Stochastic Linear Complementarity Problems on Extended Second Order Cones

S. Z. Németh

School of Mathematics, The University of Birmingham

The Watson Building, Edgbaston

Birmingham B15 2TT, United Kingdom

email: s.nemeth@bham.ac.uk

L. Xiao

School of Mathematics, The University of Birmingham

The Watson Building, Edgbaston

Birmingham B15 2TT, United Kingdom

email: Lxx490@bham.ac.uk

Abstract

In this paper, we study the stochastic linear complementarity problems on

extended second order cones (stochastic ESOCLCP). We first convert the

problem to a stochastic mixed complementarity problem on the nonegative

orthant (SMixCP). Enlightened by the idea of Chen and Lin(2011), we

introduce the Conditional Value-at-risk (CVaR) method to measure the loss

of complementarity in the stochastic case. A CVaR - based minimisation

problem is introduced to achieve a solution which is ”good enough” for

the complementarity requirement of the original SMixCP. Smoothing function

and sample average approximation methods are introduced and the the

problem is converted to a form which can be solved by Levenberg-Marquardt

smoothing SAA algorithm. At the end of the paper a numerical example

illustrates our results.

1 Introduction

Uncertainty is a common and realistic problem that results from inaccurate measurement or stochastic variation of data such as price, capacities, loads, etc. In fact, the inaccuracy or uncertainty of these real-world data are inevitable. When these data are applied as parameters in mathematical models, the constraints of models may be violated because of their stochastic characters. These violations may finally cause some difficulties in the sense that the optimal solutions obtained from the stochastic data are no longer optimal, or even infeasible. Amongst approaches proposed for modeling uncertain quantities, the stochastic models outstand because of their solid mathematical foundations, theoretical richness, and sound techniques of using real data. Complementarity problems imbedded with stochastic models occur in many areas such as finance, telecommunication and engineering. Hence, considering with uncertainty will be meaningful for practical treatments. If partial or all of the coefficients in the are uncertain, the will be turned into a stochastic linear complementarity problem (), which is firstly introduced by Chen and Fukushima [1]. Articles about can be found in [2, 3, 4, 5].

Even though the fact that only limited number of results have been obtained on the stochastic complementarity problems, there are still some meaningful results. One of them is the CVaR (conditional value-at-risk, which is also called expected shortfall) minimisation reformulation of stochastic complementarity problem [6]. In this study, the stochastic linear complementarity problem on extended second order cones (S-ESOCLCP) will be introduced. Based on the results in [7], a method of finding solutions to S-ESOCLCP will be elaborated, and a numerical example will be presented.

2 Preliminaries

For , the Euclidian space whose elements are column vectors, the definition of an inner product is given by

Let , be positive integers. The inner product of pairs of vectors , where and , is given by

Let be a Euclidian space. A set is called a convex cone if for any , and , we have

In other words, a convex cone is a set which is invariant with respect to the multiplication of vectors with positive scalars. The dual cone of a convex cone is

which is also a convex cone. A convex cone is called pointed if , or equivalently, if does not contain straight lines through the origin. A convex cone which is a closed set is called a closed convex cone. Any pointed closed convex cone with nonempty interior will be called proper cone. The cone is called subdual if , superdual if , and self-dual if .

Definition 2.1.

An indicator function

is defined as

Definition 2.2(Complementarity Set).

Let be a nonempty closed convex cone and its dual[8]. The set

is called the complementarity set of .

Denote by the corresponding Euclidean norm. Recall the definitions of the mutually dual extended second order cone [9] and in :

(1)

(2)

where . If there is no ambiguity about the dimensions, then we simply denote and by

and , respectively. The following proposition is from [7]. We restate it here for convenience.

Proposition 2.1.

Let and .

(i)

if and only if .

(ii)

if and only if and .

(iii)

if and only if and .

(iv)

if and only if there exists such that ,

and .

The linear complementarity problem defined by a convex cone and a linear function is given by

(3)

where , , .

3 The problem formulation

Let be a probability space defined by:

1.

, the sample set of possible outcomes;

2.

, a -algebra generated by (or a collection of all subsets of ); and

3.

, a function maps from events to probabilities.

The stochastic linear complementarity problem defined by a convex cone and a linear function is given by

(4)

where , is an -dimensional random vector. The notation “a.s.” is the abbreviation of “alomst surely”, which means

In this study, we assume that the coefficients and are measurable functions of with the following property:

where represents the expected value of the random vector in the square bracket.

It should be noted that if the possible outcome set contains only one single realisation (and this unique outcome definitely happens), problem (4) will degenerate to (3).

The stochastic linear complementarity problems are very useful in solving practical problems. However, because of the existence of the random vector in the function , it is very difficult and sometimes impossible of finding a solution to satisfy almost all possible outcomes of . One plausible idea to improve the viability of finding a solution to SLCP is to associate the problems with probability models, and then persuasive solutions to SLCP are obtainable by finding the solutions to the associated probability models.

Xu and Yu [6] summarised 6 different probability models for finding solutions to SLCP:

(i)

Expected value (EV) method, introduced by Gürkan et. al in [3]. By using the expectation value to replace the stochastic term , this method ultimately reformulates (4) to (3).

(ii)

Expected residual minimisation (ERM) method, introduced by Chen and Fukushima [1]. This method minimises the expectation of the square norm of the residual defined by the following C-function:

(5)

where is a multi dimensional C-function defined as

where can be any scalar C-function satisfying:

(iii)

Stochastic mathematical programs with equilibrium constraints (SMPEC) reformulation, introduced by Lin and Fukushima[4, 10, 11]. This method highlights a recourse variate to compensate the violation of complementarity in (4) for some outcomes of , then it reformulates (4) to the following model:

(6)

where . Ambiguous solutions to SCP can be obtained by minimising the objective function in (6), i.e. the expected value of the compensation to the violation of complementarity in (4).

(iv)

Stochastic programming (SP) reformation [12]. Problem (4) is reformulated to the following:

where , and is the Hadamard product of and .

(v)

Robust Optimisation [13, 14], which is a deterministic reformation of (4). And,

(vi)

CVaR minimisation (CM) reformulation [5]. By using this method, (4) is reformulated to a problem that minimises the CVaR of the norm of the loss function , namely:

The reformulation in item (vi) uses the CVaR, a measure of risk widely applied in financial industry. CVaR was built based on Value at risk (VaR)[15, 16]. Let be a vector with random outcomes and let be a mapping, the VaR of for the loss function is defined as:

(7)

where is the probability of the event in the square bracket. We call the loss function. The probability (also called confidence level) quantifies the proportion of “worst cases” (that is, ) in the group of all outcomes, and the other outcomes () would happens with probability .

Based on the definition of VaR, CVaR is defined as:

(8)

(9)

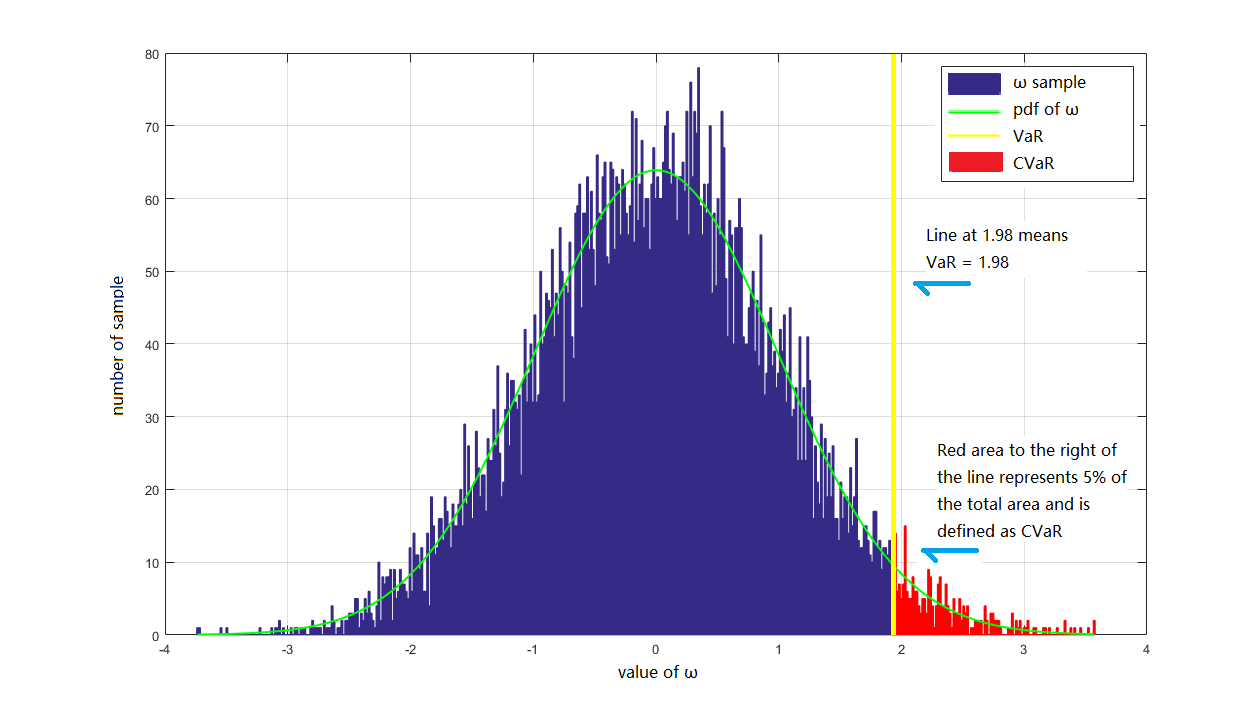

is the conditional expectation of all outcomes with . For better understanding the concept of VaR and CVaR, figure 1 gives a sample of a loss function with one-dimensional normally distributed random value . This figure shows that when the confidence level is set at , the value of VaR equals to the horizontal coordinate of the red vertical line, and the value of CVaR with confidence level equals the red area to the right of the line.

For a stochastic event with , the distribution of this event shows that only of the outcomes are above 1.98. If the confidence level is set at , then the value of VaR equals 1.98(horizontal axis marked by yellow line), and the value of CVaR equals the integral of the area marked in red color.

Figure 1: VaR and CVaR for , where

Proposition 3.1.

A risk measure has the following properties:

1.

Positive homogeneity: for all and ,

2.

Monotonicity: if for all , we have , and

3.

Sub-additivity: for all .

Proposition 3.2.

The risk measure VaR is

1.

Positive homogeneous, and

2.

Monotonic.

Proof.

1.

By the definition of VaR, we have:

2.

Suppose for all . We have

therefore

∎

We mark that VaR is not sub-additive (counter example is shown in [17]).

The positive homogeneity and monotonicity of CVaR can be easily proved by combining the Proposition 3.2 and the definition (9). To prove the Sub-additivity define . By definition (8), we have

∎

Consider defined by the function and the extended second order cone , problem (4) becomes:

where , with ,

, and ; , with , , for .

We use Corollary 3.1 to reformulate the SLCP to the stochastic mixed complementarity problem (SMixCP). Given the functions , , and a cone , the SMixCP is defined as:

Corollary 3.1.

Suppose , . We have

such that

where

and

(10)

Proof.

Suppose that . Then, , where and . Let , Then, by item (iv)

of Proposition 2.1 we have that such that

(11)

(12)

(13)

where . From equation (11) we obtain , which by equation (12) implies

, which after some algebra gives

Corollary 3.1 provides an alternative way to find the solutions to the , by converting it to the . Such conversion enables us to study through a C-function.

The scalar form of Fischer-Burmeister (FB) C-function [19, 20] is defined as:

The FB-based equation formulation of is:

(15)

where is the scalar FB C-function stated in Chapter 2. It should be mentioned that the FB C-function is convex, but non-smooth on . According to the definition of FB C-function, a point is a solution to the stochastic mixed complementarity problem , if and only if

(16)

The associated merit function of is:

(17)

Based on (15) and (17), the merit function can be written as:

By the definition of merit function, a point is a solution to the stochastic mixed complementarity problem , if

Proposition 3.4.

The associated merit function is continuously differentiable on , if and are continuously differentiable on and , respectively.

Proof.

First we prove that is continuously differentiable. We note that is continuously differentiable at every . It is easy to verify that is continuously differentiable at every . Consider the following to limits at point :

and

where , . Both partial derivatives of at are continuous, is continuously differentiable. Hence, is continuously differentiable on if and only if and are continuously differentiable on and , respectively.

∎

Since the function is not convex on , it is easy to verify that the merit function is not convex on the feasible region. We focus on finding the stationary point of the merit function (15). A point is a stationary point to the stochastic mixed complementarity problem , if:

(18)

That is

(19)

where

is a nonsingular matrix. Combining equation (19) with equation (16) implies that equation (18) is a necessary condition for to be a solution to .

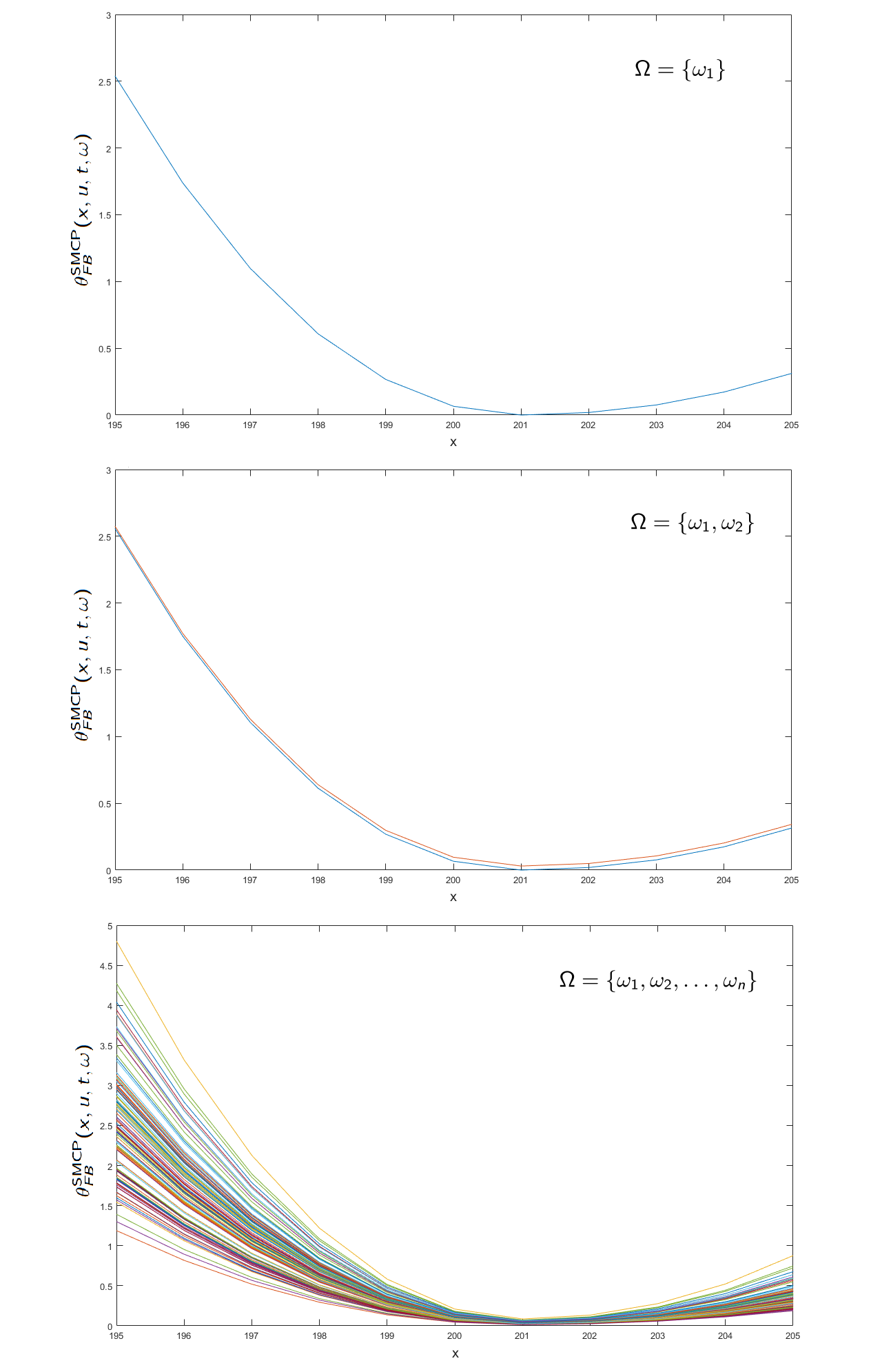

The feasible set of shrinks as (i.e., the size of the possible outcome set ) increases. When , we cannot generally find a solution to such that system (18) holds almost surely for any , because there will be a large number of equations in system (18). Figure 2 shows the situation when the size of .

As it is introduced above, probability models provide appropriate deterministic reformulations of the stochastic complementarity problems. It can be associated with the stochastic complementarity problems to find persuasive solutions. These persuasive solutions to stochastic complementarity problems would make a proper trade-off between the satisfaction of infinite complementarity constraints and solvability of the problems.

For a possible outcome set , when the size of equals 1, i.e. (figure 1), we can easily find a solution to the problem by using the merit function. When increases to 2 (figure 2), the solution for the first case is not longer suitable for both outcomes. As the size of increases (figure 3), it become almost impossible to find a solution to the problem which is suitable for all outcomes.

Figure 2: The minimum point of merit function varies as increases

Since , given a confidence level , a point is a plausible solution to if it is a solution to

(20)

This is a relaxation of problem (18). A small value of means that it prefers the satisfaction of the complementarity constraints rather than the solvability of the problem. Note that the problem (20) can be written as:

(21)

where the indicator function is neither convex nor continuously differentiable at the point . Even though the function is convex and continuously differentiable, the objective function (21) is non-smooth. If we use the indicator function in the objective function, difficulties occur when applying algorithms which are only viable for smooth objective functions. Addressing this concern, the CVaR method will be considered, which undertakes convex and continuously differentiable objective functions. It harmonises the incompatibility between the satisfaction of infinite number of complementarity constraints and solvability of the problems, as well as inherits convexity and continuous differentiability from the merit function . In the CVaR method, will be used as the “loss function” to measure the “loss” of complementarity. It should be noted that, the higher the value of the “loss function”, the more complementarity constraints of this stochastic complementarity problem are lost. We transform (20) into CVaR based objective function and then construct the stochastic programming model in the following context.

Rewritting (21) as Value-at-Risk (VaR) to measure of the loss of complementarity:

VaR is a measure of complementarity loss defined in (7). However, the disadvantages of using VaR as the measure of complementarity loss is significant: VaR is not consistent, because it is neither convex nor smooth [21]. On the other hand, CVaR (defined in (9)) has superior mathematical properties than VaR, as it inherits continuous differentiability and convexity from the merit function. Moreover, CVaR is a more conservative measure of complementarity loss than VaR.

Theorem 3.1.

If is continuously differentiable on , then for any , the measure of complementarity loss is continuously differentiable on .

Proof.

Immediate from the continuous differentiability of and (9).

∎

Theorem 3.2.

If is convex on , then for any , the measure of complementarity loss is convex on .

Proof.

Suppose that is convex on . Let , . Then we have

where . By the sub-additivity and homogeneity of CVaR, we have

Hence, is convex in .

∎

Definition 3.1.

Suppose , are two risk measures. Risk measure is said to be more conservative than risk measure if

for all and .

Proposition 3.5.

For the problem , is a more conservative measure of complementarity loss than .

Reformulate the problem to the following CVaR based minimisation problem:

(22)

where

and

It means that a solution to should minimise the “loss” of complementarity from stochasticity.

Let

and define

Lemma 3.1.

The problem (22) is equivalent to the following problem:

(23)

where is the optimal value satisfying:

Proof.

Immediate from the alternative definition of CVaR [22]:

∎

Problem (23) is simplified from (22) because it does not contain integration, and inherits convexity from the merit function . However, since the presence of the operator , the objective function in problem (23) is not smooth at the point 0. Using mathematical techniques to smooth the objective function will be more convenient and applicable than directly using semi-smooth algorithm to find the numerical solution. Four palmary smoothing functions summarised by Chen and Harker [23] are provided as follows:

The mathematical expectation is another difficulty that needs to be carefully treated. In many instances, the mathematical expectation cannot be calculated with accuracy. A common treatment is using the Sample Average Approximation (SAA) method, which is based on the Law of large numbers. SAA method provides a persuasive result of measuring an expectation value [3, 24]. If the distribution of the random vector is known, then the Monte-Carlo approach can be used to generate a sample independently and identically distributed (i.i.d.) with the distribution of . Let be an i.i.d. sample set. The SAA method estimates the mathematical expectation using averaged value of all observations . That is,

Since the objective function is continuously differentiable, Problem (24) can be solved by finding some solutions to

(28)

4 An algorithm

In the previous section, we have modified the to the problem (24) with a convex and continuously differentiable objective function. Furthermore, the solution to the can be obtained by finding some solutions to equation (28). In this section, an algorithm will be developed to solve (28). This algorithm contains Monte-Carlo approach to generate i.i.d. random vector sample sets. We denote . Given the tolerance , the stopping criterion is:

(29)

for . It is shown as follows:

Algorithm 3 (Line search smoothing SAA):

Input: initial point , , confidence level , LM parameter , the smoothing parameter , maximum iteration number for , for , the sequence of sample set sizes , parameters of the approximation , , the tolerance , , and parameters for Wolfe conditions , .

Step 1: Set .

Step 2: Set the sample size , and generate i.i.d samples .

Step 3: If , and , Stop.

Step 4: Set , and .

Step 5: If either (29) or , then set , , and go to Step 3.

Step 6: Denote , and find a direction such that

(30)

If the system (30) is not solvable or if the condition

is not satisfied, (re)set .

Step 7: Find step length such that

and

Step 8: Set and , go to Step 5.

Comment: This algorithm requires the Monte-Carlo approach to generate i.i.d. random vector samples. If the values of , are large, the algorithm is anticipated to be more accurate, but it will sacrifice time and computing power. On the other hand, if the value of ’s are small, the costs of finding result is decreased, but the accuracy of the solution is sacrificed.

5 A numerical example

This section illustrates a numerical example for the stochastic ESOCLCP. Denote by an extended second order cone in . Let and be two real vectors. Denote

A stochastic ESOCLCP defined by the extended second order cone and a stochastic linear function is:

where

with , , and ; and

with , . is a stochastic vector with i.i.d. random variables for all . Again it is easy to verify that square matrices T, A and D are nonsingular for all , .

By using Corollary 3.1, we reformulate to the following defined by , , and :

where

and

We will convert this to the form of (24) and then (28). Given , we rewrite problem (24) as:

where

Since the distribution of the random vector is known, we use the Monte Carlo (MC) method to simulate sample sets with number of observation . The solutions are shown in the following table:

1

10

(1.537, 0.273, 1.060, 0.136, -0.262)

(0.784, 29.054, -0.194, -13.466, 25.803)

2

100

(1.542, 0.263, 1.058, 0.127, -0.253)

(1.093, 28.552, -0.214, -12.609, 25.544)

3

1000

(1.549, 0.257, 1.060, 0.122, -0.252)

(1.277, 28.397, -0.162, -12.418, 25.477)

4

10000

(1.548, 0.262, 1.060, 0.125, -0.254)

(1.215, 28.605, -0.204, -12.701, 25.578)

5

100000

(1.546, 0.261, 1.059, 0.125, -0.254)

(1.186, 28.587, -0.176, -12.643, 25.516)

6

1000000

(1.546, 0.261, 1.059, 0.124, -0.254)

(1.200, 28.566, -0.177, -12.617, 25.514)

Run time(s)

Average loss of complementarity

Value of threshold

1

10

0.090439

0.347

0.063

2

100

0.696431

0.893

0.095

3

1000

5.202383

1.179

0.090

4

10000

39.39705

1.060

0.087

5

100000

553.4596

1.054

0.088

6

1000000

4759.294

1.073

0.089

Note: The first table shows the solution of and the value of the function with respect to different value of . The value of solution does not variate significantly, while the value of the function differs but converges to around 1.200 as the value of increase. The second table shows the Run time(s), average loss of complementarity, and the value of threshold. The run time increases significantly as the value increases. On the other hand, the average loss of complementarity and the value of threshold remains relative constant no matter what change to the value of .

Table 1: The result of numerical example

The average loss of complementarity (ALoC) is calculated by:

As it is shown in the table above, by the cost of increased run time, the dispersion of solution reduced as the number of iteration increases. However, increasing the number of iteration does not decrease neither the value of the threshold nor the ALoC.

6 Conclusion and comments

In this paper, we studied the stochastic linear complementarity problems on extended second order cones (stochastic ESOCLCP) that are stochastic extensions of ESOCLCP included in our previous paper [nemeth2018linear]. We used Corollary 3.1, which states the equivalent conversion from a stochastic ESOCLCP to a stochastic mixed complementarity problem on nonegative orthant ().

Enlightened by the idea from [5], we introduce the CVaR method to measure the loss of complementarity in the stochastic case. The merit function (18) is not required to equal zero almost surely for all . Instead, a CVaR - based minimisation problem (22) is introduced to obtain a solution which is “good enough” for the complementarity requirement of the original SMixCP. For solving the CVaR - based minimisation problem derived from the original SMixCP, smoothing function and sample average approximation methods are introduced and finally converted to the form in (24). Finally, a line search smoothing SAA algorithm is provided for finding the solution to this CVaR-based minimisation problem and it is illustrated by a numerical example.

Stochastic methods on complementarity problems were pioneered by Chen and Fukushima [1], who introduced the idea of square norm of the

merit function which is still commonly used. However, this approach led to non-convexity and consequently increased the difficulty of solving ESOCLCP by algorithms. Our algorithm introduced in the previous section only guarantees finding a stationary point rather than a solution to the problem. We believe that the results in this paper will remain valid and further improved under strong convexity assumptions. This question will be a topic of future research.

References

[1]

X. Chen and M. Fukushima.

Expected residual minimization method for stochastic linear

complementarity problems.

Mathematics of Operations Research, 30(4):1022–1038, 2005.

[2]

H. Fang, X. Chen, and M. Fukushima.

Stochastic r_0 matrix linear complementarity problems.

SIAM Journal on Optimization, 18(2):482–506, 2007.

[3]

G. Gürkan, A. Yonca Özge, and S. M. Robinson.

Sample-path solution of stochastic variational inequalities.

Mathematical Programming, 84(2):313–333, 1999.

[4]

G. H. Lin.

Combined Monte Carlo sampling and penalty method for stochastic

nonlinear complementarity problems.

Mathematics of Computation, 78(267):1671–1686, 2009.

[5]

X. Chen and G. H. Lin.

CVaR-based formulation and approximation method for stochastic

variational inequalities.

Numerical Algebra, Control & Optimization, 1(1):35–48, 2011.

[6]

L. Xu and B. Yu.

CVaR-constrained stochastic programming reformulation for

stochastic nonlinear complementarity problems.

Computational Optimization and Applications, 58(2):483–501,

2014.

[7]

S. Z. Németh and L Xiao.

Linear complementarity problems on extended second order cones.

Journal of Optimization Theory and Applications,

176(2):269–288, 2018.

[8]

S. Karamardian.

Generalized complementarity problem.

J. Optimization Theory Appl., 8:161–168, 1971.

[9]

S. Z. Németh and G. Zhang.

Extended Lorentz cones and mixed complementarity problems.

J. Global Optim., 62(3):443–457, 2015.

[10]

G. H. Lin, X. Chen, and M. Fukushima.

Solving stochastic mathematical programs with equilibrium constraints

via approximation and smoothing implicit programming with penalization.

Mathematical Programming, 116(1-2):343–368, 2009.

[11]

S. Mataramvura and B. Øksendal.

Risk minimizing portfolios and HJBI equations for stochastic

differential games.

Stochastics An International Journal of Probability and

Stochastic Processes, 80(4):317–337, 2008.

[12]

M. Wang and MM. Ali.

Stochastic nonlinear complementarity problems: stochastic programming

reformulation and penalty-based approximation method.

Journal of optimization theory and applications,

144(3):597–614, 2010.

[13]

A. Ben-Tal and A. Nemirovski.

Robust optimization–methodology and applications.

Mathematical Programming, 92(3):453–480, 2002.

[14]

A. Ben-Tal, L. E. Ghaoui, and A. Nemirovski.

Robust optimization.

Princeton University Press, 2009.

[15]

R T. Rockafellar, S. Uryasev, et al.

Optimization of conditional value-at-risk.

Journal of risk, 2:21–42, 2000.

[16]

A. Meucci.

Risk and asset allocation.

Springer Science & Business Media, 2009.

[17]

J. Danielsson, B. N. Jorgensen, S. Mandira, G. Samorodnitsky, and C. G.

De Vries.

Subadditivity re-examined: the case for value-at-risk.

Technical report, Cornell University Operations Research and

Industrial Engineering, 2005.

[18]

C. Acerbi and D. Tasche.

On the coherence of expected shortfall.

Journal of Banking & Finance, 26(7):1487–1503, 2002.

[19]

A. Fischer.

A special Newton-type optimization method.

Optimization, 24(3-4):269–284, 1992.

[20]

A. Fischer.

A Newton-type method for positive-semidefinite linear

complementarity problems.

Journal of Optimization Theory and Applications,

86(3):585–608, 1995.

[21]

P. Artzner, F. Delbaen, J. M. Eber, and D. Heath.

Coherent measures of risk.

Mathematical finance, 9(3):203–228, 1999.

[22]

R. T. Rockafellar and S. Uryasev.

Conditional value-at-risk for general loss distributions.

Journal of banking & finance, 26(7):1443–1471, 2002.

[23]

B. Chen and P. T. Harker.

Smooth approximations to nonlinear complementarity problems.

SIAM Journal on Optimization, 7(2):403–420, 1997.

[24]

H. Jiang and H. Xu.

Stochastic approximation approaches to the stochastic variational

inequality problem.

IEEE Transactions on Automatic Control, 53(6):1462–1475, 2008.