Dept. of Mathematics, University of Washington

11email: djclancy@uw.edu

The Gorin-Shkolnikov identity and its random tree generalization

Abstract

In a recent pair of papers Gorin and Shkolnikov GS_paper and Hariya Hariya have shown that the area under normalized Brownian excursion minus one half the integral of the square of its total local time is a centered normal random variable with variance . Lamarre and Shkolnikov generalized this to Brownian bridges GLS_RBB , and ask for a combinatorial interpretation. We provide a combinatorial interpretation using random forests on vertices. In particular, we show that there is a process level generalization for a certain infinite forest model. We also show analogous results for a variety of other related models using stochastic calculus.

Keywords:

Brownian excursionContinuous state branching processes Lévy Process Lamperti Transform Galton-Watson branching processes Jeulin’s identity Continuum random trees.MSC:

60F17 60J55 60J801 Introduction

Let denote a standard Brownian excursion, or, equivalently, a 3-dimensional Bessel bridge from 0 to 0 of unit duration, see (RY, , Chapter XII). This process is a semi-martingale with quadratic variation , and so possesses a family of local times which satisfies almost surely the occupation time formula:

In this particular case, there exists a jointly continuous modification of for which the above formula holds almost surely.

Using topics in random matrix theory Gorin and Shkolnikov GS_paper obtained, as a corollary of one of their main results, the following interesting distributional identity:

| (1) |

Gorin and Shkolnikov were studying tri-diagonal matrices of the form

| (2) |

where are independent -distributed random variables which are indexed by their parameters and are independent standard normal random variables. The ordered eigenvalues, , of in (2) are of particular interest for their connection to -ensembles. The celebrated work of Dumitriu and Edelman DE_beta shows that joint distribution of the eigenvalues has a density proportional to

Ramírez, Rider and Virág RRV.11 relate a rescaling and recentering of largest eigenvalues, i.e. the edge, of to the eigenvalues of the so-called stochastic Airy operator. In particular they show for each fixed that

converge jointly in distribution as to eigenvalues of the operator

where is a white noise on . In turn, Gorin and Shkolnikov showed the powers of the matrix converge in a certain operator-theoretic sense to the semigroup generated by . See Theorem 2.1 in GS_paper for a proper formulation of this convergence.

Proposition 2.7 in GS_paper relates the eigenvalues of to the functional in (1) by

By comparing the Laplace transform in the right-hand side with the prior work of Okounkov Okounkov_Moduli when , Gorin and Shkolnikov were able to prove the equality in distribution (1).

Lamarre and Shkolnikov GLS_RBB connected a spiked version of the matrix model in GS_paper to a reflected Brownian bridge as well. If we let denote a reflected Brownian bridge and let denote its local time, then the work of GLS_RBB relates eigenvalues of a spiked operator to the random variable

| (3) |

Lamarre and Shkolnikov are able to give an explicit formulation of the moment generating function of only in the case , which evaluates to

This leads Lamarre and Shkolnikov “to believe that admits an interesting combinatorial interpretation.” This work is devoted to giving one such combinatorial interpretation using random trees or random forests which can be generalized to the infinite forest models of Aldous_AF ; Duquesne_CRTI . We should mention that there are many relationships between the area of a Brownian excursion and limits appearing in enumerative combinatorics. For a good survey on such connections, Janson’s survey Janson_ExcursionArea is an excellent resource.

Shortly after Gorin and Shkolnikov posted their work on the arXiv, Hariya Hariya gave a path-wise interpretation and proof of the normality result (1). Hariya’s proof relies heavily on the Jeulin identity Jeulin_Iden . Define

and let denote its right-continuous inverse. Jeulin’s identity is the following identity in distribution

Lamarre and Shkolnikov GLS_RBB use Hariya’s idea and some results of Pitman Pitman_SDE to show

| (4) |

For more information on this time-change including its proof, see Jeulin’s original work (Jeulin_Iden, , pg. 264) or a random tree interpretation and generalization in AMP_Jeulin ; M_SST ; Pitman_SDE . The paper AMP_Jeulin conveys this transformation succinctly: The Jeulin identity “can be roughly interpreted as the width of the layer of the tree containing [a] vertex […] where the vertices are labeled […] in breadth-first order.”

Because of their connection to random matrix theory and the study of the stochastic Airy semigroup, the distributional properties of the random variables in (3) and the random variables

for each are of interest. Apart from the case , where tools from stochastic calculus are useful Hariya ; GLS_RBB , it is not obvious what approach to studying these random variables will be fruitful. In this article, we present a discrete forest model in order to understand these random variables which can yield a wide class of results involving the difference of an integral of a stochastic process and a constant multiple of an integral of its squared local time. See Corollaries 1 and 5 below. Some of these techniques hold even outside of a Brownian regime and do not rely on the stochastic calculus techniques of Hariya ; GLS_RBB . However, these stochastic calculus techniques can be used when we are inside the Brownian regime. We develop the techniques in Hariya ; GLS_RBB further with Theorems 1.3 and 1.4.

1.1 Random tree and branching process interpretation

We begin by giving the discrete interpretation of the Gorin-Shkolnikov identity in (1) and its generalization in (4) in terms of two statistics on a random forests. We then show that these same statistics have a functional limit for a wide class of random forest models.

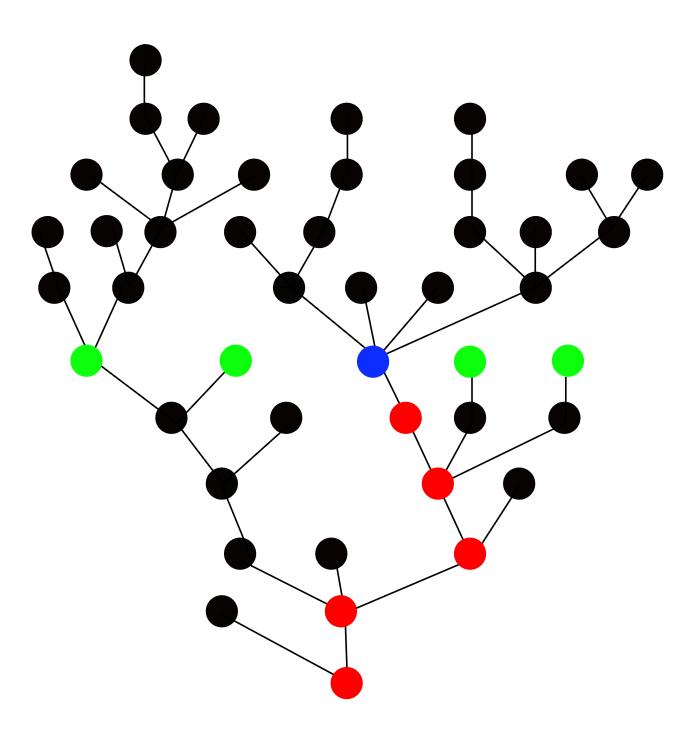

Consider the vertex set . By a forest on , we mean a cycle-free graph on the vertices . We say that a forest is rooted if each connected component has a distinguished vertex called its root. Roots will be denoted by the letter . We equip the forests with the graph distance, denoted by . Given a forest on we can define two statistics on the graph, measuring height and width. The first statistic, denoted by , is the height of the vertex, i.e. the distance from the root. The second statistic counts the number of “cousin” vertices, i.e. vertices at the same height; we denote this by . If is in the same component as the root , then the two statistics are

| (5) |

The statistics are portrayed graphically in Figure 1 below.

The following theorem describes the scaling relationship.

Theorem 1.1

Fix a sequence such that . For each , let denote a rooted forest on the vertex with roots uniformly chosen among all such forests. Then the following weak convergence holds as

The above theorem relies on the connection between random trees and forests and excursions and reflected Brownian bridges in the literature. See, for example, Aldous_CRT1 ; Pitman_SDE and references therein for more details on this connection. It also relies heavily on the extension of Jeulin’s identity implicit in the work of Pitman Pitman_SDE , which relates the local time of a reflected Brownian bridge with a time-change of a 3-dimensional Bessel bridge. We discuss some extensions of the stochastic calculus approach used in Hariya ; GLS_RBB below. Before moving to that section, we discuss a generalization using branching processes.

In the study of branching processes, there is a breadth-first model similar to the Jeulin identity. It is called the Lamperti transform originating in the work Lamperti_CSBP1 . Consider a genealogical structure with immigration depicted in Figure 2 below.

In this picture, the vertices (or individuals) come in two types. Using the language in Duquesne_CRTI , the mutant individuals are the unlabeled white vertices and the non-mutant vertices are the labeled black vertices. The mutant vertices are simply a convenient way to introduce immigration and play little to no role in much of our analysis. The non-mutant vertices are labeled by in a breadth-first order with the convention that the immigrant vertices are labeled last in each generation. The mutant vertices are unlabeled. Let denote the number of children of the vertex , and let denote the number of immigrants which arrive at height (or generation) . In Figure 2, the forest has non-mutant individuals at height 0, the sequence of ’s begins , , , etc. and the sequence of ’s begins , , and . Conversely, given a number of non-mutant vertices at height (i.e. the roots) and two sequence of non-negative integers and one can inductively construct a forest like the one in Figure 2. See Section 2.1 for more information.

If we let denote the number of non-mutant vertices appearing at or before height , then with the conventions the vertices at generation exactly are indexed by . From here it follows

Let denote the number of non-mutant vertices at height exactly , let and let . As observed in CGU_CSBPI , we can recover the successive generation sizes by solving the discrete equation

This is the discrete Lamperti transform, which was rigorously studied in CGU_CSBPI and generalized by the same authors in CPU_affine . The authors described continuous time analogs and developed robust limit theorems. In particular, the authors of CGU_CSBPI show that if is a Lévy process with no negative jumps and is an independent subordinator with Laplace transforms satisfying

then there exists a unique càdlàg solution to the equation

| (6) |

which exists until some possible explosion time. Moreover the process is a continuous state branching process started from with branching mechanism and immigration rate . We denote the law of solving (6) for these Lévy processes and by . See Section 2.4 for more details on these processes. However, throughout this work we will work under the following assumptions on and :

Assumption 1

The function is of the form

for some , and a Radon measure such that is a finite measure. We assume that in addition is conservative, meaning Grey_explosion

| (7) |

The subordinator is for all , equivalently . ∎

The first part of Assumption 1 is equivalent to being a real-valued Lévy process which has no negative jumps and is not killed, see Bertoin_LP . The second part of Assumption 1 is in some sense the most general assumption on that we can make for weak convergence arguments, see KW_BPI .

As briefly mentioned above, we can construct a forest, , from two sequences and along with a non-negative integer . We say that is a Galton-Watson immigration forest with offspring distribution and immigration distribution starting from roots if the sequences and and there are non-mutant individuals at height . We use the notation . We also label the non-mutant vertices by in a breadth-first manner. See Section 2.1 and Definition 1 therein for a more in-depth description of this model.

We can again define two statistics, and by (5). We will examine the following two processes,

| (8) |

We refer to as the cumulative breadth-first cousin process and as the cumulative breadth-first height process.

We will be concerned about distributional limits of the processes and , for sequences of forests . For ease of notation we write instead , along with similar notation shifts for other processes.

Let and be any sequence of probability measures on which satisfy Assumption 2 below.

Assumption 2

There exists a sequence of non-negative integers and a real-valued Lévy process with non-negative jumps such that its negative Laplace exponent is conservative (i.e. satisfies (7)). We assume

where are i.i.d. with common distribution . Simultaneously, for the same sequence , we suppose

for some non-random constant where are i.i.d. with common distribution .

There are many examples of sequences of distributions and which satisfy Assumption 2. Some examples are included below. In the following examples and throughout the work, we write for the integer part of a real number .

-

1.

For any with mean 1 and variance and with mean ,

by the central limit theorem and the weak law of large numbers. Hence, Assumption 2 holds for and for a standard Brownian motion (i.e. ).

-

2.

For a non-centered normal distributions, take a fixed with for sufficiently large, having mean and , then

This corresponds to and .

-

3.

Outside of a Brownian regime, we can take where for some and . Then, for we have

where is a spectrally positive stable Lévy process and when for some constant . See, for example, (Durrett_PTE, , Section 3.7). Taking, for example, for some implies

We now state the following generalization of the Gorin-Shkolnikov identity, at least as described in the Theorem 1.1 interpretation of the result.

Theorem 1.2

The above theorem relies on the following lemma.

Lemma 1

It may not be immediately clear that Theorem 1.2 is related to the integral identity in (1). We hope to illuminate the connection with this example, based on the work by Duquesne Duquesne_CRTI . Consider the sequences of measures and with and for each . For these measures Assumption 2 is clearly satisfied with the , and the Lévy process a Brownian motion .

We let . As shown by Duquesne Duquesne_CRTI , there exists an encoding (in a depth-first manner) of the non-mutant vertices in by a height process such that

Moreover, Duquesne shows that

where

for a Brownian motion with its local time at level zero and time being and . Duquesne Duquesne_CRTI also shows that the process possesses a jointly measurable (jointly continuous in this situation (RY, , Theorem VI.1.7)) family of local times satisfying the occupation time formula

We remark that we always take this definition of local time even if the process is a semi-martingale with quadratic variation not identically , which is the case in this present example.

Then Theorem 1.2, Lemma 1 and the Ray-Knight theorem Duquesne_CRTI imply the following corollary:

Corollary 1

Define by

Then

| (10) |

In particular, for each ,

This corollary can be generalized further with Corollary 5, which includes examples of processes where the right-hand side is a spectrally positive Lévy process with certain additional constraints. The integral relationship in equation (10) is analogous to the Gorin-Skholnikov identity in the sense that both relate a linear combination of the area under a curve and the integral of the squared local time to a normal distribution. Of course, the formulation in Corollary 1 gives a Gaussian process and not just a single normal distribution. This process-level generalization is further studied using stochastic calculus with Theorem 1.3.

1.2 Stochastic Calculus Approach

While Corollary 1 follows from Lemma 1 it can also be obtained by stochastic calculus without the appeal to Lamperti transform in CGU_CSBPI . Similar methods were used by Hariya Hariya and Lamarre and Shkolnikov GLS_RBB to obtain the normality results in (1) and (4). We extend their methods in this paper.

Suppose the Lévy process in Lemma 1 is of the form for and . Then an elementary calculation yields is a Gaussian process with mean and covariance function for . We can extend this to a more general Gaussian structure. To do this examine the stochastic differential equation:

| (11) |

where is a function such that is Lipschitz and , is a constant such that and is a continuous function and is a standard Brownian motion. In Section 5.2 we prove the weak existence of a solution to (11) by a sequence of time-changes.

Theorem 1.3

Suppose that is a weak solution to the stochastic differential equation in (11). Let . Define the process by

Then is a Gaussian process with continuous sample paths. Its mean is given by

and its covariance function is given by

We can also study stochastic differential equations of the form

| (12) | |||||

for a standard Brownian motion , constants and a continuous function. As shown by Pitman Pitman_SDE , the terminal local time of a reflected Brownian bridge conditioned on the event is a weak solution to the stochastic differential equation

In Section 5.1 we prove the weak existence of a solution to (12). See also Leuridans’ work L_RKConditioned on the conditioned Ray-Knight theorem. In Section 6 we extend Lemma 1 to the SDEs in (12). We prove the following theorem:

Theorem 1.4

The above theorem has the following corollary, due to GS_paper when and GLS_RBB when . See also Hariya .

Corollary 2

Let denote a reflected Brownian bridge and let denote its local time profile. Then, conditionally on ,

1.3 Another Example

We do not claim that this is the best discrete interpretation of the Gorin-Shkolnikov identity found in GS_paper and its generalization in GLS_RBB . However, the model presented in this article presents a generalization to a wide class of random forests. There are other discrete models which are asymptotically related to Brownian excursions and Brownian bridges. We briefly make note of one such example, which may be of use in order to understand for other values .

It is well known that a Brownian excursion can be constructed from a Brownian bridge by placing the origin at the bridges absolute minimum, see Vervaat . One extension of the result can be found in the work of Chassaing and Janson CJ_vervaat . In their analysis, they use another combinatorial object of study called parking functions. Certain classes of parking functions are in bijection with labeled trees on the vertex set rooted at 0. See CM_parking and references therein for more details on the specifics of the bijection. In the discrete setting, the analog of the average height of a vertex in a rooted tree is the so-called displacement for parking functions, and the average number of cousin vertices is the average number of “cars” that, at some point, want to park in a certain parking space. In this work we do not endeavor to prove weak limits for these discrete analogs; however, we do state what the limiting objects should be. Going back to the belief that there may be an “interesting combinatorial interpretation” of the quantity , parking functions may be another way to find a combinatorial interpretation of the results.

In this section we deviate from the notation in the last section. We let denote a Brownian bridge, and let denote a standard Brownian excursion. We take the (deterministic) periodic extensions of these functions so that they are defined on all of . Fix an , define the following processes

The process is just a reflected Brownian excursion with negative drift .

We now let denote either of the processes above. The occupation measure of is equal in law to the occupation measure of a reflected Brownian bridge conditioned on its local time at zero being . See (CJ_vervaat, , Cor. 2.3). The presence of the factor of comes from the different conventions for the local time at 0 used in Pitman_SDE and CJ_vervaat . Since, almost surely the occupation measure for a reflected Brownian bridge has a continuous density with respect to the Lebesgue measure, the same holds for the occupation measure of . Thus we get the following corollary of Corollary 2.

Corollary 3

Let denote either or above. Let denote a continuous version of the density of the occupation measure for . Then,

Parking functions and random forests are not the only combinatorial models that have asymptotics related to the Brownian excursion or Brownian and their local times. As mentioned previously, numerous quantities in graph enumerations are related to either a Brownian excursion or its integrals, see Janson_ExcursionArea and references therein. See also AP_BBAss for the connection between these processes and the asymptotics of uniform random mappings.

1.4 Overview of The Paper

In Section 2.1, we discuss the discrete forest model underlying our weak convergence results in Theorem 1.2. This model is based on a random forest model used by Aldous Aldous_AF and Duquesne Duquesne_CRTI . Afterward, in Section 2.2 we discuss in more detail the various processes defined on the random forest. In Sections 2.3 and 2.4 we discuss Lévy processes and continuous state branching processes respectively. Importantly, we describe the path-by-path relationship between these two classes from CGU_CSBPI . Section 2.5 contains information on -height processes and their Ray-Knight theorems.

After discussing these preliminaries we move to prove integral relationships for Lévy processes and their relationships with continuous state branching processes with immigration in Section 3. This brief discussion allows us to prove Corollary 5, which is the continuum random tree generalization of the Gorin-Shkolnikov identity.

In Section 4 we prove our weak convergence results which rely on the integral results in Section 3. The proofs of Theorems 1.1 and 1.2 are found in Section 4.1. In Section 6 we prove the normality results in Theorems 1.3 and 1.4 after studying the properties of solutions to (11) or (12) in Section 5.

Acknowledgments

The author thanks David Aldous for a helpful discussion on the random tree interpretation of Jeulin’s identity. The author thanks Soumik Pal for continued guidance during this project and providing helpful comments on clarifying several arguments in the paper. I would also like to thank the two anonymous referees for their careful reading and detailed comments on the presentation and proofs, including an idea for simplifying the proof of Lemma 8.

2 Preliminaries

2.1 Forest Constructions

In this section we describe the forest “picture” underlying some of our weak convergence arguments later. This model is based on a model used by Aldous in Aldous_AF and then by Duquesne in Duquesne_CRTI . However, since we will not be proving convergence of the contour functions, we do use a labeling which is convenient for our analysis and is not useful for any type of genealogical analysis which can be found in Duquesne_CRTI .

In this work, a forest will mean a locally finite planar graph on the vertex set

which has a finite number of connected components which themselves are rooted planar trees. The vertices of the form will be called the non-mutant vertices (depicted in Figure 2 as black vertices) and the vertices of the form will be called mutant vertices (depicted as the white unlabeled vertices in Figure 2). When referring to a forest , we will let denote the vertex set of and denote the edge set.

We will construct our random forests in a breadth-first approach from two given sequences of non-negative integers and along with a number . At each height there will be two types of vertices, mutant and non-mutant vertices. There will only be one mutant vertex in each generation, and will be omitted from most of the objects we count on our forest. Children of mutant vertices will appear last in the breadth-first ordering when restricting to each height.

Each will represent the number of offspring the non-mutant vertex will have. Each will represent the number of immigrants that will appear in generation . The immigrants will be non-mutant offspring of the mutant vertex from the previous generation.

We start with defining to be the graph with vertex set

and edge set . The vertex will be the mutant vertex. These vertices will be the roots of the random forest, and will consequently be the vertices of height . For each we construct from by adding vertices of height . There are two cases which we must consider: (1) there are no non-mutant vertices at height in or (2) the non-mutant vertices at height in are for some natural numbers .

In Case (1), we add non-mutant vertices and a single mutant vertex as offspring of the mutant vertex . The collection of non-mutant vertices of is of the form

for some . When the above set is empty. We let be the graph with vertex set and the edge set

The height of the vertices of will be the distance to the root, which inductively implies for all that . We remark that if then the only vertex in is the vertex .

In Case (2), we add non-mutant vertices as offspring for each non-mutant vertex in generation . We also add non-mutant vertices and a single mutant vertex as the offspring of . We go into more detail in order to describe the breadth-first labeling. There are non-mutant vertices at height in . These vertices will be of the form for some . Each vertex gives birth to children at height and the vertex will give birth to non-mutant children and 1 mutant child. Thus the vertex set for will be

Moreover, for each we add edges between a vertex and for . We also add edges between and along with for Again, the vertices in have distance from a root.

We continue this process ad infinitum, and define . By construction, for we must have .

Definition 1

A forest constructed as above starting from non-mutant vertices is called Galton-Watson immigration forest (GWI forest for short) when the integer sequence are i.i.d. and the sequence are i.i.d. and are independent of . We call the common distribution, say , of the offspring distribution, and we call the common distribution, say , of the immigration rate. We denote the law of by .

2.2 Processes defined on the forest

In this section we define several processes on the forest, and describe some of the relationships between the various processes and the breadth-first labeling of the vertices. Let be a forest constructed as above. We recall that the forest is rooted, and that the height of a vertex is defined as the distance from the vertex to a root in the graph distance.

Define the height profile of the forest as the process by

This counts the number of non-mutant vertices at height in the forest . We also define the cumulative height profile of as the process by

and its right-continuous inverse by

We observe that is the index of the first vertex at height . This follows easily from the convention that we start indexing at 0. Hence, and so is the width of the layer of the forest containing the vertex .

Lastly, we refer the reader back to (8) for a definition of the cumulative breadth-first cousin process and the cumulative breadth-first height process .

2.3 Lévy processes

We will provide a brief overview of spectrally positive Lévy processes. More details and proofs of the statements below can be found in Chapter VII of Bertoin’s monograph Bertoin_LP .

A (possibly killed) spectrally positive Lévy process is a Lévy process which contains no negative jumps. Its Laplace transform exists and uniquely characterizes the process . The Laplace transform must be of the form

| (13) |

Moreover, the function must be of the form

| (14) |

where , and is a Radon measure on such that . Conversely, for each such , there exists a spectrally positive Lévy process with such a Laplace transform.

A particular class of spectrally positive Lévy processes are subordinators. These are Lévy processes with increasing sample paths. A subordinator has a Laplace transform of the form

| (15) |

where is of the form

| (16) |

with and is a Radon measure with . In our work, we concern ourselves with the case where for some , which makes the subordinator .

2.4 Continuous state branching processes

Continuous state branching processes with immigration (CBI processes) arise as scaling limits of discrete Galton-Watson processes, see KW_BPI . A CBI process is a Feller process on which is absorbed at . We denote by the expectation conditionally given . As shown by KW_BPI , the Laplace transform of is of the form

where is the unique non-negative solution to the integral equation

for functions and . The function is called the branching mechanism and must be of the form (14) and the function is called the immigration rate and must be of the form (16). Conversely, given any two such functions and , there exists a CBI process with branching mechanism and immigration rate . For simplicity, we will use to refer to the law of a CBI process starting from and satisfies the above Laplace transform.

By KW_BPI , we know that continuous state branching processes with immigration are in one-to-one correspondence with pairs of Lévy processes satisfying (13) and (15). The bijection described there is in terms of the Laplace transforms of the respective processes. A path-wise identification does exist, thanks to the work of Caballero, Pérez Garmendia and Uribe Bravo CGU_CSBPI . As mentioned previously, the authors of CGU_CSBPI show that if is a spectrally positive Lévy process with Laplace exponent and is an independent subordinator with Laplace exponent then a càdlàg solution to (6) exists, is unique, and is a process. When is identically 0, the Lévy process in (6) is stopped upon hitting . The path-wise relationship when was observed by Lamperti Lamperti_CSBP1 , although proved later by Silverstein S_LT .

2.5 The -height process

In this section we recall properties of a height process . These processes were introduced by Le Gall and Le Jan in LL_BPLP , and further examined in LL_BPLP2 ; DL_Levy . The excursions of this process are the continuum random tree analog of the contour process for a discrete tree. We recall some of their properties, but do not endeavor to state things in full generality. To this end, we assume that

| (17) |

with and a Radon measure with the stronger integrability condition . We make the assumption that is conservative, i.e. it satisfies equation (7), and that further satisfies

| (18) |

Both of these assumptions on are slight restrictions on a general theory, but they imply that a Lévy process with Laplace exponent has paths of infinite variation, non-negative jumps, and does not drift towards .

Let be a Lévy process with Laplace exponent satisfying the above restrictions. The value of the height process at time is a way to “measure” the size of the set

This is done through a time-reversal approach. For each , define by and the corresponding supremum process by . The value is a normalization of the local time at 0 of the process . By (DL_Levy, , Theorem 1.4.3) has a continuous modification if and only if the condition in (18) is satisfied. Whenever (18) is satisfied, we will assume that is this modification. For more information on height processes see DL_Levy .

The process possesses a family of local times which almost surely satisfies the occupation density formula:

| (19) |

See (DL_Levy, , Proposition 1.3.3). There is also a Ray-Knight theorem for these processes as shown in (DL_Levy, , Theorem 1.4.1). Namely, define then

Similar Ray-Knight theorems were obtained by Warren Warren_RK involving sticky Brownian motion.

The Ray-Knight theorem above was extended by Lambert Lambert_CBI and Duquesne Duquesne_CRTI to allow for some immigration. Lambert’s work is slightly more general; however Duquesne’s work contains some better approximation results for the local time. For and define the left-height process by

| (20) |

By Duquesne_CRTI , there exists a jointly measurable family of local times which is continuous and increasing in and satisfies equation (19) with and replacing and . Since as , the limit is finite almost surely due to (7). Moreover, the Ray-Knight theorem, see (Duquesne_CRTI, , Theorem 1.2, Remark 3.2) and (Lambert_CBI, , Theorem 5), states

| (21) |

In the case where the branching process is a squared Bessel process and the height process is a reflected Brownian, a similar result was shown in LY_RKThms .

3 Integral Relationships for CBIs

In this section we describe various properties of continuous state branching processes and their implications for random trees. We will mostly work under the assumption that is a conservative branching mechanism; however, when discussing the implications for left-height processes we must work under slightly stricter assumptions. We recall that being conservative is equivalent, see Grey_explosion , to the almost sure finiteness of a process.

Let us start by gathering certain properties of processes related to a process . If for some then, by Theorem 2 in CGU_CSBPI , we can and do assume to be the unique càdlàg solution to

| (22) |

where is a Lévy process with Laplace exponent . Moreover, using this representation of along with Lemma 3 and Corollary 5 in CGU_CSBPI and the strong Markov property for the following lemma is easy to see.

Lemma 2

The above lemma tells us that the process defined in equation (9) is actually the two-sided inverse of . Moreover, since diverges towards infinity almost surely, the value of is finite for each .

We now move to the proof of Lemma 1.

Proof (Proof of Lemma 1)

We assume that we are working on a probability space where has the path-by-path representation in (22), for a Lévy process . The change of variable formula implies

for locally bounded functions . Moreover, since , we can claim

However, by (22) and the fact that is the two-sided inverse of ,

The result desired claim now easily follows. ∎

In fact the above proof easily implies the following corollary as well.

Corollary 4

3.1 The continuum random tree interpretation

Here we must strengthen the assumptions put onto in order to guarantee that there is a continuous -height process. As discussed in Section 2.5, we require that satisfies (7), (17) and (18).

4 Weak Convergence

Throughout this section we will let denote a sequence of forests where each is a -forest. We also assume that and satisfy Assumption 2, and is the sequence of integers specified therein.

With this we can now prove the following joint convergence lemma:

Lemma 3

If and satisfy Assumption 2, then the following joint convergence holds in the product of the Skorokhod space

| (23) |

where is a process.

Proof

We remark that by (Duquesne_CRTI, , Theorem 1.4), the convergence of rescaling of converges to a process, i.e.

We also observe

Since locally uniformly, the joint convergence

will follow once we argue the continuity of the map .

To see that is continuous we prove that continuously embeds into . Indeed, suppose that in and let be a continuity point of . For , set . Then there exists a sequence such that as . Then

The first term can easily be handled since in and the second term converges to 0 as by dominated convergence. This proves the continuity of the embedding . Since is a continuous map from and embeds continuously into , we have shown the desired continuity.

The convergence of the third coordinate in equation (3) follows from (Whitt_WC, , Theorem 7.2) and Lemma 2. Indeed, define the set to be the collection of functions which are unbounded from above with and equip this set with the Skorokhod topology. Then the map defined by is measurable and it is continuous on the set of strictly increasing functions. ∎

4.1 Proofs of Theorem 1.2 and Theorem 1.1

Proof (Proof of Theorem 1.2)

Throughout this proof we refer to as a process, the quantity and defined in (9). In what follows we sometimes write the index in the process as instead of as a subscript , and similar remarks hold for the other processes.

We recall that the first index of a vertex in at height is . Therefore

Similarly, we can see that

Consequently,

and

This easily implies the weak convergence in

Moreover this convergence is joint with the convergence in (3), and hence by a lemma on pg. 151 in B_CPM

By Lemma 1 and Slutsky’s theorem, the result follows if we can show

| (24) |

and

To argue the above convergences, we observe that . Since is increasing, we have

| (25) |

The presence of the square in the second inequality follows from the fact that

The desired convergence in (24) follows from

The above convergence then holds by Lemma 3 and standard weak convergence arguments for time-changes (see e.g. a lemma on pg. 151 in B_CPM ). Indeed, we have

| (26) |

Since by Assumption 2, the stated convergence to zero holds.

Similar arguments can yield Theorem 1.1. However, the authors of GS_paper and GLS_RBB are interested in distributional properties of the quantity

where is a reflected Brownian bridge conditioned on its local time at level zero and time 1 being exactly and is the local time of at time 1 and level . Hence, we prove the following proposition, which by taking and using Theorem 1.13 in GLS_RBB yields the formulation in Theorem 1.1.

Proposition 1

Suppose that is a uniformly chosen rooted labeled forest on vertices with roots where as . Then the following convergence in distribution holds

where and are as above.

Proof

This proof follows from arguments similar to Theorem 1.2 and the results of Pitman Pitman_SDE describing a conditional version of a result by Drmota and Gittenberger DG_Bridge . Alternatively, when we can use Jeulin’s identity along with a prior work by Drmota and Gittenberger DG_profile .

Let denote the height profile of . Then, by Theorems 4 and 7 in Pitman_SDE , we have

where the convergence above is weak convergence in the Skorokhod space.

Hence,

and, similarly

The result now easily follows. ∎

5 SDE Results

In this section we discuss the existence and uniqueness of solutions to SDEs of the form (12) and (11). We first study the situation with equation (12) and then move onto studying equation (11).

5.1 Analysis of (12)

We begin by studying a fairly different stochastic differential equation. Let be a Brownian motion on the filtered probability space and let be the unique strong solution to the stochastic differential equation

where and are constants. The process is times a Bessel bridge of dimension and so a unique strong solution exists by properties of Bessel bridges. See Section XI.3 in RY and GY_Bessel for more properties about Bessel bridges.

Now let be a continuous function and define to be the continuous martingale . Observe that , where is the Doléans-Dade exponential, is a positive continuous local martingale. Hence, by Girsanov’s theorem (RY, , Theorem VIII.1.7), the measures and are equivalent on for each . Moreover, is a -Brownian motion and so

| (27) |

Using (RY, , Theorem IX.1.11), we have the following lemma:

Lemma 4

There is weak existence and uniqueness in law to equation (27) for constants , and continuous function .

Moreover, the law of a solution to (27) is equivalent to the law of where is a Bessel bridge of dimension .

Using facts about Bessel bridges and the equivalence of measures described in the above lemma, we obtain the following corollary. See, for example, (RY, , Chapter XI), GY_Bessel . In particular, the derivation of Equation (2.6) in Hariya generalizes for -dimensional Bessel processes when .

Corollary 6

Suppose is a solution to (27) with and a continuous function. Then the following hold almost surely.

-

1.

if and for all when and .

-

2.

if .

-

3.

for all .

-

4.

The process for is strictly increasing and bounded for . It is strictly increasing and locally bounded on when and .

When , we can define the right-continuous inverse for . Since is strictly increasing is actually a two-sided inverse of . Define the process and observe on the event and for

We observe that

and, by Proposition V.1.5 and Theorem V.1.6 in RY , we can write for a Brownian motion . Hence, for

| (28) |

Finally, we observe that almost surely. Similarly, given a process satisfying (28) the process with for solves the stochastic differential equation (27).

We have thus argued the following proposition:

5.2 Analysis of (11)

Throughout this section we assume that is a continuous function and is a function such that is Lipschitz and there is some and such that .

We begin by observing that since is Lipschitz and bounded below, the function is Lipschitz. Now define the function , and observe that this function is continuous since is strictly positive and moreover, it is the unique solution to

Observe that for each the function is bounded and continuous. If we define

then is also continuous.

Since is continuous, by (FG_bbvd, , Proposition 1) and (RY, , Theorem IX.3.5), for each there exists a unique strong solution to the stochastic differential equation

where is a standard Brownian motion on some filtered probability space . But this means that there is a weak solution to the stochastic differential equation

since and . Since satisfies , by (RY, , Proposition IX.1.13), there is a weak solution to the stochastic differential equation:

But this means that solves

| (29) |

The next lemma states that the process can be bounded below by a deterministic time-change of a squared Bessel process . We recall RY that a squared Bessel process of dimension and starting from is the unique strong solution of the stochastic differential equation

for a standard Brownian motion .

Lemma 5

Suppose is a solution to (29) with respect to a Brownian motion and started from . Fix any . Then on the same probability space there exists a -dimensional squared Bessel process starting from such that

Proof

We prove this lemma by a time-change. Let and define the process by Observe

where and we used the change of variable in the drift integral. We now observe

and so by the Dambis-Dubins-Schwarz theorem (RY, , Theorem V.1.6) there is a Brownian motion such that

For each and with respect to this Brownian motion , there exists a unique strong solution to the stochastic differential equation

The comparison theorems (RY, , Theorem IX.3.7) imply that

for any . The desired claim now follows. ∎

Arguments similar to Lemma 4 and Corollary 6 give the following lemma, the details of which are omitted:

Lemma 6

Suppose is a continuous function and is a Lipschitz function with . There exists a weak solution to the stochastic differential equation:

Moreover, for any such solution the following hold almost surely:

-

1.

If and or and , then for each .

-

2.

If and then .

Observe that if then almost surely never reaches . Therefore, we can apply Itô’s rule to and see

Hence we have argued the following lemma:

Lemma 7

Suppose is a continuous function and is a Lipschitz function with . Assume that and . There exists a weak solution to the stochastic differential equation

| (30) |

Moreover, any such solution is strictly positive and so the process is continuous and strictly increasing.

Finally, we use a time change and obtain the following proposition.

Proposition 3

Suppose is a continuous function and is a Lipschitz function with . Assume that and . Then there exists a weak solution to (11). Moreover, for any such solution , the process is strictly increasing.

Proof

The proof of existence is omitted, since it follows from the arguments similar to those in Proposition 2.

We now argue that is strictly increasing. To this end let be a solution to (11) with respect to some Brownian motion . To argue that is strictly increasing, we argue its derivative is strictly positive. To this end, we argue by contradiction and suppose that . First by continuity and the fact . Hence, for and hence is strictly increasing for and we set .

We now define the right-continuous inverse of as and define . Observe that for we have

where .

Moreover, we have that

Hence, by Dambis-Dubins-Schwarz (RY, , Theorem V.1.6) there is a Brownian motion on the interval such that

Moreover, is continuous and strictly increasing by Lemma 7 and the stochastic process is strictly positive and uniformly bounded away from zero on bounded time intervals. Hence

This gives the desired contradiction and we conclude that is always strictly positive and hence is strictly increasing. ∎

6 Proofs of Normality Results

6.1 Proof of Theorem 1.4

Throughout this subsection we fix a and and let and be related as in Section 5.1. In particular, we know that and solve (27) and (12), respectively, and are related by where . As we have seen the right-continuous inverse of is equal to .

6.2 Proof of Theorem 1.3

Proof (Proof of Theorem 1.3)

We observe that given a solution to (11), we can define where satisfies (9) and then is a weak solution to (30). This follows from the proof of Proposition 3.

We observe that the left-hand side is equal to

We just need to show that

has the desired mean and covariance structure. It is easy to see

while the covariance structure follows from the following lemma. ∎

Lemma 8

Let , let be a standard Brownian motion and define Then , and consequently it is a centered Gaussian process such that for ,

Proof

The claim that is simply the stochastic Fubini theorem (Protter.05, , Theorem 65).

The covariance structure now follows by Itô’s isometry: for any

The result follows letting and . ∎

References

- (1) D. Aldous. Asymptotic fringe distributions for general families of random trees. Ann. Appl. Probab., 1(2):228–266, 1991.

- (2) D. Aldous. The continuum random tree. I. Ann. Probab., 19(1):1–28, 1991.

- (3) D. Aldous, G. Miermont, and J. Pitman. The exploration process of inhomogeneous continuum random trees, and an extension of Jeulin’s local time identity. Probab. Theory Related Fields, 129(2):182–218, 2004.

- (4) D. J. Aldous and J. Pitman. Brownian bridge asymptotics for random mappings. Random Structures Algorithms, 5(4):487–512, 1994.

- (5) J. Bertoin. Lévy processes, volume 121 of Cambridge Tracts in Mathematics. Cambridge University Press, Cambridge, 1996.

- (6) P. Billingsley. Convergence of probability measures. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons, Inc., New York, second edition, 1999. A Wiley-Interscience Publication.

- (7) M. E. Caballero, J. L. Pérez Garmendia, and G. Uribe Bravo. A Lamperti-type representation of continuous-state branching processes with immigration. Ann. Probab., 41(3A):1585–1627, 2013.

- (8) M. E. Caballero, J. L. Pérez Garmendia, and G. Uribe Bravo. Affine processes on and multiparameter time changes. Ann. Inst. Henri Poincaré Probab. Stat., 53(3):1280–1304, 2017.

- (9) P. Chassaing and S. Janson. A Vervaat-like path transformation for the reflected Brownian bridge conditioned on its local time at 0. Ann. Probab., 29(4):1755–1779, 2001.

- (10) P. Chassaing and J.-F. Marckert. Parking functions, empirical processes, and the width of rooted labeled trees. Electron. J. Combin., 8(1):Research Paper 14, 19, 2001.

- (11) M. Drmota and B. Gittenberger. On the profile of random trees. Random Structures Algorithms, 10(4):421–451, 1997.

- (12) M. Drmota and B. Gittenberger. Strata of random mappings—a combinatorial approach. Stochastic Process. Appl., 82(2):157–171, 1999.

- (13) I. Dumitriu and A. Edelman. Matrix models for beta ensembles. J. Math. Phys., 43(11):5830–5847, 2002.

- (14) T. Duquesne. Continuum random trees and branching processes with immigration. Stochastic Process. Appl., 119(1):99–129, 2009.

- (15) T. Duquesne and J.-F. Le Gall. Random trees, Lévy processes and spatial branching processes. Astérisque, (281):vi+147, 2002.

- (16) R. Durrett. Probability: theory and examples, volume 31 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, fourth edition, 2010.

- (17) G. Faraud and S. Goutte. Bessel bridges decomposition with varying dimension: applications to finance. J. Theoret. Probab., 27(4):1375–1403, 2014.

- (18) A. Göing-Jaeschke and M. Yor. A survey and some generalizations of Bessel processes. Bernoulli, 9(2):313–349, 2003.

- (19) V. Gorin and M. Shkolnikov. Stochastic Airy semigroup through tridiagonal matrices. Ann. Probab., 46(4):2287–2344, 2018.

- (20) D. R. Grey. Asymptotic behaviour of continuous time, continuous state-space branching processes. J. Appl. Probability, 11:669–677, 1974.

- (21) Y. Hariya. A pathwise interpretation of the Gorin-Shkolnikov identity. Electron. Commun. Probab., 21:Paper No. 52,6, 2016.

- (22) S. Janson. Brownian excursion area, Wright’s constants in graph enumeration, and other Brownian areas. Probab. Surv., 4:80–145, 2007.

- (23) T. Jeulin and M. Yor, editors. Grossissements de filtrations: exemples et applications, volume 1118 of Lecture Notes in Mathematics. Springer-Verlag, Berlin, 1985. Papers from the seminar on stochastic calculus held at the Université de Paris VI, Paris, 1982/1983.

- (24) K. Kawazu and S. Watanabe. Branching processes with immigration and related limit theorems. Teor. Verojatnost. i Primenen., 16:34–51, 1971.

- (25) P. Y. G. Lamarre and M. Shkolnikov. Edge of spiked beta ensembles, stochastic Airy semigroups and reflected Brownian motions. Ann. Inst. Henri Poincaré Probab. Stat., 55(3):1402–1438, 2019.

- (26) A. Lambert. The genealogy of continuous-state branching processes with immigration. Probab. Theory Related Fields, 122(1):42–70, 2002.

- (27) J. Lamperti. Continuous state branching processes. Bull. Amer. Math. Soc., 73:382–386, 1967.

- (28) J.-F. Le Gall and Y. Le Jan. Branching processes in Lévy processes: Laplace functionals of snakes and superprocesses. Ann. Probab., 26(4):1407–1432, 1998.

- (29) J.-F. Le Gall and Y. Le Jan. Branching processes in Lévy processes: the exploration process. Ann. Probab., 26(1):213–252, 1998.

- (30) J.-F. Le Gall and M. Yor. Excursions browniennes et carrés de processus de Bessel. C. R. Acad. Sci. Paris Sér. I Math., 303(3):73–76, 1986.

- (31) C. Leuridan. Le théorème de Ray-Knight à temps fixe. In Séminaire de Probabilités, XXXII, volume 1686 of Lecture Notes in Math., pages 376–396. Springer, Berlin, 1998.

- (32) G. Miermont. Self-similar fragmentations derived from the stable tree. I. Splitting at heights. Probab. Theory Related Fields, 127(3):423–454, 2003.

- (33) A. Okounkov. Generating functions for intersection numbers on moduli spaces of curves. Int. Math. Res. Not., (18):933–957, 2002.

- (34) J. Pitman. The SDE solved by local times of a Brownian excursion or bridge derived from the height profile of a random tree or forest. Ann. Probab., 27(1):261–283, 1999.

- (35) P. E. Protter. Stochastic integration and differential equations, volume 21 of Stochastic Modelling and Applied Probability. Springer-Verlag, Berlin, 2005. Second edition. Version 2.1, Corrected third printing.

- (36) J. A. Ramírez, B. Rider, and B. Virág. Beta ensembles, stochastic Airy spectrum, and a diffusion. J. Amer. Math. Soc., 24(4):919–944, 2011.

- (37) D. Revuz and M. Yor. Continuous martingales and Brownian motion, volume 293 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, third edition, 1999.

- (38) M. L. Silverstein. A new approach to local times. J. Math. Mech., 17:1023–1054, 1967/1968.

- (39) W. Vervaat. A relation between Brownian bridge and Brownian excursion. Ann. Probab., 7(1):143–149, 1979.

- (40) J. Warren. Branching processes, the Ray-Knight theorem, and sticky Brownian motion. In Séminaire de Probabilités, XXXI, volume 1655 of Lecture Notes in Math., pages 1–15. Springer, Berlin, 1997.

- (41) W. Whitt. Some useful functions for functional limit theorems. Math. Oper. Res., 5(1):67–85, 1980.