Latent Variable Model for Multivariate Data with Measure-specific Sample Weights and Its Application in Hospital Compare

Abstract

We developed a single factor model with measure-specific sample weights for multivariate data with multiple observed indicators clustered within a higher level subject. The factor is therefore a latent variable shared by multiple indicators within a same subject and the sample weights are different across different indicators and different subjects. Even after integrating out the latent variable, the likelihood of the data cannot be written as the sum of weighted likelihood of each subject because a subject has different sample weights respectively for its multiple indicators. In addition, the number of available indicators varies across subjects. We derive a pseudo likelihood for the latent variable model with measure-specific weights. We investigate various statistical properties of the latent variable model with measure-specific sample weights and its connection to the traditional factor analysis. We found that the latent variable model provides consistent estimates for its variances when the measure-specific sample weights are properly re-scaled. Two estimation procedures are developed - EM algorithm for the pseudo likelihood and marginalization of the pseudo likelihood by directly integrating out the latent variable to obtain the parameter estimates. This approach is illustrated by the analysis of publicly reported hospitals with indicators and sample weights. Numerical studies are conducted to investigate the influence of weights and their sample distribution.

Keywords— pseudo likelihood, latent variable model, factor analysis, measure-specific sample weights

1 Introduction

This work is built on the basis of factor analysis. The factor analysis is a widely used statistical tool in many fields, such as psychology, educational testing, social behavior and biomedical sciences [4, 8]. The factor analysis is popular since it provides a

convenient modeling tool for multiple observed indicators within a subject [6]. In this paper, we propose a latent variable model with a

single factor for multivariate data with measure-specific weights that vary across

indicators and across subjects. A pseudo likelihood approach is developed for our

model.

Over the years, Centers for Medicare and Medicaid Services (CMS) Hospital Compare website publishes hospitals performance scores which are called hospital indicators in this paper.

CMS hopes that these indicators will help people choose their hospitals. In 2016, CMS started to report the star ratings of more than four thousand hospitals across the whole country [10]. The goal of the CMS overall hospital quality star rating is to estimate one summary score using a total of fifty-seven hospitals indicators collected from the hospital compare database. The fifty-seven indicators are divided into seven different groups according the quality aspect they represent. Each indicator within a hospital has its sample weight representing the volume of patients that contribute to that indicator. A

group-specific factor score is derived for the indicators within the group. The goal of

this paper is to estimate the factor model within a group incorporating sample weights

for each indicator within each hospital.

The factor is an unobserved latent variable that represents the underlying

hospital performance. In addition to the presence of measure-specific weights that

vary at both indicator and hospital level, there is a missing data issue as only a few

hospitals report the complete set of all the hospitals indicators. Traditional factor

analysis using correlation matrix approach is not possible to deal with such situation

and therefore we propose a pseudo likelihood method to estimate such model.

Existing literature has dealt with subject-specific weights. [7] studied the volume related weights which are subject-specific via the hierarchical logistic models.

[9] applied subject-specific weights in multivariate multilevel models to the longitudinal data. [5] gave an approach that based on the likelihood to generalize the overall score. And [1] proposed a weighted latent likelihood method based on subject-specific weights. To the best of our knowledge, there are no studies for the latent variable model with measure-specific weights, as well as its asymptotic behaviors. Therefore, we

fill the gap by proposing a version of weighted pseudo likelihood that fits for the measure-specific weights through two algorithms: Expectation-Maximization (EM) method and the

marginalization of the pseudo likelihood to get the parameter estimates. We apply this model to the CMS hospital compare dataset.

The sum of weights for each indicator across the hospitals is set to be the sample size of that indicator so that a hospital with a smaller volume for that indicator has a smaller sample weight for that indicator comparing to a hospital with a larger volume for that indicator. However, we show in Section 3 that the sum of such intuitive sample weights across hospitals for the indicator need to be bounded below the sample size in order for the estimates of the variance for the latent variable to be

consistent. We impose such bound by multiplying each sample weight by 0.99 which in

practice remains the same interpretation.

The rest of the paper is organized as follows. In Section 2 we present our model and specify the pseudo likelihood. The statistical properties of the latent variable model are given in Section 3. In Section 4 we describe the two algorithms including the EM approach and the marginal likelihood approach. The bound of the weights is given in Section 3. In Section 5 we conduct the numerical studies. In Section 6 we analyze three datasets from US hospital compare and in Section 7 we conclude with a discussion.

2 Model Specification and Pseudo Likelihood

We start the model with the following set-up:

Suppose there are a total of indicators with hospitals (subjects) in each indicator to be evaluated. Let denote the th indicator in the hospital with and . Let denote the measure-specific weight of hospital and indicator . For each , we fit a single confirmatory factor model as:

where is the underlying factor or latent variable representing hospital ’s performance based on its all indicators. The higher the value of , the better the performance of hospital h in indicator m. The and are unknown parameters that we need to estimate.

2.1 The Pseudo Joint Likelihood of Data and Latent Variable

Given , are conditionally independent. We have the joint density for the latent variable and satisfies

We define the joint pseudo likelihood for hospital with sample weights as

| (1) |

where bounded differentiable non-negative (the sample weight) function [1] independent to .

The logarithm of the term within the product is given as :

Thus, the conditional log-density of expression (1) is given as:

| (2) | ||||

Therefore, the negative logarithm of the joint density of all indicators for hospital is

| (3) |

And the log joint density of all indicators for all hospitals is the summation of through to .

Note that we can also bring missing values of into (3) by setting the corresponding , therefore, the joint pseudo log-density of latent variable model is also compatible with missing data in .

2.2 The Marginal Pseudo Likelihood

Note that part of (3) can be rewritten as the log-density of a normal distribution:

| (4) |

The first line of (4) is exactly the density function for a normal distribution after logarithm. Denote as the indicator vector for hospital , by integration with respect to , we have the marginal pseudo log-likelihood (denoted by ) of all the parameters for hospital satisfies

| (5) |

3 Statistical Properties of the Model

3.1 Main Theorems

In this subsection, we describe the asymptotic behaviors of the latent variable model under uniform weight case (all ) and the varying weights case.

We start with the simple uniform weight case when all the weights equal to one. Without missing value, the negative marginal logarithm likelihood (denoted by ) for all the parameters for hospital satisfies

| (6) |

since all . The pseudo log-likelihood becomes log-likelihood.

The asymptotic behaviors of the latent variable model are followed by the result of a toy example:

Example 1

Let , And the covariance between and is Without missing values, we have twice the negative log-likelihood of is the same as (6) when .

Example 1 shows in the latent variable model with uniform weight, When there are no missing values, the latent variable model is the same as the confirmatory factor analysis with single factor, since they both have the same log-likelihood. However, compared to obtaining parameter estimates through the calculation of the inverse variance-covariance matrix in the confirmatory factor model with multivariate normal distribution, the estimation through the likelihood of latent variable model formulation for the factor model is easier to obtain with cases. Therefore, we can have the following results.

Theorem 1

When there are no missing values, as , we have the expected negative marginal logarithm likelihood () satisfies

and has a normal distribution with mean equals to zero, finite variance.

Theorem 1 gives the asymptotic behavior of the marginal likelihood of latent variable model with uniform weights.

Theorem 2

Let the weight matrix where , are positive constants. Then by definition of NMLL, we have the expected pseudo marginal log-likelihood (ENWMLL) for hospital satisfies

without missing, as , and the central limit theorem also holds for NWMLL.

Theorem 2 gives the asymptotic behavior of marginal likelihood of the latent variable model with the weights those are specifically assigned.

3.2 Variance Bounded From Zero

This subsection mainly address the issue that in the latent variable model, certain may become zero. In that case, the validity of the latent variable

model can be endangered. However, the can be bounded away from zero by

adjusting the weights in a simple way presented in this section.

Easy to observe that each should be bounded away from zero in order to make the negative marginal logarithm (pseudo) likelihood valid. In the mean time, the computational speed for estimating the parameters will slow down heavily at the area where certain is tiny since there are no closed form solutions for (5). In the following part, we discuss the approaches that prevent the estimated standard error from going to zero when we incorporate with varying weights.

3.2.1 Uniform Weight

We will focus on three indicators () since if the number of indicators exceeds three, we can still pick three indicators to study.

For , let , where , and the covariance between and is . Assume have the same variance, moreover, assume

is the smallest correlation. Then we have be the smallest parameter among all s since is the largest one among all three s. And, when all the weights equal to one in latent variable model, two extreme examples may cause to be exactly zero:

Example 2

Assume and are identical, then we have .

Proof: Easy to verify that

Then we have .

Example 3

Assume and satisfies Corr(1,2)Corr(1,3) Corr(2,3), then we have .

Proof: By the result in Example 1, we have

thus the latent variable model outputs as its minimized occupation.

When Example 2 or Example 3 happens, the likelihood estimates of the latent variable model will be at the boundary, thus the posterior variance of may become zero. In order to prevent it, we need proper weights to get the posterior variance bounded from zero.

3.2.2 Varying Weights

Followed by Theorem 2, let where , are positive constants. We have,

as . We can see that if we set the sum of weight equals to the sample size (), we have

since all the weights are equal to one. Both Example 2 and Example 3 can cause being zero.

Assuming there are not identical indicators among , there is at most one can be zero. Without loss of generality, assume is the smallest among all s, then we have

Thus we have for which is a constant,

| (7) | ||||

If we have , it will penalize the expected marginal weighted likelihood from being zero since both will hold, and the rest terms are bounded.

Furthermore, if we let

by the Dominated Convergence Theorem, taking derivative to (7) with respect to yields

at the neighborhood larger than zero for when . Which proves that is bounded from zero.

Similarly, if we have , then as approaching zero. And will become an optimal estimate since the pseudo likelihood then goes to infinity. Therefore, we showed that if we have , then we can ensure all the estimated standard errors are bounded from zero.

Both numerical study and data analysis will show that by setting the mean of weights smaller than one, under the case which denotes the weight matrix with arbitrary values, we still can have s bounded from zero property.

4 Estimation

Two approaches (EM [3] and the marginal) will be provided in this section.

4.1 The EM Algorithm

4.1.1 E-Step:

Since (3) has an exact form of normal distribution, we can get the posterior mean of to be

and its posterior variance is

by the definition of normal pdf. Along with these, we also need to calculate the posterior second moment in our EM approach:

given and .

4.1.2 M-Step:

Note that directly minimizing (3) has computational difficulty, an alternative way is to maximize (2) under the condition where , and repeat the process in E-step.

We adopt an iterative method by firstly taking derivatives to (2) of all hospitals with respect to and .

Therefore, our iterative method in M step is

Once the Expectation-Maximization algorithm converges, we can update the latent variables by

. We repeat this procedure several times until every becomes stable.

In the M-step, the solutions of s, s and s are consistent regardless the choices for any initial values since

In the same time, the values of in the E-step also maximize the joint pseudo log-likelihood with respect to , and

suggests that (3) is convex for all the s, s and s.

Moreover, if we assume holds for some positive number of , then

| (8) |

holds for every indicator. Since by the result in M-step, the estimated value of is closed to (8) implies

holds. Thus we have at ,

Therefore, the EM approach is the same as the coordinate descent method, we can find the minimizer, for . [2]

4.2 The Marginal Pseudo Likelihood

Given as constant, conditional on , we can get the parameter estimates directly by maximizing (5), i.e.

then use the estimates to get all s by

and their posterior variances by

where . We implement this algorithm through the NLMIXED procedure in SAS.

5 Numerical Study

In this section, we study two cases based on measure-specific weights. The weights in every indicator are set to be mean equal to one for both cases at beginning. For every , the weights satisfy: are exponentially shaped (the extreme case) and are mounded shaped (the regular case) for We show that under the regular case, the latent variable gets consistent results where those results have been incorporated with the weight information. Under the extreme case, we demonstrate that by setting the sum of the weights less than the sample size in each indicator, or, equivalently, mean of each weights to be less than one, the estimates of s can be always bounded from zero. We can then get both the variables estimates as well as the variances estimates for all the latent variables. This is consistent with the results in section (3.2.2). We also compare the performance of the latent variable model with different sample sizes through our algorithm in the extreme case.

5.1 A Regular Case

Assume there are three indicators in the group, let the sample size , the inputs are generated through a multivariate normal distribution with mean zero and variance one, the correlation among each pair of two indicators is set as .

We firstly generate random numbers with Gamma distribution to get , where is the shape parameter, and is the scale parameter. For and , we separately generate random numbers with Gamma distribution of . Then we divide the by their sample means, respectively. Thus we get the sample mean of the weights of every indicator be the same, one.

We replicate the study based on the above setting for times, and focus on both average loading () and average standard deviation () for the three indicators in the result. For contrast, we also replicate the study for uniform weights times. Table 1 shows the results:

| Weight | No Weight | |||||||

|---|---|---|---|---|---|---|---|---|

| 0.8520 | 0.4801 | 0.7084 | 0.7057 | |||||

| 0.6675 | 0.7391 | 0.7080 | 0.7088 | |||||

| 0.6700 | 0.7356 | 0.7107 | 0.7053 | |||||

We can see with uniform weights, by design, all three indicators seem to have similar average loadings and average root mean squared errors. By Theorem 1, the result with uniform weights is the same as the confirmatory factor analysis with one factor. When there are weights which are moderately skewed, the average loading for the first indicator is larger than those of the second and the third. This is meaningful since although all three weights have the same mean, is more skewed than and . The maximum value in is larger than those of and . Thus the latent variable model can also output the result with different weights.

5.2 An Extreme Case

We use the same generating method for as section (5.1), where

And we use Gamma distributions with the shape parameters are smaller than the scale parameters to generate more skewed weights.

We firstly generate random numbers with Gamma distribution of to get For and , we separately generate random numbers with Gamma distributions of . Again, we divide the by their sample means, respectively. We will find as section 5.2 suggests, thus we focus on the result of here. To make comparison, we test the performances of latent variable model under and .

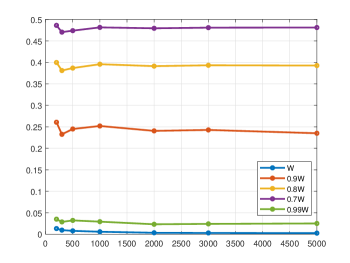

We compare the performance of all five weight matrices with sample size varies from to , we replicate the study times under each value of the sample size. Figure 1 shows the average values of .

Figure 1 shows that, with the original weights of means equal to one, the smallest average root mean squared error (ARMSE1) tends to be zero. However, the smaller the means of weights of the indicators, the larger the ARMSE1. As the sample size goes larger, the result of ARMSE1 tends to be stable. Therefore, if we have the mean of weights of the indicator to be smaller than one, we will prevent the s from being zero, then we can get the estimates of the posterior variances of the latent variables.

6 Data Analysis

We applied our latent variable model to the CMS’s Overall Hospital Quality Rating database from the CMS 2019 public data across the subjected States. This database consists seven indicator groups: Mortality; Readmission; Safety of Care (Safety); Patient Experience; Effectiveness; Timeliness and Image Efficiency. In this section, we first analyze two indicator groups in the three outcome groups: Mortality and Readmission. We will then discuss the group of Safety.

In each indicator group, hospital had the reported indicator scores. For each indicator, the scores from the available hospitals are standardized with mean zero and variance one. There also exist measure-specific weights (CMS calls them as the denominator weights) for the hospitals reflecting their volumes of admissions. Similar as sample weights, the mean of the denominator weights in every indicator is standardized as just below one. Note that those weights vary across both indicator level and hospital level, therefore, the latent variable model is appropriated for the data.

6.1 Mortality (regular)

For the group of mortality, seven indicators among hospitals are presented:

1. MORT-30-AMI: Acute Myocardial Infarction (AMI) 30-Day Mortality Rate;

2. MORT-30-CABG: Coronary Artery Bypass Graft (CABG) 30-Day Mortality Rate;

3. MORT-30-COPD: Chronic Obstructive Pulmonary Disease (COPD) 30-Day Mortality Rate;

4. MORT-30-HF: Heart Failure (HF) 30-Day Mortality Rate;

5. MORT-30-PN: Pneumonia (PN) 30-Day Mortality Rate;

6. MORT-30-STK: Acute Ischemic Stroke (STK) 30-Day Mortality Rate;

7. PSI-4-SURG-COMP: Death Among Surgical Patients with Serious Treatable Complications.

We apply both the EM approach and the marginal approach to the mortality data, and calculate the maximum absolute value of predicted the latent variables, the difference is only 2.2208e-04. This suggests that the EM and the marginal approach are identical. Table 2 shows the parameter estimates of the latent variable model. We found that the loadings are balanced across indicators, all the estimated variances are bounded from zero. This result is the same as the result from CMS via the SAS quadrature method. [10]

| Un-adj | Un-adj | Un-adj | |||

|---|---|---|---|---|---|

| 0.113 | 0.508 | 0.927 | |||

| 0.131 | 0.333 | 0.894 | |||

| 0.002 | 0.676 | 0.822 | |||

| 0.107 | 0.713 | 0.682 | |||

| -0.007 | 0.665 | 0.740 | |||

| -0.049 | 0.484 | 0.975 | |||

| -0.061 | 0.281 | 1.049 |

We also multiplied to all the weights in the mortality data, and we found there is no difference in the parameter estimates between and . Moreover, the rooted mean square error of the latent variable between the original weight and multiples the weight method is . Therefore, the times weights performs very closely to the method with un-adjusted weights in the mortality group.

6.2 Readmission (Extreme)

In the data of the readmission group, there are nine indicators among hospitals:

1. EDAC-30-AMI: Excess Days in Acute Care (EDAC) after hospitalization for Acute Myocardial Infarction (AMI);

2. EDAC-30-HF: Excess Days in Acute Care (EDAC) after hospitalization for Heart Failure (HF);

3. EDAC-30-PN: Excess Days in Acute Care (EDAC) after hospitalization for Pneumonia (PN);

4. OP-32: Facility 7-Day Risk Standardized Hospital Visit Rate after Outpatient Colonoscopy;

5. READM-30-CABG: Coronary Artery Bypass Graft (CABG) 30-Day Readmission Rate;

6. READM-30-COPD: Chronic Obstructive Pulmonary Disease (COPD) 30-Day Readmission Rate;

7. READM-30-Hip-Knee: Hospital-Level 30-Day All-Cause Risk-Standardized Readmission Rate (RSRR) Following Elective Total Hip Arthroplasty (THA)/Total Knee Arthroplasty (TKA);

8. READM-30-HOSP-WIDE: HWR Hospital-Wide All-Cause Unplanned Readmission;

9. READM-30-STK: Stroke (STK) 30-Day Readmission Rate.

After running the latent variable model, we found the estimated for the 30 day hospital-wide readmission indicator is zero. This is because in the indicator of 30 day hospital-wide readmission, the numbers of admissions varies from to , which are way larger than the rest indicators in the group. After standardization, the distribution of denominator weights are skewed much more heavily in 30 day hospital-wide readmission than the rest indicators. Thus we apply the method of times the weights to the 30 day hospital-wide readmission indicator, in order to force its standard error larger than zero, as well as keep the parameter estimates as close as possible. The result of parameter estimates is shown in Table 3.

| Un-adj | Adj | Un-adj | Adj | Un-adj | Adj | |||

|---|---|---|---|---|---|---|---|---|

| 0.031 | 0.031 | 0.316 | 0.318 | 0.710 | 0.710 | |||

| -0.175 | -0.175 | 0.427 | 0.430 | 0.748 | 0.747 | |||

| -0.243 | -0.243 | 0.410 | 0.413 | 0.775 | 0.774 | |||

| 0.198 | 0.198 | -0.002 | -0.002 | 1.228 | 1.228 | |||

| 0.106 | 0.106 | 0.303 | 0.304 | 1.024 | 1.024 | |||

| -0.068 | -0.067 | 0.522 | 0.525 | 0.972 | 0.971 | |||

| 0.194 | 0.194 | 0.388 | 0.390 | 1.043 | 1.042 | |||

| 0.000 | 0.001 | 0.975 | 0.978 | 0.000 | 0.056 | |||

| -0.051 | -0.051 | 0.499 | 0.502 | 0.983 | 0.982 |

We can see except for , all the parameters from the original weight and the adjusted weight methods have difference less than 0.001. Moreover, the 0.99 adjusted method can ensure all the variance in the readmission group bounded from zero. This is consistent with previous numerical and theoretical results.

6.3 Safety (Extreme)

Modeling the group of Safety has been challenging over the years by its unbalanced loadings and bi-peak parameter estimates through the latent variable modeling.

In the Safety of Care group, there are eight indicators among hospitals:

1. COMP-HIP-KNEE: Hospital-Level Risk-Standardized Complication Rate (RSCR) Following Elective Primary Total Hip Arthroplasty (THA) and Total Knee Arthroplasty (TKA);

2. HAI-1: Central-Line Associated Bloodstream Infection (CLABSI);

3. HAI-2: Catheter-Associated Urinary Tract Infection (CAUTI);

4. HAI-3: Surgical Site Infection from colon surgery (SSI-colon);

5. HAI-4: Surgical Site Infection from abdominal hysterectomy (SSI-abdominal hysterectomy);

6. HAI-5: MRSA Bacteremia;

7. HAI-6: Clostridium Difficile (C. difficile);

8. PSI-90-Safety: Complication/Patient Safety for Selected Indicators (PSI).

Similar to the readmission group, the safety group is also an extreme case since both COMP-HIP-KNEE and PSI-90-Safety indicators have much larger variance in numbers of admissions than the rest six indicators. After running the latent variable model with the un-adjusted sample weights, we found the loadings for HAI-1 to HAI-6 are closed to zero. This will cause the bi-peak issue of the parameter estimates since there are only two indicators loaded unto the latent factor, one or both of or can have zero variance. We provided two sets of methods to solve the issue in the safety group.

6.3.1 Solution One

One way to solve the problem is comparing the marginal pseudo log-likelihood between the two peaks. And we found when PSI-90-Safety () turned out to be zero, the marginal log-likelihood is larger. Similarly as the readmission group, we apply the methods of times weights (denoted by Adj) to both COMP-HIP-KNEE and PSI-90-Safety indicators. Table 4 shows the parameter estimates between the original weights and times weights in the Safety group. And Table 5 shows the root mean squared errors of the latent variable estimates between , , multiply weights method and the method of multiplying to the un-adjusted weights (since under the method of un-adjusted weights, the latent variable variances cannot be calculated).

| Un-adj | Adj | Un-adj | Adj | Un-adj | Adj | |||

|---|---|---|---|---|---|---|---|---|

| 0.287 | 0.287 | 0.188 | 0.189 | 1.039 | 1.039 | |||

| -0.007 | -0.007 | 0.007 | 0.007 | 0.723 | 0.723 | |||

| -0.010 | -0.010 | 0.008 | 0.008 | 0.757 | 0.757 | |||

| -0.055 | -0.055 | 0.045 | 0.046 | 0.837 | 0.837 | |||

| 0.010 | 0.010 | 0.060 | 0.060 | 0.867 | 0.867 | |||

| 0.032 | 0.032 | 0.037 | 0.037 | 0.796 | 0.796 | |||

| 0.003 | 0.003 | 0.025 | 0.025 | 0.622 | 0.622 | |||

| 0.016 | 0.016 | 0.897 | 0.901 | 0.000 | 0.033 |

| 0.99*W | 0.9*W | 0.8*W | 0.7*W | |

|---|---|---|---|---|

| RMSE | 0.0861 | 0.2123 | 0.3552 | |

| Mean | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Std | 0.8354 | 0.7711 | 0.6754 | 0.5604 |

We found that the parameters estimate are very closed between the original weight and adjusted weight, and as the weight coefficient decreases from 0.99 to 0.7, the standard error of the predicted latent variables is getting farther away from the prior variance (one).

6.3.2 Solution Two

Another idea of modeling the Safety group is smoothing the weights thus prevent the dominance of either COMP-HIP-KNEE and PSI-90-Safety. Consider the HAIs are similar in both admission volumes and indicator scores, this method is seeking a balanced loading from the latent variable model.

| log-W | log-W | log-W | |||

|---|---|---|---|---|---|

| 0.048 | 0.105 | 0.995 | |||

| 0.036 | 0.528 | 0.738 | |||

| 0.016 | 0.372 | 0.846 | |||

| 0.000 | 0.211 | 0.919 | |||

| 0.022 | 0.279 | 0.897 | |||

| 0.033 | 0.359 | 0.867 | |||

| 0.019 | 0.078 | 0.865 | |||

| 0.008 | 0.134 | 0.938 |

One option is taking logarithm transformation to the admission volume for all indicators in the Safety group. This will help to reduce the variance in skewness of the un-adjusted weights in the Safety group. The result is in Table 6. We can see that the loadings are balanced and there are more than three indicators with relatively high loadings in the latent variable. Thus taking logarithm to the admission volume in the Safety group can help make the result balanced and thus identifiable.

7 Summary and Discussion

We present a latent variable model that incorporates measure-specific sample weights via pseudo-likelihood estimation in this work. The latent variable model can handle the missing value issue as well.

The estimates obtained through the algorithms have desirable asymptotic properties. We gave examples in both numerical study and real data analysis where the latent variable model can produce zero standard error estimates for certain indicators. We showed that if the sample weights means of those indicators are less than one, the estimates of variance components are bounded away from zero. We provided a log transformation method prior to the sample weights can help to obtain nonzero variance components as well.

For future work, we plan to investigate the pseudo likelihood and the estimating algorithm of the latent variable model under random weights with Gamma distribution, thus we can discover the threshold between the choice of the shape (scale) parameters and the bounded-away-from-zero estimates of variance components. Moreover, we would also like to investigate more behaviors of the latent variable model under varies distributions of weights, such as Poisson distribution, beta distribution, etc.

References

- [1] Agostinelli, C. and Greco, L. (2013). A weighted strategy to handle likelihood uncertainty in bayesian inference. Computational Statistics, 28(1):319–339.

- [2] Daubechies, I., Defrise, M., and De Mol, C. (2004). An iterative thresholding algorithm for linear inverse problems with a sparsity constraint. Communications on Pure and Applied Mathematics: A Journal Issued by the Courant Institute of Mathematical Sciences, 57(11):1413–1457.

- [3] Dempster, A. P., Laird, N. M., and Rubin, D. B. (1977). Maximum likelihood from incomplete data via the em algorithm. Journal of the Royal Statistical Society: Series B (Methodological), 39(1):1–22.

- [4] Henderson, C. R. (1975). Best linear unbiased estimation and prediction under a selection model. Biometrics, pages 423–447.

- [5] Landrum, M. B., Bronskill, S. E., and Normand, S.-L. T. (2000). Analytic methods for constructing cross-sectional profiles of health care providers. Health Services and Outcomes Research Methodology, 1(1):23–47.

- [6] Muthen, B. and Asparouhov, T. (2013). New methods for the study of measurement invariance with many groups. Mplus (www. statmodel. com).

- [7] Shwartz, M., Ren, J., Peköz, E. A., Wang, X., Cohen, A. B., and Restuccia, J. D. (2008). Estimating a composite measure of hospital quality from the hospital compare database: differences when using a bayesian hierarchical latent variable model versus denominator-based weights. Medical care, 46(8):778–785.

- [8] Thompson, B. (2007). Factor analysis. The Blackwell Encyclopedia of Sociology.

- [9] Veiga, A., Smith, P. W., and Brown, J. J. (2014). The use of sample weights in multivariate multilevel models with an application to income data collected by using a rotating panel survey. Journal of the Royal Statistical Society: Series C (Applied Statistics), 63(1):65–84.

- [10] Venkatesh, A., Bernheim, S., Hsieh, A., et al. (2016). Overall hospital quality star ratings on hospital compare methodology report (v2. 0).

- [11] Yong, A. G. and Pearce, S. (2013). A beginner’s guide to factor analysis: Focusing on exploratory factor analysis. Tutorials in quantitative methods for psychology, 9(2):79–94.

8 Appendix

We organize this section as: (8.1) and (8.2) are the proof to Example 1, (8.3) is the proof to Theorem 1, (8.4) is the proof to Theorem 2.

Recall that For any hospital , there are indicators. Assume there exists an overall latent score from the indicators, conditional on its score, each indicator has an independent normal distribution with

where is the response for the th indicator in hospital . and are unknown parameters.

We also assume has a normal distribution with mean zero and variance one. We have, by the logged pdf of normal distribution, We have the marginal logarithm marginal likelihood for all the parameters for hospital in the safety domain satisfies

8.1 Asymptotic Behavior of LVM

We start with . Based on the marginal log-likelihood with uniform weight, we have negative marginal log-likelihood for hospital satisfies

Let

then we have

| (9) |

and the expected negative marginal log-likelihood for hospitals (denoted by ) is

| (10) |

Recall our model is

by strong law of large numbers, we have

| (11) |

holds for . Also note that

| (12) |

holds for .

holds for sufficient large . Therefore, we have

as .

8.2 Multivariate Normal Distribution

Let , moreover, assume the covariance between and is . Then we can have the Variance co-variance matrix of is:

we can show that the determinant of satisfies

and we have

let and , thus we have the negative joint log-likelihood of multivariate normal distribution for hospital satisfies

Denote , by matrix calculation, we have

Since the only difference between and is the notation . Therefore, we have for any hospital , the negative multivariate log-likelihood is equal to the negative marginal log-likelihood, since they are both negative log-likelihoods.

8.3 generalized LVM

We can generalize the latent variable mode with uniform weight from indicators into indicators. Note that, with a distance of ,

By (11) and (12), for sufficient large , we have, with indicators,

Note that

by symmetry,

which implies

Therefore, we have, for indicators

| (13) |

Furthermore, denote the right hand side of (13) by , and the 4th moment of each exists since each has a normal distribution, then by Lindeberg–Lévy central limit theorem,

holds as , since convergence almost surely for every fixed positive integer , and

where

8.4 Weighted LVM

Let the weight matrix where , are positive constants. And

Then by definition of NMLL, we have the marginal log-likelihood for hospital satisfies

By Theorem 2,

Therefore, we have, the expected negative pseudo marginal log-likelihood () for indicators satisfies

as . Similarly, the condition for Lindeberg–Lévy central limit theorem holds for NWMLL with every .