∎

22email: jean-philippe.aguilar@covea-finance.fr

The value of power-related options under spectrally negative Lévy processes

Abstract

We provide analytical tools for pricing power options with exotic features (capped or log payoffs, gap options etc.) in the framework of exponential Lévy models driven by one-sided stable or tempered stable processes. Pricing formulas take the form of fast converging series of powers of the log-forward moneyness and of the time-to-maturity; these series are obtained via a factorized integral representation in the Mellin space evaluated by means of residues in or . Comparisons with numerical methods and efficiency tests are also discussed.

Keywords:

Lévy Process Stable Distribution Tempered Stable Distribution Digital option Power option Gap option Log optionMSC:

60E07 60G51 60G52 62P05 91G201 Introduction

Spectrally negative Lévy processes are Lévy processes (see the classical textbook Bertoin96 for a complete introduction to the theory of Lévy processes, and, among many other references, Geman02 ; Schoutens03 ; Cont04 ; Tankov11 for their applications in financial modeling) whose Lévy measure is supported by the real negative axis, i.e., processes without positive jumps Kuznetsov12 ; they include Brownian motion with drift, asymmetric -stable Zolotarev86 ; Carr03 or asymmetric tempered-stable Carr02 ; Poirot06 processes and their particular cases, such as negative Gamma and Inverse Gaussian processes. Such one-sided processes have been shown to be effective for modeling the price of financial assets, because their heavy-tail induces a leptokurtosis in the distribution of returns (whose empirical evidence is known since Fama65 ), and their skewed behavior introduces the asymmetry in the occurrence of upward and downward jumps (see Carr03 ; Madan08 ; Eberlein10 for more recent discussions and justifications). Moreover, in the context of exponential market models Schoutens03 ; Cont04 , they generate a wide range of dynamics for the log returns, from almost surely continuous trajectories in the Brownian motion case Black73 , to highly discontinuous realizations with a potentially infinite number of downward jumps on any given time interval.

For the specific purpose of option pricing, spectrally negative Lévy processes have been introduced in Carr03 in the case of a totally skewed -stable dynamics, the strong asymmetry of the model combined with the presence of fat tails capturing volatility patterns for longer observable horizons more accurately than Gaussian models. They have subsequently been employed in the calibration of index options on some major equity indices (it is shown in Eberlein10 that positive jumps are not needed for long term options on most index markets); concerning path-dependent instruments, the impact of one-sided Lévy dynamics on Asian and Barrier options has also been investigated Patie13 ; Avram02 . Let us also mention that spectrally negative Lévy processes have been successfully applied in other areas of Quantitative Finance, notably in default modeling and credit exposure Madan08 , as the default of a firm is often linked to brutal losses in their assets’ value.

When it comes to practical evaluation however, things are more complicated under Lévy dynamics than in the usual Black-Scholes framework; the literature is dominated by numerical (finite difference) schemes for Partial Integro-Differential Equations Cont05 , by Monte Carlo simulations Poirot06 or Fourier transforms of option prices Carr99 . The latter approach is particularly popular, because in most exponential Lévy models, the characteristic function of the asset’s log price is available in a closed and relatively compact form; several refinements of the method have been introduced to accelerate the evaluation of Fourier integrals, notably by means of other integral transforms (among others, Fourier-cosine transform Fang08 or Hilbert transform Feng08 ) or, more recently, by application of frame duality properties Kirkby15 . Let us also mention that, in the case of European style options with non standard terminal payoffs, it is also possible to use an integral representation decomposing the contract into a sum of standard contracts (see Carr01 ) and to evaluate numerically the involved integrals, at least for smooth (twice differentiable) payoffs. For discontinuous payoffs, it is advantageous to refine this approach by assembling a series of selected payoffs and by using the theory of frames, as developed in Kirkby19 .

In this paper, we would like to take profit of the properties of another Fourier-related transform, namely the Mellin transform Flajolet95 . First, let us mention that the Mellin transform has been previously implemented in many areas of financial modeling, from providing representations for vanilla or basket options in the Black-Scholes model Panini04 , to quantifying the at-the-money implied volatility slope in various Lévy models Gerhold16 . In our approach, we will focus on expressing Mellin integrals as a sum of residues in or , so as to obtain simple series expansions for option prices. More precisely, we will show that, in the framework of exponential Lévy models driven by spectrally negative processes, option prices have a factorized form in the Mellin space (in terms of maturity and log-forward moneyness); inverting the transform, the prices can be conveniently computed by a straightforward series of residues, allowing for a very simple and fast evaluation of the options.

The Mellin residue technique has been used to derive fast convergent series for European options prices and Greeks, in the Black-Scholes Aguilar19 and Finite Moment Log Stable (FMLS) AK19 models; in this article, we will show that the technique successfully applies to a more general range of exotic power-related options (Digital, Log, Gap, European with cap etc.). This family of options offers a higher (and nonlinear) payoff than the vanilla options; it is used e.g. to increase the leverage ratio of strategies, or to lock the exposition to future volatility (see discussion in Tompkins98 ). From a more theoretical point of view, power payoffs have also been employed to determine the Lévy symbol of the underlying asset dynamics in Bouzianis19 . In the Gaussian context, closed formulas for pricing and hedging standard power options are known since Heynen96 , and have been recently generalized to include some barrier features Ibrahim13 ; studies have also been made in the setup of local volatility models, or for more generic polynomial options (decomposed a sum of power options) in Macovschi06 . The present paper will be devoted to establishing efficient pricing formulas in the context of an asymmetric -stable exponential Lévy model, and to show that it is possible to extend them to the more generic class of tempered stable processes.

The paper is organised as follows: in section 2 we start by recalling some basic facts about option pricing in exponential Lévy models; then, in section 3, we establish a factorized form for option prices in the case of a spectrally negative -stable dynamics. This factorized form enables us to derive several pricing formulas for power-related instruments in section 4, under the form of fast convergent series of powers of the time-to-maturity and of the moneyness; in this section, we also test the results numerically, and provide efficiency tests. In section 5, we show that similar formulas can also be derived if the stable distribution is tempered, and study the impact of the tempering parameter in the case of a digital option. Finally, section 6 is devoted to concluding remarks and perspectives.

2 Option pricing in exponential Lévy Models

2.1 Model specification

Notations.

Given a filtered probability space , recall that a process is a Lévy process Bertoin96 ; Kyprianou13 if there exists a triplet such that the characteristic exponent of admits the representation

| (1) |

where and is a measure concentrated on satisfying

| (2) |

Equation (1) is known as the Lévy-Khintchine formula; is the drift, is the Brownian (or diffusion) coefficient and is the Lévy measure of the process.

If , one speaks of a process with finite activity or intensity; this corresponds to processes whose realizations have a finite number of jumps on every finite interval, like in jump-diffusion models such as the Merton model Merton76 or the Kou model Kou02 . If , then one speaks of a process with infinite activity or intensity, and in this case an infinite number of jumps occur on every finite interval; this gives birth to a very rich dynamics and such processes do not need a Brownian component to generate complex behaviors. When furthermore (resp. ), the process is said to be spectrally negative (resp. spectrally positive).

As a Lévy process has stationary independent increments, its characteristic function can be written down as

| (3) |

and its moment generating function, whenever it converges, as:

| (4) |

The function is the Laplace exponent or cumulant generating function of the process, and its existence depends on the asymptotic behavior of the Lévy measure; in particular, in the case of a spectrally negative process, the absence of positive fat tail ensures that exists in the whole complex half-plane .

Exponential processes.

Let us now introduce the class of exponential Lévy models, following the classical setup of Schoutens03 ; Cont04 for instance. Let , and let denote the value of a financial asset at time ; we assume that it can be modeled as the realization of a stochastic process on the canonical space equipped with its natural filtration, and that, under the risk-neutral measure , its instantaneous variations can be written down in local form as:

| (5) |

In the stochastic differential equation (5), is the risk-free interest rate and is the dividend yield, both assumed to be deterministic and continuously compounded, and is a Lévy process; for the simplicity of notations, we will assume that , but all the results of the paper remain valid when replacing by .

The solution to (5) is the exponential Lévy process defined by:

| (6) |

where is the horizon (or time-to-maturity), and is the martingale (or convexity) adjustment computed in a way that the discounted stock price is a -martingale, which reduces to the condition:

| (7) |

or, equivalently, in terms of the Laplace exponent:

| (8) |

2.2 Option pricing

Let and be a non time-dependent payoff function depending on the terminal price and on some positive parameters , :

| (9) |

The value at time of an option with maturity and payoff is equal to the risk-neutral conditional expectation of the discounted payoff:

| (10) |

In the case where the Lévy process admits a density , then, using (6), we can re-write (10) by integrating all possible realizations for the terminal payoff over the probability density:

| (11) |

In all the following and to simplify the notations, we will forget the dependence in the stock price .

3 Spectrally negative -stable process (FMLS process)

3.1 Lévy-stable process

A Lévy-stable process Samorodnitsky94 ; Zolotarev86 is a Lévy process whose Lévy-Khintchine triplet has the form , with:

| (12) |

where and . It is known that, introducing and defined by

| (13) |

then for the characteristic exponent of the process admits the Feller parametrization:

| (14) |

for some constant (see, for instance, exercise 1.4 in the textbook Kyprianou13 ). A Lévy-stable process can therefore be represented as a 4-parameter process ): controls the behavior of the tails and their asymmetry, is a scale parameter, and is a location parameter. In particular, when then it follows from (14) that equals the mean .

It is interesting to note that when and then the characteristic function (14) degenerates into the characteristic function of the centered normal distribution:

| (15) |

and therefore the Black-Scholes model is a particular case of a Lévy-stable model for .

3.2 Fully asymmetric process

It follows from the definition of the Lévy measure (12), that the moment generating function of a Lévy-stable process exists if and only if , or equivalently that is, in the case of a spectrally negative Lévy-stable process, because it has only one fat-tail located in the real negative axis; one also speaks of a fully asymmetric process, and the condition is known as the maximal negative asymmetry hypothesis. In this context, choosing (process with zero mean), we have:

| (16) |

which is valid for . It follows from definition (8) that the martingale adjustment reads:

| (17) |

It is in Carr03 that an exponential Lévy model (5) for a process being a spectrally negative Lévy-stable process was first introduced for the purpose of option pricing. The authors gave it the name of Finite Moment Log Stable (FMLS) process, in reference to the existence of the cumulant generating function in this case. Note that the process has infinite activity, the integral of the stable measure being divergent in .

3.3 Self-similarity and option pricing

We now derive a Mellin-Barnes representation for the density of the FMLS process, and for the corresponding option price that we will denote by .

Lemma 1

Let , and . Then the density of the process admits the following Mellin-Barnes representation:

| (18) |

where and .

Proof

Using eqs. (16) and (17) and the Laplace inversion formula, we have:

| (19) |

where . Taking the Mellin transform and making the change of variables , we have:

| (20) |

for any . The remaining -integral is equal to on the condition that (see for instance Bateman54 or any monograph on Laplace transform); observe that, as , the two conditions on reduce to . Finally, the integral (18) is obtained by applying the Mellin inversion formula Flajolet95 and by changing the variable . ∎

Equation (18) shows that the density is a function of the ratio , which is actually a consequence of the self-similarity property Embrechts00 of stable processes (a scaling of time is equivalent to an appropriate scaling of space). This property allows for a nice factorization of the option price in the Mellin space; indeed, let us denote

| (21) |

and

| (22) |

and let us assume that the integral (22) converges for for some real numbers . Then, as a direct consequence of the pricing formula (11) and of lemma 1, we have:

Proposition 1 (Factorization in the Mellin space)

Let where is assumed to be nonempty. Then, under the hypothesis of lemma 1, the value at time of an option with maturity and payoff is equal to:

| (23) |

The factorized form (23) turns out to be a very practical tool for option pricing. Indeed, as an integral along a vertical line in the complex plane, it can be conveniently expressed as a sum of residues associated to the singularities of the integrand. As Gamma functions are involved, we can control the behavior of the integrand when the contour goes to infinity by using the Stirling asymptotic formula for the Gamma function Abramowitz72 : if , , , are real numbers, if and if then

| (24) |

when , and the same holds for if . Therefore, by right or left closing the contour of integration in (23), the option price will take the form of a series:

| (25) |

The only technical difficulty will in fact lie in the evaluation of : depending on the payoff’s complexity, it can be either computed directly, or via the introduction of a second Mellin complex variable .

4 Power payoffs in a spectrally negative -stable environment

In all this section, , , and ; the log-forward moneyness is defined to be:

| (26) |

and we will use the standard notation .

4.1 One complex variable payoffs

Digital power options (cash-or-nothing).

The call’s payoff is:

| (27) |

Proposition 2

The value at time of a digital power cash-or-nothing call option is:

| (28) |

Proof

As we can write:

| (29) | |||||

then, with the notation (22), the function reads:

| (30) |

for . Using proposition 1 and the functional relation , the option price is:

| (31) |

which converges for . We can note that:

| (32) |

is negative because , thus, it follows from the Stirling formula (24) that the analytic continuation of the integrand vanishes at infinity in the right half plane. Therefore, the integral (31) equals the sum of residues at the poles located in this half plane; these poles are induced by the term at every positive integer , and the associated residues are:

| (33) |

Simplifying and summing all residues yields (28).∎

Log power options.

These options were introduced in Wilmott06 in the case , and are basically options on the rate of return of the underlying asset. The call’s payoff is:

| (34) |

Proposition 3

The value at time of a Log power call option is:

| (35) |

Proof

As we can write:

| (36) |

then the function reads:

| (37) |

for . Using proposition 1 and the functional relation , the option price is:

| (38) |

which converges for . Again, , and the analytic continuation of the integrand in the right half-plane has:

-

•

a simple pole in with residue

(39) -

•

a series of poles at every positive integer with residues:

(40)

Summing the residues (39) and (40) for all and re-ordering yields (35).∎

Capped power options (cash-or-nothing).

For , the call’s payoff is:

| (41) |

Let us define . We have:

Proposition 4

The value at time of a capped cash-or-nothing call option is:

| (42) |

4.2 Two complex variables payoffs

Digital power options (asset-or-nothing).

The call’s payoff is:

| (46) |

Proposition 5

The value at time of a digital power asset-or-nothing call option is:

| (47) |

Proof

We can write:

| (48) |

Introducing a Mellin-Barnes representation for the exponential term:

| (49) |

for and integrating over the variable, the function reads:

| (50) |

and converges for in the triangle . From proposition 1, the option price is:

| (51) |

Poles of the integrand occur when and are singular; performing the change of variables , allows to compute the associated residues, which read:

| (52) |

Simplifying and summing the residues yields the series (47). The fact that one can close the contour in (51) is a consequence of the multidimensional generalization of the Stirling estimate (24) (see Passare97 or the appendix of Aguilar19 for details).∎

Gap power options.

A gap option Tankov10 offers a nonzero payoff on the condition that a trigger price is attained at . More precisely, the call’s payoff is:

| (53) |

where is the strike price and the trigger price; if the trigger is lower than the strike then a negative payoff is possible (which would not be the case with a classical knock-in barrier). From the definition of the payoff (53), the value of the gap call option is equal to:

| (54) |

European power options.

The classical European power option is a gap power option with equal strike and trigger prices (); the payoff therefore reads

| (55) |

Observing that (28) is actually a particular case of (47) for , it follows immediately from (54) that the value of the European power call is:

| (56) |

When the asset is at-the-money (ATM) forward, that is when , or, equivalently, , then (56) becomes:

| (57) |

In particular, if we choose and the normalization in the definition of the martingale adjustment (17), then (57) reads:

| (58) | |||||

which is the well-known approximation for the ATM Black-Scholes call.

Capped power options (asset-or-nothing, European).

For , the payoff of a capped power asset-or-nothing call is:

| (59) |

The presence of a cap allows the seller to protect themselves against the eventuality of enormous payoffs; using the identity (43) for the indicator function, and proceeding in a similar way than for proving proposition 5, we obtain:

Proposition 6

The value at time of a capped power asset-or-nothing call option is:

| (60) |

The value of the capped European power option is easily deduced from the values of the capped cash-or-nothing (42) and asset-or-nothing (60) options:

| (61) |

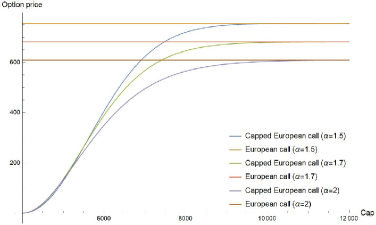

When , the value of the capped option (61) coincides with the classical uncapped option (56); this situation is displayed in figure 1. We can observe that the convergence to the uncapped price is quicker when decreases, which is no surprise given the overall factor.

4.3 Numerical tests

In this subsection, we benchmark the pricing formulas established in the previous sections by comparing them with the formulas available in the cases , (i.e., in the Black-Scholes setup); we also provide comparisons with numerical evaluation of Fourier integrals when . Except otherwise stated, we choose , , , years and we make the normalization in the martingale adjustment (17), so as to recover the Black-Scholes adjustment when .

Log options

When and , a closed pricing formula exists for the Log option Haug07 :

| (62) |

where , is the Gaussian density and is the Normal cumulative distribution function. In table 1, we compare this formula to various truncations of the series (35) for and , in several market situations (out-of-the money, at-the-money and in-the-money).

| Formula (62) | ||||

|---|---|---|---|---|

| 0.238691 | 0.237465 | 0.237525 | 0.237525 | |

| 0.125287 | 0.125286 | 0.125286 | 0.125286 | |

| ATM | 0.092106 | 0.092104 | 0.092104 | 0.092104 |

| 0.079177 | 0.079158 | 0.079158 | 0.079158 | |

| 0.025250 | 0.018797 | 0.019488 | 0.019487 |

Power options ()

For , recall the formula by Heynen and Kat Heynen96 for European power options in the Black-Scholes setup:

| (63) |

where

| (64) |

In table 2, values obtained with formula (63) are compared to various truncations of the series (56), for various powers and in the ATM situation. The convergence is very fast; of course if one is far from the money, the convergence becomes slightly slower because the moneyness grows when (for instance, if , but and ), and therefore the powers in the numerator are less quickly neutralized by the factorial/Gamma terms of the denominator.

| Heynen & Kat (62) | ||||

|---|---|---|---|---|

| 439.65 | 440.93 | 440.94 | 440.94 | |

| 723.00 | 729.86 | 730.06 | 730.06 | |

| 1057.71 | 1080.49 | 1081.64 | 1081.64 | |

| 1908.17 | 2034.41 | 2049.37 | 2049.39 |

European options ()

As a consequence of the Gil-Pelaez inversion formula for the characteristic functions, the price of an European call can be decomposed into a sum of Arrow-Debreu securities of the form (see details e.g. in Bakshi00 ):

| (65) |

The price of each security can be expressed in terms of the stable characteristic function and of the log-forward moneyness Lewis01 :

| (66) |

and

| (67) |

where is the risk-neutral characteristic function

| (68) |

satisfying the martingale condition . Given the simple form of the stable characteristic exponent (14), the integrals in (66) and (67) can be carried out very easily via a classical recursive algorithm on the truncated integration region (typically, is sufficient for a precision goal of ). In table 3, we compare the values obtained with this method with several truncations of the series (56), for a tail-index .

| Gil-Pelaez (65) | |||||

| Long term options () | |||||

| 1302.92 | 1309.86 | 1309.86 | 1309.86 | 1309.86 | |

| 679.32 | 681.56 | 681.56 | 681.56 | 681.56 | |

| ATM | 496.87 | 498.07 | 498.07 | 498.07 | 498.07 |

| 425.76 | 426.44 | 426.44 | 426.44 | 426.44 | |

| 128.50 | 92.46 | 96.50 | 96.50 | 96.50 | |

| Short term options () | |||||

| 1089.70 | 1075.64 | 1075.63 | 1075.63 | 1075.63 | |

| 383.17 | 383.30 | 383.30 | 383.30 | 383.30 | |

| ATM | 230.47 | 203.49 | 203.49 | 203.49 | 203.49 |

| 143.53 | 143.09 | 143.09 | 143.09 | 143.09 | |

| 211.44 | -27.24 | 1.04 | 1.39 | 1.39 | |

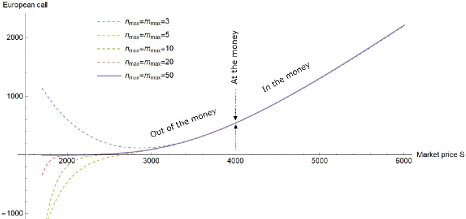

Like before, the convergence is very fast, and goes even faster in the ITM region; this is because the log-forward moneyness (26) is positive in this zone, and therefore, as , is closer to than in the OTM zone, which accelerates the convergence of the series (56). This situation is displayed in figure 2.

5 Extension to one-sided tempered stable processes

Tempered stable Lévy processes, which are known in Physics as truncated Lévy flights, combine -stable and Gaussian trends, and are an alternative solution to achieve finite moments (see details and further references in Rosinski07 ). Their Lévy-Khintchine triplet has the form where

| (69) |

for , and . When and , we recover the CGMY process Carr02 (sometimes named classical tempered stable process) and when furthermore , the Variance Gamma process Madan98 . In the case where , there is no more tempering and the process is simply a Lévy-stable process like in section 3. When , the Laplace exponent of the tempered stable process can be easily computed: for one has

| (70) |

where is a constant depending on the drift and the choice of truncation function for the characteristic function of the process; without loss of generality we choose it to be equal to .

5.1 Tempered stable densities

Let us denote by (resp. ) the negative (resp. positive) part of the Lévy measure (69), and by the associated one-sided tempered stable processes.

Lemma 2

Let and .

-

(i)

If , then its density admits the Mellin-Barnes representation:

(71) for any ;

-

(ii)

If , then its density admits the Mellin-Barnes representation:

(72) for any .

5.2 Option pricing for negative tempered stable processes

Let and ; from definition (8) and the Laplace exponent (70), the martingale adjustment reads:

| (75) |

where corresponds to the FMLS martingale adjustment (16), and as expected when . From the pricing formula (11) and using the notation (21) and (22), the value at time of an option with maturity and payoff is equal to:

| (76) |

where we have defined

| (77) |

and where is given by (75). The function can be expressed in terms of the function (22) by introducing a Mellin-Barnes representation for the exponential term:

| (78) |

for , and therefore, replacing in (76), we obtain:

Proposition 7 (Factorization)

If and if , then the value at time of an option with maturity and payoff is equal to

| (79) |

Example: digital power option (cash-or-nothing)

In that case, we know from (30) that:

| (80) |

where , and therefore it follows from (79) that the digital cash-or-nothing call reads:

| (81) |

The double integral (81) has a simple pole in with residue , and a series of simple poles in , induced by the singularities of the and functions. Summing all these residues yields:

| (82) |

Note that when , only the terms for survive and (82) degenerates into the -stable price (28), as expected. In the ATM forward case (=0), the first few terms of the series (82) read:

| (83) |

and can be Taylor-expanded for small :

| (84) |

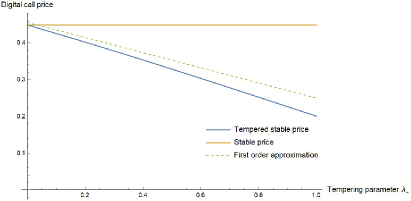

In the linear approximation (84), the intercept is the stable price, while the slope is governed by the negative left tail parameter ; the tempered stable price is therefore lower than the stable price (which is due to the tempering of the heavy tail), and the difference increases when grows. This situation is displayed on fig. 3 for , , , , , the series (28) and (82) being truncated to .

6 Conclusions and future work

In this article, we have derived generic representations in the Mellin space for path-independent options with arbitrary payoff, in the setup of exponential Lévy models driven by spectrally negative stable or tempered stable processes. These representations have allowed us to obtain simple series expansions for the price of options with an exotic power-related payoff (Power Digital, Log or Gap Power options, Capped Power European options), by means of residue summation in or . These series contain only simple terms and converge very fast, in particular when calls are in-the-money and for longer maturities; they can be very easily used for practical evaluation without requiring any help from numerical schemes.

Future work will include the investigation of path-dependent options, like Barrier or Lookback options; spectrally negative -stable processes are particularly interesting in this context, because the law of the supremum on a period of time is known to be Bingham73 :

| (85) |

which generalizes the reflection principle for the Wiener process (). Regarding path-independent instruments, the extension of the Mellin residue technique to two-sided Lévy processes is currently in progress, with a particular focus on the Variance Gamma and the Normal Inverse Gamma (NIG) processes; the technique is very well adapted to these models too, because, like in the spectrally negative case, their density functions can be expressed under the form of Mellin integrals. Ongoing work also includes the extension of the pricing formulas obtained for the one sided tempered stable process in the case of digital (cash-or-nothing) options, to the more general case of European options.

Acknowledgements.

The author thanks an anonymous reviewer for his/her insightful comments and suggestions.Conflict of interest

The authors declares that he has no conflict of interest.

References

- (1) Abramowitz, M. and Stegun, I., Handbook of Mathematical Functions, Dover Publications, Mineola, NY (1972)

- (2) Aguilar, J. Ph., On expansions for the Black-Scholes prices and hedge parameters, J. Math. Anal. Appl. 478(2), 973-989 (2019)

- (3) Aguilar, J. Ph. and Korbel, J., Simple Formulas for Pricing and Hedging European Options in the Finite Moment Log-Stable Model, Risks 7, 36 (2019)

- (4) Avram, F., Chan, T. and Usabel, M., On the valuation of constant barrier options under spectrally one-sided exponential Lévy models and Carr’s approximation for American puts, Stochastic Processes and their Applications 100, 75-107 (2002)

- (5) Bakshi, G. and Madan, D., Spanning and derivative-security valuation, Journal of Financial Economics 55, 205-238 (2000)

- (6) Bateman, H., Tables of Integral Transforms (vol. I and II), McGraw-Hill Book Company, New York (1954)

- (7) Bertoin, J., Lévy Processes, Cambridge University Press, Cambridge, New York, Melbourne (1996)

- (8) Bingham, N. H., Maxima of sums of random variables and suprema of stable processes, Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete, Vol. 26 Issue 4, Springer, Berlin, Heidelberg (1973)

- (9) Black, F. and Scholes, M., The Pricing of Options and Corporate Liabilities, Journal of Political Economy 81(3), 637-654 (1973)

- (10) Bouzianis, G. and Hughston, L. P., Determination of the Lévy Exponent in Asset Pricing Models, arXiv:1811.07220 (2019)

- (11) Carr, P. and Madan, D., Option valuation using the fast Fourier transform, Journal of Computational Finance 2, 61-73 (1999)

- (12) Carr, P. and Madan, D., Optimal positioning in derivative securities, Quantitative Finance 1, 19-37 (2001)

- (13) Carr, P., Geman, H., Madan, D., Yor, M., The Fine Structure of Asset Returns: An Empirical Investigation, Journal of Business 75(2), 305-332 (2002)

- (14) Carr, P. and Wu, L., The Finite Moment Log Stable Process and Option Pricing, The Journal of Finance 58(2), 753-777 (2003)

- (15) Cont, R. and Tankov, P., Financial Modelling with Jump Processes, Chapman & Hall, New York (2004)

- (16) Cont, R. and Voltchkova, E., A Finite Difference Scheme for Option Pricing in Jump Diffusion and Exponential Lévy Models, SIAM J. Numer. Anal. 43(4), 1596-1626 (2005)

- (17) Eberlein, E. and Madan, D., Short Positions, Rally Fears and Option Markets, Applied Mathematical Finance 17(1), 83-98 (2010)

- (18) Embrechts, P. and Maejima, M., An introduction to the theory of selfsimilar stochastic processes, International Journal of Modern Physics B14, 1399-1420 (2000)

- (19) Fama, E., The behavior of stock market prices, Journal of Business 38, 34-105 (1965)

- (20) Fang, F. and Oosterlee, C. W., A Novel Pricing Method for European Options Based on Fourier-Cosine Series Expansions, SIAM Journal on Scientific Computing 31, 826-848 (2008)

- (21) Feng, L. and Linetsky, V., Pricing Discretely Monitored Barrier Options and Defaultable Bonds in Lévy Process Models: a Fast Hilbert Transform Approach, Mathematical Finance 18(3), 337-384 (2008)

- (22) Flajolet, P., Gourdon, X. and Dumas, P., Mellin transforms and asymptotics: Harmonic sums, Theoretical Computer Science 144, 3-58 (1995)

- (23) Geman, H., Pure jump Lévy processes for asset price modelling, Journal of Banking Finance 26, 1297-1316 (2002)

- (24) Gerhold, S., Gülüm, C. and Pinter, A., Small-Maturity Asymptotics for the At-The-Money Implied Volatility Slope in Lévy Models, Applied Mathematical Finance 23(2), 135-157 (2016)

- (25) Haug, E.G., The Complete Guide to Option Pricing Formulas, McGraw-Hill Book Company, New York (2007)

- (26) Heynen, R. and Kat, H., Pricing and hedging power options, Financial Engineering and the Japanese Markets 3(3), 253-261 (1996)

- (27) Ibrahim, S. N. I., O’Hara, J. and Constantinou, N., Risk-neutral valuation of power barrier options, Applied Mathematics Letters 26(6), 595-600 (2013)

- (28) Kirkby, J. L., Efficient Option Pricing by Frame Duality with the Fast Fourier Transform, SIAM Journal on Financial Mathematics 6(1), 713-747 (2015)

- (29) Kirkby, J. L. and Deng, S. J., Static hedging and pricing of exotic options with payoff frames, Mathematical Finance 29(2), 612-658 (2019)

- (30) Kou, S., A jump-diffusion model for option pricing, Management Science 48, 1086-1101 (2002)

- (31) Kuznetsov, A., Kyprianou, A. E., Rivero, V., The Theory of Scale Functions for Spectrally Negative Lévy Processes, Lecture Notes in Mathematics vol. 2061, Springer, Berlin, Heidelberg (2011)

- (32) Kyprianou, A. E., Fluctuations of Lévy Processes with Applications, Springer, Berlin, Heidelberg (2013)

- (33) Lewis, A.L., A simple option formula for general jump-diffusion and other exponential Lévy processes, Available at SSRN: https://ssrn.com/abstract = 282110 (2001)

- (34) Macovschi, S. and Quittard-Pinon, F., On the Pricing of Power and Other Polynomial Options, The Journal of Derivatives 13(4), 61-71 (2006)

- (35) Madan, D., Carr, P., Chang, E., The Variance Gamma Process and Option Pricing, European Finance Review 2, 79-105 (1998)

- (36) Madan, D. and Schoutens, W., Break on Through to the Single Side, Working Paper, Katholieke Universiteit Leuven (2008)

- (37) Merton, R., Option pricing when underlying stock returns are discontinuous, Journal of Financial Economics 3, 125-144 (1976)

- (38) Panini, R. and Srivastav, R. P., Option Pricing with Mellin Transforms, Mathematical and Computer Modeling 40, 43-56 (2004)

- (39) Passare, M., Tsikh, A. and Zhdanov, O., A multidimensional Jordan residue lemma with an application to Mellin-Barnes integrals, Aspects of Mathematics vol. E26, Springer, Berlin, Heidelberg (1997)

- (40) Patie, P., Asian Options Under One-Sided Lévy Models, Journal of Applied Probability 50(2), 359-373 (2013)

- (41) Poirot, J. and Tankov, P., Monte Carlo Option Pricing for Tempered Stable (CGMY) Processes, Asia-Pacific Financial Markets 13, 327-344 (2006)

- (42) Rosiński, J., Tempering stable processes, Stochastic Processes and their Applications 117, 677-707 (2007)

- (43) Samorodnitsky, G. and Taqqu, M. S., Stable Non-Gaussian Random Processes: Stochastic Models with Infinite Variance, Chapman & Hall, New York (1994)

- (44) Schoutens, W., Lévy processes in finance: pricing financial derivatives, John Wiley & Sons, Hoboken, NJ (2003)

- (45) Tankov, P., Pricing and hedging gap risk, Journal of Computational Finance 13(3), 33-59 (2010)

- (46) Tankov, P., Pricing and Hedging in Exponential Lévy Models: Review of Recent Results, Lecture Notes in Mathematics vol. 2003, Springer, Berlin, Heidelberg (2011)

- (47) Tompkins, R., Power options: hedging nonlinear risks, The Journal of Risk 2(2), 29-45 (1999)

- (48) Wilmott, P., Paul Wilmott on Quantitative Finance, Wiley & Sons, Hoboken, 2006

- (49) Zolotarev, V. M., One-Dimensional Stable Distributions, American Mathematical Society, Providence (1986)