and (16) implies bias in the premium. Moreover, Especially, (17) indicates that the a priori risk characteristics affect the a posteriori as well as the a priori risk classifications. The dual role of the a priori risk characteristics resulting in biased premiums is the double-counting problem.

In general, the unbiasedness in (15) can be written as

| (18) |

where

are called pure relativity and pure priori rate, respectively. Hence, (18) is a condition for the unbiasedness of pure relativity. Concerning the PPOS and PNO, we obtain the pure relativity as

Now, from this pure relativity, we can formally define the double-counting problem as follows.

Definition 2.

The premium suffers from the double-counting problem if pure relativity has the following order:

We next provide a numerical example of the double-counting problem.

Example 1.

For the frequency random effects model, consider the specific distribution

with

and

where represents a gamma distribution with mean of and dispersion parameter . Here, further to our real data analysis in Section 5, we set , , , and .

Now, we consider a PPOS under the BMS with the transition rule and BM levels. The distribution of and the corresponding BM relativity are given in Table 3. We thus obtain the conditional expectations for pure relativity as follows:

which in turn indicates the double-counting problem

Furthermore, this bias in BM relativities leads to that in the premium:

3.2 Measure for Double-Counting Problem

Recall that an unbiased premium can be characterized by unbiasedness in pure relativity, as in (18). However, if the premium suffers from double-counting problem, the conditional expectation of pure premium

| (19) |

would be an (increasing) function of by definition. If the other conditions are identical, we would prefer the premium with smaller bias in (19), which is equivalent to having the smaller variance of pure relativity conditional expectation

| (20) |

Because is decomposed into the summation of two components

we propose the normalized version of (20)

| (21) |

as the fairness index (FIX) of the premium . For the definition of (21), we consider only the FIX of the nontrivial premium satisfying

For premium , the FIX satisfies the inequality

Note that no double-counting problem implies that . In contrast, implies the presence of a perfect double-counting problem, meaning that the a posteriori risk classification of the premium is determined purely by the a priori rate . Given that the other factors are equal, the BMS with a small value of would be preferred.

As for the PPOS , the FIX defined in (20) can be simplified as follows, for a more intuitive interpretation:

| (22) |

The FIX in (22) can be compared to the fairness measure defined in Tan et al., (2015). For a specific comparison, see Remark 3 in the appendix. The FIX calculation procedure is given in Lemma 5 in the appendix.

Example 2 (Continued from Example 1).

As regards the PPOS, we are mainly interested in the degree of double counting under various a priori rate distributions, and in how such double counting affects the quality of prediction under BMS.

In addition to the settings in Example 1, we once again numerically study the various a priori rate distributions as summarized in Table 1. Compared to our base Scenario I, where the a priori rate distributions are the same as in Example 1, Scenario II shows a smaller a priori rate variance with the same mean, whereas Scenario III shows a larger a priori rate mean with the same variance. The Scenario IV a priori rates are left-skewed. All scenarios have distinct coefficient of variation (CV) values.

| mean | variance | CV | |||||

|---|---|---|---|---|---|---|---|

| Scenario I | 0.1 | 0.5 | 0.9 | 0.5 | 0.16 | 0.80 | |

| Scenario II | 0.4 | 0.5 | 0.6 | 0.5 | 0.01 | 0.20 | |

| Scenario III | 0.6 | 1.0 | 1.4 | 1.0 | 0.16 | 0.40 | |

| Scenario IV | 0.1 | 0.2 | 1.2 | 0.5 | 0.37 | 1.22 |

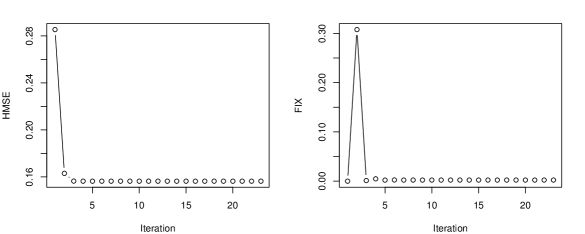

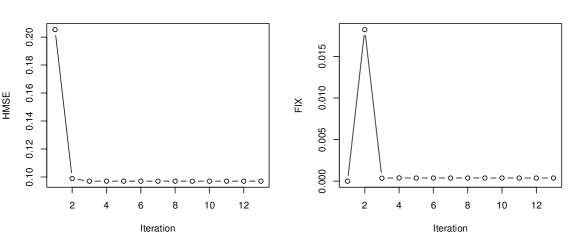

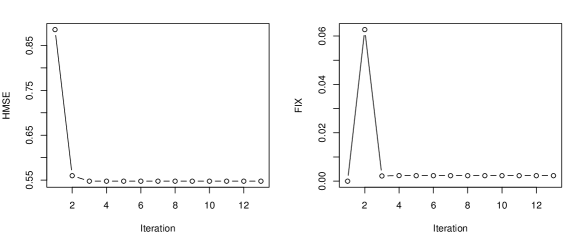

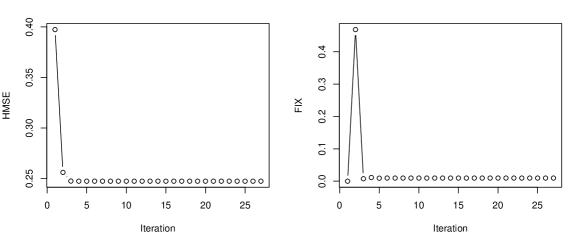

The degree of double counting and quality of prediction are based on the FIX and HMSE for each scenario, as in Table 2. The distribution of is presented for a reference. As in Taylor, (1997), we find the set of the a priori rate with larger CV increasing the double-counting problem.

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | FIX | HMSE | FIX | HMSE | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Scenario I | 0.414 | 0.048 | 0.059 | 0.030 | 0.032 | 0.029 | 0.036 | 0.049 | 0.087 | 0.217 | 0.308 | 0.163 | 0 | 0.285 | |

| Scenario II | 0.303 | 0.050 | 0.064 | 0.039 | 0.043 | 0.041 | 0.051 | 0.068 | 0.112 | 0.230 | 0.018 | 0.099 | 0 | 0.205 | |

| Scenario III | 0.170 | 0.031 | 0.040 | 0.026 | 0.030 | 0.032 | 0.043 | 0.066 | 0.133 | 0.427 | 0.063 | 0.560 | 0 | 0.885 | |

| Scenario IV | 0.492 | 0.053 | 0.063 | 0.029 | 0.029 | 0.024 | 0.027 | 0.035 | 0.062 | 0.187 | 0.469 | 0.256 | 0 | 0.397 | |

Unlike the PPOS, the PNO under any BMS is unbiased and free of the double-counting problem since the equation shows that

this can be confirmed with the FIX of zero. We know that the introduction of the a posteriori risk classification can improve the PNO’s prediction ability; for an example, see the PPOS in (14). However, the introduction of the a posteriori risk classification can lead to the double-counting problem in PPOS. In summary, the PPOS outperforms the PNO in terms of prediction power at the cost of double counting. The last two columns in Table 2 provide the FIX and HMSE for the PNO under the same settings in Example 2. A comparison of the FIX and HMSE in the PPOS and PNO in Table 2 confirms our findings.

Remark 1.

In Section 2.2, we argue that the Bayesian premium in (6) and the Bayesian estimator of the residual effect are unbiased owing to (7) and (8). This implies that the experience ratemaking based on Bayesian estimation is free of the double-counting problem. The following corollary confirms this with the FIX.

Corollary 1.

The Bayesian premium satisfies

Proof.

We prove this corollary as follows:

where the last equality is from the independence assumption and (4). ∎

Remark 2.

So far, we considered the premiums in the classical BMS literature as having nonzero FIX, and the Bayesian premium as having zero FIX. While both the premiums have the same a priori rate, the former suffers from double counting, but the latter does not, because of the a priori risk characteristics in their a posteriori risk ratemaking function. To be more specific, the premiums in the classical BMS literature are directly exposed to double counting because they use the same BM relativity table for all the policyholders; that is, the policyholders’ BM levels are determined by their claim histories, which are inevitably influenced by their a priori risk characteristics. Therefore, a zero FIX is attainable only when the a posteriori risk classification does not depend solely on the policyholders’ claim history. That is, the a posteriori risk classification should also use the policyholders’ individual risk characteristics to remove its own influence due to their claim history, which is the key to zero FIX of the Bayesian premium. In other words, the individualized a posteriori risk classification is critical to prevent the double-counting problem. In this regard, Pitrebois et al., (2003) proposed the use of several BM relativity tables to reduce the double-counting problem.

In the following subsection, we investigate the double-counting problem of the BMS with several BM relativity tables based on the a priori risk characteristics.

3.3 Double-Counting Problem and the BMS with Individualized BM Relativity Table

Using numerical examples, Pitrebois et al., (2003) show that the introduction of several BM relativity tables based on a few a priori risk characteristics can reduce the double-counting problem. In this subsection, we formally present the BMS in which all policyholders have their own BM relativity tables according to their a priori risk characteristics, and show that such a BMS does not suffer from the double-counting problem at all. First, we start with the specification of such a BMS.

Bonus-Malus System 2 (BMS with Individualized BM Relativity Table).

Consider the BMS with the following properties:

-

1.

A Priori Rate: A policyholder with the a priori risk characteristics given the a priori rate

at the time of contract.

-

2.

Relativity Table: All policyholders have their own individualized BM relativity tables depending on their a priori risk characteristics

(23) -

3.

Premium: The premium of a policyholder at the BM level with the a priori risk characteristics obtained by multiplying the a priori rate with the relativity

Now, under the BMS with individualized BM relativity table, we explain how to obtain the individualized BM relativities in (23) for all the risk characteristics . The aim is again to minimize the mean square error in Criteria 1. As in the previous section, for the sake of brevity, we choose the a priori rate function

Then, for each risk group , we choose the BM relativity in (23) as the solution to the optimization problem

| (24) |

where the RHS of (24) is optimized with the non-negative functions. For convenience, we also define

| (25) |

Premium from Optimizing the Individualized BM Relativity Table (POI). From among the various types of premiums in the BMS with individualized BM relativity table, consider the policyholder’s premium at the BM level with the a priori rate given in (25). This premium will be called the premium from optimization of individualized BM relativity table (POI).

Theorem 1.

Proof.

First, we obtain (26) from the derivative of

with respect to . Furthermore, the RHS of (26) can be calculated from the expression

where the first equation is just a rearrangement of the conditional distribution, and the last equation is obtained from the definition of the stationary distribution of .

∎

Recall that the double-counting problem arises from the shared BM relativity table, which does not consider the a priori risk characteristics as a double-counting problem. In fact, the observation

indicates removal of the bias. Here, the second inequality is from the unbiasedness of relativity

where the third equality is from the assumption of independence between and . Furthermore, the following calculation of FIX confirms our claim:

where the last equality also comes from the independence between and .

In this subsection, we show that the double counting in the BMS can be removed with the individualized BM relativity table. However, the individual system is too complex to be presented to consumers. Therefore, we discuss how to address the double-counting problem of the BMS using the shared BM relativity table in the traditional BMS format.

4 Full Optimization and Double Counting

In terms of Criteria 1, the premiums of the BMS with shared BM relativity table allow for utilizing the a priori rate function as well as the BM relativity function in the optimization process. For convenience, we predetermine the a priori rate function in PPOS as

before the optimization of in (13). However, in terms of optimization, the a priori rate function need not be predetermined for the optimization process, and can achieve a better optimization result by allowing for the a priori rate function to participate in the optimization process. In this section, we show how to utilize the a priori rate function as well as the BM relativity function for optimization with the BMS with shared BM relativity table, and study how such inclusion affects the double-counting problem.

4.1 Premium from Full Optimization of Shared BM Relativity Table

This subsection considers the premium of the BMS with shared BM relativity table, allowing for the a priori rate function to participate in the optimization process. From Criteria 1, the objective function in (12) can be further minimized by allowing for the a priori rate function to contribute to the optimization process as well as the BM relativity function . Specifically, we try to solve the optimization problem

| (27) |

where and are optimized from among the non-negative functions. Clearly, the solution of (27) is not unique. For example, if is the solution to (27), will also be the solution to (27) for any . To address this trivial difficulty, we provide the constrained version of (27) as follows:

| (28) |

for some predetermined constant , where is a floor function. For the pair of the solution of (28), we define the premium as

| (29) |

Note that the constraint in (28) is actually not a constraint in terms of optimization efficiency, and one can easily show that the two optimization problems of (27) and (28) result in the same efficiency,

| (30) |

for any with . Next, we formally define the premium obtained from full optimization of the shared BM relativity table.

Premium obtained from full optimization of shared BM relativity table (PFOS). From among the various types of premiums of the BMS with shared BM relativity table, we consider the policyholder’s premium at the BM level with the a priori rate as given in (29). This is the PFOS, meaning that both the BM relativity and a priori rate function are determined by optimizing the BMS with shared relativity table.

Clearly, the PFOS is still a premium obtained from the BMS with shared BM relativity table since its risk classification includes the following:

-

1.

The a priori classification given by , determined by the a priori risk characteristics.

-

2.

The a posteriori classification function given by , determined at the BM level .

While (28) cannot be analytically solved in general, it can be calculated with Algorithm 1 given in the appendix, where the coordinate descent algorithm is presented. A detailed discussion of the algorithm is presented in the appendix.

In fact, the PFOS can also be interpreted as the premium in the BMS with individualized BM relativities:

| (31) | ||||

where the a priori rate function is given as and the BM relativity table for the policyholder with the a priori rate is given by

Note that this individualized BM relativity can be interpreted as pure relativity, for which we can conveniently provide the following notation:

| (32) |

The optimization of (28) resembles the optimization of the POI since it can be equivalently written as

| (33) |

where the RHS of the equality is optimized among the functions with form , which can be written as

| (34) |

for some positive functions and satisfying

| (35) |

for some predetermined constant . Thus, the optimization of (33) is similar to that of (28), where the BM relativity function has a further restriction: it is optimized among the functions in (34).222Note that (35) is really not a restriction, but is introduced to avoid trivial non-unique solutions. In this context, we can obtain the following result:

Lemma 1.

The optimized value has the following relation.

Proof.

In summary, we can view the PFOS as a premium with individualized BM relativity table having restrictions on the BM relativity function, as in (34). Because the POI can perfectly solve the double-counting problem, we expect the PFOS to partially solve the double-counting problem. This solution will depend on how the BM relativity function in the POI is similar to that of the PFOS, or how the multiplicative assumption in (34) deviates from the BM relativity function in the POI. The following numerical experiments compare the performance of the PFOS with that of the PPOS and POI in terms of the double counting as well as prediction power.

Example 3 (Continued from Example 1).

Under the same setting of Example 1, we consider the various premiums for the PNO, PPOS, PFOS, and PIO. In order to calculate the a priori rate function and BM relativities in the PFOS, we set the restriction as

in (28) for a unique solution to the full optimization problem. Table 3 presents the distributions of and the BM relativities, and Table 4 presents the a priori rate function for each scenario. To compare the fairness and performance of the premium, we provide the conditional expectation of relativity given the a priori rate, FIX, and HMSE as shown in Table 5.

We first observe that the PPOS shows the worst performance in terms of both the FIX and HMSE. Obviously, the PPOS suffers from the double-penalty problem, as in Example 1 and the conditional mean of the BM relativity in Table 5. It seems that the poor HMSE of PPOS is due to the double-penalty problem. Moreover, Table 5 also shows that the PFOS has improved over the PPOS in terms of both HMSE and FIX. The improvement in HMSE can be expected from Lemma 1, although we find a rather unexpected dramatic improvement in FIX. For further comparison of the PPOS and PFOS, we match the relativity and the a priori rate pairs of two BMSs, and . While the two relativities and show no much difference, the major differences between the two BMSs are in the a priori rates. Specifically, the PFOS is biased in that the conditional expectation of the relativities deviate from 1:

| (36) |

which is very similar to the case of PPOS,

However, the bias in the a priori rates of PFOS compensates for the bias in (36),

and almost resolves the double-penalty problem, as the following conditional expectation of each premium shows:

Next, we compare the performance of the PFOS and POI. For a fair comparison, we match the pure relativity and the a priori rate function pairs of two BMSs: and . While the a priori rate is the same for both the BMSs in terms of representation, pure relativity shows a considerable difference between the two BMSs; this is the only factor affecting the difference in HMSE between the two BMSs. Despite the clear difference in relativity, the two BMSs do not show much difference in FIX, which can be explained by the hardly biased conditional pure relativity means of the PFOS:

Finally, we interpret the FIX and HMSE columns in Table 5. The FIX column shows the sequential changes in of four BMSs, normalized by maximum FIX, in the order

the HMSE is similarly defined. We examine the difference from the PNO to PPOS. While the HMSE of PPOS shows a significant improvement over that of PNO, the PPOS creates the double-penalty problem with a FIX of 0.3075. We also find significant improvement in the double-counting problem from the PPOS to PFOS, where the FIX is , and minor improvement in HMSE, where the HMSE is , and minor improvement in both the FIX and HMSE from the PFOS to PPOS.

| Risk | Level | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| group | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

| 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | ||

| 0.240 | 0.364 | 0.390 | 0.489 | 0.544 | 0.647 | 0.752 | 0.913 | 1.160 | 1.675 | ||

| 0.224 | 0.357 | 0.382 | 0.488 | 0.544 | 0.651 | 0.759 | 0.926 | 1.183 | 1.722 | ||

| low | 0.724 | 1.156 | 1.237 | 1.579 | 1.761 | 2.108 | 2.458 | 2.998 | 3.830 | 5.576 | |

| mid | 0.266 | 0.425 | 0.455 | 0.580 | 0.647 | 0.774 | 0.903 | 1.102 | 1.407 | 2.049 | |

| high | 0.208 | 0.333 | 0.356 | 0.454 | 0.507 | 0.606 | 0.707 | 0.863 | 1.102 | 1.604 | |

| low | 0.763 | 1.330 | 1.397 | 1.888 | 2.041 | 2.457 | 2.694 | 3.059 | 3.361 | 3.725 | |

| mid | 0.296 | 0.475 | 0.511 | 0.658 | 0.737 | 0.884 | 1.024 | 1.228 | 1.505 | 1.957 | |

| high | 0.180 | 0.286 | 0.309 | 0.398 | 0.451 | 0.547 | 0.651 | 0.813 | 1.072 | 1.626 | |

| 0.414 | 0.048 | 0.059 | 0.030 | 0.032 | 0.029 | 0.036 | 0.049 | 0.087 | 0.217 | ||

| Risk group | |||

|---|---|---|---|

| low | mid | high | |

| 0.10 | 0.50 | 0.90 | |

| 0.10 | 0.50 | 0.90 | |

| 0.32 | 0.59 | 0.84 | |

| 0.10 | 0.50 | 0.90 | |

| 0.10 | 0.50 | 0.90 | |

| Method | FIX | FIX | HMSE | HMSE | |||||

|---|---|---|---|---|---|---|---|---|---|

| Shared.No | 1 | 1 | 1 | 0 | - | 0.2853 | - | ||

| Shared.P | 0.304 | 0.805 | 1.069 | 0.3075 | 100 | 0.1629 | -42.9 | ||

| Shared.F | 0.291 | 0.814 | 1.089 | 0.0022 | -99.3 | 0.1563 | -2.3 | ||

| Shared.F* | 0.943 | 0.969 | 1.015 | 0.0022 | - | 0.1563 | - | ||

| Ind | 1 | 1 | 1 | 0 | -0.7 | 0.1553 | -0.4 |

In the following subsection, we heuristically explain how the PFOS can fully resolve the double-counting problem and provide numerical evidence supporting our heuristic.

4.2 Double-Counting Problem and Full Optimization

In the previous subsection, we showed that the PFOS can improve the HMSE to some extent; this can be expected because the PFOS optimizes the HMSE over the a posteriori as well as a priori rate functions, unlike the PPOS, where the a priori rate is predetermined. Following the same logic, we argue that the PFOS can improve the double-counting problem to some extent, depending on how the multiplicative assumption in (34) deviates from the BM relativity function in the BMS with the individualized BM relativity table. However, we cannot expect the PFOS to fully resolve the double-counting problem as shown in Example 3. This subsection explains that we can expect surprising success of the PFOS compared to the PPOS in resolving the double-counting problem, and that the key reason for the success is that the PFOS enables the a posteriori risk classification of the BMS with a shared BM relativity table to be involved with a priori risk characteristics.

First, recall that Remark 2 in Section 3.2 explains the double-counting problem in the PPOS as follows:

While the policyholder’s a posteriori rate in the PPOS is a function of claim histories only, this does not mean that the a posteriori rate in the PPOS is not affected by the a priori rate. Actually, the policyholder’s a posteriori rate is essentially affected by the a priori rate, because the claim histories are affected by the a priori rate. Because the claim histories are affected by the a priori rate, the a priori rate has to be used in the a posteriori risk classification to remove the a priori rate effect on the a posteriori risk classification process. This is how the POI and the Bayesian premium resolve the double-counting problem.

However, the BMS with a shared BM relativity table does not allow for the a posteriori risk classification to be a function of the a priori rate, since it is a function of the policyholder’s BM level only. The remedy is to tune the predetermined a priori rate function instead. The PFOS allows for freely choosing the a priori rate function, but the newly chosen a priori rate function is in fact really the multiplication of the predetermined a priori rate and the correction for the a posteriori rate function, as shown in (32). Thus, in the alternative representation of the PFOS in (32), the PFOS was also interpreted as the BMS with individualized BM relativity table and restriction in (34) on BM relativity. While the previous section showed that we expect only limited improvement in the double-counting problem depending on how the multiplicative restriction in (34) deviates from the BM relativity function in the POI, the inclusion of the a priori rate in the a posteriori risk classification plays the crucial rule of removing the a priori rate from the policyholder’s BM level in the a posteriori risk classification process and resolving the double-penalty problem. In fact, the following lemma explains that by merely allowing the a priori rate to participate in determining the a posteriori risk classification, we can fully resolve the double-penalty problem in the BMS with a shared BM relativity table, regardless of the BM relativity table given.

Lemma 2.

For any given positive BM relativities

consider the premium in (10) with the choice of the a priori rate function given by

| (37) |

Then, we have

| (38) |

and

Now, through a numerical experiment, we can confirm that the main causes of double-counting problem in the BMS is the predetermined a priori premium and does not allow for correcting its unfair a posteriori premium. The double-counting problem can be significantly improved by just allowing for the a priori rate function to affect the optimization process.

Example 4 (Continued from Example 1).

We consider a numerical study with the premium obtained from full optimization. As shown in Algorithm 1 in the appendix, the premium is obtained from full optimization by applying the coordinate descent algorithm, where the BM relativity and the a priori rate function are iteratively updated. Specifically, we begin with the case of no a posteriori risk classification,

| (39) |

which is then iteratively updated in the order

until the termination condition is satisfied. For convenience, we name each relativity pair and the a priori rate in sequential order; for example, we name

as the first pair, and

as the second pair. Note that the first pair corresponds to the relativity and the a priori rate of PNO as shown in (39), and the second pair corresponds to the relativity and the a priori rate of PPOS

which is implied by Lemma 4 in the appendix.

In the numerical study, we calculate the HMSE and FIX for each iterated pair, to find the updated step that most significantly contributed to the HMSE or FIX. The results are presented in Table 6 and Figure 1, where all the scenarios seem to share similar patterns in the increase and decrease of HMSE and FIX. The first pair has the largest HMSE but no double penalty with zero FIX. While the second pair accomplished a major reduction in HMSE, it created the double-penalty problem with a large FIX. However, the third pair accomplished a major reduction in FIX and some reduction in HMSE. After the third pair, both the HMSE and FIX seem stabilize. An important implication of this numerical study is that the major improvement in terms of double penalty comes from the first participation of the a priori rate in the optimization problem.

| Relativity ftn | ||||||||

|---|---|---|---|---|---|---|---|---|

| Priori ftn | ||||||||

| Scenario I | FIX | 0.0000 | 0.3075 | 0.0013 | 0.0047 | 0.0021 | 0.0022 | |

| HMSE | 0.2853 | 0.1629 | 0.1564 | 0.1563 | 0.1563 | 0.1563 | ||

| Scenario II | FIX | 0.0000 | 0.0182 | 0.0004 | 0.0004 | 0.0004 | 0.0004 | |

| HMSE | 0.2053 | 0.0988 | 0.0970 | 0.0970 | 0.0970 | 0.0970 | ||

| Scenario III | FIX | 0.0000 | 0.0626 | 0.0021 | 0.0023 | 0.0023 | 0.0023 | |

| HMSE | 0.8853 | 0.5598 | 0.5476 | 0.5476 | 0.5476 | 0.5476 | ||

| Scenario IV | FIX | 0.0000 | 0.4686 | 0.0075 | 0.0113 | 0.0093 | 0.0096 | |

| HMSE | 0.3973 | 0.2560 | 0.2474 | 0.2473 | 0.2473 | 0.2473 |

5 Real Data Analysis

To examine to what extent the double-counting problem can be resolved with the proposed full optimization process in an actual BMS, we use a collision coverage dataset for new and old vehicles from the Wisconsin Local Government Property Insurance Fund (LGPIF) in Frees et al., (2016). Collision coverage provides for coverage for impact of a vehicle with an object, impact of a vehicle with an attached vehicle, or overturn of a vehicle. In our analysis, we use the longitudinal data over the policy years 2006 to 2010 for a total of 497 governmental entities. We have two categorical variables, the entity type with six levels and coverage at three levels, as shown in Table 10 (similar to Table C.6 in Oh et al. (2019)).

Specifically, for the frequency random effect model, we consider

where is a vector of the two categorical variables in Table 10 for the -th risk group, and is the corresponding parameters. For the random effect, we assume a gamma distribution with the mean of 1 and dispersion parameter , that is, .

5.1 Estimation Result

Table 7 summarizes the estimation results of the frequency random effect model. Note that the asterisk * indicates that the parameters are significant at the 0.05. The results are quite intuitive. For example, the county entity type is expected to incur more accidents than any other entity type with the same amount of coverage. The risk group with higher coverage amount tends to incur more accidents for the same entity type.

From the estimates in Table 7, we find that Table 8 presents the results of various relativities under the -1/+2 transition rule; that is, the shared relativity table from partial optimization , shared relativity table from full optimization , pure relativity table from full optimization , and individualized relativity table . In our data analysis, we set 18 different risk class groups by combining two categorical variables, the entity type and coverage group, so that the BMS with individualized BM relativity (shared.F∗ and Ind) has 18 different BM relativity tables for the 18 risk class groups. To compare the premiums under various methods, we report the FIX and HMSE as measuring the double-counting problem and quality of predictor, respectively. The a priori rate functions are summarized in Table 9. Note that the a priori rate functions and are given by the estimated a priori rate obtained from the fixed effect estimates in Table 7.

From Table 8, we observe the impact of using the proposed optimization process on the BM premium. We can provide explanations similar to those in Example 3. The PFOS seems to mitigate the double-counting problem up to a level similar to the individualized BMS level with a much smaller FIX than that from the PPOS, and a bit smaller HMSE value, suggesting that the proposed optimization process leads to a slight increase in prediction power.

| parameter | estimate | std.error | p-value | |

|---|---|---|---|---|

| Fixed effect | ||||

| (Intercept) | -3.219 | 0.402 | .0001 | * |

| TypeCity | 0.921 | 0.424 | 0.0298 | * |

| TypeCounty | 2.066 | 0.420 | .0001 | * |

| TypeSchool | 0.748 | 0.392 | 0.0565 | |

| TypeTown | -1.194 | 0.470 | 0.0111 | * |

| TypeVillage | 0.229 | 0.409 | 0.5760 | |

| catCoverage2 | 1.439 | 0.206 | .0001 | * |

| catCoverage3 | 2.344 | 0.224 | .0001 | * |

| Random effect | ||||

| 0.782 | ||||

| Risk | Level | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| group | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | FIX | HMSE | ||

| 0.16 | 0.22 | 0.23 | 0.27 | 0.29 | 0.32 | 0.36 | 0.43 | 0.55 | 1.23 | 0.511 | 0.871 | |||

| 0.13 | 0.20 | 0.22 | 0.26 | 0.29 | 0.33 | 0.37 | 0.43 | 0.56 | 1.23 | 0.017 | 0.844 | |||

| 1 | 0.95 | 1.47 | 1.55 | 1.89 | 2.05 | 2.35 | 2.64 | 3.11 | 4.00 | 8.87 | 0.017 | 0.844 | ||

| 2 | 0.48 | 0.74 | 0.78 | 0.96 | 1.04 | 1.19 | 1.34 | 1.57 | 2.02 | 4.49 | ||||

| 3 | 0.26 | 0.40 | 0.42 | 0.51 | 0.56 | 0.64 | 0.72 | 0.84 | 1.08 | 2.40 | ||||

| 4 | 0.72 | 1.10 | 1.16 | 1.42 | 1.54 | 1.77 | 1.99 | 2.34 | 3.01 | 6.68 | ||||

| 5 | 0.26 | 0.39 | 0.42 | 0.51 | 0.55 | 0.63 | 0.71 | 0.83 | 1.07 | 2.38 | ||||

| 6 | 0.17 | 0.26 | 0.28 | 0.34 | 0.37 | 0.42 | 0.48 | 0.56 | 0.72 | 1.60 | ||||

| 7 | 0.31 | 0.47 | 0.49 | 0.60 | 0.66 | 0.75 | 0.85 | 0.99 | 1.28 | 2.84 | ||||

| 8 | 0.16 | 0.24 | 0.26 | 0.31 | 0.34 | 0.39 | 0.44 | 0.52 | 0.67 | 1.48 | ||||

| 9 | 0.13 | 0.20 | 0.21 | 0.25 | 0.28 | 0.32 | 0.36 | 0.42 | 0.54 | 1.20 | ||||

| 10 | 0.79 | 1.22 | 1.29 | 1.57 | 1.71 | 1.96 | 2.20 | 2.59 | 3.33 | 7.39 | ||||

| 11 | 0.28 | 0.43 | 0.46 | 0.56 | 0.61 | 0.70 | 0.78 | 0.92 | 1.19 | 2.63 | ||||

| 12 | 0.18 | 0.28 | 0.30 | 0.36 | 0.39 | 0.45 | 0.51 | 0.59 | 0.76 | 1.70 | ||||

| 13 | 0.99 | 1.52 | 1.60 | 1.96 | 2.13 | 2.44 | 2.74 | 3.22 | 4.14 | 9.19 | ||||

| 14 | 0.93 | 1.43 | 1.51 | 1.84 | 2.00 | 2.29 | 2.57 | 3.03 | 3.89 | 8.64 | ||||

| 15 | 0.61 | 0.93 | 0.99 | 1.20 | 1.31 | 1.50 | 1.69 | 1.98 | 2.55 | 5.66 | ||||

| 16 | 0.93 | 1.43 | 1.51 | 1.84 | 2.00 | 2.29 | 2.58 | 3.03 | 3.90 | 8.66 | ||||

| 17 | 0.40 | 0.62 | 0.65 | 0.80 | 0.87 | 0.99 | 1.12 | 1.32 | 1.69 | 3.76 | ||||

| 18 | 0.23 | 0.35 | 0.37 | 0.45 | 0.49 | 0.56 | 0.63 | 0.75 | 0.96 | 2.13 | ||||

| 1 | 0.92 | 1.65 | 1.69 | 2.39 | 2.52 | 3.16 | 3.40 | 3.96 | 4.29 | 4.80 | 0.000 | 0.834 | ||

| 2 | 0.62 | 1.03 | 1.09 | 1.44 | 1.57 | 1.86 | 2.07 | 2.35 | 2.63 | 2.97 | ||||

| 3 | 0.35 | 0.55 | 0.59 | 0.76 | 0.85 | 1.02 | 1.17 | 1.38 | 1.66 | 2.07 | ||||

| 4 | 0.77 | 1.32 | 1.39 | 1.87 | 2.02 | 2.43 | 2.67 | 3.03 | 3.32 | 3.68 | ||||

| 5 | 0.34 | 0.55 | 0.59 | 0.75 | 0.84 | 1.00 | 1.15 | 1.37 | 1.64 | 2.06 | ||||

| 6 | 0.16 | 0.25 | 0.27 | 0.35 | 0.40 | 0.48 | 0.58 | 0.73 | 0.98 | 1.55 | ||||

| 7 | 0.42 | 0.68 | 0.73 | 0.94 | 1.05 | 1.24 | 1.41 | 1.64 | 1.92 | 2.30 | ||||

| 8 | 0.13 | 0.20 | 0.22 | 0.28 | 0.32 | 0.39 | 0.47 | 0.60 | 0.84 | 1.45 | ||||

| 9 | 0.05 | 0.09 | 0.09 | 0.12 | 0.14 | 0.17 | 0.21 | 0.28 | 0.43 | 1.21 | ||||

| 10 | 0.81 | 1.41 | 1.47 | 2.01 | 2.16 | 2.61 | 2.86 | 3.25 | 3.55 | 3.93 | ||||

| 11 | 0.39 | 0.62 | 0.67 | 0.86 | 0.96 | 1.14 | 1.30 | 1.52 | 1.80 | 2.19 | ||||

| 12 | 0.19 | 0.29 | 0.32 | 0.41 | 0.46 | 0.56 | 0.66 | 0.83 | 1.08 | 1.62 | ||||

| 13 | 0.98 | 1.75 | 1.77 | 2.54 | 2.59 | 3.34 | 3.45 | 4.17 | 4.33 | 5.02 | ||||

| 14 | 0.89 | 1.59 | 1.65 | 2.30 | 2.44 | 3.03 | 3.28 | 3.79 | 4.12 | 4.58 | ||||

| 15 | 0.71 | 1.20 | 1.27 | 1.68 | 1.83 | 2.18 | 2.40 | 2.73 | 3.01 | 3.36 | ||||

| 16 | 0.90 | 1.60 | 1.65 | 2.31 | 2.45 | 3.04 | 3.29 | 3.80 | 4.13 | 4.59 | ||||

| 17 | 0.55 | 0.90 | 0.96 | 1.25 | 1.37 | 1.62 | 1.81 | 2.08 | 2.35 | 2.70 | ||||

| 18 | 0.29 | 0.46 | 0.49 | 0.64 | 0.71 | 0.85 | 0.99 | 1.19 | 1.46 | 1.91 | ||||

| 0.534 | 0.044 | 0.052 | 0.023 | 0.024 | 0.020 | 0.024 | 0.031 | 0.055 | 0.191 | |||||

| Risk group | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.04 | 0.17 | 0.42 | 0.10 | 0.42 | 1.05 | 0.32 | 1.33 | 3.29 | 0.08 | 0.36 | 0.88 | 0.01 | 0.05 | 0.13 | 0.05 | 0.21 | 0.52 | |

| 0.29 | 0.61 | 0.81 | 0.54 | 0.82 | 1.35 | 0.72 | 1.59 | 3.18 | 0.50 | 0.76 | 1.21 | 0.09 | 0.36 | 0.58 | 0.35 | 0.64 | 0.90 | |

| 0.04 | 0.17 | 0.42 | 0.10 | 0.42 | 1.05 | 0.32 | 1.33 | 3.29 | 0.08 | 0.36 | 0.88 | 0.01 | 0.05 | 0.13 | 0.05 | 0.21 | 0.52 |

6 Conclusion

In this study, we revisit the double-counting problem in the BMS. We find that the problem originated from the inefficiency in optimization, with only the a posteriori function contributing. While the double-counting problem can be fully resolved by allowing individualized BM relativity tables for each policyholder, which we call the POI, such a BMS is complicated and unsuitable for effective communication between the policyholders and insurers. By allowing for both the a priori and a posteriori rate functions to participate in the optimization process, which we call the PFOS, we show that the double-counting problem can be virtually resolved without complicating the traditional BMS. In our analysis, we found no significant difference between the PFOS and POI in terms of double counting (via FIX) or prediction ability (via HMSE). A future study may find it interesting to compare the PFOS and POI under various circumstances and identify the conditions under which two BMS show significantly different patterns both in terms of double counting and prediction ability.

Acknowledgements

Jae Youn Ahn was supported by a National Research Foundation of Korea (NRF) grant funded by the Korean Government (NRF-2017R1D1A1B03032318). Rosy Oh was supported by Basic Science Research Program through the National Research Foundation of Korea(NRF) funded by the Ministry of Education (Grant No. 2019R1A6A1A11051177).

References

- Brouhns et al., (2003) Brouhns, N., Guillén, M., Denuit, M., and Pinquet, J. (2003). Bonus-malus scales in segmented tariffs with stochastic migration between segments. Journal of Risk and Insurance, 70(4):577–599.

- De Jong and Heller, (2008) De Jong, P. and Heller, G. Z. (2008). Generalized linear models for insurance data. Cambridge University Press.

- Denuit et al., (2007) Denuit, M., Maréchal, X., Pitrebois, S., and Walhin, J.-F. (2007). Actuarial modelling of claim counts: Risk classification, credibility and bonus-malus systems. John Wiley & Sons.

- Frees et al., (2016) Frees, E. W., Lee, G., and Yang, L. (2016). Multivariate frequency-severity regression models in insurance. Risks, 4(1):4.

- Lemaire, (1998) Lemaire, J. (1998). Bonus-malus systems: The european and asian approach to merit-rating. North American Actuarial Journal, 2(1):26–38.

- Lemaire, (2012) Lemaire, J. (2012). Bonus-malus systems in automobile insurance, volume 19. Springer science & business media.

- Lemaire et al., (2015) Lemaire, J., Park, S. C., and Wang, K. C. (2015). The impact of covariates on a bonus–malus system: an application of taylor’s model. European Actuarial Journal, 5(1):1–10.

- Lemaire and Zi, (1994) Lemaire, J. and Zi, H. (1994). A comparative analysis of 30 bonus-malus systems. ASTIN Bulletin: The Journal of the IAA, 24(2):287–309.

- Luo and Tseng, (1992) Luo, Z.-Q. and Tseng, P. (1992). On the convergence of the coordinate descent method for convex differentiable minimization. Journal of Optimization Theory and Applications, 72(1):7–35.

- McCullagh and Nelder, (1989) McCullagh, P. and Nelder, J. A. (1989). Generalized Linear Models, second ed. Chapman and Hall, London.

- Norberg, (1976) Norberg, R. (1976). A credibility theory for automobile bonus systems. Scandinavian Actuarial Journal, 1976(2):92–107.

- Pitrebois et al., (2003) Pitrebois, S., Denuit, M., and Walhin, J.-F. (2003). Setting a bonus-malus scale in the presence of other rating factors: Taylor’s work revisited. ASTIN Bulletin: The Journal of the IAA, 33(2):419–436.

- Tan et al., (2015) Tan, C. I., Li, J., Li, J. S.-H., and Balasooriya, U. (2015). Optimal relativities and transition rules of a bonus–malus system. Insurance: Mathematics and Economics, 61:255–263.

- Taylor, (1997) Taylor, G. (1997). Setting a bonus-malus scale in the presence of other rating factors. ASTIN Bulletin: The Journal of the IAA, 27(2):319–327.

- Yip and Yau, (2005) Yip, K. C. and Yau, K. K. (2005). On modeling claim frequency data in general insurance with extra zeros. Insurance: Mathematics and Economics, 36(2):153–163.

Appendix A Optimization Algorithm

From the optimization perspective, the two problems in (27) and (28) are equivalent, as shown in (30). Specifically, the problem in (28) can be obtained by solving the problem of (27) by finding a constant satisfying

in this case, the problem in (28) is obtained as

Thus, for the optimization of (28), we need to solve (27). In the following algorithm, we adopt the coordinate descent algorithm, where the BM relativity and a priori rate functions are iteratively optimized.

Algorithm 1.

Under the BMS with shared BM relativity table, we can solve (28) through iterative calculation using the following coordinate descent algorithm:

-

i.

Initial step:

-

(a)

-

(b)

Define functions and as

and

respectively.

-

(a)

-

ii.

Repeat step:

-

(a)

For the given , define

(40) and for the given , define

(41) -

(b)

-

(a)

-

iii.

Termination and normalization

-

(a)

Repeat step ii until the termination test is satisfied.

-

(b)

Calculate the normalizing constant such that .

- (c)

-

(a)

The iterative updates of Step ii in Algorithm 1 come from Lemma 3, with the specific updating formula given in Lemma 4.

Lemma 3.

Algorithm 1 gives the following auxiliary results.

Proof.

The proof of part i is similar to deriving the optimal BM relativity of the premium through partial optimization of the shared BM relativity table. Finally, the optimization problem in part ii can be written as

which in turn implies that

is the solution of the optimization problem of part ii. ∎

Lemma 4.

In step ii of Algorithm 1, the updates in the coordinate algorithm can be calculated as follows.

Proof.

The proof of the first part follows from

where is the density function of at , conditional on . The proof of the second part can be similarly obtained. ∎

Since a convex and differentiable function is guaranteed to converge to the global minimizer, Lemma 3 guarantees the solution in Algorithm 1 to converge to the global solution for the objective function

which can be easily shown as a convex function and is differentiable for each coordinate. Refer to Luo and Tseng, (1992) for more details of convergence in the coordinate descent algorithm.

Appendix B Miscellaneous Results

Lemma 5.

For the premium of the BMS, we have the following results:

-

i.

.

-

ii.

.

-

iii.

.

-

iv.

.

Proof.

We omit the proof for this since the results are self-explanatory. ∎

Remark 3.

The FIX in (22) can be compared to the fairness measure defined in Tan et al., (2015). Specifically, Tan et al., (2015) defined the fairness measure as a variation in the conditional expectation of the a priori rate as follows:

| (42) |

Note that while the measure in (42) can be used to measure the fairness of the BMS in general, it cannot distinguish between two BMSs having distinct BM relativity tables. Since we are interested in the comparison of the BMSs with various BM relativity tables, the fairness measure in (42) is not suitable for our purpose.

Appendix C Table

| Categorical | Description | Proportions | ||

|---|---|---|---|---|

| variables | ||||

| Entity type | Type of local government entity | |||

| Miscellaneous | 5.03 | |||

| City | 9.66 | |||

| County | 11.47 | |||

| School | 36.42 | |||

| Town | 16.90 | |||

| Village | 20.52 | |||

| Coverage | Collision coverage amount for old and new vehicles. | |||

| Coverage | 33.40 | |||

| Coverage | 33.20 | |||

| Coverage | 33.40 | |||